41044_BZ_AR_2012 PRO30 4 GAS AR 2012

User Manual: PRO30 4 GAS AR

Open the PDF directly: View PDF ![]() .

.

Page Count: 104 [warning: Documents this large are best viewed by clicking the View PDF Link!]

SOLUTIONSBUSINESS

ANNUAL REPORT 2012

WE ARE BUNZL

WE ARE A FOCUSED AND SUCCESSFUL

INTERNATIONAL DISTRIBUTION AND

OUTSOURCING GROUP WITH

OPERATIONS ACROSS THE AMERICAS,

EUROPE AND AUSTRALASIA.

WE SUPPORT OUR CUSTOMERS ALL OVER THE

WORLD WITH A VARIETY OF PRODUCTS THAT ARE

ESSENTIAL FOR THE SUCCESSFUL OPERATION OF

THEIR BUSINESSES.

BY OUTSOURCING THE PURCHASING, CONSOLIDATION

AND DELIVERY OF A BROAD RANGE OF EVERYDAY

ITEMS, OUR CUSTOMERS ARE ABLE TO FOCUS ON

THEIR CORE BUSINESSES, ACHIEVE PURCHASING

EFFICIENCIES AND SAVINGS, FREE UP WORKING

CAPITAL, IMPROVE DISTRIBUTION CAPABILITIES AND

SIMPLIFY THEIR INTERNAL ADMINISTRATION.

Growth

2012 2011

Actual

exchange

rates

Constant

exchange

rates

Revenue £m 5,359.2 5,109.5 5% 6%

Operating profit £m 293.8 279.3 5% 7%

Operating profit* £m 352.4 335.7 5% 7%

Profit before tax £m 269.3 193.7 39% 42%

Profit before tax† £m 323.9 306.1 6% 8%

Basic earnings per share p 59.9 38.2 57% 61%

Adjusted earnings per share† p 71.8 68.5 5% 7%

Dividend per share p 28.2 26.35 7%

*Before intangible amortisation and acquisition related costs

† Before intangible amortisation, acquisition related costs and disposal of business

CONTENTS

Business review

01 Financial highlights

02 Business model

03 Strategy

04 Group at a glance

06 Key performance indicators

08 Chairman’s statement

10 Chief Executive’s review

22 Financial review

25 Principal risks and

uncertainties

27 Corporate responsibility

Governance

32 Board of directors

33 Corporate governance report

38 Directors’ remuneration report

51 Other statutory information

Financial statements

54 Consolidated income

statement

55 Consolidated statement of

comprehensive income

56 Consolidated balance sheet

57 Consolidated statement of

changes in equity

58 Consolidated cash flow

statement

59 Notes

89 Company balance sheet

90 Notes to the Company

financial statements

97 Statement of directors’

responsibilities

98 Independent auditor’s report

99 Five year review

100 Shareholder information

WHO WE ARE

The Annual Report can be

downloaded online. To find out

more visit www.bunzl.com.

FINANCIAL HIGHLIGHTS

+6%

Revenue at constant

exchange rates

+7%

Operating profit* at constant

exchange rates

+7%

Adjusted earnings per share†

at constant exchange rates

+7%

Dividend per share

BUNZL PLC ANNUAL REPORT 2012 01

WE SOURCE

WE DELIVER

WE SOURCE AND PROCURE BRANDED, OWN BRAND AND UNBRANDED

PRODUCTS GLOBALLY, WORKING WITH BOTH MULTINATIONAL AND LOCAL

SUPPLIERS, TO ENSURE THAT OUR CUSTOMERS HAVE ACCESS TO THE BEST

AND MOST SUITABLE PRODUCTS TO MEET THEIR NEEDS.

BY APPLYING OUR RESOURCES AND CONSOLIDATING A BROAD RANGE OF

PRODUCTS INTO OUR EXTENSIVE WAREHOUSING INFRASTRUCTURE, WE

ARE ABLE TO OFFER OUR CUSTOMERS A ONE-STOP-SHOP SOLUTION WHICH

REDUCES OR ELIMINATES MANY OF THE HIDDEN COSTS OF SELF-DISTRIBUTION.

WE OFFER SEVERAL DELIVERY OPTIONS, INCLUDING DIRECT STORE DELIVERY,

CROSS DOCK AND WAREHOUSE REPLENISHMENT PROGRAMMES, ON A LOCAL,

REGIONAL AND NATIONAL BASIS, TO ENSURE THAT OUR CUSTOMERS GET

THEIR PRODUCTS WHEN AND WHERE THEY ARE NEEDED.

BUSINESS MODEL

WE CONSOLIDATE

02 BUNZL PLC ANNUAL REPORT 2012

FOR MANY YEARS BUNZL

HAS CONTINUED TO PURSUE

A CONSISTENT STRATEGY OF

FOCUSING ON ITS STRENGTHS

AND CONSOLIDATING THE

MARKETS IN WHICH

IT COMPETES.

CONTINUALLY REDEFINING AND

DEEPENING OUR COMMITMENT TO

CUSTOMERS AND MARKETS, AS WELL

AS EXTENDING OUR BUSINESS INTO

NEW GEOGRAPHIES, REMAIN IMPORTANT

ELEMENTS OF OUR STRATEGY.

HOW OUR GROWTH IS ACHIEVED

Organic growth

We achieve organic growth by applying our resources and expertise to

enable customers to outsource to Bunzl the purchasing, consolidation

and delivery of a broad range of products, thereby enabling them to

achieve efficiencies and savings.

Acquisition growth

Since 2004 we have announced more than 70 acquisitions with an

average annual spend of £167 million, adding average annualised

revenue of £263 million.

Operating model efficiencies

We continually strive to make our businesses more efficient by investing

in new IT systems and warehouse facilities and implementing best

practice operational procedures.

OUR STRATEGY BUILDING BLOCKS

Unique business model

Our supply chain management and one-stop-shop offering allows our

customers to focus on their core businesses more effectively and at the

same time reduce their working capital.

Attractive markets

We operate across six fragmented markets sectors, many of which are

growing and resilient to challenging economic conditions.

Balanced business portfolio

We have a geographically balanced but diversified business portfolio

operating across 27 countries.

Operational focus

With a decentralised operational structure, our management areable

to focus on our customers’ needs while retaining full responsibility for

the financial performance of their businesses.

Strong financial discipline

Over the last 10 years we have delivered consistently good results

with very high returns on capital and operating cash flow conversion.

Experienced management

Our executive directors and business area heads have extensive

experience in managing the Group’s businesses with an average

of15 years’ service with Bunzl.

Acquisition strategy and track record

Our acquisition strategy is to seek out those businesses which satisfy key

criteria, including having good financial returns in resilient and growing

markets, while at the same time providing opportunities to extract further

value as part of the Bunzl Group.

STRATEGY

BUNZL PLC ANNUAL REPORT 2012 03

GROUP AT A GLANCE

WE PROVIDE A ONE-STOP-SHOP DISTRIBUTION AND

OUTSOURCING SERVICE SUPPLYING A BROAD RANGE

OF INTERNATIONALLY SOURCED NON-FOOD PRODUCTS

TO A VARIETY OF MARKET SECTORS.

* Before intangible amortisation and acquisition related costs

04 BUNZL PLC ANNUAL REPORT 2012

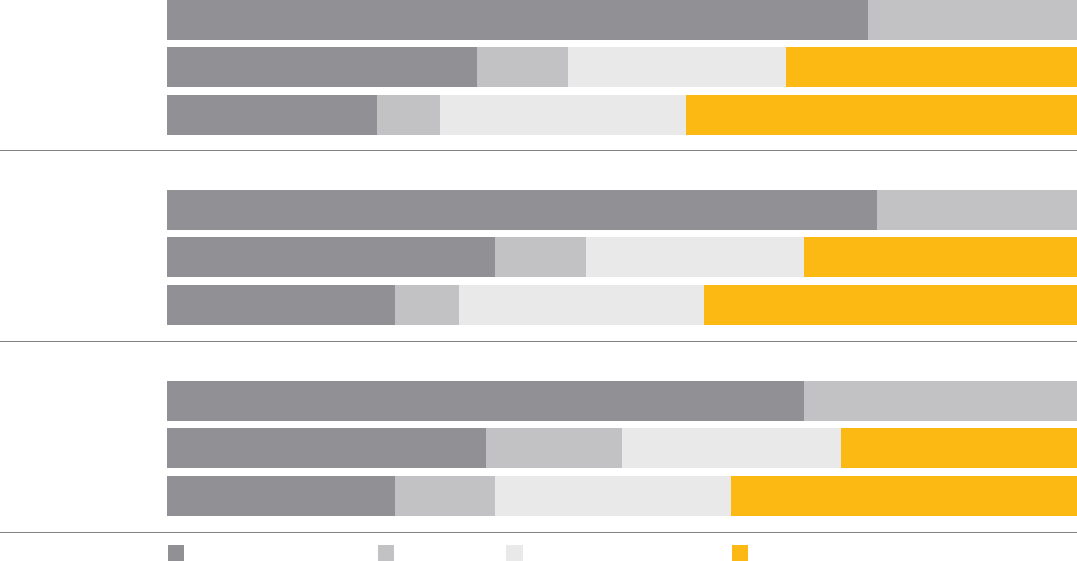

NORTH AMERICA

£2,905.8m

Revenue

£184.6m

Operating profit*

t Improvement in operating margin

from 6.2% to 6.4%.

t Six acquisitions in the year with

annualised revenue of more

than£400 million.

> Read more on page 14

CONTINENTAL

EUROPE

£1,079.4m

Revenue

£87.5m

Operating profit*

t Lower margins due to pricing

pressure and weaker euro

impacting imports.

t Revenue growth bolstered

byacquisitions.

> Read more on page 15

UK & IRELAND

£992.1m

Revenue

£65.2m

Operating profit*

t Higher organic growth and

operating margin up from

6.0% to 6.6%.

t Continued focus on operating

efficiency and own brand

development.

> Read more on page 18

REST OF

THE WORLD

£381.9m

Revenue

£33.2m

Operating profit*

t Strong organic revenue growth

in both Australasia and Brazil.

t Expansion in South America

outside Brazil with acquisition

of Vicsa.

> Read more on page 19

Growth drivers

t Increasing trend to outsourcing.

t Expansion of ‘away from home’ activity.

t Global legislative trends for health & safety.

t Favourable demographics in healthcare.

Fragmented markets

t No one does what we do, on our scale,

across our international markets.

t Bunzl’s national distribution networks provide

competitive advantage.

Customers

t Strong national, regional and local customer base.

t Working with national and international leading

companies.

MARKET CONTEXT

NON-FOOD RETAIL

Goods not for resale, including packaging

and a full range of cleaning and hygiene

products, to department stores, boutiques,

office supply companies, retail chains and

home improvement chains.

FOODSERVICE

Non-food consumables, including food packaging,

disposable tableware, guest amenities, catering

equipment, cleaning products and safety items,

to hotels, restaurants, contract caterers, food

processors and theleisure sector.

GROCERY

Goods not for resale (items grocers use but do

not actually sell), including food packaging, films,

labels and cleaning and hygiene supplies, to

grocery stores, supermarkets and retail chains.

HEALTHCARE

Disposable healthcare consumables, including

gloves, swabs, gowns and bandages, tothe

healthcare sector.

CLEANING & HYGIENE

Cleaning and hygiene materials, including

chemicals and hygiene paper, to cleaning

and facilities management companies and

industrial and healthcare customers.

OTHER

A variety of product ranges supplied to other

markets such asgovernment and education

establishments.

SAFETY

A complete range of personal protection

equipment, including hard hats, gloves,

boots and workwear, to industrial and

construction markets.

FOODSERVICE

GROCERY

CLEANING & HYGIENE

SAFETY

% 2012 REVENUE

HEALTHCARE

NON-FOOD RETAIL

OTHER

4

7

8

9

14

29

29

BUNZL PLC ANNUAL REPORT 2012 05

ORGANIC REVENUE

GROWTH %

Increase in revenue for the year

excluding the impact of currency,

current year acquisitions and

disposal of business, but including

a pro rata part year in respect

ofprior year acquisitions.

ADJUSTED EARNINGS

PER SHARE p

Earnings per share excluding the

impact of currency, intangible

amortisation, acquisition related

costsand disposal of business.

PROFIT MARGIN %

Ratio of operating profit before

intangible amortisation and

acquisition related costs to revenue.

ACQUISITION SPEND £m

Consideration paid and payable,

together with net debt assumed,

inrespect of businesses acquired

oragreed to be acquired during

theyear.

UNDERLYING PROFIT

MARGIN %

Profit margin excluding the impact of

currency, current year acquisitions

and disposal of business but

including a pro rata part year in

respect of prior year acquisitions.

ANNUALISED REVENUE

FROM ACQUISITIONS £m

Estimated revenue which would have

been contributed by acquisitions

made or agreed to be made during

the year if such acquisitions had been

completed at the beginning of the

relevant year.

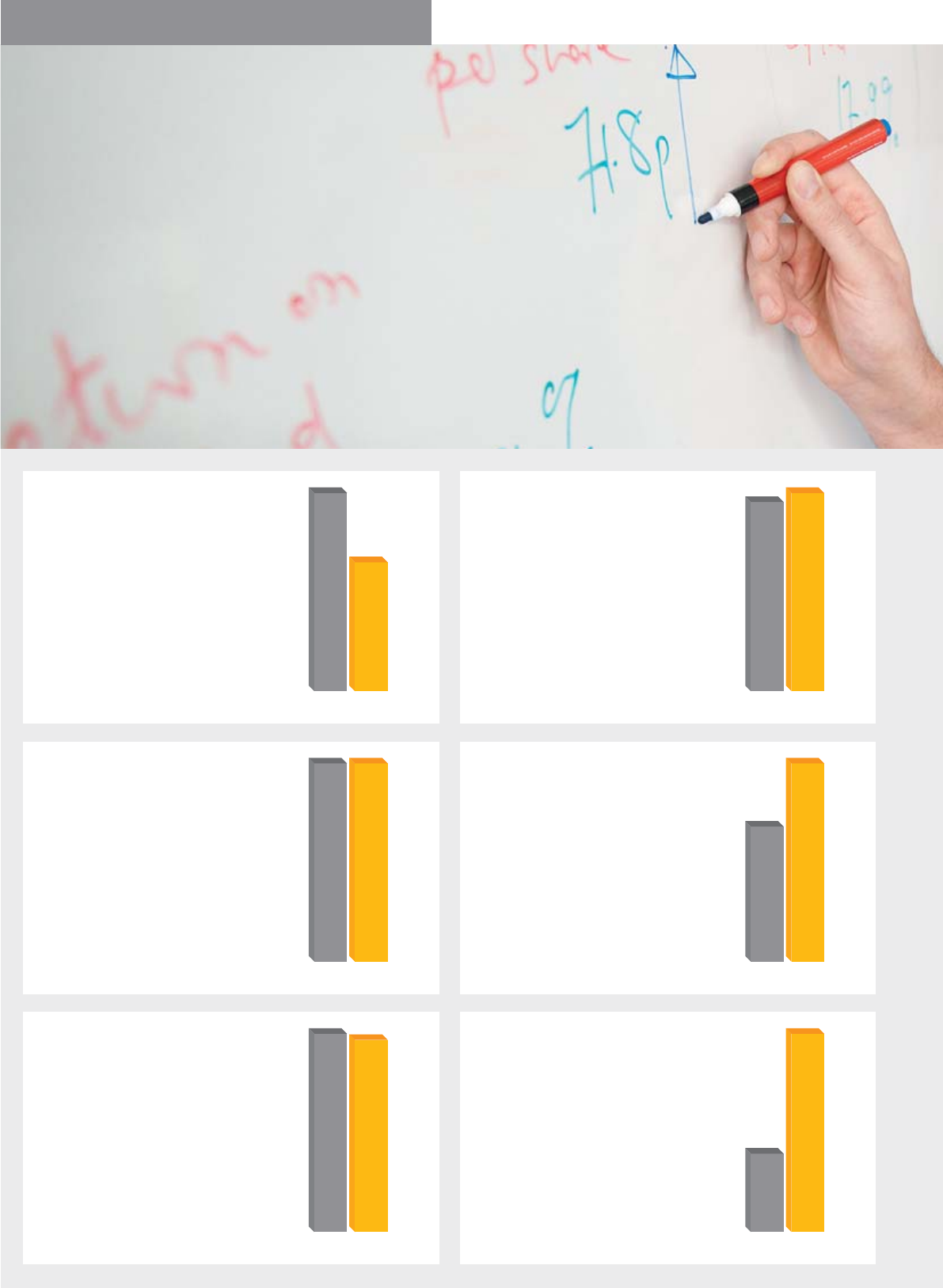

MEASURING

KEY PERFORMANCE INDICATORS

11 12

2.6

4.0

11 12

71.8

68.5

11 12

6.66.6

11 12

272

185

11 12

6.4

6.6

11 12

518

204

06 BUNZL PLC ANNUAL REPORT 2012

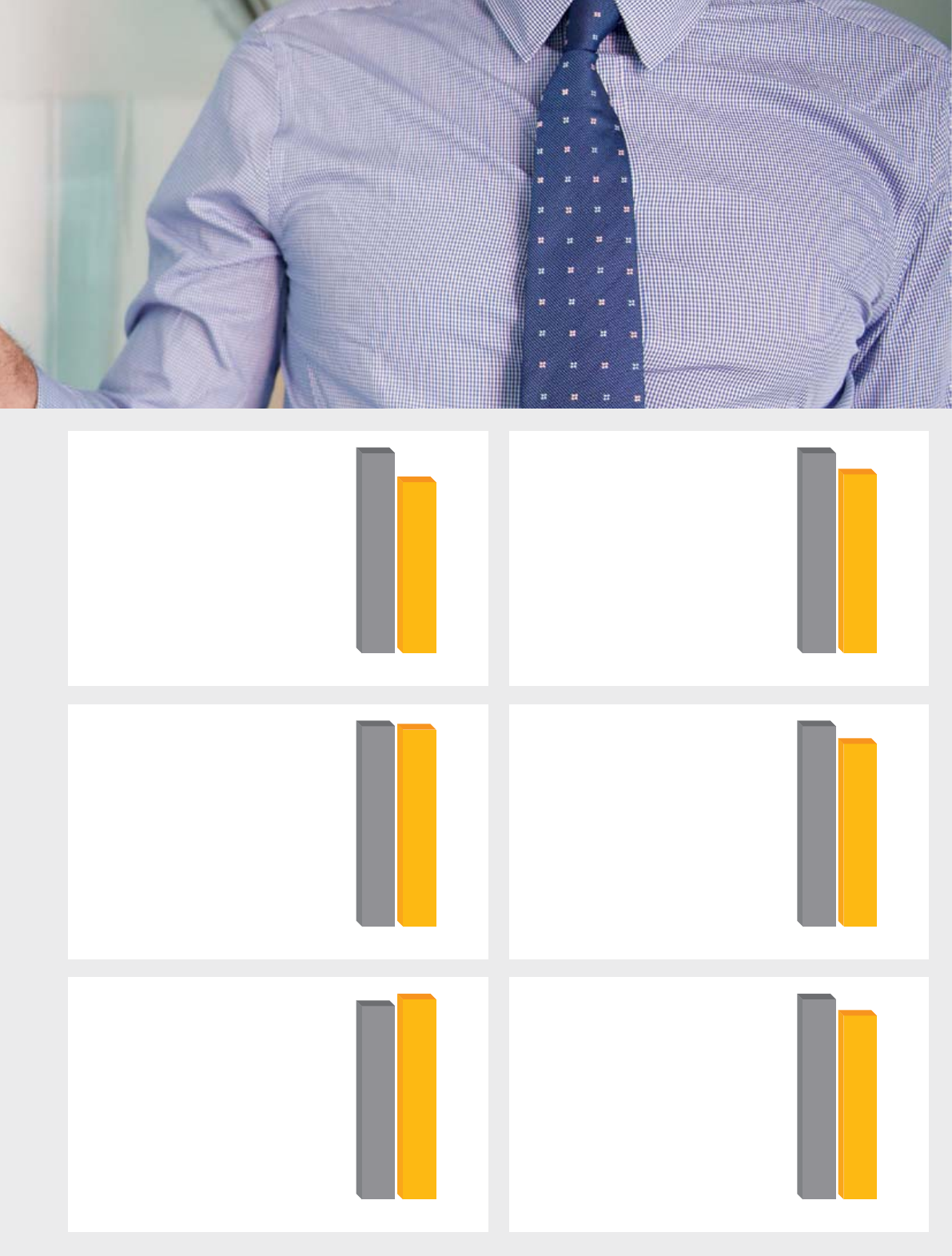

All data for carbon emissions and fuel usage for each year is based on the 12 months ended 30 September.

FREE CASH FLOW £m

Cash generated from operations

before acquisition related costs

lessnet capital expenditure,

interestand tax.

SCOPE 1 CARBON

EMISSIONS

Tonnes of CO2 per

£m revenue

Measured in accordance with the

Greenhouse Gas Protocol applying

2012 Defra conversion factors.

RETURN ON AVERAGE

OPERATING CAPITAL %

Ratio of operating profit before

intangible amortisation and acquisition

related costs tothe average of the

month end operating capital employed,

being tangible fixed assets, inventories

and trade and other receivables less

trade and other payables.

SCOPE 2 CARBON

EMISSIONS

Tonnes of CO2 per

£m revenue

Measured in accordance with the

Greenhouse Gas Protocol applying

2012 Defra conversion factors.

RETURN ON INVESTED

CAPITAL %

Ratio of operating profit before

intangible amortisation and

acquisition related costs to the

average of the month end invested

capital, being equity after adding

back net debt, retirement benefit

obligations, cumulative intangible

amortisation, acquisition related costs

and amounts written off intangible

assets, net of the related tax.

FUEL USAGE

Ltrs per £000 revenue

Diesel, petrol and LPG used

in the Group’s own vehicles.

OUR PERFORMANCE

11 12

235

275

11 12

16.0

17.9

11 12

56.4

57.4

11 12

5.2

5.7

11 12

17.9

17.3

11 12

5.6

6.1

BUNZL PLC ANNUAL REPORT 2012 07

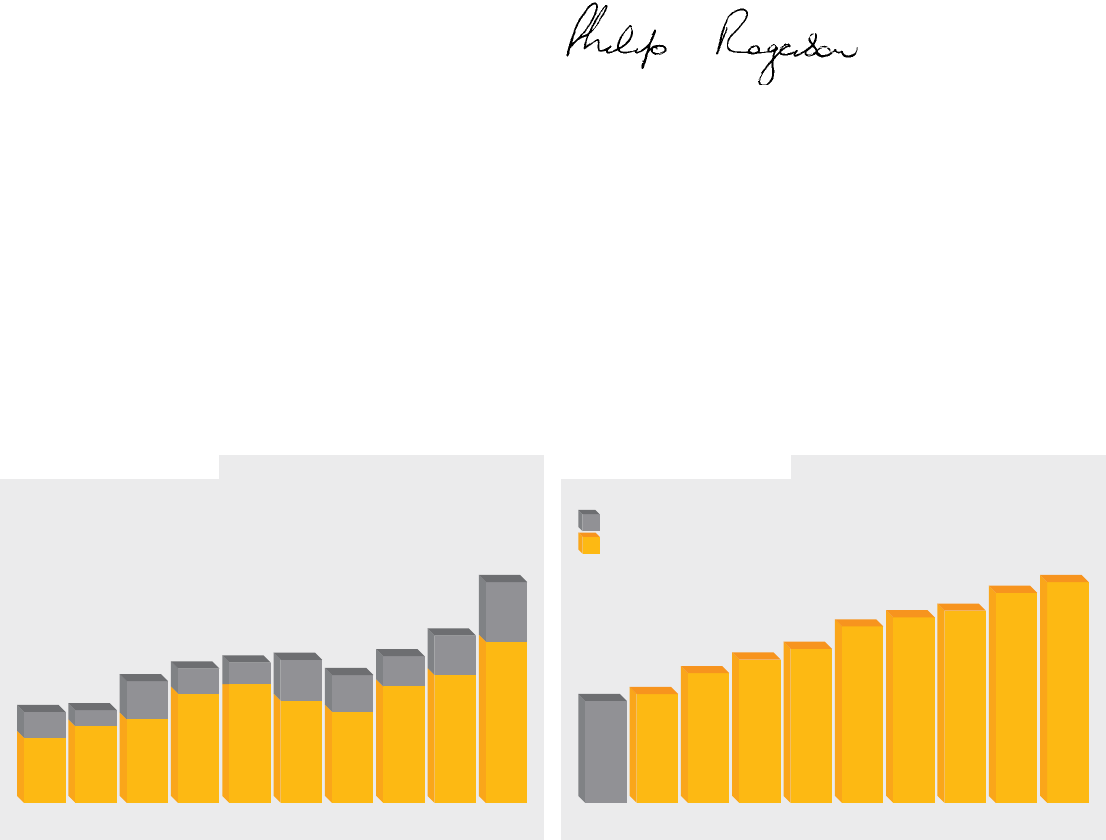

03

UK GAAP

IFRS

31.3 32.1

38.7 41.7 45.1

52.7 55.9 60.6

68.5 71.8

04 05 06 07 08 09 10 11 12 03

2.3 2.4

2.9 3.3 3.6

4.2 4.6 4.8 5.1 5.4

04 05 06 07 08 09 10 11 12

03–05 continuing operations

RESULTS

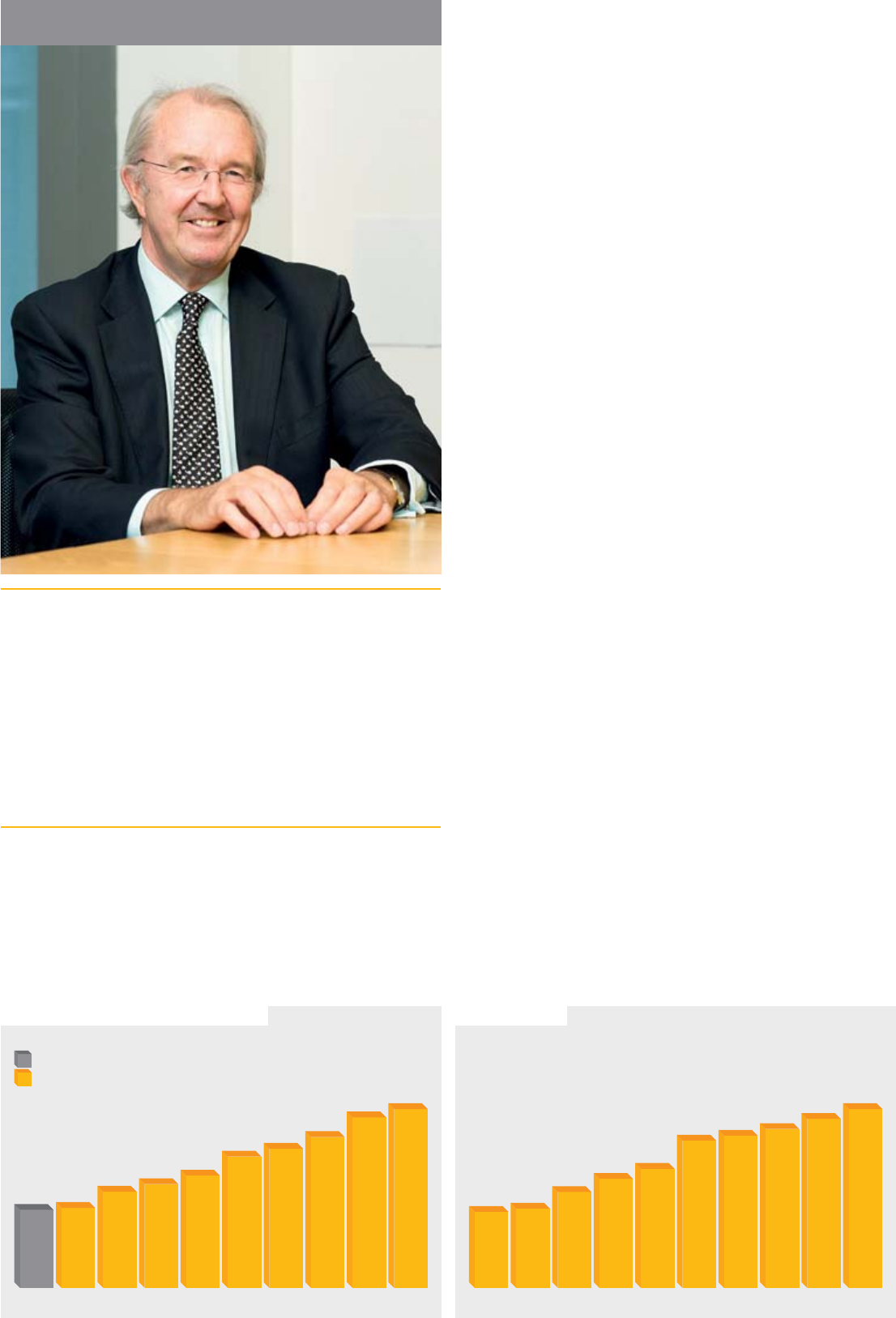

I am very pleased to be able to report another good set of results for Bunzl

despite the continuing difficult macroeconomic conditions which have

persisted for the last few years across many of the international markets

inwhich we compete.

Group revenue increased to £5,359.2 million (2011: £5,109.5 million), an

increase of 6% at constant exchange rates, due to organic growth of 2.6%

combined with the impact of recent acquisitions, net ofthe disposal of the

UK vending business in August 2011.

Operating profit before intangible amortisation and acquisition related

costs was £352.4 million (2011: £335.7 million), up 7% at constant

exchange rates, with the improvement in the Group operating margin on

the same basis being driven by the impact of acquisitions and the sale of

the UK vending business. Adjusted earnings per share before intangible

amortisation, acquisition related costs and the vending disposal were

71.8p (2011: 68.5p), an increase of 7% at constant exchange rates.

Adverse currency translation movements, principally the euro, reduced

the growth rates marginally by between 1% and 2%.

DIVIDEND

The Board is recommending a final dividend of 19.4p. This brings the total

dividend for the year to 28.2p, up 7% compared to 2011. Shareholders

will again have the opportunity to participate in our dividend reinvestment

plan.

STRATEGY

We continue to pursue our proven strategy of developing the business

through organic growth, consolidating the markets in which we compete

through focused acquisitions in both existing and new geographies and

continuously improving the efficiency of our operations.

We achieve our organic growth by applying our resources and expertise

toenable customers to outsource to Bunzl the purchasing, consolidation

and distribution of a broad range of goods not for resale. By doing so our

customers are able to focus on their core business more cost effectively

by achieving purchasing efficiencies and savings, freeing up working

capital, improving their distribution capabilities and simplifying their

internal administration.

Acquisition activity increased significantly in 2012, particularly towards

the end of the year, with 13 acquisitions announced and a total investment

of approximately £270 million adding annualised revenue of over £500

million. A key highlight this year was our first acquisition in South America

outside Brazil which has provided Bunzl with a first entry into four new

countries in the region. Having pursued our strategy consistently over

many years, we have built leading positions in a variety ofmarket sectors

across the Americas, Europe and Australasia.

ADJUSTED EARNINGS PER SHARE p REVENUE £bn

CHAIRMAN’S STATEMENT

‘ EXECUTING OUR CONSISTENT AND

PROVEN STRATEGY HAS RESULTED IN

ANOTHER SUCCESSFUL YEAR, WITH

CONTINUED GROWTH IN EARNINGS AND

DIVIDENDS, THROUGH A COMBINATION

OF ORGANIC AND ACQUISITION GROWTH

AND OPERATING EFFICIENCIES.’

Philip Rogerson

Chairman

08 BUNZL PLC ANNUAL REPORT 2012

03

UK GAAP

IFRS

171 183

218 241 259

297 312 323

353 371

04 05 06 07 08 09 10 11 12

03–05 continuing operations

*Before amortisation and acquisition related and corporate costs

INVESTMENT

While Bunzl does not have high levels of capital expenditure for a

company of its size, both organic growth and acquisitions require

investment in the business to expand and enhance its asset base.

OurITsystems and warehouse facilities are critical to our ability to serve

our customers in the most efficient and appropriate manner. We have

therefore continued to invest in order to support our growth strategy and

ensure that we retain our competitive advantage. By doing so we maintain

our leadership in the marketplace, as we integrate new businesses into

the Group and look to improve our existing infrastructure.

CORPORATE RESPONSIBILITY

Efficient and ethical management of our business and long term

relationships with all our stakeholders, whether customers, employees

orsuppliers, remain key to our sustained business success. During 2012

our managers and sales and procurement staff completed tailored training

covering our Corporate Responsibility (‘CR’) policies which included our

Business Standards/Code ofEthics and our stance on gifts and

entertainment, facilitation payments and information on our whistle

blowing process. Our employee survey again provided useful feedback

and resulted in a variety of actions. We have also continued to assist our

customers in meeting their CR objectives by providing them with product

choices, including some innovative environmentally friendly products

made from materials such as bamboo and sugar cane as well as, in some

cases, offering them a closed loop recycling facility. Our Quality Assurance

and Quality Control department based inShanghai continues to work with

our Asian suppliers to ensure that high quality and ethical standards of

operation are maintained.

EMPLOYEES

Our employees’ experience, dedication, commitment and approach to

their work remain key strengths of Bunzl. Across the world we depend

onthem to continue to provide high quality care to our customers, adding

value to our service provision. The relationships formed by our employees

with all our stakeholders shape the reputation of Bunzl and build our

culture of a positive ‘can-do’ company. As ever, we are genuinely grateful

for the loyalty and hard work of all our employees and we are delighted

that 2012 has been a year in which many new employees have joined

the Group through acquisition, providing new ideas and challenges to

continue the development of Bunzl internationally.

CREDIT FACILITIES

The Group remains highly cash generative and we continue to have

access to diverse sources of funding to achieve our strategic objectives.

InOctober 2012 we refinanced some of our debt facilities by raising

US$350.0 million of fixed interest rate borrowings in the US private

placement market with maturities ranging from seven to 11 years at an

average interest rate of 3.4%. US$110.0 million was drawn in December

with the balance due to be drawn in April 2013. During the year we also

refinanced or agreed new banking facilities totalling £150.7 million. Our

undrawn committed facilities at the end of the year were £589.3 million.

BOARD

Ulrich Wolters, who has served as a non-executive director since 2004,

will be retiring after the Company’s Annual General Meeting in April 2013.

We thank Ulrich for his significant contribution over many years and he

will leave the Board with our gratitude and best wishes for the future.

Jean-Charles Pauze was appointed as a non-executive director in January

2013 and Meinie Oldersma will join the Board in the same capacity in

April. Based in Paris, Jean-Charles is presently Chairman of Europcar and

Chairman of the Supervisory Board of CFAO Group and was Chairman

and Chief Executive of Rexel for 10 years until 2012. Prior to that he held

a number of senior positions with PPR Group, Strafor Facom Group and

Alfa Laval Group in France and Germany. A Dutch national, Meinie is

currently based in the UK and has been Chief Executive of 20:20 Mobile

Group since 2008 and previously held a variety of senior positions with

Ingram Micro, most recently as Chief Executive and President of their

China Group and Managing Director of their business in Northern Europe.

Both Jean-Charles and Meinie have extensive international experience

across a range of distribution and service sectors, particularly in Europe

and Asia, which willbe of great value to Bunzl as we continue to expand

and develop. Iamdelighted to welcome them to the Board.

Philip Rogerson

Chairman

25 February 2013

03

345 405 443

578 627 542 482

616 676

852

04 05 06 07 08 09 10 11 12

1,167

884

777

675

757

742

710

643

486

482

SHARE PRICE RANGE p OPERATING PROFIT* £m

BUNZL PLC ANNUAL REPORT 2012 09

10 BUNZL PLC ANNUAL REPORT 2012

OPERATING PERFORMANCE

The Group once again had a successful year in 2012 due to a

combination of organic growth, good performance from the acquisitions

made in 2011 and increased acquisition spend during the year.

Although some currencies, notably the US dollar, were marginally stronger

than in 2011, the translation effects of the weaker euro and overall

currency movements have reduced the reported growth rates of revenue

and operating profit. The operations, including the relevant growth rates,

are reviewed below at constant exchange rates to remove the distorting

impact of these currency movements. Changes in the level of revenue and

profits at constant exchange rates have been calculated by retranslating

the results for 2011 at the average rates used for 2012. Unless otherwise

stated, all references in this review to operating profit are to operating

profit before intangible amortisation and acquisition related costs.

Revenue increased 6% (5% at actual exchange rates) to £5,359.2 million

and operating profit was £352.4 million, an increase of 7% (5% at actual

exchange rates). The percentage growth in operating profit at constant

exchange rates was greater than that of revenue due to the improvement in

Group operating margin by 10 basis points to 6.6% as a result of the impact

of acquisitions and the sale of the UK vending business in August 2011.

In North America revenue rose 6% (7% at actual exchange rates) due to

good organic revenue growth and the impact of acquisitions completed

in2011 and 2012, while operating profit increased 8% (9% at actual

exchange rates). Revenue in Continental Europe rose 8% (1% at actual

exchange rates) as a result of some organic revenue growth and the

impact of acquisitions but operating profit was down 2% (8% at actual

exchange rates) as margins came under pressure. In UK & Ireland

revenue was flat at both constant and actual exchange rates primarily

dueto good organic revenue growth and the impact of relatively small

acquisitions being more than offset by the impact of the sale of vending

during the second half of 2011. However operating profit rose 8% at both

constant and actual exchange rates due to the positive impact of cost

reduction initiatives, product mix improvements in some businesses and

the disposal of vending. In Rest of the World revenue increased 23%

(20% at actual exchange rates) and operating profit was up 22% (17%

at actual exchange rates) due to both excellent organic revenue growth

and the impact of acquisitions.

Basic earnings per share were 61% higher (57% at actual exchange rates)

at 59.9p due to the significant impact in 2011 of the loss on disposal of

the vending business. Adjusted earnings per share, after eliminating the

effect of intangible amortisation, acquisition related costs and the disposal

of vending, were 71.8p, an increase of 7% (5% at actual exchange rates).

Although the underlying return on average operating capital increased,

the overall return decreased slightly from 57.4% to 56.4% due to the

recent acquisitions currently having a lower return on operating capital

than the rest of the Group.

Our operating cash flow continued to be strong. Despite an acquisition

cash outflow of £254.7 million and net capital expenditure of £20.2

million, our year end net debt of £738.1 million was only £85.2 million

higher than at the end of 2011. The net debt to EBITDA ratio increased

marginally to 1.8 times compared to 1.7 times at the previous year end.

Our continued focus on the sustainability of our business has once again

led to a further reduction, relative to revenue, of our Scope 1 and 2 carbon

emissions. This has been achieved partly as a result of further investment

in energy efficient lighting systems in our facilities and the introduction

MANAGEMENT TEAM

Managers from across the

Groupmeet regularly to review

performance, discuss trends

affecting our businesses and

seek further opportunities for

growth and competitive

advantage.

Patrick Larmon

President and CEO North America

Celia Baxter

Director of Group Human Resources

Brian May

Finance Director

Frank van Zanten

Managing Director Continental Europe

Andrew Mooney

Director of Corporate Development

Rodrigo Mascarenhas

Managing Director South America

Kim Hetherington

Managing Director Australasia

Paul Hussey

General Counsel and Company

Secretary

Paul Budge

Managing Director UK & Ireland

CHIEF EXECUTIVE’S REVIEW

‘ BUNZL HAS AGAIN DEMONSTRATED THE

STRENGTH OF ITS VALUE PROPOSITION

AND SHOWN ITS ABILITY TO DEVELOP

BOTH IN EXISTING AND NEW MARKETS.’

Michael Roney

Chief Executive

Having been Director of Corporate Development since 1999,

NancyLester left Bunzl at the beginning of 2013. We thank her for

hervaluable contribution and wish her all the very best for the future.

BUNZL PLC ANNUAL REPORT 2012 11

within our transport fleet of a number of vehicles which have lower

emissions. The health, safety and well-being of our staff remains a key

feature of the way in which we operate.

ACQUISITIONS

Our committed acquisition spend in 2012 of £272 million was the highest

level since 2004 with 13 transactions announced.

In February we acquired the business of CDW Merchants. Based in Chicago,

the business is principally engaged in the sale of retail gift packaging and

visual merchandising solutions and products to the specialty retail and

online retailing sectors throughout the US. Revenue inthe year ended

31 December 2011 was US$12 million. The business, which works

closely with its customers to increase brand appeal and consumer loyalty

through innovative gift packaging concepts and merchandising displays,

complements our existing non-food retail supplies business in North

America and extends our customer base, particularly inthe specialty

and online retail sector.

We acquired three businesses at the end of April. FoodHandler, also

based in Chicago, is a leading supplier of a broad range of disposable

gloves and other foodhandling products to the foodservice sector

throughout the US. Revenue in the year ended 31 December 2011

was US$99 million. The business enhances our existing foodservice

operations in North America and expands our product offering and

importprogramme in this sector. Based near Tel Aviv, Zahav is a leading

distributor of packaging supplies to the foodservice sector throughout

Israel. Revenue in the year ended 31 December 2011 was ILS66 million.

This is our second acquisition in Israel which is a market we entered in

2010 with the purchase of Silco. It has a strong and broad customer base,

especially in the bakery sector, and significantly increases the size of

our business in that country. The Group also purchased in Aprilthe

Queensland based redistribution operations of Star Services International

in Australia. Based in Brisbane and Cairns, the business is engaged in

the supply of foodservice disposable products to wholesalers and

redistributors throughout Queensland. Revenue for the year ended

30June 2012 was A$12 million. The acquisition complements our

existing foodservice supplies operations in Queensland and will allow

us to penetrate further into the redistribution sector of this market.

Based near Seattle, Service Paper was purchased in June. The business

is principally engaged in the distribution of disposable supplies to the

grocery, foodservice, food processor and industrial packaging sectors

throughout the Pacific Northwest. Revenue of the business acquired for

the year ended 31 December 2011 was US$61 million. The business,

which has a reputation for providing high levels of customer service, will

expand our existing business in the region.

At the end of June we acquired Distrimondo which is based near Zurich

and is principally engaged in the distribution of foodservice disposables

and cleaning and hygiene products throughout Switzerland. Revenue in

the year ended 31 December 2011 was CHF17 million. The acquisition

extends our operations in Switzerland which is a key market that we

entered in 2010 with the purchase of Weita.

The acquisition of Indigo Concept Packaging was completed in October.

Indigo is based in the UK and is principally engaged in the sale of quality

retail packaging products to a variety of customers. Revenue in the year

ended 31 December 2011 was £6 million.

At the end of October we acquired Atlas Health Care in Australia. Based

inAdelaide, the business is principally engaged in the supply of medical

consumables to the healthcare sector and gives us an enhanced market

position in this growing sector. Revenue in the year ended 30 June 2012

was A$22 million.

In December we entered into agreements to acquire five businesses.

Based near Toronto, McCordick Glove & Safety is a distributor of gloves

and other personal protection equipment to a variety of industrial and

retail customers as well as to redistributors. It has enabled us to enter

the personal protection equipment sector in Canada and enhances the

Company’s existing safety product offering. Revenue in the year ended

31December 2011 was C$53 million. Vicsa Safety in Chile and its

subsidiaries based in Peru, Argentina, Colombia and Mexico specialise

inthe sourcing and sale of a variety of personal protection equipment

throughout the region. The aggregate revenue of the Vicsa businesses in

2012 was US$65 million of which more than half was accounted for by

the business in Chile. At the same time we entered into an agreement to

purchase Vicsa Brasil which was completed earlier this month following

clearance from the Brazilian Competition Authority. Revenue in 2012

wasUS$9 million. The acquisition of the Vicsa businesses is an exciting

development for us as they expand our operations in South America

outside Brazil into four new countries as well as extending our business

inMexico into the safety sector. In December we also acquired Destiny

Packaging in the US which had revenue in 2012 of US$52 million.

Basedin Monterey, California, Destiny Packaging is a leading distributor

offlexible packaging supplies, principally produce bags, to fruit and

vegetable growers throughout California and Arizona and complements

both Cool-Pak and Netpak which we acquired in 2010 and 2011

respectively. Together these three businesses give us an increasing

presence in the market of innovative packaging solutions for both growers

and food retailers in North America. Finally the Company purchased

Schwarz Paper Company in the US at the end of December. Based in

Chicago and operating from 14 locations, Schwarz Paper Company is

principally engaged in the provision of consumables and supply chain

solutions for the non-food retail and grocery sectors. It significantly

increases the size of our non-food retail business and will further enhance

the Company’s market leading position in the grocery sector. Revenue

ofthe acquired business in the year ended 30 September 2012 was

US$363 million.

The acquisition of McNeil Surgical in Australia was completed at the

beginning of February 2013. With revenue of A$16 million in the year

ended 30 June 2012, the business is engaged in the sale of healthcare

consumables and equipment to aged care facilities, hospitals and medical

centres as well as to redistributors and increases our market presence in

this growing sector.

PROSPECTS

The macroeconomic outlook continues to be challenging but we believe

that our resilient customer base and the opportunities for additional

market consolidation will provide the Group with a good platform for

further growth.

In North America we expect to see stronger growth as a result of the six

acquisitions completed last year and an improvement in organic revenue

growth from the levels seen in the second half of 2012. In spite of the

difficult market conditions in Continental Europe, we currently anticipate

some growth with a stable operating margin. The performance of UK

& Ireland should continue to improve, in spite of the sluggish economies,

led by organic growth and ongoing cost reduction initiatives. Rest of the

World should see a strong performance through a combination of good

organic growth and the impact of the recent significant acquisition activity.

Acquisition growth is an important part of our strategy. The pipeline is

promising as we continue discussions with a number of potential targets.

The Board believes that the prospects for the Group are positive due

to our strong market position, growing customer sectors and good

opportunities to consolidate further the markets in which we compete.

Michael Roney

Chief Executive

25 February 2013

12 BUNZL PLC ANNUAL REPORT 2012

SOURCING

CHIEF EXECUTIVE’S REVIEW CONTINUED

WE SOURCE HUNDREDS OF THOUSANDS OF DIFFERENT PRODUCTS

FROM ALL OVER THE WORLD, LIAISING CLOSELY WITH OUR SUPPLIERS

SO THAT WE ARE ABLE TO OFFER A FULL RANGE OF ITEMS WHICH

SATISFY OUR CUSTOMERS’ DEMANDS. FROM SAFETY HARNESSES

AND HARD HATS TO BAKERY PACKAGING AND COFFEE CUPS,

WE ENSURE THAT THE PRODUCTS WE SOURCE ARE THE MOST

APPROPRIATE FOR THEIR EVERYDAY REQUIREMENTS.

BUNZL PLC ANNUAL REPORT 2012 13

EVERYDAY

ESSENTIAL

PRODUCTS

14 BUNZL PLC ANNUAL REPORT 2012

NORTH AMERICA

In North America revenue increased by 6% to £2,905.8 million due to

sales growth with existing customers, new business wins and acquisitions.

This, together with the impact of higher margin acquisitions and good cost

control, contributed to an 8% increase in operating profit to £184.6 million,

with the operating profit margin improving 20 basis points to 6.4%. Our

extensive distribution network and delivery fleet across North America and

our experienced sales force continued to produce value for our customers

in the diversified business sectors we service.

Our largest business, which serves the grocery sector, produced good

growth in 2012 principally as a result of the full year impact of a significant

customer win in the third quarter of 2011 but also as we expanded our

business with other customers by offering integrated supply chain product

and information supply chain solutions. Execution of our cornerstone

programmes of direct store delivery, cross dock and warehouse

replenishment programmes on a local, regional or national basis provides

us with a unique competitive advantage in the marketplace and generates

opportunities for us to reduce the operating costs and working capital

investment of our customers. Our overall business in the Pacific

Northwest was boosted by the acquisition of Service Paper in June.

The redistribution business also grew as we continued to enable our

distributor customers, predominantly in the foodservice, jan/san (janitorial/

sanitation) and office products sectors, to achieve increased profitability

through our proximity and scale. Our business model allows not only these

customers but all ofour customers to consolidate their sources of supply

and reduce their administrative and operating costs through our one-stop-

shop offering. Asa result of our excellent fill rates and dependable delivery

capabilities, our customers can improve their profitability and asset

utilisation by rededicating storage space, once occupied by the stock

items we now provide, to support higher revenue generating items.

Our food processor business continued to perform well, with customers

across the full breadth of the food processor supply chain from the fields

to the stores. These include growers, packers, large food companies and

meat, fresh cut produce, home meal and specialty food processors. The

recent addition of Destiny Packaging and its flexible packaging offering

complements Cool-Pak’s and Netpak’s rigid packaging product lines and

increases our ability to provide innovative packaging solutions for growers,

packers and retailers.

+8%

INCREASE IN OPERATING PROFIT AT

CONSTANT EXCHANGE RATES WITH

IMPROVEMENT IN OPERATING MARGIN.

Our business serving the non-food retail sector also developed well

despite slow US retail sales growth. Our coast to coast distribution network

gives us the scale needed to support national retail chains cost effectively

through our uniform operating platform. Our recent acquisition of Schwarz

Paper Company complements our existing non-food retail and grocery

distribution businesses. Schwarz will significantly expand our customer

base and market presence in these sectors across the US in the coming

year. We also continued to improve our expertise and breadth of product

line through our acquisition of CDW Merchants in February. Their design

and marketing offerings will further enhance our ability to introduce new

and unique point of sale designs and, together with Keenpac, allow us

to offer innovative packaging and store supply programmes that will lead

to increased business with our existing customer base as well as attract

newcustomers, particularly in the specialty and online retail sectors.

Although the convenience store sector is still impacted by higher fuel

costs, it continued to expand in 2012. We continuously work with retail

convenience store chains to provide additional programmes and products

to help them meet the demands of the new services being offered at the

store level. Our investment in a well trained sales force gives us a better

opportunity to develop more expansive programmes with these local,

regional and national chains. Wholesalers in this sector also continue to

extend their services which provides us with additional sales opportunities.

We continue to strengthen our relationships with our preferred suppliers

and further integrate our supply chains as we position their products

closer to the customer reducing their operating costs and improving their

profitability. Working as supply chain partners allows us to leverage our

combined strengths to create unique programmes and products that best

satisfy our customers’ needs at competitive prices.

Our private label import and import logistics programmes saw further

expansion by utilising our state-of-the-art Shanghai distribution centre

andquality control services and leveraging our international logistics

expertise. We also penetrated more deeply into the foodservice sector

andstrengthened our competitive position through our acquisition of

FoodHandler, a leading supplier of own brand disposable gloves and

otherfood handling products. Not only does FoodHandler expand our

foodservice product offering, it also complements our existing foodservice

operations, augments our sales force with extensive product sales and

marketing expertise and extends our customer base. In addition, our

recent acquisition of McCordick Glove & Safety enables us to enter the

personal protection equipment sector in Canada which is a product area

where wehave already been very successful in a number of other

geographies. Italso has a wide range of successful own brands that will

enhance our existing safety product offering.

We continued to manage successfully our operating costs despite ongoing

pressures on fuel, freight and healthcare costs. As part of this process

wediligently evaluate new warehouse technologies that could improve

warehouse efficiencies and continually analyse the number of facilities

werequire in order to optimise our operating costs and service levels.

CHIEF EXECUTIVE’S REVIEW CONTINUED

‘ OUR IT PLATFORM, EXTENSIVE

WAREHOUSE NETWORK AND DELIVERY

FLEET CONTINUE TO POSITION US WELL

TO MEET OUR CUSTOMERS’ DEMANDS

IN THE FUTURE.’

Patrick Larmon

President and CEO North America

BUNZL PLC ANNUAL REPORT 2012 15

CONTINENTAL EUROPE

Revenue rose by 8% to £1,079.4 million due to a combination of some

organic growth and acquisition activity in 2011 and 2012, although

operating profit fell 2% to £87.5 million. In the difficult economic

environment in most of the countries in which we are present, pricing

pressure in our markets together with a weaker euro impacting import

prices has led to a decline in gross margin. Although operating costs remain

tightly controlled, underlying revenue growth has slowed compared to

recent years such that the revenue growth, together with the impact from

acquisitions, was not sufficient to compensate for the gross margin decline.

Our largest business, the cleaning and hygiene operations in France, saw

a slight reduction in sales. Gross margin continues to be under pressure,

in particular from thehealthcare and public sectors with cost control

measures at our customers continuing to impact our business, leading

to a decline in operating profit. Measures to increase gross margin and

reduce costs have been implemented with a view to improving future

profitability. By contrast, our personal protection equipment business

in France enjoyed good sales growth with an improved operating profit.

In the Netherlands, sales continued to grow significantly in our businesses

supplying the food and non-food retail sectors. Our healthcare business

saw reasonable growth although the horeca (hotel, restaurant and

catering) sector recorded a small decline. Margins remain under pressure

although improved in the healthcare sector, partly due to synergies from

recent acquisitions. Overall underlying operating profit improved and was

further enhanced by the full year impact of the acquisition of D-Care

which was acquired in 2011.

2012 was the first full year of ownership of Majestic Products, a personal

protection equipment and safety products business in the Netherlands,

Belgium, Germany and the US. While trading in the European businesses

was soft, the US business recorded strong growth both in sales and

operating profit, in particular due to the successful introduction of new

products. It also relocated to a larger, purpose-built facility to allow for

further growth in the coming years.

£1,079.4m

RECORD LEVEL OF SALES AS

BUSINESS AREA REVENUE

INCREASES 8% AT CONSTANT

EXCHANGE RATES.

In Belgium, we recorded strong sales growth in the cleaning and hygiene

sector due to further gains with a number of existing customers although

sales in the retail sector declined following the loss of one larger account

leaving overall sales flat. Good margin management led to an overall

increase in operating profit and margins.

In Germany, sales growth was modest with gains in sales to fast food

chains, coffee shops and wholesalers being partly offset by lower sales to

contract caterers. Margins remain under pressure in particular from larger

accounts. Costs were reduced during the year to compensate for lower

margins leaving operating profit flat.

In Switzerland, our Weita business saw a slight decline in sales as the

Swiss economy, and in particular its tourism industry, has been adversely

impacted by the continuing strength of the Swiss franc, although margins

were in line with last year. At the end of June we acquired Distrimondo, a

distributor of foodservice disposables and cleaning and hygiene products

throughout Switzerland, which is integrating well into the Group and

generating synergies with Weita.

In Denmark, sales have declined in the retail and horeca sectors and

grown in the personal protection equipment sector. Gross margins are

alsounder pressure in the retail and public sectors and this, combined

with some one-off costs associated with implementing a new IT system,

resulted in a reduced operating profit.

In Spain, extremely difficult economic circumstances led to a fall in

underlying sales in both the cleaning and hygiene and personal protection

equipment businesses, although overall sales in the cleaning and hygiene

business were ahead due to the purchase of King Espana in 2011.

Margins have also fallen as a result of the weaker euro increasing import

prices and competitive pressures although this has partially been

mitigated by synergies achieved following the acquisition of King Espana.

In central Europe, sales grew after the decline of 2011 with the strongest

growth in the retail sector although the cleaning and hygiene and safety

sectors also improved. Margins, however, remain under pressure across

the region leading to a lower level of operating profit.

In Israel, our foodservice disposables business, Silco, continued to deliver

strong sales growth but margins have declined, partly due to the strength

of the US dollar. In April we acquired Zahav, a leading distributor of

packaging supplies to the foodservice sector which is integrating well

into the Group.

‘ OUR BROAD PORTFOLIO OF BUSINESSES

ACROSS A NUMBER OF MARKET SECTORS

AND GEOGRAPHIES ENABLES US TO MEET

THE CHALLENGING MARKET CONDITIONS

WE ARE FACING.’

Frank van Zanten

Managing Director Continental Europe

16 BUNZL PLC ANNUAL REPORT 2012

CONSOLIDATION

CHIEF EXECUTIVE’S REVIEW CONTINUED

WE HAVE AN EXTENSIVE FOOTPRINT OF WAREHOUSE FACILITIES

ACROSS FOUR CONTINENTS WHICH MEANS THAT OUR PRODUCTS

ARE NEVER FAR FROM WHERE THEY NEED TO BE. WHETHER

CUSTOMERS REQUIRE ORDERS FOR A NETWORK OF LOCATIONS

OR INDIVIDUAL OUTLETS, WE CAN QUICKLY AND EASILY FACILITATE

THEIR NEEDS FROM OUR BROAD RANGE OF STOCK KEEPING UNITS.

BUNZL PLC ANNUAL REPORT 2012 17

THAT OFFERS OUR

CUSTOMERS

ONE-STOP-SHOP

SOLUTIONS

18 BUNZL PLC ANNUAL REPORT 2012

UK & IRELAND

Our businesses in the UK & Ireland have shown a continued improvement

in performance in 2012. Although total revenue was flat at £992.1 million,

due to the impact of the sale of vending in August 2011, operating profit

increased 8% to £65.2 million. In a market where demand is still

suppressed and there is constant pressure from customers to make

savings, we have achieved underlying growth and margin improvement by

further developing our market position and by successfully integrating the

recent acquisitions. We have also improved results by constantly appraising

our resource levels and operating efficiency, investing in product sourcing

and procurement and the continued development of our own brands.

The London 2012 Olympics was an important event for Bunzl as we

provided a number of products specifically for the Games through our

catering and hospitality customers. These included catering disposables,

healthcare consumables and cleaning and hygiene supplies. In addition

to the business opportunity it presented, we were able to enhance our

reputation for delivering an outstanding level of service.

The safety market has continued to be subdued as a result of reduced

demand, particularly in the construction and industrial sectors, although

the results for the year of our safety supplies business were boosted by

the integration of SIG Safety and Workwear which was purchased during

2011. Our cleaning and hygiene supplies business performed well

as a result of good organic growth in the facilities management sector

and the full year impact of the Cannon Consumables business also

acquired in 2011. We remained focused on operating costs in this difficult

environment and further consolidated the branch network of our cleaning

and safety businesses, reducing the number of facilities by two.

86.5%

RETURN ON OPERATING CAPITAL,

THE HIGHEST OF ALL OF THE

BUSINESS AREAS.

In hospitality we saw good growth, particularly with high street coffee

shops and contract caterers. Our ability to offer an extensive range of own

brand products, which complement branded products, helped to make

savings for our customers and maintain our operating margins. This

remains a very competitive market, so we are conscious of the need to

provide high levels of service at low levels of operating cost. As part of our

programme to deliver these, we have further rationalised our network and

closed twolocations.

In our food retail business we have continued to increase sales by gaining

an additional major grocery retailer during the year, together with the

impact of a new grocery account won towards the end of 2011. Our

non-food retail packaging business had a successful year, despite the

significant challenges being faced by many of our high street customers,

due to continuing strong demand from luxury branded retailers and the

acquisition of Indigo Concept Packaging in October. Gross margins are

under constant pressure in the retail supplies market and it is through

offering innovative supply solutions and reducing customers’ existing costs

that we have managed to continue to be successful.

Although the healthcare market has been challenged by ongoing

government spending constraints, we have made good progress during

2012. This has been achieved by focusing on more profitable business,

expanding and developing our range of own brand products and by taking

measures to reduce operating costs. During the year we also increased

the efficiency of our operations by introducing a new electronic ordering

platform for our customers.

In spite of a continuing difficult economy in Ireland and the negative

impact of the weaker euro, our business there has seen further recovery

in 2012. This reflects the work that had already been done to reduce our

cost base and improve the sales performance. The overall market that we

serve has stabilised, reflecting an increase in demand from hotels and the

hospitality sector. We have also been successful in winning tenders for

supply to government agencies and facilities management companies.

This has enabled us to offset the ongoing weak demand from high street

retailers and the takeaway food market.

CHIEF EXECUTIVE’S REVIEW CONTINUED

‘OUR ORGANIC REVENUE GROWTH

INCREASED THIS YEAR TO ITS

HIGHEST LEVEL FOR FIVE YEARS

AS WE CONTINUED TO IMPROVE

OUR PERFORMANCE.’

Paul Budge

Managing Director UK & Ireland

BUNZL PLC ANNUAL REPORT 2012 19

REST OF THE WORLD

In Rest of the World revenue increased 23% to £381.9 million while

profits rose 22% to £33.2 million. Both Australasia and Brazil experienced

strong organic revenue growth with the results also benefitting from the

impact of recent acquisitions.

In Australasia, our largest business, Outsourcing Services, which supplies

the healthcare, cleaning and catering sectors, continued to perform

strongly and again delivered strong results. This was achieved through a

consistent strategy of focusing on the resilient market sectors and growing

market share in aged care facilities and hospitals where we supply a wide

range of disposable and medical consumables. We also saw some solid

growth with our catering and cleaning customers who supply into the

mining and resource sectors. In addition in April we made our first entry

into the redistribution sector through the acquisition of the redistribution

business of Star Services International in Queensland.

To help consolidate our market position in healthcare, in October

we acquired Atlas Health Care which is a major supplier of specialist

healthcare consumables in South Australia. This acquisition brings

additional market specialisation and expertise in woundcare and nutrition

and complements our current product offering. The purchase of McNeil

Surgical in February 2013 will further strengthen our position in this

growing sector.

Although sales in our food processor business increased in 2012, it

performed below expectations. The business is continuing to develop

expertise with major national non-meat food processors which diversifies

and balances our stronger position with retail supermarkets. We are also

growing in our traditional markets by introducing a number of new product

development initiatives. The business has created capacity for continued

growth and made a number of operational improvements, recently

implementing scanning technology into the warehouse operations,

to improve accuracy and increase productivity in the future.

Our catering equipment businesses had a disappointing year as

we continued to be challenged by further softening in the traditional

hospitality markets. To offset this, the business has been refocusing its

+22%

RISE IN OPERATING PROFIT AT

CONSTANT EXCHANGE RATES DUE

TO STRONG ORGANIC GROWTH AND

IMPACT FROM ACQUISITIONS.

efforts to grow market share in the more resilient healthcare and resources

sectors. During the year we successfully integrated our largest business

onto the main IT platform which has improved operational performance

and increased efficiency and service levels.

Our business in Australasia continues to invest in infrastructure and

technology to enable the business to grow efficiently. During 2012 two

ofour business units successfully relocated their New South Wales

operations into our new 20,000m2 distribution centre in the Sydney

suburb of Enfield. This facility will improve operational efficiency and

represents a major investment to facilitate future growth in Australia’s

most populated region. In 2013 we will consolidate two further facilities

into this location as their current property leases expire.

In Brazil our personal protection equipment businesses performed well

despite the continuing slowdown in the rate of economic growth as the

year progressed and weakness in the Brazilian real which particularly

impacted import prices. Danny, the redistribution business with a focus

on own brands acquired in November 2011, was successfully integrated

into the Group and launched a series of new products. Prot Cap also grew

and increased its profitability, partly as a result of new customer wins

particularly in the oil and gas sectors which are continuing to expand, and

developed some important relationships with additional suppliers which

has enhanced our product offering. The recent acquisition of Vicsa Brasil,

which was completed on 19 February 2013, complements and further

extends our range of safety products.

Ideal, the cleaning and hygiene business which was also acquired in

2011, gained a number of new accounts in the retail sector and was

able to realise operational efficiencies and increase the operating

margin through the implementation of a new IT system and a logistics

restructuring programme.

The purchase in December of Vicsa Safety with its operations in Chile,

Peru, Argentina, Colombia and Mexico, expands our personal protection

equipment business in the region outside Brazil and provides Bunzl with

an exciting first entry into five high growth safety markets.

‘ OUR BUSINESS IN AUSTRALASIA HAS

CONTINUED TO IMPROVE ITS OPERATIONAL

EFFICIENCY THROUGH INVESTMENT IN

NEW FACILITIES AND TECHNOLOGY WHICH

SHOULD FACILITATE FURTHER GROWTH.’

Kim Hetherington

Managing Director Australasia

‘ OUR EXPANSION INTO NEW COUNTRIES IN

SOUTH AMERICA NOT ONLY EXTENDS OUR

SAFETY BUSINESS IN THE REGION BUT

ALSO PROVIDES A PLATFORM FOR FUTURE

GROWTH INTO OTHER MARKET SECTORS. ’

Rodrigo Mascarenhas

Managing Director South America

20 BUNZL PLC ANNUAL REPORT 2012

DELIVERING

CHIEF EXECUTIVE’S REVIEW CONTINUED

WITH OUR FLEETS OF DELIVERY VEHICLES AND THIRD PARTY

CARRIERS, WE ARE ABLE TO GET PRODUCTS TO OUR CUSTOMERS

IN A TIMELY MANNER. WHETHER DELIVERIES ARE DAILY, WEEKLY

OR MONTHLY, WE WORK WITH OUR CUSTOMERS TO MEET THEIR

REQUIREMENTS AND ENABLE THEM TO FOCUS ON THEIR CORE

BUSINESSES, HELPING TO INCREASE THE EFFICIENCY AND

COMPETITIVENESS OF THEIR OPERATIONS.

BUNZL PLC ANNUAL REPORT 2012 21

ON TIME TO

KEEP YOUR

BUSINESS MOVING

22 BUNZL PLC ANNUAL REPORT 2012

GROUP PERFORMANCE

Revenue increased by 6% at constant exchange rates to £5,359.2 million

(2011: £5,109.5 million) reflecting organic growth and the benefit

of acquisitions net of the disposal of the UK vending business in August

2011. Operating profit before intangible amortisation and acquisition

related costs increased by 7% at constant exchange rates to £352.4

million (2011: £335.7 million) as a result of the revenue growth and the

operating profit margin at constant exchange rates increasing from 6.5%

to 6.6%. Currency translation had a 1% to 2% negative impact on the

results for the year principally due to some weakening of the euro and

the Brazilian real, partially offset by the strengthening of the US dollar.

At actual exchange rates, both revenue and operating profit before

intangible amortisation and acquisition related costs increased by 5%.

Intangible amortisation and acquisition related costs of £58.6 million

were up £2.2 million due to a £2.3 million increase in transaction costs

and expenses and a £1.2 million increase in intangible amortisation,

partially offset by a £1.3 million decrease in net deferred consideration

payments relating to the continued employment of former owners of

businesses acquired and earn outs.

The net interest charge of £28.5 million was down £1.1 million on 2011,

principally due to lower average net debt levels. Interest cover improved

to 12.4 times compared to 11.3 times in 2011.

The profit on disposal of business of £4.0 million reflects the reassessment

of provisions relating to the disposal of the UK vending business in 2011

(2011: loss of £56.0 million).

Profit before income tax, intangible amortisation, acquisition related

costs and disposal of business was £323.9 million (2011: £306.1 million),

up 8% on 2011 at constant exchange rates and up 6% at actual exchange

rates, due to the growth in operating profit before intangible amortisation

and acquisition related costs and the benefit from the lower

interestcharge.

TAX

A tax charge at a rate of 27.7% (2011: 27.5%) has been provided on

the profit before tax, intangible amortisation, acquisition related costs

and disposal of business. Including the impact of intangible amortisation

of £47.7 million, acquisition related costs of £10.9 million, the profit on

disposal of business of £4.0 million and the associated deferred and

current tax of £15.7 million, the overall tax rate is 27.5% (2011: 36.1%).

The underlying tax rate of 27.7% is higher than the nominal UK rate of

24.5% for 2012 principally because many of the Group’s operations are

in countries with higher tax rates.

PROFIT FOR THE YEAR

Profit after tax of £195.3 million was up £71.5 million, primarily due

to the non-recurrence of the £56.0 million loss on disposal of vending

in 2011 and the 6% increase in profit before income tax, intangible

amortisation, acquisition related costs and disposal of business.

EARNINGS

The weighted average number of shares increased to 326.1 million from

324.0 million due to employee option exercises, partially offset by shares

being purchased from the market into the Company’s employee benefit

trust. Earnings per share were 59.9p, up 57% on 2011, principally due

to the non-recurrence of the loss on disposal of business in 2011. After

adjusting for intangible amortisation, acquisition related costs and the

respective associated tax and the profit/loss on disposal of business,

earnings per share were 71.8p, an increase on 2011 of 7% at constant

exchange rates and 5% at actual exchange rates.

The intangible amortisation and associated tax and the profit/loss on

disposal of business are non-cash charges which are not taken into

account by management when assessing the underlying performance

of the business. Similarly, the acquisition related costs and associated tax

do not relate to the underlying performance of the business. Accordingly,

such charges are removed in calculating the adjusted earnings per

share on which management assesses the performance of the Group.

DIVIDENDS

An analysis of dividends per share for the years to which they relate is

shown below:

2012 2011 Growth

Interim dividend (p) 8.80 8.05 9%

Final dividend (p) 19.40 18.30 6%

Total dividend (p) 28.20 26.35 7%

Dividend cover (times)* 2.5 2.6

*Based on adjusted earnings per share

ACQUISITIONS

The principal acquisitions made or agreed to be made in 2012 were

CDW Merchants, the redistribution business of Star Services International,

FoodHandler, Zahav, Service Paper, Distrimondo, Indigo Concept

Packaging, Atlas Health Care, McCordick Glove & Safety, Vicsa Safety,

Vicsa Brasil, Destiny Packaging and Schwarz Paper Company. Annualised

revenue and operating profit before intangible amortisation and acquisition

related costs of the businesses acquired or agreed to be acquired were

£518.4 million and £36.1 million respectively. A summary of the effect

of acquisitions is as follows:

£m

Fair value of assets acquired 156.5

Goodwill 63.6

Consideration 220.1

Satisfied by:

cash consideration 206.0

deferred consideration 13.1

other consideration 1.0

220.1

Contingent payments to former owners 16.3

Net bank overdrafts acquired 21.8

Transaction costs and expenses 6.9

Total expected spend in respect of current year

completed acquisitions 265.1

Committed spend in respect of current year

acquisitions not completed 7.2

Total committed spend in respect of current year acquisitions 272.3

The net cash outflow in the year in respect of acquisitions comprised:

£m

Cash consideration 206.0

Net bank overdrafts acquired 21.8

Deferred consideration in respect of prior year acquisitions 6.7

Net cash outflow in respect of acquisitions 234.5

Acquisition related costs 20.2

Total cash outflow in respect of acquisitions 254.7

FINANCIAL REVIEW

‘ COMMITTED ACQUISITION SPEND OF

£272 MILLION WILL ADD MORE THAN

£500 MILLION OF ANNUALISED REVENUE.’

Brian May

Finance Director

BUNZL PLC ANNUAL REPORT 2012 23

CASH FLOW

Cash generated from operations before acquisition related costs was

£349.1 million, a £41.0 million decrease from 2011, primarily due to

a working capital outflow in 2012 of £22.4 million compared to a

£31.4 million inflow in 2011, attributable to a particularly low working

capital level at the end of 2011, partially offset by a £17.8 million increase

in profit before tax, intangible amortisation, acquisition related costs and

disposal of business. The Group’s free cash flow of £234.7 million was

down £40.5 million from 2011. After payment of dividends of £85.7

million in respect of 2011, a £3.7 million outflow on employee share

schemes and an acquisition cash outflow of £254.7 million, the net cash

outflow was £109.4 million. The summary cash flow for the year was

asfollows:

£m

Cash generated from operations* 349.1

Net capital expenditure (20.2)

Operating cash flow* 328.9

Operating cash flow* to operating profit†93%

Net interest (30.6)

Tax (63.6)

Free cash flow 234.7

Dividends (85.7)

Acquisitions (254.7)

Employee share schemes (3.7)

Net cash outflow (109.4)

*Before acquisition related costs

†Before intangible amortisation and acquisition related costs

BALANCE SHEET

Return on average operating capital employed before intangible

amortisation and acquisition related costs decreased to 56.4% from

57.4% in 2011 due to the impact of acquisitions having a lower return

on operating capital than the rest of the Group. Return on invested capital

increased from 17.3% in 2011 to 17.9% due to a combination of improved

returns in the underlying business and the disposal of the UK vending

business, partly offset by the impact of recent acquisitions. Intangible

assets increased by £66.1 million to £1,322.9 million reflecting goodwill

and customer relationships arising on acquisitions in the year of £158.3

million, partially offset by an amortisation charge of £47.7 million and a

reduction of £44.5 million due to exchange. The Group’s pension deficit

of £75.5 million at 31December 2012 was £1.2 million higher than at

31December 2011, with an actuarial loss of £13.5 million and a service

cost of £5.4 million being largely offset by contributions of £13.2 million,

a net financial return of £2.2 million and an exchange gain of £2.3 million.

The actuarial loss arose primarily as a result of the £28.8 million impact of

changes in assumptions relating to the present value of scheme liabilities,

principally due to lower discount rates, partially offset by the actual return

on scheme assets being £15.3 million higher than expected.

The movements in shareholders’ equity and net debt during the year were

as follows:

Shareholders’ equity £m

At 1 January 2012 806.7

Profit for the year 195.3

Dividends (85.7)

Currency (30.4)

Actuarial loss on pension schemes (13.5)

Share based payments 11.1

Other 2.0

At 31 December 2012 885.5

Net debt £m

At 1 January 2012 (652.9)

Net cash outflow (109.4)

Currency 24.2

At 31 December 2012 (738.1)

Net debt to EBITDA (times) 1.8

EXCHANGE RATES

Average 2012 2011

US$: £ 1.59 1.60

€: £ 1.23 1.15

A$: £ 1.53 1.55

C$: £ 1.58 1.59

Brazilian real: £ 3.10 2.68

Closing 2012 2011

US$: £ 1.63 1.55

€: £ 1.23 1.20

A$: £ 1.57 1.52

C$: £ 1.62 1.58

Brazilian real: £ 3.33 2.90

CAPITAL MANAGEMENT

The Group’s policy is to maintain a strong capital base so as to maintain

investor, creditor and market confidence and to sustain future

development of the business.

The Group monitors the return on average operating capital employed and

the return on invested capital as well as the level of total shareholders’

equity and the amount of dividends paid to ordinary shareholders.

The Group funds its operations through a mixture of shareholders’ equity

and bank and capital market borrowings. All of the borrowings are

managed by a central treasury function and funds raised are lent onward

to operating subsidiaries as required. The overall objective is to manage

the funding to ensure the Group has a portfolio of competitively priced

borrowing facilities to meet the demands of the business over time and,

in order to do so, the Group arranges a mixture of borrowings from

different sources with a variety of maturity dates.

The Group’s businesses provide a high and consistent level of cash

generation which helps fund future development and growth. The Group

seeks to maintain an appropriate balance between the higher returns that

might be possible with higher levels of borrowings and the advantages and

security afforded by a sound capital position.

There were no changes to the Group’s approach to capital management

during the year and the Group is not subject to any externally imposed

capital requirements.

TREASURY POLICIES AND CONTROLS

The Group has a centralised treasury department to control external

borrowings and manage liquidity, interest rate and foreign currency risks.

Treasury policies have been approved by the Board and cover the nature

of the exposure to be hedged, the types of financial instruments that may

be employed and the criteria for investing and borrowing cash. The Group

uses derivatives to manage its foreign currency and interest rate risks

arising from underlying business activities. No transactions of a speculative

nature are undertaken. The treasury department is subject to periodic

independent review by the internal audit department. Underlying policy

assumptions and activities are periodically reviewed by the executive

directors and the Board. Controls over exposure changes and transaction

authenticity are in place.

HEDGE ACCOUNTING

The Group designates derivatives which qualify as hedges for accounting

purposes as either (a) a hedge of the fair value of a recognised asset or

liability; (b) a hedge of the cash flow risk resulting from changes in interest

rates or foreign exchange rates; or (c) a hedge of a net investment in a

foreign operation. The Group tests the effectiveness of hedges on a

prospective and retrospective basis to ensure compliance with IAS 39

‘Financial Instruments: Recognition and Measurement’. Methods for

testing effectiveness include dollar offset, critical terms and

regressionanalysis.

24 BUNZL PLC ANNUAL REPORT 2012

161

BANK FACILITIES – UNDRAWN

BANK FACILITIES – DRAWN

US DOLLAR AND STERLING BONDS

13 14 16 17 18

147

31 32

112

67

31

49

86

80

50

50

123

33

287

19 20 21 22 23

59 41 32

67

15

LIQUIDITY RISK

Liquidity risk is the risk that the Group will not be able to meet its financial

obligations as they fall due. The Group continually monitors net debt and

forecast cash flows to ensure that sufficient facilities are in place to meet

the Group’s requirements in the short, medium and long term and, in

order to do so, arranges borrowings from a variety of sources. Additionally,

compliance with the Group’s biannual debt covenants is monitored on a

monthly basis. The principal covenant limits are net debt to EBITDA of no

more than 3.5 times and interest cover of no less than 3.0 times. Sensitivity

analyses using various scenarios are applied to forecasts to assess their

impact on covenants and net debt. During 2012 all covenants have been

complied with and based on current forecasts it is expected that such

covenants will continue to be complied with for the foreseeablefuture.

The Group has substantial borrowing facilities available to it comprising

multi-currency credit facilities from the Group’s banks and US dollar and

sterling bonds. During the year an issue of fixed interest rate US dollar bonds

was agreed for a total value of US$350.0 million of which US$110.0

million was drawn down in December 2012 and US$240.0 million is

due to be drawn by the Group in April 2013 to refinance bonds which

are maturing. At 31 December 2012 the total bonds outstanding were

£618.9 million (2011: £585.1 million) with maturities ranging from 2013

to 2023. During the year the Group also refinanced or agreed new banking

facilities totalling £150.7 million. The Group’s committed bank facilities

mature between 2013 and 2017. At 31December 2012 the available

committed bank facilities totalled £758.5 million (2011: £730.8 million)

of which £169.2 million (2011: £109.3 million) was drawn down. The

undrawn committed facilities available to the Group at 31 December 2012

were £589.3 million (2011: £621.5 million). The committed facilities

maturity profile at 31 December 2012 is set out in the chart below.

INTEREST RATE RISK

The Group is funded by a mixture of fixed and floating rate debt. In

addition, interest rate swaps and interest rate caps are used to manage

the interest rate risk profile. At 31 December 2012 fixed rate debt of

£472.2 million (2011: £425.2 million) related to fixed rate US dollar and

sterling bonds stated at amortised cost with maturities ranging from

2014 to 2023.

At 31 December 2012 floating rate debt comprised £174.3 million of

floating rate bank loans (2011: £109.3 million) and £146.7 million of fixed

rate US dollar bonds which have been swapped to floating rates using

interest rate swaps (2011: £159.9 million). Bank loans are drawn for

various periods of up to three months at interest rates linked to LIBOR.

The interest rate swaps reprice every three or six months.

The interest rate risk on the floating rate debt is managed using interest

rate options. Borrowings with a notional principal of £162.6 million were

capped at 31 December 2012 (2011: £266.7 million).

FOREIGN CURRENCY RISK

The principal underlying currencies of the Group’s earnings are sterling,

US dollars and euros. The Group does not hedge the impact of exchange

rate movements arising on translation of earnings into sterling at average

exchange rates. For the year ended 31 December 2012, a movement of

one cent in the US dollar and euro average exchange rates would have

changed profit before tax by £0.8 million and £0.3 million respectively

and profit before tax, intangible amortisation, acquisition related costs

and disposal of business by £0.9 million and £0.5 million respectively.

The majority of the Group’s transactions are carried out in the respective

functional currencies of the Group’s operations and so transaction

exposures are usually relatively limited. Where they do occur, the Group’s

policy is to hedge significant exposures of firm commitments for a period

of up to one year as soon as they are committed using forward foreign

exchange contracts and these are designated as cash flow hedges.