Printmgr File BENCHMARK 14/19 Ar 2014 E

User Manual: BENCHMARK 14/19

Open the PDF directly: View PDF ![]() .

.

Page Count: 208 [warning: Documents this large are best viewed by clicking the View PDF Link!]

ROYAL BANK OF CANADA ANNUAL REPORT 2014

RBC IS A

GLOBAL LEADER

Royal Bank of Canada is the largest bank in Canada, and the

12th largest bank in the world, based on market capitalization.

Our approximately 78,000 employees serve over 16 million

personal, business and corporate clients across a diversified

mix of businesses in 40 countries.

Our values define who we are:

Service – Excellent service to clients and each other

Teamwork – Working together to succeed

Responsibility – Personal responsibility for high performance

Diversity – Diversity for growth and innovation

Integrity – Trust through integrity in everything we do

CONTENTS

We Have A Focused

Strategy 1

We Create Long-term Value 2

We Have Five Key Strengths

That Drive Our Success 3

We Deliver Stability &

Opportunity Through

Diversification 4

We Make Communities

Stronger 5

Message from Dave McKay 6

Message from Katie Taylor 9

Management’s Discussion

and Analysis 10

Enhanced Disclosure Task Force

Recommendations Index 107

Reports and Consolidated

Financial Statements 108

Ten-Year Statistical Review 197

Glossary 199

Directors and

Executive Officers 202

Principal Subsidiaries 203

Shareholder Information 204

For more information, please visit: rbc.com

To view our online annual report, please visit:

rbc.com/ar2014

WE HAVE A

FOCUSED STRATEGY

Our client focus, diversified business model and commitment to our

long-term strategic priorities have been fundamental to our growth and

success in the past, and will allow us to continue to create value in the future.

STRATEGIC GOALS

In Canada, to be the

undisputed leader in

financial services

Globally, to be a leading

provider of capital

markets, investor and

wealth management

solutions

In targeted markets, to

be a leading provider of

select financial services

complementary to our

core strengths

2014 KEY HIGHLIGHTS

䊳Gained market share across key

businesses and client segments

䊳Delivered solid volume growth

(loans and deposits)

䊳Launched new products to meet

clients’ evolving needs

䊳Continued to lead the Canadian

league tables

䊳Recognized as Canada’s most

valuable brand

䊳Expanded international distribution

of our U.S. and global asset

management business

䊳Deepened offering and capabilities in

key markets to win new clients and

mandates and to grow market share

䊳Strategically added top talent

within capital markets and wealth

management in the U.S. and

internationally

䊳Continued to optimize Caribbean

banking operations for efficiency

and profitability

䊳Strengthened our cross-border

banking business in the U.S.

2015 STRATEGIC PRIORITIES

1. Extend lead in Canada through largest distribution network and increased efficiency

2. Deepen presence in the U.S., U.K./Europe and key international hubs by expanding capabilities, offering and distribution

3. Lead change with differentiated experiences to help clients achieve their goals

4. Pursue balanced growth opportunities and disciplined use of capital to create value for the long term

5. Maintain robust risk management staying within our risk appetite across our diversified business model

Royal Bank of Canada: Annual Report 2014 1

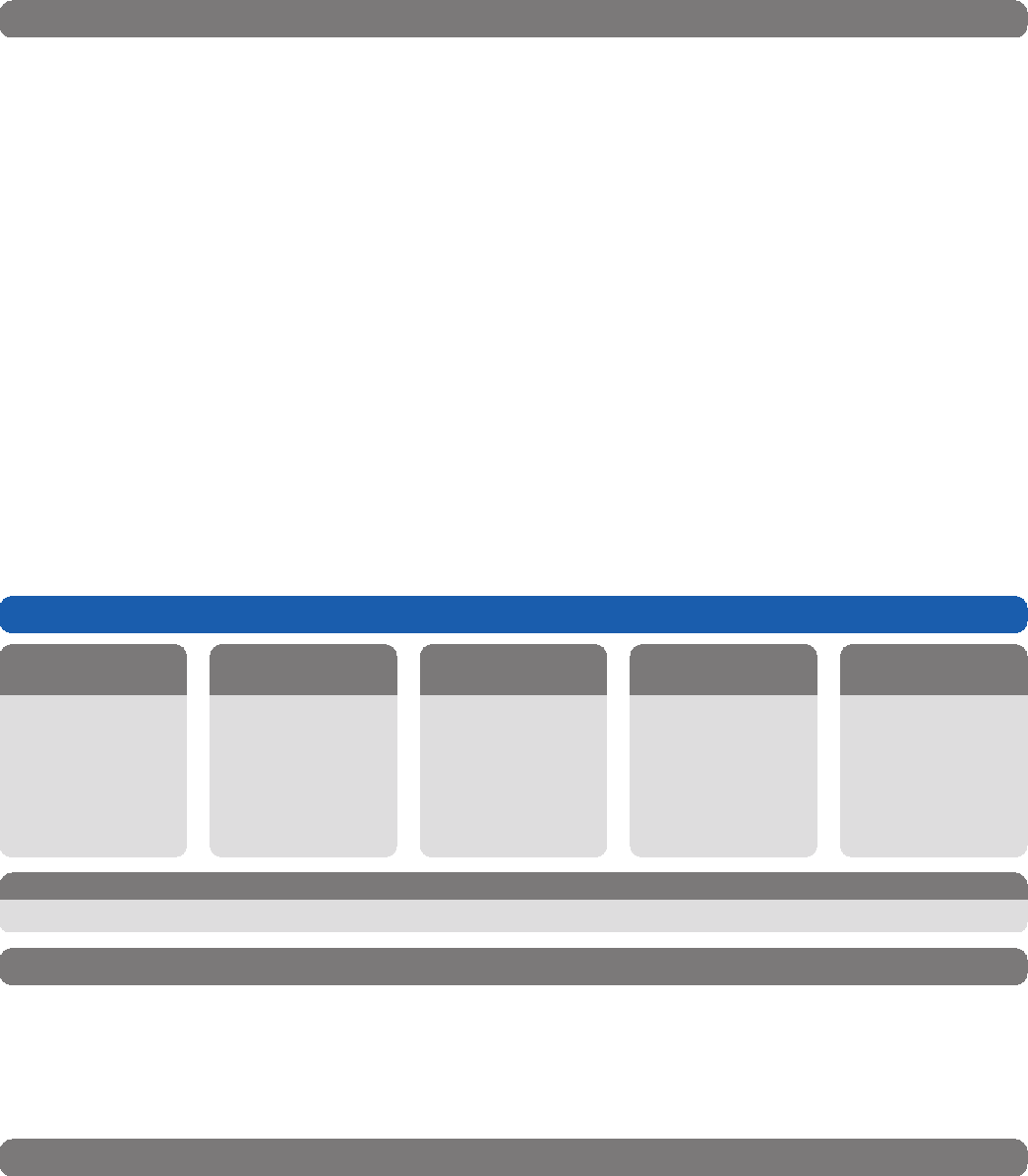

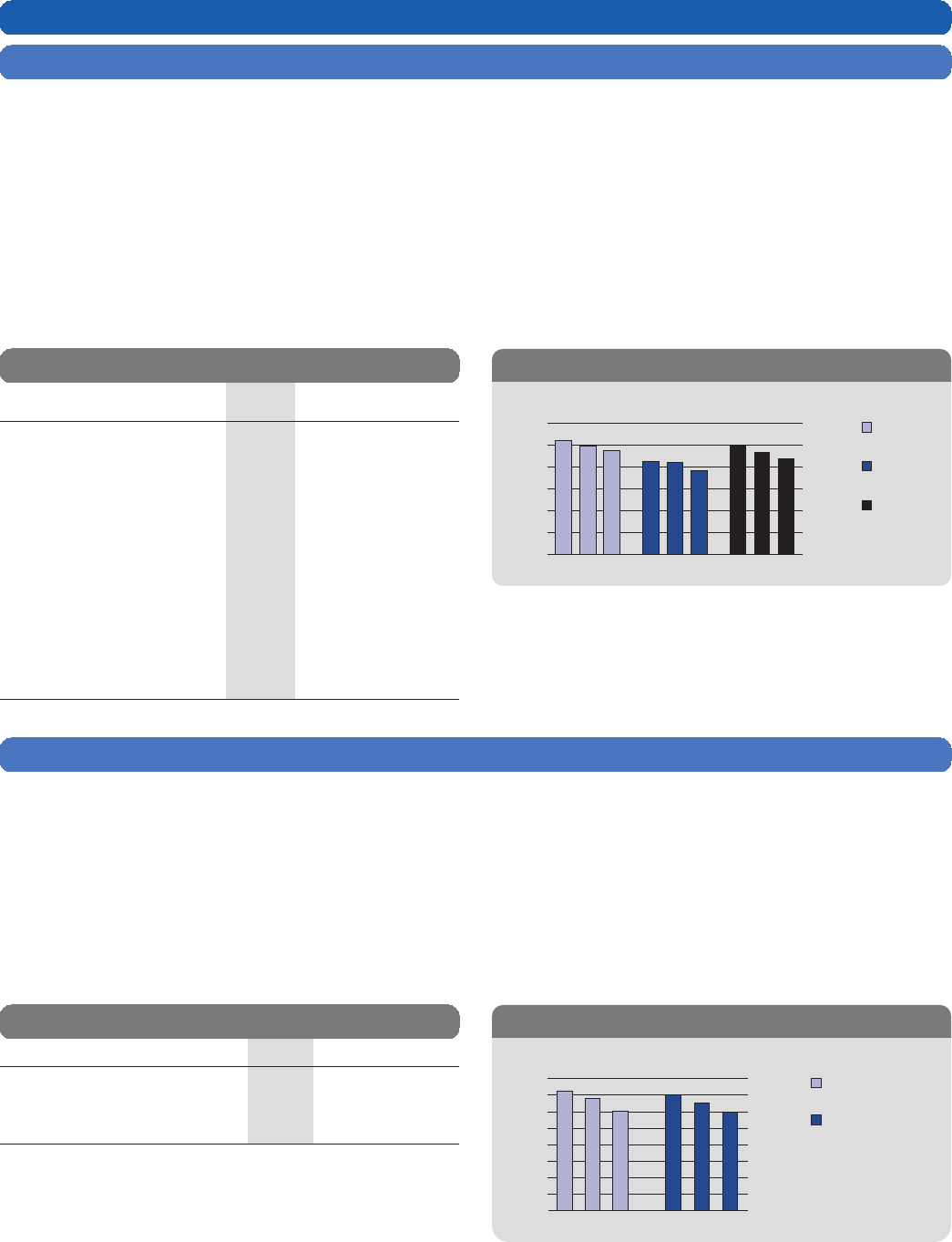

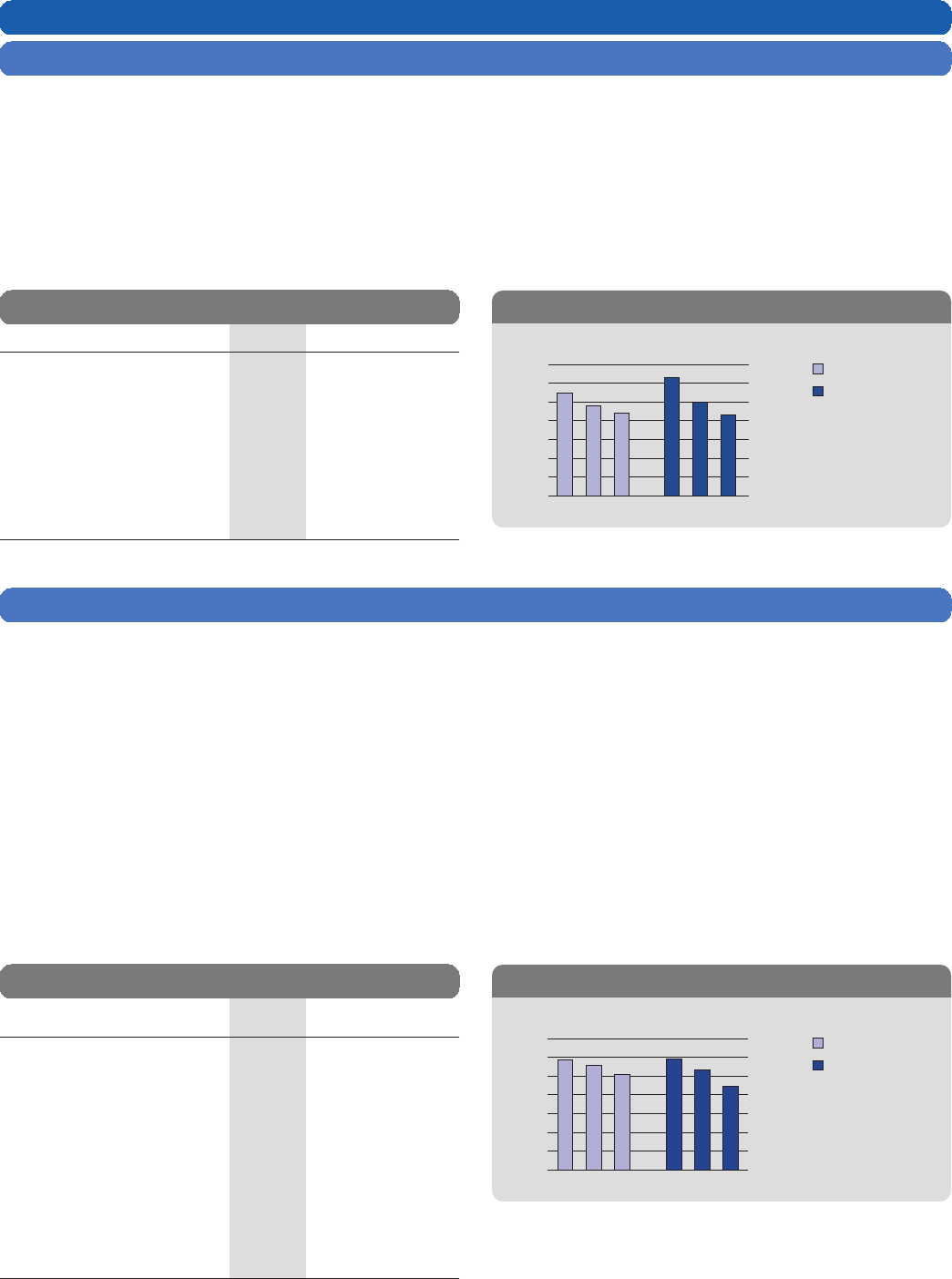

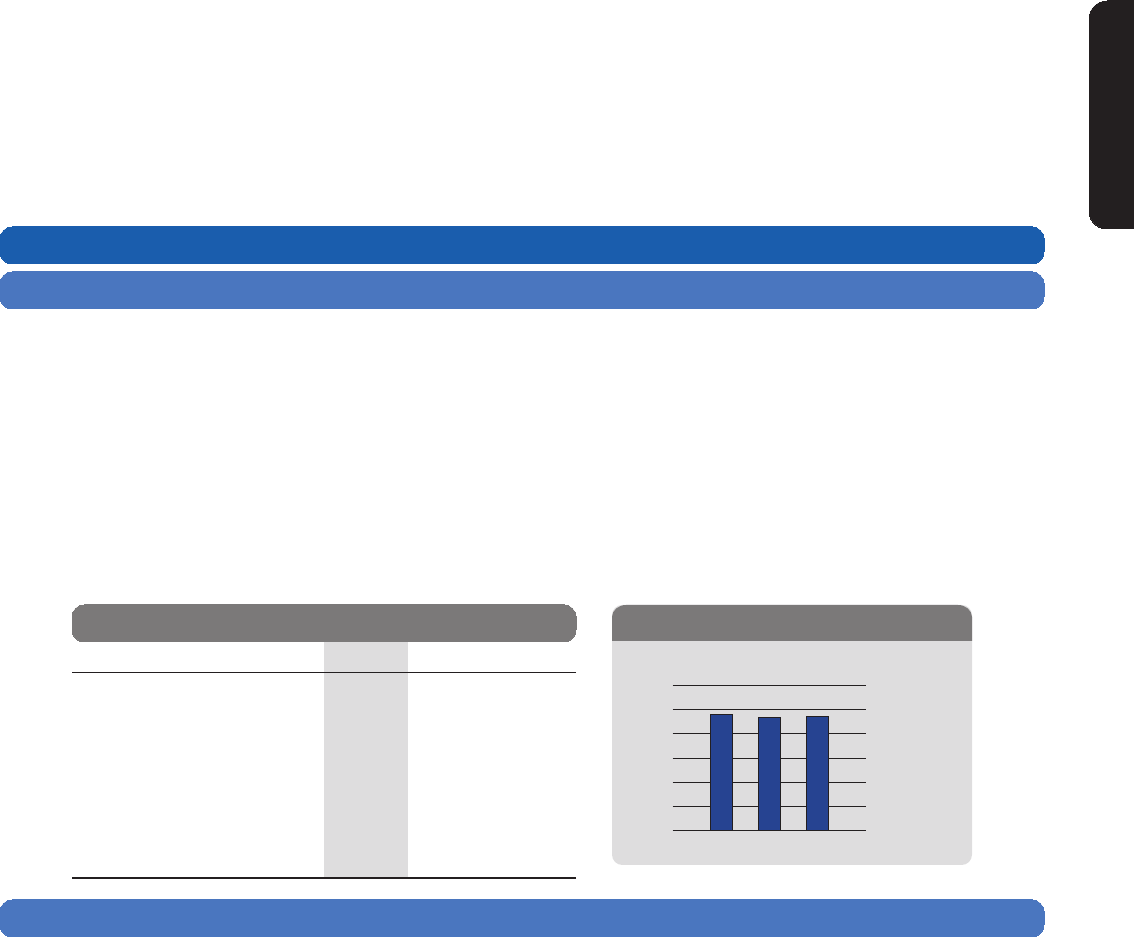

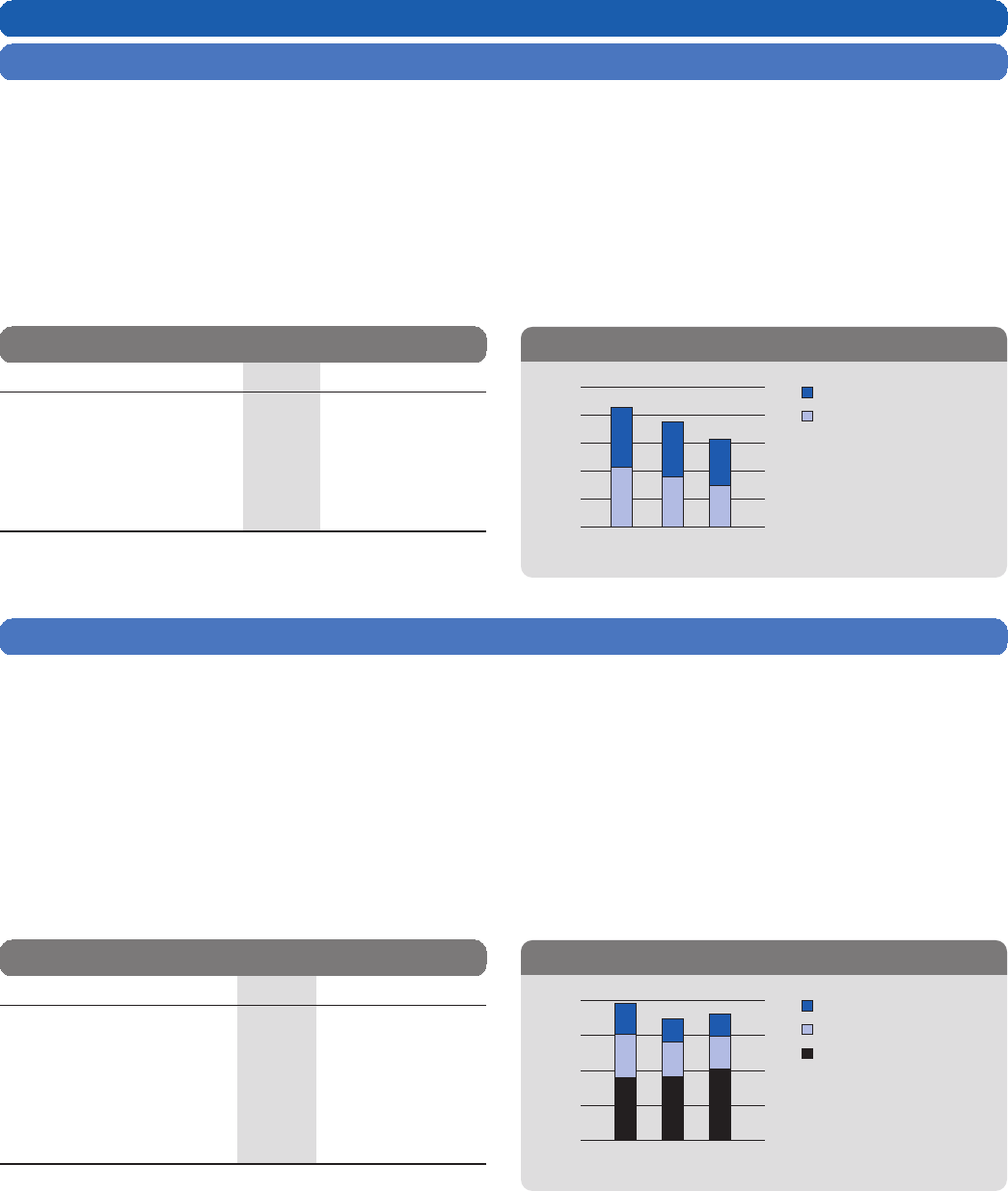

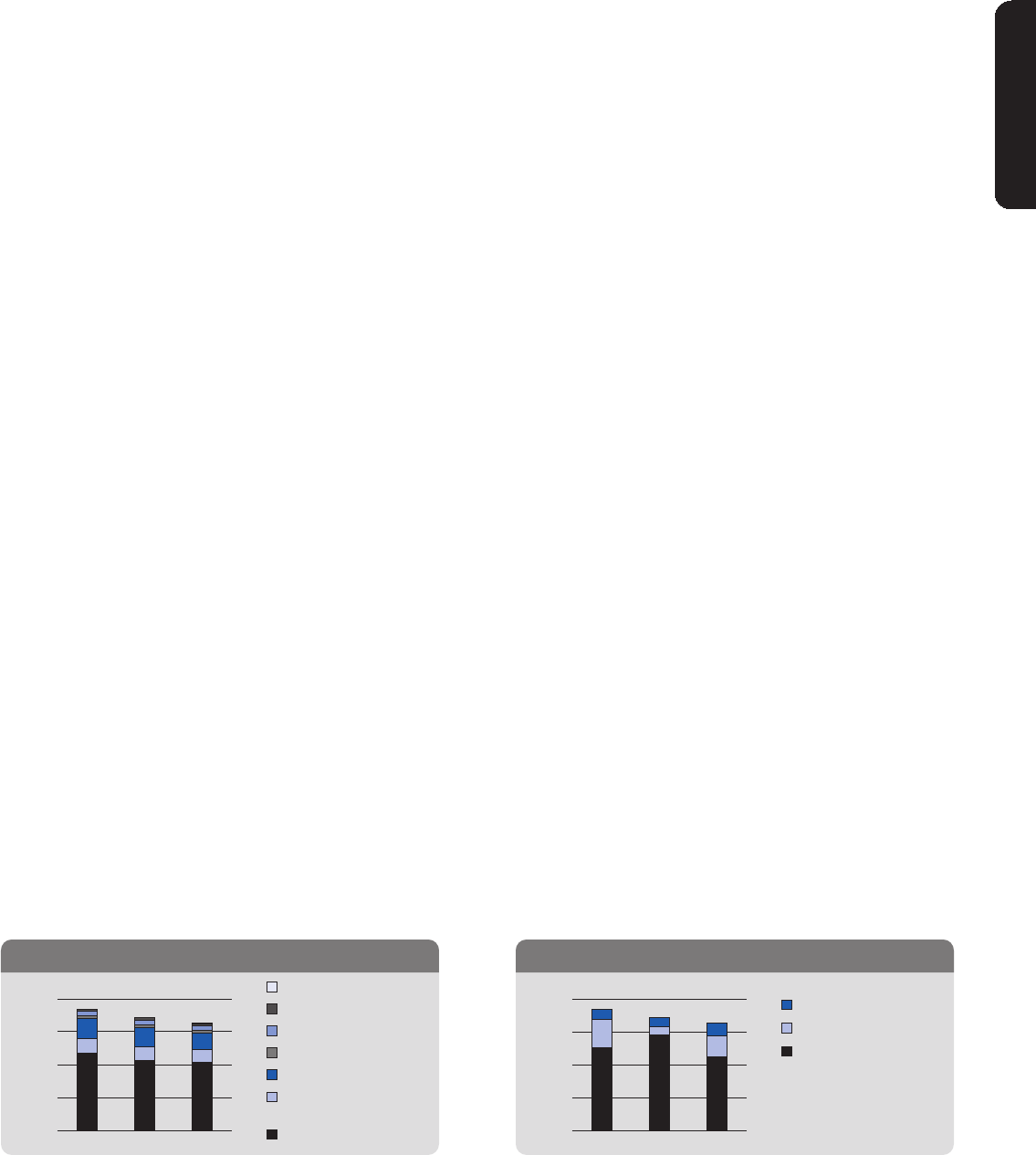

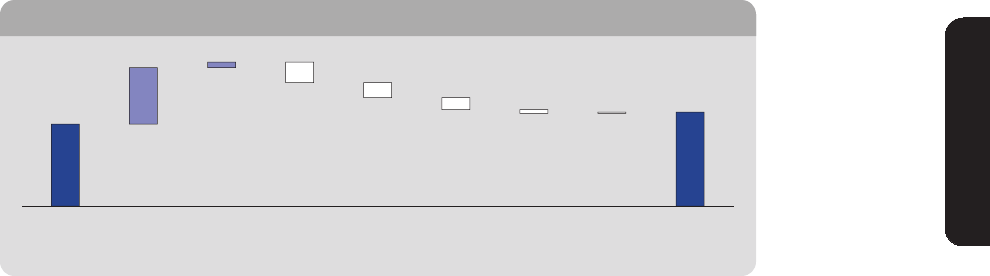

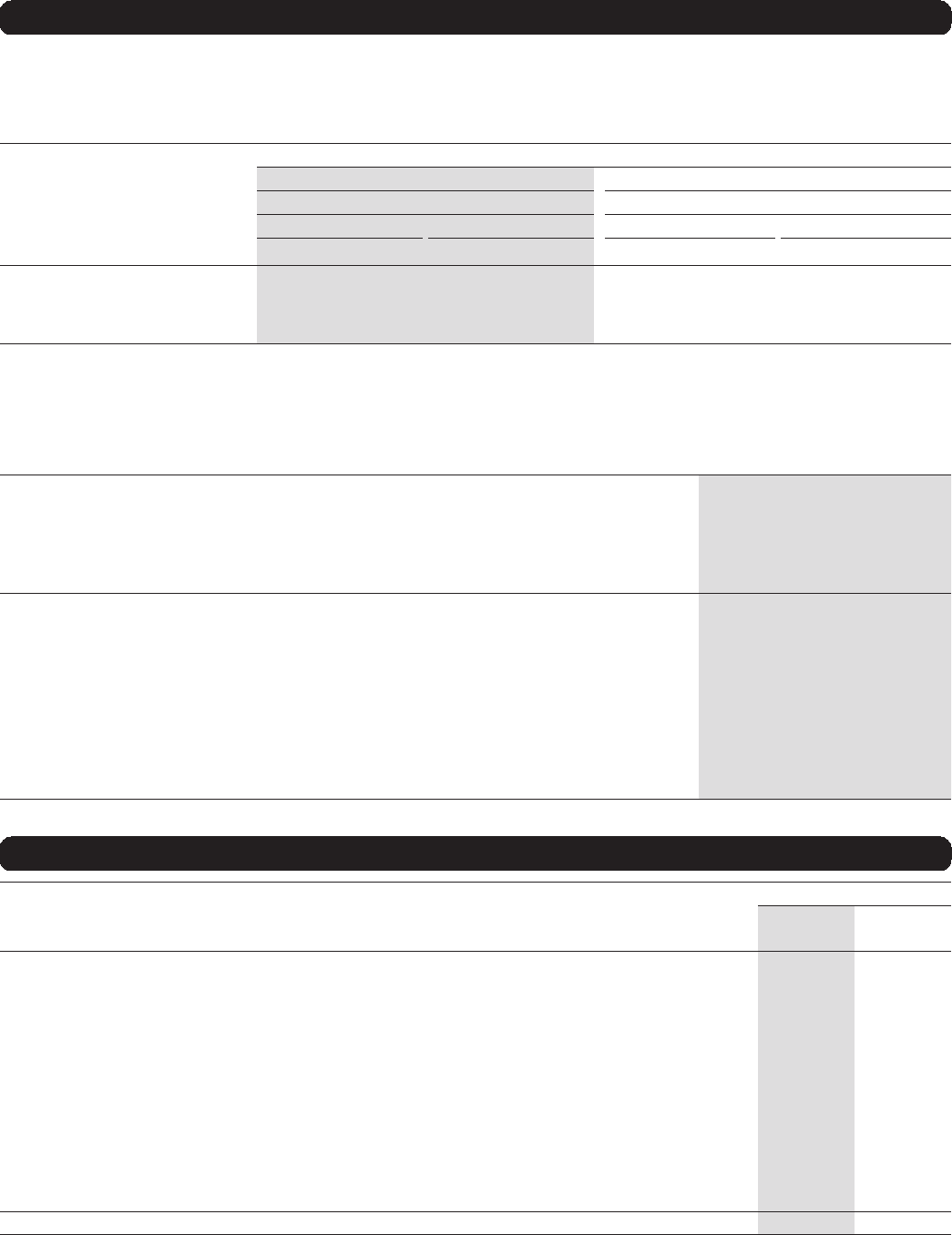

WE CREATE

LONG-TERM VALUE

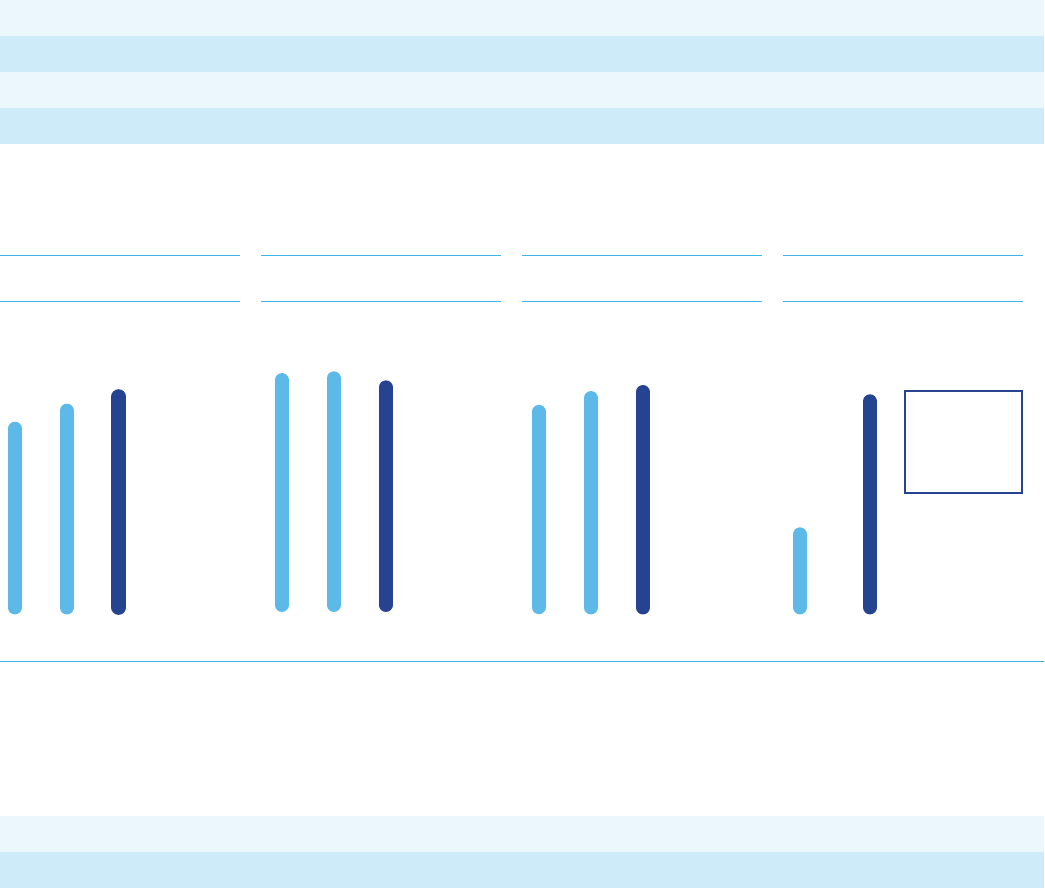

We delivered record earnings and strong returns to shareholders. In 2014, we

grew earnings by 8%, increased our quarterly dividend by 12% compared to

last year, delivered strong return on equity (ROE) of 19% and maintained a

robust capital ratio of 9.9%.

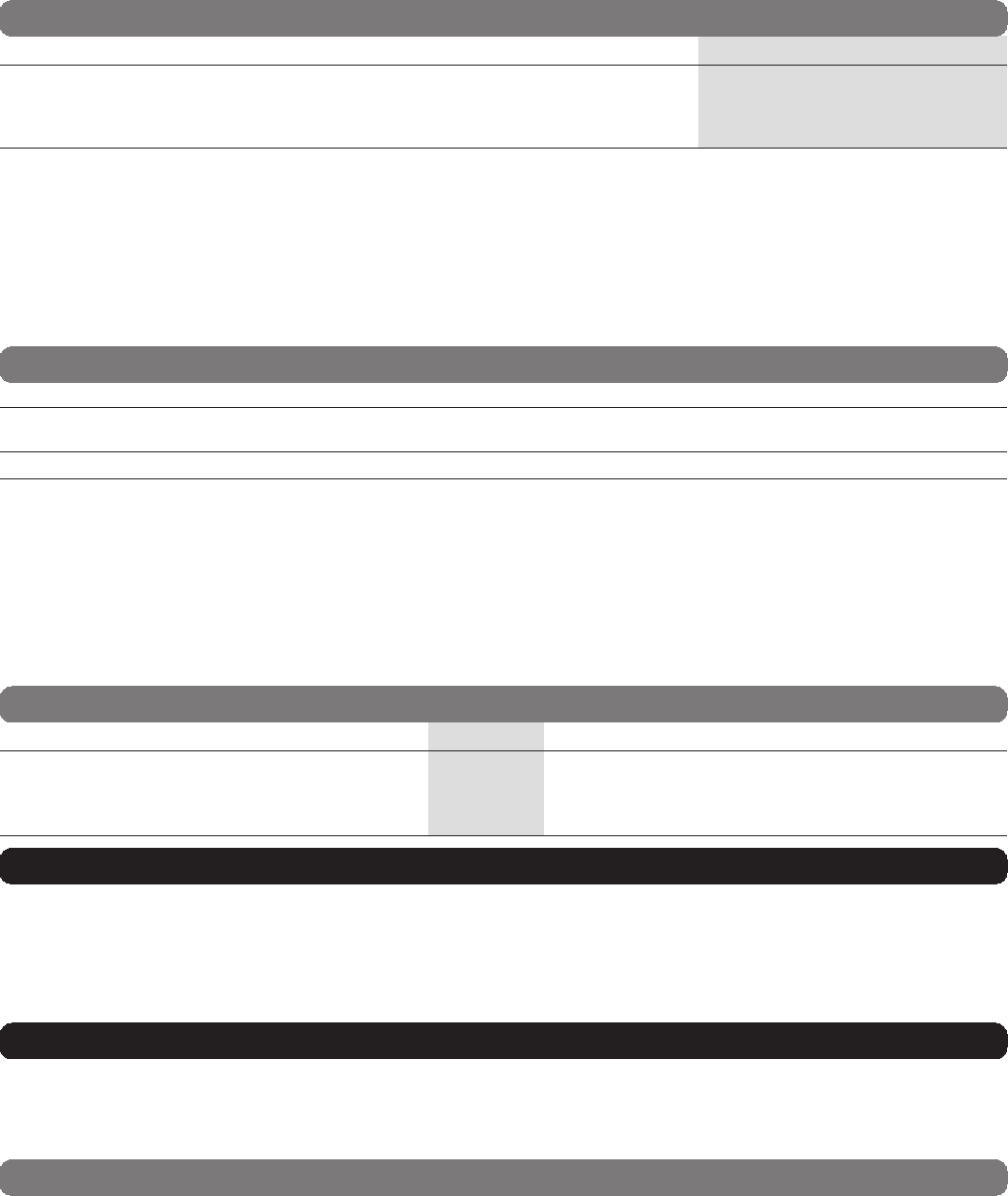

Financial Performance Metric

MEDIUM-TERM OBJECTIVE

(3 TO 5-YEAR)

2014

RESULTS ACHIEVED

Diluted EPS Growth 7%+ 9.3% ✓

Return on Equity 18%+ 19.0% ✓

Capital Ratios (CET1) Strong 9.9% ✓

Dividend Payout Ratio 40%–50% 47% ✓

Strong

Earnings

Profitable

Growth

Financial

Strength

Delivered Returns

to Shareholders

NET INCOME

(C$ BILLION)

RETURN ON EQUITY

(ROE)

COMMON EQUITY TIER 1 (CET1)

CAPITAL RATIO

DIVIDENDS DECLARED

PER SHARE

$9.0

$7.5

$8.3

1412 13

12 13 14

19.0%

19.6% 19.7%

9.9%

8.9% 9.6%

1412 13

(pro forma)

$1.01

04

$2.84

Annualized

dividend

increase of:

12% – 1 yr

11% – 10 yr CAGR

14

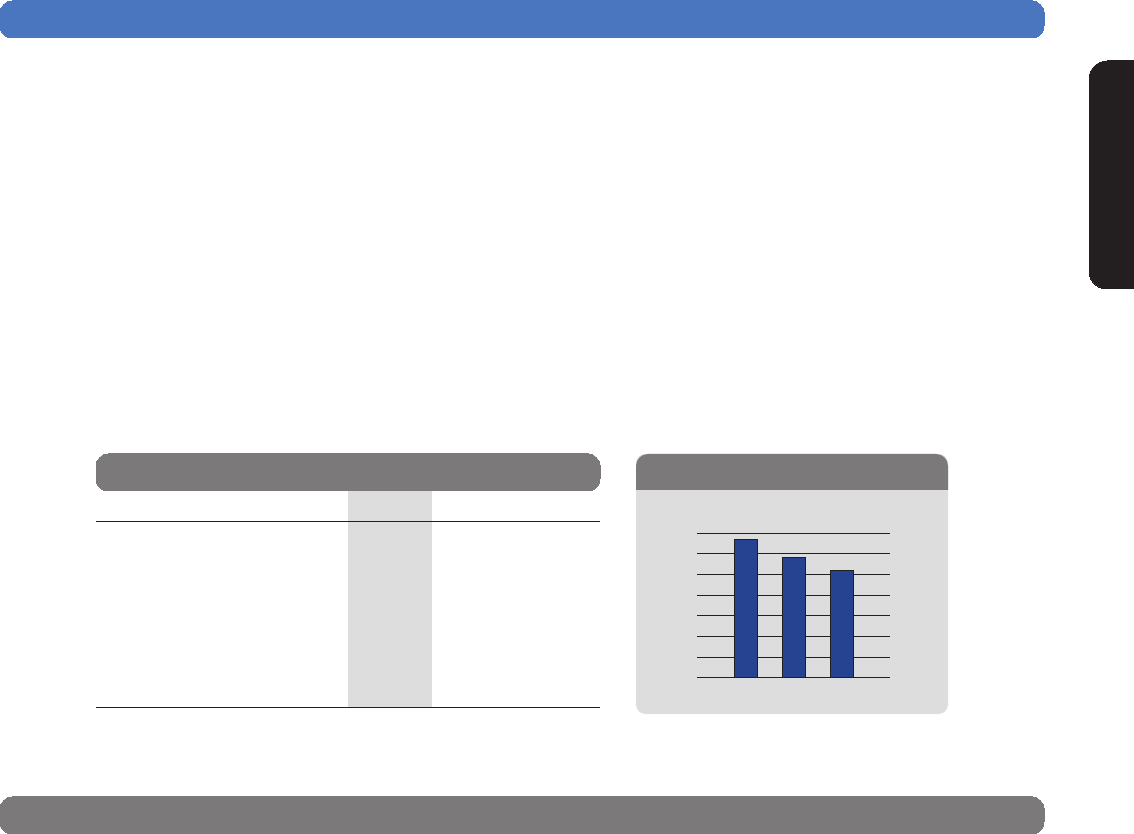

Over the past decade, we’ve delivered a strong annualized total shareholder return (TSR) of 14%, second highest among our global peer

group. Our strong TSR has been underpinned by consistent financial performance and low earnings volatility.

Total Shareholder Return1ONE-YEAR THREE-YEAR FIVE-YEAR TEN-YEAR

RBC 19% 23% 12% 14%

Global Peer Average 11% 19% 8% 5%

1. Compounded annually, as at October 31, 2014. The peer group average excludes RBC; for more information on the list of 19 financial institutions in the peer group, refer to the Financial

performance section of our 2014 Management’s Discussion and Analysis.

2 Royal Bank of Canada: Annual Report 2014

WE HAVE FIVE

KEY STRENGTHS THAT

DRIVE OUR SUCCESS

Our key strengths underpin past performance and provide a strong foundation

for future growth. These strengths enable us to successfully deliver on our

strategy.

DIVERSIFIED

BUSINESS MODEL

SIZE & SCALE IN

CANADA WITH

GLOBAL REACH

CLIENT

FOCUS

EMPLOYEES, BRAND

& REPUTATION

FINANCIAL STRENGTH &

PRUDENT RISK MANAGEMENT

@ Named Bank of the Year

for Canada1

@ Best-in-class client

service, wealth planning

and trust offerings2

@ Received Best Banking

awards for financial

planning, advice and

channel excellence3

@ Recognized as a global

leader among investment

banks in expertise and skill4

@ Diversified by

business, geography

and client segment

@ 37% of revenue from

outside Canada

@ Largest bank in Canada by

market capitalization5

• 5th in North America

• 12th globally

@ 40 countries

@ ~78,000 employees

@ ~16 million clients

@ 4.5+ million active online

& mobile clients

@ ~1,400 branches

@ Consistent earnings and

dividend growth

@ Strong capital position

and credit ratings

@ Prudent risk management

built on a culture of doing

what’s right

@ Named one of the Best Workplaces in

Canada6 for the 6th consecutive year

while attracting talented employees

globally

@ Canada’s most valuable

brand and 16th most

valuable bank brand

globally7

@ One of the World’s

Most Admired

Companies8

1. The Banker. 5. Bloomberg as at Oct. 31, 2014.

2. Private Banker International. 6. The Great Place to Work®Institute.

3. Ipsos – Best Banking Awards. 7. Brand Finance.

4. The Economist. 8. Fortune.

Royal Bank of Canada: Annual Report 2014 3

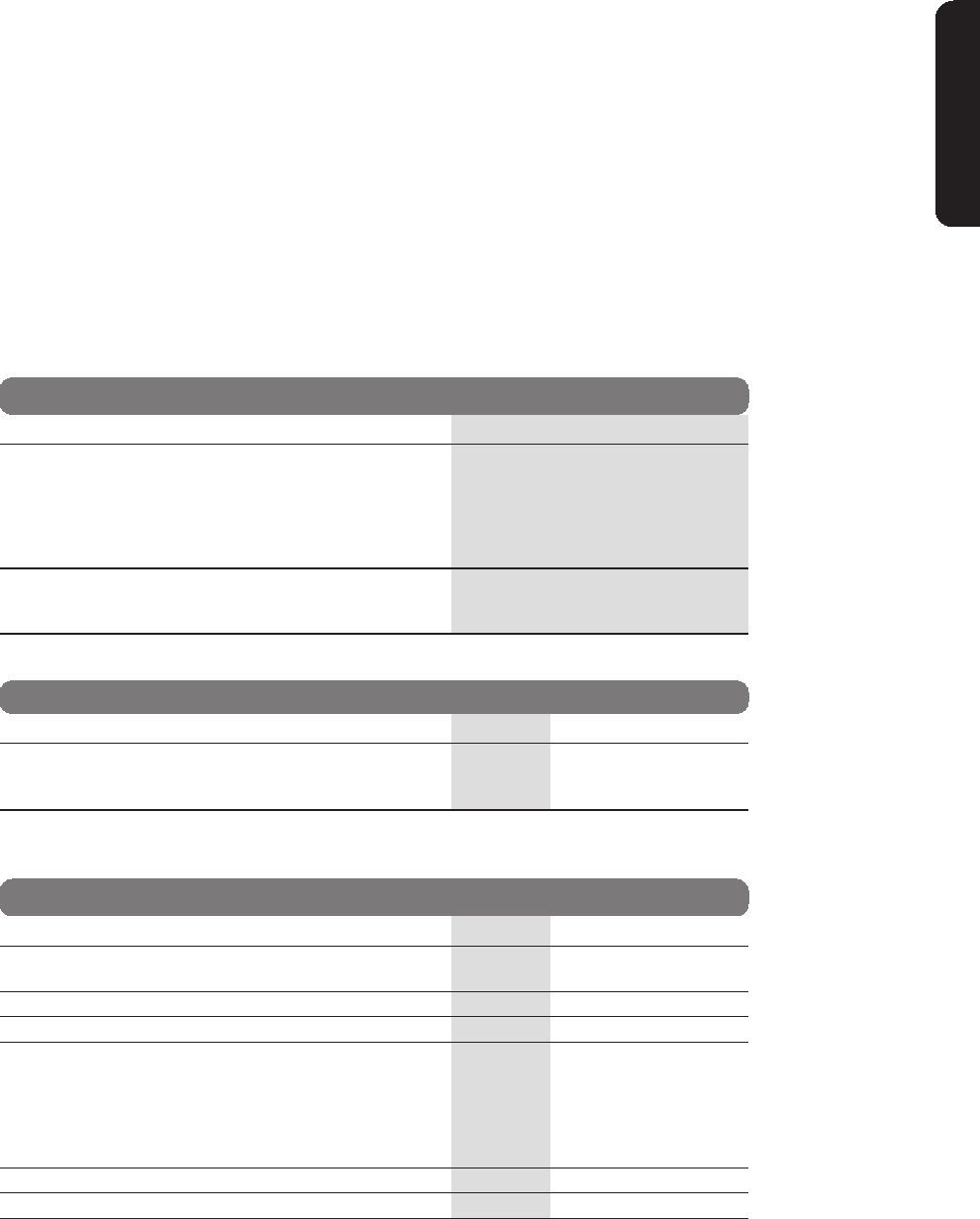

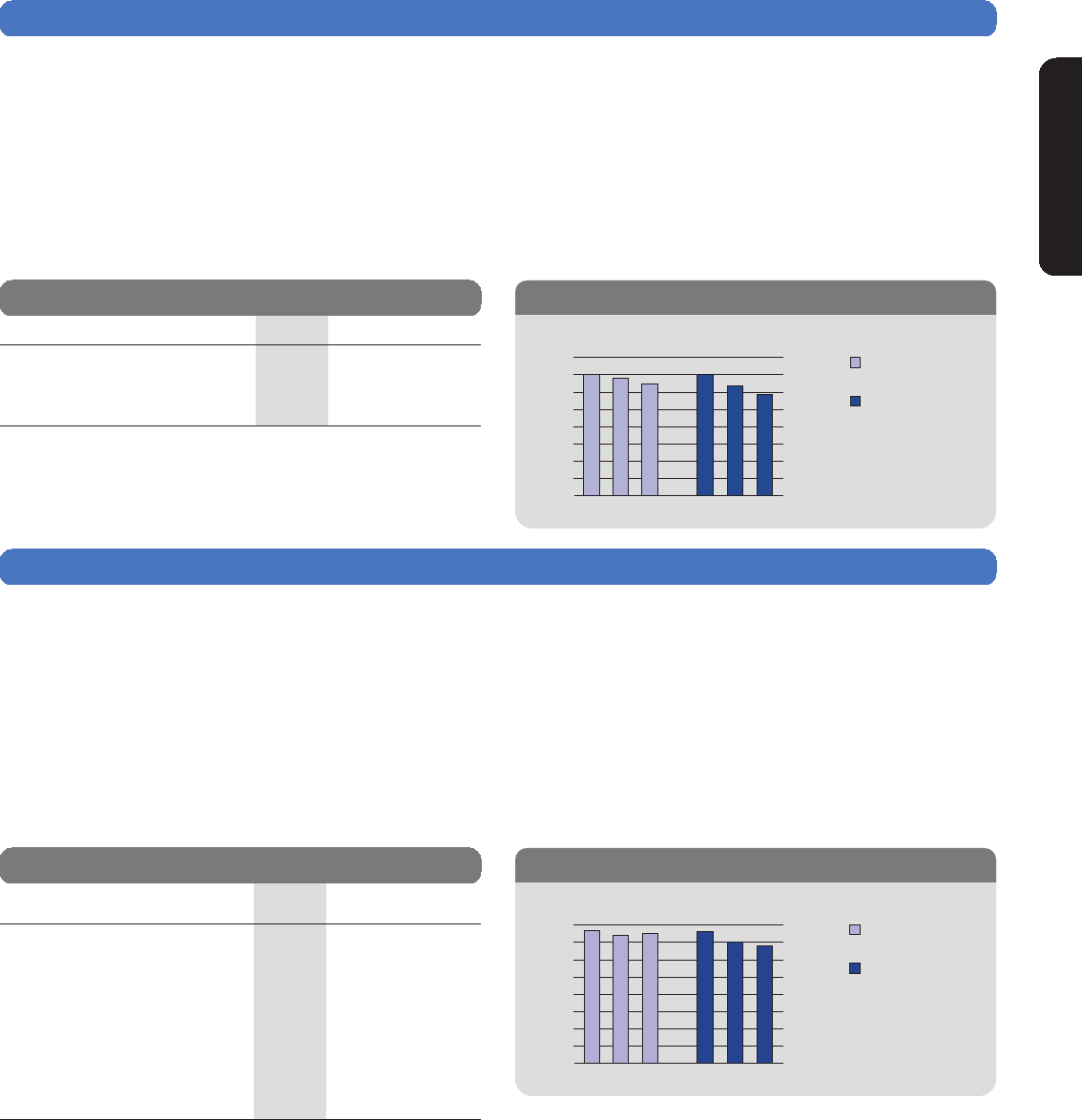

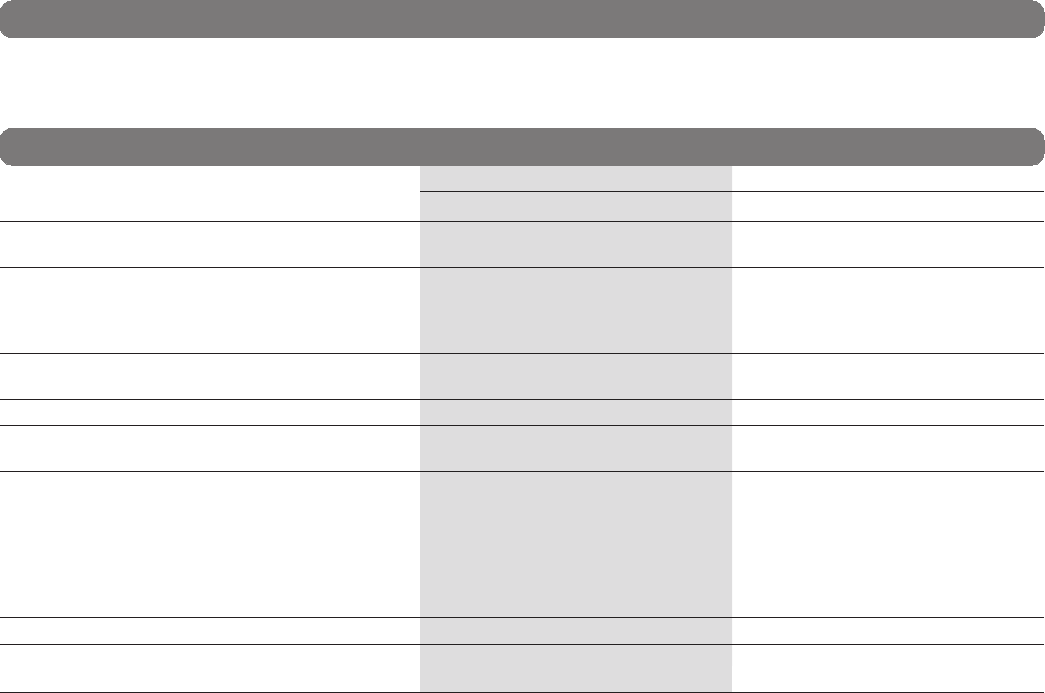

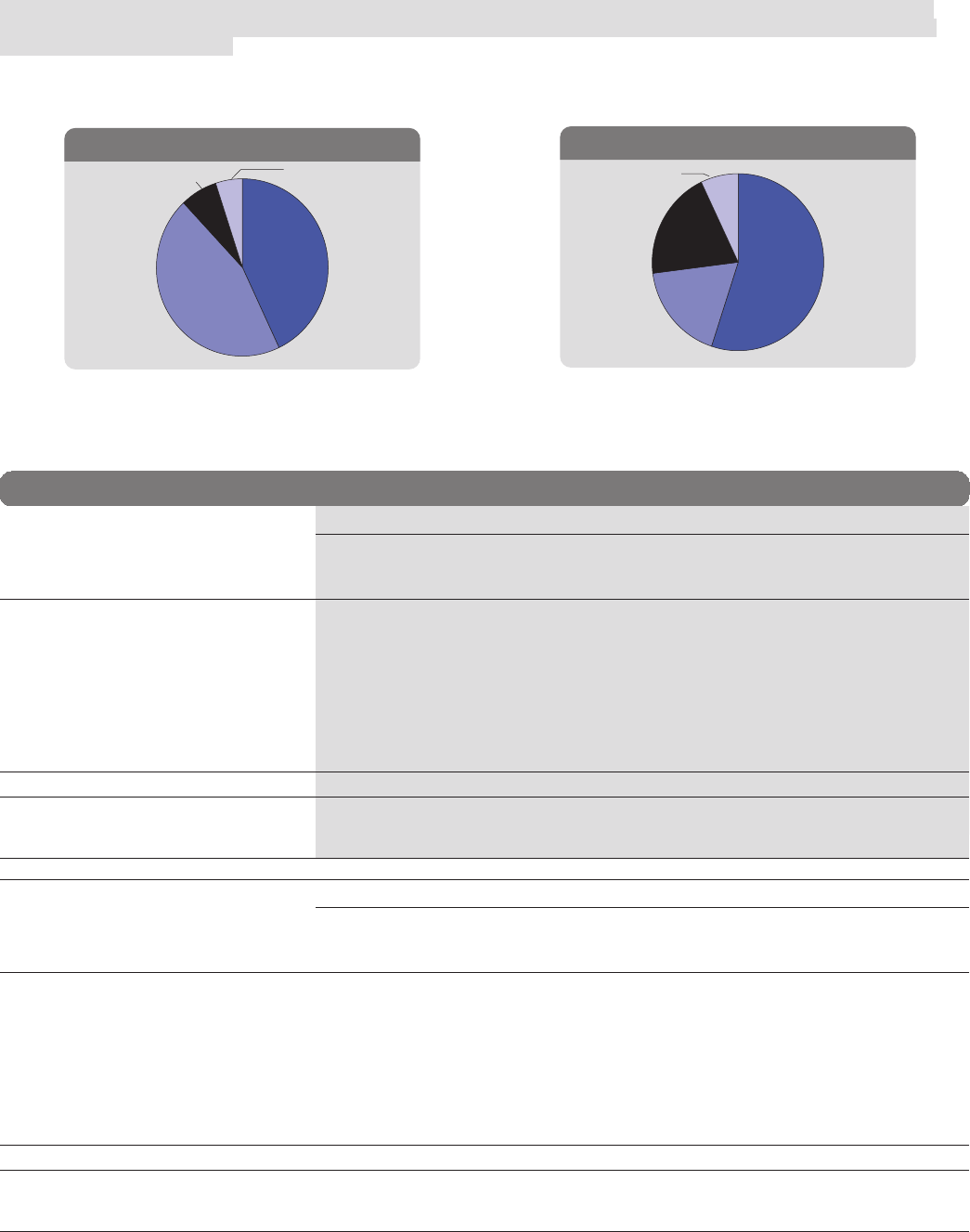

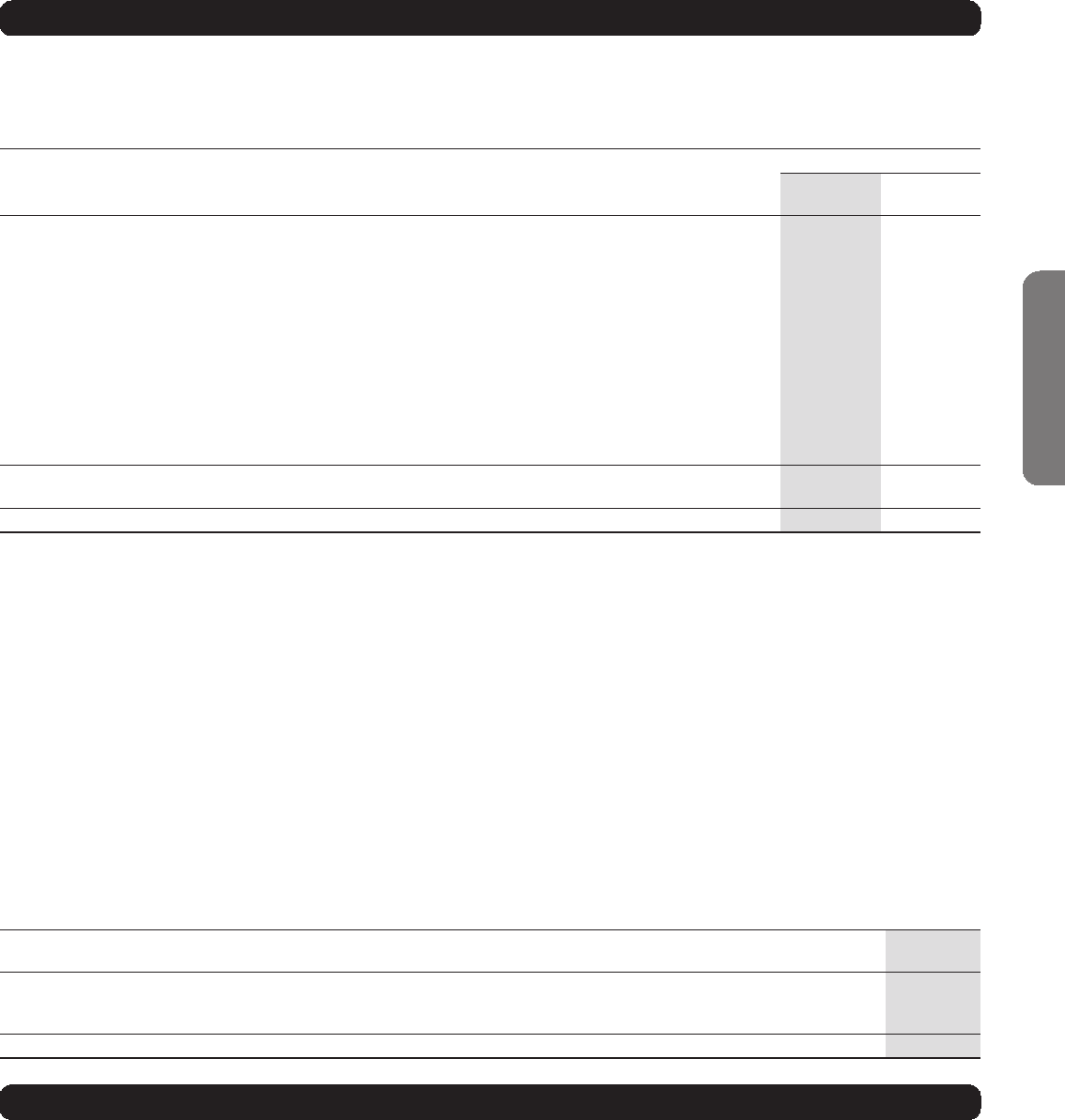

WE DELIVER

STABILITY & OPPORTUNITY

THROUGH DIVERSIFICATION

We serve our clients through a number of business lines across many geographies.

We’re confident we have the right mix to deepen client relationships, benefit from growth

opportunities and support consistent performance over the long term. Our diversified

business model positions us well to deliver superior returns and earnings stability through

the business cycle.

23%

CAPITAL MARKETS

12%

WEALTH MANAGEMENT

5%

INVESTOR &

TREASURY SERVICES

1. By client assets – Scorpio Partnership’s 2014

Global Private Banking Benchmark.

2. Pensions & Investments and Towers Watson 2014

Global Asset Manager Ranking Report.

3. By assets – Investment Funds Institute of Canada

(IFIC) as at September, 2014.

4. By assets and advisors – Company data.

5. Company data.

6. By AUA.

7. Global Investor.

8. Thomson Reuters by fees.

9. The Economist.

10. Euromoney.

11. Retail Banker International.

2014

EARNINGS

$9.0B

9%

INSURANCE

@ Among the fastest-growing insurance

organizations in Canada5

@ One of the largest Canadian bank-

owned insurance organizations

@ Top 10 global custodian6

@ Best overall global custodian7

@ Top 5 global wealth manager1 and

top 50 global asset manager2

•

Among the fastest-growing asset

managers in the world2

•

#1 in Canada in mutual funds3

•

Top 10 full-service brokerage firm

in the U.S.4

@ Top 10 global investment bank8

•

#1 in Canada

@ Recognized as the Most Trusted

Investment Bank in the World9

@ Named Best Investment Bank in

Canada across Equity, Debt and

M&A for the 7th consecutive year10

51%

PERSONAL &

COMMERCIAL BANKING

@ #1 or #2 market share in

all Canadian banking retail

product categories

@ Largest distribution network

in Canada

@ Recognized as the Global Retail

Bank of the Year11

@ First bank globally to provide a

cloud-based mobile payment

solution offering clients a choice

of paying with credit or debit, and

the first in North America to offer

the flexibility to pay a friend

through Facebook Messenger

* Amounts exclude Corporate Support

For more awards, please visit: rbc.com/aboutus/awards

4 Royal Bank of Canada: Annual Report 2014

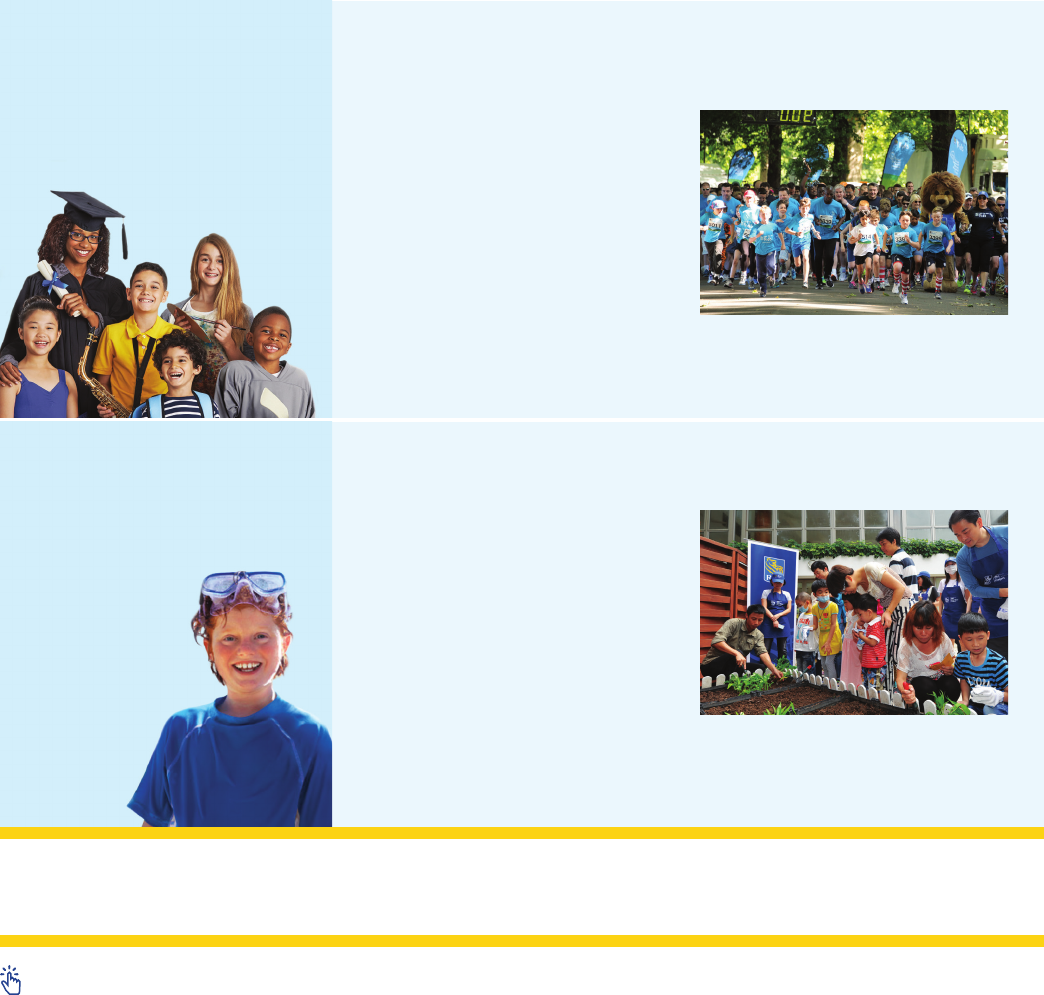

WE MAKE

COMMUNITIES

STRONGER

We contributed more than $100 million this year to causes that will have a positive and

lasting social, economic and environmental impact for generations to come. We are actively

involved with charitable organizations around the world and we support our employees in

their volunteering efforts.

RBC KIDS PLEDGE:

$100 MILLION.

5 YEARS.

We believe kids are our future: for our economic prosperity,

the health of the planet and the hope for our communities.

The RBC Kids Pledge is a commitment to

improve the well-being of at least 1 million

kids and youth. We believe kids need and

deserve our complete commitment so they

can be healthy in mind, body and spirit.

This pledge consolidates our support for a

diverse range of arts, sports, wellness,

education and employment programs to

help kids reach their full potential.

When you believe in kids, they can do

anything.

Employees laced up their running shoes to take

part in RBC Run/Race for the Kids events globally to

help raise funds for local children’s charities.

$50 MILLION.

10 YEARS.

RBC BLUE

WATER PROJECT®:

We help provide access to drinkable, swimmable, fishable water

now and for future generations.

The RBC Blue Water Project is our global

charitable commitment that is dedicated

to protecting fresh water and promoting

responsible water use. This year, RBC

Blue Water Project Leadership and

Community Action Grants provided

funding for protection and preservation

programs.

On RBC Blue Water Day, more than 20,000 employees

rolled up their sleeves and participated in over 700

‘clean up,’ ‘plant some green’ and ‘cultivate awareness’

makeover events to help protect water.

WE ALSO INVEST IN A WIDE RANGE OF EDUCATION, HEALTH, ARTS & CULTURE,

ENVIRONMENT AND SPORTS PROGRAMS AND ORGANIZATIONS

For more information, please visit: RBC Corporate Responsibility Review at rbc.com/community-sustainability

Royal Bank of Canada: Annual Report 2014 5

MESSAGE FROM

DAVE MCKAY

Dave McKay

President and Chief Executive Officer

Dear fellow shareholders,

Let me begin this letter by saying that I’m

honoured to serve as your President and

Chief Executive Officer. I started my career

at RBC more than 25 years ago as a summer

student. As I worked in different

businesses, functions and locations over

the years, I was always impressed by the

calibre of people who work here. Today, I’m

privileged to lead this tremendous team

with a shared commitment to building on

RBC’s proud history of more than 150 years.

Six years after the financial crisis it feels

like the global economy has begun to turn a

corner. The Canadian and U.S. economies

continued to improve throughout the year.

While the central banks of both countries

maintained historically low interest rates,

we saw lower unemployment, higher

consumer spending and improved housing

market activity – all signals of healthy

economic activity. The U.S. Federal Reserve

ended its asset purchase program in

October, further proof that the U.S.

economy is back on track. While growth in

Europe was slow, the U.K. continued to be a

good news story in the region. Across the

banking industry, regulation continued to

be a key theme.

Delivering record financial results in

2014 for our shareholders

Against this backdrop, I’m pleased to report

that 2014 was a record year for RBC. We

continued to extend our leadership position

in Canada and build our businesses in

select global markets. We earned $9 billion,

up 8 per cent from last year, reflecting

record results in all of our business

segments.

With these results, we achieved all of our

financial objectives. We earned $6.00 per

share (diluted EPS) with a return on equity

of 19 per cent, and we ended the year with

a strong Common Equity Tier 1 capital

ratio of 9.9 per cent.

These financial objectives measure

progress toward our medium-term

objective of maximizing Total Shareholder

Returns (TSR). We delivered compound

annual TSR of 23 per cent and 12 per cent

over the three- and five-year periods.

During 2014, our one-year TSR was 19 per

cent. We raised our dividend twice during

2014 for a combined increase of 12 per

cent while repurchasing shares, and we

renewed our share buyback program for

2015.

Building on our strengths to grow our

businesses

Looking ahead, we understand the drivers

of growth will be different from those in

the past decade, and I feel confident RBC

can adapt to changes and capitalize on

new opportunities including the shift in

demographics, the emergence of new

technologies and the changing needs and

preferences of our clients.

We know the pace of consumer borrowing

in Canada will continue to moderate

following many years of strong credit

growth, and that the shift to savings and

investing will accelerate. In fact,

investments are forecast to grow three

I am enormously proud of

what we’ve achieved

together and incredibly

excited for the

opportunities that lie

ahead

times faster than credit over the next

decade. RBC is extremely well positioned to

serve our clients as we are the largest

mutual fund provider in our home market,

selling almost twice as many mutual funds

as our nearest bank competitor. We also

have the largest full-service wealth

management business with leading market

share for high-net-worth individuals in

Canada, and we have the most mobile and

branch-based investment and financial

planners to serve our clients. We are also

among the fastest-growing insurance

organizations in Canada.

As the market leader in business financial

services in Canada, we see opportunity

from the growing demand for credit from

businesses, especially as improvements in

the U.S. economy help foster greater

confidence to spur investing. Additionally,

with over 45 per cent of businesses

expected to change ownership in the next

five to 10 years, we are well placed to help

business owners plan for succession and

with the transition itself – by finding a

buyer, financing the transaction and

managing their new wealth.

6 Royal Bank of Canada: Annual Report 2014

ANNOUNCED 37% TOTAL

INCREASE TO QUARTERLY

DIVIDENDS OVER 3 YEARS

There is no question our home market is a

competitive banking environment and

pressure from continued low interest rates

will remain a headwind for our business

next year. Within this context, we are

committed to improving on our industry

leading efficiency ratio and deepening

client relationships through cross-sell, a

proven capability for RBC. Overall, I believe

we can continue to extend our lead in

Canada to deliver profitable growth.

Globally, we have the right strategies to

build leadership in select businesses and

markets where our strengths can help us

win.

We have a strong presence in the U.S., an

advantage given the expected growth in the

American economy. In our Capital Markets

business, the U.S. now accounts for more

than 50 per cent of revenue, reflecting

strong client acquisition over the past

number of years, and we are focused on

building deeper relationships with those

clients. Our U.S. Wealth Management

business is the seventh-largest full-service

brokerage by assets and we are broadening

our product offering. Over the last few years

we’ve also added global fixed income and

equity capabilities to our asset

management business in that market,

which continues to grow.

In the U.K. and Europe, we are building our

presence, adding expertise across wealth

management, asset management and

capital markets, and benefitting from RBC’s

brand and reputation. Given the challenging

economic environment, we are taking a

prudent approach to building our

capabilities as we know the recovery will

take some time. I am encouraged by our

progress in these markets and expect it to

continue. In Capital Markets, we are

increasingly winning corporate and

investment banking mandates. We are

among the fastest growing asset

managers with strong momentum outside

of Canada. With its reputation for service

excellence, our Investor & Treasury

Services business is also well positioned

for expansion in the global investment

industry.

Across all of our businesses advance-

ments in technology are changing client

expectations, transforming business

models and redefining the competitive

landscape. Meanwhile, the regulatory

environment for banks will continue to

evolve. Our financial strength gives us the

flexibility to effectively manage regulatory

changes while investing in our

businesses. We have digitized and

simplified processes to lower costs and

deliver a faster, better client experience,

and are investing in our technology and

innovation to shape the future with new

products and services. For example, this

year we launched a new system that

automates many of the steps in

processing a new mortgage to deliver

faster service, and we are a leader in

emerging payment solutions.

Looking ahead, we will maintain our

balanced and disciplined approach to

capital deployment. Our first priority will

remain investing in our existing

businesses to generate strong returns.

Second, we remain committed to returning

capital to shareholders through dividend

increases and share buybacks. And lastly,

we will consider targeted acquisitions that

fit our strategy and risk appetite, and

deliver strong returns for our shareholders

over the long term.

Bringing the best of RBC to our clients

United by our vision of always earning the

right to be our clients’ first choice, we put

customers at the centre of everything that

we do.

Whether it’s helping them buy their first

home, start their own business, travel

worry-free, pay for their children’s

education or prepare for a comfortable

retirement, we enable more than 16 million

clients in achieving their goals. At the end

of 2014, we funded $231 billion in

mortgages and lines of credit for

homeowners in Canada and $5 billion in

small business loans for Canadian

entrepreneurs. We grew the assets

entrusted to us by investors around the

world by 13 per cent this year.

We loaned nearly $110 billion to medium

and large companies around the world to

help them build their businesses, and

ensured our institutional clients could make

informed decisions by providing top-ranked

research and investment solutions in key

international markets.

Royal Bank of Canada: Annual Report 2014 7

NAMED BANK OF

THE YEAR FOR CANADA1

Creating opportunities for our

employees

Our employees’ passion for helping

clients succeed is second to none. They

represent our brand with pride. I’m

particularly proud of how much our

employees care about doing what’s right.

Our people, culture and brand are a true

differentiator wherever we do business.

We enable success by fostering an

environment of respect and inclusion

where everyone can contribute and

achieve their potential. The diversity of

our workforce brings different

perspectives and abilities and plays a

central role in serving our clients and

driving productivity, innovation and

growth.

Making a positive difference in

communities

One of the things that defines RBC is the

positive social, economic and environ-

mental impact we make in communities.

In 2014, we invested more than

$100 million in community efforts, shared

our expertise and provided nearly

2,500 RBC Employee Volunteer grants.

We’re on track to improve the well-being

of at least one million kids and youth

through our multi-year, $100-million RBC

Kids Pledge. A key element of that

commitment is the RBC Run/Race for the

Kids, which took place in seven cities

around the world, and this year more than

8,000 employees, their families and

friends ran with us in support of local

children’s charities. Our employees are

also tremendous supporters of the RBC

Blue Water Project, our commitment to

protecting fresh water for generations to

come.

Thank you

Thank you to our clients who choose to

place their trust in us, and to our

employees who work so hard to help them

succeed.

I’d like to acknowledge and thank Gordon

Nixon, who retired as CEO this year, for his

leadership of a truly world-class

organization, and for leaving the company

with the strength and depth to build for

the future. And finally, I’d like to express

my gratitude to the Board of Directors for

their continued insight and counsel.

And to you, our shareholders, we are

committed to delivering high-quality

growth, industry-leading returns and long-

term value. I am enormously proud of

what RBC has achieved and incredibly

excited for the opportunities that lie

ahead.

David McKay

President and Chief Executive Officer

We serve more than

25% of active

Canadian digital

banking clients2

We have more than

30% share of all

mutual funds

sold by banks in

Canada – other banks

have less than 20%3

Awarded Best Fund

Group Overall4

Named Most Trusted

Investment Bank in

the World5

1. The Banker.

2. Finalta Digital and Multichannel

Banking Benchmark 2014 Study –

Big 5 Canadian banks.

3. Investment Funds Institute of Canada,

September 2014.

4. 2014 Lipper Canada Fund Awards.

5. The Economist.

8 Royal Bank of Canada: Annual Report 2014

MESSAGE FROM

KATIE TAYLOR

Katie Taylor, Chair of the Board

Dear fellow shareholders,

It is an honour to take on the role of Chair,

more than a decade after first joining RBC’s

Board of Directors in 2001.

Over the years the Board has overseen

RBC’s continued growth resulting from its

successful focus on cultivating broad and

deep client relationships, investing in

people and contributing to the economic

prosperity and betterment of communities

where it does business.

In 2014 the Board continued to engage with

the outstanding management team at RBC.

Our oversight is directed at guiding their

business decisions to deliver value to

shareholders over the long term.

RBC has the right strategy to drive

growth and create value

As strategic advisors to management, the

Board must prudently balance strategic

opportunities with risk discipline. Today’s

approach to shareholder value creation

must build agility to benefit from oppor-

tunities to allow RBC to thrive in tomorrow’s

changing environment. To that end, the

Board and management actively discuss

how RBC is positioned to grow as external

factors such as technology, regulation and

changing client demographics shape the

financial services industry.

The Board is focused on ensuring that RBC

has both the right strategy to drive

continued success and the competitive

strengths and capabilities to deliver on its

priorities. We assess the amount and type

of risk RBC will accept in pursuit of its

business objectives, and monitor the

organization’s systems and processes to

manage those risks. We work closely with

management on how best to enhance the

bank’s strong capital position and create

value by investing in organic growth,

funding dividend increases, repurchasing

shares or making strategic acquisitions.

RBC has the right team in place to

benefit from future opportunities

Succession planning, including the

selection and appointment of the senior

management team, is a fundamental

responsibility of the Board. We review the

depth and diversity of succession pools

for key leadership roles, and we monitor

the progress of succession candidates.

This year Dave McKay succeeded Gordon

Nixon as President and CEO, and there

were a number of other important

appointments at the Group Executive

level. The skills and experience of our

senior leaders are essential to achieving

sustainable growth over the long term.

The Board is confident that under Dave

McKay’s leadership, RBC will continue to

build on its past successes. His

distinguished 26-year career at RBC

includes international experience in

corporate banking and senior roles in

retail banking and risk management. His

outstanding dedication to clients, focus

on innovation, commitment to employees

and track record of performance will serve

RBC well as it continues to grow.

As the bank grows and its leadership team

transitions, we remain committed to

enhancing the diversity of experience,

perspectives and skill sets represented on

the Board. We are pleased to welcome

Dave McKay and Jacynthe Côté to the

Board, and to announce that Toos

Daruvala will join as a Director in January

2015. With a longstanding career at Rio

Tinto Alcan, most recently as President

and Chief Executive Officer, Ms. Côté

brings extensive experience in interna-

tional business. Mr. Daruvala, currently a

Director and Senior Partner at McKinsey &

Company, brings more than 30 years of

experience in advising financial institutions

on matters ranging from banking and risk

management practices to corporate strategy

and organizational effectiveness.

As we welcome these three new Directors,

we say farewell to one. Over his 13-year

tenure as CEO, Gordon Nixon added

tremendous value in earnings, returns and

client focus. Under his guidance, RBC has

taken its place among the most-respected

financial institutions globally.

RBC is committed to driving growth,

which is essential to its continued

success

The Board of Directors recognizes that RBC

succeeds when its stakeholders –

shareholders, employees, clients and

communities – succeed. As one of the

largest financial institutions in the world,

RBC sets high standards as a top employer

and leading corporate citizen. United by

strong corporate values, the Board of

Directors, management and employees

worldwide share the vision of always

earning the right to be our clients’ first

choice.

In 2014, RBC delivered significant value to

stakeholders as it continued to grow and

deliver on its strategic goals. I want to thank

my fellow Board members for their valuable

advice. The Board would like to extend its

sincere thanks to the management team at

RBC and the company’s dedicated

employees who serve and focus on clients

– each and every day.

Kathleen Taylor

Chair of the Board

For more information on our governance policies, visit: rbc.com/governance

Royal Bank of Canada: Annual Report 2014 9

MANAGEMENT’S

DISCUSSION AND

ANALYSIS

Management’s Discussion and Analysis (MD&A) is provided to enable a reader to assess our results of operations and financial condition for the fiscal year ended

October 31, 2014, compared to the preceding two years. This MD&A should be read in conjunction with our 2014 Annual Consolidated Financial Statements and related

notes and is dated December 2, 2014. All amounts are in Canadian dollars, unless otherwise specified, and are based on financial statements prepared in accordance with

International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB), unless otherwise noted.

Additional information about us, including our 2014 Annual Information Form, is available free of charge on our website at rbc.com/investorrelations, on the Canadian

Securities Administrators’ website at sedar.com and on the EDGAR section of the United States (U.S.) Securities and Exchange Commission’s (SEC) website at sec.gov.

Table of contents

Caution regarding forward-looking statements 10

Overview and outlook 11

Selected financial and other highlights 11

About Royal Bank of Canada 12

Vision and strategic goals 12

Economic and market review and outlook 12

Defining and measuring success through Total

Shareholder Returns 13

Key corporate events of 2014 14

Financial performance 14

Overview 14

Business segment results 18

Results by business segment 18

How we measure and report our business segments 19

Key performance and non-GAAP measures 19

Personal & Commercial Banking 23

Wealth Management 28

Insurance 31

Investor & Treasury Services 34

Capital Markets 35

Corporate Support 39

Quarterly financial information 39

Fourth quarter 2014 performance 39

Quarterly results and trend analysis 40

Results by geographic segment 42

Financial condition 43

Condensed balance sheets 43

Off-balance sheet arrangements 43

Risk management 46

Overview 46

Top and emerging risks 46

Enterprise risk management 47

Credit risk 52

Market risk 63

Liquidity and funding risk 68

Insurance risk 78

Regulatory compliance risk 78

Operational risk 79

Strategic risk 80

Reputation risk 80

Legal and regulatory environment risk 80

Competitive risk 82

Systemic risk 82

Overview of other risks 82

Capital management 85

Additional financial information 94

Exposures to selected financial instruments 94

Accounting and control matters 95

Critical accounting policies and estimates 95

Controls and procedures 99

Related party transactions 99

Supplementary information 100

See our Glossary for definitions of terms used throughout this document

Caution regarding forward-looking statements

From time to time, we make written or oral forward-looking statements within the meaning of certain securities laws, including the “safe harbour” provisions of the United States

Private Securities Litigation Reform Act of 1995 and any applicable Canadian securities legislation. We may make forward-looking statements in this 2014 Annual Report, in

other filings with Canadian regulators or the SEC, in other reports to shareholders and in other communications. Forward-looking statements in this document include, but are

not limited to, statements relating to our financial performance objectives, vision and strategic goals, the economic and market review and outlook for Canadian, U.S., European

and global economies, the regulatory environment in which we operate, the outlook and priorities for each of our business segments, and the risk environment including our

liquidity and funding risk. The forward-looking information contained in this document is presented for the purpose of assisting the holders of our securities and financial

analysts in understanding our financial position and results of operations as at and for the periods ended on the dates presented and our financial performance objectives,

vision and strategic goals, and may not be appropriate for other purposes. Forward-looking statements are typically identified by words such as “believe”, “expect”, “foresee”,

“forecast”, “anticipate”, “intend”, “estimate”, “goal”, “plan” and “project” and similar expressions of future or conditional verbs such as “will”, “may”, “should”, “could” or

“would”.

By their very nature, forward-looking statements require us to make assumptions and are subject to inherent risks and uncertainties, which give rise to the possibility that

our predictions, forecasts, projections, expectations or conclusions will not prove to be accurate, that our assumptions may not be correct and that our financial performance

objectives, vision and strategic goals will not be achieved. We caution readers not to place undue reliance on these statements as a number of risk factors could cause our

actual results to differ materially from the expectations expressed in such forward-looking statements. These factors – many of which are beyond our control and the effects of

which can be difficult to predict – include: credit, market, liquidity and funding, insurance, regulatory compliance, operational, strategic, reputation, legal and regulatory

environment, competitive and systemic risks and other risks discussed in the Risk management and Overview of other risks sections; anti-money laundering, growth in

wholesale credit, the high levels of Canadian household debt; cybersecurity; the business and economic conditions in Canada, the U.S. and certain other countries in which we

operate; the effects of changes in government fiscal, monetary and other policies; tax risk and transparency; our ability to attract and retain employees; the accuracy and

completeness of information concerning our clients and counterparties; the development and integration of our distribution networks; model, information technology,

information management, social media, environmental and third party and outsourcing risk.

We caution that the foregoing list of risk factors is not exhaustive and other factors could also adversely affect our results. When relying on our forward-looking statements

to make decisions with respect to us, investors and others should carefully consider the foregoing factors and other uncertainties and potential events. Material economic

assumptions underlying the forward looking statements contained in this 2014 Annual Report are set out in the Overview and outlook section and for each business segment

under the heading Outlook and priorities. Except as required by law, we do not undertake to update any forward-looking statement, whether written or oral, that may be made

from time to time by us or on our behalf.

Additional information about these and other factors can be found in the Risk management and Overview of other risks sections.

Information contained in or otherwise accessible through the websites mentioned does not form part of this report. All references in this report to websites are inactive textual references and

are for your information only.

10 Royal Bank of Canada: Annual Report 2014 Management’s Discussion and Analysis

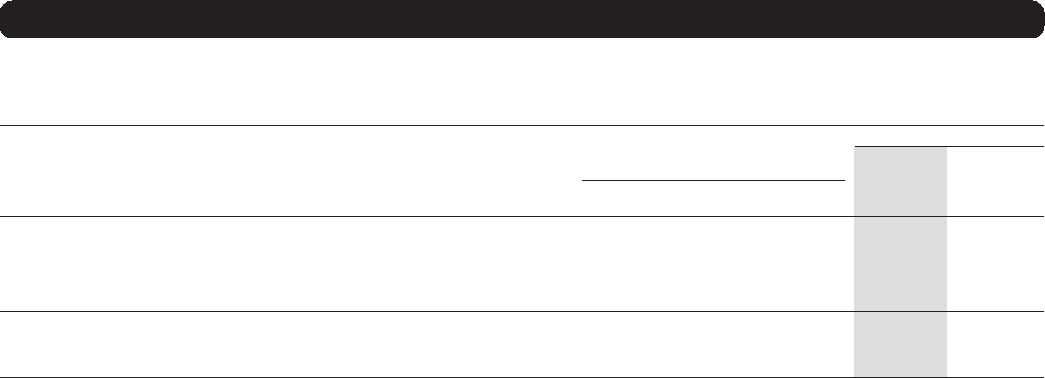

Overview and outlook

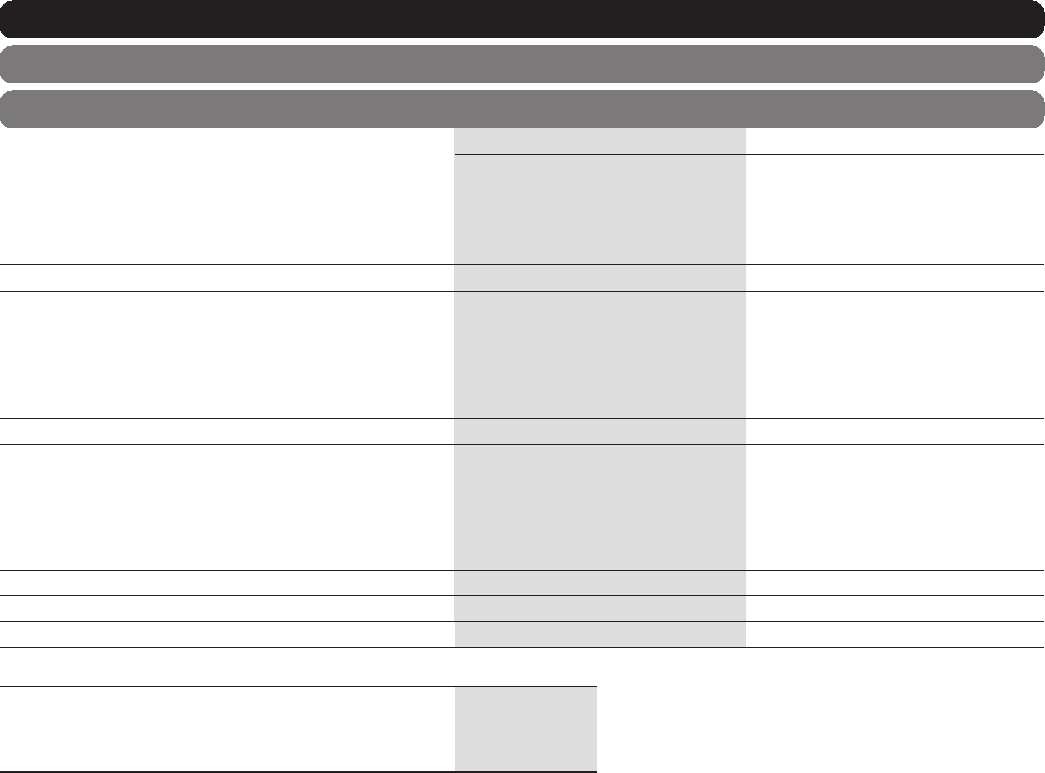

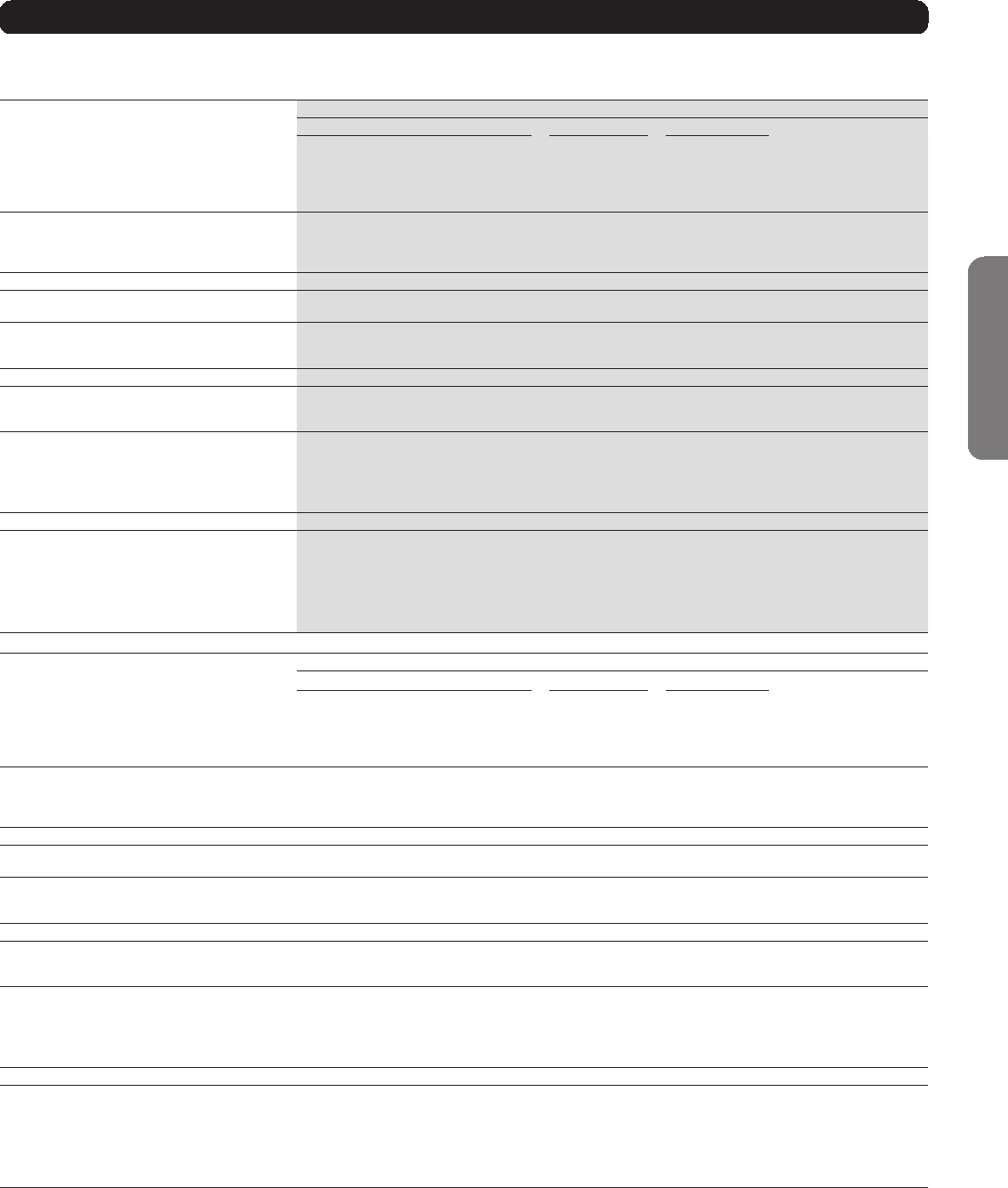

Selected financial and other highlights Table 1

(Millions of Canadian dollars, except per share, number of and percentage amounts) 2014 2013 (1) 2012 (1)

2014 vs. 2013

Increase (decrease)

Continuing operations

Total revenue $ 34,108 $ 30,682 $ 29,147 $ 3,426 11.2%

Provision for credit losses (PCL) 1,164 1,237 1,299 (73) (5.9)%

Insurance policyholder benefits, claims and

acquisition expense (PBCAE) 3,573 2,784 3,621 789 28.3%

Non-interest expense 17,661 16,214 14,641 1,447 8.9%

Net income before income taxes 11,710 10,447 9,586 1,263 12.1%

Net income from continuing operations 9,004 8,342 7,558 662 7.9%

Net loss from discontinued operations – – (51) – 0.0%

Net income $ 9,004 $ 8,342 $ 7,507 $ 662 7.9%

Segments – net income from continuing operations

Personal & Commercial Banking $ 4,475 $ 4,380 $ 4,056 $ 95 2.2%

Wealth Management 1,083 886 753 197 22.2%

Insurance 781 595 713 186 31.3%

Investor & Treasury Services 441 339 102 102 30.1%

Capital Markets 2,055 1,700 1,576 355 20.9%

Corporate Support 169 442 358 (273) (61.8)%

Net income from continuing operations $ 9,004 $ 8,342 $ 7,558 $ 662 7.9%

Selected information

Earnings per share (EPS) – basic $ 6.03 $ 5.53 $ 4.96 $ 0.50 9.0%

– diluted 6.00 5.49 4.91 0.51 9.3%

Return on common equity (ROE) (2), (3) 19.0% 19.7% 19.6% n.m. (70) bps

Selected information from continuing operations

EPS – basic $ 6.03 $ 5.53 $ 4.99 $ 0.50 9.0%

–diluted 6.00 5.49 4.94 0.51 9.3%

ROE (2), (3) 19.0%19.7% 19.7% n.m. (70) bps

PCL on impaired loans as a % of average net loans and

acceptances 0.27%0.31% 0.35% n.m. (4) bps

Gross impaired loans (GIL) as a % of loans and acceptances 0.44%0.52% 0.58% n.m. (8) bps

Capital ratios and multiples (4)

Common Equity Tier 1 (CET1) ratio (4) 9.9%9.6% n.a. n.m. 30 bps

Tier 1 capital ratio (4) 11.4%11.7% 13.1% n.m. (30) bps

Total capital ratio (4) 13.4%14.0% 15.1% n.m. (60) bps

Assets-to-capital multiple (4) 17.0X 16.6X 16.7X n.m. 40 bps

Selected balance sheet and other information

Total assets $ 940,550 $ 859,745 $ 823,954 $ 80,805 9.4%

Securities 199,148 182,710 161,602 16,438 9.0%

Loans (net of allowance for loan losses) 435,229 408,850 378,241 26,379 6.5%

Derivative related assets 87,402 74,822 91,293 12,580 16.8%

Deposits 614,100 563,079 512,244 51,021 9.1%

Common equity 48,615 43,064 38,346 5,551 12.9%

Average common equity (2) 45,700 40,600 36,500 5,100 12.6%

Total capital risk-weighted assets 372,050 318,981 280,609 53,069 16.6%

Assets under management (AUM) 457,000 391,100 343,000 65,900 16.8%

Assets under administration (AUA) (5) 4,647,000 4,050,900 3,653,300 596,100 14.7%

Common share information

Shares outstanding (000s) – average basic 1,442,553 1,443,735 1,442,167 (1,182) (0.1)%

– average diluted 1,452,003 1,466,529 1,468,287 (14,526) (1.0)%

– end of period 1,442,233 1,441,056 1,445,303 1,177 0.1%

Dividends declared per common share $ 2.84 $ 2.53 $ 2.28 $ 0.31 12.3%

Dividend yield (6) 3.8%4.0% 4.5% n.m. (20) bps

Common share price (RY on TSX) $ 80.01 $ 70.02 $ 56.94 $ 9.99 14.3%

Market capitalization (TSX) 115,393 100,903 82,296 14,490 14.4%

Business information from continuing operations (number of)

Employees (full-time equivalent) (FTE) 73,498 74,247 74,377 (749) (1.0)%

Bank branches 1,366 1,372 1,361 (6) (0.4)%

Automated teller machines (ATMs) 4,929 4,973 5,065 (44) (0.9)%

Period average US$ equivalent of C$1.00 (7) $ 0.914 $ 0.977 $ 0.997 $ (0.063) (6.4)%

Period-end US$ equivalent of C$1.00 $ 0.887 $ 0.959 $ 1.001 $ (0.072) (7.5)%

(1) Comparative amounts prior to November 1, 2013 have been restated for the adoption of new accounting standards. For further details, refer to Note 2 of our 2014 Annual Consolidated

Financial Statements.

(2) Average amounts are calculated using methods intended to approximate the average of the daily balances for the period. This includes ROE and Average common equity. For further details,

refer to the Key performance and non-GAAP measures section.

(3) These measures may not have a standardized meaning under generally accepted accounting principles (GAAP) and may not be comparable to similar measures disclosed by other financial

institutions. For further details, refer to the Key performance and non-GAAP measures section.

(4) Effective the first quarter of 2013, we calculate capital ratios and Assets-to-capital multiple using the Basel III framework. Capital ratios presented above are on an “all-in” basis. Capital ratios

and Assets-to-capital multiple in 2012 were calculated using the Basel II framework. Basel III and Basel II are not directly comparable. The CET1 ratio is a regulatory measure under the Basel

III framework and is not applicable (n.a.) for 2012. For further details, refer to the Capital management section.

(5) Includes $31.2 billion (2013 – $32.6 billion, 2012 – $38.4 billion) of securitized mortgages and credit card loans.

(6) Defined as dividends per common share divided by the average of the high and low share price in the relevant period.

(7) Average amounts are calculated using month-end spot rates for the period.

n.m. not meaningful

Management’s Discussion and Analysis Royal Bank of Canada: Annual Report 2014 11

About Royal Bank of Canada

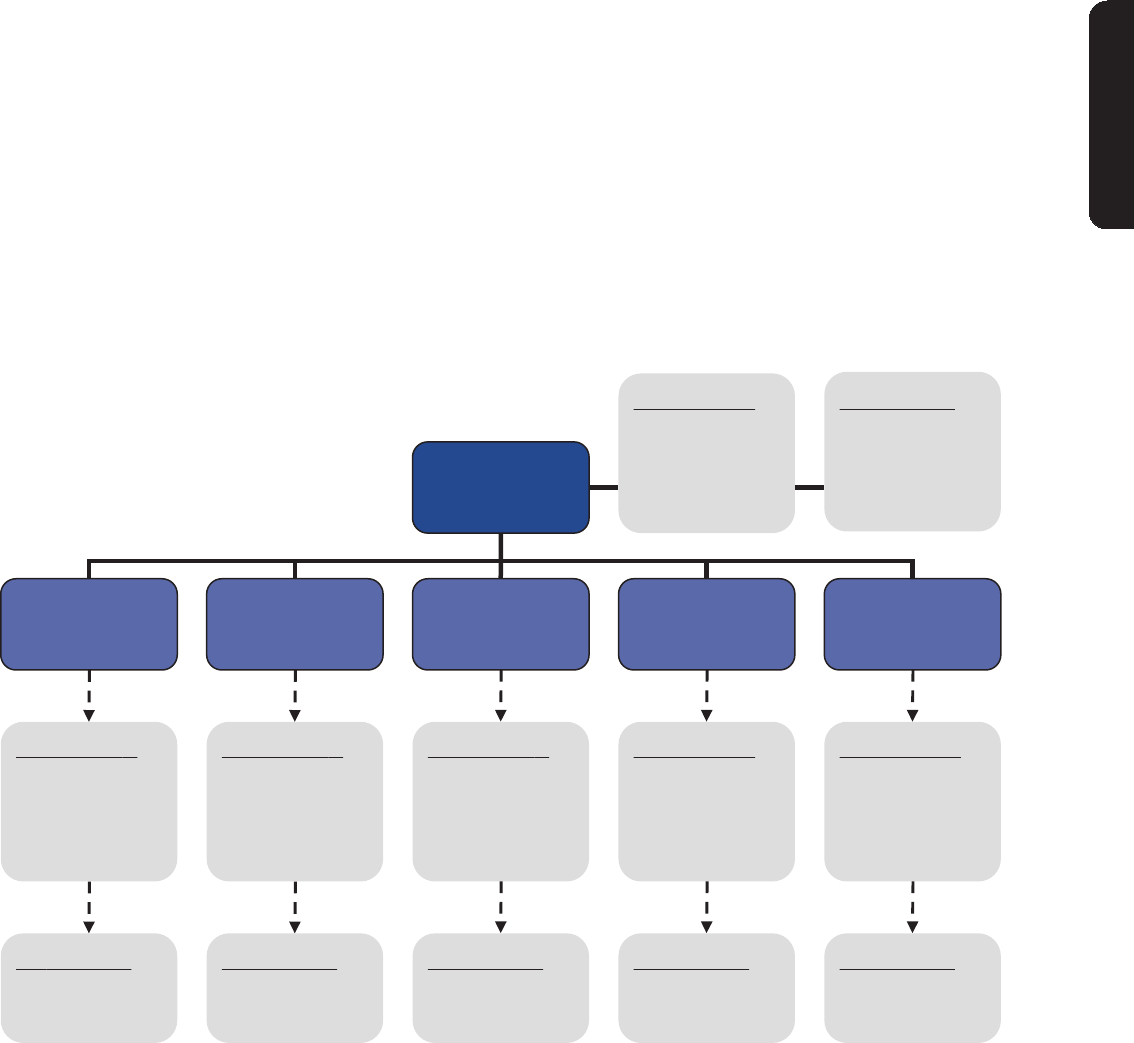

Royal Bank of Canada (RY on TSX and NYSE) is Canada’s largest bank, and one of the largest banks in the world, based on market capitalization.

We are one of North America’s leading diversified financial services companies, and provide personal and commercial banking, wealth

management services, insurance, investor services and capital markets products and services on a global basis. We employ approximately

78,000 full- and part-time employees who serve more than 16 million personal, business, public sector and institutional clients through offices

in Canada, the U.S. and 38 other countries. For more information, please visit rbc.com.

Our business segments are described below.

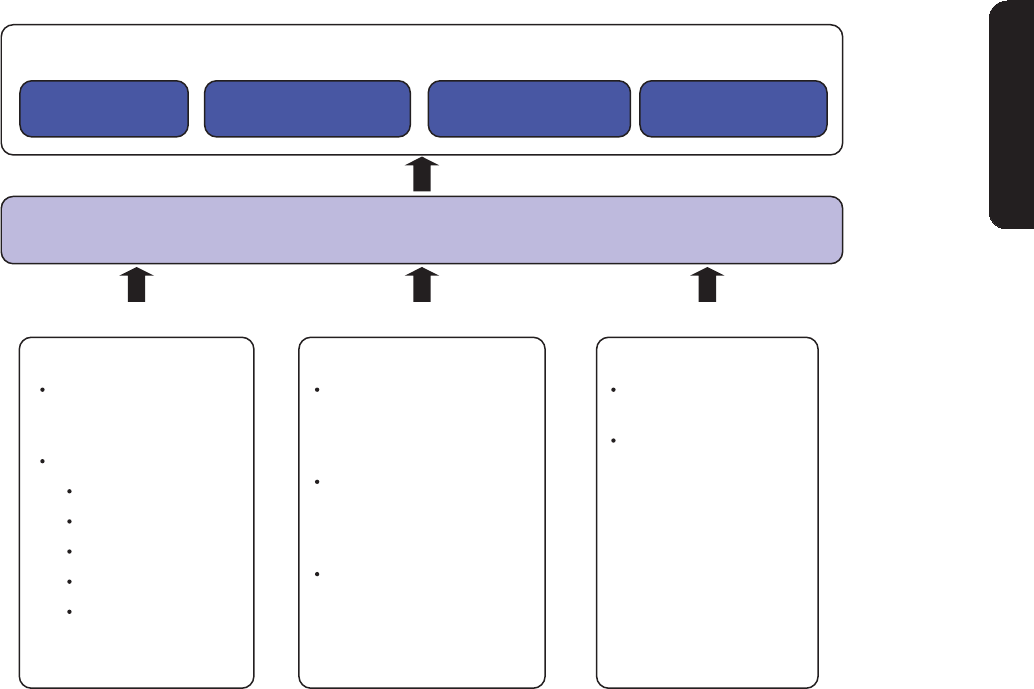

Personal & Commercial Banking operates in Canada, the Caribbean and the U.S., and comprises our personal and business banking

operations, as well as our auto financing and retail investment businesses.

Wealth Management serves affluent, high net worth and ultra-high net worth clients from our offices in key financial centres mainly in

Canada, the U.S., the U.K., Channel Islands, continental Europe, and Asia with a comprehensive suite of investment, trust, banking, credit and

other wealth management solutions. We also provide asset management products and services directly to institutional and also to individual

clients through our distribution channels and third-party distributors.

Insurance provides a wide range of life, health, home, auto, travel, wealth and reinsurance products and solutions. We offer insurance

products and services through our proprietary distribution channels, comprised of the field sales force which includes retail insurance branches,

our field sales representatives, call centres and online, as well as through independent insurance advisors and affinity relationships in Canada.

Outside Canada, we operate in reinsurance markets globally.

Investor & Treasury Services serves the needs of institutional investing clients by providing asset servicing, custodial, advisory, financing

and other services to safeguard assets, maximize liquidity and manage risk in multiple jurisdictions around the world. We also provide short-

term funding and liquidity management for RBC.

Capital Markets provides public and private companies, institutional investors, governments and central banks with a wide range of

products and services. In North America, we offer a full suite of products and services which include corporate and investment banking, equity

and debt origination and distribution, and structuring and trading. Outside North America, we offer a diversified set of capabilities in our key

sectors of expertise such as energy, mining and infrastructure and we are now expanding into industrial, consumer and health care in Europe.

Our business segments are supported by Corporate Support, which consists of Technology & Operations and Functions. Technology &

Operations provides the technological and operational foundation required to effectively deliver products and services to our clients, while

Functions includes our finance, human resources, risk management, internal audit and other functional groups.

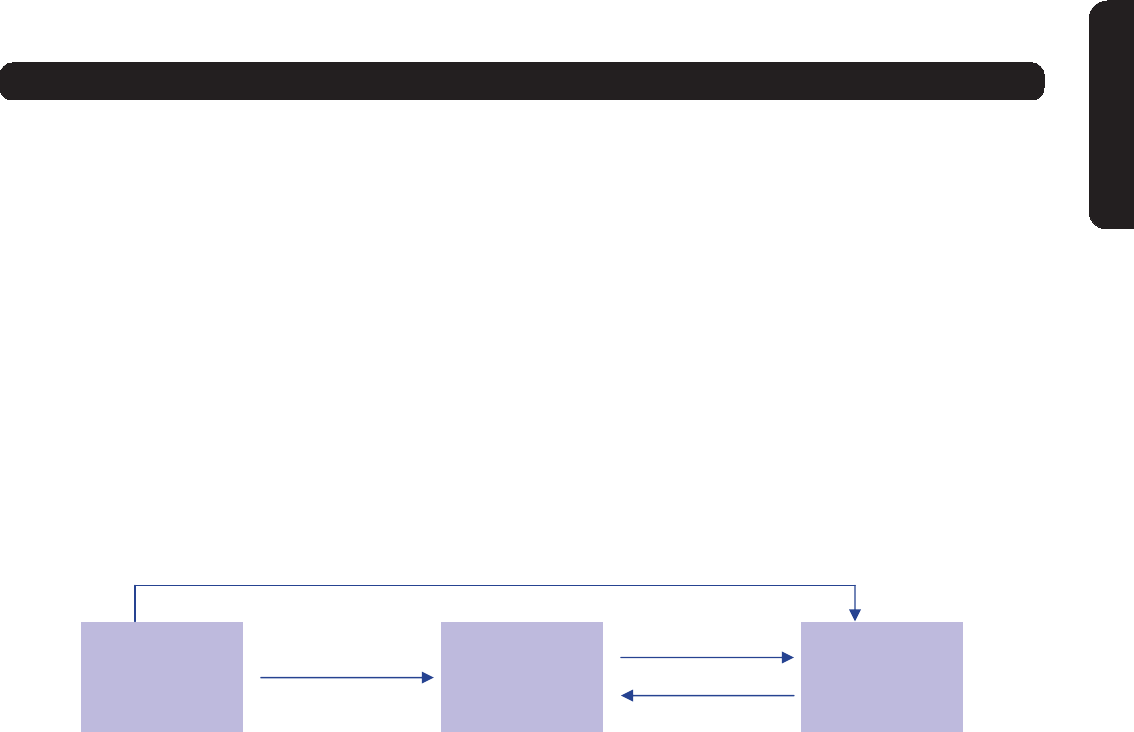

The following chart presents our business segments and respective lines of business:

ROYAL BANK OF CANADA

Personal &

Commercial Banking

Wealth

Management Insurance Investor & Treasury

Services

Capital

Markets

OCanadian Banking

OCaribbean &

U.S. Banking

OCanadian Wealth

Management

OU.S. & International

Wealth

Management

OGlobal Asset

Management

OCanadian

Insurance

OInternational

Insurance

OCorporate and

Investment

Banking

OGlobal Markets

OOther

Corporate Support

OTechnology & Operations OFunctions

Vision and strategic goals

Our business strategies and actions are guided by our vision of “Always earning the right to be our clients’ first choice.” Our three strategic

goals are:

• In Canada, to be the undisputed leader in financial services;

• Globally, to be a leading provider of capital markets, investor and wealth management solutions; and

• In targeted markets, to be a leading provider of select financial services complementary to our core strengths.

For our progress in 2014 against our business strategies and strategic goals, refer to the Business segment results section.

Economic and market review and outlook – data as at December 2, 2014

The predictions and forecasts in this section are based on information and assumptions from sources we consider reliable. If this information or

these assumptions are not accurate, actual economic outcomes may differ materially from the outlook presented in this section. For details on

risk factors from general business and economic conditions that may affect our business and financial results, refer to the Overview of other risks

section.

Canada

The Canadian economy is expected to grow at an estimated rate of 2.5% during calendar 2014, slightly below our estimate of 2.6% as at

December 4, 2013. Growth in the economy continues to be driven by solid consumer spending and strength in the labour market on employment

gains as the unemployment rate fell to its lowest level since November 2008 at 6.5% in October 2014. Housing market activity remained firm

through the year, despite the dampening impact of poor weather conditions early in 2014. Weakening commodity prices, lower expectations of

interest rate increases by the Bank of Canada (BoC) and a strengthening of the U.S. dollar compared to most world currencies due to an improving

U.S. economy and anticipated U.S. interest rate increases are key factors in the Canadian dollar depreciating against the U.S. dollar during 2014.

Interest rates remained low as the persistence of excess capacity in the economy led the BoC to maintain its overnight rate at 1% in October 2014.

12 Royal Bank of Canada: Annual Report 2014 Management’s Discussion and Analysis

In calendar 2015, we expect the Canadian economy to grow at an estimated rate of 2.7%, driven by an improvement in net exports, increase

in business investment, and steady, albeit slowing consumer spending growth. We expect growth in the housing market to ease to more

sustainable levels in 2015 as market interest rates move higher and household debt accumulation slows. As the economy strengthens and

inflation holds around the BoC’s target level of 2% on a sustained basis, we expect the BoC to begin to raise its overnight rate from the current

1% in the middle of calendar 2015.

U.S.

We expect the U.S. economy to grow at an estimated rate of 2.3% during calendar 2014, which is below our estimate of 2.7% as at December 4,

2013. Strengthening consumption and firming business investment continue to drive the economy, with weaker net exports and the impact of

poor weather early in the year limiting growth. Growth in consumer spending was driven by improvements in the labour market as the

unemployment rate fell to 5.8% in October 2014 which is the lowest level since July 2008. As a result of improving labour market conditions and

a general strengthening in the economy, the Federal Reserve (Fed) reduced its monthly asset purchases throughout 2014 and ended the program

in October 2014, although it has maintained interest rates at historically low levels.

In calendar 2015, we expect the U.S. economy to grow at a rate of 3.3%, as both household and business spending accelerate given

expected gains in household wealth and the recent momentum in the labour market. Housing market activity is expected to improve given the

easing in lending standards and the decline in long-term mortgage rates. As labour markets and core inflation levels approach target levels, we

expect the Fed to begin to raise its key interest rate from the current funds target range of 0.0% to 0.25% starting in the middle of calendar 2015.

Europe

The Euro area economy is expected to grow marginally at an estimated rate of 0.7% during calendar 2014, below our estimate of 1.0% as at

December 4, 2013. The harmonized inflation level continues to remain below the European Central Bank’s (ECB) desired range, and averaged

0.5% from January through October 2014. Labour markets remain weak and the unemployment rate has stayed elevated at 11.5% in October

2014. To support the recovery, the ECB is taking steps to provide stimulus to the Euro area economy through an asset purchase program which

will run a minimum of two years, and has reduced its key interest rate twice during the calendar year, by 10 basis points (bps) each time, to the

current 0.05%. The ECB is also encouraging liquidity and business investment in the Euro area by introducing negative deposit rates in order to

stimulate lending by European banks.

We expect the Euro area economy to grow at a rate of 1.0% during calendar 2015, as the ECB’s stimulus measures take hold, and expect the

ECB to hold its key interest rate at the current level for the foreseeable future.

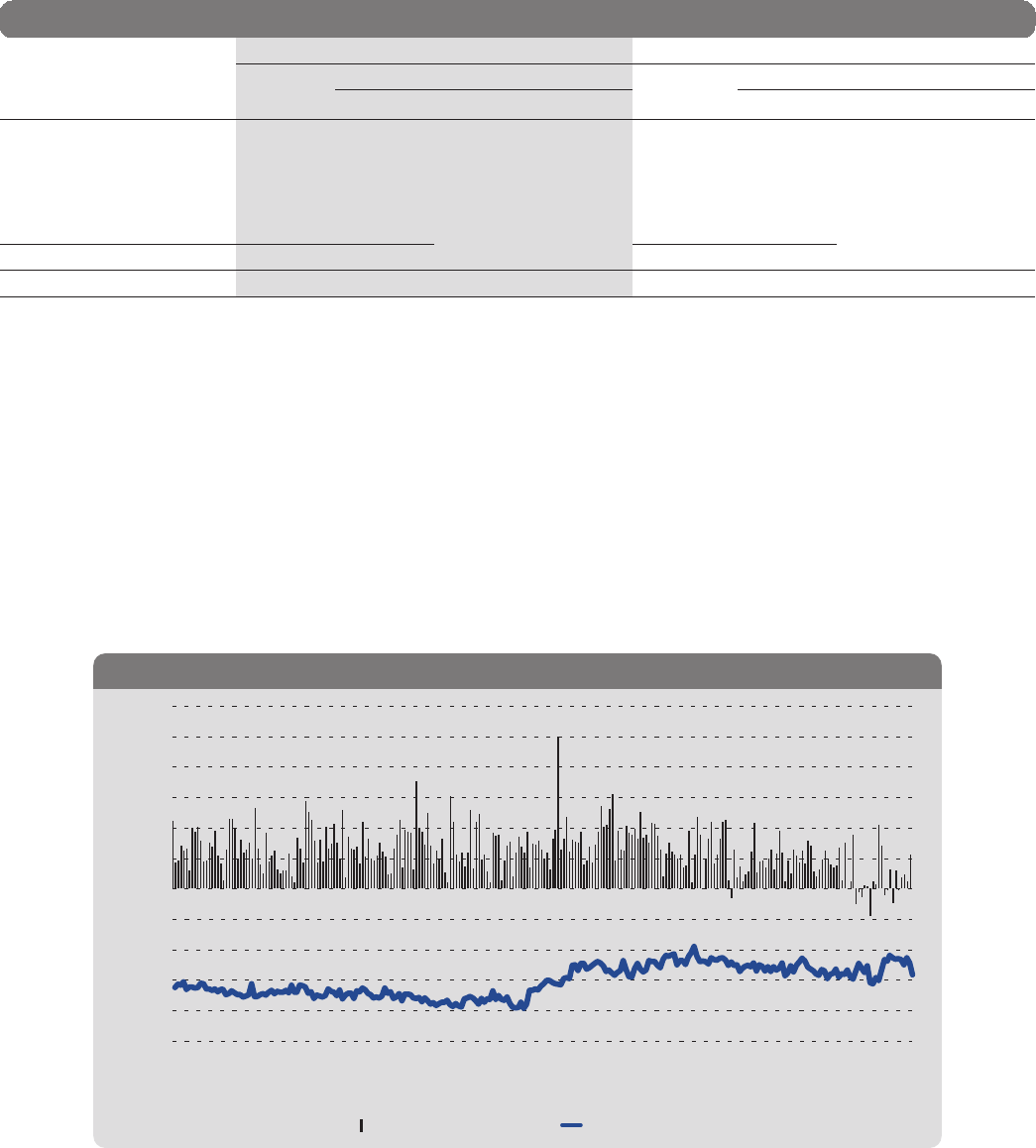

Financial markets

Equity markets in Canada, the U.S. and major European economies generally exhibited capital appreciation through most of fiscal 2014

supported by highly accommodative monetary policy, before concerns related to recent geopolitical uncertainty, the Ebola outbreak in Africa,

and expectations for recessionary conditions in Europe led to some volatility towards the end of our fiscal year. Yields on long-term government

bonds in Canada, the U.S. and major European economies have continued to decline over the year and remain near historically low levels. Credit

spreads remained relatively stable through most of fiscal 2014, but widened significantly in the last two months of fiscal 2014. Commodity

prices declined in the second half of calendar 2014. Oil prices, in particular, decreased sharply towards the end of our fiscal year due to a

combination of increased global supply and weak demand prospects.

Regulatory environment

We continue to monitor and prepare for regulatory developments in a manner that seeks to ensure compliance with new requirements while

mitigating any adverse business or economic impacts, including those with the potential to negatively impact our products or services. Such

impacts could result from new or amended regulations and the expectations of those who enforce them. Significant developments include

regulations enacted under the U.S. Dodd-Frank Wall Street Reform and Consumer Protection Act, such as restrictions on banking entities

engaging in proprietary trading and having certain relationships with hedge and private equity funds (the Volcker Rule); the Fed’s enhanced

prudential standards for Bank Holding Companies and Foreign Banking Organizations; changes to capital and liquidity rules under the Basel

Committee on Banking Supervision’s global standards (Basel III); over-the-counter (OTC) derivatives reforms; and the recently announced

voluntary commitments by MasterCard Canada and Visa Canada to reduce merchant credit card fees in Canada.

For a discussion on risk factors resulting from these and other regulatory developments which may affect our business and financial results,

refer to the Risk management – Top and emerging risks section. For further details on our framework and activities to manage risks, refer to the

Risk management and Capital management sections.

Defining and measuring success through Total Shareholder Returns

Our focus is to maximize total shareholder returns (TSR) through the achievement of top tier performance over the medium term (3-5 years) which

we believe reflects a longer term view of strong and consistent financial performance.

Maximizing TSR is aligned with our three strategic goals discussed earlier and we believe represents the most appropriate measure of

shareholder value creation. TSR is a concept used to compare the performance of our common shares over a period of time, reflecting share price

appreciation and dividends paid to common shareholders. The absolute size of the TSR will vary depending on market conditions, and the

relative position reflects the market’s perception of our overall performance relative to our peers over a period of time.

Financial performance objectives are used to measure progress against our medium-term TSR objectives. We review and revise these

financial performance objectives as economic, market and regulatory environments change. By focusing on our medium-term objectives in our

decision-making, we believe we will be well positioned to provide sustainable earnings growth and solid returns to our common shareholders.

Management’s Discussion and Analysis Royal Bank of Canada: Annual Report 2014 13

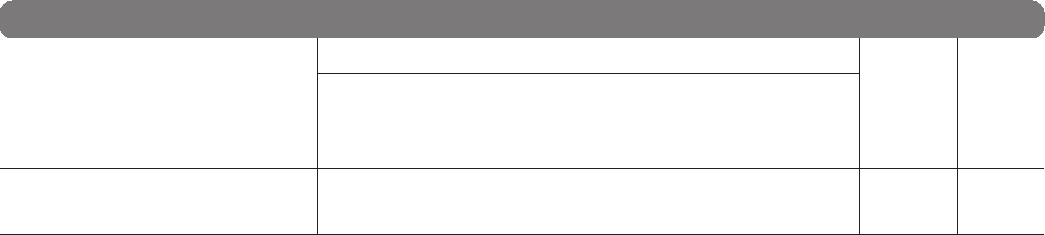

We achieved all our performance objectives in 2014. The following table provides a summary of our performance against our financial

performance objectives in 2014:

Financial performance objectives Table 2

2014 results Achieved

Diluted EPS growth of 7% + 9.3% ✓

ROE of 18% + 19.0% ✓

Strong capital ratios (CET1) (1) 9.9% ✓

Dividend payout ratio 40% – 50% 47% ✓

(1) For further details on the CET1 ratio, refer to the Capital management section.

For 2015, our financial performance objectives will remain unchanged.

We compare our TSR to that of a global peer group approved by our Board of Directors and consisting of the following 19 financial institutions:

• Canadian financial institutions: Bank of Montreal, Canadian Imperial Bank of Commerce, Manulife Financial Corporation, National Bank of

Canada, Power Financial Corporation, The Bank of Nova Scotia, and the Toronto-Dominion Bank.

• U.S. banks: Bank of America Corporation, JPMorgan Chase & Co., The Bank of New York Mellon Corporation, U.S. Bancorp, and Wells

Fargo & Company.

• International banks: Banco Bilbao Vizcaya Argentaria Group, Barclays PLC, BNP Paribas, Credit Suisse Group AG, Deutsche Bank Group,

National Australia Bank, and Westpac Banking Corporation.

Medium-term objectives – three and five year TSR vs. peer group average Table 3

Three year TSR (1) Five year TSR (1)

Royal Bank of Canada 23% 12%

2nd quartile 2nd quartile

Peer group average (excluding RBC) (2) 19% 8%

(1) The three and the five year average annual TSR are calculated based on our common share price appreciation plus reinvested dividends for the period October 31, 2011 to October 31, 2014

and October 31, 2009 to October 31, 2014 respectively, based on information as disclosed by Bloomberg L.P.

As a result of changes in the financial services industry over the past several years, and considering our performance and strategy, we recently

completed a re-evaluation of our peer group with the goal of ensuring that we include only those institutions in the global financial services

industry that are most relevant to us as competitors. Our Canadian peer group remains unchanged and we have revised our peer group of U.S.

and International banks. Our new peer group will be effective in 2015, and will include:

• Canadian financial institutions: Bank of Montreal, Canadian Imperial Bank of Commerce, Manulife Financial Corporation, National Bank of

Canada, Power Financial Corporation, The Bank of Nova Scotia, and the Toronto-Dominion Bank.

• U.S. banks: JPMorgan Chase & Co., and Wells Fargo & Company.

• International banks: Westpac Banking Corporation.

Common share and dividend information Table 4

For the year ended October 31 2014 2013 2012 2011 2010

Common share price (RY on TSX) – close, end of period $ 80.01 $ 70.02 $ 56.94 $ 48.62 $ 54.39

Dividends paid per share 2.76 2.46 2.22 2.04 2.00

Increase (decrease) in share price 14.3% 23.0% 17.1% (10.6)% (0.7)%

Total shareholder return 19.0% 28.0% 22.0% (6.7)% 2.9%

Key corporate events of 2014

Jamaican banking operations

On June 27, 2014, we completed the sale of RBC Royal Bank (Jamaica) Limited and RBTT Securities Jamaica Limited (collectively, RBC Jamaica) to

Sagicor Group Jamaica Limited, as announced on January 29, 2014. As a result of the transaction, we recorded a total loss on disposal of $100

million (before- and after-tax), including a loss of $60 million in the first quarter of 2014 and a further loss of $40 million in the third quarter of

2014, which includes foreign currency translation related to the closing of the sale. For further details, refer to Note 11 of our 2014 Annual

Consolidated Financial Statements.

Financial performance

On November 1, 2013, we adopted amendments to IAS 19 Employee benefits, as well as adopted IFRS 10 Consolidated Financial Statements and

IFRS 11 Joint Arrangements. The financial information presented in this document reflects the effects of these standards on our comparative

financial information presented for the year ended or as at October 31, 2013 and October 31, 2012. For further details, refer to Note 2 of our

2014 Annual Consolidated Financial Statements.

Overview

2014 vs. 2013

Net income of $9,004 million was up $662 million or 8% from a year ago. Diluted earnings per share (EPS) of $6.00 was up $0.51 and return on

common equity (ROE) of 19.0% was down 70 bps from 19.7% last year. Our Common Equity Tier 1 (CET1) ratio was 9.9%.

Our results reflected solid volume growth across most of our Canadian Banking businesses, higher earnings from growth in average

fee-based client assets in Wealth Management, and higher earnings in Capital Markets primarily reflecting strong equity markets, our continued

focus on origination and lending, and increased activity from client-focused strategies. The impact of foreign exchange translation also

contributed to the increase. These factors were partially offset by higher costs in support of business growth, a loss of $100 million (before- and

after-tax) related to the sale of RBC Jamaica, and higher litigation provisions and related legal costs in Capital Markets. In addition, our results

14 Royal Bank of Canada: Annual Report 2014 Management’s Discussion and Analysis

last year included a charge of $160 million ($118 million after-tax) as a result of new tax legislation in Canada, which affects the policyholders’

tax treatment of certain individual life insurance policies, as well as net favourable income tax adjustments of $214 million in Corporate Support.

For further details on our results and CET1 ratio, refer to the Business segment results and Capital management sections, respectively.

2013 vs. 2012

In 2013, net income of $8,342 million was up $835 million or 11% from 2012. Diluted EPS of $5.49 was up $0.58 and ROE of 19.7% was up

10 bps.

Our results reflected strong earnings growth across most of our business segments. Favourable income tax adjustments in 2013 of

$214 million related to prior years, lower provision for credit losses (PCL) reflecting improved credit quality, and continuing benefits from our

efficiency management activities also contributed to the increase. These factors were partially offset by lower trading revenue in Capital Markets

and a charge of $160 million ($118 million after-tax) in Insurance as a result of new tax legislation in Canada. In addition, our 2012 results were

impacted by net favourable adjustments of $60 million after-tax including a release of $128 million of tax uncertainty provisions and interest

income of $72 million ($53 million after-tax) related to a refund of taxes paid due to the settlement of several tax matters with the Canada

Revenue Agency (CRA), an adjustment related to a change in estimate of mortgage prepayment interest of $125 million ($92 million after-tax),

and a loss of $224 million ($213 million after-tax) related to the acquisition of the remaining 50% stake of RBC Dexia Investor Services Limited

(RBC Dexia).

Estimated impact of foreign currency translation on our consolidated financial results

Our foreign currency-denominated results are impacted by exchange rate fluctuations. Revenue, PCL, insurance policyholder benefits, claims and

acquisition expense (PBCAE), non-interest expense and net income denominated in foreign currency are translated at the average rate of

exchange for the year.

The following table reflects the estimated impact of foreign exchange translation on key income statement items:

Table 5

(Millions of Canadian dollars, except per share amounts) 2014 vs. 2013 2013 vs. 2012

Increase (decrease):

Total revenue $ 818 $ 213

PCL 93

PBCAE 75 8

Non-interest expense 510 110

Net income 121 53

Impact on EPS from continuing operations:

Basic $ .08 $ .04

Diluted .08 .04

The relevant average exchange rates that impact our business are shown in the following table:

Table 6

(Average foreign currency equivalent of C$1.00) (1) 2014 2013 2012

U.S. dollar 0.914 0.977 0.997

British pound 0.551 0.626 0.630

Euro 0.680 0.740 0.771

(1) Average amounts are calculated using month-end spot rates for the period.

Total revenue

Table 7

(Millions of Canadian dollars) 2014 2013 2012

Interest income $ 22,019 $ 21,148 $ 20,769

Interest expense 7,903 7,899 8,330

Net interest income $ 14,116 $ 13,249 $ 12,439

Net interest margin (on average earning assets) (1) 1.86% 1.88% 1.97%

Investments (2) $ 7,355 $ 6,408 $ 5,084

Insurance (3) 4,957 3,911 4,897

Trading 742 867 1,305

Banking (4) 4,090 3,909 3,399

Underwriting and other advisory 1,809 1,569 1,434

Other (5) 1,039 769 589

Non-interest income $ 19,992 $ 17,433 $ 16,708

Total revenue $ 34,108 $ 30,682 $ 29,147

(1) Net interest margin (on average earning assets) is calculated as net interest income divided by average earning assets.

(2) Includes securities brokerage commissions, investment management and custodial fees, and mutual fund revenue.

(3) Includes premiums and investment and fee income. Investment income includes the change in fair value of investments backing

policyholder liabilities and is largely offset in PBCAE.

(4) Includes service charges, foreign exchange revenue other than trading, card service revenue and credit fees.

(5) Includes other non-interest income, net gain (loss) on available-for-sale (AFS) securities and share of profit in associates.

2014 vs. 2013

Total revenue increased $3,426 million or 11% from last year. The impact of foreign exchange translation this year increased our total revenue by

$818 million.

Management’s Discussion and Analysis Royal Bank of Canada: Annual Report 2014 15

Net interest income increased $867 million or 7%, mainly due to solid volume growth of 5% across most of our businesses in Canadian

Banking and higher trading-related net interest income in Capital Markets. Higher lending activity in Capital Markets also contributed to the

increase. For further details on the change in net interest income, refer to the Supplementary information section.

Net interest margin was down 2 bps compared to last year largely due to the continuing low interest rate environment and competitive

pressures. For further details on net interest margin, refer to the Supplementary information section.

Investments revenue increased $947 million or 15%, mainly due to higher revenue from growth in average fee-based client assets in Wealth

Management resulting from capital appreciation and strong net sales. Higher mutual fund distribution fees also contributed to the increase.

Insurance revenue increased $1,046 million or 27%, mainly due to the change in fair value of investments backing our policyholder

liabilities resulting from a decrease in long-term interest rates, largely offset in PBCAE. Business growth in our European life and U.K. annuity

products also contributed to the increase.

Banking revenue increased $181 million or 5%, mainly due to the impact of foreign exchange translation, higher credit card balances and

transaction volumes, and higher service fee revenue. These factors were partially offset by lower loan syndication activity compared to the strong

levels last year.

Underwriting and other advisory revenue increased $240 million or 15%, mainly due to strong growth in equity origination reflecting

increased issuance activity, and higher mergers and acquisitions (M&A) activity reflecting increased mandates.

Other revenue increased $270 million or 35%, mainly due to favourable cumulative accounting adjustments in Personal & Commercial

Banking, and gains on credit default swaps used to economically hedge our corporate loan portfolio in Capital Markets compared to losses

last year.

2013 vs. 2012

Total revenue increased $1,535 million or 5% as compared to 2012, mainly due to solid volume growth across all businesses in Canadian

Banking, higher revenue from growth in average fee-based client assets across all businesses in Wealth Management, and incremental

revenue related to our additional 50% ownership of Investor Services. The inclusion of our acquisition of Ally Canada, strong growth in our

lending portfolio in Capital Markets, and in our loan syndication business primarily in the U.S., and higher debt origination reflecting solid

issuance activity also contributed to the increase. These factors were partially offset by a change in fair value of investments backing our

policyholder liabilities resulting from an increase in long-term interest rates, largely offset in PBCAE, lower fixed income trading revenue, and

spread compression. In addition, 2012 was favourably impacted by a mortgage prepayment interest adjustment of $125 million resulting from

a change in methodology with respect to the timing of recognition of mortgage prepayment interest.

Additional trading information

Table 8

(Millions of Canadian dollars) 2014 2013 2012

Total trading revenue

Net interest income $ 2,029 $ 1,661 $ 1,532

Non-interest income 742 867 1,305

Total trading revenue $ 2,771 $ 2,528 $ 2,837

Total trading revenue by product

Interest rate and credit $ 1,560 $ 1,611 $ 1,932

Equities 814 594 516

Foreign exchange and commodities 397 323 389

Total trading revenue $ 2,771 $ 2,528 $ 2,837

Trading revenue (teb) by product

Interest rate and credit $ 1,560 $ 1,611 $ 1,932

Equities 1,305 972 945

Foreign exchange and commodities 397 323 389

Total trading revenue (teb) $ 3,262 $ 2,906 $ 3,266

Trading revenue (teb) by product – Capital Markets

Interest rate and credit $ 1,293 $ 1,350 $ 1,584

Equities 1,244 942 925

Foreign exchange and commodities 333 286 323

Total Capital Markets trading revenue (teb) $ 2,870 $ 2,578 $ 2,832

2014 vs. 2013

Total trading revenue of $2,771 million, which comprises trading-related revenue recorded in Net interest income and Non-interest income, was

up $243 million, or 10%, mainly due to higher equity trading revenue reflecting strong market conditions and higher commodities trading

revenue. These factors were partially offset by lower fixed income trading revenue largely driven by the unfavourable impact of the

implementation of valuation adjustments related to funding costs on uncollateralized OTC derivatives (FVA), and the exiting of certain proprietary

trading strategies to comply with the Volcker Rule.

2013 vs. 2012

Total trading revenue of $2,528 million, which comprises trading-related revenue recorded in Net interest income and Non-interest income, was

down $309 million, or 11%, mainly due to lower fixed income trading revenue, largely in Europe, as a result of challenging market conditions.

16 Royal Bank of Canada: Annual Report 2014 Management’s Discussion and Analysis

Provision for credit losses

2014 vs. 2013

Total PCL decreased $73 million or 6% from a year ago, mainly due to lower provisions in Capital Markets and Wealth Management, partially

offset by higher provisions in Personal & Commercial Banking, primarily in Caribbean Banking.

2013 vs. 2012

Total PCL decreased $62 million or 5% as compared to 2012, mainly reflecting improved credit quality in our Personal & Commercial banking,

partially offset by higher provisions in Capital Markets and Wealth Management.

For further details on PCL, refer to the Credit quality performance section.

Insurance policyholder benefits, claims and acquisition expense

2014 vs. 2013

PBCAE increased $789 million or 28% from a year ago, mainly due to the change in fair value of investments backing our policyholder liabilities,

which was largely offset in revenue, and the impact of foreign exchange translation. These factors were partially offset by lower net claims costs.

In addition, our PBCAE last year included the unfavourable impact of the charge of $160 million related to new tax legislation in Canada, which

affects the policyholders’ tax treatment of certain individual life insurance policies, and a favourable impact from interest and asset related

activities on the Canadian life business.

2013 vs. 2012

PBCAE decreased $837 million or 23% as compared to 2012, mainly due to the change in fair value of investments backing our policyholder

liabilities, which was largely offset in insurance revenue. Favourable actuarial adjustments reflecting management actions and assumption

changes also contributed to the decrease. These factors were partially offset by the charge related to new tax legislation in Canada.

Non-interest expense

Table 9

(Millions of Canadian dollars) 2014 2013 2012

Salaries $ 4,834 $ 4,604 $ 4,089

Variable compensation 4,388 3,924 3,638

Benefits and retention compensation 1,561 1,464 1,216

Share-based compensation 248 256 139

Human resources $ 11,031 $ 10,248 $ 9,082

Equipment 1,147 1,081 913

Occupancy 1,330 1,235 1,130

Communications 779 728 748

Professional fees 763 753 666

Outsourced item processing 246 250 254

Amortization of other intangibles 666 566 494

Impairment of other intangibles 810 –

Impairment of investments in joint ventures and associates –20 168

Other 1,691 1,323 1,186

Non-interest expense $ 17,661 $ 16,214 $ 14,641

Efficiency ratio (1) 51.8% 52.8% 50.2%

(1) Efficiency ratio is calculated as non-interest expense divided by total revenue.

2014 vs. 2013

Non-interest expense increased $1,447 million or 9%, primarily due to the impact of foreign exchange translation of $510 million, higher costs in

support of business growth, and higher variable compensation driven by higher revenue in Wealth Management and higher results in Capital

Markets. Increased litigation provisions and related legal costs in Capital Markets, and the loss of $100 million related to the sale of RBC Jamaica

also contributed to the increase. These factors were partly offset by continuing benefits from our efficiency management activities.

Efficiency ratio of 51.8% decreased 100 bps from 52.8% last year, mainly due to continuing benefits from our efficiency management

activities.

2013 vs. 2012

Non-interest expense increased $1,573 million or 11% as compared to 2012, primarily reflecting incremental costs related to our additional 50%

ownership of Investor Services and higher variable compensation mainly driven by higher revenue in Wealth Management. The inclusion of our

acquisition of Ally Canada, higher costs in support of business growth, and higher litigation provisions and related legal costs in Capital Markets

also contributed to the increase. These factors were partially offset by continued benefits from our ongoing focus on efficiency management

activities, and lower variable compensation in Capital Markets reflecting a lower compensation to revenue ratio. In addition, non-interest

expense was unfavourably impacted in 2012 by an impairment loss and other costs of $188 million related to the acquisition of the remaining

50% stake of RBC Dexia.

Management’s Discussion and Analysis Royal Bank of Canada: Annual Report 2014 17

Income and other taxes

Table 10

(Millions of Canadian dollars, except percentage amounts) 2014 2013 2012

Income taxes $ 2,706 $ 2,105 $ 2,028

Other taxes

Goods and services sales taxes $ 395 $ 370 $ 343

Payroll taxes 529 497 430

Capital taxes 86 85 79

Property taxes 106 119 120

Insurance premium taxes 51 50 50

Business taxes 825 16

$ 1,175 $ 1,146 $ 1,038

Total income and other taxes $ 3,881 $ 3,251 $ 3,066

Net income before income taxes $ 11,710 $ 10,447 $ 9,586

Canadian statutory income tax rate (1) 26.3% 26.2% 26.4%

Lower average tax rate applicable to subsidiaries (2.3) (1.8) (3.1)

Goodwill impairment 0.0 0.0 0.4

Tax-exempt income from securities (3.3) (2.8) (3.4)

Tax rate change 0.0 0.0 0.0

Effect of previously unrecognized tax loss, tax credit or

temporary differences (0.1) (0.5) (0.1)

Other 2.5 (1.0) 1.0

Effective income tax rate 23.1% 20.1% 21.2%

Effective total tax rate (2) 30.1% 28.0% 28.9%

(1) Blended Federal and Provincial statutory income tax rate.

(2) Total income and other taxes as a percentage of net income before income taxes and other taxes.

2014 vs. 2013

Income tax expense increased $601 million or 29% from last year, mainly due to higher earnings before income tax. The effective income tax rate

of 23.1% increased 300 bps as last year included net favourable tax adjustments, including $214 million of income tax adjustments related to

prior years.

Other taxes increased $29 million or 3%, mainly due to higher payroll taxes and sales taxes which were partially offset by lower business

taxes and property taxes. In addition to the income and other taxes reported in our Consolidated Statements of Income, we recorded income tax