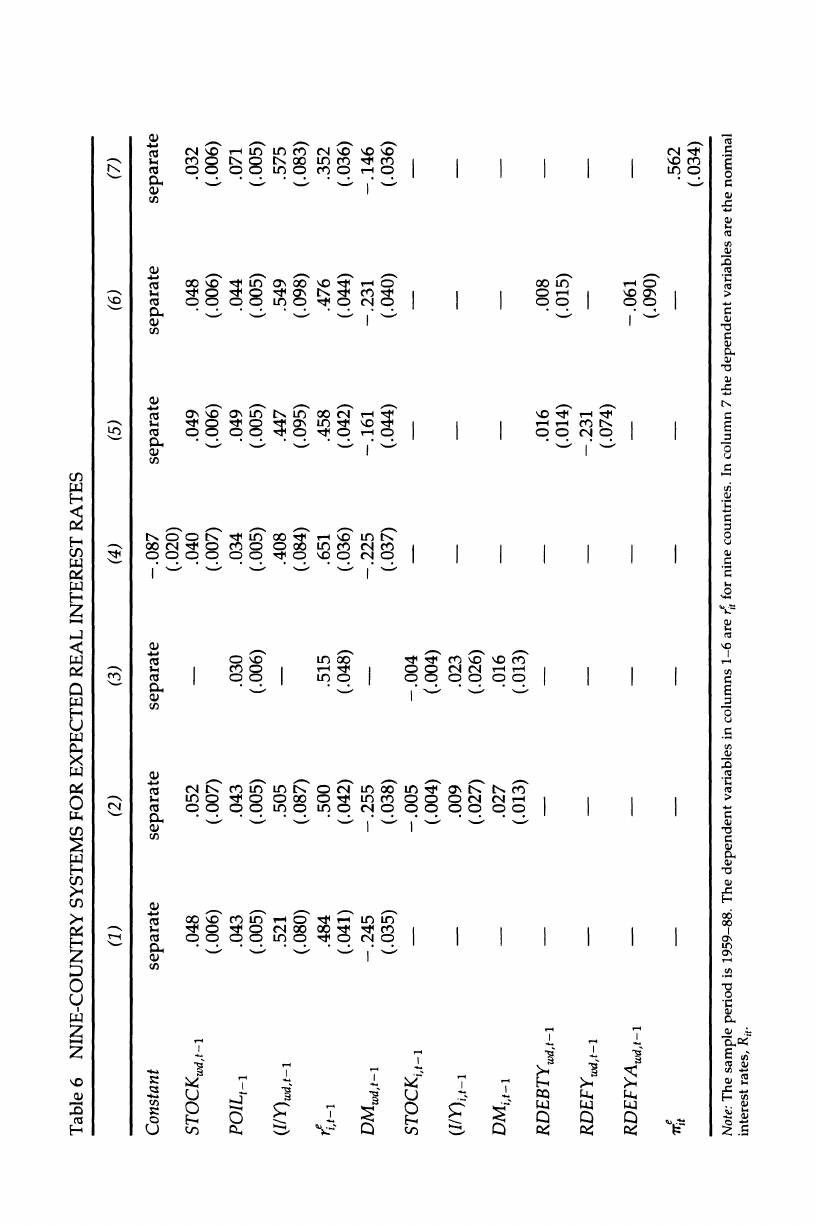

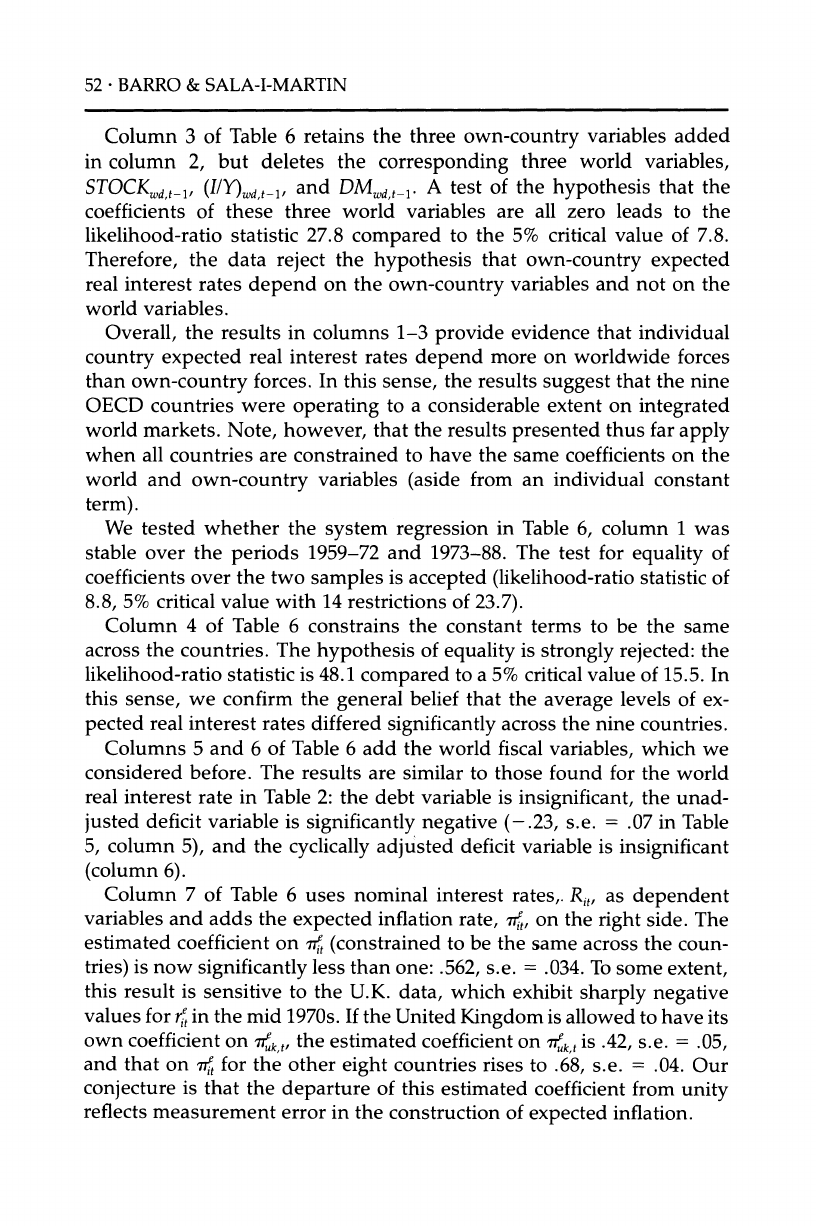

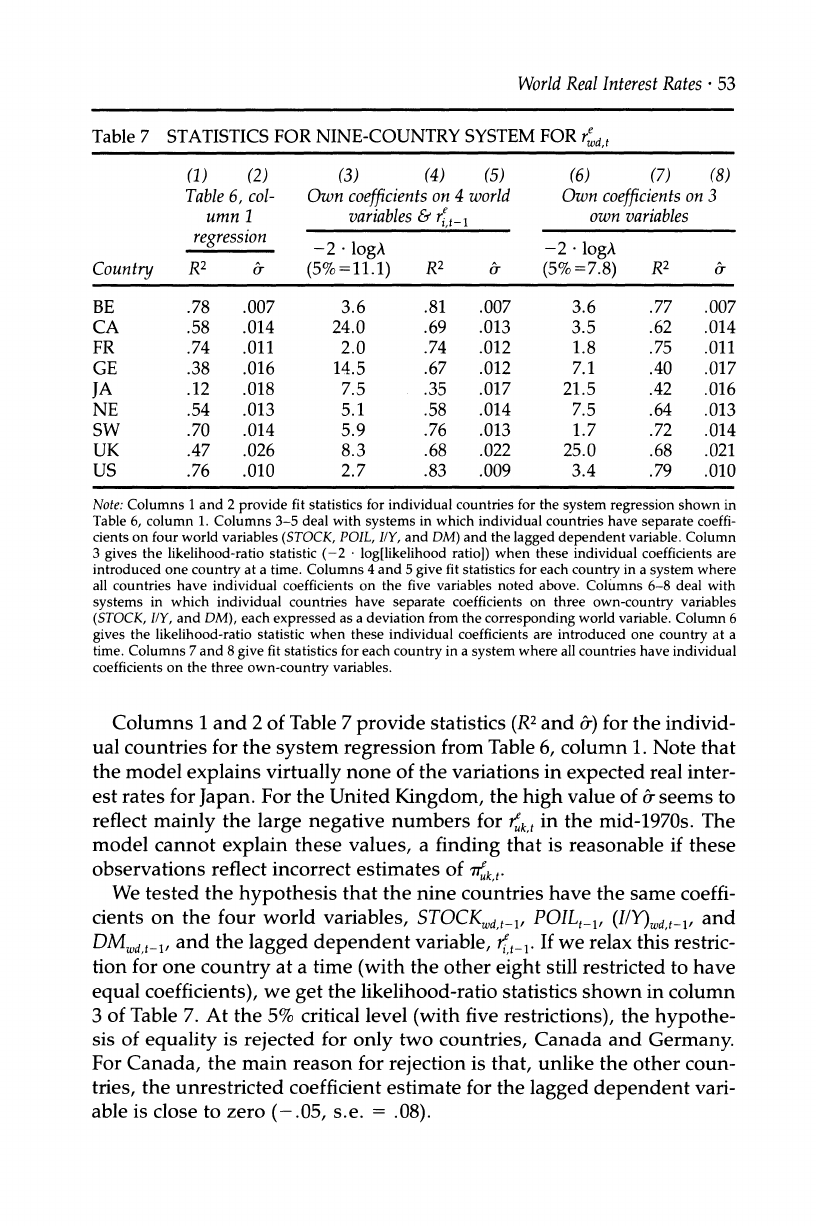

World Real Interest Rates RWD 1002 C10972

User Manual: RWD 1002

Open the PDF directly: View PDF ![]() .

.

Page Count: 61

This PDF is a selection from an out-of-print volume from the National

Bureau of Economic Research

Volume Title: NBER Macroeconomics Annual 1990, Volume 5

Volume Author/Editor: Olivier Jean Blanchard and Stanley Fischer, editors

Volume Publisher: MIT Press

Volume ISBN: 0-262-02312-1

Volume URL: http://www.nber.org/books/blan90-1

Conference Date: March 9-10, 1990

Publication Date: January 1990

Chapter Title: World Real Interest Rates

Chapter Author: Robert J. Barro, Xavier Sala-i-Martin

Chapter URL: http://www.nber.org/chapters/c10972

Chapter pages in book: (p. 15 - 74)

Robert

J. Barro

and Xavier Sala-i-Martin

HARVARD

UNIVERSITY

World

Real

Interest

Rates*

1. Introduction

This study began with the challenge to explain why real interest rates

were so high in the 1980s in the major industrialized countries. In order

to address this challenge we expanded the question to the determination

of real interest rates over a longer sample, which turned out to be 1959-

88. In considering how real interest rates were determined we focused

on the interaction between investment demand and desired saving in an

economy (ten OECD countries viewed as operating on an integrated

capital market) that was large enough to justify closed-economy assump-

tions. Within this "world" setting, high real interest rates reflect positive

shocks to investment demand (such as improvements in the expected

profitability of investment) or negative shocks to desired saving (such as

temporary reductions in world income). Our main analysis ends up

measuring the first kind of effect mainly by stock returns and the second

kind primarily by oil prices and monetary growth.

We think we have partial answers to how world real interest rates

have been determined, and, more specifically, to why real interest rates

were as high as they were in the 1980s. The key elements in the period

1981-86 appear to be favorable stock returns (which raised real interest

rates and stimulated investment) combined with high oil prices (which

also raised real interest rates, but discouraged investment).

In this paper we focus on the behavior of short-term real interest rates

since 1959 in nine OECD countries: Belgium (BE), Canada (CA), France

(FR), Germany (GE), Japan (JA), the Netherlands (NE), Sweden (SW),

the United Kingdom (UK), and the United States (US). These countries

*We are grateful for comments from Jason Barro, Olivier Blanchard, Bill Brainard, Bob

Lucas, Greg Mankiw, Larry Summers, and Andrew Warner. We appreciate the research

assistance of Casey Mulligan. The statistical analysis in this paper was carried out with

Micro TSP

16 *

BARRO & SALA-I-MARTIN

constitute the set of industrialized market economies for which we have

been able to obtain data since the late 1950s on relatively open-market

interest rates for assets that are analogous to U.S. Treasury bills. For

France and Japan, the available data are money-market rates. We were

unable to obtain satisfactory data on interest rates for Italy (IT) prior to

the early 1970s, but we included Italian data on other variables; there-

fore, parts of the analysis deal with ten OECD countries. These countries

accounted in 1960 for 65.4% of the overall real GDP for 114 market

economies, according to the PPP-adjusted data that were constructed by

Summers and Heston (1988). In 1985, the share was 63.4%. Thus, the

sample of ten countries represents a substantial fraction of the world's

real GDP.

We have concentrated thus far on short-term interest rates because of

the difficulty in measuring medium- or long-term expected inflation and,

hence, expected real interest rates. The quantification of expected infla-

tion is difficult even for short horizons, although the results in this paper

are robust to these problems. The patterns in short-term expected real

interest rates reveal a good deal of persistence; for example, the rates are

much higher for 1981-86 than for 1974-79, with the rates in the 1960s

falling in between. Given the ease with which participants in financial

markets can switch among maturities, the persisting patterns in ex-

pected real short-term rates would also be reflected in medium- and

long-term rates. Therefore, we doubt that the limitation of the present

analysis to short-term rates will be a serious drawback. We plan, how-

ever, to apply the approach also to longer-term rates.

2. Expected Inflation

and Expected

Real Interest

Rates

Investment demand and desired saving depend on expected real interest

rates. The data provide measures of nominal interest rates and realized

real rates. We could carry out the analysis with the realized real rates,

relying on a rational-expectations condition to argue that the difference

between the realized and expected real rates, which corresponds to the

negative of the difference between the actual and expected inflation rate,

involves a serially uncorrelated random error. Because the divergences

between actual and expected inflation are likely to be large in some peri-

ods, much more precise estimates could be attained by constructing rea-

sonably accurate measures of expected inflation and expected real interest

rates. Thus, we begin by estimating expected inflation rates.

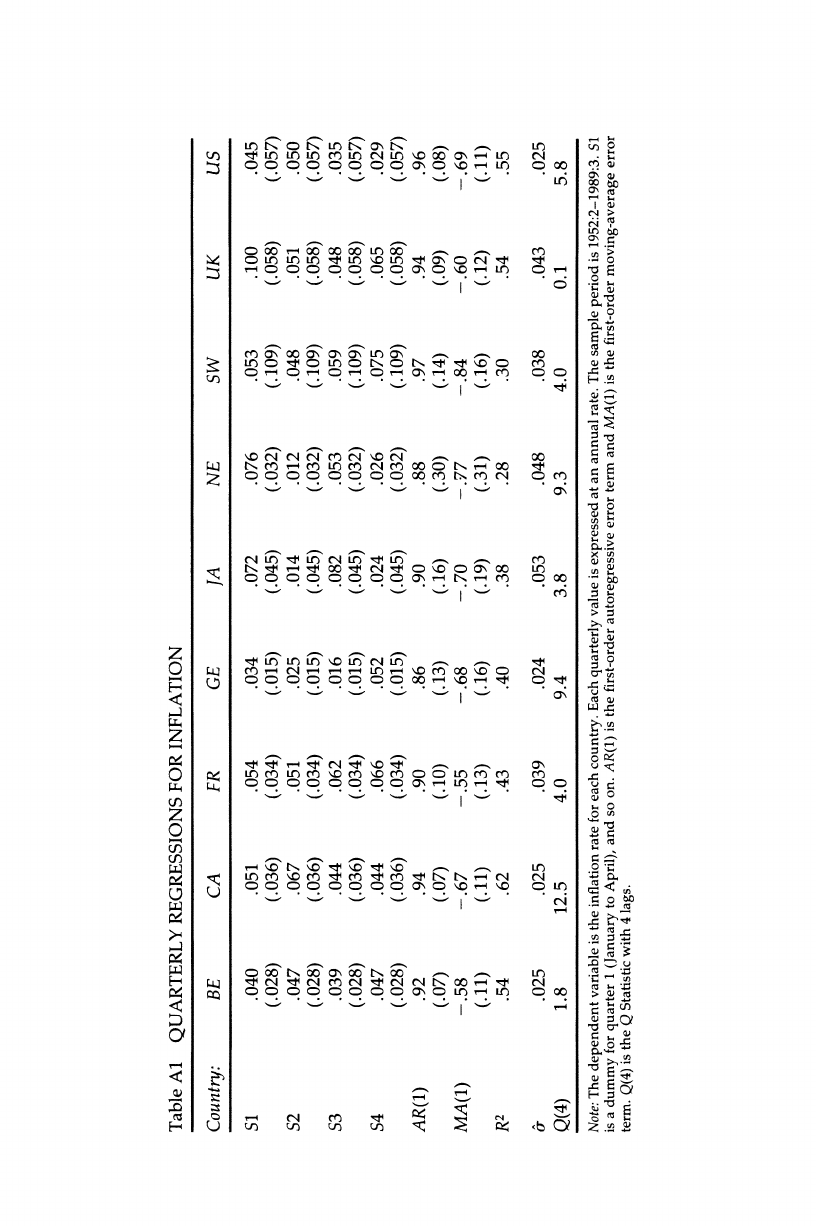

We have quarterly, seasonally unadjusted data on an index of con-

sumer prices for each country beginning in 1952:1. (For the United

States, we used the CPI less shelter to avoid problems with the treat-

World Real Interest Rates

?

17

ment of housing costs in the data prior to 1983.) The results reported in

this paper compute expected inflation for dates t = 1958:1 to 1989:4

based on regression forecasts for CPI inflation. (Quarter 1 represents the

annualized inflation rate from January to April, and so on.) Each regres-

sion uses data on inflation for country i from 1952:2 up to the quarter

prior to date t. That is, the data before date t are equally weighted, but

later data are not used to calculate forecasts.

The functional form for the inflation regressions is an ARMA (1,1)

with deterministic seasonals for each quarter; thus, expected inflation is

based solely on the history of inflation. We considered forms in which

inflation depended also on past values of M1 growth and nominal inter-

est rates, but the effects on the computed values of expected real interest

rates were minor. (The nature of the relation between inflation and past

monetary growth and interest rates also varied considerably across the

countries.) Within the ARMA (1,1) form, the results look broadly similar

across the nine OECD countries; typically, the estimated AR(1) coeffi-

cient is close to 0.9 and the estimated MA(1) coefficient ranges between

-0.4 and -0.8. Q-statistics for serial correlation are typically insignifi-

cant at the 5% level, although they are significant in some cases. The

pattern of seasonality varies a good deal across the countries. Appendix

Table Al shows the estimated equations that apply for the nine countries

over the sample 1952:2-1989:3.

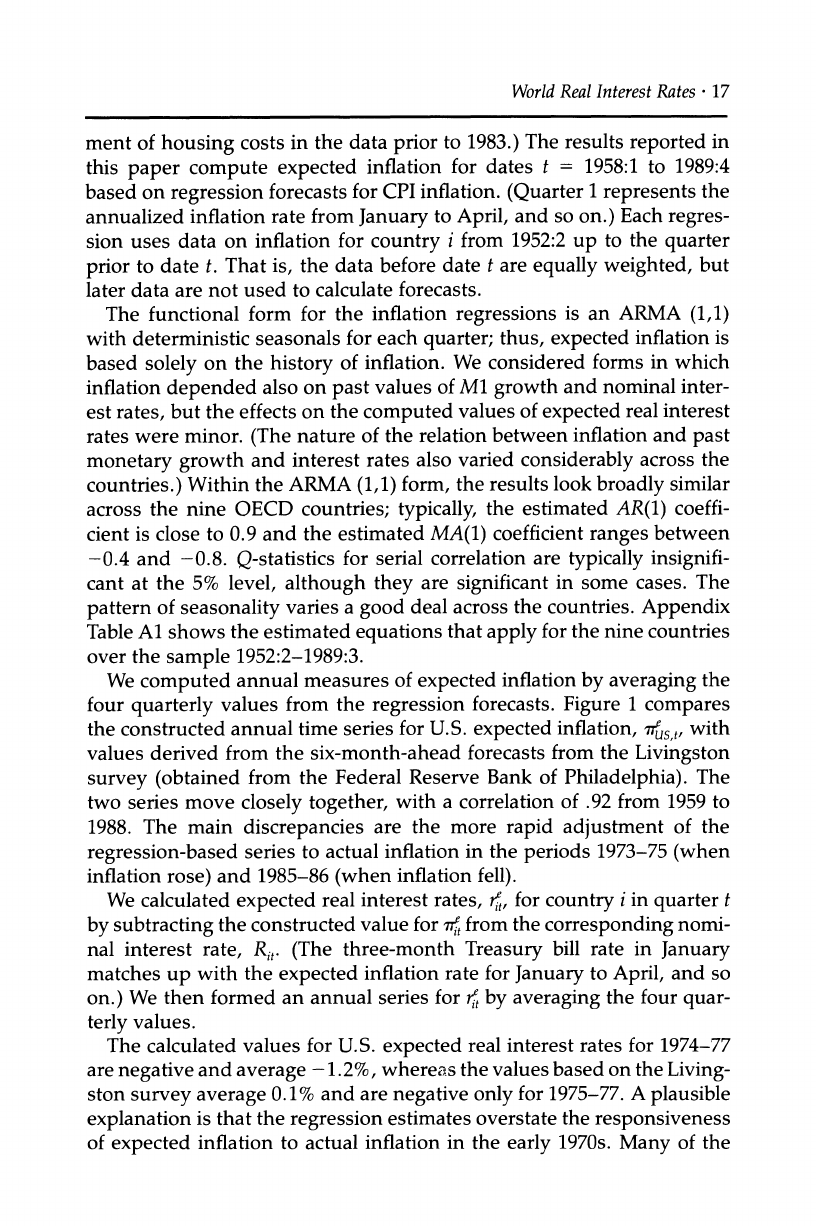

We computed annual measures of expected inflation by averaging the

four quarterly values from the regression forecasts. Figure 1 compares

the constructed annual time series for U.S. expected inflation, 7us,t, with

values derived from the six-month-ahead forecasts from the Livingston

survey (obtained from the Federal Reserve Bank of Philadelphia). The

two series move closely together, with a correlation of .92 from 1959 to

1988. The main discrepancies are the more rapid adjustment of the

regression-based series to actual inflation in the periods 1973-75 (when

inflation rose) and 1985-86 (when inflation fell).

We calculated expected real interest rates, t, for country i in quarter t

by subtracting the constructed value for Tie

from the corresponding nomi-

nal interest rate, Rit (The three-month Treasury bill rate in January

matches up with the expected inflation rate for January to April, and so

on.) We then formed an annual series for rit

by averaging the four quar-

terly values.

The calculated values for U.S. expected real interest rates for 1974-77

are negative and average -1.2%, whereas the values based on the Living-

ston survey average 0.1% and are negative only for 1975-77. A plausible

explanation is that the regression estimates overstate the responsiveness

of expected inflation to actual inflation in the early 1970s. Many of the

18 *

BARRO

& SALA-I-MARTIN

Figure

1 EXPECTED

INFLATION

RATES

FOR

THE UNITED

STATES

60 62 64 66 68 70 72 74 76 78 80 82 84 86

other eight OECD countries exhibit negative values of i for some of the

years between 1972 and 1976, and an overstatement of die

may also explain

this behavior. (If

we had used the full sample of data to compute ~it, rather

than just the data prior to period t, the calculated sensitivity of ~it to past

inflation would have been even greater. Thus, the tendency to calculate

negative values for it between 1972 and 1976 would have been even more

pronounced.) Except for the U.K. for 1975-77 (r,UK = -.115, -.027, and

-.058, respectively), the computed negative values for r since 1959 never

exceed 2% in magnitude.1

The subsequent analysis deals with the annual time series for expected

real interest rates, t. The limitation to annual values arises because some

of the other variables are available only annually.2 In any event, the high

1. Economic theory would not rule out small negative values for expected real interest rates

on nearly risk-free assets; however, opportunities for low-risk real investments without

substantial transaction costs (including storage of durables) would preclude expected

real rates that were substantially negative. It seems likely that at least the large-

magnitude negative values for rt represent mismeasurement of expected inflation. It

would be possible to recompute dt based on the restriction that the implied value for r4

exceed some lower bound, such as zero or a negative number of small magnitude. We

have not yet proceeded along these lines.

2. The main results reported below, however, involve variables that are available quarterly.

We are presently working on the results for quarterly data.

World Real Interest Rates *

19

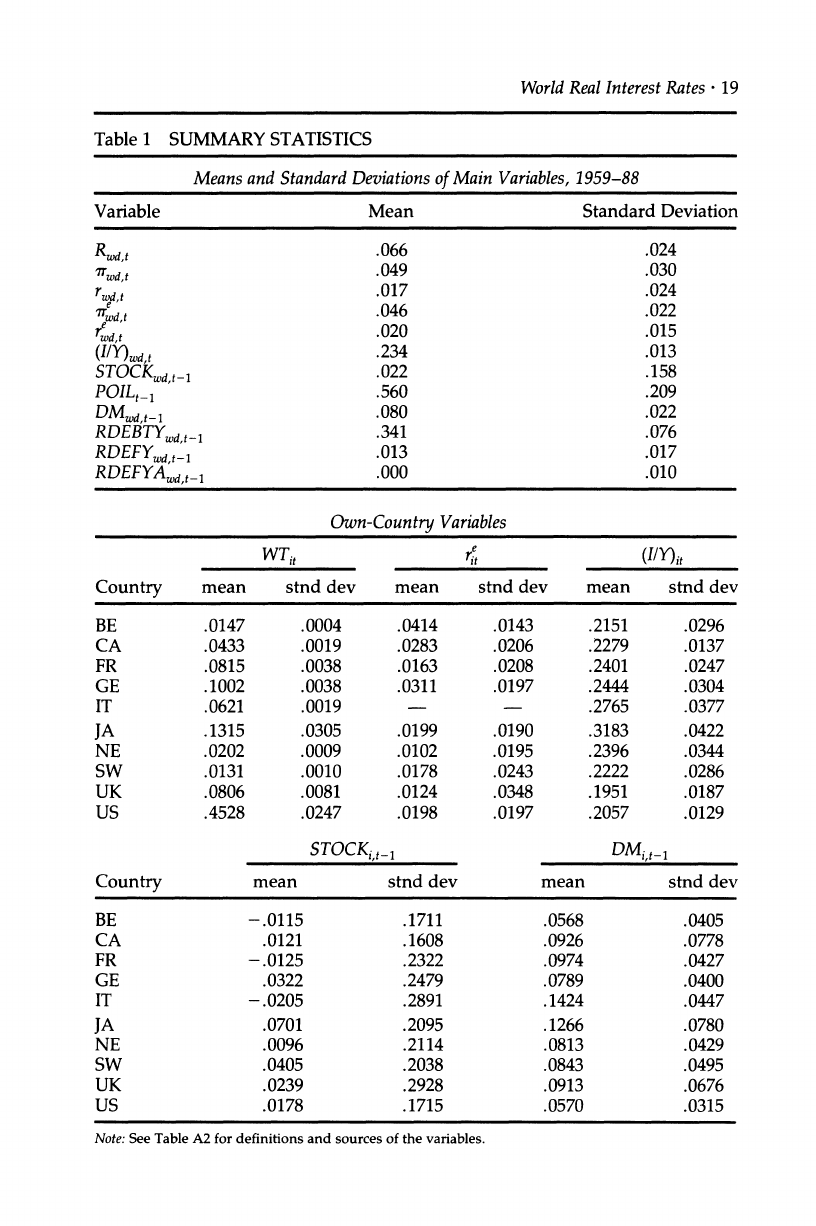

Table 1 SUMMARY STATISTICS

Means and Standard Deviations of Main Variables,

1959-88

Variable Mean Standard Deviation

Rwd,

t .066 .024

rrwd,

t .049 .030

rwd t .017 .024

erwa, .046 .022

wd,t .020 .015

(I/Y)wd,t .234 .013

STOCKwd,t_1 .022 .158

POIL_i1 .560 .209

DMWd,t-1 .080 .022

RDEBTYWd,t_ .341 .076

RDEFYwd,t1 .013 .017

RDEFYA, t_1 .000 .010

Own-Country

Variables

WTit ri (I/Y)it

Country mean stnd dev mean stnd dev mean stnd dev

BE .0147 .0004 .0414 .0143 .2151 .0296

CA .0433 .0019 .0283 .0206 .2279 .0137

FR .0815 .0038 .0163 .0208 .2401 .0247

GE .1002 .0038 .0311 .0197 .2444 .0304

IT .0621 .0019 .2765 .0377

JA .1315 .0305 .0199 .0190 .3183 .0422

NE .0202 .0009 .0102 .0195 .2396 .0344

SW .0131 .0010 .0178 .0243 .2222 .0286

UK .0806 .0081 .0124 .0348 .1951 .0187

US .4528 .0247 .0198 .0197 .2057 .0129

STOCKi,

t- DMi,,t

Country mean stnd dev mean stnd dev

BE -.0115 .1711 .0568 .0405

CA .0121 .1608 .0926 .0778

FR - .0125 .2322 .0974 .0427

GE .0322 .2479 .0789 .0400

IT -.0205 .2891 .1424 .0447

JA .0701 .2095 .1266 .0780

NE .0096 .2114 .0813 .0429

SW .0405 .2038 .0843 .0495

UK .0239 .2928 .0913 .0676

US .0178 .1715 .0570 .0315

Note: See Table

A2 for definitions and sources of the variables.

20 *

BARRO & SALA-I-MARTIN

serial correlation in the quarterly series on ri suggests that we may not

lose a lot of information by confining ourselves to the annual observa-

tions. The use of annual data means also that we do not have to deal

with possible seasonal variations in expected real interest rates.

We constructed a world index of a variable for year t by weighting the

value for country i in year t by the share of that country's real GDP for

year t in the aggregate real GDP of the nine- or ten-country sample.

(Henceforth, "world" signifies the aggregate of the nine- or ten-country

OECD sample.) In computing the weights, we used the PPP-adjusted

numbers for real GDP reported by Summers and Heston (1988). (For

1986-89, we used the shares for 1985, the final year of their data set.)

None of our results changed significantly if we weighted instead by

shares in world investment. Table 1 shows the average of each country's

Summers-Heston GDP weight (WT) from 1959 to 1988. Note that the

average share for the United States was .45, that for Japan was .13, and

so on. (In 1985, the U.S. share was .44 and the Japanese was .17.)

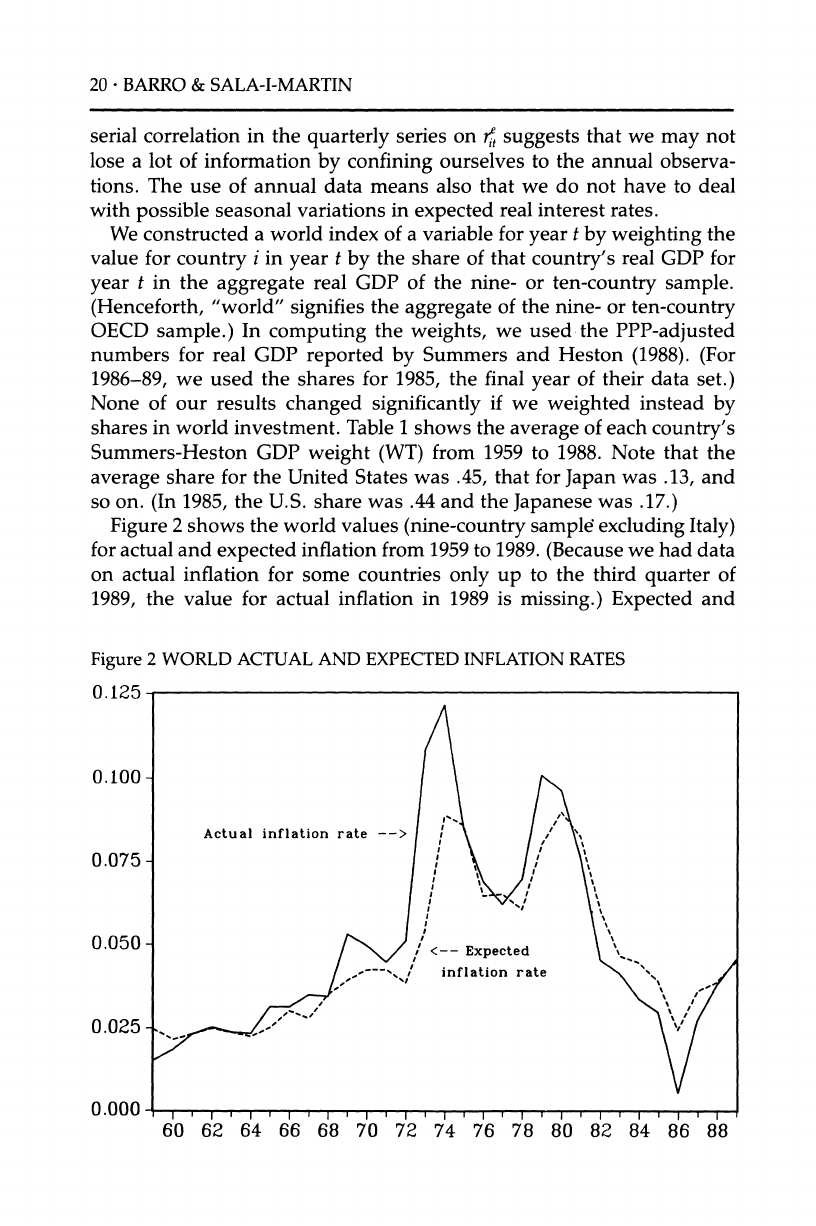

Figure 2 shows the world values (nine-country sample excluding Italy)

for actual and expected inflation from 1959 to 1989. (Because we had data

on actual inflation for some countries only up to the third quarter of

1989, the value for actual inflation in 1989 is missing.) Expected and

Figure

2 WORLD ACTUAL

AND EXPECTED INFLATION RATES

0.125

60 62 64 66 68 70 72 74 76 78 80 82 84 86 88

World Real

Interest Rates ?

21

actual inflation move together in a broad sense, but the expected values

lag behind the increases in inflation in 1969, 1972-74, and 1979-80, and

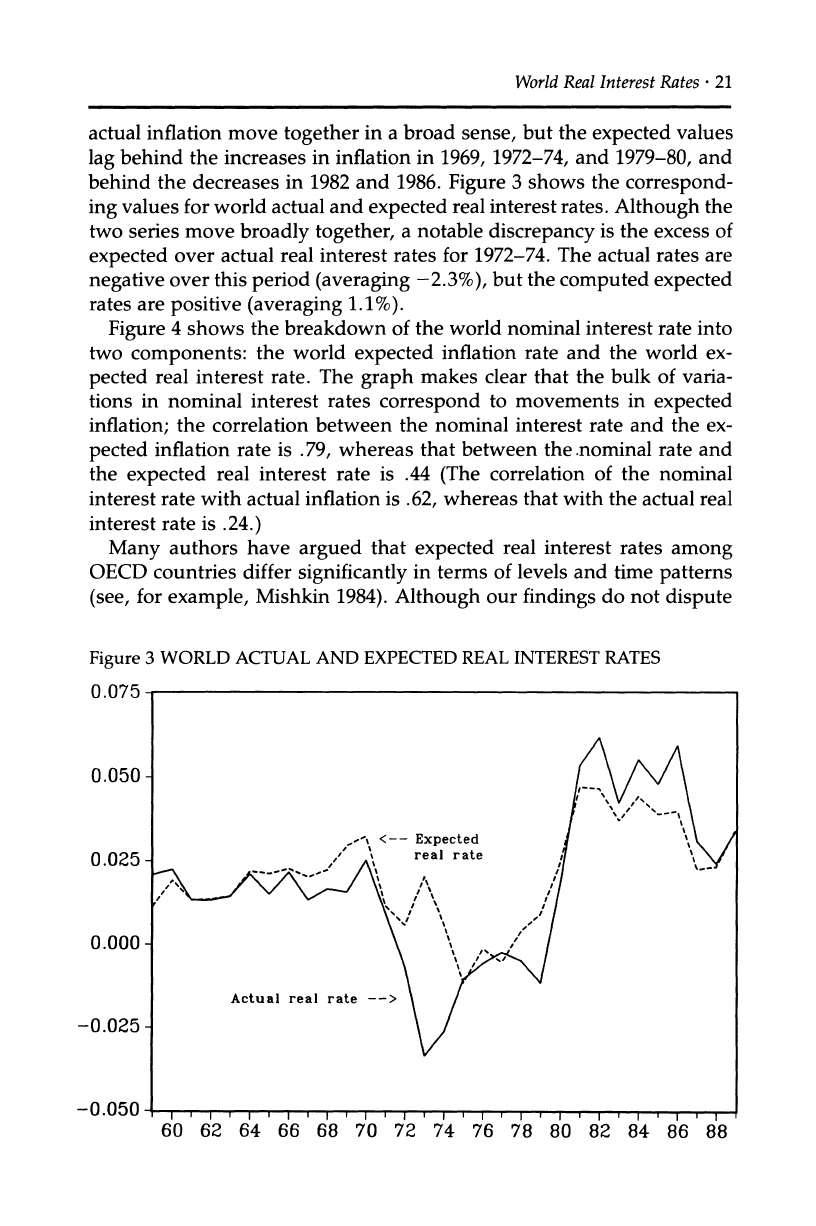

behind the decreases in 1982 and 1986. Figure 3 shows the correspond-

ing values for world actual and expected real interest rates. Although the

two series move broadly together, a notable discrepancy is the excess of

expected over actual real interest rates for 1972-74. The actual rates are

negative over this period (averaging -2.3%), but the computed expected

rates are positive (averaging 1.1%).

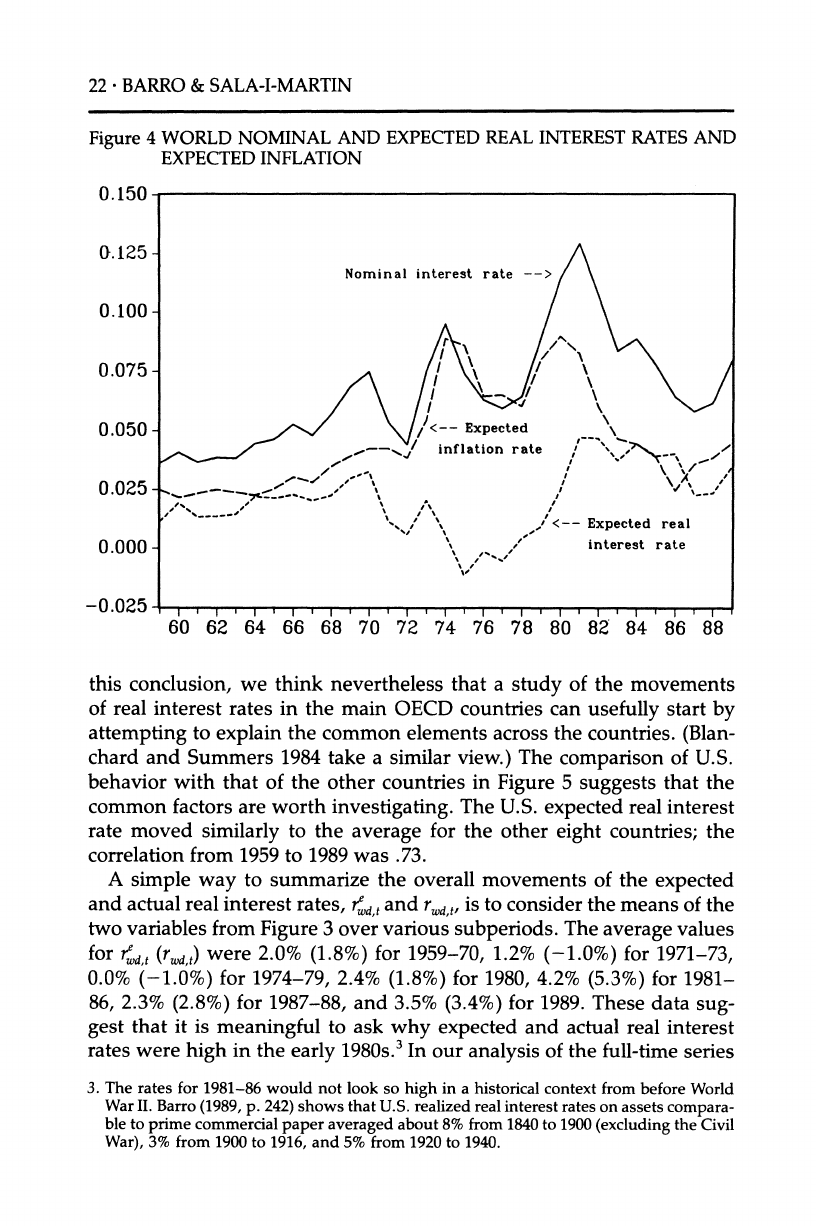

Figure 4 shows the breakdown of the world nominal interest rate into

two components: the world expected inflation rate and the world ex-

pected real interest rate. The graph makes clear that the bulk of varia-

tions in nominal interest rates correspond to movements in expected

inflation; the correlation between the nominal interest rate and the ex-

pected inflation rate is .79, whereas that between the.nominal rate and

the expected real interest rate is .44 (The correlation of the nominal

interest rate with actual inflation is .62, whereas that with the actual real

interest rate is .24.)

Many authors have argued that expected real interest rates among

OECD countries differ significantly in terms of levels and time patterns

(see, for example, Mishkin 1984). Although our findings do not dispute

Figure

3 WORLD

ACTUAL

AND EXPECTED

REAL

INTEREST RATES

70 72 74 76 78 80 82 84 86 88

22 *

BARRO

& SALA-I-MARTIN

Figure

4 WORLD NOMINAL

AND EXPECTED REAL INTEREST

RATES

AND

EXPECTED

INFLATION

0.150

0.125 -

Nominal interest rate -

0.100 -

0.075 - - xxxx

.,. / \/ .

0 /

2\ /

'<-- Expected real

0.000_- '

,, interest rate

-0.025 , , I , , i ,

60 62 64 66 68 70 72 74 76 78 80 82 84 86 88

this conclusion, we think nevertheless that a study of the movements

of real interest rates in the main OECD countries can usefully start by

attempting to explain the common elements across the countries. (Blan-

chard and Summers 1984 take a similar view.) The comparison of U.S.

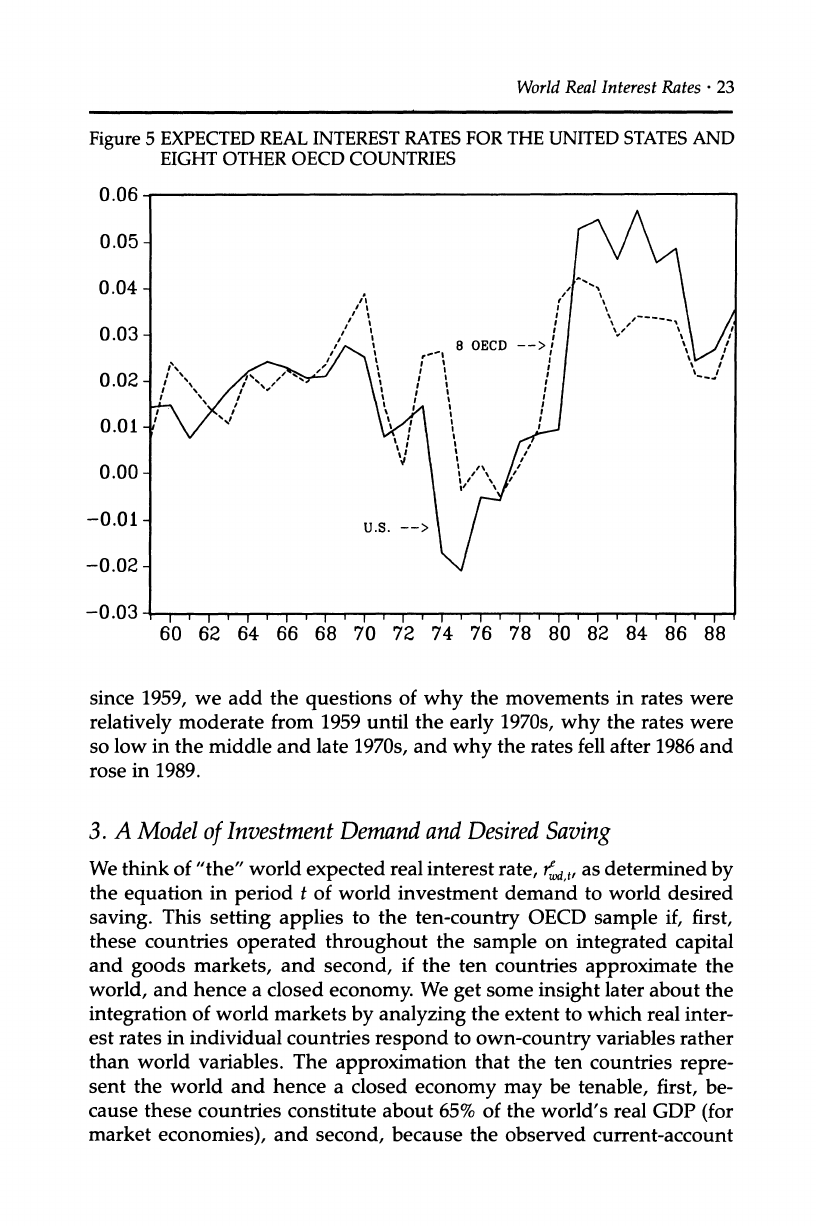

behavior with that of the other countries in Figure 5 suggests that the

common factors are worth investigating. The U.S. expected real interest

rate moved similarly to the average for the other eight countries; the

correlation from 1959 to 1989 was .73.

A simple way to summarize the overall movements of the expected

and actual real interest rates, id,t and rw,,, is to consider the means of the

two variables from Figure 3 over various subperiods. The average values

for rd,t (rwd,t)

were 2.0% (1.8%) for 1959-70, 1.2% (-1.0%) for 1971-73,

0.0% (-1.0%) for 1974-79, 2.4% (1.8%) for 1980, 4.2% (5.3%) for 1981-

86, 2.3% (2.8%) for 1987-88, and 3.5% (3.4%) for 1989. These data sug-

gest that it is meaningful to ask why expected and actual real interest

rates were high in the early 1980s.3 In our analysis of the full-time series

3. The rates for 1981-86 would not look so high in a historical context from before World

War

II. Barro (1989, p. 242) shows that U.S. realized real interest rates on assets compara-

ble to prime commercial paper averaged about 8% from 1840 to 1900 (excluding the Civil

War), 3% from 1900 to 1916, and 5% from 1920 to 1940.

World Real Interest

Rates *

23

Figure

5 EXPECTED

REAL INTEREST

RATES FOR

THE

UNITED

STATES

AND

EIGHT

OTHER

OECD COUNTRIES

0.06 -

0.05 -

0.04 - A \

0.03-

0.00- I

I

-0.01- .S.

-->' /

-0.02- -

-0.03 ,, ., , ,, , ,,,

60 62 64 66 68 70 72 74 76 78 80 82 84 86 88

since 1959, we add the questions of why the movements in rates were

relatively moderate from 1959 until the early 1970s, why the rates were

so low in the middle and late 1970s, and why the rates fell after 1986 and

rose in 1989.

3. A Model

of

Investment

Demand and

Desired

Saving

We think of "the" world expected real interest rate, r-,, as determined by

the equation in period t of world investment demand to world desired

saving. This setting applies to the ten-country OECD sample if, first,

these countries operated throughout the sample on integrated capital

and goods markets, and second, if the ten countries approximate the

world, and hence a closed economy. We get some insight later about the

integration of world markets by analyzing the extent to which real inter-

est rates in individual countries respond to own-country variables rather

than world variables. The approximation that the ten countries repre-

sent the world and hence a closed economy may be tenable, first, be-

cause these countries constitute about 65% of the world's real GDP (for

market economies), and second, because the observed current-account

24 *

BARRO & SALA-I-MARTIN

balance for the ten-country aggregate has been very small. We added up

each country's nominal current-account balance (expressed via current

exchange rates in terms of U.S. dollars) from 1960 to 1987 and divided by

the total nominal GDP (also converted by exchange rates into U.S. dol-

lars). The average value of the ratio of the aggregated current-account

balance to overall GDP was 0.1%. Moreover, the largest value from 1960

to 1987 (1971) was only 0.5% and the smallest (1984) was only -0.7%.

We now construct a simple model of investment demand and desired

saving. Although this model is used to interpret some of the empirical

findings, the general nature of the reduced-form results does not depend

on this particular framework. Hence, readers who are unimpressed by

our theory may nevertheless be interested in the empirical evidence.

We measure real investment, It, by gross domestic capital formation

(private plus public, nonresidential plus residential, fixed plus changes

in stocks). Thus, It excludes purchases of consumer durables and expen-

ditures on human capital. Investment demand, expressed as a ratio to

GDP, is determined by a q-type variable:

(IIY)t

= ao + a,1 log[PROF7/(r?+p,)]

+ u, (1)

where PROF' is expected profitability per unit of capital, r< is the ex-

pected real interest rate on assets like Treasury bills, Pt

is a risk premium,

and a1>0. The error term ut

is likely to be highly persistent because, first,

time-to-build considerations imply that current investment demand de-

pends on lagged variables that influenced past investment decisions,

and second, there may be permanent shifts in the nature of adjustment

costs, which determine the relation between investment demand and

the q variable. In first-difference form, equation (1) becomes

(I/Y)t

= a,

' Alog[PROFt/(+pt)] + (I/Y)t_1

+ Ut-Ut-1. (2)

Our analysis treats the error term, ut-ut_ , as roughly white noise.

We use the world real rate of return on the stock market through

December of the previous year STOCKt_i,

to proxy for the first difference

of the q variable, Alog[PROF/(<+pt)].4 This proxying is imperfect because

4. The stock-return

variable

for each country is the nominal rate of return

for the year

implied by the IFS December index for industrial-share prices less the December-to-

December inflation rate based on the consumer price index. We had broader stock-

return measures readily available for three countries-Canada, the United Kingdom,

and the United States-which together comprised 57% on average of the ten-country

GDP. The substitution of these numbers for the IFS values had a negligible impact on the

regression results we report later. We took this result as an indication that the IFS data

are probably satisfactory indicators of stock-market returns.

World

Real Interest Rates

*

25

of distinctions between average and marginal q,5 because of failure to

adjust for changes in the market value of bonds and depreciation of

capital stocks, and because the stock market values only a portion of the

capital that relates to our measure of investment. (The investment num-

bers include residential construction, noncorporate business invest-

ment, and public investment.) For these reasons, the best estimate of

Alog[PROFI/(re+pt)] would depend inversely on the change in rt, for a

given value of STOCKt_

.6 Therefore, we approximate the relation for

investment demand as

(IIY)t = ao + a1 *

STOCKt,1 - a, (r~-_1) + (I/Y)t_ + vt (3)

where a1>0 and a2>0.7

We assume that the desired saving rate (for the world aggregate of

national saving) is given by

(S/Y), = o + Pl(Y/Y)t + 32r~

+

+3 *

(S/Y)t-1 + error term (4)

where Yt

is current temporary income, the 3i's

are positive, and the error

term is treated as white noise. Equation (4) adopts the permanent-

income perspective in assuming that permanent changes in income do

not have important effects on the saving rate. Temporary changes in

income have little effect on consumer demand and therefore have a

positive effect on the desired saving rate, as given by the coefficient ,1.

Given the temporary-income ratio, (Y/Y)t,

the saving rate would respond

positively to r' in accordance with the coefficient /2. The variable (S/Y)t_

picks up persisting influences on the saving rate. It turns out in our

empirical estimation that 0<33<1 applies; that is, the desired saving rate

appears to exhibit less persistence than the investment-demand ratio,

which has a unitary coefficient on the lagged dependent variable in

equation (3).

We considered using measures of temporary government purchases,

5. See Hayashi (1982) for a discussion, in particular, of the adjustments of marginal q for tax

effects.

6. Let STOCKt = Alog(qt) + et, where qt = [PROFt(t+pt] and et can be interpreted as a

measurement error. Assume that the prior distribution is given by Alog(qt)

= et, that 4r

is

observed without error, and that no direct information about Pt is available. Then the

posterior estimate of Alog(qt)

gives weights to STOCKt

and (as a linear approximation) to

-rt_l, where the weight on -

t-_ rises with VAR(e)/AR(E). (Independent measure-

ment error in 4t

would lower the weight applied to 4-et-_). Our analysis uses data on

stock returns only through December of the previous year (and thereby avoids some

simultaneity problems). The omission of contemporaneous data on stock returns raises

VAR(e)

and thereby raises the weight applied to t-rte,.

7. The term (t-rte_ ) is approximately linear if pt >> applies.

26 *

BARRO

& SALA-I-MARTIN

especially defense expenditures, as influences on temporary income and

hence desired national saving rates. Up to this point, however, we have

been unable to isolate important temporary variations in the ratios of

real government purchases to real GDP over the period since 1959 for

the ten OECD countries we are studying.

We have had more success by thinking of the relative price of oil as an

indicator of world temporary income. Higher oil prices are bad for oil

importers, which predominate in the ten-country OECD sample. Be-

cause higher oil prices tend to reflect more effective cartelization of the

market for oil, an increase in prices also represents a global distortion

that is bad for the world as a whole. Moreover, high oil prices may be a

signal of disruption of international markets in a sense that goes beyond

oil; therefore, the effects on world income may be substantially greater

than those attributable to oil, per se.

Our subsequent analysis of real interest rates provides some indica-

tion that the level of the relative price of oil, rather than the change in

this relative price, is the variable that proxies for temporary income. This

result is reasonable if the relative price of oil is perceived to be stationary;

in this case, a high level for the current relative price signals a temporar-

ily high level. In the actual time series, the relative price of oil did

happen to return after 1985 to values close to those applying before 1973.

But our direct analysis of the time-series properties of the relative oil

price is inconclusive about stationarity.8

The empirical analysis uses the variable POILt,_, which is the relative

price of crude petroleum for December of the previous year from the

U.S. producer price index. The results do not change significantly if we

use instead a weighted average of relative petroleum prices for each

country. The precise concepts for these prices varied across the countries

and the data for some countries were unavailable for parts of the sample.

For these reasons, we used the U.S. variable in the main analysis.9

Thinking of POILt_1

as an inverse measure of the temporary income

ratio, (Y/Y)t,

the equation for the saving rate becomes

(S/Y)t = bo

- bi *

POILt - + b2 r + b3 (S/Y)t 1 + error term (5)

8. Even if the relative price of oil is nonstationary, the consequences of a change in the price

of oil for world income are likely to be partly transitory. In particular, the effects on

income would tend to diminish as methods of production adjusted to the new configura-

tion of relative prices.

9. The results are also similar if we use the dollar price for Venezuelan crude instead of the

U.S. PPI for crude petroleum. (The Saudi Arabian price is very close to the Venezuelan

price, but the IFS does not report the Saudi Arabian values after 1984.) The main

difference between the Venezuelan and U.S. series is that the Venezuelan one shows a

much larger proportionate increase in 1973.

World Real Interest Rates

*

27

where the bi's are positive. We assume that, given the stock return,

STOCKt_,,

the variable POILt_,

does not shift investment demand in equa-

tion (2). That is, at least the main effects of oil prices on investment

demand are assumed to be captured by the stock-market variable. With

this interpretation, the variable POILt, represents a shift to desired sav-

ing that is not simultaneously a shift to investment demand.

We also assume that the stock-market return, STOCKt_l,

has primarily

permanent effects on income; that is, we neglect effects on the tempo-

rary income ratio, (Y/Y)t, and thereby on desired saving in equation (4).

Given this assumption, the variable STOCKt_,

reflects a shift to invest-

ment demand that is not simultaneously a shift to desired saving. In

other words, the variables STOCKt_1

and POILt_1

will allow us to identify

the relations for investment demand and desired saving.

We might be able to quantify the interplay between stock returns and

temporary income by using measures of current profitability, such as

aftertax corporate profits. That is, we could estimate the implications of

stock returns for the part of temporary income that relates to the differ-

ence between current and expected future profitability. We have thus far

been unsuccessful in obtaining satisfactory measures of corporate profits

for some of the countries in the sample, and therefore have not yet

implemented this idea. (The main data series available from the OECD,

called "operating surplus," is an aggregate that is much broader than

corporate profits.) The limited data we have indicate that current stock

returns or other variables lack significant predictive content for future

changes in the ratio of corporate profits to GDP. It may, therefore, be

roughly correct that stock returns have little interplay with the tempo-

rary income that corresponds to gaps between current and expected

future corporate profits.

We now extend the analysis to consider the effects of monetary and

fiscal variables. We think of these variables as possible influences on the

desired saving rate in equation (4). In some models where money is

nonneutral-such as Keynesian models with sticky prices or wages-a

higher rate of monetary expansion raises temporary income and thereby

increases the desired saving rate.10

With respect to fiscal variables, many

economists (such as Blanchard 1985) argue that increases in public debt

or prospective budget deficits reduce desired national saving rates.

Let DMt_1

be a measure of monetary expansion and Ft_-

be a measure of

10. In the analysis

of Mundell

(1971),

higher monetary

expansion

leads to higher

expected

inflation and thereby

to a lower real demand for money. The reduction

in real

money

balances is assumed to lead to a decrease in consumer demand and hence to an

increase

in the desired saving rate. Tobin

(1965)

gets an increase in the desired

saving

rate

in a similar manner.

28 *

BARRO

& SALA-I-MARTIN

fiscal expansion, each applying up to the end of year t- 1. Then we can

expand the relation for the desired saving rate from equation (5) to

(S/Y), = bo - b, *

POILt,_ + b2re + b3(S/Y)t_, + b4DMt-_ - bFt,_, + et. (6)

The coefficients are defined so that bi > 0 applies in the theoretical

arguments discussed above.

Given our closed-economy assumption (for the ten-country OECD

sample), r' is determined by equating the investment-demand ratio,

(IIY)t

from equation (3), to the desired saving rate, (S/Y)t

from equation

(6). The reduced-form relations for r' and (I/Y)t

are as follows:

rt = b)[a0-b0 + a, *

STOCKt, + b, POILt_1

+ a2

' rt1

(a2+b2)

+ (1-b3) . (I/Y)t_ - b * DMt 1 + b5 Ft-, + vt - e,]. (7)

1

(IIY)t

= *

[a b2+ + ab a1b2

*

STOCKt-,

- a2b1,

POILt, + a2b2

* 1

(a2+b2)

+ (b2+a2b3)

(IIY),_ + a2b4 DM,t- - a2b5

Ft- + a2et

+ b2vt. (8)

The reduced form of the model in equations (7) and (8) implies the

following:

1. Higher stock returns, STOCKt 1, raise r\ and (I/Y)t,

2. Higher oil prices, POIL,_ , raise ri but lower (I/Y)t,

3. Higher monetary growth, DMt_ , lowers ri and raises (IIY)t

(in models

where monetary expansion stimulates desired saving),

4. Greater fiscal expansion, Ft,,, raises ri and lowers (IIY)t

(in models

where fiscal expansion reduces desired national saving).

Two additional implications that concern lagged dependent variables are

more dependent on the dynamic effects built into the model structure:

5. The lagged value ri-, has positive effects on ri and (IIY), (because,

holding fixed the other variables including (IIY)t_

, a higher ft_,

effec-

tively shifts up investment demand).

6. The lagged value (I/Y)t_1

has a positive effect on (IIY)t

because of the

persistence built into investment demand and desired saving. The

effect on re is positive if the persistence in investment demand is

greater than that in desired saving; that is, if b3<l.

World Real Interest Rates

?

29

Figure

6 WORLD

RATIO OF REAL INVESTMENT

TO REAL

GDP

0.27

0.26 -

0.25-

0.24 -

0.23 -

0.22 -

0.21-

0.20 ,

, , ,

, ,

60 62 64 66 68 70 72 74 76 78 80 82 84 86 88

4. Empirical

Analysis

of Expected

Real Interest Rates

and

Investment Ratios

Table 1 contains means and standard deviations for the main variables

used in the analysis. Table A2 in the Appendix has definitions and

sources for the variables. The world ratio of real investment (gross do-

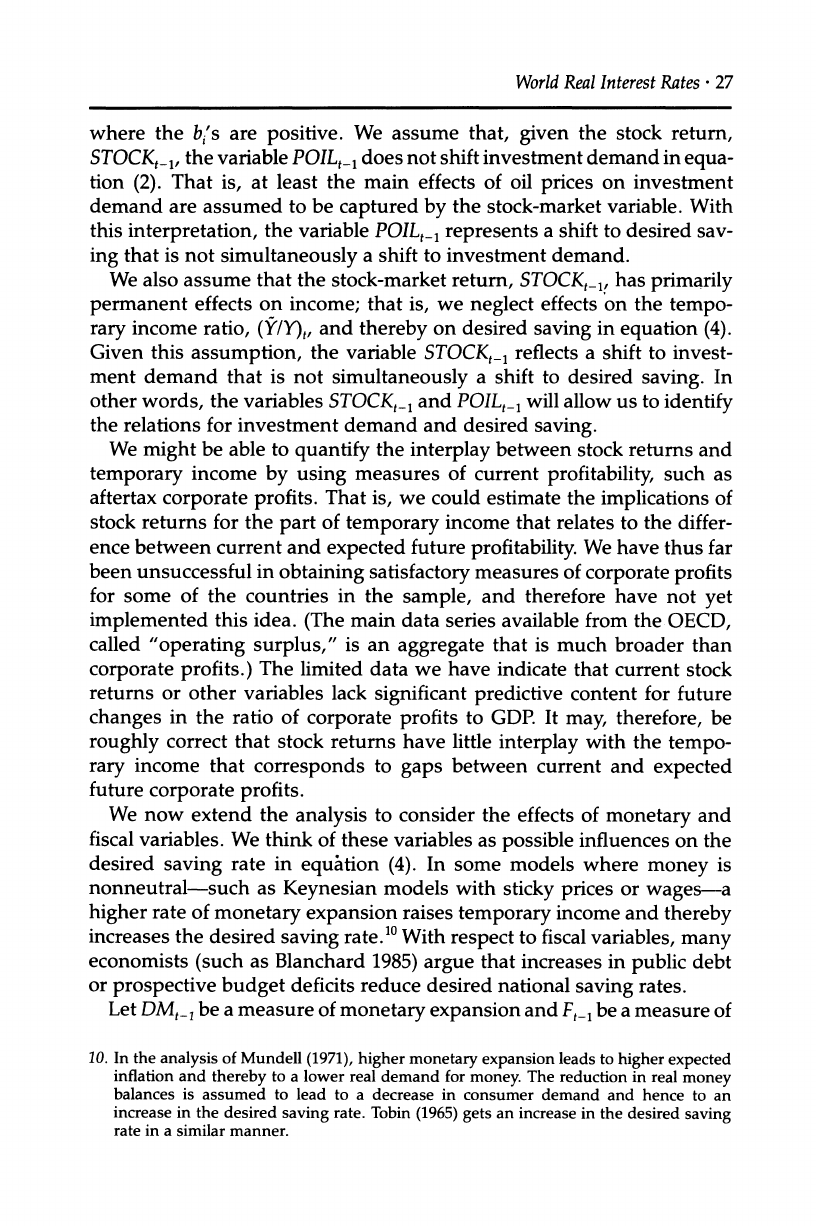

mestic capital formation) to real GDP appears in Figure 6. We use figures

on gross investment because the data on depreciation are likely to be

unreliable. As with the other world measures, the investment ratio is the

GDP-weighted value of the numbers from the ten OECD countries.

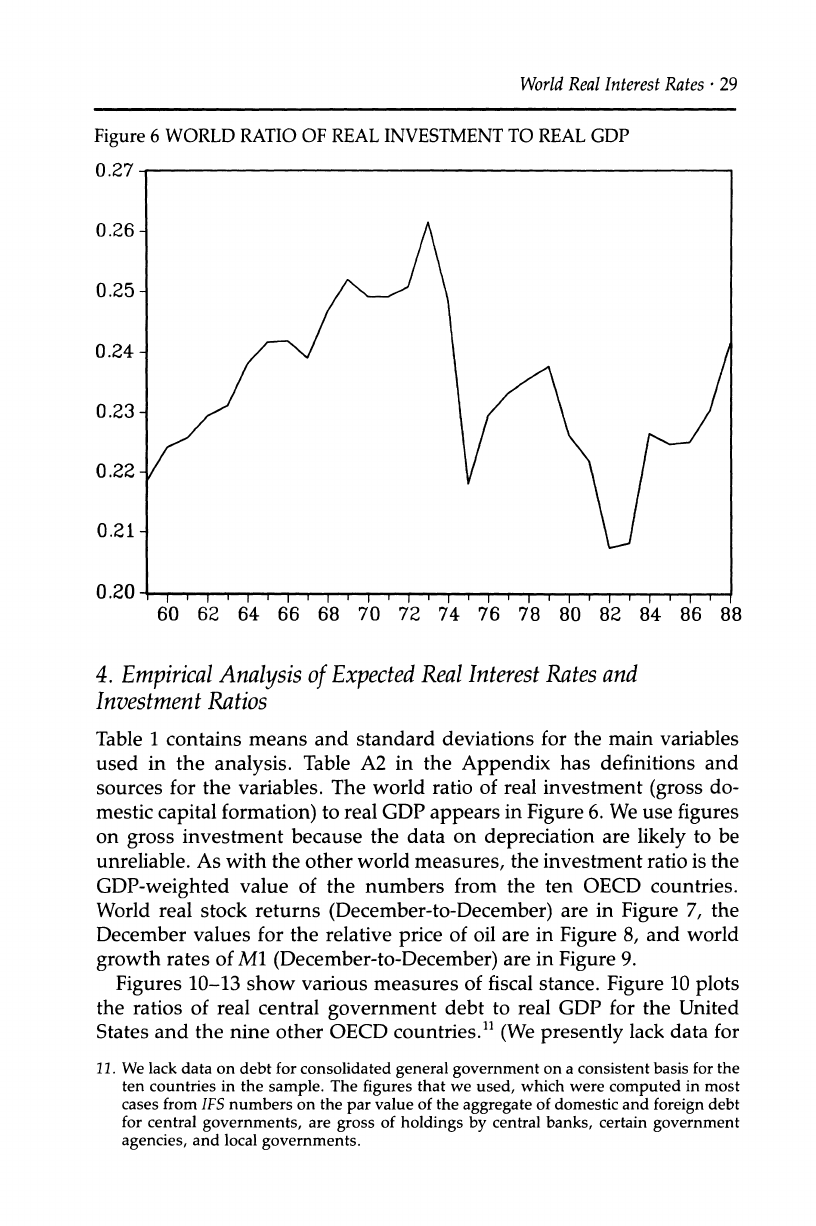

World real stock returns (December-to-December) are in Figure 7, the

December values for the relative price of oil are in Figure 8, and world

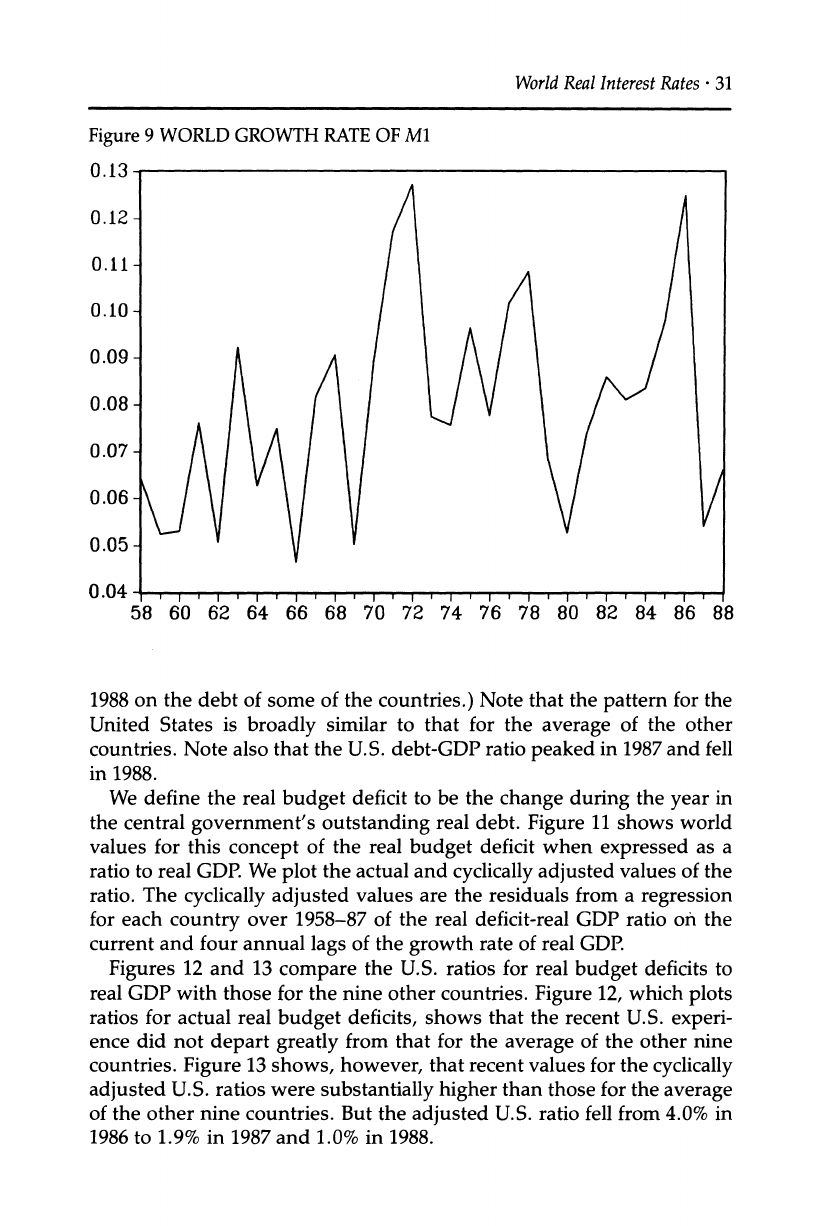

growth rates of M1 (December-to-December) are in Figure 9.

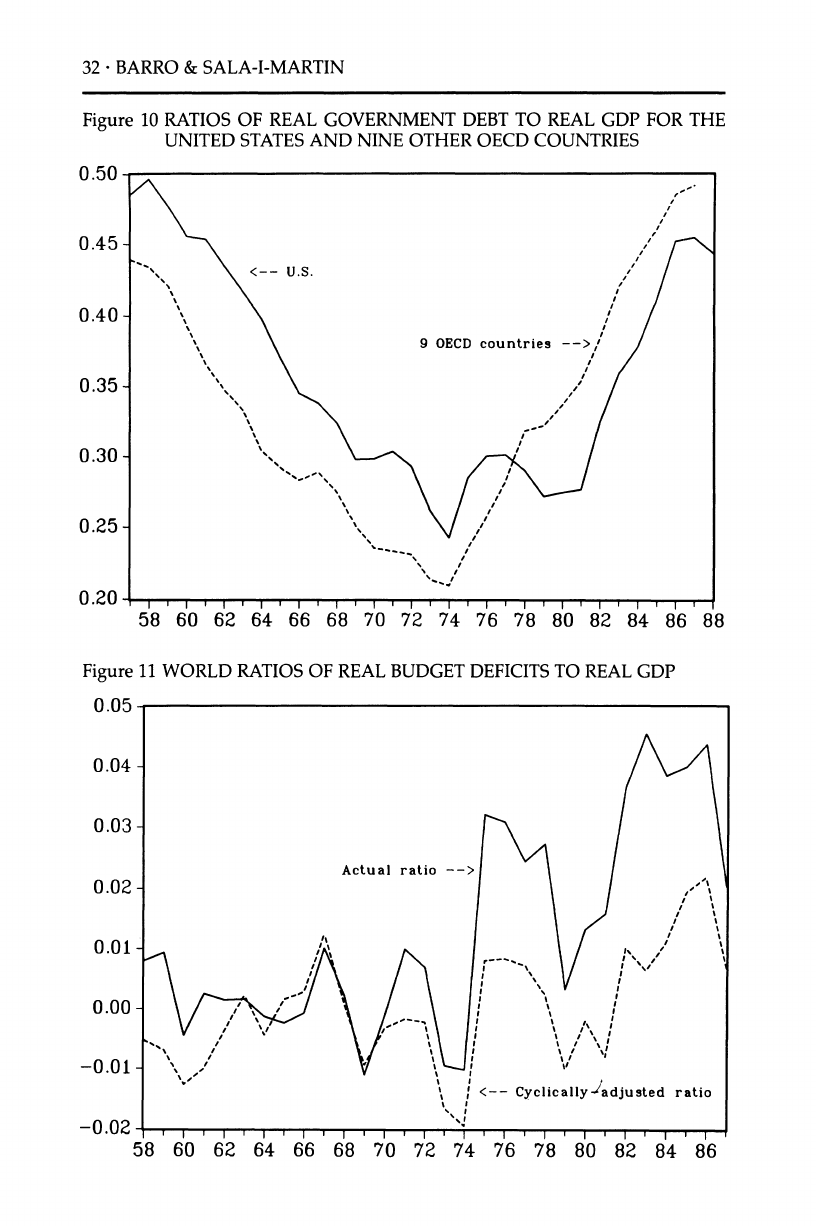

Figures 10-13 show various measures of fiscal stance. Figure 10 plots

the ratios of real central government debt to real GDP for the United

States and the nine other OECD countries.1 (We presently lack data for

11. We lack data on debt for consolidated general government on a consistent basis for the

ten countries in the sample. The figures that we used, which were computed in most

cases from IFS numbers on the par value of the aggregate of domestic and foreign debt

for central governments, are gross of holdings by central banks, certain government

agencies, and local governments.

30 ?

BARRO & SALA-I-MARTIN

Figure

7 WORLD

REAL STOCK

RETURNS

0.4

0.3 -

0.2-

0.1

0.0-

-0.1 -

-0.2-

-0.3-

-0.4 -

-0.5 ,,,, ,,,

1950 1955 1960 1965 1970 1975 1980 1985

Figure

8 RELATIVE PRICE OF CRUDE PETROLEUM

(U.S. PPI)

1.1

1.0-

0.9-

0.8-

0.7-

0.6-

0.5- /

0.4 -~~

0

.3-

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1950 1955 1960 1965 1970 1975 1980 1985

World Real

Interest Rates

*

31

Figure

9 WORLD GROWTH

RATE

OF

M1

1988 on the debt of some of the countries.) Note that the pattern for the

United States is broadly similar to that for the average of the other

countries. Note also that the U.S. debt-GDP ratio peaked in 1987 and fell

in 1988.

We define the real budget deficit to be the change during the year in

the central government's outstanding real debt. Figure 11 shows world

values for this concept of the real budget deficit when expressed as a

ratio to real GDP. We plot the actual and cyclically adjusted values of the

ratio. The cyclically adjusted values are the residuals from a regression

for each country over 1958-87 of the real deficit-real GDP ratio on the

current and four annual lags of the growth rate of real GDP.

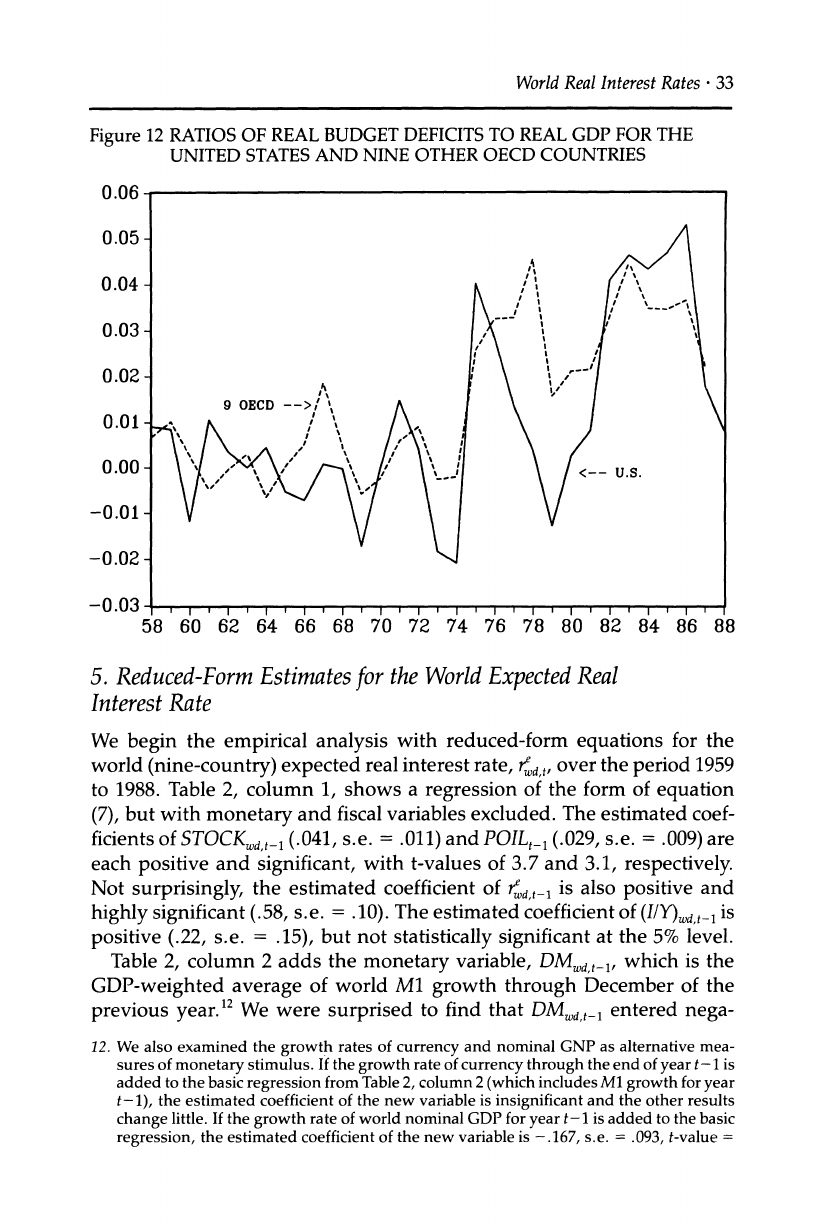

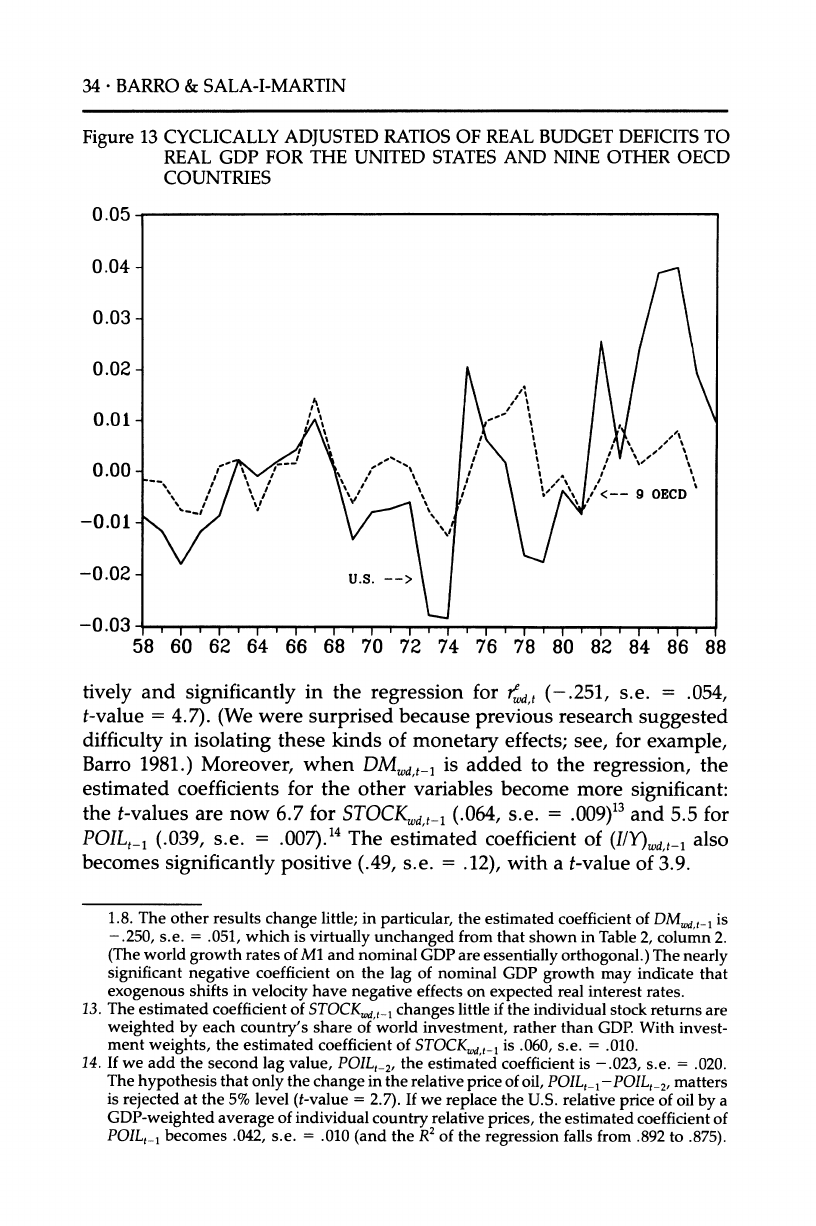

Figures 12 and 13 compare the U.S. ratios for real budget deficits to

real GDP with those for the nine other countries. Figure 12, which plots

ratios for actual real budget deficits, shows that the recent U.S. experi-

ence did not depart greatly from that for the average of the other nine

countries. Figure 13 shows, however, that recent values for the cyclically

adjusted U.S. ratios were substantially higher than those for the average

of the other nine countries. But the adjusted U.S. ratio fell from 4.0% in

1986 to 1.9% in 1987 and 1.0% in 1988.

32 *

BARRO & SALA-I-MARTIN

Figure 10 RATIOS OF REAL

GOVERNMENT

DEBT

TO REAL

GDP FOR

THE

UNITED STATES AND NINE OTHER OECD COUNTRIES

I

0.20 - I I

I, I , I

I,I

. I, ,, ,, ,

I, I I I

,

58 60 62 64 66 68 70 72 74 76 78 80 82 84 86 88

Figure

11 WORLD

RATIOS

OF REAL

BUDGET DEFICITS TO REAL GDP

0.05

World Real Interest Rates

. 33

Figure

12 RATIOS OF REAL BUDGET

DEFICITS

TO REAL

GDP

FOR

THE

UNITED

STATES

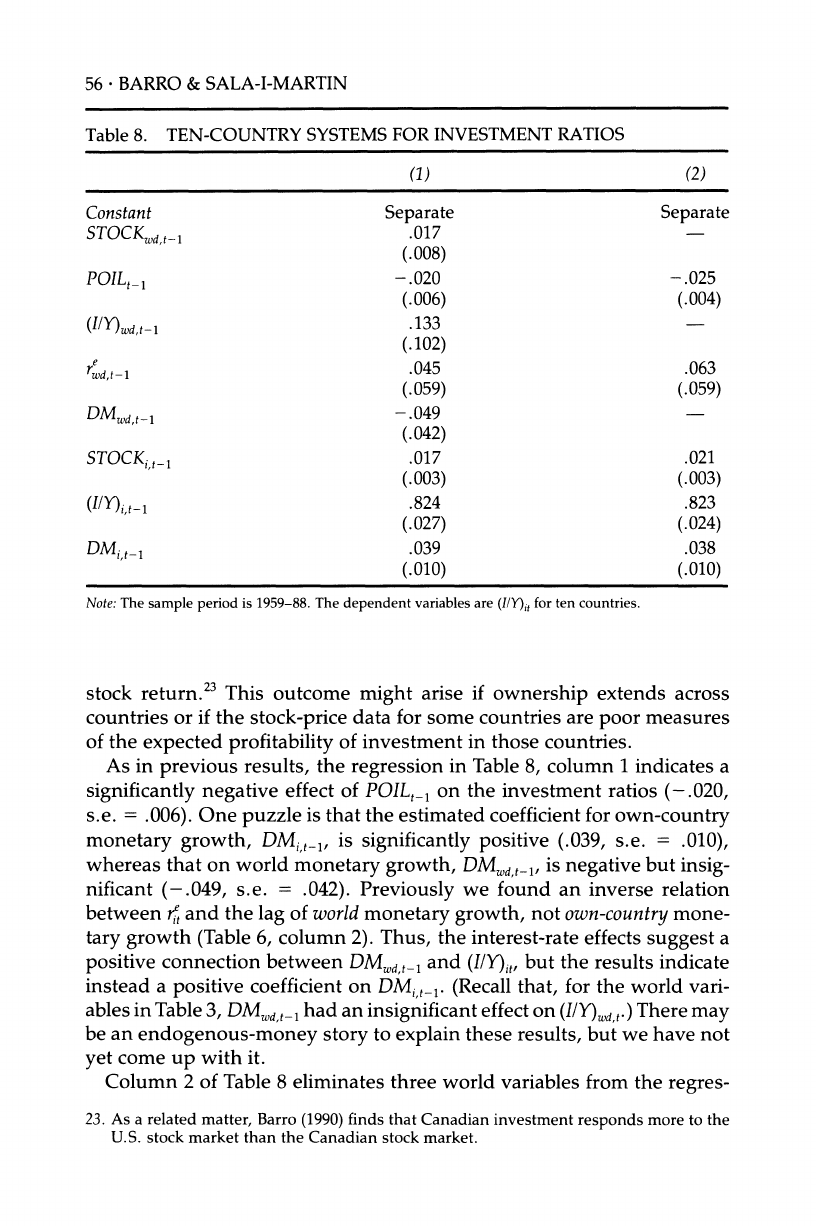

AND NINE OTHER OECD

COUNTRIES

58 60 62 64 66 68 70 72 74 76 78 80 82 84 86 88

5. Reduced-Form Estimates

for

the World

Expected

Real

Interest Rate

We begin the empirical analysis with reduced-form equations for the

world (nine-country) expected real interest rate, ,t, over the period 1959

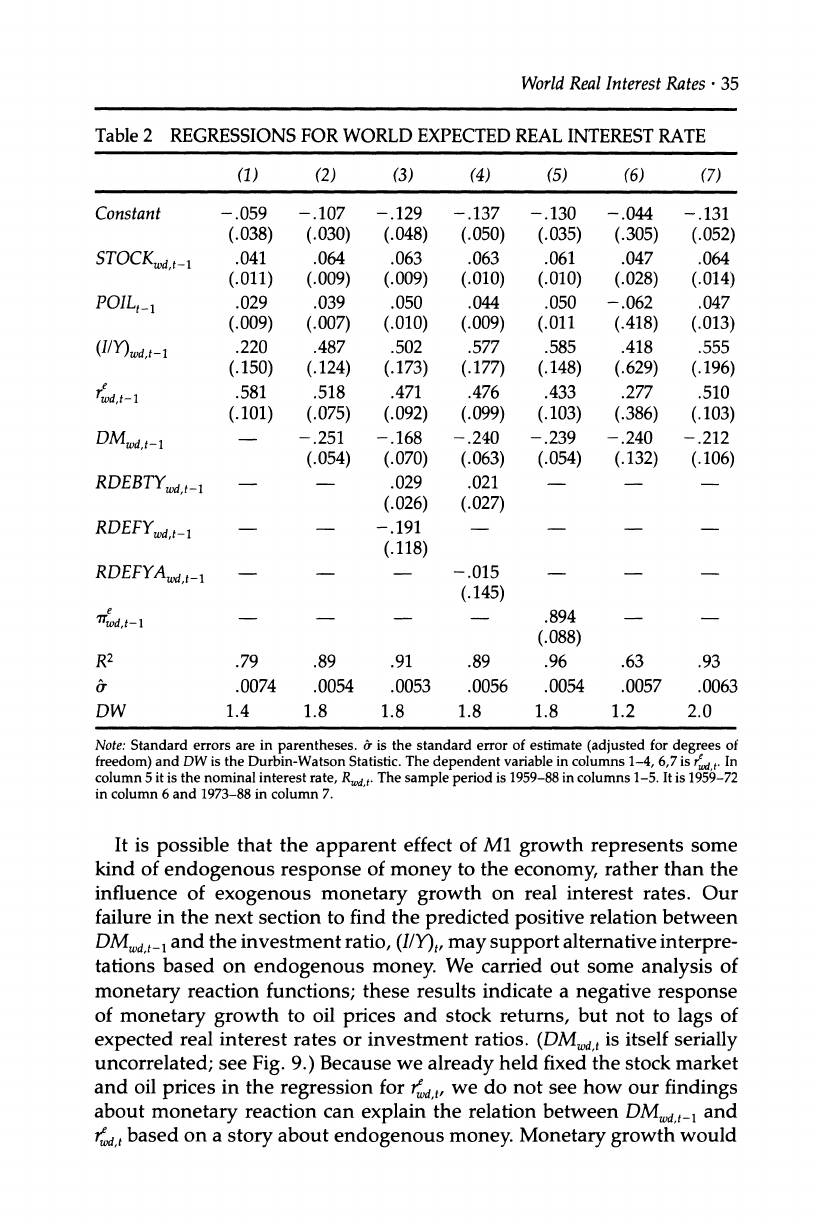

to 1988. Table 2, column 1, shows a regression of the form of equation

(7), but with monetary and fiscal variables excluded. The estimated coef-

ficients of STOCKd,

t_ (.041, s.e. = .011) and POILt_1

(.029, s.e. = .009) are

each positive and significant, with t-values of 3.7 and 3.1, respectively.

Not surprisingly, the estimated coefficient of td,t-1 is also positive and

highly significant (.58, s.e. = .10). The estimated coefficient of (I/Y)d t-_1

is

positive (.22, s.e. = .15), but not statistically significant at the 5% level.

Table 2, column 2 adds the monetary variable, DMd, t-, which is the

GDP-weighted average of world M1 growth through December of the

previous year.12

We were surprised to find that DMWdt 1 entered nega-

12. We also examined the growth rates of currency and nominal GNP as alternative mea-

sures of monetary stimulus. If the growth rate of currency through the end of year t- 1 is

added to the basic regression from Table 2, column 2 (which includes M1 growth for year

t-1), the estimated coefficient of the new variable is insignificant and the other results

change little. If the growth rate of world nominal GDP for year t- 1 is added to the basic

regression, the estimated coefficient of the new variable is -.167, s.e. = .093, t-value =

34 *

BARRO & SALA-I-MARTIN

Figure

13 CYCLICALLY

ADJUSTED

RATIOS OF REAL

BUDGET DEFICITS

TO

REAL

GDP FOR THE UNITED

STATES AND NINE OTHER

OECD

COUNTRIES

0.05

0.04 -

0.03 -

0.02 -

0.01- /

= /

\/ \V ?

/< 9 OECD

-

''

-0.03-, ,, ,, ,, , , ,, , ,

I , , , , ,

58 60 62 64 66 68 70 72 74 76 78 80 82 84 86 88

tively and significantly in the regression for r,t (-.251, s.e. = .054,

t-value = 4.7). (We were surprised because previous research suggested

difficulty in isolating these kinds of monetary effects; see, for example,

Barro 1981.) Moreover, when DMWd,t1

is added to the regression, the

estimated coefficients for the other variables become more significant:

the t-values are now 6.7 for STOCKwd,

t_ (.064, s.e. = .009)13

and 5.5 for

POILt-_

(.039, s.e. = .007).14

The estimated coefficient of (IlY)wdt-1 also

becomes significantly positive (.49, s.e. = .12), with a t-value of 3.9.

1.8. The other results change little; in particular, the estimated coefficient of DMw,d

t- is

-.250, s.e. = .051, which is virtually unchanged from that shown in Table 2, column 2.

(The world growth rates of Ml and nominal GDP are essentially orthogonal.) The nearly

significant negative coefficient on the lag of nominal GDP growth may indicate that

exogenous shifts in velocity have negative effects on expected real interest rates.

13. The estimated coefficient of STOCKw,

t-l changes little if the individual stock returns are

weighted by each country's share of world investment, rather than GDP. With invest-

ment weights, the estimated coefficient of STOCK

wd,t_1

is .060, s.e. = .010.

14. If we add the second lag value, POILt_2,

the estimated coefficient is -.023, s.e. = .020.

The hypothesis that only the change in the relative price of oil, POILt_l-POILt_2, matters

is rejected at the 5% level (t-value = 2.7). If we replace the U.S. relative price of oil by a

GDP-weighted average of individual country relative prices, the estimated coefficient of

POILt_L

becomes .042, s.e. = .010 (and the R2

of the regression falls from .892 to .875).

World

Real Interest Rates - 35

Table

2 REGRESSIONS

FOR

WORLD EXPECTED REAL

INTEREST RATE

(1) (2) (3) (4) (5) (6) (7)

Constant

(.

STOCKWd,t_1 (.

POIL,t_ (.

(I/Y)wd,t-l

r (-

M

.dt-1

--RDEBT,t-i

RDEBTYw,t-

RDEFYWd,t-1

RDEFYAWd,t-_

e

'7rwd,

t-

1_

.79

.0074

1.4

R2

DW

059 -.107 -.129

038) (.030) (.048)

041 .064 .063

011) (.009) (.009)

029 .039 .050

009) (.007) (.010)

220 .487 .502

150) (.124) (.173)

581 .518 .471

101) (.075) (.092)

- -.251 -.168

(.054) (.070)

- .029

(.026)

- - .191

(.118)

.89

.0054

1.8

.91

.0053

1.8

Note:

Standard

errors are in parentheses.

a is the standard error

of estimate

(adjusted

for degrees of

freedom)

and DW is the Durbin-Watson Statistic. The

dependent

variable

in columns

1-4, 6,7 is r4,t. In

column

5 it is the nominal

interest

rate,

Rwd,t.

The

sample period

is 1959-88

in columns

1-5. It is 1959-72

in column

6 and 1973-88

in column

7.

It is possible that the apparent effect of M1 growth represents some

kind of endogenous response of money to the economy, rather than the

influence of exogenous monetary growth on real interest rates. Our

failure in the next section to find the predicted positive relation between

DMwd,t- and the investment ratio, (I/Y)t,

may support alternative interpre-

tations based on endogenous money. We carried out some analysis of

monetary reaction functions; these results indicate a negative response

of monetary growth to oil prices and stock returns, but not to lags of

expected real interest rates or investment ratios. (DMwd t is itself serially

uncorrelated; see Fig. 9.) Because we already held fixed the stock market

and oil prices in the regression for 4rd,,

we do not see how our findings

about monetary reaction can explain the relation between DMwd,t- and

wd,t based on a story about endogenous money. Monetary growth would

-.137

(.050)

.063

(.010)

.044

(.009)

.577

(.177)

.476

(.099)

-.240

(.063)

.021

(.027)

-.130

(.035)

.061

(.010)

.050

(.011

.585

(.148)

.433

(.103)

-.239

(.054)

.894

(.088)

.96

.0054

1.8

-.044

(.305)

.047

(.028)

-.062

(.418)

.418

(.629)

.277

(.386)

-.240

(.132)

.63

.0057

1.2

-.131

(.052)

.064

(.014)

.047

(.013)

.555

(.196)

.510

(.103)

-.212

(.106)

.93

.0063

2.0

(.145)

.89

.0056

1.8

-n15.

36 *

BARRO & SALA-I-MARTIN

have to be reflecting information about future real interest rates not

already contained in the other explanatory variables.

The explanatory power of DMWdt_- for wd,t reflects in part the well-

known cutback in world M1 growth in 1979 and 1980 (6.8% and 5.3%,

respectively, compared with a mean of 8.0% for 1959-88). This monetary

contraction matches up well with the increase in r,d, from 0.9% in 1979 to

2.4% in 1980 and 4.7% in 1981. (With the monetary variable excluded in

Table 2, column 1, the fitted values of ed,t for 1980 and 1981 are 2.0% and

3.4%, respectively. With the monetary variable included in column 2,

these fitted values become 2.5% and 4.4%.) The significance of DM,d, t_

in the regression for red,

, however, does not depend on the inclusion of

the observations for 1980-81. If these two years are omitted, the esti-

mated coefficient of DMwd,t-1 becomes -.233, s.e. = .066, and the other

results do not change much from those shown in column 2.

We have carried out the estimation using the realized real interest rate,

rwd,, rather than our constructed measure of the expected rate, wd

t. The

error term in the regression can then be viewed as including the discrep-

ancy between the actual and expected real rate. Under rational expecta-

tions, this expectational error would be independent of the explanatory

variables, which are all lagged values. The estimates would therefore be

consistent, but inefficient relative to a situation where rd,t is observed

directly and used as the dependent variable. Although the standard

errors of the estimated coefficients are substantially higher when rw,

replaces 4d,t as the dependent variable, the basic pattern of the results

remains the same. Thus, the findings do not depend on our particular

measure for expected inflation.

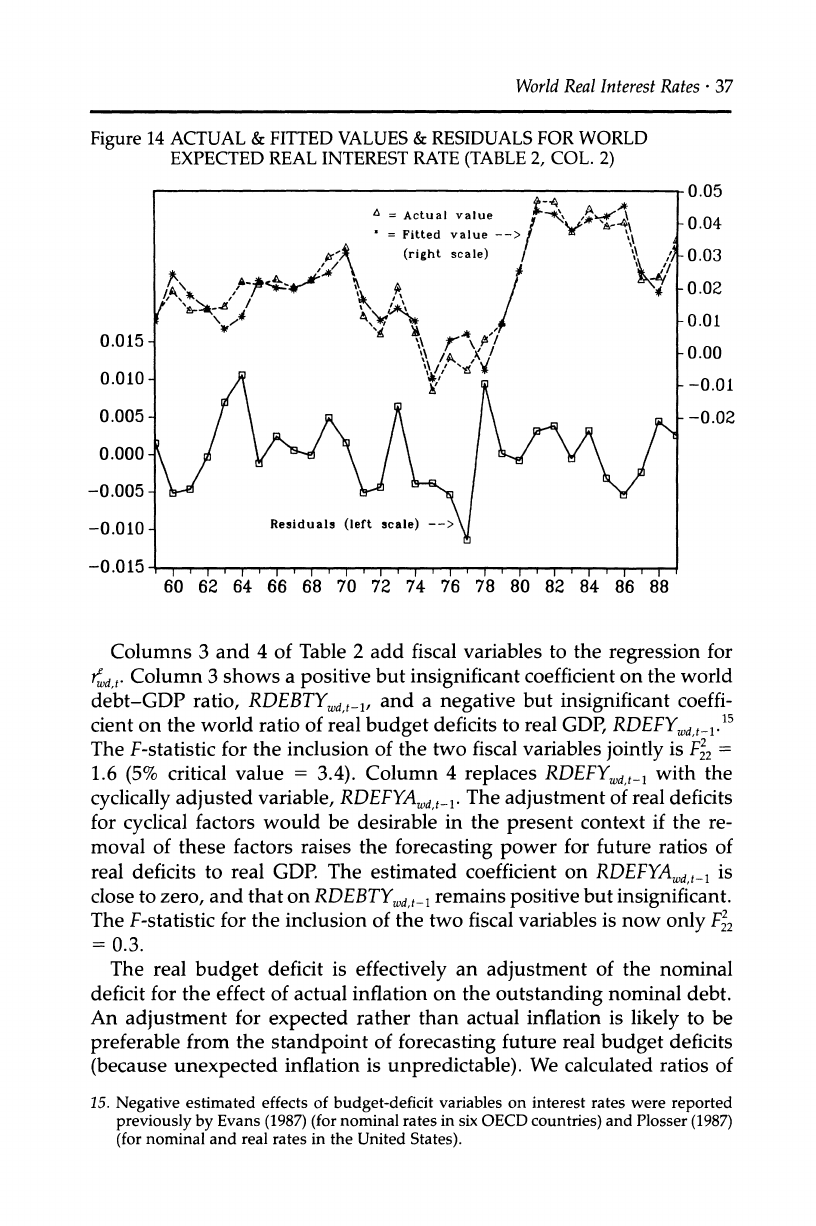

Overall, the regression equation in Table 2, column 2 does a remark-

able job of explaining the variations in expected real interest rates from

1959 to 1988; see Figure 14 for a plot of actual values against fitted values

and residuals. Note that the out-of-sample forecast of rd,t for 1989 is 3.2%

compared to an actual of 3.5%; for 1988, the estimated value was 1.9%

and the actual was 2.3%. (We promise that we generated the forecast for

1989 before finding the data on the actual value.)

We will discuss more features of the results later, but some key ele-

ments for the 1980s are the generally favorable stock-market returns

combined with high oil prices. (Blanchard and Summers 1984, argue that

improved prospects for profitability-which we pick up in the stock-

market returns-were an important element in the high real interest

rates of the 1980s.) The experience for the 1980s contrasts with the ex-

tremely poor stock returns and lower oil prices that prevailed in the mid-

1970s. The 1960s featured still lower oil prices, but better stock returns

than in the mid-1970s.

World

Real Interest

Rates *

37

Figure

14 ACTUAL & FITTED VALUES

& RESIDUALS FOR WORLD

EXPECTED REAL INTEREST

RATE

(TABLE

2, COL.

2)

0.05

= Actual value f -0.04

= Fitted value -> / '

\

(right scale) / ' 0.03

'8 /^

^/~' I A

^ o.o2

.t' - ',s. .

/** / -0.01

0.015- \

,'00 -0-00

/0.010 y,

--0

0.005 - / A /\ -0.02

0.000

-0.005 -

-0.010- Residuals (left scale) -->

-0 .015 , I, I,

I, , , , , , ,

60 62 64 66 68 70 72 74 76 78 80 82 84 86 88

Columns 3 and 4 of Table 2 add fiscal variables to the regression for

wd,t. Column 3 shows a positive but insignificant coefficient on the world

debt-GDP ratio, RDEBTYW,t-, and a negative but insignificant coeffi-

cient on the world ratio of real budget deficits to real GDP, RDEFYd, t-.15

The F-statistic for the inclusion of the two fiscal variables jointly is F2 =

1.6 (5% critical value = 3.4). Column 4 replaces RDEFYd,t 1 with the

cyclically adjusted variable, RDEFYAd, t-. The adjustment of real deficits

for cyclical factors would be desirable in the present context if the re-

moval of these factors raises the forecasting power for future ratios of

real deficits to real GDP. The estimated coefficient on RDEFYAWdt

_ is

close to zero, and that on RDEBTYWd

_1 remains positive but insignificant.

The F-statistic for the inclusion of the two fiscal variables is now only F2

=0.3.

The real budget deficit is effectively an adjustment of the nominal

deficit for the effect of actual inflation on the outstanding nominal debt.

An adjustment for expected rather than actual inflation is likely to be

preferable from the standpoint of forecasting future real budget deficits

(because unexpected inflation is unpredictable). We calculated ratios of

15. Negative estimated effects of budget-deficit

variables

on interest rates were reported

previously by Evans

(1987) (for

nominal rates

in six OECD

countries)

and Plosser

(1987)

(for

nominal and real rates

in the United

States).

38 *

BARRO

& SALA-I-MARTIN

real budget deficits to real GDP (adjusted or unadjusted for cyclical

fluctuations) in this manner, but the results differed negligibly from

those found with actual inflation.

We also held fixed the ratio of government consumption purchases to

GDP (which entered insignificantly) and experimented with the inclu-

sion of current or future real budget deficits. In all cases we obtained

similar results; the measures of fiscal stance that we have considered do

not help significantly in explaining the time series for expected real

interest rates. We are forced to conclude that the evidence supports the

Ricardian view, which deemphasizes the roles of public debt and budget

deficits in the determination of real interest rates.

Column 5 in Table 2 uses the world nominal interest rate, R, t, as the

dependent variable and adds the constructed measure of world expected

inflation, Td,

, on the right side. Measurement error

in 7ed,t would bias the

estimated coefficient toward zero, but the estimated value (.89, s.e. =

.09) differs insignificantly from one. Of course, to the extent that coun-

tries levy taxes on nominal interest payments, the predicted coefficient

would be somewhat above unity.

We tested for the stability of the relation between 4d,t and the explana-

tory variables by estimating the specification from Table 2, column 2

separately for 1959-72 and 1973-88. Thus, we split the sample before the

oil crises and the main changes in the international monetary system.

The estimates for the two subperiods appear in columns 6 and 7 of the

table. The test for stability leads to the statistic F18 = 0.2; thus, we do not

reject the hypothesis that the same equation applies over both periods.

To some extent, the failure to reject reflects the high standard errors that

apply to the estimated coefficients for 1959-72 (column 6). For example,

the standard error for the estimated coefficient of POILt_ is enormous

because of the small variations in relative oil prices from 1958 to 1971 (see

Fig. 8).16

The data for 1959-72, however, do generate marginally signifi-

cant estimated coefficients on STOCKd,

t_ (.047, s.e. = .028) and DMWdt,,-

(-.240, s.e. = .132).

6. Reduced-Form Estimates

for

World Investment Ratio

We now consider the reduced form for the investment ratio in equation

(8). Table 3 shows regressions over 1959-88 for the world ratio of real

16. The estimated coefficient of POILt_, differs insignificantly from zero for samples that

begin in 1959 and end as recently as 1979; for the 1959-79 sample, the estimated

coefficient is -.003, s.e. = .034. If the sample ends in 1980, the estimated coefficient

becomes .029, s.e. = .018. For samples that end between 1981 and 1988, the estimated

coefficient is very stable, varying between .038 and .040 with a standard error between

.007 and .010.

World Real Interest Rates *

39

Table

3. REGRESSIONS FOR WORLD

INVESTMENT

RATIO

(1) (2) (3) (4) (5) (6)

Constant .053 .057 .066 .076 -.016 .133

(.031) (.033) (.051) (.051) (.125) (.059)

STOCKwd,t-1 .036 .034 .034 .031 .018 .045

(.009) (.011) (.010) (.010) (.011) (.016)

POILt_1 -.016 -.017 -.030 -.020 .077 -.033

(.008) (.008) (.010) (.009) (.172) (.015)

(I/Y)wd,t- .814 .791 .848 .770 .92 .57

(.122) (.139) (.183) (.181) (.26) (.23)

wd,t- -.005 .000 .037 -.011 .043 -.057

(.082) (.085) (.097) (.101) (.158) (.118)

DMwd,t- .022 -.104 -.049 .064 -.127

(.060) (.075) (.064) (.054) (.122)

RDEBTYw,t-1 - -.029 -.021

(.027) (.027)

RDEFYwd,tl .306

(.125)

RDEFYAWd,t_1 .331

(.148)

R2 .82 .82 .86 .86 .97 .82

& .0060 .0061 .0056 .0057 .0023 .0073

DW 1.6 1.7 1.9 1.8 1.5 1.7

Note:

The

dependent

variable is (I/Y)wd,.

The sample period

in columns

1-4 is 1959-88. It is 1959-72 in

column 5 and 1973-88

in column 6.

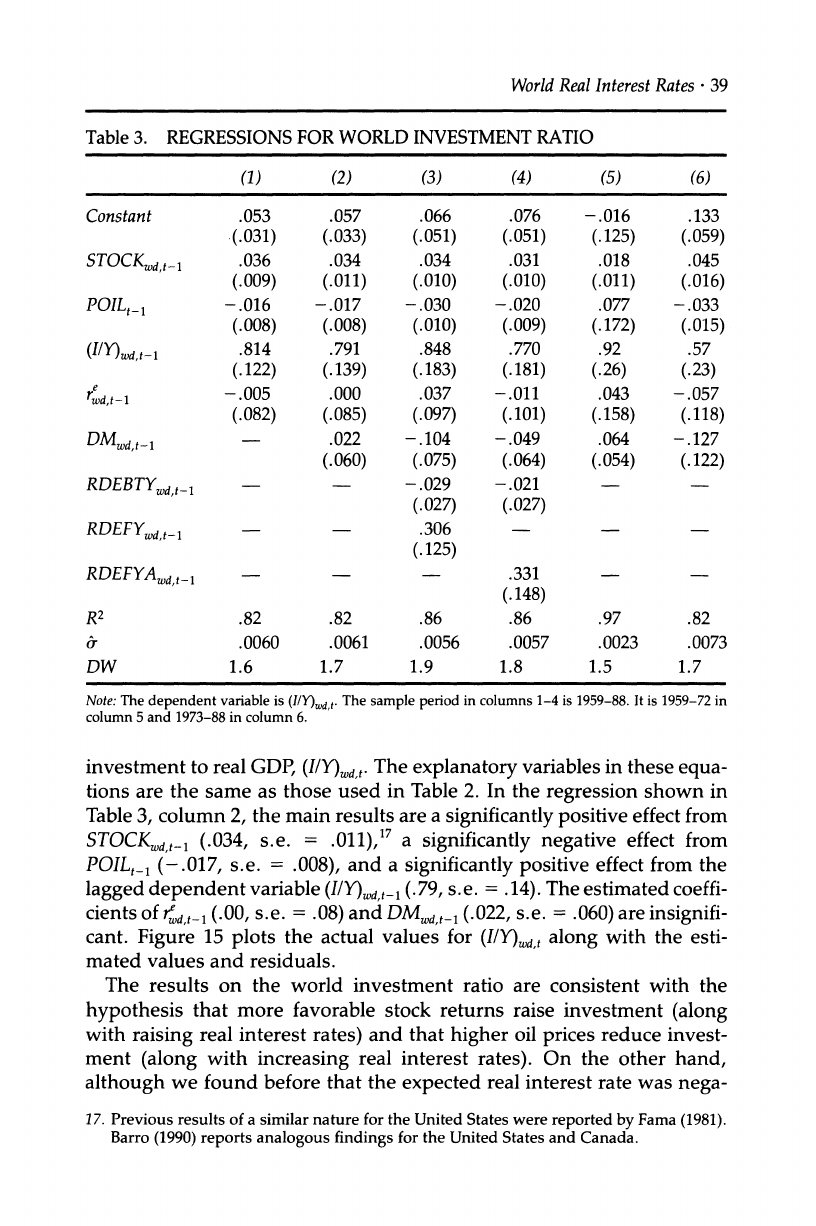

investment to real GDP, (I/Y)d,t. The explanatory variables in these equa-

tions are the same as those used in Table 2. In the regression shown in

Table 3, column 2, the main results are a significantly positive effect from

STOCKWdt,_

(.034, s.e. = .011),17 a significantly negative effect from

POILt_1

(-.017, s.e. = .008), and a significantly positive effect from the

lagged dependent variable (I/Y)wd,

t- (.79, s.e. = .14). The estimated coeffi-

cients of rd,t-1 (.00, s.e. = .08) and DMWd,t- (.022, s.e. = .060) are insignifi-

cant. Figure 15 plots the actual values for (I/Y)Wdt

along with the esti-

mated values and residuals.

The results on the world investment ratio are consistent with the

hypothesis that more favorable stock returns raise investment (along

with raising real interest rates) and that higher oil prices reduce invest-

ment (along with increasing real interest rates). On the other hand,

although we found before that the expected real interest rate was nega-

17. Previous results of a similar nature for the United States were reported by Fama (1981).

Barro (1990) reports analogous findings for the United States and Canada.

40 *

BARRO

& SALA-I-MARTIN

Figure

15 ACTUAL & FITTED

VALUES & RESIDUALS

FOR WORLD RATIO

OF INVESTMENT TO GDP (TABLE

3, COL.

2)

0.27

A$~ -~ ~

~-0.26

X\ - / t-0.25

- Actual value -0.23

0.02 X,* * =- Fitted value --> -.' \23 - 0.2

esidual

(lefright

scale) -->0.22

0.01- -0.20

-0.02 ,

60 62 64 66 68 7

772 74 76 78 80 82 84 86 88

tively related to last year's monetary growth, the results do not reveal

the expected positive response of the investment ratio.

Columns 3 and 4 of Table 3 add the fiscal variables that we considered

before; column 3 uses the world variable for ratios of real budget deficits

to real GDP, and column 4 the variable for cyclically adjusted ratios. The

estimated effect of the debt-GDP ratio, RDEBTYwd,t , is negative but

insignificant in both cases. The estimated effects of the budget-deficit

variables, RDEFYd,t-1 and RDEFYAwd,t_, are each significantly positive-

that is, the sign opposite to that predicted by models where fiscal expan-

sion lowers the desired national saving rate. The positive effect for the

unadjusted variable, RDEFYd,,_,, accords with the negative coefficient

for this variable in the interest-rate equation (Table 2, column 3). How-

ever, the cyclically adjusted variable, RDEFYAwd,

-, had a coefficient of

about zero in the interest-rate equation (Table 2, column 4). The fiscal

variables considered are jointly insignificant for the investment ratio at

the 5% level. In the regression shown in Table 3, column 3, the statistic is

F2 = 3.2 (5%

critical value = 3.4); for that in column 4, the statistic is F2 =

2.6. Thus, as with the expected real interest rate, the fiscal variables do

not have much explanatory power for the investment ratio.

We fit the equation for the investment ratio (Table 3, column 2) sepa-

World Real Interest

Rates ?

41

rately over 1959-72 and 1973-88. A test of stability for the coefficients

yields the statistic F% = 1.7 (5% critical value = 2.7). Columns 5 and 6

show the estimates obtained over the two subperiods. The standard

errors for the estimated coefficients from the 1959-72 sample tend to be

high; however, the estimated coefficient of STOCKd, t-_ is positive (.018,

s.e. = .011).

7. System

Estimates

for World

Expected

Real Interest Rate

and

Investment

Ratio

The structural model in equations (3) and (6) led to the reduced-form

equations (7) and (8) for the expected real interest rate and investment

ratio. In the previous sections, we estimated the two reduced-form equa-

tions separately, ignoring the overidentifying restrictions that came from

the structure. In this section, we estimate the two equations as a joint

system, allowing for the imposition of the model's restrictions as well as

for correlation of the error terms across the equations. Table 4 shows the

resulting estimates for the structural coefficients that appear in equation

(3) for investment demand and in equation (6) for desired saving. Col-

umns 1 and 2 apply to a system that includes monetary growth but

excludes fiscal variables. Columns 3 and 4 add two fiscal variables: the

debt-GDP ratio, RDEBTYd, t_, and the cyclically adjusted real deficit-real

GDP ratio, RDEFYAwd,t-.

We also fit the joint systems for the expected real interest rate and the

investment ratio without the restrictions imposed by the structural

model. Thereby we were able to compute likelihood-ratio tests of the

overidentifying restrictions. For the model without fiscal variables, the

test statistic (for -2 ? log[likelihood ratio]) of 9.9 compared to a 5%

critical value from the X2

distribution with 5 degrees of freedom of 11.1.

In the model with fiscal variables, the test statistic of 13.7 compared to

the 5% critical value (with 7 d.f.) of 14.1. Thus, the model's restrictions

were not rejected at the 5% level in either case. Table 4 also compares the

fits (in terms of R2

and -a

values) for restricted and unrestricted forms of

each equation separately. The fits for the investment equation appear

substantially more sensitive than those for the interest-rate equation to

the imposition of the model's overidentifying restrictions.

The two fiscal variables are jointly insignificant when added to the

restricted joint system (likelihood-ratio statistic of 5.3 compared to a 5%

critical value of 6.0). Since the other results are not sensitive to the

exclusion of the fiscal variables, we focus now on the estimates from the

model that excludes the fiscal variables (columns 1 and 2 of Table 4).

If one takes the structural model seriously, then two interesting results

42 *

BARRO & SALA-I-MARTIN

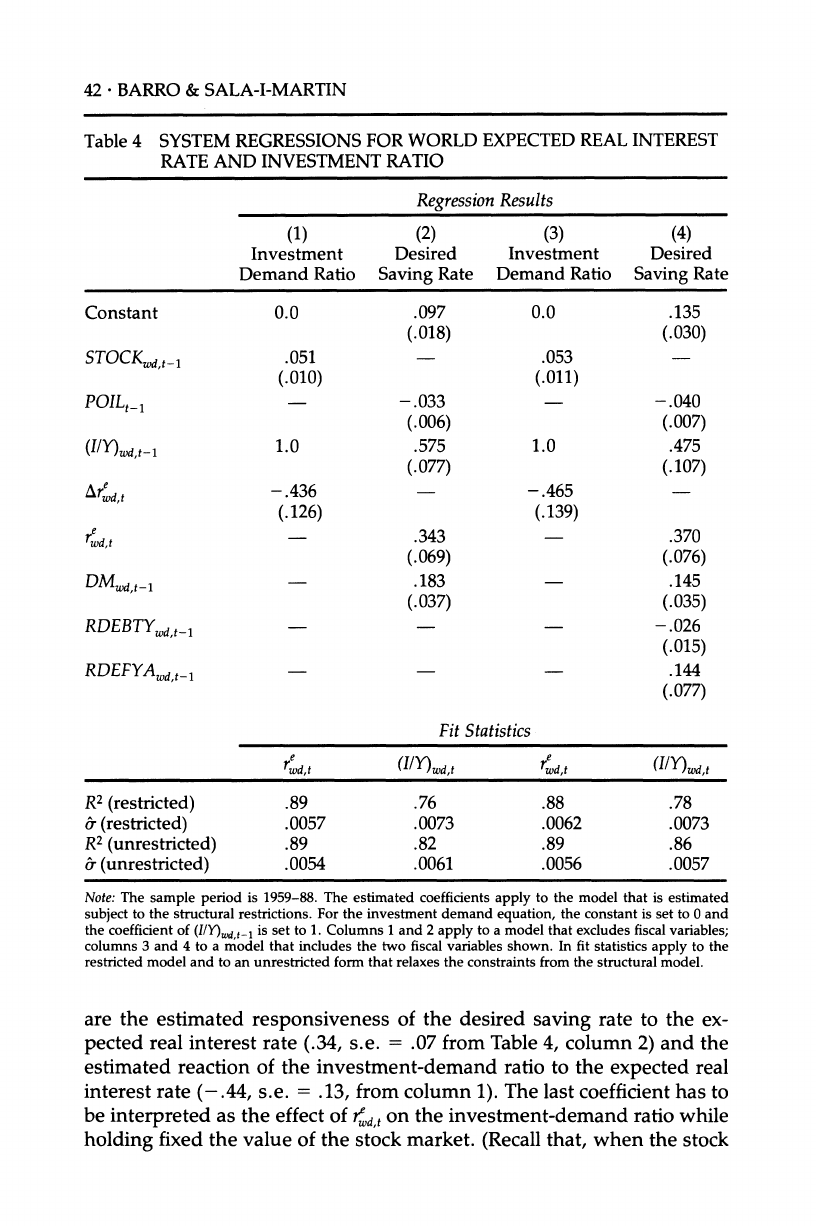

Table 4 SYSTEM REGRESSIONS FOR WORLD EXPECTED REAL INTEREST

RATE AND INVESTMENT RATIO

Regression

Results

(1) (2) (3) (4)

Investment Desired Investment Desired

Demand Ratio Saving Rate Demand Ratio Saving Rate

Constant 0.0 .097 0.0 .135

(.018) (.030)

STOCK,d

t_1 .051 .053

(.010) (.011)

POILt1 - -.033 -.040

(.006) (.007)

(I/Y)w,t-1 1.0 .575 1.0 .475

(.077) (.107)

Arwd,t -.436 -.465

(.126) (.139)

rwd,t - 343 -.370

(.069) (.076)

DMWd,t-1 .183 .145

(.037) (.035)

RDEBTYWd,t_1 -.026

(.015)

RDEFYAwd,t_1 .144

(.077)

Fit Statistics

rew,t

(I/Y)wd,t rwd,t (I/Y)wd,

R2

(restricted) .89 .76 .88 .78

a (restricted) .0057 .0073 .0062 .0073

R2

(unrestricted) .89 .82 .89 .86

r (unrestricted) .0054 .0061 .0056 .0057

Note: The sample period is 1959-88. The estimated coefficients

apply to the model that is estimated

subject

to the structural restrictions.

For the investment demand

equation,

the constant is set to 0 and

the coefficient

of (I/Y)wd,-_1

is set to 1. Columns

1 and 2 apply

to a model that

excludes fiscal

variables;

columns 3 and 4 to a model that includes the two fiscal variables shown. In fit statistics

apply to the

restricted model and to an unrestricted form

that

relaxes

the constraints from

the structural model.

are the estimated responsiveness of the desired saving rate to the ex-

pected real interest rate (.34, s.e. = .07 from Table 4, column 2) and the

estimated reaction of the investment-demand ratio to the expected real

interest rate (-.44, s.e. = .13, from column 1). The last coefficient has to

be interpreted as the effect of 4d,t on the investment-demand ratio while

holding fixed the value of the stock market. (Recall that, when the stock

World Real Interest Rates

*

43

return is an imperfect measure of Aq,,

the variable <-rt-1 provides some

independent information about Aqt.)

The dependence of the stock return

on d,t- wd,t- suggests that the estimated coefficient -.44 would underes-

timate the magnitude of the response of the investment-demand ratio to

id,t while holding fixed expected profitability, PROFg,

and the risk pre-

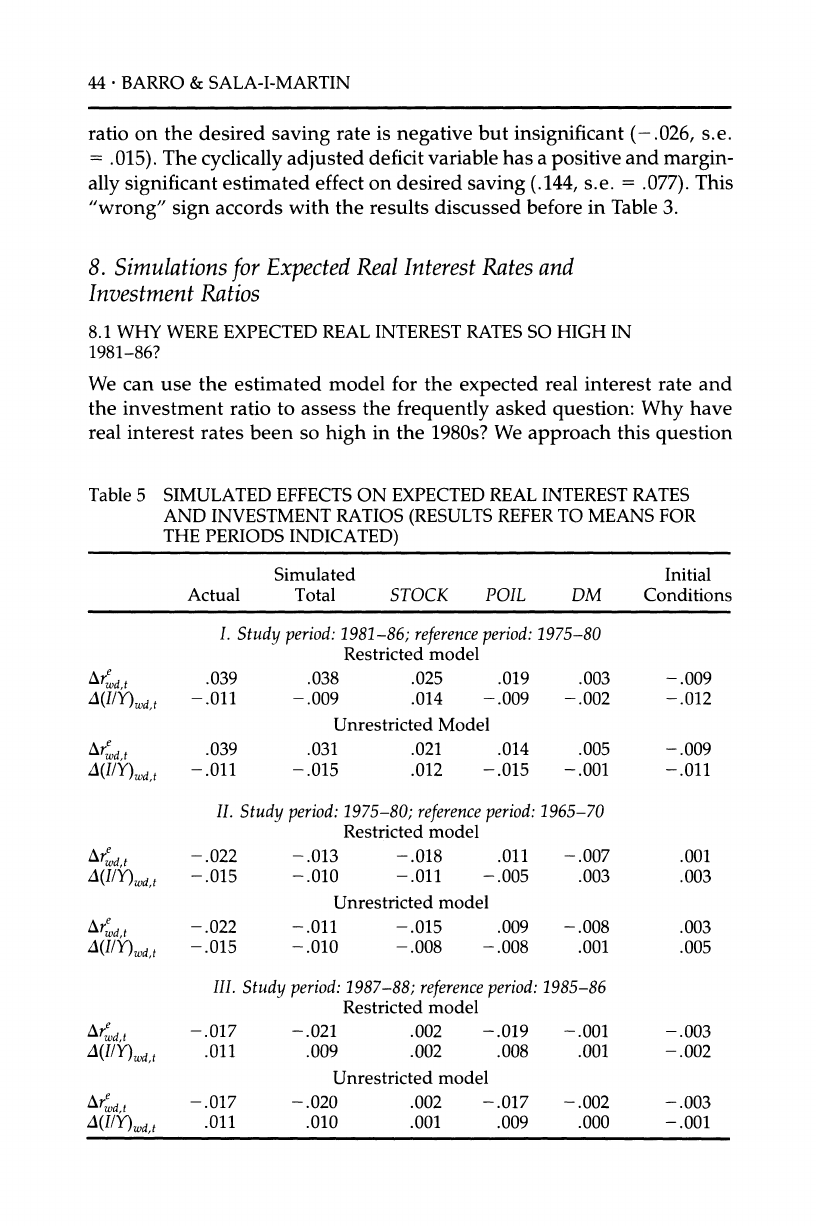

mium, Pt, but not the value of the stock market.18

The estimated model implies that desired national (gross) saving rates

rise by .34 percentage points for each percentage-point increase in ?r.

Although this form provides a natural unit for thinking of the responsive-

ness of saving rates to real interest rates, it appears to be more common

to think in terms of elasticities. Because the sample mean of (I/Y)wd,t

is .23,

whereas that for wd,t

is only .020, the implied elasticities are small-only

.03 at the sample means. The calculated elasticities would, however,

tend to be substantially greater for net saving rates.

Column 1 of Table 4 shows that the estimated effect of STOCKWd,

_ on

the investment-demand ratio is .051, s.e. = .010. Since the sample stan-

dard deviation of STOCKWd,

t is .16, the result means that a 1 s.d. move in

the stock market changes the investment-demand ratio by .008 com-

pared to a sample s.d. for (I/Y)wdt

of .013. The estimated effect of POILt,_

on the desired saving rate in col. 2 is -.033, s.e. = .006. Given the

sample s.d. for POIL_ 1 of .21, a 1 s.d. move in the relative oil price

implies a shift in the desired saving rate by .007.

Columns 1 and 2 show that the estimated effects of the lagged depen-

dent variable, (I/Y)wd,t_, are 1 for the investment-demand ratio (as con-

strained by the model) and .58, s.e. = .08, for the desired saving rate.

The greater persistence of investment demand than of desired saving

generates the positive relation in the reduced form between 4,dt and

(I/Y)wd,t-. If the coefficient on (I/Y)d, t_ in the investment-demand equa-

tion is freed up, the estimated value is .93, s.e. = .11. In this case, the

estimated coefficient of (IIY)d, t in the saving-rate equation becomes .55,

s.e. = .09. Thus, this unrestricted version of the model does indicate

significantly greater persistence in investment demand than in desired

saving.

Column 2 shows the positive estimated effect for DMWd,t- on the de-

sired saving rate (.183, s.e. = .037). The previous discussion of the

reduced form indicated that this estimate stems from the negative rela-

tion between d,t

and DMd, tl, and not from any relation between (I/Y)wdt

and DMw, _.

Column 4 of Table 4 shows that the estimated effect of the debt-GDP

18. Serial correlation of the error term in the equation for r4,, would, however, likely lead

to an overestimate of the sensitivity of investment demand to a change in the expected

real interest rate; see the coefficient a2

in equations (3) and (7).

44 *

BARRO & SALA-I-MARTIN

ratio on the desired saving rate is negative but insignificant (-.026, s.e.

= .015). The cyclically adjusted deficit variable has a positive and margin-

ally significant estimated effect on desired saving (.144, s.e. = .077). This

"wrong" sign accords with the results discussed before in Table 3.

8. Simulations

for Expected

Real

Interest

Rates and

Investment Ratios

8.1 WHY WERE

EXPECTED

REAL INTEREST

RATES

SO HIGH IN

1981-86?

We can use the estimated model for the expected real interest rate and

the investment ratio to assess the frequently asked question: Why have

real interest rates been so high in the 1980s? We approach this question

Table 5 SIMULATED

EFFECTS ON EXPECTED

REAL

INTEREST RATES

AND INVESTMENT RATIOS

(RESULTS

REFER

TO

MEANS

FOR

THE PERIODS INDICATED)

Simulated Initial

Actual Total STOCK POIL DM Conditions

I. Study period:

1981-86; reference period:

1975-80

Restricted model

Arwd,t .039 .038 .025 .019 .003 -.009

A(I/Y)d,t -.011 -.009 .014 -.009 -.002 -.012

Unrestricted Model

Arwd,t .039 .031 .021 .014 .005 -.009

A(IY)wdt -.011 -.015 .012 -.015 -.001 -.011

II. Study period:

1975-80; reference

period:

1965-70

Restricted model

Ard, t -.022 -.013 -.018 .011 -.007 .001

A(I/Y)wd,t -.015 -.010 -.011 -.005 .003 .003

Unrestricted model

Ared

t -.022 -.011 -.015 .009 -.008 .003

A(I/Y)wd,t -.015 -.010 -.008 -.008 .001 .005

III. Study period:

1987-88; reference period:

1985-86

Restricted model

Arwd,t -.017 -.021 .002 -.019 -.001 -.003

A(I/Y)wdt .011 .009 .002 .008 .001 -.002

Unrestricted model

Are d,t -.017 -.020 .002 -.017 -.002 -.003

A(I/Y)d,t .011 .010 .001 .009 .000 -.001

World

Real

Interest Rates *

45

Table

5 SIMULATED EFFECTS ON EXPECTED

REAL

INTEREST

RATES

AND INVESTMENT RATIOS

(RESULTS

REFER TO MEANS

FOR

THE PERIODS

INDICATED)

(CONTINUED)

Simulated Initial

Actual Total STOCK POIL DM Conditions

IV. Study period:

1989; reference

period:

1988

Restricted model

Ard,t .011 .014 .015 -.005 -.003 .007

A(IlY)wd,t .017 .005 .002 .001 .009

Unrestricted model

Arwd,t .011 .013 .015 -.004 -.003 .006

A(I/Y)W - .019 .008 .002 .000 .009

Means of Variables Initial Conditions

Period rwd,t (IlY)d,t STOCKWd,t-l POILt-1 DMwd,t- rwd,t- (Y)wd,t-1

1989 .0347 (.247) .1484 .406 .0661 .0233 .242

1988 .0233 .242 -.0817 .519 .0541 .0225 .230

1987-88 .0229 .236 .0847 .470 .0895 .0401 .225

1985-86 .0395 .225 .1370 .839 .0906 .0443 .226

1981-86 .0424 .219 .0769 .927 .0791 .0245 .226

1975-80 .0031 .230 -.0624 .601 .0880 .0061 .249

1965-70 .0247 .245 .0092 .407 .0677 .0219 .238

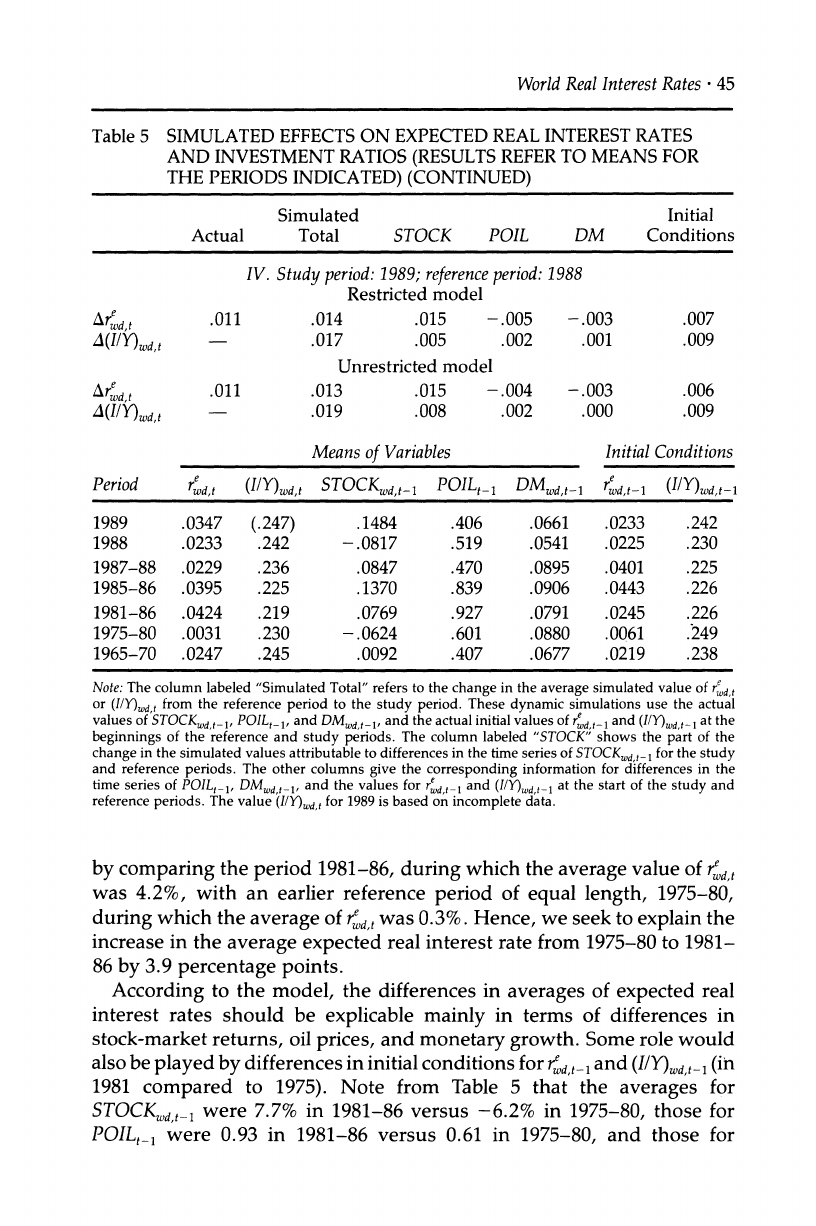

Note: The column labeled "Simulated Total" refers to the change in the average simulated value of rd, t

or (IIY)Wd,t

from the reference period to the study period. These dynamic simulations use the actual

values of STOCKwd

t 1, POILt_1,

and DMWd,t_l,

and the actual initial values of re, t-_ and (I/Y)wd

t- at the

beginnings of the reference and study periods. The column labeled "STOCK" shows the part of the

change in the simulated values attributable to differences in the time series of STOCKWd,

t_ for the study

and reference periods. The other columns give the corresponding information for differences in the

time series of POIL_1, DMWd,t-_1 and the values for rwdt-l and (I/Y)wd,t-l at the start of the study and

reference periods. The value (I/Y)d,t for 1989 is based on incomplete data.

by comparing the period 1981-86, during which the average value of rd,t

was 4.2%, with an earlier reference period of equal length, 1975-80,

during which the average of wd,t

was 0.3%. Hence, we seek to explain the

increase in the average expected real interest rate from 1975-80 to 1981-

86 by 3.9 percentage points.

According to the model, the differences in averages of expected real

interest rates should be explicable mainly in terms of differences in

stock-market returns, oil prices, and monetary growth. Some role would

also be played by differences in initial conditions for rd,t- and (I/Y)wd,t-l

(in

1981 compared to 1975). Note from Table 5 that the averages for

STOCKWdt

- were 7.7% in 1981-86 versus -6.2% in 1975-80, those for

POILt_ were 0.93 in 1981-86 versus 0.61 in 1975-80, and those for

46 *

BARRO

& SALA-I-MARTIN

DMd,t-l were 7.91% in 1981-86 versus 8.80% in 1975-80. The difference

in initial conditions were .0245 for 4d,t-1 in 1981 versus .0061 in 1975, and

.226 for (I/Y)wd,t- in 1981 versus .249 in 1975.

We can simulate the estimated model to estimate the extent to which

the higher average for r1dt in 1981-86 than in 1975-80 can be attributed to

differences in STOCKwd, t_, POIL,_

, DMWdt-,,

and the initial conditions for

4d,t-l and (I/Y)wd,t_. We consider the restricted version of the joint model

as reported in Table 4 and also the unrestricted version that does not

impose the overidentifying restrictions from the structure. We also ne-

glect any interplay among STOCK,, t, POILt,

and DMd, ; that is, we treat

the time paths of these three variables as exogenous.19

Given the actual time paths for STOCKwd,B

POILt,

and DMWd,t,

and the

actual values for w

,t- and (IY)wd,t- in 1981 and 1975, dynamic simulations

of the restricted model for 1981-86 and 1975-80 predict an increase in

the average of wd,t

of 3.8 percentage points compared to the actual in-

crease of 3.9 points (see the columns labeled "Simulated Total" and

"Actual" in section I of Table 5). We then dynamically simulated the

restricted model for 1981-86 with the values of STOCKWd,

t- from 1975-80

substituted year by year for those in 1981-86. This simulation implied

that 2.5 percentage points of the increase in the average of rwdt from 1975-

80 to 1981-86 derived from the higher average for stock returns in the

latter period (see the column labeled "STOCK"

in the table).20

Similarly,

we found that 1.9 percentage points of the rise in the average of rwd,

resulted from the increase in average oil prices (the column "POIL"),

0.3

points from the lower average monetary growth (the column "DM"),

and -0.9 points from the differences in initial conditions. The main

change in the initial conditions is the much lower value for (IIY)w

,_1 in

1981 than in 1975; this effect by itself would have lowered real interest

rates for 1981-86. The results from simulations of the unrestricted

model, shown in Table 5, are basically similar.

Table 5 also indicates the simulated results for investment ratios. The

restricted model predicts that the average of (IIY)w,t

for 1981-86 would be

19. We do find a significant negative relation between stock returns for year t and the

change in oil prices during year t. Also, M1 growth has significant negative reactions to

the contemporaneous change in oil prices and to lagged stock returns. We can filter the

stock returns to compute the component exogenous to oil-price changes, and we can

filter M1 growth to calculate the part exogenous to oil-price changes and lagged stock

returns. In the discussion below we attribute changes in expected real interest rates

and investment ratios to the behavior of stock returns, oil prices, and monetary

growth. The breakdown among these three variables would change if we shifted from

gross numbers to the filtered values.

20. The results depend not only on differences in the average value of STOCK., _,, but on

differences in the time pattern. It is possible for the simulated effects to go in the

direction opposite to that suggested just from a comparison of means.

World Real Interest Rates *

47

0.9 percentage points below the average for 1975-80, compared to the

actual shortfall of 1.1 points. The simulations attribute 0.9 percentage

points of the decline in the average investment ratio to higher oil prices,

-1.4 points to the more favorable stock returns (which, by themselves,

would have raised the investment ratio), 0.2 points to lower monetary

growth, and 1.2 points to differences in initial conditions. The main

element in the initial conditions is again the lower value for (I/Y)d,,t- in

1981 than in 1975. The results from the unrestricted model are again

similar.

8.2 WHY

WERE EXPECTED REAL

INTEREST RATES SO LOW

IN

1975-80?

We now compare the low average for rWd,t

in 1975-80, 0.3%, with the

higher value, 2.5%, that prevailed during an earlier reference period of

the same length, 1965-70. (The results are similar if we pick alternative

six-year reference periods in the 1960s or early 1970s.) Section II of Table

5 shows that simulations of the restricted model predict a decline of only

1.3 percentage points in the average of 7d, from 1965-70 to 1975-80

compared with the actual decrease of 2.2 points. The model attributes

1.8 percentage points of the decline to lower stock returns, -1.1 points

to higher oil prices (which, by themselves, would have raised expected

real interest rates), 0.7 points to higher monetary growth, and -0.1

points to differences in initial conditions. The results from the unre-

stricted model are similar.

Overall, the largest factor behind the differences in expected real inter-

est rates among the three periods, 1965-70, 1975-80, and 1981-86, is the

variation in stock returns. The fall in real interest rates from 1965-70 to

1975-80 goes along with a worsening of stock returns (from 0.9% to

-6.2%), and the steep rise in rates in 1981-86 reflects sharply higher

stock returns (7.7%). The movements in oil prices are also important,

although higher oil prices in 1975-80 compared to 1965-70 partially

counteract the movement to lower real interest rates. The increase in oil

prices in 1981-86 compared to 1975-80 reinforces the stock market in

generating a shift toward higher real interest rates.

8.3 WHY DID EXPECTED REAL INTEREST RATES FALL IN 1987-88

AND RISE IN 1989?

The average of 4dt fell by 1.7 percentage points from 1985-86 to 1987-88

and then rose by 1.1 percentage points from 1988 to 1989. Sections III