Malaysia CR1353

User Manual: CR1353

Open the PDF directly: View PDF ![]() .

.

Page Count: 77

© 2013 International Monetary Fund February 2013

IMF Country Report No. 13/53

January 28, 2013 January 29, 2001 January 29, 2001

January 29, 2001 January 29, 2001

Malaysia: Report on the Observance of Standards and Codes

This Report on the Observance of Standards and Codes in Malaysia was prepared by staff of the

International Monetary Fund and the World Bank. It is based on the information available following

discussions that ended on September 7, 2012, with the officials of Malaysia. Based on the information

available at the time of these discussions, the report was completed in January 2013. The views

expressed in this document are those of the staff team and do not necessarily reflect the views of the

government of Malaysia or the Executive Board of the IMF.

The policy of publication of staff reports and other documents by the IMF allows for the deletion of

market-sensitive information.

Copies of this report are available to the public from

International Monetary Fund Publication Services

700 19th Street, N.W. Washington, D.C. 20431

Telephone: (202) 623-7430 Telefax: (202) 623-7201

E-mail: publications@imf.org Internet: http://www.imf.org

International Monetary Fund

Washington, D.C.

FINANCIAL SECTOR ASSESSMENT PROGRAM

MALAYSIA

REPORT ON THE OBSERVANCE

OF STANDARDS AND CODES

(ROSCS)

JANUARY 2013

INTERNATIONAL MONETARY FUND

MONETARY AND CAPITAL MARKETS DEPARTMENT

THE WORLD BANK

FINANCIAL AND PRIVATE SECTOR DEVELOPMENT

VICE PRESIDENCY

EAST ASIA AND PACIFIC REGION VICE PRESIDENCY

2

Contents Page

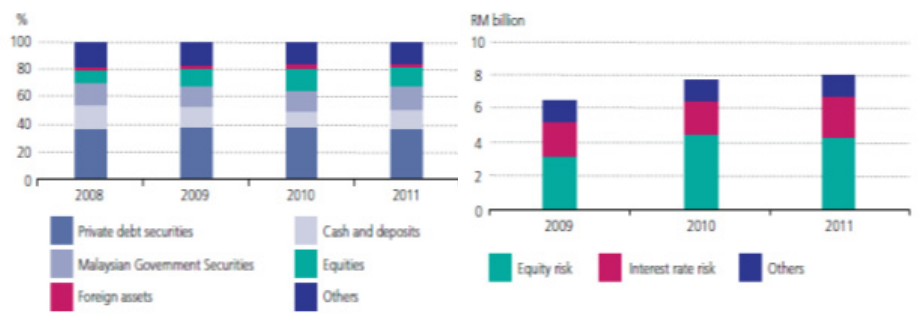

Glossary .....................................................................................................................................4

I. Basel Core Principles For Effective Banking Supervision .....................................................6

A. Summary ...................................................................................................................6

B. Institutional Setting and Market Structure Overview ...............................................7

C. Preconditions for Effective Banking Supervision .....................................................7

D. Main Findings .........................................................................................................10

E. Key Findings and Recommended Action Plan ........................................................20

F. Authorities’ Response to the Assessment ................................................................22

II. Assessment of Insurance Core Principles (ICPs) ................................................................24

A. Summary, Key Findings, and Recommendations ...................................................24

B. Introduction and Scope............................................................................................24

C. Overview: Institutional and Macro Prudential Setting ............................................25

D. Preconditions for Effective Insurance Supervision .................................................28

E. Key Findings and Recommendations ......................................................................29

F. Authorities’ Response to the Assessment ................................................................38

III. IOSCO Objectives and Principles of Securities Regulation ..............................................39

A. Summary, Key Findings, and Recommendations ...................................................39

B. Institutional and Market Structure—Overview .......................................................39

C. Preconditions for Effective Securities Regulation ..................................................41

D. Main Findings .........................................................................................................42

E. Summary Implementation and Recommended Action Plan ...................................51

F. Authorities’ Response to the Assessment ................................................................53

IV. Core Principles for Effective Deposit Insurance Systems (IADI) .....................................56

A. Methodology Used for the Assessment ..................................................................56

B. General Preconditions for an Effective Deposit Insurance System ........................56

C. Well-Developed Legal Framework .........................................................................57

D. Sound Accounting and Disclosure Regime ............................................................58

E. Main Findings ..........................................................................................................59

F. Malaysia’s Islamic Deposit Insurance System ........................................................60

G. Summary of Compliance and Recommended Actions ...........................................61

V. Summary Assessment of Observance of the CPSS-IOSCO Principles for Financial Market

Infrastructures ..........................................................................................................................65

A. Introduction .............................................................................................................65

B. Institutional and Market Structure...........................................................................65

C. Payments System and Bond Clearing and CSD ......................................................66

D. Securities Clearing and CCP ...................................................................................67

E. Central Securities Depository ..................................................................................68

F. Key Recommendations for FMIs .............................................................................69

G. Authorities’ Response to the Assessment ...............................................................73

3

Tables

1. Summary Compliance with the Basel Core Principles—Detailed Assessments .................14

2. Recommended Action Plan to Improve Compliance with the Basel Core Principles .........20

3. Summary Implementation of the ICPs .................................................................................29

4. Recommendations to Improve Observance of the ICPs ......................................................35

5. Summary Implementation of the IOSCO Principles—Detailed Assessments ....................45

6. Recommended Action Plan to Improve Implementation of the IOSCO Principles ............51

7. Summary of Compliance with the Deposit Insurance Core Principles ................................61

8. Recommended Action Plan—Deposit Insurance Core Principles .......................................64

9. FMI Recommendations—RENTAS (RTGS, CSD and SSS) ..............................................69

10. FMI Recommendations—BMDC ......................................................................................70

11. FMI Recommendations—BMSC ......................................................................................71

12. FMI Recommendations—BMDepo ...................................................................................72

13. FMI Recommendations—Authorities ................................................................................73

Figures

1. Insurance Sector: Composition of Assets ............................................................................26

2. Insurance Sector: Component of Market Risk Exposures ...................................................26

Boxes

1. Islamic Banking in Malaysia .................................................................................................8

4

GLOSSARY

AML/CFT Anti-Money Laundering/Counter Financing of Terrorism

BAFIA Banking and Financial Institutions Act 1989

BCBS Basel Committee on Banking Supervision

BCPs Basel Core Principles

BFF Bridge Financing Facility

BM Bursa Malaysia

BMD Bursa Malaysia Derivative Berhad (the derivatives exchange)

BMDC Bursa Malaysia Derivative Clearing

BMDepo Bursa Malaysia Depository Sdn Bhd (the central depository)

BMS Bursa Malaysia Securities Berhad (the stock exchange)

BNM Bank Negara Malaysia

CAR Capital Adequacy Ratio

CBA Central Bank of Malaysia Act 2009

CCP Central Counterparty

GDG Government Deposit Guarantee

CGF Clearing Guarantee Fund

CME Chicago Mercantile Exchange

CMSA Capital Markets and Services Act 2007

CPs Core Principles

CPSS Committee on Payment and Settlement Systems

CSD Central Securities Depository

DIS Deposit Insurance Scheme

DFI Development Finance Institution

DPS Differential Premium System

DVP Delivery versus Payment

FHC Financial Holding Company

FMI Financial Markets Infrastructure

FRS Financial Reporting Standards

FSA Financial Services Act

FSAP Financial Sector Assessment Program

FSEC Financial Stability Executive Committee

FSPSR Financial Systems and Payment Systems Report

IBA Islamic Banking Act 1983

ICAAP Internal Capital Adequacy Assessment Program

IDIF Islamic Deposit Insurance Fund

IFRS International Financial Reporting Standards

IOSCO International Organization of Securities Commissions

IRB Internal Rating Based

LFSA Labuan Financial Services Authority

MASB Malaysian Accounting Standards Board

5

MI Member Institution

MoF Ministry of Finance

SC Securities Commission Malaysia

NPL Non-Performing Loan

PDS Private Debt Securities

PIDM Malaysia Deposit Insurance Corporation

PFMI CPSS-IOSCO Principles for Financial Markets Infrastructure

RM Malaysian Ringgit

RENTAS Real Time Electronic Transfer of Funds and Securities

ROSC Report on Observance of Standards and Codes

RTGS Real Time Gross Settlement System

RTO Recovery Time Objective

SAA Strategic Alliance Agreement

SBL Securities Borrowing and Lending

SC Securities Commission Malaysia

SCA Securities Commission Act 1993

SKM Cooperatives Commission

SME Small and Medium Enterprises

SRU Specialist Risk Unit

SSS Securities Settlement System

SuRF Supervisory Risk Based Framework

TIPS Takaful and Insurance Benefits Protection System

6

I. BASEL CORE PRINCIPLES FOR EFFECTIVE BANKING SUPERVISION

A. Summary

1. This assessment of the current state of compliance with the BCPs in Malaysia

has been undertaken as part of a joint IMF-World Bank Report on the Observance of

Standards and Codes (ROSC) mission.1 The assessment was conducted in April 2012. It

reflects the banking supervision practices of the Bank Negara Malaysia (BNM) as at end-

March 2012.

2. BNM employs a very well developed risk-focused regulatory and supervisory

regime, consisting of a hands-on and comprehensive program of onsite supervision and

extensive off-site macro and micro surveillance that is well integrated with its on-site

supervision. BNM supervisors are guided and assisted by a generally well articulated set of

risk management and internal control expectations, specified higher than international

minimum capital requirements, a comprehensive liquidity risk framework, and effective

coordination and information sharing with foreign supervisory authorities.

3. There remain, however, several opportunities to improve the regulatory and

supervisory framework. New financial services legislation, the Financial Services Act

(FSA), seeks to address many of these gaps.2 For instance, a clear gap exists in the

application of the supervision and regulation regime to financial holding companies (FHCs).

Six of the eight large domestic banking groups have parent FHCs and the current legislative

framework does not by its terms apply to those firms on a parent or consolidated basis. The

BNM has been creative by imposing conditions on the FHCs, using legislative authority

applicable to affiliates of banks to apply reporting and examination requirements to the FHC

and its subsidiaries. More detailed regulation would be useful on interest rate risk in the

banking book, credit concentrations, country risk, and operational risk. The transparency of

the criteria applied for new licenses and for acquisitions could be improved. Finally, there

exit opportunities to better focus the information sharing arrangements with the SC and

strengthening the legal protection available for supervisors. There are also some broad policy

issues on the relationship between BNM and MOF, and between BNM and the Malaysia

Deposit Insurance Corporation (PIDM) that should be reviewed.

1 The assessment was conducted by William Rutledge (consultant to the IMF) and Katia D'Hulster (World Bank

staff).

2 The FSA was passed in December 2012; implementation will follow Royal Assent, probably by mid-2013.

7

B. Institutional Setting and Market Structure Overview

4. The banking sector, which accounts for half the financial system, is well

capitalized and profitable. The onshore banking sector—with assets of some 200 percent of

GDP—comprises nearly 50 percent of financial sector assets (Islamic banks are around

20 percent of the banking sector) and Labuan IBFC banks an additional 3 percent. The top

5 domestic banking groups comprise nearly 62 percent of total banking system assets. The

banking sector’s asset quality remained healthy with steady improvement in gross NPL ratios

to 2.7 percent in 2011. Total provisions (general and specific) were 99.4 percent of NPLs;

NPLs net of specific provisions stood at 1.8 percent. Banks remain well capitalized with

system-wide risk-weighted capital ratio and core capital ratios at 15.6 percent and

13.6 percent respectively in 2011.

5. Non-bank credit intermediation is sizable, at some 90 percent of GDP. This is

accounted for predominantly by the state-run Employee Provident Fund, insurance

companies, and DFIs. The EPF and insurance companies invest the majority of their

portfolios in the domestic bond market, in both government and private debt securities. DFIs

provide credit via direct lending to targeted sectors such as agriculture, SMEs, infrastructure,

maritime, export-oriented sector, high-technology and capital-intensive industries. They are

well capitalized.

C. Preconditions for Effective Banking Supervision

6. The legal framework in Malaysia is based on a common law legal system. Laws

are enforced through a single structured judicial system consisting of superior and

subordinate courts whose decisions are enforceable, with avenues for appeal consistent with

common law systems. In addition to the court system, alternative mechanisms for resolving

disputes and debts also exist. These include arbitration, mediation, credit counseling, and

debt management and restructuring services.

7. Accounting and auditing services are well developed and provide a sound basis

for credible disclosure and resultant market discipline. Companies are required to prepare

their accounts based on approved accounting standards issued by the Malaysian Accounting

Standards Board (MASB). Public interest entities (including banking institutions) are

required to report their accounts using Financial Reporting Standards set by the MASB,

which is in compliance with IFRS both in terms of content and timing of implementation.

Companies’ accounts are required to be audited annually by approved auditors. Reports and

the audit procedures performed are in compliance with the National Auditing Standards,

which are in full compliance with the International Standards on Auditing.

8. The Malaysian Electronic Clearing Corporation, a wholly owned subsidiary of

BNM, operates RENTAS, a real time gross settlement system for interbank funds

transfer, a securities settlement system and a securities depository for all unlisted debt

8

instruments. RENTAS is also linked with the USD Clearing House in Hong Kong to

mitigate for settlement risk for Ringgit-USD foreign exchange transactions.

9. The credit information services industry in Malaysia consists of agencies from

both the public and the private sector. The Centralized Credit Reference Information

System is operated by BNM. It collects and disseminates credit information from and to

participating financial institutions. Private sector credit reporting agencies include Credit

Bureau Malaysia, RAM Credit Information, Financial Information Services and CTOS and

are regulated by the Registrar of Credit Reporting Agencies.

10. The deposit insurance system is administered by the PIDM and provides

coverage for conventional and Islamic deposits, for all type of depositors, whether

business or individuals. The maximum limit of coverage is RM 250,000 per depositor per

member institution. All commercial and Islamic banks, domestic and foreign, are member

institutions of PIDM and are subject to a risk based differential premium system.

11. BNM has a broad range of powers to avert or reduce risks to financial stability.

These include intervention and resolution measures, with powers to reduce systemic risks

emanating from both regulated and non regulated entities and to stem institutional or market

liquidity shocks. In addition to the operational standing credit facility for banks to obtain

overnight liquidity, BNM has broad powers to provide liquidity assistance to any financial

institution through a range of instruments. A Financial Stability Committee (FSC) serves as

BNM’s internal high level forum responsible for discussing risks to financial stability and

deciding on the appropriate policy responses.

Box 1. Islamic Banking in Malaysia

Islamic banking refers to a system of banking that complies with Shariah law. Malaysia has recorded robust

growth in Islamic banking assets. Total assets in the Islamic banking sector (including DFIs) accounted for

22.4% of total banking system assets as at end-2011. In Malaysia, Islamic banking is mostly conducted through

separately incorporated banks. The 16 Islamic banks include ten which are domestically owned and six which

are foreign owned. Licensed commercial and investment banks are also given the flexibility to operate an

Islamic banking window, subject to meeting applicable standards and guidelines to ensure full Shariah

compliance – to date there are three commercial Islamic banking windows and seven investment banking

windows.

In a dual financial system in which conventional and Islamic financial products are offered in parallel, a critical

aspect of the regulatory framework is the consistency of rules and regulations across both sectors to eliminate

possibilities for regulatory arbitrage. At the same time, there is a need to reflect the differences in the nature of

risk inherent in Islamic financial products and services. Shariah requirements are observed in the formulation of

applicable standards through active involvement of the Shariah unit and consultation with the Shariah Advisory

Council on Islamic Finance established under the CBA 2009 (SAC) on any matters requiring ascertainment of

Islamic law.

The supervisory approach and practices for Islamic banks at the BNM are very similar to commercial banks.

The only major difference is that, in accordance with the risk based supervisory framework, an additional

operational risk i.e. that of Shariah compliance, is assessed for Islamic banks. This risk is analyzed in two ways;

9

Box 1. Islamic Banking in Malaysia (concluded)

first, as a compliance risk embedded in every significant activity, second as an overarching operational risk for

the whole bank. To assist with the specific detailed aspects of the assessment, a team of Shariah officers

including a Shariah compliance expert employed in the BNM Specialist Risk unit provides input.

The Islamic banks are governed by a separate Act (the Islamic Banking Act 1983 (IBA)). In some areas, the

IBA provides less legislative authority than the more recent Banking and Financial Institutions Act 1989

(BAFIA) which governs the conventional banks. The authorities state that effective implementation of a

comparable prudential framework has been conducted through guidelines issued pursuant to the general power

to issue guidelines under IBA and setting clear supervisory expectations on Islamic banks. Although the

assessors have not focused on Islamic banking, the BNM is confident that in practice it ensures consistent rules

and regulation across both sectors. There remain some areas where the legal and regulatory requirements as

well as the powers of the BNM are not formalized in the IBA.

For example

The lack of explicit power for the BNM to revoke licenses for Islamic banks;

The IBA does not have a provision that allows the MOF, on recommendation of the BNM, to revoke a

license granted when BNM has been provided with false, misleading or inaccurate information in

connection with the application or after the grant of a license. Instead BNM may rely on contravention

of any provision of the IBA for revocation.

Unlike BAFIA, there is no specific share ownership threshold driving the need for an application in

the IBA; however by regulation BNM has imposed the same 5 percent threshold.

The IBA does not currently require external auditors to report matters of material significance to

the supervisor, for example failure to comply with the licensing criteria or breaches of banking or

other laws or other matters which they believe are likely to be of material significance.

The lack of explicit power to obtain information from the holding companies of Islamic banks.

Hence, the BNM cannot currently conduct any examinations of holding companies or require holding

companies, controllers or significant owners or any group or related entities to provide information to

BNM for supervisory purposes. Most Islamic banks are held directly by a regulated banking

institution; but one Islamic bank is not part of a commercial banking group and is held by a holding

company. The BNM is of the opinion that it has been able to obtain relevant information relating to the

holding company from the Islamic banks.

The lack of power for the BNM to access auditors’ working papers. In practice however the BNM

has not yet used this power for conventional banks.

Where the law provides for certain decisions to be referred to the MOF, BAFIA explicitly provides

that decisions by the MOF should be made upon the recommendations of BNM. This is currently

not explicitly available under the IBA.

Further enhancements are envisaged under the FSA to streamline legal and regulatory requirements and powers

of BNM in regulating the Islamic financial sector alongside the conventional financial sector. Major parts of the

IFSA, for instance licensing, regulation and supervision of financial groups and examination powers, contain

mirror provisions to the FSA to ensure consistency of rules and regulation across both sectors and eliminate

potential regulatory arbitrage (about 75% of the provisions in IFSA are the same as in the FSA). In addition, the

proposed new legislation seeks to provide greater visibility to Shariah compliance and the effective

implementation of Shariah governance by Islamic financial institutions, thus ensuring a coherent regulatory

framework. Among others, proposed provisions have been put forward to allow BNM to specify standards on

Shariah matters, including rules relating to Shariah governance, principles and practices of Shariah in relation to

the business and affairs of an Islamic institution, as well as requirements for Shariah compliance audits. In line

with Shariah requirements, the proposed new law will also clarify the nature of Shariah contracts employed in

conducting Islamic banking business and the process and priority of payments in the event of a winding up of a

financial institution involved in Islamic financial business.

10

D. Main Findings

Objectives, Independence Powers, Transparency, and Cooperation (CP 1)

12. The role of BNM and other authorities is clearly defined in law. The statutory

responsibilities and objectives of BNM are stated in the CBA and BAFIA, supported by

internal governance arrangements. The adoption of the new Policy Framework will increase

the transparency in policy activities. Governance arrangements (including operational

procedures) and the roles/responsibilities of various functions within the BNM have yet to be

more explicitly defined. The BNM is well funded and its staff has credibility based on their

professionalism and integrity.

13. The assessors found some instances in the legal framework where the Minister

could interfere with BNM’s independence. In practice, however, the assessors have not

come across evidence of de facto government or industry interference. It would provide

greater legal certainty regarding the independence of the BNM if these provisions were

removed and the independence of the BNM were formally grounded in the law.

14. Legal protection for bank supervisors is in place and as a matter of practice the

employees costs of defending actions made while discharging their duties in good faith

would be borne by the BNM. But some enhancements could be made. Ideally, the CBA

should specifically state that the legal protection provided to the BNM employees is not

limited in time (i.e. provides protection beyond the termination of appointment or

employment). Also, at the minimum, it is necessary that protection against incurring the costs

of defending the actions of supervisors is stated clearly and explicitly (at least at the level of

internal procedures).

15. BNM has a good framework for information sharing with foreign supervisors,

but domestic information sharing arrangements could be improved. The MOU with the

SC should be expanded to cover more than the investment banks that the SC and BNM co-

regulate.3 Information sharing with the SKM could also be formalized. Finally, the BNM

should consider entering into MOUs with countries of major new entrants (e.g., Japan).

CP 2-5 Licensing and structure

16. The Malaysian banking law appropriately defines and controls the business of

banking, with Bank Negara strongly overseeing the evolution of the banking structure,

with some areas of needed concurrence (e.g., license approval) from the Minister of

Finance. BNM has presented publicly long term plans for banking and financial structure

that have guided ongoing decision-making—as the country responded to the Asian banking

crisis of the 1990s by consolidating banks into the current eight large banking groups that

3 The October 2012 update to the BNM-SC MoU addresses these issues.

11

dominate the domestic market. Since that consolidation, the structure has been kept relatively

stable with no new licenses for conventional commercial banks granted from 1970 until

2009; consistent with the long run plan to encourage the development of the Islamic banking

sector, a number of Islamic bank licenses have been granted since 2004. There has been little

public transparency on the criteria used in BNM’s review of licensing and acquisitions that

have occurred in recent years, as BNM has chosen to share expectations only directly with

the applicants. Enhancing transparency and ensuring that appropriate focus is given to

shareholders of banks in addition to the applicant banks are areas where improvements can

be made.

Prudential Regulation and Requirements (CPs 6-18)

17. The BNM has set prudent and appropriate minimum capital adequacy

requirements but the scope of application of capital requirements should be widened to

include the FHC. Banks are well capitalized with strong system-wide risk-weighted capital

ratio and core capital ratios. The BNM has accredited ten banks to adopt the Basel II

foundation IRB approach for credit risk and two banks to adopt the standardized approach for

operational risk. The BNM does not have the power to include the FHC in the scope of

application of capital adequacy requirements (the new FSA should remedy this gap).

Basel III implementation is planned in accordance with the international timetable.

18. BNM issued comprehensive guidelines specifying the requirements and

regulatory expectations for banking institutions to have in place an effective system for

management of problematic assets and processes to ensure the adequacy of provisions

and reserves. In the event that BNM has supervisory concerns over banking institution’s

asset quality and adequacy of provisions, BNM has the power to require banks to increase the

level of provisions and reserves as well as banking institutions’ financial strength via higher

minimum capital requirements. The regulations as well as the supervisory framework cover

the overall credit risk process in terms of identification, management and mitigation.

19. The assessors identified several other areas for strengthening of prudential

regulation. More detailed regulation and supervisory expectations in the area of interest rate

risk in the banking book, credit concentrations, operational risk and country risk are

recommended. Also, the BNM should formally require banks to have a separate and

independent risk management unit. The BNM has recently released prudential regulations

covering Pillar 2 and many banks are making good progress towards their implementation.

That said, full implementation is required to further strengthen oversight of interest rate risk

in the banking book and credit concentrations.

Methods of Ongoing Banking Supervision (BCP 19-21)

20. BNM supervises the activities of banks with a well-structured risk focused

supervisory approach that integrates well on-site supervisory practices, extensive

12

regulatory reporting, and off-site monitoring. BNM’s Supervisory Risk-based Framework

provides a strong structure for supervisors to carry out consistent and effective supervision,

both through individual firm supervision and through horizontal or thematic reviews.

Decision-making within this structure, as to onsite reviews to be conducted and special off-

site surveillance work, is carried out by teams of supervisors headed by a Relationship

Manager (RM). The supervision work carried out by the RM and his/her team is supported

by micro-surveillance personnel, a macro-surveillance unit and a Specialized Risk Unit

(SRU). A careful system of checks and balances has been implemented, involving vetting of

ratings and other supervisory products through at least one, and sometimes two, layers of

independent panels within the Supervision Department. Ratings and supervisory

recommendations and remediation requirements are conveyed effectively to banking

institutions in writing, and through extensive interaction with the Board and senior

management; necessary remediation is followed through in a highly disciplined way.

21. Emerging global practices are being introduced and BNM has incorporated

increasingly sophisticated supervisory techniques and expectations into its risk focused

approach. There are challenges in ensuring that appropriately specialized supervisory

expertise is maintained, and utilized to maximum effect. BNM is moving forward to

incorporate Basel II, Pillar 2 and ICAAP expectations, and will soon be looking to address

recovery and resolution planning. BNM currently has relatively few specialists in the SRU,

and the bulk of those experts’ time is spent in-house, providing guidance to the general

supervisors. As BNM has found with model validation requirements, specialized risk people

can provide major contributions on-site. Over time, the assessors expect that the cadre of

specialized people should be expanded, and more of their time spent in direct interaction with

bankers.

Accounting and disclosure (CP 22)

22. The BNM has adequate regulations in place in the area of accounting and

disclosure by banking institutions. The BNM approves the external auditors for banks on

an annual basis and maintains an ongoing dialogue with them during the course of the audit

cycle. Feedback from market participants reflected a need for clearer communication of

auditors’ supervisory expectations to banks. Hence, assessors recommend the BNM more

clearly communicate to banks its supervisory expectations, particularly in case additional

procedures, may be required on top of the normal audit procedures.

Corrective and Remedial Powers (CP 23)

23. BNM has broad discretion in the range of remedial actions it can take to address

problem situations, which it takes within a well designed early intervention program.

BNM’s Supervisory Intervention Guide sets out a clear set of steps to take if a bank’s

condition deteriorates and its risk increases, with BNM having the clear power to issue

directives to banks to take appropriate remediation actions.

13

24. A new Strategic Alliance between BNM and PIDM was agreed while the BCP

review was taking place, and its effectiveness should be reviewed over time. Among the

issues to address is how the assessment of the viability of an institution is to be made (and

how transparent the criteria should be) and how the resolution framework could be applied to

financial holding companies.

Consolidated and Cross-border Banking Supervision (CP 24-25)

25. A clear gap exists in BNM’s legislative authority for the supervision and

regulation of FHCs. The BNM has been effective in narrowing (but not eliminating) the

gap, and the proposed new FSA would address the statutory shortcoming. Six of the eight

large domestic banking groups have parent FHCs, and the current legislative framework does

not by its terms apply to those firms on a parent only or consolidated basis. Many of the

affiliates of the bank are regulated by the BNM, but some (such as asset managers) are not.

The BNM has been creative by imposing conditions on the FHCs incident to approval of

their investments in their banks, covering the nomination of their directors and CEO,

acquisitions of shares of other companies, the issuance of capital instruments, and more

generally complying with BNM guidelines. BNM has also used legislative authorities

applicable to affiliates of banks to apply reporting and examination requirements to the FHC

and its subsidiaries. Through these means, the BNM has been able to significantly reduce the

existing gap, but not to completely eliminate it. No consolidated capital ratios apply to the

FHCs; the liquidity framework does not apply on a consolidated basis; and no stress testing

expectations are applied on a consolidated basis. The proposed legislative change, if enacted,

would address many of these issues.

26. BNM has a very well developed program of information exchange and

supervisory cooperation with an appropriate set of foreign supervisors, although it

could make some elements of information exchange globally and domestically more

formal. BNM has put in place an extensive set of MOUs and less formal information

exchange mechanisms with a relevant set of international supervisors. In addition it has been

active in hosting and participating in supervisory colleges and carrying out its own program

of overseas examinations. It has also been in the forefront in offering training programs to

other supervisors in the region. As a matter of good practice going forward, BNM should, in

licensing foreign banks subsidiaries, do a formal independent assessment of consolidated

home country supervision and look to enter into MOUs with countries of the major new

entrants. BNM’s MOU with the SC should be modified to make it much more directed to

consolidated supervision, and an MOU with the Cooperatives Commission should be

negotiated.

14

Table 1. Summary Compliance with the Basel Core Principles—Detailed Assessments

Core Principle Comments

1. Objectives,

independence,

powers, transparency,

and cooperation

1.1 Responsibilities

and objectives

Laws are in place for banking and the role of BNM is clearly defined. Clear

responsibilities and objectives for other authorities are also in place.

The BNM has issued the “Financial Sector Blueprint 2011-2020”, a

strategic plan that lays out the future direction of the Malaysian financial

system.

The assessors recommend the BNM uses stronger language in its

guidelines and recommendations, clearly stating that banks “must”

observe the regulatory requirements instead of “shall” observe the

regulatory requirements. This will be addressed by the BNM’s Policy

Development Framework which was rolled out for implementation on 17

May 2012.

1.2 Independence,

accountability and

transparency

Transparency in the policy activities of the BNM could be

increased. This will be achieved by the adoption of the new

Policy Framework.

Governance arrangements (including operational procedures)

and the roles/responsibilities of various functions within the

BNM have yet to be disclosed to the public for clarity and

accountability.

There are some instances in legal framework where the Minister could

interfere with BNM’s independence. For example, Section 70 in BAFIA

allows the Minister at any time to direct the Bank to make an examination

of the books or other documents, accounts and transactions of any

licensed institution if he has certain suspicions with regard to a banking

institution. Also, Section 15 of BAFIA allows companies to use the word

“bank”, “banking” (…) or any derivatives of this word with the explicit

approval of the Minister. Furthermore, Section 73 of BAFIA authorizes

BNM to direct institutions to take corrective actions, with the concurrence

of the Minister remove and/or appoint new officers and directors; the BNM

can also recommend to the Minister the revocation of a banking license

and approval of transfer of significant ownership.

In practice, however, the assessors have not come across evidence of

Government interference which would seriously compromise the

independence of the BNM. It would provide greater certainty regarding the

independence of the BNM if these provisions were removed and the

independence of the BNM were formally grounded in the law.

1.3 Legal framework The BNM will further enhance transparency by wider public

consultation on proposed policy measures in accordance with

the Policy Development Framework.

For the sake of transparency, the BNM should align the

terminology used in its regulations. Circulars, guidelines and

best practices are generally considered binding for banks and

there may not be any need to distinguish between them.

1.4 Legal powers BNM has the authority to address compliance with laws and safety and

soundness concerns through a broad grant of legislative authority.

15

Core Principle Comments

1.5 Legal protection Staff and persons appointed by the BNM are covered by the statutory

immunity clause for any action taken in good faith in pursuance of their

duties.

The assumption of the legal cost for defending against lawsuits faced by

individual supervisor could be anchored in the law.

The legal coverage should not depend on the person’s employment status

at the time of the lawsuit; former employees should be explicitly included.

Further, consideration should be given to include a provision permitting the

BNM to indemnify these persons for their legal costs in the event they are

sued.

1.6 Cooperation BNM has a good framework for information sharing with foreign

supervisors, but information sharing arrangements could be improved

through:

expanding the MOU with the SC to cover more than the

investment banks that the SC and BNM co-regulate (i.e.to

include asset management companies), and provide for the SC

to share information with BNM and for BNM to alert the SC of

supervisory developments in the broader banking group that

could affect those institutions within the group regulated by the

SC.

more formalized information sharing with the SKM.

the BNM entering into MOUs with countries (e.g., Japan) of

major new entrants.

2. Permissible

activities

The existing legal and regulatory provisions appropriately define and

control the business of banking, including, in particular, deposit-taking.

There are some deposit-taking companies not regulated by BNM.

3. Licensing criteria BNM has a conservative program for the granting of new licenses, where

in the exception of the explicit inviting of companies to apply for a

stipulated set of new licenses (as occurred in 2009), no applications for

conventional commercial banks have been considered in forty years. New

legislation (FSA) would, at such time as it is enacted, deal with many of

the limitations in the current approach, listed below, but in any event,

going forward BNM should address the following:

Reflecting the infrequency with which applications have been

entertained, the degree of transparency in the criteria to be

applied has been less than in other countries and should be

improved.

The focus of the application review was most heavily on the

immediate applicant, although some review is done of ultimate

shareholders. The criteria should explicitly include an

assessment on the nature and sufficiency of financial

resources and the integrity of the shareholder.

In the case of foreign banks, there is no explicit independent

evaluation of the nature and degree of consolidated regulation

and supervision applied by the home country supervisor, as

review is focused essentially on available FSAPs.

Criteria on the suitability of officers (covering more of the senior

team than the CEO) and the achievability of business plans

need to be more explicit;

4. Transfer of

significant ownership

The framework for controlling the ownership of banks is a good one, but

should be refined:

BNM must have the capacity to address directly unauthorized

acquisitions of shares, or control, of a banking institution, such

16

Core Principle Comments

as requiring divestitures and/or cessation of control.

BNM should have an ability to learn about and deal with

changes in the suitability of major shareholders.

5. Major acquisitions Overall approach is effective but there are some improvement

opportunities:

BNM should look to codify criteria more explicitly for major

acquisitions.

BNM needs more explicit authority to take corrective action

against non-banking companies that could be acquired if they

subsequently prove to be detrimental to the interests of the

bank affiliate.

6. Capital adequacy Banks remain well capitalized with system-wide risk-weighted capital ratio

and core capital ratios at 14.9 percent and 12.9 percent respectively in

2011.

The scope of application of the capital framework should be widened to

include financial holding companies, as outlined in the Basel II scope of

application.

Some other, but minor, amendments to fully align the capital framework

with the BCBS standards should also be made. The assessors, however

believe the impact not to be material, particularly in view of the other

areas where the BNM is stricter than the Basel minimum.

Basel II consists of three mutually reinforcing pillars; the BNM should

therefore also fully implement Pillar 2 as soon as possible. Having a Pillar

1 and Pillar 3 in place without a fully fledged Pillar 2 process is, strictly

speaking, not in line with the sound Basel II implementation.

Moving forward, BNM will have enhanced legal powers under the new

financial services legislation to enable the application of capital

framework on financial holding companies and is in the process of fully

aligning the definition of capital with the implementation of Basel III in

Malaysia.

7. Risk management

process

BNM has a good framework for risk management, but there are some

improvement opportunities:

Increase the number and experience level of risk specialists and

ensure they spend more time in the field (currently, other than model

validation reviews, such specialists only occasionally do on-site

reviews);

Ensure that under the current law that prudential risk management

policies are explicitly and consistently applied to consolidated FHCs;

Ensure in particular that relevant stress tests are applied to

consolidated FHCs.

BNM needs to issue a guideline that specifically requires banks

to

have a dedicated unit responsible for the risk management

process.

8. Credit risk The regulations as well as the supervisory framework cover the overall

credit risk process in terms of identification, management and mitigation.

9. Problem assets,

provisions, and

reserves

BNM is in compliant with Principle 9. BNM issued comprehensive

guidelines specifying the requirements and regulatory expectations for

banking institutions to have in place an effective system for management

of problematic assets and processes to ensure the adequacy of provisions

and reserves.

In the event that BNM has supervisory concerns over banking institution’s

asset quality and adequacy of provisions, BNM has the power to require

17

Core Principle Comments

banks to increase the level of provisions and reserves as well as banking

institutions financial strength via higher minimum capital requirements.

10. Large exposure

limits

Generally speaking, laws, guidelines and supervisory practices are in

place to ensure banking institutions’ large exposures are prudently

managed.

Some enhancements can be made in the following areas:

a more comprehensive definition of “a group of connected

counterparties” including the notion of economic dependency;

a more active use of Pillar 2 to identify and assess credit

concentrations; and

the alignment of the large exposure limits with international

best practice

The BNM is planning to issue a revised guideline for credit concentrations:

The revised guideline is expected to comprehensively address all the

requirements of Principle 10. Specifically, the enhancements to the

guidelines include:

Clear and specific risk management expectations on

compliance with the prudential limits; and

Comprehensive guidance on determining interconnectedness

of counterparties;

Review of prudential limits; and

Guidance on measurement of exposures to properly reflect

exposures and ensure consistency.

11. Exposure to

related parties

While the overall approach to connected lending is generally sound, the

exclusion of some significant minority shareholders is a gap that should be

addressed.

12. Country and

transfer risks

Although the assessors are broadly satisfied that country risk is identified

and assessed on a timely basis as part of the supervisory framework,

there is a need for more explicit legal and regulatory requirements on

banks in the area of country and transfer risk. With the growing

internationalization of the Malaysian banking system, the BNM should

expect that country and transfer risk be managed as a separate risk

category.

The BNM is to be commended for its periodic internal reporting on country

risk.

13. Market risks The regulatory guidelines are comprehensive and clear with regard to the

trading book.

The assessors recommend more market risk specialists are trained in

market risk.

The assessors recommend the risk specialist accompany the supervisor

on onsite examinations for higher risk institutions.

14. Liquidity risk The regime for bank liquidity risk management is a sound one, but

improvements could be made in the application of the regime to FHCs.

BNM supervisors need to conduct ongoing reviews of FHC

consolidated liquidity

BNM needs to require that an FHC conducts a consolidated liquidity

stress test and table the stress test results at ALCO.

15. Operational risk Although high level operational risk management requirements are

generally in place and adhered to, the assessors recommend

the release of more detailed regulation

the training of more supervisors in the operational risk specialist risk

stream

operational risk specialists attend on site examinations for higher risk

18

Core Principle Comments

institutions.

BNM is currently developing an Operational Risk Reporting System to

upgrade eFIDS into a full-fledged operational risk event and loss reporting

system, for increased surveillance capability as well as for information

sharing with the industry. This will include revision to the fraud taxonomy

to cater for fraud events that are inherent in investment banking activities.

The system is expected to be operational in the first quarter of 2013.

The BNM is already addressing the first recommendation by drafting the

Operational Risk Management Guidelines. The guidelines will also

mandate the reporting of all operational risk loss events.

16. Interest rate risk in

the banking book

The assessors reviewed the assessment of IRRBB as part of their review

of a number of supervisory files and were satisfied with the depth and

scope of the individual institutions’ and horizontal reviews. That said:

There is currently no regulation addressing IRRBB; and

Feedback from banks indicated this is an area where

supervisory expectations need to be clarified; and

More specialists need to be trained in IRRBB and they should

attend the onsite inspections for higher risk institutions.

17. Internal control

and audit

BNM has a strong program for ensuring that effective governance,

staffing, and processes are in place for the important control functions of a

bank. The BNM focuses heavily and effectively on offering director training

programs.

18. Abuse of financial

services

The assessors recommend AML/CFT Specialists join onsite BNM

supervisors for the examination of higher risk banks.

19. Supervisory

approach

BNM has a well developed framework of supervision with a strong

mechanism to ensure effective and consistent analysis of risks, with

access to a variety of information sources to keep its assessments current.

We have several recommendations for improvement:

Increase the number and experience level of risk specialists and

provide for their spending more time in the field;

Revisit its methodology for assigning ratings to banks to provide

capacity to factor in more explicitly adverse effects from affiliates.

20. Supervisory

techniques

BNM has a strong and well structured supervisory program, using

appropriate supervisory techniques.

21. Supervisory

reporting

The assessors recommend BNM require at least annual physical sign off

of the prudential returns by the Senior Management of the bank. The

BNM is currently enhancing its on-line statistical reporting (i.e. the

Integrated Statistical System (ISS) Project) to incorporate a digital

signatory requirement by senior management for each submission by the

banks.

While the assessors commend the BNM for the legal provisions with

regard to the power of the BNM to require adjustments to the financial

statements and to obtain supporting evidence, they recommend BNM

discontinue the use of Section 41 (4) of Bafia. This specific article requires

the BNM to inform the banking institution in writing that the financial

statements and supporting documents are satisfactory in terms of form

and content. This requirement somehow interferes with the independence

and responsibility of the external auditor and unduly exposes the BNM to

reputational risk.

22. Accounting and

disclosure

Feedback from market participants reflected a need for clearer

communication of auditors’ supervisory expectations to banks. Hence,

assessors recommend the BNM more clearly communicate to banks its

supervisory expectations in case additional procedures may be required

on top of the normal audit procedures.

19

Core Principle Comments

23. Corrective and

remedial powers of

supervisors

Look to strengthen the legislative basis for the determination of non-

viability it is required to make for troubled banks.

Determine the resolution approach for FHCs.

Revise its MOU with the SC to strengthen the requirement on BNM to

notify the SC of actions being applied to the bank affiliate of an

investment bank or asset management company; the MOU is in the

process of being enhanced to provide for greater coordination and

cooperation between BNM and SC, and to provide for examinations

by BNM of entities within the financial group which are licensed by

the SC.

Expand the penalties that can be imposed on individuals under Civil

Law.

24. Consolidated

supervision

BNM has been creative and largely effective in putting in place and

implementing a consolidated supervisory framework despite obvious

shortcomings in the enabling legislation as it applies to FHCs. BNM

recognizes the need to address the legislative shortcomings, which would

be extremely helpful, although some specific supervisory changes are also

recommended.

Needs to move quickly to put in place explicit legislative authorities for

oversight and supervision of FHCs.

Whether under the current or new legislation, formalize the

application of prudential regulatory provisions to the consolidated

organization.

Needs to strengthen its guidance for the assessment of parent

companies.

The MOU with the SC should be broadened to provide for SC sharing

with BNM of information on asset management companies and other

affiliates of a bank.

BNM should have the authority to require the closing of foreign offices

or to impose conditions on their activities.

25. Home-host

relationships

BNM has a very well developed program of information exchange and

supervisory cooperation with an appropriate set of foreign supervisors.

BNM has been in the forefront in offering training programs to other

supervisors in the region. Some recommendations for improvements;

In licensing foreign banks subsidiaries, BNM should do a

formal independent assessment of consolidated home country

supervision.

BNM should enter into MOUs with countries that have major

new entrants.

20

E. Key Findings and Recommended Action Plan

Table 2. Recommended Action Plan to Improve Compliance with the Basel Core

Principles

Reference Principle Recommended Action

Objectives,

Independence, Powers,

Transparency and

Cooperation (CP 1)

Remaining provisions in law requiring consultation with the Minister for

supervisory actions should be removed and the independence of the BNM

formally grounded in the law.

Expand the MOU with the SC to: cover more than the investment banks

that the SC and BNM co-regulate (i.e., to include asset management

companies and unit trusts which can also be part of banking groups);

provide for SC to share information with BNM on entities it supervises

within FHCs; and provide for BNM alerting the SC to supervisory

developments in the broader banking group that could affect those

institutions within the group regulated by the SC

Enter into more formalized information sharing arrangements with the

SKM;

Enter into MOUs with countries (e.g., Japan) of major new entrants.

Expand legal coverage so that former employees are explicitly included.

Consider including a provision permitting the BNM to indemnify these

persons for their legal costs in the event they are sued.

Licensing Criteria (CP3)

Reflecting the infrequency with which applications have been entertained,

the degree of transparency in the criteria to be applied has been less than

in other countries and should be improved.

The focus of the application review was most heavily on the immediate

applicant, although some review is done of ultimate shareholders. The

criteria should explicitly include an assessment on the nature and

sufficiency of financial resources and the integrity of the shareholder.

In the case of foreign banks, there is no explicit independent evaluation of

the nature and degree of consolidated regulation and supervision applied

by the home country supervisor, as review is focused essentially on

available FSAPs.

Criteria on the suitability of officers (covering more of the senior team than

the CEO) and the achievability of business plans need to be more explicit;

(the draft FSA, if enacted, will require the latter)

Transfer of Significant

Ownership (CP4)

BNM must have the capacity to address directly unauthorized acquisitions

of shares, or control, of a banking institution, such as requiring

divestitures and/or cessation of control.

BNM should have an ability to learn about and deal with changes in the

suitability of major shareholders.

Major Acquisitions

(CP 5)

BNM should codify criteria for major acquisitions;

BNM needs more explicit authority to take corrective action against non-

banking companies that could be acquired if they subsequently prove to

be detrimental to the interests of the bank affiliate.

Capital adequacy (CP6)

Expand the scope of application of the capital framework to include

financial holding companies, as outlined in the Basel II scope of

application.

Make amendments to fully align the capital framework with the BCBS

standards.

Fully implement Pillar 2.

21

Risk Management

Process

(CP 7)

Increase the number and experience level of risk specialists and ensure

they spend more time in the field, performing on-site review particularly at

large and complex banks;

Ensure that prudential risk management policies are explicitly and

consistently applied to consolidated FHCs, as is provided for under the

draft FSA;

Risk Management

Process

(CP 7)

Ensure in particular that relevant stress tests are applied to consolidated

FHCs.

BNY needs to issue guidance on the requirement for firms to have

separate risk management units.

Large Exposures (CP10) Fully use Pillar 2 to identify and assess credit concentrations;

Related Parties (CP 11)

Reassess the change made to the definition of connected parties in 2008,

excluding significant (20%-50%) shareholders (unless they had a director)

and their subsidiaries and associated companies, from the definition

Country Risks (CP 12) Introduce more explicit legal and regulatory requirements on banks in the

area of country and transfer risk.

Market Risk (CP 13) Strengthen the supervisory framework by letting market risk specialist

participate in on site exams for higher risk institutions

Liquidity Risk

(CP 14)

BNM supervisors need to conduct ongoing reviews of FHC consolidated

liquidity

BNM needs to require that an FHC conducts a consolidated liquidity

stress test and table the stress test results at ALCO.

Operational Risk

(CP 15)

Release more detailed regulation and supervisory expectations in the

area of operational risk.

Train more specialists in operational risks specialist risk stream let them

accompany supervisors on onsite examinations, particularly for higher risk

institutions.

Interest Rate Risk in the

Banking Book (CP 16)

Release more detailed regulation and supervisory expectations in the

area of interest rate risk in the banking book.

Implement Pillar 2 fully.

Abuse of Financial

Services (CP 18)

Let AML/CFT specialists accompany supervisors during on site

examinations, particularly for high risk institutions.

Supervisory Approach

(CP 19)

Increase the number and experience level of risk specialists and provide

for their spending more time in the field;

Revisit methodology for assigning ratings to banks to provide capacity to

factor in more explicitly adverse effects from affiliates

Supervisory Reporting

(CP 21)

Require at least annual physical sign off of the prudential returns by the

Senior Management of the bank. The BNM is currently enhancing its on-

line statistical reporting (i.e. the Integrated Statistical System (ISS)

Project) to incorporate a digital signatory requirement by senior

management for each submission by the banks.

Discontinue the use of Section 41 (4) of BAFIA. This specific article

requires the BNM to inform the banking institution in writing that the

financial statements and supporting documents are satisfactory in terms

of form and content. This requirement somehow interferes with the

independence and responsibility of the external auditor and unduly

exposes the BNM to reputational risk. (This provision is sought to be

removed in the proposed FSA).

22

Accounting/Disclosure

(CP 22)

Ensure clear communication to banks in case additional external audit

procedures are required.

Supervisors’ Corrective

and Remedial Powers

(CP 23)

Look to strengthen the legislative basis for the determination of non-

viability it is required to make for troubled banks.

Determine the resolution approach for FHCs.

Revise its MOU with the SC to strengthen the requirement on BNM to

notify the SC of actions being applied to the bank affiliate of an investment

bank or asset management company.

Expand the penalties that can be imposed on individuals under Civil Law.

Consolidated

Supervision (CP 24)

Put in place explicit legislative authorities for oversight and supervision of

FHCs.

Whether under the current or new legislation, formalize the application of

prudential regulatory provisions to the consolidated organization.

Strengthen the guidance for the assessment of parent companies.

The MOU with the SC should be broadened to provide for SC sharing with

BNM of information on asset management companies and other affiliates

of a bank.

BNM should have the authority to require the closing of foreign offices or

to impose conditions on their activities.

Home-Host

relationships (CP 25)

In licensing foreign bank subsidiaries, BNM should do a formal

independent assessment of consolidated home country supervision

BNM should enter into MOUs with countries (e.g., Japan) with major new

entrants.

F. Authorities’ Response to the Assessment

27. The Malaysian authorities wish to express their appreciation to the assessment

team for their comprehensive work and high degree of professionalism in conducting

the assessment. We value the candour in the interactions we had with the members of the

assessment team which enabled us to exchange ideas and insights as the Bank continues

ongoing efforts to further strengthen the supervisory and regulatory regime for the Malaysian

banking sector.

28. The assessment concludes that the Malaysian banking sector is supervised under

a well developed risk-focused and comprehensive regime. The areas of recommendation

largely correspond with the Bank’s current priorities to further strengthen the regulatory and

supervisory system, and validate the various initiatives that are at advanced stages of

implementation or for which definite plans have been put in place. These measures will place

the Malaysian banking sector on a stronger footing as they expand in scope and geographic

reach.

29. A significant number of the recommendations will be addressed by the proposed

financial services legislation. Amongst others, this will provide greater clarity in licensing

standards, suitability requirements for shareholders, powers to address unauthorized

23

acquisition of shares, powers for enforcement of corrective actions, and the regulation and

supervision of financial holding companies. A number of regulatory standards are currently

being revised to enhance the framework on risk management, large exposures and corporate

governance, and the issuance of the Risk Governance guidelines in the second half of 2012

will set explicit expectations on the need for a dedicated risk management unit within banks.

With regard to Basel II implementation, the supervisory expectations for Pillar 2 is already in

place and beginning 2013, the full supervisory review and examination process will be

conducted on all banks. The report mentions in several places that additional supervisory

resources, especially in the specialist risk areas, are likely to be required to continue to

deliver on and to augment supervisory practices. This is being addressed as part of the

organizational development initiative and the participation of specialist risk units in the on-

site examination exercises will be intensified moving forward. On the comment regarding

legal protection for past employees, the legal provision applies to both current and former

employees of the Bank, as long as the suit against him is in respect of an act committed or

statement made by him in his capacity as an employee of the Bank, and in good faith. As

such, it is not necessary to expressly distinguish former employees in the legislation.

30. In line with increasing regional and international financial integration, a Home-

Host Supervisory Cooperation framework has been put in place to affirm existing

arrangements with foreign supervisors to ensure effective sharing and flow of

information. Domestically, the Strategic Alliance Agreement with the Malaysia Deposit

Insurance Corporation has since been revised to specify the triggers for non-viability and the

Memorandum of Understanding with the Securities Commission is being enhanced to

provide for clear arrangements with respect to the assessment of entities within a financial

group. The current practice of having bilateral and trilateral engagement with external

auditors will also be better documented and shared to set clear the expectations placed on the

external auditors.

31. For BCPs that were assessed as compliant, we will seek continuous

improvements particularly in light of the revised BCP that will be introduced in the

near future.

24

II. ASSESSMENT OF INSURANCE CORE PRINCIPLES (ICPS)4

A. Summary, Key Findings, and Recommendations

32. Bank Negara Malaysia (BNM) is a highly respected insurance regulator: the

regulatory guidance is comprehensive, and the supervision is effective and well-focused.

BNM has the capacity and is taking proactive steps to address shortcomings in the insurance

regulatory framework to achieve full observance of the ICPs. The proposed financial

institutions legislation5 should address concerns with BNM’s powers for group-wide

supervision and ensure that client monies with intermediaries are properly protected. The

implementation of the Internal Capital Adequacy Assessment Process (ICAAP), and new risk

governance guidance, will close current gaps in BNM’s formal expectations for better risk

management practices by insurers. Lastly BNM is not a home supervisor to any insurance

group, and cross-border activities of Malaysian insurers are not significant, so there may not

currently be a significant urgency for BMN to implement substantive measures to ensure it

can be effective in cross-border coordination during a crisis. Given the speed of change in the

financial sector, including the insurance industry, BNM should endeavor to seek continuous

improvements in its supervisory practices as well.

33. The assessment did not reveal any current potential sources of significant risk to

Malaysian financial stability from its insurance industry. The sector continues to be

relatively small and fragmented, without any major risk accumulations that could pose

stability concerns. Insurers should continue be monitored to ensure they do not introduce

imprudent practices and instability within the industry, with special attention paid to those

that may not have an extensive track record of conducting business in Malaysia, such as new

entrants and insurers where there has been a recent change of control. Also, any substantial

growth in risk accumulations in Danajamin should be very closely monitored, given the

nature of its business risks and the incomplete regulatory framework that exists for financial

guarantee insurance. BNM has indicated that efforts will be taken to strengthen the

regulatory framework for financial guarantee insurance.

B. Introduction and Scope

34. This assessment provides an understanding of the significant regulatory and

supervisory framework for the insurance sector of Malaysia. The market has been

growing for Islamic insurance products (family takaful, general takaful, and re-takaful). The

ICPs were not specifically developed with Islamic insurance products in mind. Consequently,

based on the agreed scope, details on the regulation, supervision and various workings of

4 The assessment was conducted by Mark Causevic (IMF Consultant; OSFI, Canada).

5 The FSA bill was passed in December 2012.

25

Malaysian Islamic insurance market are included in this report, but do not form part of the

ICP assessment ratings for Malaysia.

35. The assessment is based solely on the laws, regulations and other supervisory

requirements and practices that are in place at the time of the assessment. Ongoing

regulatory initiatives are noted by way of additional comments e.g., proposed legislation.

C. Overview: Institutional and Macro Prudential Setting

Market Structure and Industry Performance

36. While the market is fairly sophisticated, offering a wide range of life, non-life

and takaful insurance products, there is scope for further growth and consolidation.

Current industry challenges that BNM has identified and is addressing include asset-liability

matching in a low interest rate environment, rising claims costs and increased volatility in the

global markets.

37. Access to and foreign ownership of the Malaysian insurance market is restricted.

No direct conventional insurance license has been issued since the 1970s. New reinsurance,

takaful and retakaful licenses have been issued from time to time since 1995 to meet specific

objectives to enhance domestic reinsurance capacity and further develop the takaful industry.

The foreign equity limit for insurers is 70 percent. A foreign equity limit above 70 percent

will be considered on a case-by-case basis, particularly for players that can facilitate

consolidation and rationalization of the general insurance industry.

38. Four out of nine life insurers are owned by the large domestic banks and

domestic parties account for most of the ownership of the Malaysian general insurers.

Nevertheless, foreign-owned insurers have a major presence in Malaysia, with foreign-owned

insurers ranking as or amongst the largest insurers in the life and non-life sectors. Domestic

banks have major presence in the takaful market, with the dominant takaful operator being a

subsidiary of a large domestic bank.

39. The cross-border operations of domestic insurers remained very small in terms

of size and span. In 2011, such operations involved total assets of RM979.8 million,

amounting to only 0.5 percent of total insurance industry assets, spanning four countries near

the Malaysian borders (Figure 1).

40. Agency is the primary distribution channel for both life and general business.

The agency channel generates 59 percent and 65 percent of new premiums (life) and gross

premium (general), respectively. Bancassurance has also gained prominence in the recent

years because insurers can leverage on the banks’ existing network and customer base.

Bancatakaful is the main distribution channels in family takaful sector with 53 percent

contribution generated in 2011.

26

41. The composition of insurance fund assets (including takaful business) remained

similarly stable with private debt securities (PDS) continuing to form the majority of

assets held (Figure 1). Market and credit risk exposures arising from holdings of PDS

remained manageable with the bulk of PDS held in high-grade papers (rated ‘A’ and above).

Insurers reduced holdings in equities during the year to 15 percent of assets as at end-2011,

in favor of less risky assets such as Malaysian government securities (MGS) and fixed

deposits which accounted for 17 percent and 13.6 percent of the industry’s total assets,

respectively. The rebalancing of investments maintained the market risk exposures of

insurers at 12.6 percent of capital available, with interest rate risk from higher investments in

MGS partly offset by lower equity risk exposures. Collectively, equity and interest rate risks

formed 84.6 percent of insurers’ total market risk exposures (Figure 2).

Figure 1. Insurance Sector: Composition of

Assets

Figure 2. Insurance Sector: Component of

Market Risk Exposure

Source: Bank Negara Malaysia, FSPSR 2011.

42. A significant component of life insurance businesses are investment-linked

products which account for one third of the total new life business. Demand for

Investment-linked products has reduced significantly as a result of global market uncertainty.

The potential of the life industry can be further harnessed through the holistic pension review

being undertaken, including tax incentives to spur the private pensions industry.

43. Takaful has experienced a double-digit growth in past five years with average

annual growth of 24 percent. Family takaful has contributed considerably to the growth in

contributions compared to general takaful fund, accounting for 85 percent of total funds

in 2011. Ordinary family products continue to be the key contributor to the new business,

while in general business is dominated by motor takaful.

44. Malaysia is not a country that has significant natural catastrophe risks. While

flooding events can lead to significant gross insurance losses, commercial risks tend to be the

bigger source of large losses.

27

45. The overall business retention level for general insurers is approximately

70 percent, but this varies widely by business class. Use of reinsurance is more

pronounced for large and specialized risks in the aviation, oil & gas and engineering classes

of business, where reinsurance premium ceded amounted to 94 percent, 93 percent and

56 percent of total premiums, respectively. In contrast, for motor insurance, the dominant

general insurance line in Malaysia, the retention rate approaches 90 percent. Malaysian

insurers reinsure a substantial part of risks underwritten in the global reinsurance market,

either directly or through reinsurance placements with Malaysian branches of foreign

reinsurers.

46. While premium growth declined in 2011, capital adequacy continued to remain

strong. Persistent low yields and investment losses have been a drag on profitability.