CRA Guide To Data Reporting And Collection

User Manual: CRA

Open the PDF directly: View PDF ![]() .

.

Page Count: 64

A Guide to

CRA Data Collection

and Reporting

Federal Financial Institutions

Examination Council

January 2001

A Guide to CRA Data Collection and Reporting 2

This user’s guide was prepared by

CRA/HMDA Systems

Information Technology

Board of Governors of the Federal Reserve System

for the Federal Financial Institutions

Examination Council

A Guide to CRA Data Collection and Reporting 3

Contents Foreword 4

Executive Summary: Compliance Responsibilities 5

Purpose of CRA 5

Who Must Report 5

When to Report 5

Reporting Requirements 6

File Specifications and Edit Validations 6

Collecting the Data 8

Composite Loan Data 8

Other Loan Data 14

Consumer Loans 14

Reporting the Data 16

Reporting Tools 16

Internet Resources 19

Data Automation Cycle 19

Public Availability of Data 22

Glossary 23

Appendix A—

Regulation BB: Community Reinvestment 26

Appendix B—

Schedule RC-C, Part II.

Loans to Small Businesses and Small Farms 46

General Instructions 46

Loans to Small Businesses 49

Agricultural Loans to Small Farms 52

Examples of Reporting in Schedule RC-C, Part II 54

Appendix C—

Thrift Financial Report Instruction Manual and Form 60

Loans to Small Businesses and Small Farms 60

Appendix D—

U.S. Bureau of the Census Regional Offices 64

A Guide to CRA Data Collection and Reporting 4

Foreword

In response to numerous

requests and inquiries, the

Federal Financial Institutions

Examination Council (FFIEC)

has developed this guide for

Community Reinvestment Act

(CRA) data reporters. Data

collection, maintenance, and

reporting are important

aspects of large-institution

evaluations under CRA. This

guide can be used as a

resource when collecting and

maintaining data, creating a

submission, and posting

lending data in the CRA public

file. It is designed to reduce

burden on the approximately

2,000 financial institutions

subject to the reporting

requirements of the CRA

regulations.

Users of this guide should be

aware of its limitations. It

relates only to the collection,

maintenance, and reporting of

small-business and small-farm

loan data and to the collection,

maintenance, and reporting

(as applicable) of other loan

data (except data on home

mortgage loans) that may be

considered during CRA

evaluations. Although this

guide addresses many issues

relating to these matters, new

issues arise often; they should

be directed to the CRA

Assistance Line at (202) 872-

7584 or crahelp@frb.gov.

Use of this guide is not a

substitute for familiarity with

the CRA regulations and the

interagency questions and

answers (Qs&As) that inter-

pret those regulations. The

regulations and Qs&As may

be revised from time to time,

and you should consult them

to determine whether this

edition of the guide reflects

the most recent revisions.

Both are available on the

FFIEC’s Internet site at

www.ffiec.gov/cra.

A Guide to CRA Data Collection and Reporting 5

Executive

Summary:

Compliance

Responsibilities

Purpose of CRA

The Community Reinvestment Act of

1977 (CRA) is implemented by

regulations of the Office of the

Comptroller of the Currency (OCC),

the Board of Governors of the

Federal Reserve System (Board),

the Federal Deposit Insurance

Corporation (FDIC), and the Office of

Thrift Supervision (OTS)

(collectively, the agencies) in 12

CFR parts 25, 228, 345, and 563e.

The CRA regulations require that

information on business, farm, and

community development lending by

large insured depository institutions

be made available to the public.

CRA directs the agencies to

encourage insured depository

institutions to help meet the credit

needs of the communities in which

they are chartered. CRA does not

prohibit any activity, nor is it intended

to encourage unsafe or unsound

practices or the allocation of credit.

CRA requires that each insured

depository institution’s record in

helping to meet the credit needs of

its entire community, including low-

and moderate-income neighbor-

hoods, be assessed periodically.

That record is taken into account

when considering an institution’s

applications for deposit facilities,

including mergers and acquisitions.

The CRA regulations contain

different evaluation methods for

different types of institutions: the

lending, investment, and service

tests for large retail institutions; the

community development test for

wholesale or limited-purpose

institutions; the streamlined

performance standards for small

institutions; and the strategic-plan

option for institutions with approved

strategic plans.

The Consumer Compliance Task

Force of the FFIEC promotes

consistency in the implementation of

the CRA regulations by periodically

publishing interagency Qs&As and

examination procedures and by

facilitating uniform data reporting.

Who Must Report

All state member banks, state

nonmember banks, national banks,

and savings associations that are not

small or special-purpose institutions

are subject to the data collection and

reporting requirements of the CRA.

For the purpose of collecting and

reporting small business and small-

farm loan data, a small institution is a

bank or thrift that, as of December 31

of either of the prior two calendar

years, had total assets of less than

$250 million and was independent or

an affiliate of a holding company

that, as of December 31 of either of

the prior two calendar years, had

total banking and thrift assets of less

than $1 billion. Institutions that are

not small are considered large

institutions (see the glossary,

beginning on page 23, for

definitions).

When to Report

Data for a given year must be

submitted to the Board, the

designated processor for all of the

agencies, by March 1 of the following

year.

Merging Institutions

Following are three scenarios

describing data collection and

Executive Summary: Compliance Responsibilities

A Guide to CRA Data Collection and Reporting 6

reporting responsibilities for the

calendar year of a merger and for

subsequent years.

Scenario One

Two institutions are exempt from

CRA collection and reporting

requirements because of asset size.

The institutions merge. No data

collection is required for the year in

which the merger takes place,

regardless of the resulting asset

size. Data collection would begin

after two consecutive years in which

the combined institution had year-

end assets of at least $250 million or

was part of a holding company that

had year-end banking and thrift

assets of at least $1 billion.

Scenario Two

Institution A, an institution required

to collect and report data, and

Institution B, an exempt institution,

merge. Institution A is the surviving

institution. For the year of the

merger, data collection is required

for Institution A’s transactions. Data

collection is optional for the

transactions of the previously

exempt institution. For the following

year, all transactions of the surviving

institution must be collected and

reported.

Scenario Three

Two institutions, each of which is

required to collect and report the

data, merge. Data collection is

required for the entire year of the

merger and for subsequent years, so

long as the surviving institution is not

exempt. The surviving institution

may file either a consolidated

submission or separate submissions

for the year of the merger but must

file a consolidated report for

subsequent years.

Institutions

with No Small-Business

or Small-Farm Loans

An institution that has not purchased

or originated any small-business or

small-farm loans during the reporting

period would not submit the

composite loan records for small-

business or small-farm loans.

However, all institutions subject to

data reporting requirements must

submit the information discussed

below under “Reporting

Requirements.”

Lenders Covered by Home

Mortgage Disclosure Act

If an institution is not required to

collect home mortgage loan data by

the Home Mortgage Disclosure Act

(HMDA), it need not collect home

mortgage loan data under the CRA.

Examiners will sample an institu-

tion’s home mortgage loans to

evaluate its home mortgage lending.

If an institution wants to ensure that

examiners consider all of its home

mortgage loans, it may collect and

maintain data on these loans.

Modification, extension and

consolidation agreements (MECAs)

are transactions in which an

institution obtains loans from

another institution without actually

purchasing or refinancing the loans.

In some states, MECAs, which are

not considered loan refinancings

because the existing loan

obligations are not satisfied and

replaced, are common. Although

these transactions are not

considered to be purchases or

refinancings, as those terms have

been interpreted under CRA, they

do achieve the same results. An

institution may present information

about its MECA activities to

examiners for consideration under

the lending test as “other loan data.”

Reporting

Requirements

At a minimum, institutions must

submit, in electronic format:

·a transmittal sheet,

·a definition of its assessment

area(s),

·a record of its community

development (CD) loans. (If an

institution does not have CD loans

to report, the record should be sent

with “0” in the CD loan composite

data fields); and

·information on small-business and

small-farm loans, if applicable

CRA data are aggregated on the

census tract level, and each tract

represents one record in an entire

data submission. For example:

·Six different small-business loans

made in the same census tract

would count as one composite

record.

·Six different small-farm loans,

three in one census tract and three

in another, would count as two

composite records.

File Specifications

and Edit Validations

The FFIEC makes available free

CRA data preparation software to

any institution that wishes to use it.

The software includes some basic

analytical reports regarding an

institution’s data. To obtain a copy of

the latest version of the software,

contact the CRA Assistance Line at

(202) 872-7584.

If an institution finds that the

FFIEC’s software does not meet its

needs, it may create a data

submission using the File

Specifications and Edit Validation

Rules that have been set forth to

Executive Summary: Compliance Responsibilities

A Guide to CRA Data Collection and Reporting 7

assist with electronic data

submissions. For information about

specific electronic formatting proce-

dures, contact the CRA Assistance

Line at (202) 872-7584 or click on

“How to File” at www.ffiec.gov/cra.

File Specifications

Institutions that develop their own

programs must follow the precise

format laid out in the CRA File

Specifications. This file format

should be incorporated into an

automated system to ensure an

error-free data submission.

Edit Validation Rules

When an institution chooses to

create an electronic data

submission, it must edit its data

using the CRA Edit Validation Rules.

These rules are designed to ensure

data integrity and to prevent errors.

CRA edit validations are divided into

three edit types: syntactical, validity,

and quality. Each type corresponds

to errors of a different degree of

severity, and each must be

thoroughly understood to ensure that

the data are accurate and complete.

Syntactical (S) —Records that contain errors that may prevent them

from being uploaded to the FFIEC database. These errors range from

incorrect activity years to duplicate property locations, which indicate that

the property combination for that record identifier was used more than

once. These records will not be reflected in your disclosure statement

until the appropriate corrections have been made.

Validity (V) —Records containing incorrect information. The most

common validity errors are incorrect census tract/BNA numbers. These

records will not be reflected in your disclosure statement until the

appropriate corrections have been made.

Quality (Q) —Loan information that, while it may pass all syntactical and

validity edits, is nevertheless statistically unusual and is subject to further

investigation or review to confirm correctness. For a majority of the quality

edits, if the data are correct, no changes are necessary and the data will

be reflected.

A Guide to CRA Data Collection and Reporting 8

Collecting the

Data

Composite Loan

Data

Transmittal Sheet

The transmittal sheet is used to

identify each institution. Institutions

are asked to provide a reporter’s

identification (RID) number. This

number corresponds to the

certificate number for FDIC-

supervised institutions, the docket

number for institutions supervised

by the OTS, and the charter number

for OCC-supervised institutions. If an

institution is supervised by the

Board, the Research, Statistics,

Supervision and Regulation, and

Discount and Credit (RSSD)

Number is used. Board-supervised

institutions that do not know their

RSSD numbers should contact

the CRA Assistance Line at (202)

872-7584 or crahelp@frb.gov to

obtain it.

The transmittal sheet provides

valuable institution and contact

information. It is important that the

institution’s name, contact name,

address, phone number, and fax

number be correct since all future

correspondence will be based on

that information. Because area

codes are subject to change, it is

important to review phone and fax

numbers for accuracy before data

submission.

Assessment Area(s)

Delineation

For institutions other than those

designated as wholesale or limited-

purpose (see the glossary),

assessment areas must consist

generally of one or more metro-

politan statistical areas (MSAs) or

one or more contiguous political

subdivisions such as counties,

cities, or towns. An institution must

include the geographies in which its

main office, branches, and deposit-

taking ATMs are located as well as

the surrounding geographies in

which it has originated or purchased

a substantial portion of its loans.

Please refer to section __.41 of the

regulations and the interagency

Qs&As for further guidance,

particularly Q&A __.41(e)(4)–1,

which explains limitations on the

size of assessment areas.

Note: When you are entering

information about small-business

and small-farm loans, you need to

provide MSA, state, county, and

tract/BNA information to indicate the

location of the loan. The information

that you provide in the loan data

entry screens is

not

your assess-

ment area(s). This is simply the

loan’s location.

Assessment Area(s) Reporting

If your assessment area(s) includes

an entire MSA, you should report:

Census

Include/ Tract/

Exclude MSA State County BNA

+0520 NA NA NA

If your assessment area(s) includes

an MSA less one county, you should

report:

Census

Include/ Tract/

Exclude MSA State County BNA

+0520 NA NA NA

-0520 NA 151 NA

If your assessment area(s) includes

or consists of an entire county, you

should report:

Census

Include/ Tract/

Exclude MSA State County BNA

+0520 13 089 NA

Collecting the Data

A Guide to CRA Data Collection and Reporting 9

For more assessment area(s)

delineation examples, please refer

to the CRA Edits, which can be

found at www.ffiec.gov/cra/

edits.htm.

Community Development

Loans

Institutions subject to data reporting

requirements must report the

aggregate number and amount of

community development loans

originated or purchased during the

prior calendar year.

A community development loan has

community development as its

primary purpose. As defined in the

regulations, “community develop-

ment” means—

·affordable housing (including

multifamily rental housing) for low-

or moderate-income individuals;

·community services targeted to

low- or moderate-income

individuals;

·activities that promote economic

development by financing

businesses or farms that meet the

size eligibility standards of the

Small Business Administration’s

Development Company or Small

Business Investment Company

programs (13 CFR 121.301) or

have gross annual revenues of $1

million or less; or

·activities that revitalize or stabilize

low- or moderate-income

geographies.

In addition to having a community

development purpose, a community

development loan must also benefit

the institution’s assessment area(s)

or a broader statewide or regional

area that includes the institution’s

assessment area(s). Institutions

should be prepared to provide

examiners with information

regarding the community develop-

ment purpose and location of the

community development loans that

they report at the time of their

examination.

Note: If an institution is not a

wholesale or limited-purpose

institution, it cannot designate a loan

as a community development loan if

the loan has already been reported

or collected by the institution or an

affiliate as a small-business, small-

farm, consumer, or home mortgage

loan (except in the case of a

multifamily dwelling loan, which may

be considered a community

development loan as well as a home

mortgage loan). Further, except for

multifamily affordable housing loans,

if a loan meets the definition of a

small-business, small-farm,

consumer, or home mortgage loan,

retail institutions must collect and

report the loan in this manner. Retail

institutions may not choose to

collect and report it as a community

development loan.

Primary Purpose

As long as the primary purpose of

the loan is community development,

the full amount of the institution’s

loan should be included in its report

of aggregate community develop-

ment lending. A loan has a primary

purpose of community development

when it is designed for the express

purpose of community development.

Refer to the interagency Qs&As for

further discussion of primary

purpose, particularly Q&A __.12(i)

and 563e.12(h)–7.

Affiliate Loans

Affiliate

means any company that

controls, is controlled by, or is under

common control with another

company. The term “control” has the

meaning given to that term in 12

U.S.C. 1841(a)(2), and a company is

under common control with another

company if both companies are

directly or indirectly controlled by the

same company.

An institution is not required to

collect information on affiliate loans.

However, an institution that elects to

have its regulator consider loans by

an affiliate, for purposes of the

lending or community development

test or an approved strategic plan,

must collect, maintain, and report for

those loans the data that the

institution would have collected,

maintained, and reported had the

loans been originated or purchased

by the institution.

An institution may elect to have only

a particular category of an affiliate’s

lending considered. The basic

categories of loans are home

mortgage loans, small-business

loans, small-farm loans, community

development loans, and the five

categories of consumer loans (motor

vehicle loans, credit card loans,

home equity loans, other secured

loans, and other unsecured loans).

Affiliate’s Home Mortgage

Lending

If an institution elects to have an

affiliate’s home mortgage lending

considered in its CRA evaluation and

the affiliate is a HMDA reporter, the

institution must be prepared to

identify those loans reported by its

affiliate under 12 CFR part 203

(Regulation C, implementing HMDA).

At its option, the institution may

either provide examiners with the

affiliate’s entire HMDA disclosure

statement or just those portions

covering the loans in its assessment

area(s) that it is electing to have

considered. If the affiliate is not

Collecting the Data

A Guide to CRA Data Collection and Reporting 10

required by HMDA to report home

mortgage loans, the institution must

provide sufficient data concerning

the affiliate’s home mortgage loans

to enable the examiners to apply the

performance tests.

Constraints on the Consideration

of Affiliate Lending

No affiliate may claim a loan

origination or loan purchase if

another institution claims the same

loan origination or purchase.

However, an institution can count as

a purchase a loan originated by an

affiliate that the institution

subsequently purchases, or count as

an origination a loan later sold to an

affiliate, provided the same loans are

not sold several times to inflate their

value for CRA purposes.

If an institution elects to have its

supervisory agency consider loans

within a particular lending category

made by one or more of the

institution’s affiliates in a particular

assessment area(s), the institution

must elect to have the agency

consider all loans within that lending

category in that particular

assessment area(s) made by all of

the institution’s affiliates.

Consortium/

Third-Party Loans

Community development loans

originated or purchased by a

consortium in which an institution

participates or by a third party in

which the institution has invested:

·will be considered, at the

institution’s option, if the institution

reports the aggregate number and

aggregate amount of consortium/

third party loans originated or

purchased; and

·may be allocated among

participants or investors, as they

choose, for purposes of the

lending test, except that no

participant or investor:

—may claim a loan origination or

loan purchase if another

participant or investor claims

the same loan origination or

purchase; or

—may claim loans accounting for

more than its percentage share

(based on the level of its

participation or investment) of

the total loans originated or

purchased by the consortium or

third party.

In some circumstances, an

institution may invest in a third party,

such as a community development

bank, that is also an insured

depository institution and is thus

subject to CRA requirements.

However, if the financial institution

and the third party are not affiliates,

the third party may receive

consideration for the community

development loans it originates, and

the financial institution that invested

in the third party may also receive

consideration for its pro rata share of

the same community development

loans under Q&A __.22(d)–3.

Equity and Equity-Type

Investments in a Third Party

If an institution has made an equity

or equity-type investment in a third

party, community development loans

made by the third party may be

considered under the lending test.

On the other hand, asset-backed and

debt securities that do not represent

an equity-type interest in a third party

will not be considered under the

lending test unless the securities are

booked by the purchasing institution

as a loan.

For example, if an institution

purchases stock in a community

development corporation (CDC) that

primarily lends in low- and

moderate-income areas or to low-

and moderate-income individuals in

order to promote community

development, the institution may

claim a pro rata share of the CDC’s

loans as community development

loans. The institution’s pro rata share

is based on its percentage of equity

ownership in the CDC. See Q&A

__.22(d)–1. More information

concerning consideration of an

equity or equity-type investment

under the investment test and both

the lending and investment tests can

be found in Q&A __.23(b)–1.

Evaluation of Loans Made

by Consortia or Third Parties

under the Lending Test

Loans originated or purchased by

consortia in which an institution

participates or by third parties in

which an institution invests will only

be considered if they qualify as

community development loans and

will be considered only under the

community development criterion of

the lending test. However, loans

originated directly on the books of an

institution or purchased by the

institution are considered to have

been made or purchased directly by

the institution, even if the institution

originated or purchased the loans as

a result of its participation in a loan

consortium. These loans would be

considered under the appropriate

lending-test criteria, depending on

the type of loan. See Q&A

__.22(d)–2.

Collecting the Data

A Guide to CRA Data Collection and Reporting 11

Small-Business

and Small-Farm Loans

The CRA regulations require a large

institution to collect and maintain, in

electronic format, until the

completion of its next CRA

examination, the following data for

each small-business or small-farm

loan originated or purchased by the

institution:

·a unique number or alphanumeric

symbol that can be used to identify

the relevant loan file;

·the loan amount at origination;

·the loan location; and

·an indicator of whether the loan

was to a business or farm with

gross annual revenues of $1

million or less

Institutions are required to collect

and report only those commercial

loans that are included in “loans to

small business,” as defined in the

instructions for preparation of the

Consolidated Report of Condition

and Income (Schedule RC-C,

part II, of the Consolidated Report of

Condition and Income (Call Report)

or Schedule SB of the Thrift

Financial Report (TFR), as

applicable).

“It is the original amount of a

loan, not the annual revenue

of a business or farm, that

determines the classification

of a loan as a small-business

or small-farm loan.”

Small-business loans are defined as

those whose original amounts are $1

million or less and that were reported

on the institution’s Call Report or

TFR as either “Loans secured by

nonfarm or nonresidential real

estate” or “Commercial and industrial

loans.” Small-farm loans are defined

as those whose original amounts

are $500,000 or less and were

reported as either “Loans to finance

agricultural production and other

loans to farmers” or “Loans secured

by farmland.”

The location of a small-business or

small-farm loan must be maintained

by census tract or block numbering

area. In addition, supplemental

information contained in the file

specifications includes a date

associated with the origination or

purchase and whether the loan was

originated or purchased by an

affiliate.

It is the original amount of a loan,

not

the annual revenue

of a business or

farm, that determines the

classification of a loan as a small-

business or small-farm loan. The

sections of the Call Report and

TFR relating to small-business

and small-farm loans are included

in this guide as Appendices B

and C.

Aggregate Reporting

An institution subject to data

reporting requirements must report

the aggregate number and amount of

loans for each geography in which it

originated or purchased a small-

business or small-farm loan. Loans

to businesses and farms are

reported by origination amounts of

·$100,000 or less,

·more than $100,000 but less than

or equal to $250,000, and

·more than $250,000.

Institutions must also report loans to

businesses and farms with gross

annual revenues of $1 million or

less, using the revenues that the

institution considered in making its

credit decisions.

Original Amount

vs. Purchase Amount

When collecting and reporting

information on purchased small-

business and small-farm loans, an

institution collects and reports the

amount of the loan at origination,

not at the time of purchase. This is

consistent with the Call Report and

TFR guidelines, which use the

“original amount of the loan” to

determine (1) whether a loan should

be reported as a “loan to a small

business” or a “loan to a small farm”

and (2) in which loan-size category a

loan should be reported. When

assessing the volume of small-

business and small-farm loan

purchases for purposes of evaluating

lending-test performance under

CRA, however, examiners will

evaluate an institution’s activity

based on the amounts at purchase.

Refinances and Renewals

Data collected in 2000 and reported

in 2001.

An institution collects and

reports information about

refinancings but does not collect and

report information about renewals. A

refinancing typically involves the

satisfaction of an existing obligation

that is replaced by a new obligation

undertaken by the same borrower.

When an institution refinances a

loan, it is considered a new

origination, and loan data should be

collected and reported, if otherwise

required. Consistent with HMDA,

however, if under the original loan

agreement the institution is

unconditionally obligated to refinance

the loan subject to conditions within

the borrower’s control, the institution

should not report these events as

originations.

For purposes of CRA data collection

and reporting requirements, the

Collecting the Data

A Guide to CRA Data Collection and Reporting 12

extension of the maturity of an

existing loan is a renewal and is not

considered a loan origination.

Therefore, institutions should not

collect and report data on loan

renewals.

Data collected in 2001 and

subsequent years.

An institution

should collect information about

small-business and small-farm loans

that it refinances or renews as loan

originations. (A refinancing generally

occurs when the existing loan

obligation or note is satisfied and a

new note is written, while a renewal

is an extension of the term of a loan.

However, for purposes of small-

business and small-farm CRA data

collection and reporting, it is no

longer necessary to distinguish

between the two.) When reporting

small-business and small-farm data,

however, an institution may report

only one origination (including a

renewal or refinancing treated as an

origination) per loan per year, unless

an increase in the loan amount is

granted.

If an institution increases the

amount of a small-business or

small-farm loan when it extends the

term of the loan, it should always

report the amount of the increase as

a small-business or small-farm loan

origination. The institution should

report only the amount of the

increase if the original or remaining

amount of the loan has already

been reported one time that year.

For example, a financial institution

makes a term loan for $25,000;

principal payments have resulted in

a present outstanding balance of

$15,000. In the next year, the

customer requests an additional

$5,000, which is approved, and a

new note is written for $20,000. In

this example, the institution should

report both the $5,000 increase and

the renewal or refinancing of the

$15,000 as originations for that year.

However, the institution may report

the $5,000 increase together with

the renewal or refinancing of the

$15,000 as one origination for that

year.

Lines of Credit

Institutions must collect and report

data on lines of credit in the same

way that they provide data on loan

originations. Lines of credit are

considered originated at the time the

line is approved or increased; and

an increase is considered a new

origination.

Generally, the full amount of the

credit line is the amount that is

considered originated. In the case of

an increase to an existing line, the

amount of the increase is the

amount that is considered originated

and that amount should be reported.

For renewals of line of credit, the

rules are as follows:

Data collected in 2000 and reported

in 2001.

Like loan renewals,

renewals of lines of credit are not

considered loan originations and

should not be collected or reported.

Data collected in 2001 and subse-

quent years.

Renewals of lines of

credit for small-business, small-farm,

or consumer purposes should be

collected and reported, if appli-

cable, in the same manner as

renewals of small-business or small-

farm loans (see Q&A __.42(a)–5).

Institutions that are HMDA reporters

continue to collect and report home

equity lines of credit at their option,

in accordance with the requirements

of 12 CFR part 203.

Loans to Fisheries

and Forestries

Instructions for part I of the Call

Report and Schedule SB of the

TFR include loans “made for the

purpose of financing fisheries and

forestries, including loans to

commercial fishermen” as a

component of the definition of

“Loans to finance agricultural

production and other loans to

farmers.” Part II of Schedule RC-C

of the Call Report and Schedule

SB of the TFR, which serve as the

basis of the definition for small-

business and small-farm loans in the

regulation, capture both “Loans to

finance agricultural production and

other loans to farmers” and “Loans

secured by farmland.” These loans

are reported as small-business or

small-farm loans.

Home Equity Lines

of Credit Used Predominantly

for Small-Business Purposes

Institutions that have chosen to

report home equity lines of credit

under HMDA report only the portion

of a home equity line used for

home improvement purposes. That

portion of the loan would then be

consid-ered when examiners

evaluate home mortgage lending. If

the line meets the regulatory

definition of a “community

development loan,” the institution

should collect and report information

on the entire line as a community

development loan. If the line does

not qualify as a community

development loan, the institution

has the option of collecting and

maintaining (but not reporting) the

entire line of credit as “Other

secured lines/loans for purposes of

small business.”

Collecting the Data

A Guide to CRA Data Collection and Reporting 13

Credit Cards Issued

to Small Businesses

If an institution agrees to issue credit

cards to a business’s employees,

the institution reports all of the credit

card lines opened on a particular

date for that single business as one

small-business loan origination

rather than reporting each individual

credit card line, assuming the

criteria in the small-business loan

definition in the regulation are met.

The credit card program’s amount at

origination is the sum of all of the

employee/business credit cards’

credit limits opened on a particular

date. If subsequently issued credit

cards increase the small-business

credit line, the added amount is

reported as a new origination.

Lending Outside the United States

An institution may collect data about

small-business and small-farm loans

located outside the United States;

however, it cannot report these data

because the FFIEC CRA data

collection software will not accept

data concerning loan locations

outside the United States.

Multiple Loan Originations

to the Same Business

If an institution originates multiple

loans to the same business, the

loans should be collected and

reported as separate originations

rather than combined and reported

as they are on the Call Report or

TFR, which reflect loans outstanding,

rather than originations. However, if

institutions originate multiple loans to

the same business solely to

artificially inflate the number or

volume of loans evaluated for CRA

lending performance, the agencies

may combine these loans for

purposes of evaluation under the

CRA.

Gross Annual Revenues

The regulations do not require

institutions to request or consider

revenue information when making a

loan; however, if institutions do

gather this information from their

borrowers, they should collect and

report the gross annual revenue,

rather than the adjusted gross

annual revenue, of their small-

business or small-farm borrowers.

The purpose of small-business and

small-farm data collection is to

enable examiners and the public to

judge whether the institution is

lending to small businesses and

farms or whether it is only making

small loans to larger businesses and

farms.

The CRA regulations similarly do

not require institutions to verify

revenue amounts; thus, institutions

may rely on the gross annual

revenue amount provided by

borrowers in the ordinary course of

business. If an institution does not

collect gross annual revenue

information for its small-business

and small-farm borrowers, it would

not indicate on the CRA data

collection software that the gross

annual revenues of the borrower are

$1 million or less. The institution

should enter the code indicating

“revenues not known” on the

individual loan portion of the data

collection software or on an

internally developed system.

Generally, an institution should rely

on the revenues that it considered in

making its credit decision when

indicating whether a small-business

or small-farm borrower had gross

annual revenues of $1 million or less.

For example, in the case of affiliated

businesses, such as a parent

corporation and its subsidiary, if the

institution considered the revenues

of the entity’s parent or a subsidiary

corporation of the parent as well,

then the institution would aggregate

the revenues of both corporations to

determine whether the revenues are

$1 million or less. Alternatively, if the

institution considered the revenues

of only the entity to which the loan is

actually extended, the institution

should rely solely upon whether

gross annual revenues are above or

below $1 million for that entity.

However, if the institution considered

and relied on revenues or income of

a cosigner or guarantor that is not an

affiliate of the borrower, such as a

sole proprietor, it should not adjust

the borrower’s revenues for

reporting purposes.

For a start-up business, the

institution should use the actual

gross annual revenue to date

(including $0 if a new business has

had no revenue to date). Although

start-up businesses will provide the

institution with pro forma projected

revenue figures, these figures may

not accurately reflect actual gross

revenue.

Loan Location

Prudent banking practices dictate

that an institution know the location

of its customers and loan collateral.

Therefore, institutions typically will

know the actual location of their

borrowers or loan collateral beyond

an address consisting only of a post

office box.

Many borrowers have street

addresses in addition to post office

box numbers or rural route and box

numbers. Institutions should ask

their borrowers to provide the street

address of the main business facility

or farm or the location where the

loan proceeds otherwise will be

applied. Moreover, in many cases in

Collecting the Data

A Guide to CRA Data Collection and Reporting 14

which the borrower’s address

consists only of a rural route number

or post office box, the institution

knows the location (i.e., the census

tract or block numbering area) of the

borrower or loan collateral. Once the

institution has this information, it

should assign a census tract or

block numbering area to that

location (geocode) and report that

information as required under the

regulations.

For loans originated or purchased in

1998 or later, if the institution cannot

determine the borrower’s street

address, and does not know the

census tract or block numbering area

it should report the borrower’s state,

county, MSA, if applicable, and “NA,”

for “not available,” in lieu of a census

tract or block numbering area code.

Other Loan Data

Schedule RC-C, part II, of the Call

Report and Schedule SB of the

TFR do not allow financial

institutions to report loans for

commercial and industrial purposes

that are secured by residential real

estate. Loans extended to small

businesses with gross annual

revenues of $1 million or less may,

however, be secured by residential

real estate. If these loans promote

community development, as defined

in the regulations, the institution

should collect and report information

about these loans as community

development loans. Otherwise, at an

institution’s option, it may collect and

maintain data concerning loans,

purchases, and lines of credit

extended to small businesses and

secured by residential real estate for

consideration in the CRA evaluation

of its small-business lending.

To facilitate this optional data

collection, the software distributed

institution that chooses to collect

and maintain information on

consumer loans collects the gross

annual income of all primary

obligors for consumer loans, to the

extent that the institution considered

the income of the obligors when

making the decision to extend credit.

Primary obligors include co-

applicants and co-borrowers,

including cosigners. An institution

does not, however, collect the

income of guarantors on consumer

loans, because guarantors are only

secondarily liable for the debt.

If consumer lending constitutes a

substantial majority of an institu-

tion’s business, its supervisory

agency will evaluate the institution’s

consumer lending in one or more of

the following categories: motor

vehicle, credit card, home-equity,

other secured, and other unsecured

loans. In addition, at an institution’s

option, its supervisory agency will

evaluate one or more categories of

consumer lending, if the institution

has collected and maintained, as

required in section __.42(c)(1), the

data for each category that the

institution elects to have its

supervisory agency evaluate.

Where an institution collects data for

loans in a certain category, it must

collect data for all loans originated

or purchased within that category.

The institution must maintain these

data separately for each category

for which it chooses to collect data.

The data collected and maintained

should include for each loan:

·a unique number or alphanumeric

symbol that can be used to identify

the relevant loan file;

·the loan amount at origination or

purchase;

·the loan location; and

·the gross annual income of the

free of charge by the FFIEC

provides that an institution may

collect this information to

supplement its small-business

lending data by choosing the loan

type “Other secured lines/loans for

purposes of small business,” in the

individual loan data. (The title of the

loan type, “Other secured lines of

credit for purposes of small

business,” which was found in the

instructions accompanying the 1996

data collection software, has been

changed to “Other secured lines/

loans for purposes of small

business” in order to accurately

reflect that lines of credit and loans

may be reported under this loan

type.) This information should be

maintained at the institution but

should not be submitted for central

reporting purposes.

Loan Commitments

and Letters of Credit

Institutions are not required to

collect data on loan commitments

and letters of credit. They may,

however, provide for examiner

consideration information on letters

of credit and commitments.

Commercial

and Consumer Leases

Commercial and consumer leases

are not considered small-business

or small-farm loans or consumer

loans for purposes of the data

collection requirements for

commercial or consumer loans.

However, if an institution wishes to

collect and maintain data about

leases, it may provide these data to

examiners as “other loan data.”

Consumer Loans

There are no data reporting require-

ments for consumer loans. An

Collecting the Data

A Guide to CRA Data Collection and Reporting 15

borrower that the institution

considered in making its credit

decision.

Generally, guidance concerning

collection of data on small-business

and small-farm loans—including, for

example, guidance regarding

collecting loan location data and

data in connection with refinanced

or renewed loans—will also apply to

consumer loans.

Borrower Income

The CRA does not require

institutions to request or consider

income information when making a

loan. If an institution does not

consider income when making an

underwriting decision in connection

with a consumer loan, the institution

does not need to collect income

information. On the other hand, if

institutions gather this information

from their borrowers, the agencies

expect them to collect the borrowers’

gross annual income for purposes of

CRA.

Further, if the institution routinely

collects, but does not verify, a

borrower’s income when making a

credit decision, it need not verify the

income for purposes of data

maintenance. Institutions may rely

on the gross annual income amount

provided by borrowers in the

ordinary course of business.

The purpose of collecting income

data on consumer loans is to enable

examiners to determine the

distribution based on borrower

characteristics, including the

number and amount of consumer

loans to low-, moderate-, middle-,

and upper-income borrowers, as

determined on the basis of gross

annual income, particularly in the

institution’s assessment area(s).

An institution can list “0” in the

income field on consumer loans

made to its employees when

collecting data for CRA purposes, as

the institution would be permitted to

do under HMDA.

A Guide to CRA Data Collection and Reporting 16

Reporting

the Data

Reporting Tools

FFIEC Data Entry Software

The CRA Data Entry software is

provided free of charge by the

FFIEC to help financial institutions

automate the filing of their CRA

data. The software includes editing

and reporting features to help verify,

complete, and analyze data. Data

created using this package can be

easily exported onto a diskette and

mailed or transmitted by e-mail to

the Board.

Any institution that is interested in

receiving a copy of the software

may:

·send a written request to

Federal Reserve Board

Attn: CRA Processing

1709 New York Avenue, 5th Floor

Washington, DC 20006

or

·send an e-mail request to

crahelp@frb.gov

or

·leave a voice-mail request on the

CRA Assistance Line at

(202) 872-7584.

Please be sure to include a contact

name, mailing address, and a phone

number where you may be reached.

The geocoding utility is included in

this software; the use of this utility by

an institution is optional. If you wish

to use it, your institution will be

required to purchase the

geographical data, which is

available only on CD-ROM from PCi

Services, Inc. (PCi), of Boston,

Massachusetts. A PCi Services

order form can be downloaded from

the FFIEC’s CRA website at

www.ffiec.gov/cra/softinfo.htm.

The FFIEC also has an Internet site

that allows users to retrieve MSA,

state, county, and census tract/BNA

codes for street addresses. In

addition, some demographic

information (mainly population and

income) can be obtained for a

particular census tract/BNA. The

Internet address is

www.ffiec.gov/geocode.

Sources of Geographic

Information

The following sources may help you

report geographic data accurately.

Information about

MSA Boundaries

You can obtain information on

current and historical MSA

boundaries at www.census.gov by

selecting Subjects A–Z, then M,

then Metropolitan Areas, then

Metropolitan Definitions.

CRA uses the term MSA—

metropolitan statistical area—for

MSAs, CMSAs (consolidated

metropolitan statistical areas), and

PMSAs (primary metropolitan

statistical areas). MSAs, CMSAs,

and PMSAs are components of

metropolitan areas, or MAs. The

Office of Management and Budget,

which defines their geographic

boundaries, and the Census Bureau

refer to the generic term MA.

To determine MSA boundaries for

future years, you may need to obtain

FIPS PUB 8-5, Metropolitan

Statistical Areas. Contact:

National Technical Information

Services

U.S. Department of Commerce

Port Royal Road

Springfield, VA 22161

(703) 487-4650

A list of all valid census tract

numbers (and BNA designations) in

each MSA is available for a fee from

the Board’s HMDA Assistance Line

Reporting the Data

A Guide to CRA Data Collection and Reporting 17

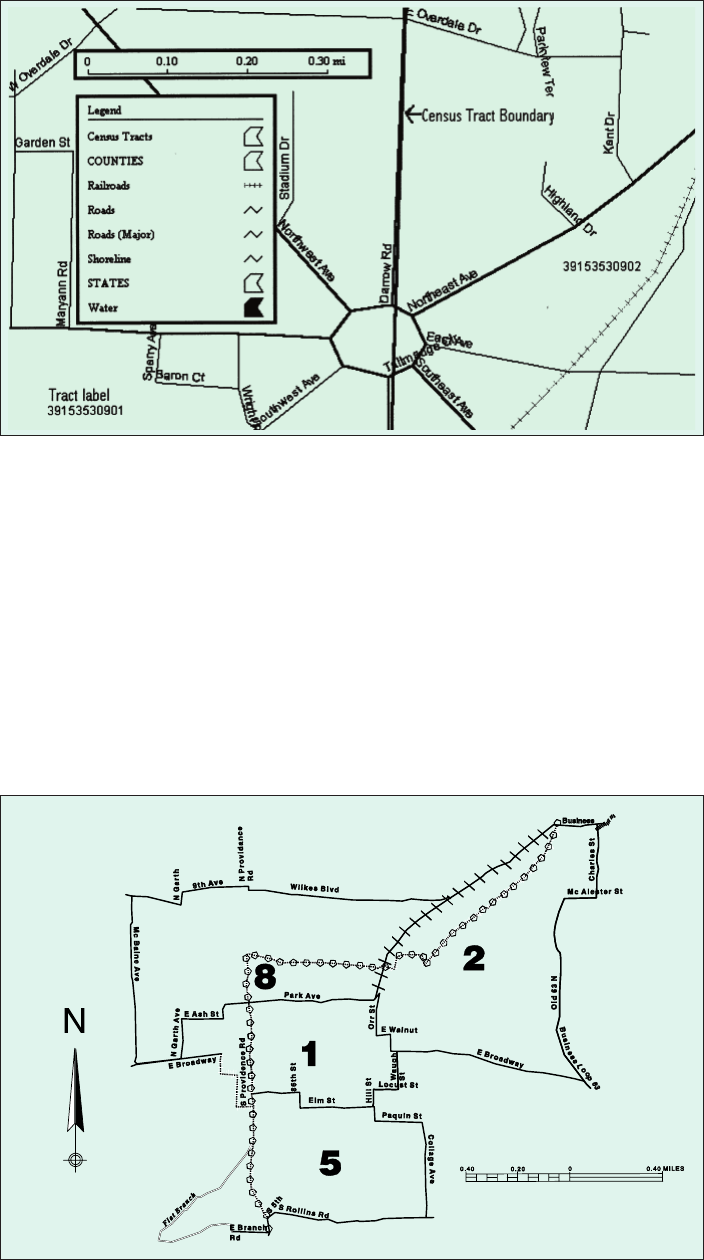

Illustration 1: LandView®III

Illustration 2: 1990 Census Tract Outline Map

at (202) 452-2016. The list will help

ensure that you are using only valid

census tract numbers; however, the

list is not a tool for geocoding your

CRA data.

The FFIEC Census Data CD-ROM

also contains census tract number

information as well as other

informative census and demographic

data. To order this software, contact

the HMDA Assistance Line at (202)

452-2016.

Census Bureau Products

The following products for deter-

mining the correct 1990 census tract

number for a given property are

available from the Census Bureau.

LandView III

LandView III is Census Bureau CD-

ROM desktop mapping software

product. It runs on Windows® 3.1,

Windows 95, Windows 98, Windows

2000, and Macintosh operating

systems. LandView III shows a

detailed network of roads

(containing address information

where available), rivers, and

railroads, along with jurisdictional

and statistical boundaries (including

census tracts). The information is

based upon the Census Bureau’s

TIGER/Line 1995 files, which reflect

the street network and address

ranges known to the Census Bureau

as of the fall of 1995. Besides

producing custom map views that

display selected user-specified map

information (see Illustration 1),

LandView also provides the

capability of displaying the FIPS

state and county codes, census tract

or block numbering area codes, and

block group codes for any location

that a user points to on the map.

This product can be ordered from

the Census Bureau Customer

Service Center.

Ordering information and a fully

functional copy of the software with

a single county’s map and data (you

can specify the county) can be

downloaded from the Census

Bureau’s website at

www.census.gov/geo/www/tiger.

Census Tract/Block Numbering Area

Outline Maps

If you prefer paper maps, you may

use the 1990 Census Tract/Block

Numbering Area Outline Maps for

the counties within the MSAs for

which you are reporting (see

Reporting the Data

A Guide to CRA Data Collection and Reporting 18

Illustration 2). Besides showing

numbers for census tracts (and

BNAs) within a particular county,

these maps display the boundaries

and names of the features used as

census tract boundaries and the

names of any counties or other

subdivisions.

The outline maps are sold by the

Census Bureau’s Customer

Services Center in county packages.

On average, there are four map

sheets per metropolitan county. The

map sheets are oversized—gener-

ally 36 by 42 inches—and map

scales vary to minimize the number

of map sheets. Maps may include

one or more insets of densely settled

areas.

The outline maps do not show

streets, street names, or address

ranges within a census tract. You will

therefore need to use the maps in

combination with up-to-date local

street maps available in your local

market, and to use a marker pen to

highlight on the street map the

boundaries of each census tract

according to the outline map.

TIGER/Census Tract Street Index®

Use the TIGER/Census Tract Street

Index (TIGER/CTSI) for the county

in which the property is located

(Illustration 3).

The TIGER/CTSI enables you to

determine the census tract numbers

for properties that use city-style

street addresses. It is arranged by

county within each MSA. The

TIGER/CTSI provides the street

name, including prefix or suffix

direction (such as “north”) and street

type (such as “street” or “avenue”),

address range, and corresponding

census tract number. Within a

county, numbered streets (for

example, 9th, 10th) precede the

streets listed alphabetically.

The TIGER/CTSI shows the census

tract number for each side of the

street and, where applicable,

provides the county subdivision

(town, township) and place codes for

each street and address range. The

latter may be helpful in determining

the census tract number when

streets with identical names and

address ranges are located in

different parts of the county. (County

subdivision and place codes and

their corresponding names are listed

in the back of TIGER/CTSI.) This

product is now available on

CD-ROM.

The TIGER/CTSI Version 2 has

certain limitations:

·Address-range and street

information are current through

April 1990. This means that

addresses or streets added since

that time are not shown.

·The index does not contain

address-range information for

areas with rural-type addresses

(such as RFD addresses).

The Census Bureau is currently

preparing the TIGER/CTSI Version 3

products for public release. These

products will reflect the street

network and address ranges known

to the Census Bureau as of summer

of 1997. Check the Census TIGER

page, www.census.gov/geo/www/

tiger, for the current status.

A special HMDA order form available

from the Bureau of the Census tells

you how to obtain the TIGER/CTSI

for selected counties. To obtain the

HMDA order form for the TIGER/

CTSI, the outline maps, and

LandView III, contact:

Customer Services Center

Bureau of the Census

Washington, DC 20233

(301) 457-4100

To obtain detailed information about

geographic products:

Geography Division—

Products and Services Staff

Bureau of the Census

Washington, DC 20233

(301) 457-1128

tiger@census.gov

You also may contact the Census

Bureau regional office serving your

state as listed in appendix D of this

guide. The costs of the census

materials will vary, depending on the

size of the county.

Illustration 3: 1990 TIGER/Census Tract Street Index®

TIGER/Census Tract Street Index

®

—Ver. 2, Part A Fairfax County, VA

From To Street Tract or ZIP 103rd FIPS

Street Name Address Address Side BNA Code Area Name Cong. Code

Barkley Dr 3100 3699 Both 4401.98 22031 Mantua CDP 11 49144

Bark Tree Ct 8285 8367 Odd 4924 22153 Lorton CDP 08 47064

Bark Tree Ct 8300 8354 Even 4924 22153 Lorton CDP 08 47064

Barkwood Ct 9500 9599 Both 4405 22032 11

Barley Rd 3100 3199 Both 4619.98 22031 Oakton CDP 11 58472

Barley Wk 7400 7416 Both 4502 22042 Jefferson CDP 11 40584

Barlow Rd 900 948 Both 4162 22060 Fort Belvoir CDP 08 29008

Barnack Dr 6700 7021 Both 4314 22152 West Springfield CDP 08 84976

Barnacle Pl 7000 7009 Both 4324 22015 Burke CDP 11 11464

Barnard Ct 3100 3150 Both 4617.98 22031 Merrifield CDP 11 51192

Barnesdale Path 6300 6536 Even 4911 22020 10

Barnesdale Path 6301 6533 Odd 4911 22022 10

Barnesville Rd 13704 13910 Even 4825 22070 10

Barney Rd 3800 3843 Both 4901 22021 10

Barnsbury Ct 9900 9939 Both 4619.98 22031 Oakton CDP 11 58472

Reporting the Data

A Guide to CRA Data Collection and Reporting 19

The Census Bureau is not able to

assist in preparing data to meet

CRA requirements or in determining

the appropriate census tract

numbers for individual addresses.

Geographic information is available

from the FFIEC’s website at

www.ffiec.gov/geocode.

Internet Resources

The Census Bureau offers a

subscription service that allows

users on-line access to information

contained in TIGER/CTSI. Institu-

tions that have an occasional need

to determine tract numbers in parts

of the country other than where they

primarily do business might be

interested in using this service.

To access this Internet site, enter

www.census.gov and select

CenStats Censtore, then

CenStats, then test drive. The test

drive page gives basic information

about the service and has links to

detailed descriptions of TIGER/CTSI

Version 2. The link at the top of each

page gives a sample of the informa-

tion you can expect.

To obtain more detailed

demographic information on the

Internet, you can access census

data through the FFIEC’s website at

http://www.ffiec.gov/webcensus/

ffieccensus.htm.

Data Automation

Cycle

Data must be submitted to the

Board, designated processor for all

the agencies, no later than March 1.

Data submissions should be mailed

to:

Federal Reserve Board

Attn: CRA Processing

1709 New York Avenue, 5th Floor

Washington, DC 20006

Data submitted via e-mail should be

encrypted using the FFIEC’s

Internet Submission Software, which

accompanies the FFIEC’s Data

Entry Software and sent to

crasub@frb.gov.

After an institution’s data have been

received and loaded, the data are

run through a batch process to

check for any errors or discrep-

ancies. The data automation cycle

has three steps that all reporting

institutions must complete for

successful CRA data submission.

These steps, described below, are

edit report review, institution register

summary confirmation, and data

resubmission.

Edit Report Review

The edit report gives an institution

an opportunity to verify submitted

statistics and provides the institution

with a listing of errors that were

discovered during the editing cycle.

Illustration 4 is an example of an edit

report with errors. Because CRA

submissions are electronically

based, the institution that submitted

these data would have to correct its

errors and send a complete

resubmission. The resubmission

replaces the institution’s previous

submission.

Institution Register

Summary (IRS)

Confirmation

If an institution provides an error-

free submission, it will receive an

IRS (see Illustration 5). The IRS is

used as a final confirmation of the

data that have been sent. The

institution’s CRA officer or individual

responsible for submitting CRA data

must sign the form included with the

IRS and fax it to the Board at (202)

530-6234.

Data Resubmission

Resubmissions are prepared by an

institution if the institution identifies

errors or needs to make changes to

data that have already been

submitted. If the resubmission is

made after the CRA data have been

aggregated and made publicly

available, the institution must send a

complete resubmission, and should

state that it is a “complete

resubmission.” After the receipt of

the resubmission, new edit or IRS

reports will be distributed.

Automatic Faxback

System

The CRA data process includes an

automatic faxback feature to make

transmission of correspondence

simpler and to reduce paper usage.

The faxback system uses the fax

number provided by the institution

on its transmittal sheet to send the

edit reports, institution register

summary, and any other

correspondence.

Reporting the Data

A Guide to CRA Data Collection and Reporting 20

20XX COMMUNITY REINVESTMENT ACT (CRA) Rundate: 01/28/20XX

EDIT REPORT Runtime: 20:00:08

Agency: 1-OCC Region: 2 Respondent ID: 0000063903 Page: 1

CRA COMPLIANCE BANK Contact: JOHN DOE REPORTER Phone: XXX-XXX-XXXX

100 MAIN STREET Fax: XXX-XXX-XXXX

ANYWHERE USA 80260-0000 Tax ID: XX-XXXXXXX

SMALL BUSINESS LOANS - 4

Number Loans/Total Loan Amount (000s)

Revenues Affiliate

MSA/ST/CTY/TR-BNA <= $100K $100K to $250K > $250K <= $1M Loans

0480/37/021/0200.00 Originated: 000001/00000006 000000/00000000 000000/00000000 000001/00000006 /

Purchased: 000000/00000000 000000/00000000 000000/00000000 000000/00000000 /

Total(O+P): 000001/00000006 000000/00000000

ERROR(S):

V320 Census Tract-BNA missing or does not = a valid census tract-BNA for the MSA/state/county combo

0480/37/021/0500.00 Originated: 000001/00000017 000000/00000000 000000/00000000 000001/00000017 /

Purchased: 000000/00000000 000000/00000000 000000/00000000 000000/00000000 /

Total(O+P): 000001/00000017 000000/00000000

ERROR(S):

V320 Census Tract-BNA missing or does not = a valid census tract-BNA for the MSA/state/county combo

1520/37/119/0000.00 Originated: 000001/00000015 000000/00000000 000000/00000000 000000/00000000 /

Purchased: 000000/00000000 000000/00000000 000000/00000000 000000/00000000 /

Total(O+P): 000000/00000000 000000/00000000

ERROR(S):

V320 Census Tract-BNA missing or does not = a valid census tract-BNA for the MSA/state/county combo

1520/37/190/0060.01 Originated: 000001/00000028 000000/00000000 000000/00000000 000001/00000028 /

Purchased: 000000/00000000 000000/00000000 000000/00000000 000000/00000000 /

Total(O+P): 000001/00000028 000000/00000000

ERROR(S):

V310 County is missing or state/county does not equal a valid combination

Illustration 4: Edit report with errors

Reporting the Data

A Guide to CRA Data Collection and Reporting 21

Illustration 5: Institution Register Summary

20XX COMMUNITY REINVESTMENT ACT (CRA) Rundate: 03/18/20XX

INSTITUTION REGISTER SUMMARY (IRS) Runtime: 20:01:17

Agency: 2-FRB Region: 5 Respondent ID: 0000891276 Page: 1

FIRST NATIONAL COMPLIANCE Contact: JENNY REGULATOR Phone: XXX-XXX-XXXX

106 S. LAFAYETTE STREET Fax: XXX-XXX-XXXX

SOMEWHERE USA 14587 Tax ID: XX-XXXXXXX

________________________________________________________________________________________________________________________

Small Business Small Farm Community Consortium/

Loans Loans Dev. Loans Third Party

# of Tracts/BNAs with Loans 29 12

Total # of Loans on File 596 29 3 0

Total Loan Amounts on File (000s) 31640 925 56480 0

Total # of Originated Loans on File 596 29

Total Originated Ln Amounts on File (000s) 31640 925

Total # of Affiliate Loans on File 0 0 0

Total Affiliate Ln Amounts on File (000s) 0 0 0

Small Business or Farm Loans

Loans with <= $1 Million in Revenues

Number 287 11

Total Loan Amount (000s) 11651 149

Small Business or Farm Loans <= $100K

Number 522 27

Total Loan Amount (000s) 11550 687

Small Bus. or Farm Lns > $100K To $250K

Number 44 2

Total Loan Amount (000s) 7284 238

Small Business or Farm Loans > $250K

Number 30 0

Total Loan Amount (000s) 12806 0

________________________________________________________________________________________________________________________

ASSESSMENT AREA

Total Number of Assessment Areas 1

Total MSAs in All Assessment Areas 0

Total non-MSA areas by state in All Assessment Areas 1

Total COUNTIES in All Assessment Areas 1

Total TRACTS-BNAS in All Assessment Areas 15

20XX COMMUNITY REINVESTMENT ACT (CRA) Rundate: 03/18/20XX

INSTITUTION REGISTER SUMMARY (IRS) Runtime: 20:01:17

Agency: 2-FRB Region: 5 Respondent ID: 0000891276 Page: 2

FIRST NATIONAL COMPLIANCE Contact: JENNY REGULATOR Phone: XXX-XXX-XXXX

________________________________________________________________________________________________________________________

To ensure that your individual disclosure statement and the aggregate

reports, represent accurate data, the statistics on the enclosed report(s)

should be verified with your institutions records.

To satisfy these requirements, please complete ONE of the following two steps:

1. If you agree with the statistics given on the Institution Register Summary,

please complete the following section.

I have verified the accuracy of the statistics with our records and found

them to be in agreement.

____________________________________ ____________________________________

Signature Date

2. If there are any discrepancies in the statistics, please fax the

corrections to (202) 530-6234. An analyst will be in contact with

you in order to resolve these discrepancies. However, if discrepancies are

known, a corrected file should be sent to the address listed below:

ATTN: CRA Processing

Federal Reserve Board

1709 New York Avenue, NW

Fifth Floor

Washington, D.C. 20006

Thank you for your prompt attention in this matter.

The Institution Register

Summary (IRS) is used by

each reporting institution to

verify and confirm CRA

statistics.

Reporting the Data

A Guide to CRA Data Collection and Reporting 22

Public Availability

of Data

Disclosure Statements

Institutions that are required to make

annual public disclosure of their

small-business, small-farm, and

community development lending

activity will receive, by September

15, a CD-ROM containing the

disclosure statement for that

institution. The CRA Aggregate and

Disclosure CD-ROM contains the

disclosure statement for that

institution and reports for all other

institutions that have reported CRA

data for that year. Most large

institutions are required to keep a

CRA disclosure statement for the

two prior calendar years in their

public files.

If a large institution (except one that

was small in the prior calendar year)

has elected to have one or more

categories of its consumer loans

considered under the lending test, it

must also make available for each

category, for the prior two calendar

years, the number and amount of

loans:

·to low-, moderate-, middle-, and

upper-income individuals;

·located in low-, moderate-,

middle-, and upper-income census

tracts; and

·located inside and outside the

institution’s assessment area(s).

Aggregate Tables

The CRA Aggregate and Disclosure

CD-ROM provides access to

aggregate tables covering the

lending activity of all institutions

subject to CRA for each MSA and

non-MSA portion of each state as

well as national aggregate tables

covering the lending activity of all

institutions nationwide.

Aggregate and Disclosure

CD-Rom Provided

by the FFIEC

in the Public File

Rather than printing a hard copy of

the CRA disclosure statement, an

institution may retain a copy of the

FFIEC compact disc in its public file.

When a consumer requests an

institution’s public file, the institution

must be able to print its CRA

disclosure statement readily from

either the compact disc or a

duplicate of the compact disc.

If the request is at a branch other

than the main office or the

designated branch office in each

state that holds the complete public

file, the institution should provide the

CRA disclosure statement on paper,

or in another format acceptable to

the requestor, within five calendar

days.

Aggregate

and Disclosure

on the Internet

The CRA aggregate and disclosure

data can be found on the Internet at

www.ffiec.gov/webcraad/

craaggr.htm.

A Guide to CRA Data Collection and Reporting 23

Glossary Affiliate. Any company that controls,

is controlled by, or is under common

control with another company. The

term “control” has the meaning given

to that term in 12 U.S.C. 1841(a)(2),

and a company is under common

control with another company if both

companies are directly or indirectly

controlled by the same company.

Area median income.

·The median family income for the

MSA, if a person or geography is

located in an MSA or

·the statewide nonmetropolitan

median family income, if a person

or geography is located outside an

MSA.

Assessment area(s). One or more

geographic area(s) delineated by an

institution and (if delineated in

compliance with the regulation) used

by the regulatory agency in

evaluating the institution’s record of

helping to meet the credit needs of

its community. The assessment

area(s) for an institution other than a

wholesale or limited-purpose

institution must:

·consist generally of one or more

MSAs (using the MSA boundaries

that were in effect as of January 1

of the calendar year in which the

delineation is made) or one or

more contiguous political

subdivisions, such as counties,

cities, or towns; and

·include the geographies in which

the bank has its main office, its

branches, and its deposit-taking

ATMs, as well as the surrounding

geographies in which the bank has

originated or purchased a

substantial portion of its loans

(including home mortgage loans,

small-business and small-farm

loans, and any other loans the

bank chooses, such as those

consumer loans on which the

bank elects to have its

performance assessed).

An assessment area(s) must consist

only of whole geographies, may not

reflect illegal discrimination, may not

arbitrarily exclude low- or moderate-

income geographies, taking into

account the institution’s size and

financial condition, and may not

extend substantially beyond a CMSA

boundary or beyond a state

boundary unless the assessment

area(s) is located in a multistate

MSA. An institution may adjust the

boundaries of its assessment area(s)

to include only the portion of a

political subdivision that it

reasonably can be expected to

serve.

Automated teller machine (ATM).

An automated, unstaffed banking

facility owned or operated by, or

operated exclusively for, the bank at

which deposits are received, cash

dispersed, or money lent.

Block numbering area (BNA). The

Bureau of Census, in conjunction

with state agencies, has established

BNAs as statistical subdivisions of

counties in which census tracts have

not been established. BNAs are

generally identified in census data

by numbers in the range 9501 to

9989.99. (For purposes of the CRA,

an institution may use BNA or

Census Tracts, as both are

“geographies”).

Branch. A staffed banking facility

authorized as a branch, whether

shared or unshared, including, for

example, a minibranch in a grocery

store or a branch operated in

conjunction with any other local

business or nonprofit organization.

Glossary