Publication D55

User Manual: D55

Open the PDF directly: View PDF ![]() .

.

Page Count: 116 [warning: Documents this large are best viewed by clicking the View PDF Link!]

- The role of central bank money in payment systems

- Foreword

- Table of Contents

- Executive summary and introduction

- 1.The coexistence of central and commercial bank money in payment systems

- 2.Influences on payment systems and their impact

- 3.Current central bank policies

- 4.Possible implications for central bank policy

- 5.Concluding remarks

- Annexes

- Annex 1 Central bank policies

- Annex 2 Access policy - specific cases

- Annex 3 Detailed tables

- Annex 4 Banknotes

- Annex 5 Members of the CPSS

- Annex 6 Members of the Working Group

Committee on Payment and

Settlement Systems

The role of central bank

money in payment systems

August 2003

Copies of publications are available from:

Bank for International Settlements

Press & Communications

CH-4002 Basel, Switzerland

E-mail: publications@bis.org

Fax: +41 61 280 9100 and +41 61 280 8100

This publication is available on the BIS website (www.bis.org).

© Bank for International Settlements 2003. All rights reserved. Brief excerpts may be reproduced

or translated provided the source is cited.

ISBN 92-9131-654-7 (print)

ISBN 92-9197-654-7 (online)

Foreword

Contemporary monetary systems are based on the mutually reinforcing roles of central bank money

and commercial bank monies. What makes a currency unique in character and distinct from other

currencies is that its different forms (central bank money and commercial bank monies) are used

interchangeably by the public in making payments, not least because they are convertible at par.

Central bank money plays a key role in payment arrangements, as it has proved safe and efficient to

have a central reference of value with which all other forms of the currency maintain this par

convertibility. This role is long-established and, for the most part, uncontroversial.

Nevertheless, as explained in this report, the role of central bank money in payment systems raises a

number of questions. Developed economies have complex and interdependent payment

arrangements in which there is a combination of competition and cooperation between the many

institutions involved. The use of central bank money is thus part of the underlying issue of the balance

between the services provided by central banks and those provided by commercial banks in the

payment system. And given the widespread and fundamental changes that have occurred over the

past decade or so, and which continue today, it is useful to consider whether an appropriate balance is

being maintained and how the composite use of both monies can best be achieved.

This report therefore looks at a range of practical policy questions. For example, which institutions

should have accounts at the central bank? What services should central banks provide to meet the

needs of account holders? When should central banks insist that payment or securities settlement

systems settle in central bank money; or - when this is not practicable - what sufficiently safe

alternatives exist to mitigate credit and liquidity risks? What are the possible benefits and risks of the

concentration of payments through a few large banks, and how might central banks approach this

issue? And to what extent can the supply of central bank money, normally confined to the area of

jurisdiction of the central bank, meet the demands of global players active in multiple currencies?

The report shows that there is much common ground among CPSS central banks in their objectives as

well as in the main tenets of their policy concerning the role of central bank money in payment

systems. These collective views and practices are presented in the form of 10 propositions. At the

same time, however, there are often differences when it comes to the implementation of policy. In

setting out both the similarities and the differences, the report is not normative but rather descriptive of

central bank policies and the motivations underlying the chosen policies. It aims to provide a useful

factual base and a strong analytical framework that will raise awareness and stimulate debate on

these key matters.

I would like to pay special tribute to a number of people who dedicated their time, talent and energy to

drafting this report. First, to Shuhei Aoki (Bank of Japan), who contributed countless hours to

coordinating this project from start to finish. Bringing the work to fruition also relied on the enthusiasm

and commitment of Robert Lindley (Bank for International Settlements/CPSS Secretariat), Masayuki

Mizuno (Bank of Japan), Travis Nesmith (Board of Governors of the Federal Reserve System), Ignacio

Terol (European Central Bank) and Alastair Wilson (Bank of England). Discussions held by the

Committee and its working group (the members of which are listed in Annex 6) provided inspiration

and numerous helpful contributions to the project.

Tommaso Padoa-Schioppa, Chairman

Committee on Payment and Settlement Systems

CPSS - The role of central bank money in payment systems - August 2003 i

Contents

Executive summary and introduction .......................................................................................................1

The coexistence of central and commercial bank monies: multiple issuers, one currency ...........1

The pivotal role of central bank money in payment systems.........................................................2

Access to central bank money .......................................................................................................3

Variations in policies ......................................................................................................................4

Current and prospective developments .........................................................................................4

Some key issues for central banks ................................................................................................5

Possible policy responses..............................................................................................................6

Conclusion......................................................................................................................................6

Structure of the report ....................................................................................................................7

1. The coexistence of central and commercial bank money in payment systems.............................7

1.1 Central bank money and central bank objectives................................................................8

1.2 How payment systems function and the role of the settlement institution...........................9

1.2.1 Simple models of how payment systems function.....................................................9

1.2.2 Risks relating to the settlement asset......................................................................11

Risks relating to the settlement institution..........................................................11

Risks between direct participants and their customers......................................12

1.3 Factors determining agents’ choice of settlement asset....................................................13

Safety .................................................................................................................................13

Liquidity and credit.............................................................................................................14

Neutrality............................................................................................................................15

Related payment services .................................................................................................15

Regulatory costs and perceived benefits...........................................................................15

1.4 Conclusion .........................................................................................................................16

2. Influences on payment systems and their impact........................................................................16

2.1 Influences on payment systems ........................................................................................16

Liberalisation......................................................................................................................17

Technological advances ....................................................................................................17

Globalisation ......................................................................................................................17

Consolidation .....................................................................................................................18

2.2 Impact on payment systems..............................................................................................18

2.2.1 The choice between direct participation and non-participation ...............................18

2.2.2 Concentrations of payment flows ............................................................................20

ii CPSS - The role of central bank money in payment systems - August 2003

2.3 Conclusion......................................................................................................................... 22

3. Current central bank policies....................................................................................................... 22

3.1 Settlement in central bank money by systems.................................................................. 22

3.2 Provision of central bank money to individual institutions................................................. 24

3.2.1 Access to accounts ................................................................................................. 26

Banks................................................................................................................. 26

Non-resident banks............................................................................................ 27

Non-banks.......................................................................................................... 28

3.2.2 Access to credit....................................................................................................... 30

3.3 The relationship between policy on systems and policy on institutions............................ 31

3.3.1 The requirement for individual institutions to settle in central bank money............ 31

3.3.2 Criteria for direct participation in systems............................................................... 32

3.4 Conclusion......................................................................................................................... 32

4. Possible implications for central bank policy............................................................................... 33

4.1 Access policy..................................................................................................................... 33

4.1.1 Relevant considerations.......................................................................................... 34

Risk.................................................................................................................... 34

Costs.................................................................................................................. 34

Neutrality............................................................................................................ 34

Other considerations.......................................................................................... 35

Alternatives ........................................................................................................ 35

4.1.2 Examples of policy reviews..................................................................................... 35

4.2 System design and central bank settlement services....................................................... 36

4.2.1 Enhancing efficiency of service .............................................................................. 37

Reducing liquidity costs at the domestic level ................................................... 37

Reducing liquidity costs at the international level.............................................. 37

Enhancing business efficiency .......................................................................... 38

4.2.2 Expanding areas of service .................................................................................... 39

Use of central bank money in ICSDs................................................................. 39

Central bank multicurrency settlement services................................................ 39

4.3 Oversight, supervision and regulation............................................................................... 40

Implications of a concentration of payment activities........................................................ 40

Relevant considerations.................................................................................................... 40

Points for further analysis.................................................................................................. 41

CPSS - The role of central bank money in payment systems - August 2003 iii

5. Concluding remarks .....................................................................................................................42

Ten propositions...........................................................................................................................42

Current challenges and the tools to respond to them ..................................................................43

Central bank policies....................................................................................................................44

Looking forward............................................................................................................................45

Annexes..................................................................................................................................................47

Annex 1 Central bank policies................................................................................................................48

Annex 2 Access policy - specific cases..................................................................................................77

Annex 3 Detailed tables .........................................................................................................................81

Annex 4 Banknotes ................................................................................................................................96

Annex 5 Members of the CPSS ...........................................................................................................107

Annex 6 Members of the Working Group.............................................................................................108

CPSS - The role of central bank money in payment systems - August 2003 1

Executive summary and introduction

Central bank money plays a key role in payment systems. This report analyses that role and looks at

how it may change as a result of current or possible future developments. It develops an analytical

framework that permits a better understanding of how central banks formulate policy in this important

area.

The coexistence of central and commercial bank monies: multiple issuers, one currency

Money is fundamental to the functioning of market economies inasmuch as these are based on

exchange and credit. In a market economy, any two economic agents are free to agree on the means

of payment to be used to settle a transaction.1 Acceptance of any form of money will, however,

depend on the receiver’s confidence that, subsequently, a third party will accept that money in trade.

Fiat money is worth nothing without the trust of a community behind it. Manifestation of this trust is

exemplified by the use of banknotes. Being intrinsically worthless pieces of paper that everyone

accepts from a stranger in exchange for valuable goods and services, banknotes testify to the

presence of certain bonds of confidence that tie together the members of a society.

Today, any widely used form of money is denominated in a given currency. By sharing a currency, the

individuals of a community have in common a measure of economic value, a means to store value,

and a set of instruments and procedures to transfer this value. However, since the value of money lies

in trust, there can be no absolute guarantee that confidence in the currency can be preserved over

time. It may be shaken by a monetary crisis or by the malfunctioning of the payment system. As a

result, maintaining trust in the currency, and thus facilitating its circulation, becomes a major public

interest. The central bank is, in most countries, the institution designated to pursue this public interest.

In pursuit of its task, the central bank issues its own liabilities for use as money (central bank money).

But the central bank is not the only issuer of money in an economy. The multiplicity both of issuers of

money and of payment mechanisms is a common feature in all developed economies. Commercial

banks are the other primary issuers, their liabilities (ie commercial bank money) representing in fact

most of the stock of money.2 A healthy, competitive commercial banking market is seen as an

essential element of an efficient and effective economy.

Thus central bank and commercial bank money coexist in a modern economy. Confidence in

commercial bank money lies in the ability of commercial banks to convert their sight liabilities into the

money of another commercial bank and/or into central bank money upon demand of their clients. In

turn, confidence in central bank money rests in the ability of the central bank to maintain the value of

the stock of currency as a whole (ie not only of the small portion it issues directly), or its inverse, to

maintain price stability.

Money therefore represents an obligation of different issuers, and consumers regularly exhibit

preferences for holding and using different forms of money, which often vary for different types of

transactions. Yet the perception of the public is such that it uses the various forms of money

interchangeably so long as they are denominated in the same currency. Two factors explain this: first,

the existence of a form of money (central bank money) which has the support of public authorities and,

second, convertibility of other monies into central bank money at par value. The combination of these

two factors gives rise to the currency’s single character, the certainty that “one dollar is one dollar”,

whatever form it takes (whether central or commercial bank money). And this “singleness” seems to

be a necessary (but by itself not sufficient) condition for a currency to effectively become “the”

measure of economic value, or the unit of account, shared by members of a modern economy, with

the associated advantages of efficiency and safety in trade.

All central banks represented in the CPSS believe that the composite of central and commercial bank

money is an essential feature of the monetary system and should be preserved. A multiplicity of

issuers of money preserves the advantages of competition in providing innovative and efficient means

1 This report analyses the concepts of money and means of payment from an economic perspective and does not try to

provide legal definitions.

2 In some economies, non-banks also issue private money in more limited amounts.

2 CPSS - The role of central bank money in payment systems - August 2003

of payment and, indeed, in providing financial services generally. The regulated or licensed character

of these issuers (commercial banks) aims at promoting their solvency and liquidity in order to preserve

confidence in the currency. And the use of central bank money in payment systems puts the value of

banks’ liabilities to the test every day by checking their convertibility into the defined unit of value.

This policy position implies a rejection of the two extreme arrangements of monobanking, where the

central bank acts as the sole issuer of money, and free banking, where commercial banks provide all

the money required by the economy. Neither of these corner solutions has proven to be sufficiently

stable or efficient to endure.

The pivotal role of central bank money in payment systems

To facilitate convertibility between different forms of money, central banks support the existence of at

least one payment system for their own currency that is widely accessible to banks. Payment systems

play a fundamental role in the economy by providing a range of mechanisms through which

transactions can be easily settled. As such, banknotes are part of this broad notion of payment

systems. In spite of the expanding role of its various substitutes, the banknote is still a fundamental

payment instrument in economic life. Yet this report focuses on a narrower concept whereby a

payment system is a defined set of instruments, procedures and rules for the transfer of funds from

one bank to another. In these systems, banks hold funds at a common agent (referred to in the report

as “settlement institution”). Payments between these banks are made by exchanging the liabilities of

this settlement institution (the “settlement asset”). Deposits at the settlement institution and the credit

of the settlement institution (when available) are both accepted as money by all the participants in the

system. “Payment systems” include payment mechanisms used by securities settlement systems

(SSSs), whether the payment mechanism is “embedded” within the SSS or external to it. This report

does not distinguish between the role central bank money plays in embedded mechanisms and in

external payment systems, and the analysis which follows is relevant to both.

In practice, most - although by no means all - payment systems settle in central bank money.3 In other

words, the settlement institution is generally the central bank. This role is consistent with the monetary

order described earlier, whereby a commercial bank honours its sight liabilities by converting them into

central bank money if their clients demand it. It also reflects the layered architecture of financial

systems, whereby private individuals and non-financial businesses hold (part of) their liquidity in

banks, and banks in turn hold (part of) their liquidity in the central bank.

The choice of settlement asset in a system - particularly in a system handling large values - is

important because of the exposures that can arise between the settlement institution and the

participants in the system and because of the crucial operational role the settlement institution plays in

the system. The widespread use of central bank money as a settlement asset reflects its overall

qualities of safety, availability, efficiency, neutrality and finality.4 Most importantly, failure of the

settlement institution can have critical systemic consequences and the use of the central bank as

settlement institution minimises the risk of this occurring. CPSS central banks’ common policy in this

area is set out in Core principles for systemically important payment systems5, (“Core Principles”)

which states that the settlement asset in systemically important systems should preferably be a claim

on the central bank or, if other assets are used, that they should carry little or no credit and liquidity

risk. A similar policy is contained in the report on Recommendations for securities settlement

systems,6 (“SSS recommendations”) which says that the assets used to settle the ultimate payment

obligations from securities transactions should carry little or no credit or liquidity risk and that, if central

bank money is not used, steps must be taken to protect members of the central securities depository

from potential losses and liquidity pressures arising from the failure of the settlement institution whose

assets are used.

3 For more information, see Annex 3, Table C.

4 These features are prominent in central bank money but none is exclusive to central bank money.

5 Core principles for systemically important payment systems, BIS, January 2001.

6 Recommendations for securities settlement systems, BIS, November 2001.

CPSS - The role of central bank money in payment systems - August 2003 3

In an era of financial globalisation, however, using the central bank as the settlement institution may

not always be practical. Global players, active in multiple currencies, are confronted with the essential

nature of the central bank as a domestic monetary authority. The supply of central bank money and

central bank services is normally confined within the area of jurisdiction of the central bank, so no

central bank alone can cater for the needs of these global players in full. Central banks can address

some of the consequences of globalisation through mutual cooperation. For example, in the

mid-1990s central banks expressed their preference for a market solution to address the need to

reduce principal risk in foreign exchange settlement.7 Continuous Linked Settlement (CLS), the

infrastructure adopted by the market, was supported by the international central banking community,

and in 2002 the first currencies were authorised by the relevant central banks for inclusion as eligible

currencies in the system. CLS Bank, a private utility which meets the international norms for risk

management laid out by the G10 Governors, is the settlement institution for CLS - ie settlement is not

in central bank money. However, all payments to and from CLS are made through the issuing central

bank, so central bank money retains a necessary role, pivotal but not central, in the settlement of

foreign exchange transactions in CLS. Similar issues arise with other systems, for example the

International Central Securities Depositories (ICSDs) Euroclear and Clearstream Luxembourg

(“Clearstream”), which service international markets and provide settlement in multiple currencies in

commercial bank money.

The pivotal role of central bank money in payment systems must be balanced against the business

decision of any commercial bank to use the payment services of another commercial bank rather than

those of the central bank. As a result of these decisions, most interbank payment systems have a

greater or lesser degree of tiering (ie several layers of settlement). Thus (and assuming that the

settlement institution is the central bank), while some banks are direct participants in a payment

system and settle in central bank money (top-tier banks), others (lower-tier banks) may instead use

the services of a top-tier bank to make and receive payments from other banks. This is standard

practice in international banking, with the widespread use of correspondent banks to make cross-

border payments. It is also the practice in most domestic banking arrangements where, for example, a

(typically) smaller bank may be a customer of a (typically) larger bank. As a result, a payment from

one bank to another may involve settlement in commercial bank money only (between two lower-tier

banks using the same top-tier bank), or in central bank money only (between two top-tier banks), or in

a combination of central and commercial bank money (eg between two lower-tier banks which do not

use the same top-tier bank).

Thus, while central bank money plays a pivotal role in the economy, no central bank sees the use of

central bank money as an end in itself. An increase in the amount of central bank money used for

payments does not necessarily indicate greater economic welfare. Rather, central banks’ interest lies

primarily in the use of central bank money at the apex of large-value payment systems, as a

complement to the use of commercial bank money in such systems.

Access to central bank money

While central banks encourage or require the use of central bank money in systemically important

payment systems, they limit access to it for other purposes. One form of central bank money - namely

banknotes - is, of course, universally available. However, central bank accounts are typically available

only to a limited range of entities, mainly banks. This reflects the fact that while central bank money

plays a key role as a settlement asset in payment systems, central banks do not in general want to

compete with commercial banks in providing banking services to the public. Because of this, central

banks typically open accounts only where there are good public policy reasons for doing so, for

example where the use of central bank money helps to eliminate exposures arising within the payment

process that could give rise to systemic risk.

Even if commercial banks are central banks’ core customers, most central banks do have some other

account holders. In general these other account holders are non-commercial entities - for example, the

government, foreign central banks or international financial institutions such as the IMF. But most

7 The risk of paying out one currency without receiving the other currency in return. See Settlement risk in foreign exchange

transactions, BIS, March 1996.

4 CPSS - The role of central bank money in payment systems - August 2003

central banks also offer accounts to supervised or licensed commercial financial institutions other than

banks - for example, securities firms or clearing houses - mostly in cases where such institutions are

also directly involved in payment or securities settlement systems. And some go further and offer

accounts to a small range of non-financial institutions.

All central banks represented in the CPSS provide access to a form of intraday credit facility to some

of their account holders, and in particular to banks. Those which undertake the privileges and

obligations of participation in the payment system generally find it valuable to have access to some

form of credit in order to use the system efficiently. Intraday credit from the central bank is generally

highly valued because it can be used to redeem any obligation, may be provided in large amounts

(although collateral is generally required), and is provided, in most cases, at quasi-zero price. As a

result, when central banks offer accounts with no credit availability, there may be little demand.

Variations in policies

However, while there are broad areas of common ground as set out above, practical distinctions exist

in the approach of central banks to the use of central bank money. For example, there are some

variations in central banks’ policies on which systems should be required, encouraged or allowed to

settle in central bank money, particularly in relation to lower-value systems.

There is also some diversity in the approach to which institutions are allowed to maintain settlement

accounts. Some central banks have broader policies than others. For example, while some CPSS

central banks are prepared in certain circumstances to permit a wide range of non-bank financial

institutions access to accounts and credit (eg the Bank of Japan, the Bank of England and the Bank of

Canada), others limit access primarily to deposit-taking institutions (eg the Federal Reserve and the

Hong Kong Monetary Authority). And while some are prepared to allow non-resident institutions to

open and operate accounts on a remote basis8 (eg the Bank of England and the Swiss National Bank),

a significant number are not, or will only do so in a limited number of well-defined cases. Finally, while

most central banks adopt a permissive approach to institutions opening settlement accounts

(specifying which institutions may, rather than must, open accounts), a few require or strongly

encourage all banks to do so (eg the Hong Kong Monetary Authority).

Current and prospective developments

The complexity in the pattern of use of central bank money is increasing. Financial markets as a whole

are affected by the powerful forces of technological change, deregulation and globalisation. Payment

arrangements are affected by these forces.

Some developments have already had significant effects on the role of central bank money. While the

role of the central bank as settlement institution is a long-standing one, in many cases this role only

required the central bank to settle the relatively small net positions of commercial banks resulting from

a netting procedure. Moreover, this occurred only once each day, at the end of the day. But with the

introduction of newer, safer systems to handle the substantially increased payment system values,

and in particular with the widespread adoption of real-time gross settlement (RTGS), where each

payment is settled in real time throughout the day, central banks and central bank money have come

to take on a much wider and more active role. Because the settlement of each payment involves a

direct transfer of the settlement asset, RTGS systems require substantially more of the asset to ensure

smooth payment flows. To enable this, most central banks provide intraday credit to banks

participating in these systems in quantities which in some cases dwarf the banks’ overnight balances

or their overnight borrowing from the central bank.

Also relevant to the use of central bank money in payment systems is the possibility of significant

concentrations of payment activities and associated exposures within individual banks. Indeed, a few

banks process very high payment values - in some cases similar to those of large-value payment

systems. Such concentrations may arise for various reasons, such as consolidation between banks,

specialisation by certain banks in correspondent banking (an area of banking that has grown relatively

8 See the discussion on access to accounts by non-resident banks in Section 3.2.1.

CPSS - The role of central bank money in payment systems - August 2003 5

rapidly because of an increase in cross-border payments), or changes in cost structures that

encourage indirect rather than direct participation in payment systems. Significant concentrations of

payments are of interest to central banks because of possible implications for risk and efficiency in the

payment system. They may also indicate that central banks should provide more competitive

settlement services. Finally, they may raise the question as to whether the scale of activity requires

additional supervision from a payment system oversight perspective, and they may call into question

the limitations on some central banks’ supervisory authority over commercial banks that engage in

systemically relevant payment activity.

The increase in cross-border flows, a result of capital liberalisation and financial globalisation, has

important implications not only for correspondent banking but also for access to central bank accounts

and credit. For example, the ICSDs, Euroclear and Clearstream, while processing the majority of their

transactions in euros, have most of their participants located outside the euro area. If the Eurosystem

were the settlement institution for the euro in these systems, it would need to facilitate remote access

to accounts and credit.9 Another example is the request, by a task force of large global banks, for

central banks to facilitate access to intraday credit by broadening the range of eligible collateral to

include a wider range of cash and securities located in other financial centres.

Further developments, while also having risk implications, are perhaps more relevant from the point of

view of competition, market structure and efficiency. For example, there have been requests in some

economies from non-bank financial institutions which are active in payments, or even from certain

non-financial institutions, for direct access to central bank accounts and payment systems. There have

also been requests for central banks to provide new or improved services that affect the way in which

central bank money is used - services such as longer operating hours, interoperability between

systems, liquidity saving mechanisms or even multicurrency functionalities.

Some key issues for central banks

The developments just described can impact on several key ongoing issues that central banks face

when providing settlement services.

• Access: who should be allowed to have a settlement account at the central bank? Should

access to settlement accounts be limited to core payment service providers, and in particular

to banks? Alternatively, how might central banks’ access policies adapt to cater for the

emergence of new forms of payment service provider and the increasing values of payments

accounted for by non-banks (particularly securities firms)? Should such institutions also have

accounts? Which account holders should be allowed credit?

• Services: do the account-related services currently provided by central banks meet the

needs of account holders and their customers? Should operating hours be longer? Does

technology offer scope to enhance services, or the design of the payment systems to which

they relate, so as to improve the safety and efficiency of the payment process? Are there

principles that place clear limits on the services central banks should offer?

• Requirements: both the Core Principles and the SSS recommendations considered the

question of when payment and settlement systems should be required to settle in central

bank money, and when an alternative (high-quality) settlement asset might be acceptable.

When should central banks insist on payment or securities settlement systems settling in

central bank money? Where that is not practicable, what sufficiently “safe” alternatives are

adequate to mitigate credit and liquidity risks?

• Concentration: as noted above, not all banks participate directly in payment systems - some

make use instead of the correspondent services provided by other banks. This brings

efficiencies, but may also lead to a concentration of payments through a few banks if there

are only a relatively small number of direct participants or if certain direct participants

9 For a definition and discussion of remote access, see Section 3.2.1.

6 CPSS - The role of central bank money in payment systems - August 2003

specialise in providing correspondent services. What risks does such tiering cause and what

might be done to mitigate them?10

Possible policy responses

While it would be hard at this stage to identify any strong or universal trend in these developments and

the potential impact they may have on the key ongoing issues, it is nevertheless the case that they are

already relevant for some central banks and may well become relevant for others in the near future.

Many central banks have thus undertaken policy reviews.

Central banks need to consider both the costs and benefits of any policy change (or of the absence of

policy change). If central banks decide that a policy response is warranted, all central banks have

broadly similar tools at their disposal. Most directly, if desirable they can modify their access policy to

allow new types of institutions as account holders. They can also alter the sorts of services that are

available to account holders (eg whether credit is provided and if so under what terms) or alter the

design of the payment systems they operate (eg change the technical means of access). More

broadly, they can use their oversight responsibilities, where appropriate in conjunction with banking

supervisors, to determine the standards applicable to payment systems and perhaps also to large

commercial providers of payment services.

Conclusion

The complex matter of competition and cooperation between central banks and commercial banks is

central to the topics examined in this report. Central and commercial bank monies are in many senses

alternatives. Nevertheless, the chain of transactions that lies behind individual payments will often

involve settlement in both central and commercial bank money. Moreover, the use of central bank

money enhances the soundness and efficiency of the payment system as a whole. Consequently,

users of commercial bank money benefit, directly or indirectly, from an externality generated by the

use of central bank money in payment systems. The convention exists that central banks avoid

competing with commercial banks in most of the payment services provided to the non-bank public. It

is this convention that generates the dichotomy between banknotes, that are available to all, and

central bank accounts, that are available only to some. At the same time, a symbiotic relationship

exists by which, on the one side, commercial banks help to extend the use of the currency while not

putting its stability at risk and, on the other side, the central bank provides them with privileged access

to its credit and, where appropriate, to some form of safety net.

However, the delimitation of the roles of central banks and commercial banks is not an absolute one.

In the provision of payment services to other banks an overlap exists. Banks may choose (and should

generally be able to choose) between a central bank and a commercial bank to process their

payments. As well as helping to promote a competitive banking system, this choice creates a healthy

incentive for central banks to provide competitive services. Central banks try to avoid unfair

competition in this area, for example by seeking to apply fair pricing policies.

This report does not attempt to set out a unique approach but instead shows the similarities and the

variations in the policies of CPSS central banks. What has been made evident by history is that policy

in this area is not static but must necessarily evolve with technological change and with changes in

financial, political and legal structures. The role and functions of the central bank itself have in fact

adapted over time, responding partly to change in the technology for making payments, and often

adopting innovations originated in the private sector. For instance, in many countries paper money or

account money represented a revolution in the technology for making payments that was initiated by

private banks.

The CPSS central banks share the conviction that the composite of central and commercial bank

money, convertible at par, is essential to the safety and efficiency of the financial system and should

remain the basis of the singleness of the currency. In other words, central banks would accept neither

10 The effects of consolidation on payment and settlement systems are discussed in the Report on consolidation in the

financial sector, Group of Ten, January 2001.

CPSS - The role of central bank money in payment systems - August 2003 7

an outcome in which central bank money crowds out private initiative, nor an outcome in which central

bank money is phased out by a market mechanism. Neither of these two outcomes is regarded as

plausible in the near future. The everyday policy decisions of central banks, illustrated in this report,

are less dramatic and more pragmatic in nature.

Central banks have generally adopted similar objectives in developing their payment system policies.

As set out in the Core Principles and the SSS recommendations, these objectives fundamentally

include the pursuit of safety and efficiency. The CPSS central banks have endorsed the Core

Principles and the SSS recommendations as the basic norms for oversight of systemically important

payment systems and of securities settlement systems and pursue similar operational strategies, such

as providing RTGS services to banking organisations.

The common ground shared by CPSS central banks in their objectives as well as in their main tenets

of policy concerning the use of central bank money can be summarised in 10 propositions that are set

out in the conclusion to this report (see Section 5).

There are also variations in payment system policies among CPSS central banks. Perhaps one

variation to note here is the degree to which central banks provide settlement services in parallel to

commercial firms (mainly banks) and the extent to which they establish norms delimiting the respective

roles of the central bank and commercial banks. Every central bank develops its own combination of

operational involvement and normative involvement, although it is true that different traditions make

them lean more towards one or the other. The variations may in some cases also involve different

trade-offs between safety and efficiency, as well as different opportunities for improving both safety

and efficiency in particular markets. They may also reflect potentially different risk tolerances in

addressing non-systemic risks. In some cases, legislation or national policies also incorporate differing

social policies or constraints involving consumer protection, banking structure, competition policy or

national security.

Structure of the report

The issues raised in this summary and introduction are explored in more detail in the rest of the report.

Section 1 considers the factors that affect the mix of central and commercial bank money in payment

systems. Section 2 then looks at some of the current developments affecting payment systems and

the impact they may have on the use of central bank money. In the light of this analysis, Sections 3

and 4 turn to central bank policies. Section 3 describes existing central bank policies, while Section 4

looks at the possible implications for these policies of the developments set out in Section 2. Section 5

provides some concluding remarks, including the 10 propositions mentioned earlier. Finally, the

annexes contain more detailed information on some of the topics discussed in the report.11

1. The coexistence of central and commercial bank money in payment

systems

Money is fundamental to the operation of a modern economy. A common feature of developed

economies is the wide variety of ways in which payments are made and the forms of money used.

There is also a wide range of economic agents whose liabilities function as money. The most familiar

issuers of money are central banks, which provide central bank money in the form of both banknotes

and deposit liabilities, and commercial banks, which generally issue private money (commercial bank

money) in the form of deposit liabilities.

Economic activity can in principle take place without the coexistence of central and commercial bank

money. Indeed, both corner solutions - on the one hand, narrow or monobanking where there was only

central bank money and, on the other hand, free banking where there was only commercial bank

11 For definitions of standard payment system terms used in this report, see A glossary of terms used in payment and

settlement systems, BIS, January 2001. (All the BIS publications referred to in this report, including the latest version of the

glossary, are on the BIS website, www.bis.org.) Terms that are specific to this report are defined as they are used.

8 CPSS - The role of central bank money in payment systems - August 2003

money - have existed in the past. But neither has proved sufficiently stable or efficient to survive.

There has been a migration away from the corner towards intermediate solutions in which both types

of money play an important part in facilitating economic activity. CPSS central banks continue to

believe that the most effective and efficient financial system is one in which there is competition

among banks and in which central bank money is used where its particular features are most

important.

An important feature of this coexistence is that, in a given currency, central and commercial bank

monies are convertible into each other at par. Conversion at par removes the very high transaction

costs that could arise for users of a currency if there were multiple issuers whose monies were

exchanged at different values. Conversion between commercial and central bank monies takes place

in a tangible manner when a commercial bank depositor withdraws banknotes from an account.

Conversion between different commercial bank monies takes place through payment systems when a

customer of one bank makes a payment to a customer of another bank, using central bank money as

the bridge in most cases.

This section looks in more detail at this coexistence of central and commercial bank money. It looks

first, in Section 1.1, at central bank money and the central bank’s objectives. Section 1.2 then

considers how payment systems function and the role of the settlement institution, while Section 1.3

discusses the factors determining the choice of settlement asset.

1.1 Central bank money and central bank objectives

Central banks provide central bank money to support their core objectives. CPSS central banks vary in

how they articulate these objectives, but they can be broadly categorised as pursuit of monetary policy

goals, maintenance of the stability of the financial system and promotion of the effectiveness or

efficiency of the financial system. Within the context of these broader objectives, CPSS central banks

recognise that the ability to make payments safely and efficiently is crucial to the functioning of the

financial system, both domestic and global. Sound and efficient payment mechanisms enhance the

allocation of resources, facilitate growth and improve social welfare. This report focuses on the role of

central bank money as a means of payment.

As noted above, central bank money takes two main forms - banknotes and deposit money.

Banknotes are probably the most visible symbol of a currency and play a widespread role in the

making of retail payments. Moreover, the value of banknotes outstanding is generally significantly

larger than the stock of central bank deposit money in existence. However, while banknotes are

undeniably important in an economy and raise a number of issues for central banks - most notably

concerning the costs of distribution and the prevention of counterfeiting - they generally do not raise

the sort of systemic risk issues of core concern to central banks because of the relatively small values

typically involved when payments are made. Banknotes are therefore not directly covered in the rest of

this report, although Annex 4 provides some more information about their features and usage.

On the other hand, central bank deposit money plays a crucial role as the settlement asset in payment

systems which transfer substantial values of funds each day and where there is significant potential for

systemic risk. The quantity of central bank money and/or the terms on which it is available are of

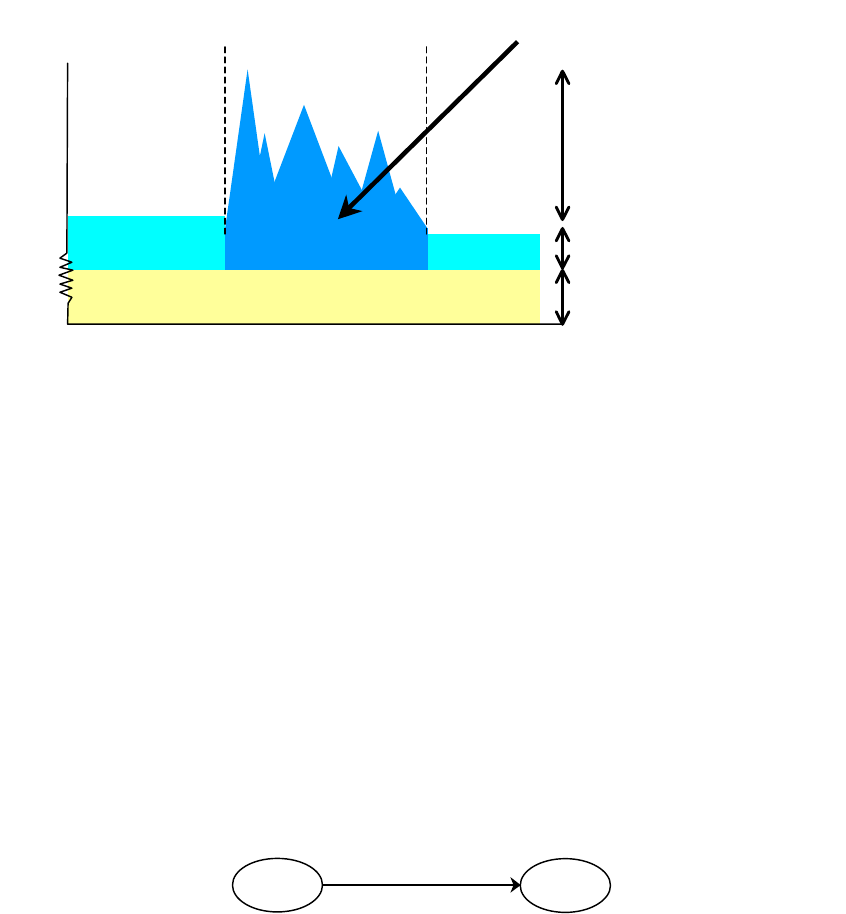

course pivotal aspects of central banks’ monetary policy. But, as illustrated in Figure 1, balances

with the central bank also play an important role from the viewpoint of payments policy. During the

day, deposits with the central bank can be used to make interbank payments, whose completion

is a critical activity for the economy at large. If the intraday balance available for payments is too

small relative to the value of payments to be made in a given time, it could result in gridlock,

preventing payments from being executed. Thus in many cases central banks provide intraday

credit to banks and other account holders. Indeed, particularly with the decline in importance of

reserve requirements in many economies, balances held by banks during the day are often

substantially larger than those held overnight.12

12 Figure 1 is a stylised diagram that is not intended to indicate actual magnitudes of central bank money. Other transactions

(such as sales/purchases of cash or provision/repayment of overnight credit) are included within “intraday balances

injected”. For data on overnight balances and intraday credit on central bank accounts, see Table B in Annex 3.

CPSS - The role of central bank money in payment systems - August 2003 9

Figure 1

Stylised diagram of central bank money

7

The smooth and safe functioning of a payment system is dependent not just on the quantity of the

settlement asset. It also depends crucially on the quality of the asset and thus on the identity of the

settlement institution. To explain this, Section 1.2 considers how payment systems function and thus

the role of the settlement institution in them.

1.2 How payment systems function and the role of the settlement institution

1.2.1 Simple models of how payment systems function

Different forms of money require more or less complex arrangements to enable them to be used to

make payments. The two most common forms of money used to make payments are banknotes and

commercial bank deposit money. Banknotes are bearer instruments and thus the payments process is

simple - the notes are simply transferred from payer to payee, as illustrated in Figure 2.

Figure 2

Payment by banknotes

However, where commercial bank deposit money is used, transfers generally take place within

organised “payment systems” where commercial and central bank money often complement each

other in more complex chains of payments. Although the term “payment system” can be used broadly

to refer to the entire web of payments within an economic area, it is often applied in a more limited

sense to refer to an interbank payment system, incorporating a particular set of payment instruments,

technical standards for the transmission of payment messages and an agreed means of settling claims

among system members, including use of a nominated settlement institution.

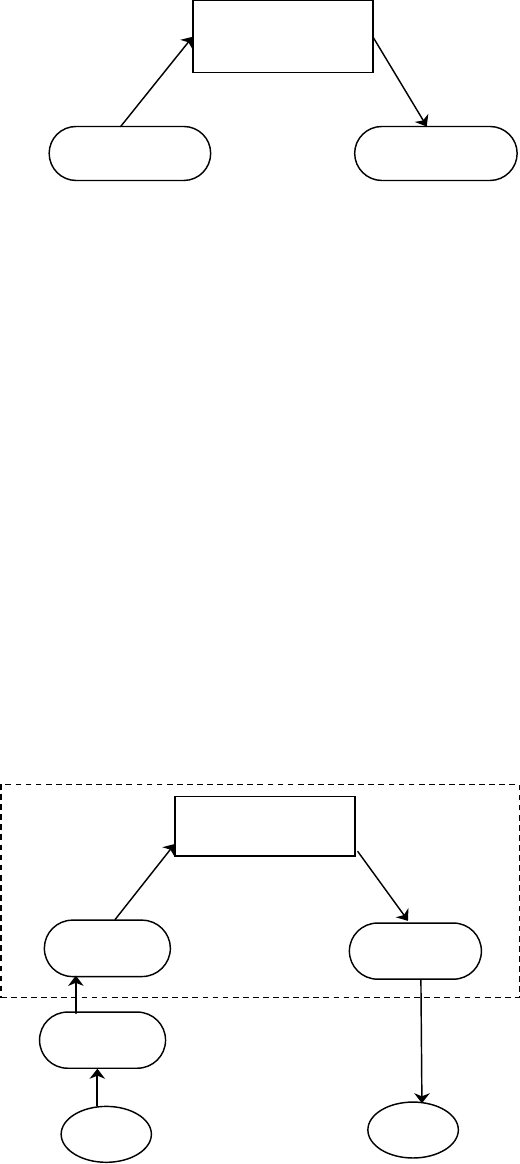

The simplest case of making a payment in an interbank payment system is shown in Figure 3. This

stylised payment system has one intermediary, generally (although not always) the central bank,

which acts as the settlement institution. The paying and receiving banks are both direct participants in

the interbank payment system and hold accounts at the settlement institution, and settlement is

effected by a debit from the account of the paying bank and a credit to the account of the receiving

bank. The payment may either be financed with funds already on the account of the paying bank, or

Payer Payee

Banknotes

value Intraday balances used for

interbank payments

time

Intraday balances

injected

Overnight balances

start of day end of day

Banknotes outstanding

10 CPSS - The role of central bank money in payment systems - August 2003

with credit provided by the settlement institution. The receiving bank may leave the funds it receives

on account at the settlement institution or it may decide to pay them away.

Figure 3

Simple interbank payment system

While this is a simple example, it illustrates the crucial role played by the settlement institution, and the

ways in which paying and receiving banks are exposed to it. Settlement takes place in the settlement

institution’s liabilities, and both paying and receiving banks need accounts with that institution. Both

are reliant on the settlement institution’s operational soundness. And they will be exposed to credit risk

on the settlement institution in relation to any funds held on account. These risks may be difficult to

avoid or to control. For example, receiving banks may have very little control over the value of

payments received and held on account with the settlement institution. The larger the value and

volume of payments the institution settles, the more important are its creditworthiness and operational

reliability.

In practice, payment arrangements, both domestic and particularly cross-border, are invariably far

more complex than this, involving tiers within and between which payments are made. As before,

those holding accounts with the settlement institution - the direct participants in the “system” - are

generally banks (“settlement” or “correspondent” banks), which in turn provide accounts and payment

services to their own customers, which may be other banks, non-bank financial institutions,

non-financial firms or individuals. In this world, the “payment system” is a broader construct, involving

various tiers of intermediation, as shown in Figure 4. For clarity, in the remainder of the report the

narrow set of arrangements involving the settlement institution and those holding accounts with it will

be referred to as the “interbank payment system”. The term “payment system” will be used to describe

the broader, tiered arrangements described below.

Figure 4

More complex payment arrangements

In this more realistic example, the payment chains are more complicated. Take a payment between a

customer of Bank A (a second-tier bank - ie one that is not a direct participant in the interbank

Paying bank Receiving bank

Settlement

institution

Interbank

payment

s

y

stem

Bank B Bank C

Settlement

institution

Bank A

Payer Payee

CPSS - The role of central bank money in payment systems - August 2003 11

payment system) and a customer of Bank C (a direct participant in the system). The payment process

involves debiting the payer’s account at Bank A, Bank A’s account with Bank B and Bank B’s account

with the settlement institution. It also involves crediting Bank C’s account with the settlement institution

and the payee’s account with Bank C.

In practice, a number of “payments” are taking place, using different types of “money”. The settlement

institution will generally (although not always) be a central bank, so settlement between direct

participants in the interbank payment system takes place in central bank money. But the accounts of

most payers and payees will be held with intermediary banks, and payments (debits) and receipts

(credits) will take place in commercial bank money issued by different commercial banks. Indeed,

while data are scarce, if the different components of payment chains are aggregated it is quite

possible that in many cases the value of payments settling in commercial bank money exceeds that

settled in central bank money (see Section 2).

The “payment chain” is actually a combination of various payments at different tiers, whose

“settlement” takes place independently. In some jurisdictions, unless otherwise contracted between

payer and payee, the point at which the underlying payment obligation has been extinguished will

coincide with the payment being “settled” within the interbank payment system. In other jurisdictions,

this is not generally the case. In any event, finality does not imply that the payee has yet received the

funds, so the payee may remain exposed to intermediaries even though the payer has legally

discharged its obligation. The moment in which final settlement takes place is defined primarily by the

rules of the interbank payment system. Furthermore, local laws may affect the timing or conditions

under which final settlement takes place.

This model is used for both domestic and cross-border payments. The latter, ie where the payer

and/or the payee is non-resident, generally involve some form of domestic payment. The

payer/payee’s bank may be able, and choose, to access the domestic interbank system directly on a

remote basis. If not, it will use the services of a correspondent bank, which may in turn access the

relevant system directly or use the services of a local bank. Final settlement may take place at a

number of levels (across the books of the settlement institution and/or those of a first- or lower-tier

commercial bank), depending on each counterparty’s payment arrangements.

The model is also applicable to the payment arrangements associated with securities settlement

systems (see Box 1). Such arrangements are included within the definition of “payment system” and

are therefore covered in the analysis in the rest of this report.

1.2.2 Risks relating to the settlement asset13

Essentially the same risks can arise within the sort of interbank payment system described above as

within the “simple” payments model outlined earlier.

Risks relating to the settlement institution

As stated earlier, direct participants have potential exposures to the settlement institution, as does the

settlement institution to the direct participants. Credit exposures may exist where funds are held with

the settlement institution or advanced by it to direct participants. There may be liquidity risks if the

settlement institution fails to meet any commitments it has made to provide liquidity to direct

participants. And direct participants are reliant on the operational capability of the settlement

institution. The nature, size and duration of these exposures depend very much on factors such as the

design of the system, the availability of credit and the arrangements for funding/defunding the

accounts held at the settlement institution.

The use of central bank money as the settlement asset in systemically important payment systems

(SIPS)14 eliminates credit and liquidity risk at the apex of the payment system, where exposures are

13 The term settlement asset is often used exclusively to refer to the asset used for settlement between direct participants in an

interbank payment system. However, for convenience, in the rest of this report the term is also used to indicate the asset

used for settlement between a direct participant and its customers.

14 For an explanation of systemically important payment systems, see Core principles for systemically important payment

systems.

12 CPSS - The role of central bank money in payment systems - August 2003

generally highest and most concentrated, and where direct participants have least choice over the

source of their exposure. And the central bank’s role as settlement institution provides assurance of

continuity in the provision of liquidity and in the provision of settlement services.

Box 1

Securities settlement systems

Securities settlement systems (SSSs) are systems which mainly provide custody services and final delivery of

securities from the seller to the buyer. When securities are traded in exchange for funds (as is usually the

case), SSSs also ensure the transfer of the related funds in the relevant payment system. This payment

system may be embedded in the SSS or external to it.15

If the payment system is embedded, both securities and cash are transferred within the same organisation.

Examples of SSSs with embedded payment systems are central bank CSDs (for the settlement of government

securities), which naturally use central bank money, or, on the other side of the spectrum, private CSDs (or

ICSDs) using commercial bank money.

An example of an SSS with an external payment system is a CSD which is privately owned but which settles in

central bank money. When the payment system is external to the SSS, a number of issues arise. For example:

• the participant of the CSD also needs to have access (directly or indirectly) to the payment system;

• the CSD and the payment system need to have compatible operating hours;

• where collateral is needed to obtain credit in the payment system, there may be advantages to CSD

participants if the assets held at the CSD can be used as collateral.

Risks between direct participants and their customers

Similar exposures arise between direct participants and their customers. Customers are operationally

reliant on their chosen intermediary to make payments on their behalf, and incur credit risk where

receipts of funds are held with the intermediary. In turn, intermediaries incur risks on their customers

where they provide them with credit for payments. Such risks are not unusual - they arise, and are

managed, in the normal course of banks’ and their customers’ activities. But exposures arising within

the payment system may be very large, especially when the customer is a bank, since the values

transferred can be very significant. They may also be difficult to control and, depending on the degree

of tiering within the system, the number of direct participants may in practice be low, limiting the choice

of intermediary.

The distribution of payments affects the distribution of risk within the system. Where large values of

payments flow through a small number of direct participants, the consequent exposures may be very

large in relation to each direct participant’s capital. Each direct participant stands between its own

customers and other direct participants, such that other direct participants are to some degree

sheltered from the risk of default by non-participants and vice versa. However, as a consequence,

direct participants acting for a large number of customers may incur very high exposures, both to their

customers and to other direct participants, and may be more vulnerable to shocks within the payment

system or their customer base. At the same time, the impact of the correspondent’s failure on others

may be greater. In systems in which flows are highly concentrated, each direct participant’s ability to

15 Other models which are neither completely embedded nor completely external also exist. An example is the settlement

model developed by the French CSD and the Bank of France. The Bank of France has granted the securities settlement

system a mandate to operate dedicated accounts in central bank money. The cash leg of securities trades is settled on

these dedicated accounts. This architecture enables Euroclear France to check the availability of the securities on the

seller’s securities account as well as the availability of cash on the buyer’s dedicated account, and to transfer

simultaneously securities and funds between the participants in a way that ensures delivery versus payment and real-time

finality in central bank money. The Bank of France has also mandated Euroclear France to operate intraday credit

operations on its behalf for those participants whose dedicated account balance is not sufficient to settle a trade. Since this

intraday credit is automatically allocated to the dedicated cash accounts operated by Euroclear France, no permanent link is

necessary with the RTGS system. Consequently, these automated intraday repos can take place even outside the RTGS

operating hours.

CPSS - The role of central bank money in payment systems - August 2003 13

manage the associated risks is one determinant of how easily financial shocks to one part of the

system are transmitted throughout the system and to other parts of the financial sector.16

1.3 Factors determining agents’ choice of settlement asset

The example in Figure 4 illustrates how different forms of settlement asset (generally central and

commercial bank money) coexist. The balance between the different forms will depend on various

factors, including the design of the interbank payment system and the policies of the relevant central

bank. These are discussed in Section 3. But a key determinant of the balance will be the choices

made by potential payment system users.

In general, payment system users have a choice between being a direct participant in the system or

using a correspondent, and in the latter case a choice between correspondents. Their choice will be

influenced by the private costs and benefits associated with each option. Some of these costs and

benefits will relate to features of the institution providing the settlement asset, such as its

creditworthiness and neutrality. Others will relate to the services, such as credit, which that institution

is prepared to provide and to the design of the payment system within which the asset will be used.17

Differences between settlement assets are usually a matter of degree - safety and many of the other

relevant features are relative concepts, not qualities which assets either do or do not possess.

Safety

The “safety” of different forms of money, in the context of their use as settlement assets, essentially

means the likelihood of the asset retaining its value to the holder, and hence its acceptability to others

as a means of payment.

Central bank money is generally completely safe in its jurisdiction. Central banks are more

creditworthy institutions than commercial banks in their own currency. They have explicit or implicit

state support. In a fiat money system, where not constrained by a convertibility rule to another

asset/currency, the central bank can always cover its obligations by issuing its own currency. In

addition, central banks tend to be risk-averse institutions which seek, as far as possible, to engage

only in low-risk financial activities. Indeed, the term “ultimate settlement” has sometimes been used to

indicate settlement in central bank money, although the term needs to be used with care (see Box 2).

The creditworthiness of commercial banks is tested through their ability to convert on demand their

sight liabilities into the money of another commercial bank or into central bank money. In practice in

CPSS countries, the generally high credit standing of commercial banks means that default risk is

unlikely to be a significant disincentive to maintaining settlement accounts with commercial banks.

Prudential supervision reduces the likelihood of default by supervised institutions, improving the safety

of claims on these institutions. And the existence of investor/depositor protection schemes has the

effect of maintaining at least partial convertibility of a failed bank’s liabilities into other forms of money,

and hence supporting their value as settlement assets. Utilities like clearing houses often go further in

lowering default risk by fully collateralising any exposure to their members and not engaging in any

further financial activities which could expose them to risk. Thus other factors, including the asset’s

availability and liquidity, are likely to be a more significant determinant of choice of settlement asset.

It should be noted, however, that the safety of both central and commercial bank money is influenced

by the ability of the central bank to maintain the value of the stock of currency as a whole - ie price

stability.

16 The analysis in Section 1.2.2 is based on the assumption that banks that are not direct participants in a system use a

commercial bank to act as their correspondent (eg in Figure 4, Bank A uses Bank B). However, in a few cases central banks

themselves provide correspondent services to customer banks that are not direct participants in systems that settle in

central bank money. In these circumstances, the risks that arise are likely to be similar to those that arise where banks are

direct participants.

17 Those choosing direct participation are of course constrained to use the settlement asset that has been collectively chosen

by the system. Thus the choice of settlement asset cannot be made independently of the wider choice between direct

participation and non-participation, which will depend on a wider range of factors than those relevant to the settlement asset

itself.

14 CPSS - The role of central bank money in payment systems - August 2003

Box 2

“Ultimate settlement”

The term “ultimate settlement” is sometimes used to denote final settlement in central bank money (see

A glossary of terms used in payment and settlement systems). As such, the term combines two distinct

concepts - finality and the nature of the settlement asset used to achieve finality in payment systems.

Finality is achieved when settlement of an obligation is irrevocable and unconditional. As discussed in the Core

Principles, finality within an interbank payment system is generally determined by the system’s rules and the

legal framework within which the rules function. The definition should apply even in abnormal circumstances.

For example, some systems have rules or procedures that allow payments to be unwound if a participant fails

to meet its settlement obligation. Settlement cannot be considered final until there is no further possibility that it

will be unwound, because all conditions have been satisfied. In practice there can be many obstacles to

achieving finality. Some can be overcome by a proper contract between the parties. Others may require

changes to the law. A significant obstacle can be insolvency law, which typically takes precedent over contract

law and can thus overturn what would otherwise be a settled transaction (eg zero hour rule). Because of the

complexity of legal regimes and system rules, a number of jurisdictions have special laws designed to secure

payment system finality (eg the European Union’s Settlement Finality Directive).

Subject to any specific requirements of the law, parties are usually free to choose which asset to use as the

settlement asset. Many interbank payment systems use central bank money, but this is not always the case

(see Annex 3, Table C). Regardless of the settlement asset used, it is necessary to establish when finality

occurs. In general, the law does not distinguish between assets in this respect: settlement finality is no easier

or harder to achieve in central bank money than in any other asset. On the other hand, as discussed in the

main text, the choice of settlement asset is important for other reasons, not least because, even when the

original payment obligation is fully extinguished, for the payee there can be both credit and liquidity risks

associated with holding the resulting settlement asset.

The term “ultimate settlement” thus combines the concept of settlement being final with the concept of the

settlement asset being the least risky possible. As noted in the Core Principles, claims on the central bank are

typically free of the credit and liquidity risks associated with settlement assets. Where this is the case, it may be

appropriate to use the term “ultimate settlement” to denote final settlement in central bank money.

Liquidity and credit

“Liquidity” is a valuable characteristic for a settlement asset to possess. Certain forms of settlement

asset are usually said to be more liquid than others, with central bank money generally held to be the

most liquid. However, used in the context of the demand for different forms of money for settlement

purposes, liquidity can have more than one meaning.

As a rule, an asset’s “liquidity” is defined as the holder’s ability to dispose of it quickly without material

loss of value. Within the payment system of an economy, that translates as its ability to be used as a

means of making payments to a wide range of counterparties. In part, that will reflect the

creditworthiness of the issuer and thus is closely related to safety. However, the efficiency with which

money can be transferred between customers of different banks is also highly relevant. This will reflect

the scope of the payment network of end users and the speed and cost of transferring funds within

and between banks and interbank payment systems.

“Liquidity” is also often used to describe the issuer’s ability to expand its balance sheet by issuing

additional liabilities to its customers at short notice. In this context, commercial banks are constrained

by the desire to avoid a destabilising “run”, perhaps supported by prudential or statutory requirements.

Central banks do not face this constraint,18 and their ability to inject very large amounts of liquidity,