2017 Form 4684 I4648A F4684

User Manual: i4648A

Open the PDF directly: View PDF ![]() .

.

Page Count: 4

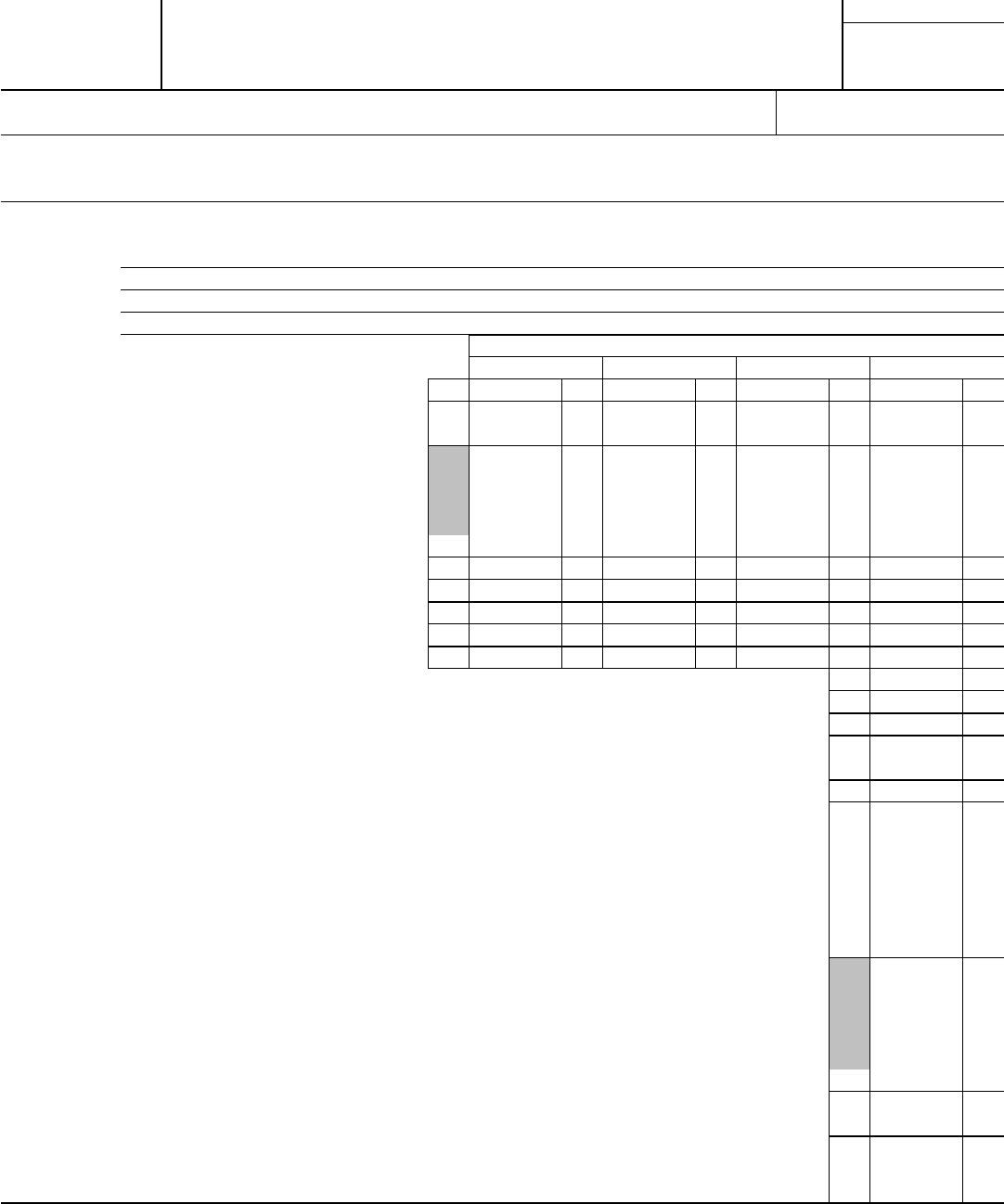

Form 4684

Department of the Treasury

Internal Revenue Service

Casualties and Thefts

▶ Go to www.irs.gov/Form4684 for instructions and the latest information.

▶ Attach to your tax return.

▶ Use a separate Form 4684 for each casualty or theft.

OMB No. 1545-0177

2017

Attachment

Sequence No. 26

Name(s) shown on tax return Identifying number

SECTION A—Personal Use Property (Use this section to report casualties and thefts of property not used in a trade

or business or for income-producing purposes. If reporting a casualty loss from a disaster, see the instructions

before completing this section.)

1

Description of properties (show type, location, and date acquired for each property). Use a separate line for each property lost or damaged from

the same casualty or theft. You must use a separate Form 4684 (through line 12) for each casualty or theft event involving personal use property.

Property A

Property B

Property C

Property D

Properties

A B C D

2 Cost or other basis of each property . . . . . . 2

3

Insurance or other reimbursement (whether or not you

filed a claim) (see instructions) . . . . . . . . 3

Note: If line 2 is more than line 3, skip line 4.

4

Gain from casualty or theft. If line 3 is more than line 2,

enter the difference here and skip lines 5 through 9 for

that column. See instructions if line 3 includes insurance

or other reimbursement you did not claim, or you

received payment for your loss in a later tax year . . 4

5 Fair market value before casualty or theft . . . . 5

6 Fair market value after casualty or theft . . . . . 6

7 Subtract line 6 from line 5 . . . . . . . . . 7

8 Enter the smaller of line 2 or line 7 . . . . . . 8

9 Subtract line 3 from line 8. If zero or less, enter -0- . . 9

10 Casualty or theft loss. Add the amounts on line 9 in columns A through D . . . . . . . . . . . . . 10

11 Enter $100 ($500 if qualified disaster loss rules apply; see instructions) . . . . . . . . . . . . . . 11

12 Subtract line 11 from line 10. If zero or less; enter -0- . . . . . . . . . . . . . . . . . . . 12

Caution: Use only one Form 4684 for lines 13 through 18.

13 Add the amounts on line 12 of all Forms 4684 . . . . . . . . . . . . . . . . . . . . . 13

14 Add the amounts on line 4 of all Forms 4684 . . . . . . . . . . . . . . . . . . . . . 14

Caution: See instructions before completing line 15.

15

• If line 14 is more than line 13, enter the difference here and on Schedule D. Do not

complete the rest of this section.

• If line 14 is equal to line 13, enter -0- here. Do not complete the rest of this section.

• If line 14 is less than line 13, and you have no qualified disaster losses subject to the

$500 reduction on line 11 on any Form(s) 4684, enter -0- here and go to line 16. If you

have qualified disaster losses subject to the $500 reduction, subtract line 14 from line 12

of the Form(s) 4684 reporting those losses. If the result is zero or less, see instructions.

Otherwise, enter that result here and on Schedule A (Form 1040), line 28, or Form

1040NR, Schedule A, line 14. If you claim the standard deduction, also include on

Schedule A (Form 1040), line 28, the amount of your standard deduction (see the

instructions for Form 1040). Do not complete the rest of this section if all of your

casualty or theft losses are subject to the $500 reduction.

}

....... 15

16 Add lines 14 and 15. Subtract the result from line 13 . . . . . . . . . . . . . . . . . . . 16

17

Enter 10% of your adjusted gross income from Form 1040, line 38, or Form 1040NR, line 37. Estates and trusts, see

instructions ............................... 17

18

Subtract line 17 from line 16. If zero or less, enter -0-. Also enter the result on Schedule A (Form 1040), line 20, or

Form 1040NR, Schedule A, line 6. Estates and trusts, enter the result on the “Other deductions” line of your tax

return ................................. 18

For Paperwork Reduction Act Notice, see instructions. Cat. No. 12997O Form 4684 (2017)

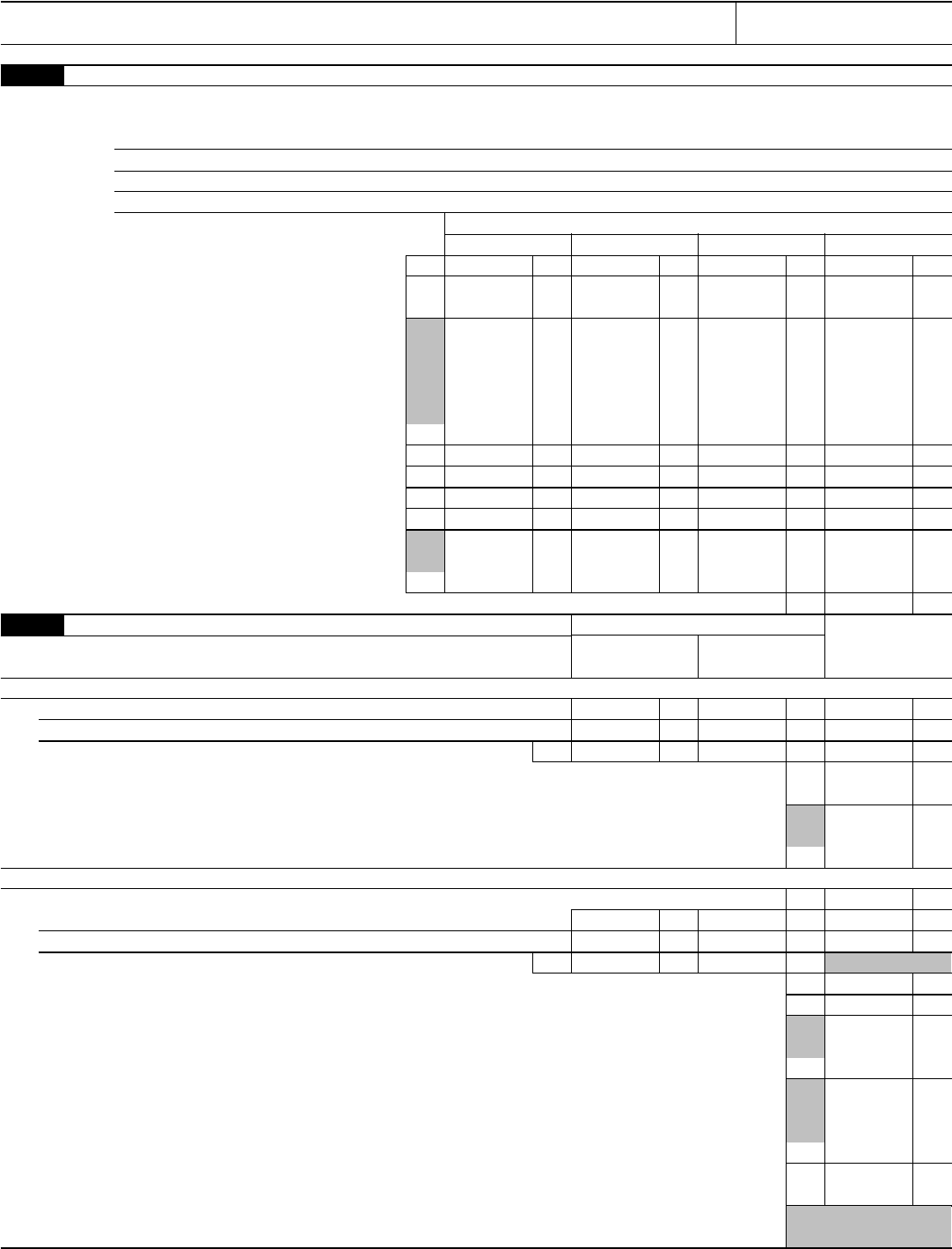

Form 4684 (2017) Attachment Sequence No. 26 Page 2

Name(s) shown on tax return. Do not enter name and identifying number if shown on other side. Identifying number

SECTION B—Business and Income-Producing Property

Part I Casualty or Theft Gain or Loss (Use a separate Part l for each casualty or theft.)

19

Description of properties (show type, location, and date acquired for each property). Use a separate line for each property lost or damaged from

the same casualty or theft. See instructions if claiming a loss due to a Ponzi-type investment scheme and Section C is not completed.

Property A

Property B

Property C

Property D

Properties

A B C D

20 Cost or adjusted basis of each property . . . . . 20

21

Insurance or other reimbursement (whether or not you

filed a claim). See the instructions for line 3 . . . . 21

Note: If line 20 is more than line 21, skip line 22.

22

Gain from casualty or theft. If line 21 is more than line 20, enter

the difference here and on line 29 or line 34, column (c), except

as provided in the instructions for line 33. Also, skip lines 23

through 27 for that column. See the instructions for line 4 if line

21 includes insurance or other reimbursement you did not

claim, or you received payment for your loss in a later tax year

22

23 Fair market value before casualty or theft . . . . 23

24 Fair market value after casualty or theft . . . . . 24

25 Subtract line 24 from line 23 . . . . . . . . 25

26 Enter the smaller of line 20 or line 25 . . . . . 26

Note: If the property was totally destroyed by casualty or

lost from theft, enter on line 26 the amount from line 20.

27 Subtract line 21 from line 26. If zero or less, enter -0- . 27

28 Casualty or theft loss. Add the amounts on line 27. Enter the total here and on line 29 or line 34 (see instructions) . 28

Part II Summary of Gains and Losses (from separate Parts l)

(a) Identify casualty or theft

(b) Losses from casualties or thefts

(i) Trade, business,

rental, or royalty

property

(ii) Income-

producing and

employee property

(c) Gains from

casualties or thefts

includible in income

Casualty or Theft of Property Held One Year or Less

29 ( ) ( )

( ) ( )

30 Totals. Add the amounts on line 29 . . . . . . . . . . . . 30 ( ) ( )

31 Combine line 30, columns (b)(i) and (c). Enter the net gain or (loss) here and on Form 4797, line 14. If Form 4797 is

not otherwise required, see instructions . . . . . . . . . . . . . . . . . . . . . . . 31

32

Enter the amount from line 30, column (b)(ii) here. Individuals, enter the amount from income-producing property on Schedule A

(Form 1040), line 28, or Form 1040NR, Schedule A, line 14, and enter the amount from property used as an employee on Schedule

A (Form 1040), line 23, or Form 1040NR, Schedule A, line 9. Estates and trusts, partnerships, and S corporations, see instructions

32

Casualty or Theft of Property Held More Than One Year

33 Casualty or theft gains from Form 4797, line 32 . . . . . . . . . . . . . . . . . . . . . . . . . 33

34 ( ) ( )

( ) ( )

35 Total losses. Add amounts on line 34, columns (b)(i) and (b)(ii) . . . . . 35 ( ) ( )

36 Total gains. Add lines 33 and 34, column (c) . . . . . . . . . . . . . . . . . . . . . . 36

37 Add amounts on line 35, columns (b)(i) and (b)(ii) . . . . . . . . . . . . . . . . . . . . 37

38 If the loss on line 37 is more than the gain on line 36:

a

Combine line 35, column (b)(i) and line 36, and enter the net gain or (loss) here. Partnerships (except electing large

partnerships) and S corporations, see the note below. All others, enter this amount on Form 4797, line 14. If Form

4797 is not otherwise required, see instructions . . . . . . . . . . . . . . . . . . . . . 38a

b

Enter the amount from line 35, column (b)(ii) here. Individuals, enter the amount from income-producing property on

Schedule A (Form 1040), line 28, or Form 1040NR, Schedule A, line 14, and enter the amount from property used as

an employee on Schedule A (Form 1040), line 23, or Form 1040NR, Schedule A, line 9. Estates and trusts, enter on

the “Other deductions” line of your tax return. Partnerships (except electing large partnerships) and S corporations,

see the note below. Electing large partnerships, enter on Form 1065-B, Part II, line 11 . . . . . . . . . 38b

39

If the loss on line 37 is less than or equal to the gain on line 36, combine lines 36 and 37 and enter here. Partnerships

(except electing large partnerships), see the note below. All others, enter this amount on Form 4797, line 3 . . . .

39

Note: Partnerships, enter the amount from line 38a, 38b, or line 39 on Form 1065, Schedule K, line 11.

S corporations, enter the amount from line 38a or 38b on Form 1120S, Schedule K, line 10.

Form 4684 (2017)

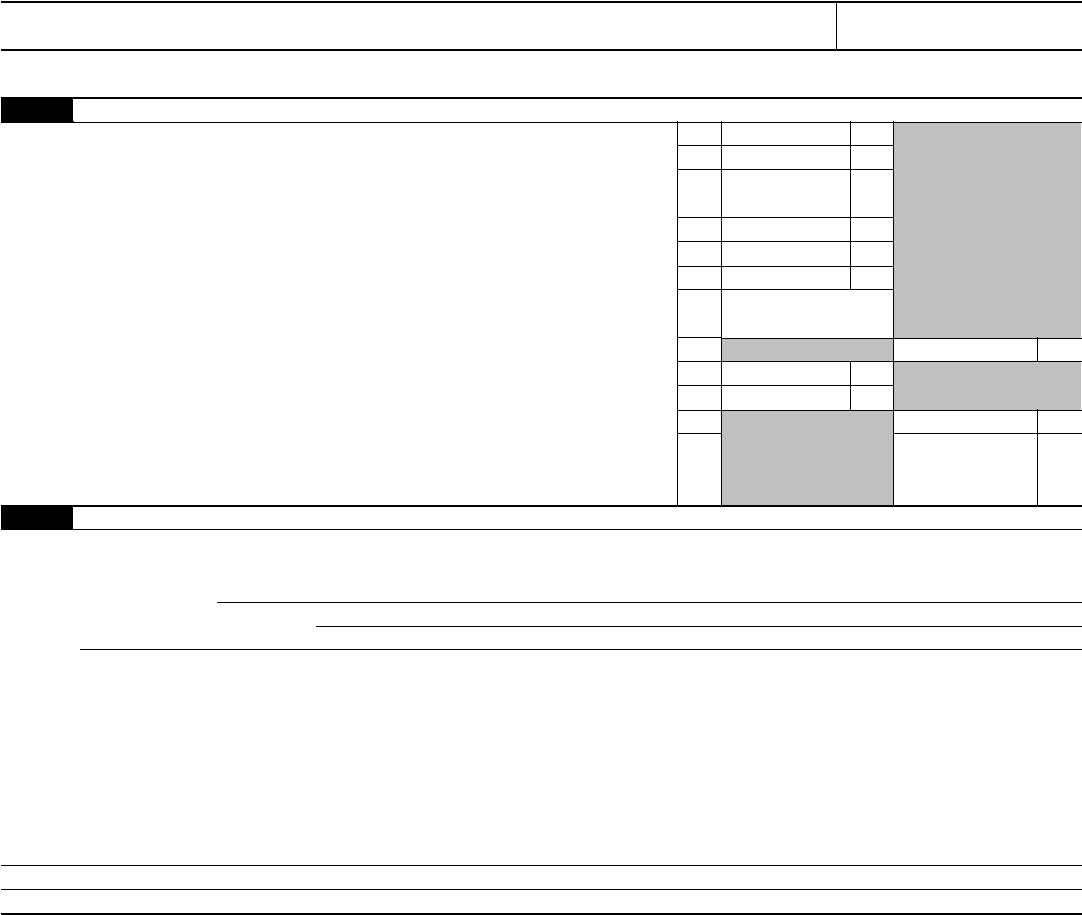

Form 4684 (2017) Attachment Sequence No. 26 Page 3

Name(s) shown on tax return Identifying number

SECTION C—Theft Loss Deduction for Ponzi-Type Investment Scheme Using the Procedures in Revenue

Procedure 2009-20 (Complete this section in lieu of Appendix A in Revenue Procedure 2009-20. See instructions.)

Part I Computation of Deduction

40 Initial investment . . . . . . . . . . . . . . . . . . . . . 40

41 Subsequent investments (see instructions) . . . . . . . . . . . . . 41

42

Income reported on your tax returns for tax years prior to the discovery year

(see instructions) . . . . . . . . . . . . . . . . . . . . 42

43 Add lines 40, 41, and 42 . . . . . . . . . . . . . . . . . . 43

44 Withdrawals for all years (see instructions) . . . . . . . . . . . . . 44

45 Subtract line 44 from line 43. This is your total qualified investment . . . . . . 45

46 Enter 0.95 (95%) if you have no potential third-party recovery. Enter 0.75 (75%) if you

have potential third-party recovery . . . . . . . . . . . . . . . 46 .

47 Multiply line 46 by line 45 . . . . . . . . . . . . . . . . . . 47

48 Actual recovery ..................... 48

49 Potential insurance/Securities Investor Protection Corporation (SIPC) recovery . . 49

50 Add lines 48 and 49. This is your total recovery . . . . . . . . . . . . 50

51 Subtract line 50 from line 47. This is your deductible theft loss. Include this amount on

line 28 of Section B, Part I. Do not complete lines 19–27 for this loss. Then complete

Section B, Part II . . . . . . . . . . . . . . . . . . . . 51

Part II Required Statements and Declarations (See instructions.)

• I am claiming a theft loss deduction pursuant to Revenue Procedure 2009-20 from a specified fraudulent arrangement conducted by the following

individual or entity.

Name of individual or entity

Taxpayer identification number (if known)

Address

• I have written documentation to support the amounts reported in Part I of this Section C.

• I am a qualified investor as defined in section 4.03 of Revenue Procedure 2009-20.

• If I have determined the amount of my theft loss deduction using 0.95 on line 46 above, I declare that I have not pursued and do not intend to pursue

any potential third-party recovery, as that term is defined in section 4.10 of Revenue Procedure 2009-20.

• I agree to comply with the conditions and agreements set forth in Revenue Procedure 2009-20 and this Section C.

• If I have already filed a return or amended return that does not satisfy the conditions in section 6.02 of Revenue Procedure 2009-20, I agree to all

adjustments or actions that are necessary to comply with those conditions. The tax year(s) for which I filed the return(s) or amended return(s) and the

date(s) on which they were filed are as follows:

Form 4684 (2017)

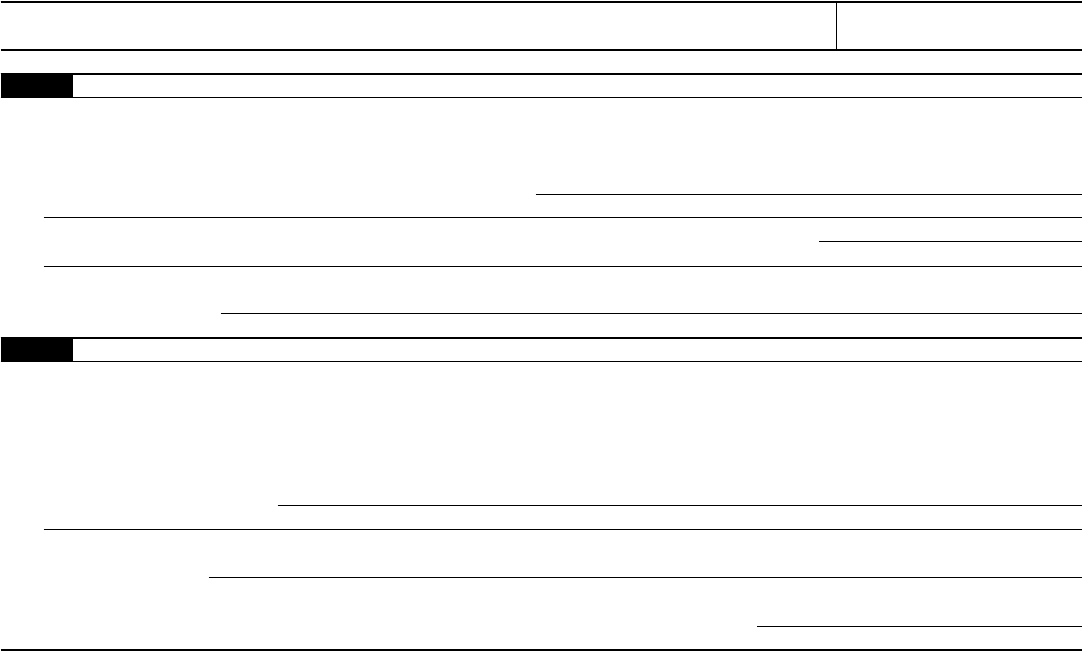

Form 4684 (2017) Attachment Sequence No. 26 Page 4

Name(s) shown on tax return Identifying number

SECTION D—Election To Deduct Federally Declared Disaster Loss in Preceding Tax Year (See instructions.)

Part I Election Statement

By providing all of the information below and attaching this Section D to a return or amended return for the preceding tax year which takes advantage

of the disaster loss deduction, you hereby elect, under section 165(i) of the Internal Revenue Code, to deduct a loss attributable to a federally declared

disaster that occurred in a federally declared disaster area and was sustained in the disaster year on your tax return for the preceding tax year.

52 Provide the name or a description of the federally declared disaster.

53 Provide the date or dates (mm/dd/yyyy) of the loss or losses that arose from the federally declared disaster.

54 Specify the address, including the city or town, county or parish, state and ZIP code where the damaged or destroyed property was located at

the time of the disaster.

Part II Revocation of Prior Election

By providing all of the information below and attaching this Section D to an amended return for the preceding tax year which eliminates the previous

disaster loss deduction, you hereby revoke a prior election under section 165(i) of the Internal Revenue Code to deduct a loss attributable to a federally

declared disaster that occurred in a federally declared disaster area and was sustained in the disaster year on your tax return for the preceding tax

year.

55 Provide the name or a description of the federally declared disaster and the address of the property that was damaged or destroyed and for

which the election was claimed.

56 Specify the date (mm/dd/yyyy) you filed the prior election, which you are now revoking. (See instructions and note that new rules went into effect

on October 13, 2016.)

57 Enclose your payment or otherwise provide evidence for, or explanation of, your arrangements for the repayment of the amount of any credit or

refund which you received and which resulted from the prior election (which you are now revoking).

Form 4684 (2017)