Form 8818 (Rev. December 2007) F8818

User Manual: 8818

Open the PDF directly: View PDF ![]() .

.

Page Count: 2

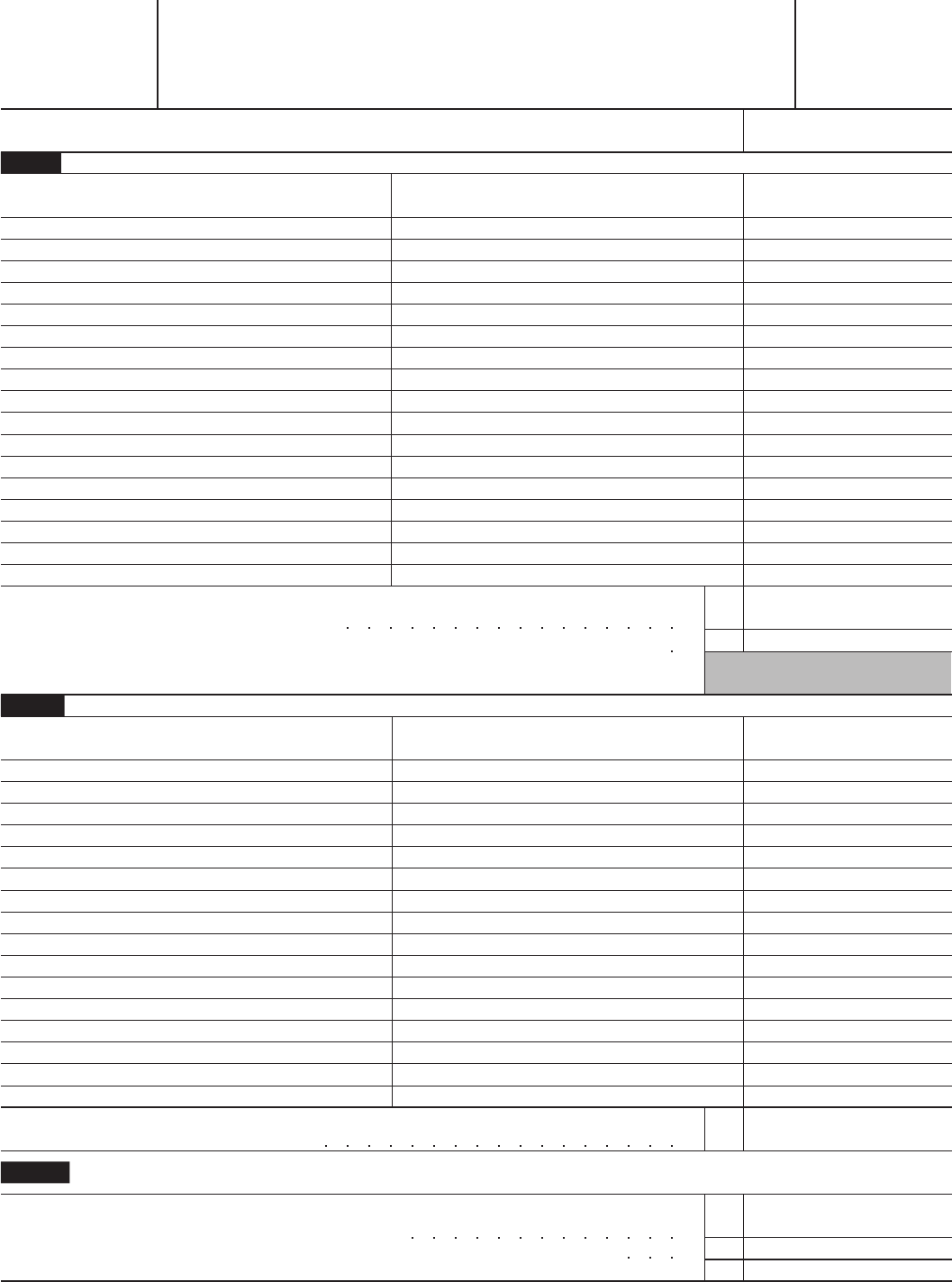

Optional Form To Record Redemption of

Series EE and I U.S. Savings Bonds Issued After 1989

Form

8818

OMB No. 1545-0074

(Rev. December 2007)

Department of the Treasury

Internal Revenue Service

©Keep for your records. Do not send to the IRS.

©See instructions on back.

Date cashed

Name

(b) Issue date

(must be after 1989)

(c) Face value

(a) Serial number

1

5

Add the amounts in column (c) of line 4. This is your cost of the series I bonds and

electronic series EE bonds cashed

5

Total redemption proceeds from the bonds listed in Parts I and II. Be sure to get this

figure from the teller when you cash the bonds

6

6

7

Add lines 3 and 5. This is your total cost of the bonds listed in Parts I and II

7

8

Subtract line 7 from line 6. This is the total interest on the bonds listed in Parts I and II

8

For Paperwork Reduction Act Notice, see back of form.

Form 8818 (Rev. 12-2007)

Cat. No. 10097L

(For Individuals With Qualified Higher Education Expenses)

Part I

Part II

Paper Series EE Bonds

Part III

Series I Bonds and Electronic Series EE Bonds

(b) Issue date (must be after 1989)

(c) Face value

(a) Serial number

4

Total Redemption Proceeds and Interest

2

2

Add the amounts in column (c) of line 1 3

Multiply line 2 by 50% (.50). This is your cost of the paper series EE bonds cashed

3

Next: If you also cashed series I bonds or electronic series EE bonds, go to Part II.

Otherwise, skip Part II and go to Part III.

Form 8818 (Rev. 12-2007)

Page 2

Specific Instructions

Line 1

For each paper series EE bond issued after 1989, enter

the correct information for columns (a), (b), and (c) of

line 1.

The average time and expenses required to

complete and file this form will vary depending on

individual circumstances. For the estimated averages,

see the instructions for your income tax return.

Use a separate Form 8818 each time you cash

series EE or series I bonds issued after 1989. If you

choose not to use Form 8818 but intend to exclude

the interest from your income, you should keep records

that include the information asked for on this form.

Bonds That Qualify for Exclusion

If you have suggestions for making this form simpler,

we would be happy to hear from you. See the

instructions for your income tax return.

Line 8

Qualified Higher Education Expenses

You may be able to exclude this interest from your

income. See Form 8815 for details.

General Instructions

Purpose of Form

Note. Keep Form 8818 for your records. Do not send it

to the IRS.

Use Form 8818 to keep a record of the post-1989

series EE and I bonds you cash. You will need the

information on this form to complete Form 8815,

Exclusion of Interest From Series EE and I U.S.

Savings Bonds Issued After 1989. Form 8815 is used

to figure the amount of interest you can exclude from

your income when you file your income tax return. The

instructions for your tax return will tell you how to take

the exclusion.

Additional Information

Note. Interest on U.S. savings bonds is exempt from

state and local income taxes.

If you cashed series EE or series I U.S. savings bonds

that were issued after 1989 and you paid qualified

higher education expenses during the year, you may

be able to exclude from income part or all the interest

on those bonds.

To qualify for the exclusion, the bonds must have been

issued after 1989 in your name, or, if you are married,

they may be issued in your name and your spouse’s

name. It does not matter who bought the bonds. Also,

you must have been age 24 or older before the bonds

were issued. A bond bought by a parent and issued in

the name of his or her child who is under age 24 will

not qualify for the exclusion by the parent or the child.

Generally, the interest on the bond will be taxed at the

child’s rate once the child reaches age 18. Prior to

reaching age 18, the interest may be taxed at the

parent’s or the child’s rate depending on the total

amount of the child’s investment income (for example,

interest and dividends).

Qualified higher education expenses include tuition

and fees, but not room and board, required for the

enrollment or attendance at a college, university, or

vocational school. Qualified expenses also include

contributions to a qualified tuition program or to a

Coverdell education savings account. The expenses

must be for you, your spouse, or your dependent.

For more details about the exclusion, including limits

that apply to the amount you may exclude, see

Pub. 550, Investment Income and Expenses, or

Pub. 970, Tax Benefits for Education.

Paperwork Reduction Act Notice. Use of this form is

optional. It is provided to help you figure your tax

liability.

You are not required to provide the information

requested on a form that is subject to the Paperwork

Reduction Act unless the form displays a valid OMB

control number. Books or records relating to a form or

its instructions must be retained as long as their

contents may become material in the administration of

any Internal Revenue law. Generally, tax returns and

return information are confidential, as required by

Internal Revenue Code section 6103.

Note. Before you cash your series EE bonds, separate

the bonds issued after 1989 from the bonds issued

before 1990.

Line 4

For each series I bond and electronic series EE bond

issued after 1989, enter the correct information for

columns (a), (b), and (c) of line 4. Include post-1989

series EE bonds converted from paper to electronic

bonds. Do not include them in Part I.