SF LLD User Guidex Freddie Mac Guide Data Dict

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 33

Single Family Loan-Level Dataset

General User Guide

August 2018

August 2018 Page 2 of 33

Single Family Loan-Level Dataset: General User Guide Single Family Loan-Level Dataset: General User Guide

Introduction ............................................................................................................................. 3

Loan Selection Criteria & Data Overview ............................................................................. 4

Dataset Overview .................................................................................................................... 6

Single Family Loan-Level Dataset ....................................................................................................... 6

Single Family Loan-Level Dataset Sample .......................................................................................... 6

Single Family HARP Loan-Level Dataset ............................................................................................ 6

File Layout & Data Dictionary ................................................................................................ 7

Origination Data File ............................................................................................................................ 7

Monthly Performance Data File ......................................................................................................... 12

Interpreting the Data............................................................................................................. 16

Zero Balance Codes .......................................................................................................................... 17

Valid Values ....................................................................................................................................... 17

Monthly Reporting Period .................................................................................................................. 18

Repurchases ..................................................................................................................................... 21

Modifications ...................................................................................................................................... 22

Actual Loss ........................................................................................................................................ 23

Interpreting HARP Data ..................................................................................................................... 25

Loan level disclosure: Data Masking ................................................................................................. 27

Additional Information ......................................................................................................... 28

A.Dataset for SAS Users ................................................................................................................. 29

B.Dataset for STATA Users ............................................................................................................ 30

C.Dataset for R code users ............................................................................................................. 30

D.HARP Dataset for SAS Users ...................................................................................................... 31

E.HARP Dataset for R Users .......................................................................................................... 32

August 2018 Page 3 of 33

Single Family Loan-Level Dataset: General User Guide Single Family Loan-Level Dataset: General User Guide

Introduction

The information provided in this document serves as a reference for understanding the Single Family

Loan-Level Dataset (the “Dataset”). The Dataset includes:

Loan-level origination, monthly loan performance, and actual loss data on a portion of the fully

amortizing 30-year fixed-rate1 Single Family mortgages2 that Freddie Mac acquired with

origination dates from 1999 to the Origination Cutoff Date (see Release Notes for details).

Loan-level origination, monthly loan performance, and actual loss data on a portion of the fully

amortizing 15- and 20-year fixed-rate Single Family mortgages that Freddie Mac acquired with

origination dates from January 1, 2005, to the Origination Cutoff Date (see Release Notes for

details).

Freddie Mac is making this Dataset available at the direction of its regulator, the Federal Housing

Finance Agency (FHFA) as part of a larger effort to increase transparency and help investors build

more accurate credit performance models in support of ongoing and future credit risk-sharing

transactions highlighted in FHFA’s 2017 Conservatorship Scorecard.3

This action builds on earlier efforts to improve data transparency, including Freddie Mac’s decision in

June 2011 to make its multifamily loan-level data available and its implementation of the Uniform

Mortgage Data Program launched in 2010 with Fannie Mae and FHFA.

The Dataset is a “living” dataset, and as such may periodically be corrected or updated over time.

Freddie Mac cannot guarantee the Dataset is complete or error-free, and use of the Dataset is entirely

at your own risk. Freddie Mac will have no liability to you or any third-party for or arising out of your use

of the Dataset. The Dataset is provided on an “as is”, as available basis, and Freddie Mac expressly

disclaims all warranties with respect thereto, including, without limitation, warranties of non-

infringement, merchantability and fitness for a particular purpose. Freddie Mac does not warrant that

the data will be error-free, corrected or provided free of interruption. No oral or written information,

advice or representations provided by Freddie Mac or any of its officers, directors, employees, agents,

or subcontractors will create a warranty.

1 For loans originated prior to 1/1/2005 the population of 30-year fixed-rate mortgages includes loans with original loan terms

between 300 months (25-year) and 420 months (35-year). For loans originated on/after 1/1/2005, the dataset includes all

fixed loans regardless of term.

2 The terms “mortgage(s)” and “loan(s)” are used interchangeably throughout the document.

3 The 2018 Conservatorship Scorecard can be found at: https://www.fhfa.gov/AboutUs/Reports/ReportDocuments/2018-

Scorecard-12212017.pdf

August 2018 Page 4 of 33

Single Family Loan-Level Dataset: General User Guide Single Family Loan-Level Dataset: General User Guide

Loan Selection Criteria & Data Overview

Freddie Mac’s Single Family Loan-Level Dataset contains loans meeting the following criteria:

Mortgages originated from January 1, 1999, through the “Origination Cutoff Date”, with monthly

loan performance data through the “Performance Cutoff Date,” that were sold to Freddie Mac or

that back Freddie Mac Participation Certificates (PCs). See Release Notes for Origination and

Performance Cutoff Dates4.

Fully amortizing 15-, 20-, and 30-year fixed-rate mortgages1.

Mortgages categorized as having verified or waived documentation (i.e. “full documentation”)5.

The following types of mortgages were excluded from the Dataset:

Adjustable Rate Mortgages (ARMs), Initial Interest, balloons, and any mortgages with step rates

Government-insured mortgages, including Federal Housing Administration/Veterans Affairs

(FHA/VA), Guaranteed Rural Housing (GRH), and HUD-Guaranteed Section 184 Native

American mortgages

Home Possible®/Home Possible Neighborhood Solution® Mortgages and other affordable

mortgages (including lender branded affordable loan products)

Mortgages delivered to Freddie Mac under alternate agreements

Mortgages for which the documentation is not verified or not waived

Mortgages associated with Mortgage Revenue Bonds purchased by Freddie Mac

Mortgages delivered to Freddie Mac with credit enhancements other than primary mortgage

insurance, with the exception of certain lender-negotiated credit enhancements

Loan performance information in the Dataset includes the monthly loan balance, delinquency status

and certain information up to and including the earliest of the following termination events:

Prepaid or Matured (Voluntary Payoff)

Foreclosure Alternative Group (Short Sale, Third Party Sale, Charge Off or Note Sale)

Repurchase prior to Property Disposition

4 The Dataset includes loans which may have been seasoned prior to purchase by Freddie Mac, as well as certain types of

mortgages, such as construction-to-perm loans (also known as “converted mortgages”) and seller-owned modified mortgages,

which are reported to Freddie Mac with the original note date of the mortgage and the converted or modified First Payment

Date.

5 Generally, Freddie Mac requires that Sellers of mortgage loans document or verify loan application information about the

Borrower’s income, assets and employment. Sellers’ documentation or verification can take several forms; for example,

Sellers may require that a Borrower provide pay stubs or W-2 or 1099 forms to verify employment and income and depository

and brokerage statements to verify assets. In some cases, because of the measured creditworthiness of the Borrower (for

example, credit score) and loan attributes (for example, a refinance loan or low loan-to-value ratio), a Seller may require a

reduced level of documentation or verification or may waive its general documentation or verification requirements. In other

cases, pursuant to programs offered by lenders, Borrowers may elect to provide a reduced level of documentation or

verification or may elect to provide no documentation or verification of some or all of this information in a loan application.

Standards to qualify for reduced levels of documentation and for waivers of documentation based on creditworthiness, and

what constitutes a material reduced level of documentation, may vary among Sellers. If Freddie Mac agrees with a Seller’s

decision to underwrite the Borrower using reduced documentation or no documentation, Freddie Mac will generally require that

Sellers deliver a special code in connection with the delivery of such mortgage loans. Freddie Mac monitors the performance

of such loans to determine whether they continue to perform at least as well as traditional full documentation loans.

August 2018 Page 5 of 33

Single Family Loan-Level Dataset: General User Guide Single Family Loan-Level Dataset: General User Guide

REO Disposition

Actual loss data components of net sale proceeds, expenses, MI recoveries, non-MI recoveries, and

due date of last paid installment (DDLPI) will be disclosed at property disposition. Current Deferred

UPB, which is also a component of actual loss, will be disclosed for the months it is legally effective.

Mortgages which were repurchased after a termination event but prior to the Performance Cutoff Date

are identified in the Dataset. Mortgages that were modified from the original loan terms are also

identified in the Dataset. Only approved and closed workouts (e.g., short sales, modifications, and

deeds-in-lieu of foreclosure) prior to the Performance Cutoff Date are included in the Dataset. The rules

for how these loans are identified and tracked in the Dataset are explained in more detail in the “How to

Interpret the Data” section of this document.

Freddie Mac is the Master Servicer for all loans in the Dataset.

August 2018 Page 6 of 33

Single Family Loan-Level Dataset: General User Guide Single Family Loan-Level Dataset: General User Guide

Dataset Overview

Single Family Loan-Level Dataset

For each calendar quarter, there is one file containing loan origination data and one file containing

monthly performance data for each loan in the origination data file. There are cases when the loan is in

the origination file but not in the performance file. This would happen when the loan gets paid off in the

month of origination or before first cycle begins. Refer to the File Layout and Data Dictionary section of

this document for more information on what data is contained in each file.

Single Family Loan-Level Dataset Sample

Freddie Mac has created a smaller dataset for those who may not require, or have the capability, to

download the full Dataset. The sample dataset is a simple random sample6 of 50,000 loans selected

from each full vintage year and a proportionate number of loans from each partial vintage year of the

full Single Family Loan-Level Dataset. Each vintage year has one origination data file and one

corresponding monthly performance data file, containing the same loan-level data fields as those

included in the full Dataset. Due to the size of the dataset, the data has been broken up and

compressed as detailed below. The files are organized chronologically by year and quarter.

Single Family HARP Loan-Level Dataset

Freddie Mac’s HARP loan level disclosures are an extension to the Single Family Loan-Level Dataset.

The population includes loans that were in Freddie Mac Single Family Loan Level dataset and went

through the Relief Refinance program between 2009 and 2016, with an LTV at the time of re-finance

above 80. Only loans that remained as Fixed Products following this refinance were included in this

disclosure. HARP files are consolidated into one origination and one performance file and not

separated by year and quarter. The files follow the same file format as the Single Family Loan-Level

Dataset except where noted.

Dataset File Name Format Contents File Type Delimiter

Full historical_data1_QnYYYY.zip historical_data1_QnYYYY.txt Origination Data Pipe (“|”)

historical_data1_time_QnYYYY.txt Monthly Performance Data

Sample sample_YYYY.zip sample_orig_YYYY.txt Origination Data

Pipe (“|”)

Sample_svcg_YYYY.txt Monthly Performance Data

HARP harp_historical_data1.zip harp_historical_data1.txt Origination Data

harp_historical_data1_time.txt Monthly Performance Data Pipe (“|”)

A comparison of the full and sample datasets across key loan attributes and performance metrics by

vintage year is available to assist with data validation at the following website:

6 A sampling method by which a subset of a population is chosen, where each member of the subset has an equal probability

of being chosen once from the larger population. A simple random sample is meant to be an unbiased representation of the

larger population.

August 2018 Page 7 of 33

Single Family Loan-Level Dataset: General User Guide Single Family Loan-Level Dataset: General User Guide

http://www.freddiemac.com/research/pdf/summary_statistics.pdf

File Layout & Data Dictionary

This section provides information regarding the layout of each origination and monthly performance

data file, in addition to information about each of the data elements contained within each file type.

Instructions for reading the data using two popular statistical packages are included in this User Guide,

and can be found in the Appendix (A and B). The information is structured as follows:

Field Description

Column Position Position of the Column in a Microsoft Excel Worksheet.

Formal Name and Definition Name and definition of the loan-level data element.

Valid Values/Calculations Allowable values for the specific data field and the calculations

used

(

if applicable

)

.

Type (Data Type) The type of data found in each column:

Alpha – contains only letters

Alpha-numeric – contains letters and numbers

Numeric – contains only numbers

Date – represents a specific date (Y = Year, M = Month)

Example: YYYYMM

(

201207

)

=Jul

y

2012

Length Represents the maximum number of characters allowed for the

data field.

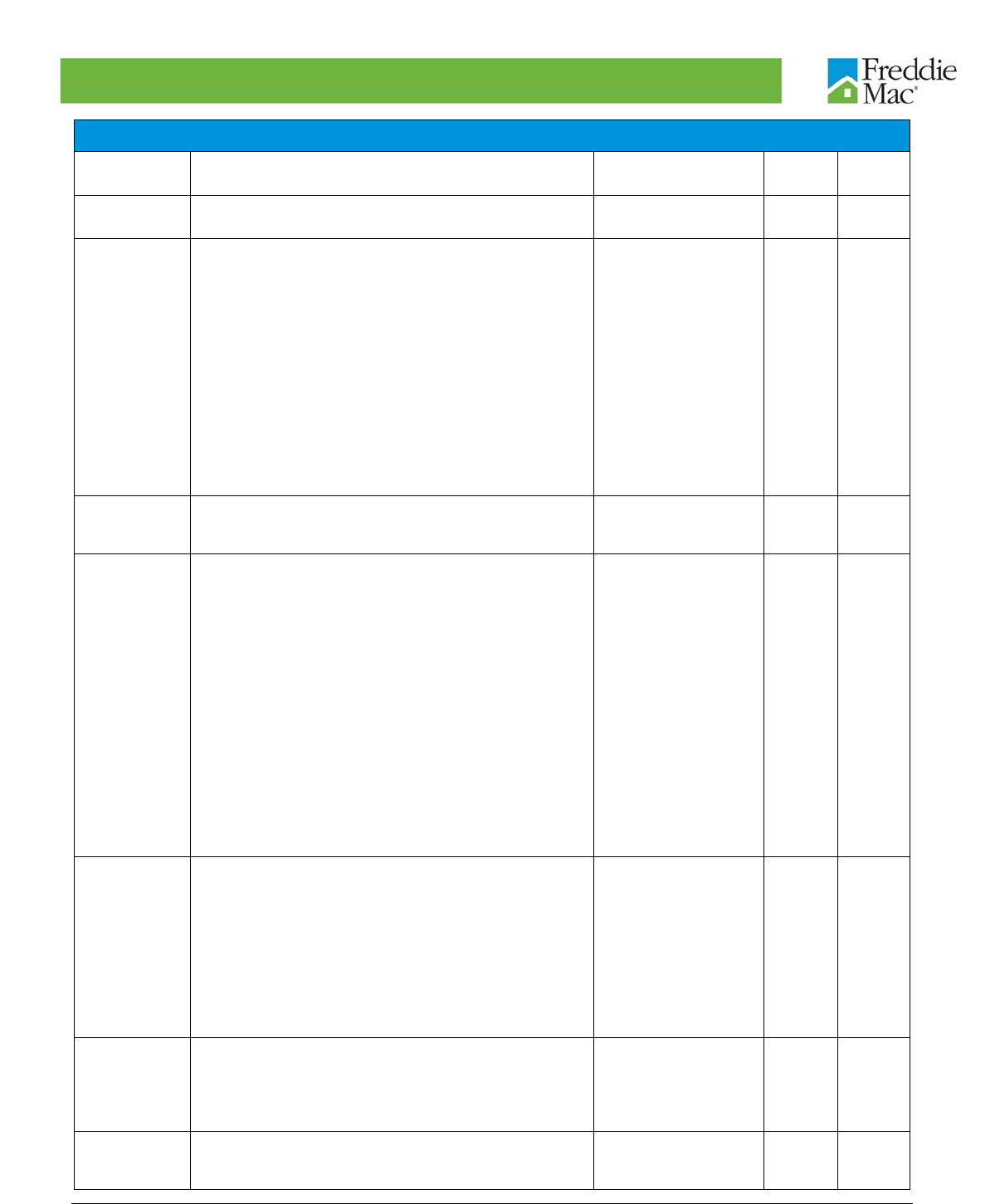

Origination Data File

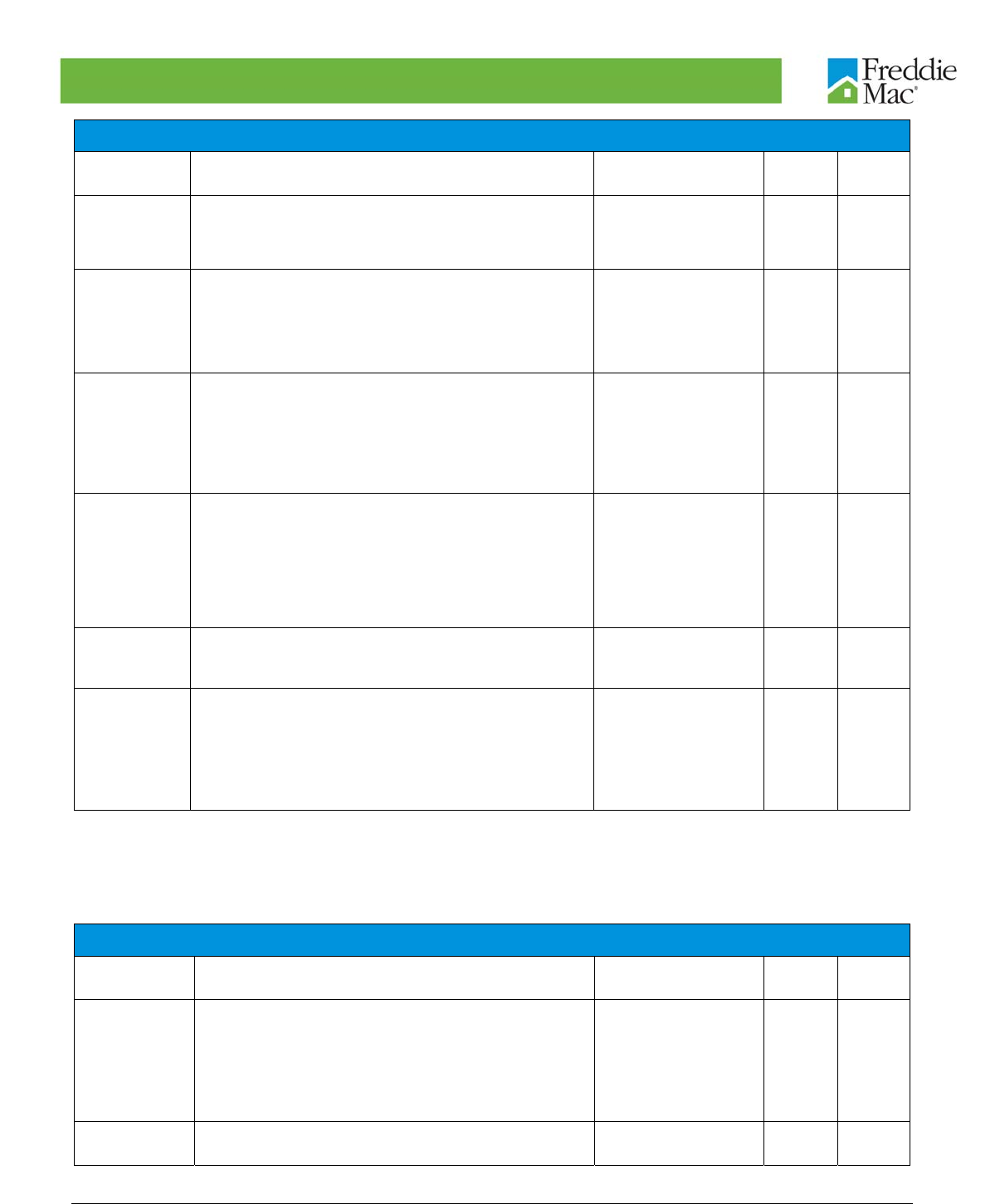

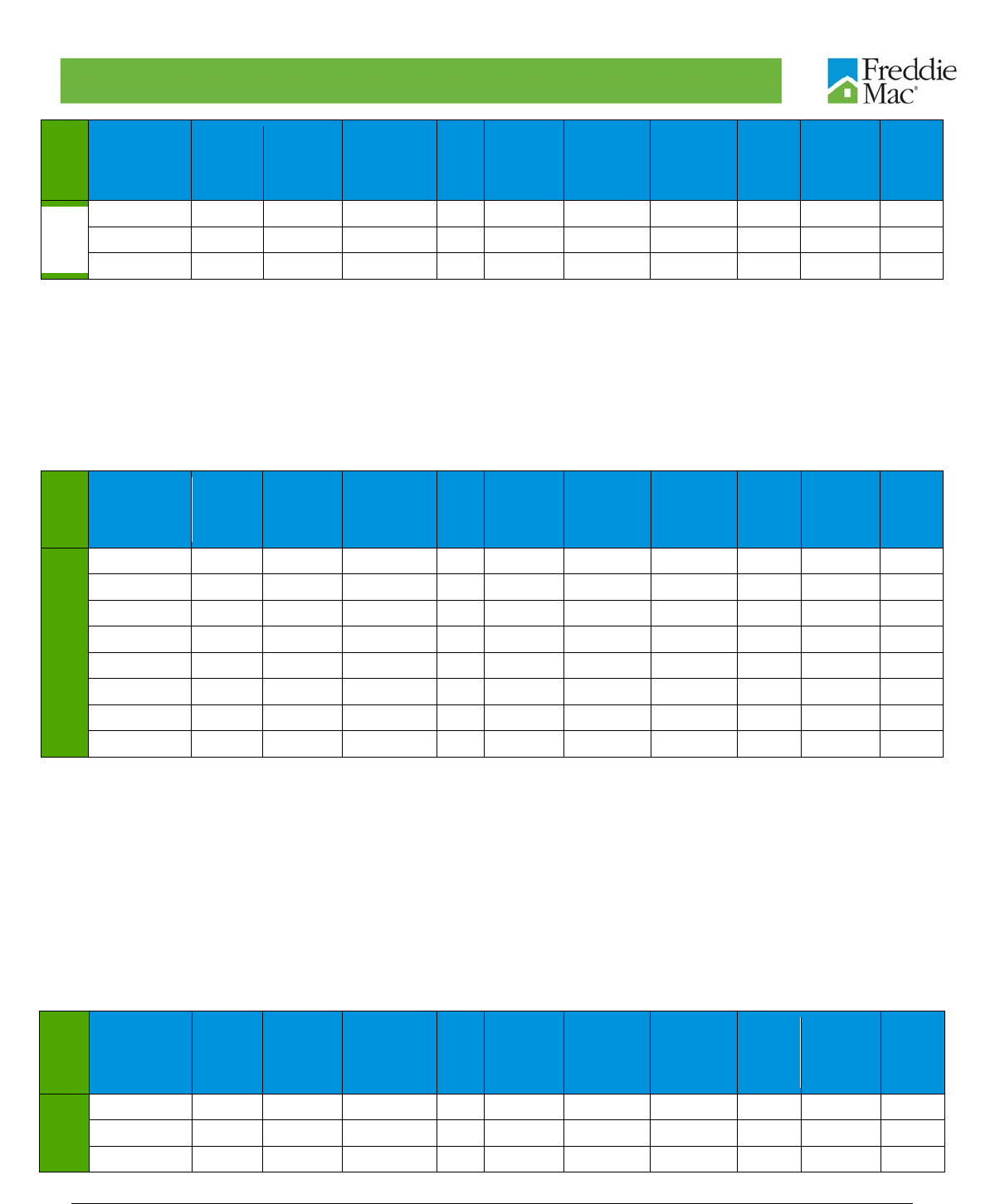

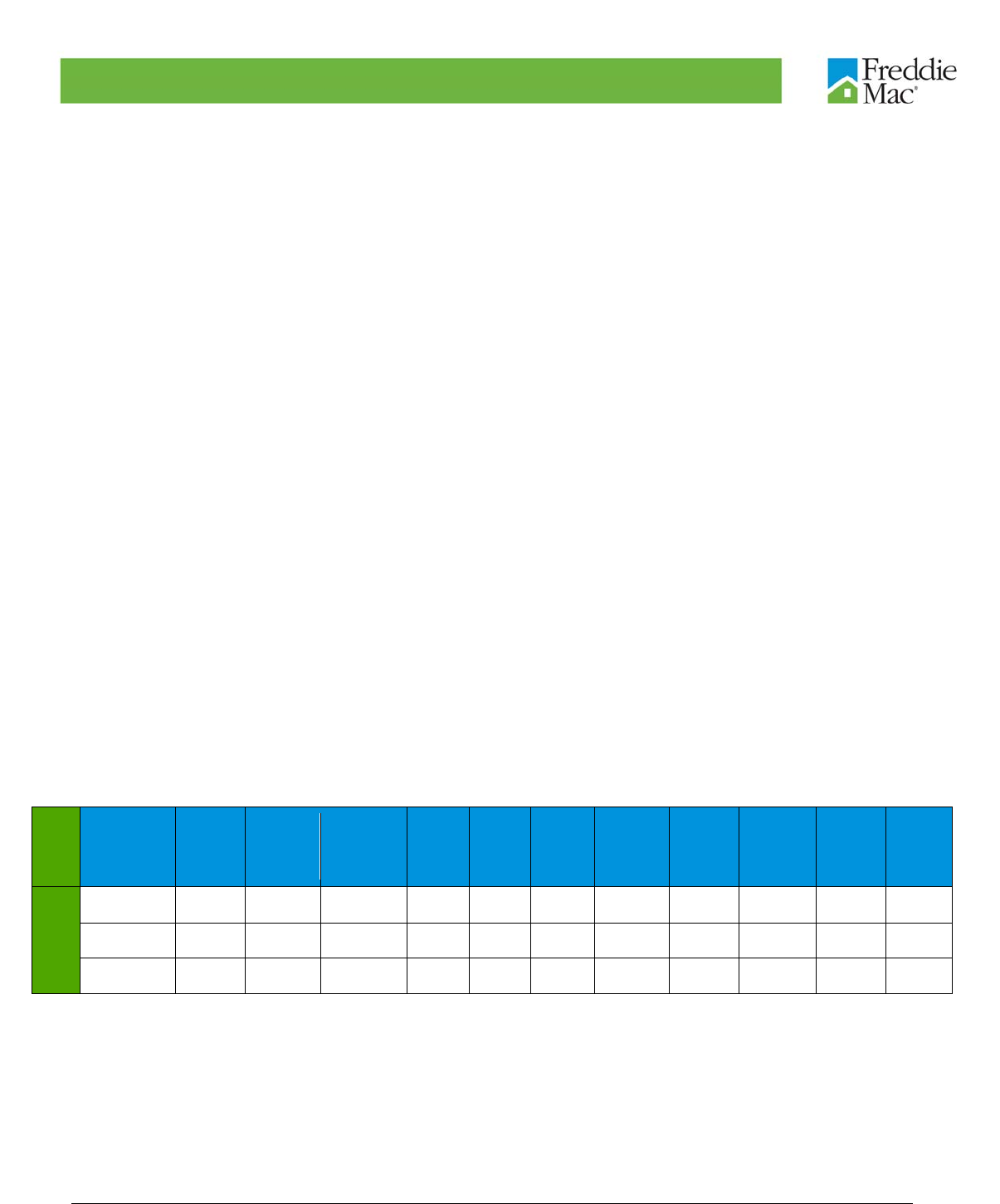

ORIGINATION DATA FILE

COLUMN

POSITION7 FORMAL NAME AND DEFINITION VALID VALUES/

CALCULATIONS TYPE LENGTH

1 CREDIT SCORE - A number, prepared by third parties, summarizing

the borrower’s creditworthiness, which may be indicative of the

likelihood that the borrower will timely repay future obligations.

Generally, the credit score disclosed is the score known at the time of

acquisition and is the score used to originate the mortgage.

301 - 850

9999 = Not Available,

if Credit Score is < 301

or > 850.

Numeric 4

7 The header record row has been removed from all files in the Dataset and sample dataset; the position of columns in each

file remains unchanged.

August 2018 Page 8 of 33

Single Family Loan-Level Dataset: General User Guide Single Family Loan-Level Dataset: General User Guide

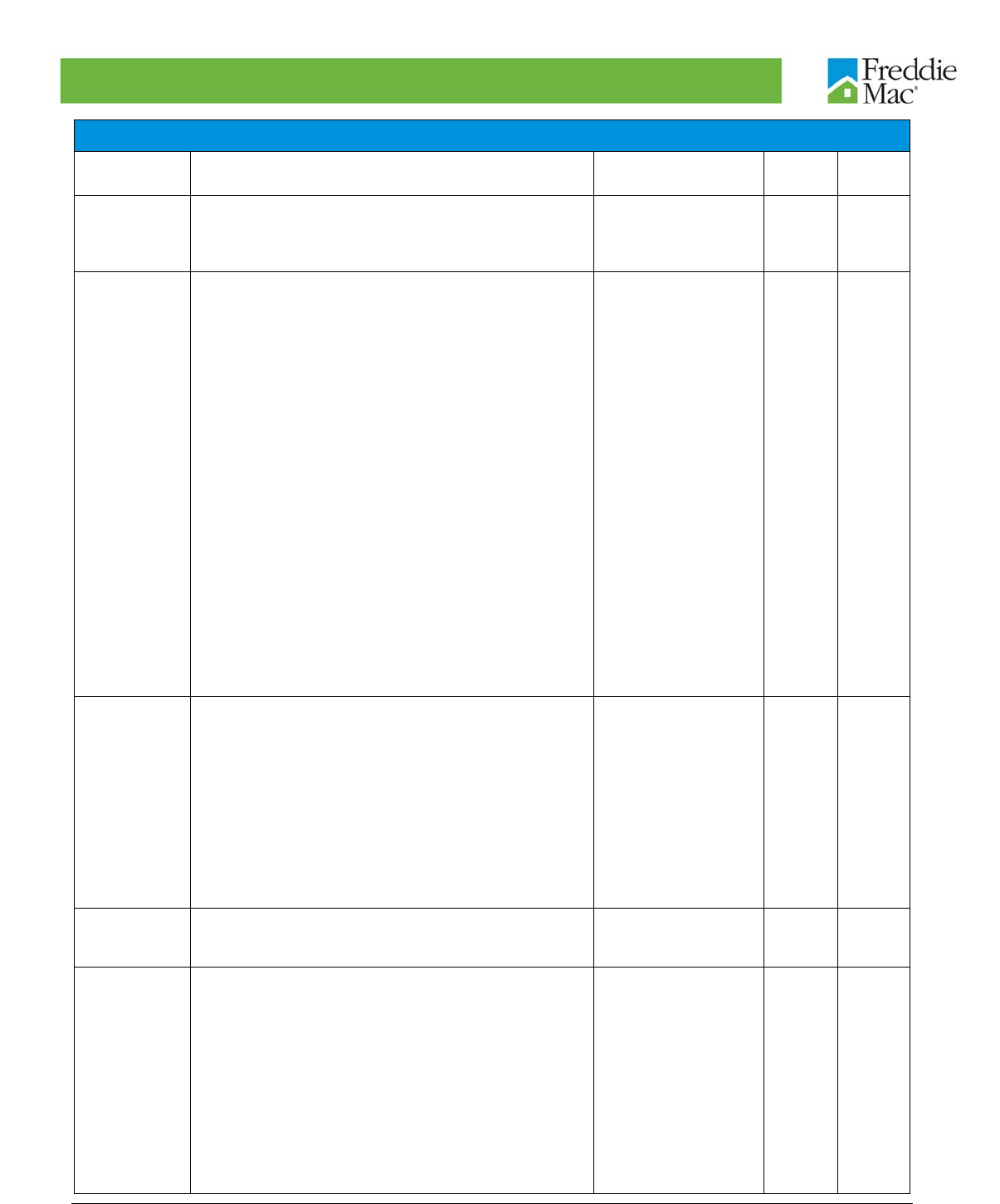

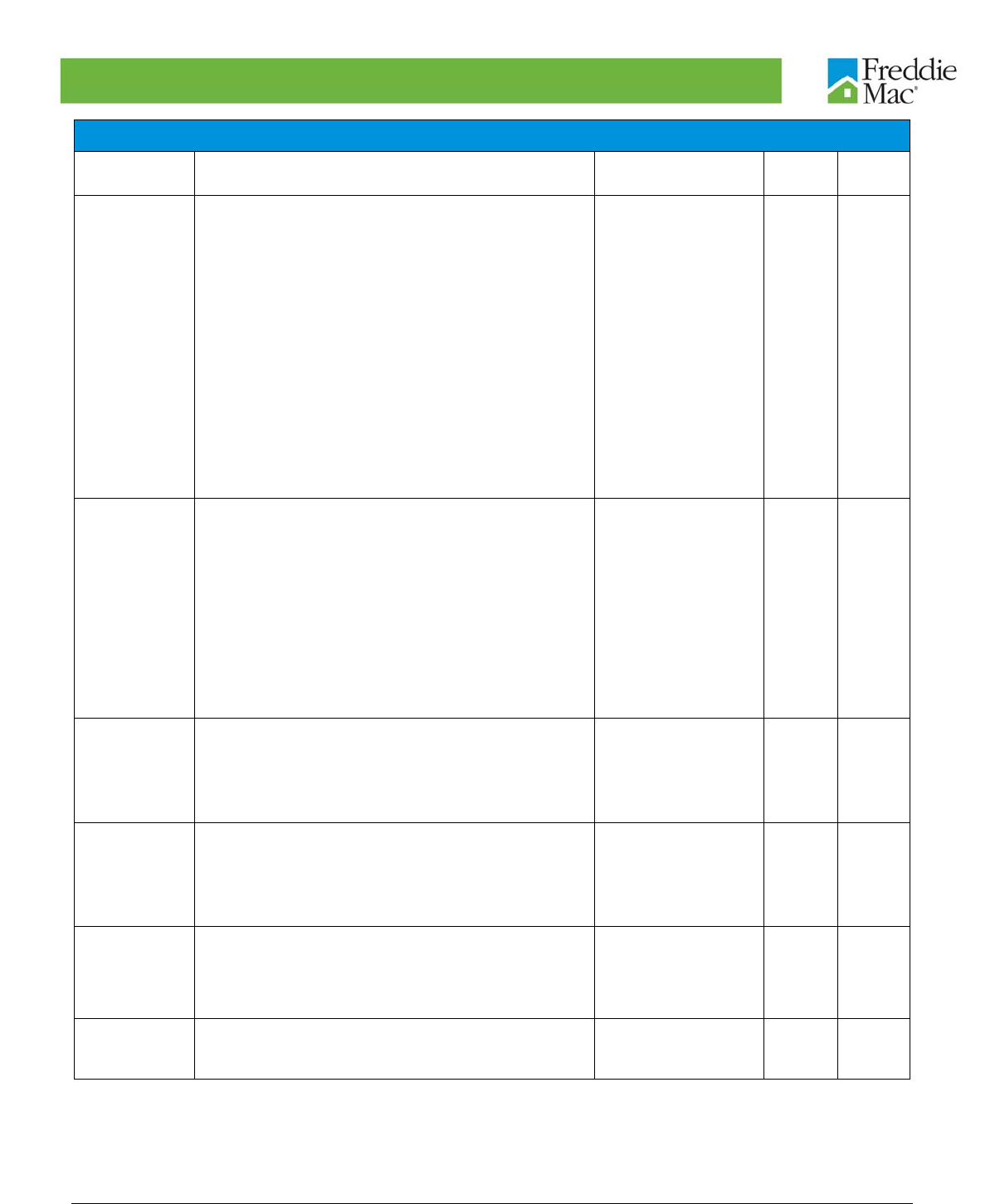

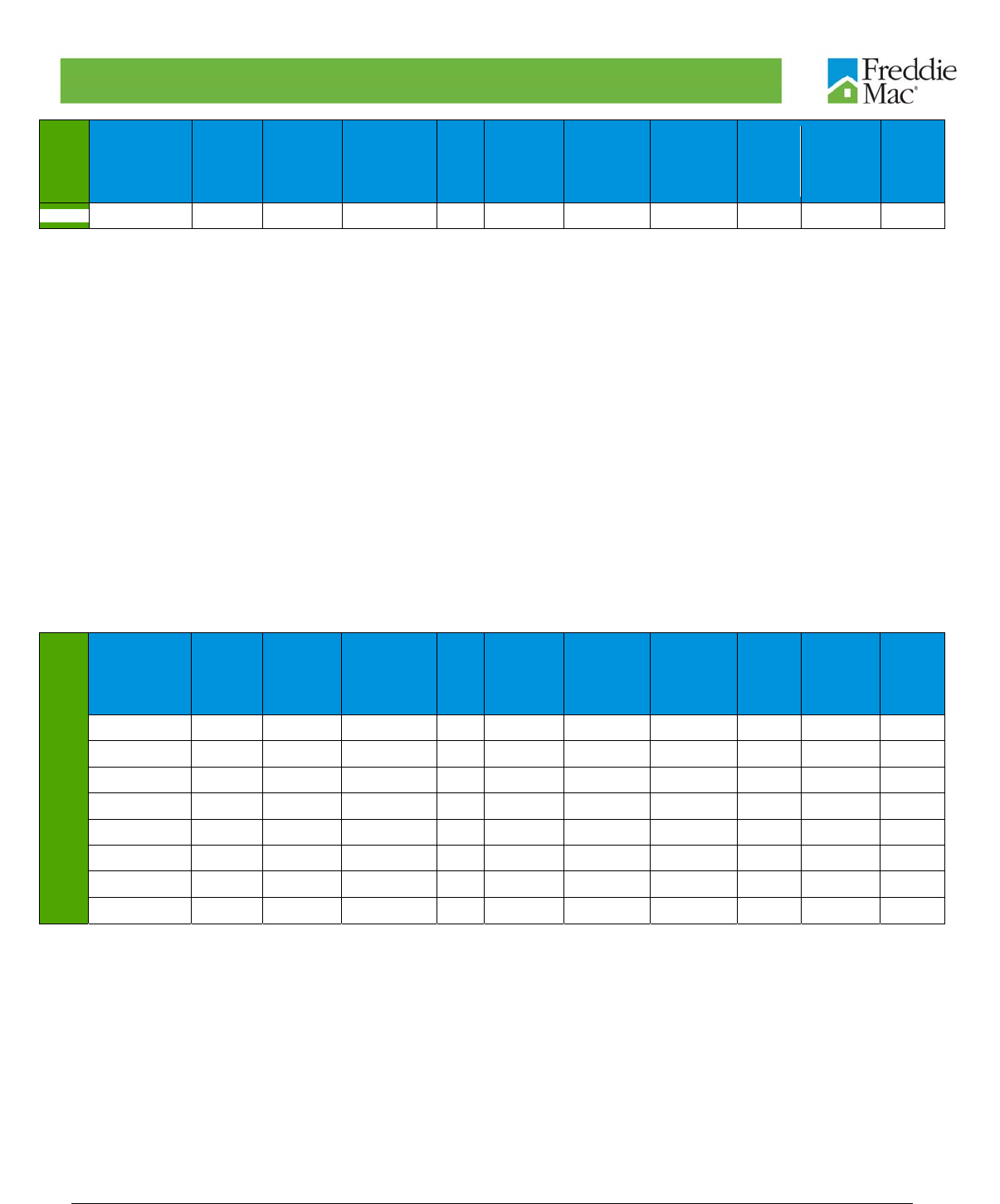

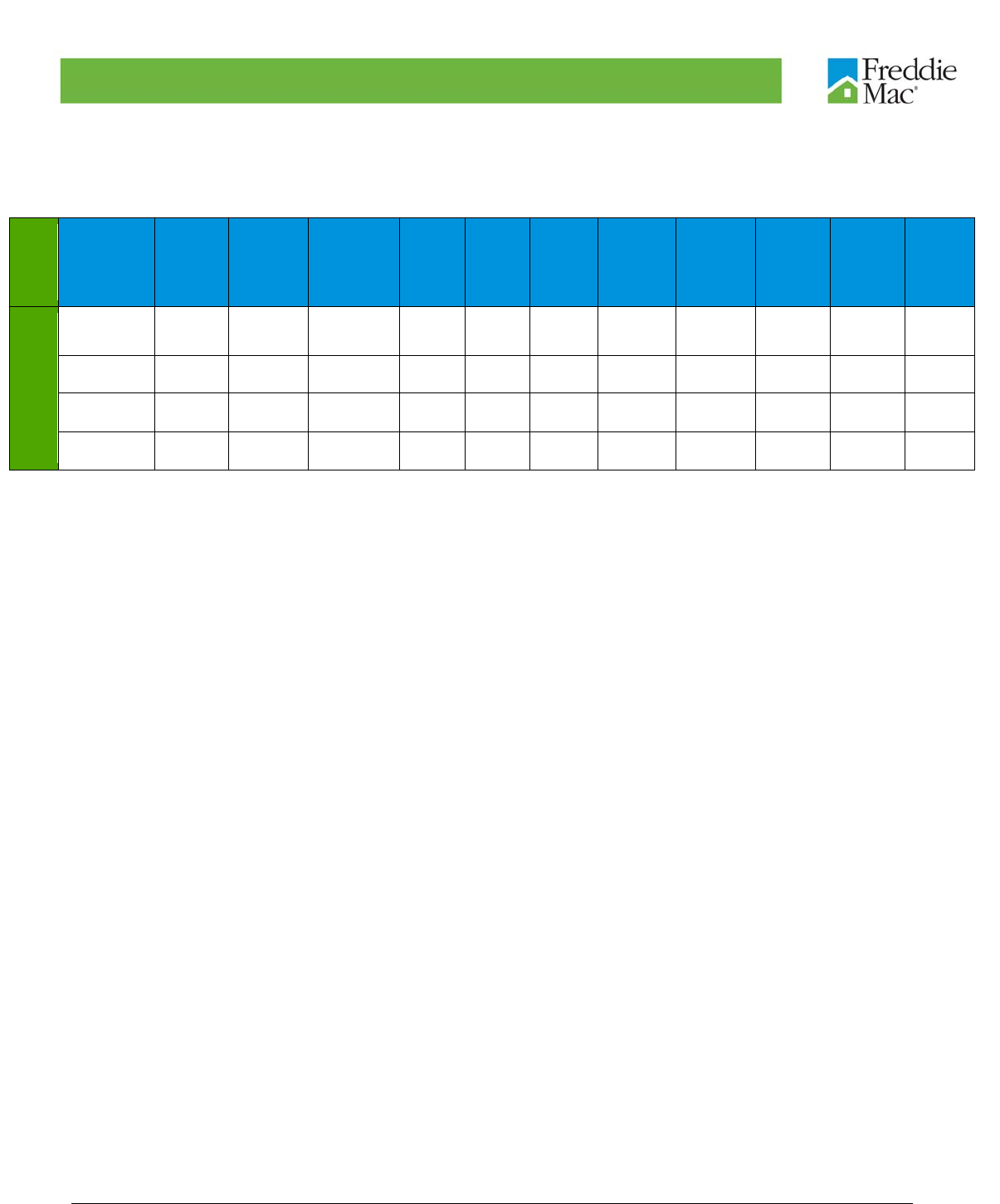

ORIGINATION DATA FILE

COLUMN

POSITION7 FORMAL NAME AND DEFINITION VALID VALUES/

CALCULATIONS TYPE LENGTH

2 FIRST PAYMENT DATE - The date of the first scheduled mortgage

payment due under the terms of the mortgage note.

YYYYMM Date

6

3 FIRST TIME HOMEBUYER FLAG - Indicates whether the Borrower,

or one of a group of Borrowers, is an individual who (1) is purchasing

the mortgaged property, (2) will reside in the mortgaged property as a

primary residence and (3) had no ownership interest (sole or joint) in a

residential property during the three-year period preceding the date of

the purchase of the mortgaged property. With certain limited

exceptions, a displaced homemaker or single parent may also be

considered a First-Time Homebuyer if the individual had no ownership

interest in a residential property during the preceding three-year period

other than an ownership interest in the marital residence with a

spouse.

Investment Properties, Second Homes and Refinance transactions

are not eligible to be considered First-Time Homebuyer transactions.

Therefore First Time Homebuyer does not apply and will be disclosed

as “Not Applicable”, which will be indicated by a blank space.

Y = Yes

N = No

9 = Not Available or

Not Applicable

Alpha 1

4 MATURITY DATE - The month in which the final monthly payment on

the mortgage is scheduled to be made as stated on the original

mortgage note.

YYYYMM Date

6

5 METROPOLITAN STATISTICAL AREA (MSA) OR

METROPOLITAN DIVISION - This disclosure will be based on the

designation of the Metropolitan Statistical Area or Metropolitan

Division based on 2010 census (for Mar 2013 and May 2013

releases) and 2013 census (for Aug 2013 and Dec 2013 releases)

data. Metropolitan Statistical Areas (MSAs) are defined by the United

States Office of Management and Budget (OMB) and have at least

one urbanized area with a population of 50,000 or more inhabitants.

OMB refers to an MSA containing a single core with a population of

2.5 million or more, which may be comprised of groupings of counties,

as a Metropolitan Division.

If an MSA applies to a mortgaged property, the applicable five-digit

value is disclosed; however, if the mortgaged property also falls within

a Metropolitan Division classification, the applicable five-digit value for

the Metropolitan Division takes precedence and is disclosed instead.

Changes and/or updates in designations of MSAs or Metropolitan

Division will not be reflected in the Single Family Historical Dataset.

Metropolitan Division

or MSA Code.

Space (5) = Indicates

that the area in which

the mortgaged

property is located is

a) neither an MSA nor

a Metropolitan

Division, or b)

unknown.

Numeric 5

6 MORTGAGE INSURANCE PERCENTAGE (MI %) - The percentage

of loss coverage on the loan, at the time of Freddie Mac’s purchase of

the mortgage loan that a mortgage insurer is providing to cover losses

incurred as a result of a default on the loan. Only primary mortgage

insurance that is purchased by the Borrower, lender or Freddie Mac is

disclosed. Mortgage insurance that constitutes “credit enhancement”

that is not required by Freddie Mac’s Charter is not disclosed.

Amounts of mortgage insurance reported by Sellers that are less than

1% or greater than 55% will be disclosed as “Not Available,” which will

be indicated 999. No MI will be indicated by three zeros.

1% - 55%

000 = No MI

999 = Not Available

Numeric 3

7 NUMBER OF UNITS - Denotes whether the mortgage is a one-, two-,

three-, or four-unit property.

1 = one-unit

2 = two-unit

3 = three-unit

4 = four-unit

99 = Not Available

Numeric 2

8 OCCUPANCY STATUS - Denotes whether the mortgage type is

owner occupied, second home, or investment property.

P = Primary

Residence

Alpha 1

August 2018 Page 9 of 33

Single Family Loan-Level Dataset: General User Guide Single Family Loan-Level Dataset: General User Guide

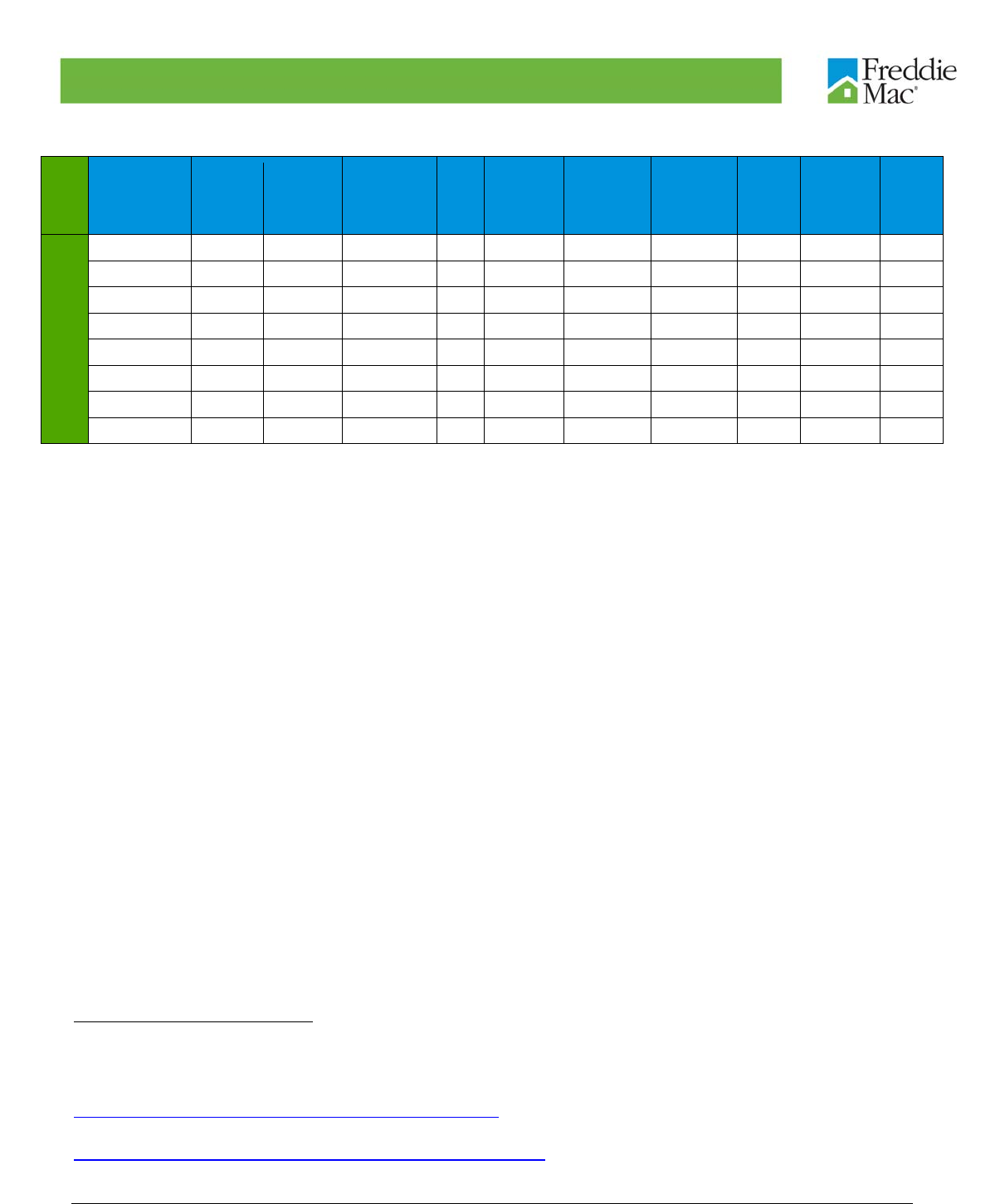

ORIGINATION DATA FILE

COLUMN

POSITION7 FORMAL NAME AND DEFINITION VALID VALUES/

CALCULATIONS TYPE LENGTH

I = Investment

Property

S = Second Home

9 = Not Available

9 ORIGINAL COMBINED LOAN-TO-VALUE (CLTV) – In the case of a

purchase mortgage loan, the ratio is obtained by dividing the original

mortgage loan amount on the note date plus any secondary mortgage

loan amount disclosed by the Seller by the lesser of the mortgaged

property’s appraised value on the note date or its purchase price. In

the case of a refinance mortgage loan, the ratio is obtained by dividing

the original mortgage loan amount on the note date plus any

secondary mortgage loan amount disclosed by the Seller by the

mortgaged property’s appraised value on the note date. If the

secondary financing amount disclosed by the Seller includes a home

equity line of credit, then the CLTV calculation reflects the disbursed

amount at closing of the first lien mortgage loan, not the maximum

loan amount available under the home equity line of credit. In the

case of a seasoned mortgage loan, if the Seller cannot warrant that

the value of the mortgaged property has not declined since the note

date, Freddie Mac requires that the Seller must provide a new

appraisal value, which is used in the CLTV calculation. In certain

cases, where the Seller delivered a loan to Freddie Mac with a special

code indicating additional secondary mortgage loan amounts, those

amounts may have been included in the CLTV calculation.

If the LTV is < 80 or > 200 or Not Available, set the CLTV to ‘Not

Available.’ If the CLTV is < LTV, set the CLTV to ‘Not Available.’

This disclosure is subject to the widely varying standards originators

use to verify Borrowers’ secondary mortgage loan amounts and will

not be updated.

0% - 200%

999 = Not Available

Full

Dataset:

Numeric

Literal

Decimal;

Sample

Dataset:

Numeric

Full

Dataset:

7;

Sample

Dataset: 3

10 ORIGINAL DEBT-TO-INCOME (DTI) RATIO - Disclosure of the debt

to income ratio is based on (1) the sum of the borrower's monthly debt

payments, including monthly housing expenses that incorporate the

mortgage payment the borrower is making at the time of the delivery

of the mortgage loan to Freddie Mac, divided by (2) the total monthly

income used to underwrite the loan as of the date of the origination of

the such loan.

Ratios greater than 65% are indicated that data is Not Available. All

loans in the HARP dataset will be disclosed as Not Available.

This disclosure is subject to the widely varying standards originators

use to verify Borrowers’ assets and liabilities and will not be updated.

0%<DTI<=65%

999 = Not Available

HARP ranges:

999 = Not Available

Numeric 3

11 ORIGINAL UPB - The UPB of the mortgage on the note date.

Amount will be

rounded to the

nearest $1,000.

Numeric 12

12 ORIGINAL LOAN-TO-VALUE (LTV) - In the case of a purchase

mortgage loan, the ratio obtained by dividing the original mortgage

loan amount on the note date by the lesser of the mortgaged

property’s appraised value on the note date or its purchase price.

In the case of a refinance mortgage loan, the ratio obtained by dividing

the original mortgage loan amount on the note date and the

mortgaged property’s appraised value on the note date.

In the case of a seasoned mortgage loan, if the Seller cannot warrant

that the value of the mortgaged property has not declined since the

note date, Freddie Mac requires that the Seller must provide a new

appraisal value, which is used in the LTV calculation.

6% - 105%

999 = Not Available

HARP ranges:

81% - 999%

999 = Not Available

Numeric 3

August 2018 Page 10 of 33

Single Family Loan-Level Dataset: General User Guide Single Family Loan-Level Dataset: General User Guide

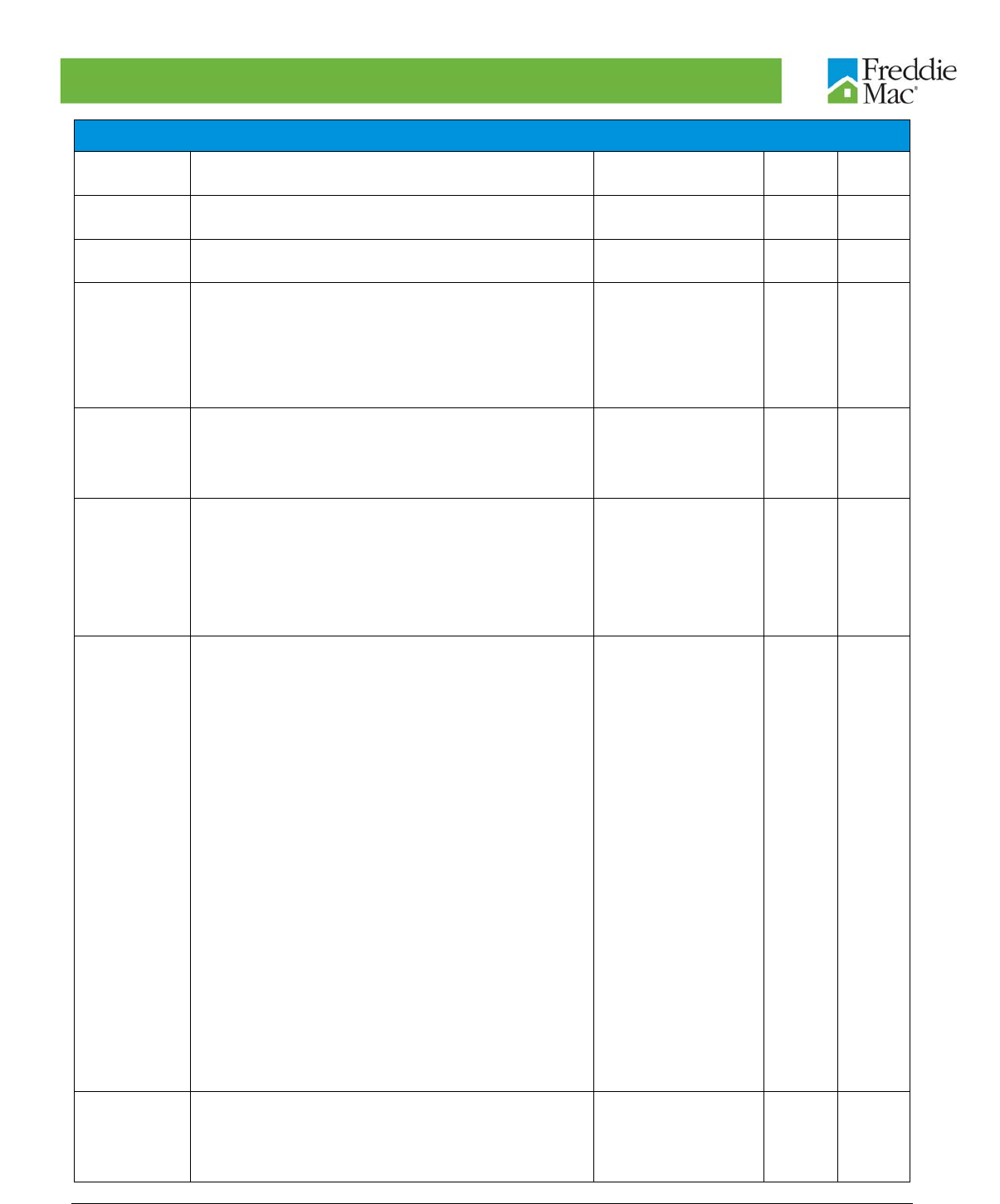

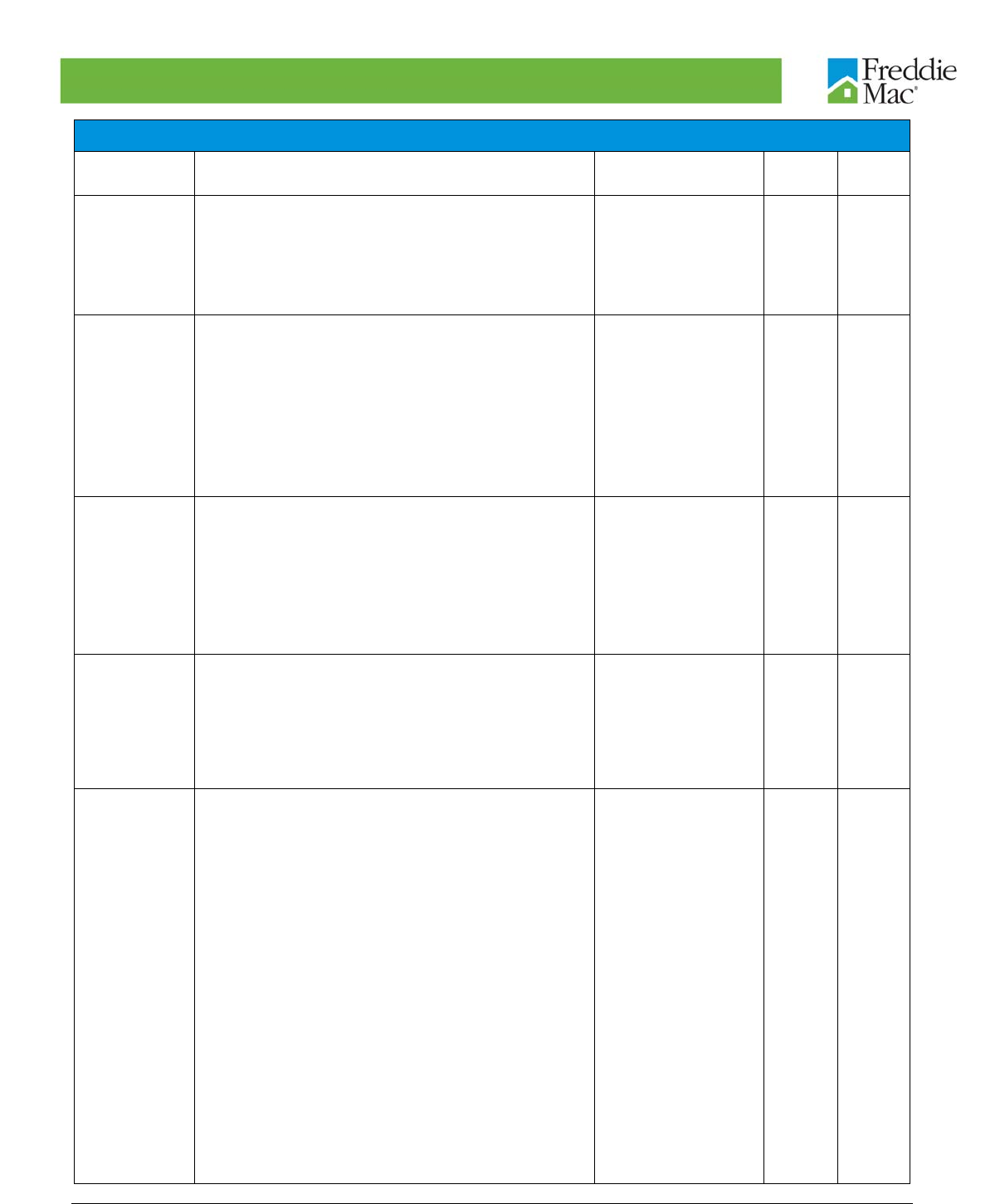

ORIGINATION DATA FILE

COLUMN

POSITION7 FORMAL NAME AND DEFINITION VALID VALUES/

CALCULATIONS TYPE LENGTH

Ratios below 6% or greater than 105% will be disclosed as “Not

Available,” indicated by 999. For loans in the HARP dataset, LTV

ratios less than or equal to 80% and greater than 999% will be

disclosed as Not Available.

13 ORIGINAL INTEREST RATE - The original note rate as indicated on

the mortgage note. Numeric

Literal

decimal

6

14 CHANNEL - Disclosure indicates whether a Broker or Correspondent,

as those terms are defined below, originated or was involved in the

origination of the mortgage loan. If a Third Party Origination is

applicable, but the Seller does not specify Broker or Correspondent,

the disclosure will indicate “TPO Not Specified”. Similarly, if neither

Third Party Origination nor Retail designations are available, the

disclosure will indicate “TPO Not Specified.” If a Broker,

Correspondent or Third Party Origination disclosure is not applicable,

the mortgage loan will be designated as Retail, as defined below.

Broker is a person or entity that specializes in loan originations,

receiving a commission (from a Correspondent or other lender) to

match Borrowers and lenders. The Broker performs some or most of

the loan processing functions, such as taking loan applications, or

ordering credit reports, appraisals and title reports. Typically, the

Broker does not underwrite or service the mortgage loan and

generally does not use its own funds for closing; however, if the

Broker funded a mortgage loan on a lender’s behalf, such a mortgage

loan is considered a “Broker” third party origination mortgage loan.

The mortgage loan is generally closed in the name of the lender who

commissioned the Broker's services.

Correspondent is an entity that typically sells the Mortgages it

originates to other lenders, which are not Affiliates of that entity, under

a specific commitment or as part of an ongoing relationship. The

Correspondent performs some, or all, of the loan processing functions,

such as: taking the loan application; ordering credit reports, appraisals,

and title reports; and verifying the Borrower's income and

employment. The Correspondent may or may not have delegated

underwriting and typically funds the mortgage loans at settlement. The

mortgage loan is closed in the Correspondent's name and the

Correspondent may or may not service the mortgage loan. The

Correspondent may use a Broker to perform some of the processing

functions or even to fund the loan on its behalf; under such

circumstances, the mortgage loan is considered a “Broker” third party

origination mortgage loan, rather than a “Correspondent” third party

origination mortgage loan.

Retail Mortgage is a mortgage loan that is originated, underwritten and

funded by a lender or its Affiliates. The mortgage loan is closed in the

name of the lender or its Affiliate and if it is sold to Freddie Mac, it is

sold by the lender or its Affiliate that originated it. A mortgage loan that

a Broker or Correspondent completely or partially originated,

processed, underwrote, packaged, funded or closed is not considered

a Retail mortgage loan.

For purposes of the definitions of Correspondent and Retail, “Affiliate"

means any entity that is related to another party as a consequence of

the entity, directly or indirectly, controlling the other party, being

controlled by the other party, or being under common control with the

other party.

R = Retail

B = Broker

C = Correspondent

T = TPO Not Specified

9 = Not Available

Alpha

1

15 PREPAYMENT PENALTY MORTGAGE (PPM) FLAG - Denotes

whether the mortgage is a PPM. A PPM is a mortgage with respect to

which the borrower is, or at any time has been, obligated to pay a

penalty in the event of certain repayments of principal.

Y = PPM

N = Not PPM

Alpha 1

August 2018 Page 11 of 33

Single Family Loan-Level Dataset: General User Guide Single Family Loan-Level Dataset: General User Guide

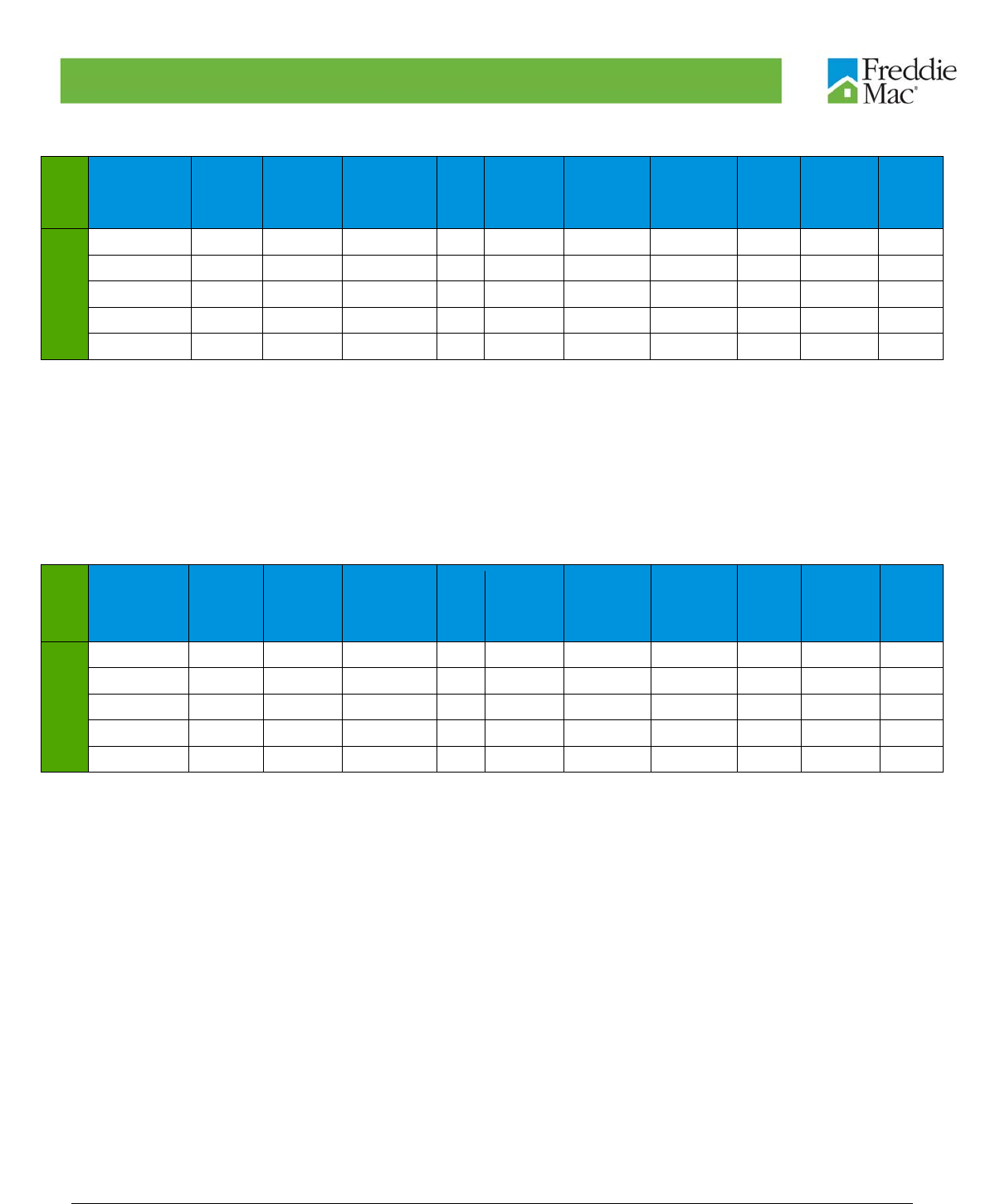

ORIGINATION DATA FILE

COLUMN

POSITION7 FORMAL NAME AND DEFINITION VALID VALUES/

CALCULATIONS TYPE LENGTH

16 PRODUCT TYPE - Denotes that the product is a fixed-rate mortgage. FRM – Fixed Rate

Mortgage

Alpha 5

17 PROPERTY STATE - A two-letter abbreviation indicating the state or

territory within which the property securing the mortgage is located.

AL, TX, VA, etc. Alpha 2

18 PROPERTY TYPE - Denotes whether the property type secured by

the mortgage is a condominium, leasehold, planned unit development

(PUD), cooperative share, manufactured home, or Single Family

home.

If the Property Type is Not Available, this will be indicated by 99.

CO = Condo

PU = PUD

MH = Manufactured

Housing

SF = 1-4 Fee Simple

CP = Co-op

99 = Not Available

Alpha 2

19 POSTAL CODE – The postal code for the location of the mortgaged

property

###00, where “###”

represents the first

three digits of the 5-

digit postal code

Space(5)= Unknown

Numeric 5

20 LOAN SEQUENCE NUMBER - Unique identifier assigned to each

loan. F1YYQnXXXXXX

F1 = product (Fixed

Rate Mortgage);

YYQn = origination

year and quarter; and,

XXXXXX = randomly

assigned digits

Alpha-

numeric 12

21 LOAN PURPOSE - Indicates whether the mortgage loan is a Cash-

out Refinance mortgage, No Cash-out Refinance mortgage, or a

Purchase mortgage.

Generally, a Cash-out Refinance mortgage loan is a mortgage loan in

which the use of the loan amount is not limited to specific purposes. A

mortgage loan placed on a property previously owned free and clear

by the Borrower is always considered a Cash-out Refinance mortgage

loan. Generally, a No Cash-out Refinance mortgage loan is a

mortgage loan in which the loan amount is limited to the following

uses:

Pay off the first mortgage, regardless of its age

Pay off any junior liens secured by the mortgaged property, that were

used in their entirety to acquire the subject property

Pay related closing costs, financing costs and prepaid items, and

Disburse cash out to the Borrower (or any other payee) not to exceed

2% of the new refinance mortgage loan or $2,000, whichever is less.

As an exception to the above, for construction conversion mortgage

loans and renovation mortgage loans, the amount of the interim

construction financing secured by the mortgaged property is

considered an amount used to pay off the first mortgage. Paying off

unsecured liens or construction costs paid by the Borrower outside of

the secured interim construction financing is considered cash out to

the Borrower, if greater than $2000 or 2% of loan amount.

This disclosure is subject to various special exceptions used by

Sellers to determine whether a mortgage loan is a No Cash-out

Refinance mortgage loan.

P = Purchase

C = Cash-out

Refinance

N = No Cash-out

Refinance

9 =Not Available

Alpha 1

22 ORIGINAL LOAN TERM - A calculation of the number of scheduled

monthly payments of the mortgage based on the First Payment Date

and Maturity Date.

Calculation: (Loan

Maturity Date (MM/YY)

– Loan First Payment

Date (MM/YY) + 1)

Numeric 3

August 2018 Page 12 of 33

Single Family Loan-Level Dataset: General User Guide Single Family Loan-Level Dataset: General User Guide

ORIGINATION DATA FILE

COLUMN

POSITION7 FORMAL NAME AND DEFINITION VALID VALUES/

CALCULATIONS TYPE LENGTH

Loans with original term of 420 or more, or 300 or less, are excluded

from the Dataset if originated prior to 1/1/2005. If loan was originated

on/after 1/1/2005, this exclusion does not apply.

23 NUMBER OF BORROWERS - The number of Borrower(s) who are

obligated to repay the mortgage note secured by the mortgaged

property. Disclosure denotes only whether there is one borrower or

more than one borrower associated with the mortgage note. This

disclosure will not be updated to reflect any subsequent assumption of

the mortgage note.

01 = 1 borrower

02 = > 1 borrowers

99 = Not Available

Numeric 2

24 SELLER NAME - The entity acting in its capacity as a seller of

mortgages to Freddie Mac at the time of acquisition.

Seller Name will be disclosed for sellers with a total Original UPB

representing 1% or more of the total Original UPB of all loans in the

Dataset for a given calendar quarter. Otherwise, the Seller Name will

be set to “Othe

r

Selle

r

s”.

Name of the seller, or

“Other Sellers”

Alpha-

numeric 20

25 SERVICER NAME - The entity acting in its capacity as the servicer of

mortgages to Freddie Mac as of the last period for which loan activity

is reported in the Dataset.

Servicer Name will be disclosed for servicers with a total Original UPB

representing 1% or more of the total Original UPB of all loans in the

Dataset for a given calendar quarter. Otherwise, the Servicer Name

will be set to “Othe

r

Service

r

s”.

Name of the servicer, or

“Other Servicers”

Alpha-

numeric 20

26 SUPER CONFORMING FLAG – For mortgages that exceed

conforming loan limits with origination dates on or after 10/1/2008 and

settlements on or after 1/1/2009

Y = Yes

Space (1) = Not

Super Conforming

Alpha 1

27 Pre-HARP LOAN SEQUENCE NUMBER – The Loan Sequence

Number link that associates this HARP loan to the Pre-HARP Loan

Sequence Number in the Single Family loan level dataset already

being published on a quarterly basis.

F1YYQnXXXXXX

F1 = product (Fixed

Rate Mortgage);

YYQn = origination

year and quarter; and,

XXXXXX = randomly

assigned digits

Alpha-

numeric

12

Monthly Performance Data File

MONTHLY PERFORMANCE DATA FILE

COLUMN

POSITION FORMAL NAME AND DEFINITION VALID VALUES/

CALCULATIONS TYPE LENGTH

1 LOAN SEQUENCE NUMBER - Unique identifier assigned to each

loan. F1YYQnXXXXXX

F1 = product (Fixed

Rate Mortgage);

YYQn = origination

year and quarter; and,

XXXXXX = randomly

assigned digits

Alpha-

numeric 12

2 MONTHLY REPORTING PERIOD – The as-of month for loan

information contained in the loan record. YYYYMM Date 6

August 2018 Page 13 of 33

Single Family Loan-Level Dataset: General User Guide Single Family Loan-Level Dataset: General User Guide

MONTHLY PERFORMANCE DATA FILE

COLUMN

POSITION FORMAL NAME AND DEFINITION VALID VALUES/

CALCULATIONS TYPE LENGTH

3 CURRENT ACTUAL UPB - The Current Actual UPB reflects the

mortgage ending balance as reported by the servicer for the

corresponding monthly reporting period. For fixed rate mortgages,

this UPB is derived from the mortgage balance as reported by the

servicer and includes any scheduled and unscheduled principal

reductions applied to the mortgage.

For mortgages with loan modifications, as indicated by “Y” in the

Modification Flag field, the current actual unpaid principal balance

may or may not include partial principal forbearance. If applicable, for

loans with partial principal forbearance, the current actual unpaid

principal balance equals the sum of interest bearing UPB (the

amortizing principal balance of the mortgage) and the deferred UPB

(the principal forbearance balance).

Current UPB will be rounded to the nearest $1,000 for the first 6

months after origination date. This was previously reported as zero for

the first 6 months after the origination date.

Calculation: (interest

bearing UPB) + (non-

interest bearing UPB)

Numeric

Literal

decimal

12

4 CURRENT LOAN DELINQUENCY STATUS – A value

corresponding to the number of days the borrower is delinquent,

based on the due date of last paid installment (“DDLPI”) reported by

servicers to Freddie Mac, and is calculated under the Mortgage

Bankers Association (MBA) method.

If a loan has been acquired by REO, then the Current Loan

Delinquency Status will reflect the value corresponding to that status

(instead of the value corresponding to the number of days the

borrower is delinquent).

XX = Unknown

0 = Current, or less

than 30 days past due

1 = 30-59 days

delinquent

2 = 60 – 89 days

delinquent

3 = 90 – 119 days

delinquent

And so on…

R = REO Acquisition

Space (3) =

Unavailable

Alpha-

numeric 3

5 LOAN AGE - The number of months since the note origination month

of the mortgage.

To ensure the age measurement commences with the first full month

after the note origination month, subtract 1.

Calculation: ((Monthly

Reporting Period) – Loan

Origination Date (MM/YY))

– 1 month

Numeric 3

6 REMAINING MONTHS TO LEGAL MATURITY - The remaining

number of months to the mortgage maturity date.

For mortgages with loan modifications, as indicated by “Y” in the

Modification Flag field, the calculation uses the modified maturity

date.

Calculation: (Maturity Date

(MM/YY) – Monthly

Reporting Period (MM/YY)

Numeric 3

7 REPURCHASE FLAG - Indicates loans that have been repurchased

or made whole (not inclusive of pool-level repurchase settlements).

This field is only populated only at loan termination month.

N = Not Repurchased

Y = Repurchased

Space (1) = Not

Applicable

Alpha 1

8 MODIFICATION FLAG – For mortgages with loan modifications,

indicates that the loan has been modified.

Y = Yes

Space (1) = Not

Modified

Alpha 1

August 2018 Page 14 of 33

Single Family Loan-Level Dataset: General User Guide Single Family Loan-Level Dataset: General User Guide

MONTHLY PERFORMANCE DATA FILE

COLUMN

POSITION FORMAL NAME AND DEFINITION VALID VALUES/

CALCULATIONS TYPE LENGTH

9 ZERO BALANCE CODE - A code indicating the reason the loan's

balance was reduced to zero.

01 = Prepaid or

Matured (Voluntary

Payoff)

03 = Foreclosure

Alternative Group

(Short Sale, Third Party

Sale or Charge Off)

06 = Repurchase prior

to Property Disposition

09 = REO Disposition

15 = Note

sale/Reperforming sale

Numeric 2

10 ZERO BALANCE EFFECTIVE DATE - The date on which the event

triggering the Zero Balance Code took place.

YYYYMM

Space(6) = Not

Applicable

Date 6

11 CURRENT INTEREST RATE - Reflects the current interest rate on

the mortgage note, taking into account any loan modifications. Numeric

Literal

Decimal

8

12 CURRENT DEFERRED UPB: The current non-interest bearing

UPB of the modified mortgage. $ Amount. Non-Interest

Bearing UPB. Numeric 12

13 DUE DATE OF LAST PAID INSTALLMENT (DDLPI): The due

date that the loan’s scheduled principal and interest is paid

through, regardless of when the installment payment was actually

made.

YYYYMM Date 6

14 MI RECOVERIES - Mortgage Insurance Recoveries are proceeds

received by Freddie Mac in the event of credit losses. These

proceeds are based on claims under a mortgage insurance

policy.

$ Amount. MI Recoveries. Numeric

Literal

Decimal

12

15 NET SALES PROCEEDS - The amount remitted to Freddie Mac

resulting from a property disposition or loan sale (which in the

case of bulk sales, may be an allocated amount) once allowable

selling expenses have been deducted from the gross sales

proceeds.

A value of “C” in Net Sales Proceeds stands for Covered, which

means that as part of the property disposition process, Freddie

Mac was “Covered” for its total indebtedness (defined as UPB at

disposition plus delinquent accrued interest) and net sale

proceeds covered default expenses incurred by Servicer during

the disposal of the loan.

A value of “U” indicates that the amount is unknown.

$ Amount. Gross Sale

Proceeds – Allowable

Selling Expenses.

C = Covered

U = Unknown

Alpha-

numeric

Literal

Decimal

14

16 NON MI RECOVERIES: Non-MI Recoveries are proceeds

received by Freddie Mac based on repurchase/make whole

proceeds, non-sale income such as refunds (tax or insurance),

hazard insurance proceeds, rental receipts, positive escrow

and/or other miscellaneous credits.

$ Amount. Non MI

Recoveries. Numeric

Literal

Decimal

12

17 EXPENSES - Expenses will include allowable expenses that

Freddie Mac bears in the process of acquiring, maintaining and/

or disposing a property (excluding selling expenses, which are

subtracted from gross sales proceeds to derive net sales

proceeds). This is an aggregation of Legal Costs, Maintenance

and Preservation Costs, Taxes and Insurance, and Miscellaneous

Expenses

$ Amount. Allowable

Expenses. Numeric

Literal

Decimal

12

August 2018 Page 15 of 33

Single Family Loan-Level Dataset: General User Guide Single Family Loan-Level Dataset: General User Guide

MONTHLY PERFORMANCE DATA FILE

COLUMN

POSITION FORMAL NAME AND DEFINITION VALID VALUES/

CALCULATIONS TYPE LENGTH

18 LEGAL COSTS - The amount of legal costs associated with the

sale of a property (but not included in Net Sale Proceeds). Prior to

population of a Zero Balance Code equal to 03 or 09, this field will

be populated as “Not Applicable,” Following population of a Zero

Balance Code equal to 03 or 09, this field will be updated (as

applicable) to reflect the cumulative total. Space(12) – Not

applicable

$ Amount Numeric

Literal

Decimal

12

19 MAINTENANCE AND PRESERVATION COSTS –The amount of

maintenance, preservation, and repair costs, including but not

limited to property inspection, homeowner’s association, utilities,

and REO management, that is associated with the sale of a

property (but not included in Net Sale Proceeds). Prior to

population of a Zero Balance Code equal to 03 or 09, this field will

be populated as “Not Applicable,” Following population of a Zero

Balance Code equal to 03 or 09, this field will be updated (as

applicable) to reflect the cumulative total. Space(12) – Not

applicable

$ Amount Numeric

Literal

Decimal

12

20 TAXES AND INSURANCE – The amount of taxes and insurance

owed that are associated with the sale of a property (but not

included in Net Sale Proceeds). Prior to population of a Zero

Balance Code equal to 03 or 09, this field will be populated as

“Not Applicable,”. Following population of a Zero Balance Code

equal to 03 or 09, this field will be updated (as applicable) to

reflect the cumulative total. Space(12) – Not applicable

$ Amount Numeric

Literal

Decimal

12

21 MISCELLANEOUS EXPENSES - Miscellaneous expenses

associated with the sale of a property (but not included in Net

Sale Proceeds). Prior to population of a Zero Balance Code equal

to 03 or 09, this field will be populated as “Not Applicable,”.

Following population of a Zero Balance Code equal to 03 or 09,

this field will be updated (as applicable) to reflect the cumulative

total. Space(12) – Not applicable

$ Amount Numeric

Literal

Decimal

12

22 ACTUAL LOSS CALCULATION

Actual Loss was calculated using the below approach:

Actual Loss = (Default UPB – Net Sale_Proceeds) + Delinquent

Accrued Interest - Expenses – MI Recoveries – Non MI

Recoveries.

Delinquent Accrued Interest = (Default_Upb – Non Interest

bearing UPB)* (Current Interest rate – 0.35) * ( Months between

Last Principal & Interest paid to date and zero balance date ) *

30/360/100.

Please note that the following business rules are applied to this

calculation:

a. For all loans, 35 bps is used as a proxy for servicing fee

.

b. The Actual Loss Calculation will be set to zero for loans with

Repurchase Flag =’Y’

c. The Actual Loss Calculation will be set to zero for loans with

Net Sale Proceeds=’C (i.e, Covered)’.

d. The Actual Loss Calculation will be set to zero for loans with

Net Sales Proceeds = ‘U” (Net Sales Proceeds are missing

or expenses are not available.

$ Amount Numeric

Literal

Decimal

12

August 2018 Page 16 of 33

Single Family Loan-Level Dataset: General User Guide Single Family Loan-Level Dataset: General User Guide

MONTHLY PERFORMANCE DATA FILE

COLUMN

POSITION FORMAL NAME AND DEFINITION VALID VALUES/

CALCULATIONS TYPE LENGTH

e. The Actual Loss Calculation will be set to missing for loans

disposed within three months prior to the performance cutoff

date.

f. Modification Costs are currently not included in the

calculation of The Actual Loss Calculation field.

23 MODIFICATION COST – The cumulative modification cost

amount calculated when Freddie Mac determines such mortgage

loan has experienced a rate modification event. Modification Cost

is applicable for loans with rate changes only. This amount will

be calculated on a monthly basis beginning with the first reporting

period a modification event is reported, and disclosed in the last

performance record.

For example:

(Original Interest Rate/1200 * Current Actual UPB) – (Current

Interest Rate/1200 * (sum(Current Actual UPB, -Current Deferred

UPB)) and aggregate each month since modification through the

Performance Cutoff Date into a cumulative amount

$ Amount Numeric

Literal

Decimal

12

24 STEP MODIFICATION FLAG – A Y/N flag will be disclosed for

every modified loan, to denote if the terms of modification

agreement call for note rate to increase over time.

Y = Yes

N = No

Space (1) = Not Step

Mod

Alpha 1

25 DEFERRED PAYMENT MODIFICATION – A Y/N flag will be

disclosed to indicate Deferred Payment Modification for the loan.

Y = Yes

N = No

Alpha 1

Interpreting the Data

The Single Family Loan-Level Dataset is split in calendar quarters, beginning with the first quarter of

1999 and ending with the quarter as of the Origination Cutoff Date. For each calendar quarter, there is

One “origination data” file containing loan-level origination information for all the loans originated

during the quarter.

One “monthly performance data” file for all of the respective loans originated during the quarter.

The monthly performance data file contains monthly loan-level credit performance and actual loss data

for each loan, starting from the time of loan acquisition by Freddie Mac until the earlier of a termination

event or the Performance Cutoff Date, which is the last period of performance data available for any

loan in the Dataset.

Termination events are described in more detail in the section below entitled “Zero Balance Codes”.

Note that the monthly performance data file does not contain monthly performance information for the

timeframe between loan origination and loan acquisition by Freddie Mac.

August 2018 Page 17 of 33

Single Family Loan-Level Dataset: General User Guide Single Family Loan-Level Dataset: General User Guide

Each loan in the origination data file is assigned a unique Loan Sequence Number. The monthly

performance data file corresponding to the origination data file may contain multiple records with the

same Loan Sequence Number, identifying the monthly performance records associated to a given loan.

Note that Loan Sequence Numbers in the Dataset do not correspond to Loan Sequence Numbers

found in existing Freddie Mac participation certificate (PC) disclosures.

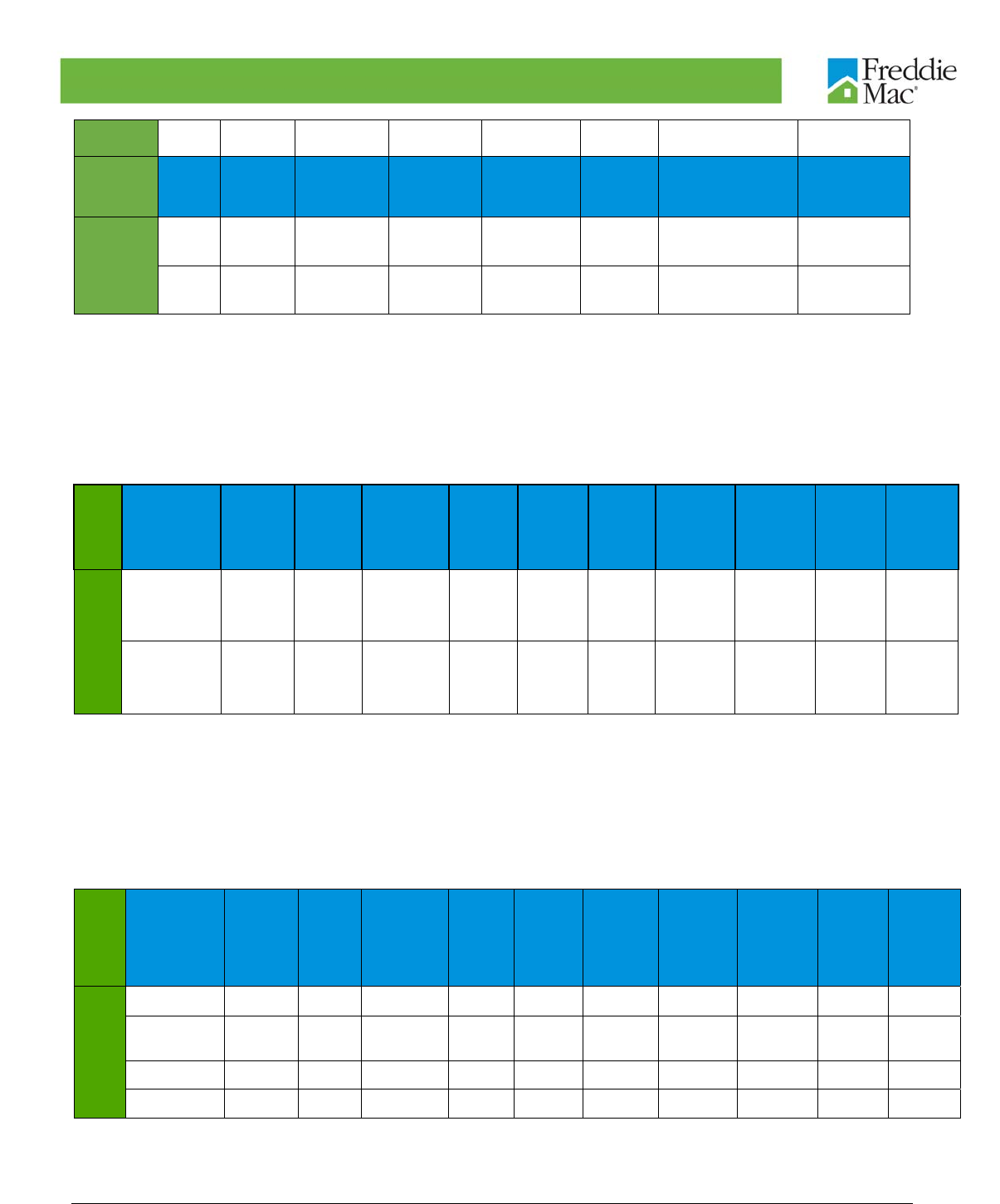

Zero Balance Codes

Loans may become inactive in the Dataset for a variety of reasons, including voluntary payoffs or credit

events, known as “termination events”. Loans that become inactive in the Dataset due to a termination

event on or before the Performance Cutoff Date will not be updated for activity in subsequent periods.

Loans that were repurchased from Freddie Mac after a termination event are the exception to this

practice, as discussed in the section below entitled “Repurchases”. The reason for loan inactivity will

be indicated by the value in the Zero Balance Code field, which is set during the Monthly Reporting

Period corresponding to the Zero Balance Effective Date.

If applicable, the Zero Balance Code may be set at most once for a given loan in the Dataset. If more

than one termination event occurs in the same reporting period for a given loan (e.g., a loan is

repurchased and REO disposed), the higher-ranking termination event is reported in the Dataset. The

table below describes each of the termination events reported in the Dataset, the associated Zero

Balance Code, and the applicable priority (5 being the lowest and 1 being the highest).

Reason for Loan Termination Zero Balance

Code Priority

Prepaid or Matured

(

Voluntar

y

Pa

y

off

)

01 5

Foreclosure Alternative Group (Short Sale, Third

Party Sale, Charge Off or Note Sale) 03 4

Repurchase prior to Propert

y

Disposition 06 2

REO Disposition 09 3

NPL/RPL Loan Sale 15 1

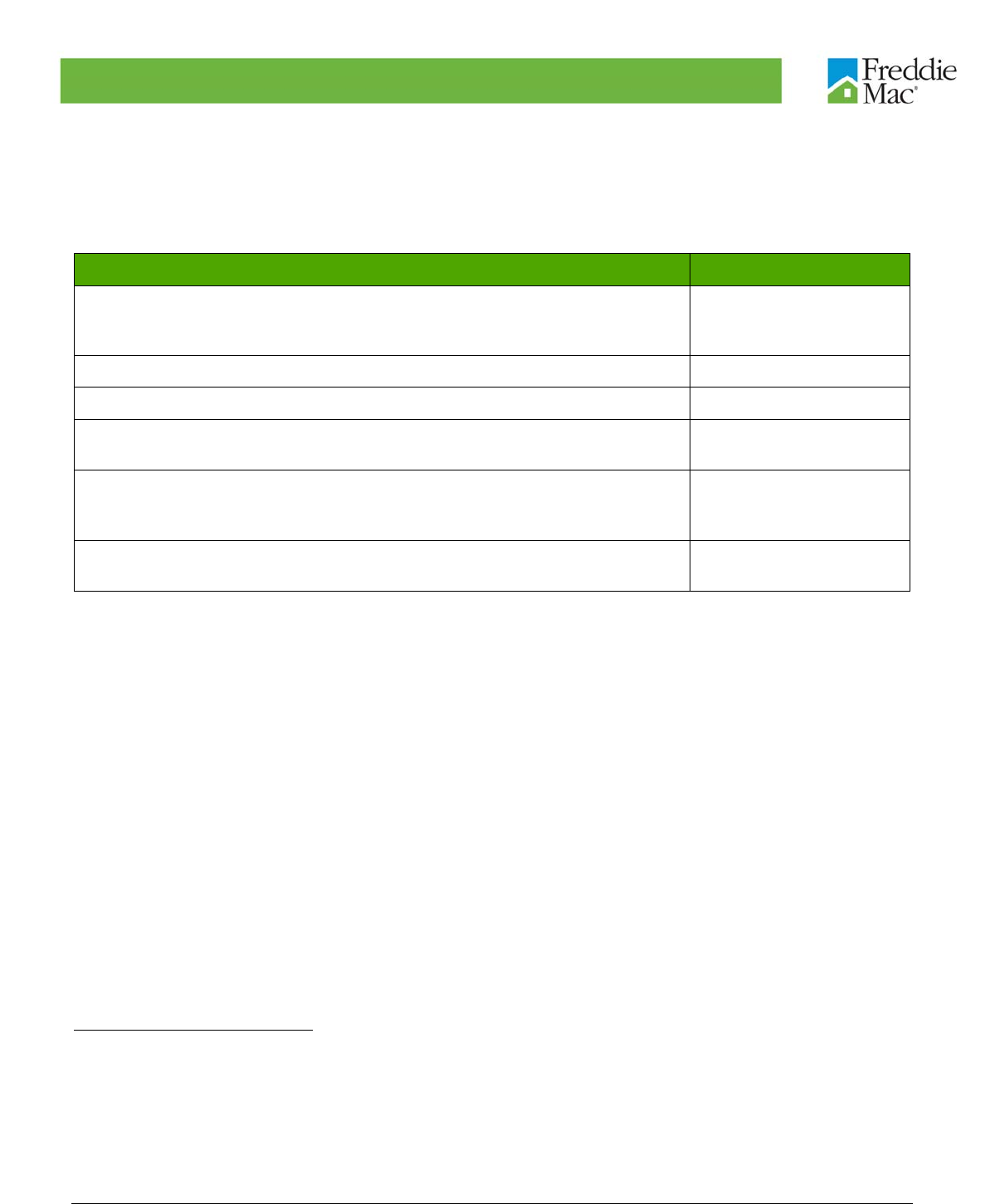

Valid Values

Certain data elements for some loans in the Single Family Loan-Level Dataset will not be disclosed if

the value is above or below reasonable thresholds, as determined by Freddie Mac and detailed in the

table below:

Data Element File T

y

pe

V

alid Values If Not Valid

Credit Score

(

FICO

)

Ori

g

ination 301 - 850 Space

(

3

)

Mort

g

a

g

e Insurance Percenta

g

e

(

MI %

)

Ori

g

ination 1% - 55% or 0

(

000

)

Space

(

3

)

Original Debt-to-Income Ratio (DTI) Origination 0%<DTI<= 65%

For HARP:

Null

Space (3) or Null

Ori

g

inal Loan-to-Value Ratio

(

LTV

)

Ori

g

ination 6% - 105% Space

(

3

)

August 2018 Page 18 of 33

Single Family Loan-Level Dataset: General User Guide Single Family Loan-Level Dataset: General User Guide

Data Element File T

y

pe

V

alid Values If Not Valid

For HARP:

81% - 999%

Ori

g

inal Combined Loan-to-Value Ratio

(

CLTV

)

Ori

g

ination 0% - 200% Space

(

3

)

Monthly Reporting Period

For a given loan, each monthly reporting period in the monthly performance data file combines data

elements from multiple reporting cycles and systems at Freddie Mac. As such, perceived data

anomalies may be a result of timing mismatches between default/delinquency reporting cycles and

investor reporting cycles. Examples of some commonly occurring anomalies in the data are included

throughout this section. In all cases, the best information available at the time the Dataset is generated,

subject to operational constraints, is used.

Other reasons why the data may be imperfect include, but are not limited to

Seller/Servicer reporting errors: Freddie Mac relies on Seller/Servicer-reported data

Data quality controls and systems have evolved and improved over time

Administrative errors

Loan delivery requirements (e.g., Form 11/13) have been updated to allow more granular

reporting over time

The Monthly Reporting Period disclosed in the monthly performance data file includes the current

month’s accounting cycle activity for performing loans and the previous calendar month’s default

reporting activity for non-performing loans. It also includes termination events that occurred during the

period, as indicated by the Zero Balance Effective Date, or modifications that became effective during

the period, as indicated by the Modification Flag.

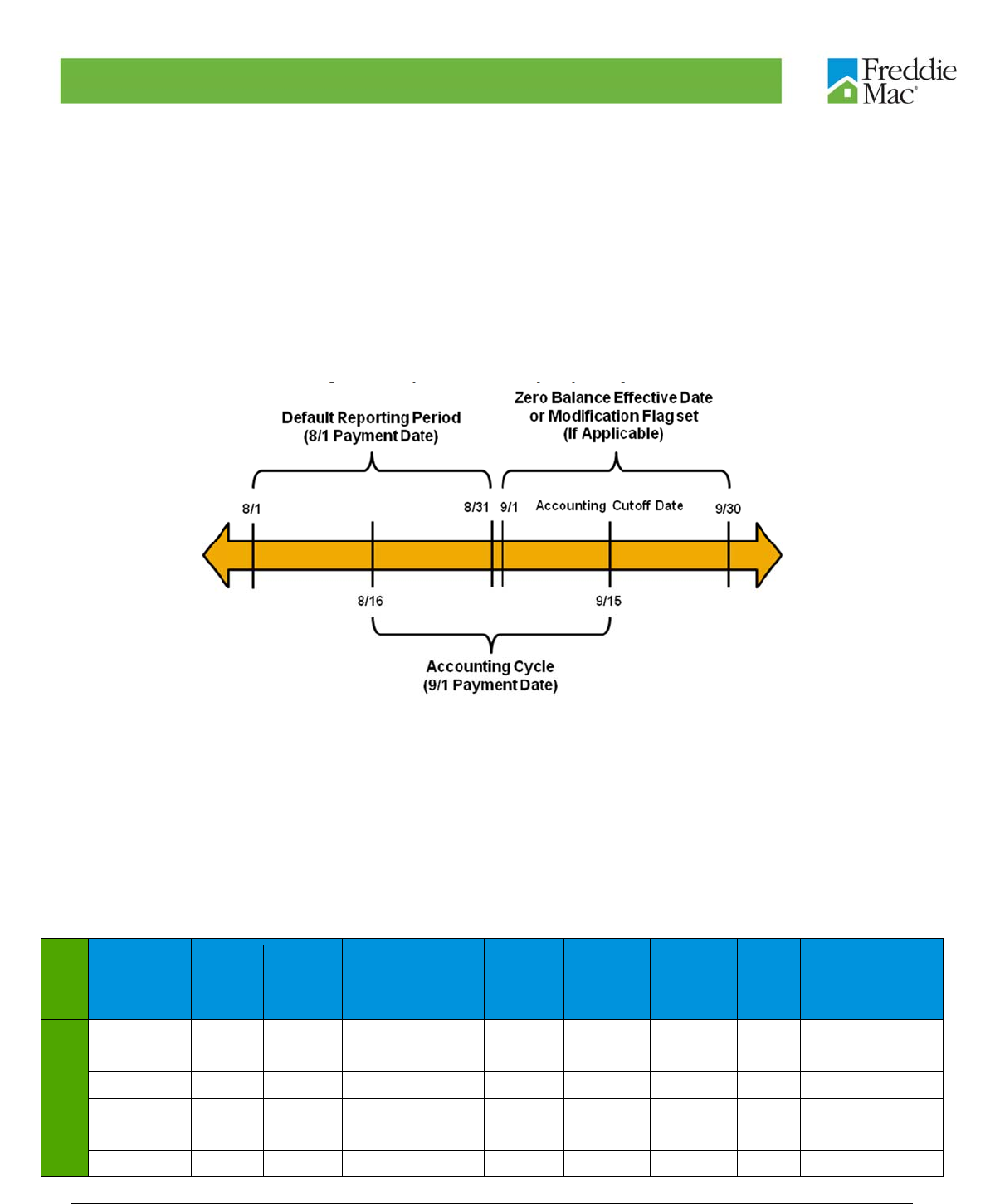

Freddie Mac’s accounting cycle begins on the 16th of each month and ends on the 15th of the following

month, for scheduled Principal and Interest (P&I) payments due on the first of the month. If the 15th

falls on a weekend, or holiday, the accounting cycle ends on the previous business day. The last day of

the accounting cycle is the Accounting Cutoff. Unscheduled principal curtailments and prepayments

received by the Accounting Cutoff date are also included in the Monthly Reporting Period. The month

in which the Accounting Cutoff occurs will correspond to the Monthly Reporting Period in the Single

Family Loan-Level Dataset.

Freddie Mac’s default reporting cycle is based on loan activity between the first day of the month and

the last day of the month, and is reported in the Single Family Loan-Level Dataset on a one-month

lagged basis. Inclusion of mortgage loans in any of the Current Loan Delinquency Status categories is

based on the due date of last paid installment (“DDLPI”) as reported by servicers to Freddie Mac8, and

is calculated under the Mortgage Bankers Association (MBA) method.9

8 Freddie Mac is not responsible for the DDLPI reported by servicers, makes no representations and warranties regarding

such reported DDLPI, and may not have independently verified such reported DDLPI.

9 In this calculation, a loan increases its delinquency status if a monthly payment is not received by the end of the day

immediately preceding the loan’s next due date.

August 2018 Page 19 of 33

Single Family Loan-Level Dataset: General User Guide Single Family Loan-Level Dataset: General User Guide

Consider a current loan with a payment due on August 1: If the Servicer does not receive a payment by

August 31, the loan would become one month (30 days) delinquent as reflected in the Servicer’s

September reporting transmission to Freddie Mac. The loan would be reflected as 30 days’ delinquent

(delinquency status of “1”) in the September Monthly Reporting Period in the Dataset.

As a result of combining data from multiple reporting cycles and systems within the monthly

performance data, the payment date corresponding to delinquency status and the payment date

corresponding to scheduled P&I payments are different, for the same Monthly Reporting Period in the

Dataset. Diagram 1 illustrates the accounting cycle, default reporting, and termination event

information that would be included in the Monthly Reporting Period of September in the Single Family

Loan-Level Dataset:

Diagram 1: September Monthly Reporting Period

Example 1 follows a loan in the Monthly Performance Data File as it transitions from current to

delinquent status’ and ends in a termination event. The loan is first reported as delinquent to Freddie

Mac in June 2010 (“201006”), which means that the loan first became 30 days delinquent in May 2010

(“201005”). The loan is disposed through a Foreclosure Alternative Sale and is terminated in the

Dataset.

Example 1: Normal Delinquent Status Progression

Formal

Name

Loan Sequence

Number

Monthly

Reporting

Period

Current

Actual UPB

Current Loan

Delinquency

Status

Loan

Age

Months

Remaining

to Legal

Maturity

Repurchase

Flag Modification

Flag

Zero

Balance

Code

Zero

Balance

Effective

Date

Current

Interest

Rate

Monthly Performance

Data

F108Q4000374 201004 79930.72 0 16 343 6.125

F108Q4000374 201005 79844.71 0 17 342 6.125

F108Q4000374 201006 79844.71 1 18 341 6.125

F108Q4000374 201007 79844.71 2 19 340 6.125

F108Q4000374 201008 79844.71 3 20 339 6.125

F108Q4000374 201009 79844.71 4 21 338 6.125

August 2018 Page 20 of 33

Single Family Loan-Level Dataset: General User Guide Single Family Loan-Level Dataset: General User Guide

Formal

Name

Loan Sequence

Number

Monthly

Reporting

Period

Current

Actual UPB

Current Loan

Delinquency

Status

Loan

Age

Months

Remaining

to Legal

Maturity

Repurchase

Flag Modification

Flag

Zero

Balance

Code

Zero

Balance

Effective

Date

Current

Interest

Rate

F108Q4000374 201010 79844.71 5 22 337 6.125

F108Q4000374 201011 79844.71 6 23 336 6.125

F108Q4000374 201012 0 7 24 335 N 03 201012 6.125

Example 2 follows a loan in the Dataset that does not complete the “normal” progression of delinquency

status. This scenario could be due to delays in reporting delinquency status by the Servicer, bounced

checks from the borrower, or mismatches in reporting cycles.

Example 2: Irregular Delinquent Status Progression

Formal

Name

Loan Sequence

Number

Monthly

Reporting

Period

Current

Actual UPB

Current Loan

Delinquency

Status

Loan

Age

Months

Remaining

to Legal

Maturity

Repurchase

Flag Modification

Flag

Zero

Balance

Code

Zero

Balance

Effective

Date

Current

Interest

Rate

Monthly Performance Data

F100Q1000049 200411 121801.43 2 56 304 7.875

F100Q1000049 200412 121672.66 2 57 303 7.875

F100Q1000049 200501 121412.59 2 58 302 7.875

F100Q1000049 200502 121801.43 1 59 301 7.875

F100Q1000049 200503 121672.66 5 60 300 7.875

F100Q1000049 200504 120960.14 1 61 299 7.875

F100Q1000049 200505 120825.85 1 62 298 7.875

F100Q1000049 200506 120690.68 1 63 297 7.875

Reporting gaps in the data, which could result from a Seller/Servicer failing to report loan information

for a given month, or timing mismatches in the initial reporting of the loan to Freddie Mac, are possible.

In Example 3, the servicing record does not include information from May 2000 (“200005”). This gap

could be due to delays in loan settlement validation and reconciliation, or if the Servicer submitted

settlement information late. Also, because this loan was aged less than six months from origination,

the Current Actual Unpaid Principal Balance (UPB) field is empty (see Data Masking section below).

Example 3: Servicing Gaps

Formal

Name

Loan Sequence

Number

Monthly

Reporting

Period

Current

Actual UPB

Current Loan

Delinquency

Status

Loan

Age

Months

Remaining

to Legal

Maturity

Repurchase

Flag Modification

Flag

Zero

Balance

Code

Zero

Balance

Effective

Date

Current

Interest

Rate

Monthly

Perform

ance

F100Q1000183 200004 0 0 360 8.875

F100Q1000183 200006 0 2 358 8.875

F100Q1000183 200007 0 3 357 8.875

August 2018 Page 21 of 33

Single Family Loan-Level Dataset: General User Guide Single Family Loan-Level Dataset: General User Guide

Formal

Name

Loan Sequence

Number

Monthly

Reporting

Period

Current

Actual UPB

Current Loan

Delinquency

Status

Loan

Age

Months

Remaining

to Legal

Maturity

Repurchase

Flag Modification

Flag

Zero

Balance

Code

Zero

Balance

Effective

Date

Current

Interest

Rate

F100Q1000183 200008 0 4 356 8.875

Repurchases

The Single Family Loan-Level Dataset identifies those loans that have been repurchased from Freddie

Mac in the monthly performance data files. Specifically, mortgages which were repurchased prior to or

after a termination event but before the Performance Cutoff Date, are identified in the Dataset. A loan

flagged as “repurchased” may also include loans where Freddie Mac was compensated for losses

incurred, or “made whole”, as well as loans where a “repurchase equivalent”, such as recourse or

indemnification, was negotiated with a seller. Loans with a closed Underwriting defect or major Servicing

defect are flagged as repurchases in the dataset.

For loans that were repurchased prior to other termination events, the final monthly performance record

of a given loan will contain “06” in the Zero Balance Code field and the date on which the repurchase

occurred in the Zero Balance Effective Date field. In some cases, the final monthly performance record

of a given loan will contain “01” in the Zero Balance Code field and the date on which the repurchase

occurred in the Zero Balance Effective Date field. The Repurchase Flag field will contain “Y”. In

Example 4, the loan was repurchased from Freddie Mac in April 2009.

Example 4: Repurchase prior to a termination event

Formal

Name

Loan Sequence

Number

Monthly

Reporting

Period

Current

Actual UPB

Current Loan

Delinquency

Status

Loan

Age

Months

Remaining

to Legal

Maturity

Repurchase

Flag Modification

Flag

Zero

Balance

Code

Zero

Balance

Effective

Date

Current

Interest

Rate

Monthly Performance Data

F106Q1111821 200809 332000.8 0 30 330 6.75

F106Q1111821 200810 331652.23 0 31 329 6.75

F106Q1111821 200811 331213.06 0 32 328 6.75

F106Q1111821 200812 330860.06 0 33 327 6.75

F106Q1111821 200901 330860.06 0 34 326 6.75

F106Q1111821 200902 330148.1 0 35 325 6.75

F106Q1111821 200903 329789.11 0 36 324 6.75

F106Q1111821 200904 0 0 37 323 6 200904 6.75

For loans that were repurchased after a termination event other than a prepayment, but prior to the

Performance Cutoff Date, the final monthly performance record of a given loan will contain the Zero

Balance Code (allowable values are 03 and 09) and the Zero Balance Effective Date, as well as “Y” in

the Repurchase Flag field. In Example 5, the loan was disposed through a Foreclosure Alternative

Sale in March 2005 and was later repurchased from Freddie Mac.

August 2018 Page 22 of 33

Single Family Loan-Level Dataset: General User Guide Single Family Loan-Level Dataset: General User Guide

Example 5: Repurchase after a termination event

Formal

Name

Loan Sequence

Number

Monthly

Reporting

Period

Current

Actual UPB

Current Loan

Delinquency

Status

Loan

Age

Months

Remaining

to Legal

Maturity

Repurchase

Flag Modification

Flag

Zero

Balance

Code

Zero

Balance

Effective

Date

Current

Interest

Rate

Monthly Performance Data

F103Q1325362 200408 171580.65 0 16 343 5.625

F103Q1325362 200409 171379.83 1 17 342 5.625

F103Q1325362 200410 171379.83 1 18 341 5.625

F103Q1325362 200411 171379.83 2 19 340 5.625

F103Q1325362 200412 171379.83 3 20 339 5.625

F103Q1325362 200501 171379.83 4 21 338 5.625

F103Q1325362 200502 171379.83 5 22 337 5.625

F103Q1325362 200503 0 6 23 336 Y 03 200503 5.625

Modifications

The origination data file will not reflect the modified loan terms of a given modified loan. In the monthly

performance data file, all or a subset of the following fields may be updated in the monthly reporting

period during which the modification became legally effective:

Current Actual UPB

Current Loan Delinquency Status

Remaining Months to Legal Maturity

Current Interest Rate

Current Deferred UPB

The Modification Flag will be set to “Y” in the period during which the modification is legally effective.

Due to the various loan modification programs available to borrowers (Standard10, HAMP11, etc.), a loan

could have been modified more than once. In these cases, the modification flag will be set to “Y” in

more than one monthly reporting period, and some or all of the fields above could be updated each

time a modification becomes legally effective. Approved modifications, but not yet closed as of the

Performance Cutoff Date, are not included in the Dataset.

Typically, the most recent accounting cycle data12 will be updated to reflect the modified terms during

the monthly reporting period the modification becomes legally effective. In Example 6, the loan

modification is effective in August 2002, and the Current Interest Rate, Remaining Months to Legal

Maturity and Current Actual UPB are updated in the same monthly reporting period. The Current Loan

Delinquency Status is updated in the subsequent period.

10 For more information about Freddie Mac’s Standard Modifications, please visit the following website:

http://www.freddiemac.com/learn/pdfs/service/std_strm_mod.pdf

11 For more information about the Home Affordable Modification Program, please visit the following website:

http://www.freddiemac.com/singlefamily/service/mha_modifi cation.html

12 For more information on accounting cycles, refer to the Monthly Reporting Period section on Page 17.

August 2018 Page 23 of 33

Single Family Loan-Level Dataset: General User Guide Single Family Loan-Level Dataset: General User Guide

Example 6: Normal Modification Reporting

Formal

Name

Loan Sequence

Number

Monthly

Reporting

Period

Current

Actual UPB

Current Loan

Delinquency

Status

Loan

Age

Months

Remaining

to Legal

Maturity

Repurchase

Flag Modification

Flag

Zero

Balance

Code

Zero

Balance

Effective

Date

Current

Interest

Rate

Monthly

Performance

Data

F101Q1173671 200205 233835.84 3 14 345 6.75

F101Q1173671 200206 233403.91 2 15 344 6.75

F101Q1173671 200207 233403.91 3 16 343 6.75

F101Q1173671 200208 241971.47 4 17 360 Y 6.625

F101Q1173671 200209 241757.98 0 18 359 6.625

However, delays in the reporting of workout information from the Servicer or caused by quality control

processes at Freddie Mac may result in updates to accounting cycle data occurring after the

modification effective date. In Example 7, below, the loan modification is effective in April 2003, but the

Current Interest Rate, Current Actual UPB, and Current Loan Delinquency Status are updated in the

subsequent Monthly Reporting Period.

Example 7: Delayed Modification Reporting

Formal

Name

Loan Sequence

Number

Monthly

Reporting

Period

Current

Actual UPB

Current Loan

Delinquency

Status

Loan

Age

Months

Remaining

to Legal

Maturity

Repurchase

Flag Modification

Flag

Zero

Balance

Code

Zero

Balance

Effective

Date

Current

Interest

Rate

Monthly

Performance

Data

F101Q1210253 200301 78747.56 1 21 339 7.25

F101Q1210253 200302 78747.56 2 22 338 7.25

F101Q1210253 200303 78677.59 3 23 337 7.25

F101Q1210253 200304 78677.59 3 24 360 Y 7.25

F101Q1210253 200305 83785.88 0 25 359 7

Actual Loss

The origination data file does not disclose any actual loss data components. With the exception of

Current Deferred UPB, which will be disclosed for the months it is legally effective, the remaining six (6)

actual loss components will be disclosed as part of the final monthly performance record at property

disposition:

i. Net Sale Proceeds

ii. Expenses

iii. MI Recoveries

iv. Non MI Recoveries

v. Current Deferred UPB

vi. Due Date of Last Paid Installment (DDLPI)

August 2018 Page 24 of 33

Single Family Loan-Level Dataset: General User Guide Single Family Loan-Level Dataset: General User Guide

In addition to providing total expenses, the components of expenses including Legal Costs,

Maintenance and Preservation Costs, Taxes and Insurance, Other Miscellaneous Costs are also

provided. All of these 4 components add up to the total expenses.

While Net Sale Proceeds, Expenses, MI Recoveries and Non MI Recoveries are $ amounts that can be

directly used in calculating actual loss, Current Deferred UPB and Due Date of Last Paid Installment

(DDLPI) are to be used for calculating actual loss based on lost interest. Note that the period when the

actual loss occurred shall not be disclosed. If a loan has trailing expenses or recoveries after the initial

disclosure, the final property disposition record will be updated in a subsequent data refresh to reflect

the respective expense or recovery amount. Proceeds received from bulk or lump sum repurchase

settlements will not be available loan level.

Actual Loss = Default UPB – Net Sales Proceeds - Expenses – MI Recoveries – Non MI Recoveries +

Delinquent Interest

For purposes of this calculation:

Default UPB is the last known non zero Current Actual UPB.

Delinquent Interest = (Zero Balance Effective Date – Due Date of Last Paid Installment in months)

X (Default UPB – Non Interest bearing UPB) X 30/360 X (Current Interest Rate – Servicing Fee

0.35)/100

We use 35 bps as a proxy for servicing fee for this field in the below examples.

Modification Costs are currently not included in calculation of The Actual Loss Calculation field.

Example 8: Calculating Actual loss for an REO loan.

Note: Calculations used are for example purposes only. Different assumptions and calculations may be used.

Calculations will be transaction specific and prescribed in the transaction’s offering documents.

Formal

Name

Loan

Sequence

Number

Monthly

Reporting

Period

Current

Actual

UPB

Current Loan

Delinquency

Status

Zero

Balance

Code

Zero

Balance

Effective

Date

Current

Interest

Rate

Due Date

of Last

Paid

Installment

(DDLPI)

MI

Recoverie

s

Net Sales

Proceeds

NON MI

Recoverie

s Expenses

Monthly

Performance

Data

F106Q1263687 201208 233688.50 15 6.375

F106Q1263687 201209 233688.50 R 6.375

F106Q1263687 201304 0 R 09 201304 0 201104 0 182400 1197 -70100

Actual Loss = 233,688.49 – 182,400 – (-70100) – 0 – 1197 + 28,626.84*= 148,818.33

* Delinquent Interest = (201304 – 201104[24months]) X 233,688.49 X 30/360 X (6.375 – 0.35)/100 =

28,159.46

August 2018 Page 25 of 33

Single Family Loan-Level Dataset: General User Guide Single Family Loan-Level Dataset: General User Guide

Example 9: Calculating Actual Loss for a Foreclosure Alternative

Note: Calculations used are for example purposes only. Calculation and treatment will be transaction specific

and prescribed in the transaction’s offering documents.

Formal

Name

Loan

Sequence

Number

Monthly

Reporting

Period

Current

Actual UPB

Current Loan

Delinquency

Status

Zero

Balance

Code

Zero

Balance

Effective

Date

Current

Interest

Rate

Due Date of

Last Paid

Installment

(DDLPI)

MI

Recoveries Net Sales

Proceeds NON MI

Recoveries Expenses

Monthly

Performance

Data

F103Q1012288 201211 125811.69 19 5.75

F103Q1012288 201212 125811.69 20 5.75

F103Q1012288 201301 125811.69 21 5.75

F103Q1012288 201302 0 22 03 201302 5.75 201103 0 99600 1734 -21753

Actual Loss = 125,811.69 – 99,600 - (-21,753) – 0 – 1,734 +13,021.51 = 59,252.2

* Delinquent Interest = (201302 – 201103[23months]) X 125,811.69 X 30/360 X (5.75 – 0.35)/100 =

13,021.51

Interpreting HARP Data

HARP dataset has 2 files:

An “origination data” file containing loan-level origination information for loans that refinanced

via HARP out of the full Single Family Loan Level Dataset

A “monthly performance data” file for all the HARP loans being included in the above stated

origination data file.

HARP data elements have the same definitions as the elements in the full Single Family Loan Level

Dataset The interpretation of these data elements should be consistent, except where noted.

The loans in HARP disclosure appear as payoff’s/repurchases in the full Single Family Loan Level

Dataset. In order to combine both the datasets, use the Pre-HARP Loan Sequence Number in the HARP

origination file, and map it back to the corresponding loan history in the existing loan level disclosure.

HARP Origination records:

August 2018 Page 26 of 33

Single Family Loan-Level Dataset: General User Guide Single Family Loan-Level Dataset: General User Guide

Column

Position # 1 2 3 8 20 25 26 27

Formal

Name

CREDIT

SCORE

FIRST

PAYMENT

DATE

FIRST TIME

HOMEBUYER

FLAG

OCCUPANCY

STATUS

Loan

Sequence

Number

SERVICER

NAME SUPERCONFORMING

FLAG

PRE-HARP Loan

Sequence

Number

Origination

data

698 200906 N O F109Q1595460

Other

servicers F107Q3047434

706 200906 N O F109Q1595461

Other

servicers F108Q2002318

The above examples represent loans that went through HARP refinance in Q1 2009, the Pre-Harp

Loan Sequence Numbers for these loans can be observed at the end of each row.

Terminal Performance record for Pre-HARP loans in existing disclosure:

Formal Name

Loan

Sequence

Number

Monthly

Reporting

Period

Current

Actual

UPB

Current

Loan

Delinquency

Status

Zero

Balance

Code

Zero

Balance

Effective

Date

Current

Interest

Rate

Due Date

of Last

Paid

Installment

(DDLPI)

MI

Recoveries Net Sales

Proceeds Expenses

Monthly

Performance Data

F107Q3047434 200903 0 0 01 200903 6.5

F108Q2002318 200903 0 0 01 200903 5.875