CE 2400O Green Ch04

User Manual: CE-2400O

Open the PDF directly: View PDF ![]() .

.

Page Count: 30

4

4

TERMS PREVIEW

journal

journalizing

entry

general journal

double-entry

accounting

source document

check

invoice

sales invoice

receipt

memorandum

As described in Chapter 3, transactions are analyzed into debit and

credit parts before information is recorded. A form for recording transac-

tions in chronological order is called a Recording transactions in

a journal is called

Transactions could be recorded in the accounting equation. However,

most companies wish to create a more permanent record by recording

transactions in a journal.

Each business uses the kind of journal that best fits the needs of that

business. The nature of a business and the number of transactions to be

recorded determine the kind of journal to be used.

The word journal comes from the Latin diurnalis, meaning daily. Most

businesses conduct transactions every day. To keep from getting over-

loaded, the businesses will make entries in their accounting journals

every day.

journalizing.

journal.

JOURNALS AND JOURNALIZING

AFTER STUDYING CHAPTER 4, YOU WILL BE ABLE TO:

1. Define accounting terms related to journalizing transactions.

2. Identify accounting concepts and practices related to jounal-

izing transactions.

3. Record in a general journal transactions to set up a business.

4. Record in a general journal transactions to buy insurance for

cash and supplies on account.

5. Record in a general journal transactions that affect owner’s

equity and receiving cash on account.

6. Start a new journal page.

Recording Transactions

in a General Journal

64

F

Y

I

The Small Business Administration (SBA)

has programs that offer free management

and accounting advice to small business

owners. The SBA sponsors various workshops

and publishes a variety of booklets for small

business owners.

CHAPTER 4 Recording Transactions in a General Journal 65

ACCOUNTING

IN YOUR CAREER

HIGH STANDARDS FOR

JOURNALIZING

Sandra Huffman has worked for

Marquesa Advertising for 30 days as

an accounting clerk, a position for

which the company owner, Ramona

Marquesa, hired her. She journalizes all

transactions, about 50 per day, handles all incoming and outgoing mail, prepares and files

all source documents, and performs other duties as assigned.

One day Ramona asked to see the journal. Sandra handed the journal to Ramona, who

scanned a few pages while Sandra fidgeted in her chair. Sandra didn’t know exactly what

to expect, but she knew she had not done as good a job with journalizing transactions as

she should have.

Ramona then sighed and said, “I’m concerned about this journal, Sandra. You have

recorded all transactions in pencil, and I notice numerous erasures. I don’t know if the

debits equal the credits, but I can see right away that this one transaction for $20,000

should have been for $2,000. Some of the dates are missing and some are out of order.

What do you suggest we do to turn this situation around?”

After apologizing, Sandra thanked Ramona for giving her the chance to improve her

work. She explained that she realized she had not been giving the journal the priority it

required and went on to describe how she would improve her performance in the future.

Critical Thinking:

1. What do you think Sandra should say about the journal to demonstrate that she knows it is

important?

2. What specific improvements do you think Sandra should make?

Using a Journal

Information for each transaction recorded in

a journal is called an A journal with two

amount columns in which all kinds of entries

can be recorded is called a

Encore Music uses a general journal.

The columns in Encore Music’s general

journal are Date, Account Title, Doc. No., Post.

Ref., Debit, and Credit. The use of each column

is described later in this chapter.

Accuracy

Information recorded in a journal includes

the debit and credit parts of each transaction

recorded in one place. The information can be

verified by comparing the data in the journal

with the transaction data to assure that all infor-

mation is correct.

Chronological Record

Transactions are recorded in a journal by

date in the order in which the transactions occur.

All information about each transaction is record-

ed in one place, making the information for a

specific transaction easy to locate.

Double-Entry Accounting

The recording of debit and credit parts of a

transaction is called

In double-entry accounting, each transaction

affects at least two accounts. Both the debit part

and the credit part are recorded for each transac-

tion. This procedure reflects the dual effect of

each transaction on the business’s records.

Double-entry accounting assures that debits

equal credits.

Source Documents

A business paper from which information is

obtained for a journal entry is called a

Each transaction is described

by a source document that proves that the trans-

action did occur. For example, Encore Music pre-

pares a check stub for each cash payment made.

The check stub describes information about the

cash payment transaction for which the check is

prepared. The accounting concept, Objective

Evidence, is applied when a source document is

prepared for each transaction. (CONCEPT:

Objective Evidence)

A transaction should be journalized only if it

actually occurs. The amounts recorded must be

accurate and true. Nearly all transactions result

in the preparation of a source document. Encore

Music uses five source documents: checks, sales

invoices, receipts, calculator tapes, and

memorandums.

source document.

double-entry accounting.

general journal.

entry.

66 CHAPTER 4 Recording Transactions in a General Journal

4-1 Journals, Source Documents, and

Recording Entries in a Journal

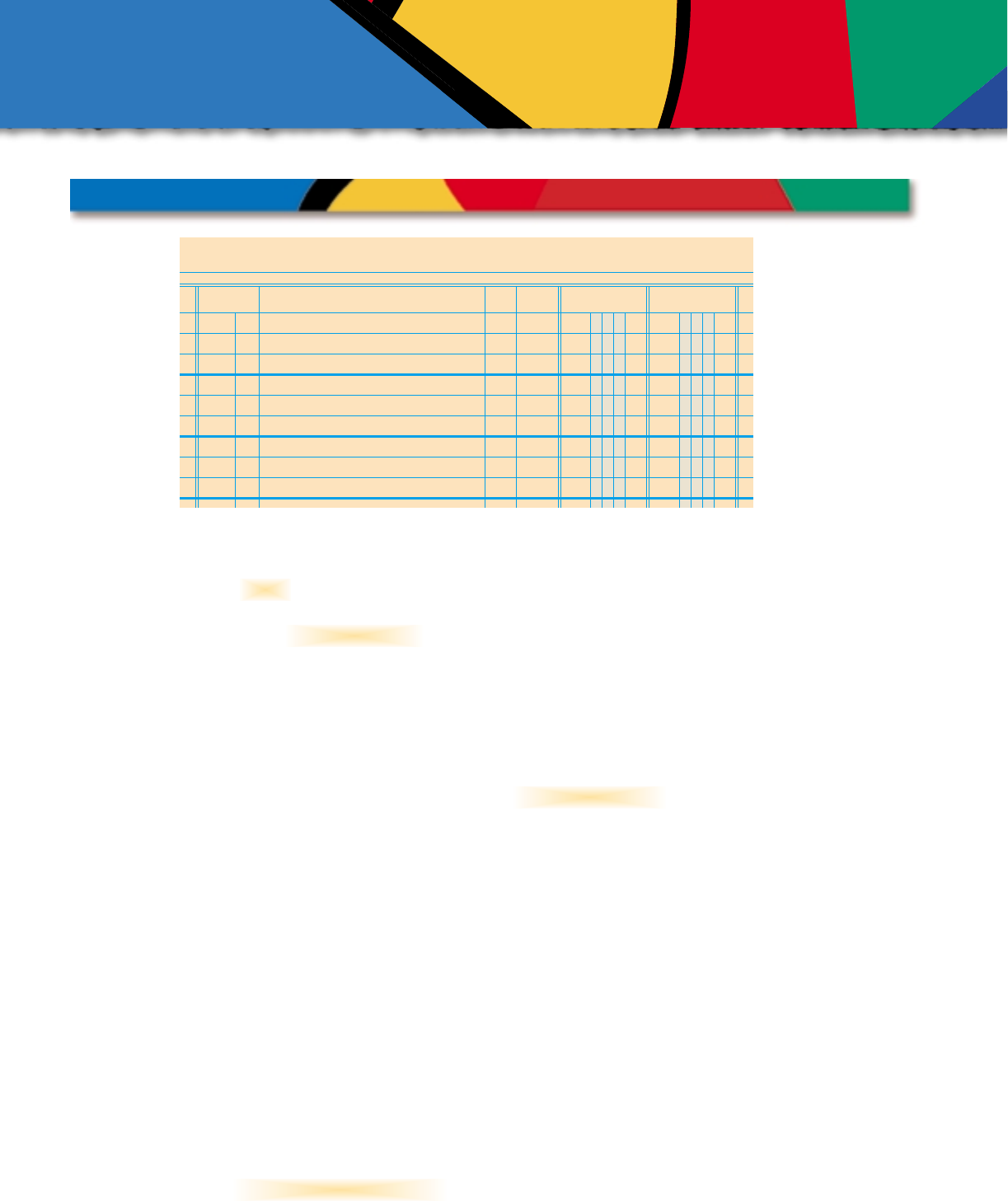

A GENERAL JOURNAL

GENERAL JOURNAL PAGE

1

2

3

4

5

6

7

8

9

1

2

3

4

5

6

7

8

9

DATE ACCOUNT TITLE DEBIT CREDIT

DOC.

NO.

POST.

REF.

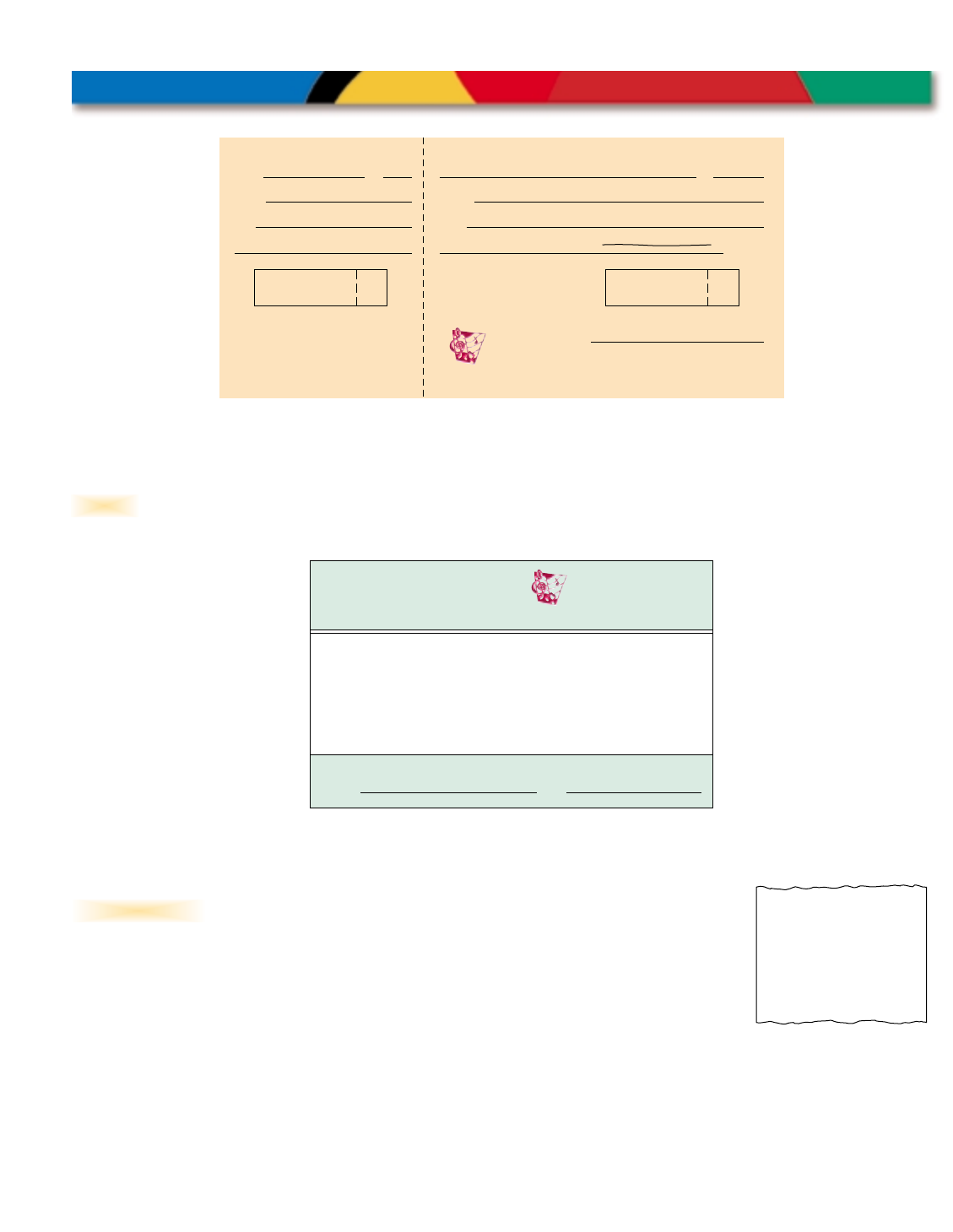

A business form ordering a bank to pay cash

from a bank account is called a The

source document for cash payments is a check.

Encore Music makes all cash payments by check.

The checks are prenumbered to help Encore

Music account for all checks. Encore Music’s

record of information on a check is the check

stub prepared at the same time as the check. A

check and check stub prepared by Encore Music

are shown.

Procedures for preparing checks and check

stubs are described in Chapter 6.

check.

CHECKS

SALES INVOICES

NO. 1 $

Date 20

To

For

BAL. BRO’T. FOR’D. . . . . . . . . . . .

AMT. DEPOSITED . . .

SUBTOTAL . . . . . . . . . . . . . . . . . . .

OTHER:

SUBTOTAL. . . . . . . . . . . . . . . . . . .

AMT. THIS CHECK . . . . . . . . . . . .

BAL. CAR’D. FOR’D. . . . . . . . . . . .

Date

063101098 43452119

FOR

$

20

PAY TO THE

ORDER OF

NO. 1 63-109

631

For Classroom Use Only

DOLLARS

peoples national bank

530 Anoka Avenue

Tampa, FL 33601

Tampa, FL 33602

1,577.00

August 3, --

Quick Clean Supplies Co.

Supplies

0 00

10,000 00

10,000 00

81 --

10,000 00

1,577 00

8,423 00

August 3, --

Quick Clean Supplies Co. 1,577.00

One thousand five hundred seventy-seven and no

100

Supplies Barbara Treviño

Encore Music

CHAPTER 4 Recording Transactions in a General Journal 67

When services are sold on account, the seller

prepares a form showing information about the

sale. A form describing the goods or services

sold, the quantity, and the price is called an

An invoice used as a source document

for recording a sale on account is called a

A sales invoice is also referred to

as a sales ticket or a sales slip.

A sales invoice is prepared in duplicate. The

original copy is given to the customer. The copy

is used as the source document for the sale on

account transaction. (CONCEPT: Objective

Evidence) Sales invoices are numbered in

sequence.

sales invoice.

invoice.

530 Anoka Avenue

Tampa, FL 33601

Sold to: No.

Date

Terms

Kids Time

405 Michigan Avenue

Tampa, FL 33619

1

8/12/--

30 days

Description Amount

Individual lessons on Aug. 12

Total

$200.00

$200.00

Encore Music

68 CHAPTER 4 Recording Transactions in a General Journal

Receipts

A business form giving written

acknowledgement for cash received is called a

When cash is received from sources

other than sales, Encore Music prepares a

receipt. The receipts are prenumbered to help

account for all of the receipts. A receipt is the

source document for cash received from transac-

tions other than sales. (CONCEPT: Objective

Evidence)

receipt.

OTHER SOURCE DOCUMENTS

530 Anoka Avenue

Tampa, FL 33601

Encore Music

August 1,

No. 1

Date 20

From

For

$$

Receipt No. 1

20

Rec’d

from

For

Dollars

Amount

Received By

--

Barbara Treviño

Investment

10,000 00 10,000 00

August 1, --

Barbara Treviño

Investment

Ten thousand and no/100

Barbara Treviño

530 Anoka Avenue

Tampa, FL 33601

Encore

Music

Signed: Date:

MEMORANDUM No. 1

Bought supplies on account from

Ling Music Supplies, $2,720.00

Barbara Treviño August 7, 20--

Memorandums

A form on which a brief message is written

describing a transaction is called a

When no other source

document is prepared for a transaction, or when

an additional explanation is needed about a

transaction, Encore Music prepares a memoran-

dum. (CONCEPT: Objective Evidence) Encore

Music’s memorandums are prenumbered to help

account for all of the memorandums. A brief

note is written on the memorandum to describe

the transaction.

Calculator Tapes

Encore Music collects cash at the time

services are rendered to customers. At the end of

each day, Encore Music uses a printing electronic

calculator to total the amount of cash received

from sales for that day. By totaling all the

individual sales, a single

source document is

produced for the total

sales of the day. Thus,

time and space are saved

by recording only one

entry for all of a day’s

sales. The calculator tape is the source document

for daily sales. (CONCEPT: Objective Evidence) A

calculator tape used as a source document is

shown.

Encore Music dates and numbers each calcu-

lator tape. For example, in the illustration, the

number, T12, indicates that the tape is for the

twelfth day of the month.

memorandum.

0

.

00

150

.

00

65

.

00

110

.

00

325

.

00

*

*

Aug. 12, 20--

T12

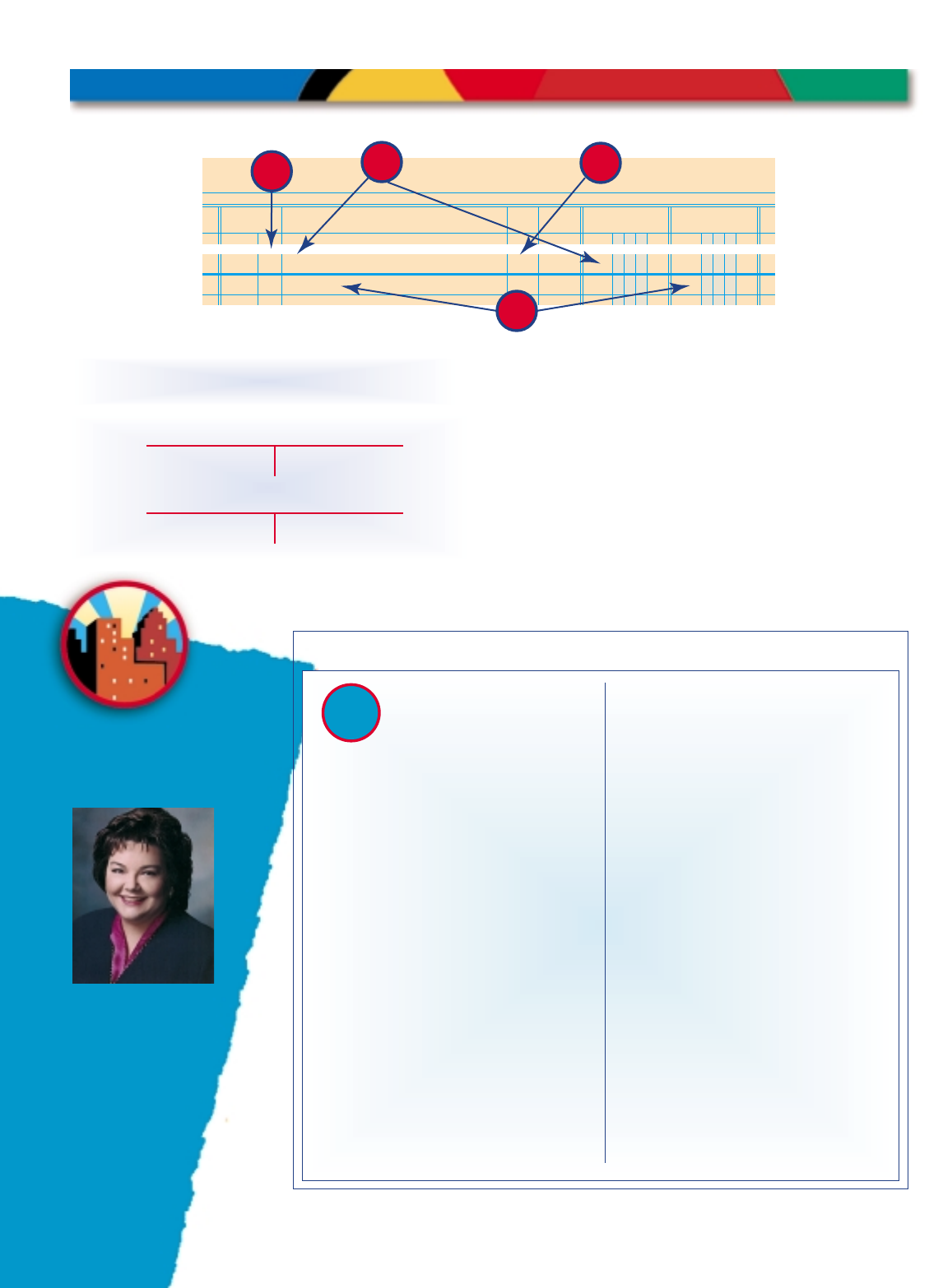

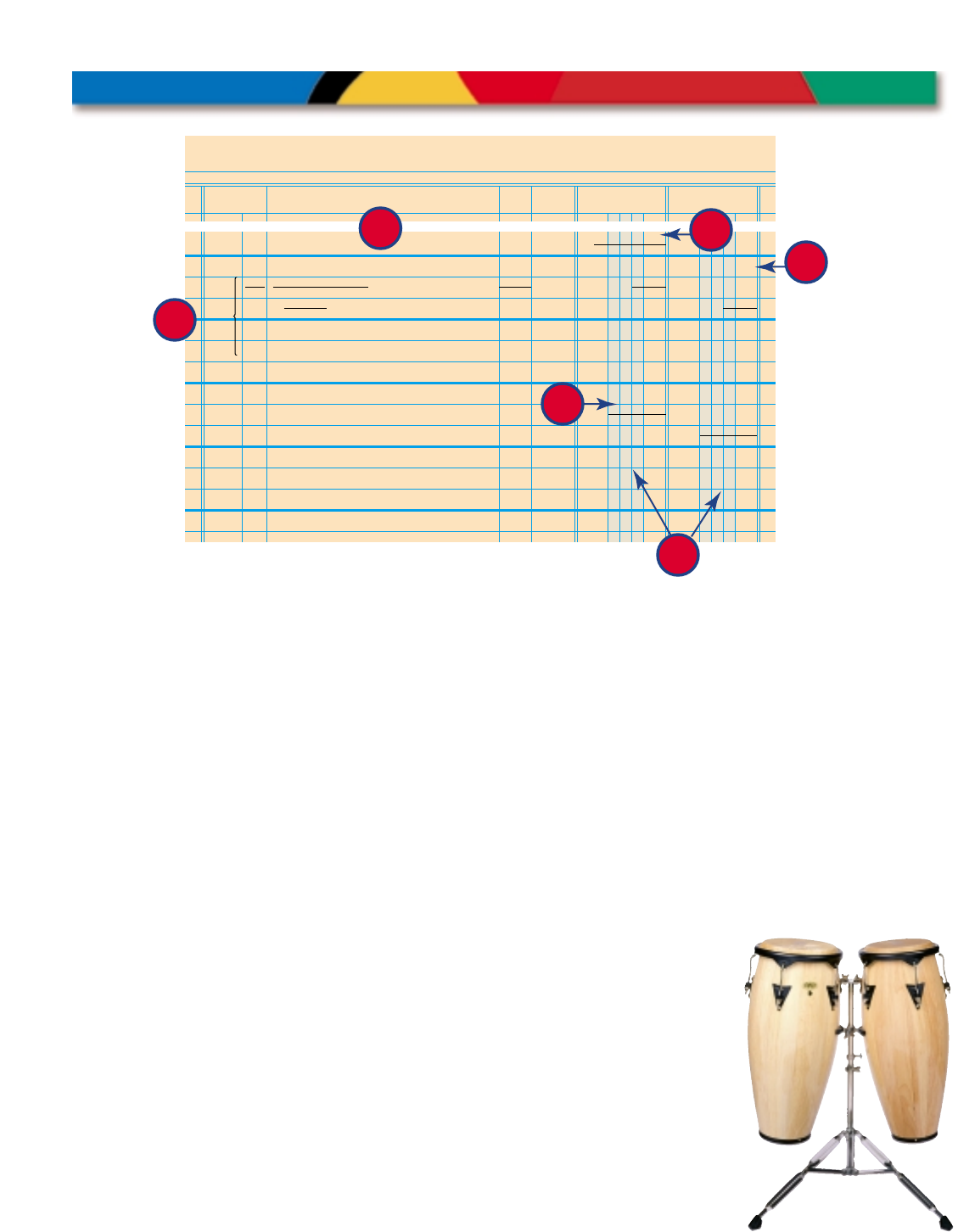

Information for each transaction recorded in

a journal is known as an entry. An entry consists

of four parts: (1) date, (2) debit, (3) credit, and

(4) source document. Before a transaction is

recorded in a journal, the transaction is analyzed

into its debit and credit parts.

The source document for this transaction is

Receipt No. 1. (CONCEPT: Objective Evidence)

The analysis of this transaction is shown in the

T accounts.

The asset account, Cash, is increased by a

debit, $10,000.00. The owner’s capital account,

Barbara Treviño, Capital, is increased by a credit,

$10,000.00.

August 1. Received cash from owner as an

investment, $10,000.00. Receipt No. 1.

CHAPTER 4 Recording Transactions in a General Journal 69

RECEIVED CASH FROM OWNER AS AN INVESTMENT

GENERAL JOURNAL PAGE 1

1

2

1

2

DATE ACCOUNT TITLE DEBIT CREDIT

Aug.

20-- 1 Cash

Barbara Treviño, Capital

DOC.

NO.

POST.

REF.

1000000

1000000

R1

4Source

Document

3Credit

2Debit

1Date

F

Y

I

Dollars and cents signs and decimal points

are not used when writing amounts on

ruled accounting paper. Sometimes a color

tint or a heavy vertical rule is used on

printed accounting paper to separate the

dollars and cents columns.

Journalizing cash received from owner as an investment

1. Date. Write the date, 20--, Aug. 1, in the Date column. This entry is the first one on this journal page.

Therefore, the year and month are both written for this entry. Neither the year nor the month are written

again on the same page.

2. Debit. Write the title of the account debited, Cash, in the Account Title column. Write the debit amount,

$10,000.00, in the Debit column.

3. Credit. On the next line, indented about 1 centimeter, write the title of the account credited, Barbara

Treviño, Capital, in the Account Title column. This account title is indented to indicate that this account is

credited. Write the credit amount, $10,000.00, in the Credit column.

4. Source document. On the first line of the entry, write the source document number, R1, in the Doc. No.

column. The source document number, R1, indicates that this is Receipt No. 1. (The source document num-

ber is a cross reference from the journal to the source document. If more details are needed about this

transaction, a person can refer to Receipt No. 1.)

Debits must equal credits for each entry in a general journal. After the entry is journalized, the equality of

debits and credits is verified. For this entry, the total debits, $10,000.00, equal the total credits,

$10,000.00.

S

T

E

P

S

Cash

10,000.00

Barbara Treviño, Capital

10,000.00

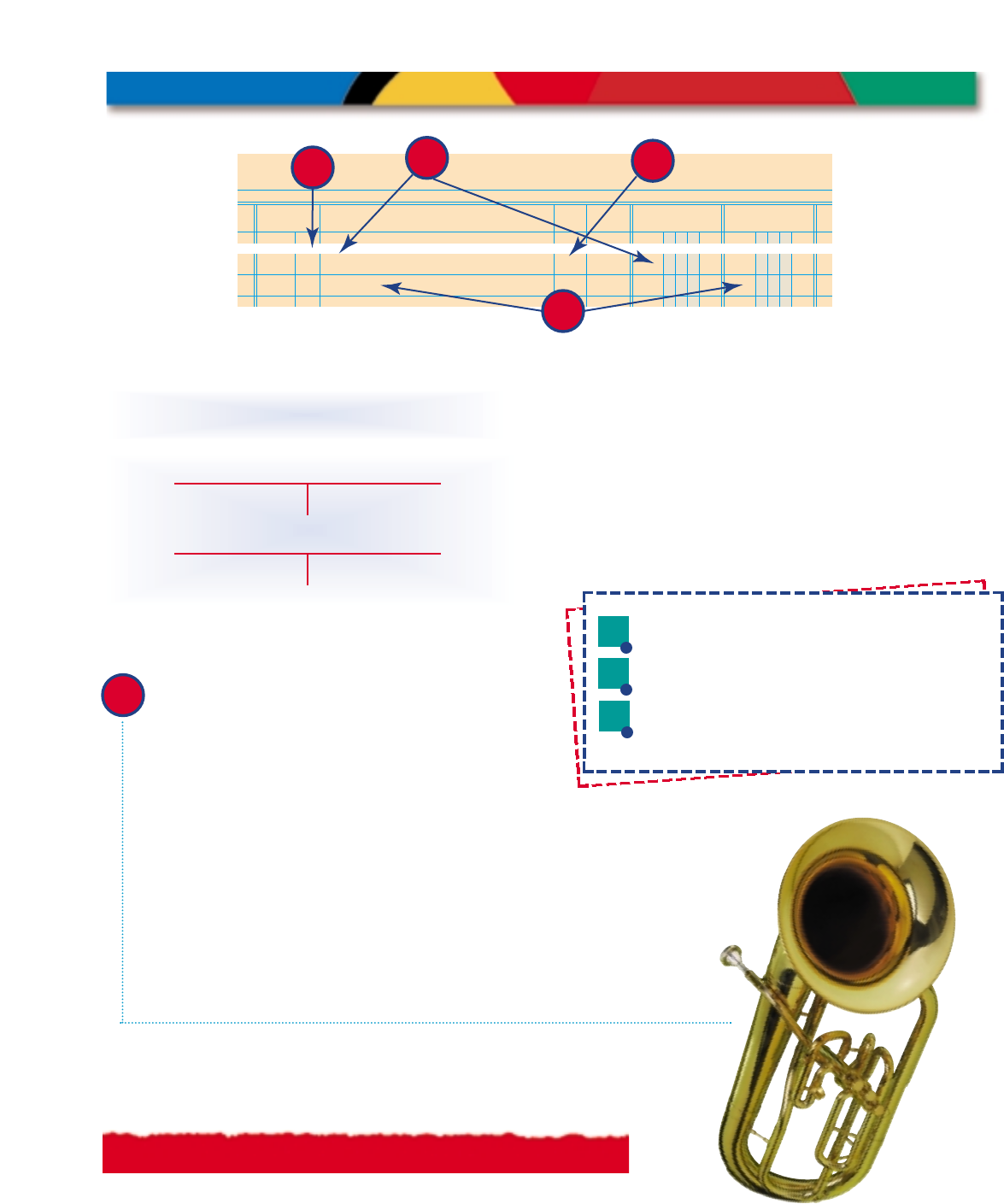

The source document for this transaction is

Check No. 1. (CONCEPT: Objective Evidence) The

analysis of this transaction is shown in the

T accounts.

The asset account, Supplies, is increased by a

debit, $1,577.00. The asset account, Cash, is

decreased by a credit, $1,577.00.

August 3. Paid cash for supplies, $1,577.00.

Check No. 1.

70 CHAPTER 4 Recording Transactions in a General Journal

PAID CASH FOR SUPPLIES

GENERAL JOURNAL PAGE 1

3

4

3

4

DATE ACCOUNT TITLE DEBIT CREDIT

3 Supplies

Cash

DOC.

NO.

POST.

REF.

157700

157700

C1

4Source

Document

3Credit

2Debit

1Date

Supplies

1,577.00

Cash

1,577.00

F

Y

I

If you draw T accounts for analyzing trans-

actions, it will make journalizing easier.

Journalizing cash paid for supplies

1. Date. Write the date, 3, in the Date column. This is not the first entry on the

journal page. Therefore, the year and month are not written for this entry.

2. Debit. Write the title of the account debited, Supplies, in the Account Title

column. Write the debit amount, $1,577.00, in the Debit column.

3. Credit. On the next line, indented about 1 centimeter, write the title

of the account credited, Cash, in the Account Title column. Write

the credit amount, $1,577.00, in the Credit column.

4. Source document. On the first line on this entry, write the

source document number, C1, in the Doc. No. column. The source

document number, C1, indicates that this is Check No. 1.

For this entry, the total debits, $1,577.00, equal the total credits,

$1,577.00.

S

T

E

P

S

REMEMBER

If you misspell words in your written communications, people may mistrust the quality of your accounting skills. Note

that in the word receipt the “e” comes before the “i” and there is a silent “p” before the “t” at the end of the word.

Journalizing entries into a general journal

A journal is given in the Working Papers. Your instructor will guide you through the following

example.

Ruth Muldoon owns Muldoon Copy Center, which uses the following accounts:

Cash Prepaid Insurance Ruth Muldoon, Drawing Rent Expense

Accts. Rec.—Lester Dodge Accts. Pay.—Ron’s Supplies Sales Utilities Expense

Supplies Ruth Muldoon, Capital Miscellaneous Expense

Transactions: Apr. 1. Received cash from owner as an investment, $7,000.00. R1.

2. Paid cash for supplies, $425.00. C1.

4. Journalize each transaction completed during April of the current year. Use page 1 of the jour-

nal. Source documents are abbreviated as follows: check, C; memorandum, M; receipt, R; sales

invoice, S; calculator tape, T. Save your work to complete Work Together on page

75

.

Journalizing entries into a general journal

A journal is given in the Working Papers. Work this problem independently.

Gale Klein owns Klein’s Service Center, which uses the following accounts:

Cash Prepaid Insurance Gale Klein, Drawing Miscellaneous Expense

Accts. Rec.—Connie Vaughn Accts. Pay.—Osamu Supply Co. Sales Rent Expense

Supplies Gale Klein, Capital Advertising Expense

Transactions: June 2. Received cash from owner as an investment, $1,500.00. R1.

3. Paid cash for supplies, $35.00. C1.

5. Journalize each transaction completed during June of the current year. Use page 1 of the jour-

nal. Source documents are abbreviated as follows: check, C; memorandum, M; receipt, R; sales

invoice, S; calculator tape, T. Save your work to complete On Your Own on page

75

.

journal

journalizing

entry

general

journal

double-entry

accounting

source

document

check

invoice

sales invoice

receipt

memorandum

1. In what order are transactions recorded

in a journal?

2. Why are source documents important?

3. List the four parts of a journal entry.

ERMS

REVIEW

ERMS

REVIEW

T

TUDIT YOUR

UNDERSTANDING

UDIT YOUR

UNDERSTANDING

A

A

N YOUR

OWN

ON YOUR

OWN

O

ORK

TOGETHER

W

ORK

TOGETHER

W

CHAPTER 4 Recording Transactions in a General Journal 71

72 CHAPTER 4 Recording Transactions in a General Journal

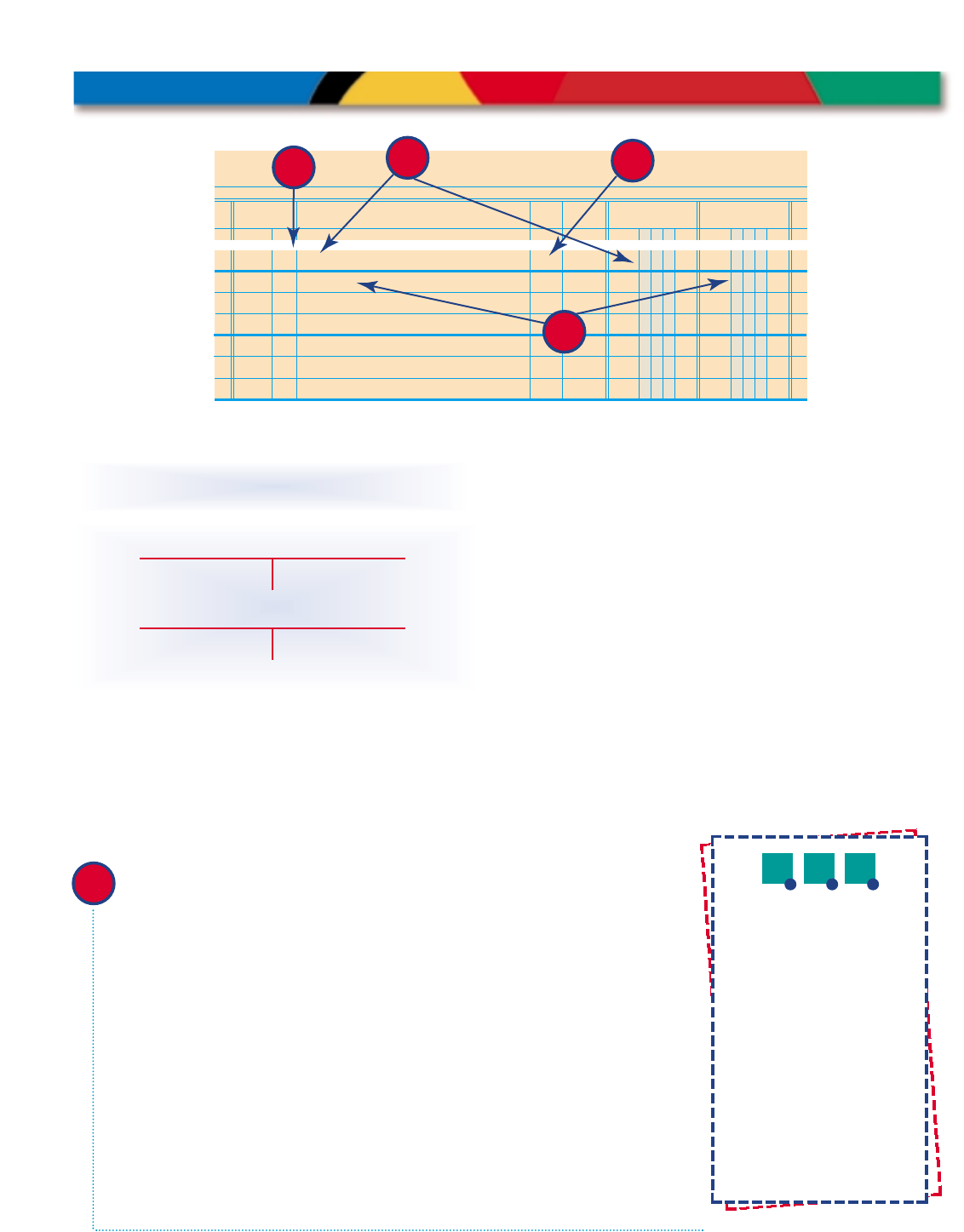

The source document for this transaction is

Check No. 2. (CONCEPT: Objective Evidence) The

analysis of this transaction is shown in the

T accounts.

The asset account, Prepaid Insurance, is

increased by a debit, $1,200.00. The asset

account, Cash, is decreased by a credit, $1,200.00.

August 4. Paid cash for insurance, $1,200.00.

Check No. 2.

PAID CASH FOR INSURANCE

Prepaid Insurance

1,200.00

Cash

1,200.00

GENERAL JOURNAL PAGE 1

5

6

5

6

DATE ACCOUNT TITLE DEBIT CREDIT

4 Prepaid Insurance

Cash

DOC.

NO.

POST.

REF.

120000

120000

C2

Source

Document

3Credit

2Debit

1Date 4

Journalizing cash paid for insurance

1. Date. Write the date, 4, in the Date column.

2. Debit. Write the title of the account debited, Prepaid

Insurance, in the Account Title column. Write the debit amount,

$1,200.00, in the Debit column.

3. Credit. On the next line, indented about 1 centimeter, write the

title of the account credited, Cash, in the Account Title column. Write

the credit amount, $1,200.00, in the Credit column.

4. Source document. On the first line of this entry, write the source docu-

ment number, C2, in the Doc. No. column.

For this entry, the total debits, $1,200.00, equal the total credits,

$1,200.00.

S

T

E

P

S

REMEMBER

All amounts recorded in the general journal must have an account title writ-

ten in the Account Title column.

4-2 Journalizing Buying Insurance, Buying on

Account, and Paying on Account

CHAPTER 4 Recording Transactions in a General Journal 73

Encore Music ordered these supplies by tele-

phone. Encore Music wishes to record this trans-

action immediately. Therefore, a memorandum

is prepared that shows supplies received on

account.

The source document for this transaction is

Memorandum No. 1. (CONCEPT: Objective

Evidence) The analysis of this transaction is

shown in the T accounts.

The asset account, Supplies, is increased by a

debit, $2,720.00. The liability account, Accounts

Payable—Ling Music Supplies, is increased by a

credit, $2,720.00

August 7. Bought supplies on account from

Ling Music Supplies, $2,720.00. Memorandum

No. 1.

BOUGHT SUPPLIES ON ACCOUNT

GENERAL JOURNAL PAGE 1

7

8

7

8

DATE ACCOUNT TITLE DEBIT CREDIT

7 Supplies

Accts. Pay.—Ling Music Supplies

DOC.

NO.

POST.

REF.

272000

272000

M1

4Source

Document

2Debit

1Date

3Credit

F Y I

Of all service

businesses in the

United States, only 4

percent employ 50 or

more people and 80

percent have fewer

than 10 employees.

Journalizing supplies bought on account

1. Date. Write the date, 7, in the Date column.

2. Debit. Write the title of the account debited, Supplies, in the

Account Title column. Write the debit amount, $2,720.00,

in the Debit column.

3. Credit. On the next line, indented about 1 centimeter, write

the title of the account credited, Accounts Payable—Ling Music

Supplies, in the Account Title column. Write the credit amount,

$2,720.00, in the Credit column.

4. Source document. On the first line of this entry, write the source

document number, M1, in the Doc. No. column.

For this entry, the total debits, $2,720.00, equal the total credits,

$2,720.00.

S

T

E

P

S

Supplies

2,720.00

Accts. Pay.—Ling Music Supplies

2,720.00

REMEMBER

When recording transactions in a general journal, the account title that is credited is normally indented.

The source document for this transaction is

Check No. 3. (CONCEPT: Objective Evidence) The

analysis of this transaction is shown in the

T accounts.

The liability account, Accounts Payable—Ling

Music Supplies, is decreased by a debit, $1,360.00.

The asset account, Cash, is decreased by a credit,

$1,360.00.

August 11. Paid cash on account to Ling

Music Supplies, $1,360.00. Check No. 3.

PAID CASH ON ACCOUNT

GENERAL JOURNAL PAGE 1

9

10

9

10

DATE ACCOUNT TITLE DEBIT CREDIT

11 Accts. Pay.—Ling Music Supplies

Cash

DOC.

NO.

POST.

REF.

136000

136000

C3

4Source

Document

3Credit

2Debit

1Date

Cash

1,360.00

Accts. Pay.—Ling Music Supplies

1,360.00

n high school, Mary M.

Witherspoon considered

pursuing a degree in

accounting. Her career choice was

confirmed by ACCUMATION, a

career education program for high

school students sponsored by the

Dallas Chapter of the Texas Society of

CPAs. Students participate in this

week-long summer program, which

includes visits to an international

accounting firm and the chance to sit

in on university accounting classes.

Mary graduated with a BBA in

Accounting and works for Oryx

Energy Company, a large

independent producer of oil and gas

in Dallas. Currently in gas balancing

accounting, she reconciles records of

jointly owned properties to ensure

Oryx receives their entitled gas

volumes. Working in the corporate

environment has allowed Mary to

change job responsibilities over her

career to gain additional experience.

Mary believes that exceptional

people skills coupled with technical

experience is the formula for business

success. People skills include

written and verbal communication,

respecting diversity, and the ability

to work in teams.

Mary also serves as a district

vice-president of the American

Business Women’s Association

(ABWA). ABWA promotes the

advancement of women in business by

sponsoring continuing education, pro-

viding leadership training, and offer-

ing encouragement.

“High school students can contact

their state or local society of certified

public accountants for accounting

career information,” says Mary. “We

CPAs support programs to encourage

student interest in our field.”

I

M

ARY

W

ITHERSPOON

A

CCOUNTING

AT

W

ORK

74

Journalizing entries into a general journal

Use the journal that you started for Work Together on page

71

. Your instructor will guide you

through the following example.

Ruth Muldoon owns Muldoon Copy Center, which uses the following accounts:

Cash Prepaid Insurance Ruth Muldoon, Drawing Rent Expense

Accts. Rec.—Lester Dodge Accts. Pay.—Ron’s Supplies Sales Utilities Expense

Supplies Ruth Muldoon, Capital Miscellaneous Expense

Transactions: Apr. 5. Bought supplies on account from Ron’s Supplies, $300.00. M1.

7. Paid cash for insurance, $600.00. C2.

9. Paid cash on account to Ron’s Supplies, $300.00. C3.

5. Journalize the transactions continuing on the next blank line of page 1 of the journal. Save

your work to complete Work Together on page

81

.

Journalizing entries into a general journal

Use the journal that you started for On Your Own on page

71

. Work this problem

independently.

Gale Klein owns Klein’s Service Center, which uses the following accounts:

Cash Prepaid Insurance Gale Klein, Drawing Miscellaneous Expense

Accts. Rec.—Connie Vaughn Accts. Pay.—Osamu Supply Co. Sales Rent Expense

Supplies Gale Klein, Capital Advertising Expense

Transactions: June 5. Paid cash for insurance, $100.00. C2.

9. Bought supplies on account from Osamu Supply Co., $155.00. M1.

10. Paid cash on account to Osamu Supply Co., $155.00. C3.

6. Journalize the transactions continuing on the next blank line of page 1 of the journal. Save

your work to complete On Your Own on page

81

.

1. When cash is paid for insurance, which account is listed on the first line of the entry?

2. When supplies are bought on account, which account is listed on the first line of the entry?

3. When supplies are bought on account, which account is listed on the second line of the entry?

4. When cash is paid on account, which account is listed on the second line of the entry?

UDIT YOUR

UNDERSTANDING

UDIT YOUR

UNDERSTANDING

A

A

N YOUR

OWN

ON YOUR

OWN

O

ORK

TOGETHER

W

ORK

TOGETHER

W

CHAPTER 4 Recording Transactions in a General Journal 75

76 CHAPTER 4 Recording Transactions in a General Journal

The source document for this transaction is

Calculator Tape No. 12. (CONCEPT: Objective

Evidence) The analysis of this transaction is

shown in the T accounts.

The asset account, Cash, is increased by a

debit, $325.00. The revenue account, Sales, is

increased by a credit, $325.00.

The reason that Sales is increased by a credit

is discussed in the previous chapter. The

owner’s capital account has a normal credit bal-

ance. Increases in the owner’s capital account

are shown as credits.

Because revenue increases owner’s equity,

increases in revenue are recorded as credits. A

revenue account, therefore, has a normal credit

balance.

August 12. Received cash from sales,

$325.00. Tape No. 12.

RECEIVED CASH FROM SALES

GENERAL JOURNAL PAGE 1

11

12

11

12

DATE ACCOUNT TITLE DEBIT CREDIT

12 Cash

Sales

DOC.

NO.

POST.

REF.

32500

32500

T12

4Source

Document

3Credit

2Debit

1Date

4-3 Journalizing Transactions That Affect Owner’s

Equity and Receiving Cash on Account

Journalizing cash received from sales

1. Date. Write the date, 12, in the Date column.

2. Debit. Write the title of the account debited, Cash, in the Account Title column. Write the debit amount,

$325.00, in the Debit column.

3. Credit. On the next line, indented about 1 centimeter, write the title of the account credited, Sales, in the

Account Title column. Write the credit amount, $325.00, in the Credit column.

4. Source document. On the first line of this entry, write the source document number, T12, in the Doc.

No. column.

For this entry, the total debits, $325.00, equal the total credits, $325.00.

S

T

E

P

S

Sales

325.00

Cash

325.00

REMEMBER

Don’t forget to record the source document in the Doc. No. column of the general journal.

CHAPTER 4 Recording Transactions in a General Journal 77

The source document for this transaction is

Sales Invoice No. 1. (CONCEPT: Objective

Evidence) The analysis of this transaction is

shown in the T accounts.

The asset account, Accounts Receivable—Kids

Time, is increased by a debit, $200.00. The

revenue account, Sales, is increased by a credit,

$200.00.

August 12. Sold services on account to Kids

Time, $200.00. Sales Invoice No. 1.

SOLD SERVICES ON ACCOUNT

GENERAL JOURNAL PAGE 1

13

14

13

14

DATE ACCOUNT TITLE DEBIT CREDIT

12 Accounts Rec.—Kids Time

Sales

DOC.

NO.

POST.

REF.

20000

20000

S1

4Source

Document

3Credit

2Debit

1Date

Sales

200.00

Accts. Rec.—Kids Time

200.00

Journalizing services sold on account

1. Date. Write the date, 12, in the Date column.

2. Debit. Write the title of the account debited,

Accounts Receivable—Kids Time, in the Account

Title column. Write the debit amount, $200.00, in

the Debit column.

3. Credit. On the next line, indented about 1 centimeter, write the title

of the account credited, Sales, in the Account Title column. Write the

credit amount, $200.00, in the Credit column.

4. Source document. Write the source document number, S1, in the

Doc. No. column.

For this entry, the total debits, $200.00, equal the total credits,

$200.00.

S

T

E

P

S

REMEMBER

In double-entry accounting, each transaction affects at least two

accounts. At least one account will be debited and at least one account

will be credited.

F

Y

I

Accounting is not just for accountants. For

example, a performing artist earns revenue

from providing a service. Financial

decisions must be made such as the cost of

doing a performance, the percentage of rev-

enue paid to a manager, travel expenses,

and the cost of rehearsal space.

78 CHAPTER 4 Recording Transactions in a General Journal

The source document for this transaction is

Check No. 4. (CONCEPT: Objective Evidence) The

analysis of this transaction is shown in the

T accounts.

The expense account, Rent Expense, is

increased by a debit, $250.00. The asset account,

Cash, is decreased by a credit.

The reason that Rent Expense is increased by

a debit is discussed in the previous chapter. The

owner’s capital account has a normal credit bal-

ance. Decreases in the owner’s capital account

are shown as debits.

Because expenses decrease owner’s equity,

increases in expenses are recorded as debits. An

expense account, therefore, has a normal debit

balance.

August 12. Paid cash for rent, $250.00.

Check No. 4.

GENERAL JOURNAL PAGE 1

15

16

17

18

19

20

21

15

16

17

18

19

20

21

DATE ACCOUNT TITLE DEBIT CREDIT

12

12

Rent Expense

Cash

Utilities Expense

Cash

DOC.

NO.

POST.

REF.

25000

4500

25000

4500

C4

C5

4Source

Document

2Debit

1Date

3Credit

PAID CASH FOR AN EXPENSE

Journalizing cash paid for an expense

1. Date. Write the date, 12, in the Date column.

2. Debit. Write the title of the account debited, Rent Expense, in the

Account Title column. Write the debit amount, $250.00, in the Debit

column.

3. Credit. On the next line, indented about 1 centimeter, write the title of

the account credited, Cash, in the Account Title column. Write the credit

amount, $250.00, in the Credit column.

4. Source document. Write the source document number, C4, in the

Doc. No. column.

For this entry, the total debits, $250.00, equal the total credits, $250.00.

Whenever cash is paid for an expense, the journal entry is similar to the

entry discussed above. Therefore, the journal entry to record paying cash

for utilities is also illustrated.

S

T

E

P

S

Cash

250.00

Rent Expense

250.00

F Y I

Source documents

can be critically

important in

tracking down

errors. Businesses file

their source

documents so they

can be referred to if

it is necessary to

verify information

entered into their

journals.

CHAPTER 4 Recording Transactions in a General Journal 79

The source document for this transaction is

Receipt No. 2. (CONCEPT: Objective Evidence)

The analysis of this transaction is shown in the

T accounts.

The asset account, Cash, is increased

by a debit, $100.00. The asset account,

Accounts Receivable—Kids Time, is

decreased by a credit, $100.00.

August 12. Received cash on account from

Kids Time, $100.00. Receipt No. 2.

RECEIVED CASH ON ACCOUNT

GENERAL JOURNAL PAGE 1

19

20

19

20

DATE ACCOUNT TITLE DEBIT CREDIT

12 Cash

Accounts Rec.—Kids Time

DOC.

NO.

POST.

REF.

10000

10000

R2

4Source

Document

3Credit

2Debit

1Date

Accts. Rec.—Kids Time

100.00

Cash

100.00

Journalizing cash received on account

1. Date. Write the date, 12, in the Date column.

2. Debit. Write the title of the account debited, Cash, in the Account

Title column. Write the debit amount, $100.00, in the Debit

column.

3. Credit. On the next line, indented about 1 centimeter, write the

title of the account credited, Accounts Receivable—Kids

Time, in the Account Title column. Write the credit

amount, $100.00, in the Credit column.

4. Source document. Write the source document

number, R2, in the Doc. No. column.

For this entry, the total debits, $100.00, equal

the total credits, $100.00.

S

T

E

P

S

REMEMBER

Increases in expenses and in withdrawals decrease owner’s equity. Decreases in owner’s equity are recorded as deb-

its. Therefore, increases in expenses and in withdrawals are recorded as debits.

The source document for this transaction is

Check No. 6. (CONCEPT: Objective Evidence) The

analysis of this transaction is shown in the

T accounts.

The reason that Barbara Treviño, Drawing is

increased by a debit is discussed in the previous

chapter. Decreases in the owner’s capital account

are shown as debits. Because withdrawals

decrease owner’s equity, increases in

withdrawals are recorded as debits. A withdraw-

al account, therefore, has a normal debit balance.

August 12. Paid cash to owner for personal

use, $100.00. Check No. 6.

PAID CASH TO OWNER FOR PERSONAL USE

GENERAL JOURNAL PAGE 1

21

22

21

22

DATE ACCOUNT TITLE DEBIT CREDIT

12 Barbara Treviño, Drawing

Cash

DOC.

NO.

POST.

REF.

10000

10000

C6

4Source

Document

3Credit

2Debit

1Date

Cash

100.00

Barbara Treviño, Drawing

100.00

L

EGAL

I

SSUES

IN

A

CCOUNTING

proprietorship is a business

owned and controlled by

one person. The advantages

of a proprietorship include:

•Ease of formation.

•Total control by the owner.

•Profits that are not shared.

However, there are some

disadvantages of organizing a propri-

etorship:

•Limited resources. The owner is the

only person who can invest cash

and other assets in the business.

•Unlimited liability. The owner is

totally responsible for the liabilities

of the business. Personal assets,

such as a car, can be claimed by

creditors to pay the business’s

liabilities.

•Limited expertise. Limited time,

energy, and experience can be put

into the business by the owner.

•Limited life. A proprietorship must

be dissolved when the owner dies

or decides to stop doing business.

The owner is required to follow

the laws of both the federal

government and the state and city in

which the business is formed. Most

cities and states have few, if any, legal

procedures to follow. Once any legal

requirements are met, the proprietor-

ship can begin business.

Should the owner decide to

dissolve the proprietorship, he or she

merely needs to stop doing business.

Noncash assets can be sold, with the

cash used to pay any creditors.

A

F

ORMING AND

D

ISSOLVING A

P

ROPRIETORSHIP

80

Journalizing transactions that affect owner’s equity into a general journal

Use the chart of accounts and journal from Work Together on page 75. Your instructor will guide

you through the following example.

Transactions: Apr. 12. Paid cash for rent, $950.00. C4.

13. Received cash from sales, $2,200.00. T13.

14. Sold services on account to Lester Dodge, $625.00. S1.

19. Paid cash for electric bill, $157.00. C5.

20. Received cash on account from Lester Dodge, $300.00. R2.

21. Paid cash to owner for personal use, $1,400.00. C6.

6. Journalize the transactions continuing on the next blank line of page 1 of the journal. Save

your work to complete Work Together on page 85.

Journalizing transactions that affect owner’s equity into a general journal

Use the chart of accounts and journal from On Your Own on page 75. Work this problem

independently.

Transactions: June 11. Paid cash for rent, $200.00. C4.

12. Sold services on account to Connie Vaughn, $200.00. S1.

16. Received cash from sales, $1,050.00. T16.

17. Paid cash for postage (Miscellaneous Expense), $32.00. C5.

19. Received cash on account from Connie Vaughn, $100.00. R2.

20. Paid cash to owner for personal use, $250.00. C6.

7. Journalize the transactions continuing on the next blank line of page 1 of the journal. Save

your work to complete On Your Own on page 85.

1. When cash is received from sales, which account is listed on the first line of the entry?

2. When cash is received from sales, which account is listed on the second line of the entry?

3. When services are sold on account, which account is listed on the second line of the entry?

4. When cash is paid for any reason, what abbreviation is used for the source document?

5. When cash is received on account, what abbreviation is used for the source document?

UDIT YOUR

UNDERSTANDING

UDIT YOUR

UNDERSTANDING

A

A

ORK

TOGETHER

W

ORK

TOGETHER

W

N YOUR

OWN

ON YOUR

OWN

O

CHAPTER 4 Recording Transactions in a General Journal 81

82 CHAPTER 4 Recording Transactions in a General Journal

A general journal page is complete when

there is insufficient space to record any more

entries. A partial view of Encore Music’s

completed page 1 of the general journal is

shown.

Encore Music has one blank line remaining

at the bottom of page 1. However, each journal

entry requires at least two lines. If a journal

entry is split between two different pages, the

equality of debits and credits for the entry is not

as easily verified. Also, to a person examining a

single journal page, a split entry will appear

incorrect. Therefore, a journal entry should not

be split and journalized on two different pages.

If there is only one blank line remaining on a

journal page, a new page is started.

4-4 Starting a New Journal Page

A COMPLETED JOURNAL PAGE

GENERAL JOURNAL PAGE 1

1

2

3

4

31

32

33

34

35

1

2

3

4

31

32

33

34

35

DATE ACCOUNT TITLE DEBIT CREDIT

Aug.

20-- 1

3

18

20

Cash

Barbara Treviño, Capital

Supplies

Cash

Advertising Expense

Cash

Supplies

Accts. Pay.—Sullivan Office Supplies

DOC.

NO.

POST.

REF.

1000000

157700

20000

2000

1000000

157700

20000

2000

R1

C1

C9

M2

Successful small business owners typically have the following

characteristics: confidence to make decisions, determination to

keep trying during hard times for the business, willingness to

take risks, creativity to surpass the competition, and an inner

need to achieve.

SMALL

BUSINESS

SSPPOOTTLLIIGGHHTT

STARTING A NEW GENERAL JOURNAL PAGE

After one page of a general journal is filled, a

new journal page is started. A new page is

started by writing the page number in the space

provided in the journal heading.

GENERAL JOURNAL PAGE 2

1

2

3

4

1

2

3

4

DATE ACCOUNT TITLE DEBIT CREDIT

DOC.

NO.

POST.

REF.

G

LOBAL

P

ERSPECTIVE

s our world becomes

smaller and global trade

increases, U.S. businesses

become more involved in transactions

with foreign businesses. These

transactions can be stated in terms of

U.S. dollars or in the currency of the

other country. If the transaction

involves foreign currency, a U.S. busi-

ness must convert the foreign currency

into U.S. dollars before the transaction

can be recorded. (CONCEPT: Unit of

Measurement)

The value of foreign currency may

change daily. In the United States, the

exchange rate is the value of foreign

currency in relation to the U.S. dollar.

Current exchange rates can be found

in many daily newspapers, on-line

services, or banks.

The exchange rate is stated in

terms of one unit of foreign currency.

Using Germany as an example, pre-

sume that one German mark is worth

0.5789 U.S. dollars (or about 58 U.S.

cents). This rate would be used when

exchanging German marks for U.S.

dollars.

A conversion formula can be used

to find out how many foreign currency

units can be purchased with one U.S.

dollar. The formula is:

1/exchange rate foreign

currency per U.S. dollar

1 dollar/0.5789 1.7272

marks per dollar

A

F

OREIGN

C

URRENCY

83

84 CHAPTER 4 Recording Transactions in a General Journal

In completing accounting work, Encore

Music follows standard accounting practices.

These practices include procedures for error cor-

rections, abbreviating words, writing dollar and

cents signs, and rulings.

1. Errors are corrected in a way that does not

cause doubts about what the correct infor-

mation is. If an error is recorded, cancel

the error by neatly drawing a line through

the incorrect item. Write the correct item

immediately above the canceled item.

2. Sometimes an entire entry is incorrect and

is discovered before the next entry is jour-

nalized. Draw neat lines through all parts

of the incorrect entry. Journalize the entry

correctly on the next blank lines.

3. Sometimes several correct entries are

recorded after an incorrect entry is made.

The next blank lines are several entries

later. Draw neat lines through all incorrect

parts of the entry. Record the correct items

on the same lines as the incorrect items,

directly above the canceled parts.

4. Words in accounting records are written

in full when space permits. Words may be

abbreviated only when space is limited.

All items are written legibly.

5. Dollars and cents signs and decimal

points are not used when writing

amounts on ruled accounting paper.

Sometimes a color tint or a heavy vertical

rule is used on printed accounting paper

to separate the dollars and cents columns.

6. Two zeros are written in the cents column

when an amount is in even dollars, such

as $500.00. If the cents column is left

blank, doubts may

arise later about

the cor-

rect amount.

7. Neatness is very

important in

accounting

records so that

there is never any

doubt about what

information has

been recorded. A

ruler is used to

draw lines.

GENERAL JOURNAL PAGE 2

9

10

11

12

13

14

15

16

17

18

19

20

21

22

DATE ACCOUNT TITLE DEBIT CREDIT

28

29

29

29

30

30

Cash

Sales

Rent Expense

Cash

Repair Expense

Cash

Supplies

Cash

Miscellaneous Expense

Cash

Barbara Treviño, Drawing

Cash

DOC.

NO.

POST.

REF.

350000

500

5000

1000

10000

50000

35000

500

5000

1000

10000

50000

T28

C22

C21

C22

C23

C24

35000

1000

1000

4

3

1

2

6

9

10

11

12

13

14

15

16

17

18

19

20

21

22

5

STANDARD ACCOUNTING PRACTICES

1. When is a general journal page complete?

2. If an entire entry is incorrect and is discovered before the next entry is journalized, how

should the incorrect entry be corrected?

3. If several correct entries are recorded after an incorrect entry is made, how should the

incorrect entry be corrected?

Journalizing transactions and starting a new general journal page

Use the journal from Work Together on page 81. Your instructor will guide you through the follow-

ing examples.

Transactions: Apr. 22. Paid cash for water bill (Utilities Expense), $150.00. C7.

23. Sold services on account to Lester Dodge, $317.00. S2.

26. Received cash from sales, $1,560.00. T26.

27. Paid cash to owner for personal use, $750.00. C8.

27. Paid cash for supplies, $24.00. C9.

27. Paid cash for postage (Miscellaneous Expense), $35.00. C10.

29. Received cash on account from Lester Dodge, $75.00. R3.

30. Received cash from sales, $743.00. T30.

4. Journalize the transactions for April 22 through 27.

5. Use page 2 of the journal to journalize the remaining transactions for April.

Journalizing transactions and starting a new general journal page

Use the journal from On Your Own on page 81. Work these problems independently.

Transactions: June 23. Sold services on account to Connie Vaughn, $135.00. S2.

24. Paid cash for advertising, $48.00. C7.

25. Received cash from sales, $850.00. T25.

26. Paid cash for delivery charges (Miscellaneous Expense), $17.00. C8.

26. Received cash on account from Connie Vaughn, $100.00. R3.

26. Paid cash for postage (Miscellaneous Expense), $15.00. C9.

27. Paid cash for supplies, $21.00. C10

30. Received cash from sales, $235.00. T30.

6. Journalize the transactions for June 23 through 26.

7. Use page 2 of the journal to journalize the remaining transactions for June.

CHAPTER 4 Recording Transactions in a General Journal 85

UDIT YOUR

UNDERSTANDING

UDIT YOUR

UNDERSTANDING

A

A

N YOUR

OWN

ON YOUR

OWN

O

ORK

TOGETHER

W

ORK

TOGETHER

W

PRENUMBERED

DOCUMENTS

As one way to control the

operations of the business, a

company often will use

prenumbered documents. Such

a document is one that has the

form number printed on it in

advance. The most common

example in everyday life is the

personal check.

Businesses use several

prenumbered documents.

Examples include business

checks, sales invoices, purchase

orders, receipts, and

memorandums.

The use of prenumbered

documents allows a simple way

to ensure that all documents

are recorded. For example,

when a business records the

checks written during a period

of time, all check numbers

should be accounted for in

numeric order. The person

recording the checks must

watch to see that no numbers

are skipped. In this way,

the business is more

confident that all checks

are recorded.

By using

several types of

prenumbered

documents, the

business helps ensure

that all transactions are

properly recorded.

Another way a business

tries to control operations is

through the use of batch totals.

When many (sometimes

hundreds) of documents are

being recorded, the total

amount can be used to help

ensure that all documents are

recorded.

For example, when sales

invoices are recorded, the total

of all the invoices is calculated

prior to the invoices being

recorded. Once all invoices

are recorded, another total

can be calculated. If the

two totals are equal,

it can be assumed

that all invoices

have been recorded. If

the totals

do not equal

, it

may indicate that a document

was skipped.

Research: Contact a local

business and ask what

prenumbered documents are

used there. Determine how the

business uses the documents to

ensure that all documents are

recorded properly.

explore accounting

After completing this chapter, you can

1. Define important accounting terms related to journalizing transactions.

2. Identify accounting concepts and practices related to journalizing

transactions.

3. Record in a general journal transactions to set up a business.

4. Record in a general journal transactions to buy insurance for cash and

supplies on account.

5. Record in a general journal transactions that affect owner’s equity and

receiving cash on account.

6. Start a new journal page.

CHAPTER

SUMMARY

4

86 CHAPTER 4 Recording Transactions in a General Journal

CHAPTER 4 Recording Transactions in a General Journal 87

APPLICATION PROBLEM

Journalizing transactions into a general journal

Dennis Gilbert owns a service business called D & G Company, which uses the following accounts:

Cash Accts. Pay.—Ronken Supplies Miscellaneous Expense

Accts. Rec.—Hetland Company Dennis Gilbert, Capital Rent Expense

Supplies Dennis Gilbert, Drawing Utilities Expense

Prepaid Insurance Sales

Transactions:

Feb. 1. Received cash from owner as an investment, $10,000.00. R1.

4. Paid cash for supplies, $1,000.00. C1.

Instructions:

Journalize the transactions completed during February of the current year. Use page 1 of the journal

given in the Working Papers. Source documents are abbreviated as follows: check, C; memorandum, M;

receipt, R; sales invoice, S; calculator tape, T.

Save your work to complete Application Problem 4-2.

APPLICATION PROBLEM

Journalizing buying insurance, buying on account, and paying on account

into a general journal

Use the chart of accounts and general journal from Application Problem 4-1.

Transactions:

Feb. 6. Paid cash for insurance, $1,200.00 C2.

7. Bought supplies on account from Ronken Supplies, $1,400.00. M1.

8. Paid cash on account to Ronken Supplies, $700.00. C3.

12. Paid cash on account to Ronken Supplies, $700.00. C4.

Instructions:

Journalize the transactions. Source documents use the same abbreviations as stated in Application

Problem 4-1. Save your work to complete Application Problem 4-3.

APPLICATION PROBLEM

Journalizing transactions that affect owner’s equity into a general journal

Use the chart of accounts given in Application Problem 4-1 and general journal from Application Problem

4-2.

Transactions:

Feb. 12. Paid cash for rent, $600.00. C5.

13. Received cash from sales, $500.00. T13.

14. Sold services on account to Hetland Company, $450.00. S1.

15. Paid cash to owner for personal use, $1,800.00. C6.

18. Received cash from sales, $278.00. T18.

19. Paid cash for postage (Miscellaneous Expense), $64.00. C7.

21. Received cash an account from Hetland Company, $250.00. R2.

4-1

4-2

4-3

88 CHAPTER 4 Recording Transactions in a General Journal

Feb. 22. Received cash from sales, $342.00. T22.

22. Paid cash for heating fuel bill, $329.00. C8.

Instructions:

Journalize the transactions. Source documents use the same abbreviations as stated in Application

Problem 4-1.

Save your work to complete Application Problem 4-4.

APPLICATION PROBLEM

Journalizing transactions and starting a new page of a general journal

Use the chart of accounts given in Application Problem 4-1 and the general journal from Application

Problem 4-3.

Transactions:

Feb. 25. Received cash on account from Hetland Company, $200.00. R3.

25. Paid cash for a delivery (Miscellaneous Expense), $18.00. C9.

26 Sold services on account to Hetland Company, $136.00. S2.

26. Paid cash for supplies, $44.00. C10.

27. Paid cash for rent, $600.00. C11.

27. Paid cash for postage (Miscellaneous Expense), $10.00. C12.

28. Received cash from sales, $1,365.00. T28.

28. Paid cash to owner for personal use, $1,000.00. C13.

Instructions:

1. Journalize the transactions for February 25. Source documents use the same abbreviations as stated in

Application Problem 4-1.

2. Use page 2 of the journal to journalize the rest of the transactions for February.

APPLICATION PROBLEM

Journalizing transactions

Nick Bonnocotti owns a service business called The Lawn Doctor, which uses the following accounts:

Cash Nick Bonnocotti, Capital

Accts. Rec.—Leon Quarve Nick Bonnocotti, Drawing

Supplies Sales

Prepaid Insurance Advertising Expense

Accts. Pay.—Western Supplies Utilities Expense

Transactions:

Apr. 1. Nick Bonnocotti invested $2,000.00 of his own money in the business. Receipt No. 1.

3. Used business cash to purchase supplies costing $37.00. Wrote Check No. 1.

4. Wrote Check No. 2 for insurance, $120.00.

5. Purchased supplies for $50.00 over the phone from Western Supplies, promising to send the

check next week. Memorandum No. 1.

11. Sent Check No. 3 to Western Supplies, $50.00.

12. Sent a check for the electricity bill, $65.00. Check No. 4.

15. Wrote a $850.00 check to Mr. Bonnocotti for personal use. Used Check No. 5.

4-4

4-5

CHAPTER 4 Recording Transactions in a General Journal 89

Apr. 16. Sold services for $259.00 to Leon Quarve, who agreed to pay for them within 10 days. Sales

Invoice No. 1.

17. Recorded cash sales of $1,668.00.

18. Paid $50.00 for advertising. Wrote Check No. 6.

25. Received $259.00 from Leon Quarve for the services we performed last week. Wrote Receipt

No. 2.

Instructions:

Journalize the transactions completed during April of the current year. Use page 1 of the journal given in

the Working Papers. Remember to enter source document numbers as necessary.

MASTERY PROBLEM

Journalizing transactions

Jill Statsholt owns a service business called Jill’s Car Wash, which uses the following accounts:

Cash Accts. Pay.—Long Supplies Miscellaneous Expense

Accts. Rec.—David’s Limos Jill Statsholt, Capital Rent Expense

Supplies Jill Statsholt, Drawing Repair Expense

Prepaid Insurance Sales Utilities Expense

Accts. Pay.—Akita Supplies Advertising Expense

Transactions:

June 1. Received cash from owner as an investment, $17,500.00. R1.

2. Paid cash for rent, $400.00. C1.

3. Paid cash for supplies, $1,200.00. C2.

4. Bought supplies on account from Akita Supplies, $2,000.00. M1.

5. Paid cash for insurance, $4,500.00. C3.

8. Paid cash on account to Akita Supplies, $1,500.00. C4.

8. Received cash from sales, $750.00. T8.

8. Sold services on account to David’s Limos, $200.00. S1.

9. Paid cash for electric bill, $75.00. C5.

10. Paid cash for miscellaneous expense, $7.00. C6.

10. Received cash from sales, $750.00. T10.

11. Paid cash for repairs, $100.00. C7.

11. Received cash from sales, $850.00. T11.

12. Received cash from sales, $700.00. T12.

15. Paid cash to owner for personal use, $350.00. C8.

15. Received cash from sales, $750.00. T15.

16. Paid cash for supplies, $1,500.00. C9.

17. Received cash on account from David’s Limos, $200.00. R2.

17. Bought supplies on account from Long Supplies, $750.00. M2.

17. Received cash from sales, $600.00. T17.

18. Received cash from sales, $800.00. T18.

19. Received cash from sales, $750.00. T19.

22. Bought supplies on account from Long Supplies, $80.00. M3.

22. Received cash from sales, $700.00. T22.

23. Paid cash for advertising, $130.00. C10.

23. Sold services on account to David’s Limos, $650.00. S2.

4-6

90 CHAPTER 4 Recording Transactions in a General Journal

June 24. Paid cash for telephone bill, $60.00. C11.

24. Received cash from sales, $600.00. T24.

25. Received cash from sales, $550.00. T25.

26. Paid cash for supplies, $70.00. C12.

26. Received cash from sales, $600.00. T26.

29. Received cash on account from David’s Limos, $650.00. R3.

30. Paid cash to owner for personal use, $375.00. C13.

30. Received cash from sales, $800.00. T30.

Instructions:

1. The journals for Jill’s Car Wash are given in the Working Papers. Use page 1 of the journal to

journalize the transactions for June 1 through June 16. Source documents are abbreviated as follows:

check, C; memorandum, M; receipt, R; sales invoice, S; calculator tape, T.

2. Use page 2 of the journal to journalize the transactions for the remainder of June.

CHALLENGE PROBLEM

Journalizing transactions using a variation of the general journal

Tony Wirth owns a service business called Wirth’s Tailors, which uses the following accounts:

Cash Accts. Pay.—Marker Supplies Rent Expense

Accts. Rec.—Amy’s Uniforms Tony Wirth, Capital Utilities Expense

Supplies Tony Wirth, Drawing

Prepaid Insurance Sales

Transactions:

June 1. Received cash from owner as an investment, $17,000.00. R1.

2. Paid cash for insurance, $3,000.00. C1.

3. Bought supplies on account from Marker Supplies, $2,500.00. M1.

4. Paid cash for supplies, $1,400.00. C2.

8. Paid cash on account to Marker Supplies, $1,300.00. C3.

9. Paid cash for rent, $800.00. C4.

12. Received cash from sales, $550.00. T12.

15. Sold services on account to Amy’s Uniforms, $300.00. S1.

16. Paid cash for telephone bill, $70.00. C5.

22. Received cash on account from Amy’s Uniforms, $300.00. R2.

25. Paid cash to owner for personal use, $900.00. C6.

Instructions:

The journal for Wirth’s Tailors is given in the Working Papers. Wirth’s Tailors uses a journal that is slightly

different from the journal used in this chapter. Use page 1 of the journal to journalize the transactions.

Source documents are abbreviated as follows: check, C; memorandum, M; receipt, R; sales invoice, S;

calculator tape, T.

4-7

CHAPTER 4 Recording Transactions in a General Journal 91

During the summer, Willard Kelly does odd jobs to earn money. Mr. Kelly keeps

all his money in a single checking account. He writes checks to pay for personal

items and for business expenses. These payments include personal clothing,

school supplies, gasoline for his car, and recreation. Mr. Kelly uses his check stubs as his

accounting records. Are Mr. Kelly’s accounting procedures and records correct? Explain

your answer.

INTERNET ACTIVITY

Applied Communication

Careful research about careers will help prepare you

for making career choices. There are several U.S.

government publications that provide detailed

descriptions of many job titles. Two that are available

in most public libraries are the Dictionary of

Occupational Titles (DOT) and the Occupational Outlook

Handbook.

Instructions: Go to the library and, using one of the

two publications listed or any other appropriate

resource, find the description for any accounting-

related job. Record information you find, such as qual-

ifications needed, job outlook, and earnings. Write one

paragraph describing the pros and cons of working in

such a job. Be sure to write a topic sentence and a

conclusion.

Point your browser to

http://accounting.swpco.com

Choose First-Year Course, choose

Activities, and complete the activity

for Chapter 4.

General Journal

A journal with two amount

columns in which all kinds of

entries can be recorded is

called a general journal.

General journal entries are

entered in the automated

accounting system through the

General Journal tab. In a later

chapter, special journals will be

discussed to instruct you on how

to use the other journals on the

Journal Entries screen for spe-

cific types of transactions. The

other tabs on the Journal Entries

screen are used for entering

purchases, cash payments, cash

receipts, and sales.

In an automated accounting

system, the transactions that are

entered and posted in the gen-

eral journal update ledger

account balances immediately.

For verification purposes, a

general ledger report can be

displayed or printed to prove

account balances.

Recording Transactions

in the General Journal

Screen

Entering general journal

entries can be done in five

steps.

1. Enter the date of the

transaction, then press the

Tab key.

2. Enter the source document

number in the Reference col-

umn, then press the Tab key.

3. Enter the account number to

be debited, then press the

Tab key. The account title

will be displayed at the bot-

tom of the general journal,

just above the command

buttons. (In Automated

Accounting 8.0, the account

title is displayed next to the

account number after

tabbing to the next column.

4. Enter the debit amount, then

press the Tab key twice. The

cursor will automaticaly

position itself in the Account

Number field on the next

line of the journal. Enter the

account number to be cred-

ited, press the Tab key twice,

then enter the credit amount.

A

UTOMATED

A

CCOUNTING

RECORDING TRANSACTIONS

92 CHAPTER 4 Recording Transactions in a General Journal

5. When the transaction is

complete, click the Post but-

ton. Posting will be

discussed in Chapter 5.

General Journal

Transaction Additions,

Changes, and Deletions

If you wish to add a part of

a transaction, select the journal

entry transaction to which you

want to add a debit or credit.

Click on the Insert button. When

the blank line appears, enter the

additional transaction debit or

credit and click the Post button.

When changing or deleting

general journal transactions,

you need to select any portion

of the desired transaction. Make

corrections to the entry, then

click the Post button. If you wish

to delete the transaction, click

the Delete button.

General Journal Report

In this section you will learn

how to generate journal reports

and specify which journal

entries are to appear in the jour-

nal report. The general journal

report will display or print the

general journal entries that were

posted for a specified period.

Reports are useful in detecting

errors and verifying that debits

and credits are equal.

A general journal report can

be generated in three steps:

1. Choose the Report Selection

menu item from the Reports

menu or click the Reports

toolbar button.

2. When the Report Selection

window appears, choose the

Journals option. To change

the run date, shown in the

upper right corner of the

screen, enter the desired

date or use the key to

increase and the key to

decrease the date. You may

also click on the calendar.

3. Select the General Journal

report, then click the OK

button. You can choose to

include all general journal

entries or to customize your

report.

AUTOMATING

APPLICATION PROBLEM

4-5: Journalizing trans-

actions

Instructions:

1. Load Automated Accounting

7.0 or higher software.

2. Select database F04-1 from

the appropriate directory/

folder.

3. Select File from the menu

bar and choose the Save As

menu command. Key the

path to the drive and direc-

tory that contains your data

files. Save the database with

a file name of XXX041

(where XXX are your

initials). (Automated

Accounting 8.0 allows long

file names. Your instructor

may direct you to use your

full name when saving your

files.)

4. Access Problem Instructions

through the Help menu.

Read the Problem

Instructions screen. (In

Automated Accounting 8.0,

Problem Instructions are

accessed by clicking the

Browser toolbar button.)

5. Key the transactions listed

on pages 90–91.

6. Exit the Automated

Accounting software.

AUTOMATING MASTERY

PROBLEM 4-6:

Journalizing

transactions and

proving and ruling a

journal

Instructions:

1. Load Automated Accounting

7.0 or higher software.

2. Select database F04-2 from

the appropriate directory/

folder.

3. Select File from the menu

bar and choose the Save As

menu command. Key the

path to the drive and direc-

tory that contains your data

files. Save the database with

a file name of XXX042

(where XXX are your

initials). (Automated

Accounting 8.0 allows long

file names. Your instructor

may direct you to use your

full name when saving your

files.)

4. Access Problem Instructions

through the Help menu.

Read the Problem

Instructions screen. (In

Automated Accounting 8.0,

Problem Instructions are

accessed by clicking the

Browser toolbar button.)

5. Key the transactions listed

on pages 91–92.

6. Exit the Automated

Accounting software.

A

UTOMATED

A

CCOUNTING

CHAPTER 4 Recording Transactions in a General Journal 93