Gust Guide To Incorporation

gust-guide-to-incorporation

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 28

Gust’s Guide to

Startup Incorporation

Contents

01 04

05

06

07

02

03

Introduction

What Is a Company &

Why Do I Even Need One?

Types of companies

Reason 1: Limited liability

Reason 2: Collecting and owning assets & IP

Reason 3: Dividing and distributing ownership

When it’s time to form a company

LLCs & Common

Corporation Types

LLCs

C-Corporations

Benefit Corporations and Certified B-Corporations

S-Corporations

Which Type Should a High-

Growth Startup Choose?

The startup founder perspective

QSBS

The investor perspective

Why Delaware?

How Incorporation Works

How Company Formation Works

Corporate bylaws

Moving from incorporation to ownership

Issuing stock

Foreign Qualification

4

15

17

18

19

22

24

25

10

11

12

13

5

6

7

8

Gust’s Guide to Startup Incorporation / 2

Gust’s Guide to Startup Incorporation / 3

1. Introduction

Welcome to Gust’s Guide to Startup Incorporation! If you’d like the easy way

through this process, close this pdf and direct your browser to gust.com/

launch, where you can apply to join our Company-as-a-Service™ platform,

Gust Launch, and take care of your incorporation the right way in just a few

minutes. For a thorough account of the possibilities and potential concerns

your startup will face as it chooses a path through the incorporation process,

read on.

Incorporation is a term that refers to starting a company. When it’s time

to engage in business activities, it can be tough to assess which sort of

company provides the most benefits to a potential business, and to find out

specifically what these costs are ahead of time.

This book was written specifically for people who plan to build high-growth

startups1, such as the Airbnbs, Ubers, and Facebooks of the world. It is the

product of research by Gust’s legal and product experts, and sets out to

answer the following questions, which anyone starting their first (or second,

or tenth) business will have about the process:

1 Not sure if you’re starting a high-growth startup? It’s likely that your company is a high-growth startup if you are expecting to do any or all of these things: hire employees,

issue equity, seek professional investment, grow rapidly, and exit via either an initial public oering (IPO) or acquisition by a larger company.

To answer these and other questions, we’ll present everything you need to

know and explain how each piece of information relates to your situation: a

founder looking to create a company that is optimized for stability, growth,

and investment.

What is a company and why should I create one?

What type of incorporation is right for my company?

How do I go about incorporating my company?

1.

2.

3.

Gust’s Guide to Startup Incorporation / 4

2. What Is a Company? Why Do You Need One?

In the simplest terms, a company is a legal designation that you can

create by telling your various governments (state, local, and federal) about

your intention to do business under that name. Within the category of

“companies,” there are several kinds of entity, which can be understood

as a handful of categories (with more specific types inside each category).

Some of the most common categories are:

2 This paragraph specifically concerns General Partnerships. In a Limited Liability Partnership, all limited partners will be protected by the same limited liability functions as

partners in an LLC, while any general partners will be treated as members of a General Partnership, i.e. they will not receive protections.

The first two are simply ways for a person or a group of people to announce

that they will be doing business under a name other than their legal name.

For example, a slushy salesman named John might do business as the sole

proprietor of John’s Slushies. If he had a partner, Maureen, they might do

business as The John & Maureen Slushy Partnership. In either case, John

(and/or Maureen) have no protection as actors in situations involving the

company: they are the company and are personally responsible for any

debts or obligations they enter into as the company. 2

Because companies often work on scales much larger than individual

people do, the law permits the creation of companies which exist separately

from the people who own and/or run the company from a legal standpoint.

The rest of the types of companies above have this trait, which enables the

law to consider them separately from their owners, employees, or operators

in some or all of the following ways. Each of these eects can separately be

a compelling reason to create a company.

1. Sole Proprietorship

3. Limited Liability Company

(LLC)

2. Partnership

• C-Corporation

• B-Corporation

• S-Corporation

• General Partnership

• Limited Liability

Partnership

4. Corporation

Gust’s Guide to Startup Incorporation / 5

Limited liability

LLPs, LLCs, and corporations are meaningfully

distinct entities from the people who own them,

but can mostly do the same things (like enter into

contracts or buy and sell products). But while a

person who is doing business activities as herself

is personally liable for them (and their eects),

members of a corporation are not personally

liable for the activities and agreements made by

the corporation. This is called “limited liability”

and it is one of the most compelling reasons to

form a company.

So, if a court judges against your startup for

some reason in a suit, or if you find yourself

unable to fulfill contracts—whether they’re

with employees, contractors, suppliers, or

customers—the courts or the other party in the

contract won’t come after you and your personal

assets. Instead, the corporation is responsible

for bearing any penalty.

REASON #1

Gust’s Guide to Startup Incorporation / 6

Collecting and owning assets & IP

Like liability, many of the benefits of incorporation are tied to the company’s

status as an independent entity. This entity can own assets like capital,

equipment, and intellectual property (IP). All of these assets increase your

company’s value, especially from the perspective of future investors and

existing shareholders.

The last kind, intellectual property, is especially crucial for high-growth

startups, which tend to focus on developing disruptive new technologies or

techniques (rather than reusing established business models, as many other

small businesses do).

Just like with debt, you want ownership of these intellectual property assets

to be the property of the startup, not the individual founders. In this arrange-

ment, each founder’s contributions will remain with the company even if

they leave, which has two big benefits: first, it means that nobody can hold

the company’s future hostage purely on the basis of their past contributions,

and second, it provides a sensible justification for each contributor’s equity

stake. There’s also a financial benefit, which is that the value created by the

intellectual property can be considered part of the value of the company,

which is the main mechanism investors use to decide how much money to

put into a startup.

If you do not protect your IP early then you’ll introduce downstream risks on

future financings and/or in the market through competition. Keeping that IP

within the walls of an incorporated entity reduces risks if done properly, and

they can benefit from corporate laws that have already been built around

scenarios like this.

REASON #2:

Gust’s Guide to Startup Incorporation / 7

The assets and revenue created and owned by a

company as well as any investment it takes in all

contribute to the company’s overall value. This

value manifests itself in a few forms—corpora-

tions may distribute some profits to sharehold-

ers as dividends; the assets may help justify a

valuation in the minds of investors; capital con-

tributed by investors might be added on top of

a valuation as a representation of the company’s

overall worth.

In all of these ways, the relevant parties

understand the value as being divided up

according to shares. A business entity, unlike a

person doing business without forming a new

legal entity, can have multiple owners, whose

ownership (also known as equity) is divided

into an arbitrary number of pieces. This concept

is legally complicated, because equity can be

distributed in many forms depending on the

company’s type, structure, and bylaws, but in

all cases the point of the division is to explain

who owns the company and how much of the

company each shareholder owns.

Investors usually put money into companies in

exchange for some amount of equity. Employees

often receive equity as an incentive to work hard

on behalf of the company. Company founders

retain large portions of equity in exchange for

their hard (and usually free) work before the

company had any real value. The existence of

a legal entity that can have many owners makes

it possible to articulate all these relationships

and make sense of how they deliver value to

each party.

Dividing and distributing ownership

REASON #3

A partner A customer

An investor

An employee A grant

A need for a bank account

Any intellectual property

(including trademarks or

computer code)

Any potential liability

Any assets

Gust’s Guide to Startup Incorporation / 8

When it’s time to form a company

Incorporation can be both expensive and confusing, which is why many founders delay the process. So

when exactly should you incorporate your startup? The short answer is: as early as possible.

Specifically, you’ll want to be incorporated as soon as (or before) you have any of the following:

For reasons that vary case-by-case, every event on this list separately amounts to a need for an entity

separate from yourself that can be held liable in case of debt or penalty, can own an asset, or can

distribute shares of itself to investors.

3. LLCs and Common Corporations

Gust’s Guide to Startup Incorporation / 9

As we mentioned in the previous chapter, companies come in many types.

For high-growth startups in the United States, there is really only one ideal

choice (a Delaware C-Corporation3), but there are technically many options.

3 It’s important to note that most types of companies are registered with state governments, not the federal government, so there may be slight dierences in the ways these

entities behave on a state-by-state basis. We’ll discuss this a little in chapter 4, under the heading “Why Delaware?”

The four most popular of these are an LLC or three slightly dierent types of

corporation: C-Corporation, B-Corporation, and S-Corporation.

Gust’s Guide to Startup Incorporation / 10

Limited liability companies

LLCs are extremely simple

arrangements in which every

owner is a partner. An LLC

basically provides the limited

liability protection for which

people form companies, but does not do much

else. Each company which chooses to incorpo-

rate as an LLC drafts an “operating agreement”

among the owners, which contains all the rules

by which the company operates. This operating

agreement is similar in function to the bylaws of

a corporation, but due to the bespoke nature

of each LLC’s structure, there are no standard

components for this document (although there

are common features).

LLCs are also not independently subject to

corporate tax: an LLC is eectively invisible (for

tax purposes), and “passes through” any net

income (without being taxed at the LLC level) to

its owners, who then treat it as taxable personal

income. Whether or not any money actually

passes from the LLC to the individual, the

individual owner must pay income tax on their

share of the profits (or losses) generated by the

LLC. Every year at tax time, every LLC must send

every one of its members (and the IRS) a Form

K-1, showing that member’s personal share of

the company’s profit or loss.

The features which tend to make LLCs popular—

namely, their pass-through taxation structure

and their liability limitation without the need for a

full corporate structure—make them well-suited

for people who simply want a business entity

through which to do business. For high-growth

startups, they are generally not well-suited, for

reasons we will address in subsequent sections.

LLCS

Gust’s Guide to Startup Incorporation / 11

C-Corporations

C-Corporations are the most popular type of American cor-

poration. They are dierent from LLCs in a few ways. The

first is that, rather than an operating agreement, corporations

abide by bylaws written into their articles of incorporation, for

which there are many regularized and standard structures.

Due in large part to their popularity, C-Corporations enjoy the benefit of

having both state and national courts which are familiar with their features

and behaviors, so the operating a corporation as it scales is somewhat

easier and less lawyer-intensive than other types of companies.

The second key dierence between a C-Corporation and an LLC is the way

in which it is taxed. C-Corporations are subject to a separate set of taxes

than their owners or operators are. A C-Corporation pays annual corporate

taxes based on its taxable net income, and then if it distributes any money to

its shareholders (known as “distributions”), the shareholders themselves are

required to pay personal income taxes on the amount they receive.

The third defining feature of a C-Corporation is that it comes with an out-of-

the-box mechanism for distributing equity. This is called stock. At incorpora-

tion, corporations authorize a certain number of shares of themselves (which

can be increased at any time) and can subsequently issue these shares to

their owners (such as founders and investors). Because this instrument is

well-understood, this is easy to accomplish without involving lawyers.

C-Corporations are by far the best-suited corporate entity for high-

growth startups. We’ll specifically address the reasons why this is so in

subsequent chapters.

B CORPS

Gust’s Guide to Startup Incorporation / 12

Most corporations are generally assumed to have the

primary goal of maximizing their value for shareholders. In

the past few decades, many companies (especially startups)

have shown interest in expanding their range of aims to

include various kinds of altruistic and socially positive

goals—traditionally solely the concern of nonprofit organizations—to which

the law refers generally as “public benefit.”

Corporations who seek to include some public benefit in their purpose

have a legal entity option called a Benefit Corporation (sometimes confused

with a B-Corporation). This entity is not available to companies in all states,

and generally diers primarily in ways that are related to its public benefit

goals, such as accountability to shareholders and transparency—for most

other structural and tax-related concerns, it is similar or identical to a

C-Corporation.

These companies can also (optionally) choose to become Certified B Corpo-

rations, which is a third-party certification oered by the group responsible

for the creation of the Benefit Corporation legal entity and is not a type of

corporate legal structure in its own right.

Benefit Corporations and Certified B-Corporations

Gust’s Guide to Startup Incorporation / 13

Some C-Corporations can optionally file Form 2553 with the

IRS, which changes the C-Corporation into a “Small Business

Corporation,” popularly known as an S-Corporation. S-Cor-

porations are essentially just an election for pass-through

taxation status, and are perhaps best considered a subcat-

egory of C-Corporation designed to compromise between the corporate

rigidity and standardization of a C-Corporation and the tax-invisible nature

of an LLC.

The rules that determine which businesses can elect to be treated as S-Cor-

porations are somewhat restrictive and a little confusing, but in practice end

up working for most high-growth startups. To be eligible, a company can’t

operate within certain industries, and must have fewer than 100 sharehold-

ers (although a married couple or an estate can count as a single sharehold-

er), all of whom are individuals (or “certain trusts” and estates) rather than

corporations or partnerships, and all of whom are residents of the United

States. In addition, an S-Corporation can only have one class of stock.

S-Corporations

CCORP BCORP LLC SOLE PROP. GEN.

PRTNRSHP

LTD.

PRTNRSHP

Oers liability protection ✓✓✓

Can own assets & IP ✓✓✓

Can grant stock ✓ ✓

Owners can split profits/losses w/

business ✓ ✓

Owners can report profits/losses on

personal tax returns ✓✓✓✓✓

Created by state-level registration ✓✓✓

Ease of raising funds Easy Moderate Moderate Dicult Dicult Moderate

Ongoing record keeping reqs. Extensive Extensive Moderate Few Few Few

May have an unlimited number of

owners ✓ ✓ ✓ ✓

Gust’s Guide to Startup Incorporation / 14

Business structure comparison

Gust’s Guide to Startup Incorporation / 15

Now that we’ve looked at the myriad types of

companies available to an entrepreneur seeking

to become the founder of a high-growth startup,

we can compare them to each other on the

basis of their benefits and drawbacks. There are

two main categories of stakeholder a startup

founder should consider: themselves (and their

cofounders) and the investment community.

There’s a right answer—spoilers: it’s a Delaware

C-Corporation—but to understand exactly why,

we’ll walk through all the potential ramifications

of each choice.

The startup founder’s perspective

As Daniel DeWolf at Mintz Levin puts it, “Incorpo-

rating as a C-Corporation in Delaware is the gold

standard for high growth startups. It provides

limited liability, ease of use, ease of setup, the

ability to issue stock options, and tax benefits

upon sale for many qualified small businesses.”

The two key dierences between an LLC and a

C-Corporation are the ability to divide ownership

and the way in which their income is taxed.

While it’s possible to develop workarounds for

an LLC to divide its ownership structure, notably

profits interest (which signals an intent to divide

profits at a later date, counting from when the

interest was granted) and capital interest (which

represent portions of the value of the company

if it were to be liquidated), these don’t exactly

translate to stock or ownership in the obvious,

comparatively intuitive ways that shares of a

C-Corp do.

4. Which Type of Company Should

a High-Growth Startup Choose?

Gust’s Guide to Startup Incorporation / 16

On top of these dierences, LLCs entirely lack a way to grant options, which

are a common equity incentive format that startups give to employees and

advisors that more or less represent the ability to purchase shares of the

company at a discount when it’s advantageous to do so. Since almost any

successful high-growth startup will seek professional investment, these

structures will need to be converted into analogous C-Corp ownership units

(i.e. shares). In short, that’s a lot of expensive lawyer time.

Despite the comparative diculty an LLC introduces as a result of its inability

to directly issue stock, many startup founders are still hesitant to choose a

C-Corp structure. The number-one reason is because they’ve heard about

the “tax advantages” of LLCs: many first-time founders hear that a C-Cor-

poration’s profits are “taxed twice,” compared to an LLC’s profits, which are

only taxed once, and should therefore be avoided.

This belief is based on a misunderstanding of the pass-through taxation

structure. Since few high-growth startups turn profits in their first few years,

there is eectively nothing to “double-tax.” Startups tend to reinvest any

revenue they generate in growth, and no profits to tax means no tax on

profits. No profits also means no dividends paid to shareholders, so there

will be no personal tax on those nonexistent profits either. In other words,

“double taxation” in a high-growth startup usually amounts to 2 x $0 = $0, or

double taxation on nothing.

However, LLCs operating at a loss do oer their owners the ability to pass

through some of that loss directly to their personal tax returns, thus reducing

their net taxable income. This is genuinely attractive to many startup entre-

preneurs, who are likely to be bootstrapping their businesses and forgoing

a salary, and are therefore very grateful to reduce their tax burden.

Startup founders who are interested in taking advantage of pass-through

taxation while still choosing the standard and well-suited C-Corporation

structure for their startup can choose to elect S-Corporation status. There

are two distinct disadvantages to this approach, one of which can be

handled easily and one of which cannot be mitigated at all.

The first disadvantage is that S-Corporations are eectively investor-proof.

S-corporations, as noted above, are limited to one class of stock and 100

individual shareholders (who cannot be businesses or partnerships). Still,

an S-Corp is perfect for an initially founder-funded startup, and then when

the startup’s first investors arrive, the company can simply drop its S-Corpo-

ration election and turn into an investor-friendly C-Corp with the ability to

issue the Preferred stock that they will insist on purchasing.

The second disadvantage is that an S-Corporation (as well as an LLC or any

other non-C-Corporation entity type) is not eligible to take advantage of the

Qualified Small Business Stock tax write-o, which can amount to millions

and millions of dollars in savings.

Gust’s Guide to Startup Incorporation / 17

QUALIFIED SMALL BUSINESS STOCK QSBS:

Under certain circumstances, stock issued by C-Corporations counts as Qualified Small Business Stock

(QSBS). After five years of ownership, the gains made on the value of this stock can be written o the

personal taxes of the stockholder up to $10,000,000 or 10x the stockholder’s adjusted basis in the

stock, whichever is greater. In other words, the $10M in non-taxable gains is the minimum, provided you

have $10M in gains in the first place.

The requirements for equity to qualify for the QSBS exemption are relatively straightforward: stock

issued by an active, domestic, C-Corporation that has less than $50,000,000 in assets right after

issuing the stock. Virtually all newly-incorporated, high-growth, US C-Corp startups would meet

these requirements.

For both startup founders, who are expecting (or hoping for) a massively successful exit, as well as

investors in such a startup, this $10M+ in tax exemptions should be an extremely compelling reason to

choose C-Corporation status. After all, is the possibility of saving a small amount in taxes deducted from

your personal income this year worth potentially paying taxes on up to ten million dollars in personal

gains when you make it big?

A key consideration for everyone

Gust’s Guide to Startup Incorporation / 18

The investor’s perspective

Like founders, investors’ primary cause of

aversion to LLCs is the diculty created by their

non-standard equity mechanisms. Remember

that since LLCs are technically always partner-

ships, any equity-like features need to be cus-

tom-written into the operating agreement each

time they are issued in order to approximate the

equity functions of corporations.

Sophisticated professional investors often have

portfolios with dozens—or even hundreds—of

companies. If an LLC is among them, investors

are required to deal with these ad-hoc equity

agreements on an individual basis. Even though

these may look and behave similarly to stock

in a C-Corporation, the reality is that each one

must be treated separately because there are

no standards. Compare this to the known and

understood mechanisms of C-Corporation

shares, and it’s easy to understand why investors

prefer the known commodity: it’s less work for

the investors and their lawyers, making these

types of investments significantly more ecient.

It’s also important to note that the eciency

isn’t just a one-time benefit at the moment of

investment. It remains a concern for the duration

of the relationship as it impacts everything from

additional equity issuances to investor protective

provisions. The crux of this issue is the LLC’s

mandatory IRS form filing, known as a K-1.

Recall that the LLC is invisible for tax purposes.

In tax season, the partners (i.e. all equity-hold-

ers, including each of the investors) have to

file a document with the IRS that explains the

attributed income they received (whether or not

they actually received any of it in cash) from the

partnership. These forms are called K-1s, and

they are not popular with investors.

If an investor held a stake in an LLC (i.e. was a

partner) in any given year, the IRS requires that

the file a K-1 in order to complete their taxes, so

the investor’s tax filing can easily be blocked by

a single company’s tardiness in distributing the

forms. In other words, a startup founder can ac-

cidentally expose their investors to tax penalties

for late filing, which is unlikely to have a positive

eect on what should be a mutually beneficial,

satisfying relationship.

Between the sheer annoyance of K-1s, the

legal and accounting diculties created by

LLCs’ ad-hoc approaches to equity, S-Corpora-

tions’ inability to issue preferred stock or take

investment from business or partnerships, and

the $10M+ in potential tax exemptions available

only to C-Corporations, professional startup

investors almost exclusively choose to invest in

C-Corporations..

Delaware’s filing oces and court

systems are prompt and oer good

customer service.

The state has predictable, well-

developed corporate laws that

experienced businesspeople and

lawyers worldwide understand.

The laws are the most business-

friendly and protective of a company

and its management and board of

directors.

As it grows with more board

members and investors, a Delaware

corporation oers flexibility for Board

actions and shareholder rights.

Benefits of incorporating in Delaware:

Gust’s Guide to Startup Incorporation / 19

Why Delaware?

Corporations (and most types of companies) are chartered by state governments rather than the federal

government. Because Delaware is a small state, it developed a series of tax and regulatory laws (notably

the Delaware General Corporation Law) and court systems that are more advantageous to the corpora-

tion than almost anywhere else in the country, leading it to be the most favorable place to incorporate

for both companies and investors. It’s a revenue win for them; a tax and regulatory win for companies.

The net result is that most investors will prefer to invest in startups incorporated in Delaware, since its

laws and regulations are both familiar and preferable to professional investment groups and startup

lawyers. In some circumstances, there are compelling reasons to incorporate elsewhere, but most

startups stick with Delaware as “The First State” and file a foreign qualification form to operate in their

own home state.

Gust’s Guide to Startup Incorporation /20

5. How Incorporation Works

Incorporation refers to a charter granted by a governmental jurisdiction, in

this case the State of Delaware, for a group of people to do business as a

legal entity rather than as individuals. This involves filing a Certificate of In-

corporation, which means picking a name, signing a document, and sending

it to the oce of Delaware’s Secretary of State.

To actually draft and file the Certificate, a founder will need to engage a

lawyer or legal filing service. Gust Launch’s incorporation process is the

latter—it is a quick and easy software experience that fills out and files the

Certificate of Incorporation, using a set of documents which have been

custom-tailored for use by high-growth startup companies by experienced

startup lawyers.

As part of the incorporation process, companies authorize themselves to

issue shares of stock. Most high-growth startup companies, including all

those who use Gust Launch, authorize themselves to issue 10,000,000

shares, each at a par value of at least $0.00001.

Setting a company up with millions of shares lets the company give relatively

small grants to advisors and employees. To understand why millions of

shares are necessary, it’s important to mention that most shareholder grants

4 To learn more about vesting, read “How Vesting Protects Companies and Founders” on the Gust Launch Blog.

use vesting, which (in extremely simplified language) makes the shares

available incrementally over time4. Startup grants often vest over 48 months,

meaning that 1/48 of the shares vest every month. If a startup has 10,000,000

authorized shares and grants 0.1% to a new advisor, the grantee would have

10,000 shares, which is easily and meaningfully divisible by 48 (to ~208

shares per month). By contrast, if you authorized only 5,000 shares, an 0.1%

grant would be 5 shares. This math doesn’t work nearly as well, because a

grantee cannot easily vest 5 shares over 48 months.

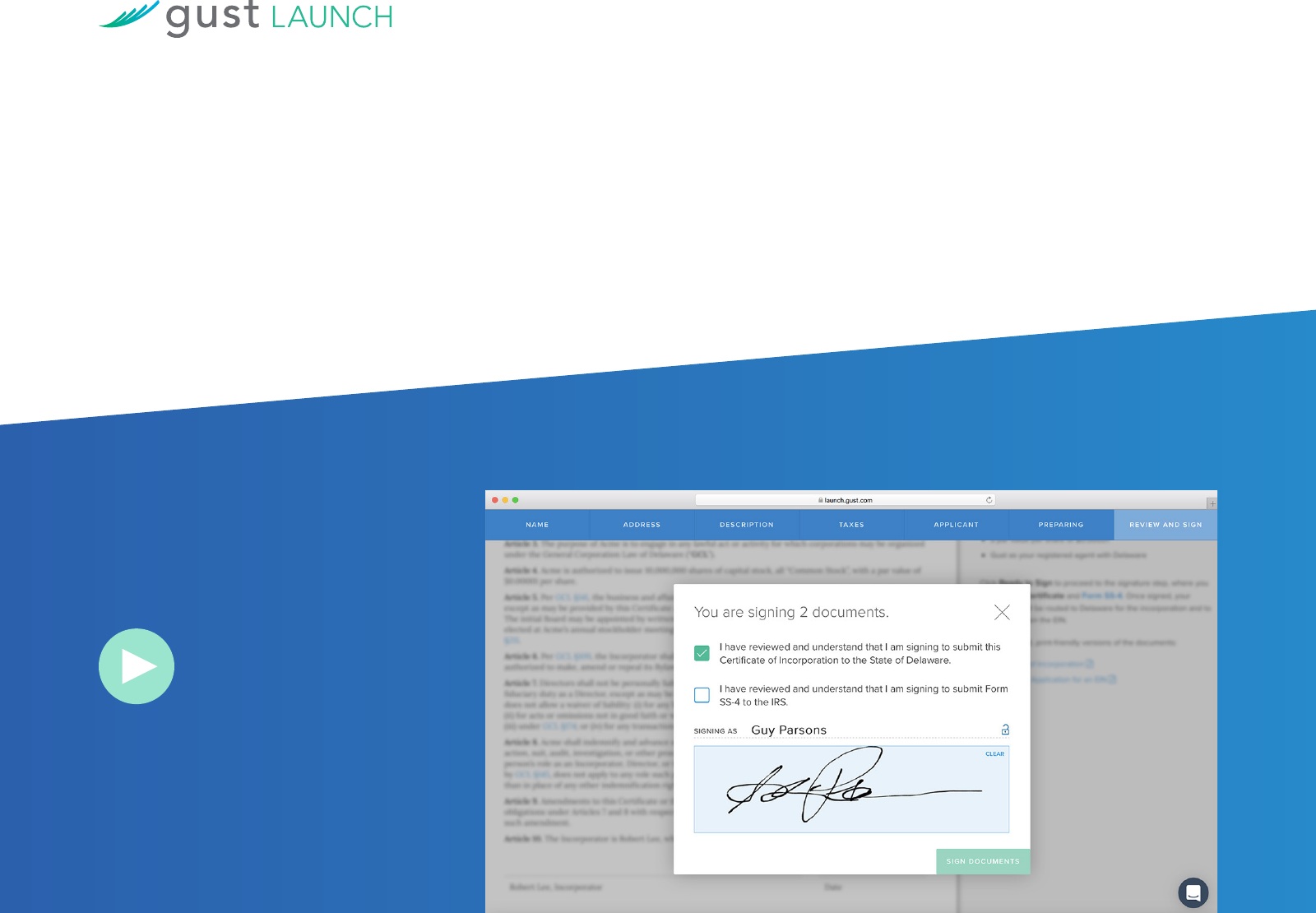

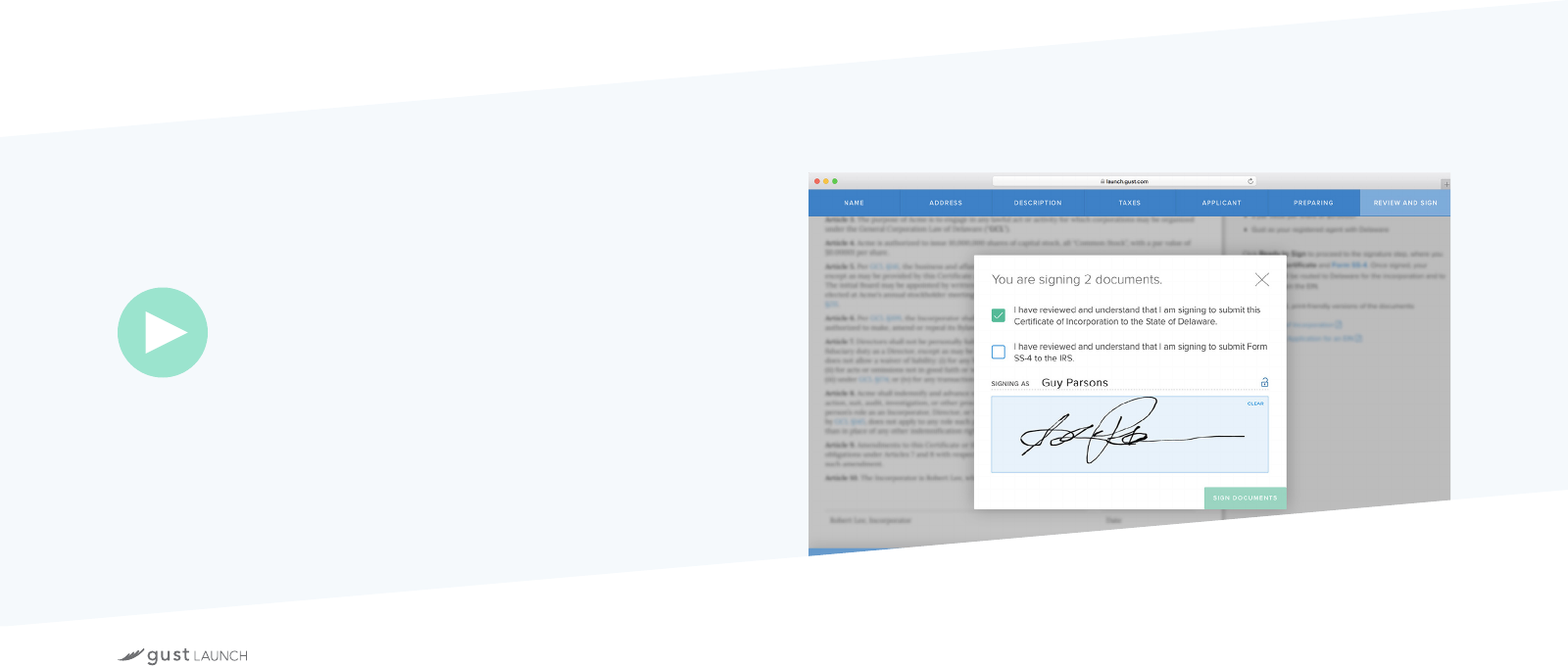

Watch a video demo of the Gust

Launch incorporation process

Gust’s Guide to Startup Incorporation / 21

The per-share price (or par value) of $0.00001 is possible because the startup has no assets, so the

taxes each grantee must pay on their stock grants can be kept extremely minimal by declaring an

overall value of the company at $100.

Gust Launch’s incorporation process also includes an SS-4, which is the application for an Employer

Identification Number (EIN). This IRS-assigned ID number is used when paying taxes and otherwise

identifying the company to the US government. It’s necessary for opening a company bank account, as

well as for paying employees when the company is ready to hire.

The Gust Launch incorporation process is quick and easy—to get started, visit gust.com/launch or

watch a video demo at http://gust.ly/incdemo.

Gust’s Guide to Startup Incorporation /22

6. How Company Formation Works

The term “company formation” refers to a series of decisions to make

and documents and actions to adopt reflecting those decisions that

ensure that the brand-new C-Corporation has the structure and traits that

investorsexpect.

Some online incorporation services either skip the formation step or simply

send the founder general-purpose documents that aren’t appropriately

customized for specific types of companies—for example, a family-run

retail store would have very dierent formation documents than a ven-

ture-funded startup. Often, a startup will bring in an experienced lawyer at

this point if they are using one of the more general-purpose online legal

filing services.

We’ll describe the Gust Launch approach, which takes the process step by

step, using online documents specifically intended for startups.

Establish corporate bylaws

STEP ONE:

Immediately after filing for incorporation, a

company needs to draft and adopt its bylaws.

These are operating rules to specify the orga-

nization, structure, and governance functions of

the corporation.

Gust’s Guide to Startup Incorporation / 23

There are a few other pieces to the bylaws.

Many will be dierent for startups than for other

kinds of companies. For example, startups can

save countless time and money by including

provisions in their bylaws to take advantage of

new Delaware laws that allow for paperless stock

records and online votes and notices. This is one

of many reasons to hire a startup lawyer or use

startup-oriented legal automation software, such

as Gust Launch, that use documents appropriate

to startups.

BASIC CATEGORIES OF BYLAWS

how the company’s stock ownership is tracked, including how the company records

ownership, rights to receive dividends from the stock, and other specifications.

Stock:

the organization’s top management, what they do for the organization, and how

they will be appointed. In the beginning, this might mean co-founders as well as

any advisors or investors the company has.

Ocers:

people who own shares of the company have meetings and vote to elect Board

members, among other things.

Stockholders:

this section specifies the number of people on the Board, what their powers are,

and the rules that apply to them.

Board of Directors:

the corporation accepts the responsibility to cover legal actions brought against

certain people who act on its behalf. In other words, if a founder or ocer is sued,

the corporation will pay the attorney fees and any damages assessed, rather than

leaving the founder on their own.

Indemnification:

Gust’s Guide to Startup Incorporation /24

Move from incorporation to ownership

There are several ways to go about the next formation steps. Gust’s process

is optimized for simplicity and speed of execution.

In the incorporation process, the person signing and filing the Certificate

with the state of Delaware is known as the “Incorporator,” and has certain

initial duties specified by the Certificate and by Delaware law. For conve-

nience, Gust asks the primary founder to sign as Incorporator, and in that

role to adopt the initial bylaws by signing an “Action of the Incorporator.” By

that document, the Incorporator also appoints the first Board members—in

this case, appointing themself to be the first member of the Board, and then

resigns as Incorporator (because the position has no further duties).

The new Board is empowered by the bylaws to appoint ocers of the

company. The next step is for the Board’s newly appointed initial member

to appoint the company’s first CEO (usually themselves), secretary, and

treasurer (the three “statutory” ocer positions required by Delaware

and the bylaws), as well as any other initial ocer positions they wish to

set up initially. The co-founding team are now the ocers and Board of the

company, but they do not yet actually own the company. In fact, nobody does.

That’s what shares of stock are for. The next step is to solve thisproblem.

STEP TWO:

Gust’s Guide to Startup Incorporation /25

Issue stock

Per Delaware law, the Board directs the issuance

of shares of company ownership. The Gust Launch

Certificate of Incorporation provides for 10,000,000

authorized shares of the new company, which just

means that the company can theoretically be divided

in up to 10,000,000 equal pieces. To create actual

ownership, stock will have to be “issued,” meaning that

the company pushes out shares from being merely

authorized to being actually outstanding, and then

“granted,” meaning that the shares are sold to one

or more people or business entities. The initial stock

grants will likely make up a significant but not complete portion of the 10,000,000 authorized shares,

split among the co-founding team and any other initial participants5.

Once the Board approves the initial stock grants, the CEO oversees and signs the issuance and grant

of stock to each recipient, who will need to sign a package of stock grant documents and purchase the

stock (at the nominal “par value” of $0.00001 per share specified in the Certificate of Incorporation) for

the grant to be complete. Most companies with multiple founders and team members opt to make stock

ownership subject to vesting. There is also a stockholder agreement to handle a myriad of terms that

apply to stock ownership, like transferability of shares. This is the point at which the co-founders would

file their 83(b) elections, which relate to taxation of future gains in value of vested stock.

5 For more background on how this all works, check out Gust’s guide to startup equity terms and principles.

STEP THREE:

Obtain a charter by filing its Certificate

with Delaware

Apply for and receive an EIN from the

IRS so that it can open a bank account,

hire employees, and pay taxes

Adopt bylaws containing the rules and

structure that investors expect, and set

out its operations and powers

Elect a Board of Directors

Appoint the founder and others to

be ocers

Issue and sell stock to founders, giving

them ownership of the company

Incorporation & company

formation, step by step:

1.

2.

3.

4.

5.

6.

Gust’s Guide to Startup Incorporation /26

7. Foreign Qualification

The last step of incorporating and setting up a company is only relevant to

companies which incorporate in states other than the state in which they

are physically located or active. In this case, a company will need to file

for foreign qualification, which means submitting a document to the state

in which they are actually based asking for permission to do business in

thatstate.

In other words, if a company is based in Delaware but has its headquarters

in Alabama, it will need to file a foreign qualification with Alabama in order

to operate. This will inform Alabama of the company’s existence, and gives

that state the power to regulate and tax the company.

The actual document that must be filed varies from state to state (as does

the fee which the company must pay to file it), but most states refer to this

document as a “Certificate of Authority.” The requirements of the applica-

tion may dier but usually include a mix of information about your business

(such as how many shares you’ve authorized) and sometimes a certification

from your state of incorporation called a “Certificate of Good Standing” that

attests that your business conforms to local laws.

The fee is generally a flat rate, and for the most part, this fee is not especially

substantial: it’s on the order of a few hundred dollars. However, in a few

states, the burden can vary greatly, especially for high-growth startups. For

example, in Virginia, the fee is calculated on the basis of the number of

authorized shares, which results in a fee of over $2,500 for startups with

10,000,000 shares. Nevada, on the other hand, calculates its fee according

to the value of the startup’s equity using a minimum par value of $0.001

per share, which ends up putting the fee for new startups with 10,000,000

shares at around $75.

Actually filing for foreign qualification is as simple as looking up the forms

for the state in which you wish to qualify, filling them out, and sending them

in. However, due to the variant nature of the fees (and forms), consulting

a lawyer about this process is often advised. A Gust Launch subscription

includes the process of foreign qualification and files the appropriate

documents on its startup’s behalf, leaving founders responsible only for the

fees charged by the state as well as a small filing fee charged by our filing

partner, which depends on the state in which you wish to qualify.

Gust’s Guide to Startup Incorporation / 27

Gust is the global SaaS platform for founding, operating, and investing in

scalable, high growth companies. Gust’s online tools support corporate legal

and financial formation and operation for entrepreneurs, as well as deal flow

and relationship management for investors, from startup through exit. As the

world’s largest community of entrepreneurs and early-stage investors from

191 countries, Gust pioneered the equity funding collaboration industry and

is the ocial platform of the world’s leading angel investor federations and

venture accelerators. More than 500,000 startups have already used Gust to

connect with over 70,000 investment professionals. Gust powers the ocial

online hubs of the world’s largest innovation ecosystems including New

York City (Digital.NYC), Boston (StartHub.org) and London (Tech.London).

For more information about Gust, please visit gust.com.

Credits

CONTRIBUTORS: EDITOR:

Alan McGee

Head of Product

Ryan Kutter, Esq.

Relationship Manager

Gil Silberman

Startup Lawyer

David S. Rose

Founder & CEO

Andrew Crimer

Marketing Manager

ABOUT GUST