Instructions For Form 7004 (Rev. December 2017) I7004

User Manual: i7004

Open the PDF directly: View PDF ![]() .

.

Page Count: 6

Userid: CPM Schema: instrx Leadpct: 100% Pt. size: 9 Draft Ok to Print

AH XSL/XML Fileid: … ns/I7004/201712/A/XML/Cycle05/source (Init. & Date) _______

Page 1 of 6 15:44 - 1-Feb-2018

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Instructions for Form 7004

(Rev. December 2017)

Application for Automatic Extension of Time To File Certain Business Income Tax,

Information, and Other Returns

Department of the Treasury

Internal Revenue Service

Section references are to the Internal Revenue Code unless

otherwise noted.

Future Developments

For the latest information about developments related to Form

7004 and its instructions, such as legislation enacted after they

were published, go to IRS.gov/Form7004.

What’s New

Form revisions. Form 7004 has been simplified and now

consists of two parts. Part I includes, in form number order, all

the forms for which Form 7004 is used to request an extension of

time to file. Filers requesting an extension will enter (in the box

located at the top of Part I) the form code for the return for which

the extension is requested. Part II includes questions for all filers.

Address changes for filing Form 7004. The address for filing

Form 7004 has changed for some entities located in Georgia,

Illinois, Kentucky, Michigan, Tennessee, and Wisconsin. See

Where To File, later.

General Instructions

Purpose of Form

Use Form 7004 to request an automatic extension of time to file

certain business income tax, information, and other returns. The

extension will be granted if you complete Form 7004 properly,

make a proper estimate of the tax (if applicable), file Form 7004

by the due date of the return to which the extension is requested,

and pay any tax that is due.

Note. Do not use Form 7004 to request an automatic extension

of time to file Form 1041-A. Instead, use Form 8868.

When To File

Generally, Form 7004 must be filed on or before the due date of

the applicable tax return. The due dates of the returns can be

found in the instructions for the applicable return.

Exceptions. See the instructions for Part II, line 2, for foreign

corporations with no office or place of business in the United

States. See the instructions for Part II, line 4, for foreign and

certain domestic corporations and for certain partnerships.

How and Where To File

Form 7004 can be filed electronically for most returns. However,

Form 7004 cannot be filed electronically for Forms 8612, 8613,

8725, 8831, 8876, or 706-GS(D). For details on electronic filing,

visit IRS.gov/efile7004.

If you do not file electronically, file Form 7004 with the Internal

Revenue Service Center at the applicable address for your

return as shown in Where To File, later in the instructions.

If you file Form 7004 on paper and file your tax return

electronically, your return may be processed before the

extension is granted. This may result in a penalty notice.

Signature. No signature is required on this form.

CAUTION

!

No Blanket Requests

File a separate Form 7004 for each return for which you are

requesting an extension of time to file. This extension will apply

only to the specific return identified on Part I, line 1. For

consolidated group returns, see the instructions for Part II, line 3.

Extension Period

The IRS will no longer send a notification that your extension has

been approved. We will notify you only if your request for an

extension is disallowed. Properly filing Form 7004 will

automatically give you the maximum extension allowed from the

due date of your return to file the return.

Maximum extension period. The automatic extension period

for time to file is generally 6 months. Exceptions apply for certain

filers of Form 1041 and for C corporations with tax years ending

June 30. An estate (other than a bankruptcy estate) and a trust

filing Form 1041 are eligible for an automatic 512-month

extension of time to file. C corporations with tax years ending

June 30 are eligible for an automatic 7-month extension of time

to file (6-month extension if filing Form 1120-POL). See the

instructions for Part II, lines 2 and 4, for exceptions for foreign

corporations, certain domestic corporations, and certain

partnerships with books and records outside of the United States

and Puerto Rico. See the instructions for the applicable return for

its due date.

Note. A corporation with a short tax year ending anytime in

June is treated as if the short tax year ended on June 30.

Termination of extension period. The IRS may terminate the

automatic extension at any time by mailing a notice of

termination to the entity or person that requested the extension.

The notice will be mailed at least 10 days before the termination

date given in the notice.

Rounding Off to Whole Dollars

The entity can round off cents to whole dollars on its return and

schedules. If the entity does round to whole dollars, it must

round all amounts. To round, drop amounts under 50 cents and

increase amounts from 50 to 99 cents to the next dollar (for

example, $1.39 becomes $1 and $2.50 becomes $3).

If two or more amounts must be added to figure the amount to

enter on a line, include cents when adding the amounts and

round off only the total.

Payment of Tax

Form 7004 does not extend the time to pay any tax due.

Generally, payment of any balance due on Part II, line 8, is

required by the due date of the return for which this extension is

filed. See the instructions for line 8.

No checks of $100 million or more accepted. The IRS

cannot accept a single check (including a cashier’s check) for

amounts of $100,000,000 ($100 million) or more. If you are

sending $100 million or more by check, you will need to spread

the payments over two or more checks with each check made

out for an amount less than $100 million. The $100 million or

CAUTION

!

Feb 01, 2018 Cat. No. 51607V

Page 2 of 6 Fileid: … ns/I7004/201712/A/XML/Cycle05/source 15:44 - 1-Feb-2018

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

more amount limit does not apply to other methods of payments

(such as electronic payments).

Penalty for late filing of return. Generally, a penalty is

charged if a return is filed after the due date (including

extensions) unless you can show reasonable cause for not filing

on time.

Penalty for late payment of tax. Generally, a penalty of 12 of

1% of any tax not paid by the due date is charged for each

month or part of a month that the tax remains unpaid. The

penalty cannot exceed 25% of the amount due. The penalty will

not be charged if you can show reasonable cause for not paying

on time.

If a corporation is granted an extension of time to file a

corporation income tax return, it will not be charged a late

payment penalty if the tax shown on Part II, line 6 (or the amount

of tax paid by the regular due date of the return), is at least 90%

of the tax shown on the total tax line of your return, and the

balance due shown on the return is paid by the extended due

date.

Interest. Interest is charged on any tax not paid by the regular

due date of the return from the due date until the tax is paid. It

will be charged even if you have been granted an extension or

have shown reasonable cause for not paying on time.

Forms 1065, 1065-B, and 1066. A penalty may be assessed

against the partnership or REMIC if it is required to file a return,

but fails to file it on time, including extensions, or files a return

that fails to show all the information required. The penalty can be

waived if the entity can show reasonable cause for not filing on

time. See the Instructions for Forms 1065, 1065-B, or 1066 for

more information.

Reasonable cause. If you receive a notice about a penalty

after you file your return, send the IRS an explanation and we will

determine if you meet reasonable-cause criteria. Do not attach

an explanation when you file your return.

Specific Instructions

Name and identifying number. If your name has changed

since you filed your tax return for the previous year, enter on

Form 7004 your name as you entered it on the previous year's

income tax return. If the name entered on Form 7004 does not

match the IRS database and/or the identifying number is

incorrect, you will not have a valid extension. Enter the

applicable employer identification number (EIN) or social

security number.

Address. Include the suite, room, or other unit number after the

street address. If the post office does not deliver mail to the

street address and the entity has a P.O. box, show the box

number instead of the street address.

If the entity's address is outside the United States or its

possessions or territories, enter in the space for “city, town,

state, and ZIP code,” the information in the following order: city,

province or state, and country. Follow the country's practice for

entering the postal code. Do not abbreviate the country name.

If your mailing address has changed since you filed your last

return, use Form 8822, Change of Address, or Form 8822-B,

Change of Address or Responsible Party—Business, to notify

the IRS of the change. A new address shown on Form 7004 will

not update your record.

Part I — Automatic Extension for

Certain Business Income Tax,

Information, and Other Returns

Line 1

Enter the appropriate form code in the boxes on line 1 to indicate

the type of return for which you are requesting an extension. See

Maximum extension period, earlier.

If an association is electing to file Form 1120-H, U.S. Income

Tax Return for Homeowners Association, it should file for an

extension on Form 7004 using the original form type assigned to

the entity. See the Instructions for Form 1120-H.

Note. The trustee of a trust required to file Form 1041-A must

use Form 8868, instead of Form 7004, to request an extension

of time to file.

Part II — All Filers Must Complete

This Part

Line 2

Check the box on line 2 if you are requesting an extension of

time to file for a foreign corporation that does not have an office

or place of business in the United States. The entity must file

Form 7004 by the due date of the return (the 15th day of the 6th

month following the close of the tax year) to request an

extension.

Line 3

Only the common parent or agent of a consolidated group can

request an extension of time to file the group's consolidated

return.

Attach a list of all members of the consolidated group

showing the name, address, and EIN for each member of the

group. If you file a paper return, you must provide this

information using the following format: 8.5 x 11, 20 lb. white

paper; 12 point font in Courier, Arial, or Times New Roman;

black ink; one-sided printing; and at least a one-half inch margin.

Information is to be presented in a two column format, with the

left column containing affiliates' names and addresses, and the

right column containing the TIN with one-half inch between the

columns. There should be two blank lines between listed

affiliates.

Generally, all members of a consolidated group must use the

same taxable year as the common parent corporation. If,

however, a particular member of a consolidated group is

required to file a separate income tax return for a short period

and seeks an extension of time to file the return, that member

must file a separate Form 7004 for that period. See Regulations

section 1.1502-76 for details.

Any member of either a controlled group of corporations

or an affiliated group of corporations not joining in a

consolidated return must file a separate Form 7004.

Note. Failure to list members of the affiliated group on an

attachment may result in the group's inability to elect to file a

consolidated return. However, see Regulations sections

301.9100-1 through 301.9100-3 for information about extensions

of time for making elections.

Line 4

Certain foreign and domestic corporations and certain

partnerships (as described below) are entitled to an automatic

extension of time to file and pay under Regulations section

CAUTION

!

-2-

Page 3 of 6 Fileid: … ns/I7004/201712/A/XML/Cycle05/source 15:44 - 1-Feb-2018

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

1.6081-5. These entities do not need to file Form 7004 to take

this automatic extension and must file (or request an additional

extension of time to file) and pay any balance due by the 15th

day of the 6th month following the close of the tax year.

This includes:

Partnerships that keep their books and records outside the

United States and Puerto Rico,

A foreign corporation that maintains an office or place of

business in the United States,

A domestic corporation that transacts its business and keeps

its books and records of account outside the United States and

Puerto Rico, or

A domestic corporation whose principal income is from

sources within the possessions of the United States.

Attach a statement to the entity’s tax return stating that the

entity qualifies for the extension to file and pay. If the entity is

unable to file its return on or before the 15th day of the 6th month

following the close of the tax year, check the box on line 4 of

Form 7004 to request an additional extension of time to file (not

an extension of time to pay). The additional extension period is 3

months for partnerships and S corporations and 4 months for C

corporations and filers of Form 1120-POL.

Line 5a

If you do not use a calendar year, complete the lines showing the

beginning and ending dates for the tax year.

Line 5b

Check the applicable box on line 5b for the reason for the short

tax year.

If the box for “Change in accounting period” is checked, the

entity must have applied for approval to change its tax year

unless certain conditions have been met. For more information,

see Form 1128, Application To Adopt, Change, or Retain a Tax

Year, and Pub. 538, Accounting Periods and Methods.

If you have a short tax year and none of the reasons listed

apply, check the box for “Other” and attach a statement

explaining the reason for the short tax year. Clearly explain the

circumstances that caused the short tax year.

If Form 7004 is filed for a return covering a short tax year

ending in June, see Maximum extension period, earlier.

Line 6

Enter the total tax, including any nonrefundable credits, the

entity expects to owe for the tax year. See the specific

instructions for the applicable return to estimate the amount of

the tentative tax. If you expect this amount to be zero, enter -0-.

Line 7

Enter the total payments and refundable credits. For more

information about “write-in” payments and credits, see the

instructions for the applicable return.

Line 8

Form 7004 does not extend the time to pay tax. If the entity is a

corporation or affiliated group of corporations filing a

consolidated return, the corporation must remit the amount of

the unpaid tax liability shown on line 8 on or before the due date

of the return.

Most entities must use electronic funds transfer to make all

federal tax deposits, including deposits for corporate income

taxes. Generally, electronic funds transfers are made using the

Electronic Federal Tax Payment System (EFTPS). To get more

information about EFTPS or to enroll in EFTPS, visit

www.eftps.gov or call 1-800-555-4477.

If the entity does not want to use EFTPS, it can arrange for its

tax professional, financial institution, payroll service, or other

trusted third party to make deposits on its behalf.

If you file Form 7004 electronically, you can pay by Electronic

Funds Withdrawal (EFW). See Form 8878-A, IRS e-file

Electronic Funds Withdrawal Authorization for Form 7004. If the

corporation expects to have a net operating loss carryback, the

corporation can reduce the amount to be deposited to the extent

of the overpayment resulting from the carryback, provided all

other prior year tax liabilities have been fully paid and Form

1138, Extension of Time for Payment of Taxes by a Corporation

Expecting a Net Operating Loss Carryback, is filed with Form

7004.

Foreign corporations that maintain an office or place of

business in the United States should pay their tax as described

above.

Foreign corporations that do not maintain an office or place of

business in the United States, see the instructions for the

corporation's applicable tax return (Form 1120-F or Form

1120-FSC) for information on depositing any tax due.

A trust (Form 1041), electing large partnership (Form

1065-B), or REMIC (Form 1066) will be granted an extension

even if it cannot pay the full amount shown on line 8. But it

should pay as much as it can to limit the amount of penalties and

interest it will owe.

If you are requesting an extension of time to file Form 1042,

see the deposit rules in the Instructions for Form 1042 to

determine how payment must be made.

Privacy Act and Paperwork Reduction Act Notice. We ask

for the information on this form to carry out the Internal Revenue

laws of the United States. We need it to ensure that you are

complying with these laws and to allow us to figure and collect

the right amount of tax. This information is needed to process

your application for the requested extension of time to file. You

are not required to request an extension of time to file. However,

if you do so, Internal Revenue Code sections 6001, 6011(a),

6081, and 6109 require you to provide the information requested

on this form, including identification numbers. Failure to provide

the information may delay or prevent processing your

application; providing any false information may subject you to

penalties.

You are not required to provide the information requested on

a form that is subject to the Paperwork Reduction Act unless the

form displays a valid OMB control number. Books or records

relating to a form or its instructions must be retained as long as

their contents may become material in the administration of any

Internal Revenue law. Generally, tax returns and return

information are confidential, as required by section 6103.

However, section 6103 allows or requires the Internal

Revenue Service to disclose or give such information to the

Department of Justice for civil or criminal litigation, and to cities,

states, the District of Columbia, and United States possessions

and commonwealths for use in administering their tax laws. We

may also disclose this information to other countries under a tax

treaty, to Federal and state agencies to enforce Federal nontax

criminal laws, or to Federal law enforcement and intelligence

agencies to combat terrorism.

The time needed to complete and file this form will vary

depending on individual circumstances. The estimated burden

for business taxpayers filing this form is approved under OMB

control number 1545-0123 and is included in the estimates

shown in the instructions for their business return. The estimated

burden for all other taxapyers who file this form is shown below.

The estimated average time is:

-3-

Page 4 of 6 Fileid: … ns/I7004/201712/A/XML/Cycle05/source 15:44 - 1-Feb-2018

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Recordkeeping ........................ 3 hr., 35 min.

Learning about the law or the form ............ 1 hr., 3 min.

Preparing the form ...................... 2 hr., 6 min.

Copying, assembling, and sending the form to the

IRS ................................ 16 min.

If you have comments concerning the accuracy of these time

estimates or suggestions for making this form simpler, we would

be happy to hear from you. You can send us comments from

IRS.gov/FormComments. Or you can write to the Internal

Revenue Service, Tax Forms and Publications Division, 1111

Constitution Ave. NW, IR-6526, Washington, DC 20224. Do not

send the tax form to this address. Instead, see Where To File,

below.

-4-

Page 5 of 6 Fileid: … ns/I7004/201712/A/XML/Cycle05/source 15:44 - 1-Feb-2018

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

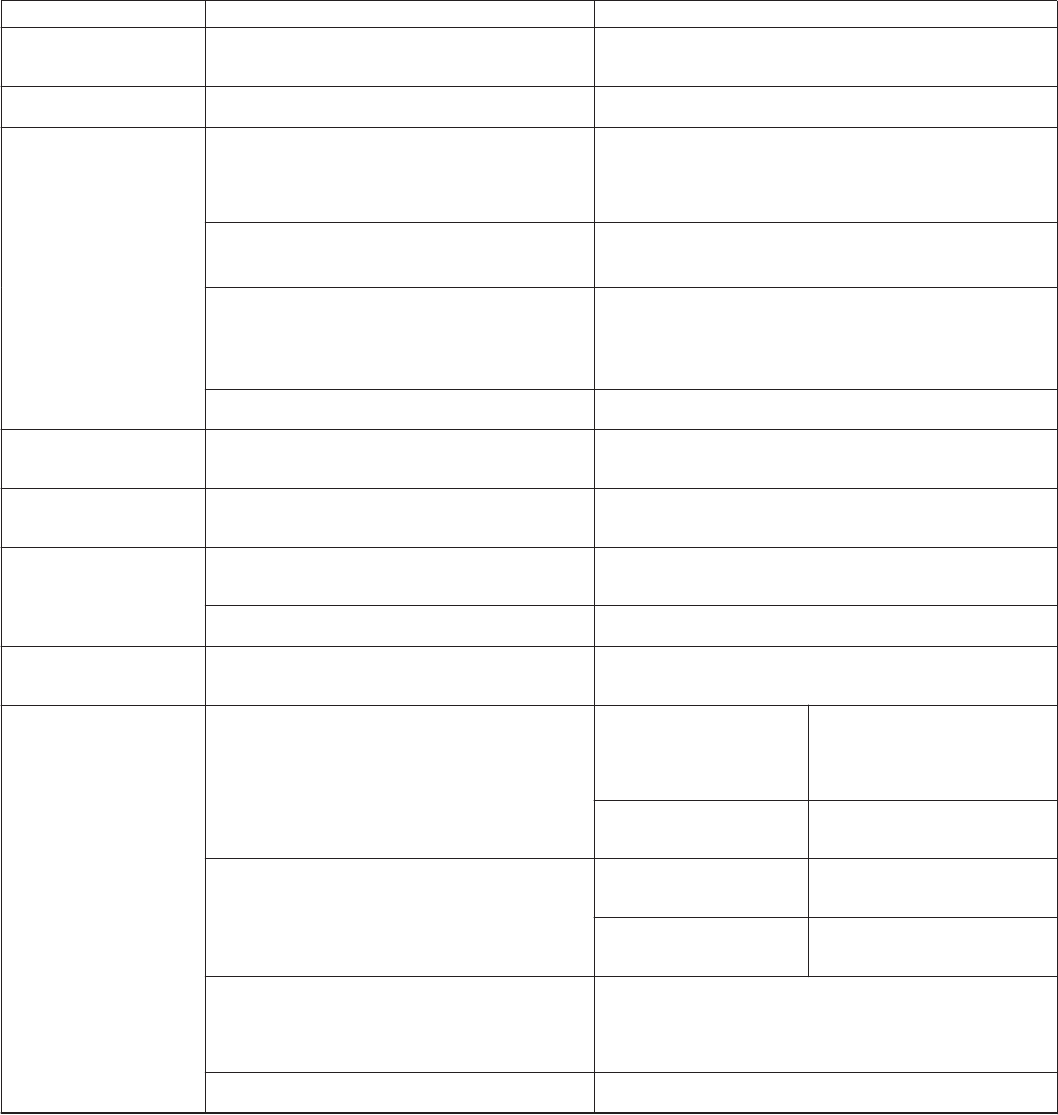

Where To File

IF the form is . . . AND the settler is (or was at death) . . . THEN file Form 7004 at:

706-GS(D) &

706-GS(T)

A resident U.S. citizen, resident alien,

nonresident U.S. citizen, or alien

Department of the Treasury, Internal Revenue Service Center,

Cincinnati, OH 45999-0045, or for private delivery service:

201 W. Rivercenter Blvd., Covington, KY 41011-1424

IF the form is . . . AND your principal business, office, or agency is

located in . . . THEN file Form 7004 at:

Connecticut, Delaware, District of Columbia, Florida,

Indiana, Maine, Maryland, Massachusetts, New

Hampshire, New Jersey, New York, North Carolina, Ohio,

Pennsylvania, Rhode Island, South Carolina, Vermont,

Virginia, West Virginia

Department of the Treasury

Internal Revenue Service Center

Cincinnati, OH 45999-0045

1041, 1120-H

Georgia, Illinois, Kentucky, Michigan, Tennessee,

Wisconsin

Department of the Treasury

Internal Revenue Service Center

Kansas City, MO 64999-0019

Alabama, Alaska, Arizona, Arkansas, California, Colorado,

Hawaii, Idaho, Iowa, Kansas, Louisiana, Minnesota,

Mississippi, Missouri, Montana, Nebraska, Nevada, New

Mexico, North Dakota, Oklahoma, Oregon, South Dakota,

Texas, Utah, Washington, Wyoming

Department of the Treasury

Internal Revenue Service Center

Ogden, UT 84201-0045

A foreign country or U.S. possession Internal Revenue Service Center

P.O. Box 409101, Ogden, UT 84409

1041-QFT,

8725, 8831,

8876, 8924, 8928

Any location

Department of the Treasury

Internal Revenue Service Center

Cincinnati, OH 45999-0045

1042, 1120-F,

1120-FSC,

3520-A, 8804

Any location

Internal Revenue Service Center

P.O. Box 409101, Ogden, UT 84409

1066, 1120-C,

1120-PC

The United States

Department of the Treasury

Internal Revenue Service Center

Ogden, UT 84201-0045

A foreign country or U.S. possession Internal Revenue Service Center

P.O. Box 409101, Ogden, UT 84409

1041-N, 1065-B, 1120-POL Any location

Department of the Treasury

Internal Revenue Service Center

Ogden, UT 84409-0045

1065, 1120,

1120-RIC, 1120S

Connecticut, Delaware, District of Columbia, Florida,

Indiana, Maine, Maryland, Massachusetts, New

Hampshire, New Jersey, New York, North Carolina, Ohio,

Pennsylvania, Rhode Island, South Carolina, Vermont,

Virginia, West Virginia

And the total assets at the

end of the tax year are:

Less than $10 million Department of the Treasury

Internal Revenue Service Center

Cincinnati, OH 45999-0045

$10 million or more

Department of the Treasury

Internal Revenue Service Center

Ogden, UT 84201-0045

Georgia, Illinois, Kentucky, Michigan, Tennessee,

Wisconsin

And the total assets at the

end of the tax year are:

Less than $10 million

Department of the Treasury

Internal Revenue Service Center

Kansas City, MO 64999-0019

$10 million or more

Department of the Treasury

Internal Revenue Service Center

Ogden, UT 84201-0045

Alabama, Alaska, Arizona, Arkansas, California, Colorado,

Hawaii, Idaho, Iowa, Kansas, Louisiana, Minnesota,

Mississippi, Missouri, Montana, Nebraska, Nevada, New

Mexico, North Dakota, Oklahoma, Oregon, South Dakota,

Texas, Utah, Washington, Wyoming

Department of the Treasury

Internal Revenue Service Center

Ogden, UT 84201-0045

A foreign country or U.S. possession Internal Revenue Service Center

P.O. Box 409101, Ogden, UT 84409

-5-

Page 6 of 6 Fileid: … ns/I7004/201712/A/XML/Cycle05/source 15:44 - 1-Feb-2018

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

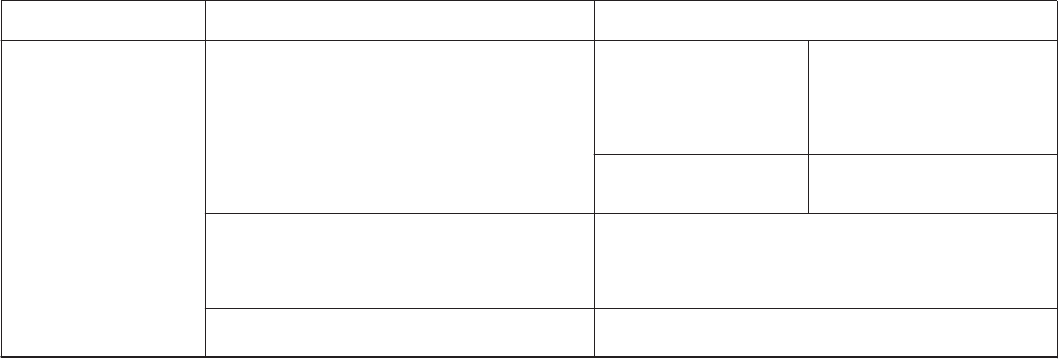

IF the form is . . . AND your principal business, office, or agency is

located in . . . THEN file Form 7004 at:

1120-L, 1120-ND,

1120-REIT,

1120-SF, 8612, 8613

Connecticut, Delaware, District of Columbia, Florida,

Georgia, Illinois, Indiana, Kentucky, Maine, Maryland,

Massachusetts, Michigan, New Hampshire, New Jersey,

New York, North Carolina, Ohio, Pennsylvania, Rhode

Island, South Carolina, Tennessee, Vermont, Virginia,

West Virginia, Wisconsin

And the total assets at the

end of the tax year are:

Less than $10 million

Department of the Treasury

Internal Revenue Service Center

Cincinnati, OH 45999-0045

$10 million or more

Department of the Treasury

Internal Revenue Service Center

Ogden, UT 84201-0045

Alabama, Alaska, Arizona, Arkansas, California, Colorado,

Hawaii, Idaho, Iowa, Kansas, Louisiana, Minnesota,

Mississippi, Missouri, Montana, Nebraska, Nevada, New

Mexico, North Dakota, Oklahoma, Oregon, South Dakota,

Texas, Utah, Washington, Wyoming

Department of the Treasury

Internal Revenue Service Center

Ogden, UT 84201-0045

A foreign country or U.S. possession Internal Revenue Service Center

P.O. Box 409101, Ogden, UT 84409

-6-