Listed Volatility And Variance Derivatives A Python Based Guide

listed%20volatility%20and%20variance%20derivatives%20-%20a%20python-based%20guide%20(2016)

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 357 [warning: Documents this large are best viewed by clicking the View PDF Link!]

- 10.1002@9781119167945.ch0.pdf (p.1-10)

- 10.1002@9781119167945.ch1.pdf (p.11-25)

- 10.1002@9781119167945.ch2.pdf (p.26-62)

- 10.1002@9781119167945.ch3.pdf (p.63-75)

- 10.1002@9781119167945.ch4.pdf (p.76-100)

- 10.1002@9781119167945.ch5.pdf (p.101-134)

- 10.1002@9781119167945.ch6.pdf (p.135-184)

- 10.1002@9781119167945.ch7.pdf (p.185-225)

- 10.1002@9781119167945.ch8.pdf (p.226-230)

- 10.1002@9781119167945.ch9.pdf (p.231-254)

- 10.1002@9781119167945.ch10.pdf (p.255-272)

- 10.1002@9781119167945.ch11.pdf (p.273-284)

- 10.1002@9781119167945.ch12.pdf (p.285-300)

- 10.1002@9781119167945.ch13.pdf (p.301-318)

- 10.1002@9781119167945.ch14.pdf (p.319-347)

- 10.1002@9781119167945.ch15.pdf (p.348-349)

- 10.1002@9781119167945.ch16.pdf (p.350-357)

Listed Volatility

and Variance

Derivatives

Founded in 1807, John Wiley & Sons is the oldest independent publishing company in the

United States. With ofces in North America, Europe, Australia and Asia, Wiley is glob-

ally committed to developing and marketing print and electronic products and services for

our customers’ professional and personal knowledge and understanding.

The Wiley Finance series contains books written specically for nance and invest-

ment professionals as well as sophisticated individual investors and their nancial advi-

sors. Book topics range from portfolio management to e-commerce, risk management,

nancial engineering, valuation and nancial instrument analysis, as well as much more.

For a list of available titles, visit our Web site at www.WileyFinance.com.

Listed Volatility

and Variance

Derivatives

A Python-based Guide

DR. YVES J. HILPISCH

This edition rst published 2017

©2017 Yves Hilpisch

Registered ofce

John Wiley & Sons Ltd, The Atrium, Southern Gate, Chichester, West Sussex, PO19 8SQ, United

Kingdom

For details of our global editorial ofces, for customer services and for information about how to apply

for permission to reuse the copyright material in this book please visit our website at www.wiley.com.

The right of the author to be identied as the author of this work has been asserted in accordance with

the Copyright, Designs and Patents Act 1988.

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or

transmitted, in any form or by any means, electronic, mechanical, photocopying, recording or

otherwise, except as permitted by the UK Copyright, Designs and Patents Act 1988, without the prior

permission of the publisher.

Wiley publishes in a variety of print and electronic formats and by print-on-demand. Some material

included with standard print versions of this book may not be included in e-books or in

print-on-demand. If this book refers to media such as a CD or DVD that is not included in the version

you purchased, you may download this material at http://booksupport.wiley.com. For more information

about Wiley products, visit www.wiley.com.

Designations used by companies to distinguish their products are often claimed as trademarks. All

brand names and product names used in this book are trade names, service marks, trademarks or

registered trademarks of their respective owners. The publisher is not associated with any product or

vendor mentioned in this book.

Limit of Liability/Disclaimer of Warranty: While the publisher and author have used their best efforts

in preparing this book, they make no representations or warranties with respect to the accuracy or

completeness of the contents of this book and specically disclaim any implied warranties of

merchantability or tness for a particular purpose. It is sold on the understanding that the publisher is

not engaged in rendering professional services and neither the publisher nor the author shall be liable

for damages arising herefrom. If professional advice or other expert assistance is required, the services

of a competent professional should be sought.

Library of Congress Cataloging-in-Publication Data is available

A catalogue record for this book is available from the British Library.

ISBN 978-1-119-16791-4 (hbk) ISBN 978-1-119-16792-1 (ebk)

ISBN 978-1-119-16793-8 (ebk) ISBN 978-1-119-16794-5 (ebk)

Cover Design: Wiley

Top Image: ©grapestock/Shutterstock

Bottom Image: ©stocksnapper/iStock

Set in 10/12pt Times by Aptara Inc., New Delhi, India

Printed in Great Britain by TJ International Ltd, Padstow, Cornwall, UK

Contents

Preface xi

PART ONE

Introduction to Volatility and Variance

CHAPTER 1

Derivatives, Volatility and Variance 3

1.1 Option Pricing and Hedging 3

1.2 Notions of Volatility and Variance 6

1.3 Listed Volatility and Variance Derivatives 7

1.3.1 The US History 7

1.3.2 The European History 8

1.3.3 Volatility of Volatility Indexes 9

1.3.4 Products Covered in this Book 10

1.4 Volatility and Variance Trading 11

1.4.1 Volatility Trading 11

1.4.2 Variance Trading 13

1.5 Python as Our Tool of Choice 14

1.6 Quick Guide Through the Rest of the Book 14

CHAPTER 2

Introduction to Python 17

2.1 Python Basics 17

2.1.1 Data Types 17

2.1.2 Data Structures 20

2.1.3 Control Structures 22

2.1.4 Special Python Idioms 23

2.2 NumPy 28

2.3 matplotlib 34

2.4 pandas 38

2.4.1 pandas DataFrame class 39

2.4.2 Input-Output Operations 45

2.4.3 Financial Analytics Examples 47

2.5 Conclusions 53

v

vi CONTENTS

CHAPTER 3

Model-Free Replication of Variance 55

3.1 Introduction 55

3.2 Spanning with Options 56

3.3 Log Contracts 57

3.4 Static Replication of Realized Variance and Variance Swaps 57

3.5 Constant Dollar Gamma Derivatives and Portfolios 58

3.6 Practical Replication of Realized Variance 59

3.7 VSTOXX as Volatility Index 65

3.8 Conclusions 67

PART TWO

Listed Volatility Derivatives

CHAPTER 4

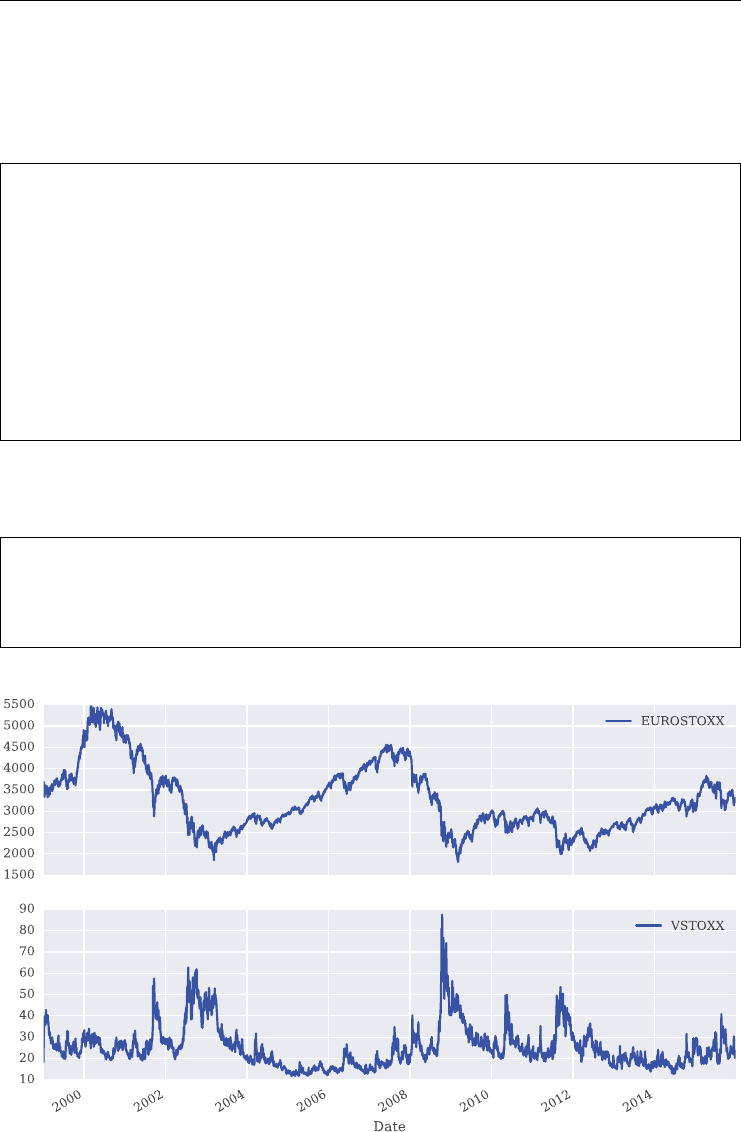

Data Analysis and Strategies 71

4.1 Introduction 71

4.2 Retrieving Base Data 71

4.2.1 EURO STOXX 50 Data 71

4.2.2 VSTOXX Data 74

4.2.3 Combining the Data Sets 76

4.2.4 Saving the Data 78

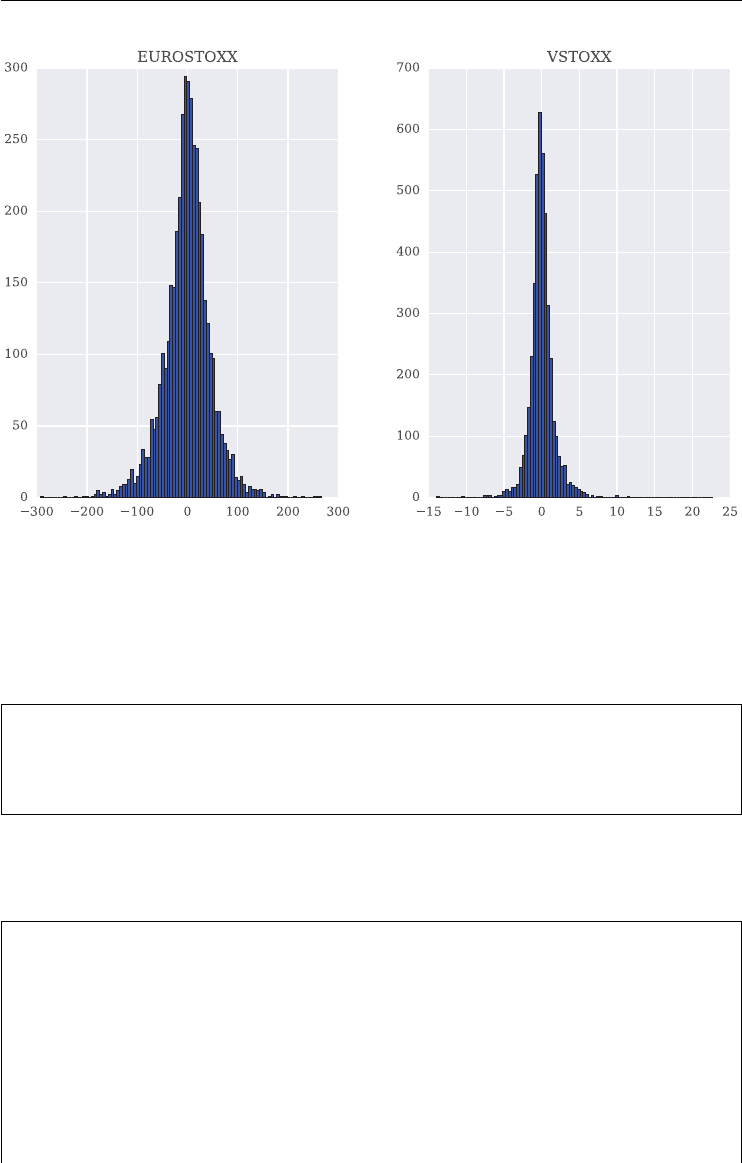

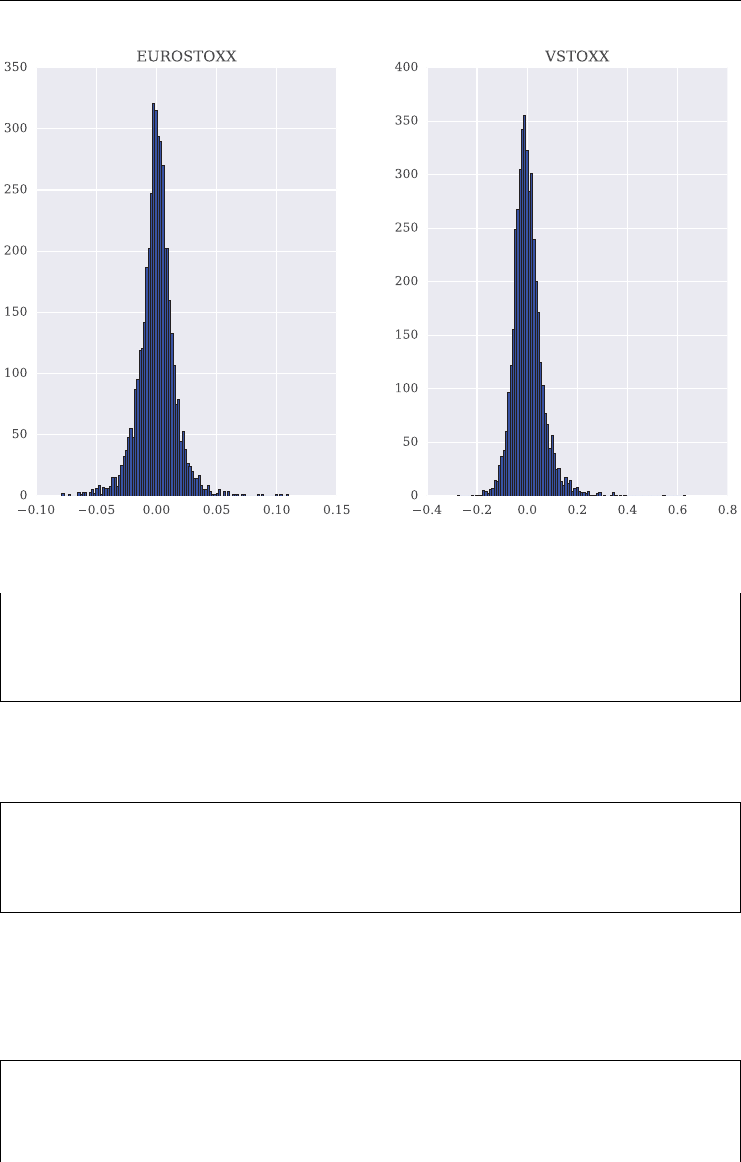

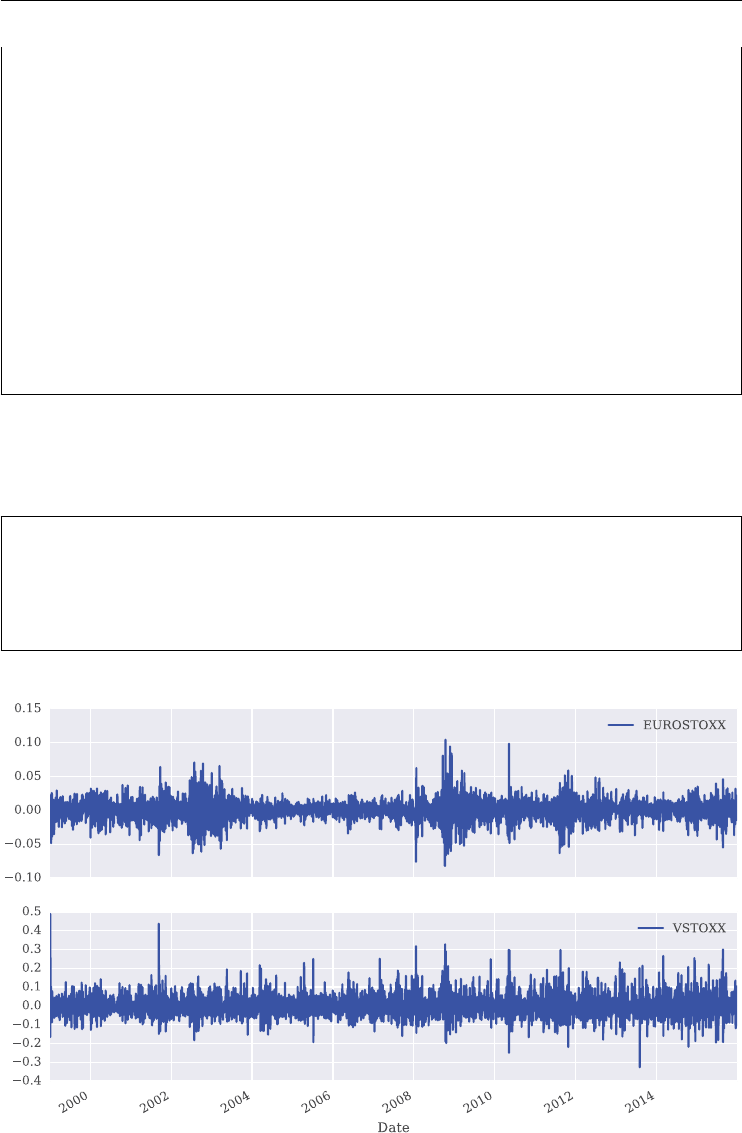

4.3 Basic Data Analysis 78

4.4 Correlation Analysis 83

4.5 Constant Proportion Investment Strategies 87

4.6 Conclusions 93

CHAPTER 5

VSTOXX Index 95

5.1 Introduction 95

5.2 Collecting Option Data 95

5.3 Calculating the Sub-Indexes 105

5.3.1 The Algorithm 106

5.4 Calculating the VSTOXX Index 114

5.5 Conclusions 118

5.6 Python Scripts 118

5.6.1 index collect option_data.py 118

5.6.2 index_subindex_calculation.py 123

5.6.3 index_vstoxx_calculation.py 127

CHAPTER 6

Valuing Volatility Derivatives 129

6.1 Introduction 129

6.2 The Valuation Framework 129

6.3 The Futures Pricing Formula 130

Contents vii

6.4 The Option Pricing Formula 132

6.5 Monte Carlo Simulation 135

6.6 Automated Monte Carlo Tests 141

6.6.1 The Automated Testing 141

6.6.2 The Storage Functions 145

6.6.3 The Results 146

6.7 Model Calibration 153

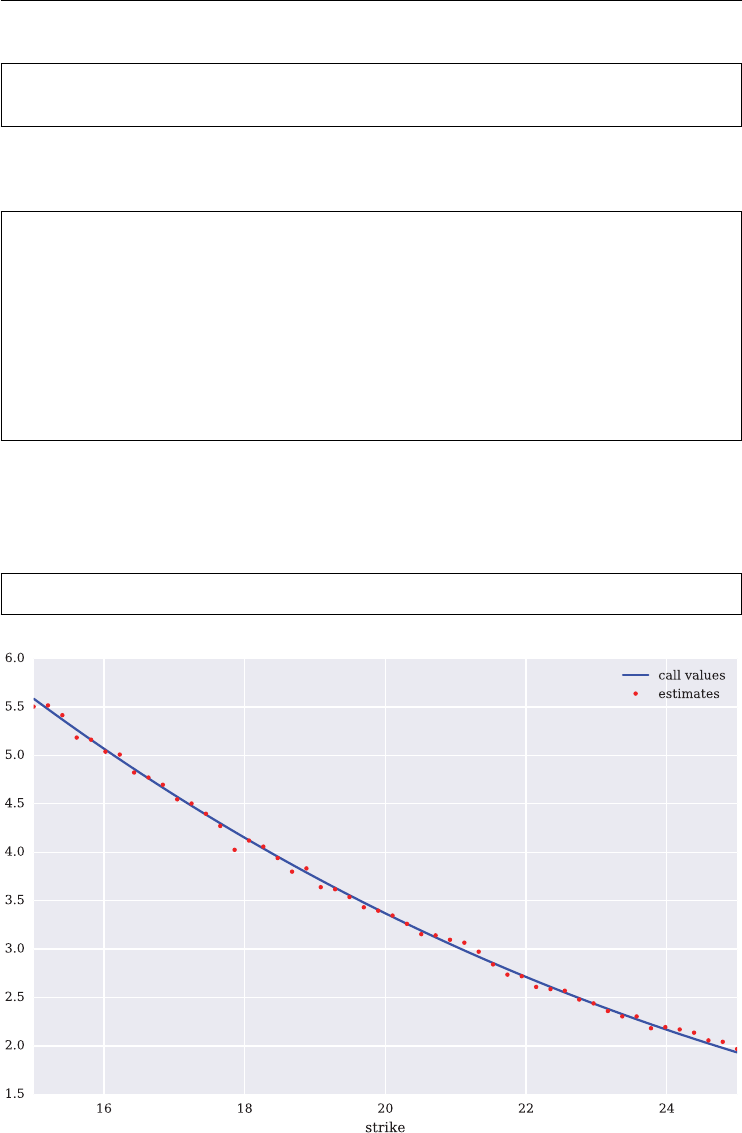

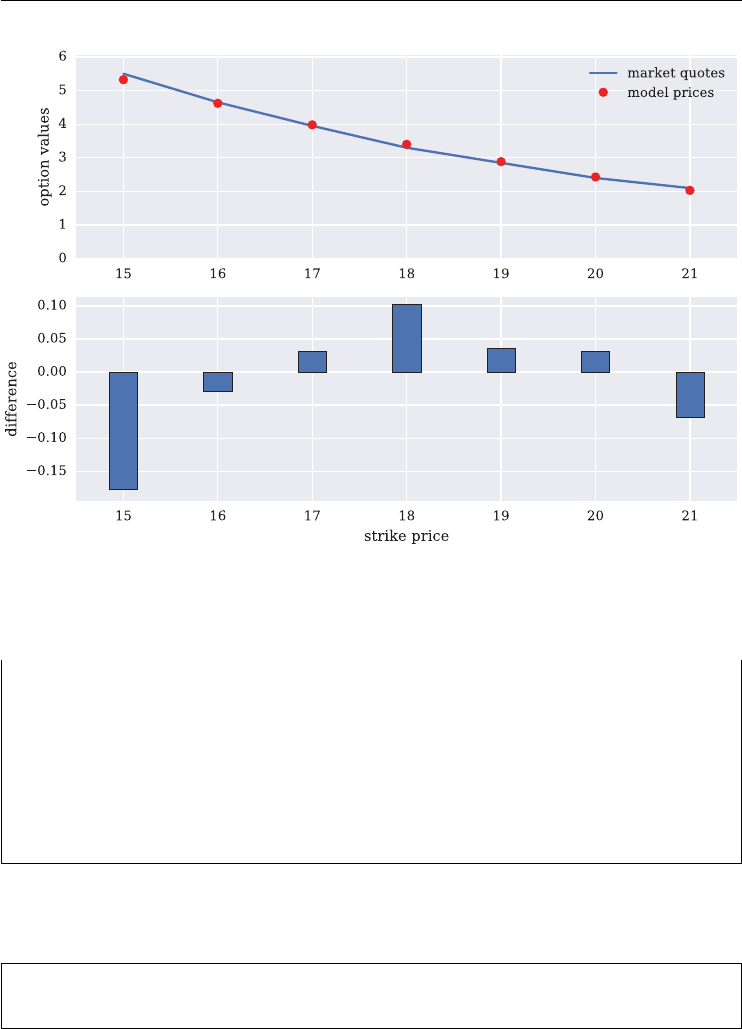

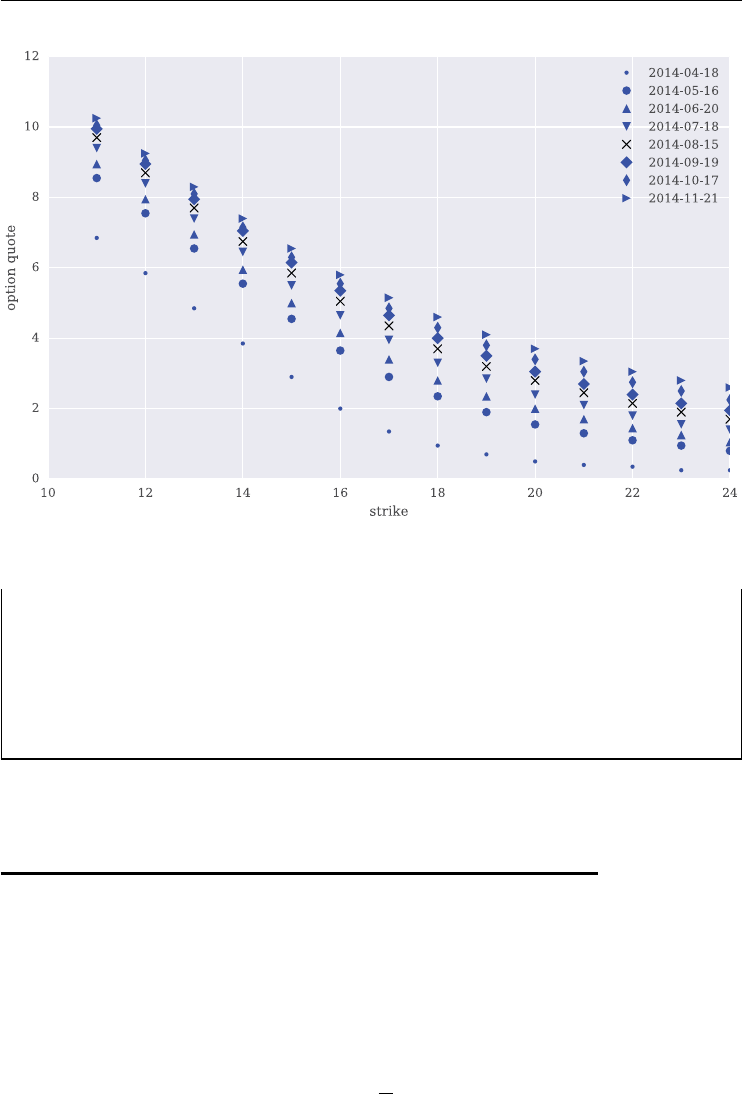

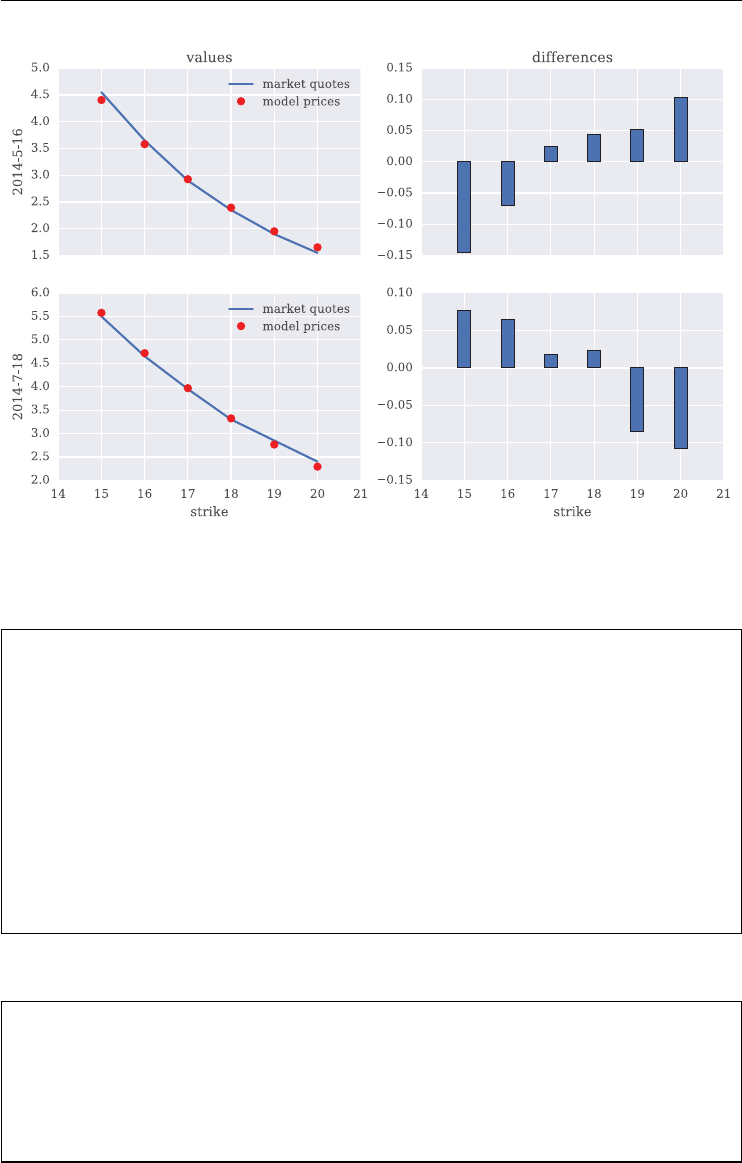

6.7.1 The Option Quotes 154

6.7.2 The Calibration Procedure 155

6.7.3 The Calibration Results 160

6.8 Conclusions 163

6.9 Python Scripts 163

6.9.1 srd_functions.py 163

6.9.2 srd simulation analysis.py 167

6.9.3 srd simulation results.py 171

6.9.4 srd model calibration.py 174

CHAPTER 7

Advanced Modeling of the VSTOXX Index 179

7.1 Introduction 179

7.2 Market Quotes for Call Options 179

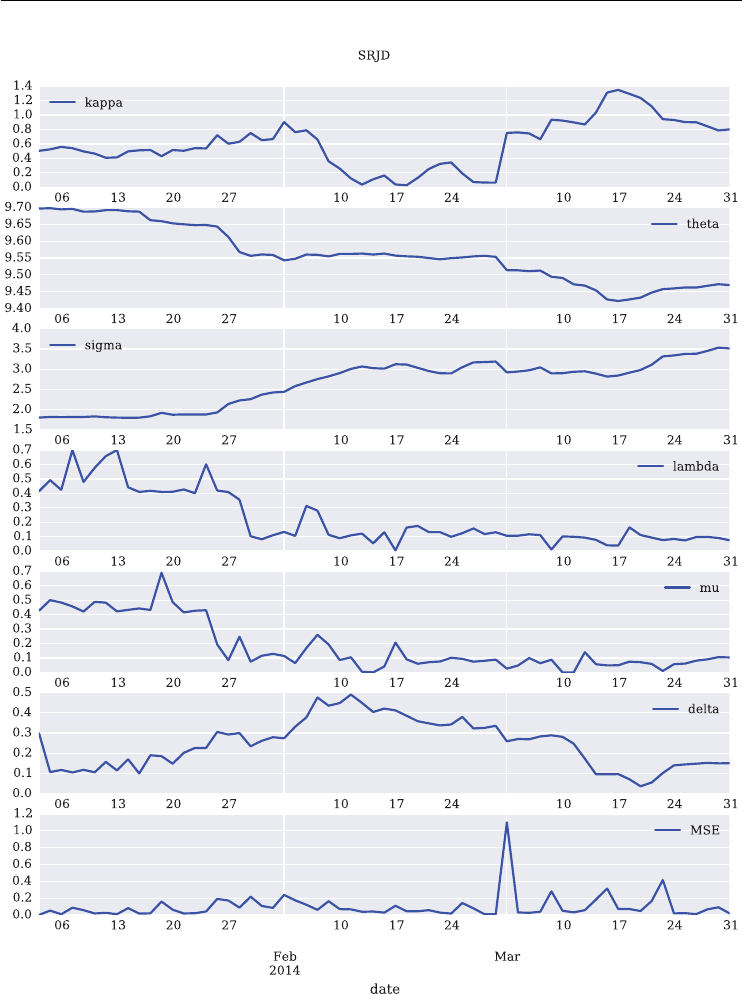

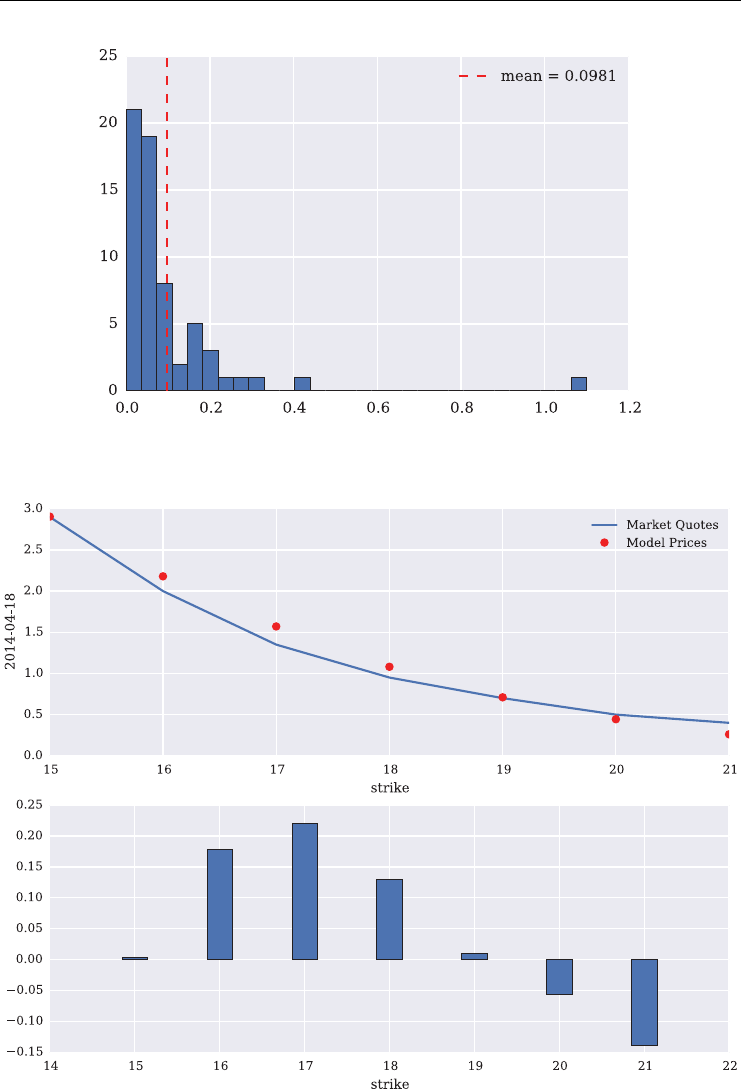

7.3 The SRJD Model 182

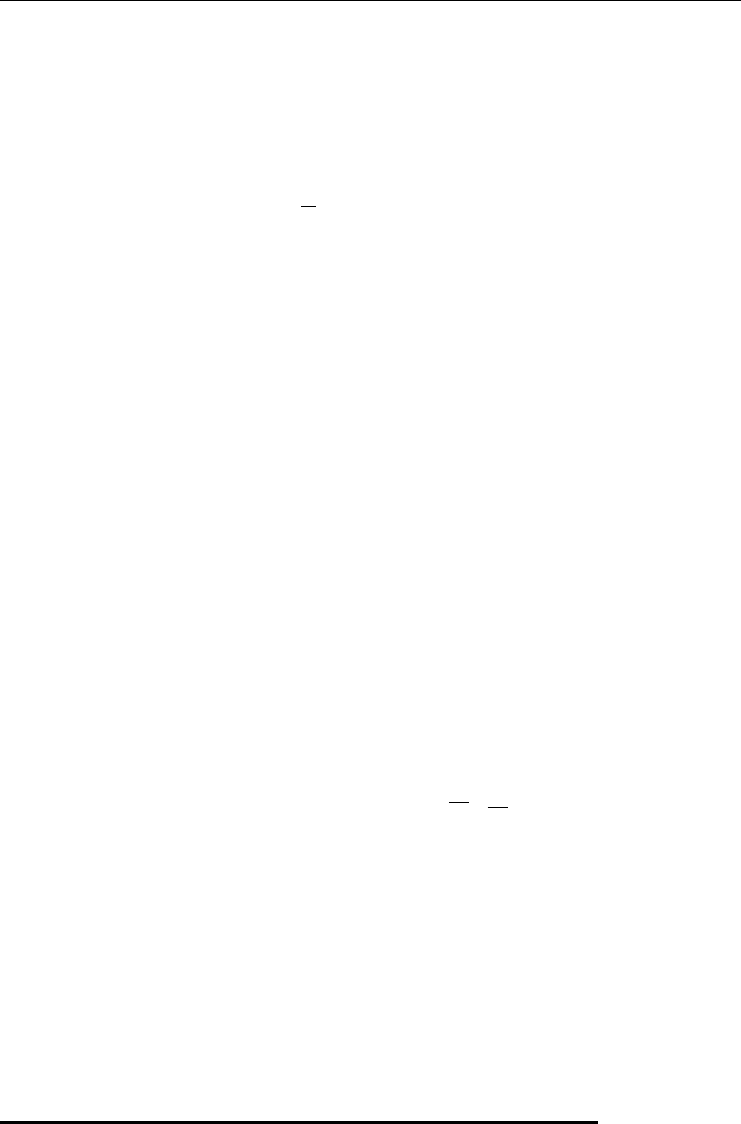

7.4 Term Structure Calibration 183

7.4.1 Futures Term Structure 184

7.4.2 Shifted Volatility Process 190

7.5 Option Valuation by Monte Carlo Simulation 191

7.5.1 Monte Carlo Valuation 191

7.5.2 Technical Implementation 192

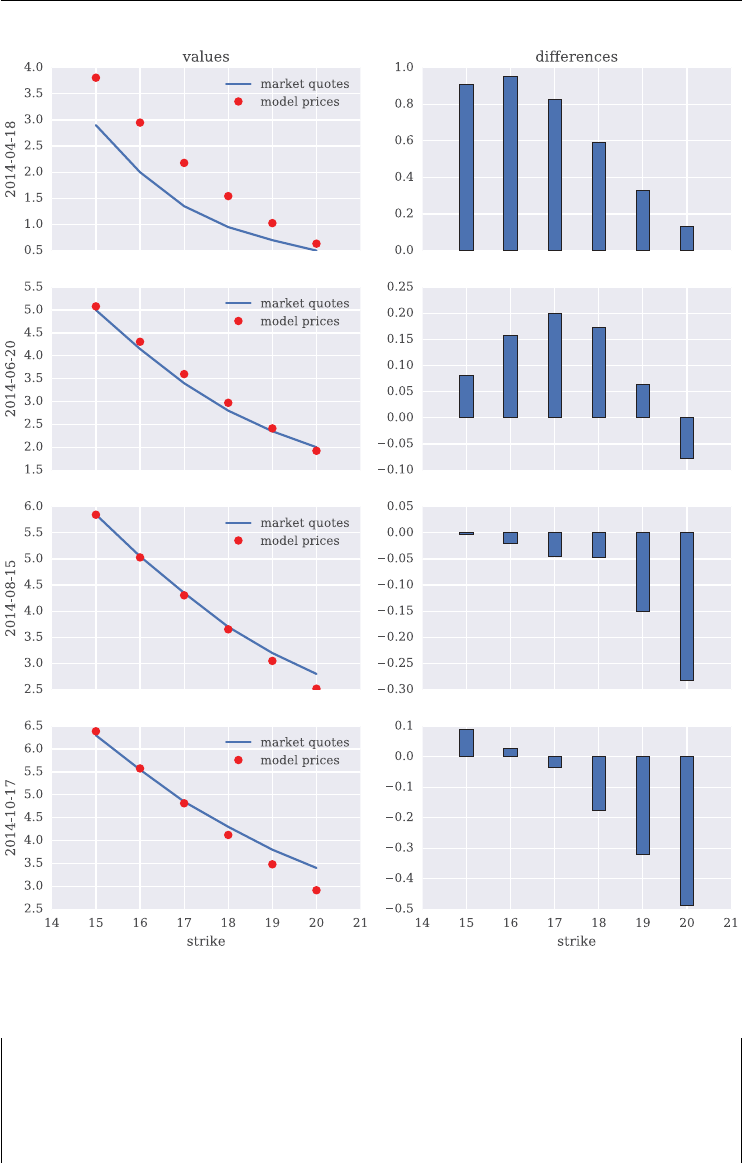

7.6 Model Calibration 195

7.6.1 The Python Code 196

7.6.2 Short Maturity 199

7.6.3 Two Maturities 201

7.6.4 Four Maturities 203

7.6.5 All Maturities 205

7.7 Conclusions 209

7.8 Python Scripts 210

7.8.1 srjd fwd calibration.py 210

7.8.2 srjd_simulation.py 212

7.8.3 srjd_model_calibration.py 215

CHAPTER 8

Terms of the VSTOXX and its Derivatives 221

8.1 The EURO STOXX 50 Index 221

8.2 The VSTOXX Index 221

8.3 VSTOXX Futures Contracts 223

8.4 VSTOXX Options Contracts 224

8.5 Conclusions 225

viii CONTENTS

PART THREE

Listed Variance Derivatives

CHAPTER 9

Realized Variance and Variance Swaps 229

9.1 Introduction 229

9.2 Realized Variance 229

9.3 Variance Swaps 235

9.3.1 Denition of a Variance Swap 235

9.3.2 Numerical Example 235

9.3.3 Mark-to-Market 239

9.3.4 Vega Sensitivity 241

9.3.5 Variance Swap on the EURO STOXX 50 242

9.4 Variance vs. Volatility 247

9.4.1 Squared Variations 247

9.4.2 Additivity in Time 247

9.4.3 Static Hedges 250

9.4.4 Broad Measure of Risk 250

9.5 Conclusions 250

CHAPTER 10

Variance Futures at Eurex 251

10.1 Introduction 251

10.2 Variance Futures Concepts 252

10.2.1 Realized Variance 252

10.2.2 Net Present Value Concepts 252

10.2.3 Traded Variance Strike 257

10.2.4 Traded Futures Price 257

10.2.5 Number of Futures 258

10.2.6 Par Variance Strike 258

10.2.7 Futures Settlement Price 258

10.3 Example Calculation for a Variance Future 258

10.4 Comparison of Variance Swap and Future 265

10.5 Conclusions 268

CHAPTER 11

Trading and Settlement 269

11.1 Introduction 269

11.2 Overview of Variance Futures Terms 269

11.3 Intraday Trading 270

11.4 Trade Matching 274

11.5 Different Traded Volatilities 275

11.6 After the Trade Matching 277

11.7 Further Details 279

11.7.1 Interest Rate Calculation 279

11.7.2 Market Disruption Events 280

11.8 Conclusions 280

Contents ix

PART FOUR

DX Analytics

CHAPTER 12

DX Analytics – An Overview 283

12.1 Introduction 283

12.2 Modeling Risk Factors 284

12.3 Modeling Derivatives 287

12.4 Derivatives Portfolios 290

12.4.1 Modeling Portfolios 292

12.4.2 Simulation and Valuation 293

12.4.3 Risk Reports 294

12.5 Conclusions 296

CHAPTER 13

DX Analytics – Square-Root Diffusion 297

13.1 Introduction 297

13.2 Data Import and Selection 297

13.3 Modeling the VSTOXX Options 301

13.4 Calibration of the VSTOXX Model 303

13.5 Conclusions 308

13.6 Python Scripts 308

13.6.1 dx srd calibration.py 308

CHAPTER 14

DX Analytics – Square-Root Jump Diffusion 315

14.1 Introduction 315

14.2 Modeling the VSTOXX Options 315

14.3 Calibration of the VSTOXX Model 320

14.4 Calibration Results 325

14.4.1 Calibration to One Maturity 325

14.4.2 Calibration to Two Maturities 325

14.4.3 Calibration to Five Maturities 325

14.4.4 Calibration without Penalties 331

14.5 Conclusions 332

14.6 Python Scripts 334

14.6.1 dx srjd calibration.py 334

Bibliography 345

Index 347

Preface

Volatility and variance trading has evolved from something opaque to a standard tool in

today’s nancial markets. The motives for trading volatility and variance as an asset class

of its own are numerous. Among others, it allows for effective option and equity portfolio hedg-

ing and risk management as well as straight out speculation on future volatility (index) move-

ments. The potential benets of volatility- and variance-based strategies are widely accepted

by researchers and practitioners alike.

With regard to products it mainly started out around 1993 with over-the-counter (OTC)

variance swaps. At about the same time, the Chicago Board Options Exchange introduced the

VIX volatility index. This index still serves today – after a signicant change in its method-

ology – as the underlying risk factor for some of the most liquidly traded listed derivatives

in this area. The listing of such derivatives allows for a more standardized, cost efcient and

transparent approach to volatility and variance trading.

This book covers some of the most important listed volatility and variance derivatives

with a focus on products provided by Eurex. Larger parts of the content are based on the

Eurex Advanced Services tutorial series which use Python to illustrate the main concepts of

volatility and variance products. I am grateful that Eurex allowed me to use the contents of the

tutorial series freely for this book.

Python has become not only one of the most widely used programming languages but also

one of the major technology platforms in the nancial industry. It is more like a platform since

the Python ecosystem provides a wealth of powerful libraries and packages useful for nancial

analytics and application building. It also integrates well with many other technologies, like

the statistical programming language R, used in the nancial industry. You can nd links to

all Python resources under http://lvvd.tpq.io.

I thank Michael Schwed for providing parts of the Python code. I also thank my family

for all their love and support over the years, especially my wife Sandra and our children Lilli

and Henry. I dedicate this book to my beloved dog Jil. I miss you.

Y

Voelklingen, Saarland, April 2016

xi

PART

One

Introduction to Volatility

and Variance

CHAPTER 1

Derivatives, Volatility and Variance

The rst chapter provides some background information for the rest of the book. It mainly

covers concepts and notions of importance for later chapters. In particular, it shows how the

delta hedging of options is connected with variance swaps and futures. It also discusses differ-

ent notions of volatility and variance, the history of traded volatility and variance derivatives

as well as why Python is a good choice for the analysis of such instruments.

1.1 OPTION PRICING AND HEDGING

In the Black-Scholes-Merton (1973) benchmark model for option pricing, uncertainty with

regard to the single underlying risk factor S(stock price, index level, etc.) is driven by a geo-

metric Brownian motion with stochastic differential equation (SDE)

dSt=𝜇Stdt +𝜎StdZt

Throughout we may think of the risk factor as being a stock index paying no dividends. Stis

then the level of the index at time t,𝜇the constant drift, 𝜎the instantaneous volatility and Ztis

a standard Brownian motion. In a risk-neutral setting, the drift 𝜇is replaced by the (constant)

risk-less short rate r

dSt=rStdt +𝜎StdZt

In addition to the index which is assumed to be directly tradable, there is also a risk-less bond

Bavailable for trading. It satises the differential equation

dBt=rBtdt

In this model, it is possible to derive a closed pricing formula for a vanilla European call option

Cmaturing at some future date Twith payoff max[ST−K,0], Kbeing the xed strike price.

It is

C(S,K,t,T,r,𝜎)=St⋅N(d1)−e−r(T−t)⋅K⋅N(d2)

3

Listed Volatility and Variance Derivatives: A

Python-based Guide

By Dr. Yves J. Hilpisch

© 2017 Yves Hilpisch

4LISTED VOLATILITY AND VARIANCE DERIVATIVES

where

N(d)=1

2𝜋∫d

−∞

e−1

2x2dx

d1=

log St

K+r+𝜎2

2(T−t)

𝜎T−t

d2=

log St

K+r−𝜎2

2(T−t)

𝜎T−t

The price of a vanilla European put option Pwith payoff max[K−ST, 0] is determined by

put-call parity as

Pt=Ct−St+e−r(T−t)K

There are multiple ways to derive this famous Black-Scholes-Merton formula. One way relies

on the construction of a portfolio comprised of the index and the risk-less bond that perfectly

replicates the option payoff at maturity. To avoid risk-less arbitrage, the value of the option

must equal the payoff of the replicating portfolio. Another method relies on calculating the

risk-neutral expectation of the option payoff at maturity and discounting it back to the present

by the risk-neutral short rate. For detailed explanations of these approaches refer, for example,

to Bj¨

ork (2009).

Yet another way, which we want to look at in a bit more detail, is to perfectly hedge

the risk resulting from an option (e.g. from the point of view of a seller of the option) by

dynamically trading the index and the risk-less bond. This approach is usually called delta

hedging (see Sinclair (2008), ch. 1). The delta of a European call option is given by the rst

partial derivative of the pricing formula with respect to the value of the risk factor, i.e. 𝛿t=𝛿Ct

𝛿St

.

More specically, we get

𝛿t=𝛿Ct

𝛿St

=N(d1)

When trading takes place continuously, the European call option position hedged by 𝛿tindex

units short is risk-less:

dΠt≡dCt−𝛿tSt=0

This is due to the fact that the only (instantaneous) risk results from changes in the index level

and all such (marginal) changes are compensated for by the delta short index position.

Continuous models and trading are a mathematically convenient description of the real

world. However, in practice trading and therefore hedging can only take place at discrete points

in time. This does not lead to a complete breakdown of the delta hedging approach, but it

Derivatives, Volatility and Variance 5

introduces hedge errors. If hedging takes place at every discrete time interval of length Δt,the

Prot-Loss (PL) for such a time interval is roughly (see Bossu (2014), p. 59)

PLΔt≈1

2Γ⋅ΔS2+Θ⋅Δt

Γis the gamma of the option and measures how the delta (marginally) changes with the chang-

ing index level. ΔSis the change in the index level over the time interval Δt. It is given by

Γ= 𝜕2C

𝜕S2=N′(d1)

S𝜎T−t

Θis the theta of the option and measures how the option value changes with the passage of

time. It is given approximately by (see Bossu (2014), p. 60)

Θ≈−

1

2ΓS2𝜎2

With this we get

PLΔt≈1

2Γ⋅ΔS2−1

2ΓS2𝜎2⋅Δt

=1

2Γ⋅S2ΔS

S2

−𝜎⋅Δt2

The quantity 1

2Γ⋅S2is called the dollar gamma of the option and gives the second order change

in the option price induced by a (marginal) change in the index level. (ΔS

S)2is the squared

realized return over the time interval Δt– it might be interpreted as the (instantaneously)

realized variance if the time interval is short enough and the drift is close to zero. Finally,

(𝜎⋅Δt)2is the xed, “theoretical” variance in the model for the time interval.

The above reasoning illustrates that the PL of a discretely delta hedged option position is

determined by the difference between the realized variance during the discrete hedge interval

and the theoretically expected variance given the model parameter for the volatility. The total

hedge error over N=T

Δtintervals is given by

Cumulative PLΔt≈1

2

N

t=1

Γt−1⋅S2

t−1ΔSt

St−12

−𝜎⋅Δt2(1.1)

This little exercise in option hedging leads us to a result which is already quite close to a

product intensively discussed in this book: listed variance futures. Variance futures, and their

Over-the-Counter (OTC) relatives variance swaps, pay to the holder the difference between

realized variance over a certain period of time and a xed variance strike.

6LISTED VOLATILITY AND VARIANCE DERIVATIVES

1.2 NOTIONS OF VOLATILITY AND VARIANCE

The previous section already touches on different notions of volatility and variance. This

section provides formal denitions for these and other quantities of importance. For a more

detailed exposition refer to Sinclair (2008). In what follows we assume that a time series is

given with quotes Sn,n∈{0, …,N} (see Hilpisch (2015, ch. 3)). We do not assume any spe-

cic model that might generate the time series data. The log return for n>0 is dened by

Rn≡log Sn−logSn−1=log Sn

Sn−1

realized or historical volatility: this refers to the standard deviation of the log returns of

a nancial time series; suppose we observe N(past) log returns Rn,n∈{1, …,N}, with

mean return ̂𝜇 =1

NN

n=1Rn; the realized or historical volatility ̂𝜎 is then given by

̂𝜎 =

1

N−1

N

n=1

(Rn−̂𝜇)2

instantaneous volatility: this refers to the volatility factor of a diffusion process; for

example, in the Black-Scholes-Merton model the instantaneous volatility 𝜎is found in

the respective (risk-neutral) stochastic differential equation (SDE)

dSt=rStdt +𝜎StdZt

implied volatility: this is the volatility that, if put into the Black-Scholes-Merton option

pricing formula, gives the market-observed price of an option; suppose we observe today

a price of C∗

0for a European call option; the implied volatility 𝜎imp is the quantity that

solves ceteris paribus the implicit equation

C∗

0=CBSM(S0,K,t=0, T,r,𝜎imp)

These volatilities all have squared counterparts which are then named variance, such as real-

ized variance, instantenous variance or implied variance. We have already encountered realized

variance in the previous section. Let us revisit this quantity for a moment. Simply applying the

above denition of realized volatility and squaring it we get

̂𝜎2=1

N−1

N

n=1

(Rn−̂𝜇)2

In practice, however, this denition usually gets adjusted to

̂𝜎2=1

N

N

n=1

R2

n

Derivatives, Volatility and Variance 7

The drift of the process is assumed to be zero and only the log return terms get squared. It

is also common practice to use the denition for the uncorrected (biased) standard deviation

with factor 1

Ninstead of the denition for the corrected (unbiased) standard deviation with

factor 1

N−1. This explains why we call the term ( ΔSt

St−1

)2from the delta hedge PL in the previous

section realized variance over the time interval Δt. In that case, however, the return is the

simple return instead of the log return.

Other adjustments in practice are to scale the value to an annual quantity by multiplying

it by 252 (trading days) and to introduce an additional scaling term (to get percent values

instead of decimal ones). One then usually ends up with (see chapter 9, Realized Variance and

Variance Swaps)

̂𝜎2≡10000 ⋅

252

N

⋅

N

n=1

R2

n

Later on we will also drop the hat notation when there is no ambiguity.

1.3 LISTED VOLATILITY AND VARIANCE DERIVATIVES

Volatility is one of the most important notions and concepts in derivatives pricing and analytics.

Early research and nancial practice considered volatility as a major input for pricing and

hedging. It is not that long ago that the market started thinking of volatility as an asset class

of its own and designed products to make it directly tradable.

The idea for a volatility index was conceived by Brenner and Galai in 1987 and pub-

lished in the note Brenner and Galai (1989) in the Financial Analysts Journal. They write in

their note:

“While there are efcient tools for hedging against general changes in overall market

directions, so far there are no effective tools available for hedging against changes

in volatility. …We therefore propose the construction of three volatility indexes on

which cash-settled options and futures can be traded.”

In what follows, we focus on the US and European markets.

1.3.1 The US History

The Chicago Board Options Exchange (CBOE) introduced an equity volatility index, called

VIX, in 1993. It was based on a methodology developed by Fleming, Ostdiek and Whaley

(1995) – a working paper version of which was circulated in 1993 – and data from S&P 100

index options. The methodology was changed in 2003 to the now standard practice which uses

the robust, model free replication results for variance (see chapter 3 Model-Free Replication

of Variance) and data from S&P 500 index options (see CBOE (2003)). While the rst version

represented a proxy for the 30 day at-the-money implied volatility, the current version is a

proxy for the 30 day variance swap rate, i.e. the xed variance strike which gives a zero value

for a respective swap at inception.

8LISTED VOLATILITY AND VARIANCE DERIVATIVES

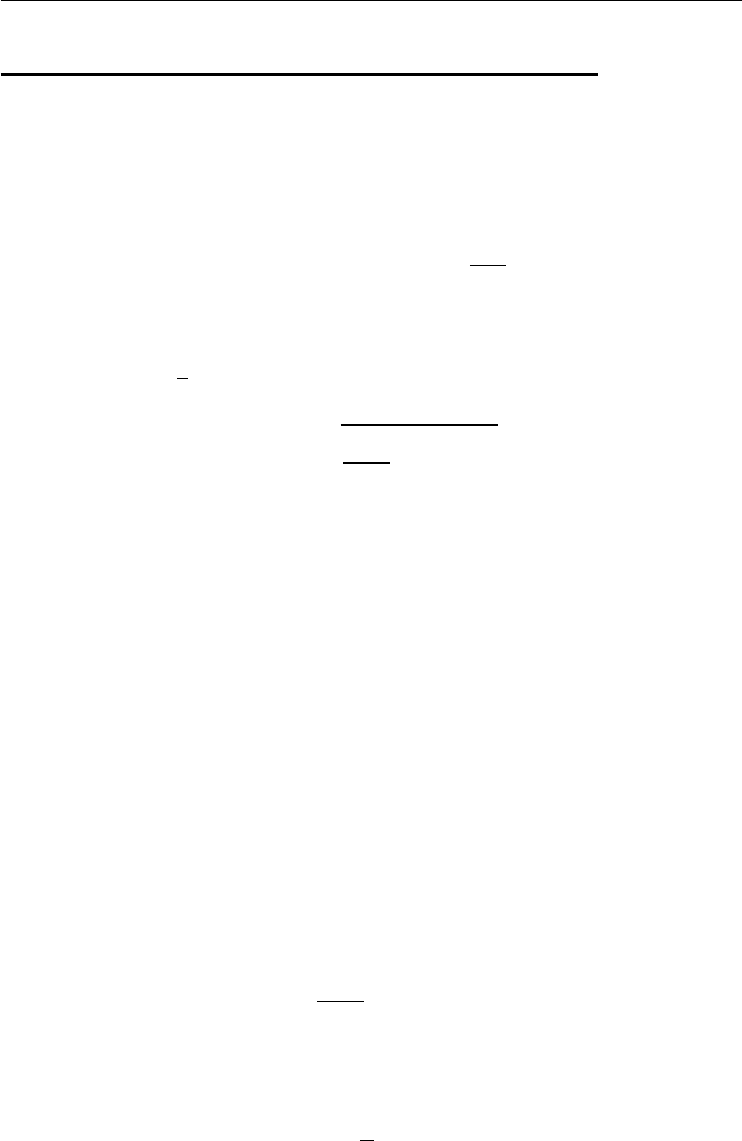

FIGURE 1.1 Historical volume of traded VIX derivatives on a log scale. Data source:

http://cfe.cboe.com/data/historicaldata.aspx

Carr and Lee (2009) provide a brief history of both OTC and listed volatility and variance

products. They claim that the rst OTC variance swap has been engineered and offered by

Union Bank of Switzerland (UBS) in 1993, at about the same time the CBOE announced the

VIX. These were also the rst traded contracts to attract some liquidity in contrast to volatility

swaps which were also introduced shortly afterwards. One reason for this is that variance swaps

can be robustly hedged – as we will see in later chapters – while volatility swaps, in general,

cannot. It is more or less the same reasoning behind the change of methodology for the VIX

in 2003.

Trading in futures on the VIX started in 2004 while the rst options on the index were

introduced in 2006. These instruments are already described in Whaley (1993), although their

market launch took more than 10 years after the introduction of the VIX. These were not the

rst listed volatility derivatives but the rst to attract signicant liquidity and they are more

actively traded at the time of writing than ever. Those listed instruments introduced earlier,

such as volatility futures launched in 1998 by Deutsche Terminb¨

orse (now Eurex), could not

attract enough liquidity and are now only a footnote in the nancial history books.

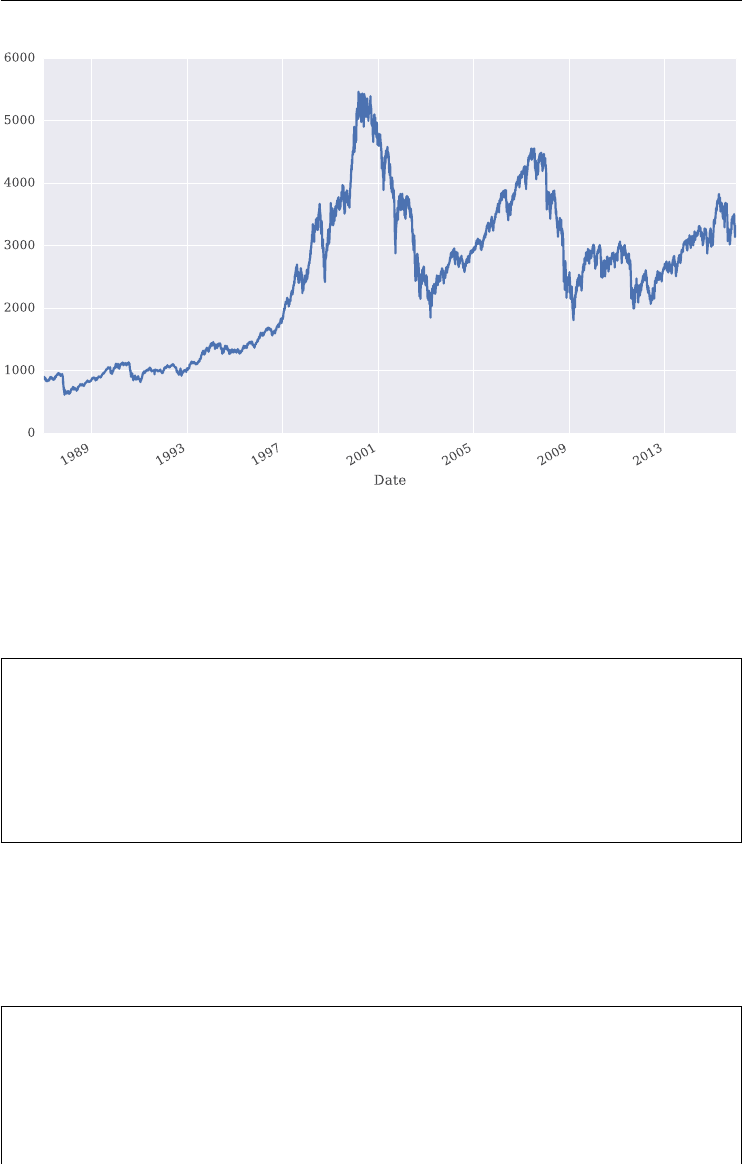

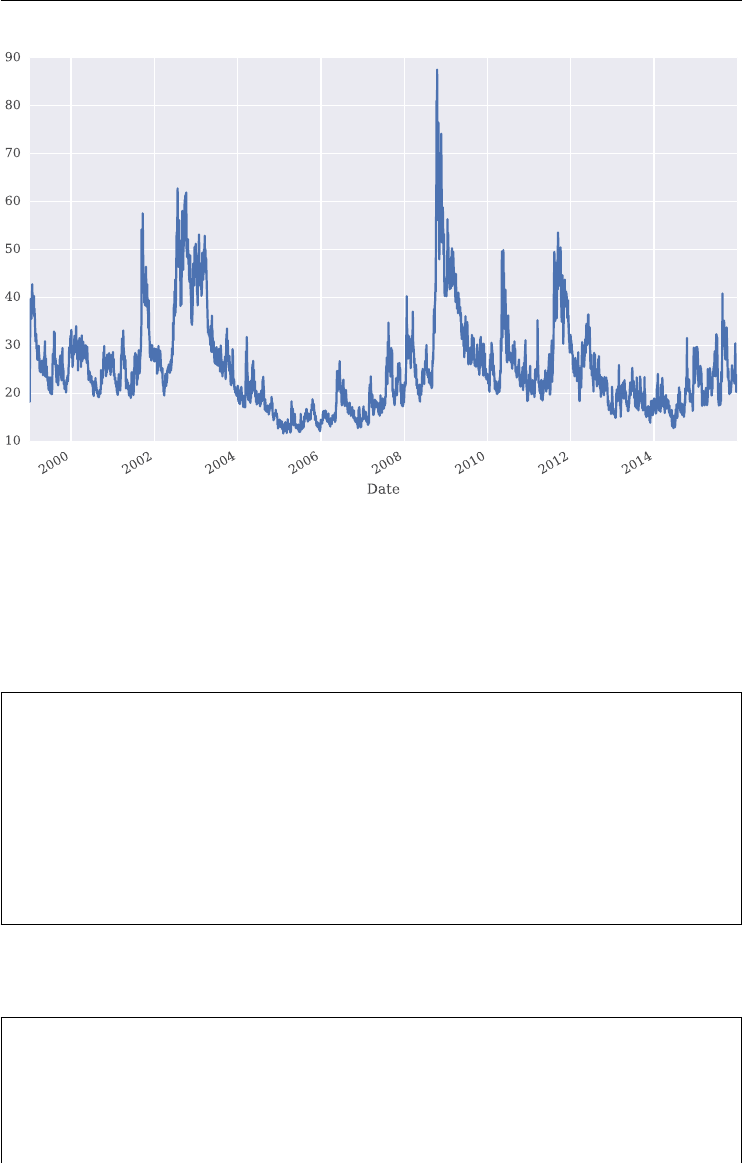

The volume of traded contracts on the VIX has risen sharply on average over recent years

as Figure 1.1 illustrates. The volume varies rather erratically and is inuenced inter alia by

seasonal effects and the general market environment (bullish or bearish sentiment).

In December 2012, the CBOE launched the S&P 500 variance futures contract –almost

20 years after their OTC counterparts started trading. After some early successes in building

liquidity in 2013, liquidity has dried up almost completely in 2014 and 2015.

1.3.2 The European History

Eurex – back then Deutsche Terminb¨

orse – introduced in 1994 the VDAX volatility index,an

index representing the 45 day implied volatility of DAX index options. As mentioned before,

Derivatives, Volatility and Variance 9

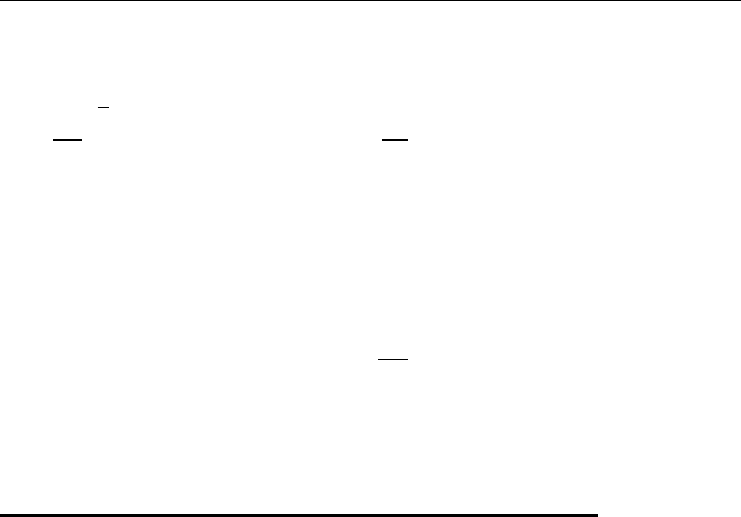

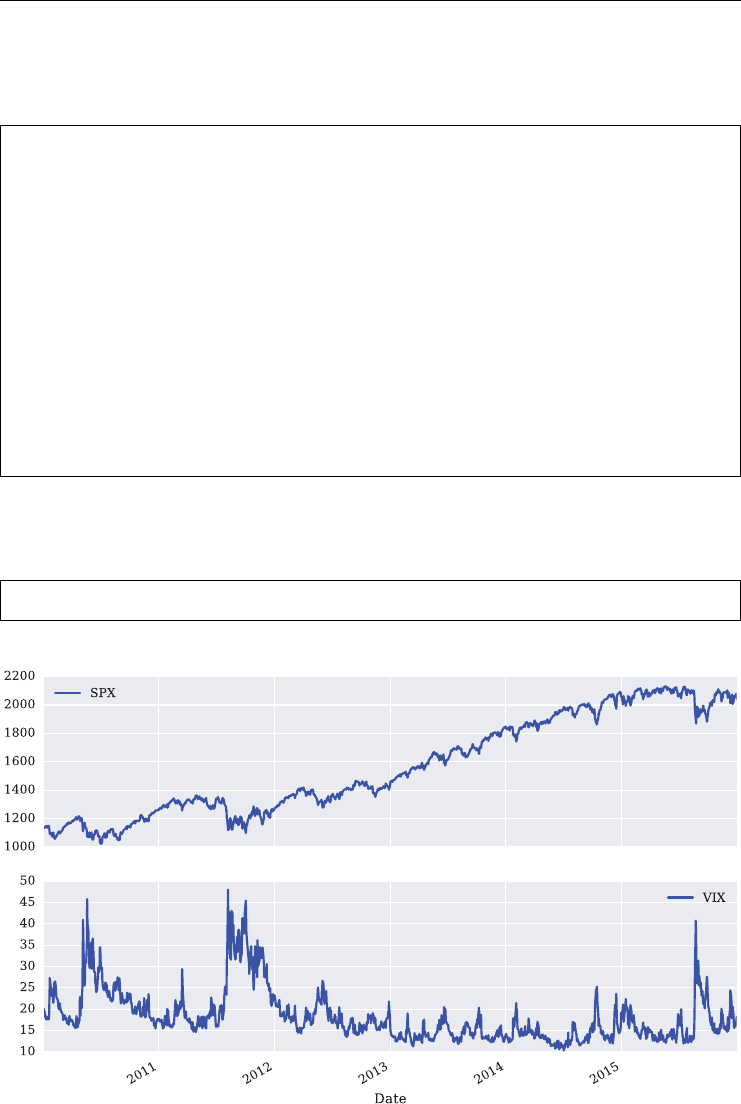

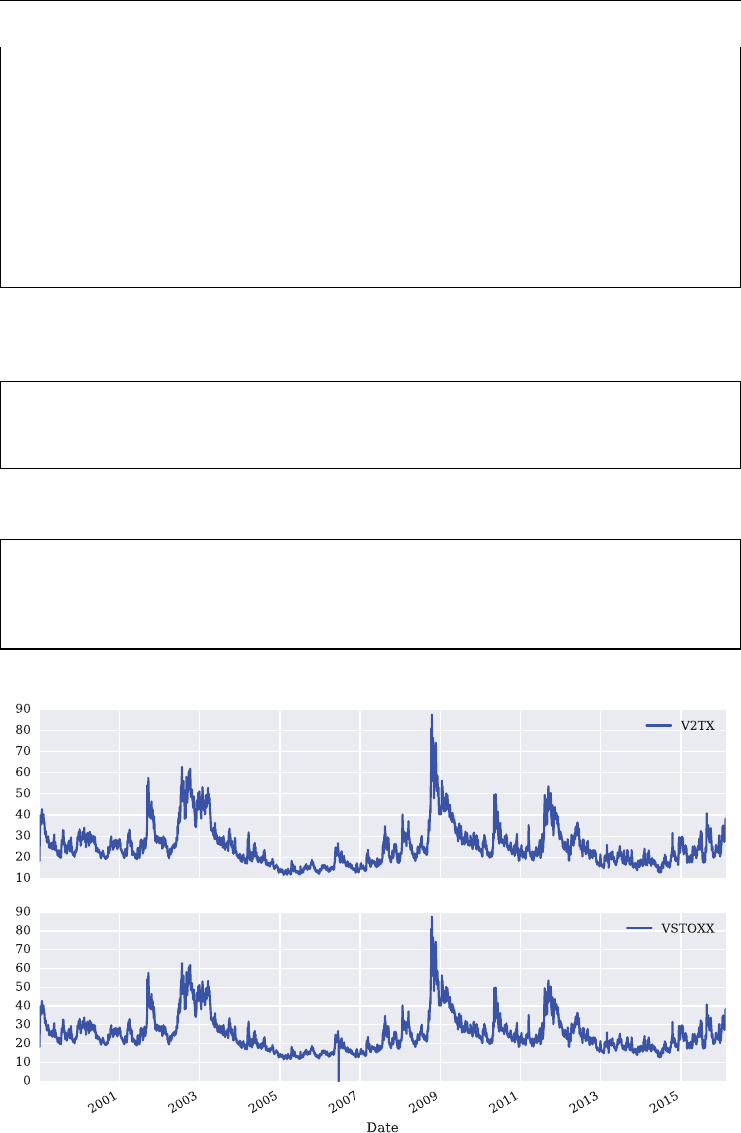

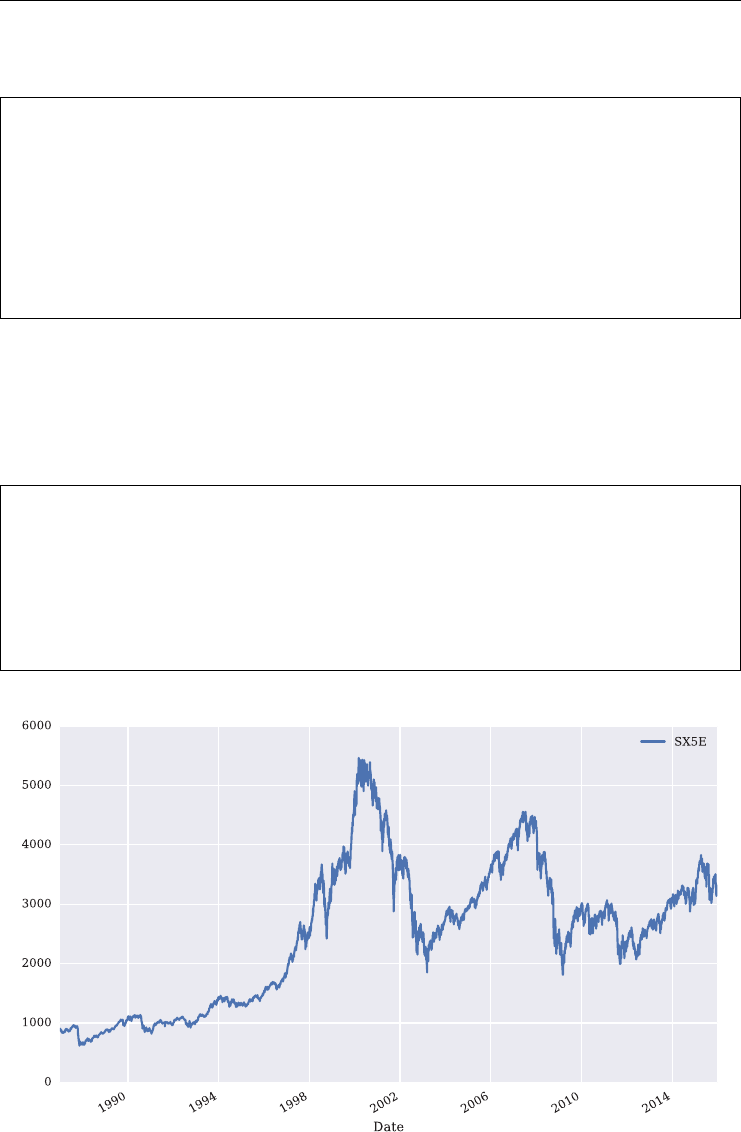

FIGURE 1.2 Historical daily closing levels for the VIX and the VSTOXX volatility indexes. Data

source: Yahoo! Finance and http://stoxx.com

in 1998 Eurex introduced futures on the VDAX which could, however, not attract enough

liquidity and were later delisted. In 2005, the methodolgy for calculating the index was also

changed to the more robust, model-free replication approach for variance swaps. The index

was renamed VDAX-NEW and a new futures contract on this index was introduced.

In 2005, Eurex also launched futures on the VSTOXX volatility index which is based on

options on the EURO STOXX 50 index and uses the by now standard methodology for volatil-

ity index calculation as laid out in CBOE (2003). In 2009 they were re-launched as “Mini

VSTOXX Futures” with the symbol FVS. At the same time, Eurex stopped the trading of

other volatility futures, such as those on the VDAX-NEW and the VSMI.

Since the launch of the new VSTOXX futures, they have attracted signicant liquidity and

are now actively traded. A major reason for this can be seen in the nancial crisis of 2007–2009

when volatility indexes saw their highest levels ever. This is illustrated in Figure 1.2 where the

maximum values for the VIX and VSTOXX are observed towards the end of 2008. This led

to a higher sensitivity of market participants to the risks that spikes in volatility can bring and

thus increased the demand for products to hedge against such adverse market environments.

Observe also in Figure 1.2 that the two indexes are positively correlated in general, over the

period shown with about +0.55.

In March 2010, Eurex introduced options on the VSTOXX index. These instruments also

attracted some liquidity and are at the time of writing actively traded. In September 2014,

Eurex then launched a variance futures contract on the EURO STOXX 50 index.

1.3.3 Volatility of Volatility Indexes

Nowadays, we are already one step further on. There are now indexes available that measure

the volatility of volatility (vol-vol). The so-called VVIX of the CBOE was introduced in March

10 LISTED VOLATILITY AND VARIANCE DERIVATIVES

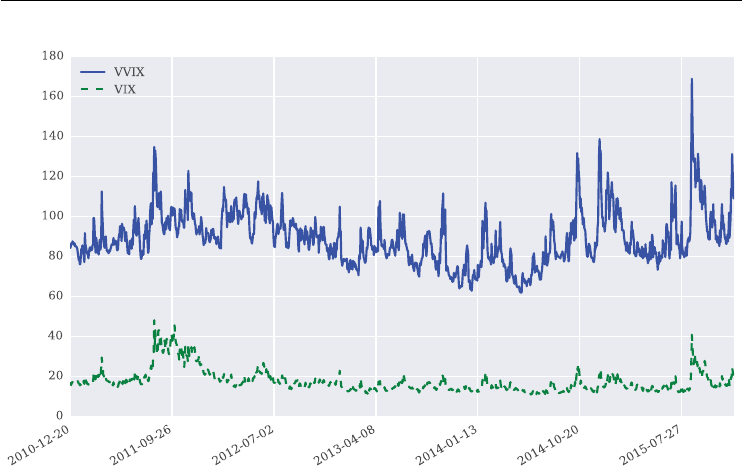

FIGURE 1.3 Historical daily closing levels for the VIX and the VVIX volatility (of volatility)

indexes. Data source: Thomson Reuters Eikon

2012. In October 2015 the index provider STOXX Limited introduced the V-VSTOXX indexes

which are described on www.stoxx.com as follows:

“The V-VSTOXX Indices are based on VSTOXX realtime options prices and are

designed to reect the market expectations of near-term up to long-term volatility-

of-volatility by measuring the square root of the implied variance across all options

of a given time to expiration.”

These new indexes and potential products written on them seem to be a benecial addition to

the volatility asset class. Such products might be used, for example, to hedge options written

on the volatility index itself since the vol-vol is stochastic in nature rather than constant or

deterministic.

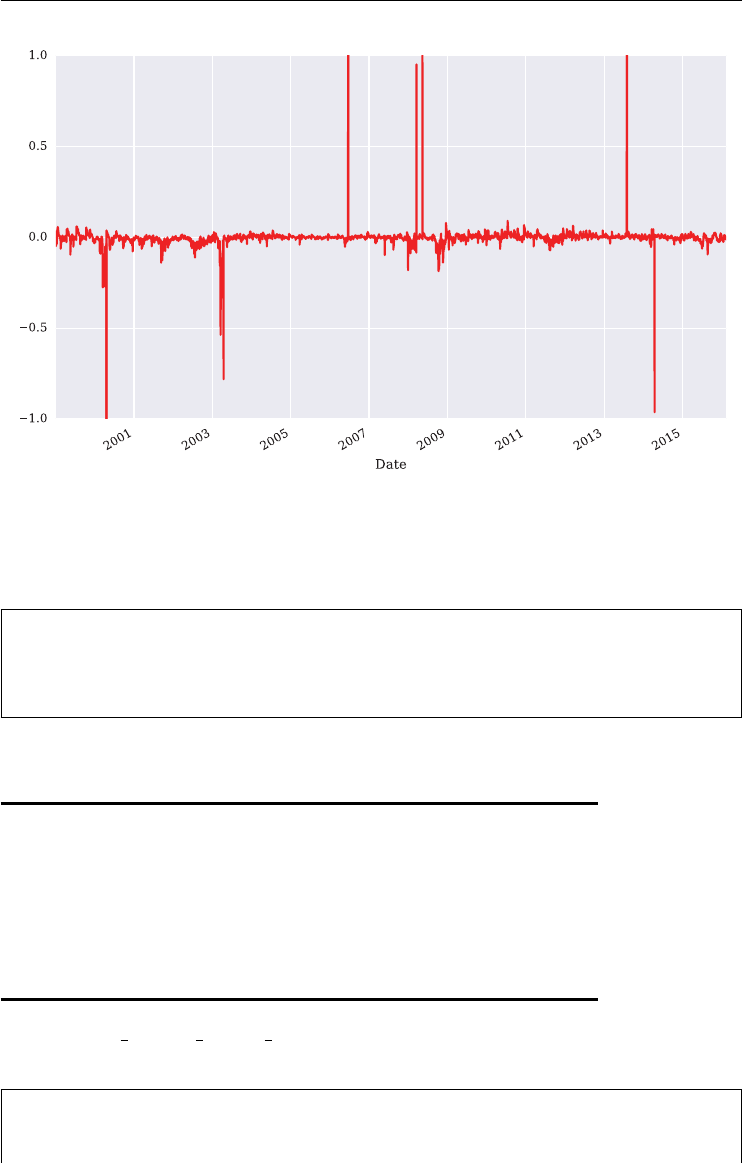

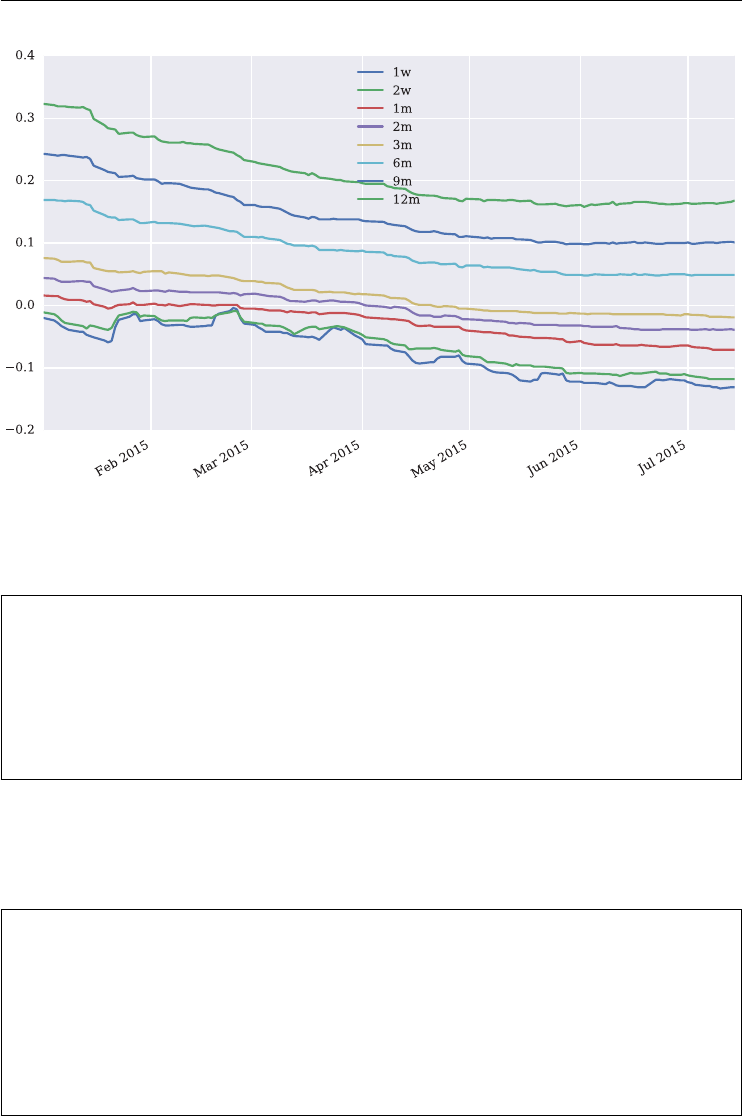

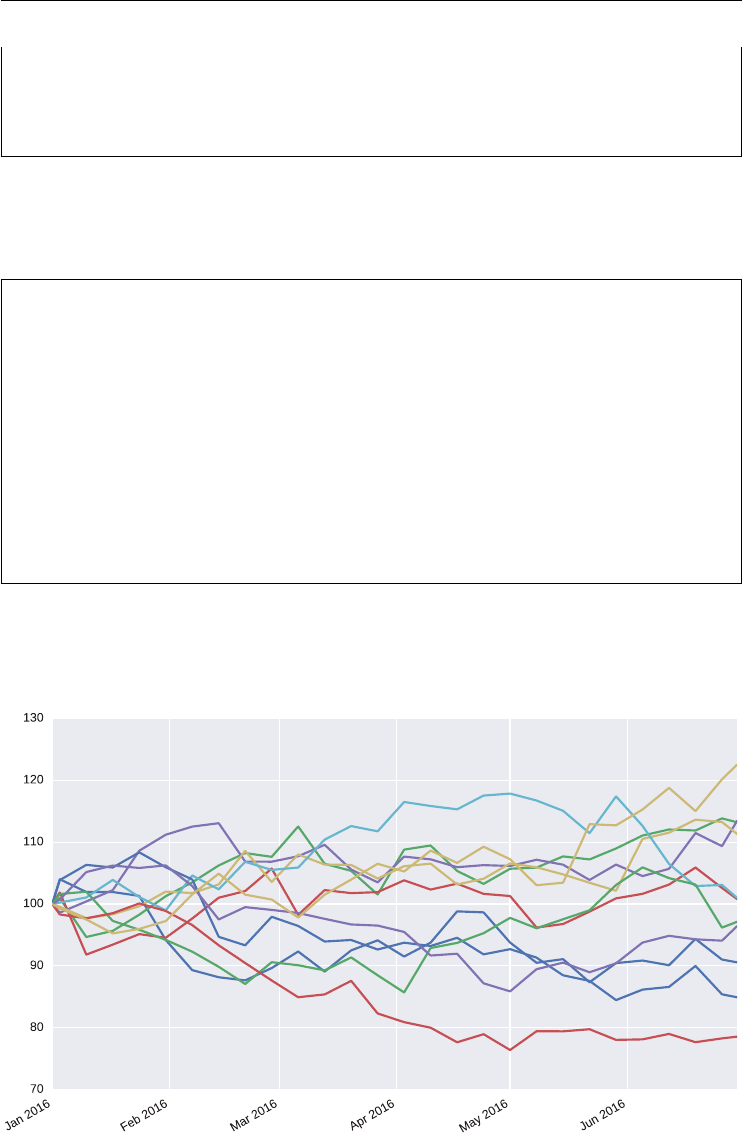

The VVIX index is generally on a much higher level than the VIX index as Figure 1.3

illustrates. This indicates a much higher volatility for the VIX index itself compared to the

S&P 500 volatility.

Over the period shown, the VVIX is highly positively correlated with the VIX at a level

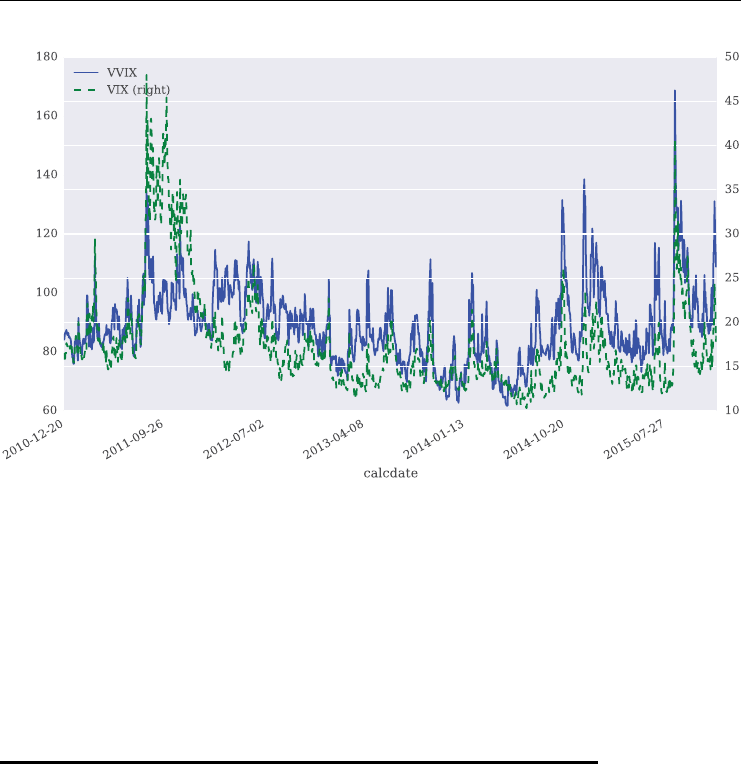

of about +0.66. Figure 1.4 plots the time series data for the two indexes on two different scales

to show this stylized fact graphically.

1.3.4 Products Covered in this Book

There is quite a diverse spectrum of volatility and variance futures available. Out of all possible

products, the focus of this book is on the European market and these instruments:

VSTOXX as a volatility index

VSTOXX futures

VSTOXX options

Eurex Variance Futures.

Derivatives, Volatility and Variance 11

FIGURE 1.4 Different scalings for the VVIX and VIX indexes to illustrate the positive correlation.

Data Source: Thomson Reuters Eikon

The majority of the material has originally been developed as part of the Eurex Advanced

Services. Although the focus is on Europe, the methods and approaches presented can usu-

ally be tranferred easily to the American landscape, for instance. This results from the fact

that some methodological unication has taken place over the past few years with regard to

volatility and variance related indexes and products.

1.4 VOLATILITY AND VARIANCE TRADING

This section discusses motives and rationales for trading listed volatility and variance deriva-

tives. It does not cover volatility (variance) trading strategies that can be implemented with,

for example, regular equity options (see Cohen (2005), ch. 4).

1.4.1 Volatility Trading

It is instructive to rst list characteristics of volatility indexes. We focus on the VSTOXX

and distinguish between facts (which follow from construction) and stylized facts (which are

supported by empirical evidence):

market expection (fact): the VSTOXX represents a 30 day implied volatility average

from out-of-the money options, i.e. the market consensus with regard to the “to be real-

ized” volatility over the next 30 days

non-tradable asset (fact): the VSTOXX itself is not directly tradable, only derivatives on

the VSTOXX can be traded

mean-reverting nature (fact): the VSTOXX index is mean-reverting, it does not show a

positive or negative drift over longer periods of time

12 LISTED VOLATILITY AND VARIANCE DERIVATIVES

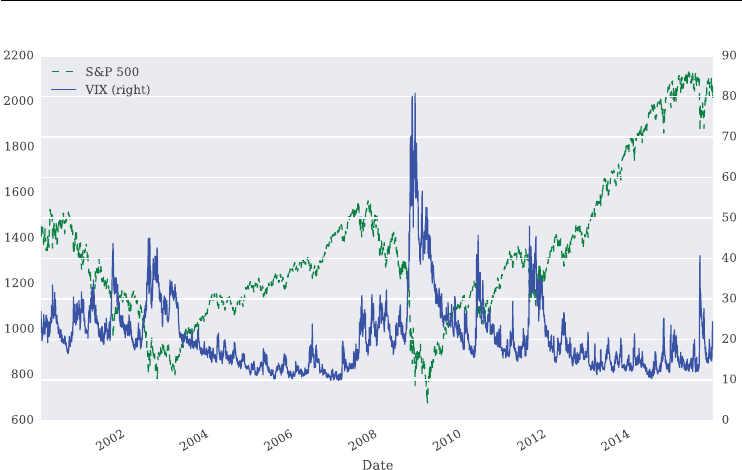

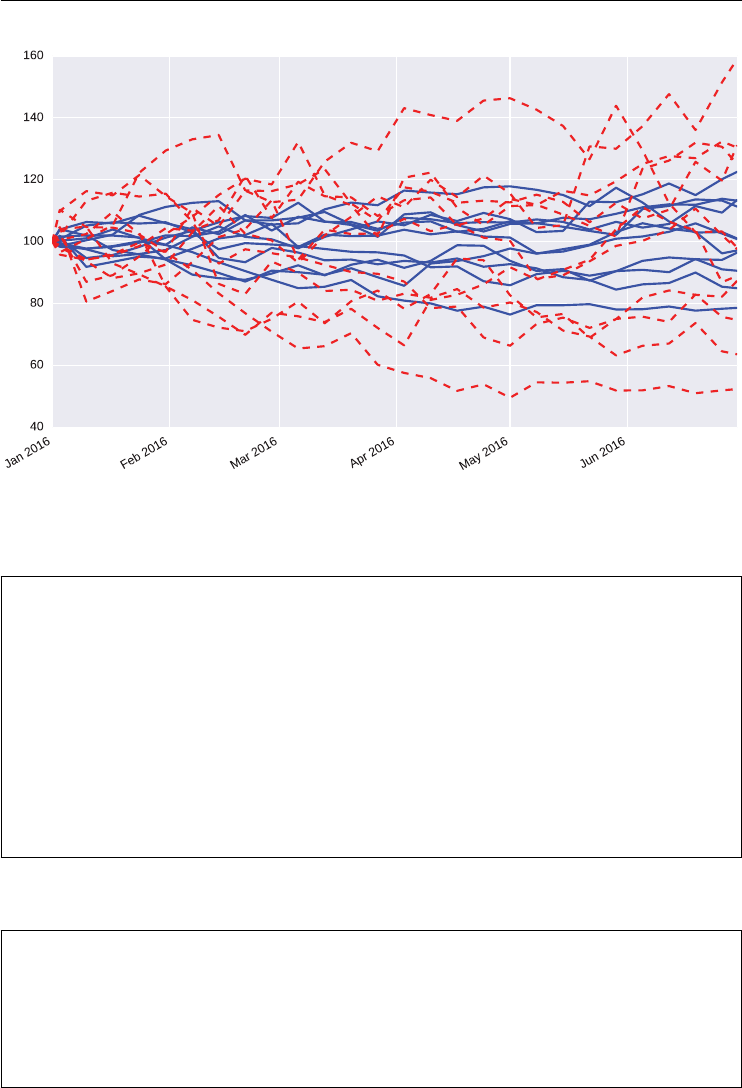

FIGURE 1.5 Different scalings for the S&P 500 and VIX indexes to illustrate the negative

correlation. Data source: Yahoo! Finance

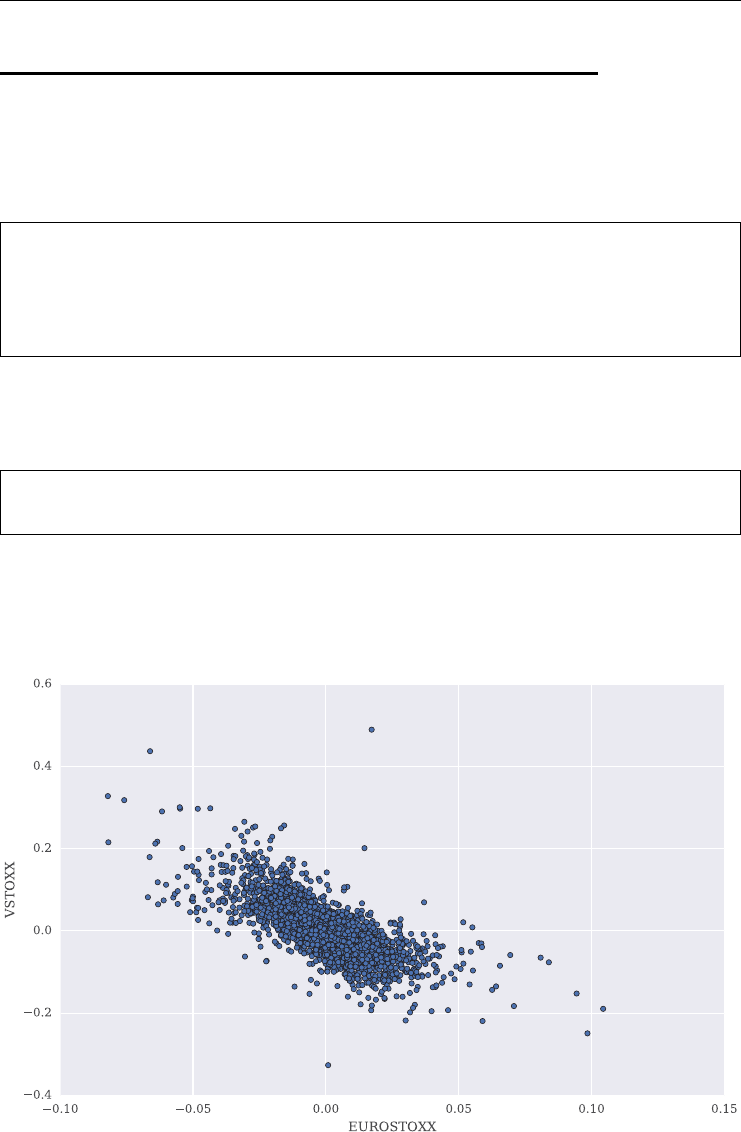

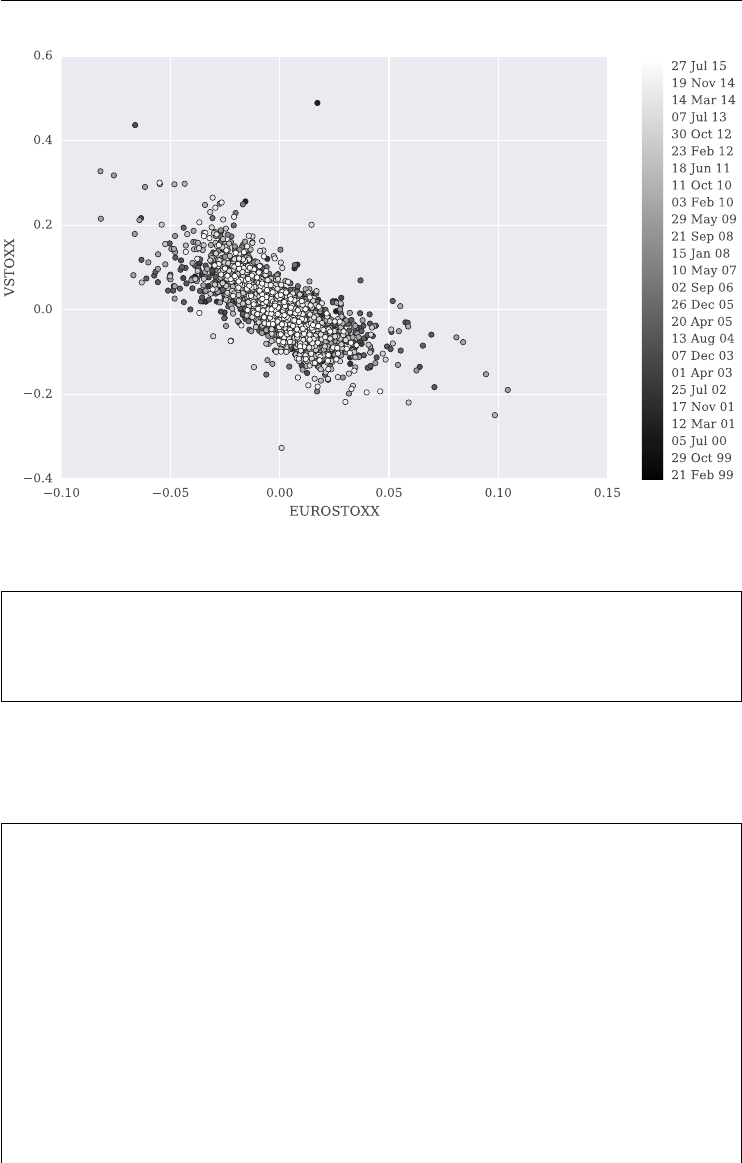

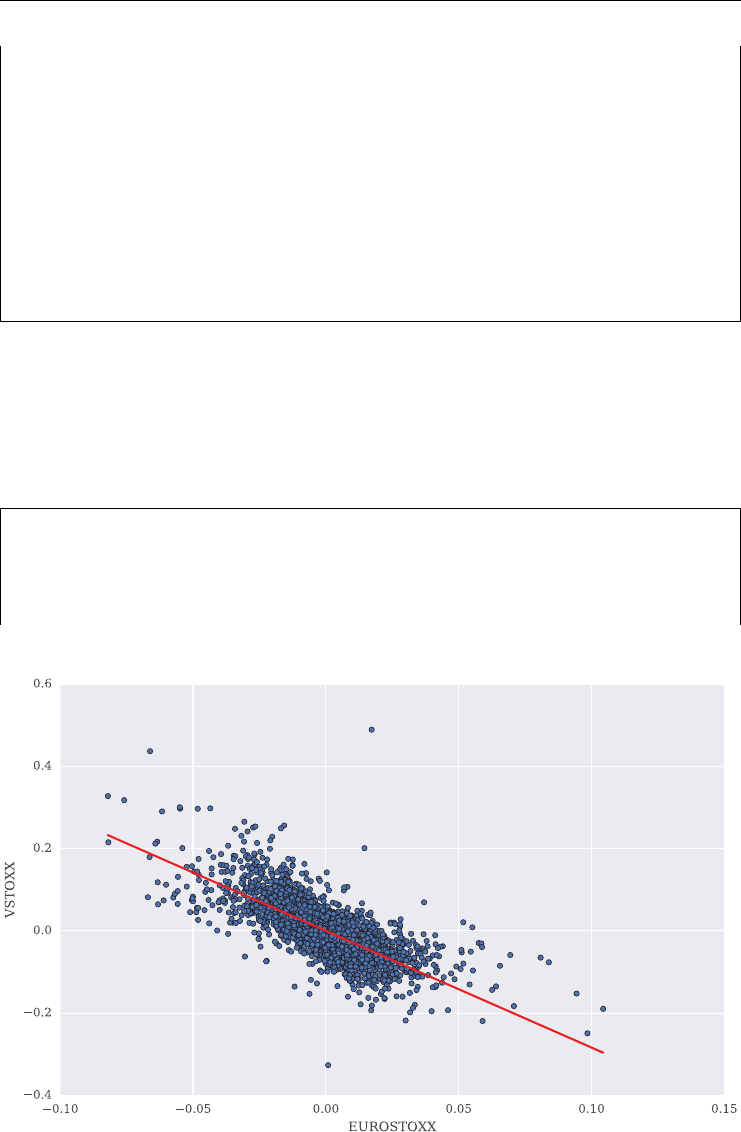

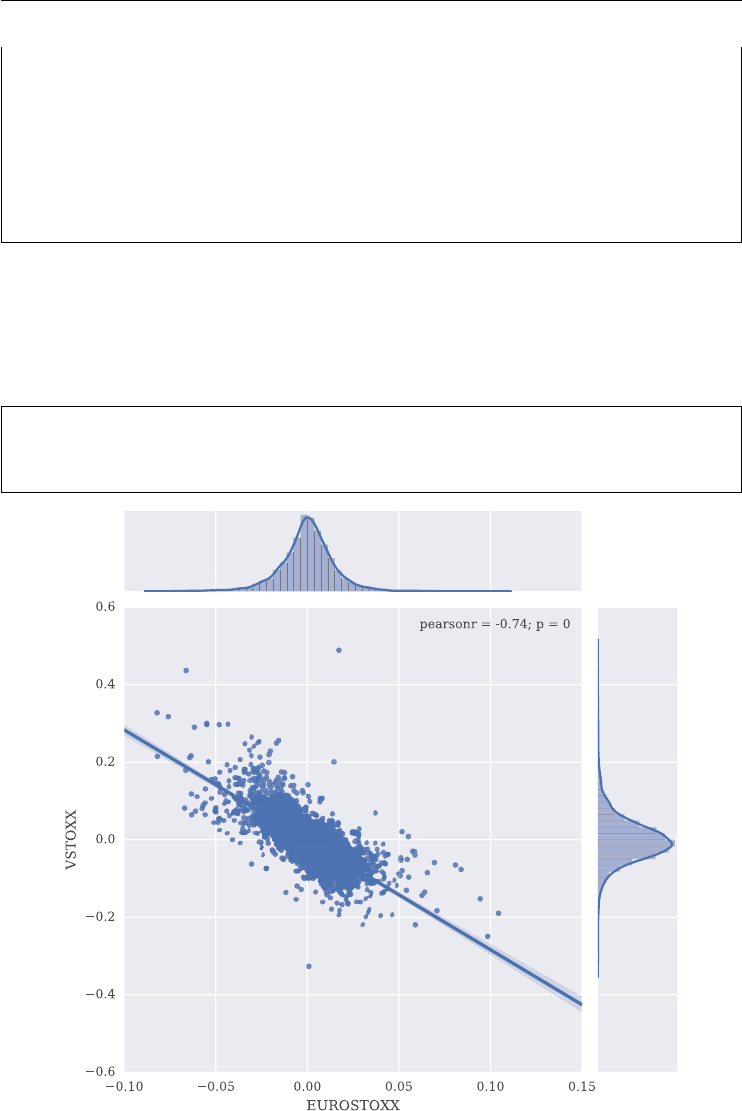

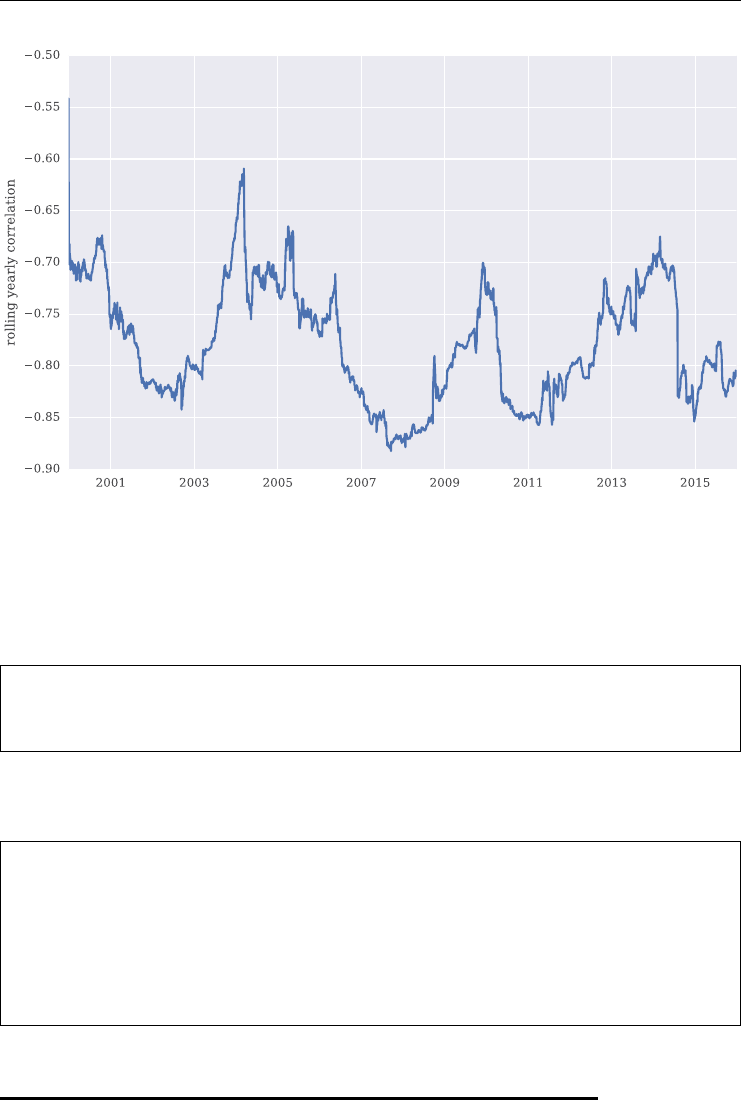

negative correlation (stylized fact): the VSTOXX is (on average) negatively correlated

with the respective equity index, the EURO STOXX 50

positive jumps (stylized fact): during times of stock market crisis, the VSTOXX can jump

to rather high levels; the mean reversion generally happens much more slowly

higher than realized volatility (stylized fact): on average, the VSTOXX index is higher

than the realized volatility over the next 30 days.

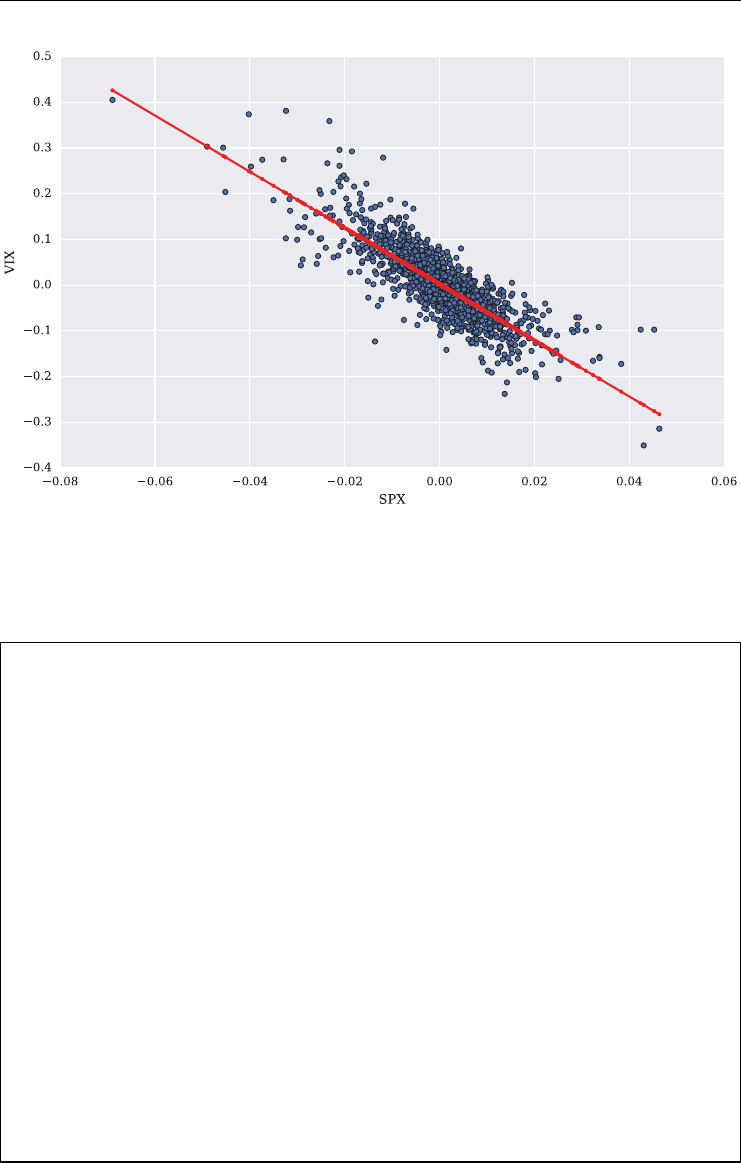

Figure 1.5 illustrates the negative correlation between the S&P 500 index and the VIX index

graphically. Over the period shown, the correlation is about −0.75.

The value of a VSTOXX future represents the (market) expectation with regard to the

future value of the VSTOXX at the maturity date of the future. Given this background, typical

volatility trading strategies involving futures include the following:

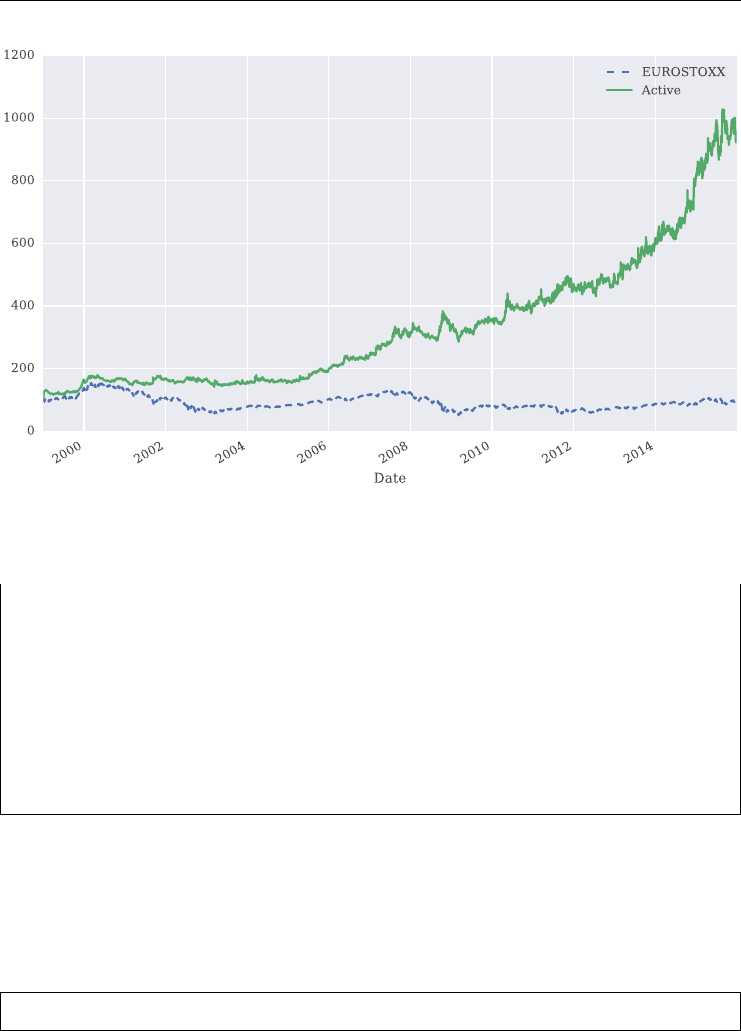

long VSTOXX future: such a position can be used to hedge equity positions (due to the

negative correlation with the EURO STOXX 50) or to increase returns of an equity port-

folio (e.g. through a constant-proportion investment strategy, see chapter 4, Data Analysis

and Strategies); it can also be used to hedge a short realized volatility strategy

short VSTOXX future: such a trade can be entered, for example, when the VSTOXX

spikes and the expectation is that it will revert (fast enough) to its mean; it might also

serve to reduce vega exposure in long vega option portfolios

term structure arbitrage: for example, shorting the front month futures contract and

going long the nearby futures contract represents a typical term structure arbitrage strategy

when the term structure is in contango; this is due to different carries associated with

different futures contracts and maturities, respectively

Derivatives, Volatility and Variance 13

relative value arbitrage: VSTOXX futures can also be traded against other volatility/-

variance sensitive instruments and positions, like OTC variance swaps, equity options

portfolios, etc.

Similar and other strategies can be implemented involving VSTOXX options. With regard to

exercise they are European in nature and can be delta hedged by using VSTOXX futures which

is yet another motive for trading in futures. Typical trading strategies involving VSTOXX

options are:

long OTM calls: such a position might protect an equity portfolio from losses due to a

market crash (again due to the negative correlation between VSTOXX and EURO STOXX

50)

short ATM calls: writing ATM calls, and pocketing the option premium, might be attrac-

tive when the current implied volatility levels are relatively high

long ATM straddle: buying put and call options on the VSTOXX with same (ATM) strike

and maturity yields a prot when the VSTOXX moves fast enough in one direction; this

is typically to be expected when the volatility of volatility (vol-vol) is high.

For both VSTOXX futures and options many other strategies can be implemented that exploit

some special situation (e.g. contango or backwardation in the futures prices) or reect a certain

expectation of the trader (e.g. that realized volatility will be lower/higher than the implied/

expected volatility).

1.4.2 Variance Trading

The motives and rationales for trading in EURO STOXX 50 variance futures are not too dif-

ferent from those involving VSTOXX derivatives (see Bossu et al. (2005)). Typical strategies

include:

long variance future: this position benets when the realized variance is higher than

the variance strike (implied variance at inception); it might also be used to hedge equity

portfolio risks or short vega options positions

short variance future: this position benets when the realized variance is below the vari-

ance strike which tends to be the case on average; it can also hedge a long vega options

position

forward volatility/variance trading: since variance is additive over time (which volatil-

ity is not), one can get a perfect exposure to forward implied volatility by, for exam-

ple, shorting the September variance future and going long the October contract; this

gives an exposure to the forward implied volatility from September maturity to October

maturity

correlation trading: variance futures can be traded to exploit (statistical) arbitrage oppor-

tunities between, for example, the (implied) variance of an equity index and its compo-

nents or the (implied) variance of one equity index versus another one; in both cases, the

rationale is generally based on the correlation of the different assets and their variance,

respectively.

14 LISTED VOLATILITY AND VARIANCE DERIVATIVES

1.5 PYTHON AS OUR TOOL OF CHOICE

There are some general reasons why Python is a good choice for computational nance and

nancial data science these days. Among others, these are:

open source: Python is open source and can be used by students and big nancial insti-

tutions alike for free

syntax: Python’s readable and concise syntax make it a good choice for presenting formal

concepts, like those in nance

ecosystem: compared to other languages Python has an excellent ecosystem of libraries

and packages that are useful for data analytics and scientic computing in general and

nancial analytics in particular

performance: in recent years, the ecosystem of Python has grown especially in the

area of performance libraries, making it much easier to get to computing speeds more

than sufcient for the most computationally demanding algorithms, such as Monte Carlo

simulation

adoption: at the time of writing, Python has established itself as a core technology at

major nancial institutions, be it leading investment banks, big hedge funds or more tra-

ditional asset management rms

career: given the widespread adoption of Python, learning and mastering the language

seems like a good career move for everybody working in the industry or planning to

do so.

In view of the scope and style of the book, one special feature is noteworthy:

interactivity: the majority of the code examples presented in this book can be executed

in interactive fashion within the Jupyter Notebook environment (see http://jupyter.org);

in this regard, Python has a major advantage as an interpreted language compared to a

compiled one with its typical edit-compile-run cycle.

Chapter 1 of Hilpisch (2014) provides a more detailed overview of aspects related to

Python for Finance. All the code presented in this book is available via resources listed

under http://lvvd.tpq.io, especially on the Quant Platform for which you can register under

http://lvvd.quant-platform.com.

1.6 QUICK GUIDE THROUGH THE REST OF THE BOOK

The remainder of this introductory part of the book is organized as follows:

chapter 2: this chapter introduces Python as a technology platform for (interactive) nan-

cial analytics; a more detailed account of Python for Finance is provided in Hilpisch

(2014)

chapter 3: this chapter presents the model-free replication approach for variance; it is

important for both volatility indexes and derivatives written on them as well as for variance

futures.

Derivatives, Volatility and Variance 15

The second part of the book is about the VSTOXX and listed volatility derivatives. It comprises

the following chapters:

chapter 4: as a starting point, chapter 4 uses Python to analyze historical data for the

VSTOXX and EURO STOXX 50 indexes; a focal point is the analysis of some simple

trading strategies involving the VSTOXX

chapter 5: using the model-free replication approach for variance, this chapter shows in

detail how the VSTOXX index is calculated and how to use Python to (re-)calculate it

using raw option data as input

chapter 6:Gr

¨

unbichler and Longstaff (1996) were among the rst to propose a parame-

terized model to value futures and options on volatility indexes; chapter 6 presents their

model which is based on a square-root diffusion process and shows how to simulate and

calibrate it to volatility option market quotes

chapter 7: building on chapter 6, chapter 7 presents a more sophisticated framework – a

deterministic shift square-root jump diffusion (SRJD) process – to model the VSTOXX

index and to better capture the implied volatility smiles and volatility term structure

observed in the market; the exposition is slightly more formal compared to the rest of

the book

chapter 8: this brief chapter discusses terms of the VSTOXX volatility index as well as

the futures and options traded on the VSTOXX.

Part three of the book is about the Eurex Variance Futures contract as listed in September 2014.

This part comprises three chapters:

chapter 9: listed variance futures are mainly based on the popular OTC variance swap

contracts with some differences introduced by intraday trading; chapter 9 therefore cov-

ers variance swaps in some detail and also discusses differences between variance and

volatility as an underlying asset

chapter 10: this chapter provides a detailed discussion of all concepts related to the listed

Eurex Variance Futures contract and shows how to (re-)calculate its value given historical

data; it also features a comparison between the futures contract and a respective OTC

variance swap contract

chapter 11: this chapter discusses all those special characteristics of the Eurex Variance

Futures when it comes to (intraday) trading and settlement.

Part four of the book focuses on the DX Analytics nancial library (see http://dx-

analytics.com) to model the VSTOXX index and to calibrate different models to VSTOXX

options quotes. It consists of three chapters:

chapter 12: this chapter introduces basic concepts and API elements of the DX Analytics

library

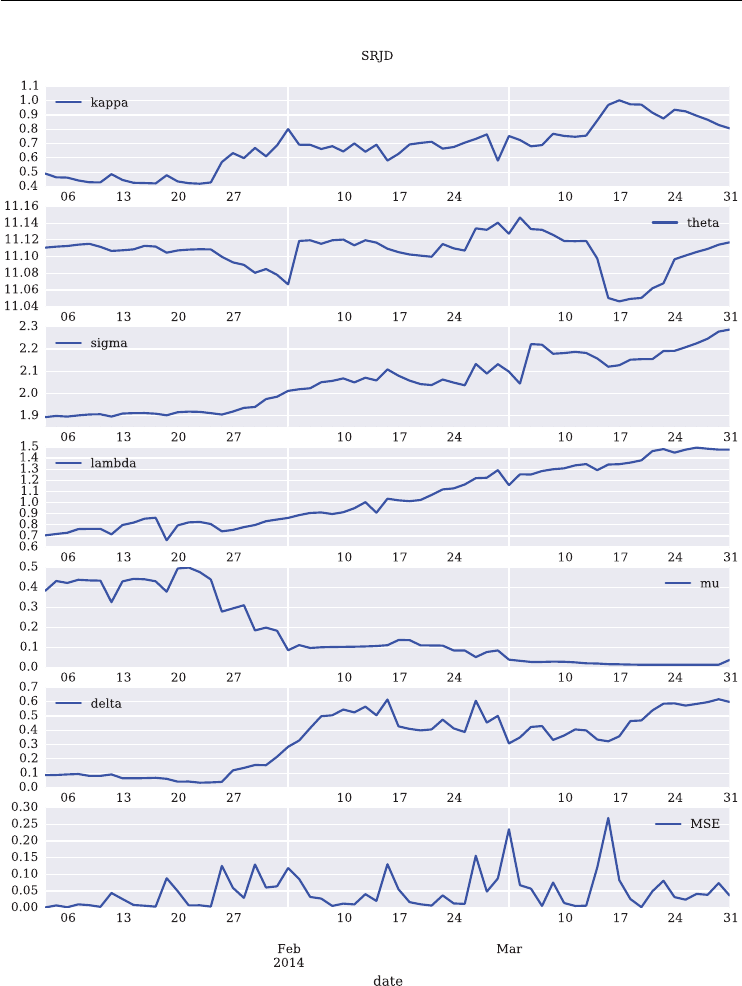

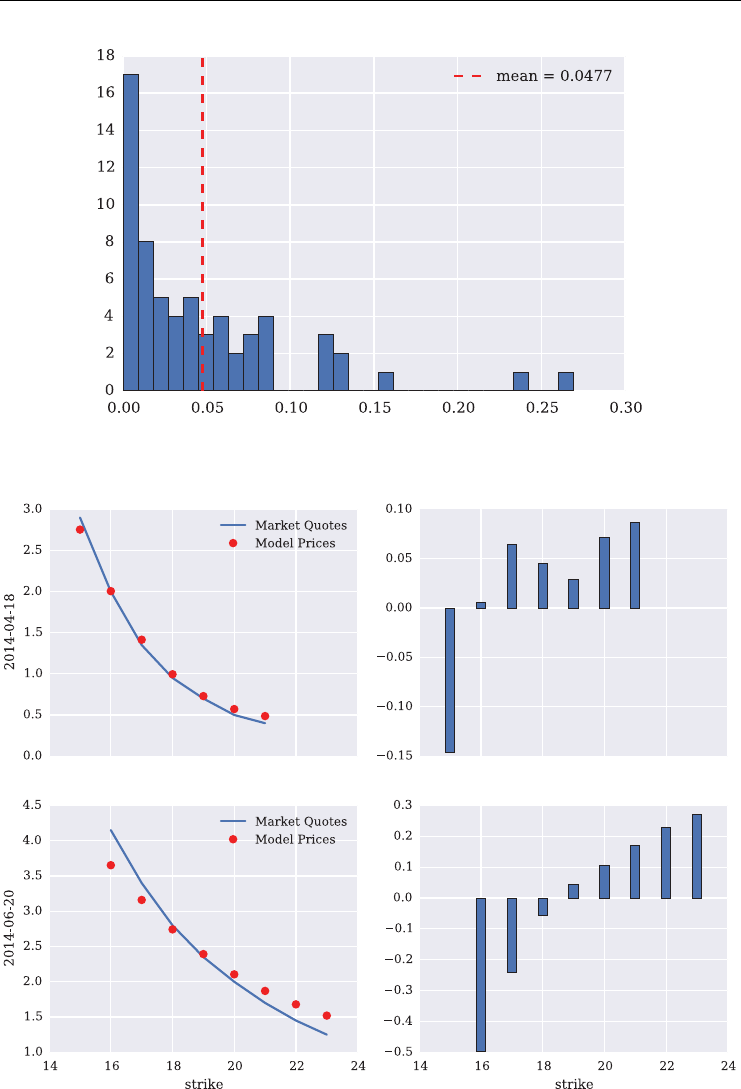

chapter 13: using the square-root diffusion model as introduced in chapter 6, this chapter

implements a calibration study to a single maturity of VSTOXX options over the rst

quarter of 2014

chapter 14: chapter 14 replicates the same calibration study but in a more sophisticated

fashion; it calibrates the deterministic shift square-root jump diffusion process not only

to a single maturity of options but to as many as ve simultaneously.

CHAPTER 2

Introduction to Python

Python has become a powerful programming language and has developed a huge ecosystem

of helpful libraries over the last couple of years. This chapter provides a concise overview

of Python and two of the major pillars of the the so-called scientic stack:

NumPy (see http://numpy.scipy.org)

pandas (see http://pandas.pydata.org)

NumPy provides performant array operations on numerical data while pandas is specif-

ically designed to handle more complex data analytics operations, e.g. on (nancial) times

series data.

Such an introductory chapter – only addressing selected topics relevant to the contents

of this book – can of course not replace a thorough introduction to Python and the libraries

covered. However, if you are rather new to Python or programming in general you might get

a rst overview and a feeling of what Python is all about. If you are already experienced in

another language typically used in quantitative nance (e.g. Matlab, R, C++, VBA), you see

what typical data structures, programming paradigms and idioms in Python look like.

For a comprehensive overview of Python applied to nance see Hilpisch (2014). Other,

more general introductions to the language with a scientic and data analysis focus are Haenel

et al. (2013), Langtangen (2009) and McKinney (2012).

This chapter and the rest of the book is based on Python 2.7 although the majority of the

code should be easily transformed to Python 3.5 after some minor modications.

2.1 PYTHON BASICS

This section introduces basic Python data types and structures, control structures and some

Python idioms.

2.1.1 Data Types

It is noteworthy that Python is a dynamically typed system which means that types of objects

are inferred from their contexts. Let us start with numbers.

17

Listed Volatility and Variance Derivatives: A

Python-based Guide

By Dr. Yves J. Hilpisch

© 2017 Yves Hilpisch

18 LISTED VOLATILITY AND VARIANCE DERIVATIVES

In [1]: a=3 # defining an integer object

In [2]: type(a)

Out[2]: int

In [3]: a.bit_length() # number of bits used

Out[3]: 2

In [4]: b=5. # defining a float object

In [5]: type(b)

Out[5]: float

Python can handle arbitrarily large integers which is quite benecial for number of theoretical

applications, for instance:

In [6]: c = 10 ** 100 # googol number

In [7]: type(c)

Out[7]: long

In [8]: c# long integer object

Out[8]: 1000000000000000000000000000000000000000000000000000000000000000

0000000000000000000000000000000000000L

In [9]: c.bit_length() # number of bits used

Out[9]: 333

Arithmetic operations on these objects work as expected.

In [10]: 3/5. # division

Out[10]: 0.6

In [11]: a*b # multiplication

Out[11]: 15.0

In [12]: a-b # difference

Out[12]: -2.0

In [13]: b+a # addition

Out[13]: 8.0

In [14]: a**b # power

Out[14]: 243.0

Introduction to Python 19

However, be aware of the oor division which is standard in Python 2.7.

In [15]: 3/5 # int type inferred => floor division

Out[15]: 0

Many often used mathematical functions are found in the math module which is part of

Python’s standard library.

In [16]: import math # importing the library into the namespace

In [17]: math.log(a) # natural logarithm

Out[17]: 1.0986122886681098

In [18]: math.exp(a) # exponential function

Out[18]: 20.085536923187668

In [19]: math.sin(b) # sine function

Out[19]: -0.9589242746631385

Another important basic data type is string objects.

In [20]: s = 'Listed Volatility and Variance Derivatives.'

In [21]: type(s)

Out[21]: str

This object type has multiple methods attached.

In [22]: s.lower() # converting to lower case characters

Out[22]: 'listed volatility and variance derivatives.'

In [23]: s.upper() # converting to upper case characters

Out[23]: 'LISTED VOLATILITY AND VARIANCE DERIVATIVES.'

String objects can be easily sliced. Note that Python has in general zero-based numbering and

indexing.

In [24]: s[0:6]

Out[24]: 'Listed'

20 LISTED VOLATILITY AND VARIANCE DERIVATIVES

Such objects can also be combined using the +operator. The index value -1 represents the last

character of a string (or last element of a sequence in general).

In [25]: st = s[0:6] + s[-13:-1]

In [26]: print st

Listed Derivatives

String replacements are often used to parametrize text output.

In [27]: repl = "My name is %s,Iam%d years old and %4.2f m tall."

# replace %s by a string, %d by an integer and

# %4.2f by a float showing 2 decimal values

In [28]: print repl % ('Peter', 35, 1.88)

My name is Peter, I am 35 years old and 1.88 m tall.

A different way to reach the same goal is the following:

In [29]: repl = "My name is {:s}, I am {:d} years old and {:4.2f} m tall."

In [30]: print repl.format('Peter', 35, 1.88)

My name is Peter, I am 35 years old and 1.88 m tall.

2.1.2 Data Structures

A lightweight data structure is tuples. These are immutable collections of other objects and

are constucted by objects separated by commas – with or without parentheses.

In [31]: t1 = (a, b, st)

In [32]: t1

Out[32]: (3, 5.0, 'Listed Derivatives')

In [33]: type(t1)

Out[33]: tuple

In [34]: t2 = st, b, a

In [35]: t2

Out[35]: ('Listed Derivatives', 5.0, 3)

In [36]: type(t2)

Out[36]: tuple

Introduction to Python 21

Nested structures are also possible.

In [37]: t = (t1, t2)

In [38]: t

Out[38]: ((3, 5.0, 'Listed Derivatives'), ('Listed Derivatives', 5.0, 3))

In [39]: t[0][2] # take 3rd element of 1st element

Out[39]: 'Listed Derivatives'

List objects are mutable collections of other objects and are generally constructed by providing

a comma separated collection of objects in brackets.

In [40]: l = [a, b, st]

In [41]: l

Out[41]: [3, 5.0, 'Listed Derivatives']

In [42]: type(l)

Out[42]: list

In [43]: l.append(s.split()[3]) # append 4th word of string

In [44]: l

Out[44]: [3, 5.0, 'Listed Derivatives', 'Variance']

Sorting is a typical operation on list objects which can also be constructed using the list

constructor (here applied to a tuple object).

In [45]: l = list(('Z', 'Q', 'D', 'J', 'E', 'H', 5., a))

In [46]: l

Out[46]: ['Z', 'Q', 'D', 'J', 'E', 'H', 5.0, 3]

In [47]: l.sort() # in-place sorting

In [48]: l

Out[48]: [3, 5.0, 'D', 'E', 'H', 'J', 'Q', 'Z']

Dictionary objects are so-called key-value stores and are generally constructed with curly

brackets.

22 LISTED VOLATILITY AND VARIANCE DERIVATIVES

In [49]: d = {'int_obj': a,

....: 'float_obj': b,

....: 'string_obj': st}

....:

In [50]: type(d)

Out[50]: dict

In [51]: d

Out[51]: {'float_obj': 5.0, 'int_obj': 3, 'string_obj': 'Listed Derivatives'}

In [52]: d['float_obj'] # look-up of value given key

Out[52]: 5.0

In [53]: d['long_obj'] = c / 10 ** 90 # adding new key value pair

In [54]: d

Out[54]:

{'float_obj': 5.0,

'int_obj': 3,

'long_obj': 10000000000L,

'string_obj': 'Listed Derivatives'}

Keys and values of a dictionary object can be retrieved as list objects.

In [55]: d.keys()

Out[55]: ['long_obj', 'int_obj', 'float_obj', 'string_obj']

In [56]: d.values()

Out[56]: [10000000000L, 3, 5.0, 'Listed Derivatives']

2.1.3 Control Structures

Iterations are very important operations in programming in general and nancial analytics in

particular. Many Python objects are iterable which proves rather convenient in many circum-

stances. Consider the special list object constructor range.

In [57]: range(5) # all integers from zero to 5 excluded

Out[57]: [0, 1, 2, 3, 4]

In [58]: range(3, 15, 2) # start at 3, step with 2 until 15 excluded

Out[58]: [3, 5, 7, 9, 11, 13]

Introduction to Python 23

Such a list object constructor is often used in the context of a for loop.

In [59]: for iin range(5):

....: print i**2,

....:

014916

However, you can iterate over any sequence.

# iteration over list object

In [60]: for _in l:

....: print _,

....:

35.0DEHJQZ

# iteration over string object

In [61]: for cin st:

....: print c + '|',

....:

L|i|s|t|e|d||D|e|r|i|v|a|t|i|v|e|s|

while loops are similar to their counterparts in other languages.

In [62]: i=0 # initialize counter

In [63]: while i<5:

....: print i ** 0.5, # output

....: i+=1 # increase counter by 1

....:

0.0 1.0 1.41421356237 1.73205080757 2.0

The if-elif-else control structure is introduced below in the context of Python function

denitions.

2.1.4 Special Python Idioms

Python relies in many places on a number of special idioms. Let us start with a rather popular

one, the list comprehension.

In [64]: lc=[i**2for iin range(10)]

In [65]: lc

Out[65]: [0, 1, 4, 9, 16, 25, 36, 49, 64, 81]

24 LISTED VOLATILITY AND VARIANCE DERIVATIVES

As the name suggests, the result is a list object.

In [66]: type(lc)

Out[66]: list

So-called lambda or anonymous functions are useful helpers in many places.

In [67]: f=lambda x: math.cos(x) # returns cos of x

In [68]: f(5)

Out[68]: 0.28366218546322625

List comprehensions can be combined with lambda functions to achieve concise constructions

of list objects.

In [69]: lc = [f(x) for xin range(10)]

In [70]: lc

Out[70]:

[1.0,

0.5403023058681398,

-0.4161468365471424,

-0.9899924966004454,

-0.6536436208636119,

0.28366218546322625,

0.960170286650366,

0.7539022543433046,

-0.14550003380861354,

-0.9111302618846769]

However, there is an even more concise way of constructing the same list object – using func-

tional programming approaches, in the following case with map.

In [71]: map(lambda x: math.cos(x), range(10))

Out[71]:

[1.0,

0.5403023058681398,

-0.4161468365471424,

-0.9899924966004454,

-0.6536436208636119,

0.28366218546322625,

0.960170286650366,

0.7539022543433046,

-0.14550003380861354,

-0.9111302618846769]

Introduction to Python 25

In general, one works with regular Python functions (as opposed to lambda functions) which

are constructed as follows:

In [72]: def f(x):

....: return math.exp(x)

....:

The general construction looks like this:

In [73]: def f(*args): # multiple arguments

....: for arg in args:

....: print arg

....: return None # return result(s) (not necessary)

....:

In [74]: f(l)

[3, 5.0, 'D', 'E', 'H', 'J', 'Q', 'Z']

Consider the following function denition which returns different values/strings based on an

if-elif-else control structure:

In [75]: import random # import random number library

In [76]: a = random.randint(0, 999) # draw random number between 0 and 999

In [77]: print "Random number is %d"%a

Random number is 627

In [78]: def number_decide(number):

....: if a < 10:

....: return "Number is single digit."

....: elif 10 <= a < 100:

....: return "Number is double digit."

....: else:

....: return "Number is triple digit."

....: number_decide(a)

....:

Out[78]: 'Number is triple digit.'

A specialty of Python is generator objects. One constructor for such objects that is commonly

used is xrange.

26 LISTED VOLATILITY AND VARIANCE DERIVATIVES

In [79]: g = xrange(10)

In [80]: type(g) # object type

Out[80]: xrange

In [81]: g# object instance

Out[81]: xrange(10)

In [82]: for _in g:

....: print _, # integers are "generated" when needed

....:

0123456789

Generator objects can in many scenarios replace (typical) list objects and have the major advan-

tage that they are in general much more memory efcient. Consider a nancial algorithm that

requires 10 mn loops. Iterating over a list of integers from 0 to 9,999,999 is not efcient since

the algorithm (in general) does not need to have all these numbers available at the same time.

But this is what happens when using range for such a loop.

Consider the following construction of the respective list object containing all integers:

In [83]: %time r = range(10000000)

CPU times: user 87.4 ms, sys: 211 ms, total: 299 ms

Wall time: 299 ms

This object consumes 80 MB (!) of RAM (10 mn times 8 bytes).

In [84]: import sys

In [85]: sys.getsizeof(r) # size in bytes of object

Out[85]: 80000072

On the other hand, consider the analogous construction based on a generator (xrange) object.

It is much, much faster since no memory has to be allocated, no list object has to be generated

up-front, etc.

In [86]: %time xr = xrange(10000000)

CPU times: user 3 us, sys: 1e+03 ns, total: 4 us

Wall time: 5.96 us

Memory consumption is also much, much more efcient – 40 bytes compared to 80 MB.

Introduction to Python 27

In [87]: sys.getsizeof(xr)

Out[87]: 40

However, in practical applications the two can be used often interchangeably such that one

should always resort to the more efcient alternative when possible. The following examples

calculate – using the functional programming operation reduce – the sum of all integers

from 0 to 9,999,999. Although in this case there is hardly a performance difference, the rst

operation requires 80 MB of memory while the second might only require less than 100 bytes.

In [88]: %time reduce(lambda x, y:x+y,range(1000000))

CPU times: user 131 ms, sys: 15.9 ms, total: 147 ms

Wall time: 147 ms

Out[88]: 499999500000

In [89]: %time reduce(lambda x, y:x+y,xrange(1000000))

CPU times: user 118 ms, sys: 0 ns, total: 118 ms

Wall time: 117 ms

Out[89]: 499999500000

More Pythonic (and faster in general) is to calculate the sum using the built-in sum function

– in this case a signicant performance advantage for the generator approach emerges.

In [90]: %timeit sum(range(1000000))

10 loops, best of 3: 26.6 ms per loop

In [91]: %timeit sum(xrange(1000000))

100 loops, best of 3: 12.9 ms per loop

There is also a way of indirectly constructing a generator object, i.e. by the use of parentheses.

The following code results in a generator object for the sine values of the numbers from 0 to

99:

In [92]: g = (math.sin(x) for xin xrange(100))

In [93]: g

Out[93]: <generator object <genexpr> at 0x2ab247901f50>

Such an object stores its internal state and yields the next value when the method next() is

called.

28 LISTED VOLATILITY AND VARIANCE DERIVATIVES

In [94]: g.next()

Out[94]: 0.0

In [95]: g.next()

Out[95]: 0.8414709848078965

Yet another way of constructing a generator object is by a denition style that resembles the

standard function denition closely. The difference is that instead of the return statement,

the yield statement is used.

In [96]: def g(start, end):

....: while start <= end:

....: yield start # yield "next" value

....: start += 1 # increase by one

....:

Usage then might be as follows:

In [97]: go = g(15, 20)

In [98]: for _in go:

....: print _,

....:

15 16 17 18 19 20

2.2 NumPy

Many operations in computational nance take place over (large) arrays of numerical data.

NumPy is a Python library that allows the efcient handling of and operation on such data

structures. Although quite a mighty library with a wealth of functionality, it sufces for the

purposes of this book to cover the basics of NumPy.

In [99]: import numpy as np

The workhorse is the NumPy ndarray class which provides the data structure for n-

dimensional, immutable array objects. You can generate an ndarray object e.g. out of a

list object.

Introduction to Python 29

In [100]: a = np.array(range(24))

In [101]: a

Out[101]:

array([ 0, 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16,

17, 18, 19, 20, 21, 22, 23])

The power of these objects lies in the management of n-dimensional data structures (e.g. matri-

ces or cubes of data).

In [102]: b = a.reshape((4, 6))

In [103]: b

Out[103]:

array([[ 0, 1, 2, 3, 4, 5],

[ 6, 7, 8, 9, 10, 11],

[12, 13, 14, 15, 16, 17],

[18, 19, 20, 21, 22, 23]])

In [104]: c = a.reshape((2, 3, 4))

In [105]: c

Out[105]:

array([[[ 0, 1, 2, 3],

[4,5, 6, 7],

[ 8, 9, 10, 11]],

[[12, 13, 14, 15],

[16, 17, 18, 19],

[20, 21, 22, 23]]])

So-called standard arrays (in contrast to e.g. structured arrays) have a single dtype (i.e.

NumPy data type). Consider the following operation which changes the dtype parameter of

the bobject to oat:

In [106]: b = np.array(b, dtype=np.float)

In [107]: b

Out[107]:

array([[ 0., 1., 2., 3., 4., 5.],

[ 6., 7., 8., 9., 10., 11.],

[ 12., 13., 14., 15., 16., 17.],

[ 18., 19., 20., 21., 22., 23.]])

30 LISTED VOLATILITY AND VARIANCE DERIVATIVES

A major strength of NumPy is vectorized operations.

In [108]: 2*b

Out[108]:

array([[ 0., 2., 4., 6., 8., 10.],

[ 12., 14., 16., 18., 20., 22.],

[ 24., 26., 28., 30., 32., 34.],

[ 36., 38., 40., 42., 44., 46.]])

In [109]: b**2

Out[109]:

array([[ 0., 1., 4., 9., 16., 25.],

[ 36., 49., 64., 81., 100., 121.],

[ 144., 169., 196., 225., 256., 289.],

[ 324., 361., 400., 441., 484., 529.]])

You can also pass ndarray objects to lambda or standard Python functions.

In [110]: f=lambda x:x**2-2*x+0.5

In [111]: f(a)

Out[111]:

array([ 0.5, -0.5, 0.5, 3.5, 8.5, 15.5, 24.5, 35.5,

48.5, 63.5, 80.5, 99.5, 120.5, 143.5, 168.5, 195.5,

224.5, 255.5, 288.5, 323.5, 360.5, 399.5, 440.5, 483.5])

In many scenarios, only a (small) part of the data stored in an ndarray object is of interest.

NumPy supports basic and advanced slicing and other selection features.

In [112]: a[2:6] # 3rd to 6th element

Out[112]: array([2, 3, 4, 5])

In [113]: b[2, 4] # 3rd row, final (5th)

Out[113]: 16.0

In [114]: b[1:3, 2:4] # middle square of numbers

Out[114]:

array([[ 8., 9.],

[ 14., 15.]])

Boolean operations are also supported in many places.

Introduction to Python 31

# which numbers are larger than 10?

In [115]: b>10

Out[115]:

array([[False, False, False, False, False, False],

[False, False, False, False, False, True],

[ True, True, True, True, True, True],

[ True, True, True, True, True, True]], dtype=bool)

# only those numbers (flat) that are larger than 10

In [116]: b[b > 10]

Out[116]:

array([ 11., 12., 13., 14., 15., 16., 17., 18., 19., 20., 21.,

22., 23.])

Furthermore, ndarray objects have multiple (convenience) methods already built in.

In [117]: a.sum() # sum of all elements

Out[117]: 276

In [118]: b.mean() # mean of all elements

Out[118]: 11.5

In [119]: b.mean(axis=0) # mean along 1st axis

Out[119]: array([ 9., 10., 11., 12., 13., 14.])

In [120]: b.mean(axis=1) # mean along 2nd axis

Out[120]: array([ 2.5, 8.5, 14.5, 20.5])

In [121]: c.std() # standard deviation for all elements

Out[121]: 6.9221865524317288

Similarly, there is a wealth of so-called universal functions that the NumPy library provides.

Universal in the sense that they can be applied in general to NumPy ndarray objects and to

standard numerical Python data types.

In [122]: np.sum(a) # sum of all elements

Out[122]: 276

In [123]: np.mean(b, axis=0) # mean along 1st axis

Out[123]: array([ 9., 10., 11., 12., 13., 14.])

In [124]: np.sin(b).round(2) # sine of all elements (rounded)

Out[124]:

array([[ 0. , 0.84, 0.91, 0.14, -0.76, -0.96],

[-0.28, 0.66, 0.99, 0.41, -0.54, -1. ],

32 LISTED VOLATILITY AND VARIANCE DERIVATIVES

[-0.54, 0.42, 0.99, 0.65, -0.29, -0.96],

[-0.75, 0.15, 0.91, 0.84, -0.01, -0.85]])

In [125]: np.sin(4.5) # sine of Python float object

Out[125]: -0.97753011766509701

However, you should be aware that applying NumPy universal functions to standard Python

data types generally comes with a signicant performance burden.

In [126]: %time l = [np.sin(x) for x in xrange(100000)]

CPU times: user 188 ms, sys: 3.89 ms, total: 192 ms

Wall time: 192 ms

In [127]: import math

In [128]: %time l = [math.sin(x) for x in xrange(100000)]

CPU times: user 27.7 ms, sys: 0 ns, total: 27.7 ms

Wall time: 27.7 ms

Using the vectorized operations from NumPy is faster than both of the above alternatives which

result in list objects.

In [129]: %time np.sin(np.arange(100000))

CPU times: user 5.23 ms, sys: 0 ns, total: 5.23 ms

Wall time: 5.24 ms

Out[129]:

array([ 0. , 0.84147098, 0.90929743, ..., 0.10563876,

0.89383946, 0.86024828])

Here, we use the ndarray object constructor arange which yields an ndarray object of

integers – below is a simple example:

In [130]: ai = np.arange(10)

In [131]: ai

Out[131]: array([0, 1, 2, 3, 4, 5, 6, 7, 8, 9])

In [132]: ai.dtype

Out[132]: dtype('int64')

Using this constructor, you can also generate ndarray objects with different dtype

attributes:

Introduction to Python 33

In [133]: af = np.arange(0.5, 9.5, 0.5) # start, end, step size

In [134]: af

Out[134]:

array([ 0.5, 1. , 1.5, 2. , 2.5, 3. , 3.5, 4. , 4.5, 5. , 5.5,

6. , 6.5, 7. , 7.5, 8. , 8.5, 9. ])

In [135]: af.dtype

Out[135]: dtype('float64')

In this context the linspace operator is also useful, providing an ndarray object with

evenly spaced numbers.

In [136]: np.linspace(0, 10, 12) # start, end, number of elements

Out[136]:

array([ 0. , 0.90909091, 1.81818182, 2.72727273,

3.63636364, 4.54545455, 5.45454545, 6.36363636,

7.27272727, 8.18181818, 9.09090909, 10. ])

In nancial analytics one often needs (pseudo-)random numbers. NumPy provides many func-

tions to sample from different distributions. Those needed in this book are the standard normal

distribution and the Poisson distribution. The respective functions are found in the sub-library

numpy.random.

In [137]: np.random.standard_normal(10)

Out[137]:

array([ 1.70352821, -1.30223997, -0.16846238, -0.33605234, 0.84842565,

-0.7012202 , 1.31232816, 1.34394536, -0.08358828, 1.53690444])

In [138]: np.random.poisson(0.5, 10)

Out[138]: array([0, 1, 0, 1, 0, 0, 1, 2, 2, 0])

Let us generate an ndarray object which is a bit more “realistic” and which we work with

in what follows:

In [139]: np.random.seed(1000) # fix the rng seed value

In [140]: data = np.random.standard_normal(( 5, 100))

Although this is a slightly larger array one cannot expect that the 500 numbers are indeed

standard normally distributed in the sense that the rst moment is 0 and the second moment is

1. However, at least this can be easily corrected.

34 LISTED VOLATILITY AND VARIANCE DERIVATIVES

In [141]: data.mean() # should be 0.0

Out[141]: -0.02714981205311327

In [142]: data.std() # should be 1.0

Out[142]: 1.0016799134894265

The correction is called moment matching and can be implemented with NumPy by vectorized

operations.

In [143]: data = data - data.mean() # correction for the 1st moment

In [144]: data = data / data.std() # correction for the 2nd moment

In [145]: data.mean() # now really close to 0.0

Out[145]: 7.105427357601002e-18

In [146]: data.std() # now really close to 1.0

Out[146]: 1.0

2.3 matplotlib

At this stage, it makes sense to introduce plotting with matplotlib, the plotting work horse in the

Python ecosystem. We use matplotlib (see http://matplotlib.org) with the settings of another

library throughout, namely seaborn (see http://stanford.edu/∼mwaskom/software/seaborn/) –

this results in a more modern plotting style.

In [147]: import matplotlib.pyplot as plt # import main plotting library

In [148]: import seaborn as sns; sns.set() # set seaborn standards

In [149]: import matplotlib

# set font to serif

In [150]: matplotlib.rcParams['font.family'] = 'serif'

A standard plot is the line plot. The result of the code below is shown as Figure 2.1.

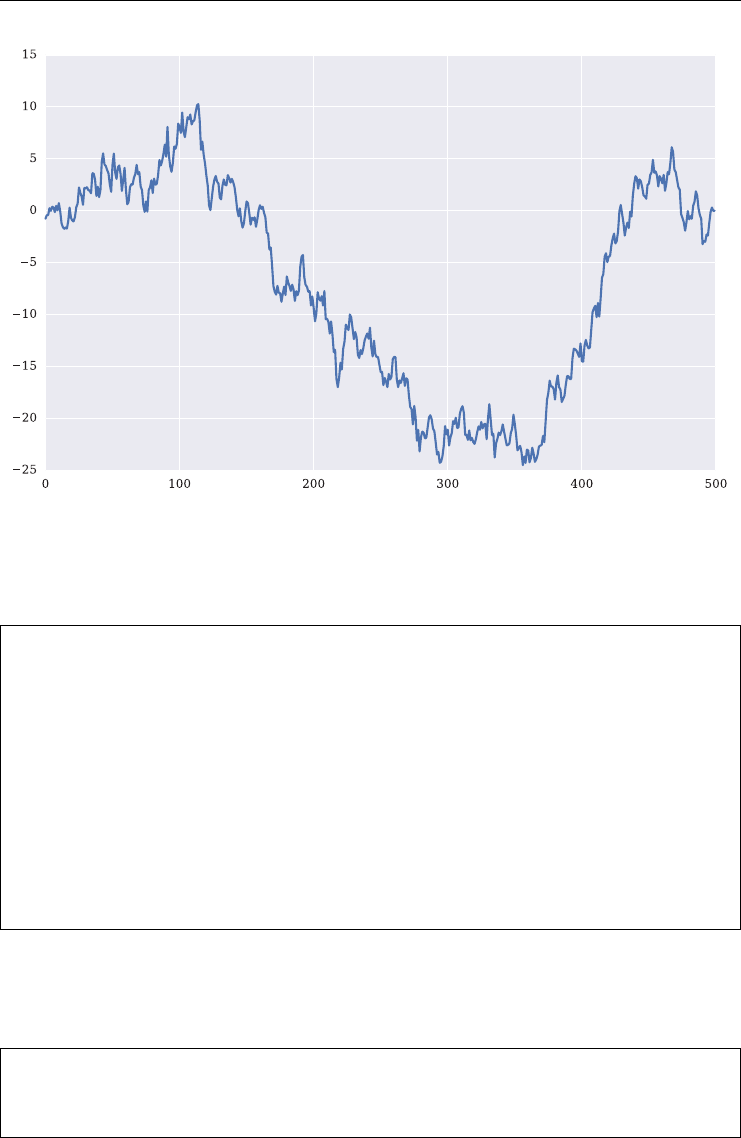

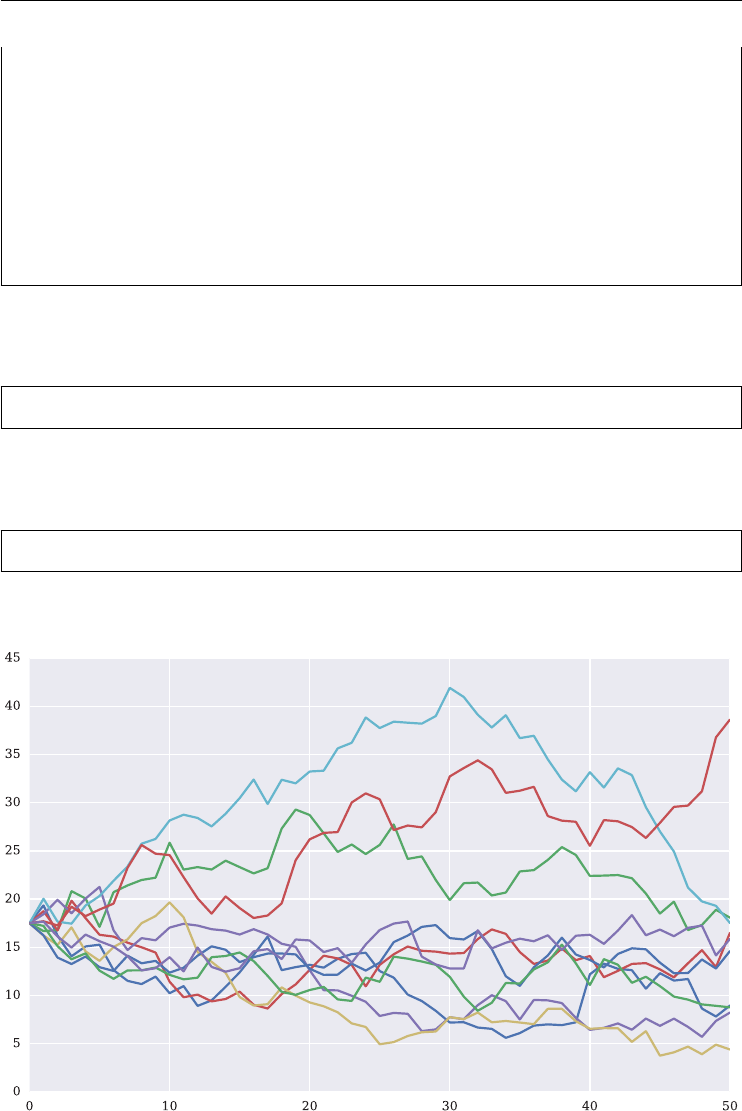

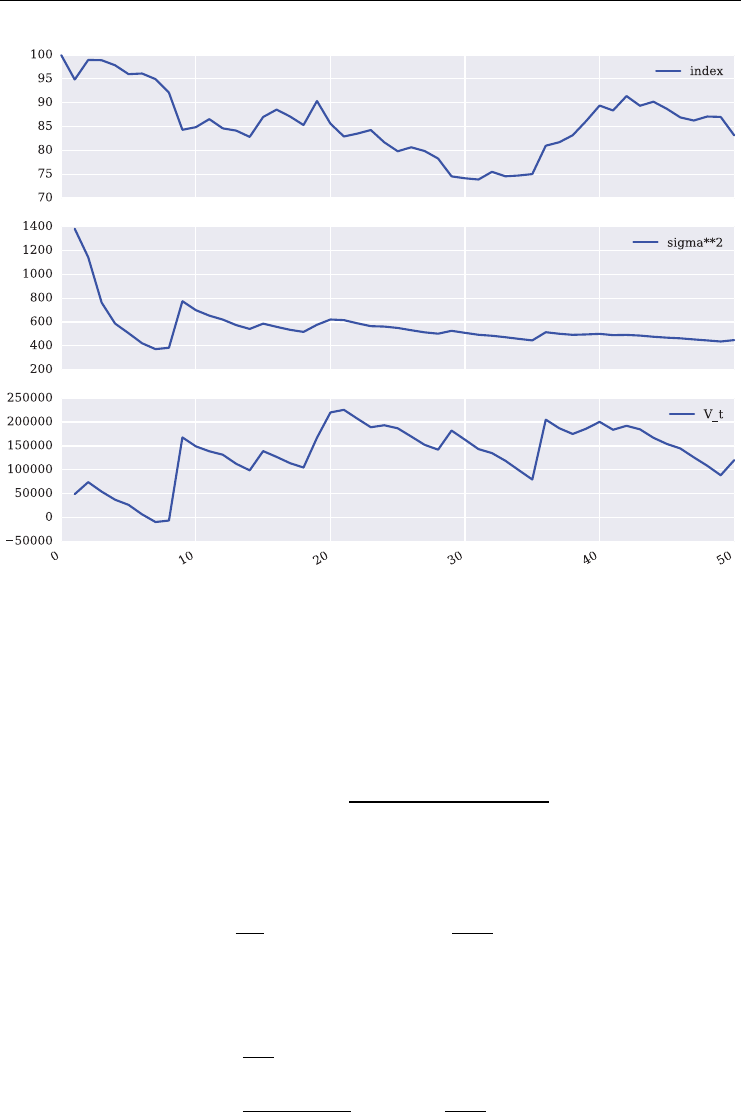

In [151]: plt.figure(figsize=(10, 6)); # size of figure

In [152]: plt.plot(data.cumsum()); # cumulative sum over all elements

Introduction to Python 35

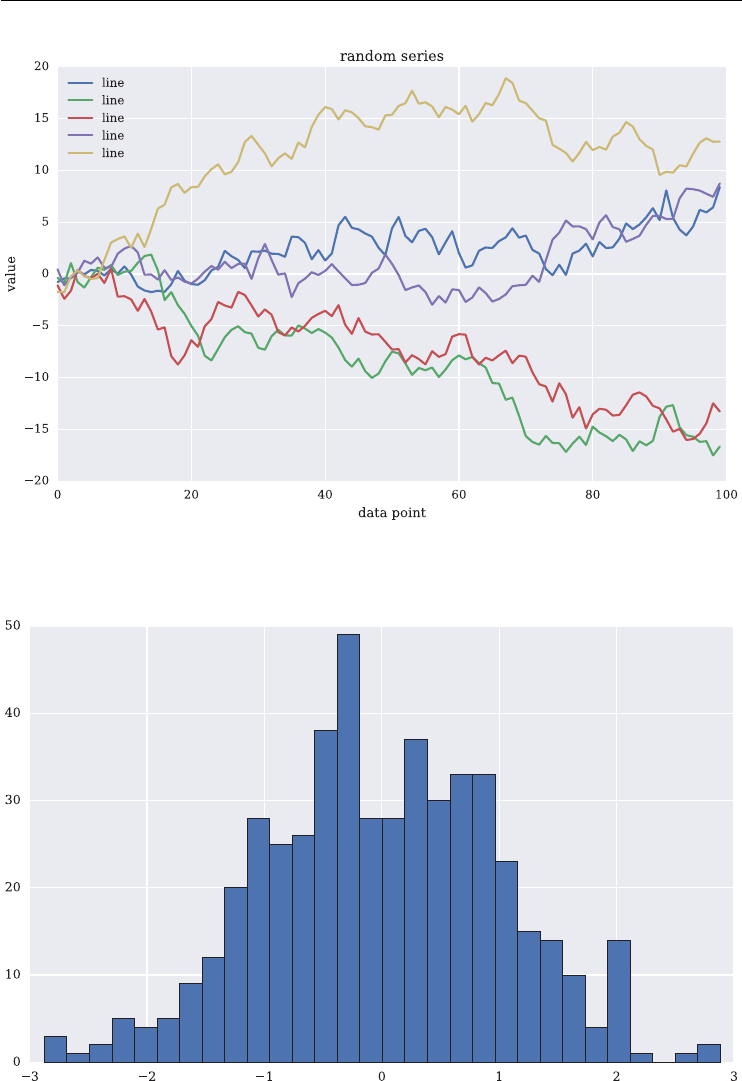

FIGURE 2.1 Standard line plot with matplotlib.

Multiple lines plots are also easy to generate (see Figure 2.2). The operator Tstands for

the transpose of the ndarray object (“matrix”).

In [153]: plt.figure(figsize=(10, 6)); # size of figure

# plotting five cumulative sums as lines

In [154]: plt.plot(data.T.cumsum(axis=0), label='line');

In [155]: plt.legend(loc=0); # legend in best location

In [156]: plt.xlabel('data point'); # x axis label

In [157]: plt.ylabel('value'); # y axis label

In [158]: plt.title('random series'); # figure title

Other important plotting types are histograms and bar charts. A histogram for all 500 values

of the data object is shown as Figure 2.3. In the code, the flatten() method is used to

generate a one-dimensional array from the two-dimensional one.

In [159]: plt.figure(figsize=(10, 6)); # size of figure

In [160]: plt.hist(data.flatten(), bins=30);

36 LISTED VOLATILITY AND VARIANCE DERIVATIVES

FIGURE 2.2 Multiple lines plot with matplotlib.

FIGURE 2.3 Histrogram with matplotlib.

Introduction to Python 37

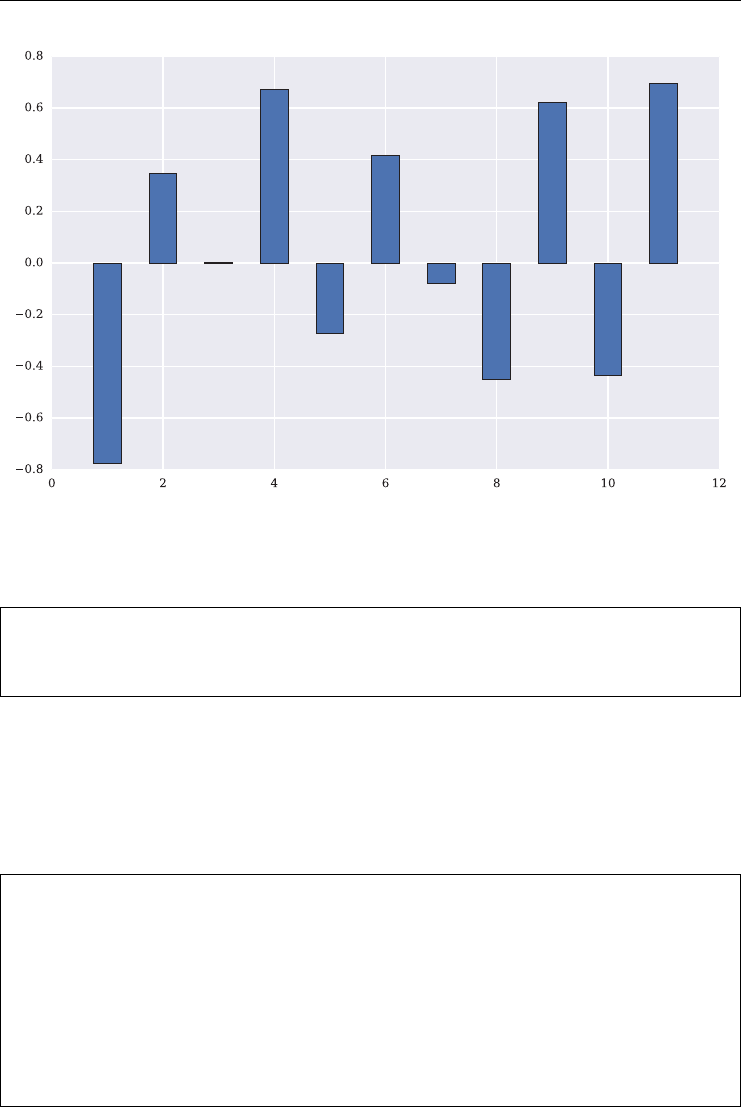

FIGURE 2.4 Bar chart with matplotlib.

Finally, consider the bar chart presented in Figure 2.4.

In [161]: plt.figure(figsize=(10, 6)); # size of figure

In [162]: plt.bar(np.arange(1, 12) - 0.25, data[0, :11], width=0.5);

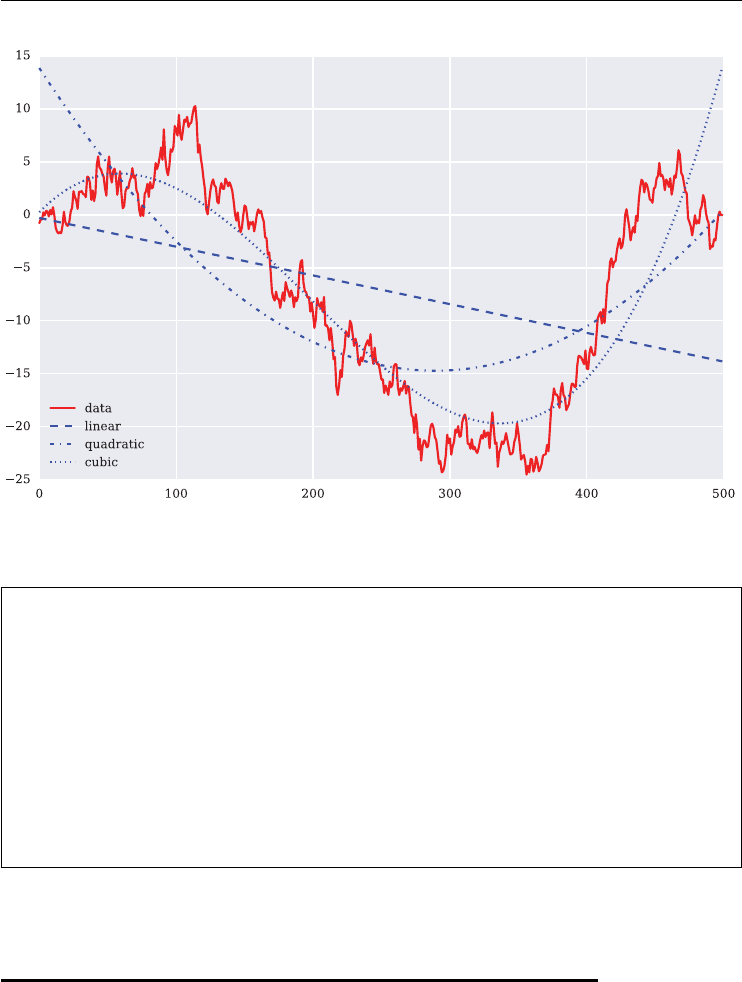

To conclude the introduction to matplotlib consider the ordinary least squares (OLS) regres-

sion of the sample data displayed in Figure 2.1. NumPy provides with the two functions

polyfit() and polyval() convenience functions to implement OLS based on sim-

ple monomials i.e. x,x2,x3,...,xn. For illustration purposes consider linear, quadratic and

cubic OLS.

In [163]: x = np.arange(len(data.cumsum()))

In [164]: y = data.cumsum()

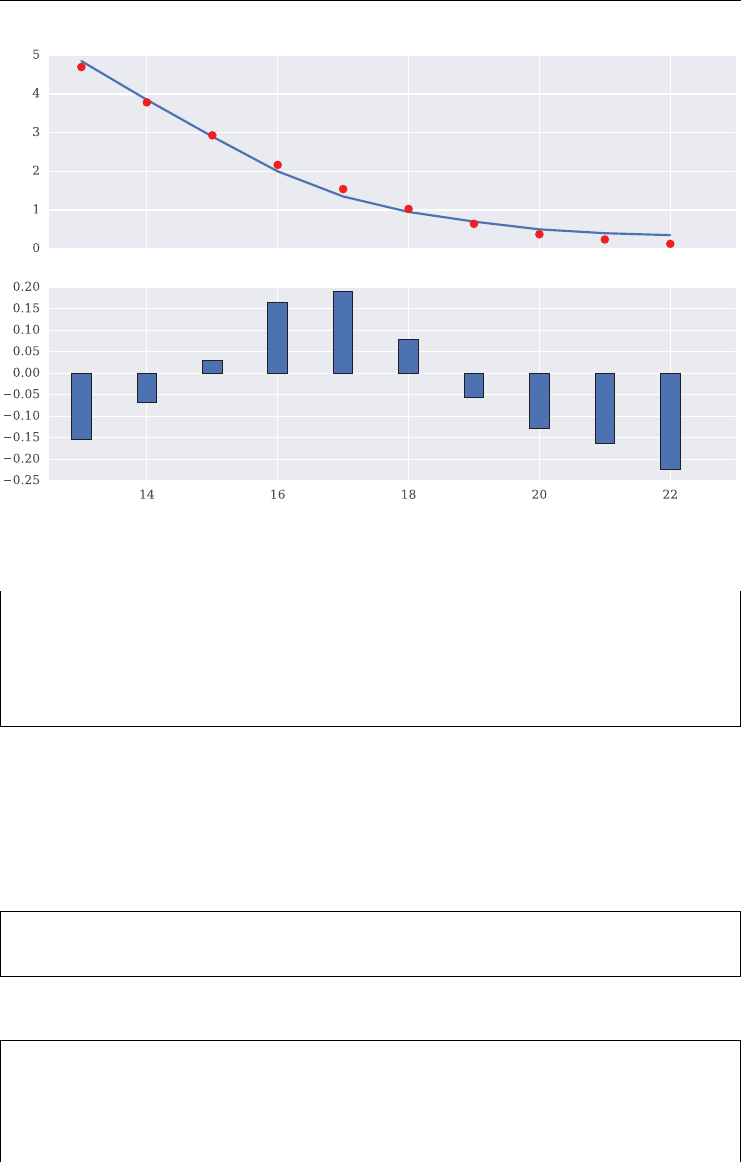

In [165]: rg1 = np.polyfit(x, y, 1) # linear OLS

In [166]: rg2 = np.polyfit(x, y, 2) # quadratic OLS

In [167]: rg3 = np.polyfit(x, y, 3) # cubic OLS

Figure 2.5 illustrates the regression results graphically.

38 LISTED VOLATILITY AND VARIANCE DERIVATIVES

FIGURE 2.5 Linear, quadratic and cubic regression.

In [168]: plt.figure(figsize=(10, 6));

In [169]: plt.plot(x, y, 'r', label='data');

In [170]: plt.plot(x, np.polyval(rg1, x), 'b--', label='linear');

In [171]: plt.plot(x, np.polyval(rg2, x), 'b-.', label='quadratic');

In [172]: plt.plot(x, np.polyval(rg3, x), 'b:', label='cubic');

In [173]: plt.legend(loc=0);

2.4 pandas

pandas is a library with which you can manage and operate on time series data and other

tabular data structures. It allows implementation of even sophisticated data analytics tasks on

larger data sets. While the focus lies on in-memory operations, there are also multiple options

for out-of-memory (on-disk) operations. Although pandas provides a number of different data

structures, embodied by powerful classes, the structure most often used is the DataFrame

class which resembles a typical table of a relational (SQL) database and is used to manage,

for instance, nancial time series data. This is what we focus on in this section.

Introduction to Python 39

2.4.1 pandas DataFrame class

In its most basic form, a DataFrame object is characterized by an index, column names and

tabular data. To make this more specic, consider the following sample data set:

In [174]: np.random.seed(1000)

In [175]: a = np.random.standard_normal(( 10, 3)).cumsum(axis=0)

Also, consider the following dates which shall be our index:

In [176]: index = ['2016-1-31', '2016-2-28', '2016-3-31',

.....: '2016-4-30', '2016-5-31', '2016-6-30',

.....: '2016-7-31', '2016-8-31', '2016-9-30',

.....: '2016-10-31']

.....:

Finally, the column names:

In [177]: columns = ['no1', 'no2', 'no3']

The instantiation of a DataFrame object then looks as follows:

In [178]: import pandas as pd

In [179]: df = pd.DataFrame(a, index=index, columns=columns)

A look at the new object reveals its resemblance with a typical table from a relational database

(or e.g. an Excel spreadsheet).

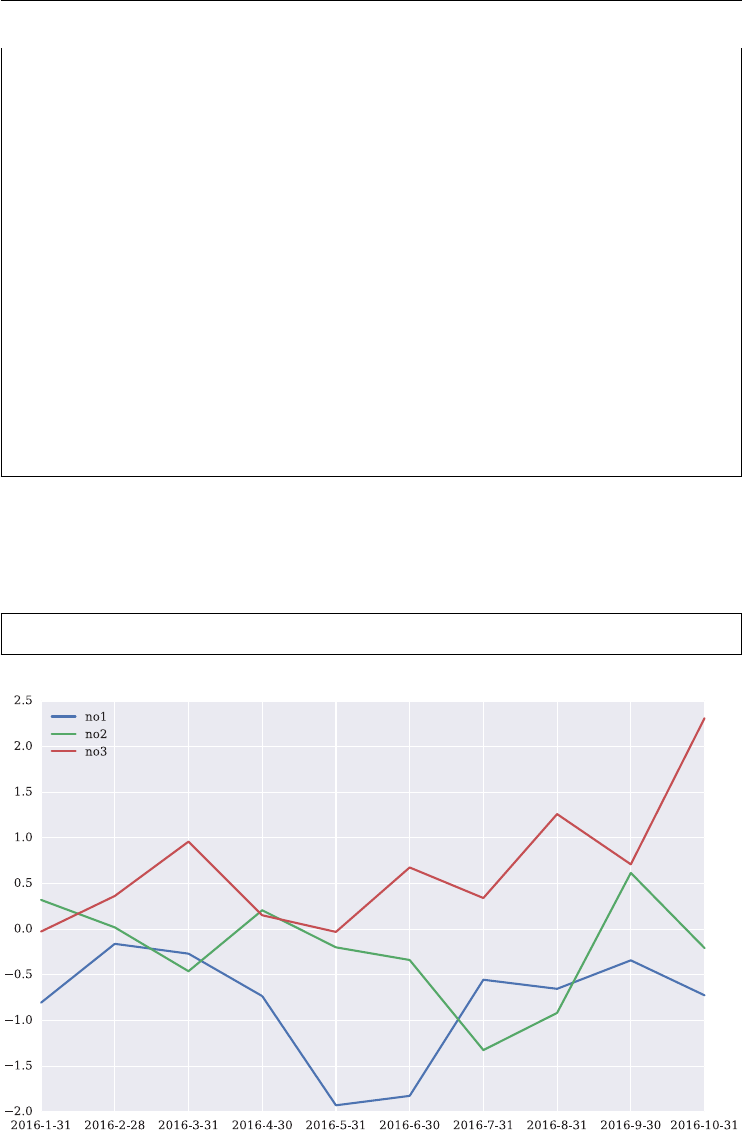

In [180]: df

Out[180]:

no1 no2 no3

2016-1-31 -0.804458 0.320932 -0.025483

2016-2-28 -0.160134 0.020135 0.363992

2016-3-31 -0.267572 -0.459848 0.959027

2016-4-30 -0.732239 0.207433 0.152912

2016-5-31 -1.928309 -0.198527 -0.029466

2016-6-30 -1.825116 -0.336949 0.676227

2016-7-31 -0.553321 -1.323696 0.341391

2016-8-31 -0.652803 -0.916504 1.260779

2016-9-30 -0.340685 0.616657 0.710605

2016-10-31 -0.723832 -0.206284 2.310688

40 LISTED VOLATILITY AND VARIANCE DERIVATIVES

DataFrame objects have built in a multitude of basic, advanced and convenience methods, a

few of which are illustrated without much commentary below.

In [181]: df.head() # first five rows

Out[181]:

no1 no2 no3

2016-1-31 -0.804458 0.320932 -0.025483

2016-2-28 -0.160134 0.020135 0.363992

2016-3-31 -0.267572 -0.459848 0.959027

2016-4-30 -0.732239 0.207433 0.152912

2016-5-31 -1.928309 -0.198527 -0.029466

In [182]: df.tail() # last five rows

Out[182]:

no1 no2 no3

2016-6-30 -1.825116 -0.336949 0.676227

2016-7-31 -0.553321 -1.323696 0.341391

2016-8-31 -0.652803 -0.916504 1.260779

2016-9-30 -0.340685 0.616657 0.710605

2016-10-31 -0.723832 -0.206284 2.310688

In [183]: df.index # index object

Out[183]:

Index([u'2016-1-31', u'2016-2-28', u'2016-3-31', u'2016-4-30', u'2016-5-31',

u'2016-6-30', u'2016-7-31', u'2016-8-31', u'2016-9-30', u'2016-10-31'],

dtype='object')

In [184]: df.columns # column names

Out[184]: Index([u'no1', u'no2', u'no3'], dtype='object')

In [185]: df.info() # meta information

<class 'pandas.core.frame.DataFrame'>

Index: 10 entries, 2016-1-31 to 2016-10-31

Data columns (total 3 columns):

no1 10 non-null float64

no2 10 non-null float64

no3 10 non-null float64

dtypes: float64(3)

memory usage: 320.0+ bytes

In [186]: df.describe() # typical statistics

Out[186]:

no1 no2 no3

count 10.000000 10.000000 10.000000

mean -0.798847 -0.227665 0.672067

std 0.607430 0.578071 0.712430

min -1.928309 -1.323696 -0.029466

Introduction to Python 41

25% -0.786404 -0.429123 0.200031

50% -0.688317 -0.202406 0.520109

75% -0.393844 0.160609 0.896922

max -0.160134 0.616657 2.310688

Numerical operations are in general as easy with DataFrame objects as with NumPy ndar-

ray objects. They are also quite close in terms of syntax.

In [187]: df*2 # vectorized multiplication

Out[187]:

no1 no2 no3

2016-1-31 -1.608917 0.641863 -0.050966

2016-2-28 -0.320269 0.040270 0.727983

2016-3-31 -0.535144 -0.919696 1.918054

2016-4-30 -1.464479 0.414866 0.305823

2016-5-31 -3.856618 -0.397054 -0.058932

2016-6-30 -3.650232 -0.673898 1.352453

2016-7-31 -1.106642 -2.647393 0.682782

2016-8-31 -1.305605 -1.833009 2.521557

2016-9-30 -0.681369 1.233314 1.421210

2016-10-31 -1.447664 -0.412568 4.621376

In [188]: df.std() # standard deviation by column

Out[188]:

no1 0.607430

no2 0.578071

no3 0.712430

dtype: float64

In [189]: df.mean(axis=1) # mean by index value

Out[189]:

2016-1-31 -0.169670

2016-2-28 0.074664

2016-3-31 0.077202

2016-4-30 -0.123965

2016-5-31 -0.718767

2016-6-30 -0.495280

2016-7-31 -0.511875

2016-8-31 -0.102843

2016-9-30 0.328859

2016-10-31 0.460191

dtype: float64

In [190]: np.mean(df) # mean via universal function

Out[190]:

42 LISTED VOLATILITY AND VARIANCE DERIVATIVES

no1 -0.798847

no2 -0.227665

no3 0.672067

dtype: float64

Pieces of data can be looked up via different mechanisms.

In [191]: df['no2'] # 2nd column

Out[191]:

2016-1-31 0.320932

2016-2-28 0.020135

2016-3-31 -0.459848

2016-4-30 0.207433

2016-5-31 -0.198527

2016-6-30 -0.336949

2016-7-31 -1.323696

2016-8-31 -0.916504

2016-9-30 0.616657

2016-10-31 -0.206284

Name: no2, dtype: float64

In [192]: df.iloc[0] # 1st row

Out[192]:

no1 -0.804458