Manual

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 66

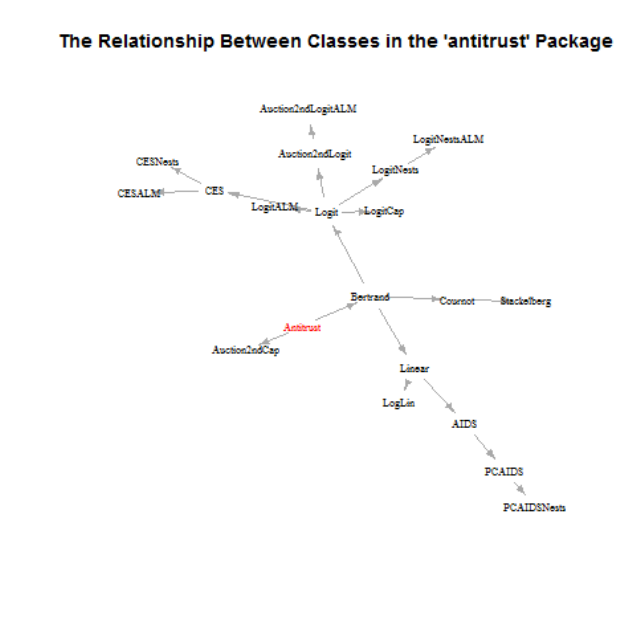

The antitrust Package

Charles Taragin Michael Sandfort

June 9, 2018

The views expressed herein are entirely those of the authors and should not be purported

to reflect those of the U.S. Department of Justice. The antitrust package has been

released into the public domain without warranty of any kind, expressed or implied. We

thank Ronald Drennan, Robert Majure, Russell Pittman, Gloria Sheu, Nathan Miller,

Randy Chugh, Marc Remer, Alexander Raskovich, William Drake, Thomas Jeitschko,

Greg Werden, Luke Froeb, Nicholas Hill, and Conor Ryan. Address: Economic Analysis

Group, Antitrust Division, U.S. Department of Justice, 450 5th St. NW, Washington

DC 20530. E-mail: charles.taragin@usdoj.gov and michael.sandfort@usdoj.gov.

Contents

I Unilateral Effects 6

1 The Bertrand Pricing Game 7

1.1 The Game . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

1.1.1 The Mathematical Model . . . . . . . . . . . . . . . . . . . . 8

1.1.2 Adding Exogenous Capacity Constraints . . . . . . . . . . . . 9

1.2 Calibrating Model Demand and Cost Parameters . . . . . . . . . . 10

1.2.1 Linear Demand . . . . . . . . . . . . . . . . . . . . . . . . . . 12

1.2.2 Log-Linear Demand . . . . . . . . . . . . . . . . . . . . . . . 14

1.2.3 LA-AIDS Demand . . . . . . . . . . . . . . . . . . . . . . . . 15

1.2.4 Logit Demand . . . . . . . . . . . . . . . . . . . . . . . . . . 18

1.2.5 CES Demand . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

1.2.6 Marginal Costs . . . . . . . . . . . . . . . . . . . . . . . . . . 25

1.3 Simulating Merger Effects . . . . . . . . . . . . . . . . . . . . . . . . 26

1.3.1 Summarizing Results . . . . . . . . . . . . . . . . . . . . . . . 27

1.3.2 Plotting Results (experimental) . . . . . . . . . . . . . . . . 28

1.3.3 Simulating Price Effects With Efficiencies . . . . . . . . . . . 28

1.3.4 Excluding Products From the Market (experimental) . . . 29

1.3.5 Measuring Changes In Consumer Welfare . . . . . . . . . . . 29

1.3.6 Defining Antitrust Markets . . . . . . . . . . . . . . . . . . . 30

1.3.7 Simulating Merger Effects With Known Demand Parameters 31

1.4 Gotchas . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

1.4.1 Market Definition . . . . . . . . . . . . . . . . . . . . . . . . 32

1.4.2 Log-Linear Demand . . . . . . . . . . . . . . . . . . . . . . . 32

1.4.3 LA-AIDS Demand . . . . . . . . . . . . . . . . . . . . . . . . 32

2 The Cournot Quantity Game 33

2.1 The Game . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

2.1.1 The Mathematical Model . . . . . . . . . . . . . . . . . . . . 34

2.2 Calibrating Model Demand and Cost Parameters . . . . . . . . . . 34

2.3 Simulating Merger Effects . . . . . . . . . . . . . . . . . . . . . . . . 35

2.3.1 Summarizing Results . . . . . . . . . . . . . . . . . . . . . . . 35

2

2.3.2 Simulating Price Effects With Marginal Cost Efficiencies . . . 35

2.3.3 Simulating Price Effects With Capacity Constraints . . . . . 36

2.3.4 Excluding Products or Plants . . . . . . . . . . . . . . . . . . 36

2.3.5 Measuring Changes In Consumer Welfare . . . . . . . . . . . 37

2.3.6 Allowing For First-Mover Advantage . . . . . . . . . . . . . . 37

3 Auction Models 38

3.1 2nd Price Auction with Capacity Constraints . . . . . . . . . . . . . 39

3.1.1 The Game . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

3.1.2 Calibrating Model Parameters . . . . . . . . . . . . . . . . . 41

3.1.3 Simulating Merger Effects (experimental) . . . . . . . . . . 43

3.2 2nd Score Auction with Differentiated Products . . . . . . . . . . . . 43

3.2.1 The Game . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

3.2.2 Calibrating Model Demand and Cost Parameters . . . . . . . 45

3.2.3 Simulating Merger Effects . . . . . . . . . . . . . . . . . . . . 47

4 Other Tools 49

4.1 CMCR . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

4.2 Generalized Pricing Pressure . . . . . . . . . . . . . . . . . . . . . . 50

4.3 HHI . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51

II Coordinated Effects 52

5 A Collusion Game with Bertrand Reversion as Punishment 53

5.1 The Game . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54

5.1.1 The Incentive to Collude Under Grim Trigger . . . . . . . . . 55

5.2 Comparing Incentives to Collude and Defect Under Grim Trigger

(experimental) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56

III Under The Hood 57

6 Getting Help 58

7 Modifying and Extending antitrust 59

7.1 The Bertrand Model . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

7.2 The Auction Models . . . . . . . . . . . . . . . . . . . . . . . . . . . 60

3

antitrust is a suite of tools that may be used in assessing the implications of

horizontal mergers. The package contains functions that can calibrate the under-

lying parameters of a number of different supply and demand models as well as

simulate the effects of a horizontal merger in different strategic environments. The

output generated by these tools includes interesting features such as predicted price

increases, welfare measures, demand elasticities, and the Hypothetical Monopolist

Test. antitrust also includes functions that can assess the effects of a horizontal

merger in other ways, including: compensating marginal cost reduction and upwards

pricing pressure.

There are four features of antitrust that make it particularly useful for antitrust

practitioners. First, antitrust collects a number of useful models onto a common

platform, making it easy for practitioners to compare and contrast the results from

different models.

Second, antitrust is open source software that runs on the Ropen source platform.

Practically speaking, this means that practitioners not only have the flexibility to

run this software wherever and whenever they wish, but they can also modify and

extend the software as they see fit. We hope that having this collection of tools on

a common, open source platform will facilitate discussion and collaboration among

practitioners.

Third, antitrust includes a web interface built using shiny. While this interface

does not give users acess to the full array of functionality in antitrust, it is simple

to use and may provide first-time users, particularly those who are unfamiliar with

R, a gentler introduction to antitrust. The interface may be invoked using the

antitrust_shiny function.

Finally, the functions included in antitrust vary in the amount of information they

require. Some functions, such as upp.bertrand,cmcr.bertrand and cmcr.cournot

require only information on the merging parties’ products, while functions like

linear,pcaids, and logit require at least some information on all market par-

ticipants. Table 7.1 summarizes the information requirements of all the functions

included in antitrust.

The limited information needed for the economic models used in antitrust comes

at some cost. First, the output of these models is sensitive to the supplied inputs.

For instance, when employing the Bertrand model, inaccurate margins, shares and

prices can yield inaccurate estimates of demand and cost parameters which can in

turn yield incorrect predictions of a merger’s effects. Calibrating model parameters

with an array of plausible inputs will yield a range of outputs and illustrate the

sensitivity of each model to those inputs.

4

Second, none of the parameters calibrated by antitrust may be used in frequen-

tist statistical hypothesis testing. In other words, while the economic models in

antitrust may be used to generate reliable estimates of the effects of the merger,

statistical tests cannot be used to determine the accuracy of these estimates. Accom-

plishing this requires additional data and is beyond the current scope of antitrust.

This document provides an introduction to the economic theory upon which the

antitrust packages’ functions are built. Please use the help function for assis-

tance invoking any of the functions, classes, or methods included in antitrust. In

particular, note that the help pages for all the functions listed in Table 7.1 contain

examples illustrating how to use the function.

5

Part I

Unilateral Effects

6

1 The Bertrand Pricing Game

Much of antitrust’s functionality is built around the Bertrand pricing game. This

version of the game assumes that firms producing multiple differentiated products

with distinct, constant, marginal costs simultaneously set their products’ prices to

maximize their profits. In this model, prices are strategic complements in the sense

that increasing the price of one product causes some customers to switch to other

products, raising the quantities sold and therefore the profit-maximizing prices of

these other products. Ultimately, it is the magnitude of these lost sales that, at the

margin, dissuades firms from raising their prices further .

Mergers are modeled by assuming that the merging parties’ products are placed

under common ownership, which, if the products are substitutes, allows the merged

entity to recapture some of the sales that would otherwise be lost. As a result,

the Bertrand model (for some demand systems) predicts that absent any efficiencies

affecting the marginal cost of production, the prices of all of the merging parties’

products will increase, and the price of all other products in the market will not

decrease.

Currently, this version of the Bertrand model does not allow firms to add or reposi-

tion products, or allow firms to engage in some forms of price discrimination.1

1.1 The Game

Suppose that there are Kfirms in a market, and that each of the k∈Kfirms

produces nkproducts.2Let n=P

k∈K

nkdenote the number of products sold by all

Kfirms. The Bertrand model assumes that firms simultaneously set their products’

prices in order to maximize their profits. This model also assumes that all firms can

perfectly observe each others’ prices, quantities, costs, and product characteristics.

Functions in antitrust’s Bertrand model also adopt the additional assumption that

1In particular, this version of the Bertrand model does not accommodate non-linear pricing, such

as is used in 2nd or 3rd degree price discrimination.

2Throughout, we abuse the notation slightly by treating variables like Kas both the set of firms

as well as the number of firms.

7

each product is produced using its own distinct constant marginal cost technology

ci, for all i∈n. As we will see, this assumption is necessary when information is

limited.

1.1.1 The Mathematical Model

Firm k∈Kchooses the prices {pi}nk

i=1 of its products so as to maximize profits.

Mathematically, firm ksolves:

max

{pi}nk

i=1

n

X

i=1

ωik(pi−ci)qi,

where ωik is the share of product i’s profits earned by firm k, so that P

k∈K

ωik ≤1.

qi, the quantity sold of product i, is assumed to be a twice differentiable function of

all product prices.

Differentiating profits with respect to each piyields the following first order condi-

tions (FOCs):

∂pi≡ωik qi+

n

X

j=1

ωjk(pj−cj)∂qj

∂pi

= 0 for all i∈nk

which may be rewritten as

∂pi≡ωik ri+

n

X

j=1

ωjkrjmjji = 0 for all i∈nk,

where ri≡piqi

n

P

j=1

pjqj

is product i’s revenue share, mi≡pi−ci

piis product i’s gross

margin, and ij ≡∂qi

∂pj

pj

qiis the elasticity of product iwith respect to the price of

product j.

The FOCs for all products may be stacked and then represented using the following

matrix notation:

(r◦diag(Ω)) + (E◦Ω)0(r◦m) = 0 (1.1.1)

8

rearranging yields

mBertrand =−{(E◦Ω)0−1(r◦diag(Ω))} ◦ 1

r(1.1.2)

where rand mare n-length vectors of revenue shares and margins, E=11 ... 1n

.

.

.....

.

.

n1... nn

is a n×nmatrix of own- and cross-price elasticities, and Ω = ω11 ... ω1n

.

.

.....

.

.

ωn1... ωnn is an

n×nmatrix whose i, jth element equals the share of product j’s profits owned by

the firm setting product i’s price3. In many cases, product iand jare wholly owned

by a single firm, in which cases the i, jth element of Ω equals 1 if iand jare owned

by the same firm and 0 otherwise. Under partial ownership, the columns of the

matrix formed from the unique rows of Ω must sum to 1. ‘diag’ returns the diagonal

of a square matrix and ‘◦’ is the Hadamard (entry-wise) product operator.

The solution to system 1.1.1 yields equilibrium prices conditional on the ownership

structure Ω. A (partial) merger is modeled as the solution to system 1.1.1 where Ω

is changed to reflect the change in ownership.

1.1.2 Adding Exogenous Capacity Constraints

The Bertrand model described above assumes that products are produced with con-

stant marginal costs and no capacity constraints. Here, we extend this model to

allow for exogenous capacity constraints.4

Firm k∈Kchooses the prices {pi}nk

i=1 of its products so as to maximize profits,

subject to capacity constraints {ti}nk

i=1. Mathematically, firm ksolves:

max

{pi}nk

i=1

n

X

i=1

ωik(pi−ci)qi,

subject to

qi≤ti, i = 1 . . . nk

3The Bertrand model assumes that while any firm can receive a portion of another firm’s profits

(e.g. through owning a share of that firms’ assets), only one firm can set a product’s price.

4This section is based on the model described in Froeb et al. [2003, p. 51-55]

9

In general, either the capacity constraint for product iwill bind and the firm will be

forced to produce less of ithan it would find optimal, or the capacity constraint will

not bind, and the firm will produce the optimal amount implied by the FOCs. In

the former, it can be shown that ∂pi≤0 and qi−ti= 0, while in the latter ∂pi= 0

and qi−ti≤0. Mathematically, these cases can be written as

max{∂pi, qi−ti}= 0,i = 1 . . . nk(1.1.3)

1.2 Calibrating Model Demand and Cost Parameters

Although the functions listed in the “Bertrand” section of Table 7.1 are based on

the Bertrand model and use similar inputs, they can yield very different equilibrium

price predictions. This can occur for two reasons. First, these functions use different

demand systems with very different curvatures to simulate the price effects from a

merger. Indeed, equation 1.1.1 indicates that it is these curvatures, embodied in

the matrix of own- and cross-price elasticities E, that play an important role in

calculating price effects.

Second, binding capacity constraints can limit the incentive of the merging parties to

raise prices, or the ability of other firms in the market to respond to a price increase.

If, pre-merger, none of the merging parties’ products are capacity constrained but

some of the other firms’ products are, then post-merger equilibrium prices will typ-

ically be higher than if none of the capacity constraints were binding pre-merger.

Also, if pre-merger, some of the merging parties’ products are capacity constrained

but none of the other firms’ products are constrained, then post-merger equilibrium

prices will typically be lower than if none of the capacity constraints were binding

pre-merger.

For all the demand specifications listed in the “Bertrand” section of Table 7.1, the

calibration strategy is the same. First, we assume that quantities/shares and (with

the exception of LA-AIDS) prices are observed for all products in the market, and

that margins for some products are observed. Our decision to treat quantities,

prices, and margins as primitives comes directly from equation 1.1.1. For capacity-

constrained models, equation 1.1.3 indicates that all product capacities must be

observed as well.

In addition to quantities, prices, some margins and capacities, we assume that users

observe diversion ratios. Diversion ratios come in two forms: quantity diversion and

revenue diversion. The quantity diversion from product ito product j dq

ij is defined

as the percentage of all of i’s lost unit sales that switch to jdue to a price increase

10

in product i, while the revenue diversion from product ito product j dr

ij is defined

as the percentage of all of i’s lost revenue that switches to jdue to a price increase

in product i. Mathematically, quantity and revenue diversion may be represented as

dq

ij =−

∂qj

∂pi

∂qi

∂pi

=−jiqj

iiqi

(1.2.1)

dr

ij =−

∂pjqj

∂pi

∂piqi

∂pi

=−ji(jj −1)rj

jj (ii −1)ri

(1.2.2)

Note that dq

ij , dr

ij are restricted to be between -1 and 1, and are positive if products i

and jare substitutes and negative if they are complements. Additionally, conditional

on customers switching from product i, they must switch to another product (i.e.

Pjdij ≤0). For all the models included in antitrust , we assume that iand jare

not complements (dij ≥0) and for some demand models (i.e. AIDS) we will assume

that Pjdij = 0.

Although diversion ratios are not present in either equation 1.1.1 or 1.1.3, these

definitions indicate that diversion ratios may be helpful in recovering the matrix of

own- and cross-price elasticities E. Indeed, for a number of the demand systems

described below, diversions will be used for just this purpose.

We further assume that all of this information represents the outcome of the unique

pre-merger equilibrium for firms in the market playing the static Bertrand pricing

game described above. We then substitute observed margins, shares and prices into

either equation 1.1.1 or 1.1.3, which is now solely a function of demand parameters,

and then solve for the coefficient(s) on prices. Once the price coefficients have

been estimated, we use observed prices and the demand equations to estimate the

intercepts.

Often, there are more FOCs than unknown price coefficients. For instance, under

Logit demand, there is only one price parameter that needs to be estimated and

up to nFOCs with which to estimate it. This means that at a minimum, users

need only supply enough margin information to complete a single product’s FOC. If

that product happens to be owned by a single-product firm, then only one margin

is necessary. On the other hand, if the product happens to be owned by a multi-

11

product firm, then at a minimum, all the margins for products owned by that firm

must be supplied.

The (Marshallian) demand specifications used in antitrust can be grouped into

two categories: demand systems that are derived from a representative consumer’s

expenditure function and demand systems that are derived from a representative

consumer’s indirect utility function. The linear, log-linear, and LA-AIDS demand

systems fall into the former category, while the Logit and CES fall into the latter

category. Below, we briefly discuss these demand systems as well as the assumptions

and/or data needed to recover estimates of the demand parameters.

We conclude this section with a discussion of how calibrated demand parameters

and the FOCs can be used to calibrate product-specific constant marginal costs.

1.2.1 Linear Demand

The Bertrand model with linear demand may be implemented using the linear

function.

The linear demand system assumes that the demand for each product i∈nin the

market is given by

qi=αi+X

j∈n

βij pjfor all i∈n,

which may be written in matrix notation as

q=α+Bp,

where q≥0, p > 0 are vectors of product quantities and prices, αis a vector

of product specific demand intercepts and Bis a matrix of slopes. This demand

system yields the following own- and cross-price elasticities:

ii =βii

pi

qi

, ii <0

ij =βij

pi

qj

, ij ≥0

Without additional restrictions and/or data, there are 2nequations (nFOCs and

ndemand equations) but n(n+ 1) unknown parameters, which means that there

12

are more unknowns than equations and the demand parameters α, B cannot be

recovered. To remedy this, we assume that the quantity diversion is observed.5

With the linear model, this assumption increases the number of equations to n(n+1),

allowing estimates of αand Bto be recovered if prices, quantities and margins are

observed for all products.

One known issue with the linear demand system is that, while analytically tractable,

it is not rooted in consumer choice theory. Indeed, it has been shown that the linear

demand system without income effects is consistent with the axioms of consumer

choice if Bis a symmetric matrix and satisfies homogeneity of degree 0 in prices.6

Imposing these additional assumptions reduces the number of unknown parameters

to n(n+3)

2(n(n+1)

2elements of Band nintercepts), which means that the system is

over-identified.7

The linear demand system can be modified to allow for substitution to an outside

(numeraire) good. To accomplish this, assume that the price of the outside product

is not set strategically (i.e. not set as part of the Nash-Bertrand game played by

the manufacturers of the nproducts included in the simulation). It can be shown

that if Bis symmetric and satisfies homogeneity of degree 0 in prices when the

outside good is included, then Pj∈ndij <0.8. In other words, under symmetry and

homogeneity of degree 0, users may include a non-strategically priced outside good

5By default, linear assumes diversion according to quantity share. Diversion according to quantity

share assumes that dq

ij =sj

1−si, where si, sjare the quantity share of iand j. As we will see,

this is the assumption underlying the Logit demand system.

6See [von Haefen, 2002, pp. 283].

7In fact, it turns out that only one element of Bmust be estimated.To see why, note that under

symmetry, βjj =dij

dji βii. Hence, if βii is known, then the preceding equation indicates that all

the βjj s may be recovered. From here, the definition of diversion may be used to recover all the

βij s.

8To see this, note:

X

i∈n

βij <0 (homogeneity of degree 0 with outside good)

⇔βii +X

j6=i

βji <0 (symmetry)

⇔βii −X

j6=i

dij βii <0

⇔βii(1 −X

j6=i

dij )<0

⇒X

j∈n

dij <0

where the last line follows since βii <0⇒1−Pj6=idij >0.

13

by simply allowing the rows of the diversion matrix to sum to less than zero. The

extent to which consumers substitute from product ito the outside good may be

controlled by increasing the magnitude of Pj∈ndij .

By default, the calcSlopes method, called by the linear function to calibrate

the linear demand parameters, assumes that the above assumptions hold and uses

a minimum distance algorithm to find the elements of Bthat best satisfy i) all

the FOCs for which there is sufficient information and ii) the diversion equations

dij =−βji

βii , subject to the constraints that βij ≥0 for all i6=jand Pjbij ≤0 for

all i. The model intercepts can then be recovered from the linear demand equations.

For completeness, linear includes the ‘symmetry’ argument that, when set equal

to FALSE, instructs calcSlopes to calibrate demand parameters without impos-

ing symmetry and homogeneity of degree zero in prices on B. Note that when

‘symmetry’ is FALSE, the system of equations is just-identified, which means that

prices, quantities, and margins must be observed for all products. Also, note that

when ‘symmetry’ is FALSE, Linear demand is unlikely to be consistent with con-

sumer choice theory, and welfare measures such as compensating variation cannot

be calculated.9

1.2.2 Log-Linear Demand

The Bertrand model with log-linear demand may be implemented using the loglinear

function.

The log-linear demand system assumes that the demand for each product i∈nin

the market is given by

log(qi) =αi+X

j∈n

βij log(pj) for all i∈n, βii <0

which may be written in matrix notation as

log(q) =α+Blog(p),

where q, p are vectors of product quantities and prices, αis a vector of product

specific demand intercepts and Bis a matrix of slopes. This demand system yields

9The CV method used to compute compensating variation checks to see if Bis symmetric and

returns an error if it isn’t.

14

the following own- and cross-price elasticities:

ii =βii

ij =βij

As with linear demand, there are 2nequations but n(n+ 1) unknown parameters,

which means the demand parameters α, B cannot be recovered without additional

assumptions. As before, we will assume that quantity diversion is known and by

default occurs according to quantity share. However, it turns out that the parame-

ter restrictions needed to make log-linear demand consistent with consumer choice

theory are likely to be inconsistent with the Bertrand model.10 As such, loglinear

employs only the first assumption. Consequently, the demand parameters are just-

identified, which means that users must supply loglinear with prices, margins, and

quantities for all products in the market.

1.2.3 LA-AIDS Demand

The Bertrand model with the linear approximate Almost Ideal Demand System

(LA-AIDS) may be implemented using the aids function.

The LA-AIDS without income effects assumes that the demand for each product

i∈nin the market is given by

ri=αi+X

j∈n

βij log(pj) for all i∈n, βii <0

which may be written in matrix notation as

r=α+Blog(p),

10In order for log-linear demand without income effects to be consistent with consumer choice

theory, either i) βij = 1 + βii,−16=βii ≤0 or ii) βij = 0, βii =−1 for all i, j ∈n. Condition

i) is unlikely to be true, since when products iand jare substitutes (typically the case we are

most interested in evaluating), βij >0 which in turn implies that βii >−1. However, if the

owner of product ionly manufacturers a single product (a typical occurrence), then the FOCs

from the Bertrand model imply that βii ≤ −1, a contradiction. Condition ii) is unlikely to hold

since it implies that product ihas no close substitutes and has marginal costs equal to 0. See

LaFrance [1986] and von Haefen [2002] for more details.

15

where r, p are vectors of product revenue shares and prices, αis a vector of product-

specific demand intercepts and Bis a matrix of slopes11.

The LA-AIDS model yields the following own- and cross-price elasticities:

ii =−1 + βii

ri

+ri(1 + ), ii <0

ij =βij

ri

+rj(1 + ), ij ≥0

where is the market elasticity of demand.

As with the linear demand system, the LA-AIDS model assumes that Bis sym-

metric, satisfies homogeneity of degree zero in prices, and that diversion is known.

The LA-AIDS model, however, assumes that revenue diversion, rather than quan-

tity diversion is observed.12 Under these two assumptions, there are n(n+3)

2unknown

demand parameters (n(n−1)

2diagonal elements in B,ndiagonal elements,and nin-

tercepts) and up to n(n+ 1) equations (n(n−1) diversion equations, nFOCs and

ndemand equations), in which case the system is over-identified.13

One interesting feature of the LA-AIDS that distinguishes it from the linear and

log-linear demand systems included in antitrust is that LA-AIDS elasticities in-

corporate , the market elasticity. Roughly speaking, controls the extent to which

consumers substitute to products outside the nproducts included in the simulation

given a small change in market-wide product prices. Here, we assume that is a

parameter whose value is not a function of product prices.14 While in some cases

can be readily observed, in others it cannot. For the latter, the calcSlopes method

(called by aids) exploits the fact that there are more equations than unknowns to

identify both the unknown demand parameters described above as well as .

The calcSlopes method, called by the aids function to calibrate the AIDS param-

eters uses a minimum distance algorithm to find the and a single diagonal element

of Bthat best satisfy i) all the FOCs for which there is sufficient information and ii)

the diversion equations dij =−βji

βii , and iii) the market elasticity (if supplied using

11LA-AIDS differs from AIDS in that LA-AIDS substitutes the AIDS price index with Stone’s price

index. Since this version of LA-AIDS is without income effects, Stone’s price index is only used

to derive the own- and cross-price elasticities.

12If the ‘diversion’ argument to aids is missing, aids assumes diversion according to revenue share.

13In fact, it turns out that only one element of Bmust be estimated.To see why, note that under

symmetry, βjj =dij

dji βii. Hence, if βii is known, then the preceding equation indicates that all

the βjj s may be recovered. From here, the definition of diversion may be used to recover all the

βij s.

14This assumption implies that customers substitute to products outside of the simulation in re-

sponse to price increases by all products in the simulation at the same rate pre- and post-merger.

16

the ‘mktElast’ argument). The βiis are recovered from the fact that Pjdij = 0;

customers must switch to a product included in the model.

If only a single product’s own-price elasticity and is observed, then pcaids may

be used in lieu of aids to calibrate the LA-AIDS parameters.15

Another distinguishing feature of the LA-AIDS model is that it does not require

any information on product prices in order to simulate merger price effects. The

LA-AIDS accomplishes this by using the supplied margin and revenue information

to estimate B, but not α. There are however, a few drawbacks to not using pricing

information. First, while merger-specific price changes may be calculated, pre- and

post-merger price levels cannot. Second, welfare measures like compensating vari-

ation cannot be calculated. Prices are an optional input to aids and pcaids, and

when they are supplied both price levels and welfare measures may be calculated.

Nested LA-AIDS

The nested LA-AIDS may be implemented using pcaids.nests.

By default, aids and pcaids assume that pre-merger, diversion occurs according to

revenue share. While convenient, one potential drawback of this assumption is that

diversion according to share may not accurately represent consumer substitution

patterns. antitrust provides two ways to relax diversion according to share. First,

both of these functions contain a ‘diversions’ argument that may be used to supply

ak×kmatrix of revenue diversions.

Alternatively, users can place the nproducts into H≥2nests, with products in

the same nest assumed to be closer substitutes than products in different nests.16

This approach requires users to calibrate H(H−1)

2nesting parameters, where each

parameter measures the extent to which the diversion between any two products in

different nests deviates from diversion according to share.17 Accordingly, users must

supply margin information for at least H(H−1)

2products.18

15The main difference between pcaids and aids is that while aids requires users to supply revenue

shares and at least two margins (or a single margin and the market elasticity) as inputs, pcaids

requires the user to supply revenue shares, (using the ‘mktElast’ argument), and the own-price

elasticity for one of the products (using the ‘knownElast’ argument). A value for ‘knownElast’

may be found by inverting the margin of a single-product firm. A value for ‘mktElast’ may be

inferred from such sources as merging party documents, industry reports, and academic studies.

16No function in antitrust currently permits a hierarchy of nests.

17The nesting parameters are constrained to be between 0 and 1, where 1 means that diversion

between nests occurs according to share. The diversion between two nests is assumed to be

symmetric; the diversion from nest ato nest bis the same as the diversion from bto a.

18Note that these margins are in addition to the margin information that may be necessary to

17

1.2.4 Logit Demand

The Bertrand model with Logit demand may be implemented using the logit func-

tion.

Logit demand is based on a discrete choice model that assumes that each consumer

is willing to purchase at most a single unit of one product from the nproducts

available in the market. The assumptions underlying Logit demand imply that the

probability that a consumer purchases product i∈nis given by

si=exp(Vi)

P

k∈n

exp(Vk),

where siis product i’s quantity share and Viis the (average) indirect utility that

a consumer receives from purchasing product i. We assume that Vitakes on the

following form

Vi=δi+αpi, α < 0.

The Logit demand system yields the following own- and cross-price elasticities:

ii =α(1 −si)pi

ij =−αsjpj

Logit demand has n+ 1 parameters to estimate (n δs and α) and up to 2nequations

with which to estimate them (up to ncomplete FOCs and nchoice probabilities).

calcSlopes exploits this over-identification by employing a minimum distance al-

gorithm to find the value for αthat best satisfies all the FOCs for which there are

data. The δs are then recovered from the choice probabilities.

One feature of the logit function is that the function allows users to specify whether

or not consumers must purchase one of the nproducts sold in the market or whether

consumers can choose to purchase an “outside” good. logit determines whether

users wish to include an outside option by determining if the user-supplied quantity

shares sisum to 1. If the shares sum to 1, then no outside good is included and

by default δ1is normalized to 0.19 Otherwise, an outside good is included whose δ

identify the elasticity of a single product (‘knownElast’).

19It can be shown that when there is no outside option in the Logit model, not all of the δs can be

separately identified. Users can control which product’s δis normalized to 0 by setting logit’s

‘normIndex’ argument equal to the index (position) of the desired product.

18

is normalized to 0, price is set equal to ‘priceOutside’ (default 0), and whose share

equals s0= 1 −P

i∈n

si.20

Logit With Capacity Constraints

The capacity-constrained Bertrand model with Logit demand may be implemented

using the logit.cap function.

The Logit Model with capacity constraints is calibrated by noting that in the pre-

merger equilibrium, if product iis capacity constrained then ∂qi

∂pj= 0 for all j∈n.

This condition implies that an estimate of the price coefficient αmay be obtained by

starting with the FOCs in equation 1.1.1, deleting all rows pertaining to a capacity-

constrained product and then for the remaining rows, zeroing out the appropriate

elements of the Logit elasticity matrix E. A minimum distance estimator on the

surviving FOCs is then employed to estimate the price coefficient. Once the price

coefficient has been estimated, the technique outlined above may be used to uncover

the vector of mean valuations.

Nested Logit

The Bertrand model with nested Logit demand may be implemented using the

logit.nests function.

By construction, Logit demand assumes that diversion occurs according to quantity

share. While convenient, one potential drawback of this assumption is that diversion

according to share may not accurately represent consumer substitution patterns.

One way to relax this assumption is to group the nproducts into n>H≥2nests,

with products in the same nest assumed to be closer substitutes than products in

different nests.21 logit.nests’s ‘nests’ argument may be used to specify a length-n

vector identifying which nest each product belongs to.

The assumptions underlying nested Logit demand imply that the probability that a

consumer purchases product iin nest h∈His given by

20Essentially ‘priceOutside’ controls how the mean valuations are scaled. Scaling is particularly

important when computing compensating variation. See Werden and Froeb [1994, p.412] for

further details.

21No function in antitrust currently permits a hierarchy of nests. Singleton nests (nests containing

only a single product) are technically permitted, but their nesting parameter is not identified

and is therefore normalized to 1.

19

si=si|hsh,

si|h=exp( Vi

σh)

P

k∈h

exp(Vk

σh),1≥σh≥0

sh=exp(σhIh)

P

l∈H

exp(σlIl), Ih= log X

k∈h

exp Vk

σh.

We assume that Vitakes on the following form

Vi=δi+αpi, α ≤0.

The Nested Logit demand system yields the following own- and cross-price elastici-

ties:

ii =[1 −si+ ( 1

σh

−1)(1 −si|h)]αpi,

ij =(−[sj+ ( 1

σh−1)sj|h]αpj,if i, j are both in nest h.

−αsjpj,if iis not in nest hbut jis.

Notice how these cross-price elasticities are identical to the non-nested Logit elas-

ticities when products i, j are in different nests, but are larger when products i, j

are in the same nests. This observation is consistent with the claim that products

within a nest are closer substitutes than products outside of a nest.

In contrast to nested LA-AIDS, which must calibrate H(H−1)

2nesting parameters,

only Hnesting parameters must be calibrated. By default, calcSlopes constrains

all the nesting parameters to be equal to one another, σh=σfor all h∈H.

This reduces the number of parameters that need to be estimated to n+ 2 (n δs,

α, σ) which means users must furnish enough margin information to complete at

least two FOCs. Setting logit.nests’s ‘constraint’ argument to FALSE causes

the calcSlopes method to relax the constraint and calibrate a separate nesting

parameter for each nest. Relaxing the constraint increases the number of parameters

that must be estimated to n+H+ 1, which means that users must furnish margin

information sufficient to complete at least H+1 FOCs. Moreover, users must supply

at least one margin per nest for each non-singleton nest. In other words, if nest h∈H

contains nh>1 products, then at least one product margin from nest hmust be

supplied.

20

Like logit,logit.nests also allows users to specify whether or not consumers

must purchase one of the nproducts sold in the market or whether consumers can

choose to purchase an “outside” good. This works almost the same in logit.nests

as logit, except that when the sum of market revenue shares is less than 1, the

outside good is placed in its own nest with its nesting parameter normalized to 1.

(Nested) Logit With Unobserved Outside Share

The Bertrand model with (nested) Logit demand and unobserved outside share may

be implemented using the (logit.nests.alm)logit.alm function.

The Bertrand model with Logit demand described above assumes that when an

outside good is included, its share is known. In some instances, however, users may

find it difficult to reliably estimate the share of the outside good. The logit.alm

function attempts to circumvent this issue by treating the share of the outside good

as a nuisance parameter and using additional margin information to estimate that

parameter.22

logit.alm accomplishes this by noting that the probability that a consumer pur-

chases product i∈ncan be rewritten as

si=si|IsI,

si|I=exp(Vi)

P

k∈I

exp(Vk),

sI=1 −s0,

where si|Iis product i’s quantity share, conditional on a product being chosen from

the set of inside goods I. This implies that

X

k∈I

sk|I=1,

As in the Logit Model, we assume that Vitakes on the following form

Vi=δi+αpi, α ≤0.

Likewise, the own- and cross-price elasticities may be rewritten as

22The outside good is a nuisance parameter because it is only needed to obtain estimates of the

other demand parameters and is not used to solve for equilibrium prices.

21

ii =α(1 −si|I(1 −s0))pi

ij =−αsj|I(1 −s0)pj

This version of the Logit model has n+ 2 parameters to estimate (n δs, α, and s0)

and up to 2nequations with which to estimate them (up to ncomplete FOCs and

nchoice probabilities). calcSlopes exploits this over-identification by employing

a minimum distance algorithm to find the values for αand s0that best satisfy all

the FOCs for which there are data. The δs are then recovered from the choice

probabilities.

Similar logic may be used to formulate the nested logit with unobserved outside

share. Under the assumption that the outside good is the sole member of its own

nest H0, the probability that a consumer purchases product iin nest h∈H\H0

can be rewritten as

si=si|hshsI,

sI=1 −s0,

where si|hand share defined in the section on Nested Logit demand, and sIis the

unobserved probability that an inside good is selected. This version of the nested

Logit model has n+h+2 parameters to estimate (n δs, hnesting parameters, α, and

s0) and up to 2nequations with which to estimate them (up to ncomplete FOCs

and nchoice probabilities).

1.2.5 CES Demand

The Bertrand model with Constant Elasticity of Substitution (CES) demand may

be implemented using the ces function.

Like the Logit, CES demand is based on a discrete choice model. However, CES

differs from the Logit model in that under CES consumers do not purchase a single

unit of a product but instead spend a fixed proportion of their budget on one of the

nproducts available in the market.23

23Formally, each consumer chooses the product i∈nthat yields the maximum utility Ui= ln(δiqi)+

αln(q0) + i, subject to the budget constraint y=piqi+q0. Here, qiis the amount of product

iconsumed by a consumer, δiis a measure of product i’s quality, q0is the amount of the

numeraire, yis consumer income, and iare random variables independently and identically

distributed according to the Type I Extreme Value distribution.

22

The assumptions underlying CES demand imply that the probability that a con-

sumer purchases product i∈nis given by

ri=Vi

P

k∈n

Vk

for all i∈n,

where riis product i’s revenue share and Viis the (average) indirect utility that

a consumer receives from purchasing product i. We assume that Vitakes on the

following form

Vi=δip1−γ

i, γ > 1.

The CES demand system yields the following own- and cross-price elasticities:

ii =−γ+ (γ−1)ri

ij =(γ−1)rj

Functional form differences aside, one important difference between the CES and

Logit demand systems is that the Logit model’s choice probabilities are based on

quantity shares, while the CES model’s choice probabilities are based on revenue

shares.

Like Logit demand, CES demand has n+ 1 parameters to estimate (n δs and γ)

and up to 2nequations with which to estimate them (up to ncomplete FOCs and n

choice probabilities). ces exploits this over-identification by employing a minimum

distance algorithm to find the value for γthat best satisfies all the FOCs for which

there are data. The δs are then recovered from the choice probabilities.

ces also allows users to specify whether or not consumers must purchase one of

the nproducts sold in the market or whether consumers can choose to purchase an

“outside” good. ces determines whether users wish to include an outside option by

determining if the user-supplied revenue shares risum to 1. If the shares sum to 1,

then no outside good is included and by default δ1is normalized to 1.24 Otherwise,

an outside good is included whose price and δare normalized to 1, and whose share

equals r0= 1 −P

i∈n

ri.

24It can be shown that when there is no outside option in the CES model, not all of the δs can be

separately identified. Users can control which product’s δis normalized to 1 by setting ces’s

‘normIndex’ argument equal to the index (position) of the desired product.

23

In addition to specifying an outside option, ces has the ‘shareInside’ argument that

may be used to specify the proportion of the representative consumer’s budget that

the consumer is willing to spend on the n+ 1 products that are within the market.25

By default, ‘shareInside’ equals 1, which indicates that the customer spends her

entire budget on the n+ 1 products within the market.

Nested CES

The Bertrand model with nested CES demand may be implemented using the

ces.nests function.

Like the Logit, CES demand assumes that diversion occurs according to share.26

While convenient, one potential drawback of this assumption is that diversion ac-

cording to share may not accurately represent consumer substitution patterns. As

with Logit demand, one way to relax this assumption is to group the nproducts

into H≥2nests, with products in the same nest assumed to be closer substitutes

than products in different nests.27 logit.nests’s ‘nests’ argument may be used to

specify a length-n vector identifying which nest each product belongs to.

The assumptions underlying nested CES demand imply that the probability that a

consumer purchases product iin nest h∈His given by

ri=ri|hrh,

ri|h=Vi

Ih

, Ih=X

k∈h

Vk

rh=I

1−γ

1−σh

h

P

l∈H

I

1−γ

1−σl

l

.

We assume that Vitakes on the following form

Vi=δip1−σh

i,

251-‘shareInside’ equals the proportion of the representative consumer’s income that is spent on all

other products (i.e. the numeraire).

26CES assumes diversion according to revenue rather than quantity share.

27No function in antitrust currently permits a hierarchy of nests.

24

where σh> γ > 1 for all nests h∈H. The Nested Logit demand system yields the

following own- and cross-price elasticities:

ii =−σh+ (γ−1)ri+ (σh−γ)ri|h,

ij =((γ−1)rj+ (σh−γ)rj|hif i, j are both in nest h.

(γ−1)rj,if iis not in nest hbut jis.

Like ces,ces.nests also allows users to specify whether or not consumers must

purchase one of the nproducts sold in the market or whether consumers can choose

to purchase an “outside” good. This works almost the same in ces.nests as ces,

except that when the sum of market revenue shares is less than 1, the outside good

is placed in its own nest with its nesting parameter normalized to 0.

By default, calcSlopes constrains all the nesting parameters to be equal to one

another σh=σfor all h∈H. This reduces the number of parameters that need to

be estimated to n+ 2 (n δs, α, σ) which means users must furnish enough margin

information to complete at least two FOCs. Setting ces.nests’s ‘constraint’ argu-

ment to FALSE causes the calcSlopes method to relax the constraint and calibrate

a separate nesting parameter for each nest. Relaxing the constraint increases the

number of parameters that must be estimated to n+H+ 1, which means that users

must furnish margin information sufficient to complete at least H+ 1 FOCs. More-

over, users must supply at least one margin per nest for each non-singleton nest.

In other words, if nest h∈Hcontains nh>1 products, then at least one product

margin from nest hmust be supplied.

1.2.6 Marginal Costs

If all nproduct margins are observed, estimating marginal costs can be accomplished

by noting that mi≡pi−ci

piand using observed prices to calculate pre-merger marginal

costs.

Rather than using observed margins to compute marginal costs, antitrust instead

relies on the margins predicted by the Bertrand model. Rearranging the FOCs

yields an expression for margins as a function of the demand parameters, product

ownership, and revenue shares:

ˆmpre =−((E0

pre ◦Ωpre)−1rpre)◦(1

rpre

),

where Epre, rpre are elasticities and revenues calculated from the assumed demand

model, evaluated at observed prices.

25

The main advantage of using ˆmpre over mis that not all of the product margins

must be observed in order to estimate marginal costs.28 Once ˆmpre has been calcu-

lated, observed prices and the margin definition may be used to estimate pre-merger

marginal costs.

Because antitrust’s Bertrand model assumes that marginal costs are constant,

product i’s post-merger marginal costs are equal to its pre-merger marginal costs,

multiplied by (1 + ∆mci), the change in marginal costs due to any merger-specific

efficiencies. All of the functions described above have a ‘mcDelta’ argument that

allows users to specify a length-nvector of marginal cost changes.29 By default,

‘mcDelta’ is equal to a length-nvector of zeros, indicating that the merger will not

yield any efficiencies.

For the Bertrand model with capacity constraints, product margins for capacity-

constrained products cannot be recovered from the first-order conditions.30 There-

fore, marginal costs for capacity-constrained products must be recovered from user-

supplied margins and prices.

The calcMC method may be used to calculate pre- and post-merger marginal costs.

1.3 Simulating Merger Effects

For most of the demand systems included in antitrust’s Bertrand model, a closed-

form solution in prices to the FOCs equation does not exist. We therefore employ the

non-linear equation solver BBsolve from the BB package to find equilibrium prices.

It is worth noting that the FOCs in equation 1.1.1 are necessary but not sufficient

conditions for finding a price equilibrium to the Bertrand model. Unfortunately,

there does not appear to be any theoretical result guaranteeing that, for many of

the demand systems discussed here, there is a unique equilibrium to the Bertrand

game in prices.31 Practitioners sometimes address this problem by starting the

28Of course, enough margins must be observed to calibrate the demand parameters. For Log-Linear

demand as well as Linear demand with a matrix of asymmetric slopes (B), all product margins

must be supplied and m= ˆmpre .

29Negative values for ‘mcDelta’ imply that a product’s marginal cost will decrease, while positive

values imply a price increase. Users will receive a warning if ‘mcDelta’ is supplied with positive

values or if the values are greater than 1 in absolute value implying a cost change that is greater

than 100%.

30To see why, note that equation 1.1.3 implies that if product iis capacity constrained pre-merger,

then ij = 0 for all j. Since ij is always multiplied by the margin of product i, that margin

does not appear in the FOCs and is therefore not identified.

31To our knowledge, there is no theoretical result indicating that a unique Nash equilibrium in

prices exists for most of the demand systems discussed here, i.e. when i) firms produce multiple

26

non-linear solver at different starting points in the price space, and seeing if these

different initial values converge to distinct price equilibria. All of the constructor

functions (e.g. linear,loglinear,logit) have a ‘priceStart’ argument that may

be used to specify the non-linear solver’s starting values. Moreover, many of these

functions also include the ‘isMax’ argument, which when set equal to TRUE tests

to see whether the candidate pre-merger and post-merger price equilibria identified

by the non-linear solver are in fact (local) maxima.

antitrust users can also test the robustness of the predicted prices by modifying

how the non-linear equation solver BBsolve used by most antitrust functions solves

for the pre- and post-merger price equilibrium. Modifications to BBsolve’s default

behavior may be accomplished by including BBsolve arguments in any of the an-

titrust functions described above.32 See BBsolve’s help page for more information

on how to modify BBsolve’s behavior.

The FOCs for the capacity-constrained Bertrand game (equation 1.1.3) suffer from

an additional complication: the max function introduces a kink that can make it

difficult for the non-linear equation solver to find equilibrium prices. Froeb et al.

[2003, p. 54] suggests replacing equation 1.1.3 with

F OCi+qi−ti+qF OC2

i+ (qi−ti)2= 0,i = 1, . . . , n

which has the same roots as equation 1.1.3, but is smoother. The calcPrices

method for all classes based on the capacity-constrained Bertrand Model use this

smoothed system to solve for equilibrium prices.

In addition to computing pre- and post-merger equilibrium prices, antitrust’s

Bertrand model contains methods that can compute many other features of the

model. Below, we discuss a few of the methods that we expect users will find help-

ful. Table 7.2 provides a more extensive list of methods.

1.3.1 Summarizing Results

The summary method may be used to summarize the results of a merger between

two firms for a given demand model. By default, the summary method reports pre-

and post-merger equilibrium prices, revenue shares, weighted average compensating

marginal cost reduction, and compensating variation.33 Quantity shares rather than

products and ii) marginal costs are constant. The primary exception to this is linear demand.

32linear’s calcPrices method employs constrOptim rather than BBsolve.

33For some demand systems (e.g. Logit and CES), output shares as opposed to levels are reported.

Compensating variation as well as equilibrium price levels for LA-AIDS models are reported

27

revenue shares may be reported by setting summary’s ‘revenue’ argument equal to

FALSE. Likewise, levels, either in units or in revenues, rather than shares may be

reported by setting summary’s ‘shares’ argument equal to FALSE. Calibrated demand

parameters may be reported by setting summary’s ‘parameters’ argument equal to

TRUE.The number of significant digits can be altered using the ‘digits’ argument.

In addition to printing the equilibrium price and output information to the screen,

the summary method invisibly returns a matrix containing this information. Users

can save this matrix to a new object for later use.

1.3.2 Plotting Results (experimental)

The plot method employs ggplot to plot pre- and post-merger product residual

demand, marginal costs and equilibria. This method has a ‘scale’ argument, a

number between 0 and 1 which controls how much of the demand curve above the

equilibrium price and below marginal cost is plotted. The default for ‘scale’ is .1.

plot returns a ggplot object.

1.3.3 Simulating Price Effects With Efficiencies

Absent efficiencies, the Bertrand model with the demand systems described here will

almost always produce a (possibly negligible) post-merger price increase among sub-

stitutes. These price increases, however, can be offset by merger-specific efficiencies

that decrease the incremental costs of some of the merging firms’ products.34

All the functions discussed above allow users to evaluate these efficiencies in two

different ways. First, all of these functions contain the ‘mcDelta’ argument, which

allows users to specify the proportional change in a product’s marginal costs that

may result from a merger. These cost changes are factored into the post-merger

price equilibrium calculation made by the calcPrices method.

Second, users can call the cmcr method on the output of any of the functions de-

scribed above. This method computes the compensating marginal cost reduction

(CMCR) on the merging parties’ products. CMCR is the percentage decrease in the

marginal costs of the merging parties’ products necessary to prevent a post-merger

price increase. See the cmcr help page for further details.

only if the user supplied pre-merger prices. Compensating variation is only reported for the

Linear model if ‘symmetry’ equals TRUE.

34Costs that are not strictly increasing with a product’s output (i.e. fixed or sunk costs) do not

affect the price setting behavior of firms in a Bertrand pricing game.

28

1.3.4 Excluding Products From the Market (experimental)

By default, the Bertrand model calculates a merger’s effects under the assumption

that the acquisition does not change the set of products available to consumers. A

merger’s effects, however, may differ if the merger induces either the merging parties

or another market participant to eliminate some products from their portfolio.

To accommodate the possibility that some products may be removed from the market

following an acquisition, all the constructor functions described above have a ‘subset’

argument that allows users to specify a length-nlogical vector that equals TRUE if

a product should be included in the post-merger simulation and FALSE otherwise.

By default, ‘subset’ is equal to a length-nvector of TRUEs.

1.3.5 Measuring Changes In Consumer Welfare

All of the demand models included in antitrust’s Bertrand model have a CV method

which may be used to calculate compensating variation. Compensating variation is

the amount of money needed to make a consumer as well off as they were before

the merger increased prices. Table 7.3 lists the formula for calculating compensating

variation for the demand models included in antitrust. The last column in this

table indicates whether the formula for compensating variation returns compensating

variation in levels (e.g. dollars) or as a percent of the representative consumer’s total

income.35

Compensating variation can be calculated only if i) the demand system is consistent

with both consumer choice theory as well as the Bertrand model described above and

ii) all the demand parameters can be estimated. As discussed earlier, the parameter

restrictions necessary for the Log-linear demand system to satisfy consumer choice

theory will typically not satisfy the parameter restrictions implied by the Bertrand

model. Consequently, there is no CV method defined for the Log-linear demand

system. Similarly, the CV method returns an error if Linear demand is calibrated

without imposing symmetry and homogeneity of degree 0 in prices on the matrix of

slope coefficients B(i.e. setting ‘symmetry’ equal to FALSE). Lastly, the CV method

for LA-AIDS demand will return an error if LA-AIDS demand is calibrated without

prices. This occurs because prices are needed to uncover estimates of the LA-AIDS

demand intercepts, which are needed to compute compensating variation.

35The CV method for CES demand has a ‘revenueInside’ argument, which if set equal to the total

revenue of all products included in the market, converts the percent to levels. Similarly, the

CV method for LA-AIDS demand has a ‘totalRevenue’ argument, which if set equal to the

representative agent’s income (e.g. area GDP), converts the percent to levels.

29

Finally, it is worth noting that since none of the demand models included in an-

titrust contain income effects, it can be shown that compensating variation equals

two other measures of consumer welfare: equivalent variation and consumer sur-

plus.36

1.3.6 Defining Antitrust Markets

According to the 2010 Horizontal Merger Guidelines issued by the U.S Department

of Justice (DOJ) and the Federal Trade Commission (FTC), the purpose of market

definition is twofold:

First, market definition helps specify the line of commerce and section

of the country in which the competitive concern arises. In any merger

enforcement action, the Agencies will normally identify one or more rele-

vant markets in which the merger may substantially lessen competition.

Second, market definition allows the Agencies to identify market par-

ticipants and measure market shares and market concentration. [U.S

Department of Justice and the Federal Trade Commission, 2010, p. 7]

To assist users in identifying antitrust product and geographic markets, antitrust

includes the HypoMonTest method. HypoMonTest assumes that i) firms are playing

the differentiated Bertrand pricing game described earlier and ii) consumer demand

is characterized by one of the demand systems described earlier, and then performs

an implementation of the Hypothetical Monopolist Test described in the Guidelines

for a set of products specified in HypoMonTest’s ‘prodIndex’ argument. 37

Specifically, HypoMonTest first determines if ‘prodIndex’ contains at least one of the

merging parties’ products. If so, then by default HypoMonTest calls the calcPriceDeltaHypoMon

method to find the profit-maximizing prices that the Hypothetical Monopolist would

set on the products in ‘prodIndex’, holding the prices of all other products fixed at

36See Willig [1976].

37The Guidelines define the Hypothetical Monopolist Test for product market as positing

... a hypothetical profit-maximizing firm, not subject to price regulation, that was

the only present and future seller of those products (“hypothetical monopolist”) likely

would impose at least a small but significant and non-transitory increase in price

(“SSNIP”) on at least one product in the market, including at least one product sold

by one of the merging firms. For the purpose of analyzing this issue, the terms of

sale of products outside the candidate market are held constant. [U.S Department of

Justice and the Federal Trade Commission, 2010, p. 9]

The Guidelines describe a similar test for geographic market definition [U.S Department of

Justice and the Federal Trade Commission, 2010, p. 13]

30

(predicted) pre-merger levels. HypoMonTest then compares the largest price change

across the merging parties’ products indexed in ‘prodIndex’ to the specified ‘ssnip’.

If this price change is greater than the specified ‘ssnip’, HypoMonTest returns TRUE.

Otherwise, HypoMonTest returns FALSE.

The Guidelines state that

... if the market includes a second product, the Agencies will normally

also include a third product if that third product is a closer substitute

for the first product than is the second product. The third product is a

closer substitute if, in response to a SSNIP on the first product, greater

revenues are diverted to the third product than the second product [U.S

Department of Justice and the Federal Trade Commission, 2010, p. 9].

To facilitate such comparisons, antitrust’s Bertrand model includes the diversionHypoMon

method, which, for a set of products specified using the ‘prodIndex’ argument, re-

turns the revenue diversion (as defined by equation 1.2.2)38 matrix for all products

included in the merger simulation (i.e. all products placed under the Hypothetical

Monopolist’s control as well as those outside of its control).

1.3.7 Simulating Merger Effects With Known Demand Parameters

Until now, most of the discussion has focused on how to recover demand parame-

ters when users have information on shares, margins, and in most cases, prices. To

accommodate known demand parameters (e.g. there is sufficient data to employ

econometric methods to estimate demand parameters), antitrust contains the sim

function. The sim function allows users to simulate price effects (or the output from

any method listed in Table 7.2) from a merger under the assumption that firms are

playing a Bertrand differentiated pricing game. sim requires users to specify a vector

of market prices, demand form (either “Linear”, “AIDS”, “LogLin”, “Logit”, “CES”,

“LogitNests”, “LogitCap”, or “CESNests”), a list containing the known demand pa-

rameters, and pre- and post-merger ownership information. See the sim help page

for further details.

1.4 Gotchas

This section alerts users to some instances where antitrust may produce seemingly

surprising results, and provides some potential explanations for these behaviors.

38The Guidelines do not provide a formula for revenue diversion.

31

1.4.1 Market Definition

As discussed above, HypoMon method is a post-simulation command and therefore

is run only after the user has assumed i) which firms (and products) are playing

a differentiated Bertrand pricing game, and ii) the demand system. As a result,

HypoMon and diversionHypoMon can never be applied to a set of products that

includes any product excluded from the merger simulation.

1.4.2 Log-Linear Demand

loglinear always predicts no price effects for single-product firms in the market who

are not party to the acquisition. This occurs because the FOC for a single-product

firm producing iis mi=1

ii =1

βii . Since the Bertrand model described earlier

assumes constant marginal costs, a constant ii implies that prices are constant as

well.

Although a single-product non-merging party’s prices will not change, its output will

increase. This occurs because the acquisition will increase the price of the merging

parties’ products as well as the prices of multi-product non-merging parties. These

price increases will entice some customers to switch towards the single-product firms’

products, increasing their output.

1.4.3 LA-AIDS Demand

As discussed earlier, aids attempts to calibrate , the market elasticity parameter,

by using the FOCs, LA-AIDS demand, and additional margins. For some combina-

tions of margins and shares, however, this procedure can yield a very large market

elasticity estimate, which in turn will yield small price effects from the merger. This

issue appears to occur because the set of FOCs that are being used to calibrate this

parameter are nearly co-linear. Issues arising from co-linearity can be often be reme-

died by supplying additional margin information, supplying margin information for

products with disparate market shares, or supplying the market elasticity parameter

directly.

32

2 The Cournot Quantity Game

Another model included in antitrust is the Cournot quantity game. This version

of the game assumes that multi-plant firms with distinct, increasing marginal costs

producing multiple products simultaneously set plant output for each product to

maximize their profits. All firms producing a particular product are assumed to

be undifferentiated. In this model, quantities are strategic substitutes in the sense

that decreasing the quantity of one product causes some customers to switch to

competing manufacturers, raising their quantities and profits. Ultimately, it is the

magnitude of these lost sales that, at the margin, dissuades firms from reducing their

output further .

Similar to the Bertrand model, mergers are modeled by assuming that the merg-

ing parties’ plants are placed under common ownership, which allows the merged

entity to recapture some of the sales that would otherwise be lost to competitors.

As a result, the Cournot model (for some demand systems) predicts that absent

any efficiencies affecting the marginal cost of production, the prices of all products

produced by the merging parties will increase, possibly by a small amount.

Because all firms are manufacturing an identical version of the product, this version

of the Cournot model allows firms post-merger to start or stop producing other

products. This model does not allow for firms to engage in some forms of price

discrimination.1

2.1 The Game

Suppose that there are Kfirms in a market, each producing a subset Jkof Jproducts.

Further, suppose that that each of the k∈Kfirms manufactures its Jkproducts

at nkplants. Let n=Pk∈Knkdenote the total number of plants producing any

of the Jproducts. The Cournot model assumes that firms simultaneously set the

amount of each product produced at each plant in order to maximize their profits.

This model also assumes that all firms can perfectly observe each others’ quantities,

1In particular, this version of the Bertrand model does not accommodate non-linear pricing, such

as is used in 2nd or 3rd degree price discrimination.

33

and costs, as well as the demand for each product.

Functions in antitrust’s Cournot model also adopt the additional assumption that

each firm’s plant has its own distinct marginal cost technology.

2.1.1 The Mathematical Model

Firm k∈Kchooses product output at each plant {qr

j}j∈jk,

r∈nk

so as to maximize profits.

Mathematically, firm ksolves:

max

{qr

j}j∈Jk,

r∈nk

,X

j∈Jk,

r∈nk

pjqr

j−X

r∈nk

cr(qr)

subject to

qr

j≥0,

qr=X

j∈Jk

qr

j

where pj, the price sold of product i, is assumed to be a twice differentiable function

of all firm quantities with ∂pj

∂qr

j<0 for all plants and firms . Likewise, additively

separable plant variable costs crassumed to be twice differentiable with ∂cr

∂qr

j>0 .

Differentiating profits with respect to each qr

jyields the following first order condi-

tions (FOCs):

∂qr

j≡pj+X

l∈nk

ql

j

∂pj

∂qr

j

−∂cr

∂qr

j

= 0 for all j∈Jk,r∈nk(2.1.1)

2.2 Calibrating Model Demand and Cost Parameters

The Cournot model can yield different equilibrium quantity and price predictions

depending on 1) the curvature of plant variable costs and 2) the curvature of demand.

antitrust allows users to explore the consequences of different cost and demand

assumptions.

34

Currently, cournot contains two different ways to specify plant costs. First, users

can set the ‘cost’ option equal to a n-length character vector whose values are either

equal to “linear” for linear marginal costs (∂cr

∂qr

j= 0.5γrPj∈nrqr

j) or “constant” for

constant marginal costs ( ∂cr

∂qr

j=γr) . When the ‘cost’ option is employed, cournot’s

calcSlopes method uses observed costs (implied by predicted margins and prices)

and prices to calibrate plant-level cost parameters γr.

Alternatively, users can specify both plant level marginal and variable costs. Marginal

costs may be specified by setting the ‘mcfunPre’ argument equal to a length nlist

of functions that each take as an input the vector of product quantities produced

at a plant and then return the marginal cost associated with producing that level

of output at that plant. Likewise, the ‘vcfunPre’ argument can be similarly used to

specify plant-level variable costs. Note that when marginal costs and variable costs

are specified in this manner, cournot makes no attempt to calibrate any parameters

on the cost side.

Currently, cournot allows users to specify that product demand is either linear (pj=

bj+ajPk∈nqk

j) or log-linear (ln(pj) = bj+ajln(Pk∈nqk

j)) Users can specify product

demand by setting cournot’s ‘demand’ argument equal to a j-length character vector

equal to either “linear” for linear demand or “log” for log-linear demand.

2.3 Simulating Merger Effects

2.3.1 Summarizing Results

The summary method may be used to summarize the results of a merger between two

firms. By default, the summary method reports pre- and post-merger equilibrium

prices and quantities for each product included in the simulation. Also reported is the

compensating marginal cost reduction (CMCR) as well as the change in consumer

surplus from the merger. Setting the ‘market’ argument equal to FALSE returns

plant-level equilibrium price effects.

2.3.2 Simulating Price Effects With Marginal Cost Efficiencies

Absent efficiencies, the Cournot model with the demand systems described here will

almost always produce a (possibly negligible) post-merger price increase among sub-

stitutes. These price increases, however, can be offset by merger-specific efficiencies

35

that decrease the incremental costs of some of the merging firms’ products.2

All the functions discussed above allow users to evaluate these efficiencies in two

different ways. First, all of these functions contain the ‘mcDelta’ argument, which

allows users to specify the proportional change in a product’s marginal costs that

may result from a merger. These cost changes are factored into the post-merger price

equilibrium calculation made by the calcPrices method. If changes in marginal

costs are not expected to be proportional, then users can instead set the ‘mcfun-

Pre’ and ‘mcfunPost’ arguments equal to lists containing functions that return each

plants’ pre- and post-merger marginal costs3.

Second, users can call the cmcr method on the output of any of the functions de-

scribed above. This method computes the compensating marginal cost reduction

(CMCR) on the merging parties’ products. CMCR is the percentage decrease in the

marginal costs of the merging parties’ products necessary to prevent a post-merger

price increase. See the cmcr help page for further details.

2.3.3 Simulating Price Effects With Capacity Constraints

The Cournot model allows users to impose capacity constraints that may potentially

change as a result of the merger. The “capacitiesPre” argument allows users to

specify a vector of pre-merger plant-specific capacity constraints (default is Inf, or

no constraint). The “capacitiesPost” argument allows users to specify a vector of

post-merger constraints (default is “capacitiesPre”).

2.3.4 Excluding Products or Plants

By default, the Cournot model calculates a merger’s effects under the assumption

that the acquisition does not change the set of products available to consumers or

the set of plants that are in production. A merger’s effects, however, may differ

if the merger induces either the merging parties or another market participant to

eliminate some products from their portfolio or to alter the mix of plants used in

producing their products.

To accommodate the possibility that some products or plants may be removed from

the market following an acquisition, all the constructor functions described above

have a ‘productsPre’ and a ‘productsPost’ arguments that allows users to specify

2Costs that are not strictly increasing with a product’s output (i.e. fixed or sunk costs) do not

affect the price setting behavior of firms in a Bertrand pricing game.

3Users will also have to specify plant-specific variable costs as well using the ‘vcfunPre’ and ‘vc-

funPost’ arguments.

36

an nby Jlogical matrix which equals TRUE if a product produced at a particular

plant should be included in the merger simulation and FALSE otherwise. By default,

‘productsPre’ equals TRUE if the ‘quantities’ is not NA, and FALSE otherwise, while

‘productsPost’ equals ‘productsPre’.

2.3.5 Measuring Changes In Consumer Welfare

The Cournot model has a CV method which may be used to calculate the change in

consumer surplus from a merger.

2.3.6 Allowing For First-Mover Advantage

The package contains a stackelberg function that is similar to cournot, but also

allows for one or more firms to be designated as output leaders for certain products.

Output leaders are assumed to set their output levels first, and conditional on the

leaders’ output decisions, output followers (defined as everyone who is not a leader)