2017 Publication 225 P225

User Manual: 225

Open the PDF directly: View PDF ![]() .

.

Page Count: 90

- Contents

- Introduction

- Future Developments

- What's New for 2017

- What's New for 2018

- Reminders

- Chapter 1 Importance of Records

- Chapter 2 Accounting Methods

- Chapter 3 Farm Income

- Chapter 4 Farm Business Expenses

- What's New for 2017

- Introduction

- Deductible Expenses

- Prepaid Farm Supplies

- Prepaid Livestock Feed

- Labor Hired

- Repairs and Maintenance

- Interest

- Breeding Fees

- Fertilizer and Lime

- Taxes

- Insurance

- Rent and Leasing

- Depreciation

- Business Use of Your Home

- Truck and Car Expenses

- Travel Expenses

- Marketing Quota Penalties

- Tenant House Expenses

- Items Purchased for Resale

- Other Expenses

- Domestic Production Activities Deduction

- Capital Expenses

- Nondeductible Expenses

- Losses From Operating a Farm

- Not-for-Profit Farming

- Chapter 5 Soil and Water Conservation Expenses

- Chapter 6 Basis of Assets

- Chapter 7 Depreciation, Depletion, and Amortization

- What's New for 2017

- What’s New for 2018

- Introduction

- Overview of Depreciation

- What Property Can Be Depreciated?

- What Property Cannot Be Depreciated?

- When Does Depreciation Begin and End?

- Can You Use MACRS To Depreciate Your Property?

- What Is the Basis of Your Depreciable Property?

- How Do You Treat Repairs and Improvements?

- Do You Have To File Form 4562?

- How Do You Correct Depreciation Deductions?

- Section 179 Expense Deduction

- Claiming the Special Depreciation Allowance

- Figuring Depreciation Under MACRS

- Which Depreciation System (GDS or ADS) Applies?

- Which Property Class Applies Under GDS?

- What Is the Placed-in-Service Date?

- What Is the Basis for Depreciation?Basis of assets

- Which Recovery Period Applies?

- Which Convention Applies?Modified ACRS (MACRS)

- Which Depreciation Method Applies?

- How Is the Depreciation Deduction Figured?Modified ACRS (MACRS)

- How Do You Use General Asset Accounts?

- When Do You Recapture MACRS Depreciation?

- Additional Rules for Listed Property

- Depletion

- Amortization

- Chapter 8 Gains and Losses

- Chapter 9 Dispositions of Property Used in Farming

- Chapter 10 Installment Sales

- Chapter 11 Casualties, Thefts, and Condemnations

- Chapter 12 Self-Employment Tax

- Chapter 13 Employment Taxes

- What's New for 2017

- What's New for 2018

- Reminders

- Important Dates for 2018

- Introduction

- Farm Employment

- Family Employees

- Crew Leaders

- Social Security and Medicare Taxes

- Federal Income Tax Withholding

- Required Notice to Employees About Earned Income Credit (EIC)

- Reporting and Paying Social Security, Medicare, and Withheld Federal Income Taxes

- Federal Unemployment (FUTA) Tax

- Chapter 14 Fuel Excise Tax Credits and Refunds

- Chapter 15 Estimated Tax

- Chapter 16 How To Get Tax Help

- Index

Contents

Introduction .................. 1

What's New for 2017 ............. 2

What's New for 2018 ............. 2

Reminders ................... 3

Chapter 1. Importance of Records .... 3

Chapter 2. Accounting Methods ..... 5

Chapter 3. Farm Income .......... 8

Chapter 4. Farm Business

Expenses ................ 18

Chapter 5. Soil and Water

Conservation Expenses ....... 26

Chapter 6. Basis of Assets ....... 29

Chapter 7. Depreciation, Depletion,

and Amortization ........... 35

Chapter 8. Gains and Losses ...... 47

Chapter 9. Dispositions of

Property Used in Farming ..... 55

Chapter 10. Installment Sales ..... 59

Chapter 11. Casualties, Thefts, and

Condemnations ............ 64

Chapter 12. Self-Employment Tax ... 72

Chapter 13. Employment Taxes .... 76

Chapter 14. Fuel Excise Tax

Credits and Refunds ......... 81

Chapter 15. Estimated Tax ....... 84

Chapter 16. How To Get Tax Help ... 86

Index ..................... 88

Introduction

You are in the business of farming if you culti-

vate, operate, or manage a farm for profit, either

as owner or tenant. A farm includes livestock,

dairy, poultry, fish, fruit, and truck farms. It also

includes plantations, ranches, ranges, and or-

chards and groves.

This publication explains how the federal tax

laws apply to farming. Use this publication as a

guide to figure your taxes and complete your

farm tax return. If you need more information on

a subject, get the specific IRS tax publication

covering that subject. We refer to many of these

free publications throughout this publication.

See chapter 16 for information on ordering

these publications.

The explanations and examples in this publi-

cation reflect the Internal Revenue Service's in-

terpretation of tax laws enacted by Congress,

Treasury regulations, and court decisions. How-

ever, the information given does not cover ev-

ery situation and is not intended to replace the

Department

of the

Treasury

Internal

Revenue

Service

Publication 225

Cat. No. 11049L

Farmer's

Tax Guide

For use in preparing

2017 Returns

Acknowledgment: The valuable advice and assistance given us each

year by the National Farm Income Tax Extension Committee is

gratefully acknowledged.

Get forms and other information faster and easier at:

•IRS.gov (English)

•IRS.gov/Spanish (Español)

•IRS.gov/Chinese (中文)

•IRS.gov/Korean (한국어)

•IRS.gov/Russian (Pусский)

•IRS.gov/Vietnamese (TiếngViệt)

Userid: CPM Schema: tipx Leadpct: 100% Pt. size: 8 Draft Ok to Print

AH XSL/XML Fileid: … tions/P225/2017/A/XML/Cycle02/source (Init. & Date) _______

Page 1 of 90 15:09 - 19-Oct-2017

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Oct 19, 2017

law or change its meaning. This publication

covers subjects on which a court may have ren-

dered a decision more favorable to taxpayers

than the interpretation of the Service. Until

these differing interpretations are resolved by

higher court decisions, or in some other way,

this publication will continue to present the in-

terpretation of the Service.

The IRS Mission. Provide America's taxpay-

ers top quality service by helping them under-

stand and meet their tax responsibilities and by

applying the tax law with integrity and fairness

to all.

Comments and suggestions. We welcome

your comments about this publication and your

suggestions for future editions.

You can send us comments from IRS.gov/

FormsPubs. Or you can write to:

Internal Revenue Service

Tax Forms and Publications

1111 Constitution Ave. NW, IR-6526

Washington, DC 20224

Although we cannot respond individually to

each comment received, we do appreciate your

feedback and will consider your comments as

we revise our tax products.

Ordering forms and publications. Visit

IRS.gov/FormsPubs to download forms and

publications. Otherwise, you can go to IRS.gov/

FormsPubs to order current and prior-year

forms and instructions. Your order should arrive

within 10 business days.

Tax questions. If you have a tax question

not answered by this publication, check

IRS.gov and How To Get Tax Help at the end of

this publication.

Comments on IRS enforcement actions.

The Small Business and Agricultural Regulatory

Enforcement Ombudsman and 10 Regional

Fairness Boards were established to receive

comments from small business about federal

agency enforcement actions. The Ombudsman

will annually evaluate the enforcement activities

of each agency and rate its responsiveness to

small business. If you wish to comment on the

enforcement actions of the IRS, you can:

Call 1-888-734-3247,

Fax your comments to 202-481-5719,

Write to

Office of the National Ombudsman

U.S. Small Business Administration

409 3rd Street, S.W.

Washington, DC 20416

Send an email to ombudsman@sba.gov,

or

Complete and submit a Federal Agency

Comment Form online at

www.sba.gov/ombudsman/comment.

Treasury Inspector General for Tax Admin-

istration (TIGTA). If you want to confidentially

report misconduct, waste, fraud, or abuse by an

IRS employee, you can call 1-800-366-4484

(1-800-877-8339 for TTY/TDD users). You can

remain anonymous.

Farm tax classes. Many state Cooperative

Extension Services conduct farm tax work-

shops in conjunction with the IRS. Contact your

county or regional extension office for more in-

formation.

Rural Tax Education website. The Rural Tax

Education website is a source for information

concerning agriculturally related income and

deductions and self-employment tax. The web-

site is available for farmers and ranchers, other

agricultural producers, Extension educators,

and any one interested in learning about the tax

side of the agricultural community. Members of

the National Farm Income Tax Extension Com-

mittee are contributors for the website and the

website is hosted by Utah State University Co-

operative Extension. You can visit the website

at www.ruraltax.org.

Future Developments

The IRS has created a page on IRS.gov for

information about Pub. 225, at

IRS.gov/Pub225. Information about recent

developments affecting Pub. 225 will be posted

on that page.

What's New for 2017

The following items highlight a number of

administrative and tax law changes for 2017.

They are discussed in more detail throughout

the publication.

Disaster relief for Hurricanes Harvey, Irma,

and Maria. Disaster tax relief was enacted for

those impacted by Hurricane Harvey, Irma, or

Maria, including provisions that modified (the

limit on the deduction for charitable contribu-

tions/the treatment of withdrawal of retirement

funds/disaster-related employment relief/the

calculation of casualty and theft losses). See

Pub. 976, Disaster Relief, for more information.

Standard mileage rate. For 2017, the stand-

ard mileage rate for the cost of operating your

car, van, pickup, or panel truck for each mile of

business use is 53.5 cents. See chapter 4.

Increased section 179 expense deduction

dollar limits. The maximum amount you can

elect to deduct for most section 179 property

you placed in service in 2017 is $510,000. This

limit is reduced by the amount by which the cost

of the property placed in service during the tax

year exceeds $2,030,000. See chapter 7.

Disaster losses. A new Section D has been

added to Form 4684 to make an election (or re-

voke a prior election) to deduct a loss attributa-

ble to a federally declared disaster in the tax

year immediately before the disaster year. See

Pub. 547 for more information about disaster

losses. See chapter 11.

Maximum net earnings. The maximum net

self-employment earnings subject to the social

security part (12.4%) of the self-employment tax

is $127,200 for 2017, up from $118,500 in both

2016 and 2015. There is no maximum limit on

earnings subject to the Medicare part (2.9%) or,

if applicable, the Additional Medicare Tax

(0.9%). See chapter 12.

Social security and Medicare tax for 2017.

The social security tax rate is 6.2% each for the

employee and employer, unchanged from

2016. The social security wage base limit is

$127,200.

The Medicare tax rate is 1.45% each for the

employee and employer, unchanged from

2016. There is no wage base limit for Medicare

tax. See chapter 13.

New certification program for professional

employer organizations. The Tax Increase

Prevention Act of 2014 required the IRS to es-

tablish a voluntary certification program for pro-

fessional employer organizations (PEOs).

PEOs handle various payroll administration and

tax reporting responsibilities for their business

clients and are typically paid a fee based on

payroll costs. To become and remain certified

under the certification program, certified profes-

sional employer organizations (CPEOs) must

meet various requirements described in sec-

tions 3511 and 7705 and related published

guidance. Certification as a CPEO may affect

the employment tax liabilities of both the CPEO

and its customers. A CPEO is generally treated

as the employer of any individual who performs

services for a customer of the CPEO and is cov-

ered by a contract described in section 7705(e)

(2) between the CPEO and the customer

(CPEO contract), but only for wages and other

compensation paid to the individual by the

CPEO. For more information, go to IRS.gov/

CPEO. Also see Rev. Proc. 2017-14, 2017-3

I.R.B. 426, available at IRS.gov/irb/

2017-03_IRB/ar14.html. See chapter 13.

Qualified small business payroll tax credit

for increasing research activities. For tax

years beginning after December 31, 2015, a

qualified small business may elect to claim up

to $250,000 of its credit for increasing research

activities as a payroll tax credit against the em-

ployer's share of social security tax. The portion

of the credit used against the employer's share

of social security tax is allowed in the first calen-

dar quarter beginning after the date that the

qualified small business filed its income tax re-

turn. The first Form 943 that you can claim this

credit on is Form 943 filed for calendar year

2017. For more information, see the Instructions

for Form 943. See chapter 13.

What's New for 2018

Phase down of the special depreciation al-

lowance. The special depreciation allowance

will be phased down to 40% for certain property

placed in service after December 31, 2017, and

certain plants bearing fruits and nuts or grafted

after December 31, 2017. See chapter 7.

Maximum net earnings. The maximum net

self-employment earnings subject to the social

security part of the self-employment tax for

2018 will be discussed in the 2017 Pub. 334.

See chapter 12.

Social security and Medicare tax for 2018.

The employee and employer tax rates for social

security and the maximum amount of wages

subject to social security tax for 2018 will be

discussed in Pub. 51 (For use in 2018).

The Medicare tax rate for 2018 will also be

discussed in Pub. 51 (For use in 2018). There is

no limit on the amount of wages subject to Med-

icare tax. See chapter 13.

Page 2 of 90 Fileid: … tions/P225/2017/A/XML/Cycle02/source 15:09 - 19-Oct-2017

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Page 2 Publication 225 (2017)

Reminders

The following reminders and other items may

help you file your tax return.

IRS e-file (Electronic Filing)

You can file your tax returns electronically

using an IRS e-file option. The benefits of IRS

e-file include faster refunds, increased accu-

racy, and acknowledgment of IRS receipt of

your return. You can use one of the following

IRS e-file options.

Use an authorized IRS e-file provider.

Use a personal computer.

Visit a Volunteer Income Tax Assistance

(VITA) or Tax Counseling for the Elderly

(TCE) site.

For details on these fast filing methods, see

your income tax package.

Principal agricultural activity codes. You

must enter on line B of Schedule F (Form 1040)

a code that identifies your principal agricultural

activity. It is important to use the correct code

because this information will identify market

segments of the public for IRS Taxpayer Educa-

tion programs. The U.S. Census Bureau also

uses this information for its economic census.

See the list of Principal Agricultural Activity Co-

des on page 2 of Schedule F (Form 1040).

Publication on employer identification num-

bers (EINs). Pub. 1635, Understanding Your

Employer Identification Number, provides gen-

eral information on EINs. Topics include how to

apply for an EIN and how to complete Form

SS-4.

Change of address. If you change your home

address, you should use Form 8822, Change of

Address, to notify the IRS. If you change your

business address, you should use Form

8822-B, Change of Address or Responsible

Party — Business, to notify the IRS. Be sure to

include your suite, room, or other unit number.

Reportable transactions. You must file Form

8886, Reportable Transaction Disclosure State-

ment, to report certain transactions. You may

have to pay a penalty if you are required to file

Form 8886 but do not do so. Reportable trans-

actions include (1) transactions the same as or

substantially similar to tax avoidance transac-

tions identified by the IRS, (2) transactions of-

fered to you under conditions of confidentiality

and for which you paid an advisor a minimum

fee, (3) transactions for which you have or a re-

lated party has a right to a full or partial refund

of fees if all or part of the intended tax conse-

quences from the transaction are not sustained,

(4) transactions that result in losses of at least

$2 million in any single year or $4 million in any

combination of years, and (5) transactions with

asset holding periods of 45 days or less and

that result in a tax credit of more than $250,000.

For more information, see the Instructions for

Form 8886.

Form W-4 for 2017. You should make new

Forms W-4 available to your employees and en-

courage them to check their income tax with-

holding for 2017. Those employees who owed

a large amount of tax or received a large refund

for 2016 may need to submit a new Form W-4.

Form 1099-MISC. Generally, file Form

1099-MISC if you pay at least $600 in rents,

services, and other miscellaneous payments in

your farming business to an individual (for ex-

ample, an accountant, an attorney, or a veteri-

narian) who is not your employee. Payments

made to corporations for medical and health

care payments, including payments made to

veterinarians, generally must be reported on

Form 1099.

Limited liability company (LLC). For purpo-

ses of this publication, a limited liability com-

pany (LLC) is a business entity organized in the

United States under state law. Unlike a partner-

ship, all of the members of an LLC have limited

personal liability for its debts. An LLC may be

classified for federal income tax purposes as a

partnership, corporation, or an entity disregar-

ded as separate from its owner by applying the

rules in Regulations section 301.7701-3. See

Pub. 3402 for more details.

Photographs of missing children. The Inter-

nal Revenue Service is a proud partner with the

National Center for Missing & Exploited

Children® (NCMEC). Photographs of missing

children selected by the Center may appear in

this publication on pages that would otherwise

be blank. You can help bring these children

home by looking at the photographs and calling

1-800-THE-LOST (1-800-843-5678) (24 hours

a day, 7 days a week) if you recognize a child.

1.

Importance of

Records

Introduction

A farmer, like other taxpayers, must keep re-

cords to prepare an accurate income tax return

and determine the correct amount of tax. This

chapter explains the benefits of keeping re-

cords, what kinds of records you must keep,

and how long you must keep them for federal

tax purposes.

Tax records are not the only type of records

you need to keep for your farming business.

You should also keep records that measure

your farm's financial performance. This publica-

tion only discusses tax records.

The Farm Financial Standards Council has

produced a publication that provides a detailed

explanation of the recommendations of the

Council for financial reporting and analysis. For

information on recordkeeping, you can pur-

chase and download 2017 Financial Guidelines

for Agriculture at www.ffsc.org. For more infor-

mation, contact Countryside Marketing, Inc. in

the following manner.

Call 262-253-6902.

Send a fax to 262-253-6903.

Write to:

Farm Financial Standards Council

N78 W14573 Appleton Ave., #287

Menomonee Falls, WI 53051.

Topics

This chapter discusses:

Benefits of recordkeeping

Kinds of records to keep

How long to keep records

Useful Items

You may want to see:

Publication

(Circular A), Agricultural Employer's

Tax Guide

Travel, Entertainment, Gift, and Car

Expenses

See chapter 16 for information about getting

publications.

Benefits of

Recordkeeping

Everyone in business, including farmers, must

keep appropriate records. Recordkeeping will

help you do the following.

Monitor the progress of your farming busi-

ness. You need records to monitor the pro-

gress of your farming business. Records can

show whether your business is improving,

which items are selling, or what changes you

need to make. Records can help you make bet-

ter decisions that may increase the likelihood of

business success.

Prepare your financial statements. You

need records to prepare accurate financial

statements. These include income (profit and

loss) statements, cash flow statements, and

balance sheets. These statements can help you

in dealing with your bank or creditors and help

you to manage your farm business.

Identify source of receipts. You will receive

money, property, and/or services from many

sources. Your records can identify the source of

your receipts. You need this information to sep-

arate farm from nonfarm receipts and taxable

from nontaxable income.

Keep track of deductible expenses. You

may forget expenses when you prepare your

tax return unless you record them when they

occur.

Prepare your tax returns. You need records

to prepare your tax return. For example, your

records must support the income, expenses,

and credits you report. Generally, these are the

same records you use to monitor your farming

business and prepare your financial statements.

Support items reported on tax returns. You

must keep your business records available at all

51

463

Page 3 of 90 Fileid: … tions/P225/2017/A/XML/Cycle02/source 15:09 - 19-Oct-2017

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Chapter 1 Importance of Records Page 3

times for inspection by the IRS. If the IRS exam-

ines any of your tax returns, you may be asked

to explain the items reported. A complete set of

records will speed up the examination.

Kinds of Records

To Keep

Except in a few cases, the law does not require

any specific kind of records. You can choose

any recordkeeping system suited to your farm-

ing business that clearly shows, for example,

your income and expenses.

You should set up your recordkeeping sys-

tem using an accounting method that clearly

shows your income for your tax year. If you are

in more than one business, you should keep a

complete and separate set of records for each

business. A corporation should keep minutes of

board of directors' meetings. See

chapter 2 for more information.

Your recordkeeping system should include a

summary of your business transactions. This

summary is ordinarily made in accounting jour-

nals and ledgers. For example, they must show

your gross income, as well as your deductions

and credits. In addition, you must keep support-

ing documents. Purchases, sales, payroll, and

other transactions you have in your business

generate supporting documents such as invoi-

ces and receipts. These documents contain the

information you need to record in your journals

and ledgers.

It is important to keep these documents be-

cause they support the entries in your journals

and ledgers and on your tax return. Keep them

in an orderly fashion and in a safe place. For in-

stance, organize them by year and type of in-

come or expense.

Electronic records. All requirements that ap-

ply to hard copy books and records also apply

to electronic storage systems that maintain tax

books and records. When you replace hard

copy books and records, you must maintain the

electronic storage systems for as long as they

are material to the administration of tax law.

An electronic storage system is any system

for preparing or keeping your records either by

electronic imaging or by transfer to an elec-

tronic storage media. The electronic storage

system must index, store, preserve, retrieve,

and reproduce the electronically stored books

and records in legible format. All electronic stor-

age systems must provide a complete and ac-

curate record of your data that is accessible to

the IRS.

Electronic storage systems are also subject

to the same controls and retention guidelines as

those imposed on your original hard copy

books and records. The original hard copy

books and records may be destroyed provided

that the electronic storage system has been

tested to establish that the hard copy books and

records are being reproduced in compliance

with IRS requirements for an electronic storage

system and procedures are established to en-

sure continued compliance with all applicable

rules and regulations. You still have the respon-

sibility of retaining any other books and records

that are required to be retained.

The IRS may test your electronic storage

system, including the equipment used, indexing

methodology, software, and retrieval capabili-

ties. This test is not considered an examination

and the results must be shared with you. If your

electronic storage system meets the require-

ments mentioned earlier, you will be in compli-

ance. If not, you may be subject to penalties for

non-compliance, unless you continue to main-

tain your original hard copy books and records

in a manner that allows you and the IRS to de-

termine your correct tax. For details on elec-

tronic storage system requirements, see Rev.

Proc. 97-22. You can find Rev. Proc. 97-22 on

page 9 of Internal Revenue Bulletin 1997-13 at

IRS.gov/Pub/irs-irbs/irb97-13.pdf.

Travel, transportation, entertainment, and

gift expenses. Specific recordkeeping rules

apply to these expenses. For more information,

see Pub. 463.

Employment taxes. There are specific em-

ployment tax records you must keep. For a list,

see Pub. 51 (Circular A).

Excise taxes. See How To Claim a Credit or

Refund in chapter 14 for the specific records

you must keep to verify your claim for credit or

refund of excise taxes on certain fuels.

Assets. Assets are the property, such as ma-

chinery and equipment, you own and use in

your business. You must keep records to verify

certain information about your business assets.

You need records to figure your annual depreci-

ation deduction and the gain or (loss) when you

sell the assets. Your records should show all

the following.

When and how you acquired the asset.

Purchase price.

Cost of any improvements.

Section 179 deduction taken.

Deductions taken for depreciation.

Deductions taken for casualty losses, such

as losses resulting from fires or storms.

How you used the asset.

When and how you disposed of the asset.

Selling price.

Expenses of sale.

The following are examples of records that

may show this information.

Purchase and sales invoices.

Real estate closing statements.

Canceled checks.

Bank statements.

Financial account statements as proof of

payment. If you do not have a canceled check,

you may be able to prove payment with certain

financial account statements prepared by finan-

cial institutions. These include account state-

ments prepared for the financial institution by a

third party. These account statements must be

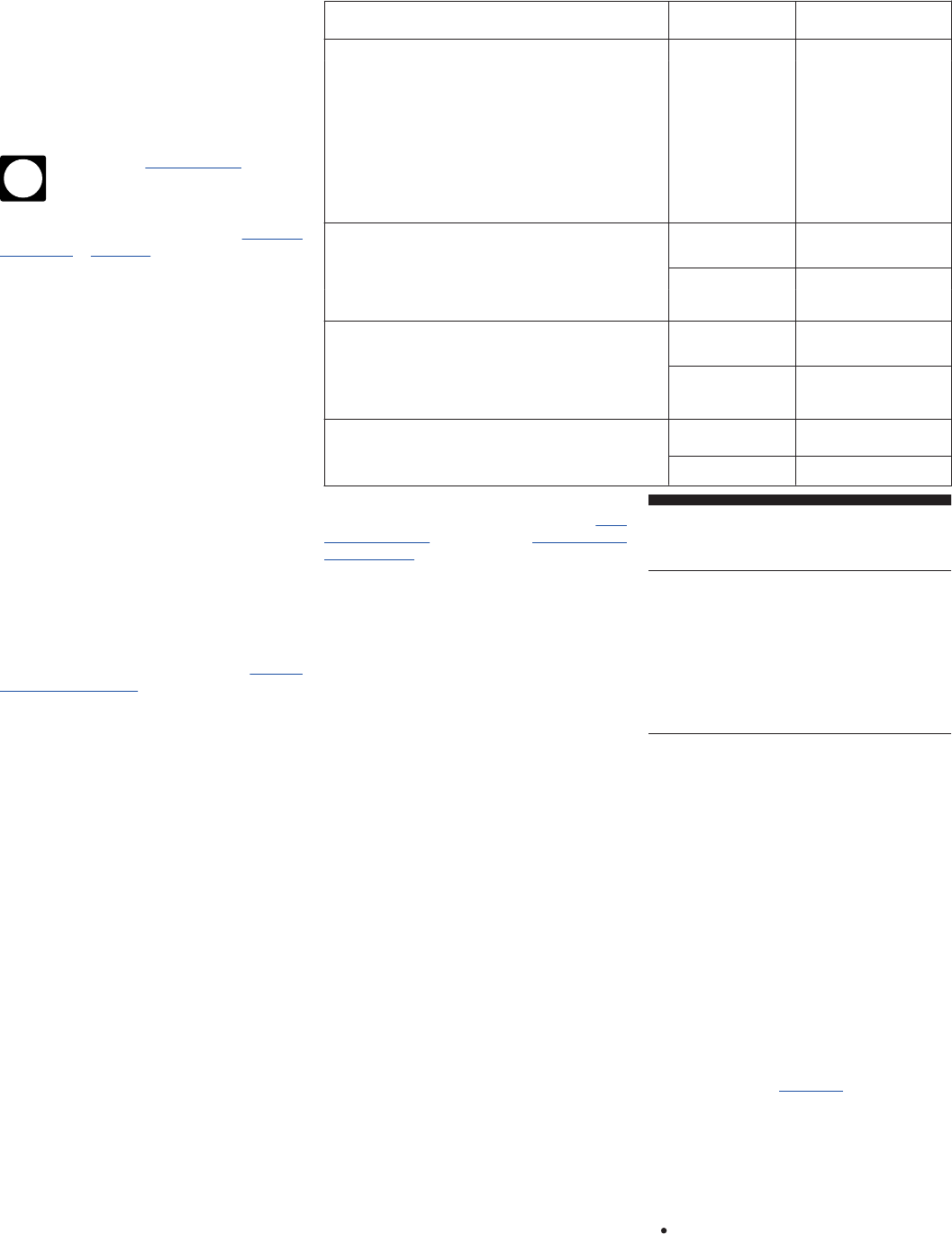

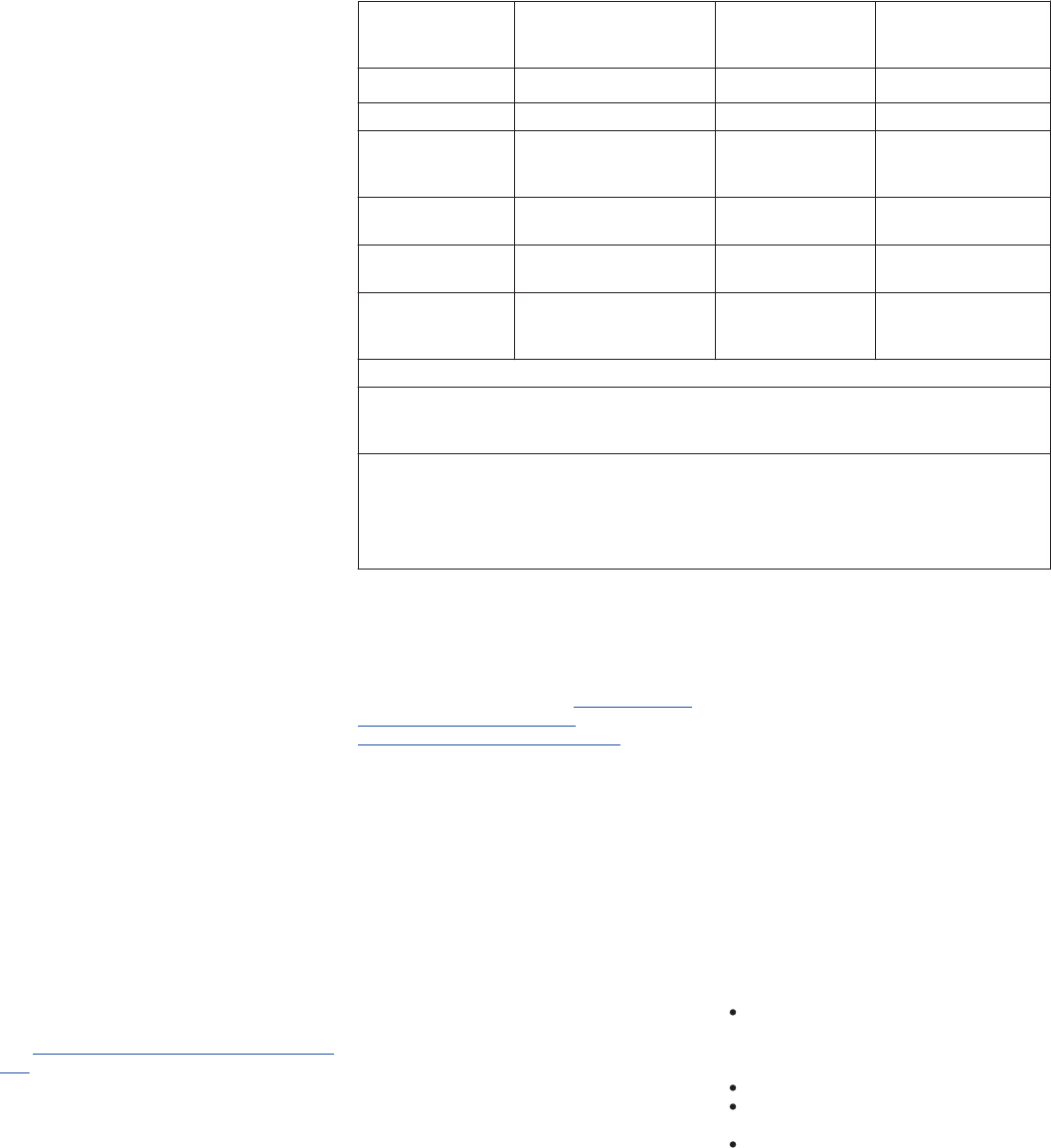

legible. The following table lists acceptable ac-

count statements.

IF payment is by...

THEN the statement must

show the...

Check Check number.

Amount.

Payee's name.

Date the check amount

was posted to the

account by the financial

institution.

Electronic funds

transfer

Amount transferred.

Payee's name.

Date the transfer was

posted to the account by

the financial institution.

Credit card Amount charged.

Payee's name.

Transaction date.

Proof of payment of an amount, by it-

self, does not establish you are entitled

to a tax deduction. You should also

keep other documents, such as credit card

sales slips and invoices, to show that you also

incurred the cost.

Tax returns. Keep copies of your filed tax re-

turns. They help in preparing future tax returns

and making computations if you file an amen-

ded return. Keep copies of your information re-

turns such as Form 1099, Schedule K-1, and

Form W-2.

How Long To Keep

Records

You must keep your records as long as they

may be needed for the administration of any

provision of the Internal Revenue Code. Keep

records that support an item of income or a de-

duction appearing on a return until the period of

limitations for the return runs out. A period of

limitations is the period of time after which no le-

gal action can be brought. Generally, that

means you must keep your records for at least

3 years from when your tax return was due or

filed or within 2 years of the date the tax was

paid, whichever is later. However, certain re-

cords must be kept for a longer period of time,

as discussed below.

Employment taxes. If you have employees,

you must keep all employment tax records for at

least 4 years after the date the tax becomes

due or is paid, whichever is later.

Assets. Keep records relating to property until

the period of limitations expires for the year in

which you dispose of the property in a taxable

disposition. You must keep these records to fig-

ure any depreciation, amortization, or depletion

deduction and to figure your basis for comput-

ing gain or (loss) when you sell or otherwise dis-

pose of the property.

You may need to keep records relating to

the basis of property longer than the period of

limitation. Keep those records as long as they

are important in figuring the basis of the original

or replacement property. Generally, this means

as long as you own the property and, after you

dispose of it, for the period of limitations that ap-

plies to you. For example, if you received

CAUTION

!

Page 4 of 90 Fileid: … tions/P225/2017/A/XML/Cycle02/source 15:09 - 19-Oct-2017

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Page 4 Chapter 1 Importance of Records

property in a nontaxable exchange, you must

keep the records for the old property, as well as

for the new property, until the period of limita-

tions expires for the year in which you dispose

of the new property in a taxable disposition. For

more information on basis, see chapter 6.

Records for nontax purposes. When your

records are no longer needed for tax purposes,

do not discard them until you check to see if

you have to keep them longer for other purpo-

ses. For example, your insurance company or

creditors may require you to keep them longer

than the IRS does.

2.

Accounting

Methods

Introduction

You must use an accounting method that

clearly shows the income and expenses used to

figure your taxable income. You must also file

an income tax return for an annual accounting

period called a tax year.

This chapter discusses accounting meth-

ods. For information on accounting periods, see

Pub. 538, Accounting Periods and Methods,

and the Instructions for Form 1128, Application

To Adopt, Change, or Retain a Tax Year.

Topics

This chapter discusses:

Cash method

Accrual method

Farm inventory

Special methods of accounting

Changes in methods of accounting

Useful Items

You may want to see:

Publication

Accounting Periods and Methods

Business Expenses

Form (and Instructions)

Application To Adopt, Change, or

Retain a Tax Year

Application for Change in

Accounting Method

See chapter 16 for information about getting

publications and forms.

538

535

1128

3115

Accounting Methods

An accounting method is a set of rules used to

determine when and how your income and ex-

penses are reported on your tax return. Your

accounting method includes not only your over-

all method of accounting, but also the account-

ing treatment you use for any material item.

Facts and circumstances affect whether an

item is material. Generally, an item considered

material for financial statement purposes is also

considered material for income tax purposes.

See Pub. 538 for more information.

You generally choose an accounting

method for your farm business when you file

your first income tax return that includes a

Schedule F (Form 1040), Profit or Loss From

Farming. If you later want to change your ac-

counting method, you generally must get IRS

approval. How to obtain IRS approval is dis-

cussed later under Changes in Methods of Ac-

counting.

Types of accounting methods. Generally,

you can use any of the following accounting

methods. Each method is discussed in detail

below.

Cash method.

Accrual method.

Special methods of accounting for certain

items of income and expenses.

Combination (hybrid) method using ele-

ments of two or more of the above meth-

ods.

Business and other items. You can account

for business and personal items using different

accounting methods. For example, you can fig-

ure your business income under an accrual

method, even if you use the cash method to fig-

ure personal items.

Two or more businesses. If you operate two

or more separate and distinct businesses, you

can use a different accounting method for each

business. Generally, no business is separate

and distinct unless a complete and separate set

of books and records is maintained for each

business.

Cash Method

Most farmers use the cash method because

they find it easier to keep records using the

cash method. However, certain farm corpora-

tions and partnerships and all tax shelters must

use an accrual method of accounting. See Ac-

crual Method Required, later. Also, see Inven-

tory, later.

Income

Under the cash method, include in your gross

income all items of income you actually or con-

structively received during the tax year. Items of

income include money received as well as

property or services received. If you receive

property or services, you must include the fair

market value (FMV) of the property or services

in income. See chapter 3 for information on how

to report farm income on your income tax re-

turn.

Constructive receipt. Income is construc-

tively received when an amount is credited to

your account or made available to you without

restriction. You do not need to have possession

of the income for it to be treated as income for

the tax year. If you authorize someone to be

your agent and receive income for you, you are

considered to have received the income when

your agent receives it. Income is not construc-

tively received if your receipt of the income is

subject to substantial restrictions or limitations.

Delaying receipt of income. You cannot

hold checks or postpone taking possession of

similar property from one tax year to another to

avoid paying tax on the income. You must re-

port the income in the year the money or prop-

erty is received or made available to you with-

out restriction.

Example. Frances Jones, a farmer who

uses the cash method of accounting, was enti-

tled to receive a $10,000 payment on a grain

contract in December 2017. She was told in De-

cember that her payment was available. She re-

quested not to be paid until January 2018. Fran-

ces must include this payment in her 2017

income because it was made available to her in

2017.

Debts paid by another person or can-

celed. If your debts are paid by another person

or are canceled by your creditors, you may

have to report part or all of this debt relief as in-

come. If you receive income in this way, you

constructively receive the income when the

debt is canceled or paid. See Cancellation of

Debt in chapter 3 for more information.

Deferred payment contract. If you sell an

item under a deferred payment contract that

calls for payment in a future year, there is no

constructive receipt in the year of sale. How-

ever, if the sales contract states that you have

the right to the proceeds of the sale from the

buyer at any time after delivery of the item, then

you must include the sales price in income in

the year of the sale, regardless of when you ac-

tually receive payment.

Example. You are a farmer who uses the

cash method and a calendar tax year. You sell

grain in December 2017 under a bona fide

arm's-length contract that calls for payment in

2018. You include the proceeds from the sale in

your 2018 gross income since that is the year

payment is received. However, if the contract

states that you have the right to the proceeds

from the buyer at any time after the grain is de-

livered, you must include the sales price in your

2017 income, even if payment is received in the

following year.

Repayment of income. If you include an

amount in income and in a later year you have

to repay all or part of it, then you can usually de-

duct the repayment in the year repaid. If the re-

payment is more than $3,000, a special rule ap-

plies. For details, see Repayments in

chapter 11 of Pub. 535, Business Expenses.

Page 5 of 90 Fileid: … tions/P225/2017/A/XML/Cycle02/source 15:09 - 19-Oct-2017

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Chapter 2 Accounting Methods Page 5

Expenses

Under the cash method, generally you deduct

expenses in the tax year you pay them. This in-

cludes business expenses for which you con-

test liability. However, you may not be able to

deduct an expense paid in advance or you may

be required to capitalize certain costs, as ex-

plained under Uniform Capitalization Rules in

chapter 6. See chapter 4 for information on how

to deduct farm business expenses on your in-

come tax return.

Prepayment. Generally, you cannot deduct

expenses paid in advance. This rule applies to

any expense paid far enough in advance to, in

effect, create an asset with a useful life extend-

ing substantially beyond the end of the current

tax year.

Example. On November 1, 2017, you

signed and paid $3,600 for a 3-year (36-month)

insurance contract for equipment. In 2017, you

are allowed to deduct only $200 (2/36 x $3,600)

of the cost of the policy that is attributable to

2017. In 2018, you'll be able to deduct $1,200

(12/36 x $3,600); in 2019, you'll be able to de-

duct $1,200 (12/36 x $3,600); and in 2020 you'll

be able to deduct the remaining balance of

$1,000.

An exception applies if the expense qualifies

for the 12-month rule. See Pub. 538 for more in-

formation and examples.

See chapter 4 for special rules for prepaid

farm supplies and prepaid livestock feed.

Accrual Method

Under an accrual method of accounting, you

generally report income in the year earned and

deduct or capitalize expenses in the year incur-

red. The purpose of an accrual method of ac-

counting is to correctly match income and ex-

penses. Certain businesses engaged in farming

must use an accrual method of accounting for

its farm business and for sales and purchases

of inventory items. See Accrual Method Re-

quired and Farm Inventory, later.

Income

Generally, you include an amount in income for

the tax year in which all events that fix your right

to receive the income have occurred, and you

can determine the amount with reasonable ac-

curacy. Under this rule, include an amount in in-

come on the earliest of the following dates.

When you receive payment.

When the income amount is due to you.

When you earn the income.

When title passes.

If you use an accrual method of accounting,

complete Part III of Schedule F (Form 1040) to

report your income.

Inventory

If you keep an inventory, generally you must

use an accrual method of accounting to deter-

mine your gross income. An inventory is neces-

sary to clearly show income when the produc-

tion, purchase, or sale of merchandise is an

income-producing factor. See Pub. 538 for

more information. Also, see Farm Inventory,

later, for more information on items that must be

included in inventory by farmers, and inventory

valuation methods for farmers.

Expenses

Under an accrual method of accounting, you

generally deduct or capitalize a business ex-

pense when both of the following apply.

1. The all-events test has been met. This test

is met when:

a. All events have occurred that fix the

fact that you have a liability, and

b. The amount of the liability can be de-

termined with reasonable accuracy.

2. Economic performance has occurred.

Economic performance. Generally, you can-

not deduct or capitalize a business expense un-

til economic performance occurs. If your ex-

pense is for property or services provided to

you, or for your use of property, economic per-

formance occurs as the property or services are

provided or as the property is used. If your ex-

pense is for property or services you provide to

others, economic performance occurs as you

provide the property or services.

Example. Jane, who is a farmer, uses a

calendar tax year and an accrual method of ac-

counting. She entered into a contract with ABC

Farm Consulting in 2016. The contract stated

that Jane pay ABC Farm Consulting $2,000 in

December 2016. It further stipulates that ABC

Farm Consulting will develop a plan for integrat-

ing her farm with a larger farm operation based

in a neighboring state by March 1, 2017. Jane

paid ABC Farm Consulting $2,000 in December

2016. Integration of operations according to the

plan began in May 2017 and they completed

the integration in December 2017.

Economic performance for Jane's liability in

the contract occurs as the services are provi-

ded. Jane incurs the $2,000 cost in 2017, even

though a payment was made in the prior year.

An exception to the economic performance

rule allows certain recurring items to be treated

as incurred during a tax year even though eco-

nomic performance has not occurred. For more

information, see Economic Performance in Pub.

538.

Special rule for related persons. Business

expenses and interest owed to a related person

who uses the cash method of accounting are

not deductible until you make the payment and

the corresponding amount is includible in the

related person's gross income. Determine the

relationship for this rule as of the end of the tax

year for which the expense or interest would

otherwise be deductible.

Accrual Method Required

Generally, the following businesses, if engaged

in farming, must use an accrual method of ac-

counting.

1. A corporation (other than a family corpora-

tion) that had gross receipts of more than

$1,000,000 for any tax year beginning af-

ter 1975.

2. A family corporation that had gross re-

ceipts of more than $25,000,000 for any

tax year beginning after 1985.

3. A partnership with a corporation as a part-

ner, if that corporation meets the require-

ments of (1) or (2) above.

4. A tax shelter.

Note. Items (1), (2), and (3) above do not

apply to an S corporation or a business operat-

ing a nursery or sod farm, or the raising or har-

vesting of trees (other than fruit and nut trees).

Family corporation. A family corporation is

generally a corporation that meets one of the

following ownership requirements.

Members of the same family own at least

50% of the total combined voting power of

all classes of stock entitled to vote and at

least 50% of the total shares of all other

classes of stock of the corporation.

Members of two families have owned, di-

rectly or indirectly, since October 4, 1976,

at least 65% of the total combined voting

power of all classes of voting stock and at

least 65% of the total shares of all other

classes of the corporation's stock.

Members of three families have owned, di-

rectly or indirectly, since October 4, 1976,

at least 50% of the total combined voting

power of all classes of voting stock and at

least 50% of the total shares of all other

classes of the corporation's stock. In addi-

tion, substantially all the stock not owned

by the three families is owned directly by

either the employees of the corporation,

family members of employees, or a trust

for the benefit of the employees.

For more information on family corporations,

see Internal Revenue Code section 447.

Tax shelter. A tax shelter is a partnership,

noncorporate enterprise, or S corporation that

meets either of the following tests.

1. Its principal purpose is the avoidance or

evasion of federal income tax.

2. It is a farming syndicate. A farming syndi-

cate is an entity that meets either of the

following tests.

a. Interests in the activity have been of-

fered for sale in an offering required to

be registered with a federal or state

agency with the authority to regulate

the offering of securities for sale.

b. More than 35% of the losses during

the tax year are allocable to limited

partners or limited entrepreneurs.

A “limited partner” is one whose personal li-

ability for partnership debts is limited to the

money or other property the partner contributed

or is required to contribute to the partnership.

A “limited entrepreneur” is one who has an

interest in an enterprise other than as a limited

partner and does not actively participate in the

management of the enterprise.

Page 6 of 90 Fileid: … tions/P225/2017/A/XML/Cycle02/source 15:09 - 19-Oct-2017

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Page 6 Chapter 2 Accounting Methods

Farm Inventory

If you are required to keep an inventory, you

should keep a complete record of your inven-

tory as part of your farm records. This record

should show the actual count or measurement

of the inventory. It should also show all factors

that enter into its valuation, including quality and

weight, if applicable. Below are some items that

could be included in inventory.

Hatchery business. If you are in the hatchery

business, and use an accrual method of ac-

counting, you must include in inventory eggs in

the process of incubation.

Products held for sale. All harvested and pur-

chased farm products held for sale or for feed

or seed, such as grain, hay, silage, concen-

trates, cotton, tobacco, etc., must be included in

inventory.

Supplies. Supplies acquired for sale or that

become a physical part of items held for sale

must be included in inventory. Deduct the cost

of supplies in the year used or consumed in op-

erations. Do not include incidental supplies in

inventory as these are deductible in the year of

purchase.

Livestock. Livestock held primarily for sale

must be included in inventory. Livestock held

for draft, breeding, or dairy purposes can either

be depreciated or included in inventory. Also

seeUnit-livestock-price method, later. If you are

in the business of breeding and raising chinchil-

las, mink, foxes, or other fur-bearing animals,

these animals are livestock for inventory purpo-

ses.

Growing crops. Generally, growing crops are

not required to be included in inventory. How-

ever, if the crop has a preproductive period of

more than 2 years, you may have to capitalize

(or include in inventory) costs associated with

the crop. See Uniform capitalization rules be-

low. Also, see Uniform Capitalization Rules in

chapter 6.

Items to include in inventory. Your inventory

should include all items held for sale, or for use

as feed, seed, etc., whether raised or pur-

chased, that are unsold at the end of the year.

Uniform capitalization rules. The following

applies if you are required to use an accrual

method of accounting.

The uniform capitalization rules apply to all

costs of raising a plant, even if the prepro-

ductive period of raising a plant is 2 years

or less.

The costs of animals are subject to the uni-

form capitalization rules.

Inventory valuation methods. The following

methods, described below, are those generally

available for valuing inventory. The method you

use must conform to generally accepted ac-

counting principles for similar businesses and

must clearly reflect income.

Cost.

Lower of cost or market.

Farm-price method.

Unit-livestock-price method.

Cost and lower of cost or market meth-

ods. See Pub. 538 for information on these val-

uation methods.

If you value your livestock inventory at

cost or the lower of cost or market, you

do not need IRS approval to change to

the unit-livestock-price method. However, if you

value your livestock inventory using the

farm-price method, then you must obtain per-

mission from the IRS to change to the unit-live-

stock-price method.

Farm-price method. Under this method,

each item, whether raised or purchased, is val-

ued at its market price less the direct cost of

disposition. Market price is the current price at

the nearest market in the quantities you usually

sell. Cost of disposition includes broker's com-

missions, freight, hauling to market, and other

marketing costs. If you use this method, you

must use it for your entire inventory, except that

livestock can be inventoried under the unit-live-

stock-price method.

Unit-livestock-price method. This method

recognizes the difficulty of establishing the ex-

act costs of producing and raising each animal.

You group or classify livestock according to

type and age and use a standard unit price for

each animal within a class or group. The unit

price you assign should reasonably approxi-

mate the normal costs incurred in producing the

animals in such classes. Unit prices and classi-

fications are subject to approval by the IRS on

examination of your return. You must annually

reevaluate your unit livestock prices and adjust

the prices upward or downward to reflect in-

creases or decreases in the costs of raising

livestock. IRS approval is not required for these

adjustments. Any other changes in unit prices

or classifications do require IRS approval.

If you use this method, include all raised

livestock in inventory, regardless of whether

they are held for sale or for draft, breeding,

sport, or dairy purposes. This method accounts

only for the increase in cost of raising an animal

to maturity. It does not provide for any decrease

in the animal's market value after it reaches ma-

turity. Also, if you raise cattle, you are not re-

quired to inventory hay you grow to feed your

herd.

Do not include sold or lost animals in the

year-end inventory. If your records do not show

which animals were sold or lost, treat the first

animals acquired as sold or lost. The animals

on hand at the end of the year are considered

those most recently acquired.

You must include in inventory all livestock

purchased primarily for sale. You can choose

either to include in inventory or depreciate live-

stock purchased for draft, breeding, sport, or

dairy purposes. However, you must be consis-

tent from year to year, regardless of the method

you have chosen. You cannot change your

method without obtaining approval from the

IRS.

You must include in inventory animals pur-

chased after maturity or capitalize them at their

purchase price. If the animals are not mature at

purchase, increase the cost at the end of each

tax year according to the established unit price.

However, in the year of purchase, do not in-

crease the cost of any animal purchased during

the last 6 months of the year. This “no increase”

TIP

rule does not apply to tax shelters which must

make an adjustment for any animal purchased

during the year. It also does not apply to taxpay-

ers that must make an adjustment to reasona-

bly reflect the particular period in the year in

which animals are purchased, if necessary to

avoid significant distortions in income.

Uniform capitalization rules. A farmer

can determine costs required to be allocated

under the uniform capitalization rules by using

the farm-price or unit-livestock-price inventory

method. This applies to any plant or animal,

even if the farmer does not hold or treat the

plant or animal as inventory property.

Cash Versus Accrual Method

The following examples compare the cash and

accrual methods of accounting.

Example 1. You are a farmer who uses an

accrual method of accounting. You keep your

books on the calendar year basis. You sell grain

in December 2017 but you are not paid until

January 2018. Because the accrual method

was used and 2017 was the tax year in which

the grain was sold, you must include both the

sales proceeds and deduct the costs incurred in

producing the grain on your 2017 tax return.

Example 2. Assume the same facts as in

Example 1 except that you use the cash

method and there was no constructive receipt

of the sales proceeds in 2017. Under the cash

method, you include the sales proceeds in in-

come in 2018, the year you receive payment.

Deduct the costs of producing the grain in the

year you pay for them.

Special Methods

of Accounting

There are special methods of accounting for

certain items of income and expense.

Crop method. If you do not harvest and dis-

pose of your crop in the same tax year that you

plant it, you can, with IRS approval, use the

crop method of accounting. You cannot use the

crop method for any tax return, including your

first tax return, unless you receive approval

from the IRS. Under this method, you deduct

the entire cost of producing the crop, including

the expense of seed or young plants, in the year

you realize income from the crop.

See chapter 4 for details on deducting the

costs of operating a farm. Also see Regulations

section 1.162-12.

Other special methods. Other special meth-

ods of accounting apply to the following items.

Amortization, see chapter 7.

Casualties, see chapter 11.

Condemnations, see chapter 11.

Depletion, see chapter 7.

Depreciation, see chapter 7.

Farm business expenses, see chapter 4.

Farm income, see chapter 3.

Installment sales, see chapter 10.

Soil and water conservation expenses, see

chapter 5.

Thefts, see chapter 11.

Page 7 of 90 Fileid: … tions/P225/2017/A/XML/Cycle02/source 15:09 - 19-Oct-2017

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Chapter 2 Accounting Methods Page 7

Combination Method

Generally, you can use any combination of

cash, accrual, and special methods of account-

ing if the combination clearly shows your in-

come and expenses and you use it consistently.

However, the following restrictions apply.

If you use the cash method for figuring

your income, you must use the cash

method for reporting your expenses.

If you use an accrual method for reporting

your expenses, you must use an accrual

method for figuring your income.

Changes in Methods of

Accounting

A change in your method of accounting in-

cludes a change in:

Your overall method, such as from the

cash method to an accrual method, and

Your treatment of any material item, such

as a change in your method of valuing in-

ventory (for example, a change from the

farm-price method to the unit-live-

stock-price method, discussed earlier).

Generally, once you have set up your account-

ing method, you must receive approval from the

IRS before you can change either an overall

method of accounting or the accounting treat-

ment of any material item. A user fee may be re-

quired for any non-automatic change requests.

To obtain approval, you must generally file

Form 3115. However, there are instances when

you can obtain automatic consent to change

certain methods of accounting. For more infor-

mation, see the Instructions for Form 3115.

Also, see Pub. 538.

3.

Farm Income

Introduction

You may receive income from many sources.

You must report the income from all the differ-

ent sources on your tax return, unless it is ex-

cluded by law. Where you report the income on

your tax return depends on its source.

This chapter discusses farm income you re-

port on Schedule F (Form 1040), Profit or Loss

From Farming. For information on where to re-

port other income, see the Instructions for Form

1040, U.S. Individual Income Tax Return.

Accounting method. The rules discussed in

this chapter assume you use the cash method

of accounting. Under the cash method, you

generally include an item of income in gross in-

come in the year you receive it. See Cash

Method in chapter 2.

If you use an accrual method of accounting,

different rules may apply to your situation. See

Accrual Method in chapter 2.

Topics

This chapter discusses:

Schedule F

Sales of farm products

Rents (including crop shares)

Agricultural program payments

Income from cooperatives

Cancellation of debt

Income from other sources

Income averaging for farmers

Useful Items

You may want to see:

Publication

Taxable and Nontaxable Income

Sales and Other Dispositions of

Assets

Investment Income and Expenses

Bankruptcy Tax Guide

Passive Activity and At-Risk Rules

Canceled Debts, Foreclosures,

Repossessions, and Abandonments

Form (and Instructions)

Reduction of Tax Attributes Due to

Discharge of Indebtedness

Supplemental

Income and Loss

Income Averaging for

Farmers and Fishermen

Certain Government Payments

Taxable Distributions

Received From Cooperatives

Sales of Business Property

Farm Rental Income and

Expenses

See chapter 16 for information about getting

publications and forms.

Schedule F (Form 1040)

Individuals, trusts, and partnerships report farm

income on Schedule F (Form 1040). Use this

schedule to figure the net profit or loss from reg-

ular farming operations.

525

544

550

908

925

4681

982

Sch E (Form 1040)

Sch J (Form 1040)

1099-G

1099-PATR

4797

4835

Corporations use Form 1120 to report

the income or loss from regular farming

operations.

Income from farming reported on Sched-

ule F includes amounts you receive from culti-

vating, operating, or managing a farm for gain

or profit, either as owner or tenant. This in-

cludes income from operating a stock, dairy,

poultry, fish, fruit, or truck farm and income from

operating a plantation, ranch, range, orchard, or

grove. It also includes income from the sale of

crop shares if you materially participate in pro-

ducing the crop. See Rents (Including Crop

Shares), later.

Income received from operating a nursery,

which specializes in growing ornamental plants,

is considered to be income from farming.

Income reported on Schedule F doesn't in-

clude gains or losses from sales or other dispo-

sitions of the following farm assets.

Land.

Depreciable farm equipment.

Buildings and structures.

Livestock held for draft, breeding, sport, or

dairy purposes.

Gains and losses from most dispositions of

farm assets are discussed in chapters 8 and 9.

Gains and losses from casualties, thefts, and

condemnations are discussed in chapter 11.

Sales of Farm Products

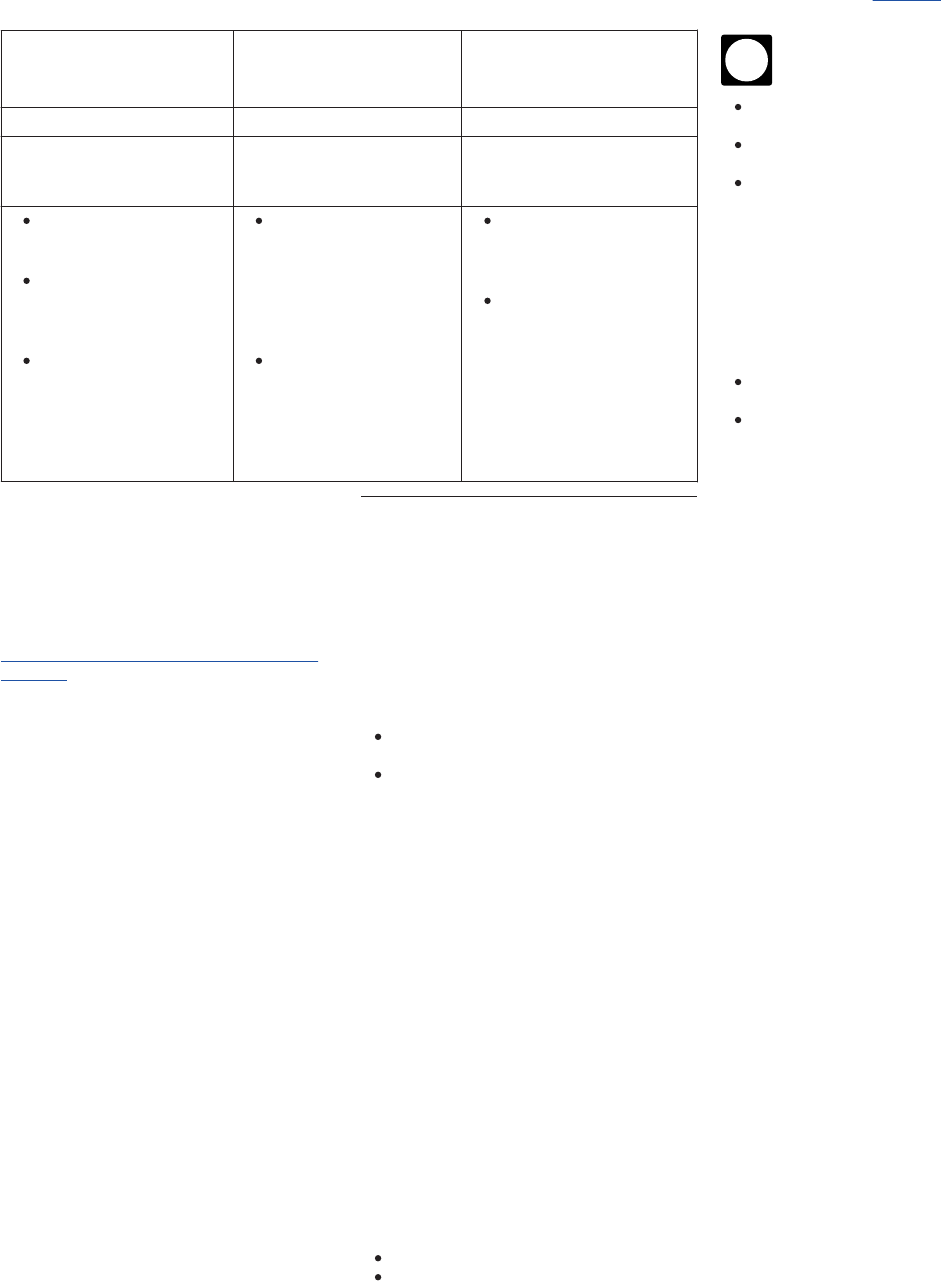

Where to report. Table 3-1 shows where to

report the sale of farm products on your tax re-

turn.

Schedule F. Amounts received from the

sales of products you raised on your farm for

sale (or bought for resale), such as livestock,

produce, or grains, are reported on Schedule F.

This includes money and the fair market value

of any property or services you receive. When

you sell farm products bought for resale, your

profit or loss is the difference between your sell-

ing price (money plus the fair market value of

any property) and your basis in the item (usually

the cost). See chapter 6 for information on the

basis of assets. You generally report these

amounts on Schedule F for the year you receive

payment.

Example. In 2016, you bought 20 feeder

calves for $27,000 for resale. You sold them in

2017 for $35,000. You report the $35,000 sales

price on Schedule F, line 1a, subtract your

$27,000 basis on line 1b, and report the

resulting $8,000 profit on line 1c.

TIP

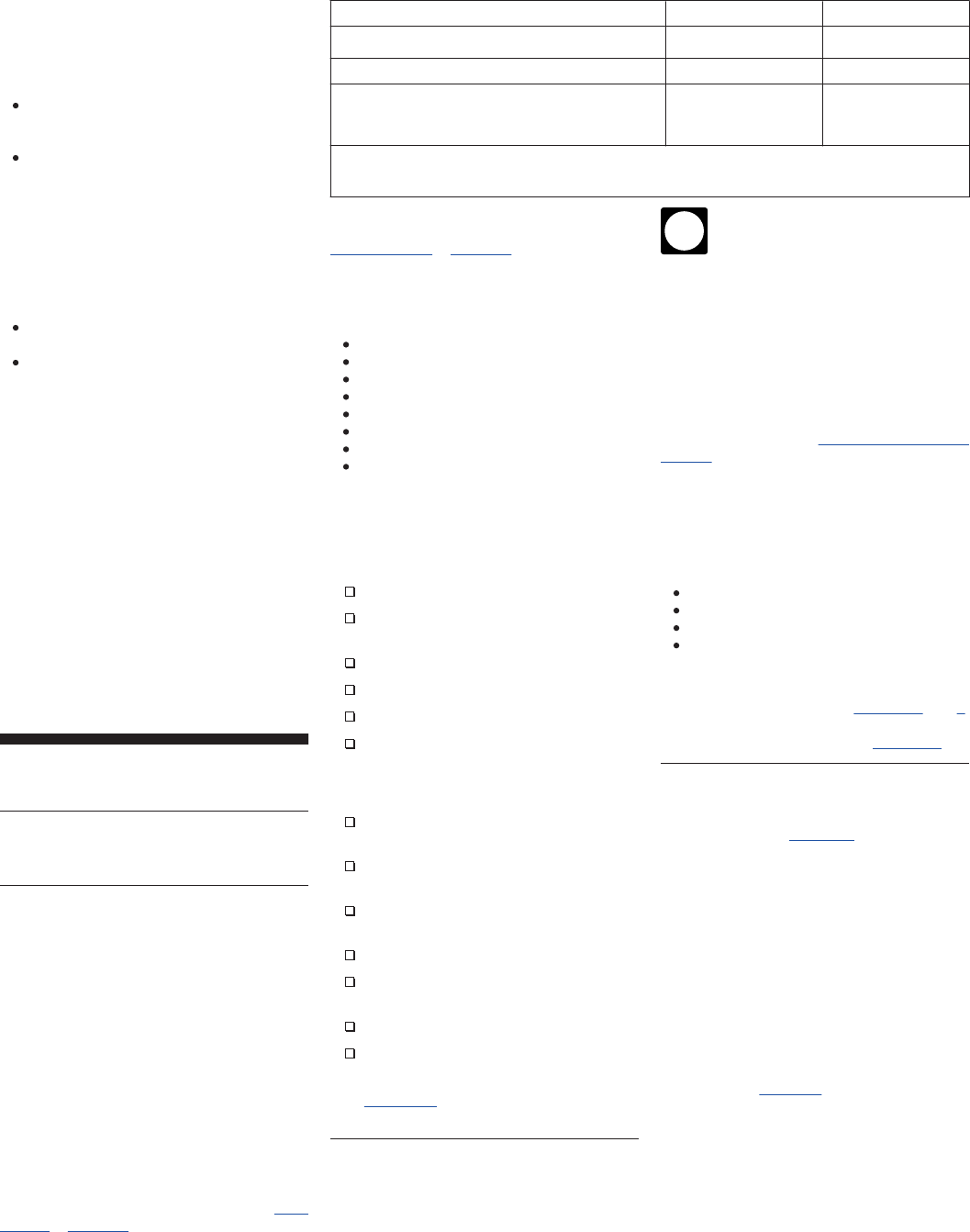

Table 3-1. Where To Report Sales of Farm Products

Item Sold Schedule F* Form 4797**

Farm products raised for sale X

Farm products bought for resale X

Farm assets not held primarily for sale, such as

livestock held for draft, breeding, sport, or dairy

purposes (bought or raised), equipment X

* See the Instructions for Schedule F for more information.

** See the Instructions for Form 4797 for more information.

Page 8 of 90 Fileid: … tions/P225/2017/A/XML/Cycle02/source 15:09 - 19-Oct-2017

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Page 8 Chapter 3 Farm Income

Form 4797. Sales of livestock held for

draft, breeding, sport, or dairy purposes may re-

sult in ordinary or capital gains or losses, de-

pending on the circumstances. In either case,

you should always report these sales on Form

4797 instead of Schedule F. See Livestock un-

der Ordinary or Capital Gain or Loss in chap-

ter 8. Animals you don't hold primarily for sale

are considered business assets of your farm.

Sale by agent. If your agent sells your farm

products, you have constructive receipt of the

income when your agent receives payment and

you must include the net proceeds from the sale

in gross income for the year the agent receives

payment. This applies even if your agent pays

you in a later year. For a discussion on con-

structive receipt of income, see Cash Method

under Accounting Methods in chapter 2.

Sales Caused by

Weather-Related Conditions

If you sell or exchange more livestock, including

poultry, than you normally would in a year be-

cause of a drought, flood, or other weather-rela-

ted condition, you may be able to postpone re-

porting the gain from the additional animals until

the next year. You must meet all the following

conditions to qualify.

Your principal trade or business is farming.

You use the cash method of accounting.

You can show that, under your usual busi-

ness practices, you wouldn't have sold or

exchanged the additional animals this year

except for the weather-related condition.

The weather-related condition caused an

area to be designated as eligible for assis-

tance by the federal government.

Disaster assistance and emergency

relief for individuals and busi-

nesses. Special tax law provisions

may help taxpayers and businesses recover fi-

nancially from the impact of a disaster, espe-

cially when the federal government declares

their location to be a major disaster area. Get

the latest tax relief guidance in disaster situa-

tions at IRS.gov/uac/tax-relief-in-disaster-

situations and in disaster area losses - agricul-

ture tax tips at IRS.gov/businesses/small-

businesses-self-employed/disaster-assistance-

and-emergency-relief-for-individuals-and-

businesses.

Sales or exchanges made before an area

became eligible for federal assistance qualify if

the weather-related condition that caused the

sale or exchange also caused the area to be

designated as eligible for federal assistance.

The designation can be made by the President,

the Department of Agriculture (or any of its

agencies), or by other federal departments or

agencies.

A weather-related sale or exchange of

livestock (other than poultry) held for

draft, breeding, or dairy purposes may

be an involuntary conversion. See Other Invol-

untary Conversions in chapter 11.

Usual business practice. You must deter-

mine the number of animals you would have

sold had you followed your usual business

TIP

TIP

practice in the absence of the weather-related

condition. Do this by considering all the facts

and circumstances, but don't take into account

your sales in any earlier year for which you

postponed the gain. If you haven't yet estab-

lished a usual business practice, rely on the

usual business practices of similarly situated

farmers in your general region.

Connection with affected area. The livestock

doesn't have to be raised or sold in an area af-

fected by a weather-related condition for the

postponement to apply. However, the sale must

occur solely because of a weather-related con-

dition that affected the water, grazing, or other

requirements of the livestock. This requirement

generally won't be met if the costs of feed, wa-

ter, or other requirements of the livestock affec-

ted by the weather-related condition aren't sub-

stantial in relation to the total costs of holding

the livestock.

Classes of livestock. You must figure the

amount to be postponed separately for each

generic class of animals—for example, hogs,

sheep, and cattle. Don’t separate animals into

classes based on age, sex, or breed.

Amount to be postponed. Follow these steps

to figure the amount of gain to be postponed for

each class of animals.

1. Divide the total income realized from the

sale of all livestock in the class during the

tax year by the total number of such live-

stock sold. For this purpose, don't treat

any postponed gain from the previous

year as income received from the sale of

livestock.

2. Multiply the result in (1) by the excess

number of such livestock sold solely be-

cause of weather-related conditions.

Example. You are a calendar year taxpayer

and you normally sell 100 head of beef cattle a

year. As a result of drought, you sold 135 head

during 2016. You realized $236,250 from the

sale ($236,250 ÷ 135= $1,750 per head). On

August 10, 2016, as a result of drought, the af-

fected area was declared a disaster area eligi-

ble for federal assistance. The income you can

postpone until 2017 is $61,250 [($236,250 ÷

135) × 35].

How to postpone gain. To postpone gain, at-

tach a statement to your tax return for the year

of the sale. The statement must include your

name and address and give the following infor-

mation for each class of livestock for which

you're postponing gain.

A statement that you're postponing gain

under section 451(e).

Evidence of the weather-related conditions

that forced the early sale or exchange of

the livestock and the date, if known, on

which an area was designated as eligible

for assistance by the federal government

because of weather-related conditions.

A statement explaining the relationship of

the area affected by the weather-related

condition to your early sale or exchange of

the livestock.

The number of animals sold in each of the

3 preceding years.

The number of animals you would have

sold in the tax year had you followed your

normal business practice in the absence of

weather-related conditions.

The total number of animals sold and the

number sold because of weather-related

conditions during the tax year.

A computation, as described above, of the

income to be postponed for each class of

livestock.

Generally, you must file the statement and

the return by the due date of the return, includ-

ing extensions. However, for sales or ex-

changes treated as an involuntary conversion

from weather-related sales of livestock in an

area eligible for federal assistance (discussed

in chapter 11), you can file this statement at any

time during the replacement period. For other

sales or exchanges, if you timely filed your re-

turn for the year without postponing gain, you

can still postpone gain by filing an amended re-

turn within 6 months of the due date of the re-

turn (excluding extensions). Attach the state-

ment to the amended return and write “Filed

pursuant to section 301.9100-2” at the top of

the amended return. File the amended return at

the same address you filed the original return.

Once you have filed the statement, you can

cancel your postponement of gain only with the

approval of the IRS.

Rents (Including Crop

Shares)

The rent you receive for the use of your farm-

land is generally rental income, not farm in-

come. However, the rent is farm income if:

1. Your arrangement with your tenant pro-

vides that the you will materially partici-

pate in the production or management of

production of the farm products on the

land, and

2. You materially participate.

See Landlord Participation in Farming in chap-

ter 12.

Pasture income and rental. If you pasture

someone else's livestock and take care of them

for a fee, the income is from your farming busi-

ness. You must enter it as Other income on

Schedule F. If you simply rent your pasture or

other farm real estate for a flat cash amount

without providing services, report the income as

rent on Part I of Schedule E (Form 1040).

Crop Shares

You must include rent you receive in the form of

crop shares in income in the year you convert

the shares to money or the equivalent of

money. It doesn't matter whether you use the

cash method of accounting or an accrual

method of accounting.

If you receive rent in the form of crop shares

or livestock, the rental income is included in

self-employment income if:

1. Your arrangement with your tenant pro-

vides that the you will materially partici-

pate in the production or management of

Page 9 of 90 Fileid: … tions/P225/2017/A/XML/Cycle02/source 15:09 - 19-Oct-2017

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Chapter 3 Farm Income Page 9

production of the farm products on the

land, and

2. You materially participate.

See Landlord Participation in Farming in chap-

ter 12. Report the rental income on Schedule F.

If

1. Your arrangement with your tenant doesn’t

provide that you will materially participate

in the production or management of pro-

duction of the farm products on the land,

or

2. You don't materially participate in operat-

ing the farm, report this income on Form

4835 and carry the net income or loss to

Schedule E (Form 1040).

The income isn't included in self-employment

income.

Crop shares you use to feed livestock.

Crop shares you receive as a landlord and feed

to your livestock are considered converted to

money when fed to the livestock. You must in-

clude the fair market value of the crop shares in

income at that time. You're entitled to a busi-

ness expense deduction for the livestock feed

in the same amount and at the same time you

include the fair market value of the crop share

as rental income. Although these two transac-

tions cancel each other for figuring adjusted

gross income on Form 1040, they may be nec-

essary to figure your self-employment tax. See

Landlord Participation in Farming and Farm Op-

tional Method in chapter 12.

Crop shares you give to others (gift). Crop

shares you receive as a landlord and give to

others are considered converted to money

when you make the gift. You must report the fair