2016 Publication 575 P575

User Manual: 575

Open the PDF directly: View PDF ![]() .

.

Page Count: 43

- Contents

- Reminders

- Introduction

- General Information

- Cost (Investment in the Contract)

- Taxation of Periodic Payments

- Taxation of Nonperiodic Payments

- Rollovers

- Special Additional Taxes

- Survivors and Beneficiaries

- How To Get Tax Help

- Index

Userid: CPM Schema: tipx Leadpct: 100% Pt. size: 10 Draft Ok to Print

AH XSL/XML Fileid: … tions/P575/2016/A/XML/Cycle02/source (Init. & Date) _______

Page 1 of 43 12:08 - 4-Jan-2017

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Department of the Treasury

Internal Revenue Service

Publication 575

Cat. No. 15142B

Pension

and Annuity

Income

For use in preparing

2016 Returns

Get forms and other information faster and easier at:

•IRS.gov (English)

•IRS.gov/Spanish (Español)

•IRS.gov/Chinese (中文)

•IRS.gov/Korean (한국어)

•IRS.gov/Russian (Pусский)

•IRS.gov/Vietnamese (TiếngViệt)

Contents

Reminders ............................... 1

Introduction .............................. 2

General Information ........................ 3

Variable Annuities ........................ 4

Section 457 Deferred Compensation Plans ...... 5

Disability Pensions ....................... 5

Insurance Premiums for Retired Public Safety

Officers ............................. 6

Railroad Retirement Benefits ................ 6

Withholding Tax and Estimated Tax ........... 9

Cost (Investment in the Contract) ............ 10

Taxation of Periodic Payments .............. 11

Fully Taxable Payments .................. 11

Partly Taxable Payments .................. 12

Taxation of Nonperiodic Payments ........... 15

Figuring the Taxable Amount ............... 15

Loans Treated as Distributions ............. 18

Transfers of Annuity Contracts .............. 19

Lump-Sum Distributions .................. 20

Rollovers ............................... 27

Special Additional Taxes ................... 31

Tax on Early Distributions ................. 32

Tax on Excess Accumulation ............... 35

Survivors and Beneficiaries ................. 37

How To Get Tax Help ...................... 37

Worksheet A. Simplified Method ............. 41

Index .................................. 42

Reminders

Future developments. For the latest information about

developments related to Pub. 575, such as legislation

enacted after it was published, go to www.irs.gov/pub575.

Net investment income tax. For purposes of the net in-

vestment income tax (NIIT), net investment income

doesn't include distributions from a qualified retirement

plan (for example, 401(a), 403(a), 403(b), 408, 408A, or

457(b) plans). However, these distributions are taken into

account when determining the modified adjusted gross in-

come threshold. Distributions from a nonqualified retire-

ment plan are included in net investment income. See

Form 8960, Net Investment Income Tax - Individuals, Es-

tates, and Trusts, and its instructions for more information.

Expanded exception to the tax on early distributions

from a governmental plan for qualified public safety

employees. For tax years beginning after December 31,

Jan 04, 2017

Page 2 of 43 Fileid: … tions/P575/2016/A/XML/Cycle02/source 12:08 - 4-Jan-2017

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

2015, in addition to those employees described in Quali

fied public safety employees, the definition is expanded to

include the following:

Federal law enforcement officers,

Federal customs and border protection officers,

Federal firefighters,

Air traffic controllers,

Nuclear materials couriers,

Members of the United States Capitol Police,

Members of the Supreme Court Police, and

Diplomatic security special agents of the United

States Department of State.

In addition, the exception to the tax is extended to distri-

butions from governmental defined contribution plans, as

well as governmental defined benefit plans.

For more information, see Tax on Early Distributions

later.

Rollovers to SIMPLE retirement accounts. You can

roll over amounts from a qualified retirement plan (as de-

scribed under Rollovers, later) or an IRA into a SIMPLE

retirement account as follows:

1. During the first 2 years of participation in a SIMPLE

retirement account, you may roll over amounts from

one SIMPLE retirement account into another SIMPLE

retirement account, and

2. After the first 2 years of participation in a SIMPLE re-

tirement account, you may roll over amounts from a

SIMPLE retirement account, a qualified retirement

plan or an IRA into a SIMPLE retirement account.

For more information, see Rollovers later.

Photographs of missing children. The Internal Reve-

nue Service is a proud partner with the National Center for

Missing & Exploited Children® (NCMEC). Photographs of

missing children selected by the Center may appear in

this publication on pages that would otherwise be blank.

You can help bring these children home by looking at the

photographs and calling 1-800-THE-LOST

(1-800-843-5678) if you recognize a child.

Introduction

This publication discusses the tax treatment of distribu-

tions you receive from pension and annuity plans and also

shows you how to report the income on your federal in-

come tax return. How these distributions are taxed de-

pends on whether they are periodic payments (amounts

received as an annuity) that are paid at regular intervals

over several years or nonperiodic payments (amounts not

received as an annuity).

What is covered in this publication? This publication

contains information that you need to understand the fol-

lowing topics.

How to figure the tax-free part of periodic payments

under a pension or annuity plan, including using a

simple worksheet for payments under a qualified plan.

How to figure the tax-free part of nonperiodic pay-

ments from qualified and nonqualified plans, and how

to use the optional methods to figure the tax on

lump-sum distributions from pension, stock bonus,

and profit-sharing plans.

How to roll over certain distributions from a retirement

plan into another retirement plan or IRA.

How to report disability payments, and how beneficia-

ries and survivors of employees and retirees must re-

port benefits paid to them.

How to report railroad retirement benefits.

When additional taxes on certain distributions may ap-

ply (including the tax on early distributions and the tax

on excess accumulation).

For additional information on how to report pen

sion or annuity payments on your federal income

tax return, be sure to review the instructions on

the back of Copies B, C, and 2 of the Form 1099R that

you received and the instructions for Form 1040, lines 16a

and 16b (Form 1040A, lines 12a and 12b or Form

1040NR, lines 17a and 17b).

A “corrected” Form 1099R replaces the corre

sponding original Form 1099R if the original

Form 1099R contained an error. Make sure you

use the amounts shown on the corrected Form 1099R

when reporting information on your tax return.

What isn't covered in this publication? The following

topics aren't discussed in this publication.

The General Rule. This is the method generally used

to determine the tax treatment of pension and annuity in-

come from nonqualified plans (including commercial an-

nuities). For a qualified plan, you generally can't use the

General Rule unless your annuity starting date is before

November 19, 1996. Although this publication will help

you determine whether you can use the General Rule, it

won't help you use it to determine the tax treatment of

your pension or annuity income. For that and other infor-

mation on the General Rule, see Pub. 939, General Rule

for Pensions and Annuities.

Individual retirement arrangements (IRAs). Infor-

mation on the tax treatment of amounts you receive from

an IRA is in Pub. 590-B, Distributions from Individual Re-

tirement Arrangements (IRAs).

Civil service retirement benefits. If you are retired

from the federal government (regular, phased, or disability

retirement) or are the survivor or beneficiary of a federal

employee or retiree who died, get Pub. 721, Tax Guide to

U.S. Civil Service Retirement Benefits. Pub. 721 covers

the tax treatment of federal retirement benefits, primarily

TIP

CAUTION

!

Page 2 Publication 575 (2016)

Page 3 of 43 Fileid: … tions/P575/2016/A/XML/Cycle02/source 12:08 - 4-Jan-2017

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

those paid under the Civil Service Retirement System

(CSRS) or the Federal Employees' Retirement System

(FERS). It also covers benefits paid from the Thrift Sav-

ings Plan (TSP).

Social security and equivalent tier 1 railroad retire

ment benefits. For information about the tax treatment of

these benefits, see Pub. 915, Social Security and Equiva-

lent Railroad Retirement Benefits. However, this publica-

tion (575) covers the tax treatment of the non-social se-

curity equivalent benefit portion of tier 1 railroad retirement

benefits, tier 2 benefits, vested dual benefits, and supple-

mental annuity benefits paid by the U.S. Railroad Retire-

ment Board.

Taxsheltered annuity plans (403(b) plans). If you

work for a public school or certain tax-exempt organiza-

tions, you may be eligible to participate in a 403(b) retire-

ment plan offered by your employer. Although this publi-

cation covers the treatment of benefits under 403(b) plans

and discusses in-plan Roth rollovers from 403(b) plans to

designated Roth accounts, it doesn't cover other tax provi-

sions that apply to these plans. For that and other informa-

tion on 403(b) plans, see Pub. 571, Tax-Sheltered Annuity

Plans (403(b) Plans) For Employees of Public Schools

and Certain Tax-Exempt Organizations.

Comments and suggestions. We welcome your com-

ments about this publication and your suggestions for fu-

ture editions.

You can send us comments from irs.gov/formspubs.

Click on “More Information” and then on “Give us feed-

back.”

Or you can write to:

Internal Revenue Service

Tax Forms and Publications

1111 Constitution Ave. NW, IR-6526

Washington, DC 20224

We respond to many letters by telephone. Therefore, it

would be helpful if you would include your daytime phone

number, including the area code, in your correspondence.

Although we cannot respond individually to each com-

ment received, we do appreciate your feedback and will

consider your comments as we revise our tax products.

Ordering forms and publications. Visit irs.gov/

formspubs to download forms and publications. Other-

wise, you can go to irs.gov/orderforms to order current

and prior-year forms and instructions. Your order should

arrive within 10 business days.

Tax questions. If you have a tax question not an-

swered by this publication, check IRS.gov and How To

Get Tax Help at the end of this publication.

Useful Items

You may want to see:

Publication

Credit for the Elderly or the Disabled 524

Taxable and Nontaxable Income

Retirement Plans for Small Business (SEP,

SIMPLE, and Qualified Plans)

Tax-Sheltered Annuity Plans (403(b) Plans) For

Employees of Public Schools and Certain

Tax-Exempt Organizations

Contributions to Individual Retirement

Arrangements (IRAs)

Distributions from Individual Retirement

Arrangements (IRAs)

Tax Guide to U.S. Civil Service Retirement

Benefits

Social Security and Equivalent Railroad

Retirement Benefits

General Rule for Pensions and Annuities

Form (and Instructions)

Withholding Certificate for Pension or Annuity

Payments

Distributions From Pensions, Annuities,

Retirement or Profit-Sharing Plans, IRAs,

Insurance Contracts, etc.

Tax on Lump-Sum Distributions

Additional Taxes on Qualified Plans (Including

IRAs) and Other Tax-Favored Accounts

See How To Get Tax Help near the end of this publication

for information about getting publications and forms.

General Information

Definitions. Some of the terms used in this publication

are defined in the following paragraphs.

Pension. A pension is generally a series of definitely

determinable payments made to you after you retire from

work. Pension payments are made regularly and are

based on such factors as years of service and prior com-

pensation.

Annuity. An annuity is a series of payments under a

contract made at regular intervals over a period of more

than 1 full year. They can be either fixed (under which you

receive a definite amount) or variable (not fixed). You can

buy the contract alone or with the help of your employer.

Qualified employee plan. A qualified employee plan

is an employer's stock bonus, pension, or profit-sharing

plan that is for the exclusive benefit of employees or their

beneficiaries and that meets Internal Revenue Code re-

quirements. It qualifies for special tax benefits, such as tax

deferral for employer contributions and capital gain treat-

ment or the 10-year tax option for lump-sum distributions

(if participants qualify). To determine whether your plan is

a qualified plan, check with your employer or the plan ad-

ministrator.

Qualified employee annuity. A qualified employee

annuity is a retirement annuity purchased by an employer

525

560

571

590-A

590-B

721

915

939

W-4P

1099-R

4972

5329

Publication 575 (2016) Page 3

Page 4 of 43 Fileid: … tions/P575/2016/A/XML/Cycle02/source 12:08 - 4-Jan-2017

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

for an employee under a plan that meets Internal Revenue

Code requirements.

Designated Roth account. A designated Roth ac-

count is a separate account created under a qualified

Roth contribution program to which participants may elect

to have part or all of their elective deferrals to a 401(k),

403(b), or 457(b) plan designated as Roth contributions.

Elective deferrals that are designated as Roth contribu-

tions are included in your income. However, qualified dis-

tributions (explained later) aren't included in your income.

You should check with your plan administrator to deter-

mine if your plan will accept designated Roth contribu-

tions.

Taxsheltered annuity plan. A tax-sheltered annuity

plan (often referred to as a 403(b) plan or a tax-deferred

annuity plan) is a retirement plan for employees of public

schools and certain tax-exempt organizations. Generally,

a tax-sheltered annuity plan provides retirement benefits

by purchasing annuity contracts for its participants.

Types of pensions and annuities. Pensions and annui-

ties include the following types.

Fixedperiod annuities. You receive definite

amounts at regular intervals for a specified length of time.

Annuities for a single life. You receive definite

amounts at regular intervals for life. The payments end at

death.

Joint and survivor annuities. The first annuitant re-

ceives a definite amount at regular intervals for life. After

he or she dies, a second annuitant receives a definite

amount at regular intervals for life. The amount paid to the

second annuitant may or may not differ from the amount

paid to the first annuitant.

Variable annuities. You receive payments that may

vary in amount for a specified length of time or for life. The

amounts you receive may depend upon such variables as

profits earned by the pension or annuity funds, cost-of-liv-

ing indexes, or earnings from a mutual fund.

Disability pensions. You receive disability payments

because you retired on disability and haven't reached

minimum retirement age.

More than one program. You may receive employee

plan benefits from more than one program under a single

trust or plan of your employer. If you participate in more

than one program, you may have to treat each as a sepa-

rate pension or annuity contract, depending upon the

facts in each case. Also, you may be considered to have

received more than one pension or annuity. Your former

employer or the plan administrator should be able to tell

you if you have more than one contract.

Example. Your employer set up a noncontributory

profit-sharing plan for its employees. The plan provides

that the amount held in the account of each participant will

be paid when that participant retires. Your employer also

set up a contributory defined benefit pension plan for its

employees providing for the payment of a lifetime pension

to each participant after retirement.

The amount of any distribution from the profit-sharing

plan depends on the contributions (including allocated for-

feitures) made for the participant and the earnings from

those contributions. Under the pension plan, however, a

formula determines the amount of the pension benefits.

The amount of contributions is the amount necessary to

provide that pension.

Each plan is a separate program and a separate con-

tract. If you get benefits from these plans, you must ac-

count for each separately, even though the benefits from

both may be included in the same check.

Distributions from a designated Roth account are

treated separately from other distributions from

the plan.

Qualified domestic relations order (QDRO). A QDRO

is a judgment, decree, or order relating to payment of child

support, alimony, or marital property rights to a spouse,

former spouse, child, or other dependent of a participant

in a retirement plan. The QDRO must contain certain spe-

cific information, such as the name and last known mailing

address of the participant and each alternate payee, and

the amount or percentage of the participant's benefits to

be paid to each alternate payee. A QDRO may not award

an amount or form of benefit that isn't available under the

plan.

A spouse or former spouse who receives part of the

benefits from a retirement plan under a QDRO reports the

payments received as if he or she were a plan participant.

The spouse or former spouse is allocated a share of the

participant's cost (investment in the contract) equal to the

cost times a fraction. The numerator of the fraction is the

present value of the benefits payable to the spouse or for-

mer spouse. The denominator is the present value of all

benefits payable to the participant.

A distribution that is paid to a child or other dependent

under a QDRO is taxed to the plan participant.

Variable Annuities

The tax rules in this publication apply both to annuities

that provide fixed payments and to annuities that provide

payments that vary in amount based on investment results

or other factors. For example, they apply to commercial

variable annuity contracts, whether bought by an em-

ployee retirement plan for its participants or bought di-

rectly from the issuer by an individual investor. Under

these contracts, the owner can generally allocate the pur-

chase payments among several types of investment port-

folios or mutual funds and the contract value is deter-

mined by the performance of those investments. The

earnings aren't taxed until distributed either in a with-

drawal or in annuity payments. The taxable part of a distri-

bution is treated as ordinary income.

For information on the tax treatment of a transfer or ex-

change of a variable annuity contract, see Transfers of

Annuity Contracts under Taxation of Nonperiodic Pay

ments, later.

CAUTION

!

Page 4 Publication 575 (2016)

Page 5 of 43 Fileid: … tions/P575/2016/A/XML/Cycle02/source 12:08 - 4-Jan-2017

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Net investment income tax. Annuities under a nonqua-

lified plan are included in calculating your net investment

income for the net investment income tax (NIIT). For infor-

mation see the Instructions for Form 8960, Net Investment

Income Tax — Individuals, Estates and Trusts.

Withdrawals. If you withdraw funds before your annuity

starting date and your annuity is under a qualified retire-

ment plan, a ratable part of the amount withdrawn is tax

free. The tax-free part is based on the ratio of your cost

(investment in the contract) to your account balance under

the plan.

If your annuity is under a nonqualified plan (including a

contract you bought directly from the issuer), the amount

withdrawn is allocated first to earnings (the taxable part)

and then to your cost (the tax-free part). However, if you

bought your annuity contract before August 14, 1982, a

different allocation applies to the investment before that

date and the earnings on that investment. To the extent

the amount withdrawn doesn't exceed that investment and

earnings, it is allocated first to your cost (the tax-free part)

and then to earnings (the taxable part).

If you withdraw funds (other than as an annuity) on or

after your annuity starting date, the entire amount with-

drawn is generally taxable.

The amount you receive in a full surrender of your an-

nuity contract at any time is tax free to the extent of any

cost that you haven't previously recovered tax free. The

rest is taxable.

For more information on the tax treatment of withdraw-

als, see Taxation of Nonperiodic Payments, later. If you

withdraw funds from your annuity before you reach age 59

12, also see Tax on Early Distributions under Special Addi

tional Taxes, later.

Annuity payments. If you receive annuity payments un-

der a variable annuity plan or contract, you recover your

cost tax free under either the Simplified Method or the

General Rule, as explained under Taxation of Periodic

Payments, later. For a variable annuity paid under a quali-

fied plan, you generally must use the Simplified Method.

For a variable annuity paid under a nonqualified plan (in-

cluding a contract you bought directly from the issuer),

you must use a special computation under the General

Rule. For more information, see Variable annuities in Pub.

939 under Computation Under the General Rule.

Death benefits. If you receive a single-sum distribution

from a variable annuity contract because of the death of

the owner or annuitant, the distribution is generally taxable

only to the extent it is more than the unrecovered cost of

the contract. If you choose to receive an annuity, the pay-

ments are subject to tax as described above. If the con-

tract provides a joint and survivor annuity and the primary

annuitant had received annuity payments before death,

you figure the tax-free part of annuity payments you re-

ceive as the survivor in the same way the primary annui-

tant did. See Survivors and Beneficiaries, later.

Section 457 Deferred

Compensation Plans

If you work for a state or local government or for a tax-ex-

empt organization, you may be able to participate in a

section 457 deferred compensation plan. If your plan is an

eligible plan, you aren't taxed currently on pay that is de-

ferred under the plan or on any earnings from the plan's

investment of the deferred pay. You are generally taxed

on amounts deferred in an eligible state or local govern-

ment plan only when they are distributed from the plan.

You are taxed on amounts deferred in an eligible tax-ex-

empt organization plan when they are distributed or other-

wise made available to you.

Your 457(b) plan may have a designated Roth account

option. If so, you may be able to roll over amounts to the

designated Roth account or make contributions. Elective

deferrals to a designated Roth account are included in

your income. Qualified distributions (explained later) aren't

included in your income. See the Designated Roth ac

counts discussion under Taxation of Periodic Payments,

later.

This publication covers the tax treatment of benefits un-

der eligible section 457 plans, but it doesn't cover the

treatment of deferrals. For information on deferrals under

section 457 plans, see Retirement Plan Contributions un-

der Employee Compensation in Pub. 525.

Is your plan eligible? To find out if your plan is an eligi-

ble plan, check with your employer. Plans that aren’t eligi-

ble section 457 plans include the following:

Bona fide vacation leave, sick leave, compensatory

time, severance pay, disability pay, or death benefit

plans.

Nonelective deferred compensation plans for nonem-

ployees (independent contractors).

Deferred compensation plans maintained by

churches.

Length of service award plans for bona fide volunteer

firefighters and emergency medical personnel. An ex-

ception applies if the total amount paid to a volunteer

exceeds $3,000 for any year of service.

Disability Pensions

If you retired on disability, you generally must include in in-

come any disability pension you receive under a plan that

is paid for by your employer. You must report your taxable

disability payments as wages on line 7 of Form 1040 or

Form 1040A or on line 8 of Form 1040NR until you reach

minimum retirement age. Minimum retirement age gener-

ally is the age at which you can first receive a pension or

annuity if you aren't disabled.

You may be entitled to a tax credit if you were per

manently and totally disabled when you retired.

For information on this credit, see Pub. 524.

Beginning on the day after you reach minimum retire-

ment age, payments you receive are taxable as a pension

TIP

Publication 575 (2016) Page 5

Page 6 of 43 Fileid: … tions/P575/2016/A/XML/Cycle02/source 12:08 - 4-Jan-2017

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

or annuity. When you receive pension or annuity pay-

ments you are able to recover your cost or investment.

Your cost is generally your net investment in the plan as of

your annuity starting date. It doesn't include pre-tax contri-

butions. For more information, see Cost (Investment in the

Contract) and Taxation of Periodic Payments, later.

Report the payments on Form 1040, lines 16a and 16b;

Form 1040A, lines 12a and 12b; or on Form 1040NR,

lines 17a and 17b.

Disability payments for injuries incurred as a di

rect result of a terrorist attack directed against the

United States (or its allies) aren't included in in

come. For more information about payments to survivors

of terrorist attacks, see Pub. 3920, Tax Relief for Victims

of Terrorist Attacks.

Military and government disability pensions. Certain

military and government disability pensions aren’t taxable.

Serviceconnected disability. You may be able to

exclude from income amounts you receive as a pension,

annuity, or similar allowance for personal injury or sick-

ness resulting from active service in one of the following

government services:

The armed forces of any country,

The National Oceanic and Atmospheric Administra-

tion,

The Public Health Service, or

The Foreign Service.

Insurance Premiums for Retired

Public Safety Officers

If you are an eligible retired public safety officer (law en-

forcement officer, firefighter, chaplain, or member of a res-

cue squad or ambulance crew), you can elect to exclude

from income distributions made from your eligible retire-

ment plan that are used to pay the premiums for accident

or health insurance or long-term care insurance. The pre-

miums can be for coverage for you, your spouse, or de-

pendents. The distribution must be made directly from the

plan to the insurance provider. You can exclude from in-

come the smaller of the amount of the insurance premi-

ums or $3,000. You can only make this election for

amounts that would otherwise be included in your income.

The amount excluded from your income can't be used to

claim a medical expense deduction.

An eligible retirement plan is a governmental plan that

is:

a qualified trust,

a section 403(a) plan,

a section 403(b) annuity, or

a section 457(b) plan.

If you make this election, reduce the otherwise taxable

amount of your pension or annuity by the amount

excluded. The amount shown in box 2a of Form 1099-R

TIP

doesn't reflect this exclusion. Report your total distribu-

tions on Form 1040, line 16a; Form 1040A, line 12a; or

Form 1040NR, line 17a. Report the taxable amount on

Form 1040, line 16b; Form 1040A, line 12b; or Form

1040NR, line 17b. Enter “PSO” next to the appropriate line

on which you report the taxable amount.

If you are retired on disability and reporting your disabil-

ity pension on line 7 of Form 1040 or Form 1040A, or

line 8 of Form 1040NR, include only the taxable amount

on that line and enter “PSO” and the amount excluded on

the dotted line next to the applicable line.

Railroad Retirement Benefits

Benefits paid under the Railroad Retirement Act fall into

two categories. These categories are treated differently

for income tax purposes.

The first category is the amount of tier 1 railroad retire-

ment benefits that equals the social security benefit that a

railroad employee or beneficiary would have been entitled

to receive under the social security system. This part of

the tier 1 benefit is the social security equivalent benefit

(SSEB) and you treat it for tax purposes like social secur-

ity benefits. If you received, repaid, or had tax withheld

from the SSEB portion of tier 1 benefits during 2016, you

will receive Form RRB-1099, Payments by the Railroad

Retirement Board (or Form RRB-1042S, Statement for

Nonresident Alien Recipients of Payments by the Railroad

Retirement Board, if you are a nonresident alien) from the

U.S. Railroad Retirement Board (RRB).

For more information about the tax treatment of the

SSEB portion of tier 1 benefits and Forms RRB-1099 and

RRB-1042S, see Pub. 915.

The second category contains the rest of the tier 1 rail-

road retirement benefits, called the non-social security

equivalent benefit (NSSEB). It also contains any tier 2

benefit, vested dual benefit (VDB), and supplemental an-

nuity benefit. Treat this category of benefits, shown on

Form RRB-1099-R, as an amount received from a quali-

fied employee plan. This allows for the tax-free (nontaxa-

ble) recovery of employee contributions from the tier 2

benefits and the NSSEB part of the tier 1 benefits. (The

NSSEB and tier 2 benefits, less certain repayments, are

combined into one amount called the Contributory

Amount Paid on Form RRB-1099-R.) Vested dual benefits

and supplemental annuity benefits are non-contributory

pensions and are fully taxable. See Taxation of Periodic

Payments, later, for information on how to report your ben-

efits and how to recover the employee contributions tax

free. Form RRB-1099-R is used for U.S. citizens, resident

aliens, and nonresident aliens.

Nonresident aliens. A nonresident alien is an individual

who isn't a citizen or a resident alien of the United States.

Nonresident aliens are subject to mandatory U.S. tax with-

holding unless exempt under a tax treaty between the Uni-

ted States and their country of legal residency. A tax

treaty exemption may reduce or eliminate tax withholding

from railroad retirement benefits. See Tax withholding

next for more information.

Page 6 Publication 575 (2016)

Page 7 of 43 Fileid: … tions/P575/2016/A/XML/Cycle02/source 12:08 - 4-Jan-2017

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

If you are a nonresident alien and your tax withholding

rate changed or your country of legal residence changed

during the year, you may receive more than one Form

RRB-1042S or Form RRB-1099-R. To determine your to-

tal benefits paid or repaid and total tax withheld for the

year, you should add the amounts shown on all forms you

received for that year. For information on filing require-

ments for aliens, see Pub. 519, U.S. Tax Guide for Aliens.

For information on tax treaties between the United States

and other countries that may reduce or eliminate U.S. tax

on your benefits, see Pub. 901, U.S. Tax Treaties.

Tax withholding. To request or change your income tax

withholding from SSEB payments, U.S. citizens should

contact the IRS for Form W-4V, Voluntary Withholding Re-

quest, and file it with the RRB. To elect, revoke, or change

your income tax withholding from NSSEB, tier 2, VDB,

and supplemental annuity payments received, use Form

RRB W-4P, Withholding Certificate for Railroad Retire-

ment Payments. If you are a nonresident alien or a U.S.

citizen living abroad, you should provide Form RRB-1001,

Nonresident Questionnaire, to the RRB to furnish citizen-

ship and residency information and to claim any treaty ex-

emption from U.S. tax withholding. Nonresident U.S. citi-

zens can't elect to be exempt from withholding on

payments delivered outside of the United States.

Help from the RRB. To request an RRB form or to get

help with questions about an RRB benefit, you should

contact your nearest RRB field office if you reside in the

United States (call 1-877-772-5772 for the nearest field of-

fice) or U.S. consulate/Embassy if you reside outside the

United States. You can visit the RRB on the Internet at

https://secure.rrb.gov/

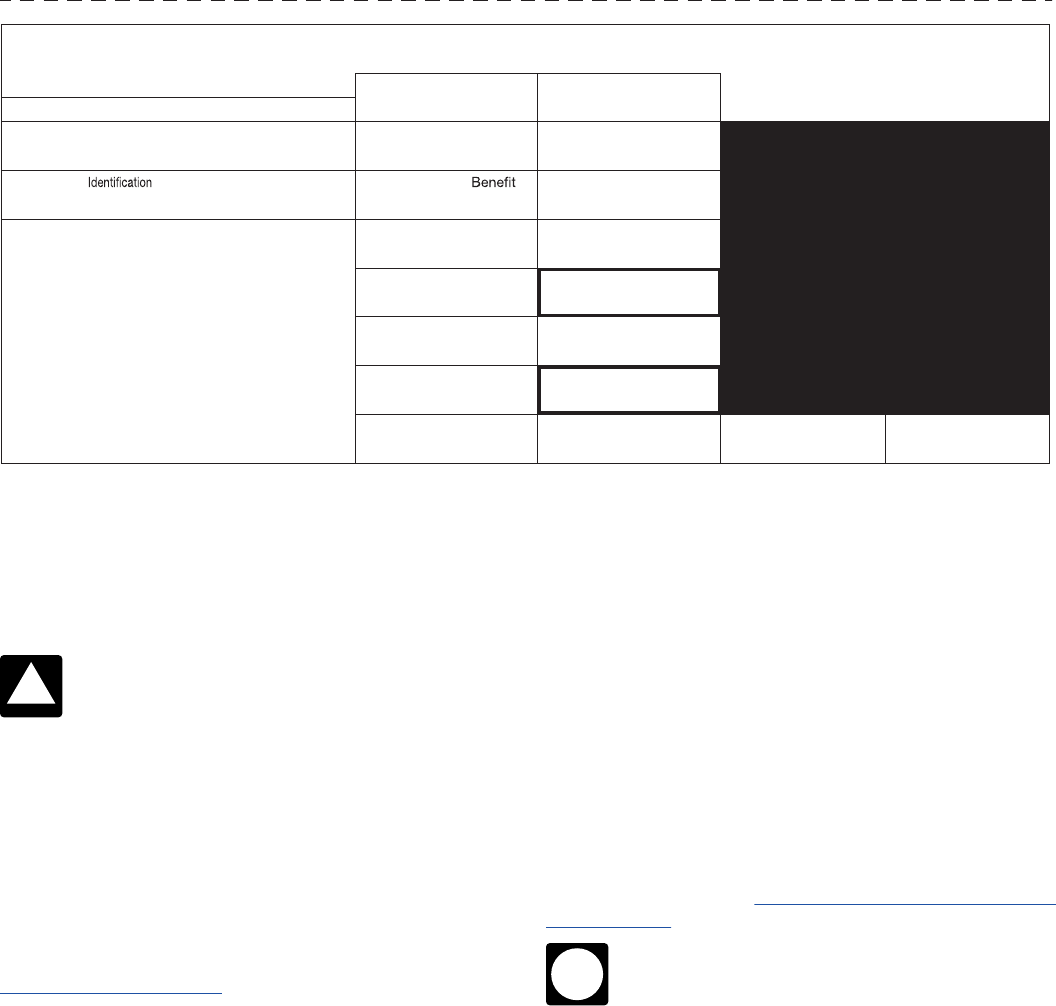

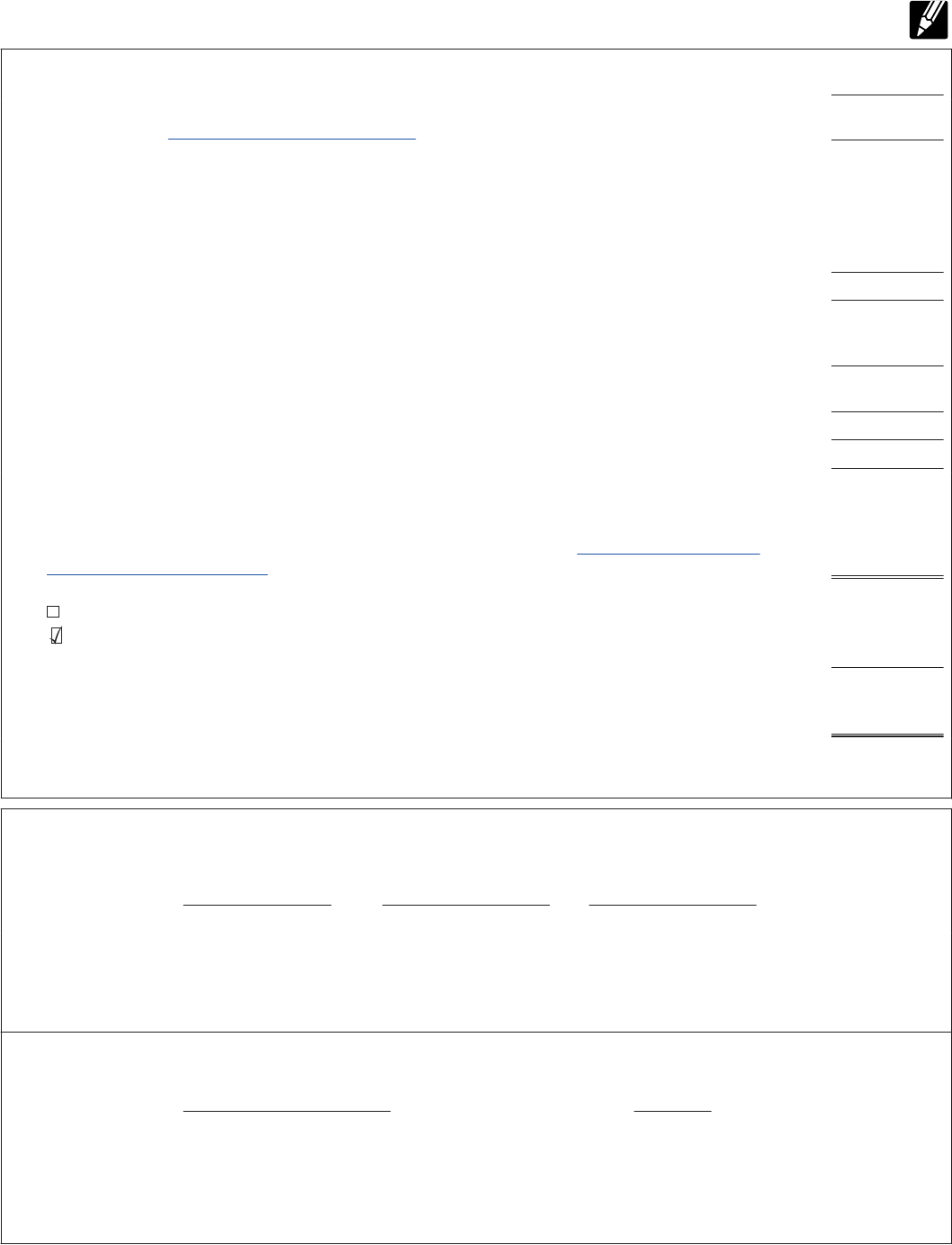

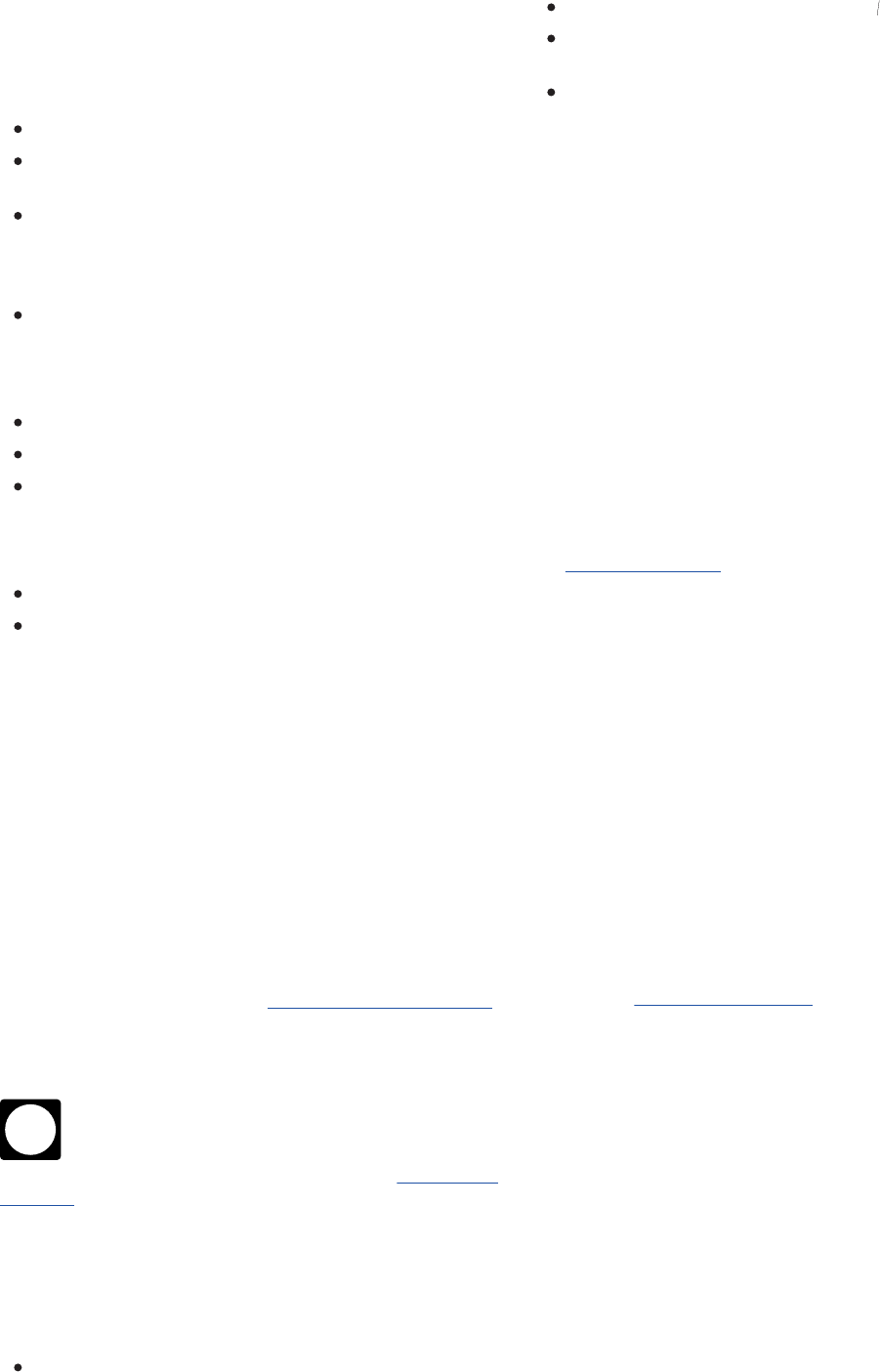

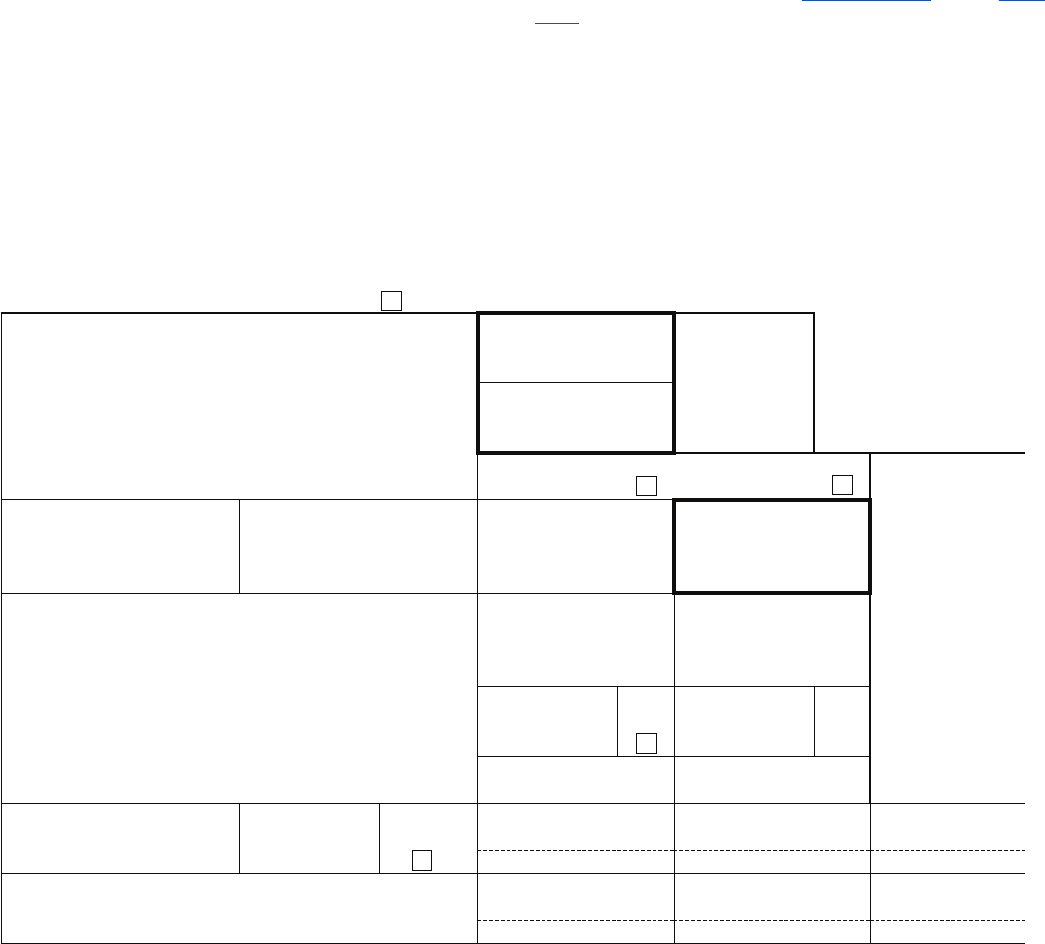

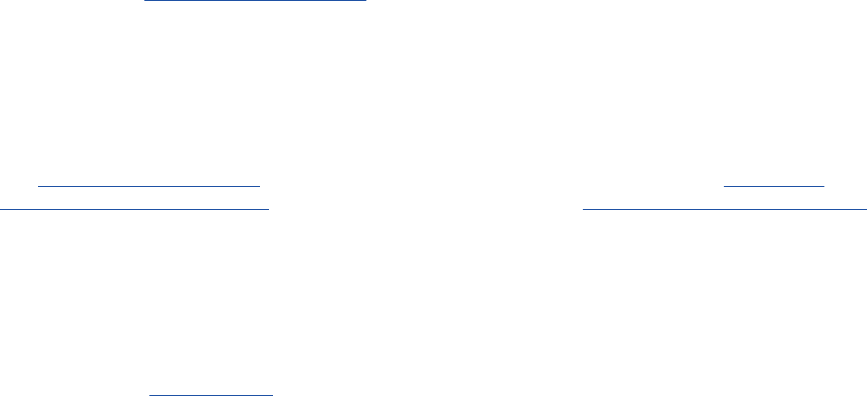

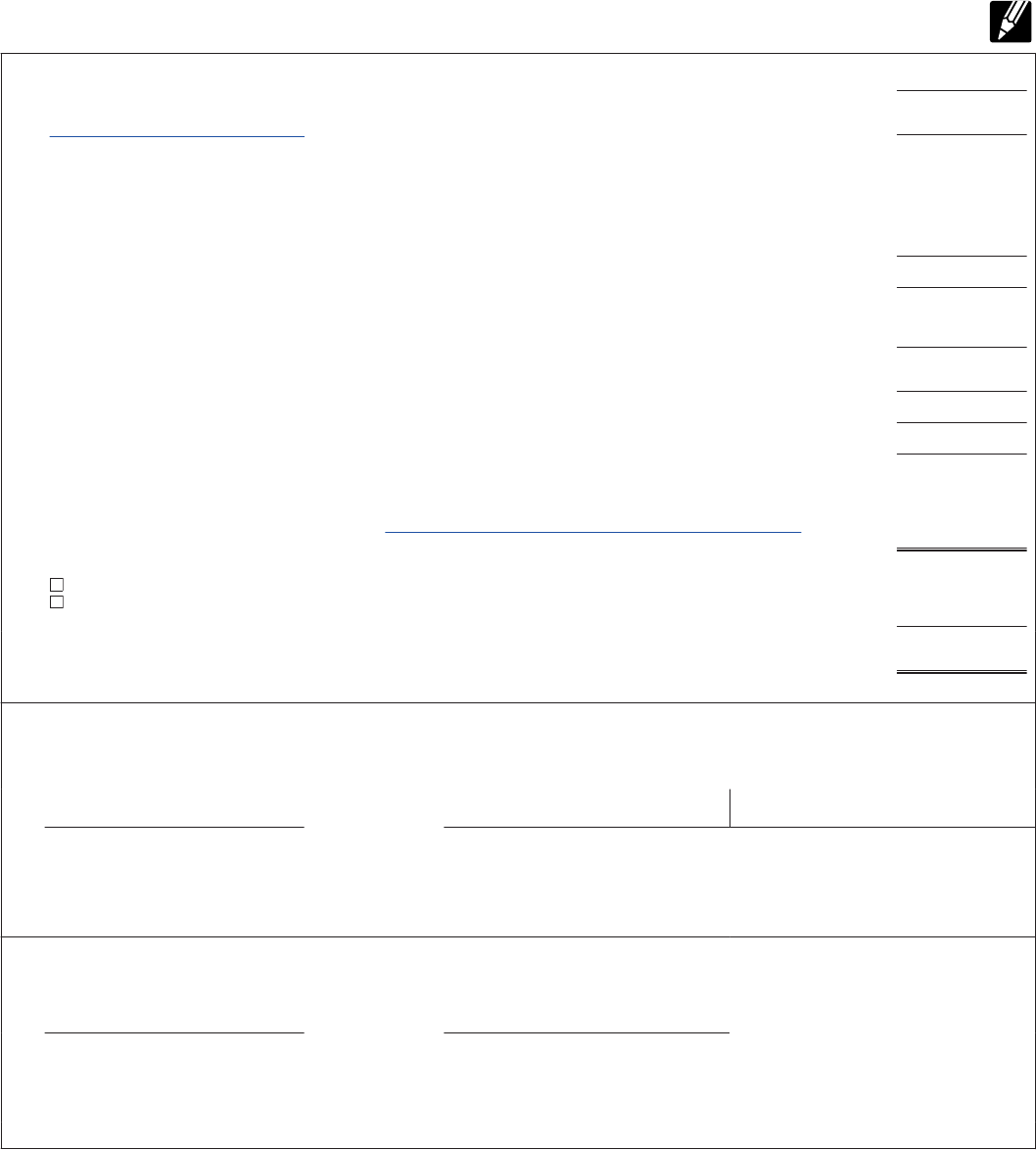

Form RRB-1099-R. The following discussion explains

the items shown on Form RRB-1099-R. The amounts

shown on this form are before any deduction for:

Federal income tax withholding,

Medicare premiums,

Legal process garnishment payments,

Recovery of a prior year overpayment of an NSSEB,

tier 2 benefit, VDB, or supplemental annuity benefit, or

Recovery of Railroad Unemployment Insurance Act

benefits received while awaiting payment of your rail-

road retirement annuity.

The amounts shown on this form are after any offset

for:

Social Security benefits,

Age reduction,

Public Service pensions or public disability benefits,

Dual railroad retirement entitlement under another

RRB claim number,

Work deductions,

Legal process partition deductions,

Actuarial adjustment,

Annuity waiver, or

Recovery of a current-year overpayment of NSSEB,

tier 2, VDB, or supplemental annuity benefits.

The amounts shown on Form RRB-1099-R do not re-

flect any special rules, such as capital gain treatment or

the special 10-year tax option for lump-sum payments, or

tax-free rollovers. To determine if any of these rules apply

to your benefits, see the discussions about them later.

Generally, amounts shown on your Form RRB-1099-R

are considered a normal distribution. Use distribution

code “7” if you are asked for a distribution code. Distribu-

tion codes aren't shown on Form RRB-1099-R.

There are three copies of this form. Copy B is to be in-

cluded with your income tax return if federal income tax is

withheld. Copy C is for your own records. Copy 2 is filed

with your state, city, or local income tax return, when re-

quired. See the illustrated Copy B (Form RRB-1099-R)

above.

Each beneficiary will receive his or her own Form

RRB1099R. If you receive benefits on more than

one railroad retirement record, you may get more

than one Form RRB1099R. So that you get your form

timely, make sure the RRB always has your current mail

ing address.

Box 1—Claim Number and Payee Code. Your claim

number is a six- or nine-digit number preceded by an al-

phabetical prefix. This is the number under which the RRB

paid your benefits. Your payee code follows your claim

number and is the last number in this box. It is used by the

RRB to identify you under your claim number. In all your

correspondence with the RRB, be sure to use the claim

number and payee code shown in this box.

Box 2—Recipient's Identification Number. This is

the recipient's U.S. taxpayer identification number. It is the

social security number (SSN), individual taxpayer identifi-

cation number (ITIN), or employer identification number

(EIN), if known, for the person or estate listed as the recip-

ient.

If you are a resident or nonresident alien who

must furnish a taxpayer identification number to

the IRS and aren’t eligible to obtain an SSN, use

Form W7, Application for IRS Individual Taxpayer Identifi

cation Number, to apply for an ITIN. The Instructions for

Form W7 explain how and when to apply.

Box 3—Employee Contributions. This is the amount

of taxes withheld from the railroad employee's earnings

that exceeds the amount of taxes that would have been

withheld had the earnings been covered under the social

security system. This amount is the employee's cost that

you use to figure the tax-free part of the NSSEB and tier 2

benefit you received (the amount shown in box 4). (For in-

formation on how to figure the tax-free part, see Partly

Taxable Payments under Taxation of Periodic Payments,

later.) The amount shown is the total employee contribu-

tion amount, not reduced by any amounts that the RRB

calculated as previously recovered. It is the latest amount

reported for 2016 and may have increased or decreased

TIP

TIP

Publication 575 (2016) Page 7

Page 8 of 43 Fileid: … tions/P575/2016/A/XML/Cycle02/source 12:08 - 4-Jan-2017

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

from a previous Form RRB-1099-R. If this amount has

changed, the change is retroactive. You may need to re-

figure the tax-free part of your NSSEB/tier 2 benefit for

2016 and prior tax years. If this box is blank, it means that

the amount of your NSSEB and tier 2 payments shown in

box 4 is fully taxable.

If you had a previous annuity entitlement that

ended and you are figuring the taxfree part of

your NSSEB/tier 2 benefit for your current annuity

entitlement, you should contact the RRB for confirmation

of your correct employee contribution amount.

Box 4—Contributory Amount Paid. This is the gross

amount of the NSSEB and tier 2 benefit you received in

2016, less any 2016 benefits you repaid in 2016. (Any

benefits you repaid in 2016 for an earlier year or for an un-

known year are shown in box 8.) This amount is the total

contributory pension paid in 2016. It may be partly taxable

and partly tax free or fully taxable. If you determine you

are eligible to compute a tax-free part as explained later in

Partly Taxable Payments under Taxation of Periodic Pay

ments, use the latest reported employee contribution

amount shown in box 3 as the cost.

Box 5—Vested Dual Benefit. This is the gross

amount of vested dual benefit (VDB) payments paid in

2016, less any 2016 VDB payments you repaid in 2016. It

is fully taxable. VDB payments you repaid in 2016 for an

earlier year or for an unknown year are shown in box 8.

Note. The amounts shown in boxes 4 and 5 may rep-

resent payments for 2016 and/or other years after 1983.

Box 6—Supplemental Annuity. This is the gross

amount of supplemental annuity benefits paid in 2016,

less any 2016 supplemental annuity benefits you repaid in

2016. It is fully taxable. Supplemental annuity benefits you

repaid in 2016 for an earlier year or for an unknown year

are shown in box 8.

CAUTION

!

Box 7—Total Gross Paid. This is the sum of boxes 4,

5, and 6. The amount represents the total pension paid in

2016. Include this amount on Form 1040, line 16a; Form

1040A, line 12a; or Form 1040NR, line 17a.

Box 8—Repayments. This amount represents any

NSSEB, tier 2 benefit, VDB, and supplemental annuity

benefit you repaid to the RRB in 2016 for years before

2016 or for unknown years. The amount shown in this box

hasn't been deducted from the amounts shown in boxes

4, 5, and 6. It only includes repayments of benefits that

were taxable to you. This means it only includes repay-

ments in 2016 of NSSEB benefits paid after 1985, tier 2

and VDB benefits paid after 1983, and supplemental an-

nuity benefits paid in any year. If you included the benefits

in your income in the year you received them, you may be

able to deduct the repaid amount. For more information

about repayments, see Repayment of benefits received in

an earlier year, later.

You may have repaid an overpayment of benefits

by returning a payment, by making a payment, or

by having an amount withheld from your railroad

retirement annuity payment.

Box 9—Federal Income Tax Withheld. This is the

total federal income tax withheld from your NSSEB, tier 2

benefit, VDB, and supplemental annuity benefit. Include

this on your income tax return as tax withheld. If you are a

nonresident alien and your tax withholding rate and/or

country of legal residence changed during 2016, you will

receive more than one Form RRB-1099-R for 2016. Deter-

mine the total amount of U.S. federal income tax withheld

from your 2016 RRB NSSEB, tier 2, VDB, and supple-

mental annuity payments by adding the amounts in box 9

of all original 2016 Forms RRB-1099-R, or the latest cor-

rected or duplicate Forms RRB-1099-R you receive.

Box 10—Rate of Tax. If you are taxed as a U.S. citi-

zen or resident alien, this box doesn't apply to you. If you

TIP

Sample

PAYER’S NAME, STREET ADDRESS, CITY, STATE, AND ZIP CODE

UNITED STATES RAILROAD RETIREMENT BOARD

844 N RUSH ST CHICAGO IL 60611-2092

ANNUITIES OR PENSIONS BY THE

RAILROAD RETIREMENT BOARD

PAYER’S FEDERAL IDENTIFYING NO.

FORM RRB-1099-R

COPY B -

REPORT THIS INCOME ON

YOUR FEDERAL TAX

RETURN. IF THIS FORM

SHOWS FEDERAL INCOME

TAX WITHHELD IN BOX 9

ATTACH THIS COPY TO

YOUR RETURN.

THIS INFORMATION IS BEING

FURNISHED TO THE INTERNAL

REVENUE SERVICE.

1.

2.

Claim Number and Payee Code

Recipient’s Number

Recipient’s Name, Street Address, City, State, and Zip Code

3.

4.

5.

6.

7.

8.

9.

10. 11.

Employee Contributions

Contributory Amount Paid

Vested Dual

Supplemental Annuity

Total Gross Paid

(Sum of boxes 4, 5, and 6)

Repayments

Federal Income Tax

Withheld

Rate of Tax Country

12.

Medicare Premium Total

2016

Page 8 Publication 575 (2016)

Page 9 of 43 Fileid: … tions/P575/2016/A/XML/Cycle02/source 12:08 - 4-Jan-2017

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

are a nonresident alien, an entry in this box indicates the

rate at which tax was withheld on the NSSEB, tier 2, VDB,

and supplemental annuity payments that were paid to you

in 2016. If you are a nonresident alien whose tax was with-

held at more than one rate during 2016, you will receive a

separate Form RRB-1099-R for each rate change during

2016.

Box 11—Country. If you are taxed as a U.S. citizen or

resident alien, this box doesn't apply to you. If you are a

nonresident alien, an entry in this box indicates the coun-

try of which you were a resident for tax purposes at the

time you received railroad retirement payments in 2016. If

you are a nonresident alien who was a resident of more

than one country during 2016, you will receive a separate

Form RRB-1099-R for each country of residence during

2016.

Box 12—Medicare Premium Total. This is for infor-

mation purposes only. The amount shown in this box rep-

resents the total amount of Part B Medicare premiums de-

ducted from your railroad retirement annuity payments in

2016. Medicare premium refunds aren't included in the

Medicare total. The Medicare total is normally shown on

Form RRB-1099 (if you are a citizen or resident alien of

the United States) or Form RRB-1042S (if you are a non-

resident alien). However, if Form RRB-1099 or Form

RRB-1042S isn't required for 2016, then this total will be

shown on Form RRB-1099-R. If your Medicare premiums

were deducted from your social security benefits, paid by

a third party, refunded to you, and/or you paid the premi-

ums by direct billing, your Medicare total won't be shown

in this box.

Repayment of benefits received in an earlier year. If

you had to repay any railroad retirement benefits that you

had included in your income in an earlier year because at

that time you thought you had an unrestricted right to it,

you can deduct the amount you repaid in the year in which

you repaid it.

If you repaid $3,000 or less in 2016, deduct it on

Schedule A (Form 1040), line 23. The 2%-of-adjus-

ted-gross-income limit applies to this deduction. You can't

take this deduction if you file Form 1040A.

If you repaid more than $3,000 in 2016, you can either

take a deduction for the amount repaid on Schedule A

(Form 1040), line 28 or you can take a credit against your

tax. For more information, see Repayments in Pub. 525.

Withholding Tax

and Estimated Tax

Your retirement plan distributions are subject to federal in-

come tax withholding. However, you can choose not to

have tax withheld on payments you receive unless they

are eligible rollover distributions. (These are distributions,

described later under Rollovers, that are eligible for roll-

over treatment but aren't paid directly to another qualified

retirement plan or to a traditional IRA.) If you choose not to

have tax withheld or if you don't have enough tax withheld,

you may have to make estimated tax payments. See Esti

mated tax, later.

The withholding rules apply to the taxable part of pay-

ments you receive from:

An employer pension, annuity, profit-sharing, or stock

bonus plan,

Any other deferred compensation plan,

A traditional individual retirement arrangement (IRA),

or

A commercial annuity.

For this purpose, a commercial annuity means an annuity,

endowment, or life insurance contract issued by an insur-

ance company.

There will be no withholding on any part of a dis

tribution where it is reasonable to believe that it

won't be includible in gross income.

Choosing no withholding. You can choose not to have

income tax withheld from retirement plan payments unless

they are eligible rollover distributions. You can make this

choice on Form W-4P for periodic and nonperiodic pay-

ments. This choice generally remains in effect until you re-

voke it.

The payer will ignore your choice not to have tax with-

held if:

You don't give the payer your social security number

(in the required manner), or

The IRS notifies the payer, before the payment is

made, that you gave an incorrect social security num-

ber.

To choose not to have tax withheld, a U.S. citizen or

resident alien must give the payer a home address in the

United States or its possessions. Without that address,

the payer must withhold tax. For example, the payer has

to withhold tax if the recipient has provided a U.S. address

for a nominee, trustee, or agent to whom the benefits are

delivered, but hasn't provided his or her own U.S. home

address.

If you don't give the payer a home address in the Uni-

ted States or its possessions, you can choose not to have

tax withheld only if you certify to the payer that you aren't a

U.S. citizen, a U.S. resident alien, or someone who left the

country to avoid tax. But if you so certify, you may be sub-

ject to the 30% flat rate withholding that applies to nonres-

ident aliens. This 30% rate won't apply if you are exempt

or subject to a reduced rate by treaty. For details, get Pub.

519.

Periodic payments. Unless you choose no withholding,

your annuity or similar periodic payments (other than eligi-

ble rollover distributions) will be treated like wages for

withholding purposes. Periodic payments are amounts

paid at regular intervals (such as weekly, monthly, or

yearly) for a period of time greater than 1 year (such as for

15 years or for life). You should give the payer a comple-

ted withholding certificate (Form W-4P or a similar form

provided by the payer). If you don't, tax will be withheld as

if you were married and claiming three withholding allow-

ances.

TIP

Publication 575 (2016) Page 9

Page 10 of 43 Fileid: … tions/P575/2016/A/XML/Cycle02/source 12:08 - 4-Jan-2017

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Tax will be withheld as if you were single and were

claiming no withholding allowances if:

You don't give the payer your social security number

(in the required manner), or

The IRS notifies the payer (before any payment is

made) that you gave an incorrect social security num-

ber.

You must file a new withholding certificate to change

the amount of withholding.

Nonperiodic distributions. Unless you choose no with-

holding, the withholding rate for a nonperiodic distribution

(a payment other than a periodic payment) that isn't an eli-

gible rollover distribution is 10% of the distribution. You

can also ask the payer to withhold an additional amount

using Form W-4P. The part of any loan treated as a distri-

bution (except an offset amount to repay the loan), ex-

plained later, is subject to withholding under this rule.

Eligible rollover distribution. If you receive an eligible

rollover distribution, 20% of it generally will be withheld for

income tax. You can't choose not to have tax withheld

from an eligible rollover distribution. However, tax won't be

withheld if you have the plan administrator pay the eligible

rollover distribution directly to another qualified plan or an

IRA in a direct rollover. For more information about eligible

rollover distributions, see Rollovers, later.

Estimated tax. Your estimated tax is the total of your ex-

pected income tax, self-employment tax, and certain other

taxes for the year, minus your expected credits and with-

held tax. Generally, you must make estimated tax pay-

ments for 2017 if you expect to owe at least $1,000 in tax

(after subtracting your withholding and credits) and you

expect your withholding and credits to be less than the

smaller of:

1. 90% of the tax to be shown on your 2017 return, or

2. 100% of the tax shown on your 2016 return.

If your adjusted gross income for 2016 was more than

$150,000 ($75,000 if your filing status for 2017 is married

filing separately), substitute 110% for 100% in (2) above.

For more information, get Pub. 505, Tax Withholding and

Estimated Tax.

In figuring your withholding or estimated tax, re

member that a part of your monthly social security

or equivalent tier 1 railroad retirement benefits

may be taxable. See Pub. 915. You can choose to have

income tax withheld from those benefits. Use Form W4V

to make this choice.

Cost (Investment

in the Contract)

Distributions from your pension or annuity plan may in-

clude amounts treated as a recovery of your cost (invest-

ment in the contract). If any part of a distribution is treated

TIP

as a recovery of your cost under the rules explained in this

publication, that part is tax free. Therefore, the first step in

figuring how much of a distribution is taxable is to deter-

mine the cost of your pension or annuity.

In general, your cost is your net investment in the con-

tract as of the annuity starting date (or the date of the dis-

tribution, if earlier). To find this amount, you must first fig-

ure the total premiums, contributions, or other amounts

you paid. This includes the amounts your employer con-

tributed that were taxable to you when paid. (However,

see Foreign employment contributions, later.) It doesn't in-

clude amounts withheld from your pay on a tax-deferred

basis (money that was taken out of your gross pay before

taxes were deducted). It also doesn't include amounts you

contributed for health and accident benefits (including any

additional premiums paid for double indemnity or disability

benefits).

From this total cost you must subtract the following

amounts.

1. Any refunded premiums, rebates, dividends, or unre-

paid loans that weren't included in your income and

that you received by the later of the annuity starting

date or the date on which you received your first pay-

ment.

2. Any other tax-free amounts you received under the

contract or plan by the later of the dates in (1).

3. If you must use the Simplified Method for your annuity

payments, the tax-free part of any single-sum pay-

ment received in connection with the start of the an-

nuity payments, regardless of when you received it.

(See Simplified Method, later, for information on its re-

quired use.)

4. If you use the General Rule for your annuity pay-

ments, the value of the refund feature in your annuity

contract. (See General Rule, later, for information on

its use.) Your annuity contract has a refund feature if

the annuity payments are for your life (or the lives of

you and your survivor) and payments in the nature of

a refund of the annuity's cost will be made to your

beneficiary or estate if all annuitants die before a sta-

ted amount or a stated number of payments are

made. For more information, see Pub. 939.

The tax treatment of the items described in (1) through (3)

is discussed later under Taxation of Nonperiodic Pay

ments.

Form 1099R. If you began receiving periodic

payments of a life annuity in 2016, the payer

should show your total contributions to the plan in

box 9b of your 2016 Form 1099R.

Annuity starting date defined. Your annuity starting

date is the later of the first day of the first period for which

you received a payment or the date the plan's obligations

became fixed.

Example. On January 1, you completed all your pay-

ments required under an annuity contract providing for

TIP

Page 10 Publication 575 (2016)

Page 11 of 43 Fileid: … tions/P575/2016/A/XML/Cycle02/source 12:08 - 4-Jan-2017

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

monthly payments starting on August 1 for the period be-

ginning July 1. The annuity starting date is July 1. This is

the date you use in figuring the cost of the contract and

selecting the appropriate number from Table 1 for line 3 of

the Simplified Method Worksheet.

Designated Roth accounts. Your cost in these ac-

counts is your designated Roth contributions that were in-

cluded in your income as wages subject to applicable

withholding requirements. Your cost will also include any

in-plan Roth rollovers you included in income.

Foreign employment contributions. If you worked

abroad, your cost may include contributions by your em-

ployer to the retirement plan, but only if those contribu-

tions would be excludible from your gross income had

they been paid directly to you as compensation. The con-

tributions that apply are:

1. Contributions before 1963 by your employer,

2. Contributions after 1962 by your employer if the con-

tributions would be excludible from your gross income

(not including the foreign earned income exclusion)

had they been paid directly to you, or

3. Contributions after 1996 by your employer if you per-

formed the services of a foreign missionary (a duly or-

dained, commissioned, or licensed minister of a

church or a lay person) but only if the contributions

would be excludible from your gross income had they

been paid directly to you.

Foreign employment contributions while a nonres

ident alien. In determining your cost, special rules apply

if you are a U.S. citizen or resident alien who received dis-

tributions in 2016 from a plan to which contributions were

made while you were a nonresident alien. Your contribu-

tions and your employer's contributions aren't included in

your cost if the contribution:

Was made based on compensation which was for

services performed outside the United States while

you were a nonresident alien, and

Wasn't subject to income tax under the laws of the

United States or any foreign country, but only if the

contribution would have been subject to income tax if

paid as cash compensation when the services were

performed.

Taxation of

Periodic Payments

This section explains how the periodic payments you re-

ceive from a pension or annuity plan are taxed. Periodic

payments are amounts paid at regular intervals (such as

weekly, monthly, or yearly) for a period of time greater

than 1 year (such as for 15 years or for life). These pay-

ments are also known as amounts received as an annuity.

If you receive an amount from your plan that isn't a peri-

odic payment, see Taxation of Nonperiodic Payments,

later.

In general, you can recover the cost of your pension or

annuity tax free over the period you are to receive the pay-

ments. The amount of each payment that is more than the

part that represents your cost is taxable (however, see In

surance Premiums for Retired Public Safety Officers, ear-

lier).

Designated Roth accounts. If you receive a qualified

distribution from a designated Roth account, the distribu-

tion isn't included in your gross income. This applies to

both your cost in the account and income earned on that

account. A qualified distribution is generally a distribution

that is:

Made after a 5-tax-year period of participation, and

Made on or after the date you reach age 5912, made to

a beneficiary or your estate on or after your death, or

attributable to your being disabled.

If the distribution isn't a qualified distribution, the rules

discussed in this section apply. The designated Roth ac-

count is treated as a separate contract.

Period of participation. The 5-tax-year period of par-

ticipation is the 5-tax-year period beginning with the first

tax year for which the participant made a designated Roth

contribution to the plan. Therefore, for designated Roth

contributions made for 2016, the first year for which a

qualified distribution can be made is 2021.

However, if a direct rollover is made to the plan from a

designated Roth account under another plan, the

5-tax-year period for the recipient plan begins with the first

tax year for which the participant first had designated Roth

contributions made to the other plan.

Your 401(k), 403(b), or 457(b) plan may permit you to

roll over amounts from those plans to a designated Roth

account within the same plan. This is known as an in-plan

Roth rollover. For more details, see Inplan Roth rollovers,

later.

Fully Taxable Payments

The pension or annuity payments that you receive are fully

taxable if you have no cost in the contract because any of

the following situations applies to you (however, see In

surance Premiums for Retired Public Safety Officers, ear-

lier).

You didn't pay anything or aren't considered to have

paid anything for your pension or annuity. Amounts

withheld from your pay on a tax-deferred basis aren't

considered part of the cost of the pension or annuity

payment.

Your employer didn't withhold contributions from your

salary.

You got back all of your contributions tax free in prior

years (however, see Exclusion not limited to cost un-

der Partly Taxable Payments, later).

Report the total amount you received on Form 1040,

line 16b; Form 1040A, line 12b; or on Form 1040NR,

line 17b. You should make no entry on Form 1040,

Publication 575 (2016) Page 11

Page 12 of 43 Fileid: … tions/P575/2016/A/XML/Cycle02/source 12:08 - 4-Jan-2017

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

line 16a; Form 1040A, line 12a; or Form 1040NR,

line 17a.

Deductible voluntary employee contributions. Distri-

butions you receive that are based on your accumulated

deductible voluntary employee contributions are generally

fully taxable in the year distributed to you. Accumulated

deductible voluntary employee contributions include net

earnings on the contributions. If distributed as part of a

lump sum, they don't qualify for the 10-year tax option or

capital gain treatment, explained later.

Partly Taxable Payments

If you have a cost to recover from your pension or annuity

plan (see Cost (Investment in the Contract), earlier), you

can exclude part of each annuity payment from income as

a recovery of your cost. This tax-free part of the payment

is figured when your annuity starts and remains the same

each year, even if the amount of the payment changes.

The rest of each payment is taxable (however, see Insur

ance Premiums for Retired Public Safety Officers, earlier).

You figure the tax-free part of the payment using one of

the following methods.

Simplified Method. You generally must use this

method if your annuity is paid under a qualified plan (a

qualified employee plan, a qualified employee annuity,

or a tax-sheltered annuity plan or contract). You can't

use this method if your annuity is paid under a non-

qualified plan.

General Rule. You must use this method if your an-

nuity is paid under a nonqualified plan. You generally

can't use this method if your annuity is paid under a

qualified plan.

You determine which method to use when you first begin

receiving your annuity, and you continue using it each

year that you recover part of your cost.

If you had more than one partly taxable pension or an-

nuity, figure the tax-free part and the taxable part of each

separately.

Qualified plan annuity starting before November 19,

1996. If your annuity is paid under a qualified plan and

your annuity starting date (defined earlier under Cost (In

vestment in the Contract)) is after July 1, 1986, and before

November 19, 1996, you could have chosen to use either

the Simplified Method or the General Rule. If your annuity

starting date is before July 2, 1986, you use the General

Rule unless your annuity qualified for the Three-Year

Rule. If you used the Three-Year Rule (which was re-

pealed for annuities starting after July 1, 1986), your annu-

ity payments are generally now fully taxable.

Exclusion limit. Your annuity starting date determines

the total amount of annuity payments that you can exclude

from income over the years. Once your annuity starting

date is determined, it doesn't change. If you calculate the

taxable portion of your annuity payments using the simpli-

fied method worksheet, the annuity starting date deter-

mines the recovery period for your cost. That recovery pe-

riod begins on your annuity starting date and isn't affected

by the date you first complete the worksheet.

Exclusion limited to cost. If your annuity starting

date is after 1986, the total amount of annuity income that

you can exclude over the years as a recovery of the cost

can't exceed your total cost. Any unrecovered cost at your

(or the last annuitant's) death is allowed as a miscellane-

ous itemized deduction on the final return of the decedent.

This deduction isn't subject to the 2%-of-adjus-

ted-gross-income limit.

Example 1. Your annuity starting date is after 1986,

and you exclude $100 a month ($1,200 a year) under the

Simplified Method. The total cost of your annuity is

$12,000. Your exclusion ends when you have recovered

your cost tax free, that is, after 10 years (120 months). Af-

ter that, your annuity payments are generally fully taxable.

Example 2. The facts are the same as in Example 1,

except you die (with no surviving annuitant) after the

eighth year of retirement. You have recovered tax free

only $9,600 (8 × $1,200) of your cost. An itemized deduc-

tion for your unrecovered cost of $2,400 ($12,000 –

$9,600) can be taken on your final return.

Exclusion not limited to cost. If your annuity starting

date is before 1987, you can continue to take your

monthly exclusion for as long as you receive your annuity.

If you chose a joint and survivor annuity, your survivor can

continue to take the survivor's exclusion figured as of the

annuity starting date. The total exclusion may be more

than your cost.

Simplified Method

Under the Simplified Method, you figure the tax-free part

of each annuity payment by dividing your cost by the total

number of anticipated monthly payments. For an annuity

that is payable for the lives of the annuitants, this number

is based on the annuitants' ages on the annuity starting

date and is determined from a table. For any other annu-

ity, this number is the number of monthly annuity pay-

ments under the contract.

Who must use the Simplified Method. You must use

the Simplified Method if your annuity starting date is after

November 18, 1996, and you meet both of the following

conditions.

1. You receive your pension or annuity payments from

any of the following plans.

a. A qualified employee plan.

b. A qualified employee annuity.

c. A tax-sheltered annuity plan (403(b) plan).

2. On your annuity starting date, at least one of the fol-

lowing conditions applies to you.

a. You are under age 75.

b. You are entitled to less than 5 years of guaranteed

payments.

Page 12 Publication 575 (2016)

Page 13 of 43 Fileid: … tions/P575/2016/A/XML/Cycle02/source 12:08 - 4-Jan-2017

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Guaranteed payments. Your annuity contract pro-

vides guaranteed payments if a minimum number of pay-

ments or a minimum amount (for example, the amount of

your investment) is payable even if you and any survivor

annuitant don't live to receive the minimum. If the mini-

mum amount is less than the total amount of the pay-

ments you are to receive, barring death, during the first 5

years after payments begin (figured by ignoring any pay-

ment increases), you are entitled to less than 5 years of

guaranteed payments.

Annuity starting before November 19, 1996. If your

annuity starting date is after July 1, 1986, and before No-

vember 19, 1996, and you chose to use the Simplified

Method, you must continue to use it each year that you re-

cover part of your cost. You could have chosen to use the

Simplified Method if your annuity is payable for your life

(or the lives of you and your survivor annuitant) and you

met both of the conditions listed earlier under Who must

use the Simplified Method.

Who can't use the Simplified Method. You can't use

the Simplified Method if you receive your pension or annu-

ity from a nonqualified plan or otherwise don't meet the

conditions described in the preceding discussion. See

General Rule, later.

How to use the Simplified Method. Complete Work-

sheet A in the back of this publication to figure your taxa-

ble annuity for 2016. Be sure to keep the completed work-

sheet; it will help you figure your taxable annuity next year.

To complete line 3 of the worksheet, you must deter-

mine the total number of expected monthly payments for

your annuity. How you do this depends on whether the an-

nuity is for a single life, multiple lives, or a fixed period. For

this purpose, treat an annuity that is payable over the life

of an annuitant as payable for that annuitant's life even if

the annuity has a fixed-period feature or also provides a

temporary annuity payable to the annuitant's child under

age 25.

You don't need to complete line 3 of the work

sheet or make the computation on line 4 if you re

ceived annuity payments last year and used last

year's worksheet to figure your taxable annuity. Instead,

enter the amount from line 4 of last year's worksheet on

line 4 of this year's worksheet.

Singlelife annuity. If your annuity is payable for your

life alone, use Table 1 at the bottom of the worksheet to

determine the total number of expected monthly pay-

ments. Enter on line 3 the number shown for your age on

your annuity starting date. This number will differ depend-

ing on whether your annuity starting date is before No-

vember 19, 1996, or after November 18, 1996.

Multiplelives annuity. If your annuity is payable for

the lives of more than one annuitant, use Table 2 at the

bottom of the worksheet to determine the total number of

expected monthly payments. Enter on line 3 the number

shown for the annuitants' combined ages on the annuity

starting date. For an annuity payable to you as the primary

annuitant and to more than one survivor annuitant,

TIP

combine your age and the age of the youngest survivor

annuitant. For an annuity that has no primary annuitant

and is payable to you and others as survivor annuitants,

combine the ages of the oldest and youngest annuitants.

Don't treat as a survivor annuitant anyone whose entitle-

ment to payments depends on an event other than the pri-

mary annuitant's death.

However, if your annuity starting date is before 1998,

don't use Table 2 and don't combine the annuitants' ages.

Instead, you must use Table 1 at the bottom of the work-

sheet and enter on line 3 the number shown for the pri-

mary annuitant's age on the annuity starting date. This

number will differ depending on whether your annuity

starting date is before November 19, 1996, or after No-

vember 18, 1996.

Fixedperiod annuity. If your annuity doesn't depend

in whole or in part on anyone's life expectancy, the total

number of expected monthly payments to enter on line 3

of the worksheet is the number of monthly annuity pay-

ments under the contract.

Line 6. The amount on line 6 should include all

amounts that could have been recovered in prior years. If

you didn't recover an amount in a prior year, you may be

able to amend your returns for the affected years.

Example. Bill Smith, age 65, began receiving retire-

ment benefits in 2016 under a joint and survivor annuity.

Bill's annuity starting date is January 1, 2016. The benefits

are to be paid for the joint lives of Bill and his wife, Kathy,

age 65. Bill had contributed $31,000 to a qualified plan

and had received no distributions before the annuity start-

ing date. Bill is to receive a retirement benefit of $1,200 a

month, and Kathy is to receive a monthly survivor benefit

of $600 upon Bill's death.

Bill must use the Simplified Method to figure his taxable

annuity because his payments are from a qualified plan

and he is under age 75. Because his annuity is payable

over the lives of more than one annuitant, he uses his and

Kathy's combined ages and Table 2 at the bottom of

Worksheet A in completing line 3 of the worksheet. His

completed worksheet is shown later.

Bill's tax-free monthly amount is $100 ($31,000 ÷ 310)

as shown on line 4 of the worksheet. Upon Bill's death, if

Bill hasn't recovered the full $31,000 investment, Kathy

will also exclude $100 from her $600 monthly payment.

The full amount of any annuity payments received after

310 payments are paid must be included in gross income.

If Bill and Kathy die before 310 payments are made, a

miscellaneous itemized deduction will be allowed for the

unrecovered cost on the final income tax return of the last

to die. This deduction isn’t subject to the 2%-of-adjus-

ted-gross-income limit.

Multiple annuitants. If you and one or more other annui-

tants receive payments at the same time, you exclude

from each annuity payment a pro rata share of the

monthly tax-free amount. Figure your share by taking the

following steps.

1. Complete your worksheet through line 4 to figure the

monthly tax-free amount.

Publication 575 (2016) Page 13

Page 14 of 43 Fileid: … tions/P575/2016/A/XML/Cycle02/source 12:08 - 4-Jan-2017

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

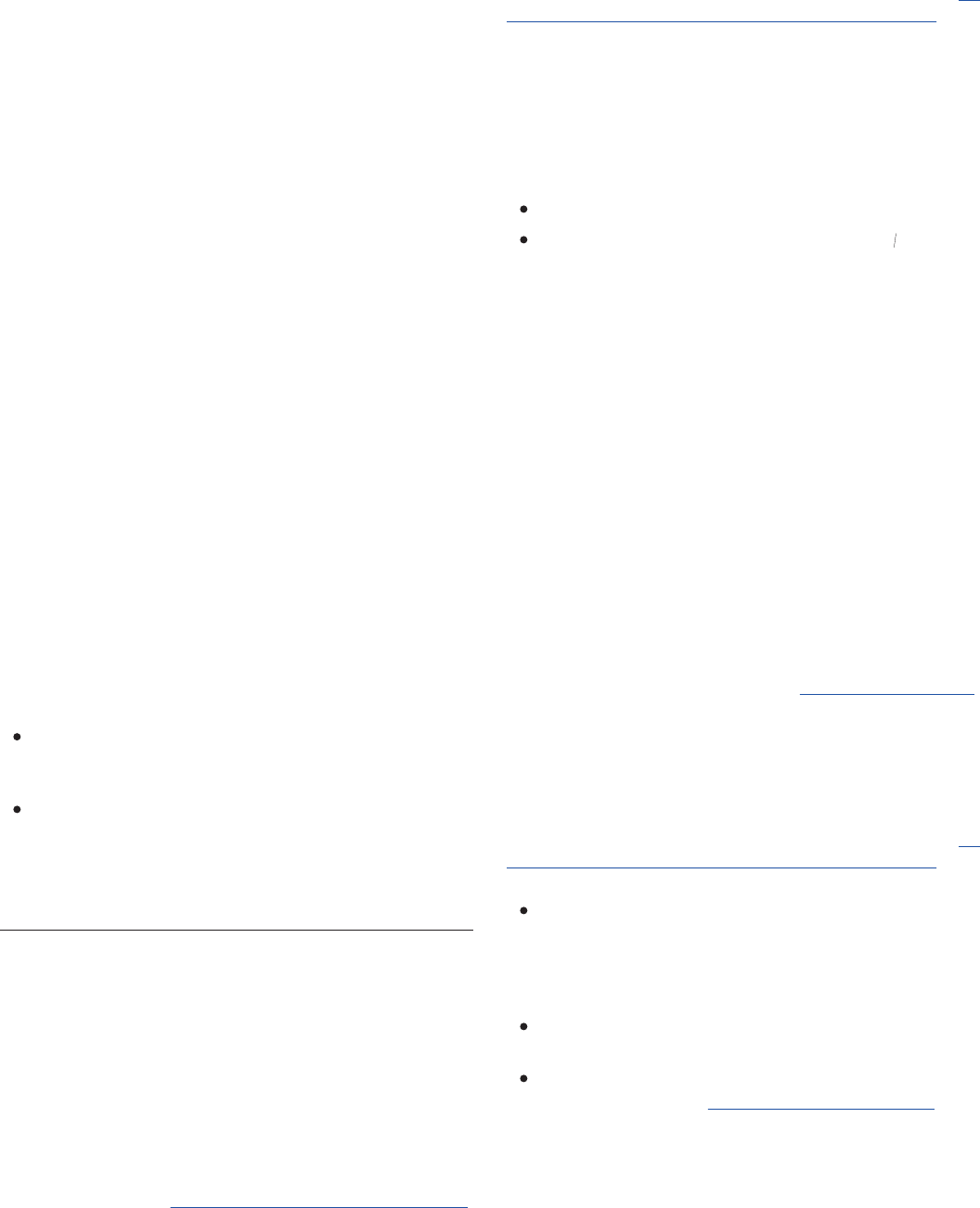

Worksheet A. Simplified Method Worksheet for Bill Smith

Keep for Your Records

1. Enter the total pension or annuity payments received this year. Also, add this amount to the total

for Form 1040, line 16a; Form 1040A, line 12a; or Form 1040NR, line 17a ................... 1. $ 14,400

2. Enter your cost in the plan (contract) at the annuity starting date plus any death benefit

exclusion.* See Cost (Investment in the Contract), earlier ................................. 2. 31,000

Note. If your annuity starting date was before this year and you completed this worksheet last

year, skip line 3 and enter the amount from line 4 of last year's worksheet on line 4 below (even if

the amount of your pension or annuity has changed). Otherwise, go to line 3.

3. Enter the appropriate number from Table 1 below. But if your annuity starting date was after

1997 and the payments are for your life and that of your beneficiary, enter the appropriate