2017 Publication 946 Amana Air Conditioner RCB18C2CP1247513C P946

User Manual: Amana Air Conditioner RCB18C2CP1247513C

Open the PDF directly: View PDF ![]() .

.

Page Count: 115 [warning: Documents this large are best viewed by clicking the View PDF Link!]

- Contents

- Future Developments

- What's New for 2017

- What's New for 2018

- Reminders

- Introduction

- Chapter 1 Overview of Depreciation

- Introduction

- What Property Can Be Depreciated?

- What Property Cannot Be Depreciated?

- When Does Depreciation Begin and End?

- What Method Can You Use To Depreciate Your Property?

- What Is the Basis of Your Depreciable Property?

- How Do You Treat Repairs and Improvements?

- Do You Have To File Form 4562?

- How Do You Correct Depreciation Deductions?

- Chapter 2 Electing the Section 179 Deduction

- Chapter 3 Claiming the Special Depreciation Allowance

- Chapter 4 Figuring Depreciation Under MACRS

- Introduction

- Which Depreciation System (GDS or ADS) Applies?

- Which Property Class Applies Under GDS?

- What Is the Placed in Service Date?

- What Is the Basis for Depreciation?

- Which Recovery Period Applies?

- Which Convention Applies?

- Which Depreciation Method Applies?

- How Is the Depreciation Deduction Figured?

- How Do You Use General Asset Accounts?

- When Do You Recapture MACRS Depreciation?

- Chapter 5 Additional Rules for Listed Property

- Chapter 6 How To Get Tax Help

- Appendix B — Table of Class Lives and Recovery Periods

- Index

Userid: CPM Schema: tipx Leadpct: 100% Pt. size: 10 Draft Ok to Print

AH XSL/XML Fileid: … tions/P946/2017/A/XML/Cycle03/source (Init. & Date) _______

Page 1 of 115 15:20 - 28-Feb-2018

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Department of the Treasury

Internal Revenue Service

Publication 946

Cat. No. 13081F

How To

Depreciate

Property

• Section 179 Deduction

• Special Depreciation

Allowance

• MACRS

• Listed Property

For use in preparing

2017 Returns

Get forms and other information faster and easier at:

•IRS.gov (English)

•IRS.gov/Spanish (Español)

•IRS.gov/Chinese (中文)

•IRS.gov/Korean (한국어)

•IRS.gov/Russian (Pусский)

•IRS.gov/Vietnamese (TiếngViệt)

Contents

Future Developments ....................... 2

What's New for 2017 ........................ 2

What's New for 2018 ........................ 2

Reminders ............................... 3

Introduction .............................. 3

Chapter 1. Overview of Depreciation .......... 3

What Property Can Be Depreciated? .......... 4

What Property Cannot Be Depreciated? ........ 6

When Does Depreciation Begin and End? ...... 7

What Method Can You Use To Depreciate

Your Property? ........................ 8

What Is the Basis of Your Depreciable

Property? ........................... 11

How Do You Treat Repairs and

Improvements? ...................... 13

Do You Have To File Form 4562? ........... 13

How Do You Correct Depreciation

Deductions? ......................... 13

Chapter 2. Electing the Section 179

Deduction ............................ 15

What Property Qualifies? .................. 15

What Property Does Not Qualify? ........... 18

How Much Can You Deduct? ............... 19

How Do You Elect the Deduction? ........... 23

When Must You Recapture the Deduction? .... 23

Chapter 3. Claiming the Special Depreciation

Allowance ............................ 24

What Is Qualified Property? ................ 24

Election To Accelerate Certain Credits in Lieu

of the Special Depreciation Allowance ...... 28

How Much Can You Deduct? ............... 28

How Can You Elect Not To Claim an

Allowance? ......................... 29

When Must You Recapture an Allowance? ..... 29

Chapter 4. Figuring Depreciation Under

MACRS .............................. 29

Which Depreciation System (GDS or ADS)

Applies? ........................... 30

Which Property Class Applies Under GDS? .... 31

What Is the Placed in Service Date? .......... 34

What Is the Basis for Depreciation? .......... 34

Which Recovery Period Applies? ............ 35

Which Convention Applies? ................ 37

Which Depreciation Method Applies? ......... 38

How Is the Depreciation Deduction Figured? ... 40

How Do You Use General Asset Accounts? .... 50

When Do You Recapture MACRS

Depreciation? ........................ 54

Feb 28, 2018

Page 2 of 115 Fileid: … tions/P946/2017/A/XML/Cycle03/source 15:20 - 28-Feb-2018

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Chapter 5. Additional Rules for Listed

Property ............................. 55

What Is Listed Property? .................. 55

Can Employees Claim a Deduction? ......... 57

What Is the Business-Use Requirement? ...... 58

Do the Passenger Automobile Limits Apply? .... 62

What Records Must Be Kept? .............. 66

How Is Listed Property Information

Reported? .......................... 67

Chapter 6. How To Get Tax Help ............. 68

Appendix A .............................. 71

Appendix B .............................. 99

Glossary ............................... 111

Index ................................. 113

Future Developments

For the latest information about developments related to

Pub. 946, such as legislation enacted after this publication

was published, go to IRS.gov/Pub946.

What's New for 2017

Increased section 179 deduction dollar limits. The

maximum amount you can elect to deduct for most sec-

tion 179 property you placed in service in tax years begin-

ning in 2017 is $510,000 ($545,000 for qualified enter-

prise zone property). This limit is reduced by the amount

by which the cost of section 179 property placed in serv-

ice during the tax year exceeds $2,030,000. See Dollar

Limits in chapter 2.

Special depreciation allowance for certain property.

You may be able to take a 50% special depreciation al-

lowance for certain property acquired before September

28, 2017, and placed in service before January 1, 2018,

and certain plants bearing fruits and nuts, planted or graf-

ted before September 28, 2017. The special allowance

will be phased down to 40% for certain property acquired

before September 28, 2017, and placed in service in

2018. Also, you may be able to take a 100% special de-

preciation allowance for certain property and certain

plants bearing fruits and nuts acquired or planted or graf-

ted after September 27, 2017, and placed in service or

planted or grafted after September 27, 2017, and placed

in service or planted or grafted before January 1, 2023.

You may elect to apply a 50% special depreciation allow-

ance instead of the 100% allowance for the first tax year

ending after September 27, 2017. See Certain qualified

property acquired before September 28, 2017, Certain

property acquired after September 27, 2017, and Certain

plants bearing fruits and nuts, later.

Special depreciation allowance for qualified second

generation biofuel plant property. The special depre-

ciation allowance will not apply to qualified second

generation biofuel plant property placed in service after

December 31, 2017. See Qualified Second Generation Bi-

ofuel Plant Property in chapter 3.

Certain race horses. The 3-year recovery period for

race horses two years old or younger will not apply to

horses placed in service after December 31, 2017. See

Which Property Class Applies Under GDS in chapter 4.

Qualified motor sports entertainment complexes.

Qualified motor sports entertainment complex property

placed in service after December 31, 2017, will not be

treated as 7-year property under MACRS. See Which

Property Class Applies Under GDS in chapter 4.

Accelerated depreciation for qualified Indian reser-

vation property. The accelerated depreciation of prop-

erty on an Indian reservation will not apply to property

placed in service after December 31, 2017, or, if you

make an irrevocable election out of all property in a class

of property that is placed in service in a tax year beginning

after December 31, 2016. See Indian Reservation Prop-

erty in chapter 4.

Depreciation limits on business vehicles. The total

section 179 deduction and depreciation you can deduct

for a passenger automobile (that is not a truck or van) you

use in your business and first placed in service in 2017 is

$3,160, if the special depreciation allowance does not ap-

ply. The maximum deduction you can take for a truck or

van you use in your business and first placed in service in

2017 is $3,560, if the special depreciation allowance does

not apply. See Maximum Depreciation Deduction in chap-

ter 5.

What's New for 2018

Section 179 deduction dollar limits. The maximum

amount you can elect to deduct for most section 179 prop-

erty you placed in service in tax years beginning in 2018 is

$1,000,000. This limit is reduced by the amount by which

the cost of section 179 property placed in service during

the tax year exceeds $2,500,000.

Section 179 qualified real property. For property

placed in service in tax years beginning after December

31, 2017, section 179 qualified real property is qualified

improvement property (as defined in section 168(e)(6)),

and certain specified improvements to nonresidential real

property placed in service after the nonresidential real

property was first placed in service.

Computers and related peripheral equipment. Com-

puters and related peripheral equipment placed in service

after December 31, 2017, in tax years ending after De-

cember 31, 2017, are not listed property.

Electing real property trade or business and electing

farm business. An electing real property trade or busi-

ness (as defined in section 163(j)(7)(B)) and electing

farming business (as defined in section 163(j)(7)(C)) are

required to use the alternative depreciation system for

certain property to figure depreciation under MACRS for

tax years beginning after December 31, 2017.

Page 2 Publication 946 (2017)

Page 3 of 115 Fileid: … tions/P946/2017/A/XML/Cycle03/source 15:20 - 28-Feb-2018

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Reminders

Photographs of missing children. The Internal Reve-

nue Service is a proud partner with the National Center for

Missing & Exploited Children® (NCMEC). Photographs of

missing children selected by the Center may appear in

this publication on pages that would otherwise be blank.

You can help bring these children home by looking at the

photographs and calling 1-800-THE-LOST

(1-800-843-5678) if you recognize a child.

Introduction

This publication explains how you can recover the cost of

business or income-producing property through deduc-

tions for depreciation (for example, the special deprecia-

tion allowance and deductions under the Modified Accel-

erated Cost Recovery System (MACRS)). It also explains

how you can elect to take a section 179 deduction, in-

stead of depreciation deductions, for certain property, and

the additional rules for listed property.

The depreciation methods discussed in this publi-

cation generally do not apply to property placed in

service before 1987. For more information, see

Pub. 534, Depreciating Property Placed in Service Before

1987.

Definitions. Many of the terms used in this publication

are defined in the Glossary near the end of the publica-

tion. Glossary terms used in each discussion under the

major headings are listed before the beginning of each

discussion throughout the publication.

Do you need a different publication? The following ta-

ble shows where you can get more detailed information

when depreciating certain types of property.

For information

on depreciating:

See Publication:

A car 463, Travel, Entertainment, Gift, and

Car Expenses

Residential rental

property

527, Residential Rental Property

(Including Rental of Vacation Home)

Office space in

your home

587, Business Use of Your Home

(Including Use by Daycare Providers)

Farm property 225, Farmer's Tax Guide

Comments and suggestions. We welcome your com-

ments about this publication and your suggestions for fu-

ture editions.

You can send us comments from IRS.gov/

FormsComments. Or you can write to:

Internal Revenue Service

Tax Forms and Publications

1111 Constitution Ave. NW, IR-6526

Washington, DC 20224

CAUTION

!

Although we cannot respond individually to each com-

ment received, we do appreciate your feedback and will

consider your comments as we revise our tax products.

Ordering forms and publications. Visit IRS.gov/

FormsPubs to download forms and publications. Other-

wise, you can go to IRS.gov/OrderForms to order current

and prior-year forms and instructions. Your order should

arrive within 10 business days.

Tax questions. If you have a tax question not an-

swered by this publication, check IRS.gov and How To

Get Tax Help at the end of this publication.

1.

Overview of Depreciation

Introduction

Depreciation is an annual income tax deduction that al-

lows you to recover the cost or other basis of certain prop-

erty over the time you use the property. It is an allowance

for the wear and tear, deterioration, or obsolescence of

the property.

This chapter discusses the general rules for depreciat-

ing property and answers the following questions.

What property can be depreciated?

What property cannot be depreciated?

When does depreciation begin and end?

What method can you use to depreciate your prop-

erty?

What is the basis of your depreciable property?

How do you treat repairs and improvements?

Do you have to file Form 4562?

How do you correct depreciation deductions?

Useful Items

You may want to see:

Publication

Depreciating Property Placed in Service Before

1987

Business Expenses

Accounting Periods and Methods

Basis of Assets

Form (and Instructions)

Profit or Loss From Business

Net Profit From Business

534

535

538

551

Sch C (Form 1040)

Sch C-EZ (Form 1040)

Page 3

Page 4 of 115 Fileid: … tions/P946/2017/A/XML/Cycle03/source 15:20 - 28-Feb-2018

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Employee Business Expenses

Unreimbursed Employee Business

Expenses

Application for Change in Accounting Method

Depreciation and Amortization

See chapter 6 for information about getting publications

and forms.

What Property Can Be

Depreciated?

Terms you may need to know

(see Glossary):

Adjusted basis

Basis

Commuting

Disposition

Fair market value

Intangible property

Listed property

Placed in service

Tangible property

Term interest

Useful life

You can depreciate most types of tangible property (ex-

cept land), such as buildings, machinery, vehicles, furni-

ture, and equipment. You also can depreciate certain in-

tangible property, such as patents, copyrights, and

computer software.

To be depreciable, the property must meet all the fol-

lowing requirements.

It must be property you own.

It must be used in your business or income-producing

activity.

It must have a determinable useful life.

It must be expected to last more than one year.

The following discussions provide information about these

requirements.

Property You Own

To claim depreciation, you usually must be the owner of

the property. You are considered as owning property even

if it is subject to a debt.

Example 1. You made a down payment to purchase

rental property and assumed the previous owner's mort-

gage. You own the property and you can depreciate it.

2106

2106-EZ

3115

4562

Example 2. You bought a new van that you will use

only for your courier business. You will be making pay-

ments on the van over the next 5 years. You own the van

and you can depreciate it.

Leased property. You can depreciate leased property

only if you retain the incidents of ownership in the property

(explained below). This means you bear the burden of ex-

haustion of the capital investment in the property. There-

fore, if you lease property from someone to use in your

trade or business or for the production of income, you

generally cannot depreciate its cost because you do not

retain the incidents of ownership. You can, however, de-

preciate any capital improvements you make to the prop-

erty. See How Do You Treat Repairs and Improvements

later in this chapter, and Additions and Improvements un-

der Which Recovery Period Applies in chapter 4.

If you lease property to someone, you generally can

depreciate its cost even if the lessee (the person leasing

from you) has agreed to preserve, replace, renew, and

maintain the property. However, if the lease provides that

the lessee is to maintain the property and return to you the

same property or its equivalent in value at the expiration of

the lease in as good condition and value as when leased,

you cannot depreciate the cost of the property.

Incidents of ownership. Incidents of ownership in

property include the following.

The legal title to the property.

The legal obligation to pay for the property.

The responsibility to pay maintenance and operating

expenses.

The duty to pay any taxes on the property.

The risk of loss if the property is destroyed, con-

demned, or diminished in value through obsolescence

or exhaustion.

Life tenant. Generally, if you hold business or investment

property as a life tenant, you can depreciate it as if you

were the absolute owner of the property. However, see

Certain term interests in property under Excepted Prop-

erty, later.

Cooperative apartments. If you are a tenant-stock-

holder in a cooperative housing corporation and use your

cooperative apartment in your business or for the produc-

tion of income, you can depreciate your stock in the cor-

poration, even though the corporation owns the apart-

ment.

Figure your depreciation deduction as follows.

1. Figure the depreciation for all the depreciable real

property owned by the corporation in which you have

a proprietary lease or right of tenancy. If you bought

your cooperative stock after its first offering, figure the

depreciable basis of this property as follows.

a. Multiply your cost per share by the total number of

outstanding shares, including any shares held by

the corporation.

Page 4 Chapter 1 Overview of Depreciation

Page 5 of 115 Fileid: … tions/P946/2017/A/XML/Cycle03/source 15:20 - 28-Feb-2018

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

b. Add to the amount figured in (a) any mortgage

debt on the property on the date you bought the

stock.

c. Subtract from the amount figured in (b) any mort-

gage debt that is not for the depreciable real prop-

erty, such as the part for the land.

2. Subtract from the amount figured in (1) any deprecia-

tion for space owned by the corporation that can be

rented but cannot be lived in by tenant-stockholders.

3. Divide the number of your shares of stock by the total

number of outstanding shares, including any shares

held by the corporation.

4. Multiply the result of (2) by the percentage you figured

in (3). This is your depreciation on the stock.

Your depreciation deduction for the year cannot be

more than the part of your adjusted basis in the stock of

the corporation that is allocable to your business or in-

come-producing property. You must also reduce your de-

preciation deduction if only a portion of the property is

used in a business or for the production of income.

Example. You figure your share of the cooperative

housing corporation's depreciation to be $30,000. Your

adjusted basis in the stock of the corporation is $50,000.

You use one half of your apartment solely for business

purposes. Your depreciation deduction for the stock for

the year cannot be more than $25,000 (12 of $50,000).

Change to business use. If you change your cooper-

ative apartment to business use, figure your allowable de-

preciation as explained earlier. The basis of all the depre-

ciable real property owned by the cooperative housing

corporation is the smaller of the following amounts.

The fair market value of the property on the date you

change your apartment to business use. This is con-

sidered to be the same as the corporation's adjusted

basis minus straight line depreciation, unless this

value is unrealistic.

The corporation's adjusted basis in the property on

that date. Do not subtract depreciation when figuring

the corporation's adjusted basis.

If you bought the stock after its first offering, the corpo-

ration's adjusted basis in the property is the amount fig-

ured in (1) above. The fair market value of the property is

considered to be the same as the corporation's adjusted

basis figured in this way minus straight line depreciation,

unless the value is unrealistic.

For a discussion of fair market value and adjusted ba-

sis, see Pub. 551.

Property Used in Your Business or

Income-Producing Activity

To claim depreciation on property, you must use it in your

business or income-producing activity. If you use property

to produce income (investment use), the income must be

taxable. You cannot depreciate property that you use

solely for personal activities.

Partial business or investment use. If you use prop-

erty for business or investment purposes and for personal

purposes, you can deduct depreciation based only on the

business or investment use. For example, you cannot de-

duct depreciation on a car used only for commuting, per-

sonal shopping trips, family vacations, driving children to

and from school, or similar activities.

You must keep records showing the business, in-

vestment, and personal use of your property. For

more information on the records you must keep

for listed property, such as a car, see What Records Must

Be Kept in chapter 5.

Although you can combine business and invest-

ment use of property when figuring depreciation

deductions, do not treat investment use as quali-

fied business use when determining whether the busi-

ness-use requirement for listed property is met. For infor-

mation about qualified business use of listed property, see

What Is the Business-Use Requirement in chapter 5.

Office in the home. If you use part of your home as

an office, you may be able to deduct depreciation on that

part based on its business use. For information about de-

preciating your home office, see Pub. 587.

Inventory. You cannot depreciate inventory because it is

not held for use in your business. Inventory is any property

you hold primarily for sale to customers in the ordinary

course of your business.

If you are a rent-to-own dealer, you may be able to treat

certain property held in your business as depreciable

property rather than as inventory. See Rent-to-own dealer

under Which Property Class Applies Under GDS in chap-

ter 4.

In some cases, it is not clear whether property is held

for sale (inventory) or for use in your business. If it is un-

clear, examine carefully all the facts in the operation of the

particular business. The following example shows how a

careful examination of the facts in two similar situations re-

sults in different conclusions.

Example. Maple Corporation is in the business of

leasing cars. At the end of their useful lives, when the cars

are no longer profitable to lease, Maple sells them. Maple

does not have a showroom, used car lot, or individuals to

sell the cars. Instead, it sells them through wholesalers or

by similar arrangements in which a dealer's profit is not in-

tended or considered. Maple can depreciate the leased

cars because the cars are not held primarily for sale to

customers in the ordinary course of business, but are

leased.

If Maple buys cars at wholesale prices, leases them for

a short time, and then sells them at retail prices or in sales

in which a dealer's profit is intended, the cars are treated

as inventory and are not depreciable property. In this sit-

uation, the cars are held primarily for sale to customers in

the ordinary course of business.

Containers. Generally, containers for the products

you sell are part of inventory and you cannot depreciate

them. However, you can depreciate containers used to

RECORDS

CAUTION

!

Chapter 1 Overview of Depreciation Page 5

Page 6 of 115 Fileid: … tions/P946/2017/A/XML/Cycle03/source 15:20 - 28-Feb-2018

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

ship your products if they have a life longer than one year

and meet the following requirements.

They qualify as property used in your business.

Title to the containers does not pass to the buyer.

To determine if these requirements are met, consider

the following questions.

Does your sales contract, sales invoice, or other type

of order acknowledgment indicate whether you have

retained title?

Does your invoice treat the containers as separate

items?

Do any of your records state your basis in the contain-

ers?

Property Having a Determinable

Useful Life

To be depreciable, your property must have a determina-

ble useful life. This means that it must be something that

wears out, decays, gets used up, becomes obsolete, or

loses its value from natural causes.

Property Lasting More Than One Year

To be depreciable, property must have a useful life that

extends substantially beyond the year you place it in serv-

ice.

Example. You maintain a library for use in your profes-

sion. You can depreciate it. However, if you buy technical

books, journals, or information services for use in your

business that have a useful life of one year or less, you

cannot depreciate them. Instead, you deduct their cost as

a business expense.

What Property Cannot Be

Depreciated?

Terms you may need to know

(see Glossary):

Amortization

Basis

Goodwill

Intangible property

Remainder interest

Term interest

Certain property cannot be depreciated. This includes

land and certain excepted property.

Land

You cannot depreciate the cost of land because land does

not wear out, become obsolete, or get used up. The cost

of land generally includes the cost of clearing, grading,

planting, and landscaping.

Although you cannot depreciate land, you can depreci-

ate certain land preparation costs, such as landscaping

costs, incurred in preparing land for business use. These

costs must be so closely associated with other deprecia-

ble property that you can determine a life for them along

with the life of the associated property.

Example. You constructed a new building for use in

your business and paid for grading, clearing, seeding, and

planting bushes and trees. Some of the bushes and trees

were planted right next to the building, while others were

planted around the outer border of the lot. If you replace

the building, you would have to destroy the bushes and

trees right next to it. These bushes and trees are closely

associated with the building, so they have a determinable

useful life. Therefore, you can depreciate them. Add your

other land preparation costs to the basis of your land be-

cause they have no determinable life and you cannot de-

preciate them.

Excepted Property

Even if the requirements explained in the preceding dis-

cussions are met, you cannot depreciate the following

property.

Property placed in service and disposed of in the

same year. Determining when property is placed in

service is explained later.

Equipment used to build capital improvements. You

must add otherwise allowable depreciation on the

equipment during the period of construction to the ba-

sis of your improvements. See Uniform Capitalization

Rules in Pub. 551.

Section 197 intangibles. You must amortize these

costs. Section 197 intangibles are discussed in detail

in chapter 8 of Pub. 535. Intangible property, such as

certain computer software, that is not section 197 in-

tangible property, can be depreciated if it meets cer-

tain requirements. See Intangible Property, later.

Certain term interests.

Certain term interests in property. You cannot depre-

ciate a term interest in property created or acquired after

July 27, 1989, for any period during which the remainder

interest is held, directly or indirectly, by a person related to

you. A term interest in property means a life interest in

property, an interest in property for a term of years, or an

income interest in a trust.

Related persons. For a description of related per-

sons, see Related Persons, later. For this purpose, how-

ever, treat as related persons only the relationships listed

in items (1) through (10) of that discussion and substitute

“50%” for “10%” each place it appears.

Page 6 Chapter 1 Overview of Depreciation

Page 7 of 115 Fileid: … tions/P946/2017/A/XML/Cycle03/source 15:20 - 28-Feb-2018

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Basis adjustments. If you would be allowed a depre-

ciation deduction for a term interest in property except that

the holder of the remainder interest is related to you, you

generally must reduce your basis in the term interest by

any depreciation or amortization not allowed.

If you hold the remainder interest, you generally must

increase your basis in that interest by the depreciation not

allowed to the term interest holder. However, do not in-

crease your basis for depreciation not allowed for periods

during which either of the following situations applies.

The term interest is held by an organization exempt

from tax.

The term interest is held by a nonresident alien indi-

vidual or foreign corporation, and the income from the

term interest is not effectively connected with the con-

duct of a trade or business in the United States.

Exceptions. The above rules do not apply to the

holder of a term interest in property acquired by gift, be-

quest, or inheritance. They also do not apply to the holder

of dividend rights that were separated from any stripped

preferred stock if the rights were purchased after April 30,

1993, or to a person whose basis in the stock is deter-

mined by reference to the basis in the hands of the pur-

chaser.

When Does Depreciation

Begin and End?

Terms you may need to know

(see Glossary):

Basis

Exchange

Placed in service

You begin to depreciate your property when you place it in

service for use in your trade or business or for the produc-

tion of income. You stop depreciating property either

when you have fully recovered your cost or other basis or

when you retire it from service, whichever happens first.

Placed in Service

You place property in service when it is ready and availa-

ble for a specific use, whether in a business activity, an in-

come-producing activity, a tax-exempt activity, or a per-

sonal activity. Even if you are not using the property, it is

in service when it is ready and available for its specific

use.

Example 1. Donald Steep bought a machine for his

business. The machine was delivered last year. However,

it was not installed and operational until this year. It is con-

sidered placed in service this year. If the machine had

been ready and available for use when it was delivered, it

would be considered placed in service last year even if it

was not actually used until this year.

Example 2. On April 6, Sue Thorn bought a house to

use as residential rental property. She made several re-

pairs and had it ready for rent on July 5. At that time, she

began to advertise it for rent in the local newspaper. The

house is considered placed in service in July when it was

ready and available for rent. She can begin to depreciate

it in July.

Example 3. James Elm is a building contractor who

specializes in constructing office buildings. He bought a

truck last year that had to be modified to lift materials to

second-story levels. The installation of the lifting equip-

ment was completed and James accepted delivery of the

modified truck on January 10 of this year. The truck was

placed in service on January 10, the date it was ready and

available to perform the function for which it was bought.

Conversion to business use. If you place property in

service in a personal activity, you cannot claim deprecia-

tion. However, if you change the property's use to use in a

business or income-producing activity, then you can begin

to depreciate it at the time of the change. You place the

property in service in the business or income-producing

activity on the date of the change.

Example. You bought a home and used it as your per-

sonal home several years before you converted it to rental

property. Although its specific use was personal and no

depreciation was allowable, you placed the home in serv-

ice when you began using it as your home. You can begin

to claim depreciation in the year you converted it to rental

property because its use changed to an income-produc-

ing use at that time.

Idle Property

Continue to claim a deduction for depreciation on property

used in your business or for the production of income

even if it is temporarily idle (not in use). For example, if

you stop using a machine because there is a temporary

lack of a market for a product made with that machine,

continue to deduct depreciation on the machine.

Cost or Other Basis Fully Recovered

You stop depreciating property when you have fully recov-

ered your cost or other basis. You recover your basis

when your section 179 and allowed or allowable deprecia-

tion deductions equal your cost or investment in the prop-

erty. See What Is the Basis of Your Depreciable Property,

later.

Retired From Service

You stop depreciating property when you retire it from

service, even if you have not fully recovered its cost or

other basis. You retire property from service when you

permanently withdraw it from use in a trade or business or

Chapter 1 Overview of Depreciation Page 7

Page 8 of 115 Fileid: … tions/P946/2017/A/XML/Cycle03/source 15:20 - 28-Feb-2018

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

from use in the production of income because of any of

the following events.

You sell or exchange the property.

You convert the property to personal use.

You abandon the property.

You transfer the property to a supplies or scrap ac-

count.

The property is destroyed.

If you included the property in a general asset ac-

count, see How Do You Use General Asset Ac-

counts in chapter 4 for the rules that apply when

you dispose of that property.

What Method Can You Use To

Depreciate Your Property?

Terms you may need to know

(see Glossary):

Adjusted basis

Basis

Convention

Exchange

Fiduciary

Grantor

Intangible property

Nonresidential real property

Placed in service

Related persons

Residential rental property

Salvage value

Section 1245 property

Section 1250 property

Standard mileage rate

Straight line method

Unit-of-production method

Useful life

You must use the Modified Accelerated Cost Recovery

System (MACRS) to depreciate most property. MACRS is

discussed in chapter 4.

You cannot use MACRS to depreciate the following

property.

Property you placed in service before 1987.

Certain property owned or used in 1986.

Intangible property.

CAUTION

!

Films, video tapes, and recordings.

Certain corporate or partnership property acquired in

a nontaxable transfer.

Property you elected to exclude from MACRS.

The following discussions describe the property listed

above and explain what depreciation method should be

used.

Property You Placed in Service

Before 1987

You cannot use MACRS for property you placed in serv-

ice before 1987 (except property you placed in service af-

ter July 31, 1986, if MACRS was elected). Property placed

in service before 1987 must be depreciated under the

methods discussed in Pub. 534.

For a discussion of when property is placed in service,

see When Does Depreciation Begin and End, earlier.

Use of real property changed. You generally must use

MACRS to depreciate real property that you acquired for

personal use before 1987 and changed to business or in-

come-producing use after 1986.

Improvements made after 1986. You must treat an im-

provement made after 1986 to property you placed in

service before 1987 as separate depreciable property.

Therefore, you can depreciate that improvement as sepa-

rate property under MACRS if it is the type of property that

otherwise qualifies for MACRS depreciation. For more in-

formation about improvements, see How Do You Treat

Repairs and Improvements, later, and Additions and Im-

provements under Which Recovery Period Applies in

chapter 4.

Property Owned or Used in 1986

You may not be able to use MACRS for property you ac-

quired and placed in service after 1986 if any of the situa-

tions described below apply. If you cannot use MACRS,

the property must be depreciated under the methods dis-

cussed in Pub. 534.

For the following discussions, do not treat prop-

erty as owned before you placed it in service. If

you owned property in 1986 but did not place it in

service until 1987, you do not treat it as owned in 1986.

Personal property. You cannot use MACRS for per-

sonal property (section 1245 property) in any of the follow-

ing situations.

1. You or someone related to you owned or used the

property in 1986.

2. You acquired the property from a person who owned

it in 1986 and as part of the transaction the user of the

property did not change.

CAUTION

!

Page 8 Chapter 1 Overview of Depreciation

Page 9 of 115 Fileid: … tions/P946/2017/A/XML/Cycle03/source 15:20 - 28-Feb-2018

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

3. You lease the property to a person (or someone rela-

ted to this person) who owned or used the property in

1986.

4. You acquired the property in a transaction in which:

a. The user of the property did not change, and

b. The property was not MACRS property in the

hands of the person from whom you acquired it

because of (2) or (3) above.

Real property. You generally cannot use MACRS for

real property (section 1250 property) in any of the follow-

ing situations.

You or someone related to you owned the property in

1986.

You lease the property to a person who owned the

property in 1986 (or someone related to that person).

You acquired the property in a like-kind exchange, in-

voluntary conversion, or repossession of property you

or someone related to you owned in 1986. MACRS

applies only to that part of your basis in the acquired

property that represents cash paid or unlike property

given up. It does not apply to the carried-over part of

the basis.

Exceptions. The rules above do not apply to the follow-

ing.

1. Residential rental property or nonresidential real prop-

erty.

2. Any property if, in the first tax year it is placed in serv-

ice, the deduction under the Accelerated Cost Recov-

ery System (ACRS) is more than the deduction under

MACRS using the half-year convention. For informa-

tion on how to figure depreciation under ACRS, see

Pub. 534.

3. Property that was MACRS property in the hands of

the person from whom you acquired it because of (2)

above.

Related persons. For this purpose, the following are re-

lated persons.

1. An individual and a member of his or her family, in-

cluding only a spouse, child, parent, brother, sister,

half-brother, half-sister, ancestor, and lineal descend-

ant.

2. A corporation and an individual who directly or indi-

rectly owns more than 10% of the value of the out-

standing stock of that corporation.

3. Two corporations that are members of the same con-

trolled group.

4. A trust fiduciary and a corporation if more than 10% of

the value of the outstanding stock is directly or indi-

rectly owned by or for the trust or grantor of the trust.

5. The grantor and fiduciary, and the fiduciary and bene-

ficiary, of any trust.

6. The fiduciaries of two different trusts, and the fiducia-

ries and beneficiaries of two different trusts, if the

same person is the grantor of both trusts.

7. A tax-exempt educational or charitable organization

and any person (or, if that person is an individual, a

member of that person's family) who directly or indi-

rectly controls the organization.

8. Two S corporations, and an S corporation and a regu-

lar corporation, if the same persons own more than

10% of the value of the outstanding stock of each cor-

poration.

9. A corporation and a partnership if the same persons

own both of the following.

a. More than 10% of the value of the outstanding

stock of the corporation.

b. More than 10% of the capital or profits interest in

the partnership.

10.

The executor and beneficiary of any estate.

11.

A partnership and a person who directly or indirectly

owns more than 10% of the capital or profits interest

in the partnership.

12.

Two partnerships, if the same persons directly or indi-

rectly own more than 10% of the capital or profits in-

terest in each.

13.

The related person and a person who is engaged in

trades or businesses under common control. See

section 52(a) and 52(b) of the Internal Revenue Code.

When to determine relationship. You must deter-

mine whether you are related to another person at the

time you acquire the property.

A partnership acquiring property from a terminating

partnership must determine whether it is related to the ter-

minating partnership immediately before the event caus-

ing the termination. For this rule, a terminating partnership

is one that sells or exchanges, within 12 months, 50% or

more of its total interest in partnership capital or profits.

Constructive ownership of stock or partnership in-

terest. To determine whether a person directly or indi-

rectly owns any of the outstanding stock of a corporation

or an interest in a partnership, apply the following rules.

1. Stock or a partnership interest directly or indirectly

owned by or for a corporation, partnership, estate, or

trust is considered owned proportionately by or for its

shareholders, partners, or beneficiaries. However, for

a partnership interest owned by or for a C corporation,

this applies only to shareholders who directly or indi-

rectly own 5% or more of the value of the stock of the

corporation.

2. An individual is considered to own the stock or part-

nership interest directly or indirectly owned by or for

the individual's family.

3. An individual who owns, except by applying rule (2),

any stock in a corporation is considered to own the

Chapter 1 Overview of Depreciation Page 9

Page 10 of 115 Fileid: … tions/P946/2017/A/XML/Cycle03/source 15:20 - 28-Feb-2018

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

stock directly or indirectly owned by or for the individ-

ual's partner.

4. For purposes of rule (1), (2), or (3), stock or a partner-

ship interest considered to be owned by a person un-

der rule (1) is treated as actually owned by that per-

son. However, stock or a partnership interest

considered to be owned by an individual under rule

(2) or (3) is not treated as owned by that individual for

reapplying either rule (2) or (3) to make another per-

son considered to be the owner of the same stock or

partnership interest.

Intangible Property

Generally, if you can depreciate intangible property, you

usually use the straight line method of depreciation. How-

ever, you can choose to depreciate certain intangible

property under the income forecast method (discussed

later).

You cannot depreciate intangible property that is

a section 197 intangible or that otherwise does

not meet all the requirements discussed earlier

under What Property Can Be Depreciated.

Straight Line Method

This method lets you deduct the same amount of depreci-

ation each year over the useful life of the property. To fig-

ure your deduction, first determine the adjusted basis, sal-

vage value, and estimated useful life of your property.

Subtract the salvage value, if any, from the adjusted ba-

sis. The balance is the total depreciation you can take

over the useful life of the property.

Divide the balance by the number of years in the useful

life. This gives you your yearly depreciation deduction.

Unless there is a big change in adjusted basis or useful

life, this amount will stay the same throughout the time

you depreciate the property. If, in the first year, you use

the property for less than a full year, you must prorate your

depreciation deduction for the number of months in use.

Example. In April, Frank bought a patent for $5,100

that is not a section 197 intangible. He depreciates the

patent under the straight line method, using a 17-year

useful life and no salvage value. He divides the $5,100

basis by 17 years to get his $300 yearly depreciation de-

duction. He only used the patent for 9 months during the

first year, so he multiplies $300 by 912 to get his deduction

of $225 for the first year. Next year, Frank can deduct

$300 for the full year.

Patents and copyrights. If you can depreciate the cost

of a patent or copyright, use the straight line method over

the useful life. The useful life of a patent or copyright is the

lesser of the life granted to it by the government or the re-

maining life when you acquire it. However, if the patent or

copyright becomes valueless before the end of its useful

life, you can deduct in that year any of its remaining cost

or other basis.

CAUTION

!

Computer software. Computer software is generally a

section 197 intangible and cannot be depreciated if you

acquired it in connection with the acquisition of assets

constituting a business or a substantial part of a business.

However, computer software is not a section 197 intan-

gible and can be depreciated, even if acquired in connec-

tion with the acquisition of a business, if it meets all of the

following tests.

It is readily available for purchase by the general pub-

lic.

It is subject to a nonexclusive license.

It has not been substantially modified.

If the software meets the tests above, it may also qual-

ify for the section 179 deduction and the special deprecia-

tion allowance, discussed later. If you can depreciate the

cost of computer software, use the straight line method

over a useful life of 36 months.

Tax-exempt use property subject to a lease. The

useful life of computer software leased under a lease

agreement entered into after March 12, 2004, to a tax-ex-

empt organization, governmental unit, or foreign person or

entity (other than a partnership), cannot be less than

125% of the lease term.

Certain created intangibles. You can amortize certain

intangibles created on or after December 31, 2003, over a

15-year period using the straight line method and no sal-

vage value, even though they have a useful life that can-

not be estimated with reasonable accuracy. For example,

amounts paid to acquire memberships or privileges of in-

definite duration, such as a trade association member-

ship, are eligible costs.

The following are not eligible.

Any intangible asset acquired from another person.

Created financial interests.

Any intangible asset that has a useful life that can be

estimated with reasonable accuracy.

Any intangible asset that has an amortization period or

limited useful life that is specifically prescribed or pro-

hibited by the Code, regulations, or other published

IRS guidance.

Any amount paid to facilitate an acquisition of a trade

or business, a change in the capital structure of a

business entity, and certain other transactions.

You also must increase the 15-year safe harbor amorti-

zation period to a 25-year period for certain intangibles re-

lated to benefits arising from the provision, production, or

improvement of real property. For this purpose, real prop-

erty includes property that will remain attached to the real

property for an indefinite period of time, such as roads,

bridges, tunnels, pavements, and pollution control facili-

ties.

Page 10 Chapter 1 Overview of Depreciation

Page 11 of 115 Fileid: … tions/P946/2017/A/XML/Cycle03/source 15:20 - 28-Feb-2018

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Income Forecast Method

You can choose to use the income forecast method in-

stead of the straight line method to depreciate the

following depreciable intangibles.

Motion picture films or video tapes.

Sound recordings.

Copyrights.

Books.

Patents.

Under the income forecast method, each year's depre-

ciation deduction is equal to the cost of the property, mul-

tiplied by a fraction. The numerator of the fraction is the

current year's net income from the property, and the de-

nominator is the total income anticipated from the property

through the end of the 10th taxable year following the tax-

able year the property is placed in service. For more infor-

mation, see section 167(g) of the Internal Revenue Code.

Films, video tapes, and recordings. You cannot use

MACRS for motion picture films, video tapes, and sound

recordings. For this purpose, sound recordings are discs,

tapes, or other phonorecordings resulting from the fixation

of a series of sounds. You can depreciate this property us-

ing either the straight line method or the income forecast

method.

Participations and residuals. You can include partici-

pations and residuals in the adjusted basis of the property

for purposes of computing your depreciation deduction

under the income forecast method. The participations and

residuals must relate to income to be derived from the

property before the end of the 10th taxable year after the

property is placed in service. For this purpose, participa-

tions and residuals are defined as costs which by contract

vary with the amount of income earned in connection with

the property.

Instead of including these amounts in the adjusted ba-

sis of the property, you can deduct the costs in the taxable

year that they are paid.

Videocassettes. If you are in the business of renting

videocassettes, you can depreciate only those videocas-

settes bought for rental. If the videocassette has a useful

life of one year or less, you can currently deduct the cost

as a business expense.

Corporate or Partnership Property

Acquired in a Nontaxable Transfer

MACRS does not apply to property used before 1987 and

transferred after 1986 to a corporation or partnership (ex-

cept property the transferor placed in service after July 31,

1986, if MACRS was elected) to the extent its basis is car-

ried over from the property's adjusted basis in the trans-

feror's hands. You must continue to use the same depre-

ciation method as the transferor and figure depreciation

as if the transfer had not occurred. However, if MACRS

would otherwise apply, you can use it to depreciate the

part of the property's basis that exceeds the carried-over

basis.

The nontaxable transfers covered by this rule include

the following.

A distribution in complete liquidation of a subsidiary.

A transfer to a corporation controlled by the transferor.

An exchange of property solely for corporate stock or

securities in a reorganization.

A contribution of property to a partnership in exchange

for a partnership interest.

A partnership distribution of property to a partner.

Election To Exclude Property

From MACRS

If you can properly depreciate any property under a

method not based on a term of years, such as the

unit-of-production method, you can elect to exclude that

property from MACRS. You make the election by report-

ing your depreciation for the property on line 15 in Part II

of Form 4562 and attaching a statement as described in

the Instructions for Form 4562. You must make this elec-

tion by the return due date (including extensions) for the

tax year you place your property in service. However, if

you timely filed your return for the year without making the

election, you can still make the election by filing an amen-

ded return within six months of the due date of the return

(excluding extensions). Attach the election to the amen-

ded return and write “Filed pursuant to section

301.9100-2” on the election statement. File the amended

return at the same address you filed the original return.

Use of standard mileage rate. If you use the standard

mileage rate to figure your tax deduction for your business

automobile, you are treated as having made an election to

exclude the automobile from MACRS. See Pub. 463 for a

discussion of the standard mileage rate.

What Is the Basis of Your

Depreciable Property?

Terms you may need to know

(see Glossary):

Abstract fees

Adjusted basis

Basis

Exchange

Fair market value

To figure your depreciation deduction, you must deter-

mine the basis of your property. To determine basis, you

need to know the cost or other basis of your property.

Chapter 1 Overview of Depreciation Page 11

Page 12 of 115 Fileid: … tions/P946/2017/A/XML/Cycle03/source 15:20 - 28-Feb-2018

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Cost as Basis

The basis of property you buy is its cost plus amounts you

paid for items such as sales tax (see Exception below),

freight charges, and installation and testing fees. The cost

includes the amount you pay in cash, debt obligations,

other property, or services.

Exception. You can elect to deduct state and local

general sales taxes instead of state and local income

taxes as an itemized deduction on Schedule A (Form

1040). If you make that choice, you cannot include those

sales taxes as part of your cost basis.

Assumed debt. If you buy property and assume (or buy

subject to) an existing mortgage or other debt on the prop-

erty, your basis includes the amount you pay for the prop-

erty plus the amount of the assumed debt.

Example. You make a $20,000 down payment on

property and assume the seller's mortgage of $120,000.

Your total cost is $140,000, the cash you paid plus the

mortgage you assumed.

Settlement costs. The basis of real property also in-

cludes certain fees and charges you pay in addition to the

purchase price. These generally are shown on your settle-

ment statement and include the following.

Legal and recording fees.

Abstract fees.

Survey charges.

Owner's title insurance.

Amounts the seller owes that you agree to pay, such

as back taxes or interest, recording or mortgage fees,

charges for improvements or repairs, and sales com-

missions.

For fees and charges you cannot include in the basis of

property, see Real Property in Pub. 551.

Property you construct or build. If you construct, build,

or otherwise produce property for use in your business,

you may have to use the uniform capitalization rules to de-

termine the basis of your property. For information about

the uniform capitalization rules, see Pub. 551 and the reg-

ulations under section 263A of the Internal Revenue

Code.

Other Basis

Other basis usually refers to basis that is determined by

the way you received the property. For example, your ba-

sis is other than cost if you acquired the property in ex-

change for other property, as payment for services you

performed, as a gift, or as an inheritance. If you acquired

property in this or some other way, see Pub. 551 to deter-

mine your basis.

Property changed from personal use. If you held prop-

erty for personal use and later use it in your business or

income-producing activity, your depreciable basis is the

lesser of the following.

1. The fair market value (FMV) of the property on the

date of the change in use.

2. Your original cost or other basis adjusted as follows.

a. Increased by the cost of any permanent improve-

ments or additions and other costs that must be

added to basis.

b. Decreased by any deductions you claimed for

casualty and theft losses and other items that re-

duced your basis.

Example. Several years ago, Nia paid $160,000 to

have her home built on a lot that cost her $25,000. Before

changing the property to rental use last year, she paid

$20,000 for permanent improvements to the house and

claimed a $2,000 casualty loss deduction for damage to

the house. Land is not depreciable, so she includes only

the cost of the house when figuring the basis for deprecia-

tion.

Nia's adjusted basis in the house when she changed its

use was $178,000 ($160,000 + $20,000 − $2,000). On the

same date, her property had an FMV of $180,000, of

which $15,000 was for the land and $165,000 was for the

house. The basis for depreciation on the house is the

FMV on the date of change ($165,000), because it is less

than her adjusted basis ($178,000).

Property acquired in a nontaxable transaction. Gen-

erally, if you receive property in a nontaxable exchange,

the basis of the property you receive is the same as the

adjusted basis of the property you gave up. Special rules

apply in determining the basis and figuring the MACRS

depreciation deduction and special depreciation allow-

ance for property acquired in a like-kind exchange or in-

voluntary conversion. See Like-kind exchanges and invol-

untary conversions under How Much Can You Deduct in

chapter 3, and Figuring the Deduction for Property Ac-

quired in a Nontaxable Exchange in chapter 4.

There are also special rules for determining the basis of

MACRS property involved in a like-kind exchange or invol-

untary conversion when the property is contained in a

general asset account. See How Do You Use General As-

set Accounts in chapter 4.

Adjusted Basis

To find your property's basis for depreciation, you may

have to make certain adjustments (increases and decrea-

ses) to the basis of the property for events occurring be-

tween the time you acquired the property and the time you

placed it in service. These events could include the follow-

ing.

Installing utility lines.

Paying legal fees for perfecting the title.

Settling zoning issues.

Receiving rebates.

Page 12 Chapter 1 Overview of Depreciation

Page 13 of 115 Fileid: … tions/P946/2017/A/XML/Cycle03/source 15:20 - 28-Feb-2018

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Incurring a casualty or theft loss.

For a discussion of adjustments to the basis of your prop-

erty, see Adjusted Basis in Pub. 551.

If you depreciate your property under MACRS, you also

may have to reduce your basis by certain deductions and

credits with respect to the property. For more information,

see What Is the Basis for Depreciation in chapter 4.

Basis adjustment for depreciation allowed or allowa-

ble. You must reduce the basis of property by the depre-

ciation allowed or allowable, whichever is greater. Depre-

ciation allowed is depreciation you actually deducted

(from which you received a tax benefit). Depreciation al-

lowable is depreciation you are entitled to deduct.

If you do not claim depreciation you are entitled to de-

duct, you must still reduce the basis of the property by the

full amount of depreciation allowable.

If you deduct more depreciation than you should, you

must reduce your basis by any amount deducted from

which you received a tax benefit (the depreciation al-

lowed).

How Do You Treat Repairs and

Improvements?

If you improve depreciable property, you must treat the

improvement as separate depreciable property. Improve-

ment means an addition to or partial replacement of prop-

erty that is a betterment to the property, restores the prop-

erty, or adapts it to a new or different use. See section

1.263(a)-3 of the regulations.

You generally deduct the cost of repairing business

property in the same way as any other business expense.

However, if the cost is for a betterment to the property, to

restore the property, or to adapt the property to a new or

different use, you must treat it as an improvement and de-

preciate it.

Example. You repair a small section on one corner of

the roof of a rental house. You deduct the cost of the re-

pair as a rental expense. However, if you completely re-

place the roof, the new roof is an improvement because it

is a restoration of the building. You depreciate the cost of

the new roof.

Improvements to rented property. You can depreciate

permanent improvements you make to business property

you rent from someone else.

Do You Have To File

Form 4562?

Terms you may need to know

(see Glossary):

Amortization

Listed property

Placed in service

Standard mileage rate

Use Form 4562 to figure your deduction for depreciation

and amortization. Attach Form 4562 to your tax return for

the current tax year if you are claiming any of the following

items.

A section 179 deduction for the current year or a sec-

tion 179 carryover from a prior year. See chapter 2 for

information on the section 179 deduction.

Depreciation for property placed in service during the

current year.

Depreciation on any vehicle or other listed property,

regardless of when it was placed in service. See

chapter 5 for information on listed property.

A deduction for any vehicle if the deduction is reported

on a form other than Schedule C (Form 1040) or

Schedule C-EZ (Form 1040).

Amortization of costs if the current year is the first year

of the amortization period.

Depreciation or amortization on any asset on a corpo-

rate income tax return (other than Form 1120S, U.S.

Income Tax Return for an S Corporation) regardless

of when it was placed in service.

You must submit a separate Form 4562 for each

business or activity on your return for which a

Form 4562 is required.

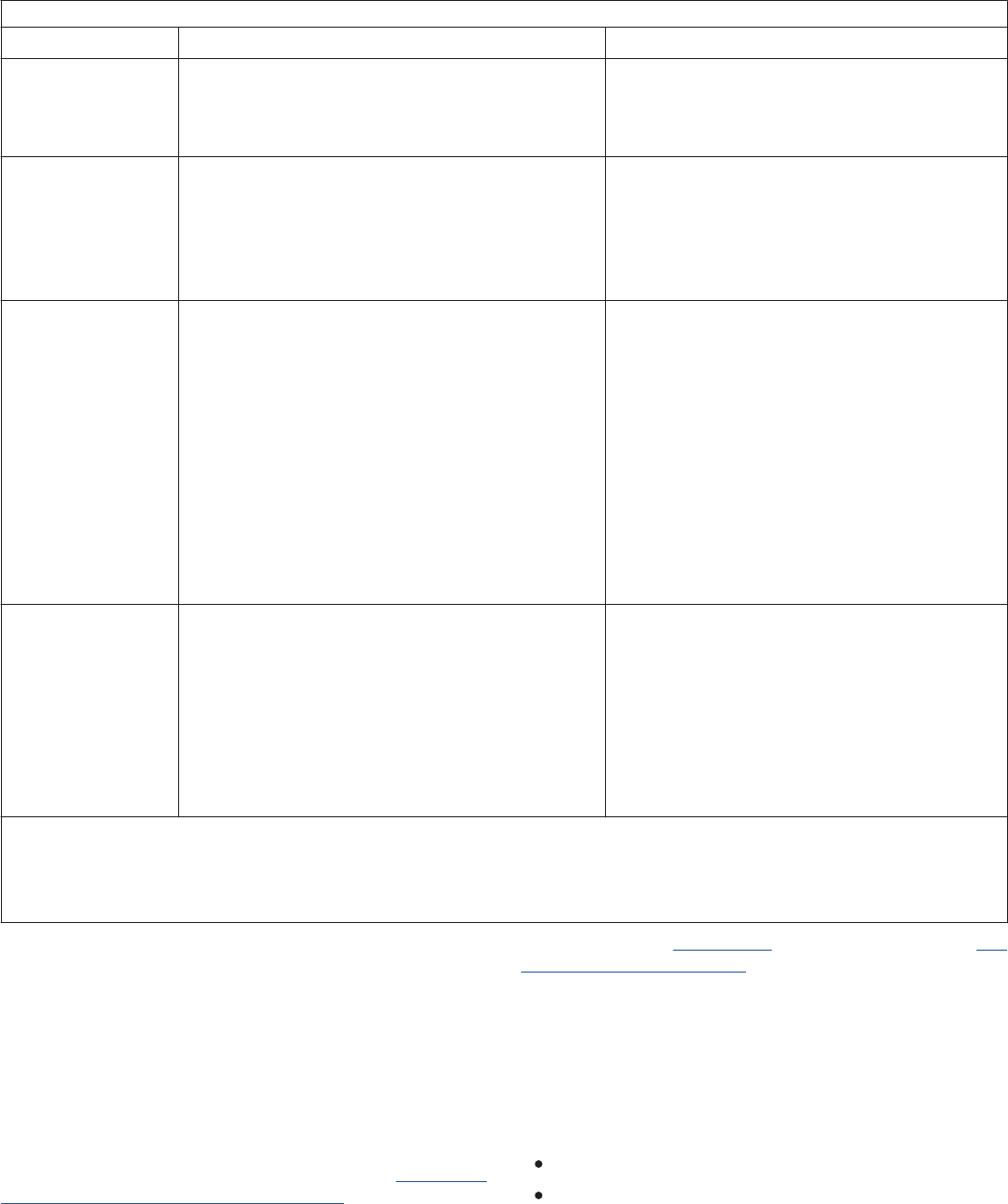

Table 1-1 presents an overview of the purpose of the

various parts of Form 4562.

Employee. Do not use Form 4562 if you are an em-

ployee and you deduct job-related vehicle expenses using

either actual expenses (including depreciation) or the

standard mileage rate. Instead, use either Form 2106 or

Form 2106-EZ. Use Form 2106-EZ if you are claiming the

standard mileage rate and you are not reimbursed by your

employer for any expenses.

How Do You Correct

Depreciation Deductions?

If you deducted an incorrect amount of depreciation in any

year, you may be able to make a correction by filing an

amended return for that year. See Filing an Amended Re-

turn, next. If you are not allowed to make the correction on

an amended return, you may be able to change your ac-

counting method to claim the correct amount of deprecia-

tion. See Changing Your Accounting Method, later.

CAUTION

!

Chapter 1 Overview of Depreciation Page 13

Page 14 of 115 Fileid: … tions/P946/2017/A/XML/Cycle03/source 15:20 - 28-Feb-2018

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Filing an Amended Return

You can file an amended return to correct the amount of

depreciation claimed for any property in any of the follow-

ing situations.

You claimed the incorrect amount because of a math-

ematical error made in any year.

You claimed the incorrect amount because of a post-

ing error made in any year.

You have not adopted a method of accounting for

property placed in service by you in tax years ending

after December 29, 2003.

You claimed the incorrect amount on property placed

in service by you in tax years ending before December

30, 2003.

Adoption of accounting method defined. Generally,

you adopt a method of accounting for depreciation by us-

ing a permissible method of determining depreciation

when you file your first tax return, or by using the same im-

permissible method of determining depreciation in two or

more consecutively filed tax returns.

For an exception to the 2-year rule, see Revenue Pro-

cedure 2017-30 on page 1139 of Internal Revenue Bulle-

tin 2017-18, available at www.irs.gov/irb/2017-18_IRB.

When to file. If an amended return is allowed, you must

file it by the later of the following.

3 years from the date you filed your original return for

the year in which you did not deduct the correct

amount. A return filed before an unextended due date

is considered filed on that due date.

2 years from the time you paid your tax for that year.

Changing Your Accounting Method

Generally, you must get IRS approval to change your

method of accounting. You generally must file Form 3115,

Application for Change in Accounting Method, to request

a change in your method of accounting for depreciation.

The following are examples of a change in method of

accounting for depreciation.

A change from an impermissible method of determin-

ing depreciation for depreciable property, if the imper-

missible method was used in two or more consecu-

tively filed tax returns.

A change in the treatment of an asset from nondepre-

ciable to depreciable or vice versa.

A change in the depreciation method, period of recov-

ery, or convention of a depreciable asset.

A change from not claiming to claiming the special de-

preciation allowance if you did not make the election

to not claim any special allowance.

A change from claiming a 50% special depreciation al-

lowance to claiming a 30% special depreciation allow-

ance for qualified property (including property that is

included in a class of property for which you elected a

30% special allowance instead of a 50% special al-

lowance).

Changes in depreciation that are not a change in

method of accounting (and may only be made on an

amended return) include the following.

An adjustment in the useful life of a depreciable asset

for which depreciation is determined under section

167.

A change in use of an asset in the hands of the same

taxpayer.

Making a late depreciation election or revoking a

timely valid depreciation election (including the elec-

tion not to deduct the special depreciation allowance).

If you elected not to claim any special depreciation al-

lowance, a change from not claiming to claiming the

special depreciation allowance is a revocation of the

election and is not an accounting method change.

Generally, you must get IRS approval to make a late

depreciation election or revoke a depreciation elec-

tion. You must submit a request for a letter ruling to

make a late election or revoke an election.

Any change in the placed in service date of a depreci-

able asset.

See section 1.446-1(e)(2)(ii)(d) of the regulations for

more information and examples.

IRS approval. If your change in method of accounting for

depreciation is described in Revenue Procedure 2017-30,

you may be able to get approval from the IRS to make that

change under the automatic change request procedures

generally covered in Revenue Procedure 2015-13 on

page 419 of Internal Revenue Bulletin 2015-5. If you do

not qualify to use the automatic procedures to get appro-

val, you must use the advance consent request proce-

dures generally covered in Revenue Procedure 2015-13.

Also see the Instructions for Form 3115 for more informa-

tion on getting approval, including lists of scope limitations

and automatic accounting method changes.

Additional guidance. For additional guidance and

special procedures for changing your accounting method,

automatic change procedures, amending your return, and

filing Form 3115, see Revenue Procedure 2015-13 on

page 419 of Internal Revenue Bulletin 2015-5 and Reve-

nue Procedure 2017-30 on page 1131 of Internal Reve-

nue Bulletin 2017-18, available at www.irs.gov/irb/

2017-18_IRB.

Section 481(a) adjustment. If you file Form 3115 and

change from an impermissible method to a permissible

method of accounting for depreciation, you can make a

section 481(a) adjustment for any unclaimed or excess

amount of allowable depreciation. The adjustment is the

difference between the total depreciation actually deduc-

ted for the property and the total amount allowable prior to

the year of change. If no depreciation was deducted, the

adjustment is the total depreciation allowable prior to the

year of change. A negative section 481(a) adjustment

Page 14 Chapter 1 Overview of Depreciation

Page 15 of 115 Fileid: … tions/P946/2017/A/XML/Cycle03/source 15:20 - 28-Feb-2018

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

results in a decrease in taxable income. It is taken into ac-

count in the year of change and is reported on your busi-

ness tax returns as “other expenses.” A positive section

481(a) adjustment results in an increase in taxable in-

come. It is generally taken into account over 4 tax years

and is reported on your business tax returns as “other in-

come.” However, you can elect to use a one-year adjust-

ment period and report the adjustment in the year of

change if the total adjustment is less than $50,000. Make

the election by completing the appropriate line on

Form 3115.

If you file a Form 3115 and change from one permissi-

ble method to another permissible method, the section

481(a) adjustment is zero.

2.

Electing the Section 179

Deduction

Introduction

You can elect to recover all or part of the cost of certain

qualifying property, up to a limit, by deducting it in the year

you place the property in service. This is the section 179

deduction. You can elect the section 179 deduction in-

stead of recovering the cost by taking depreciation deduc-

tions.

Estates and trusts cannot elect the section 179

deduction.

This chapter explains what property does and does not

qualify for the section 179 deduction, what limits apply to

the deduction (including special rules for partnerships and

corporations), and how to elect it. It also explains when

and how to recapture the deduction.

Useful Items

You may want to see:

Publication

Installment Sales

Sales and Other Dispositions of Assets

Tax Incentives for Distressed Communities

Form (and Instructions)

Depreciation and Amortization

Sales of Business Property

See chapter 6 for information about getting publications

and forms.

What Property Qualifies?

Terms you may need to know

(see Glossary):

Adjusted basis

Basis

Class life

CAUTION

!

537

544

954

4562

4797

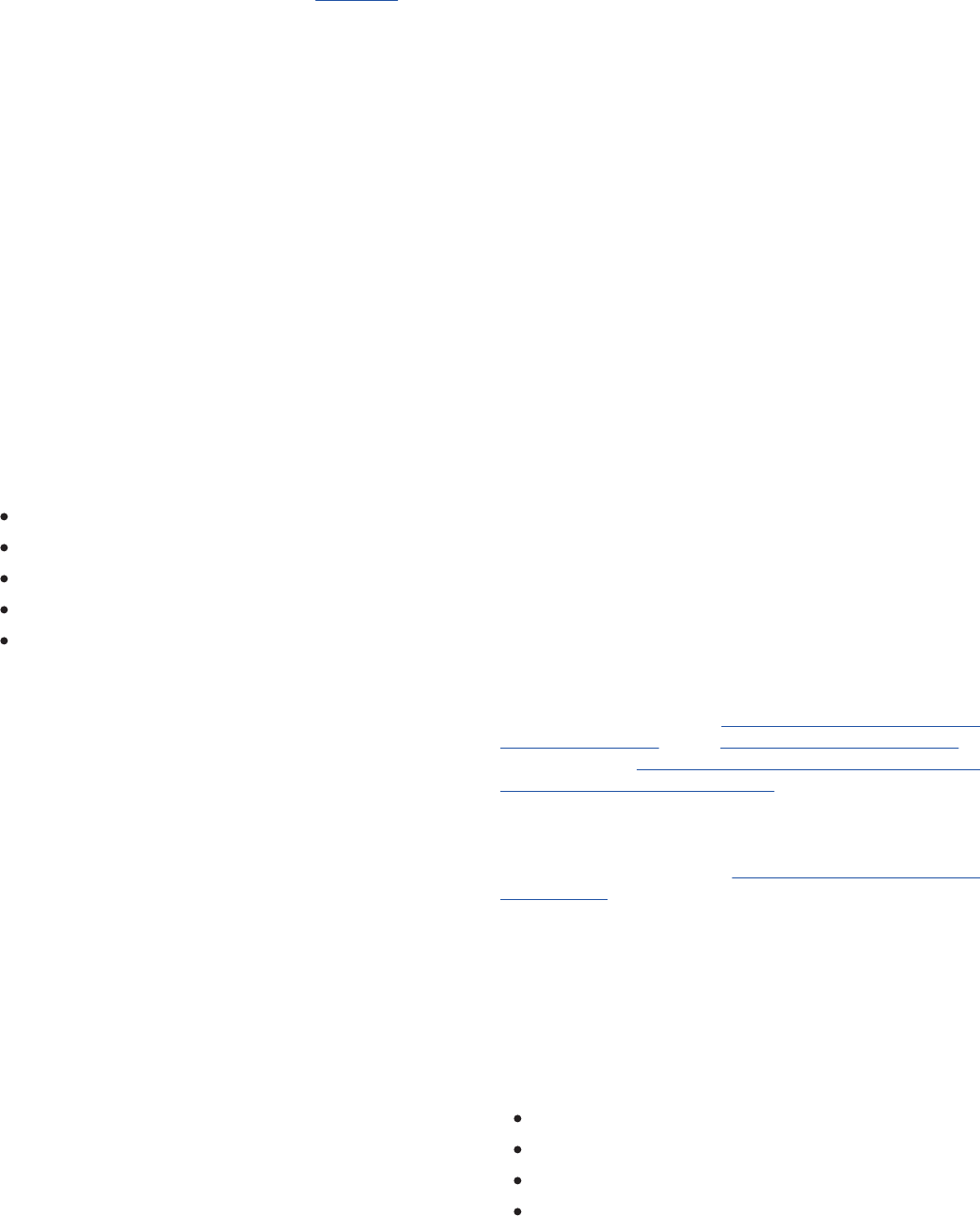

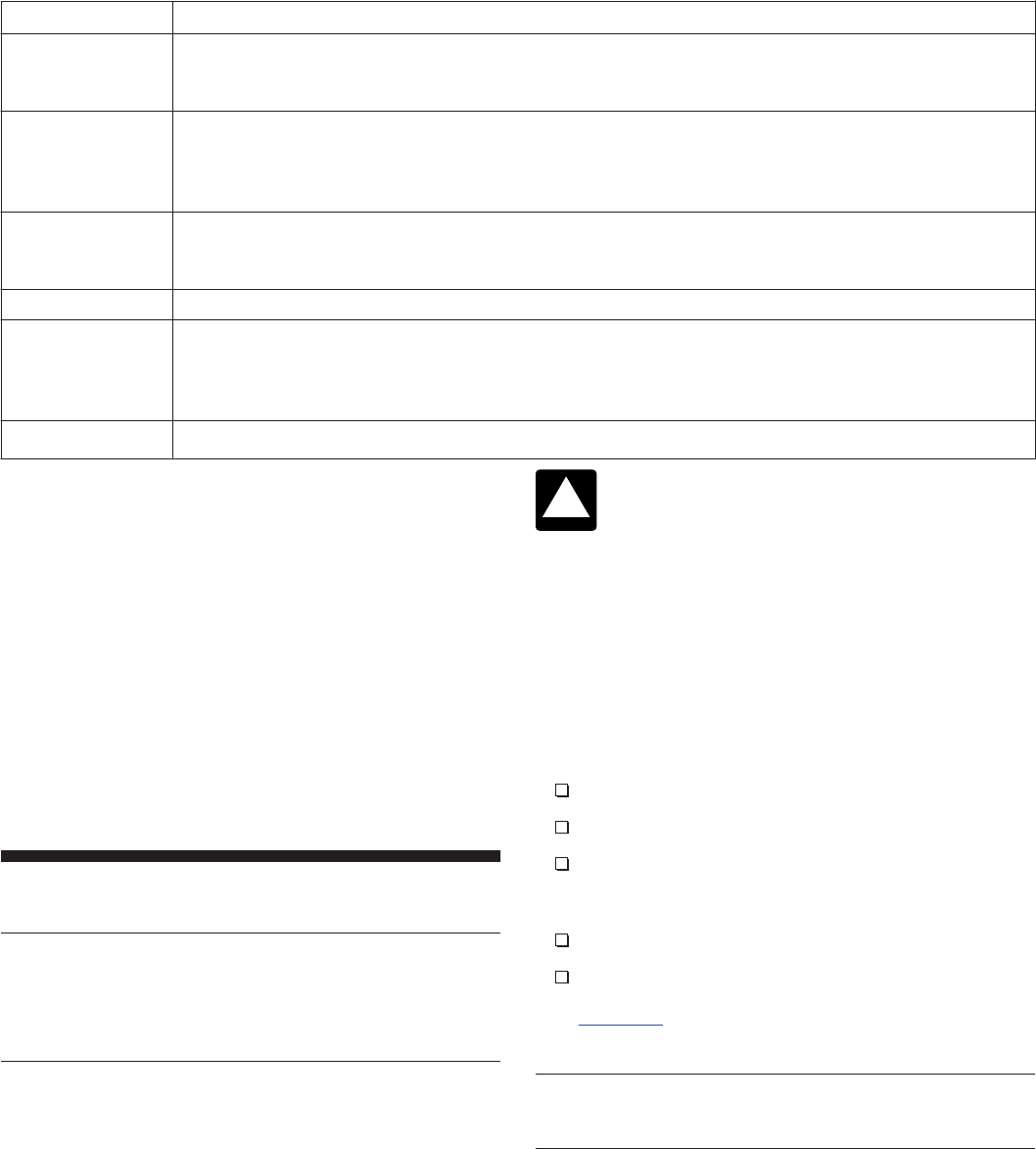

Purpose of Form 4562

This table describes the purpose of the various parts of Form 4562. For more information, see Form 4562

and its instructions.

Part Purpose

I • Electing the section 179 deduction

• Figuring the maximum section 179 deduction for the current year

• Figuring any section 179 deduction carryover to the next year

II • Reporting the special depreciation allowance for property (other than listed property) placed in

service during the tax year

• Reporting depreciation deductions on property being depreciated under any method other than

Modified Accelerated Cost Recovery System (MACRS)

III • Reporting MACRS depreciation deductions for property placed in service before this year

• Reporting MACRS depreciation deductions for property (other than listed property) placed in

service during the current year

IV • Summarizing other parts