W166 Wisconsin Employers Withholding Tax Guide December 2017 WDR 1040 W Pb166

User Manual: WDR 1040 W

Open the PDF directly: View PDF ![]() .

.

Page Count: 48

- W-166 only tables.pdf

- I. FEDERAL EMPLOYER’S TAX GUIDE

- II. REGISTRATION AND GENERAL WITHHOLDING TAX PROVISIONS

- A. Application Process

- B. Wisconsin Withholding Tax Number

- C. Filing Frequency

- D. Reactivate Withholding Account

- E. Change In Business Entity

- F. Employee’s Withholding Exemption Certificate

- G. Special Situations Regarding Form WT4 And Form WT4A

- H. Employees Claiming Exemption From Withholding (Forms W-4 and WT-4)

- I. Withholding Calculator.

- J. New Hire Reporting Requirements

- K. Wages Paid To Residents Who Work Outside Wisconsin

- L. Special Minnesota Withholding Arrangement

- M. Out-of-State Disaster Relief Responders

- N. Wages Paid To Nonresidents Who Work In Wisconsin

- O. Nonresident Employers

- P. Withholding On Nonresident Entertainers

- Q. Withholding For Noncash Fringe Benefits

- R. Health Savings Accounts

- S. Third Party Sick Pay

- T. Pensions

- U. Reporting Of Wages For Agricultural, Domestic, Or Other Employees Exempt From Withholding

- V. Willful Misclassification Penalty for Construction Contractors

- W. Payments Made To Decedent Estate Or Beneficiary

- III. DEPOSITING WITHHELD TAXES

- A. Reporting Requirements

- B. Deposit Report (WT6) Filing Options

- C. Reporting Periods

- D. Reporting Changes To Wisconsin Employer Account Information

- E. Filing Due Dates

- F. Extensions

- G. Failure To File Or Pay By The Due Date

- H. Failure To Report Amount Of Taxes Withheld

- I. Refund/Credit For Overpayment(s)

- J. Other

- IV. RECONCILIATION PROCESS

- V. OTHER TAXES TO BE AWARE OF

- VI. KEEPING AWARE OF CHANGES IN WISCONSIN TAX LAWS

State of Wisconsin

Department of Revenue

Wisconsin

Withholding Tax Guide

Effective for Withholding Periods

Beginning On or After April 1, 2014

Publication W-166 (12/17)

Printed on

Recycled Paper

2

TABLE OF CONTENTS Page

I. FEDERAL EMPLOYER’S TAX GUIDE .................................................................................................................... 4

II. REGISTRATION AND GENERAL WITHHOLDING TAX PROVISIONS ........................................................... 4

A. Application Process ................................................................................................................................................... 4

B. Wisconsin Withholding Tax Number ........................................................................................................................ 4

C. Filing Frequency ........................................................................................................................................................ 5

D. Reactivate Withholding Account ............................................................................................................................... 5

E. Change In Business Entity ......................................................................................................................................... 5

F. Employee’s Withholding Exemption Certificate ....................................................................................................... 5

G. Special Situations Regarding Form WT-4 And Form WT-4A .................................................................................. 5

H. Employees Claiming Exemption From Withholding (Forms W-4 and WT-4) .......................................................... 6

I. Withholding Calculator.............................................................................................................................................. 7

J. New Hire Reporting Requirements ............................................................................................................................ 7

K. Wages Paid To Residents Who Work Outside Wisconsin ......................................................................................... 7

L. Special Minnesota Withholding Arrangement ........................................................................................................... 7

M. Out-of-State Disaster Relief Responders. .................................................................................................................. 7

N. Wages Paid To Nonresidents Who Work In Wisconsin ............................................................................................ 8

O. Nonresident Employers.............................................................................................................................................. 8

P. Withholding On Nonresident Entertainers ................................................................................................................. 8

Q. Withholding For Noncash Fringe Benefits ................................................................................................................ 9

R. Health Savings Accounts ........................................................................................................................................... 9

S. Third Party Sick Pay ................................................................................................................................................ 10

T. Pensions ................................................................................................................................................................... 10

U. Reporting Of Wages For Agricultural, Domestic, Or Other Employees Exempt From Withholding ..................... 10

V. Willful Misclassification Penalty for Construction Contractors .............................................................................. 10

W. Payments Made To Decedent Estate Or Beneficiary ............................................................................................... 10

III. DEPOSITING WITHHELD TAXES .......................................................................................................................... 11

A. Reporting Requirements .......................................................................................................................................... 11

B. Deposit Report (WT-6) Filing Options .................................................................................................................... 11

C. Reporting Periods .................................................................................................................................................... 11

D. Reporting Changes To Wisconsin Employer Account Information ........................................................................ 12

E. Filing Due Dates ...................................................................................................................................................... 12

F. Extensions ................................................................................................................................................................ 13

G. Failure To File Or Pay By The Due Date ................................................................................................................ 13

H. Failure To Report Amount Of Taxes Withheld ....................................................................................................... 13

I. Refund/Credit For Overpayment(s) ......................................................................................................................... 14

J. Other ........................................................................................................................................................................ 14

IV. RECONCILIATION PROCESS ................................................................................................................................. 14

A. Preparing Employee W-2......................................................................................................................................... 14

B. Furnishing Employees With Wage And Tax Statements ......................................................................................... 14

C. Annual Reconciliation (WT-7) Filing Options ........................................................................................................ 15

D. Wage and Information Return Requirements .......................................................................................................... 16

E. Filing Wage and Information Returns ..................................................................................................................... 16

F. Extensions ................................................................................................................................................................ 17

G. Discontinuing Withholding ...................................................................................................................................... 17

H. Wisconsin Information Return Form 9b .................................................................................................................. 17

V. OTHER TAXES TO BE AWARE OF ........................................................................................................................ 18

VI. KEEPING AWARE OF CHANGES IN WISCONSIN TAX LAWS ....................................................................... 19

WISCONSIN INCOME TAX WITHHOLDING TABLES AND METHODS .................................................................. 20

Introduction .................................................................................................................................................................... 20

Supplemental Wage Payments ........................................................................................................................................ 20

Daily and Miscellaneous ................................................................................................................................................. 21

Weekly ............................................................................................................................................................................ 23

Biweekly ......................................................................................................................................................................... 29

Semi-Monthly ................................................................................................................................................................. 35

Monthly .......................................................................................................................................................................... 41

Alternate Methods of Withholding Wisconsin Income Tax ........................................................................................... 47

3

TABLE OF WISCONSIN WITHHOLDING FORMS AND FEDERAL COUNTERPART

IMPORTANT NEWS

No changes in withholding rates for 2018. The current withholding tax rates remain in effect.

2017 Wisconsin Act 59 made several changes to W-2 and information return reporting requirements. Beginning with

payments made in 2017:

• Required e-file of W-2s and information returns. An employer or payer required to file 10 or more W-2s or 10 or

more of any one type of information return with the department must file such returns electronically. The prior thresh-

old was 50 or more.

• All W-2s and information returns required to be filed with the department are due January 31. The prior due

dates for statements of nonwage payments and rent and royalties with the department were February 28 and March 15.

• A 30-day extension is available for filing these returns. Under prior law, a 60-day extension period was available for

rent and royalty statements and nonwage statements.

• The department may not issue a refund to an employed individual before March 1, unless the individual and indi-

vidual's employer have filed all required returns and forms for the taxable year for which the individual claims a

refund.

CAUTION

The information in this publication reflects the position of the Wisconsin Department of Revenue of laws enacted by the

Wisconsin Legislature as of December 1, 2017. Laws enacted after that date, administrative rules, and court decisions

may change the interpretations in this publication.

WI FORM

NUMBER

FORM TITLE

FEDERAL

COUNTERPART

BTR-101

Application for Business Tax Registration

SS-4

WT-4

Employee’s Wisconsin Withholding Exemption Certificate & New Hire Reporting

W-4

WT-4A

Wisconsin Employee Withholding Agreement

None

WT-6

Withholding Tax Deposit Report

Form 8109

WT-7

Employer’s Annual Reconciliation of Wisconsin Income Tax Withheld from Wages

W-3

None*

Wage and Tax Statement

W-2

Form 9b

Wisconsin Information Return

1099, W-2G

WT-11

Nonresident Entertainer’s Receipt for Withholding by Employer

None

W-200

Certificate of Exemption from Wisconsin Income Tax Withholding

None

W-220

Nonresident Employee’s Withholding Reciprocity Declaration

None

* Wisconsin uses federal Form W-2

4

I. FEDERAL EMPLOYER’S TAX GUIDE

Wisconsin individual income and withholding tax laws generally conform to the federal Internal Revenue Code. Most

definitions and instructions are identical to those used by the Internal Revenue Service (IRS) and published in the Federal

Employer’s Tax Guide Circular E (Publication 15) and the Employer’s Supplemental Tax Guide (Publication 15-A).

These publications may be obtained at irs.gov, your local IRS office, or by calling 1-800-829-3676.

II. REGISTRATION AND GENERAL WITHHOLDING TAX PROVISIONS

A. Application Process

Every employer who pays wages subject to Wisconsin withholding, or voluntarily withholds Wisconsin tax, must register

for a Wisconsin withholding tax number. Register online at tap.revenue.wi.gov/btr or complete Form BTR-101, Applica-

tion for Wisconsin Business Tax Registration. An application may also be obtained by contacting any of our local offices,

or by calling (608) 266-2776.

If you register online you will receive a Wisconsin withholding tax number within one to two business days. No expedite

fee is charged for this service. Allow 15 business days for processing of paper applications.

Fully complete your application. Failure to include information such as the first date of withholding, your federal employ-

er identification number, or an estimate of the amount of tax to be withheld could delay the processing of your

application.

Business Tax Registration Renewal Fee: The initial $20 registration fee covers a period of two years. At the end of that

period, a $10 renewal fee applies every two years to all persons holding permits or certificates subject to Business Tax

Registration provisions.

Expedited Fee: You may receive immediate service on your application when you visit the department’s Madison office

located at 2135 Rimrock Road or when you fax your application to (608) 264-6884 as explained below. We charge a $10

expedite fee for this service.

When faxing the application:

• Include a cover sheet with the contact's name, fax and telephone numbers,

• Use black ink,

• Write “Expedite” across top of application.

B. Wisconsin Withholding Tax Number

Employers should use the 15-digit Wisconsin withholding tax number assigned to your business for all state with-

holding tax reporting.

The Wisconsin withholding tax number has 15 digits and appears as: 036-0000000000-00. You will retain your number

permanently, unless you no longer have a withholding requirement and close your account. If you have more than one

withholding tax number, notify us. We will let you know which number to use.

Each corporation (subsidiary) of an affiliated group, which has its own employees and its own federal employer identifi-

cation number, must apply for its own Wisconsin withholding tax number. Each corporation is considered a separate

employer. Unlike the Internal Revenue Service, Wisconsin does not permit the use of a Common Paymaster. Howev-

er, a corporation that has several divisions (not separate entities) must have a single Wisconsin withholding tax number to

report withholding for all divisions.

The Wisconsin withholding tax number is different from the federal employer identification number. Always use the Wis-

consin withholding tax number when corresponding with us.

5

C. Filing Frequency

We assign your filing frequency based on information provided in your application. If your withholding liability changes,

you may be notified in writing of a change to your filing frequency starting with the period beginning January 1 of the

next calendar year.

Send requests to file more frequently by letter or email. You must include the reason you are requesting a change and your

Wisconsin withholding tax number. Mail your request to Wisconsin Department of Revenue, Mail Stop 3-80,

P.O. Box 8902, Madison, WI 53708-8902 or email your request to DORWithholdingTax@wisconsin.gov.

Continue to file according to your assigned filing frequency. If we approve your request, we will send you a letter with the

new filing frequency and effective date.

D. Reactivate Withholding Account

If you resume business or rehire employees, and previously held a Wisconsin withholding tax number, request reinstate-

ment of your prior number if ownership of your business is the same. Call (608) 266-2776 or email your request to

DORRegistration@wisconsin.gov.

E. Change In Business Entity

An employer who changes the type of business entity (e.g., sole proprietorship to partnership or corporation, or partner-

ship to corporation) must obtain a new Wisconsin withholding tax account number. An employer who acquires the

business of another employer may NOT use the former employer's tax number. The new employer must apply for his or

her own number.

Note: The department has adopted a policy similar to the IRS regarding partner changes. Generally, if you are required to

obtain a new federal employer identification number, you are also required to register for a new Wisconsin withholding

tax number.

A continuing partnership with an ownership change of less than 50% may continue using the same Wisconsin withholding

tax account number. When the change in ownership is 50% or more, follow federal requirements. If a new federal identi-

fication number is required, a new Wisconsin withholding number is required. Send the names, addresses, and social

security numbers of added or dropped partners to the department within 10 days after a change takes place.

A separate annual reconciliation (WT-7) and wage and information returns must be filed for each legal entity.

Single-Member LLC:

A disregarded entity is automatically considered an “employer” for purposes of federal withholding taxes. Wisconsin fol-

lows this treatment. This means a single-owner entity that is disregarded as a separate entity under Internal Revenue Code

is an “employer” for Wisconsin withholding tax purposes.

As an “employer,” a disregarded entity must obtain a Wisconsin withholding tax number.

F. Employee’s Withholding Exemption Certificate

The Wisconsin Withholding Exemption Certificate (Form WT-4) is used to determine the amount of Wisconsin income

tax to be withheld from employee wages. Every newly-hired employee must give Form WT-4 to his or her employer, un-

less claiming the same number of withholding exemptions for federal and state purposes. Employers may also use this

form to comply with new hire reporting requirements.

G. Special Situations Regarding Form WT-4 And Form WT-4A

ADDITIONAL WITHHOLDING: If the amount withheld is insufficient to meet an employee’s annual income tax liability,

the employee can avoid making estimated tax payments or paying a large amount with their income tax return by reducing

the number of withholding exemptions claimed. If no exemptions are claimed, and underwithholding still results, the em-

6

ployee may designate an additional amount to be withheld using Wisconsin Form WT-4 or submit a written request to the

employer to have an additional amount withheld each pay period.

LESS WITHHOLDING: If the maximum number of allowable exemptions is claimed and over withholding still occurs,

the employee may request the employer withhold a lesser amount. In such instances, the employee must complete an Em-

ployee Withholding Agreement (Form WT-4A).

The employee must provide a copy of the agreement to the employer and the department. The department is authorized to

void an agreement by written notification to the employer and employee if it is determined that the agreement is incorrect

or incomplete.

NO WITHHOLDING: An employer is not required to deduct and withhold Wisconsin income tax from the employee’s

wages when the employee certifies to the employer on Form WT-4 that the employee had no income tax liability for the

prior year and anticipates no liability for the current year. Federal Form W-4 cannot be used by an employee to claim

complete exemption from Wisconsin withholding. See item H, for an explanation of the employer’s responsibility to fur-

nish a copy of the exemption certificate to this department.

Employers must retain copies of Forms WT-4 and WT-4A submitted by their employees. Note: A claim for total exemp-

tion from withholding tax must be renewed annually. Employers should review their records at the beginning of each year

to ensure they have a current Form WT-4 on file for each employee claiming total exemption from withholding tax.

EMPLOYEES WHO PREPAY THEIR WISCONSIN INCOME TAX: An employee may prepay with the department

100 percent of his or her estimated tax for the next year before the last day of the current year.

We will issue a Certificate of Exemption From Wisconsin Income Tax Withholding (Form W-200) for the employee to

present to his or her employer. The employee is then entitled to a complete exemption from Wisconsin withholding for the

designated year. This is a voluntary action by the employee and may not be forced by the employer. The employer should

not ask the employee to complete, nor should the employer accept, a Form WT-4 which claims total exemption for the

year of the prepayment.

See our Prepayment of Tax common question for addition information.

H. Employees Claiming Exemption From Withholding (Forms W-4 and WT-4)

Wisconsin law requires that a copy of the appropriate exemption form be filed with the department whenever either of the

following conditions exists:

• The employee claims more than 10 exemptions.

• The employee claims complete exemption from Wisconsin withholding and earns over $200 a week.

Employers. Send Forms W-4/WT-4 copies claiming more than 10 exemptions or complete exemption from withholding

to Wisconsin Department of Revenue, Audit Bureau, P.O. Box 8906, Madison, WI 53708-8906. Form WT-4 is the only

form that may be used to claim complete exemption from Wisconsin withholding. Federal Form W-4 cannot be substitut-

ed.

Copies of employee exemption certificates filed during a quarter must be submitted at the end of the quarter. No copy is

required if the employee is no longer working for the employer at the end of the quarter.

We will review certificates filed by the employer upon receipt. Employers withhold taxes as requested by their employee,

unless the employer receives written instructions from the department to withhold on some other basis.

Employees. When an employee claims complete exemption from Wisconsin withholding tax, a new Form WT-4 must be

filed annually. The employer must receive a completed Form WT-4 for the current income year on or before April 30, of

that year. If the employee fails to furnish an exemption form, the employee shall be considered as claiming zero withhold-

ing exemptions.

7

I. Withholding Calculator

An employee with too much or too little withheld from his or her paycheck may find our withholding calculator helpful.

The calculator estimates the amount of Wisconsin income tax withheld by an employer based on the number of withhold-

ing exemptions the employee claims, the employee's withholding status and pay information. To access the calculator,

download the Department of Revenue Mobile App.

J. New Hire Reporting Requirements

All employers with a federal employer identification number must report all newly-hired or rehired employees to the New

Hire Program within 20 days of hire or re-hire.

The easiest and most cost effective way to report new hires is via the Internet. For more information, visit

https://wi-newhire.com or contact the New Hire Processing Center toll free at 1-888-300-4473.

K. Wages Paid To Residents Who Work Outside Wisconsin

Wages paid to Wisconsin residents are subject to Wisconsin withholding, whether paid for services performed entirely in

Wisconsin, partly in and partly outside Wisconsin, or entirely outside Wisconsin. The Secretary of Revenue may authorize

special withholding arrangements in hardship cases resulting from situations in which persons domiciled in Wisconsin are

subjected to withholding in some other state because they perform substantial personal services in such other state.

L. Special Minnesota Withholding Arrangement

The Secretary of Revenue has authorized a special withholding arrangement for employers of Wisconsin residents work-

ing in Minnesota. Wisconsin withholding will not be required under the following circumstances:

• The employee is a legal resident of Wisconsin (i.e., domiciled in Wisconsin) when the wages are earned in Min-

nesota, and

• The same wages earned by the Wisconsin resident are subject to Minnesota withholding and would also be sub-

ject to Wisconsin withholding.

Employees who do not have Wisconsin income tax withheld from wages earned in Minnesota must make regular estimat-

ed tax payments if they expect to owe $500 or more with their Wisconsin income tax return for the year. For more

information see, revenue.wi.gov/Pages/FAQS/ise-mnrecipro.aspx.

M. Out-of-State Disaster Relief Responders

2015 Wisconsin Act 84 provides qualifying out-of-state employers and out-of-state employees an exemption from em-

ployer withholding registration and income tax reporting requirements, if the qualifying employer or employee is in

Wisconsin solely to perform disaster relief work in connection with a state of emergency declared by the Governor.

“Disaster relief work” means work, including repairing, renovating, installing, building, or performing other services or

activities, relating to infrastructure in this state that has been damaged, impaired, or destroyed in connection with a de-

clared state of emergency.

“Infrastructure” includes property and equipment owned or used by a telecommunications provider or cable operator or

that is used for communications networks, including telecommunications, broadband, and multichannel video networks;

electric generation, transmission, and distribution systems; gas distribution systems; water pipelines; and any related sup-

port facilities that service multiple customers or citizens, including buildings, offices, lines, poles, pipes, structures,

equipment, and other real or personal property.

In order to claim an exemption under the Act, the qualifying business or employee must contact the department within 90

days of the last day of the disaster period. See Publication 411, Disaster Relief, for more information. The above provi-

sions first apply to taxable years beginning on January 1, 2015.

8

N. Wages Paid To Nonresidents Who Work In Wisconsin

All wages paid to nonresidents (persons domiciled outside Wisconsin), for services performed in Wisconsin*, are subject

to withholding unless:

1. Employers are interstate rail or motor carriers, subject to the jurisdiction of the federal Interstate Commerce

Commission and the employee regularly performs duties in two or more states.

2. Payment is for retirement, pension and profit sharing benefits received after retirement.

3. Employees are residents of a state with which Wisconsin has a reciprocity agreement; refer to the Reciprocity

section.

4. Employees are residents of a state with which Wisconsin does not have a reciprocity agreement and either:

a. the employer is an interstate air carrier and the employee earns 50% or less of his or her compensation in Wis-

consin, or

b. the employer can reasonably expect the annual Wisconsin earnings to be less than $1,500.

If the employee wage estimate in 4b above exceeds $1,500, the employer must withhold from wages paid thereafter, suffi-

cient amounts to offset amounts not withheld from wages previously paid.

*If a nonresident earns wages both in and outside of Wisconsin, only that part of the wages earned in Wisconsin in each

payroll period is subject to Wisconsin withholding. It may be necessary for the employer to make a reasonable division of

wages for each payroll period with regard to services performed in and outside of Wisconsin. The employer may also be

required to withhold income tax for the employee’s state of residence. Contact the department in that state for more in-

formation.

Reciprocity: Wisconsin has reciprocity agreements with Illinois, Indiana, Kentucky, and Michigan. Persons who employ

residents of those states are not required to withhold Wisconsin income taxes from wages paid to such employees. Written

verification is required to relieve the employer from withholding Wisconsin income taxes from such employee’s wages.

Form W-220, Nonresident Employee's Withholding Reciprocity Declaration, may be used for this purpose.

O. Nonresident Employers

Employers engaged in business in Wisconsin (e.g., organized under Wisconsin law, licensed to do business in Wisconsin,

or transacting business in Wisconsin) have the same requirements to withhold as Wisconsin employers.

Employers who are not engaged in business in Wisconsin, but who employ Wisconsin residents outside of Wisconsin,

may voluntarily register to withhold Wisconsin tax. If the employer chooses not to withhold the tax, the employee may be

required to make estimated payments of Wisconsin income tax. Payments may be made online at tap.revenue.wi.gov/pay

or by using Form 1-ES, Estimated Tax for Individuals, Estates and Trusts.

P. Withholding On Nonresident Entertainers

Wisconsin law requires nonresident entertainers to submit a surety bond or cash deposit if the accumulative total contract

price for their performance(s) in Wisconsin exceeds $7,000.

If the bond or deposit is not filed and the total contract price for the entertainer's performance(s) exceeds $7,000, the "em-

ployer" must withhold a flat 6% tax from the total contract price from the payment made to the nonresident entertainer.

As of January 1, 2014, total contract price does not include travel expense payments made to, or on behalf of, an enter-

tainer that are 1) made under an accountable plan and 2) for actual transportation, lodging, and meals that are directly

related to the entertainer's performance in Wisconsin.

9

This withholding is separate from regular employee withholding and applies only to nonresident entertainers. Any tax

withheld under this nonresident entertainer law must be submitted separately from regular withholding taxes.

A surety bond or cash deposit must be made in the amount of 6% of the total contract price at least seven days prior to the

Wisconsin performance. Cash deposits and withholding payments should be made electronically through our Online Ser-

vices for businesses at revenue.wi.gov.

If payment is not made electronically:

• Mail Form WT-11 and the remittance to Wisconsin Department of Revenue, PO Box 8966, Madison WI

53708-8966, or

• Deliver to the department’s Madison office at 2135 Rimrock Road.

One copy of Form WT-11 should be given to the nonresident entertainer and one copy should be retained by the employ-

er. If you need more information on Form WT-11, call (608) 264-1032.

A nonresident entertainer is:

• A nonresident person who furnishes amusement, entertainment, or public speaking services, or performs in one or

more sporting events in Wisconsin for consideration or,

• A foreign corporation, partnership, or other type of entity, not regularly engaged in business in Wisconsin, that

derives income from amusement, entertainment, or sporting events in Wisconsin or from the services of a nonres-

ident person as defined above.

For more information, see Publication 508, Wisconsin Tax Requirements Relating to Nonresident Entertainers.

Q. Withholding For Noncash Fringe Benefits

Taxable noncash fringe benefits provided to employees must be treated as additional wages that are subject to withhold-

ing. Generally the determination of whether a fringe benefit is taxable for Wisconsin is based on federal income tax law.

Noncash fringe benefits that are subject to federal withholding tax are also subject to Wisconsin withholding, at the same

value and for the same payroll period.

Examples of taxable noncash fringe benefits that are subject to withholding include: use of employer-provided automo-

biles for commuting, an employer-provided vacation, free or discounted commercial airline flights, and employer-

provided tickets to entertainment events.

The amount of Wisconsin income tax to be withheld from an employee who receives taxable noncash fringe benefits can

be determined by:

1. Combining the employee’s taxable noncash fringe benefits and regular wages and determining the withholding as

though the total constituted a single wage payment.

2. Treating the taxable noncash fringe benefit as a supplemental wage payment and determining the amount to be

withheld by following the instructions for supplemental wage payments found on page 20 of this guide.

Note: Federal law permits an employer to elect not to withhold federal income tax for taxable noncash fringe benefits

which employees realize from the use of an employer-provided vehicle. Employers who make this election for federal

purposes will not be required to withhold Wisconsin income tax for the same vehicle fringe benefits.

R. Health Savings Accounts

Effective for taxable years beginning in 2011 and thereafter, Wisconsin follows federal provisions relating to HSAs. The

only difference is the imposition of penalties. For details, see revenue.wi.gov/DOR Publications/1105healthsavings.pdf.

10

S. Third Party Sick Pay

Wisconsin does not follow the federal provisions relating to payments of sick pay made by third parties (e.g., an insurance

company). Wisconsin statutes provide that when a third party payer of sick pay makes payments directly to the employee

and the employee has provided a written request to withhold Wisconsin income tax from those payments, the third party

payer must report and remit the income tax withheld from sick pay, not the employer.

For Wisconsin purposes, the payer of third party sick pay plans who withhold Wisconsin income tax must issue a wage

statement (federal Form W-2) directly to the individual who received the sick pay. The Form W-2 must report the amount

of taxable sick pay and the total amount of Wisconsin income tax withheld.

T. Pensions

If a pension recipient requests in writing that Wisconsin income tax be withheld from his or her pension, the payer, if en-

gaged in business in Wisconsin, must withhold tax in accordance with Wisconsin withholding tables in this booklet or in

the amount that the pension recipient designates to the payer. However, the amount withheld from each pension payment

may not be less than $5.

U. Reporting Of Wages For Agricultural, Domestic, Or Other Employees Exempt From Withholding

"Wages" means all remuneration for services performed by an employee for an employer. Wages are subject to Wisconsin

withholding tax with the exception of agricultural, domestic or other employee wages exempt from withholding as pro-

vided in sec. 71.63, Wis. Stats.

All entities with activities in Wisconsin whether paying taxable wages or not, are required to provide their payees a feder-

al Form W-2, 1099-MISC or 1099-R and should follow these reporting guidelines:

• Wages, regardless of the amount, are to be reported on federal Form W-2.

• All payments which are not wages but from which Wisconsin income tax has been withheld are to be reported on

federal Form W-2, 1099-MISC or 1099-R as appropriate.

• Payments of $600 or more that are not wages and from which no Wisconsin income tax has been withheld are to

be reported on federal Form 1099.

If you do not hold a Wisconsin withholding tax number because you are not required to withhold from employees wages

(agriculture, domestic, etc.), did not withhold, and never held a Wisconsin withholding tax number, enter

036888888888801 on the W-2 in the box titled "Employer's State ID Number."

Forms W-2, W-2G, 1099-MISC, and 1099-R must be filed with the department as outlined in Publication 117, Guide to

Wisconsin Wage Statements and Information Returns. If the forms report Wisconsin withholding, you must also file the

annual reconciliation (WT-7) by January 31. If the due date falls on a weekend or legal holiday, the due date becomes the

business day immediately following the weekend or legal holiday.

V. Willful Misclassification Penalty for Construction Contractors

Any employer engaged in the construction of roads, bridges, highways, sewers, water mains, utilities, public buildings,

factories, housing, or similar construction projects who willfully provides false information to the department, or who

willfully and with intent to evade any withholding requirement, misclassifies or attempts to misclassify an individual who

is an employee of the employer as a nonemployee shall be fined $25,000 for each violation.

W. Payments Made To Decedent Estate Or Beneficiary

Various types of payments are made to the estate or to beneficiaries of a deceased employee which result from the de-

ceased person's employment. The department follows IRS policy in determining whether withholding of income tax is

required from these payments.

11

SUBJECT TO WITHHOLDING: An uncashed check originally received by a decedent prior to the date of death and reis-

sued to the decedent's personal representative shall be subject to withholding of Wisconsin income tax.

NOT SUBJECT TO WITHHOLDING: The following types of payments to a decedent's personal representative or heir

shall not be subject to withholding of Wisconsin income tax:

• Payments representing wages accrued to the date of death but not paid until after death.

• Accrued vacation and sick pay.

• Termination and severance pay.

• Death benefits such as pensions, annuities and distributions from a decedent's interest in an employer's qualified

stock bonus plan or profit sharing plan, as provided in s. 71.63(6)(j), Wis. Stats.

III. DEPOSITING WITHHELD TAXES

A. Reporting Requirements

Wisconsin income taxes are to be withheld from employees in accordance with the instructions in this guide. Withholding

liability is incurred when wages are paid to employees, not when wages are earned. The tax withheld is to be held in trust

for the state by the employer and remitted via the withholding deposit report (WT-6) or annual reconciliation (WT-7), ac-

cording to each employer’s assigned filing frequency.

Withholding deposit reports and the annual withholding reconciliation must be submitted electronically unless you've

been granted a department waiver from electronic filing. Annual filers are not required to file deposit reports.

B. Deposit Report (WT-6) Filing Options

Form WT-6 filing and payment options include:

• My Tax Account - tap.revenue.wi.gov

• Telephone - call 608-261-5340 or 414-227-3895

• Credit Card - through Official Payments 800-272-9829; use jurisdiction code 5800

• ACH Credit - through your financial institution

• File Transmission – DOR website

If an electronic filing waiver has been granted, you may mail your deposit report.

WAGE ATTACHMENTS: Amounts collected from certification (garnishment) of employee wages should NOT be remit-

ted with Wisconsin income tax withheld from employees. All employers must submit wage attachment payments

electronically unless they have been granted an exception. We offer two electronic payment methods:

• My Tax Account

• ACH Credit

For more information, visit revenue.wi.gov/Pages/OnlineServices/wage-wage.aspx.

C. Reporting Periods

The filing frequency assigned to you by the department has a set number of reporting periods per calendar year. When

determining the appropriate reporting period, it is helpful to remember that withholding liability is incurred when wages

are paid to the employee, not when wages are earned.

12

Filing Frequency

# of Reporting Periods Per Calendar Year

WT-7 WT-6

Tax Period End Date

Annual

1

*

12/31

Quarterly

1

4

3/31, 6/30, etc.

Monthly

1

12

1/31, 2/28, etc.

Semi-monthly

1

24

1/15, 1/31, etc.

*No WT-6 deposit report required

Example: Each month a semi-monthly filer must file a report for the 1st through the 15th of the month and a report for

the 16th through the end of month. An employer that files on a semi-monthly basis pays employees on January 11. As a

result, the income tax withheld is reported in the period ending January 15 (tax period end date). This report is due to the

department by January 31 (tax period due date).

Example: An employer that files on a monthly basis pays employees on December 26. As a result, the income tax with-

held is reported in the period ending December 31 (tax period end date). This report is due to the department by

January 31 (tax period due date).

A withholding deposit report must be submitted whether or not any taxes are withheld during the period.

ACH debit payments made via the My Tax Account program must be initiated by 4:00 p.m. central standard time of the

due date to be considered timely paid. The electronic withholding deposit report must be made by the due date to be con-

sidered timely filed.

All withholding filers with an active withholding tax account are required to file an annual reconciliation (WT-7).

D. Reporting Changes To Wisconsin Employer Account Information

Employers are obligated to keep the department current of any changes of name or address. You can notify the department

by one of the methods below:

• Submit address change through My Tax Account

• Email: DORRegistration@wisconsin.gov

• Write: Wisconsin Department of Revenue, PO Box 8902, Madison, WI 53708-8902

• Fax to: (608) 264-6884, Attn: Registration Unit

E. Filing Due Dates

Note – If the original due date falls on a weekend or holiday, the return and/or payment is due the business day following

the weekend or holiday.

Deposit Reports (WT-6)

Annual filers – No deposit report required. Withholding is reported on annual reconciliation.

Monthly or quarterly filers – Deposit report is due on or before the last day of the month following the monthly or quar-

terly withholding period.

Semi-monthly filers – When the employee pay date is on or between the 1st and the 15th of the month, the amount deduct-

ed and withheld for the period ending the 15th of the month is due on or before the last day of the month.

When the employee pay date is on or between the 16th and the end of the month, the amount deducted and withheld for

the period ending the last day of the month is due on or before the 15th of the following month.

13

Example: An employee is paid December 16. The employer reports withholding on the deposit report for period ending

December 31. This deposit report is due January 15.

Annual Reconciliation (WT-7)

All filers – The annual reconciliation, wage statements, and information returns are due to the department by January 31,

the last day of the month following the calendar year. When the withholding account is closed before December 31, the

annual reconciliation is due within 30 days of the account cease date. File wage and information returns reflected on the

reconciliation by January 31.

F. Extensions

The department may grant a one-month extension to file the deposit report (WT-6). Extension requests must be received

by the original due date of the deposit report. Note: Interest will be imposed during the one-month extension period at the

rate of one percent. To request an extension, do one of the following:

• Complete the Request Extension to File in My Tax Account

• Email DORRegistration@wisconsin.gov

• Write to Wisconsin Department of Revenue, P.O. Box 8902, Madison, WI 53708-8902

• Fax to (608) 264-6884

G. Failure To File Or Pay By The Due Date

Failure to receive a Wisconsin withholding tax account number does not relieve the employer from timely reporting and

depositing the tax withheld.

LATE FILING FEE: Any person who is required to file a withholding report and deposit withholding taxes that fails to do

so timely and the department shows that the taxpayer's action or inaction was due to the taxpayer's willful neglect and not

to reasonable cause, shall be subject to a $50 late fee, except for corporations taxed under subch. IV or insurance compa-

nies taxed under subch. VII of ch. 71, Wis. Stats., the late fee is $150.

PENALTIES: Any employer who fails or refuses to file a report or statement or remit taxes withheld from employee wag-

es on or by the due date may be subject to penalties upon a showing by the department that the taxpayer's action or

inaction was due to the taxpayer's willful neglect and not to reasonable cause.

A negligence penalty of 5% of the tax due for each month the report is filed after the due date may be imposed. The max-

imum negligence penalty for late filing is 25% of the tax due. The negligence penalty may be waived on appeal if a return

is filed late due to reasonable cause.

A penalty of 25% of the amount not withheld or properly reported, deposited or paid over may also be imposed.

INTEREST: Interest accrues at the rate of 18% per year on any taxes that are not deposited in a timely manner. During a

period in which an extension is granted, interest accrues at the rate of 1% per month.

H. Failure To Report Amount Of Taxes Withheld

An estimated tax amount may be assessed to an employer who fails to timely report the amount of tax withheld for a peri-

od. This estimated amount, if left unanswered, may become final and due. An estimated tax amount, once delinquent, may

only be adjusted by the filing of an actual deposit report and/or annual reconciliation and accompanying employee wage

and tax statements.

14

I. Refund/Credit For Overpayment(s)

A claim for refund of an overpayment must be filed within four years from the due date of the income or franchise return.

A written request for a refund must be submitted to the department within the four-year period and the request must be

accompanied by an amended annual reconciliation and employee wage and tax statements (if changed).

Mail claims for refund to Wisconsin Department of Revenue, Mail Stop 3-14, P.O. Box 8920, Madison, WI 53708-8920.

EXCEPTION: When an overpayment occurs on a prior period, the withholding liability and payment may be re-

duced on a later period within the same calendar year, provided the annual reconciliation for that year has not

been filed.

J. Other

A person required to collect, account for, or pay withholding taxes, who willfully fails to collect, account for, or pay those

taxes to the department, may be held personally liable for such taxes, including interest and penalties.

IV. RECONCILIATION PROCESS

A. Preparing Employee W-2

The following must be reported as Wisconsin wages in Box 16 of Form W-2:

• All wages earned by Wisconsin residents, regardless of where services were performed.

• All wages earned by nonresidents for services performed in Wisconsin, unless the individual is a resident of Illi-

nois, Indiana, Kentucky or Michigan and has properly completed Form W-220, Nonresident Employee's

Withholding Reciprocity Declaration.

Additional W-2 preparation guidance is available at: revenue.wi.gov/Pages/TaxPro/news-2014-140124.aspx.

B. Furnishing Employees With Wage And Tax Statements

A wage and tax statement (federal Form W-2) must be prepared for each employee to whom wages were paid during the

previous calendar year, regardless of the amount of wages paid, and, even though no tax was withheld.

Give the proper copies of this statement to the employee by the following January 31, or at the time employment is termi-

nated. See “Discontinuing Withholding” on page 16 for more information. The copy designated for the department must

be sent to the department along with the annual reconciliation. Filing options are provided in this publication.

If it is necessary to correct a wage and tax statement after it has been given to an employee, a W-2c must be issued to the

employee. If the error affects a reconciliation already filed, file an amended reconciliation.

File corrected wage statements with the department. Options include:

• Submit a corrected EFW2 file to revenue.wi.gov/Pages/OnlineServices/w-2.aspx,

• Send a W-2c to:

Wisconsin Department of Revenue

PO Box 8920

Madison WI 53708-8920

If a wage statement is lost or destroyed, furnish a copy marked “Reissued by Employer” to the employee.

Any “employee” copies of wage statements which, after reasonable effort, cannot be delivered to employees should be

retained by the employer for four years.

15

Note: Any employer who furnishes a false or fraudulent wage statement or who intentionally fails to furnish a wage

statement is subject to a penalty under Wisconsin law.

C. Annual Reconciliation (WT-7) Filing Options

If your Wisconsin withholding tax account was active for any part of the calendar year, you must file an annual reconcilia-

tion. Filing and payment options include:

• My Tax Account - tap.revenue.wi.gov

• Telephone - call 608-261-5340 or 414-227-3895

• eFile Transmission - DOR website

The WT-7 reconciles the amount withheld from wages paid to employees with the amount deposited throughout the cal-

endar year on the WT-6 deposit reports. In addition to filing the WT-7, submit supporting wage statements and

information returns.

Failure to file a completed annual reconciliation or its equivalent can result in the disallowance of the wage deduction on

your individual income tax return or corporation franchise or income tax return.

If an electronic filing waiver has been granted, you may mail Form WT-7 along with supporting wage and information

returns.

Note: Amounts collected from the certification (garnishment) of wages should NOT be included as Wisconsin tax with-

held on the W-2 form or annual reconciliation.

LATE FILING FEES: Any person who is required to file a withholding report and deposit withholding taxes that fails to

do so timely, and the department shows that the taxpayer's action or inaction was due to the taxpayer's willful neglect and

not to reasonable cause, shall be subject to a $50 late fee, except for corporations taxed under subch. IV or insurance

companies taxed under subch. VII of Ch. 71, Wis. Stats., the late fee is $150.

PENALTIES: A penalty of 25% of the amount not withheld, properly deposited or paid over may be imposed, upon a

showing by the department that the taxpayer's action or inaction was due to the taxpayer's willful neglect and not to rea-

sonable cause.

APPEALS: If you are appealing an amount due, you must submit your appeal through My Tax Account, or send a letter to

Wisconsin Department of Revenue, P.O. Box 8981, Madison, WI 53708-8981. If sending a letter, be sure to include your

Wisconsin withholding number. We do not accept appeal requests made by email or telephone.

16

D. Wage and Information Return Requirements

Wage and Information Return Reporting Requirements

Required

information

Send

information

Required

format for paper filers

Do not

send

• 15 digit Wisconsin

withholding number(those

who did not withhold, are

not required to withhold

and never held a Wisconsin

withholding number must

use 036888888888801

• Nine digit federal employer

identification number(FEIN)

• Legal name must match

numbers above

• Nine digit payee tax

identification number

• Wisconsin as top state(if

possible)

Before filing:

• Register, if required, or

make any name changes

• Verify the first three items

above using look-up in My

Tax Account

• Payroll providers use our

withholding data exchange

to verify client information

Electronic:

• If you file 10 or more wage

statements or information

returns, you must file

them electronically. See

Publication 117 for

"How to file".

Paper

• If you file less than 10, we

encourage you to file

electronically. Otherwise,

mail them to the following

address:

Wisconsin Department of

Revenue

P O Box 8920

Madison, WI 53708-8920

Do not send to any other

address

• Data must be in similar

location of federal form

on IRS website

• Must be form format. We

will not accept text lists

• No more than four

statements or returns per

page

• Page no larger than 8.5"

×11"

• Page no smaller than

2.75" high or 4.25" wide

• Send only one statement

or return per

employee/payee(no

duplicates)

• Use blue or black ink

• 1096-federal transmittal

form

• 1099- DIV or 1099-INT if no

Wisconsin withholding(do

not include on WT-7)

• CDs, magnetic tapes or

transmit non-SSA PDFs

• Carbon copies

• Correspondence

• Duplicate W-2s with no

change(if change made, file

W-2c only)

• Duplicate WT-7

• Old version of WT-7 if paper

filing

• W-2 or 1099 file with no

Wisconsin connection

• W-2s or 1099s with no

Wisconsin connection if

paper filing

• WT2

E. Filing Wage and Information Returns

If you file are required to file 10 or more wage statements (W-2) or 10 or more information returns (1099-MISC,

1099-R, W-2G), you must file these statements/returns electronically. Filing options include:

• Key W-2's, 1099-MISCs and 1099-Rs in My Tax Account when filing the annual reconciliation (WT-7).

• Transfer a PDF file (for W-2s) created at the Social Security Administration website to

revenue.wi.gov/Pages/OnlineServices/w-2.aspx.

• Transfer an EFW2 file (for W-2s) to revenue.wi.gov/Pages/OnlineServices/w-2.aspx. See Publication 172 for

Wisconsin specifications.

• Transfer an IRS formatted file (for 1099-MISCs, 1099-Rs and W-2Gs) to

revenue.wi.gov/Pages/OnlineServices/w-2.aspx. See Publication 172 for Wisconsin specifications.

Note:

• Employers and payers required to file electronically may request a waiver from electronic filing using

Form EFT-102, if filing electronically would cause an undue hardship.

• We do not accept magnetic media.

17

If you file fewer than 10 wage statements or fewer than 10 information returns, we encourage you to file electroni-

cally. A 13-digit receipt number will be issued upon completion. Otherwise, mail wage and information returns to

Wisconsin Department of Revenue, PO Box 8920, Madison, WI 53708-8920.

See Publication 117, Guide to Wisconsin Wage and Information Returns, for specific wage and information reporting in-

structions.

F. Extensions

We may grant a one-month extension to file the annual reconciliation. If an extension is granted, it also applies to

Forms W-2, 1099-MISC and 1099-R. Due dates for the following cannot be extended:

• Furnishing wage statements to employees

• Furnishing information returns to recipients

Extensions must be requested through My Tax Account, in writing, or via email, on or before the due date of the annual

reconciliation.

Attn: Extension request

Registration Unit

Mail Stop 3-80

PO Box 8902

Madison WI 53708-8902

DORRegistration@wisconsin.gov

G. Discontinuing Withholding

When an employer goes out of business, the employer must notify the department of the last date of withholding. We will

send a letter confirming the account closure. The annual reconciliation must be filed within 30 days of discontinuing

withholding.

If the employer ceases to pay taxable wages, or all of the employees are exempt from withholding based on the Employ-

ees Wisconsin Withholding Exemption Certificate (Form WT-4), the employer should request to have its Wisconsin

withholding account inactivated.

If taxes are again withheld, the employer can request that the account be reactivated by calling (608) 266-2776 or email-

ing DORRegistration@wisconsin.gov.

H. Wisconsin Information Return Form 9b

Note: Federal Form 1099 may be used in lieu of Wisconsin Form 9b. The due dates shown below apply to both forms.

Who must file—Any person, including individuals, partnerships, fiduciaries, and corporations, making payments to indi-

viduals of rents, royalties, or other income reportable on federal Forms 1099-R and 1099-MISC.

Items reportable on Forms 9b due January 31-Annuities, pensions, and other nonwage compensation of $600 or more

not reported on a wage statement. Report only payments made to Wisconsin residents or payments to nonresidents for

services performed in Wisconsin. If an employee receives wages subject to withholding and additional amounts not sub-

ject to withholding, the total compensation must be reported on a wage statement.

Items reportable on Forms 9b due January 31 for corporations and January 31 for persons other than a corpora-

tion-Rents and royalties of $600 or more paid to a Wisconsin resident, regardless of the location of the property to which

such payments relate. Rents and royalties of $600 or more paid to a nonresident of Wisconsin on property located in Wis-

consin.

Where to file-For the most current information, refer to Publication 117, Guide to Wisconsin Wage Statements and In-

formation Returns.

18

Note: If Wisconsin withholding is reported on a 1099, the 1099 must be included on the annual reconciliation.

Combined Federal/State Filing Program-Payers who participate in the Combined Federal/State Filing Program are not

required to file Forms 1099 with the Wisconsin Department of Revenue unless there is Wisconsin withholding. Any

Form 1099 with Wisconsin withholding must be filed along with the annual reconciliation, Form WT-7.

V. OTHER TAXES TO BE AWARE OF

If you have business activities or earn income in Wisconsin, you may be subject to other Wisconsin taxes. Although the

information below is not intended to be all inclusive, it may help you in obtaining information about other Wisconsin tax-

es. More information is available on our website.

SALES AND USE TAX: A state sales and use tax is imposed in Wisconsin. In addition, some counties in the state impose a

county sales/use tax. Also, the counties of Milwaukee, Ozaukee, Racine, Washington and Waukesha have a 0.1% baseball

stadium tax. A chart showing the state, county and stadium tax rates by county is available at: reve-

nue.wi.gov/Pages/FAQS/pcs-taxrates.aspx.

The sales tax is imposed on the sales price from the retail sale, lease, or rental of all tangible personal property, unless

specifically exempt, and taxable services. If you make retail sales of items subject to the Wisconsin sales and use tax, you

must register for a Wisconsin seller’s permit.

Wisconsin also imposes a use tax on the purchase of tangible personal property or taxable services that are stored, used, or

consumed in this state on which sales tax was not charged. This most commonly occurs when tangible personal property

is purchased from out-of-state retailers and no sales tax is charged.

Individuals, partnerships, corporations and other organizations registered for sales or use tax with the department should

report any use tax on their Wisconsin state and county sales and use tax return. Individuals who are not registered for sales

or use tax with the department may report the tax from out-of-state purchases on their income tax return. A line is provid-

ed on individual income tax returns called “Sales and use tax due on Internet, mail order, or other out-of-state purchases.”

INDIVIDUAL INCOME TAX: Every person who is a resident of Wisconsin and who has gross income exceeding a certain

amount is subject to Wisconsin income taxes, regardless of where the income is earned.

A person who is a nonresident of Wisconsin is subject to Wisconsin income taxes if he or she has gross income of $2,000

or more from Wisconsin sources, such as personal services performed in Wisconsin or income from a business or property

in Wisconsin.

CORPORATION INCOME OR FRANCHISE TAX: Every corporation organized under the laws of Wisconsin or licensed

to do business in Wisconsin (except certain organizations exempt under sec. 71.26(1)(a) or 71.45(1), Wis. Stats.) is re-

quired to file a Wisconsin corporate franchise or income tax return, regardless of whether or not business was transacted.

Unlicensed corporations are also required to file returns for each year they do business or have certain business activities

in Wisconsin.

ESTIMATED TAX FOR INDIVIDUALS: Estimated income tax payments are generally required if you expect to owe $500

or more of income tax with your income tax return. The estimated tax requirement applies to full-year residents, part-year

residents, and nonresidents. Interest may be imposed if you fail to make these payments.

ESTIMATED TAX FOR CORPORATIONS: Corporations must generally make estimated income or franchise tax pay-

ments if their current year tax liability will be $500 or more.

UNEMPLOYMENT INSURANCE: For more information contact the Wisconsin Department of Workforce Development.

WORKERS COMPENSATION: For more information contact the Wisconsin Department of Workforce Development.

Remittances for unemployment tax should be made according to Wisconsin Department of Workforce Development in-

structions. Funds are separate from employee withholding.

19

VI. KEEPING AWARE OF CHANGES IN WISCONSIN TAX LAWS

If you are required to file Wisconsin tax returns, you should be aware of changes in the tax laws, court cases, and other

published guidance which may affect how you file returns and compute tax. Information available from our website in-

cludes:

WITHHOLDING TAX UPDATE

The Withholding Tax Update is an annual publication that provides updated material on general withholding tax laws.

The Withholding Tax Update is a supplement to the Wisconsin Employer’s Withholding Tax Guide.

WISCONSIN TAX BULLETIN

The Wisconsin Tax Bulletin is a quarterly publication prepared by the department. The bulletin includes information on

most taxes administered by the department, including sales and use, income, franchise, and excise taxes. It includes up-to-

date information on new tax laws, interpretations of existing laws, information on filing various types of returns, and on

current tax topics. It also gives a brief excerpt of major Wisconsin tax cases decided by the courts and the Wisconsin Tax

Appeals Commission.

RULES-WISCONSIN ADMINISTRATIVE CODE

The Wisconsin Administrative Code includes administrative rules that interpret the Wisconsin Statutes. Rules have the

force and effect of law. The department has adopted a number of rules concerning interpretations of the various Wisconsin

tax laws.

TOPICAL AND COURT CASE INDEX

The Topical and Court Case Index will help you find a particular Wisconsin Statute, Administrative Rule, Wisconsin Tax

Bulletin article or tax release, publication, Attorney General opinion, or court decision that deals with your particular

Wisconsin tax question.

QUESTIONS? CONTACT US

Wisconsin Department of Revenue

Mail Stop 5-77

P.O. Box 8949

Madison, WI 53708-8949

DORWithholdingTax@wisconsin.gov

(608) 266-2776

revenue.wi.gov

Department of Revenue Office Locations

Offices Providing Daily Assistance (Monday-Friday)

Location

Address

Telephone

Hours

Appleton

265 W. Northland Ave.

(608) 266-2776

7:45-4:30

Eau Claire

718 W. Clairemont Ave.

(608) 266-2776

7:45-4:30

Green Bay

200 N. Jefferson St., Rm. 526

(608) 266-2776

7:45-1:00

Madison

2135 Rimrock Rd.

(608) 266-2776

7:45-4:30

Milwaukee

819 N. Sixth St. Rm. 408

(608) 266-2776

7:45-4:30

Offices Providing Assistance on Mondays Only

Location

Address

Telephone

Hours

Wausau

730 N. Third St.

(608) 266-2776

7:45-1:00 (Monday only)

20

WISCONSIN INCOME TAX WITHHOLDING TABLES AND METHODS

INTRODUCTION

Use the wage-bracket tables to determine the amount of income

tax to be withheld on the following pages in the same way as

those appearing in federal Circular E. There are two alternate

methods of determining the amount of tax to be withheld which

have been approved by the department. The instructions for

these methods appear immediately following the wage-bracket

tables. Employers who desire to use a method other than the

wage-bracket tables or the approved alternate methods must

receive permission from the department before the beginning of

the payroll period for which the employer desires to withhold

the tax by such other method.

An employer has the discretion of withholding an entire

month’s taxes in one pay period when payroll periods are more

than once a month.

SUPPLEMENTAL WAGE PAYMENTS

If supplemental wages - such as bonuses, commissions, or over-

time pay - are paid at the same time as regular wages, the

income tax to be withheld should be determined as if the total of

the supplemental and regular wages were a single wage pay-

ment for the regular payroll period.

If supplemental wages are paid between regular payroll periods,

the employer may determine the tax to be withheld by adding

the supplemental wages either to the regular wages for the cur-

rent payroll period or to the regular wages for the last preceding

payroll period within the same calendar year.

As an alternative to the above methods, the withholding on sup-

plemental wage payments may be determined by estimating the

employee’s annual gross salary and applying flat percentages to

the supplemental payments. (These flat percentages may be

used only where supplemental payments are involved; they

cannot be used for determining the withholding liability for

regular wages and salaries.)

Approved Flat Percentages

Annual Gross Salary

At

Least

But Less

Than %

0

10,910 ........................................ 4.00

10,910

21,820 ........................................ 5.84

21,820

240,190 ........................................ 6.27

240,190 and over ............................................... 7.65

USE OF DAILY OR MISCELLANEOUS TABLES

If an employee has no payroll period, determine the tax to be withheld as if the wages were paid on a “daily or mis-

cellaneous” payroll period. This method requires a determination of the number of days (including Sundays and

holidays) in the period covered by the wage payment. If the wages are unrelated to a specific length of time (for ex-

ample, commissions paid on completion of a sale), then the number of days must be counted from the date of

payment back to the latest of these three events: (a) the last payment of wages made during the same calendar year,

(b) the date employment commenced if during the same calendar year, or (c) January 1 of the same year.

In cases where an employee is paid for a period of less than 1 week and signs a written statement (under penalties of

perjury) that the employee does not work for wages subject to withholding for any other employer during the same

calendar week, then the employer is permitted to compute the withholding on the basis of a weekly, instead of a dai-

ly or miscellaneous payroll period.

Please go to the next page to see the “daily or miscellaneous” charts.

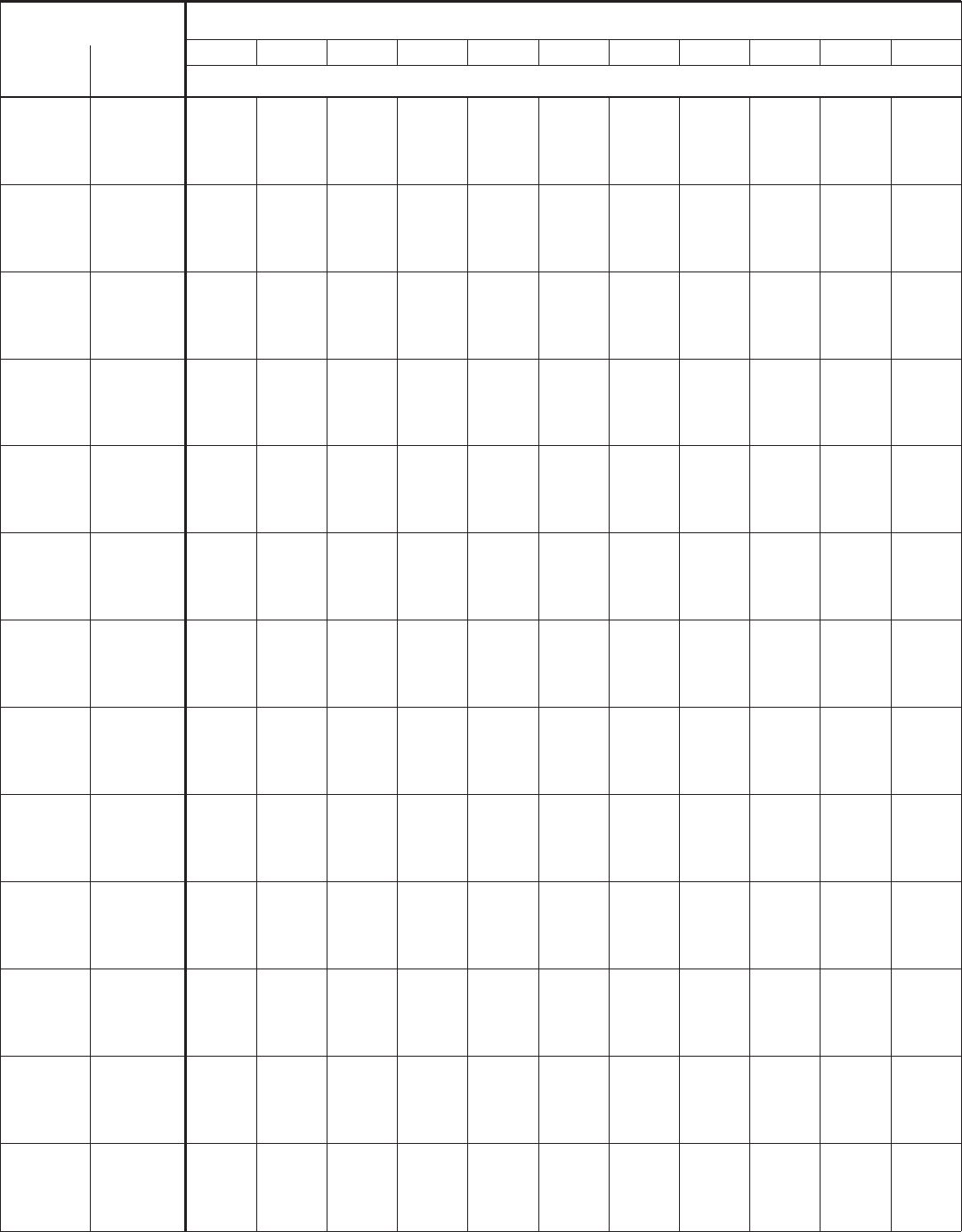

0 9 0 0 0 0 0 0 0 0 0 0 0

9 14 0

14 19 0

19 24 .20 .20 .10 .10 .10

24 29 .40 .40 .30 .30 .30 .20 .20 .10 .10

29 34 .60 .60 .50 .50 .50 .40 .40 .30 .30 .20 .20

34 34 .70 .70 .60 .60 .60 .50 .50 .40 .40 .30 .30

39 44 1.00 1.00 .90 .90 .90 .80 .80 .70 .70 .60 .60

44 49 1.30 1.20 1.20 1.10 1.10 1.00 1.00 .90 .90 .90 .80

49 54 1.60 1.50 1.50 1.40 1.40 1.30 1.20 1.20 1.10 1.10 1.00

54 59 1.90 1.90 1.80 1.70 1.70 1.60 1.60 1.50 1.40 1.40 1.30

59 64 2.30 2.20 2.10 2.10 2.00 1.90 1.90 1.80 1.80 1.70 1.60

64 69 2.60 2.50 2.50 2.40 2.30 2.30 2.20 2.10 2.10 2.00 2.00

69 74 2.90 2.90 2.80 2.70 2.70 2.60 2.50 2.50 2.40 2.30 2.30

74 79 3.30 3.20 3.10 3.10 3.00 2.90 2.90 2.80 2.70 2.70 2.60

79 84 3.60 3.50 3.50 3.40 3.30 3.30 3.20 3.10 3.10 3.00 2.90

84 89 4.00 3.90 3.80 3.80 3.70 3.60 3.60 3.50 3.40 3.40 3.30

89 94 4.30 4.30 4.20 4.10 4.00 4.00 3.90 3.80 3.80 3.70 3.60

94 99 4.70 4.60 4.50 4.50 4.40 4.30 4.30 4.20 4.10 4.10 4.00

99 104 5.00 5.00 4.90 4.80 4.70 4.70 4.60 4.50 4.50 4.40 4.30

104 109 5.40 5.30 5.20 5.20 5.10 5.00 5.00 4.90 4.80 4.80 4.70

109 114 5.70 5.70 5.60 5.50 5.50 5.40 5.30 5.20 5.20 5.10 5.00

114 119 6.10 6.00 5.90 5.90 5.80 5.70 5.70 5.60 5.50 5.50 5.40

119 124 6.40 6.40 6.30 6.20 6.20 6.10 6.00 5.90 5.90 5.80 5.70

124 129 6.80 6.70 6.60 6.60 6.50 6.40 6.40 6.30 6.20 6.20 6.10

129 134 7.10 7.10 7.00 6.90 6.90 6.80 6.70 6.60 6.60 6.50 6.40

134 139 7.50 7.40 7.30 7.30 7.20 7.10 7.10 7.00 6.90 6.90 6.80

139 144 7.80 7.80 7.70 7.60 7.60 7.50 7.40 7.40 7.30 7.20 7.10

144 149 8.20 8.10 8.00 8.00 7.90 7.80 7.80 7.70 7.60 7.60 7.50

149 154 8.50 8.50 8.40 8.30 8.30 8.20 8.10 8.10 8.00 7.90 7.80

154 159 8.90 8.80 8.70 8.70 8.60 8.50 8.50 8.40 8.30 8.30 8.20

159 164 9.20 9.20 9.10 9.00 9.00 8.90 8.80 8.80 8.70 8.60 8.50

164 169 9.60 9.50 9.50 9.40 9.30 9.20 9.20 9.10 9.00 9.00 8.90

169 174 9.90 9.90 9.80 9.70 9.70 9.60 9.50 9.50 9.40 9.30 9.30

174 179 10.30 10.20 10.10 10.10 10.00 9.90 9.80 9.80 9.70 9.60 9.60

179 184 10.60 10.50 10.40 10.40 10.30 10.20 10.20 10.10 10.00 10.00 9.90

184 189 10.90 10.80 10.70 10.70 10.60 10.50 10.50 10.40 10.30 10.30 10.20

189 194 11.20 11.10 11.10 11.00 10.90 10.90 10.80 10.70 10.70 10.60 10.50

194 199 11.50 11.40 11.40 11.30 11.20 11.20 11.10 11.00 11.00 10.90 10.80

199 204 11.80 11.80 11.70 11.60 11.60 11.50 11.40 11.30 11.30 11.20 11.10

204 209 12.10 12.10 12.00 11.90 11.90 11.80 11.70 11.70 11.60 11.50 11.50

209 214 12.50 12.40 12.30 12.20 12.20 12.10 12.00 12.00 11.90 11.80 11.80

214 219 12.80 12.70 12.60 12.60 12.50 12.40 12.40 12.30 12.20 12.10 12.10

219 224 13.10 13.00 12.90 12.90 12.80 12.70 12.70 12.60 12.50 12.50 12.40

224 229 13.40 13.30 13.30 13.20 13.10 13.10 13.00 12.90 12.80 12.80 12.70

229 234 13.70 13.60 13.60 13.50 13.40 13.40 13.30 13.20 13.20 13.10 13.00

234 239 14.00 14.00 13.90 13.80 13.70 13.70 13.60 13.50 13.50 13.40 13.30

239 244 14.30 14.30 14.20 14.10 14.10 14.00 13.90 13.90 13.80 13.70 13.60

244 249 14.60 14.60 14.50 14.40 14.40 14.30 14.20 14.20 14.10 14.00 14.00

249 254 15.00 14.90 14.80 14.80 14.70 14.60 14.50 14.50 14.40 14.30 14.30

254 259 15.30 15.20 15.10 15.10 15.00 14.90 14.90 14.80 14.70 14.70 14.60

259 264 15.60 15.50 15.50 15.40 15.30 15.20 15.20 15.10 15.00 15.00 14.90

264 269 15.90 15.80 15.80 15.70 15.60 15.60 15.50 15.40 15.40 15.30 15.20

269 274 16.20 16.10 16.10 16.00 15.90 15.90 15.80 15.70 15.70 15.60 15.50

274 279 16.50 16.50 16.40 16.30 16.30 16.20 16.10 16.00 16.00 15.90 15.80

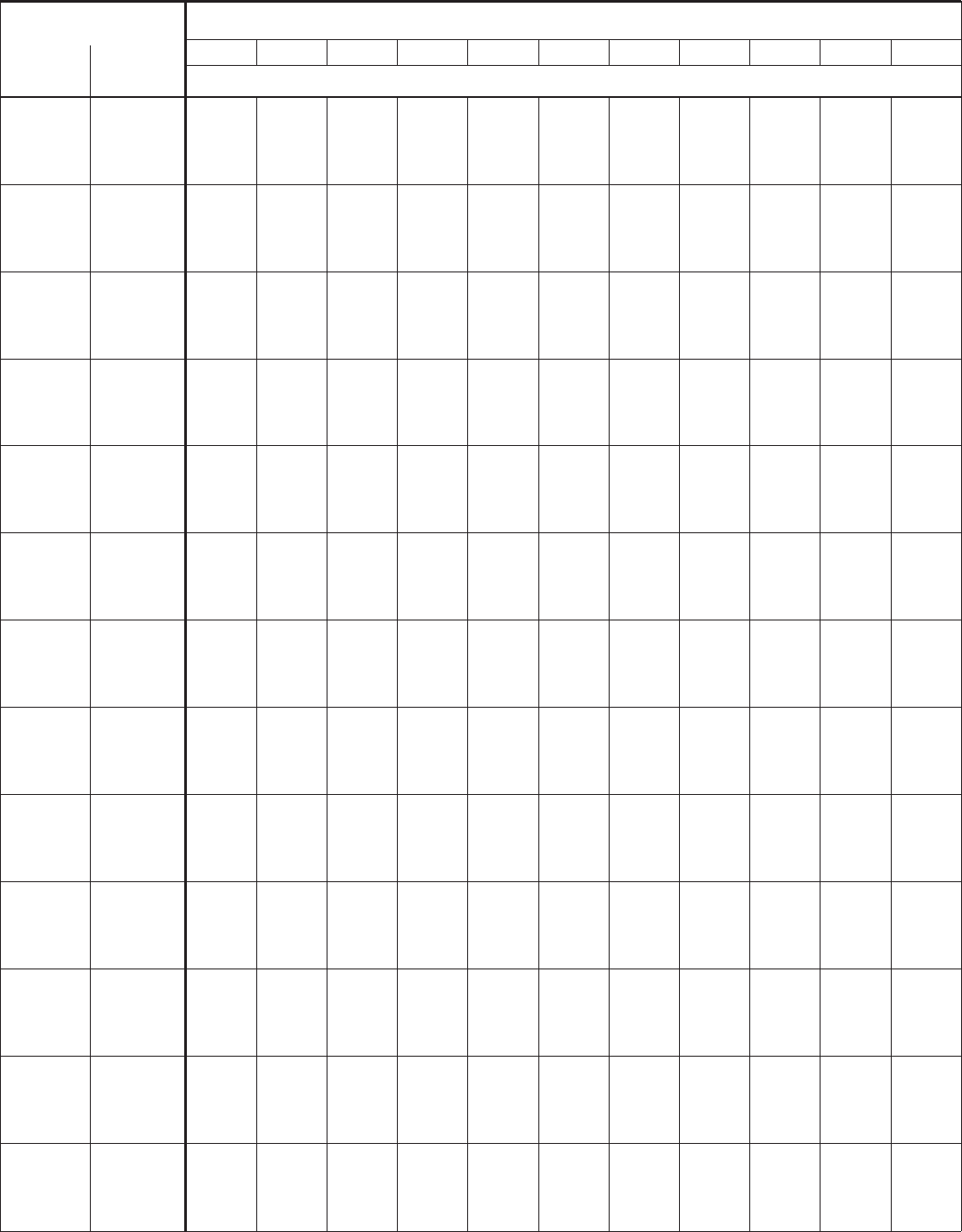

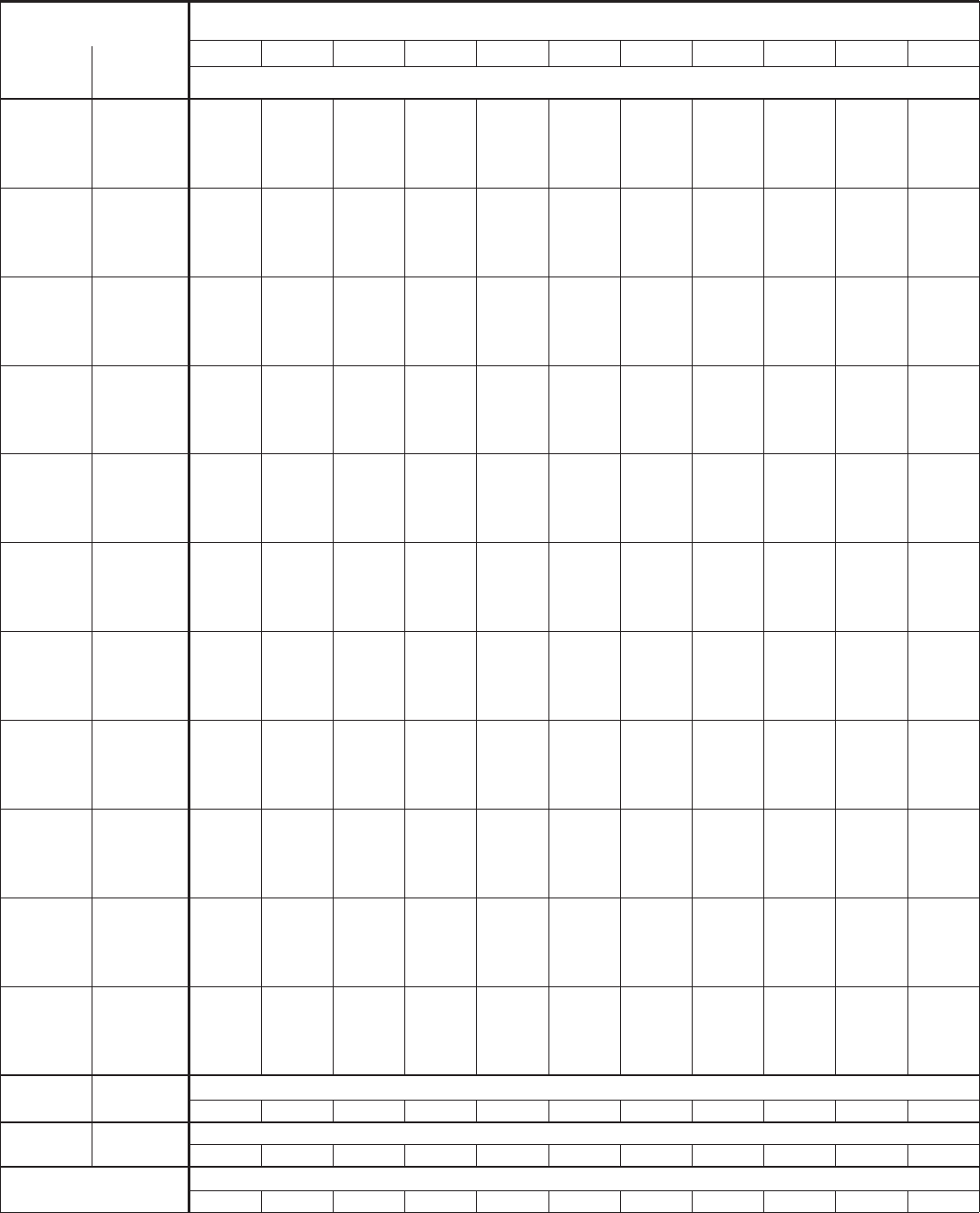

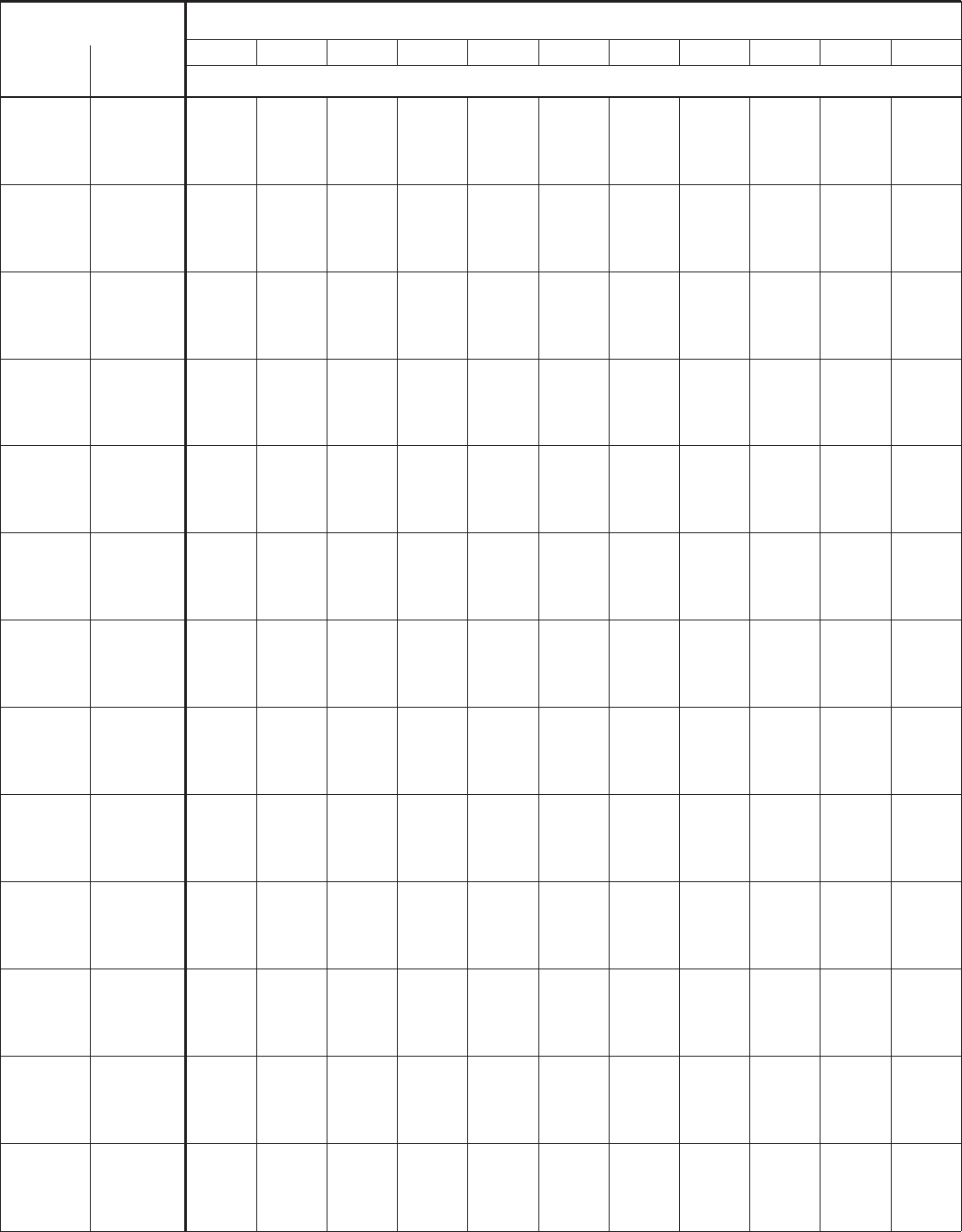

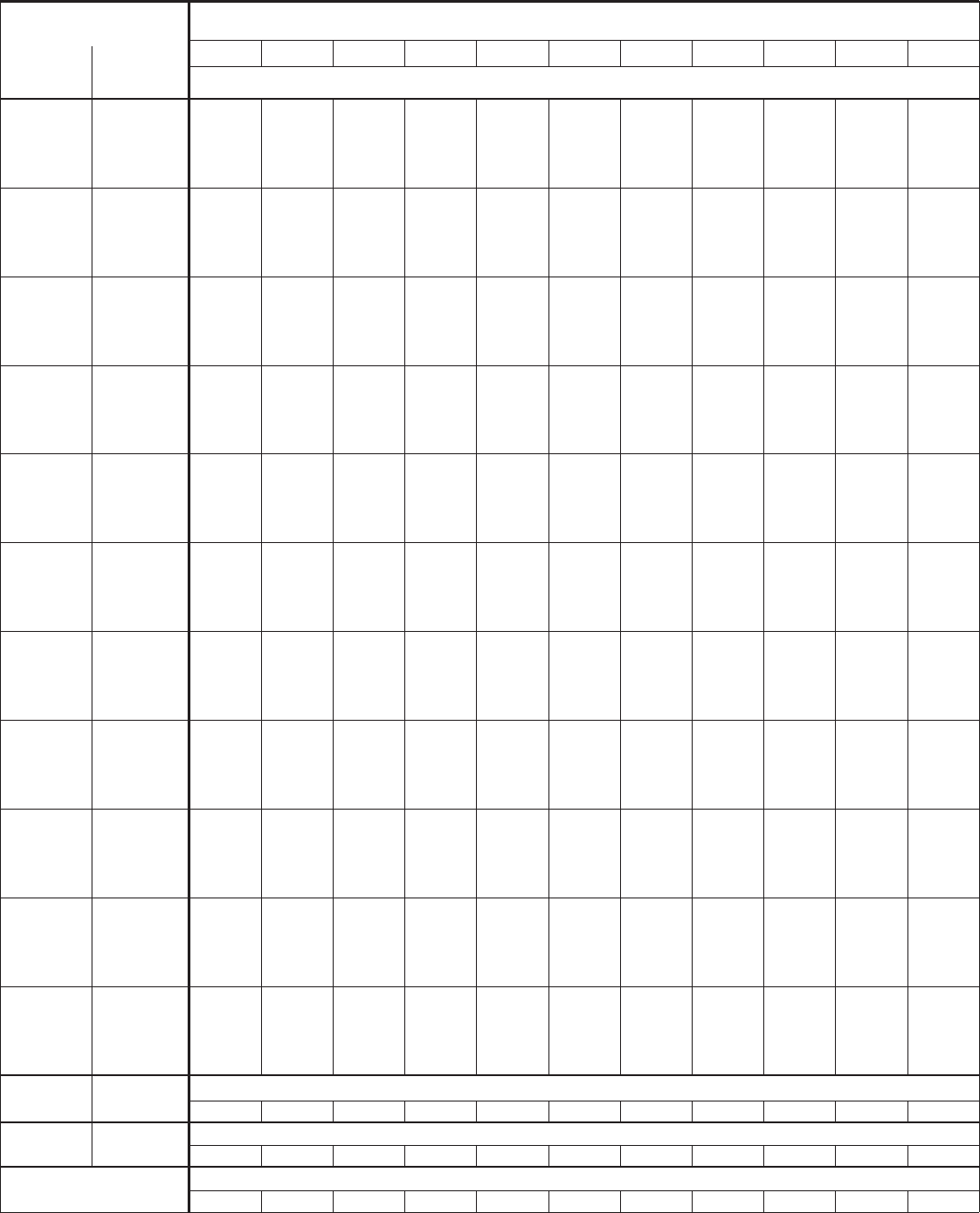

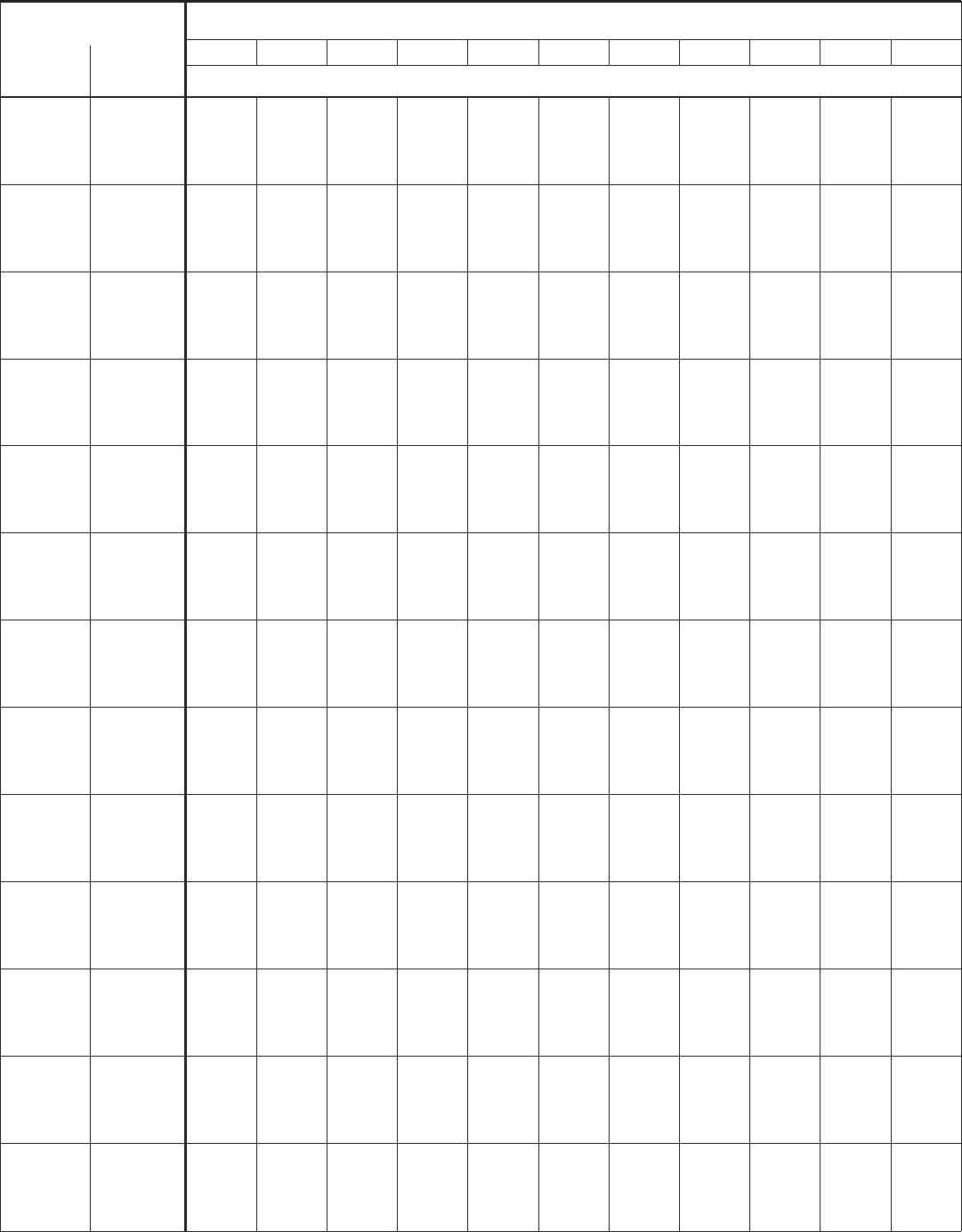

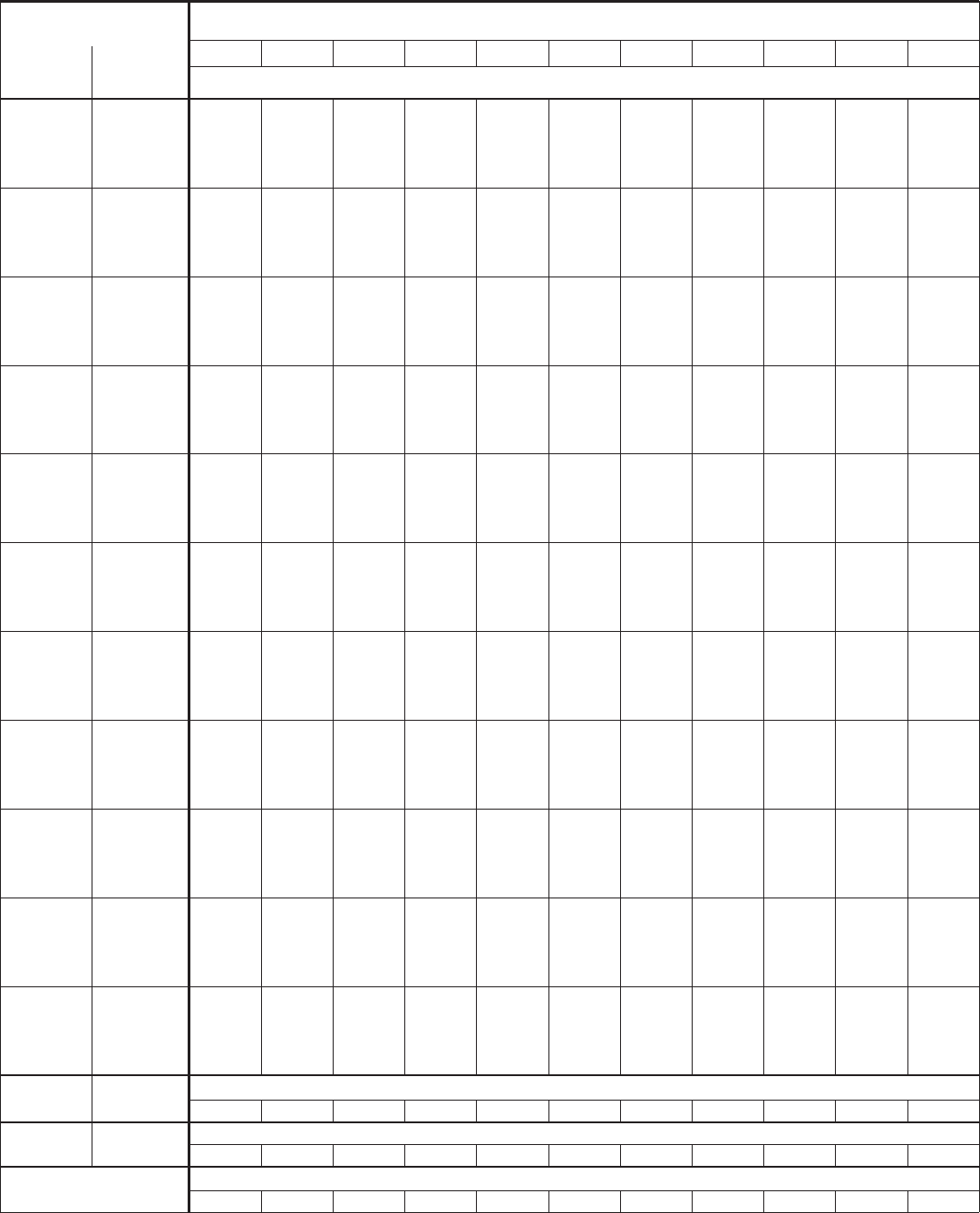

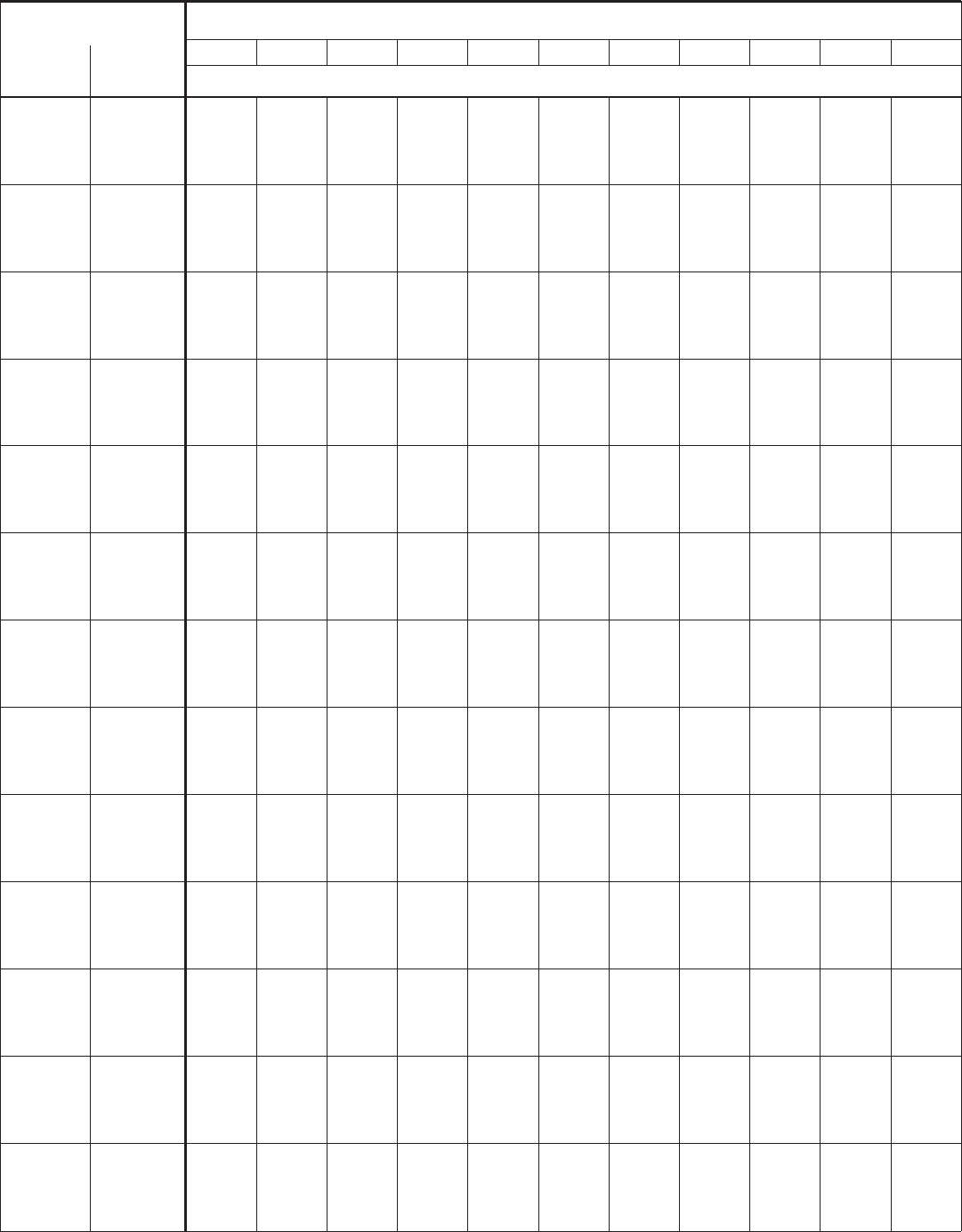

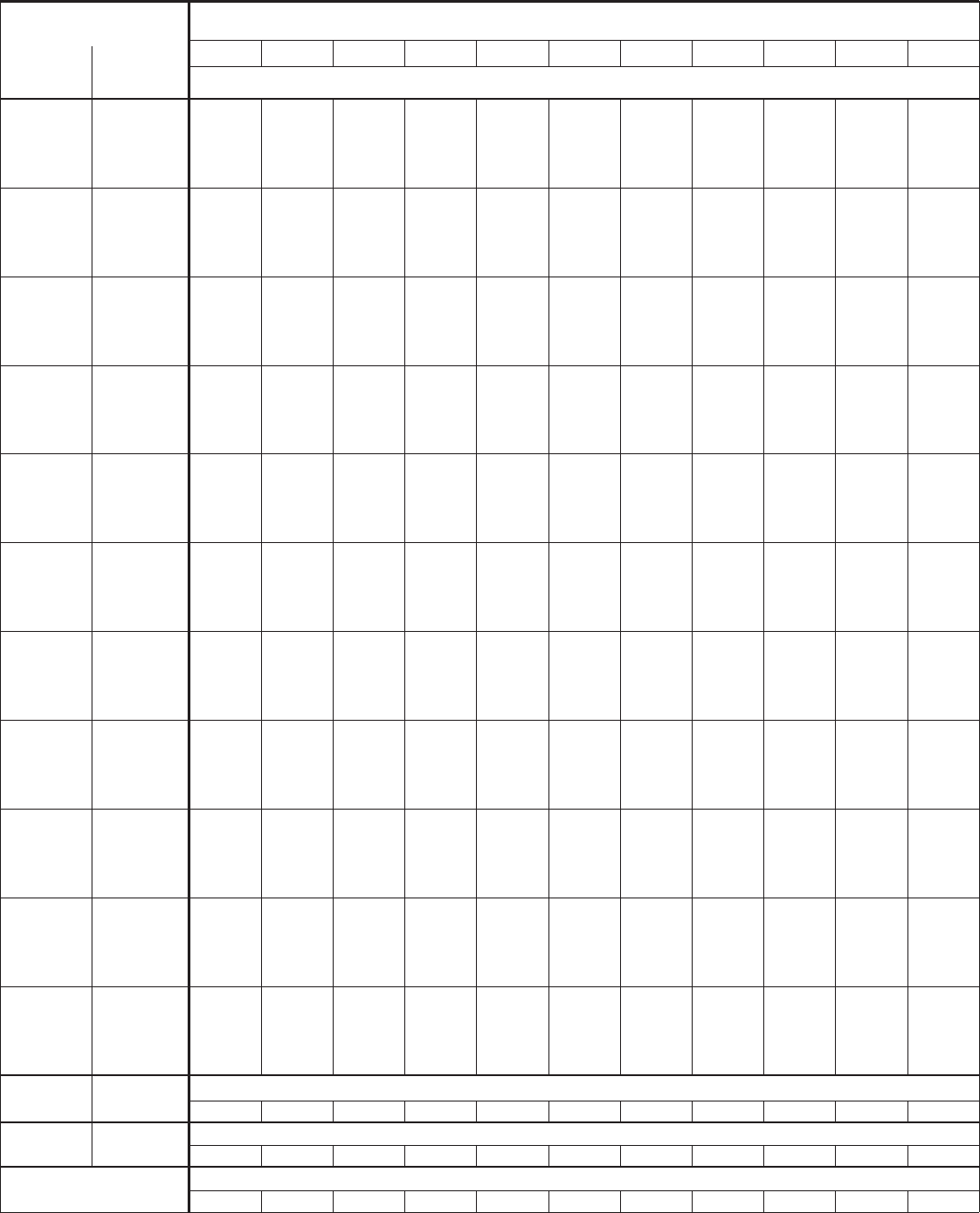

0.0627 of the excess over $279 plus:

279 658 16.70 16.60 16.50 16.50 16.40 16.30 16.30 16.20 16.10 16.10 16.00

0.0765 of the excess over $658 plus:

658 and over 40.40 40.40 40.30 40.20 40.20 40.10 40.00 40.00 39.90 39.80 39.80

21

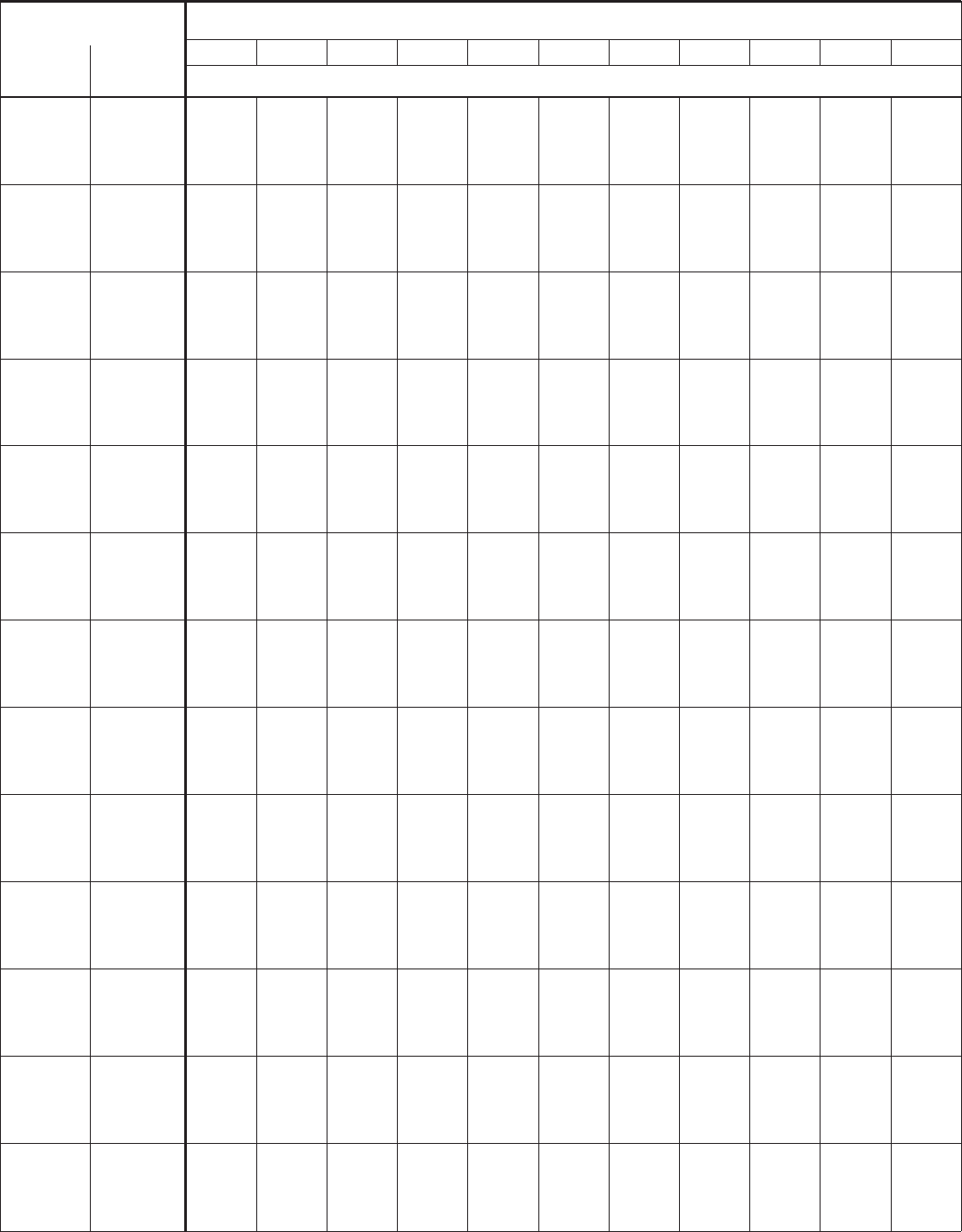

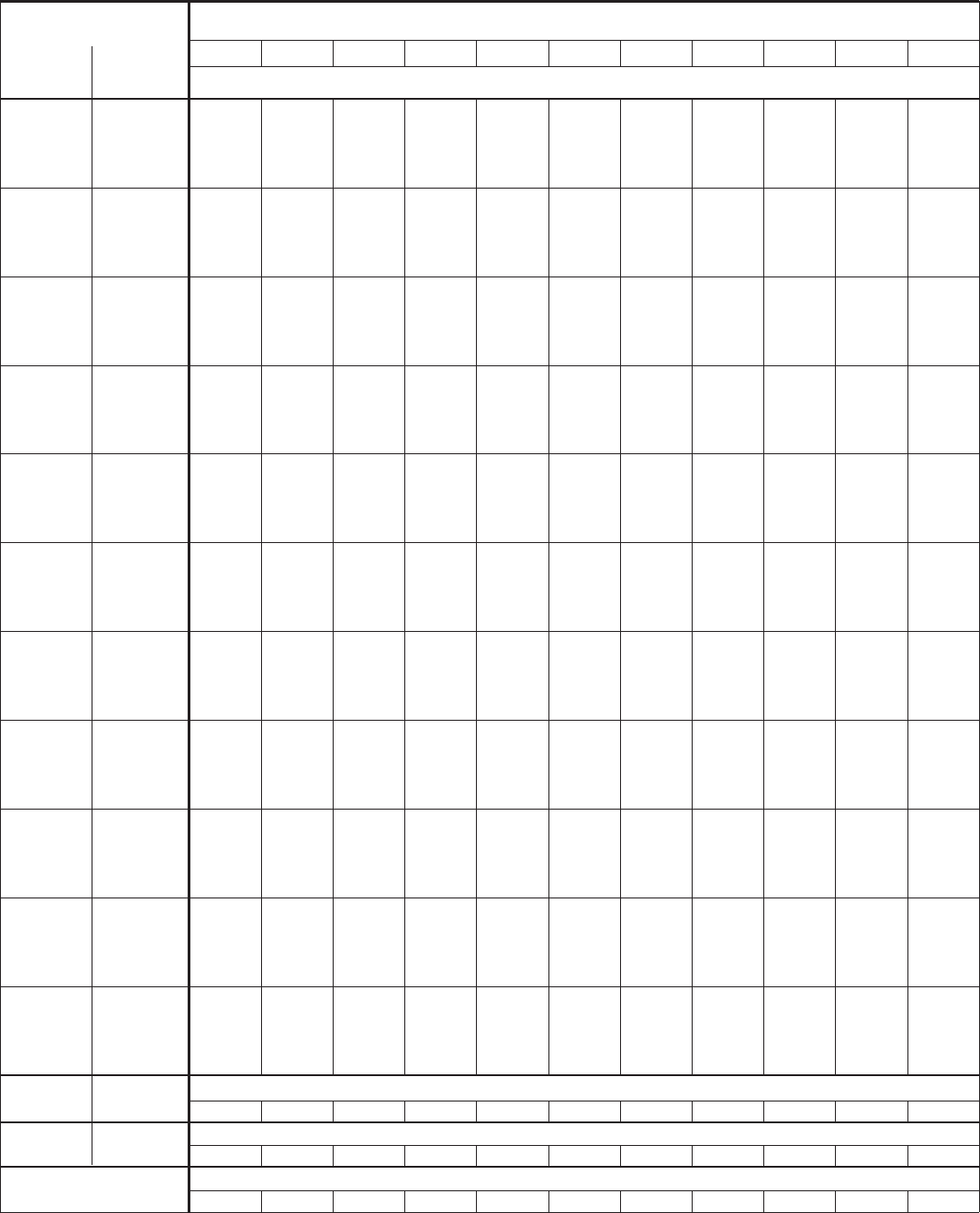

012345678910*

And the wages are:

At

least But

less than

And the number of withholding exemptions claimed is:

The amount of Wisconsin income tax to be withheld shall be:

* More than 10 exemptions: Reduce amount from 10 exemption column by .10 for each additional exemption claimed.

SINGLE PERSONS – DAILY AND MISCELLANEOUS PAYROLL PERIOD

$ $ $ $ $ $ $ $ $ $ $

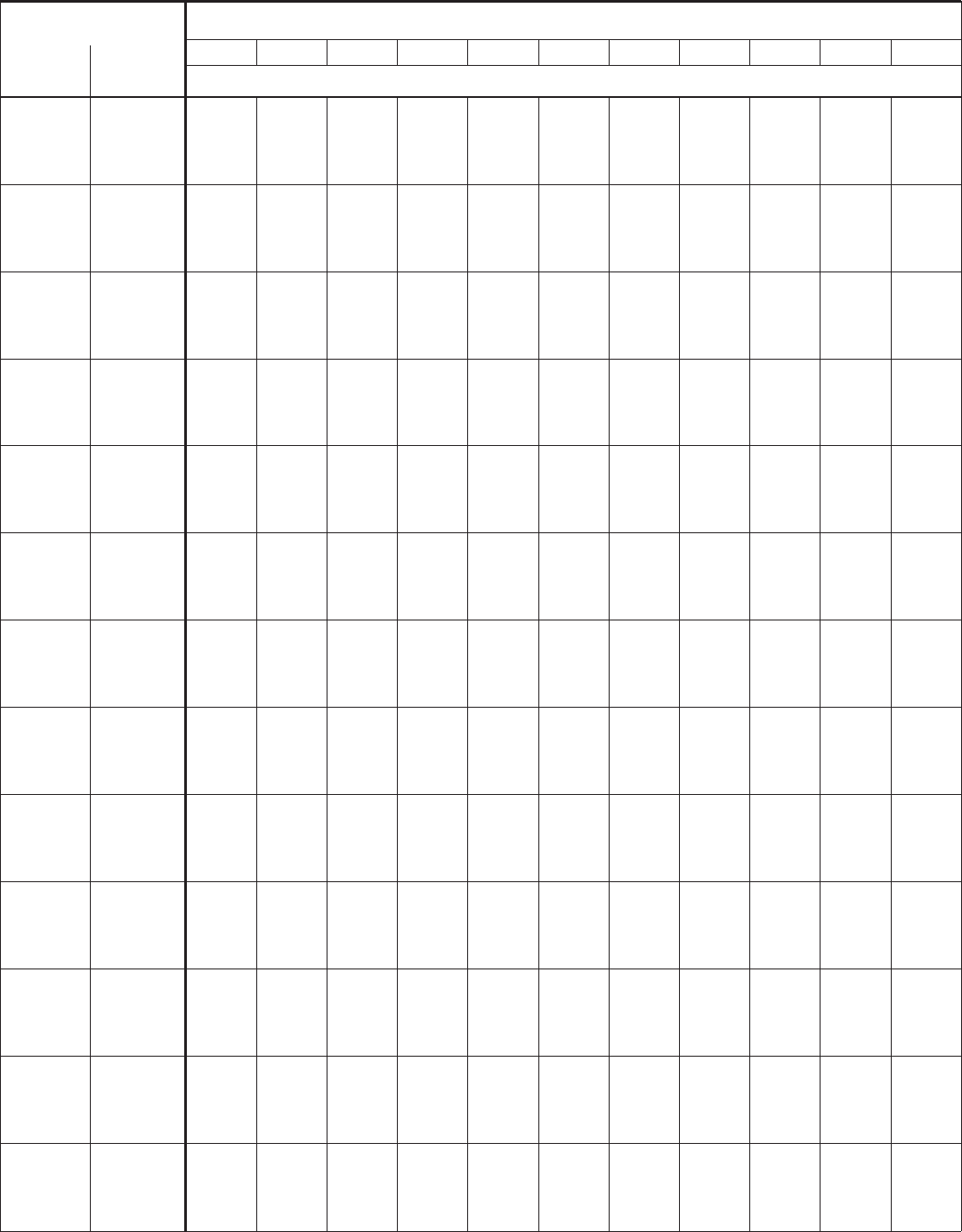

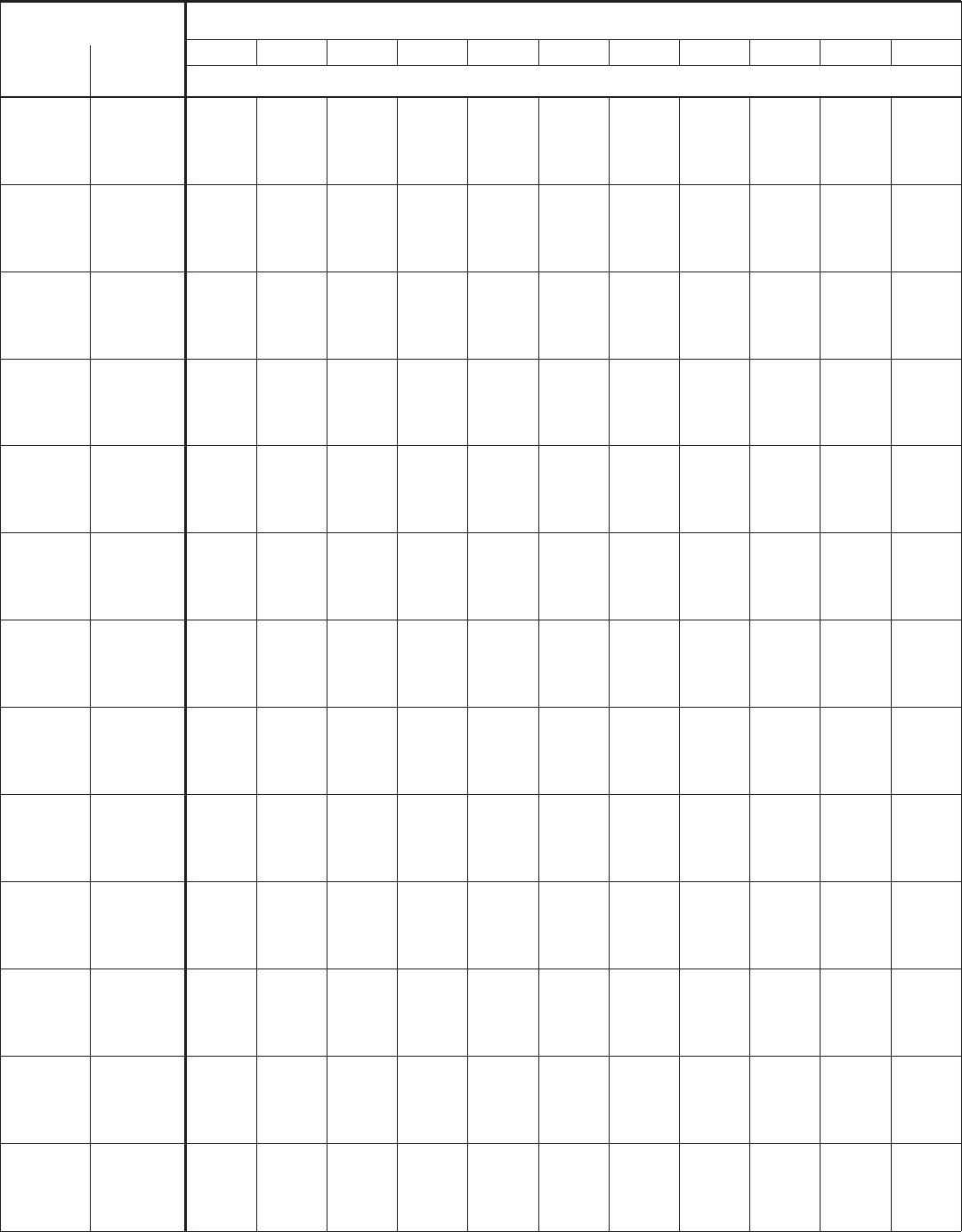

0 13 0 0 0 0 0 0 0 0 0 0 0

13 18 0

18 23 0

23 28 .20 .10 .10

28 33 .40 .30 .30 .20 .20 .10 .10 .10

33 38 .60 .50 .50 .40 .40 .30 .30 .30 .20 .20 .10

38 43 .80 .70 .70 .60 .60 .50 .50 .50 .40 .40 .30

43 48 1.00 .90 .90 .80 .80 .70 .70 .70 .60 .60 .50

48 53 1.20 1.10 1.10 1.00 1.00 .90 .90 .90 .80 .80 .70

53 58 1.40 1.40 1.30 1.20 1.20 1.10 1.10 1.10 1.00 1.00 .90

58 63 1.70 1.70 1.60 1.60 1.50 1.40 1.40 1.30 1.20 1.20 1.10

63 68 2.10 2.00 2.00 1.90 1.80 1.80 1.70 1.60 1.60 1.50 1.50

68 73 2.40 2.40 2.30 2.30 2.20 2.10 2.10 2.00 1.90 1.90 1.80

73 78 2.80 2.70 2.70 2.60 2.50 2.50 2.40 2.30 2.30 2.20 2.20

78 83 3.20 3.10 3.00 3.00 2.90 2.80 2.80 2.70 2.60 2.60 2.50

83 88 3.50 3.50 3.40 3.30 3.30 3.20 3.10 3.10 3.00 2.90 2.90

88 93 3.90 3.80 3.80 3.70 3.60 3.60 3.50 3.40 3.40 3.30 3.20

93 98 4.30 4.20 4.20 4.10 4.00 3.90 3.90 3.80 3.70 3.70 3.60

98 103 4.70 4.60 4.50 4.50 4.40 4.30 4.30 4.20 4.10 4.00 4.00

103 108 5.00 5.00 4.90 4.80 4.80 4.70 4.60 4.60 4.50 4.40 4.40

108 113 5.40 5.40 5.30 5.20 5.10 5.10 5.00 4.90 4.90 4.80 4.70

113 118 5.80 5.70 5.70 5.60 5.50 5.50 5.40 5.30 5.20 5.20 5.10

118 123 6.20 6.10 6.00 6.00 5.90 5.80 5.80 5.70 5.60 5.60 5.50

123 128 6.50 6.50 6.40 6.30 6.30 6.20 6.10 6.10 6.00 5.90 5.90

128 133 6.90 6.90 6.80 6.70 6.60 6.60 6.50 6.40 6.40 6.30 6.20

133 138 7.30 7.20 7.20 7.10 7.00 7.00 6.90 6.80 6.80 6.70 6.60

138 143 7.70 7.60 7.50 7.50 7.40 7.30 7.30 7.20 7.10 7.10 7.00

143 148 8.10 8.00 7.90 7.80 7.80 7.70 7.60 7.60 7.50 7.40 7.40

148 153 8.40 8.40 8.30 8.20 8.20 8.10 8.00 7.90 7.90 7.80 7.70

153 158 8.80 8.70 8.70 8.60 8.50 8.50 8.40 8.30 8.30 8.20 8.10

158 163 9.20 9.10 9.00 9.00 8.90 8.80 8.80 8.70 8.60 8.60 8.50

163 168 9.60 9.50 9.40 9.40 9.30 9.20 9.10 9.10 9.00 8.90 8.90

168 173 9.90 9.80 9.70 9.70 9.60 9.50 9.50 9.40 9.30 9.30 9.20

173 178 10.20 10.10 10.10 10.00 9.90 9.90 9.80 9.70 9.60 9.60 9.50

178 183 10.50 10.40 10.40 10.30 10.20 10.20 10.10 10.00 10.00 9.90 9.80

183 188 10.80 10.80 10.70 10.60 10.50 10.50 10.40 10.30 10.30 10.20 10.10

188 193 11.10 11.10 11.00 10.90 10.90 10.80 10.70 10.70 10.60 10.50 10.50

193 198 11.50 11.40 11.30 11.20 11.20 11.10 11.00 11.00 10.90 10.80 10.80

198 203 11.80 11.70 11.60 11.60 11.50 11.40 11.40 11.30 11.20 11.10 11.10

203 208 12.10 12.00 11.90 11.90 11.80 11.70 11.70 11.60 11.50 11.50 11.40

208 213 12.40 12.30 12.30 12.20 12.10 12.00 12.00 11.90 11.80 11.80 11.70

213 218 12.70 12.60 12.60 12.50 12.40 12.40 12.30 12.20 12.20 12.10 12.00

218 223 13.00 12.90 12.90 12.80 12.70 12.70 12.60 12.50 12.50 12.40 12.30