1 Jukebox Case AV100 Presentation

User Manual: Jukebox Case AV100

Open the PDF directly: View PDF ![]() .

.

Page Count: 83

- Slide Number 1

- Conference Materials

- Continuing Education Credits

- Tips for Optimal Quality

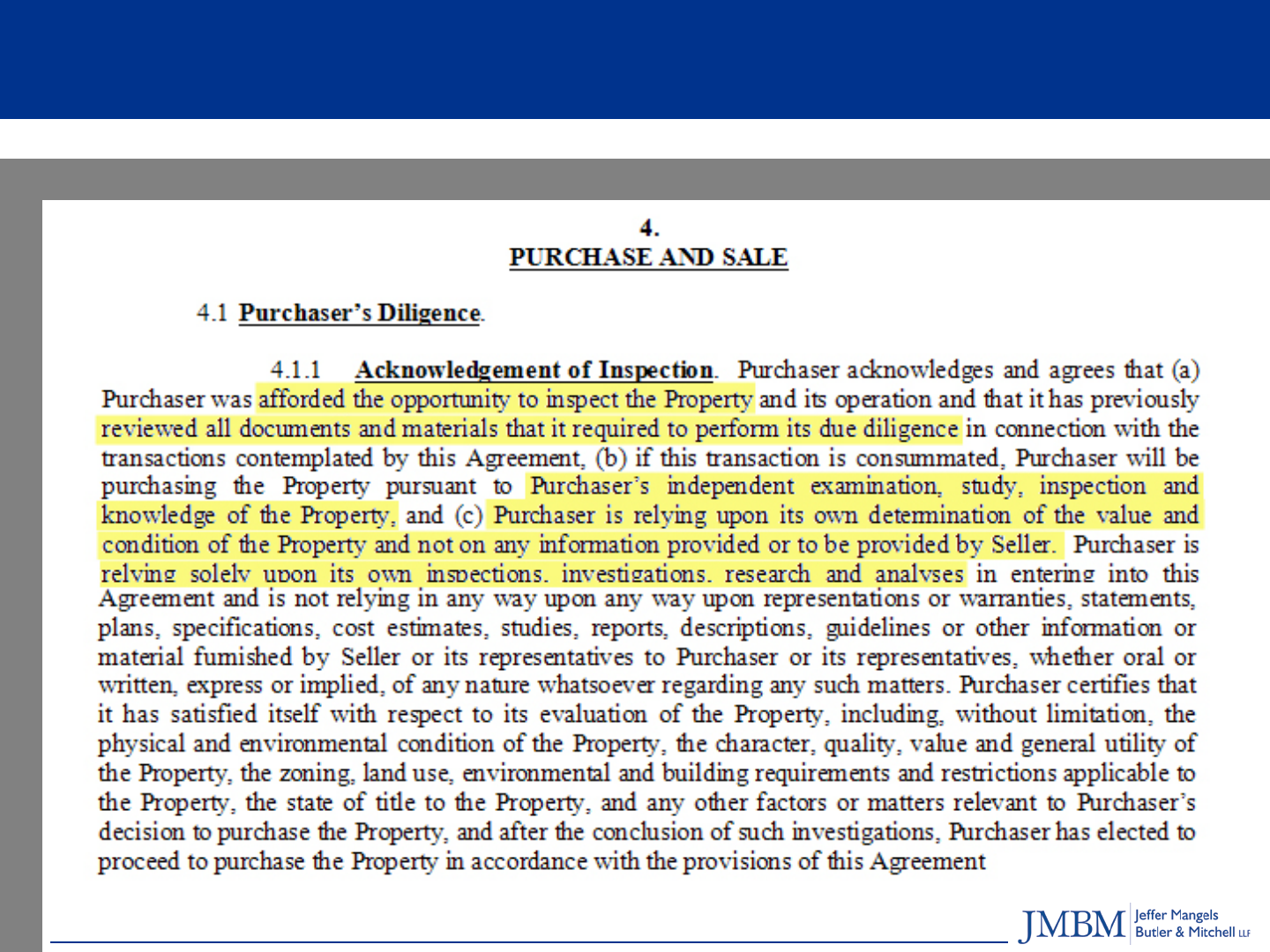

- Representations and Warranties in Commercial Real Estate Sales Contracts

- Critical Issues for Buyer

- Due Diligence

- Due Diligence (Cont’d)

- Due Diligence Items

- Due Diligence Items (Cont’d)

- Due Diligence Items (Cont’d)

- AS-IS Language

- Representation and Warranties

- Representation and Warranties(Cont’d)

- Knowledge Standards

- Seller Liability Issues

- Remedies/Survival

- Conclusion

- Liner Grode Stein Yankelevitz Sunshine Regenstreif & Taylor LLP

- Representations and Warranties in Commercial Real Estate Sales Contracts

- Representations and Warranties from the Seller’s Perspective: You’ll Get Nothing and Like It!

- Representations and Warranties in General

- General Types of Real Estate Contract Representations and Warranties

- Status of the Seller Representations and Warranties (“R/W”)

- Status of the Seller Representations and Warranties

- Status of the Property Representations and Warranties

- Status of the Property Representations and Warranties

- Operation of the Property Representations and Warranties

- General Seller Warranty Limitations

- General Seller Warranty Limitations

- Seller Warranty Remedies Provisions

- Warranties and Representations: A Philosophy

- LARRY N. WOODARD Robbins, Salomon & Patt, Ltd.

- DISCLAIMER

- Slide Number 35

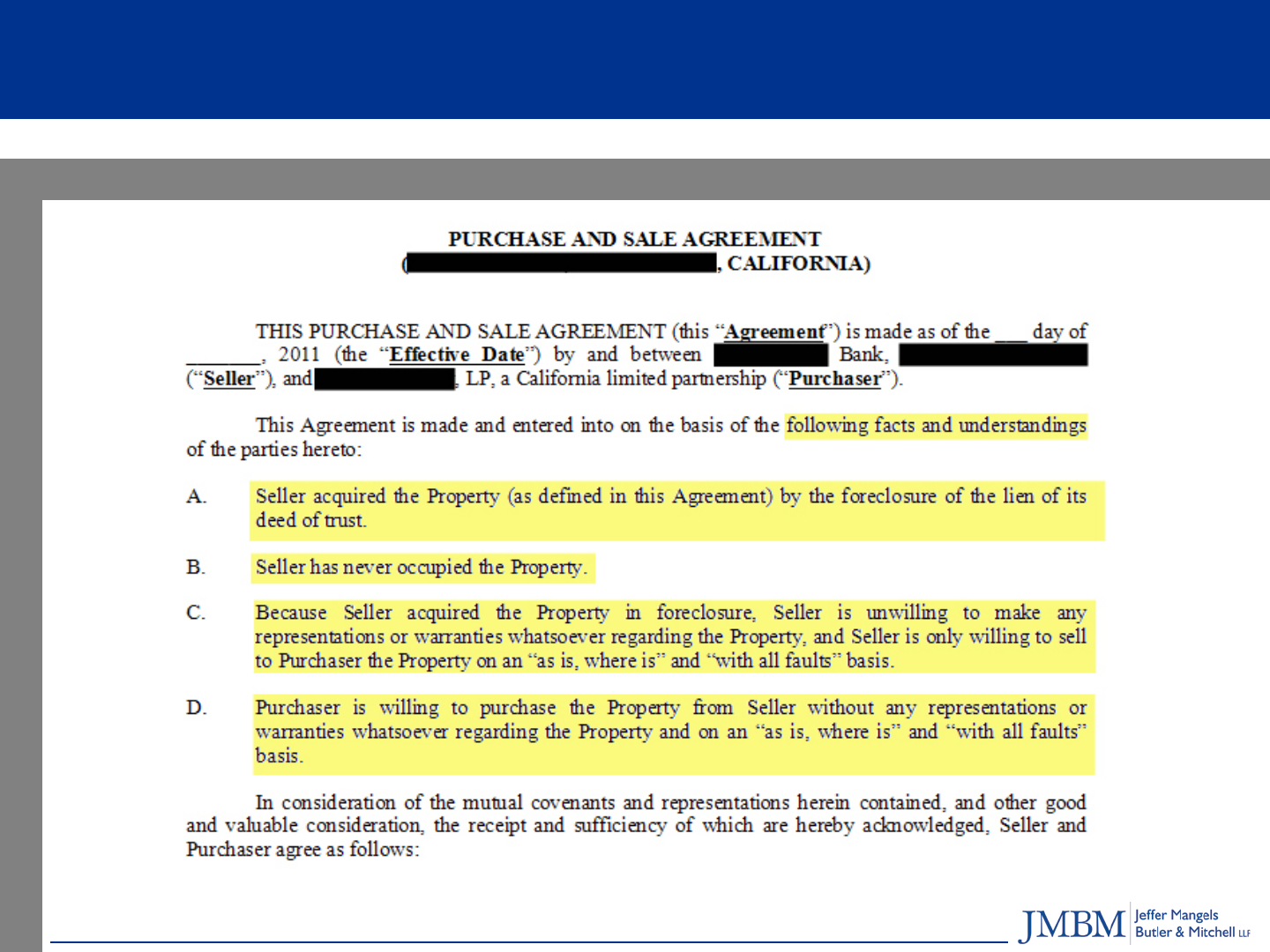

- Distressed Deals

- Distressed Deals

- Distressed Sale Risk Factors

- Distressed Sale Risk Factors

- Understanding the Seller's History

- What is the Loan History?

- How Was the Property Acquired?

- Property Management

- Type of Lender/Seller (Bank or Servicer?)

- Buyer Beware: Discounted Price = Risk

- Transactional Shifting of Risk of Unknowns

- Leases and Foreclosure Issues

- Buyer's Due Diligence

- Representations and Warranties

- Seller's Representations and Warranties

- Buyer's Wish List

- Buyer's Wish List

- Expanding Seller's Representations

- Limitations on Recourse

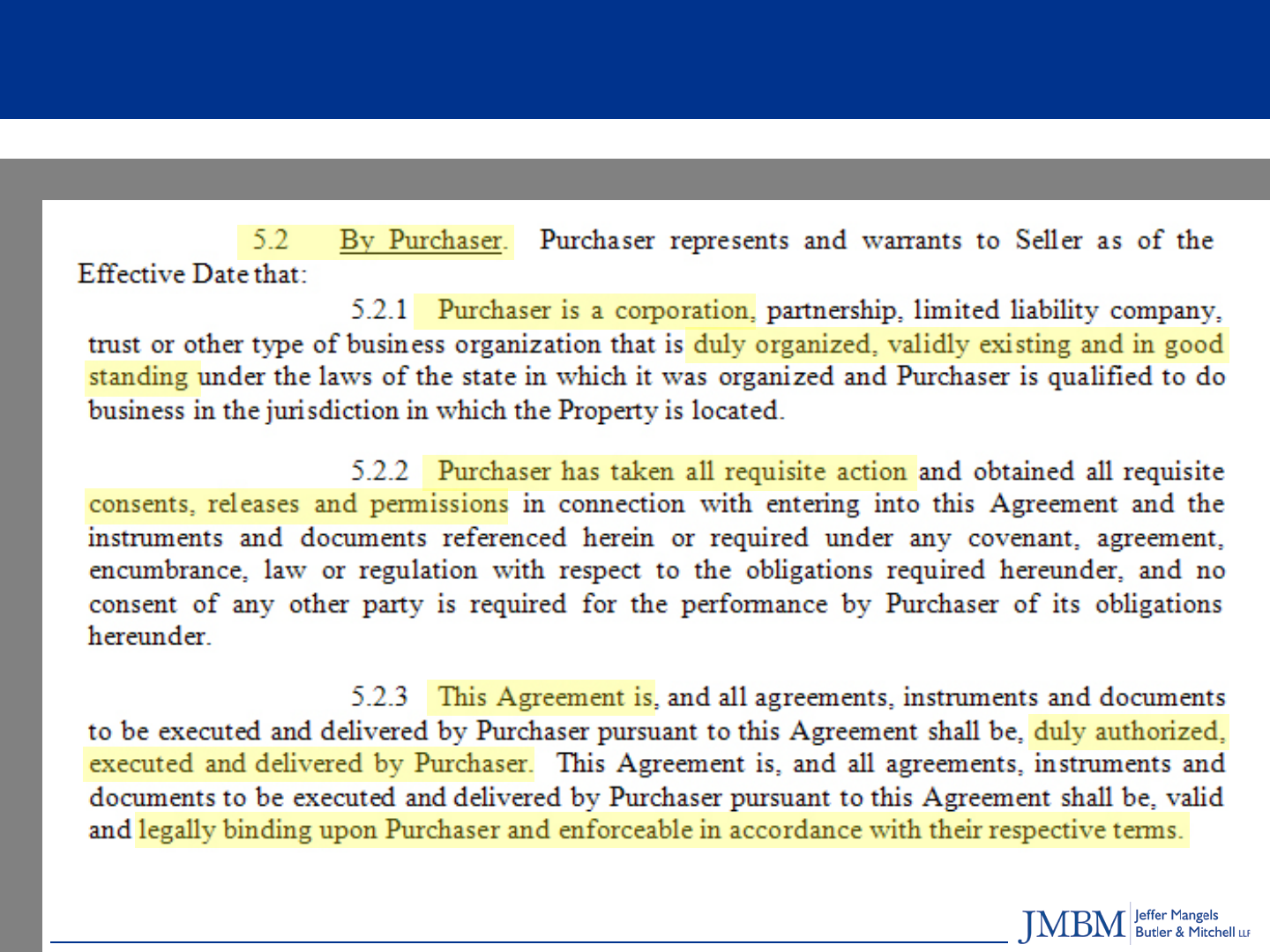

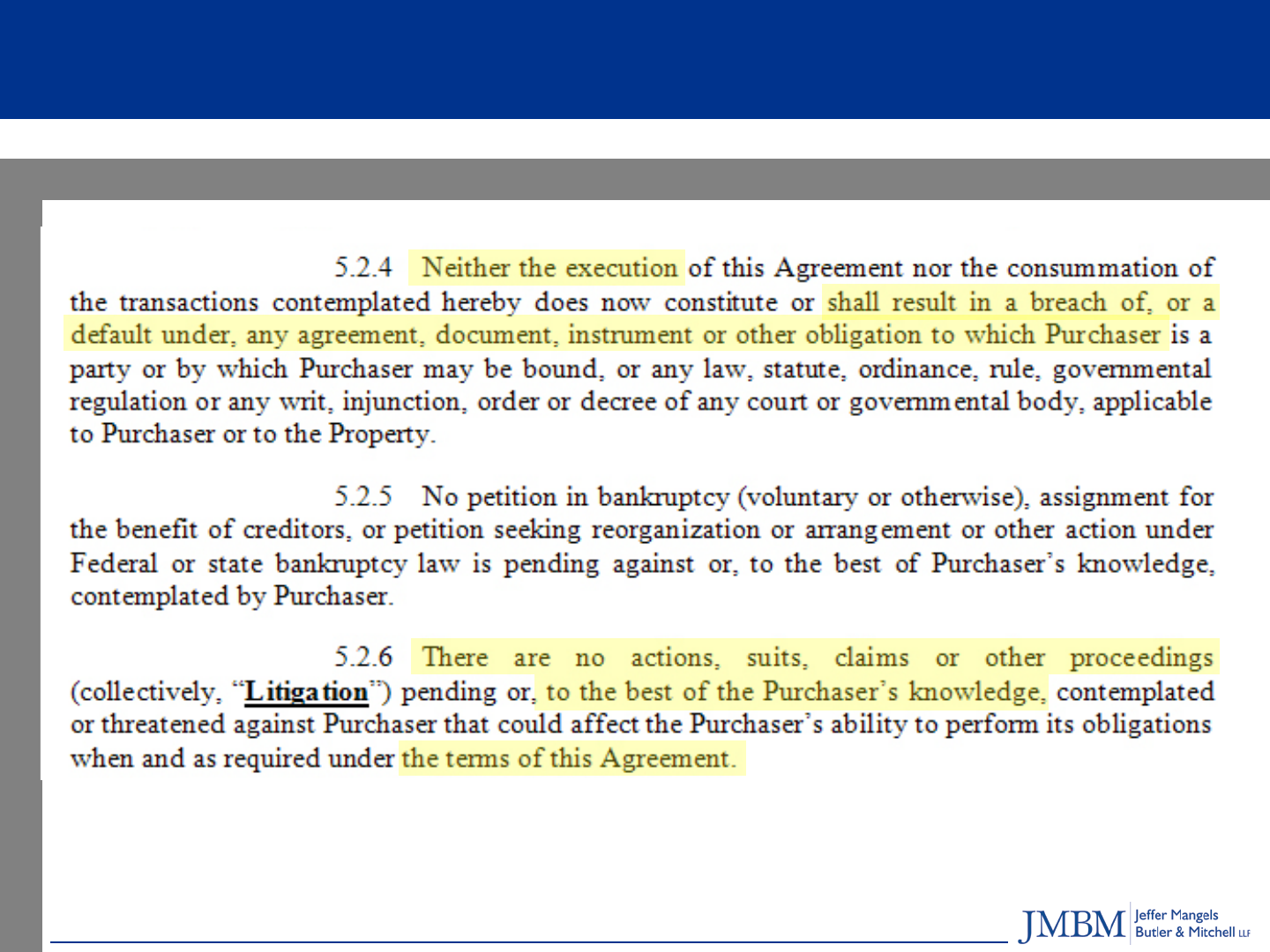

- Slide Number 55

- Slide Number 56

- Slide Number 57

- Slide Number 58

- Slide Number 59

- Slide Number 60

- Slide Number 61

- Slide Number 62

- Slide Number 63

- Slide Number 64

- Slide Number 65

- Slide Number 66

- Slide Number 67

- Slide Number 68

- Slide Number 69

- Slide Number 70

- Slide Number 71

- Slide Number 72

- Slide Number 73

- Slide Number 74

- Slide Number 75

- Slide Number 76

- Slide Number 77

- Slide Number 78

- Slide Number 79

- Slide Number 80

- Slide Number 81

- Slide Number 82

- Jeffer Mangels Butler & Mitchell LLP

- Slide Number 84

- Slide Number 85

- Slide Number 86

Representations and Warranties in

Commercial Real Estate Sales Contracts

Strategies for Buyers and Sellers Negotiating Agreements of Sale

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

WEDNESDAY, FEBRUARY 15, 2012

Presenting a live 90-minute webinar with interactive Q&A

Mitchell C. Regenstreif, Founding Partner, Liner Grode Stein Yankelevitz Sunshine Regenstreif & Taylor, Los Angeles

Larry N. Woodard, Shareholder, Robbins Salomon & Patt, Chicago

David P. Waite, Partner, Jeffer Mangels Butler & Mitchell, Los Angeles

Conference Materials

If you have not printed the conference materials for this program, please

complete the following steps:

•Click on the + sign next to “Conference Materials” in the middle of the left-

hand column on your screen.

•Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program.

•Double click on the PDF and a separate page will open.

•Print the slides by clicking on the printer icon.

Continuing Education Credits

For CLE purposes, please let us know how many people are listening at your

location by completing each of the following steps:

•Close the notification box

•In the chat box, type (1) your company name and (2) the number of

attendees at your location

•Click the SEND button beside the box

FOR LIVE EVENT ONLY

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality of

your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory and you are listening via your computer

speakers, you may listen via the phone: dial 1-866-871-8924 and enter your

PIN -when prompted. Otherwise, please send us a chat or e-mail

sound@straffordpub.com immediately so we can address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

5

Presented by:

Mitchell C. Regenstreif

Liner Grode LLP

310.500.3570

mregenstreif@linerlaw.com

Strategies for Buyers and Sellers

when Negotiating Agreements of Sale

Important Topics for Buyers

when Negotiating a Purchase and Sale Agreement

Representations and Warranties in

Commercial Real Estate Sales Contracts

6

Critical Issues for Buyer

Negotiating the Purchase and Sale

Agreement can be expensive and time

consuming

Outside pressures and costs can limit review

and negotiation

Most current form contracts favor Seller

Focus on fundamental issues to Buyer

The Market Dictates/Limits What is Realistic

for Well-represented Sellers and Buyers!!

7

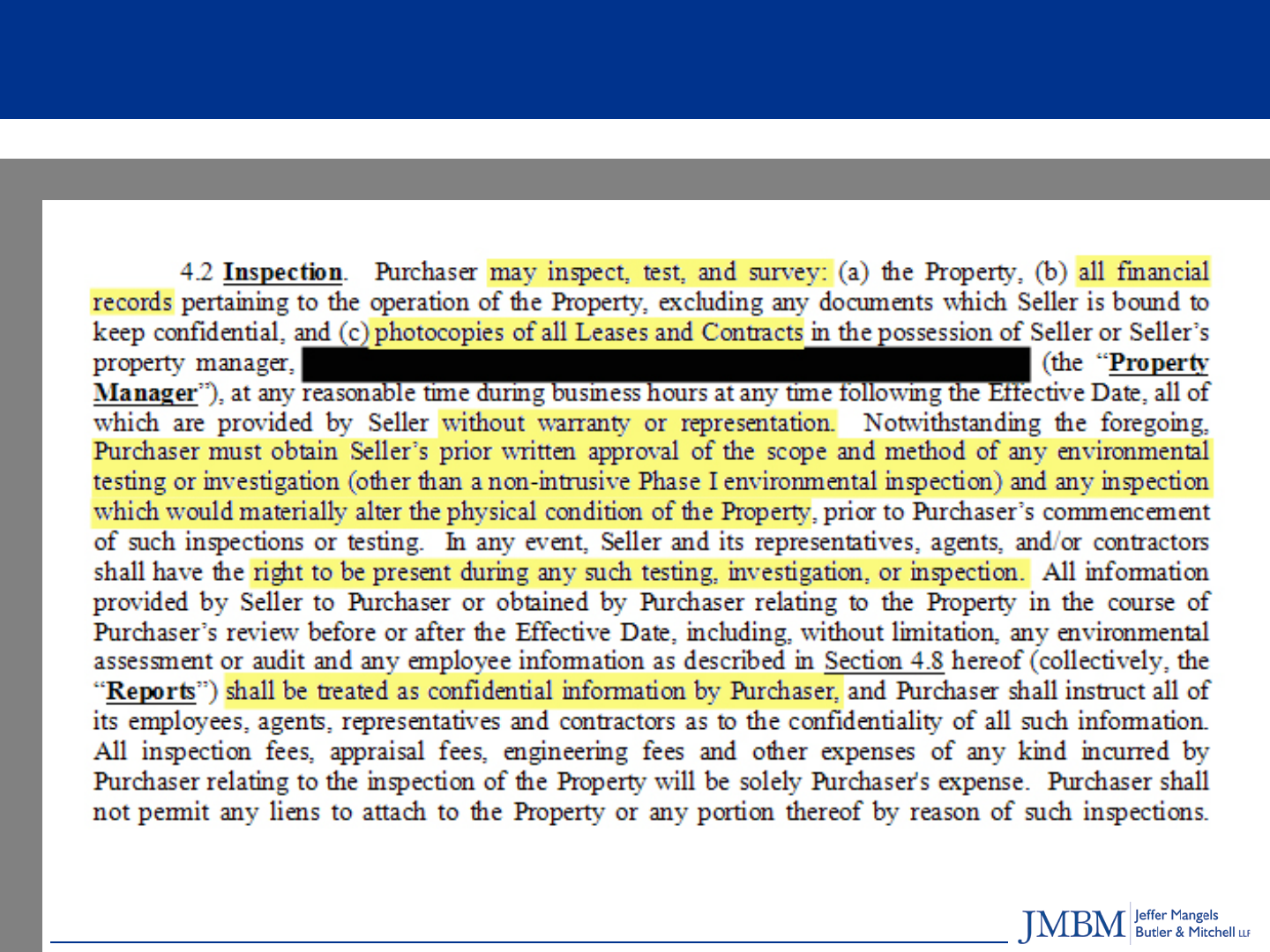

Due Diligence

Buyer is almost always entitled to perform

due diligence investigation of the property

Differing Requirements for Property Types:

Investment Property Types

Office, Industrial, Retail, Multi-family, Mixed Use,

Development Property

Special Situations

Brownfields

8

Due Diligence (Cont’d)

Timing and Scope of Due Diligence

Due Diligence Period

Land Use Conditions

Intrusive Testing

Limitations on Contract Representations

based upon Findings of Buyer’s Due

Diligence

9

Due Diligence Items

Materials from Seller in Seller’s possession

Books and records

Title and Survey

Plans and Specifications

Agreements and other materials outside of

public records

Permits, licenses and approvals

10

Due Diligence Items (Cont’d)

Violations/emergency repairs

Threatened or pending litigation

Including condemnation proceedings

Proposed assessments

Engineering reports

Rent roll and arrears report

Leases and lease abstracts

Environmental reports and assessments

11

Due Diligence Items (Cont’d)

Physical site inspection reports

Zoning/land use reports

Insurance

Existing financing documents

12

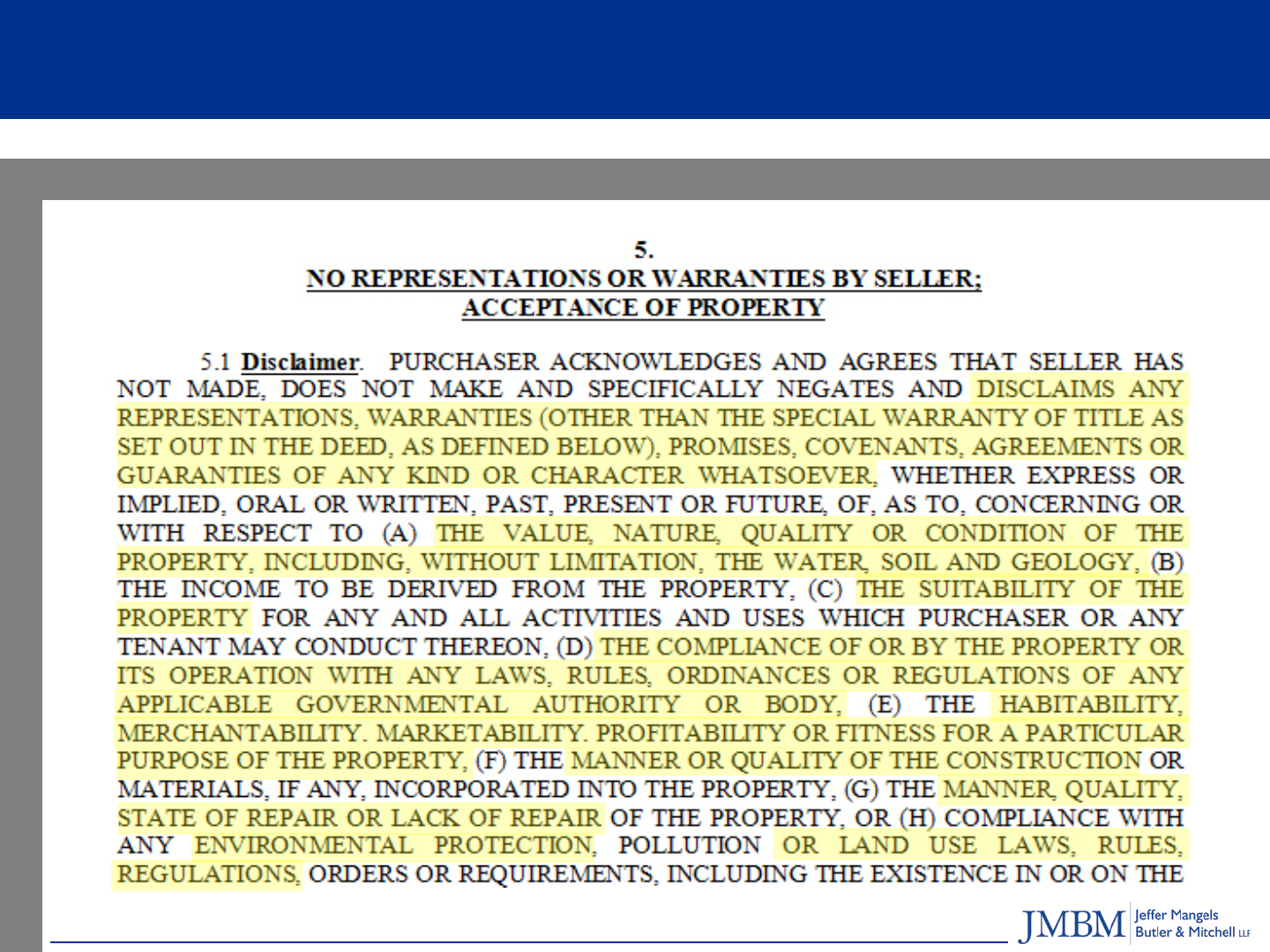

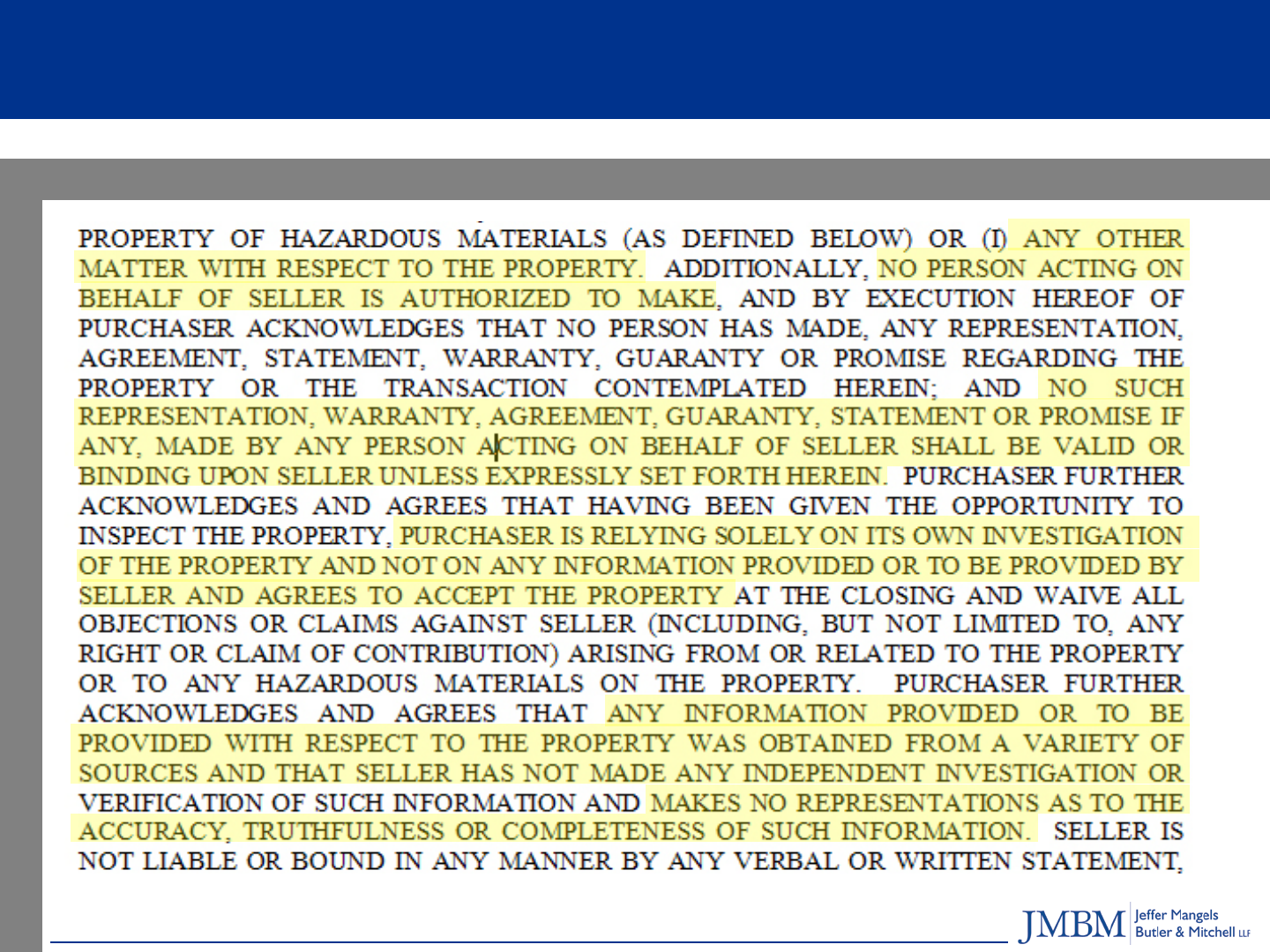

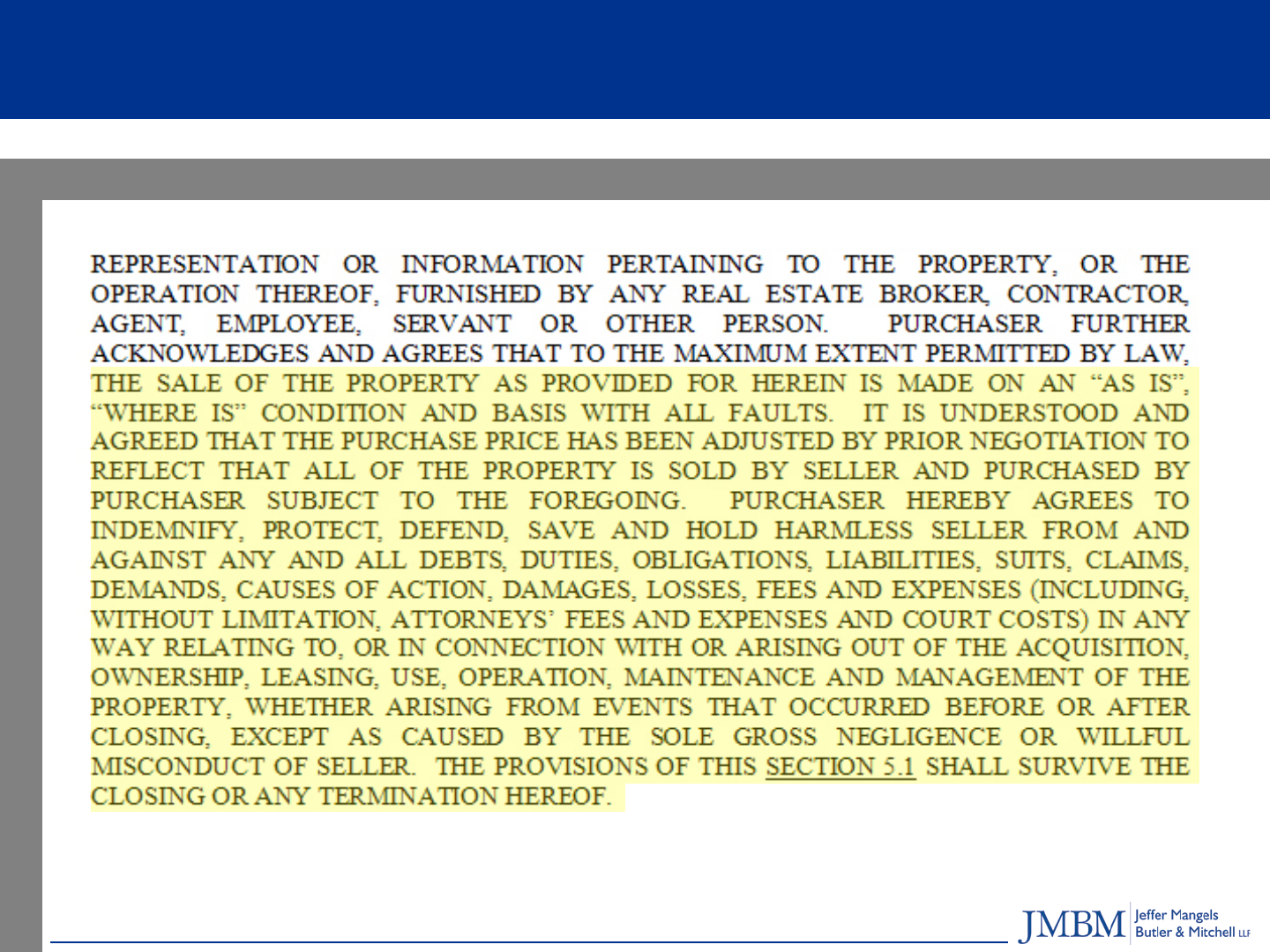

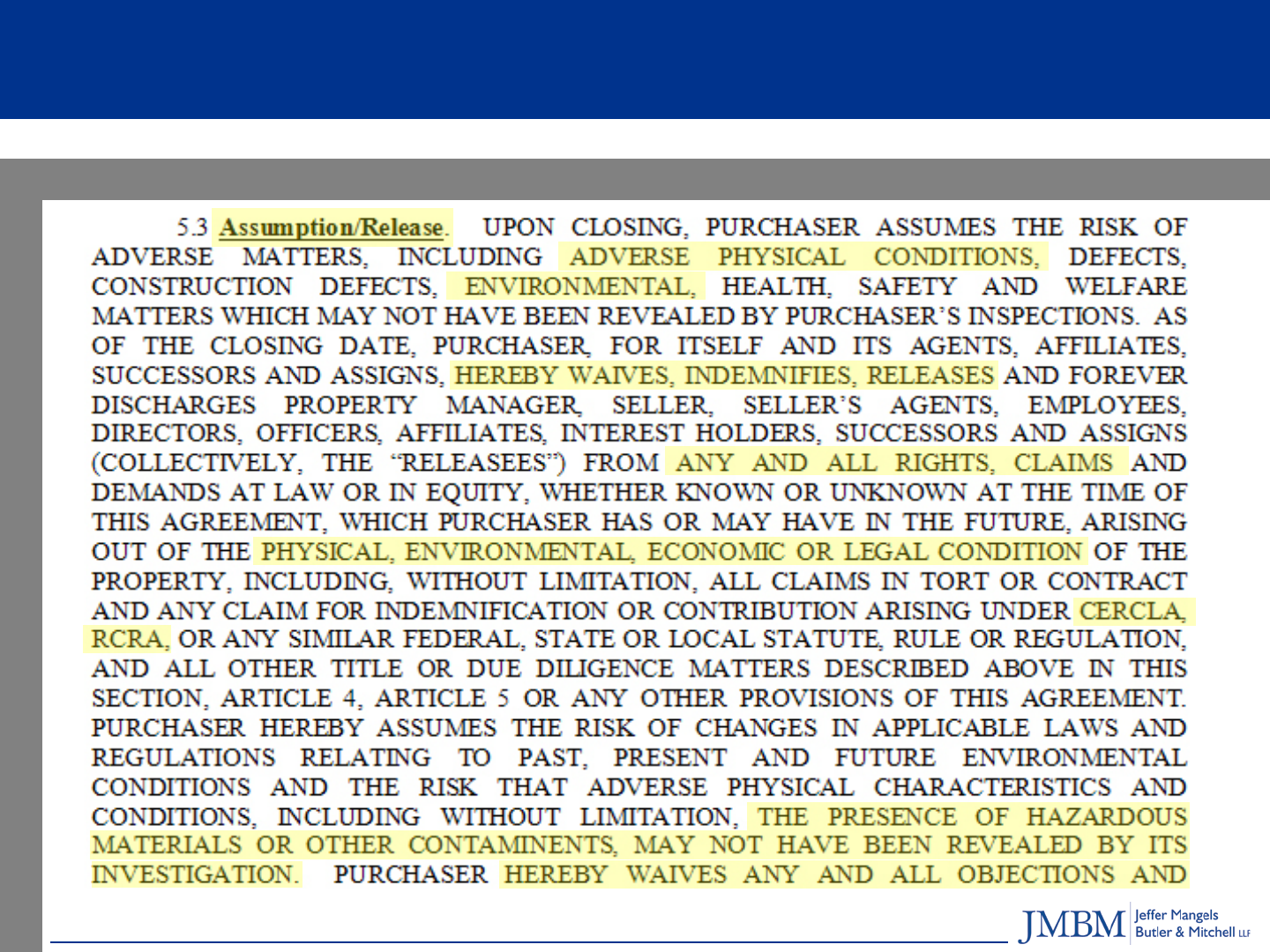

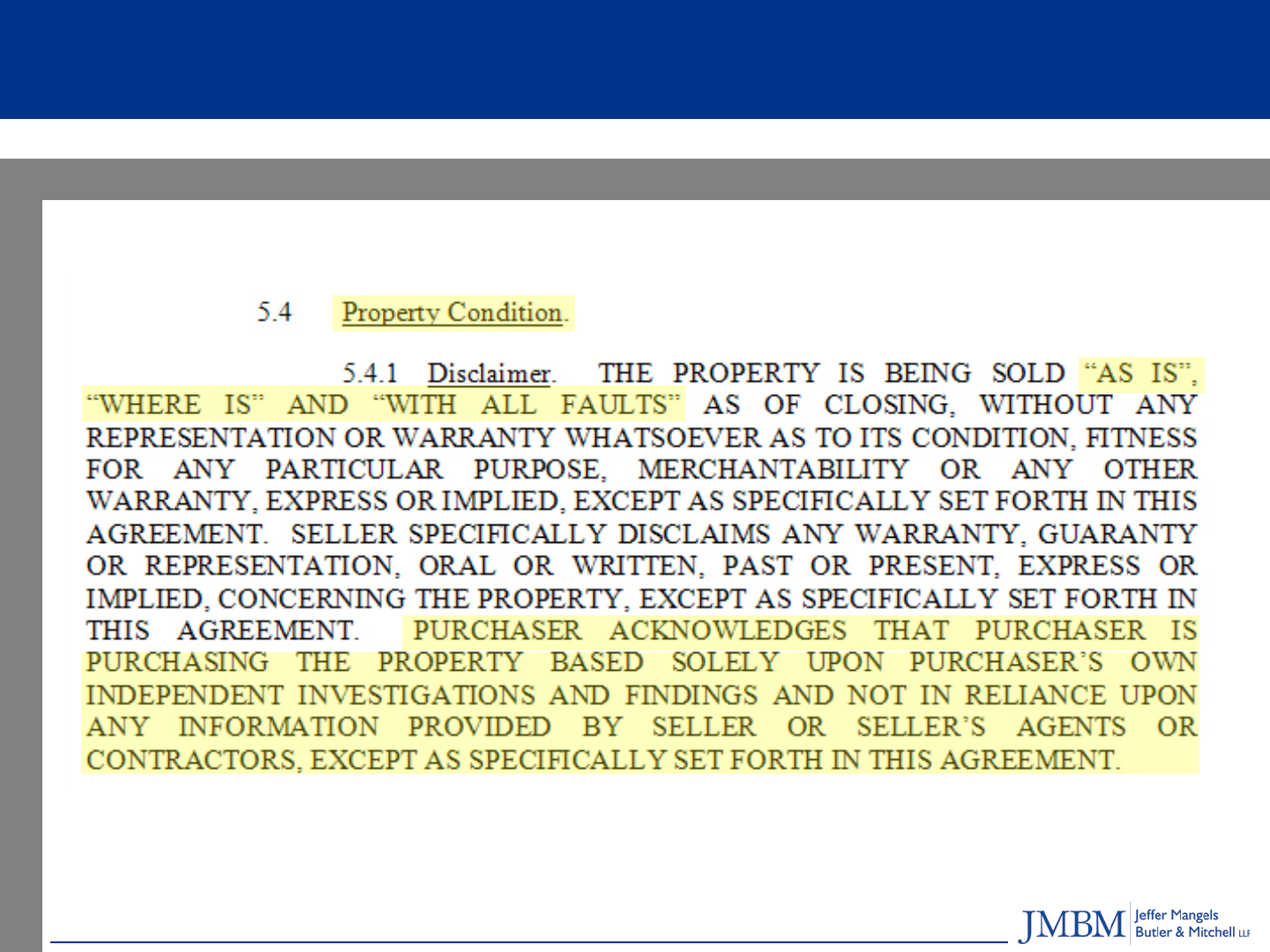

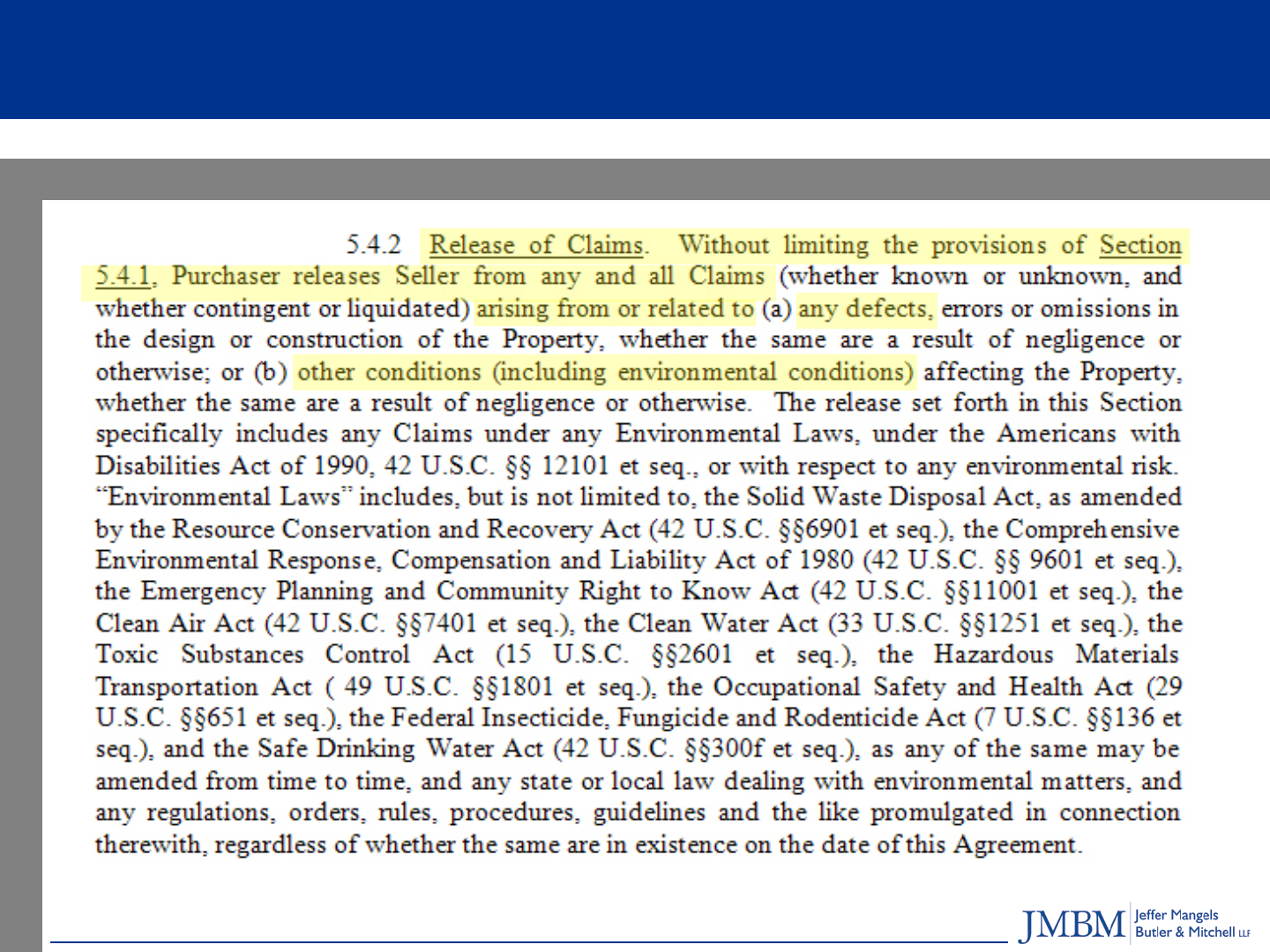

AS-IS Language

Typically comprehensive provision

(“disclaimer”)

Risk Shifting to Buyer

Exceptions to As-Is Language

“Except as expressly otherwise provided in this

Agreement,…”

Trade for longer due diligence period

13

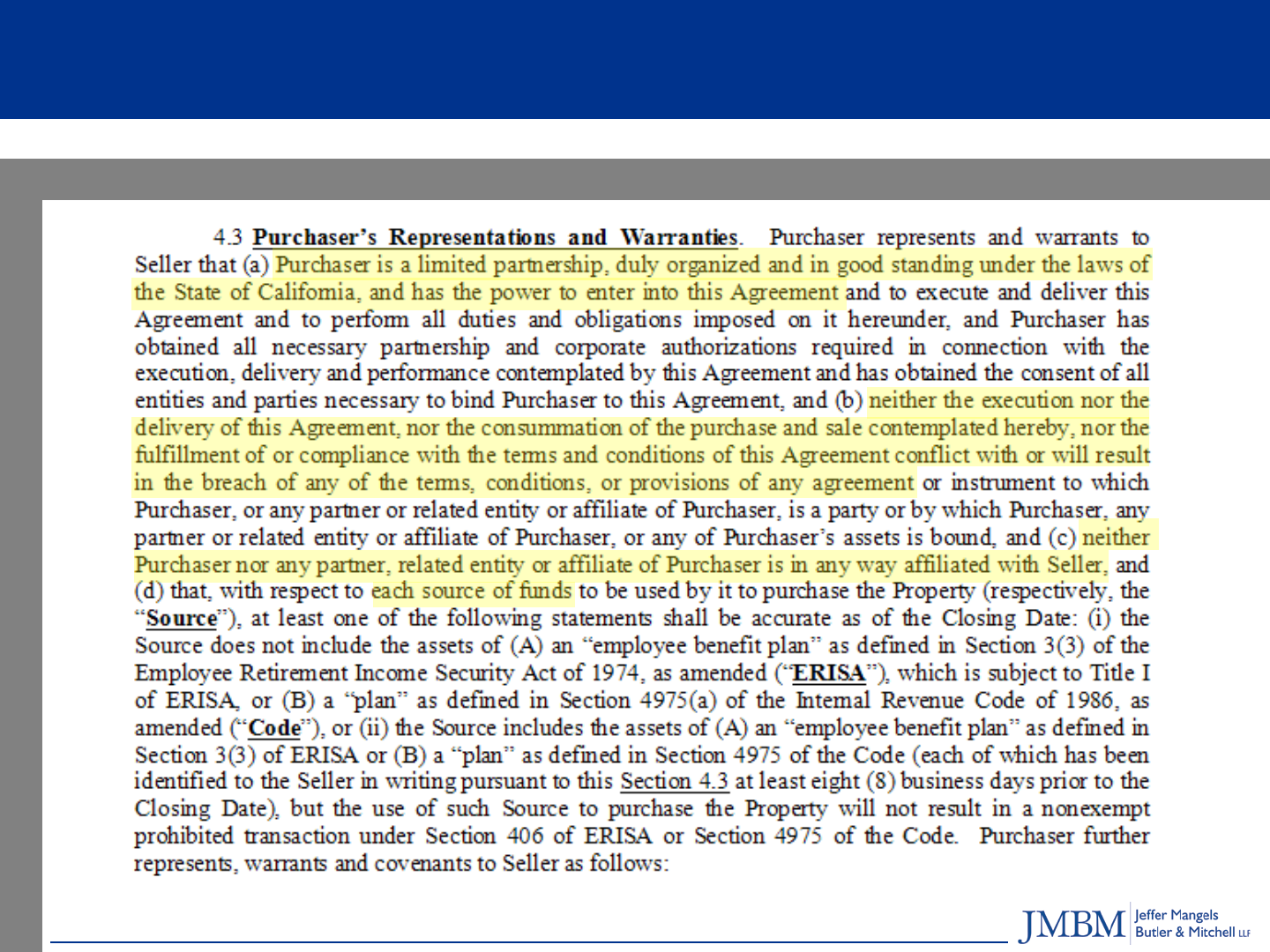

Representation and Warranties

Usually heavily negotiated

Buyer wants Extensive Reps (as much as

Buyer can get)

All material information

Knowledge vs. absolute reps

Implied reps in Deed, Closing Documents

Agree when negotiating contract

Protections under law

Fraud, concealment

Remedies

14

Representation and Warranties(Cont’d)

Seller wants Limited (as narrow as possible)

Shift responsibility to Buyer

No liability for matters discoverable during due

diligence

Duration and other limitations on remedies

See sample provisions

15

Knowledge Standards

“Knowledge” and qualifications

Various Standards

Knowledge-of whom?

Investigation/inquiry?

Knowledge about due diligence materials?

Extensively negotiated

16

Seller Liability Issues

Seller as “special purpose entity” (“SPE”)

Exculpation provisions

Release; indemnity

Forms of security

Escrow Holdback

Common for environmental issues

Letters of credit

Personal Guaranties

Liquidity is always the issue

17

Remedies/Survival

Merge with deed or survive closing?

Failure of Condition vs. Default…

What are Buyer’s remedies/options?

Survival Period

Bringing suit/timing

“Floor”/“ceiling”

18

Conclusion

Buyer to thoroughly investigate

Identify potential issues early

Use closing conditions/remedies provisions

as an “out”/possibility to get back to where

Buyer was before entering into the

Agreement

Maintain adequate security and survival of

representations

19

Liner Grode Stein Yankelevitz

Sunshine Regenstreif & Taylor LLP

Los Angeles

100 Glendon Avenue,

14th Floor

Los Angeles, CA 90024

San Francisco

199 Fremont Street,

20th Floor

San Francisco, CA 94105

Representations and Warranties

from the Seller’s Perspective:

You’ll Get Nothing and Like It!

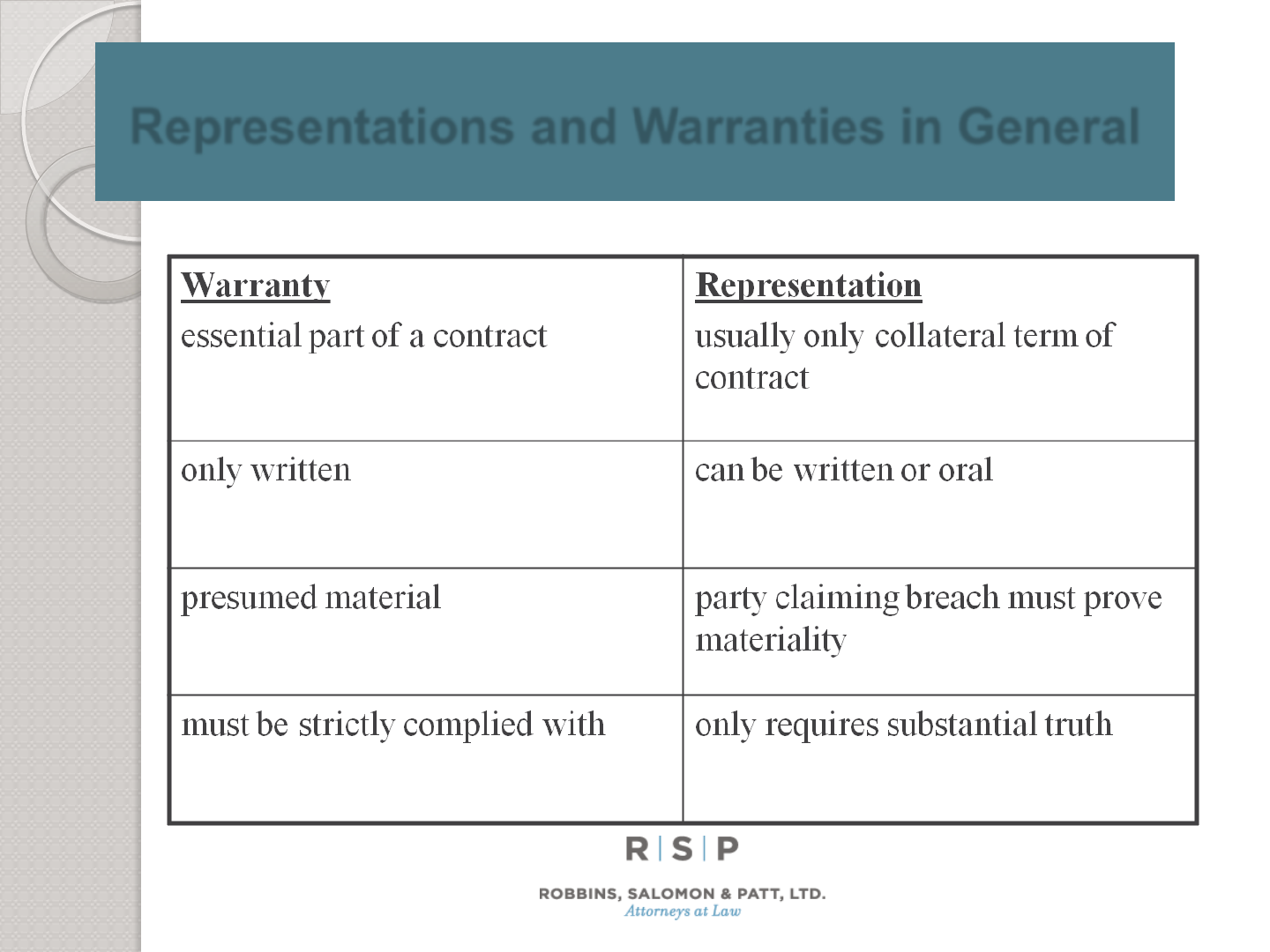

Representations and Warranties in General

Representation: Statement of fact made to induce another to

enter into a contract

» Cause of Action: fraud or negligent misrepresentation

» Remedy: rescission/specific performance/damages for benefit of

the bargain

Warranty: A promise that a proposition of fact is true

» Cause of Action: breach of contract—no need to prove intent to

defraud or reliance

» Remedy: actual and benefit of the bargain damages; requirement

to cure

21

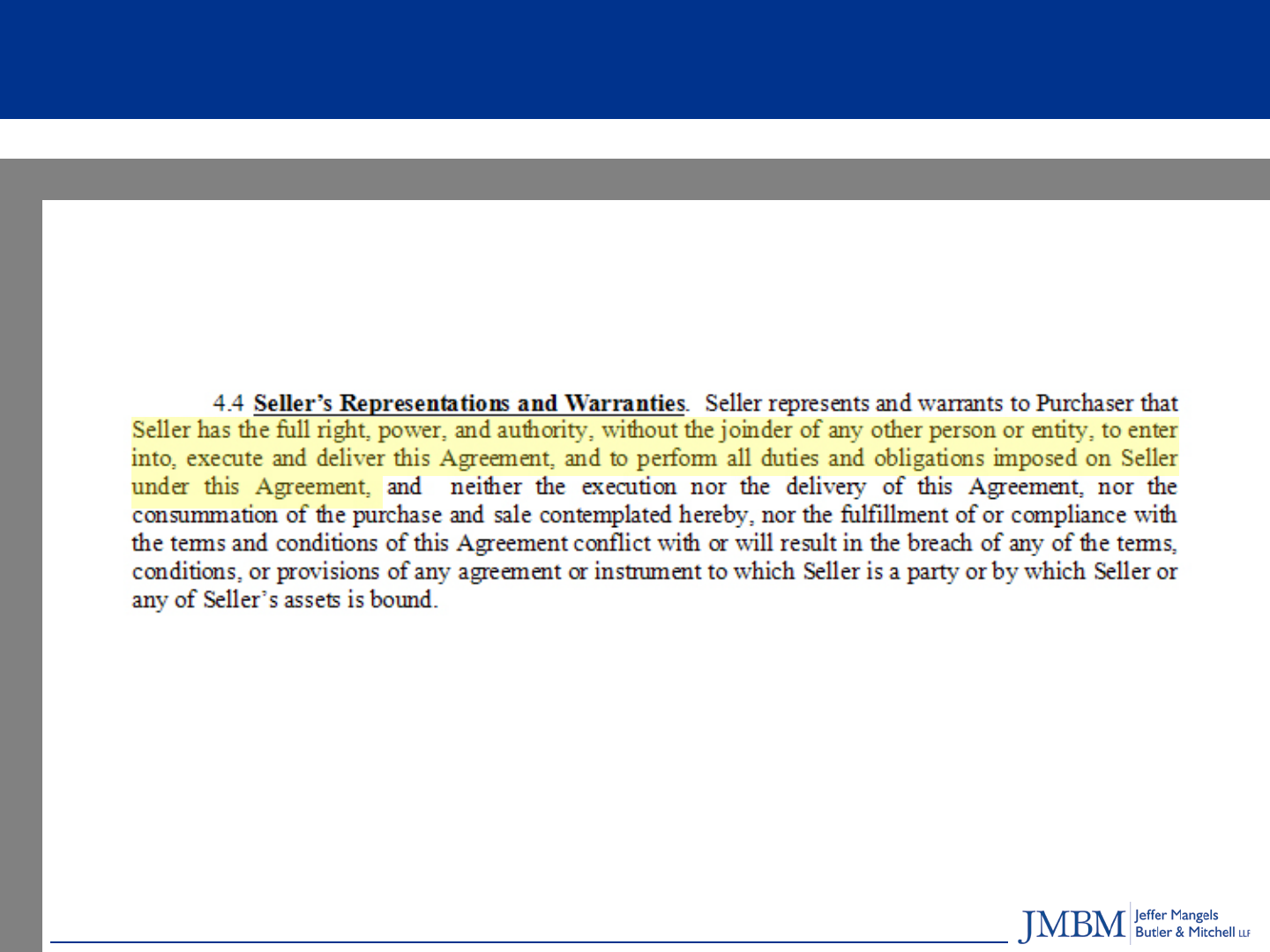

General Types of Real Estate Contract

Representations and Warranties

Status and Authority of the Seller

Examples: Seller is valid entity in good standing; agreement will not default

other agreements; no bankruptcy or insolvency; contract enforceable against

Seller; no additional consents; FIRPTA/no foreign person; etc.

Current Status of the Property

Examples: Good title; no condemnation; compliance with codes and ordinances;

no litigation; no unrecorded liens; no other contracts concerning property; no

access issues; no environmental issues; no other parties in possession; no

increased taxes/special assessments; no litigation; all utilities present; no

strikes or work stoppages; etc.

Operation of the Property

Examples: All leases in effect; no breach of leases; rent roll and books and

records are accurate; no deferred maintenance; no bulk

sales/employment/sales tax issues; no management agreements or

agreements surviving sale; etc.

23

Status of the Seller

Representations and Warranties (“R/W”)

I. Seller’s entity: no knowledge carve out (?); limit to selling entity; Limit to

good standing as of the date of the contract; What is a “valid” entity?

II. Authority to enter into agreement: no knowledge carve out—do not want

to have to share operating or partnership agreement; Limit to as of the date of

the contract

III. Pending litigation: limit to selling entity; Limit to actual knowledge, or better,

R/W received no notice of pending or threatened litigation; Limit notice

received only to selling entity and not to any agent or affiliate; Cannot give

absolute as litigation may be pending but not yet served; Limit to actions

affecting ability to perform agreement

IV. Bankruptcy/insolvency: no knowledge carve out for bankruptcy; Define

insolvency or delete it (if single purpose entity, sale of property could render it

“insolvent”); Delete representations about settling or compromising debts to

creditors—or better define and limit

24

Status of the Seller

Representations and Warranties

V. Does not Violate Other Agreements: Knowledge carve out (?) or

limit to written agreements

VI. Is not Prohibited by Governmental Regulations: All R/Ws

regarding governmental issues must be with knowledge carve out

VII. Enforceability of Sales Contract: Will Purchaser pay for legal

opinion?; Limit to knowledge as calls for legal conclusion

VIII. Foreign Person and No Consents Required: No issue with

representing

25

Status of the Property

Representations and Warranties

I. Marketable Title: Limit definition or change to “indefeasible title”; Subject to

permitted exceptions or attach commitment; Issuance of title policy

constitutes proof of marketable title

II. Property Complies with all Applicable Laws: Need knowledge carve out,

or better, “received no notice” carve out; Limit definition of “applicable laws”

III. No Condemnation: Limit to knowledge, or better, no notice received; Omit

any reference to personal property;

IV. No Litigation Affecting Property: Same concerns as Seller’s pending

litigation; Left hand-right hand issues; Ideally, “received no notice”

V. No Liens Affecting Property: Why have title insurance?; In large projects,

ongoing work done and professional property managers that have lien rights

that Seller may not be able to make this representation

26

Status of the Property

Representations and Warranties

VI. No Other Parties in Possession: Limit to knowledge; Exception to Leases

and licenses provided during due diligence; Exceptions to matters shown on

survey or in title commitment

VII. No Other Contracts relating to Property or Seller: Carve out for contracts

with seller in normal course of business, that do not survive closing or that are

cancelable within X days; Exception to contracts provided during due

diligence

VIII. No Environmental Violations: Attempt to strike completely; Limit to

knowledge or notice; Carve out for time limits, damage limits and types of

damages (only to remediation costs and exclude lost profit or benefit of

bargain damages); Limit warranty to purchaser only

IX. No Change in Assessed Value: Limit to notice

X. No strikes or Work Stoppages: Limit to notice

27

Operation of the Property

Representations and Warranties

I. Tenant Leases in Effect: Try to omit or give only to the extent not

Purchaser provided estoppel certificate; Limit to knowledge

regardless; Limit to as of the date of the statement provided; Limit

due diligence production to all leases and exhibits in possession or

control (there is always an exhibit missing)

II. Books and Record Accurate: Attempt knowledge carve out;

Attempt to limit to that which is not otherwise disclosed in the leases;

Carve out materials not prepared by Seller (“blame the manager”)

III. Operations/Maintenance: Try to avoid, especially if AS IS (any rep

may limit AS IS clause); Limit to knowledge; Limit to as of the date of

the contract

IV. Bulk Sales/Employment/Sales Tax: Depends on state and type of

property; Obtain clearance from local departments to eliminate

representation

28

General Seller Warranty Limitations

I. Identify Party/Parties having “Knowledge”: Limit knowledge of

R/W to a particular person or persons, ideally property manager or

operations personnel; Left hand—Right hand issues; Multiple entities

II. Limit Knowledge to “Actual Current Knowledge”: Avoids

constructive knowledge (filed but not served); Avoids matters arising

after date of contract

III. Limit Warranties Only to Particular Paragraph: Only R/W are

contained in Paragraph X; Cannot rely on any statements from

anyone other than in Paragraph X

29

General Seller Warranty Limitations

IV. Warranties Limited to Due Diligence Materials: Limit all R/W to

matters that were provided during due diligence or discovered during

due diligence; Attempt to carve out matters that could have been

discovered during due diligence; Attempt to carve out for matters that

could have been reasonable inferred or implied from due diligence

material

V. No Warranties on Any Documents Provided: “Popeye” carve out:

They are What They Are

VI. Omit Requirement to Investigate or Confirm: Knowledge limited

to just that—knowledge; Why have Purchaser’s due diligence?

VII. Only Reaffirm Particular Reps at Closing: Pre-closing versus

post-closing breach

30

Seller Warranty Remedies Provisions

I. Time and Dollar Limits: Create time limitation in which to bring claims; Limit

warranty liability to minimum and maximum amounts—warranty damages too

indefinite to not limit

II. Pre-Closing Breach: Right to Cancel/Failed condition to closing; Out of

pocket costs; Specific Performance; Agreed reduction in purchase price

(Seller’s reluctant because uncertain—include limits); If relating to property’s

income, agree on cap rate to determine purchase price

III. Post-Closing Breach: Specific performance useless?; Cap damage

amounts to the lesser of actual costs incurred or pre-determined X dollars;

Benefit of the bargain damages; Rescind contract

IV. No Escrows or Letters of Credit: Invites claims; Agree to not disburse

proceeds to members/partners/shareholders until claim time expires

31

Warranties and Representations:

A Philosophy

I. Insurance Against Fraud

II. Should not Cause Seller’s Counsel’s Insomnia—If

you don’t know it; don’t say it

III. Argument for SPEs—Buyer may be S.O.L.

IV. Are you “Judgment Proof”? Do you want to find

out?

V. Buyer’s should not Rely—Not a Substitute for Due

Diligence

32

Larry Woodard is a shareholder in the Real Estate Group and chair of the

Construction Law Group of Robbins, Salomon & Patt, Ltd., in Chicago,

Illinois. Larry has represented Fortune 500 companies, private developers,

condominium associations, units of local government, investors, landlords,

tenants, private REITs and syndications in the development, financing,

leasing, zoning, acquisition or disposal of their real estate interests. His

practice also extends into general business transactions and governance,

construction and mechanics lien litigation and asset protection. He has

experience negotiating and documenting a broad range of transactional

matters, including letters of intent, asset and stock sales, joint ventures, buy-

sell agreements, operating agreements, partnership agreements and non-

disclosure agreements.

Larry is a real estate developer and investor and is an Illinois licensed real

estate broker and Illinois licensed real estate brokerage instructor. He is a

periodic speaker and contributor on the subject of real estate law to

numerous publications and is the General Editor for Illinois Institute for

Continuing Legal Education’s (IICLE) ILLINOIS CONDOMINIUM LAW

handbook.

33

LARRY N. WOODARD

ROBBINS, SALOMON & PATT, LTD.

DISCLAIMER

This information and any presentation accompanying it (collectively the "Content") has been prepared

by Larry N. Woodard of Robbins, Salomon & Patt, Ltd., an Illinois corporation (collectively “RSP”) for

general informational purposes only. It is not intended as and should not be regarded or relied upon

as legal advice or opinion, or as a substitute for the advice of counsel. You should not rely on, take

any action or fail to take any action based upon the Content.

As between RSP and you, RSP at all times owns and retains all right, title and interest in and to the

Content. You may only use and copy the Content, or portions of the Content, for your personal, non-

commercial use, provided that you place all copyright and any other notices applicable to such

Content in a form and place that you believe complies with the requirements of the United States'

Copyright and all other applicable law. Except as granted in the foregoing limited license with

respect to the Content, you may not otherwise use, make available or disclose the Content, or

portions of the Content, or mention RSP in connection with the Content, or portions of the Content, in

any review, report, public announcement, transmission, presentation, distribution, republication or

other similar communication, whether in whole or in part, without the express prior written consent of

RSP in each instance.

This information or your use or reliance upon the Content does not establish a lawyer-client

relationship between you and RSP. If you would like more information or specific advice of matters

of interest to you please contact us directly.

© 2012 Robbins, Salomon & Patt, Ltd., All Rights Reserved.

34

35

David P. Waite

310.785.5319

DWaite@jmbm.com

February 15, 2012

DISTRESSED TRANSACTIONS:

How Much Risk Can You Afford?

©2012 Jeffer Mangels Butler & Mitchell LLP. All Rights Reserved

36

Distressed Deals

•The lender/seller may have little or no information or

operational experience with respect to the property

•The lender/seller unwilling to provide any representations

even as to what is at least theoretically "known"

•The property was or is a troubled property (low occupancy,

deferred maintenance, uncertain entitlement status,

environmental liabilities undefined, etc.)

•The lender/seller is a single purpose entity with no other

assets

37

Distressed Deals

•The buyer is paying a “REO Price”

instead of “Retail Price”

•The lender/seller is particularly risk

adverse

•Decision making control and authority

over the asset uncertain

38

Distressed Sale Risk Factors

•The realities of REO sales

•How the lender/seller acquired the loan

(originator, syndicator, note purchaser, etc.)

•How the lender/seller acquired the property

(judicial or non-judicial foreclosure, receiver,

deed in lieu, etc.)

39

Distressed Sale Risk Factors

•How the property was managed/operated before

acquisition by the lender/seller (decision making

and control during forbearance period)

•How the property has been managed/operated by

the lender/seller (active or passive?)

•How long has the lender/seller operated the

property?

40

Understanding the Seller's History

Understanding the history of the property will

help the buyer understand and assess:

–The extent to which the lender/seller may be willing

(or unwilling) to negotiate various provisions in the

Purchase Agreement and the Lender’s/Seller’s

rationale for that position

–The risks that the buyer will be taking on with its

purchase of the property and the magnitude of those

risks.

41

What is the Loan History?

•How did the lender/seller acquire the loan?

•How long did the lender/seller hold the loan?

•How does the length of the loan affect the

information available and the lender/seller's

risk tolerance?

42

How Was the Property Acquired?

•How did the lender/seller acquire the

property?

•What does a more cooperative

borrower mean?

43

Property Management

•How has the property been

managed/operated?

–Prior to the lender/seller’s acquisition?

–After the lender/seller’s acquisition?

–Entitlements, Approvals, Regulatory

Compliance?

44

Type of Lender/Seller (Bank or Servicer?)

•Lender/seller’s experience with REO

•Lender/seller’s internal approval issues

•Lender/seller’s particular risk tolerance

issues

•Closing timing may be driven by financial

statement dates

45

Buyer Beware: Discounted Price = Risk

Beyond the dirt and the improvements,

it’s important that the buyer identify

critical components of the acquisition

and confirm that, as a legal matter, they

will be conveyed to the buyer as of the

closing.

46

Transactional Shifting of Risk of Unknowns

•Analysis of the lender/seller’s

acquisition

•Concern re express or implied

representations/warranties by

lender/seller

•Purchase Agreement Limitations

47

Leases and Foreclosure Issues

If the lender/seller acquired the property by

foreclosure, the buyer will need to confirm whether or

not the Leases survived the foreclosure.

•Analysis of the effect of the foreclosure

•Lease vs. Lease amendments

•Comfort regarding survival

•Estoppels, Security Deposits, Unfunded TI's

48

Buyer's Due Diligence

The buyer’s due diligence is even more critical

because of the nature of a REO sale.

•Limits on information provided by the

lender/seller

•Limits on the lender/seller’s representations

49

Representations and Warranties

•Limited representations and warranties from

the lender/seller reflect the allocation of risk

•Buyer post-closing considerations

50

Seller's Representations and Warranties

•Typical lender/seller Representations:

–Lender/seller organization

–Lender/seller authority to sell

–FIRPTA compliance

•Representations may also (though not always) include:

–OFAC compliance

–Pending litigation naming the lender/seller relating to the property

51

Buyer's Wish List

•Property related matters (physical condition,

environmental matters, tenant and lease issues)

•Material adverse conditions of which the

lender/seller has actual knowledge

•Delivery of material information in the

lender/seller’s possession (including

representation as to accuracy and completeness)

52

Buyer's Wish List

•Leases and Assigned Contracts (copies,

estoppels, termination rights, adequate

review period)

•Governmental Actions

•For loans acquired from the FDIC, receipt of

all necessary FDIC approvals

53

Expanding Seller's Representations

•Limit representations to actual knowledge of specified

individuals

•Limit representations to lender/seller’s period of

ownership

•Limit representations to material adverse matters

•Cap Survival period and damages

•Each limitation dilutes the value of the representation to

the buyer

54

Limitations on Recourse

•Reality of SPE lender/seller

•Time limit for assertion of

representation breach claims

•Additional dollar limitation on the

lender/seller’s liability

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

Jeffer Mangels Butler & Mitchell LLP

Los Angeles

1900 Avenue of the Stars, 7th Floor

Los Angeles, California 90067

Phone: 310.203.8080 Fax: 310.203.0567

Orange County

3 Park Plaza, Suite 1100

Irvine, California 92614

Phone: 949.623.7200 Fax: 949.623.7202

San Francisco

Two Embarcadero Center, 5th Floor

San Francisco, California 94111

Phone: 415.398.8080 Fax: 415.398.5584

jmbm.com