DEF 14A 1 Def14a DLTSage TM Tape Security PX500 Series Quantum Annual Report 06

User Manual: DLTSageTM Tape Security PX500 Series

Open the PDF directly: View PDF ![]() .

.

Page Count: 147 [warning: Documents this large are best viewed by clicking the View PDF Link!]

Fiscal 2006 Annual Report

and Proxy Statement

Contents:

Letter to Stockholders

Notice of 2006 Annual

Meeting and Proxy

Statement

2006 Annual Report on

Form 10-K

Stockholder Information

To Our Stockholders:

In 2002, we strategically transitioned Quantum to focus

exclusively on the market for backup, recovery and archive. It

was our belief that this would be an area ripe for innovation and

growth as more and more companies require their data to be both

protected and more accessible, creating stringent system

availability requirements and ever-expanding capacity needs. In

fact, backup capacity continues to grow by more than 50% each

year and shows no sign of abating. Part of what is driving this

growth is the increasing awareness by companies of the need for

disaster recovery and data protection. We are seeing more and

more mid-sized businesses starting to deploy backup data

centers, and there is a greater focus on the need to protect the increasing amount of corporate

data in remote branch offices and remote locations.

Meanwhile, recovery time objectives continue to shorten as the cost of downtime per hour ranges

from a damaging $18,000 for a small business to upwards of $1 million for a large business. As

such, disk-based backup continues to gain momentum as a near line storage alternative within a

tiered storage environment. To increase the utilization and efficiency of primary storage and

improve recovery time, data can be quickly moved from active storage to disk-based storage

solutions before it is ultimately moved to tape for archive. While disk-based backup solutions are

significantly cheaper than primary storage, tape-based archive is still the best way to lower

storage and recovery costs by a factor of two over any other investment, with 85% of all digital

archive capacity still stored on tape media today.

Security is also becoming an increasingly important dimension of storage. In 2005, there were

130 publicly disclosed data breaches exposing the personal information of 55 million Americans.

While this is not a new phenomenon, recent regulations, with even more on the way, stipulate

that consumers must be notified of a breach in security related to their personal data. Such highly

visible disclosures have caused embarrassment for several companies, including Bank of

America, Citicorp and Marriott. As a result, security has emerged as a critical concern for

businesses of all sizes, with significant focus on protecting data stored on tape cartridges that are

transported offsite.

It is evident that backup, archive and recovery is a dynamic area with considerable opportunity

as customers seek more efficient and effective ways to securely retain, protect and rapidly

recover ever-increasing volumes of data.

2006 A Pivotal Year

Fiscal 2006 was a pivotal year for Quantum as it executed against many of the priorities that

were set over the last couple of years. In doing so, we substantially improved Quantum’s

competitiveness across a broad range of areas, including our cost structure, manufacturing

processes and product positioning with the launch of an unprecedented number of new products.

We also strengthened our ability to service and market to our customers, built upon our branded

strategy, and extended our growth platform with the introduction of new disk-based backup

appliances and a value-added security framework.

Specific highlights for the year include:

• Completing the integration of Certance into our operations

• Launching a record number of new products, including:

o Four tape automation products: SuperLoader™ 3 and the PX500 Series (PX502,

PX506 and PX510)

o Four storage devices: DLT-S4, DLT-V4, SDLT 600A and GoVault™

o Three disk-based backup appliances: DX3000, DX5000 and DPM5500

• Significantly increasing shipments of our new SuperLoader 3 and PX500 Series libraries

every quarter since launch

• Expanding into new vertical markets with SDLT 600A, the first data tape drive specifically

designed for professional video

• Increasing volume sales of our SDLT 600 and VS160 tape drives by 75 and 44 percent,

respectively

• Growing branded sales as a percentage of revenue from 23 percent in fiscal year 2005 to 30

percent in fiscal year 2006

• Increasing sales of LTO tape drives in excess of double digits every quarter in fiscal year

2006

• Introducing the first phase of a multi-layered data security framework with DLTSage™ Tape

Security, a firmware feature that uses an electronic key to prevent or allow reading and

writing of data on a tape cartridge

• Being recognized as the highest-rated, pure-play storage vendor in Computer Reseller News’

Channel Champions Survey for the third consecutive year

• Winning a NorthFace ScoreBoardSM Award for exemplary customer service from Omega

Management Group Corp. and being honored as the winner of a Service & Support

Professionals Association (SSPA) 2006 STAR Award for Best Practices

Financial Results

The accomplishments we made in delivering on our goals were reflected in our financial results

for the fiscal year. In fiscal 2006, we saw revenues grow for the first time in three years,

primarily due to strong growth within our LTO product line that was added through the Certance

acquisition, despite continued pricing pressures on older products, as well as volume sales

declines of such products and product transition-related issues that impacted our overall

performance. We achieved a second consecutive year of non-GAAP profitability, with non-

GAAP net income increasing by 44 percent. We also remained aggressive in controlling costs,

as both GAAP and non-GAAP operating expenses as a percentage of revenue continued their

declines from previous years. In fact, on a year-over-year basis, non-GAAP operating expenses

were relatively flat, even though fiscal 2006 reflected a full year’s worth of Certance costs

compared to just a quarter in fiscal 2005. And as new products were completed and launched

through the year, we made corresponding reductions in research and development investments.

In addition, we were able to achieve positive cash flow from operations for the year.

Total revenue was $834 million for the full fiscal year 2006. Non-GAAP net income for this

period was $18.8 million, or ten cents per diluted share, compared to non-GAAP net income of

$13.0 million or seven cents per diluted share for fiscal year 2005. Our GAAP net loss was

$42.0 million, or 23 cents per diluted share for fiscal year 2006, compared to a net loss of $3.5

million, or two cents per diluted share for fiscal year 2005. The increased GAAP net loss for

fiscal 2006 compared to fiscal 2005 was primarily due to charges related to the legal settlement

with StorageTek, higher restructuring costs and the fact that fiscal year 2005 results included a

one-time tax benefit resulting from a favorable resolution of IRS audits.

A quantitative reconciliation of any GAAP to non-GAAP financial measure included in this

letter can be found in our quarterly earnings press releases for fiscal year 2006 located under

“Quarterly Earnings” in the Investor Relations section of our website at www.quantum.com.

Forward and Onward

Quantum’s strategic priorities for the near term are three-fold. First, we want to develop a

stronger execution platform that leverages Quantum’s breadth to create sustainable cost and

quality advantages. Second, we want to build on our leading independent tape business by

capitalizing on our unique position as a developer of tape drives, automation systems and media.

Third, we want to create a growth platform beyond tape with solutions that include disk,

software and services and that are optimized for tiered storage environments.

With this in mind, we announced in early May that we will be acquiring Advanced Digital

Information Corporation (ADIC). This combination will create one of the industry’s largest,

independent storage companies with combined revenues currently exceeding $1.2 billion and one

that will be able to address customers’ evolving data protection requirements with the most

comprehensive, integrated and best-of-breed set of solutions for securely storing, managing,

protecting and recovering their data. We will also be able to provide customers greater support

with larger and better leveraged sales and service capabilities. In addition, the combined

company will enable Quantum to drive synergies to create an efficient operational structure that

can produce tangible financial benefits. We will also capitalize on revenue growth opportunities

through enhanced market access with a well-balanced OEM, branded and geographic business.

Lastly, the new company will be able to more effectively invest in a leadership product roadmap

that can gain critical mass and extend our growth platform.

While we have made tremendous strides in recent years to turn Quantum into a company that is

more efficient, competitive and better positioned in the marketplace, we know that more remains

to be done for us to consistently deliver long-term growth and profitability. We are committed

to building upon these efforts and to executing against our objectives to accomplish this.

Thank you for your continued support.

Rick Belluzzo

Safe Harbor Statement under the Private Securities Litigation Reform Act of 1995 for Quantum Corporation

This letter contains certain "forward-looking" statements within the meaning of the Private Securities Litigation Reform Act of 1995.

Specifically, the statements relating to: (1) our expectations regarding future demand for back-up, archive and recovery solutions, including

demand for tape-based backup and archive solutions; (2) our beliefs and expectations about our prospects in fiscal year 2007 and beyond,

including our strategic priorities; (3) our ability to complete our acquisition of ADIC and successfully integrate its operations into ours, including

expected synergies from the acquisition and the effect of the acquisition on Quantum’s financial position; (4) the storage and macro-economic

environments; and (5) our beliefs regarding customer expectations, and our ability to capitalize on the market opportunities, are forward-looking

statements within the meaning of the Safe Harbor. These statements are based on management's current expectations and are subject to risks and

uncertainties that could cause actual results to differ materially, including, without limitation, the risk that we may not successfully execute to our

product roadmaps and timely ship our products, the risk that lower sales volumes and continuing price and cost pressures could lead to lower

gross margins, media royalties from media manufacturers coming in at lower levels than expected, acceptance of, or demand for, our products

being lower than anticipated, and the risk that we may not consummate our acquisition of ADIC or fail to successfully integrate ADIC, its

products and employees into Quantum after the closing and achieve expected synergies. More detailed information about these risks, and

additional risks, are set forth under "Risk Factors" in the Company’s Form 10-K for the annual period ended March 31, 2006 included with this

letter. Quantum expressly disclaims any obligation to update or alter its forward-looking statements, whether as a result of new information,

future events or otherwise.

1

QUANTUM CORPORATION

______________________

NOTICE OF ANNUAL MEETING OF STOCKHOLDERS

______________________

TO BE HELD ON

August 28, 2006

TO THE STOCKHOLDERS:

NOTICE IS HEREBY GIVEN that the Annual Meeting of Stockholders of Quantum Corporation (the “Company” or

“Quantum”), a Delaware corporation, will be held on Monday, August 28, 2006 at 9:00 a.m., Pacific Daylight Time, at

Quantum’s corporate headquarters at 1650 Technology Drive, San Jose, CA 95110, for the following purposes:

1. To elect eight directors to serve until the next Annual Meeting of Stockholders or until their successors are elected and

qualified;

2. To ratify the appointment of Ernst & Young LLP as the independent registered public accounting firm of the Company

for the fiscal year ending March 31, 2007; and

3. To transact such other business as may properly come before the meeting or any adjournment thereof.

The foregoing items of business are more fully described in the Proxy Statement accompanying this Notice.

Only stockholders of record at the close of business on June 30, 2006 are entitled to notice of and to vote at the meeting

and any adjournment thereof.

All stockholders are cordially invited to attend the meeting in person. However, to ensure your representation at the

meeting, you are urged to vote, sign, date and return the enclosed proxy as promptly as possible in the postage-prepaid envelope

enclosed for that purpose. Any stockholder attending the meeting may vote in person even if he or she previously returned a

proxy.

By Order of the Board of Directors,

Shawn D. Hall

Vice President, General Counsel and Secretary

San Jose, California

July 11, 2006

2

QUANTUM CORPORATION

PROXY STATEMENT

INFORMATION CONCERNING SOLICITATION AND VOTING

General

The enclosed proxy is solicited on behalf of Quantum Corporation (the “Company” or “Quantum”) for use at the Annual

Meeting of Stockholders to be held August 28, 2006 at 9:00 a.m., Pacific Daylight Time, or at any adjournment or

postponement thereof (the “Annual Meeting” or “Meeting”), for the purposes set forth herein and in the accompanying Notice

of Annual Meeting of Stockholders. The Annual Meeting will be held at the Company’s corporate headquarters at 1650

Technology Drive, San Jose, CA 95110. The Company’s telephone number is (408) 944-4000 and the Internet address for its

website is http://www.quantum.com.

These proxy solicitation materials were mailed on or about July 11, 2006 to all stockholders entitled to notice of and to

vote at the Meeting. A copy of the Company’s Annual Report to Stockholders for the year ended March 31, 2006 (“Fiscal

2006”), including financial statements, was sent to the stockholders of the Company prior to or concurrently with this Proxy

Statement.

Record Date; Outstanding Shares

Stockholders of record at the close of business on June 30, 2006 (the “Record Date”) are entitled to notice of and to vote at

the Meeting. At the Record Date, 188,984,708 shares of the Company’s Common Stock, $0.01 par value (the “Common

Stock”), were issued and outstanding. The closing price of the Common Stock on the Record Date, as reported by the New

York Stock Exchange, was $2.62 per share.

Revocability of Proxies

Any proxy given pursuant to this solicitation may be revoked by the person giving it at any time before it is voted. Proxies

may be revoked by (i) filing a written notice of revocation bearing a later date than the proxy with the Secretary of the

Company (currently Shawn D. Hall) at or before the taking of the vote at the Meeting, (ii) duly executing a later dated proxy

relating to the same shares and delivering it to the Secretary of the Company at or before the taking of the vote at the Annual

Meeting or (iii) attending the Meeting and voting in person (although attendance at the Meeting will not in and of itself

constitute a revocation of a proxy). Any written notice of revocation or subsequent proxy must be delivered to the Secretary of

the Company, or hand delivered to the Secretary of the Company at or before the taking of the vote at the Meeting.

Voting and Solicitation

Each share of Common Stock has one vote, as provided in the Company’s Amended and Restated Certificate of

Incorporation. Accordingly, a total of 188,984,708 votes may be cast at the Meeting. Holders of Common Stock vote together

as a single class on all matters covered by this Proxy Statement. For voting with respect to the election of directors,

stockholders may cumulate their votes. Cumulative voting will allow you to allocate among the director nominees, as you see

fit, the total number of votes equal to the number of director positions to be filled multiplied by the number of shares you hold.

For example, if you own 100 shares of Common Stock, and there are eight directors to be elected at the Annual Meeting, you

could allocate 800 "FOR" votes (eight times one-hundred) among as few or as many of the eight nominees to be voted on at the

Meeting as you choose. See “PROPOSAL ONE — ELECTION OF DIRECTORS — REQUIRED VOTE.”

3

The cost of soliciting proxies will be borne by the Company. The Company has not retained the services of a solicitor. The

Company may reimburse brokerage firms and other persons representing beneficial owners of shares for their expenses in

forwarding solicitation material to such beneficial owners. Proxies may also be solicited by certain of the Company’s directors,

officers and regular employees, without additional compensation, personally or by telephone, email or otherwise.

Stockholder Proposals (Other than for Nominees to the Board of Directors)

Proposals of stockholders of the Company which are to be presented at the Company’s annual meeting of stockholders for

the year ended March 31, 2007 must be received by the Secretary of the Company no later than March 29, 2007 to be

considered for inclusion in the proxy materials relating to that meeting.

Alternatively, under the Company’s Bylaws, a proposal that the stockholder does not seek to include in the Company’s

proxy materials for the 2007 annual meeting must be received by the Secretary of the Company not less than sixty (60) days nor

more than ninety (90) days prior to the meeting; provided, however, that in the event that less than seventy (70) days notice or

prior public disclosure of the date of the meeting is given or made to stockholders, notice by the stockholder to be timely must

be so received not later than the close of business on the tenth day following the day on which such notice of the date of the

annual meeting was mailed or such public disclosure was made. The stockholder’s submission must include the information

specified in the Company’s Bylaws.

Proposals not meeting the requirements of the preceding paragraph will not be entertained at the 2007 annual meeting.

Stockholders should contact the Secretary of the Company in writing at 1650 Technology Drive, Suite 700, San Jose CA

95110, to make any submission or to obtain additional information as to the proper form and content of submissions.

The Company has not been notified by any stockholder of his or her intent to present a stockholder proposal from the floor

at this year’s Annual Meeting. The enclosed proxy card grants the proxy holders discretionary authority to vote on any matter

(other than stockholder proposals relating to nominees to the Board of Directors) properly brought before the Annual Meeting.

Stockholder Proposals (for Nominees to the Board of Directors)

Nominations of persons for election to the Board of Directors of the Company may be made by a stockholder of the

Company entitled to vote in the election of directors at the meeting who complies with the notice procedures set forth in the

Company’s Bylaws. Such nominations, other than those made by or at the direction of the Board of Directors, shall be made

pursuant to timely notice in writing to the Secretary of the Company. To be timely, a stockholder’s notice must be delivered to

or mailed and received at the principal executive offices of the Company not less than twenty (20) days nor more than sixty

(60) days prior to the meeting. The stockholder’s submission must include the information specified in the Company’s Bylaws.

Proposals not meeting the requirements of the preceding paragraph will not be entertained at the 2007 annual meeting.

Stockholders should contact the Secretary of the Company in writing at 1650 Technology Drive, Suite 700, San Jose CA

95110, to make any submission or to obtain additional information as to the proper form and content of submissions.

The Company has not been notified by any stockholder of his or her intent to present any stockholder proposals for

nominees to the Board of Directors from the floor at this year’s Annual Meeting.

Quorum; Abstentions; Broker Non-Votes

A majority of the shares of Common Stock issued and outstanding on the Record Date will constitute a quorum for the

transaction of business at the Annual Meeting.

While there is no definite statutory or case law authority in Delaware as to the proper treatment of abstentions, the

Company believes that abstentions should be counted for purposes of determining both (i) the presence or absence of a quorum

for the transaction of business and (ii) the total number of shares entitled to vote at the Annual Meeting (“Votes Cast”) with

respect to a proposal (other than the election of directors). In the absence of controlling precedent to the contrary, the Company

intends to treat abstentions in this manner. Accordingly, abstentions will have the same effect as a vote against the proposal.

Broker non-votes (i.e., votes from shares held of record by brokers as to which the beneficial owners have given no voting

instructions) will be counted for purposes of determining the presence or absence of a quorum for the transaction of business,

but will not be counted for purposes of determining the number of Votes Cast with respect to the particular proposal on which

the broker has expressly not voted. Accordingly, broker non-votes will not affect the outcome of the voting on a proposal that

requires a majority of the Votes Cast. Thus, a broker non-vote will make a quorum more readily attainable, but the broker non-

vote will not otherwise affect the outcome of the vote on a proposal.

4

Section 16(a) Beneficial Ownership Reporting Compliance

Section 16(a) of the Exchange Act requires the Company’s Section 16 officers, directors and persons who own more than

10% of a registered class of the Company’s equity securities to file reports of ownership and changes in ownership with the

Securities and Exchange Commission (the “SEC”). Such executive officers, directors and greater than ten-percent stockholders

are also required by SEC rules to furnish the Company with copies of all forms that they file pursuant to Section 16(a). Based

solely on its review of the copies of such reports received by the Company, or on written representations from certain reporting

persons, the Company believes that all filing requirements were met during Fiscal 2006.

PROPOSAL ONE

ELECTION OF DIRECTORS

Nominees

There are eight nominees for election to the Company’s Board of Directors this year. All of the nominees are currently

serving on the Company’s Board. Unless otherwise instructed, the proxy holders will vote the proxies received by them for the

nominees named below. Each nominee has consented to be named as a nominee in the Proxy Statement and to serve as a

director if elected. In the event that additional persons are nominated at the time of the Annual Meeting, the proxy holders

intend to vote all proxies received by them in such a manner (in accordance with cumulative voting) as will ensure the election

of as many of the nominees listed below as possible (or, if new nominees have been designated by the Board, in such a manner

as to elect such nominees). In such event, the specific nominees for whom such votes will be cumulated will be determined by

the proxy holders. The Company is not aware of any reason that any nominee will be unable or will decline to serve as a

director. The term of office of each person elected as a director will continue until the next annual meeting of stockholders or

until a successor has been elected and qualified. There are no arrangements or understandings between any director or executive

officer and any other person pursuant to which he or she is or was to be selected as a director or officer of the Company.

The Board’s key roles include, but are not limited to: (i) the selection and evaluation of the Company’s Chief Executive

Officer (“CEO”), and overseeing CEO succession planning; (ii) advising the CEO and management on the Company’s

fundamental strategies; (iii) reviewing and approving the CEO’s objectives; (iv) approving acquisitions, divestitures and other

fundamental corporate actions; (v) advising the CEO on the performance of senior management, and fundamental

organizational changes, including succession planning; and (vi) approving the annual operating financial plan.

The names of the nominees and certain information about them as of June 1, 2006, are set forth below.

Name of Nominee Age Director

Since Principal Occupation Since

Richard E. Belluzzo ………............ 52 2002 Chief Executive Officer of Quantum, 2002

Chairman of the Board of Quantum, 2003

Michael A. Brown ……………….. 47 1995 Chairman of the board of Line 6, 2005

Former Chairman of Quantum, 2003

Thomas S. Buchsbaum†…………… 56 2005 Independent Consultant, 2005

Alan L. Earhart* ……..................... 62 2003 Independent Consultant, 2001

Edward M. Esber, Jr.*+ †………… 53 1988 Chairman and President of The Esber Group, 1991

Elizabeth A. Fetter+………………. 47 2005 Director and Consultant, 2005

John M. Partridge+ ………………. 57 2005 President and Chief Executive Officer of Inovant, 1999

Steven C. Wheelwright*†………… 62 2004 Professor and University Administrator, 1970

* Member of Audit Committee.

+ Member of Leadership and Compensation Committee.

† Member of the Corporate Governance and Nominating Committee.

5

Except as set forth below, each of the nominees has been engaged in his or her principal occupation described above during

the past five years. There are no family relationships between any directors or executive officers of the Company.

Mr. Richard E. Belluzzo has been Chief Executive Officer since joining the Company in September 2002 and Chairman of

the Board since July 2003. Before joining Quantum, from September 1999 to May 2002, Mr. Belluzzo held senior management

positions with Microsoft Corp., most recently President and Chief Operating Officer. Prior to Microsoft, from January 1998 to

September 1999, Mr. Belluzzo was Chief Executive Officer of Silicon Graphics, Inc. Before his tenure at Silicon Graphics,

from 1975 to January 1998, Mr. Belluzzo was with Hewlett-Packard, most recently as Executive Vice President of the

computer organization. Currently Mr. Belluzzo is a member of the board of directors of PMC-Sierra and JDS Uniphase, and is a

member of the board of trustees for Golden Gate University.

Mr. Michael A. Brown served as Chief Executive Officer of Quantum from September 1995 to September 2002 and as

Chairman of its Board of Directors from May 1998 to July 2003. From 1993 to September 1995, he was President of the

Company’s desktop group, from 1992 to 1993 he was Chief Operating Officer responsible for the Company’s hard disk drive

business, and from 1984 to 1992 he held various marketing position with the Company. Mr. Brown also serves as Chairman of

the board of directors of Line 6 and on the boards of EqualLogic, Nektar Therapeutics and Symantec Corporation.

Mr. Thomas S. Buchsbaum has been an independent consultant since March 2005. Prior to that, Mr. Buchsbaum served as

vice president of the U.S. Federal Business Segment, as well as vice president and general manager of the K12 and Higher

Education customer segments of Dell, Inc. from March 1997 to March 2005. Before Dell, Mr. Buchsbaum spent ten years at

Zenith Data Systems, a computer manufacturing company, until February 1997, where he was general manager for the federal

systems business unit and general manager of the state and local government and education segments. Mr. Buchsbaum served

as a director on the board and compensation committee of Group 1 Software, an application software provider, from 1989 to

2004. Mr. Buchsbaum also serves as an advisor to the board of Dick Blick Holdings and is a member of the Advisory Board of

Augmentix Corp. Mr. Buchsbaum is a member of the Company’s Corporate Governance and Nominating Committee.

Mr. Alan L. Earhart has been an independent consultant since 2001. From 1970 to 2001, Mr. Earhart held a variety of

positions with Coopers & Lybrand and its successor entity, Pricewaterhouse Coopers LLP, an accounting and consulting firm,

including most recently as the Managing Partner for Pricewaterhouse Coopers’ Silicon Valley office. Mr. Earhart also serves on

the board of directors and as Chairman of the audit committees of Foundry Networks and of Monolithic Power Systems, Inc.

and on the Board of Directors and the audit committee of Network Appliance. Mr. Earhart is the Chairman of Quantum’s Audit

Committee.

Mr. Edward M. Esber Jr. has served as Chairman and President of The Esber Group, a strategy consulting firm, since

February 1991. Mr. Esber has also been an angel investor in The Angels Forum since 1997. Mr. Esber is Chairman of the

Company’s Leadership and Compensation Committee and a member of the Company’s Corporate Governance and Nominating

Committee and of the Company’s Audit Committee.

Ms. Elizabeth A. Fetter served as president and CEO of QRS Corp., a retail supply chain software and services company,

from October 2001 to November 2004. Prior to joining QRS in 2001, Ms. Fetter was president and CEO of NorthPoint

Communications, a broadband services company from March 1999 to April 2001 and vice president and general manager of the

Consumer Services Group at US West (now Qwest), a telecommunications company, from January 1998 to March 1999.

Before US West, she was an officer at SBC/Pacific Bell, where she held a number of senior leadership positions. Ms. Fetter

also serves on the boards of Symmetricom, Berbee Inc. (a privately held company) and several non-profit organizations. Ms.

Fetter is a member of the Company’s Leadership and Compensation Committee.

Mr. John M. Partridge has served as President and Chief Executive Officer of Inovant, a transaction processing company

and a wholly owned subsidiary of Visa, since October 1999. Prior to that, from March 1998 to August 1999, he was Senior

Vice President of Program Management and Chief Information Officer for UNUM Corporation, a disability insurance

company. Before UNUM, he worked for Banco de Credito del Peru from August 1983 to March 1998 and Wells Fargo Bank

from April 1974 to July 1983. Mr. Partridge also serves on the board of directors of Inovant and Delta Dental. Mr. Partridge is

a member of the Company’s Leadership and Compensation Committee.

Mr. Steven C. Wheelwright has been a Professor at Harvard Business School since July 1970 and Senior Associate Dean at

Harvard Business School since July 2003 and from September 1995 to June 2000. From July 1979 to June 1988, Mr.

Wheelwright was a professor at the Stanford Graduate School of Business. Outside of his academic career, Mr. Wheelwright

was Vice President of Sales in a family-owned printing business from July 1973 to June 1974 and a consultant to numerous

companies from July 1970 to June 2000. He previously served on Quantum's board of directors from 1989 to 2000. He also

serves on the board of directors of Zions BanCorp. and is chairman of the board of Harvard Business School Publishing. Mr.

6

Wheelwright is Chairman of the Company’s Corporate Governance and Nominating Committee, a member of the Company’s

Audit Committee, and the Company’s lead independent director.

Board Independence

Quantum's Corporate Governance Principles provide that a majority of the Board shall consist of independent directors.

The Board has determined that each of the director nominees standing for election, except for Richard E. Belluzzo and Michael

A. Brown, and each member of each Board Committee, has no material relationship with Quantum (either directly or as a

partner, shareholder or officer of an organization that has a relationship with Quantum) and is independent within the meaning

of Quantum’s director independence standards. These standards reflect all applicable regulations, including the rules of the

New York Stock Exchange and the Securities and Exchange Commission.

Board Meetings and Committees

The Board of Directors of the Company held a total of six (6) meetings during Fiscal 2006. In addition, in Fiscal 2006, the

non-management directors held four (4) meetings without management present. During Fiscal 2006, no director attended fewer

than 75% of the meetings of the Board and the meetings of committees, if any, upon which such director served. All of our

directors are expected to attend each meeting of the Board and the committees on which they serve and are encouraged to

attend annual stockholder meetings, to the extent reasonably possible. All of our directors who were elected at our 2005

Annual Meeting, except for Mr. Esber, attended our 2005 Annual Meeting.

The Company has an Audit Committee, Leadership and Compensation Committee, and Corporate Governance and

Nominating Committee. Steven Wheelwright is the Company’s lead independent director and as such presides at the non-

management directors’ meetings.

The Audit Committee of the Board currently consists of Mr. Earhart, Chairman of the Committee, Mr. Esber and Mr.

Wheelwright, all of whom are independent directors and financially literate, as defined in the applicable New York Stock

Exchange listing standards and SEC rules and regulations. In addition to serving as a Chairman of the Company’s Audit

Committee, Mr. Earhart also serves as a member of the audit committees of Foundry Networks, Monolithic Power Systems and

Network Appliance, all of which are public companies. Mr. Earhart has informed the Board that aside from his service on these

four audit committees, his professional endeavors include only occasional consulting services with respect to financial and

accounting matters. The Board believes that Mr. Earhart’s simultaneous service on the audit committees of several public

companies may help provide valuable perspective on potential financial and accounting matters and other issues that may arise,

including with respect to corporate governance best practices. After discussion with Mr. Earhart concerning his service on the

Company’s Audit Committee and competing demands on his time, the Board has determined that Mr. Earhart’s simultaneous

service on the audit committees of three other public companies does not impair his ability to effectively serve on the

Company’s Audit Committee. The Audit Committee, which generally meets at least twice per quarter, once prior to quarterly

earnings releases and again prior to the filing of the Company’s quarterly and annual financial statements, appoints the

Company’s independent registered public accounting firm and is responsible for approving the services performed by the

Company’s independent registered public accounting firm and for reviewing and evaluating the Company’s accounting

principles and its systems of internal accounting controls. At each meeting, the Audit Committee first meets with Company

management and the Company’s independent registered public accounting firm in order to review financial results and conduct

other appropriate business. Then, the Audit Committee typically meets with the Company’s independent registered public

accounting firm, without the presence of management. The Audit Committee held a total of nine (9) meetings during Fiscal

2006.

The Leadership and Compensation Committee of the Board is currently composed of Mr. Esber, Chairman of the

Committee, Ms. Fetter and Mr. Partridge, all of whom are independent directors, as defined in the applicable New York Stock

Exchange listing standards. The Leadership and Compensation Committee generally meets in conjunction with Board meetings

and at other times as deemed necessary by the Committee or the Board. The Company’s lead independent director, Mr.

Wheelwright, typically attends the Committee meetings. The Committee's primary mission is to ensure the Company provides

and designs appropriate leadership and compensation programs to enable the successful execution of its corporate strategy and

objectives and to ensure the Company's programs and practices are competitive and consistent with corporate governance best

practices. The Committee has responsibility for reviewing the Company's strategy and practices relating to the attraction,

retention, development, performance and succession of its leadership team. The Committee also has responsibility for

approving all compensation packages for the Company’s Section 16 officers, including the CEO. The Leadership and

Compensation Committee held a total of six (6) meetings during Fiscal 2006.

The Corporate Governance and Nominating Committee is currently composed of Mr. Wheelwright, Chairman of the

Committee, Mr. Buchsbaum and Mr. Esber, all of whom are independent directors, as defined in the applicable New York

Stock Exchange listing standards. The Corporate Governance and Nominating Committee, which meets at least twice annually,

7

assists the Board by identifying and recommending prospective director nominees, develops corporate governance principles

for Quantum and advises the Board on corporate governance matters, advises the Board regarding Board composition,

procedures and committees, recommends to the Board a lead independent director, oversees the evaluation of the Board, and

considers questions of possible conflicts of interest of Board members and of senior executives. The Corporate Governance and

Nominating Committee will consider nominees recommended by stockholders pursuant to the procedures outlined in the

Company’s Bylaws and as set forth below. The Corporate Governance and Nominating Committee held three (3) meetings

during Fiscal 2006.

Each of our committees is governed by a written charter, copies of which are posted on our website. The Internet address

for our website is http://www.quantum.com, where the charters may be found by clicking “Investors” from the home page and

selecting “Corporate Governance.” A free printed copy of the charters also is available to any stockholder who requests it from

Quantum’s Investor Relations Department at the address stated below in the Section of this Proxy Statement entitled

“Communicating with the Company” or who submits an online request by visiting the Company’s website at

http://www.quantum.com, where the request form may be found by clicking “Investors” from the home page and selecting

“Contact Investor Relations.”

COMMUNICATING WITH THE COMPANY

Consideration of Director Nominees

Stockholder Recommendations and Nominations

Recommendations

It is the policy of the Corporate Governance and Nominating Committee to consider recommendations for candidates to the

Board from stockholders. A stockholder that desires to recommend a candidate for election to the Board must direct the

recommendation in writing to Quantum Corporation, attention: Company Secretary, 1650 Technology Drive, Suite 700, San

Jose, CA 95110. The letter must include the candidate’s name, contact information, detailed biographical data, relevant

qualifications (in light of Quantum’s established director considerations, as described below), information regarding any

relationships between the candidate and Quantum, a statement from the recommending stockholder in support of the candidate,

references, and a written indication by the candidate of her or his willingness to serve, if elected.

Nominations

A stockholder that desires to nominate a person directly for election to the Board must meet the deadlines and other

requirements set forth in Section 2.5 of Quantum’s Bylaws, and the rules and regulations of the Securities and Exchange

Commission. Quantum’s Bylaws can be found on our website. The Internet address for our website is

http://www.quantum.com, where the Bylaws may be found by clicking “Investors” from the home page and then selecting

“Corporate Governance.”

Identifying and Evaluating Nominees for Director

The Corporate Governance and Nominating Committee uses the following procedures to identify and evaluate individuals

recommended or offered for nomination to the Board:

• The Committee regularly reviews the current composition and size of the Board.

• The Committee annually evaluates the performance of the Board as a whole and the performance and qualifications of

individual members of the Board eligible for re-election at the annual meeting of stockholders.

• In evaluating and identifying candidates, the Committee has the authority to retain and terminate any third party search

firm that is used to identify director candidates, and has the authority to approve the fees and retention terms of any

search firm.

• The Committee reviews the qualifications of any candidate who has been properly recommended or nominated by a

stockholder, as well as any candidate who has been identified by management, individual members of the Board or, if

the Committee determines, a search firm. Such review may, in the Committee’s discretion, include a review solely of

information provided to the Committee or may also include discussions with persons familiar with the candidate, an

interview with the candidate or other actions that the Committee deems proper, including the retention of third parties

to review potential candidates.

8

• The Committee will evaluate each candidate in light of the general and specific considerations that follow. The

Committee evaluates all nominees, whether or not recommended by a stockholder, in the same manner, as described in

this Proxy Statement.

• After reviewing and considering all candidates presented to the Committee, the Committee will recommend a slate of

director nominees to be approved by the full Board.

• The Committee will endeavor to promptly notify, or cause to be notified, all director candidates of its decision as to

whether to nominate such individual for election to the Board.

General Considerations

A candidate will be considered in the context of the current perceived needs of the Board as a whole. Generally, the

Committee believes that candidates and nominees must reflect a Board that is comprised of directors who (i) are predominantly

independent, (ii) are of high integrity, (iii) have qualifications that will increase overall Board effectiveness and (iv) meet other

requirements as may be required by applicable rules, such as financial literacy or financial expertise with respect to audit

committee members.

Specific Considerations

Specific considerations include the following:

• The current size and composition of the Board, and the needs of the Board and its committees.

• Previous experience serving on a public company board, or as a member of the senior management of a public

company.

• The possession of such knowledge, experience, skills, expertise and diversity so as to enhance the Board's ability to

manage and direct the affairs and business of the Company.

• Key personal characteristics such as strategic thinking, objectivity, independent judgment, integrity, intellect, and the

courage to speak out and actively participate in meetings.

• Knowledge of, and familiarity with, information technology.

• The absence of conflicts of interest with the Company’s business.

• A willingness to devote a sufficient amount of time to carry out his or her duties and responsibilities effectively,

including a commitment to serve on a committee.

• Whether the candidate is committed to serve on the Board for an extended period of time.

• Diversity of thinking or background.

• Such other factors as the Committee may consider appropriate.

The Company believes that all of the nominees for election to our Board meet the general and specific considerations

outlined above.

All of the nominees for election to our Board have previously served as Quantum directors.

Communications to the Board

Stockholders may contact any of our directors by writing to them c/o Quantum Corporation, attention: Company Secretary,

1650 Technology Drive, Suite 700, San Jose, CA 95110, or by email at BoardofDirectors@Quantum.com. Stockholders and

employees who wish to contact the Board or any member of the Audit Committee to report questionable accounting or auditing

matters may do so anonymously by using the address above and designating the communication as “confidential.”

Alternatively, concerns may be reported anonymously by phone or via the world-wide-web to the following toll-free phone

number or Internet address 1-866-ETHICSP (1-866-384-4277); www.ethicspoint.com. These resources are operated by

Ethicspoint, an external third-party vendor that has trained professionals to take calls, in confidence, and to report concerns to

the appropriate persons for proper handling. Communications raising safety, security or privacy concerns, or that otherwise

relate to improper activities will be addressed in an appropriate manner.

Director Compensation

During Fiscal 2006, each director who was not an employee of the Company (each, a “Non-Management Director”)

received a base annual retainer of $42,000, plus an additional annual retainer of $7,500 for each committee on which such

director served as a member. The aggregate retainer is paid 75% in cash and 25% in restricted stock. The restricted stock vests

50% upon grant and 50% after one year from the grant date provided that the director continues to be a member of Quantum’s

Board at that time. No per-meeting fees are paid. In addition, the Chairman of each Board Committee and the lead

9

independent director received the following annual retainers, all of which were paid in cash: $10,000 for the Chairman of the

Audit Committee and for the lead independent director and $7,500 for the Chairman of the Leadership and Compensation

Committee and for the Chairman of the Governance and Nominating Committee.

Options and restricted stock are granted to Non-Management Directors under the 2003 Nonemployee Director Equity

Incentive Plan (“Director Plan”), which was approved by the Company’s stockholders at the 2003 annual meeting of

Stockholders. The Board, in its discretion, selects Non-Management Directors to whom options may be granted, the time or

times at which such options may be granted, the number of shares subject to each grant and the period over which such options

become exercisable. During Fiscal 2006, Michael A. Brown, Alan L. Earhart, Edward M. Esber, Jr., and Steven C.

Wheelwright each received an option to purchase 18,750 shares of Common Stock. Mary Agnes Wilderotter, who left the

Company’s Board in Fiscal 2006, also received an option to purchase 18,750 shares of Common Stock. John M. Partridge,

who joined the Board in February 2005, received an option to purchase 9,375 shares of Common Stock. All options were

granted at an exercise price of $2.89. These options will fully vest on September 1, 2006. In addition, in Fiscal 2006, Quantum

granted to each of Elizabeth A. Fetter and Thomas S. Buchsbaum, both of whom joined the Board in that fiscal year, an option

to purchase 45,000 shares of Common Stock at the following exercise prices: $2.89 for Ms. Fetter’s option and $2.98 for Mr.

Buchsbaum’s option. The options granted to Ms. Fetter and Mr. Buchsbaum vest 25% approximately one year after they are

granted. Thereafter, the remaining options vest 1/36th per month over the next three years. All options granted to Non-

Management Directors in Fiscal 2006 contain the following terms: (i) the exercise price per share of Common Stock was 100%

of the fair market value of the Company’s Common Stock on the date the option was granted; (ii) the options expire seven

years after the date of grant; and (iii) the option may be exercised only while the director remains a director or within 12 months

after the date the director ceases to be a director of the Company, or such longer period as may be determined by the

administrator of the Director Plan. On November 14, 2005, the Leadership and Compensation approved an amendment to each

existing Board member stock option grant with a grant price greater than the closing price of Quantum’s stock on November

14, 2005 of $2.98 so that it terminates 12 months following termination of Board service rather than 90 days following such

termination, which had traditionally been the post-termination exercise period. Board member stock option grants with grant

prices less than $2.98 were not amended and continue to terminate 90 days following the termination of Board service.

The Board generally may amend or terminate the Director Plan at any time and for any reason, except that the Board will

obtain stockholder approval for material amendments to such plan, as required by the rules of the New York Stock Exchange.

Employee directors are not compensated for their service on the Board or on committees of the Board.

Leadership and Compensation Committee Interlocks and Insider Participation in Compensation Decisions

The members of the Company’s Leadership and Compensation Committee are Edward M. Esber, Jr., Chairman of the

Committee, Elizabeth A. Fetter and John M. Partridge. No member of the Leadership and Compensation Committee is

currently, nor has any been at any time since the formation of the Company, an officer or employee of the Company or any of

its subsidiaries. Likewise, no member of the Leadership and Compensation Committee has entered into a transaction, or series

of similar transactions, in which they will have a direct or indirect material interest adverse to the Company.

Required Vote

Each stockholder voting in the election of directors may cumulate such stockholder’s votes and give one candidate a

number of votes equal to the number of directors to be elected multiplied by the number of votes to which the stockholder’s

shares are entitled. Alternatively, a stockholder may distribute the stockholder’s votes on the same principle among as many

candidates as the stockholder would like, provided that votes cannot be cast for more than eight (8) candidates. However, no

stockholder shall be entitled to cumulate votes for a candidate unless such candidate’s name has been properly placed in

nomination according to the Company’s Bylaws and notice of the intention to cumulate votes is received at the principal

executive offices of the Company at least twenty (20), and no more than sixty (60), days prior to the Annual Meeting. The

proxy holders may exercise discretionary authority to cumulate votes and to allocate such votes among management’s

nominees in the event that additional persons are nominated at the Annual Meeting for election of directors.

If a quorum is present and voting, the eight nominees for director receiving the highest number of votes will be elected to

the Board. Votes withheld from any director are counted for purposes of determining the presence or absence of a quorum, but

have no other legal effect under Delaware law. See “Quorum; Abstentions; Broker Non-Votes.”

MANAGEMENT RECOMMENDS A VOTE “FOR” EACH OF THE NOMINEES LISTED ABOVE.

10

PROPOSAL TWO

RATIFICATION OF APPOINTMENT OF THE INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

The Board has selected Ernst & Young LLP as the Company’s independent registered public accounting firm to audit the

financial statements of the Company for the fiscal year ending March 31, 2007. The Board recommends that stockholders vote

for ratification of such appointment. In the event of a vote against such ratification, the Board of Directors will reconsider its

selection. A representative of Ernst & Young LLP is expected to be available at the Annual Meeting with the opportunity to

make a statement if such representative desires to do so, and is expected to be available to respond to appropriate questions. The

affirmative vote of a majority of the Votes Cast is required to ratify the appointment of Ernst & Young LLP.

MANAGEMENT RECOMMENDS A VOTE “FOR” THE RATIFICATION OF THE APPOINTMENT OF ERNST &

YOUNG LLP AS THE COMPANY’S INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM FOR THE

FISCAL YEAR ENDING MARCH 31, 2007.

11

EXECUTIVE COMPENSATION

Summary Compensation

The following table shows, as to any person serving as Chief Executive Officer during Fiscal 2006 and each of the four

other most highly compensated executive officers (the “Named Executive Officers”), information concerning compensation

paid for services to the Company in all capacities during Fiscal 2006, as well as the total compensation paid to each such

individual for the Company’s previous two fiscal years.

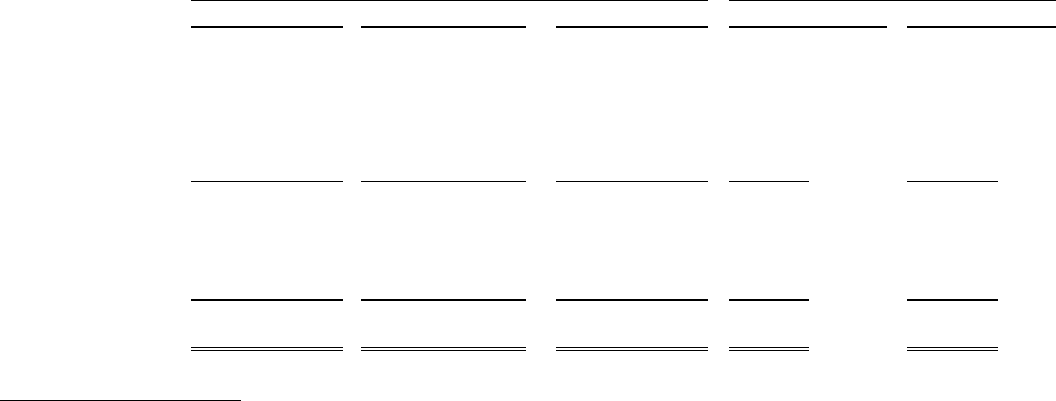

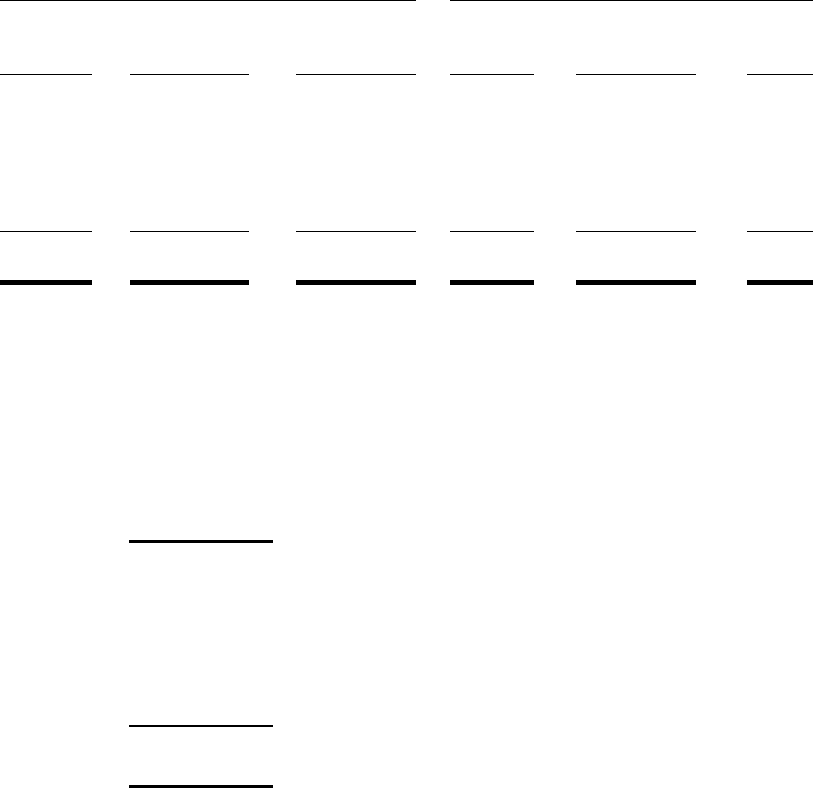

SUMMARY COMPENSATION TABLE

Annual Compensation Long-Term Compensation (1)

Name and Principal Position Fiscal

Year Salary ($) Bonus ($)

Other

Annual

Compensation

($)(2)

Restricted

Stock

Awards

($)(3)

Securities

Underlying

Options/S

ARs

(#)

All Other

Compensation

($)(4)

Richard E. Belluzzo …………………

Chief Executive Officer and Chairman

of the Board(*)

2006

2005

2004

648,269

597,692

600,000

—

250,000

—

—

—

89,093

(5)

—

81,900

—

(6)

—

—

2,000,000

7,115

5,977

1,615

Anthony E. Carrozza ………………

Senior Vice President of Worldwide

Sales

2006

2005

2004

315,000

313,788

315,000

—

10,000

—

78,314

150,866

138,327

(7)

(8)

(9)

61,838

73,711

—

(10)

(11)

262,500

52,500

100,000

5,900

6,370

5,810

Edward J. Hayes, Jr. …..………………

Executive Vice President and Chief

Financial Officer(**)

2006

2005

2004

350,004

269,234

—

20,000

10,000

—

—

—

—

24,735

296,000

—

(12)

(13)

325,000

400,000

—

7,069

3,431

—

Howard L. Matthews, III ……………

President and Chief Operating

Officer(***)

2006

2005

2004

280,003

37,019

—

(14) —

—

—

1,013,956

485,072

—

(15)

(16)

261,000

—

—

(17)

1,500,000

—

—

4,906

—

—

Jim L. Wold …………………………...

Senior Vice President, Removable

Storage and Automation(****)

_____________________

2006

2005

2004

264,615

46,723

—

—

—

—

78,699

196,834

—

(18)

(19)

61,838

28,875

—

(20)

(21)

462,500

127,500

—

2,869

—

—

(*) The amounts listed in the table reflect compensation paid to Mr. Belluzzo as Chief Executive Officer.

(**) Mr. Hayes, Jr. has been Executive Vice President and Chief Financial Officer of the Company since July 2004.

(***) Mr. Howard Matthews, III became the Company’s President and Chief Operating Officer on June 1, 2005.

(****) Mr. Wold has been the Company’s Senior Vice President, Removable Storage and Automation since January 2005.

(1) The Company has not granted any stock appreciation rights and does not have any long-term incentive plans, as that term

is defined in regulations promulgated by the SEC.

(2) Other annual compensation in the form of perquisites and other personal benefits, securities or property has been omitted

in those cases where the aggregate amount of such compensation is the lesser of either $50,000 or 10% of the total annual

salary and bonus reported for such executive officer.

(3) The restricted stock values set forth in the table are calculated as of the grant date while the footnotes to the numbers listed

in the table give a value as of March 31, 2006.

(4) Represents 401(k) plan matching contributions.

(5) $62,288 represents reimbursement for relocation expenses and $26,805 represents reimbursement for tax liabilities in

connection with reimbursement for these relocation expenses.

12

(6) Represents 35,000 shares of restricted stock, all of which vested on July 1, 2005. Based on the stock price on March 31,

2006, the value of the aggregate restricted stock holdings was $130,550. No dividends were paid on the restricted stock

holdings and Quantum currently does not expect to pay any dividends on such restricted stock holdings in the future.

(7) Represents sales commissions.

(8) $100,866 represents sales commissions and $50,000 represents loan forgiveness pursuant to the terms of a forgivable loan

granted to Mr. Carrozza on May 18, 2000. The loan was in the amount of $200,000, forgivable over four years, and

accrued interest at an annual rate of 8%.

(9) $88,327 represents sales commissions and $50,000 represents loan forgiveness pursuant to the terms of the forgivable loan

granted to Mr. Carrozza on May 18, 2000. See Note 8.

(10) Represents 21,250 shares of restricted stock, of which 5,313 shares vested on July 1, 2006, 5,313 shares are scheduled to

vest on July 1, 2007 and 5,312 shares are rescheduled to vest on each of July 1, 2008 and July 1, 2009, provided that Mr.

Carrozza continues to be employed by Quantum on those future dates. The value of the aggregate restricted stock

holdings, calculated as if they were fully vested as of March 31, 2006, was $79,263. No dividends were paid on the

restricted stock holdings and Quantum currently does not expect to pay any dividends on such restricted stock holdings in

the future.

(11) Represents, 26,400 shares of restricted stock, of which 3,650 shares vested on April 1, 2005, 5,500 shares vested on July 1,

2005, 10,250 shares vested on January 1, 2006, 3,500 shares vested on July 1, 2006 and 3,500 shares are scheduled to vest

on July 1, 2007, provided that Mr. Carrozza continues to be employed by Quantum on that future date. Based on the stock

price on March 31, 2006, the value of the aggregate restricted stock holdings was $98,472. No dividends were paid on the

restricted stock holdings and Quantum currently does not expect to pay any dividends on such restricted stock holdings in

the future.

(12) Represents 8,500 shares of restricted stock, of which 2,125 shares vested on July 1, 2006 and 2,125 shares are scheduled to

vest on each of July 1, 2007, July 1, 2008 and July 1, 2009, provided that Mr. Hayes continues to be employed by Quantum

on those future dates. The value of the aggregate restricted stock holdings, calculated as if they were fully vested as of

March 31, 2006, was $31,705. No dividends were paid on the restricted stock holdings and Quantum currently does not

expect to pay any dividends on such restricted stock holdings in the future.

(13) Represents 100,000 shares of restricted stock, of which 50,000 shares vested on July 1, 2004 and 25,000 vested on each of

July 1, 2005 and July 1, 2006. The value of the aggregate restricted stock holdings, calculated as if they were fully vested

as of March 31, 2006, was $373,000. No dividends were paid on the restricted stock holdings and Quantum currently does

not expect to pay any dividends on such restricted stock holdings in the future.

(14) Represents salary payments made by Quantum to Mr. Matthews as a Certance employee after Quantum’s acquisition of

Certance LLC.

(15) $25,000 represents reimbursement for commuting expenses, $825,000 represents severance payments pursuant to the

Transaction Bonus and Severance Protection Letter, dated January 4, 2005, between Mr. Matthews and Certance LLC, and

$163,956 represents payments for Certance LLC stock options made in connection with Quantum’s acquisition of Certance

LLC.

(16) $75,000 represents severance payments and $410,072 represents a transaction bonus paid to Mr. Matthews pursuant to a

Transaction Bonus and Severance Protection Letter, dated January 4, 2005 between Mr. Matthews and Certance LLC.

(17) Represents 100,000 shares of restricted stock, of which 25,000 vested on June 1, 2006 and 25,000 are scheduled to vest on

each of June 1, 2007, June 1, 2008 and June 1, 2009, provided that Mr. Matthews continues to be employed by Quantum

on those future dates. The value of the aggregate restricted stock holdings, calculated as if they were fully vested as of

March 31, 2006, was $373,000. No dividends were paid on the restricted stock holdings and Quantum currently does not

expect to pay any dividends on such restricted stock holdings in the future.

(18) Represents payments for Certance LLC stock option made in connection with Quantum’s acquisition of Certance LLC.

(19) Represents a transaction bonus paid to Mr. Wold pursuant to a Transaction Bonus and Severance Protection Letter, dated

January 4, 2005 between Mr. Wold and Certance LLC.

(20) Represents 21,250 shares of restricted stock, of which 5,313 shares vested July 1, 2006, 5,313 shares are scheduled to vest

on July 1, 2007 and 5,312 shares are scheduled to vest on each of July 1, 2008 and July 1, 2009, provided that Mr. Wold

continues to be employed by Quantum on those future dates. The value of the aggregate restricted stock holdings,

calculated as if they were fully vested as of March 31, 2006, was $79,263. No dividends were paid on the restricted stock

holdings and Quantum currently does not expect to pay any dividends on such restricted stock holdings in the future.

(21) Represents 10,500 shares of restricted stock, of which 3,500 shares fully vested on January 25, 2006 and 3,500 shares are

scheduled to vest on each of January 25, 2007 and January 25, 2008, provided that Mr. Wold continues to be employed by

Quantum on those future dates. The value of the aggregate restricted stock holdings, calculated as if they were fully vested

as of March 31, 2006, was $39,165. No dividends were paid on the restricted stock holdings and Quantum currently does

not expect to pay any dividends on such restricted stock holdings in the future.

13

Stock Option Grants and Exercises

The following tables show, as to each Named Executive Officer, information concerning stock options granted during

Fiscal 2006.

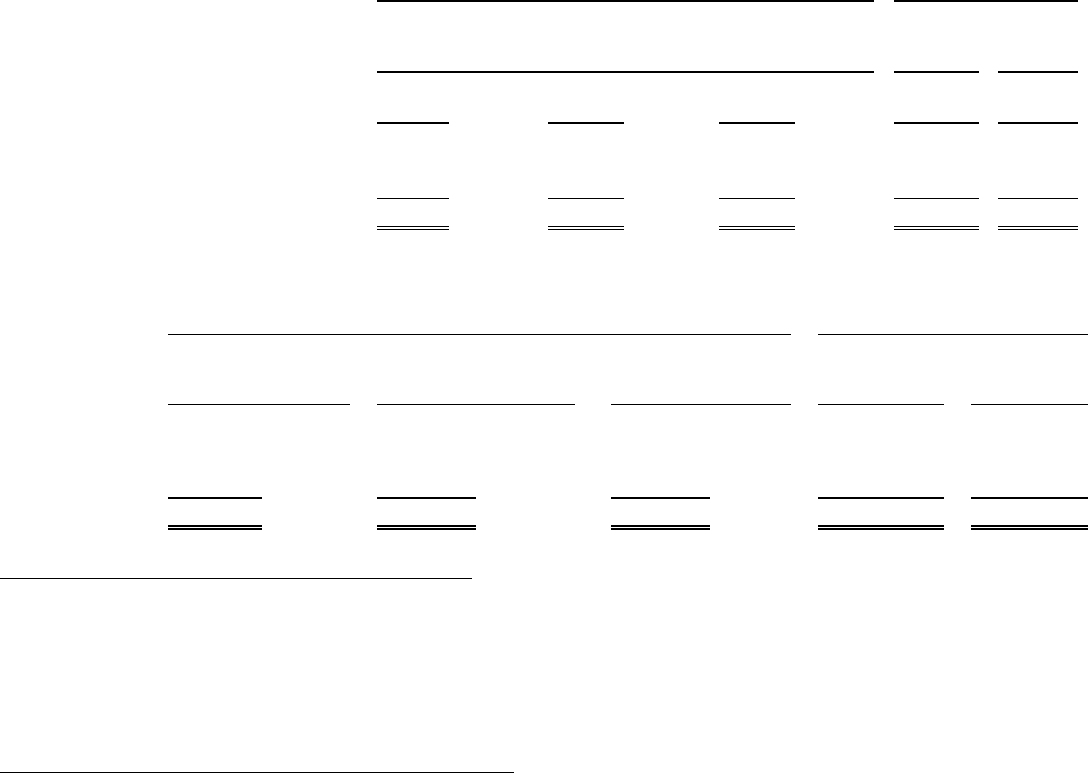

OPTION GRANTS IN FISCAL 2006

Individual Grants

Number of

Securities

Underlying

Options Granted

Percent of Total

Options Granted to

Employees in Fiscal

Year 2006

Expiration

Potential Realizable Value

at Assumed Annual Rates

of Stock Price

Appreciation

for Option Terms (3)

Name (#)(1) (2)

Exercise

Price

($/share) Date 5% ($) 10% ($)

Richard E. Belluzzo………... — — — — — —

Anthony E. Carrozza..……… 200,000 3.33% $2.62 05/31/2012 213,222 496,861

………... 62,500 1.04% $2.92 06/28/2012 74,296 173,141

Edward J. Hayes, Jr. ……….. 300,000 4.99% $2.62 05/31/2012 319,833 745,292

………... 25,000 0.42% $2.92 06/28/2012 29,718 69,256

Howard L. Matthews, III…… 1,500,000 24.97% $2.62 05/31/2012 1,599,166 3,726,459

Jim L. Wold ………………… 400,000 6.66% $2.62 05/31/2012 426,444 993,722

…………... 62,500 1.04% $2.92 06/28/2012 74,296 173,141

(1)

The exercise price of each option is determined by the Leadership and Compensation Committee of the Board of Directors and

in Fiscal 2006 was not less than 100% of the fair market value of the Common Stock on the date of grant. The options may be

exercised only while the optionee provides services to the Company or within such period of time following termination of the

optionee’s services to the Company as is determined by the Board. The options for the Named Executive Officers listed above

expire approximately seven years from the date of grant and vest monthly over four years beginning at or about the time o

f

grant.

(2) Based on options to purchase an aggregate of 6,007,929 shares of the Company’s Common Stock granted to employees of the

Company in Fiscal 2006, including the Named Executive Officers.

(3) Potential realizable value is based on an assumption that the stock price of the Common Stock appreciates at the annual rate

shown (compounded annually) from the date of grant until the end of the option term. These numbers are calculated based on

the regulations promulgated by the SEC based on an arbitrarily assumed annualized compound rate of appreciation of the

market price of 5% and 10% from the date the option was granted to the end of the option term, less the exercise price. Actual

gains, if any, on option exercises are dependent on the future performance of the Common Stock.

14

The following table provides information regarding options exercised by Named Executive Officers during Fiscal 2006 and

options held by them at fiscal year end.

AGGREGATED OPTION EXERCISES IN FISCAL 2006 AND

FISCAL YEAR-END OPTION VALUES

Shares

Acquired on

Value

Realized

Number of Securities

Underlying Unexercised Options

Held at Fiscal Year-End (#)

Value of Unexercised In-the-

Money Options Held at Fiscal

Year-End ($) (2)

Name Exercise (#) ($)(1) Exercisable Unexercisable Exercisable Unexercisable

Richard E. Belluzzo…………………… — — 3,277,777 722,223 1,368,888 171,112

Anthony E. Carrozza…………………. — — 409,061 249,209 208,125 255,050

Edward J. Hayes, Jr.………………….. — — 227,082 497,918 194,749 469,751

Howard L. Matthews, III…………….. — — 0 1,500,000 0 1,680,000

Jim L. Wold………………………….. — — 121,040 468,960 129,687 502,763

(1)

Total value realized is calculated based on the fair market value of the Common Stock at the close of business on the date o

f

exercise, less the exercise price.

(2) Total value of unexercised options is based on $3.74 per share of Common Stock, the fair market value of the Common Stock

as of March 31, 2006, less the exercise price.

Employment Terms, Termination of Employment and Change-In-Control Arrangements

The Company entered into agreements (the “Agreements”) with its Named Executive Officers whereby in the event that

there is a “change of control” of the Company (which is defined in the Agreements to include, among other things, a merger or

sale of all or substantially all of the assets of the Company or a reconstitution of the Company’s Board) and, within 18 months

of the change of control, there is an “Involuntary Termination” of such executives’ employment, then the executives are entitled

to specified severance compensation and benefits. The Agreements define “Involuntary Termination” to include, among other

things, any termination of the employee by the Company without “cause” or a significant reduction of the employee’s duties

without such employee’s express written consent.

For the CEO, the principal severance benefits are as follows: (1) 300% of the CEO’s then established base compensation;

(2) 300% of the average of the CEO’s actual annual bonuses received over the previous two (2) years; (3) payment of COBRA

premiums for twelve (12) months; (4) vesting of any unvested equity-based compensation award then held by the CEO; and (5)

if applicable, a gross-up payment in the amount of any excise tax incurred by the CEO as a result of the benefits received under

the Agreement. For the other Named Executive Officers the principal benefits are: (1) 200% of the officer’s then established

base compensation; (2) 200% of the average of the officer’s actual annual bonuses received over the previous two (2) years; (3)

payment of COBRA premiums for twelve (12) months; (4) vesting of any unvested equity-based compensation award then held

by the officer; and (5) if applicable, a gross-up payment in the amount of any excise tax incurred by the officer as a result of the

benefits received under the Agreement. The purpose of the Agreements is to ensure that the Company will have the continued

dedication of its officers by providing such individuals with compensation arrangements that are competitive with those of

other corporations, to provide sufficient incentive to the individuals to remain with the Company, to enhance their financial

security, as well as protect them against unwarranted termination in the event of a change of control.

If Mr. Belluzzo is constructively terminated or involuntarily terminated by the Company other than for “cause”, he will

receive a payment in the amount of 18 months base salary. If Mr. Belluzzo leaves the Company within four (4) years of his start

date of September 3, 2002, he must repay his $1,000,000 real estate compensation supplement, less $250,000 for each year of

employment; provided that should he leave pursuant to a constructive termination or an involuntary termination (other than for

“cause”), the repayment will be determined as if Mr. Belluzzo had been employed by the Company for an additional twelve

(12) months following his termination date.

15

In connection with the termination of Mr. Gannon as the Company’s President and Chief Operating Officer on May 27,

2005, the Company entered into an agreement to pay Mr. Gannon $500,010 in cash in a single lump sum and $123,067.50 in

cash, representing the cash value of his unvested restricted stock valued as of the termination date. In addition, the vesting of

his unvested stock options has been accelerated by 12 months and the exercise period for his vested stock options was extended

to May 26, 2006. He is also entitled to receive relocation assistance through June 2006 in an amount currently estimated to be

$107,658. In accordance with the terms of a forgivable loan that Quantum had granted to Mr. Gannon on October 18, 2001,

Quantum released Mr. Gannon from any obligation to repay the outstanding principal portion of and interest accrued on this

loan in the total amount of $31,000.

In connection with the termination of Mr. Kreigler’s employment as the Company’s Senior Vice President and General

Manager of the Storage Systems business unit on June 1, 2005, the Company entered into an agreement to pay Mr. Kreigler

$304,500 in a single lump sum.

In connection with the hiring of Howard L. Matthews III as the Company’s President and Chief Operating Officer as of

June 1, 2005, Quantum entered into an employment offer letter with Mr. Matthews pursuant to which Mr. Matthews receives an

annual salary of $350,000 and pursuant to which he received 1,500,000 stock options and 100,000 shares of restricted stock.

25% of the stock options fully vested on June 1, 2006 and the remainder will vest monthly thereafter at the rate of 1/48th of the

original grant amount over the following three years. 25% of the restricted stock vested on June 1, 2006 and 25% is scheduled

to vest on each of June 1, 2007, June 1, 2008 and June 1, 2009, provided that Mr. Matthews continues to be employed by

Quantum on such dates. To assist with commuting expenses, Quantum will also pay Mr. Matthews $25,000 in cash annually.

In the event the employment of Mr. Matthews is terminated involuntarily other than for “cause”, where there has not occurred a

change of control, he will receive: i) the equivalent of 52 weeks base salary; ii) the equivalent of 12 months benefits coverage;

and iii) the greater of a) accelerated vesting of 50% of his unvested stock options and restricted stock, or b) 12 months of

accelerated vesting of his unvested stock options and restricted stock. On January 4, 2005, Mr. Matthews entered into a

Transaction Bonus and Severance Protection Letter with Certance LLC, which was subsequently acquired by Quantum.

Pursuant to this agreement, Mr. Matthews received a cash transaction bonus of $410,072 and severance benefits of $900,000

due to the termination of his employment with Certance LLC.

In connection with the hiring of Mr. Hayes as Chief Financial Officer as of July 1, 2004, Quantum and Mr. Hayes entered

into an employment offer letter pursuant to which Mr. Hayes receives an annual salary of $350,000 and pursuant to which he

received 400,000 stock options and 100,000 shares of restricted stock. 25% of the stock options vested on July 1, 2005 and the

remainder vests monthly thereafter at the rate of 1/48th of the original grant amount over the following three years. 50% of the

restricted stock vested on July 1, 2004, 25% vested on July 1, 2005 and the remaining 25% vested on July 1, 2006. In the event

the employment of Mr. Hayes is terminated involuntarily where there has not occurred a change of control, he will receive: i)

the equivalent of 52 weeks base salary; ii) the equivalent of 12 months benefits coverage; and iii) the greater of a) accelerated

vesting of 50% of his unvested stock options and restricted stock, or b) 12 months of accelerated vesting of his unvested stock

options and restricted stock.

REPORT OF THE LEADERSHIP AND COMPENSATION COMMITTEE OF THE BOARD OF DIRECTORS1

Introduction

The Leadership and Compensation Committee (the “Committee”) of the Board of directors consists of Edward M. Esber,

Jr., John M. Partridge and Elizabeth A. Fetter. Mary Agnes Wilderotter served on the Committee until her resignation from the

Board on March 1, 2006. Mr. Esber serves as Chairman of the Committee. None of these individuals had any interlocking

relationships and all qualify as “outside directors” and “nonemployee directors” as defined by the Internal Revenue Code and

the Securities Exchange Act of 1934, respectively. During fiscal year 2006 the Committee met six times.

The Committee has responsibility for annually reviewing and approving the Company’s total compensation philosophy,

strategy and practices and administering the Company’s executive compensation plans and stock incentive plans. The

Committee reviews the Company’s strategy and practices relating to the retention, development, performance and succession of

its employees and approves all compensation actions for the Company’s executive officers including all Named Executive

Officers. The Company’s Human Resource organization and independent compensation consultants provide support to the

Committee.

1 This report of the Leadership and Compensation Committee of the Board of Directors shall not be deemed “soliciting material,” nor is it to be filed with the

SEC, nor incorporated by reference in any filing of the Company under the Securities Act of 1933, or the Securities Exchange Act of 1934, whether made

before or after the date hereof and irrespective of any general incorporation language in any such filing.

16

A more complete description of the Committee’s charter and responsibilities may be found on the Company’s website.

The Internet address for the website is http://www.quantum.com, where the charter may be found by clicking “Investors” from

the home page and selecting “Corporate Governance.”

General Total Compensation Philosophy

The objectives of the Company’s total compensation philosophy are to:

• Enable the achievement of the Company’s long and short term strategic goals

• Attract and retain the best talent needed to accomplish those strategies

• Ensure compensation levels are competitively benchmarked against a peer group

• Provide a strong link between pay and performance on both an individual and Company level

• Align long term incentives with stockholders’ interests

• Take into consideration economic and market conditions

This philosophy applies to all employees, with a more significant level of variability and compensation at risk as an

employee’s level of responsibility increases. The Company incorporates these objectives in the design of the following