TaxYear 2013 Resident_Booklet MD 512 FE Resident Booklet

User Manual: MD 512 FE

Open the PDF directly: View PDF ![]() .

.

Page Count: 32

Scan to check your refund

status after ling.

In 1989, the Maryland Blue Crab (Callinectes sapidus Rathbun) was designated the State Crustacean. Its

scientic name honors Mary Jane Rathbun (1860-1943), the scientist who described the species in 1896.

The blue crab’s scientic name translates as “beautiful swimmer that is savory.”

MARYLAND

Peter Franchot, Comptroller

2013 STATE & LOCAL TAX FORMS & INSTRUCTIONS

For ling personal state and local income taxes for full- or part-year Maryland residents

A Message from

Comptroller Peter Franchot

Dear Maryland Taxpayers:

Ove r the las t s even year s, it has been my privilege to s er ve as Mar ylan d’s Comptr oller. I’ve trie d

to honor the legacy of my legendary predecessors – Louis Goldstein, William Donald Schaefer

and Millard Tawes – and also forge my own path by promoting scal responsibility, fostering a

fair and predictable regulatory environment and providing superior taxpayer service.

The agency’s dedication to customer service remains my top priority. I recently announced

my renewed commitment to this endeavor with the introduction of my “Three R’s of Taxpayer

Service” – a guide post for the way we do business in the Comptroller’s Ofce.

My employees are committed to providing Respect, Responsiveness and Results to every

taxpayer we serve, each and every day. Whether it’s a phone operator, front line staff at

one of the agency’s 12 branch ofces or a member of my senior staff, I’ve asked each of the

hardworking members of our team to redouble our commitment to providing outstanding

service to the citizens of Maryland.

One of the ways we can serve Marylanders most effectively in these tough times is to give

taxpayers back their money as quickly as possible. You can “help us, help you” by ling your

individual state tax returns electronically this year. It is the fastest, easiest and most secure

way to le taxes, and it saves the state millions in administrative costs. Most importantly, it

generally allows you to receive your refund within three business days if you choose to direct

deposit. Electronic ling is one of the many commonsense, cost-saving approaches we have

employed at the agency to achieve better results for taxpayers at a lower cost.

The Comptroller’s website offers easy, step-by-step assistance in completing your state income

tax return for FREE through the agency’s iFile program. For those who prefer in-person tax

assistance, we continue to offer free, state tax assistance at all of the agency’s 12 taxpayer

service ofces.

I’m proud of the enduring tradition of excellence by our 1,100 agency employees who work

hard each day to ensure you have the service you deserve as taxpayers.

As your Comptroller, I will continue to be an independent voice and scal watchdog, safeguarding

your hard-earned tax dollars and promoting the long-term scal health of the State of Maryland.

Sincerely,

Peter Franchot

i

TABLE OF CONTENTS

Filing Information ...........................ii

INSTRUCTION .....................PAGE

1. Do I have to le? .........................1

2. Use of federal return .......................2

3. Form 502 or 503 .........................2

4. Name and Address ........................2

5. Social Security Number(s) ...................2

6. County, city, town information ................2

7. Filing status .............................2

8. Special instructions for married ling separately. ...2

9. Part-year residents ........................4

10. Exemptions .............................4

11. Income ................................4

12. Additions to income .......................4

13. Subtractions from income ................. 5-8

14. Itemized Deductions .......................8

15. Figure your Maryland Adjusted Gross Income .....8

16. Figure your Maryland taxable net income ........8

17. Figure your Maryland tax. . . . . . . . . . . . . . . . . . . 10

18. Earned income credit, poverty level credit and

credits for individuals and business tax credits ..10-12

19. Local income tax and local credits ............12

20. Total Maryland tax, local tax and contributions ...12

21. Taxes paid and refundable credits. ............13

22. Overpayment or balance due ................13

23. Telephone numbers, code number, signatures and

attachments. ...........................14

24. Electronic and PC ling, mailing and payment

instructions, deadlines and extension. ..........14

25. Fiscal year. ............................15

26. Special instructions for part-year residents. ......15

27. Filing return of deceased taxpayer ............16

28. Amended returns ........................16

29. Special instructions for military taxpayers .......17

• Tax Tables .........................18-24

Other information included in this booklet:

• Privacy act information

• State Department of Assessments and Taxation

Information

NEW FOR 2013

Inclusive language: We have modied our instructions to use

more inclusive language as a result of Maryland’s recognition of

same sex marriage.

Reporting your Federal earned income: If you are claiming a

federal Earned Income Credit (EIC), enter the earned income you

used to calculate your federal EIC on line 1b. on Form 502. Earned

income includes wages, salaries, tips, professional fees and other

compensation received for personal services you performed. It

also includes any amount received as a scholarship that you

included in your federal adjusted gross income.

Limits on your itemized deductions: Limits on itemized

deductions based on your income level has returned to both the

federal and Maryland returns. In addition, Maryland has decoupled

from the federal 2013 itemized deduction threshold limiting

itemized deductions. See Instruction 14 for more information.

(Use calculator at www.marylandtaxes.com.)

New subtraction modications: There are two new subtraction

modications available. See Instructions 13 for more information.

New business tax credits: There are four new business tax

credits available. See Instructions to Form 500CR available at

www.marylandtaxes.com.

New income tax credit of Form 502CR: Health Enterprise Zone

Practitioner Tax Credit. If you are a qualied “Health Enterprise

Zone (HEZ) Practitioner,” you may be able to claim a credit against

your state tax liability for income that you earned for practicing

health care in a HEZ.

Electronic Format: The paper version of Maryland Form 500CR

Business Income Tax Credits no longer is available. You must le

your Maryland return electronically to claim the business income

credits available from Form 500CR. Form 500CR Instructions are

available at www.marylandtaxes.com.

Attachment Sequence Numbers: Most of our major paper

resident tax returns have Attachment Sequence Numbers to aid in

the placement order of tax returns to speed tax return processing.

GETTING HELP

• Ta x Fo rms, Tax Tip s , Br oc hures and In s t r uc t i ons: These

are available online at www.marylandtaxes.com and branch

ofces of the Comptroller (see back cover). For forms only,

call 410-260-7951.

• Telephone: Februar y 3 - April 15, 2014, 8:00 a.m. until 7:00

p.m., Monday through Friday. From Central Maryland, call

410-260-7980. From other locations, call 1-800-MDTAXES

(1-800-638-2937).

• Email: Contact taxhelp@comp.state.md.us.

• Extensions: To telele an extension, call 410-260-7829; to

le an extension online, visit www.marylandtaxes.com.

RECEIVING YOUR REFUND

• Direct Deposit: To have your refund deposited to your bank

or other nancial account, enter your account and routing

numbers at the bottom of your return.

• Deposit of Income Ta x Refun d t o m o r e t han on e a c c ount:

Form 588 allows income tax refunds to be deposited to more

than one account. See Instruction 22 for more information.

Check with your nancial institution to make sure your direct

deposit will be accepted and to get the correct routing and

account numbers. The State of Maryland is not responsible

for a lost refund if you enter the wrong account information.

Verify Your Tax Preparer

If you use a paid tax preparer in Maryland, other than a CPA, Enrolled Agent or attorney, make sure the preparer is registered with the Maryland Board of Individual

Tax Preparers.

You can check the REGISTRATION SEARCH on the Department of Labor, Licensing and Regulation Web site: http://www.dllr.state.md.us/license/taxprep

You can check the LICENSE SEARCH for CPAs on the Department of Labor, Licensing and Regulation Web site: http://www.dllr.state.md.us/license/cpa/

You can check the ACTIVE STATUS for attorneys on the Maryland Courts Web site: http://www.courts.state.md.us/cpf/attylist.html

ii

• Check: Unless otherwise requested, we will mail you a paper

check.

• Refund Information: To request information about your

refund, see OnLine Services at www.marylandtaxes.com,

or call 410-260-7701 from central Maryland. From other

locations, call 1-800-218-8160.

FILING ELECTRONICALLY

• Go Green! eFile saves paper. In addition, you will receive

your refund faster; receive an acknowledgement that your

return has been received; and, if you owe, you can extend

your payment date until April 30th if you both eFile and make

your payment electronically.

• Security: Yo ur infor matio n is tran s mit te d se cur ely when yo u

choose to le e le c tr onic ally. It is p r otec ted by s eve r al s e c urit y

measures, such as multiple rewalls, state of the art threat

detection and encrypted transmissions.

• iFile: Fr e e Internet ling is available for Mar ylan d inc ome t a x

returns with no limitation. Visit www.marylandtaxes.com

and click iFile for eligibility.

• PC Retail Software: Check the software requirements to

de t e r mine eFil e e ligi bilit y be f o r e you pur c hase c omme r cial of f-

the-shelf software. Use software or link directly to a provider

site to prepare and le your return electronically.

• eFile: Ask yo ur pr ofe s s ional tax prepar er to eFil e your retur n.

You may use any tax professional who participates in the

Maryland Electronic Filing Program.

• IRS Free File: Free Internet ling is available for federal

income tax returns; some income limitations may apply.

Visit www.irs.gov for eligibility. Fees for state tax returns

also may apply; however, you may always return to www.

marylandtaxes.com to use the free iFile Internet ling for

Maryland income tax returns after using the IRS Free File for

your federal return.

AVOID COMMON ERRORS

• Social Security Number(s): Enter each Social Security

Number in the space provided at the top of your tax return.

Also enter the Social Security Number for children and other

de p e n dents. T he So c ial Se c urit y Nu mber will b e validated by

the IRS before the return has completed processing.

• L o c a l Ta x : Use the correct local income tax rate, based on

your county of residence on the last day of the tax year for

where you lived on December 31, 2013, or the last day of

the year for scal lers. See Instruction 19.

• Original Return: Please send only your original completed

Maryland tax return. Photocopies can delay processing of

your refund. If you led electronically, do not send a paper

return.

• Federal Forms: Do not send federal forms, schedules or

copies of federal forms or schedules unless requested.

• Photocopies: Remem b e r t o keep c opies of all fe d e r al f or m s

an d s c he dul e s and any oth e r d o c ument s that may be required

later to substantiate your Maryland return.

• Ink: Use only blue or black ink to complete your return. Do

not use pencil.

• Attachments: Ple a s e m ake sure to send all wag e s t atement s

such as W-2s, 1099s and K-1s. Ensure that the state tax

withheld is readable on all forms. Ensure that the state

in c o me m o dicati o ns and s t ate t ax credit s ar e clear l y shown

on all K-1s.

• Colored Paper: D o not pr int the Mar yland r e t urn o n colo r e d

paper.

• Bar Codes: Do not staple or destroy the bar code.

PAYING YOUR TAXES

• Direct Debit: If you le electronically and have a balance

due, you can have your income tax payment deducted

dir e c tl y from your b ank acc ount . Thi s free s er vi c e allows you

to choose your payment date, anytime until April 30, 2014.

Visit www.marylandtaxes.com for details.

• Bill Pay Electronic Payments: If your paper or electronic

tax return has a balance due, you may pay electronically at

www.marylandtaxes.com by sele ctin g B illPay. The amo unt

you designate will be debited from your bank or nancial

institution on the date that you choose.

• Checks and Money Orders: Make check or money order

payable to Comptroller of Maryland. We recommend you

in c lude your Social Secur it y Number on your check o r mo ney

or der.

ALTERNATIVE PAYMENT METHODS

For alternative methods of payment, such as a credit card, visit

our Web site at www.marylandtaxes.com.

GET YOUR 1099-G ELECTRONICALLY

Go to our web site www.marylandtaxes.com to sign up to

receive your 1099-G electronically. Once registered, you can

download and print your 1099-G from our secure Web site

www.marylandtaxes.com

PRIVACY ACT INFORMATION

The Tax-General Article of the Annotated Code of Maryland

authorizes the Revenue Administration Division to request

information on tax returns to administer the income tax laws

of Maryland, including determination and collection of correct

taxes. Code Section 10-804 provides that you must include

your Social Security Number on the return you le. This is so

we know who you are and can process your return and papers.

If you fail to provide all or part of the requested information,

exemptions, exclusions, credits, deductions or adjustments

may be disallowed and you may owe more tax. In addition, the

law provides penalties for failing to supply information required

by law or regulations.

You may look at any records held by the Revenue Administration

Division which contain personal information about you. You may

inspect such records, and you have certain rights to amend or

correct them.

As authorized by law, information furnished to the Revenue

Administration Division may be given to the United States

Internal Revenue Service, an authorized ofcial of any state

that exchanges tax information with Maryland and to an

ofcer of this State having a right to the information in that

ofcer’s ofcial capacity. The information may be obtained in

accordance with a proper legislative or judicial order.

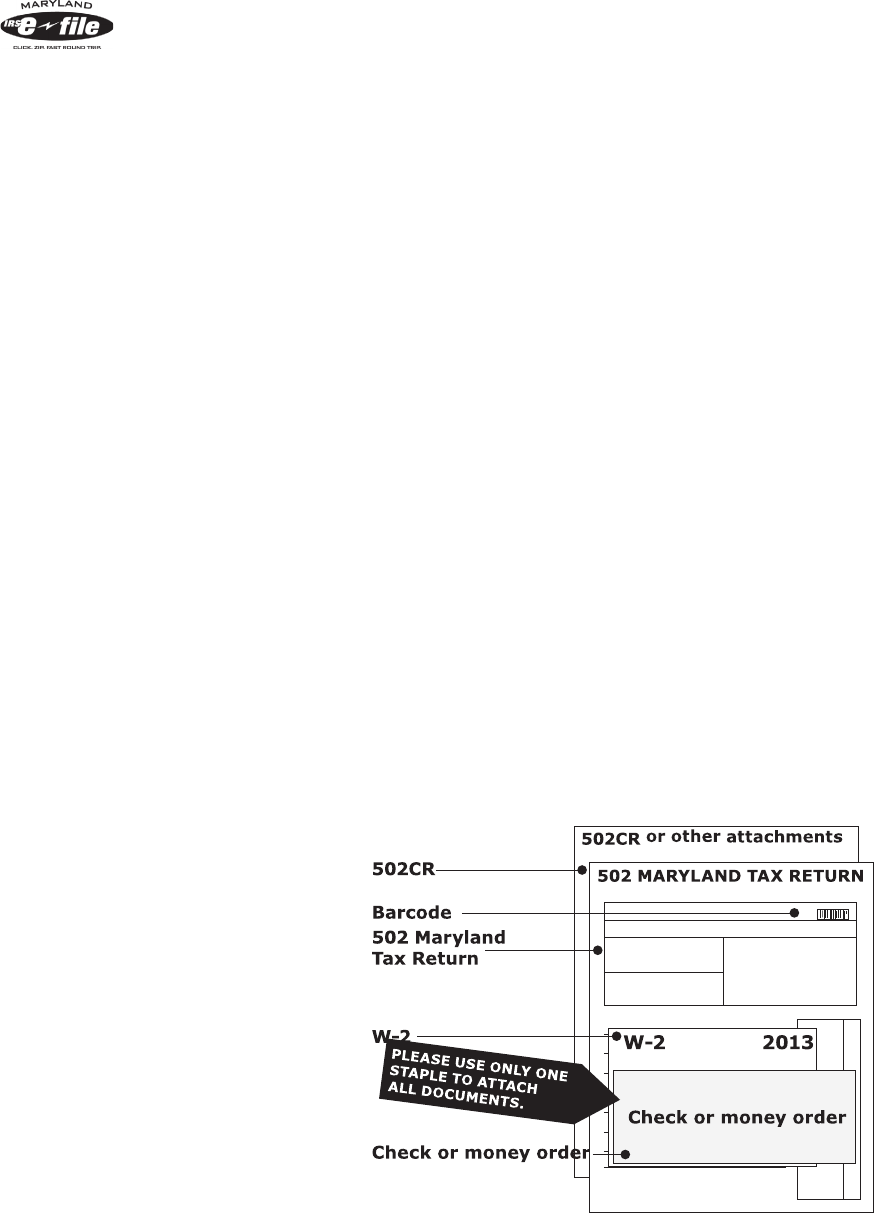

ASSEMBLING YOUR RETURN

WHAT YOU SHOULD SEND:

• Your original, completed Maryland income tax return (Form 502

iii

SERVICES FOR INDIVIDUALS

Bill Pay - Personal Taxes . . . . . . . . . . . . . . .https://interactive.marylandtaxes.com/Individuals/Payment/

iFile - Personal Taxes . . . . . . . . . . . . . . . . . .https://ile.marylandtaxes.com/

iFile - Estimated Taxes . . . . . . . . . . . . . . . . .https://interactive.marylandtaxes.com/Individuals/iFile_ChooseForm/default.asp#list

Estimated Tax Calculator for Tax Year 2013 . .https://interactive.marylandtaxes.com/webapps/percentage/502for2013.asp

Estimated Nonresident Tax Calculator . . . . . .http://interactive.marylandtaxes.com/Extranet/Calculators/estimatednr/default.aspx

Extension Request - Personal Tax . . . . . . . . .https://interactive.marylandtaxes.com/individuals/extension/default.asp

Individual Payment Agreement Request . . . . .https://interactive.marylandtaxes.com/extranet/compliance/payagr/

Refund Status . . . . . . . . . . . . . . . . . . . . . . .https://interactive.marylandtaxes.com/INDIV/refundstatus/home.aspx

Refund Questions . . . . . . . . . . . . . . . . . . . .http://taxes.marylandtaxes.com/Individual_Taxes/Individual_Tax_Types/Income_Tax/

Refund_Information/Questions_About_My_Refund.shtml

Unclaimed Property Search . . . . . . . . . . . . .https://interactive.marylandtaxes.com/individuals/unclaim/default.aspx

Income Tax Interest Calculator . . . . . . . . . . .http://taxes.marylandtaxes.com/Resource_Library/Online_Services/Interest_

Calculator/IntCalc.shtml

Appeals of Personal Income Tax Assessments and Refund Denials

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .https://interactive.marylandtaxes.com/extranet/compliance/harequest/default.aspx

Sign-up for future electronic 1099-G .......https://interactive.marylandtaxes.com/Individuals/paperless/1099g/default.asp

or 503) and Dependent Form 502B as applicable.

• Form 588 if you elect to have your refund direct deposited to

more than one account.

• W-2(s)/1099(s) showing Maryland tax withheld.

• K-1s showing Maryland tax withheld and or Maryland tax credit.

• If you have a balance due, and if not filing and paying

electronically, a check or money order payable to Comptroller

of Maryland with your Social Security Number on the check

or money order.

• Maryland schedules or other documents that may be required

according to the instructions if you claim certain credits or

subtractions. These may include the following: 500DM, 502CR,

502TP, 502UP, 502V, 502S and 502SU.

• A copy of the tax return you led in the other state if you’re

claiming a tax credit on Form 502CR, Part A.

DO NOT SEND:

• Photocopies of your Maryland return.

• Federal forms or schedules unless requested.

• Any forms or statements not requested.

• Returns by fax.

• Returns on colored paper.

• Returns completed in pencil.

• Returns with the bar code stapled or destroyed.

CollegeSavingsMD.org

How to Maximize Your

M

aryland 529 Tax Benefits

Did you know that the College Savings Plans of Maryland are the only 529

plans that oer a State income deduction to Maryland taxpayers? Here’s an

example of how your family could maximize their State income deduction.

• Maryland College Investment Plan (MCIP)

• Maryland Prepaid College Trust (MPCT)

$10,000 combined

annual income deduction

Visit CollegeSavingsMD.org for complete details.

Please carefully read the Enrollment Kit, available online, which describes the investment objectives, risks, expenses, and other important information that you should consider before you invest in the College

Savings Plans of Maryland. Also, if you or your beneficiary live outside of Maryland, you should consider before investing whether your state or your beneficiary’s state offers state tax or other benefits for

investing in its 529 plan. As with all State and Federal tax matters, please consult with your tax advisor.

Deduct up to $2,500 for each account/beneficiary you hold

in each plan. Deductions apply to Maryland taxable income

for your contributions in that tax year.

Each family member who opens an account

is eligible for income deductions

Contribute to both plans to increase

your income deductions

ANNUAL ACCOUNT HOLDER CONTRIBUTIONS

MCIP $2,500 $2,500 $2,500

MPCT $2,500 $2,500 $2,500

$5,000 $5,000 $5,000

PLANS

Account Holders can deduct contributions

regardless of their marital or tax filing

status (individual or joint).

AVAILABLE

PLANS:

1

RESIDENT INCOME TAX

RETURN INSTRUCTIONS

MARYLAND

FORMS

502

and

503

2013

DUE DATE

Your return is due by April 15, 2014. If you are a scal year taxpayer,

see Instruction 25. If any due date falls on a Saturday, Sunday or legal

holiday, the return must be led by the next business day.

To speed up the processing of your tax refund, consider ling

electronically. You must le within three years of the original due date

to receive any refund. Visit our Web site at www.marylandtaxes.

com.

COMPLETING THE RETURN

You must write legibly using blue or black ink when completing your

return.

DO NOT use pencil or red ink. Submit the original return, not a

photocopy. If no entry is needed for a specic line, leave blank. Do not

enter words such as “none” or “zero” and do not draw a line to indicate

no entry. Failure to follow these instructions may delay the processing

of your return.

You may round off all cents to the nearest whole dollar. Fifty cents

and above should be rounded to the next dollar. State calculations are

rounded to the nearest penny.

ELECTRONIC FILING INSTRUCTIONS

The instructions in this booklet are designed specically for lers of

paper returns.

If you are ling electronically and these instructions differ from the

instructions for the electronic method being used, you should comply

with the instructions appropriate for that method.

Free internet ling is available for Maryland income tax returns. Visit

www.marylandtaxes.com and select iFile.

Software vendors should refer to the e-le handbook for their

instructions.

SUBSTITUTE FORMS

You may le your Maryland income tax return on a computer-

prepared or computer-generated substitute form provided the form

is approved in advance by the Revenue Administration Division. The

fact that a software package is available for retail purchase does not

guarantee that it has been approved for use.

For additional information, see Administrative Release 26, Procedures

for Computer-Printed Substitute Forms, on our web site at www.

marylandtaxes.com.

PENALTIES

There are severe penalties for failing to le a tax return, failing to pay

any tax when due, ling a false or fraudulent return, or making a false

certication. The penalties include criminal nes, imprisonment and a

penalty on your taxes. In addition, interest is charged on amounts not

paid.

To collect unpaid taxes, the Comptroller is directed to enter liens

against the salary, wages or property of delinquent taxpayers.

TABLE 1

MINIMUM FILING LEVELS FOR TAXPAYERS UNDER 65

Single person (including dependent taxpayers) ..... $ 10,000

Joint Return ............................. $ 20,000

Married persons ling separately ............... $ 3,900

Head of Household ........................ $ 12,850

Qualifying widow(er) ....................... $ 16,100

TABLE 2

MINIMUM FILING LEVELS FOR TAXPAYERS 65 OR OVER

Single, age 65 or over ...................... $ 11,500

Joint Return, one spouse, age 65 or over ......... $ 21,200

Joint Return, both spouses, age 65 or over ....... $ 22,400

Married persons ling separately, age 65 or over ... $ 3,900

Head of Household, age 65 or over ............. $ 14,350

Qualifying widow(er), age 65 or over ............ $ 17,300

1

DO I HAVE TO FILE?

This booklet and forms are for residents of Maryland. In general, you

must le a Maryland return if you are or were a resident of Maryland

AND you are required to le a federal return. Information in this

section will allow you to determine if you must le a return and pay

taxes as a resident of Maryland. If you are not a resident but had

Maryland tax withheld or had income from sources in Maryland, you

must use Form 505 or 515, Nonresident Tax return.

WHO IS A RESIDENT?

You are a resident of Maryland if:

a. Your permanent home is or was in Maryland (the law refers to this

as your domicile).

OR

b. Your permanent home is outside of Mar yland, but you maintained

a place of abode (a place to live) in Maryland for more than

six months of the tax year. If this applies to you and you were

physically present in the state for 183 days or more, you must le

a full-year resident return.

PART-YEAR RESIDENTS

If you began or ended residence in Maryland during the tax year, you

must le a Maryland resident income tax return. See Instruction 26.

MILITARY AND OTHERS WORKING OUTSIDE OF MARYLAND

Military and other individuals whose domicile is in Maryland, but who

are stationed or work outside of Maryland, including overseas, retain

their Mar yland l egal re s id enc e. Mar yland re sid ence is not lo st bec aus e

of duty assignments outside of the State; see Administrative Release

37. Military personnel and their spouses should see Instruction 29.

TO DETERMINE IF YOU ARE REQUIRED TO FILE A MARYLAND

RETURN

a. Add up all of your federal gross income to determine your total

federal income. Gross income is dened in the Internal Revenue

Code and, in general, consists of all income regardless of source.

It includes wages and other compensation for services, gross

income derived from business, gains (not losses) derived from

dealings in proper ty, interest, rents, royalties, dividends, alimony,

annuities, pensions, income from partnerships or duciaries, etc.

If modications or deduc tions reduce your gross income below t he

minimum ling level, you are still required to le. IRS Publication

525 provides additional information on taxable and nontaxable

income.

b. Do not include Social Security or railroad retirement benets in

your total federal income.

c. Add to your total federal income any Maryland additions to income.

Do not include any additions related to periods of nonresidence.

See Instruction 12. This is your Maryland gross income.

d. If you are a dependent taxpayer, add to your total federal income

any Maryland additions and subtract any Maryland subtractions.

See Instructions 12 and 13. This is your Maryland gross

income.

e. You must le a Maryland return if your Maryland gross income

MINIMUM FILING LEVELS TABLES

2

equals or exceeds the income levels in the MINIMUM FILING

LEVEL TABLE 1.

f. If you or your spouse is 65 or over, use the MINIMUM FILING

LEVEL TABLE 2.

IF YOU ARE NOT REQUIRED TO FILE A MARYLAND RETURN

BUT HAD MARYLAND TAXES WITHHELD

To get a refund of Maryland income taxes withheld, you must le a

Maryland return.

Taxpayers who are ling for refund only should complete all of the

information at the top of Form 502 or Form 503 and complete the

following lines:

Form 502 Form 503

1-16 1, 7a*, 10a*

23*, 30* 13-19

35-43 21

45, 47

*Enter a zero unless you claim an earned income credit on your

federal return.

Sign the form and attach withholding statements (all W-2 and

1099 forms) showing Maryland and local tax withheld equal to the

withholding you are claiming. Your form is then complete.

2

USE OF FEDERAL RETURN.

First complete your 2013 federal income tax return.

You will need information from your federal return to complete your

Maryland return. Complete your federal return before you continue

beyond this point. Maryland law requires that your income and

deductions be entered on your Maryland return exactly as they were

reported on your federal return. If you use federal Form 1040NR,

visit our Web page at http://www.marylandtaxes.com/QR/19.

asp for further information. All items reported on your Maryland

return are subject to verication, audit and revision by the Maryland

State Comptroller’s Ofce.

3

FORM 502 OR 503?

Decide whether you will use Form 502 (long form) or Form

503 (short form). You must use Form 502 if your federal

adjusted gross income is $100,000 or more.

FORM 502

All taxpayers may use Form 502. You must use this form if you itemize

deductions, if you have any Maryland additions or subtractions, if

you have made estimated payments or if you are claiming business

or personal income tax credits. You must also use this form if you

have moved into or out of Maryland during the tax year.

Note: You must le Form 502 electronically if you are claiming

business income tax credits on Form 500CR.

FORM 503

If you use the standard deduction, have no additions or subtractions,

and claim only withholding or the refundable or other earned income

credits, you may use the short Form 503. Answer the questions

on the back of Form 503 to see if you qualify to use it. Do not use

Form 503 if you are claiming more than two dependents. NOTE:

If you are eligible for the pension exclusion, you must use

Form 502.

4

NAME AND ADDRESS.

Print using blue or black ink.

Enter your name exactly as entered on your federal tax return. If

you changed your name because of marriage, divorce, etc., be sure

to report the change to the Social Security Administration before

ling your return. This will prevent delays in the processing of your

return.

Enter your current address using the spaces provided. If using a

foreign address enter the city or town and state or province in the

“City or Town” box. Enter the name of the country in the “State” box.

Enter the postal code in the “ZIP Code” box.

5

SOCIAL SECURITY NUMBER(S) (SSN).

It is important that you enter each Social Security Number in

the space provided. You must enter each SSN legibly because

we validate each number. If not correct and legible, it will

affect the processing of your return.

The Social Security Number(s) (SSN) must be a valid number

issued by the Social Security Administration of the United States

Government. If you or your spouse or dependent(s) do not have a

SSN and you are not eligible to get a SSN, you must apply for an

Individual Tax Identication Number (ITIN) with the IRS and

you should wait until you have received it before you le; and

enter it wherever your SSN is requested on the return.

A missing or incorrect SSN or ITIN could result in the disallowance

of any credits or exemptions you may be entitled to and result in a

balance due.

A valid SSN or ITIN is required for any claim or exemption for a

dependent. If you have a dependent who was placed with you for

legal adoption and you do not know his or her SSN, you must get an

Adoption Taxpayer Identication Number (ATIN) for the dependent

from the IRS.

If your child was born and died in this tax year and you do not have

a SSN for the child, complete just the name and relationship of the

dependent and enter code 322, in one of the code number boxes

located to the right of the telephone number area on page 2 of the

form; attach a copy of the child’s death certicate to your return.

6

COUNTY, CITY, TOWN INFORMATION.

Fill in the boxes for MARYLAND COUNTY and CITY, TOWN or

TAXING AREA based on your residence on the last day of the

tax period:

BALTIMORE CITY RESIDENTS:

Leave the MARYLAND COUNTY box blank.

Write “Baltimore City” in the CITY, TOWN OR TAXING AREA box.

RESIDENTS OF MARYLAND COUNTIES (NOT BALTIMORE CITY):

1. Write the name of your county in the MARYLAND COUNTY box.

2. Find your county in the list below.

3. If you lived within the incorporated tax boundaries of one of the

areas listed under your county, write the name in the CITY, TOWN

OR TAXING AREA box.

4. If you did not live in one of the areas listed for your county, leave

the CITY, TOWN OR TAXING AREA box blank.

7

FILING STATUS.

Use the FILING STATUS chart to determine your ling status.

Check the correct FILING STATUS box on the return.

8

SPECIAL INSTRUCTIONS FOR MARRIED

PERSONS FILING SEPARATELY.

If you and your spouse le a joint federal return but are ling

separate Maryland returns according to Instruction 7, follow

the instructions below.

If you and your spouse le a joint federal return but are ling

separate Maryland returns according to Instruction 7, you should

report the income you would have reported had you led a separate

federal return. The income from jointly held securities, property,

etc., must be divided evenly between spouses.

If you itemized your deductions on the joint federal return, one

spouse may use the standard deduction and the other spouse may

claim those deductions on the federal return that are “attributable

exclusively” to that spouse, plus a prorated amount of the remaining

deductions. If it is not possible to determine these deductions, the

deduction must be allocated proportionately based on your share of

the income.

“Attributable exclusively” means that the individual is solely

3

If you are: Check the box for: Additional Information

SINGLE PERSON

(Single on the last day of the

tax year.)

Any person who can be claimed as a

dependent on his or her parent’s (or any

other person’s) federal return

Dependent

taxpayer

Filing Status 6

Single Dependent taxpayers, regardless of whether income is earned or unearned,

are not required to file a Maryland income tax return unless the gross income

including Maryland additions and subtractions is $10,000 or more. See Instruction

1 if you are due a refund. You do not get an exemption for yourself. Put a zero in

Exemption Box A.

Any person who filed as a head of

household on his or her federal return

Head of household

Filing Status 4

A qualifying widow(er) with dependent child

who filed a federal return with this status

Qualifying widow(er) with

dependent child

Filing Status 5

All other single persons Single

Filing Status 1

If your spouse died during the year AND you filed a joint federal return with your

deceased spouse, you may still file a joint Maryland return.

MARRIED PERSONS

(Married on the last day of the tax year.)

Any person who can be claimed as a

dependent on his or her parent’s (or any

other person’s) federal return

Dependent taxpayer

Filing Status 6

You do not get an exemption for yourself. Put a zero in Exemption Box A. You and

your spouse must file separate returns.

Any person who filed as a head of

household on his or her federal return

Head of household

Filing Status 4

Married couples who filed separate federal

returns

Married filing separately

Filing Status 3

Each taxpayer must show his or her spouse’s Social Security number in the blank

next to the filing status box.

Married couples who filed joint federal

returns but had different tax periods

Joint return

Filing Status 2

or Married filing separately

Filing Status 3

If you are not certain which filing status to use, figure your tax both ways to

determine which status is best for you. See Instructions 8 and 26(g) through (p).

Married couples who filed joint federal

returns but were domiciled in different

counties, cities, towns or taxing areas on

the last day of the year

Joint return

Filing Status 2

or Married filing separately

Filing Status 3

If you are filing separately, see Instruction 8. If you are filing a joint return see

SPECIAL NOTE in Instruction 19.

Married couples who filed joint federal

returns but were domiciled in different

states on the last day of the year

If you are filing separately, see Instruction 8. If you are filing a joint return, you must

attach a pro forma Form 505 and 505NR. See Administrative Releases 1 & 3.

All other married couples who filed joint

federal returns

Joint return

Filing Status 2

FILING STATUS

LIST OF INCORPORATED CITIES, TOWNS AND TAXING AREAS IN MARYLAND

ALLEGANY COUNTY

BARTON

BELAIR

BOWLING GREEN-

ROBERT’S PLACE

CRESAPTOWN

CUMBERLAND

ELLERSLIE

FROSTBURG

LAVALE

LONACONING

LUKE

MCCOOLE

MIDLAND

MT. SAVAGE

POTOMAC PARK

ADDITION

WESTERNPORT

ANNE ARUNDEL

COUNTY

ANNAPOLIS

HIGHLAND BEACH

BALTIMORE COUNTY

NO INCORPORATED

CITIES OR TOWNS

BALTIMORE CITY

CALVERT COUNTY

CHESAPEAKE BEACH

NORTH BEACH

CAROLINE COUNTY

DENTON

FEDERALSBURG

GOLDSBORO

GREENSBORO

HENDERSON

HILLSBORO

MARYDEL

PRESTON

RIDGELY

TEMPLEVILLE

CARROLL COUNTY

HAMPSTEAD

MANCHESTER

MT. AIRY

NEW WINDSOR

SYKESVILLE

TANEYTOWN

UNION BRIDGE

WESTMINSTER

CECIL COUNTY

CECILTON

CHARLESTOWN

CHESAPEAKE CITY

ELKTON

NORTH EAST

PERRYVILLE

PORT DEPOSIT

RISING SUN

CHARLES COUNTY

INDIAN HEAD

LA PLATA

PORT TOBACCO

DORCHESTER COUNTY

BROOKVIEW

CAMBRIDGE

CHURCH CREEK

EAST NEW MARKET

ELDORADO

GALESTOWN

HURLOCK

SECRETARY

VIENNA

FREDERICK COUNTY

BRUNSWICK

BURKITTSVILLE

EMMITSBURG

FREDERICK

MIDDLETOWN

MT. AIRY

MYERSVILLE

NEW MARKET

ROSEMONT

THURMONT

WALKERSVILLE

WOODSBORO

GARRETT COUNTY

ACCIDENT

DEER PARK

FRIENDSVILLE

GRANTSVILLE

KITZMILLER

LOCH LYNN HEIGHTS

MOUNTAIN LAKE PARK

OAKLAND

HARFORD COUNTY

ABERDEEN

BEL AIR

HAVRE DE GRACE

HOWARD COUNTY

NO INCORPORATED

CITIES OR TOWNS

KENT COUNTY

BETTERTON

CHESTERTOWN

GALENA

MILLINGTON

ROCK HALL

MONTGOMERY COUNTY

BARNESVILLE

BROOKEVILLE

CHEVY CHASE SEC. 3

TOWN OF CHEVY CHASE

(FORMERLY SEC. 4)

CHEVY CHASE SEC. 5

CHEVY CHASE VIEW

CHEVY CHASE VILLAGE

DRUMMOND

FRIENDSHIP HEIGHTS

GAITHERSBURG

GARRETT PARK

GLEN ECHO

KENSINGTON

LAYTONSVILLE

MARTIN’S ADDITION

NORTH CHEVY CHASE

OAKMONT

POOLESVILLE

ROCKVILLE

SOMERSET

TAKOMA PARK

WASHINGTON GROVE

PRINCE GEORGE’S

COUNTY

BERWYN HEIGHTS

BLADENSBURG

BOWIE

BRENTWOOD

CAPITOL HEIGHTS

CHEVERLY

COLLEGE PARK

COLMAR MANOR

COTTAGE CITY

DISTRICT HEIGHTS

EAGLE HARBOR

EDMONSTON

FAIRMOUNT HEIGHTS

FOREST HEIGHTS

GLENARDEN

GREENBELT

HYATTSVILLE

LANDOVER HILLS

LAUREL

MORNINGSIDE

MT. RAINIER

NEW CARROLLTON

NORTH BRENTWOOD

RIVERDALE PARK

SEAT PLEASANT

UNIVERSITY PARK

UPPER MARLBORO

QUEEN ANNE’S COUNTY

BARCLAY

CENTREVILLE

CHURCH HILL

MILLINGTON

QUEEN ANNE

QUEENSTOWN

SUDLERSVILLE

TEMPLEVILLE

ST. MARY’S COUNTY

LEONARDTOWN

SOMERSET COUNTY

CRISFIELD

PRINCESS ANNE

TALBOT COUNTY

EASTON

OXFORD

QUEEN ANNE

ST. MICHAELS

TRAPPE

WASHINGTON COUNTY

BOONSBORO

CLEARSPRING

FUNKSTOWN

HAGERSTOWN

HANCOCK

KEEDYSVILLE

SHARPSBURG

SMITHSBURG

WILLIAMSPORT

WICOMICO COUNTY

DELMAR

FRUITLAND

HEBRON

MARDELA SPRINGS

PITTSVILLE

SALISBURY

SHARPTOWN

WILLARDS

WORCESTER COUNTY

BERLIN

OCEAN CITY

POCOMOKE CITY

SNOW HILL

responsible for the payment of an expense claimed as an itemized

deduction, including compliance with a valid court order or separation

agreement; or the individual jointly responsible for the payment

of an expense claimed as an itemized deduction can demonstrate

payment of the full amount of the deduction with funds that are

not attributable in whole or in part, to the other jointly responsible

individual.

If both spouses choose to itemize on their separate Maryland

returns, then each spouse must determine which deductions are

attributable exclusively to him or her and prorate the remaining

deductions using the Maryland Income Factor. See Instruction

26(k). If it is not possible to determine deductions in this manner,

they must be allocated proportionately based on their respective

shares of the income. The total amount of itemized deductions for

both spouses cannot exceed the itemized deductions on the federal

return.

If yo u c h o os e to u s e t h e st a n d a r d de d u c tion m e t h o d, u s e S TA N DAR D

DEDUCTION WORKSHEET (16A) in Instruction 16. Each spouse must

claim his or her own personal exemption. Each spouse may allocate

the dependent exemptions in any manner they choose. The total

number of exemptions claimed on the separate returns may not

exceed the total number of exemptions claimed on the federal return

except for the additional exemptions for being 65 or over or blind.

Complete the remainder of the form using the instructions for

each line. Each spouse should claim his or her own withholding and

other credits. Joint estimated tax paid may be divided between the

spouses in any manner provided the total claimed does not exceed

the total estimated tax paid.

4

EXEMPTION AMOUNT CHART

The personal exemption is $3,200. This exemption is reduced once the taxpayer’s federal adjusted gross income exceeds $100,000 ($150,000

if ling Joint, Head of Household, or Qualifying Widow(er) with Dependent Child). This reduction applies to the additional dependency

exemptions as well; however it does not apply to the taxpayer’s age or blindness exemption of $1,000. Use the chart to determine the

allowable exemption amount based upon the ling status. NOTE: For certain taxpayers with interest from U.S. obligations see Instruction 13,

line 13, code hh for applicable exemption adjustment.

If Your federal AGI is

Single or Married Filing

Separately

Each Exemption is

Joint, Head of Household

or Qualifying Widow(er)

Each Exemption is

Dependent Taxpayer (eligible

to be claimed on another

taxpayer’s return)

Each Exemption is

$100,000 or less $3,200 $3,200 $0

Over But not over

$100,000 $125,000 $1,600 $3,200 $0

$125,000 $150,000 $800 $3,200 $0

$150,000 $175,000 $0 $1,600 $0

$175,000 $200,000 $0 $800 $0

In excess of $200,000 $0 $0 $0

Total the exemption amount on the front of Form 502 or Form 503 to determine the total exemption allowance to subtract on line 19 of

Form 502 or on line 4 of Form 503.

9

PART-YEAR RESIDENTS.

If you began or ended legal residence in Maryland in 2013 go

to Instruction 26.

Military taxpayers. If you have non-Maryland military income,

see Administrative Release 1.

10 EXEMPTIONS.

Determine what exemptions you are entitled to and complete

the EXEMPTIONS area on Form 502 or Form 503. Form 502B

must be completed and attached to Form 502 if you are

claiming one or more dependents.

EXEMPTIONS ALLOWED

You are permitted the same number of exemptions which you are

permitted on your federal return; however, the exemption amount is

different on the Maryland return. Even if you are not required to le

a federal return, the federal rules for exemptions still apply to you.

Refer to the federal income tax instructions for further information.

In addition to the exemptions allowed on your federal return, you

and your spouse are permitted to claim exemptions for being age

65 or over or for blindness. These additional exemptions are in the

amount of $1,000 each. If any other dependent claimed is 65 or

over, you also receive an extra exemption of up to $3,200. Make

sure you check both boxes (6) and (7) of Form 503 or the Dependent

Form 502B for each of your dependents who are age 65 or over.

Enter the number of exemptions in the appropriate boxes based

upon your entries in parts A, B, and C of the exemption area of

the form. Enter the total number of exemptions in Part D. For

Form 502, the number of exemptions for Part C is from Total

Dependent Exemptions, Line 3 of Form 502B.

NOTE: Do not use Form 503 if you are claiming more than two

dependents. Form 502B must be completed and attached to Form

502 if you are claiming one or more dependents.

KIDS FIRST EXPRESS LANE ELIGIBILITY ACT

Check the appropriate yes or no box on Form 503 dependent area

or Form 502B if the dependent who is eligible to be claimed as an

exemption is under age 19 before the end of the taxable year.

For each “dependent under age 19”, please also check ( ) either

the yes or no box to indicate whether or not that child currently has

health insurance.

Answering these questions will tell us whether to send you

information about affordable health care coverage for your children.

Check ( ) yes to authorize us to share your tax information with

the Medical Assistance Program. It will be used ONLY to identify and

help enroll your eligible children in affordable health care programs.

PART-YEAR RESIDENTS AND MILITARY

You must prorate your exemptions based on the percentage of

your income subject to Maryland tax. See Instruction 26 and

Administrative Release 1.

11 INCOME.

Line 1. Copy the gure for federal adjusted gross income

from your federal return onto line 1 of Form 502 or Form 503.

Line 1a. Copy the total of your wages, salaries and tips from

your federal return onto line 1a of Form 502 or Form 503. Use

the chart below to nd the gures that you need. If you and your

spouse le a joint federal return but are ling separate Maryland

returns, see Instruction 8.

To Maryland

Form From Federal Form

502 & 503 1040 1040A 1040EZ

line 1

line 1a

line 1b

line 37

line 7

See below.

line 21

line 7

line 7

line 4

line 1

line 1

Line 1b. If you are claiming a federal earned income credit

(EIC), or poverty level credit (PLC), enter the earned income

you used to calculate your credit. Earned income includes

wages, salaries, tips, professional fees and other

compensation received for personal services you

performed. It also includes any amount received as a

scholarship that you included in your federal AGI.

12

ADDITIONS TO INCOME.

Determine which additions to income apply to you. Write the

correct amounts on lines 2-5 of Form 502. Instructions for

each line:

Line 2. TAX EXEMPT STATE OR LOCAL BOND INTEREST.

Enter the interest from non-Maryland state or local bonds or

other obligations (less related expenses). This includes interest

from mutual funds that invest in non-Maryland state or local

obligations. Interest earned on obligations of Maryland or any

Maryland subdivision is exempt from Maryland tax and should not

be entered on this line.

Line 3. STATE RETIREMENT PICKUP. Pickup contributions of a

State retirement or pension system member. The pickup amount

will be stated separately on your W-2 form. The tax on this portion

of your wages is deferred for federal but not for state purposes.

Line 4. LUMP SUM DISTRIBUTION FROM A QUALIFIED

RETIREMENT PLAN. If you received such a distribution, you will

receive a Form 1099R showing the amounts distributed. You must

report part of the lump sum distribution as an addition to income if

you le federal Form 4972.

Use the LUMP SUM DISTRIBUTION WORKSHEET (12A) to determine

the amount of your addition.

5

LUMP SUM DISTRIBUTION WORKSHEET (12A)

1. Ordinary income portion of distribution from

Form 1099R reported on federal Form 4972

(taxable amount less capital gain amount) .....$ _____________

2. 40% of capital gain portion of distribution from

Form 1099R ...........................

3. Add lines 1 and 2. .......................$ _____________

4. Enter minimum distribution allowance from

Form 4972 ............................$ _____________

5. Subtract line 4 from line 3. This is your addition

to income for your lump sum distribution. Enter

on Form 502, line 4. If this amount is less than

zero, enter zero ........................$ _____________

Note: If you were able to deduct the death benet exclusion on Form

4972, allocate that exclusion between the ordinary and capital gain

portions of your distribution in the same ratio before completing this

schedule.

Line 5. OTHER ADDITIONS TO INCOME. If one or more of these

apply to you, enter the total amount on line 5 and identify each item

using the code letter:

CODE LETTER

a. Part-year residents: losses or adjustments to federal income

that were realized or paid when you were a nonresident of

Maryland.

b. Net additions to income from pass-through entities not

attributable to decoupling.

c. Net additions to income from a trust as reported by the

duciary.

d. S corporation taxes included on line 8 of Maryland Form 502CR,

Part A, Tax Credits for Income Taxes Paid to Other States. (See

instructions for Part A of Form 502CR.)

e. Total amount of credit(s) claimed in the current tax year to

the extent allowed on Form 500CR for the following Business

Tax Credits: Enterprise Zone Tax Credit, Maryland Disability

Employment Tax Credit, Employment of Qualied Ex-Felons Tax

Credit, Research and Development Tax Credit,

Small Business

Research & Development Tax Credit, Maryland Employer Security

Clearance Costs Tax Credit (do not include Small Business First-

Year Leasing Costs Tax Credit),

and Cellulosic Ethanol Technology

Research and Development Tax Credit.

f. Oil percentage depletion allowance claimed under IRC Section

613.

g. Income exempt from federal tax by federal law or treaty that is

not exempt from Maryland tax.

h. Net operating loss deduction to the extent of a double benet.

See Administrative Release 18 at www.marylandtaxes.com.

i. Taxable tax preference items from line 5 of Maryland Form

502TP. The items of tax preference are dened in IRC Section

57. If the total of your tax preference items is more than

$10,000 ($20,000 for married taxpayers ling joint returns)

you must complete and attach Maryland Form 502TP, whether

or not you are required to le federal Form 6251 (Alternative

Minimum Tax) with your federal Form 1040.

j. Amount deducted for federal income tax purposes for expenses

attributable to operating a family day care home or a child care

center in Maryland without having the registration or license

required by the Family Law Article.

k. Any refunds of advanced tuition payments made under the

Maryland Prepaid College Trust, to the extent the payments were

subtracted from federal adjusted gross income and were not

used for qualied higher education expenses, and any refunds

of contributions made under the Maryland College Investment

Plan or the Maryland Broker-Dealer College Investment Plan,

to the extent the contributions were subtracted from federal

adjusted gross income and were not used for qualied higher

education expenses. See Administrative Release 32.

l. Net addition modication to Maryland taxable income when

claiming the federal depreciation allowances from which the

State of Maryland has decoupled. Complete and attach Form

500DM. See Administrative Release 38.

m. Net addition modication to Maryland taxable income when

the federal special 5-year carryback period was used for a net

operating loss under federal law compared to Maryland taxable

income without regard to federal provisions. Complete and

attach Form 500DM. See Administrative Release 38.

n. Amount deducted on your federal income tax return for

domestic production activities (line 35 of Form 1040).

o. Amount deducted on your federal income tax return for tuition

and related expenses. Do not include adjustments to income

for Educator Expenses or Student Loan Interest deduction.

p. Amount attributable to Maryland’s decoupling from the federal

itemized deduction limitation threshold. This addition applies to

taxpayers who are itemizing deductions if their federal adjusted

gross income is $178,150 or more (or $89,075 if Married Filing

Separately). See ITEMIZED DEDUCTION WORKSHEET (14A),

Part II, line 13 in Instruction 14. You will need to complete this

worksheet before continuing fur ther with your Mar yland return.

cd. Net addition modication to Maryland taxable income resulting

from the federal deferral of income arising from business

indebtedness discharged by reacquisition of a debt instrument.

See Form 500DM and Administrative Release 38.

dm. Net addition modication from multiple decoupling provisions.

See the table at the bottom of Form 500DM for the line numbers

and code letters to use.

dp. Net addition decoupling modication from a pass-through

entity. See Form 500DM.

13 SUBTRACTIONS FROM INCOME.

Determine which subtractions from income apply to you.

Write the correct amounts on lines 8–14 of Form 502.

Instructions for each line:

Line 8. STATE TAX REFUNDS. Copy onto line 8 the amount of

refunds of state or local income tax included in line 1 of Form 502.

Line 9. CHILD CARE EXPENSES. You may subtract the cost of

caring for your dependents while you work. There is a limitation of

$3,000 ($6,000 if two or more dependents receive care). Copy onto

line 9 the amount from line 6 of federal Form 2441. You may also be

entitled to a credit for these taxable expenses. See instructions for

Part B of Form 502CR.

Line 10. PENSION EXCLUSION. You may be able to subtract

some of your taxable pension and retirement annuity income. This

subtraction applies only if:

a. You were 65 or over or totally disabled, or your spouse was

totally disabled, on the last day of the tax year, AND

b. You included on your federal return taxable income received as

a pension, annuity or endowment from an “employee retirement

system” qualied under Sections 401(a), 403 or 457(b) of

the Internal Revenue Code. [A traditional IRA, a Roth IRA, a

simplied employee plan (SEP), a Keogh plan, an ineligible

deferred compensation plan or foreign retirement income does

not qualify.]

Each spouse who receives taxable pension or annuity income and

is 65 or over or totally disabled may be entitled to this exclusion. In

addition, if you receive taxable pension or annuity income but you

are not 65 or totally disabled, you may be entitled to this exclusion

if your spouse is totally disabled. Complete a separate column in

the PENSION EXCLUSION COMPUTATION WORKSHEET (13A) for

each spouse. Combine your allowable exclusion and enter the total

amount on line 10, Form 502.

To be considered totally disabled, you must have a mental or physical

impairment which prevents you from engaging in substantial gainful

activity. You must expect the impairment to be of long, continued or

indenite duration or to result in your death. You must attach to your

return a certication from a qualied physician stating the nature

of your impairment and that you are totally disabled. If you have

previously submitted a physician’s certication, attach your own

statement that you are still totally disabled and that a physician’s

certication was submitted before.

If you are a part-year resident, complete PENSION EXCLUSION

COMPUTATION WORKSHEET (13A) using total taxable pension and

total Social Security and railroad retirement benets as if you were

a full-year resident. Prorate the amount on line 5 by the number of

months of Maryland residence divided by 12.

However, if you began to receive your pension during the tax year

you became a Maryland resident, use a proration factor of the

6

number of months you were a resident divided by the number of

months the pension was received.

For example, Pat Taxpayer moved to Maryland on March 1. If he

started to receive his pension on March 1, he would prorate the

pension exclusion by 10/10, which would mean he would be entitled

to the full pension exclusion. However, if he began to receive his

pension on February 1, Pat would prorate his pension by 10/11.

Please note that, in either case, the pro ration factor may not exceed

1.

Complete the PENSION EXCLUSION COMPUTATION WORKSHEET

(13A). Copy the amount from line 5 of the worksheet onto line 10

of Form 502.

L i n e 11 . FEDERALLY TAXED SOCIAL SECURITY AND RAILROAD

RETIREMENT BENEFITS. If you included in your federal adjusted

gross income Social Security, Tier I, Tier II and/or supplemental

railroad retirement benets, then you must include the total amount

of such benets on line 11. Social Security and railroad retirement

benets are exempt from state tax.

Line 12. NONRESIDENT INCOME. If you began or ended your

residence in Maryland during the year, you may subtract the portion

of your income received when you were not a resident of Maryland.

See Instruction 26 for part-year residents and Administrative

Release 1 for military personnel.

If your state of residence or your period of Maryland residence was

not the same as that of your spouse and you led a joint return,

follow Instruction 26 (c) through (p).

Line 13. SUBTRACTIONS FROM INCOME ON FORM 502SU.

Other certain subtractions for which you may qualify will be reported

on Form 502SU. Determine which subtractions apply to you and

enter the amount for each on Form 502SU. Enter the sum of all

applicable subtractions from Form 502SU on line 13 of Form 502,

and enter the code letters that represent the four highest dollar

amounts in the code letter boxes. If multiple subtractions apply,

be sure to identify all of them on Form 502SU and attach it to your

Form 502.

Note: If only one of these subtractions applies to you, enter the

amount and the code letter on line 13 of Form 502; then the use of

Form 502SU may be optional.

CODE LETTER

a. Payments from a pension system to remen and policemen

for job related injuries or disabilities (but not more than the

amount of such payments included in your total income).

b. Net allowable subtractions from income from pass-through

entities, not attributable to decoupling.

c. Net subtractions from income reported by a duciary.

d. Distributions of accumulated income by a duciary, if income

tax has been paid by the duciary to the State (but not more

than the amount of such income included in your total income).

e. Prot (without regard to losses) from the sale or exchange of

bonds issued by the State or local governments of Maryland.

f. Benets received from a Keogh plan on which State income tax

was paid prior to 1967. Attach statement.

g. Amount of wages and salaries disallowed as a deduction due to

the work opportunity credit allowed under the Internal Revenue

Code Section 51.

h. Expenses up to $5,000 incurred by a blind person for a reader,

or up to $1,000 incurred by an employer for a reader for a blind

employee.

i. Expenses incurred for reforestation or timber stand improvement

of commercial forest land. Qualications and instructions are

on Form DNR393, available from the Department of Natural

Resources, telephone 410-260-8531.

j. Amount added to taxable income for the use of an ofcial

vehicle by a member of a state, county or local police or re

department. The amount is stated separately on your W-2

form.

k. Up to $6,000 in expenses incurred by parents to adopt a child

with special needs through a public or nonprot adoption

agency and up to $5,000 in expenses incurred by parents to

adopt a child without special needs.

l. Purchase and installation costs of certain enhanced agricultural

management equipment as certied by the Maryland

Department of Agriculture. Attach a copy of the certication.

m. Deductible artist’s contribution. Attach Maryland Form 502AC.

n. Payment received under a re, rescue, or ambulance personnel

length of service award program that is funded by any county

or municipal corporation of the State.

o. Value of farm products you donated to a gleaning cooperative

as certied by the Maryland Department of Agriculture. Attach

a copy of the certication.

p. Up to $15,000 of military pay included in your federal adjusted

SPECIFIC INSTRUCTIONS

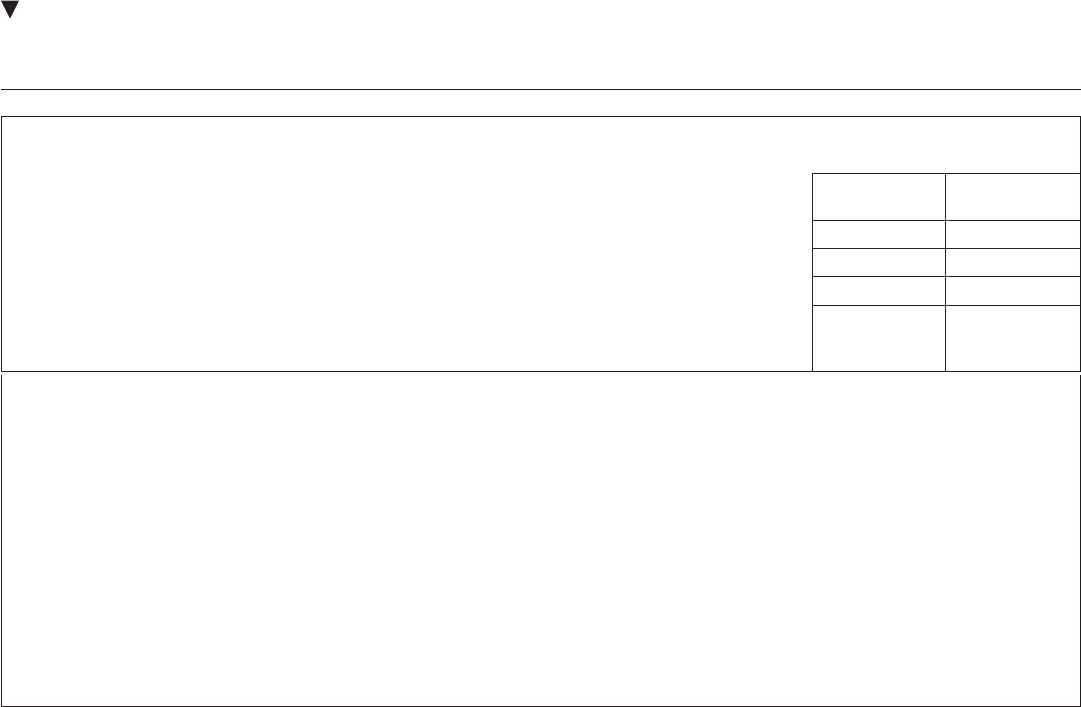

NOTE: When both you and your spouse qualify for the pension exclusion, a separate column must be completed for each spouse.

Line 1. Enter your net taxable pension and retirement annuity included in your federal adjusted gross income. Do not include any

amount subtracted for military retirement income. See code letter u in Instruction 13. Do not include Social

Security and/or Railroad Retirement income on this line.

Line 2. The maximum allowable exclusion is $27,800.

Line 3. Enter your total Social Security and/or Railroad Retirement benefits. Include all Social Security and/or Railroad Retirement

benefits whether or not you included any portion of these amounts in your federal adjusted gross income. Include both Tier

I and Tier II Railroad Retirement benefits. If you are filing a joint return and both spouses received Social Security and/or

Railroad Retirement benefits but only one spouse received a pension, enter only the Social Security and/or Railroad Retirement

benefits of the spouse receiving the pension on the worksheet.

Line 4. Subtract line 3 from line 2 to determine your tentative exclusion.

Line 5. Your pension exclusion is the smaller of your net taxable pension (line 1) or the tentative exclusion (line 4). Enter the smaller

amount on this line.

Review carefully the age and disability requirements in the instructions before completing this worksheet.

You Spouse

1. Net taxable pension and retirement annuity included in your federal adjusted gross income

(Do not include Social Security or Railroad Retirement). . . . . . . . . . . . . . . . . . . . . . . . . . . .

2. Maximum allowable exclusion. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $27,800 $27,800

3. Total benefits you received from Social Security and/or Railroad Retirement (Tier I and Tier II)

4. Tentative exclusion (Subtract line 3 from line 2.) (If less than 0, enter 0.). . . . . . . . . . . . . . .

5. Pension Exclusion (Enter the smaller of line 1 or 4 here and on line 10, Form 502.) If you and

your spouse both qualify for the pension exclusion, combine your allowable exclusions and

enter the total amount on line 10, Form 502. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

PENSION EXCLUSION COMPUTATION WORKSHEET (13A)

7

gross income that you received while in the active service of

any branch of the armed forces and which is attributable to

service outside the boundaries of the U.S. or its possessions. To

compute the subtraction, follow the directions on the MILITARY

OVERSEAS INCOME WORKSHEET (13B). If your total military

pay exceeds $30,000, you do not qualify for the subtraction.

p. MILITARY OVERSEAS INCOME WORKSHEET (13B)

When both you and your spouse qualify for this military

subtraction, complete separate computations for each spouse.

1. ENTER the amount of military pay included in

your federal adjusted gross income

attributable to service outside the U.S.

If greater than $15,000, enter $15,000 ........$ _________

2. ENTER total military pay received

during the tax year ............$ _________

3. Maximum subtraction ..........$ 15,000

__________

4. SUBTRACT the amount on line 3 from line 2.

If this amount is less than zero (0), enter

zero (0) ..............................$ _________

5. SUBTRACT line 4 from line 1. This is your

subtraction from income. If the amount is zero

(0) or less, you are not eligible for this

subtraction. INCLUDE this amount on

line p of Form 502SU .....................$ _________

q. Unreimbursed vehicle travel expenses for:

1. A volunteer re company;

2. Service as a volunteer for a charitable organization whose

principal purpose is to provide medical, health or nutritional

care; AND

3. Assistance (other than providing transportation to and

from the school) for handicapped students at a Maryland

community college. Attach Maryland Form 502V .

r. Amount of pickup contribution shown on Form 1099R from the

state retirement or pension systems included in federal adjusted

gross income. The subtraction is limited to the amount of

pickup contribution stated on the 1099R or the taxable pension,

whichever is less. Any amount not allowed to be claimed on the

current year return may be carried forward to the next year

until the full amount of the State pickup contribution has been

claimed.

s. Amount of interest and dividend income (including capital gain

distributions) of a dependent child which the parent has elected

to include in the parent’s federal gross income under Internal

Revenue Code Section 1(g)(7).

t. Payments received from the State of Maryland under Title 12

Subtitle 2 of the Real Property Article (relocation and assistance

payments).

u. Up to $5,000 of military retirement income received by a

qualifying individual during the tax year. To qualify, you must

have been a member of an active or reserve component of

the armed forces of the United States, an active duty member

of the commissioned corps of the Public Health Service, the

National Oceanic and Atmospheric Administration, or the Coast

and Geodetic Survey, a member of the Maryland National

Guard, or the member’s surviving spouse or ex-spouse.

v. The Honorable Louis L. Goldstein Volunteer Police, Fire, Rescue

and Emergency Medical Services Personnel Subtraction

Modication Program. $3,500 for each taxpayer who is a

qualifying volunteer as certied by a Maryland re, police,

rescue or emergency medical services organization. $3,500 for

each taxpayer who is a qualifying member of the U.S. Coast

Guard Auxiliary or Maryland Defense Force as certied by these

organizations. Attach a copy of the certication.

• Code w is not being used this year. Please see Code l.

xa. Up to $2,500 per contract purchased for advanced tuition

payments made to the Maryland Prepaid College Trust. See

Administrative Release 32.

xb. Up to $2,500 per account holder per beneciary of the total

of all amounts contributed to investment accounts under the

Maryland College Investment Plan and Maryland Broker-Dealer

College Investment Plan. See Administrative Release 32.

y. Any income of an individual that is related to tangible or

intangible property that was seized, misappropriated or lost

as a result of the actions or policies of Nazi Germany towards

a Holocaust victim. For additional information, contact the

Revenue Administration Division.

z. Expenses incurred to buy and install handrails in an existing

elevator in a health care facility (as dened in Section 19-114

of the Health General Article) or other building in which at least

50% of the space is used for medical purposes.

aa. Payments from a pension system to the surviving spouse or

other beneciary of a law enforcement ofcer or reghter

whose death arises out of or in the course of their employment.

ab. Income from U.S. Government obligations. Enter interest on

U.S. Savings Bonds and other U.S. obligations. Capital gains

from the sale or exchange of U.S. obligations should be included

on this line. Dividends from mutual funds that invest in U.S.

government obligations also are exempt from state taxation.

However, only that portion of the dividends attributable to

interest or capital gain from U.S. government obligations can

be subtracted. You cannot subtract income from Government

National Mortgage Association securities. See Administrative

Releases 10 & 13.

bb. Net subtraction modication to Maryland taxable income when

claiming the federal depreciation allowances from which the

State of Maryland has decoupled. Complete and attach Form

500DM. See Administrative Release 38.

cc. Net subtraction modication to Maryland taxable income when

the federal special 5-year carryback period was used for a net

operating loss under federal law compared to Maryland taxable

income without regard to federal provisions. Complete and

attach Form 500DM. See Administrative Release 38.

cd. Net subtraction modication to Maryland taxable income

resulting from the federal ratable inclusion of deferred income

arising from business indebtedness discharged by reacquisition

of a debt instrument. Complete and attach Form 500DM. See

Administrative Release 38.

dd. Income derived within an arts and entertainment district by a

qualifying residing artist from the publication, production, or

sale of an artistic work that the artist created, wrote, composed

or executed. Complete and attach Form 502AE.

dm. Net subtraction modication from multiple decoupling

provisions. See the table at the bottom of Form 500DM.

dp. Net subtraction decoupling modication from a pass-through

entity. See Form 500DM.

ee. The amount received as a grant under the Solar Energy Grant

Program administered by the Maryland Energy Administration

(but not more than the amount included in your total income).

ff. Amount of the cost difference between a conventional on-site

sewage disposal and a system that uses nitrogen removal

technology, for which the Department of Environment’s

payment assistance program does not cover.

hh. Exemption adjustment for certain taxpayers with interest

on U.S. obligations. If you have received income from U.S.

obligations and your federal adjusted gross income exceeds

$100,000 ($150,000 if ling Joint, Head of Household, or

Qualifying Widow(er)), enter the difference, if any, between

the exemption amount based on your federal adjusted gross

income and the exemption amount based upon your federal

adjusted gross income after subtracting your U.S. obligations

using the EXEMPTION ADJUSTMENT WORKSHEET (13C).

hh. EXEMPTION ADJUSTMENT WORKSHEET (13C)

Line 1: ENTER the exemption amount to be

reported on line 19 of Form 502 using the

chart in Instruction 10. (If you are a

part-year resident, enter the amount to be

reported on line 19 before it is prorated.) ..$ __________

Line 2: ENTER your federal adjusted gross income

as reported on line 1 of your Form 502 ...$ __________

Line 3: ENTER your income from U.S. obligations

(line ab, Form 502SU) ...............$ __________

Line 4: SUBTRACT amount on line 3 from amount

reported on line 2. ..................$ __________

8

Line 5: RECALCULATE your exemption amount

using the chart in Instruction 10, using the

income from line 4. Remember to add your

$1,000 exemptions for age and blindness if

applicable ........................$ __________

Line 6: SUBTRACT the exemption amount

calculated on line 1 from the exemption

amount calculated on line 5. If the amount

is less than zero (0), enter zero (0). If the

amount is zero, you have already received

the maximum exemption that you are

entitled to claim on Form 502 ..........$ __________

If the amount is greater than zero (0), enter this amount as

a subtraction on line hh of Form 502SU.

Example:

Pat and Chris Jones had a federal adjusted gross income of $180,000.

They also had $40,000 on interest from U.S. Savings Bonds and had a

dependent son whom they claimed on the Maryland tax return. Using

Instruction 10, they found the exemption amount on their Maryland

return (based upon $180,000 of income) was $2,400 ($800 for three

exemptions). If it were not for the $40,000 of U.S. Savings Bonds,

their federal adjusted gross income would have been $140,000 and

their exemption amount would have been $9,600 ($3,200 for three

exemptions). Therefore, Pat and Chris Jones are entitled to claim a

subtraction of $7,200 ($9,600 - $2,400) on line hh of Form 502SU.

ii. Interest on any Build America Bond that is included in your

federal adjusted gross income. See Administrative Release 13.

jj. Gain resulting from a payment from the Maryland Department

of Transportation as a result of the acquisition of a portion of

the property on which your principal residence is located.

kk. Qualied conservation program expenses up to $500 for an

application approved by the Department of Natural Resources

to enter into a Forest Conservation and Management Plan.

ll. Payment received as a result of a foreclosure settlement

negotiated by the Maryland Attorney General.

mm. Amount received by a claimant for noneconomic damages

as a result of a claim of unlawful discrimination under

Internal Revenue Code Section 62(e).

Line 14. TWO-INCOME SUBTRACTION. You may subtract up to

$1,200 if both spouses have income subject to Maryland tax and you

le a joint return. To compute the subtraction, complete the TWO-

INCOME MARRIED COUPLE SUBTRACTION WORKSHEET (13D).

14 ITEMIZED DEDUCTIONS.

If you gure your tax by the ITEMIZED DEDUCTION

METHOD, complete lines 17a and b on Maryland Form 502.

(See Instruction 16 to see if you will use the ITEMIZED

DEDUCTION METHOD.)

USE FEDERAL FORM 1040 SCHEDULE A

To use the ITEMIZED DEDUCTION METHOD, you must itemize your

deductions on your federal return and complete federal Form 1040

Schedule A.

Maryland has decoupled from the federal 2013 itemized

deduction threshold limiting itemized deductions.

If your federal adjusted gross income is less than $178,150

($89,075 if Married Filing Separately), simply copy the amount from

federal Schedule A, line 29, Total Itemized Deductions, on to line

17a of Form 502. Certain items of federal itemized deductions are

not eligible for State purposes and must be subtracted from line

17a. State and local income taxes used as a deduction for federal

purposes must be entered on line 17b. Also, any amounts deducted

as contributions of Preservation and Conservation Easements for

which a credit is claimed on Form 502CR must be added to line 17b.

If your federal adjusted gross income is greater than

$178,150 ($89,075, if Married Filing Separately), copy the amount

from federal Schedule A, line 29, Total Itemized Deductions, onto

line 17a of Form 502. Next complete the ITEMIZED DEDUCTION

WO RKSHE ET (14A), if you elect to itemize deductions on your

Maryland return.

Part I of this worksheet is used to calculate federal itemized

deductions that would have existed but for the 2013 federal

legislation.

Part II is used to calculate the amount of the required

decoupling modication for itemized deductions that is

included on line 5 of Form 502. (See Instruction 12.)

Part III is used by taxpayers to calculate the amount of state

and local income taxes that were limited. Enter the amount

from line 20 of Part III on line 17b of Form 502.