Presentation IQ 10/15 Sp Capitaliq Fixed Income North America Q2 2015

User Manual: IQ 10/15

Open the PDF directly: View PDF ![]() .

.

Page Count: 25

- Slide Number 1

- TABLE OF CONTENTS North America

- EDITORS’ NOTE

- MARKET TRENDS

- Relative Performance of Fixed Income Indices

- 10 Year BBB Sector Z-Spreads

- Z-Spread Ratings Term Structure (Quarter over Quarter)

- Slide Number 8

- Sovereign CDS Heat Map

- Sovereign CDS Regional Focus: United States

- CREDIT TRENDS

- S&P Ratings Trends

- Slide Number 13

- CDS Market Outliers

- Slide Number 15

- Slide Number 16

- Quantitatively Viewed Ratings Outliers

- FINANCIAL RATIO TRENDS

- Financial Ratio Trends

- ISSUANCE TRENDS

- Issuance Trends By Rating Category

- Covenants for High Yield Issuance

- Contact Us

- Disclosures

- Slide Number 25

FIXED INCOME IQ

Credit Markets

Quarterly Fixed Income Trends

North America

July 2015│ Issue 6

2

TABLE OF CONTENTS

North America

Market Trends……..………………………………………………………..5

Market Indices

Corporate Yield Curves

Investment Grade vs. High Yield Market Activity

Sovereign CDS Heat Map

Sovereign CDS Deep Dive: United States

Credit Trends...……………………………………………………………..12

Ratings Trends

CDS Market Sentiment

CDS Market Outliers

Fundamental and Market Implied Default Risk

̶PD Market Signals and PD Fundamentals

Quantitatively Viewed Ratings Outliers

Financial Ratio Trends..……………………………………………….…..19

Issuance Trends..…………………………………………………………...21

Ratings Issuance

Security Issuance

High Yield Covenant Trends

Please click on the links below to access research on other regions or visit http://www.spcapitaliq.com/our-

thinking/research.html?category=market:

Latin America

Europe

3

EDITORS’ NOTE

High yield performed well in Q2 2015, while investment grade posted losses as the market began to anticipate rate increases in the

second half of 2015. Spreads increased but other risk signals remained varied.

Q2 2015 Overview:

-Overall, credit markets were mixed – Anticipation of rate increases caused investors to shed investment grade debt while high yield

posted positive returns for second quarter in a row.

-U.S. sovereign risk decreased as global market volatility in China and Europe strengthened the U.S. as a safe haven.

-Spreads increased for most sectors and investment grade – Markets re-priced risk upwards this quarter for all sectors and for

investment grade debt. Only high yield debt saw spreads tighten from last quarter.

-Risk signals mixed this quarter - Median equity market-based probabilities of default improved on a quarterly basis while fundamental

probabilities of default showed deterioration in all but one sector.

-Issuance continues to be healthy – Issuance increased in most ratings categories on a year-over-year basis with the biggest increase

coming from the BBB spectrum, following a similar trend from last quarter.

Jay Bhankharia, CFA

Senior Manager

Investment Management

S&P Capital IQ

AUTHORS:

James Elder

Director

Corporates and Financial Institutions

S&P Capital IQ

MARKET TRENDS

5

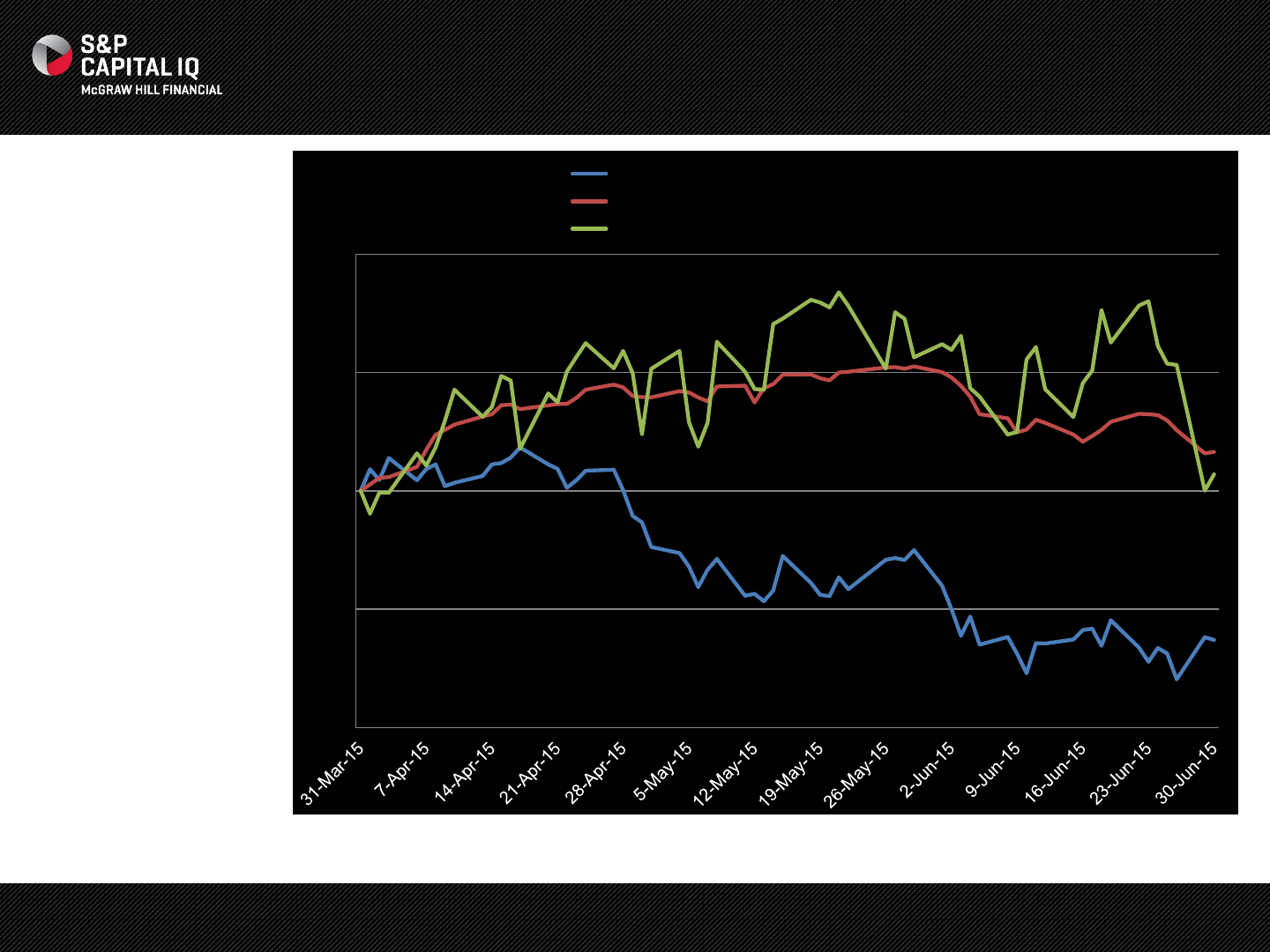

Relative Performance of Fixed Income Indices

NOTES:

•As of June 30th, the S&P

U.S. Investment Grade and

High Yield Corporate Bond

Indices generated -2.52%

and .66% in total returns,

respectively during the last

three months. During that

same period, the S&P 500®

finished the quarter with a

.28% gain.

•As the economy slowly

continued to strengthen

with labor markets

maintaining momentum,

investors were looking for

rates to increase which

caused investment grade

bonds to drop in Q2 2015.

High yield was the top

performer in Q2 as equity

prices were volatile due to

global market issues

stemming from Greece and

China.

Source: S&P Capital IQ as of July 1, 2015.

-4%

-2%

0%

2%

4%

S&P U.S. Investment Grade Corporate Bond Index QTD TRR %

S&P U.S. High Yield Corporate Bond Index QTD TRR %

S&P 500 (TR) QTD TRR %

6

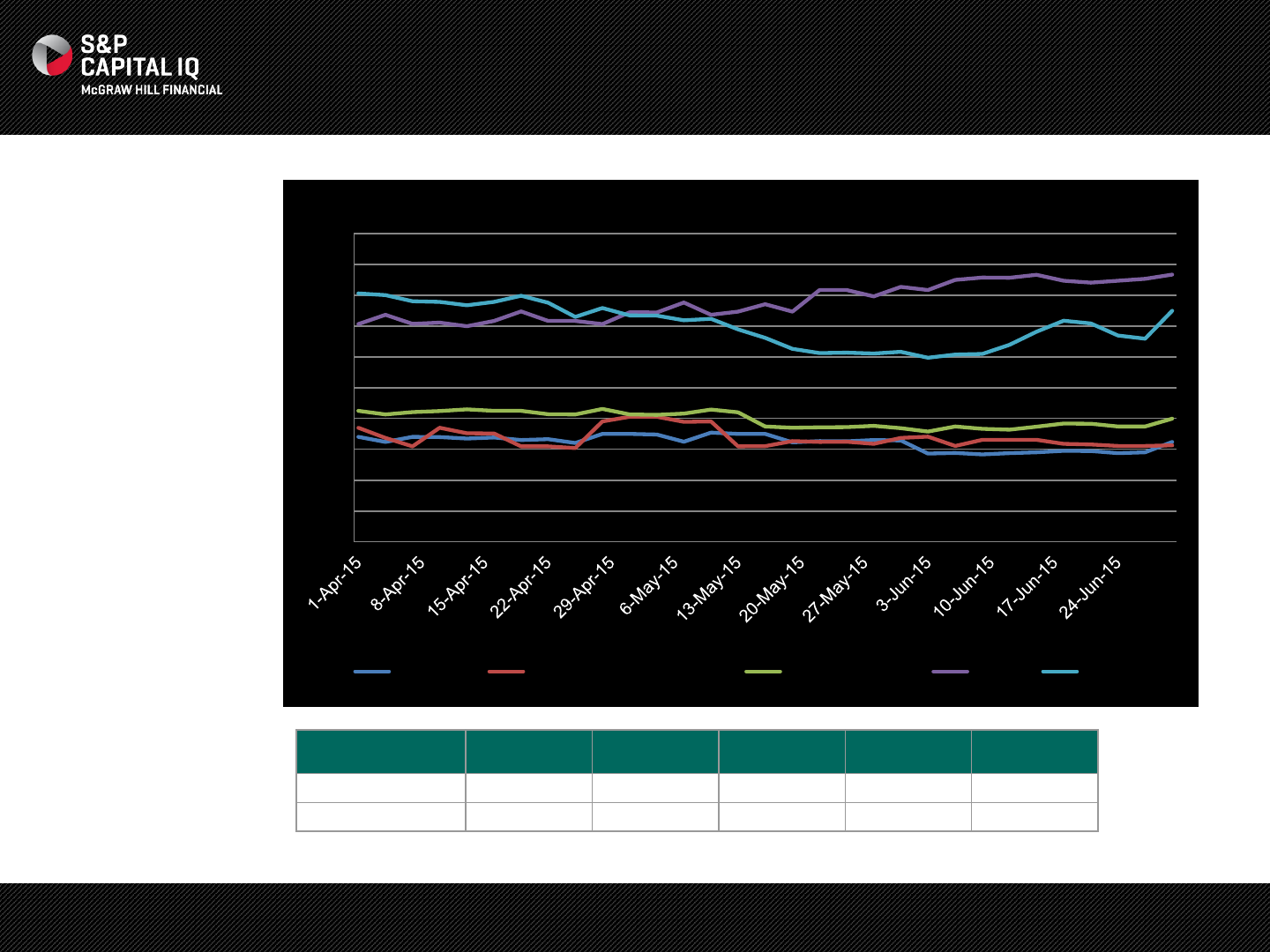

NOTES:

•All sector z-spreads

widened this quarter,

coinciding with similar

movement in Treasury

rates.

•The largest widening on a

percentage basis in Q2

was in financials, which

moved from 160bps to

181bps.

•Telecom and IT ended the

quarter with the smallest

widening on an absolute

basis.

All spreads and yield curves are proprietary data developed from buy-side indicative quotes. All bonds are USD denominated.

Source: S&P Capital IQ as of July 1, 2015.

Cons. Discr. Cons. Staples

Energy Financials Healthcare Industrials IT Materials Telecom. Utilities

BPS

Change 20

16

12

21

18

13

11

15

7

18

Total %

Change 11.49%

10.46%

5.48%

13.13%

11.54%

8.18%

5.70%

8.52%

3.45%

11.92%

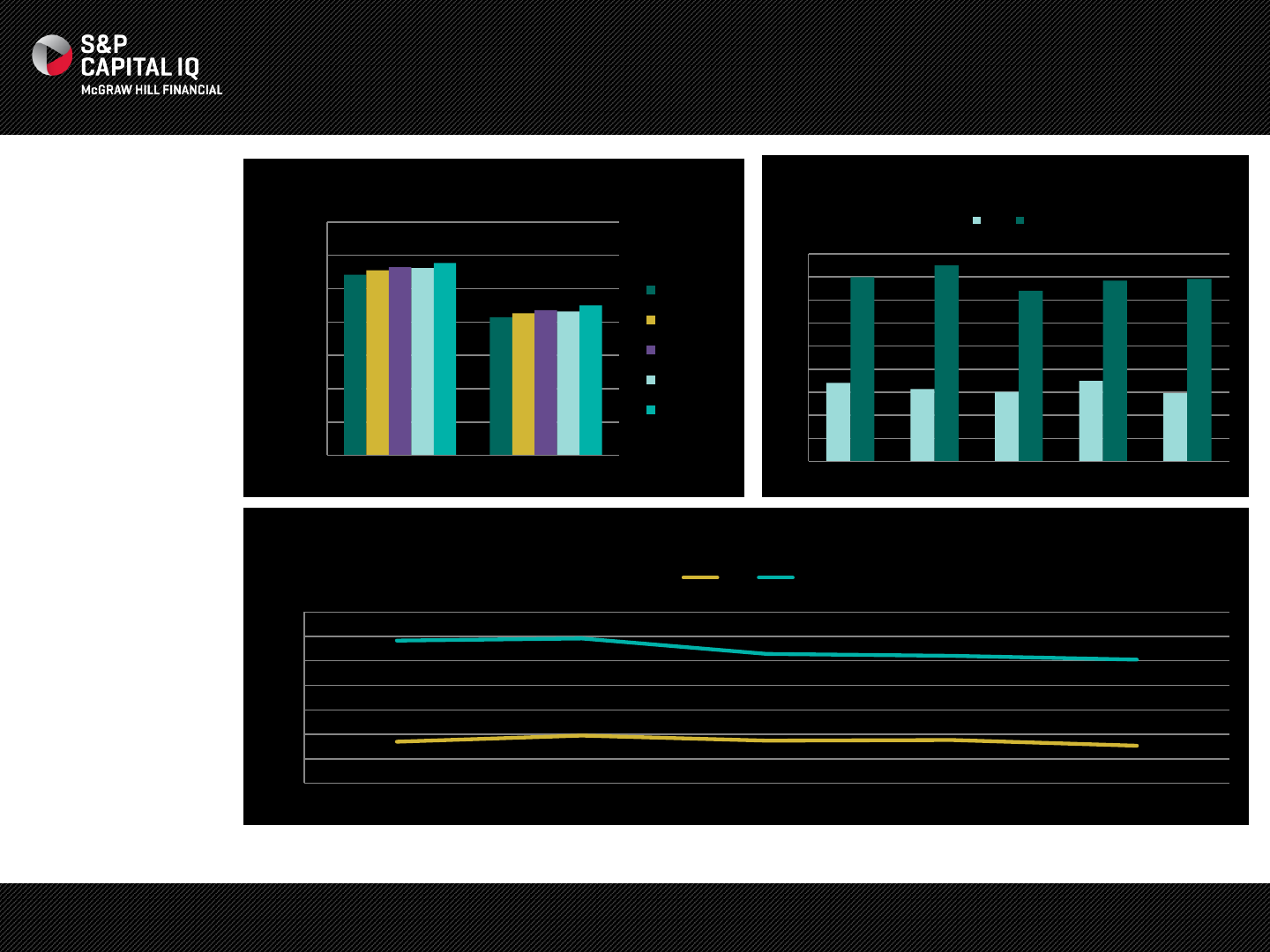

10 Year BBB Sector Z-Spreads

120

140

160

180

200

220

240

Bps

Cons. Discr.

Cons. Staples

Energy

Financials

Healthcare

Industrials

IT

Materials

Telecom.

Utilities

7

bps Change QoQ

1Y 5Y 10Y 15Y 20Y 30Y

AAA 4.67 4.67 4.67 4.67 4.67 4.67

AA 7.40 7.40 7.40 7.40 7.40 7.40

A 11.17 11.17 11.17 11.17 11.17 11.17

BBB 13.35 13.35 13.35 13.35 13.35 13.35

BB -8.82 -17.90 -25.96 -25.96 -33.81 -35.23

B -22.85 -17.82 -13.35 -13.35 -9.01 -8.22

All spreads and yield curves are proprietary data developed from buy-side indicative quotes. All bonds are USD denominated.

Source: S&P Capital IQ as of July 1, 2015.

NOTES:

•Investment grade z-

spreads widened over the

quarter, across the term

structure.

•Within the investment

grade space, we observed

a parallel shift upward

throughout the term

structure.

•Similar to last quarter in

high yield, we noticed the

BB curve tightened much

more on the long end while

the B curve experienced

greater tightening on the

short end. The tightening

of the BB spreads was

much stronger this quarter

than Q1 2015.

Z-Spread Ratings Term Structure (Quarter over Quarter)

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

1M

3M

6M

9M

1Y

2Y

3Y

4Y

5Y

6Y

7Y

8Y

9Y

10Y

11Y

12Y

13Y

14Y

15Y

16Y

17Y

18Y

19Y

20Y

21Y

22Y

23Y

24Y

25Y

26Y

27Y

28Y

29Y

30Y

AAA15 Q2

AAA15 Q1

AA15 Q2

AA15 Q1

A15 Q2

A15 Q1

BBB15 Q2

BBB15 Q1

BB15 Q2

BB15 Q1

B15 Q2

B15 Q1

8

NOTES:

•Market activity fell from its

a 12-month high in March

for both investment grade

and high yield. In the

second quarter, activity hit

lows in May but rebounded

in June.

•Within high yield, telecom

and energy had the most

activity. Within investment

grade, telecom and IT led

the way with the most

activity.

Investment Grade vs. High Yield Market Activity

Source: S&P Capital IQ as of July 1, 2015. Market Activity Score (MAS) is a derived analytic created to provide an indication of the level of trade and market activity

associated with a given security. It is developed from a review of all available trades and quotes based on price staleness, number of quotes/market makers and trade

data. It is scaled from 1 (high MAS) to 5 (low MAS).

MAS 6/30/14

7/31/14

8/29/14

9/30/14

10/31/14

11/30/14

12/31/14

1/30/15 2/27/15 3/31/15 4/30/15

5/29/15

6/30/15

S&P High Yield Corporate

Index 1.71

1.80

1.67

1.66

1.70

1.87

2.02

1.93

2.02

1.62

1.82

1.85

1.66

S&P Investment Grade

Corporate Index 1.61

1.60

1.61

1.60

1.62

1.70

1.79

1.78

1.73

1.58

1.67

1.72

1.66

1.45

1.55

1.65

1.75

1.85

1.95

2.05

S&P High Yield Corporate Index (MAS) S&P Investment Grade Corporate Index (MAS)

More

Market

Activity

Less

Market

Activity

9

Source: S&P Capital IQ as of July 1, 2015.

Sovereign CDS Heat Map

Country

6/30/2015

CDS

Spread

Avg # Quotes

per Day

CDS Most Risky

Greece

6739

200 to 10

Venezuela

4691

>200

Ukraine

4096

200 to 10

Cyprus

437

<10

Nigeria

425

<10

El

Salvador

416

<10

Pakistan

410

<10

Lebanon

358

<10

Russia

341

>200

Egypt

313

<10

CDS Least Risky

Swiss Confederation

14

<10

Norway

15

200 to 10

Sweden

15

200 to 10

United States of America

16

200 to 10

Germany

16

>200

Denmark

20

200 to 10

United

Kingdom

20

>200

Netherlands

20

>200

Finland

21

200 to 10

New Zealand

31

<10

NOTES:

•The heat map

provides a quarter-

over-quarter view

of the bps change

in sovereign CDS

spreads.

•The country with

the largest

increase in CDS

spreads was

Greece, as debt

repayment issues

lingered. Its

spreads widened

by 3,974 bps

throughout the

quarter.

•The countries with

the largest

improvement in

CDS spread were

Ukraine and

Venezuela. Their

spreads tightened

by 3,521 and 300

bps, respectively.

10

NOTES:

•The U.S. CDS spread

compared to G5 nations.

•The U.S. saw a tightening

in its CDS spread

throughout the quarter

moving from 18.5 to 15.6

bps.

•The U.S. is now the

country with the tightest

CDS spread closely

followed by Germany and

the U.K.

•Japan was the biggest

mover again this quarter,

with its spread widening by

22.7% to 43.3 bps.

Source: S&P Capital IQ as of July 1, 2015.

United States

United

Kingdom Japan France Germany

BPS Change -2.84

-1.27

8.03

-

2.79

-0.82

Total % Change -15.3%

-6.0%

22.7%

-6.9%

-4.8%

Sovereign CDS Regional Focus: United States

0

5

10

15

20

25

30

35

40

45

50

Bps

Germany United States of America United Kingdom Japan France

CREDIT TRENDS

12

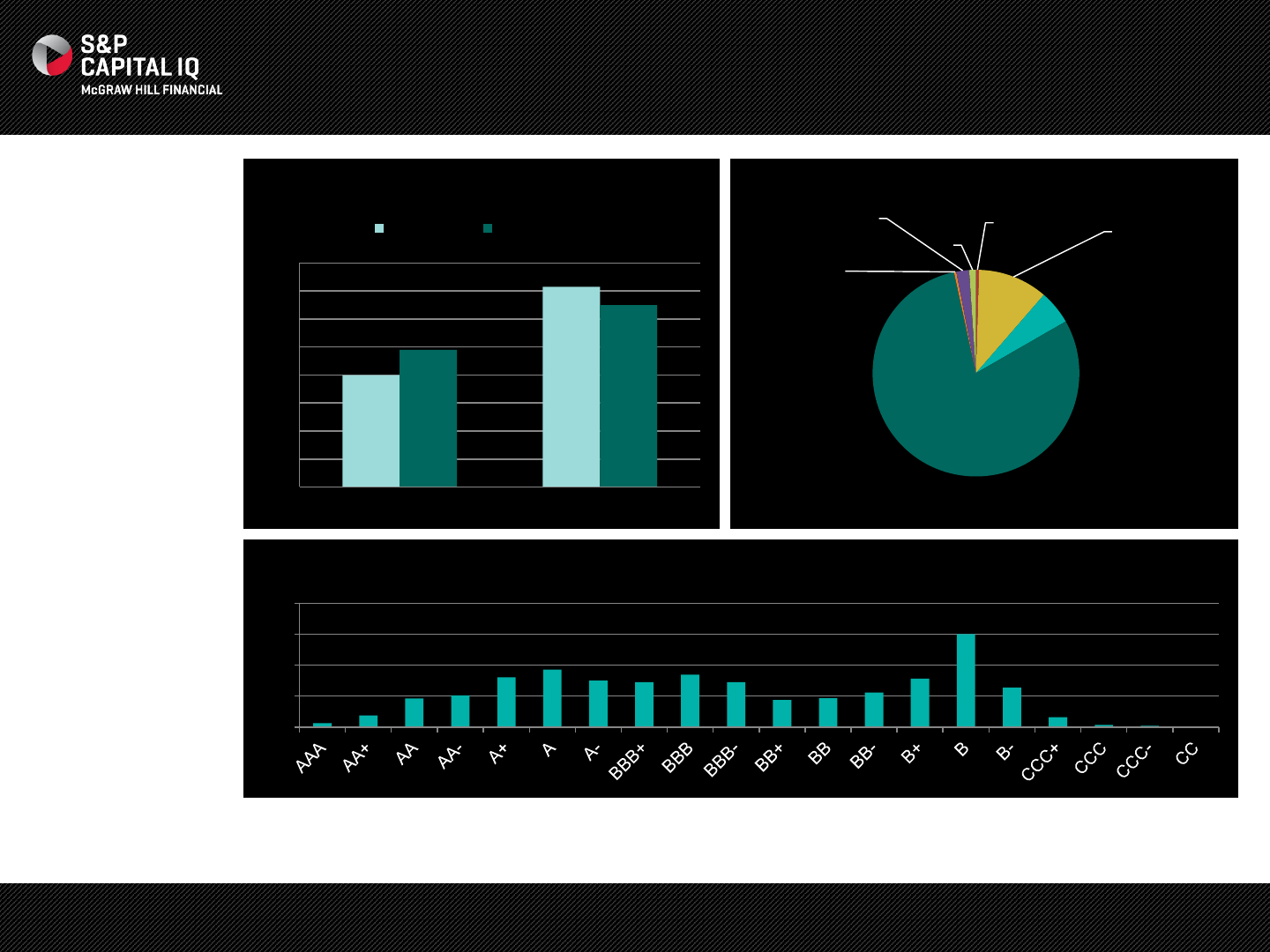

NOTES:

•There was much more

activity as the count of

upgrades and downgrades

surpassed last quarter. Q2

2015 saw a reversal in the

upgrade to downgrade

trend for the 3rd straight

quarter. The number of

companies with positive

outlook decreased this

quarter to 5% from 8% last

quarter.

S&P Ratings Services

Outlook:

•Risk aversion could be

amplified by Greece's exit

from the Eurozone, or from

credit contagion associated

with decelerating Chinese

GDP growth, but we see

these as manageable near-

term risks.

•The need for monetary

stimulus in the U.S. is

fading, but disrupted credit

markets or disappointing

economic news could slow

the pace of Fed policy

normalization.

Constituents include all rated companies with a Local Currency Long Term Rating and S&P Capital IQ sector classification in the U.S. and Canada.

Source: S&P Capital IQ as of July 1, 2015 and Global Credit Portal ‘Credit Conditions: A Resilient U.S. Economy Shields North America Credit Conditions

From Increasing Risks’ published on July 14, 2015.

S&P Ratings Trends

0

20

40

60

80

100

120

140

160

2015 Q1 2015 Q2

Rating Actions

Upgrades Downgrades Developing

1% Negative

11%

Positive

5%

Stable

80%

Watch Dev

0%

Watch Neg

2% Watch Pos

1%

Outlook/Credit Watch

0

200

400

600

800

Rating Distribution

13

The Market Derived Signal (MDS) is a quantitative analytic that uses Credit Default Swaps (CDS) to facilitate the interpretation of how the CDS markets generally view the credit quality of

well-known firms and sovereigns. It aims to capture the market’s sentiment regarding an entity’s perceived credit risk. One of the objectives of the MDS is to identify where market sentiment

may differ from the issuer credit rating. CDS spreads are used to compute the difference between an entity’s actual spread and expected spread for a given rating. Universe is all

companies that have an S&P Long-Term Local Rating, primary headquarters in the U.S. or Canada, and an S&P Capital IQ sector classification. Source: S&P Capital IQ as of July 1, 2015.

NOTES:

•Overall, the CDS market

indicated better perceived

credit quality in 5 of the 10

sectors than did their

corresponding S&P Ratings.

The reversal came in the

telecom sector. The highest

positive notch differences

came from industrials.

•Financials and telecom had

the strongest negative

sentiment in CDS vs. S&P

Ratings in Q2 2015.

S&P

Rating

CDS

MDS Value

AAA

aaa 23

AA+

aa+ 22

AA

aa 21

AA

- aa- 20

A+

a+ 19

A

a 18

A

- a- 17

BBB+

bbb+ 16

BBB

bbb 15

BBB

- bbb- 14

BB+

bb+ 13

BB

bb 12

BB

- bb- 11

B+

b+ 10

B

b 9

B

- b- 8

CCC+

ccc+ 7

CCC

ccc 6

CCC

- ccc- 5

CC

cc 4

C

c 3

D

d 2

SD

sd 1

NR

nr 0

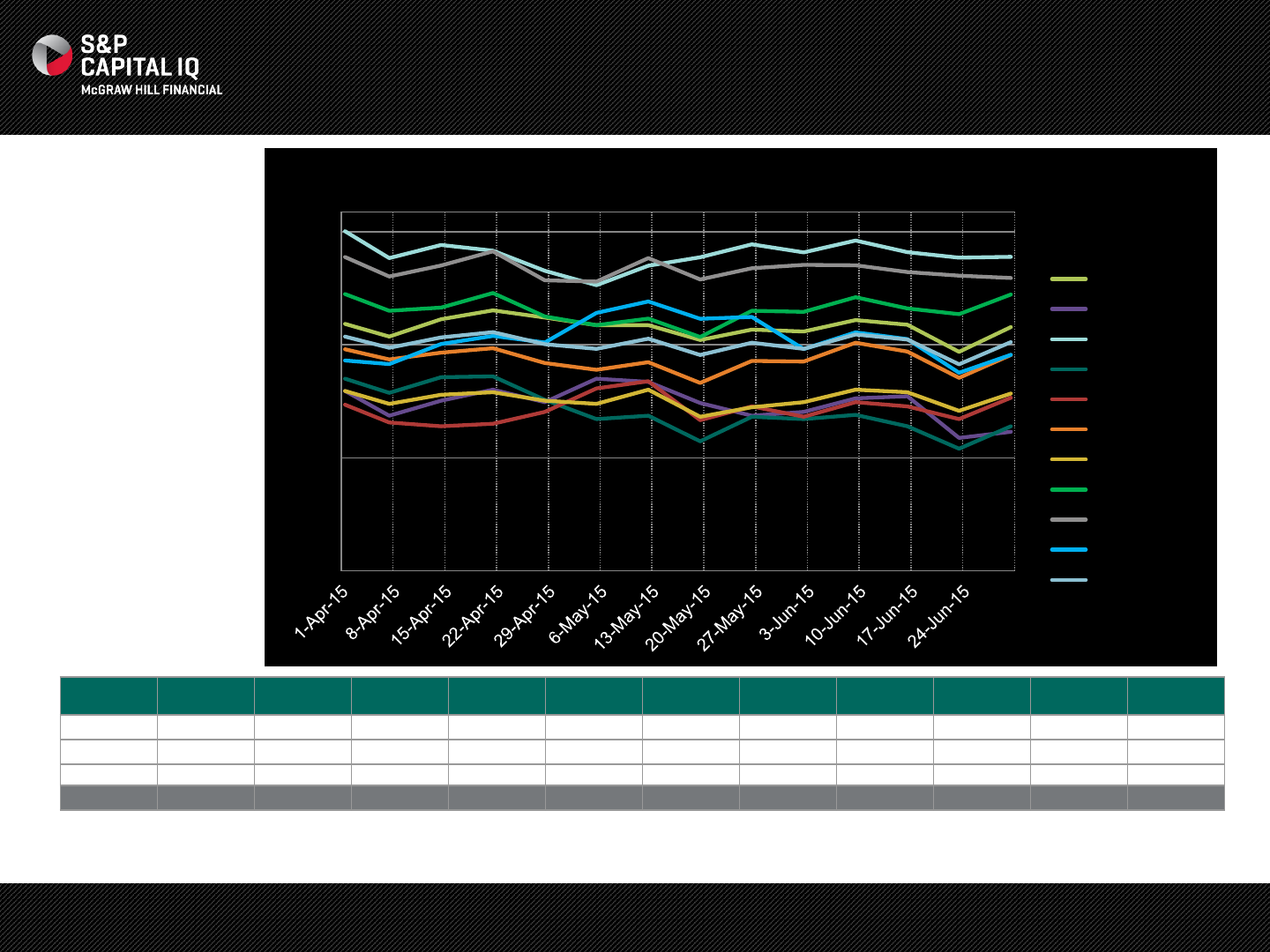

CDS Market Sentiment By Sector

Cons. Discr. Cons. Staples Energy Financials Healthcare Industrials IT Materials Telecom. Utilities

CDS

MDS

S&P

Rating

CDS

MDS

S&P

Rating

CDS

MDS

S&P

Rating

CDS

MDS

S&P

Rating

CDS

MDS

S&P

Rating

CDS

MDS

S&P

Rating

CDS

MDS

S&P

Rating

CDS

MDS

S&P

Rating

CDS

MDS

S&P

Rating

CDS

MDS

S&P

Rating

14 Q3 13.01

12.93

15.25

15.47

15.17

15.29

15.51

15.88

16.53

16.10

15.65

15.02

14.84

15.29

14.52

14.46

13.80

13.80

16.18

15.23

14 Q4 13.18

12.89

15.54

15.43

14.98

15.35

15.64

15.90

16.57

16.07

15.78

15.12

14.84

15.35

14.37

14.46

13.50

13.80

15.90

15.23

15 Q1 13.16

12.98

15.62

15.27

14.92

15.12

15.63

15.90

16.70

16.10

15.89

15.07

15.19

15.35

14.33

14.35

13.60

13.60

16.13

15.23

15 Q2 13.15

12.98

15.68

15.22

14.61

14.92

15.50

15.90

16.40

16.13

15.64

15.13

15.26

15.35

14.11

14.35

13.20

13.60

15.73

15.22

VALUE CONVERSION:

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

Notch Difference

14 Q3

14 Q4

15 Q1

15 Q2

14

NOTES:

•We have highlighted

companies with some of

the biggest divergences

between their S&P Rating

and their CDS Market

Derived Signal in red. This

provides us with a list of

firms whose market

sentiment is significantly

different than its Rating.

As shown by the blue

circles, the vast majority of

firms were scored +/- 3

notches from their Credit

Rating.

•We notice that the CDS

market has more bullish

outliers than bearish,

especially in the lower end

of the investment grade

spectrum. In addition, as

compared to last quarter

we observe more outliers in

the B rated spectrum that

have CDS spreads trading

at higher levels. Both

trends are similar to last

quarter.

Company

CDS MDS

S&P Rating

CDS

MDS Positive

Divergence

American Electric Power

Co., Inc.

a+

BBB

MeadWestvaco

Corporation

a+

BBB

Rohm and Haas Company

a+

BBB

Hospira Inc.

a

BBB-

Kinder Morgan Energy

Partners, L.P.

a

BBB-

The E. W. Scripps

Company

bbb+

BB

H. J. Heinz Company

bbb

BB-

Alcatel

-Lucent USA, Inc.

bb+

B

CDS

MDS Negative

Divergence

General Electric Capital

Corporation

a

AA+

Berkshire Hathaway Inc.

a

- AA

Amazon.com Inc.

bbb+

AA-

The Toronto

-Dominion

Bank

bbb+

AA-

Diamond Offshore Drilling,

Inc.

bb

BBB+

Chesapeake Energy

Corporation

b

BB+

Transocean Inc.

b

BB+

General Electric Company

a

- AA+

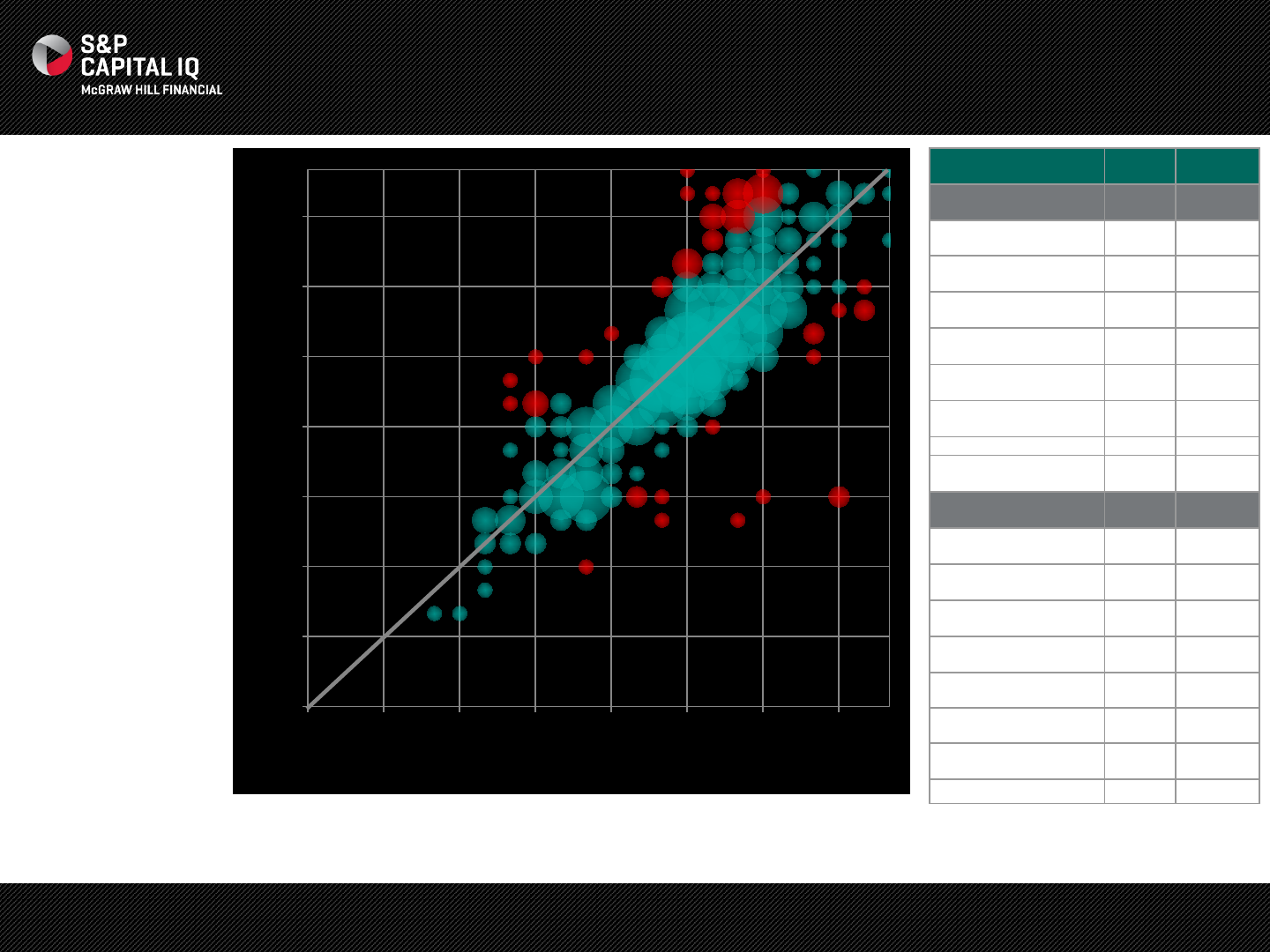

CDS Market Outliers

The Market Derived Signal (MDS) is a quantitative analytic that uses Credit Default Swaps (CDS) to facilitate the interpretation of how the CDS markets generally view the credit quality of

well-known firms and sovereigns. It aims to capture the market’s sentiment regarding an entity’s perceived credit risk. One of the objectives of the MDS is to identify where market sentiment

may differ from the issuer credit rating. CDS spreads are used to compute the difference between an entity’s actual spread and expected spread for a given rating. Universe is all

companies that have an S&P Long-Term Local Rating, primary headquarters in the U.S. or Canada, and an S&P Capital IQ sector classification. Source: S&P Capital IQ as of July 1, 2015

CDS MDS Score

Rating

bb

aaa

a

bbb

bb

b

ccc

c

d

aa

D/NR C CCC B BB BBB A AA AAA

15

S&P Capital IQ’s proprietary probability of default (PD) model, ‘Market Signals’, is a unique analytical model which provides daily changing, 1-year forward looking PDs of publicly listed

companies based on a cutting-edge econometric framework. Universe is all companies that have an S&P Long-Term Local Rating, primary headquarters in the U.S. or Canada, and an

S&P Capital IQ sector classification. Source: S&P Capital IQ as of July 1, 2015.

NOTES:

•In Q2 2015, 8 of the 10

sectors had improving PD

Market Signals. Telecom,

consumer staples, and

financials changed to

tightening from widening

PDs this quarter.

•Overall median PDs

decreased by 11% in Q2

continuing its trend from

Q1.

•Financials had the largest

improvement in PD in

addition to being one of the

safer sectors. Additionally,

energy continued to see its

credit improve as oil prices

stabilized.

Equity Market Sentiment Implied Default Risk By Sector

Cons. Discr.

Cons.

Staples Energy Financials Healthcare Industrials IT Materials Telecom. Utilities Grand Total

4/1/2015

0.15%

0.04%

1.01%

0.05%

0.03%

0.09%

0.04%

0.28%

0.60%

0.07%

0.12%

6/30/2015

0.14%

0.02%

0.60%

0.02%

0.03%

0.08%

0.04%

0.28%

0.39%

0.08%

0.11%

% Change

-6.23%

-56.41%

-40.54%

-62.00%

15.25%

-10.99%

-5.13%

-0.71%

-34.73%

12.41%

-10.59%

0.00%

0.01%

0.10%

1.00%

PD Market Signals (Median)

Cons. Discr.

Cons. Staples

Energy

Financials

Healthcare

Industrials

IT

Materials

Telecom.

Utilities

Grand Total

16

S&P Capital IQ’s proprietary probability of default (PD) model, ‘PD Model Fundamentals’, provides an innovative approach to assessing potential default that separates credit risk into two

components—financial risk and business risk. The PDs are applicable for any public or private company and provide a short- to mid-term view of credit risk. They are based purely on

fundamental data—financial ratios and macro factors – and are updated when new financials are released or there is some change in the macro factors. Universe is all companies that

have an S&P Long-Term Local Rating, primary headquarters in the U.S. or Canada, and an S&P Capital IQ sector classification. Source: S&P Capital IQ as of July 1, 2015.

NOTES:

•Fundamentals deteriorated

during the second quarter as

median PDs increased by 3%

year-over-year.

•9 of the 10 sectors show

worsening PDs on a year-over-

year basis as compared to only 4

out of 10 last quarter.

•The healthcare sector had two

consecutive quarters of median

credit improvement.

•Telecom sector fundamentals

continue to worsen by the largest

percentage, similar to last

quarter.

Fundamental Implied Default Risk By Sector

Cons.

Discr.

Cons.

Staples Energy Financials Healthcare Industrials IT Materials Telecom. Utilities Grand Total

% Change

(YoY) 5%

7%

1%

3%

-

3%

2%

0%

11%

13%

5%

3%

PD Level

(Median) 0.75%

0.39%

0.39%

0.15%

0.37%

0.56%

0.53%

0.70%

1.03%

0.21%

0.41%

Cons. Discr.

Cons. Staples

Energy

Financials

Healthcare

Industrials

IT

Materials

Telecom

Utilities

Grand Total

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

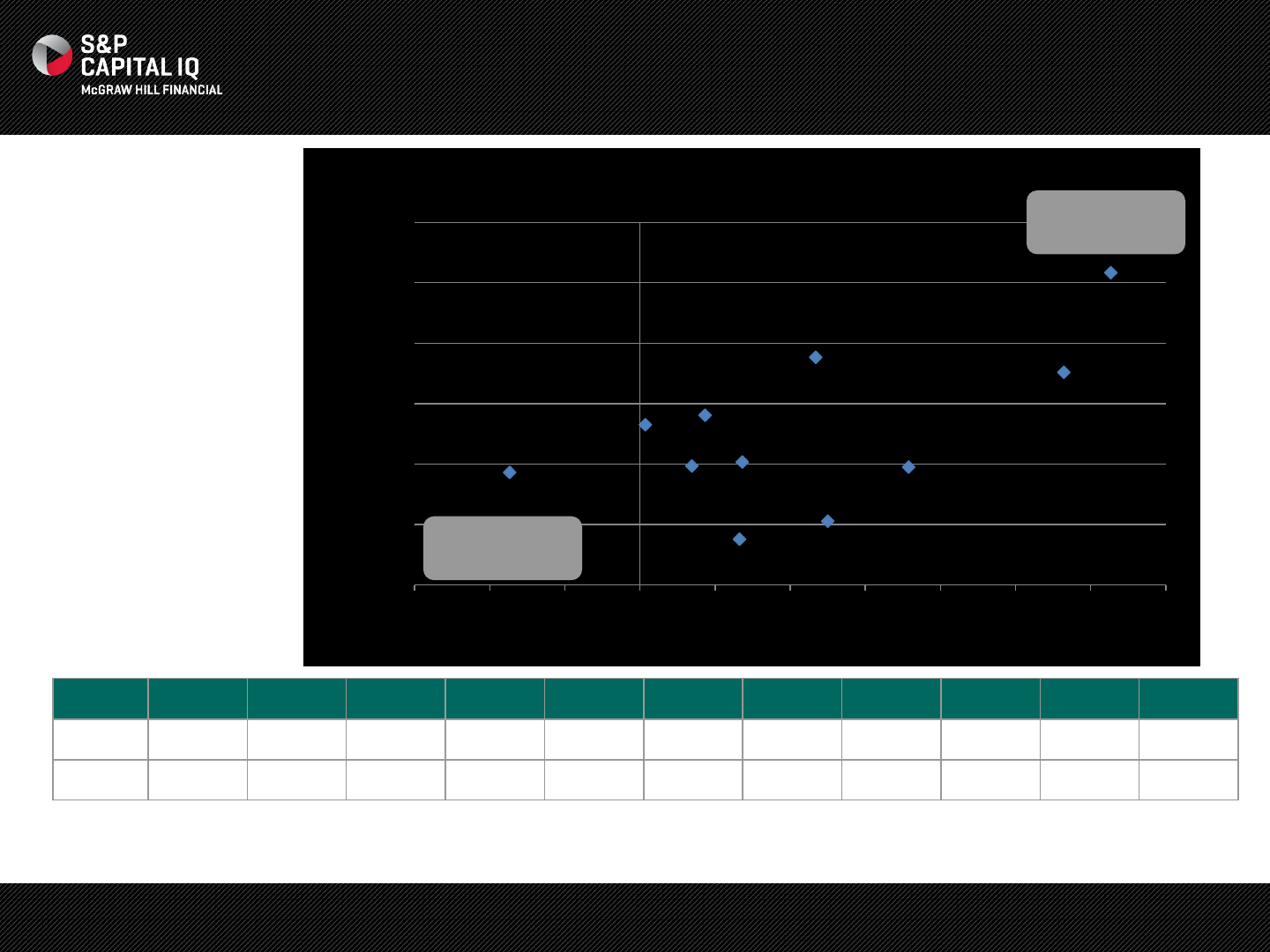

-6% -4% -2% 0% 2% 4% 6% 8% 10% 12% 14%

Probabiity of Default Level

% Change in PD Level (YoY)

PD Fundamentals

Most Risky and

Worsening

Least Risky and

Improving

17

NOTES:

•We have highlighted

companies with some of

the biggest divergences

between their S&P

Rating and their purely

quantitative

CreditModel (CM)

Score in red. This

provides us with a list of

firms with fundamental

attributes that make

them positive or

negative outliers. As

shown by the blue

circles, the vast majority

of firms were scored +/-

3 notches from their

Credit Rating.

•Within the universe we

observed a higher

distribution of

companies with higher

CM Scores than

Ratings, continuing

from last quarter.

Company

CM Score

S&P Rating

CreditModel Positive

Divergence

CVR Refining, LP

bbb

- B+

IAMGOLD Corp.

bbb

- B+

Visteon Corporation

bbb

- B+

Gulfport Energy Corp.

bb+

B

Life Time Fitness, Inc.

bb+

B

Paragon Offshore plc

bb+

B

The Wendy's Company

bb+

B

Office Depot, Inc.

bb

B-

CreditModel

Negative

Divergence

Madison Gas and Electric

Company

bbb

+ AA-

Northwest Natural Gas

Company

bbb

A+

Gaz Métro inc

bbb

- A

The Sherwin

-Williams

Company

bbb

- A

Adobe Systems

Incorporated

bb+

A-

Altera Corp.

bb+

A-

Northern Natural Gas

Company

bb+

A-

Nova Gas Transmission

Ltd.

bb+

A-

Lower-case nomenclature is used to differentiate S&P Capital IQ’s PD CreditModel Scores from credit ratings issued by Standard & Poor’s Rating Services. CreditModel

Score is trained on ratings, rather than on default data, which helps CreditModel generate a long-term stable view of credit risk that is aligned with a ratings process.

Source: S&P Capital IQ as of July 1, 2015.

Quantitatively Viewed Ratings Outliers

CM Score

Rating

aaa

a

bbb

bb

b

ccc

c

d

aa

D/NR C CCC B BB BBB A AA AAA

FINANCIAL RATIO TRENDS

19

NOTES:

•Debt/Total Capital

levels continued to

rise year-over-year

for both universes.

On a quarter-over-

quarter basis,

investment grade

companies have

seen debt/total

capital levels rise to

45% from 44%.

•EBITDA/Interest

Coverage levels

were down

significantly for high

yield companies

going from 6.9 to 5.9

over the last year.

Investment grade

remains relatively

flat for the past year.

•Cash Flows/Debt

levels declined as

companies

continued to issue

more debt due to

low interest rates.

Universe is all non-financial companies that have an S&P Long-Term Local Rating, primary headquarters in the U.S. or Canada, and an S&P

Capital IQ sector classification. Source: S&P Capital IQ as of July 1, 2015.

Financial Ratio Trends

0

10

20

30

40

50

60

70

HY IG

(%)

Debt/Total Capital

2011 Q1

2012 Q1

2013 Q1

2014 Q1

2015 Q1

0

2

4

6

8

10

12

14

16

18

2011 Q1 2012 Q1 2013 Q1 2014 Q1 2015 Q1

EBITDA/Interest Coverage

HY IG

0.00

0.02

0.04

0.06

0.08

0.10

0.12

0.14

2011 Q1 2012 Q1 2013 Q1 2014 Q1 2015 Q1

Cash Flow From Ops/Debt

HY IG

ISSUANCE TRENDS

21

Issuance Trends By Rating Category

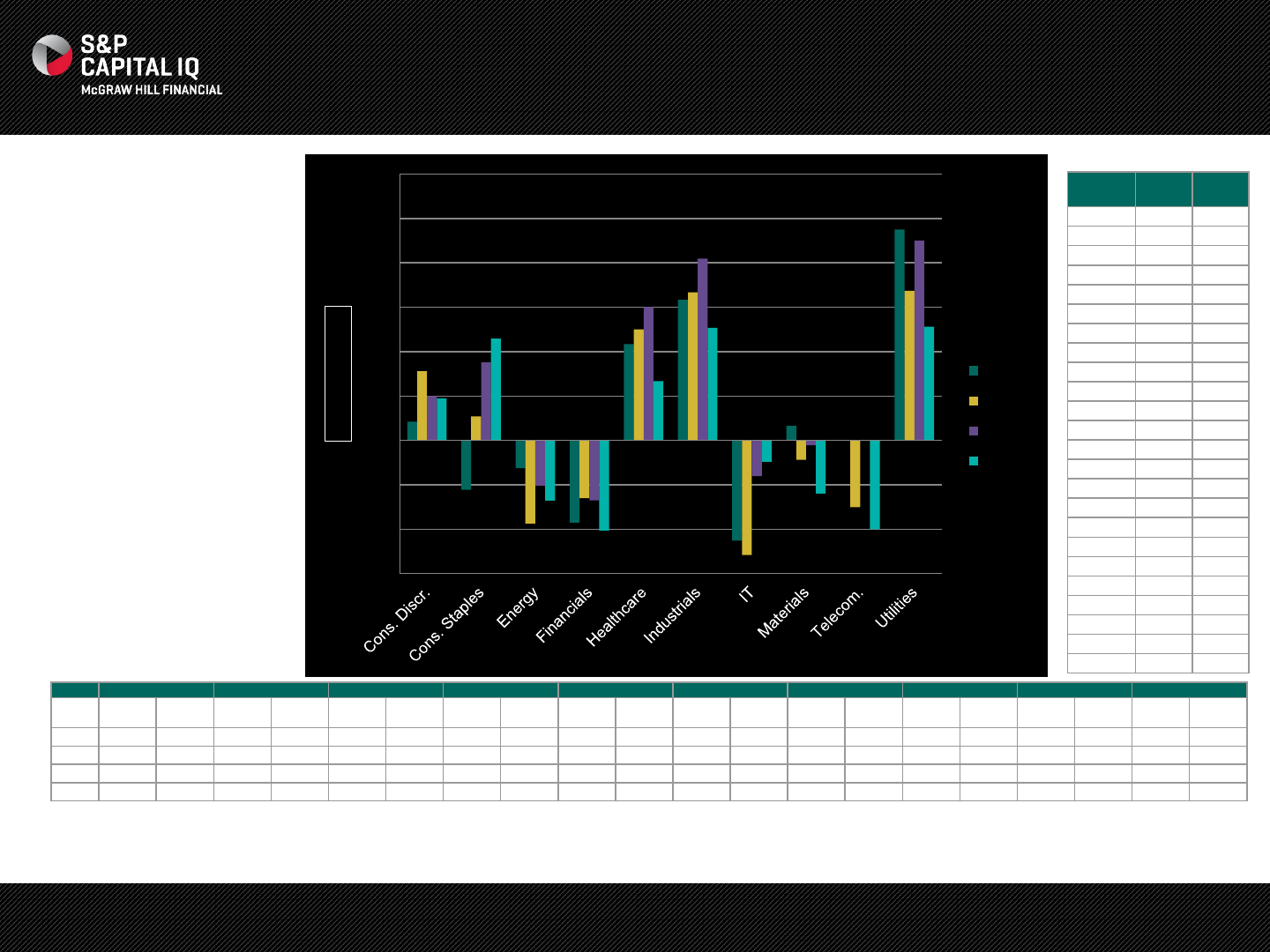

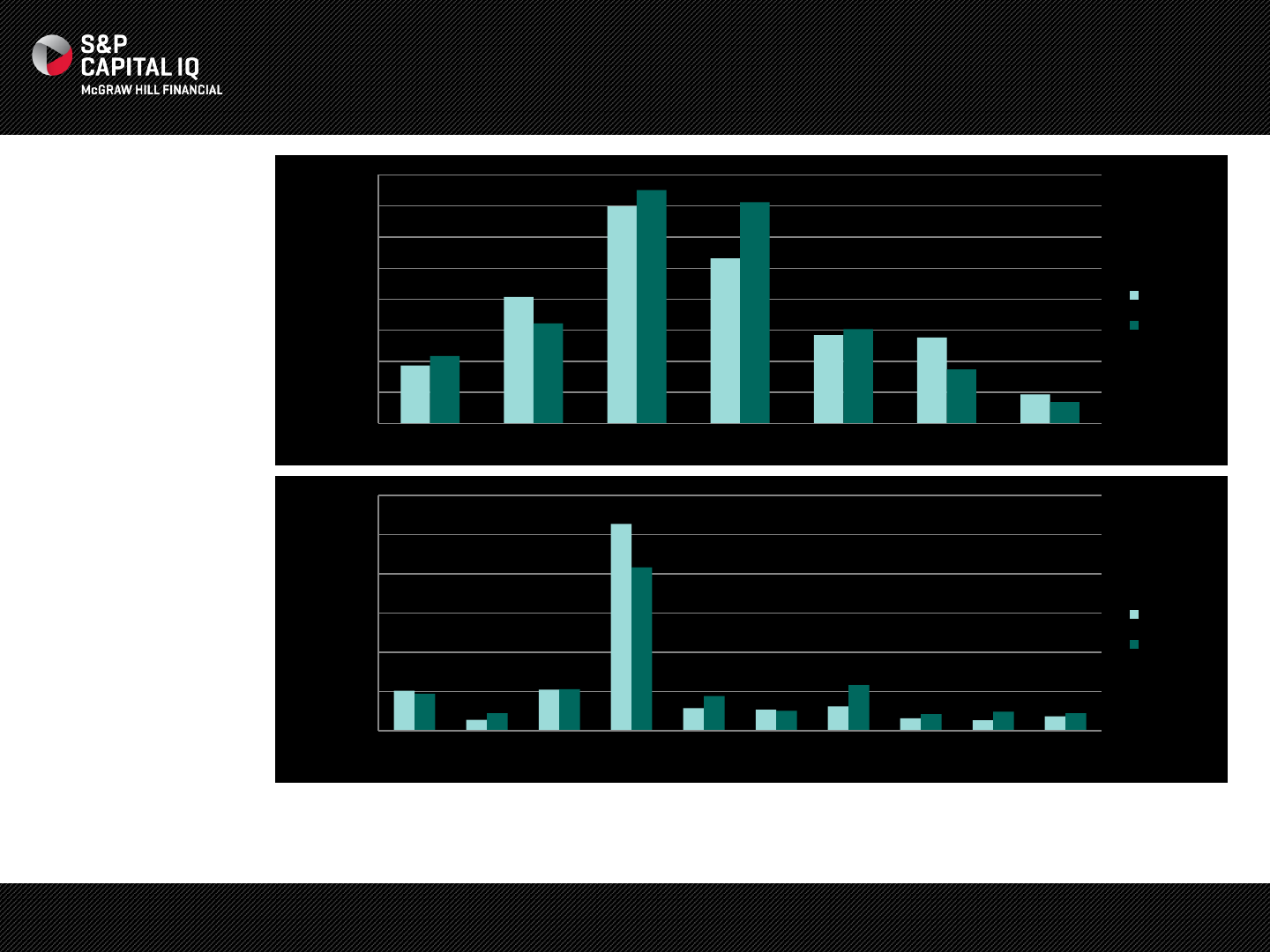

NOTES:

•Issuance was higher at

the lower end of

investment grade

issuers. BBB saw the

largest increase in new

volume.

•Only BB issuers

increased issuance

within high yield, while

the riskiest areas in

high yield saw declines

in issuance.

•7 of the 10 sectors

increased issuance

year-over-year with IT

having the largest

increase.

•Some of the biggest

issuers this quarter

include AT&T and

Abbvie.

Issuers are public and private companies globally that issue USD debt in U.S. bond markets. Securities include bonds, convertibles, notes and

MTNs. Amounts are aggregated by Date of Issuance. All values in USD $ billions. Source: S&P Capital IQ as of July 1, 2015.

$0

$50

$100

$150

$200

$250

$300

Cons.

Discr.

Cons.

Staples

Energy Financials Healthcare Industrials IT Materials Telecom. Utilities

($($Bil))

Q2 2014

Q2 2015

$0

$20

$40

$60

$80

$100

$120

$140

$160

AAA AA ABBB BB BCCC

($($Bil))

Q2 2014

Q2 2015

22

Covenants for High Yield Issuance

NOTES:

•The graph represents

the percentage of

companies with each

type of covenant within

new high yield

issuance.

•We observed a slight

increase in Q2 2015

covenants from low

levels in Q1 amid

weaker high yield

issuance markets.

•The fixed charge

covenant continues to

stay at lower levels

compared to 2014.

Universe incudes all high yield corporate debt issuance that is denominated in USD.

Source: S&P Capital IQ as of July 1, 2015.

0%

5%

10%

15%

20%

25%

30%

2013 Q2 2013 Q3 2013 Q4 2014 Q1 2014 Q2 2014 Q3 2014 Q4 2015 Q1 2015 Q2

Fixed Charge Coverage Dividend Related Payments Indebtedness

23

Contact Us

The Americas

+1 212 438 8701

+1 888 806 5541

Asia-Pacific

+852 2533 3588

Europe, Middle East or Africa

+44 (0) 20 7176 1233

How to Subscribe to Fixed Income IQ

Fixed Income IQ is published for S&P Capital IQ clients and select professionals. To receive a copy of the report, please register

online or send an email to fixedincomeiq@spcapitaliq.com and request inclusion in our distribution.

Submit Feedback to the Editor

Please contact us at fixedincomeiq@spcapitaliq.com with feedback and editorial suggestions.

Media Inquiries

Please contact Michael Privitera at michael.privitera@spcapitaliq.com.

www.spcapitaliq.com/trial

24

Disclosures

S&P Capital IQ is analytically and editorially independent from S&P Ratings Services. CreditModel and PD Market Signals (and various Market Derived Signals) are analytical tools but are not credit

ratings. Neither CreditModel, PD Market Signals nor credit ratings should be considered to be investment advice. A credit rating from Standard & Poor's Ratings Services is an opinion of the rated

organization's creditworthiness and involves both qualitative and quantitative characteristics. CreditModel and PD Scores are based on but differ significantly from Standard & Poor's Ratings

Services criteria and do not include a qualitative assessment or opinion. CreditModel and PD Market Signal scores are represented by lowercase nomenclature to differentiate them from S&P

Ratings Services credit ratings.

Charts, graphs and screenshots are provided for illustrative purposes only.

Copyright © 2015 by Standard & Poor’s Financial Services LLC (S&P), a part of McGraw Hill Financial. All rights reserved. STANDARD & POOR’S and S&P are registered trademarks of Standard

& Poor’s Financial Services LLC. CAPITAL IQ is a registered trademark of Capital IQ, Inc. iPad is a trademark of Apple Inc., registered in the U.S. and other countries. Microsoft, Excel, PowerPoint,

and Outlook are registered trademarks of Microsoft Corporation in the United States and/or other countries.

No content (including ratings, credit-related analyses and data, valuations model, software or other application or output therefrom) or any part thereof (Content) may be modified, reverse

engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval system, without the prior written permission of Standard & Poor’s Financial Services LLC or its

affiliates (collectively, S&P). The Content shall not be used for any unlawful or unauthorized purposes. S&P and any third-party providers, as well as their directors, officers, shareholders,

employees or agents (collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are not responsible for any errors or omissions

(negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or for the security or maintenance of any data input by the user. The Content is provided on an

“as is” basis. S&P PARTIES DISCLAIM ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS

FOR A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT’S FUNCTIONING WILL BE UNINTERRUPTED OR THAT

THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no event shall S&P Parties be liable to any party for any direct, indirect, incidental, exemplary,

compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs or losses caused by

negligence) in connection with any use of the Content even if advised of the possibility of such damages. Credit-related and other analyses, including ratings, and statements in the Content are

statements of opinion as of the date they are expressed and not statements of fact. S&P’s opinions, analyses and rating acknowledgment decisions (described below) are not recommendations to

purchase, hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security. S&P assumes no obligation to update the Content following publication

in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment and experience of the user, its management, employees, advisors and/or clients when

making investment and other business decisions. S&P does not act as a fiduciary or an investment advisor except where registered as such. While S&P has obtained information from sources it

believes to be reliable, S&P does not perform an audit and undertakes no duty of due diligence or independent verification of any information it receives. To the extent that regulatory authorities

allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certain regulatory purposes, S&P reserves the right to assign, withdraw or suspend such

acknowledgement at any time and in its sole discretion. S&P Parties disclaim any duty whatsoever arising out of the assignment, withdrawal or suspension of an acknowledgment as well as any

liability for any damage alleged to have been suffered on account thereof.

S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective activities. As a result, certain business units of

S&P may have information that is not available to other S&P business units. S&P has established policies and procedures to maintain the confidentiality of certain non-public information received in

connection with each analytical process.

S&P may receive compensation for its ratings and certain analyses, normally from issuers or underwriters of securities or from obligors. S&P reserves the right to disseminate its opinions and

analyses. S&P’s public ratings and analyses are made available on its Web sites, www.standardandpoors.com (free of charge), and www.ratingsdirect.com and www.globalcreditportal.com

(subscription), and may be distributed through other means, including via S&P publications and third-party redistributors. Additional information about our ratings fees is available at

www.standardandpoors.com/usratingsfees.