File 98722000 V409676 Summit Healthcare REITInc 10Qasfiled

User Manual: 98722000

Open the PDF directly: View PDF ![]() .

.

Page Count: 29

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

(Mark One)

For the quarterly period ended March 31, 2015

Or

Commission File Number 000-52566

SUMMIT HEALTHCARE REIT, INC. AND SUBSIDIARIES

(Exact name of registrant as specified in its charter)

800-978-8136

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by section 13 or 15(d) of the Exchange Act of 1934 during the preceding

12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past

90 days. Yes No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be

submitted and posted pursuant to Rule 405 of Regulation S-T (Sec.232.405 of this chapter) during the preceding 12 months (or for such shorter period that the

registrant was required to submit and post such files). Yes No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the

definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes No

As of May 11, 2015 we had 23,028,014 shares issued and outstanding.

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

MARYLAND 73-1721791

(State or other jurisdiction of (I.R.S. Employer

incorporation or organization) Identification No.)

2 SOUTH POINTE DRIVE, LAKE FOREST, CA 92630

(Address of

p

rinci

p

al executive offices) (Zi

p

Code)

Large accelerated file

r

Accelerated file

r

N

on-accelerated file

r

(Do not check if a smaller reporting company) Smaller reporting company

FORM 10-Q

SUMMIT HEALTHCARE REIT, INC. AND SUBSIDIARIES

TABLE OF CONTENTS

PART I. FINANCIAL INFORMATION

Item 1. Financial Statements: 3

Condensed Consolidated Balance Sheets (unaudited) 3

Condensed Consolidated Statements of Operations (unaudited) 4

Condensed Consolidated Statement of Equity (unaudited) 5

Condensed Consolidated Statements of Cash Flows (unaudited) 6

N

otes to Condensed Consolidated Financial Statements (unaudited) 7

Item 2. Mana

g

ement’s Discussion and Anal

y

sis of Financial Condition and Results of O

p

erations 18

Item 3. Quantitative and Qualitative Disclosures About Market Ris

k

23

Item 4. Controls and Procedures 23

PART II. OTHER INFORMATION

Item 1. Le

g

al Proceedin

g

s23

Item 1A. Risk Factors 23

Item 2. Unre

g

istered Sales of E

q

uit

y

Securities and Use of Proceeds 24

Item 3. Defaults U

p

on Senior Securities 24

Item 4. Mine Safet

y

Disclosures 24

Item 5. Other Information 24

Item 6. Exhibits 24

SIGNATURES 26

EX-31.1

EX-31.2

EX-32

2

PART I — FINANCIAL INFORMATION

Item 1. Financial Statements

SUMMIT HEALTHCARE REIT, INC. AND SUBSIDIARIES

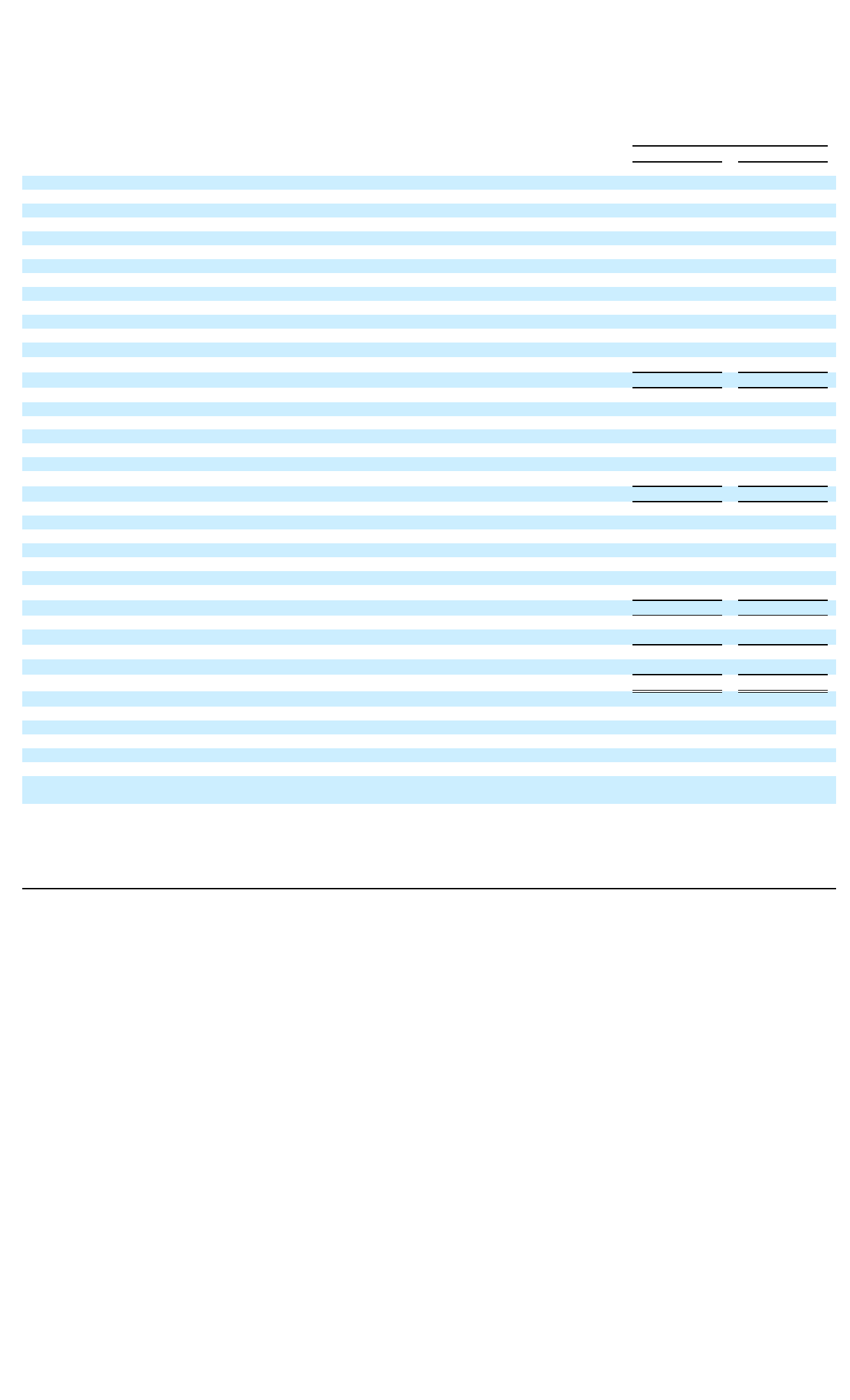

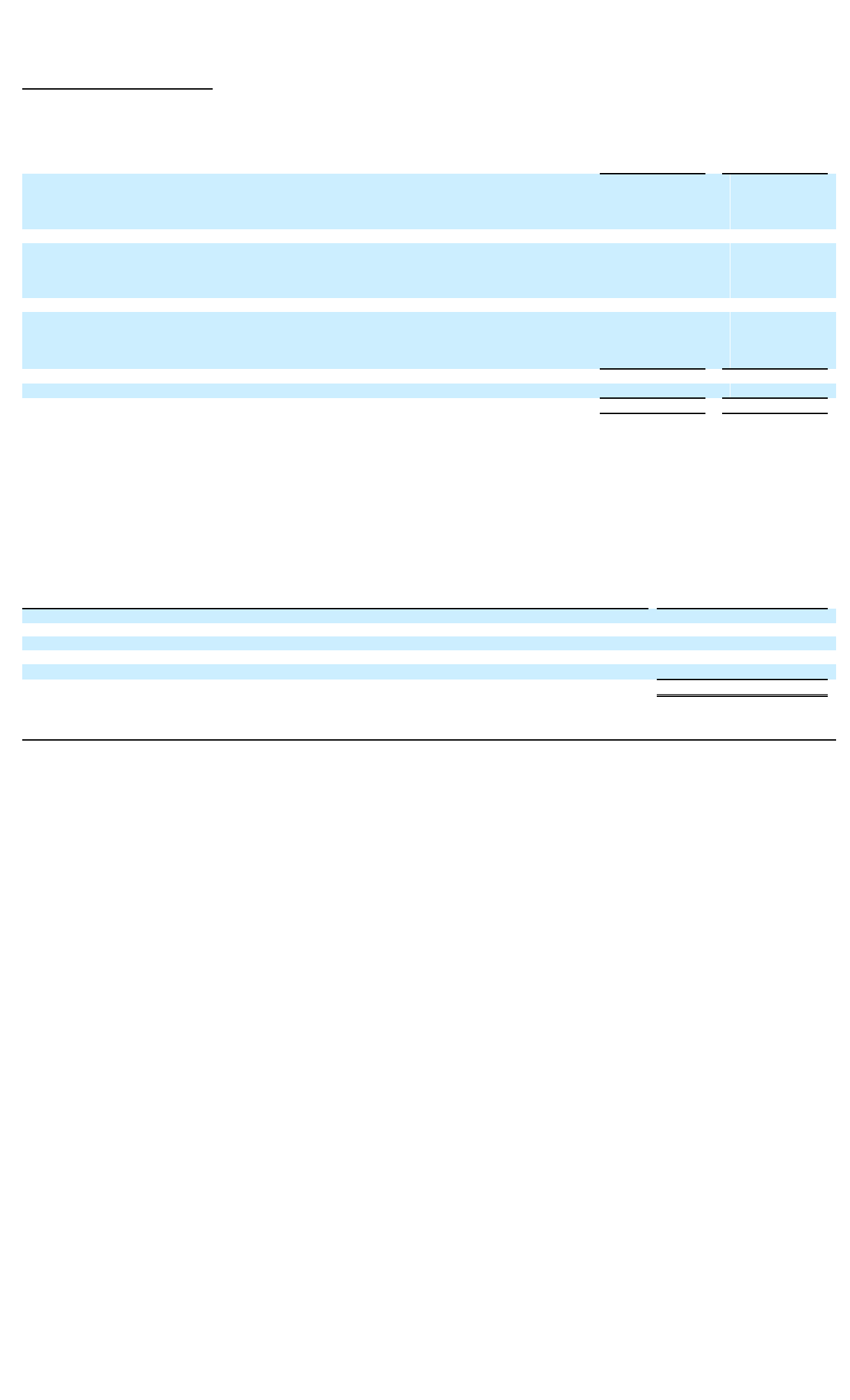

CONDENSED CONSOLIDATED BALANCE SHEETS (Unaudited)

The accompanying notes are an integral part of these Condensed Consolidated Financial Statements.

March 31,

2015 December 31,

2014

ASSETS

Cash and cash equivalents $ 1,486,000 $ 4,405,000

Restricted cash 4,112,000 3,759,000

Real estate properties (certain assets held in variable interest entity):

Lan

d

8,932,000 8,432,000

Buildin

g

s and im

p

rovements, net 97,006,000 84,428,000

Furniture and fixtures, net 6,161,000 5,862,000

Real estate properties, net 112,099,000 98,722,000

N

otes receivable 4,855,000 132,000

Deferred costs and deposits 142,000 356,000

Deferred financing costs, net 1,400,000 1,453,000

Tenant and other receivables, net 3,464,000 2,599,000

Deferred leasing commissions, net 1,818,000 1,859,000

Other assets, net 459,000 657,000

Assets of variable interest entity held for sale

—

4,139,000

Total assets $ 129,835,000 $ 118,081,000

LIABILITIES AND STOCKHOLDERS’ EQUITY

Accounts

p

a

y

able and accrued liabilities $ 2,208,000 $ 1,995,000

Accrued salaries and benefits 205,000 342,000

Securit

y

de

p

osits 2,325,000 2,029,000

Liabilities

(

certain liabilities held in variable interest entit

y)

:

Loans

p

a

y

able, net of debt discounts 89,154,000 77,972,000

Liabilities of variable interest entity held for sale

—

2,700,000

Total liabilities 93,892,000 85,038,000

Commitment, contingencies and subsequent events

Stockholders’ E

q

uit

y

Preferred stock, $0.001 par value; 10,000,000 shares authorized; no shares issued or outstanding at March 31,

2015 and December 31, 2014

Common stock, $0.001 par value; 290,000,000 shares authorized; 23,028,014

shares issued and outstanding at March 31, 2015 and

December 31, 2014 23,000 23,000

Additional

p

ai

d

-in ca

p

ital 117,226,000 117,226,000

Accumulated deficit (82,846,000) (80,873,000)

Total stockholders’ equity 34,403,000 36,376,000

N

oncontrolling interest 1,540,000

(

3,333,000)

Total equity 35,943,000 33,043,000

Total liabilities and stockholders’ equity $ 129,835,000 $ 118,081,000

3

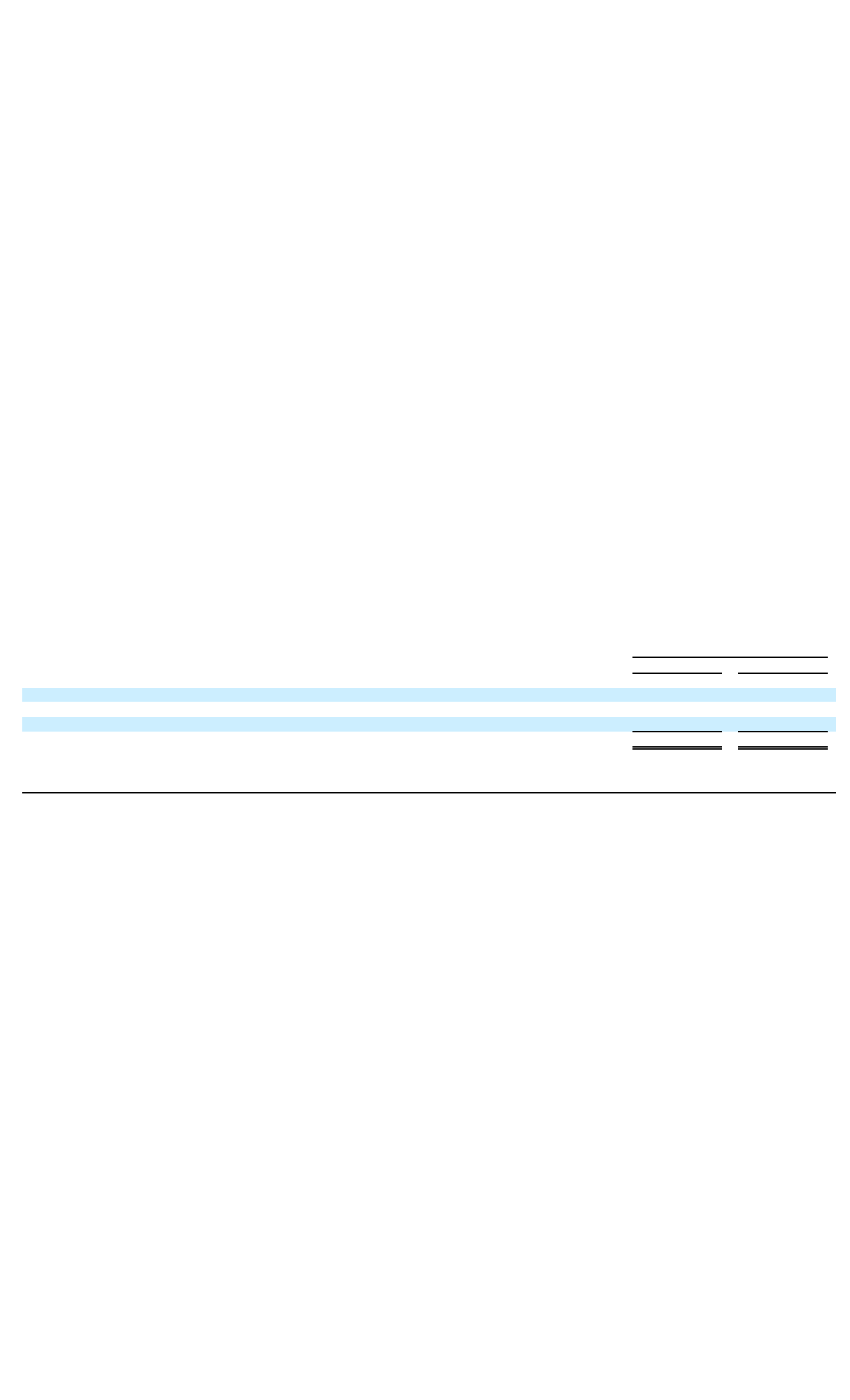

SUMMIT HEALTHCARE REIT, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (Unaudited)

The accompanying notes are an integral part of these Condensed Consolidated Financial Statements.

Three Months Ended March 31,

2015 2014

Revenues:

Rental revenues $ 2,671,000 $ 1,736,000

Resident services and fee income 2,243,000

—

Tenant reimbursements and other income 312,000 202,000

Interest income from notes receivable 2,000 4,000

5,228,000 1,942,000

Ex

p

enses:

Pro

p

ert

y

o

p

eratin

g

costs 575,000 348,000

Resident services costs 1,737,000

—

General and administrative 944,000 670,000

Asset mana

g

ement fees and ex

p

enses

—

205,000

Real estate ac

q

uisition costs

—

4,000

De

p

reciation and amortization 1,245,000 1,238,000

Reserve for excess advisor obligation

—

189,000

4,501,000 2,654,000

Operating income (loss) 727,000 (712,000)

Other income and

(

ex

p

ense

)

:

Other income 2,000 13,000

Interest expense (1,083,000) (720,000)

Loss from continuing operations (354,000) (1,419,000)

Discontinued operations:

Loss from discontinued operations

(

1,582,000)

(

165,000)

Loss from discontinued operations

(

1,582,000)

(

165,000)

N

et loss

(

1,936,000

)

(

1,584,000

)

Noncontrolling interests’ share in losses (37,000) 345,000

N

et loss applicable to common stockholders $

(

1,973,000) $

(

1,239,000)

Basic and diluted loss per common share

Continuing operations applicable to common stockholders $ (0.02) $ (0.06)

Discontinued operations $

(

0.07)$0.01

Net loss applicable to common stockholders $

(

0.09)$

(

0.05)

Weighted average shares used to calculate basic

and diluted net loss per common share 23,028,014 23,028,285

4

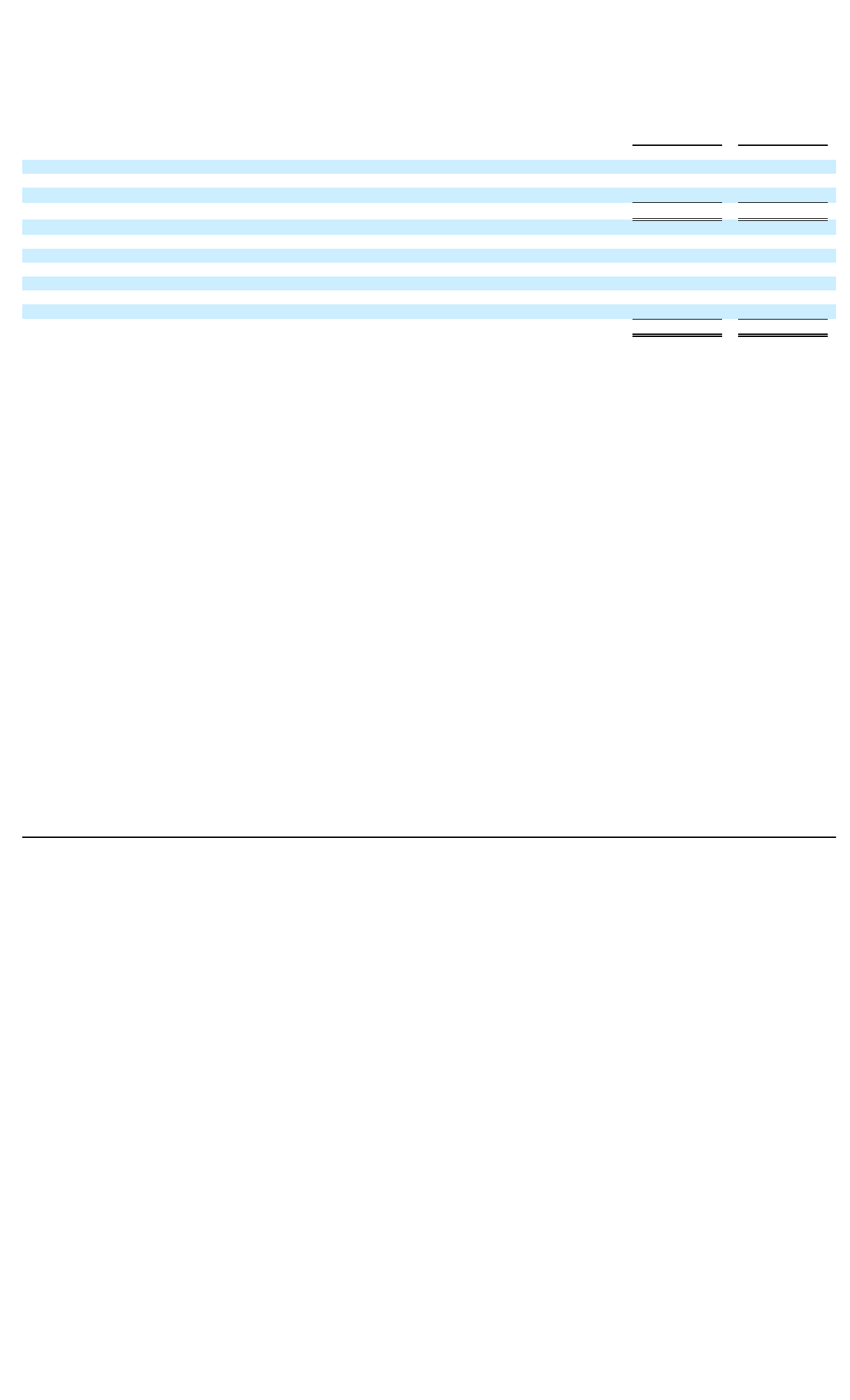

SUMMIT HEALTHCARE REIT, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENT OF EQUITY

For the Three Months Ended March 31, 2015

(Unaudited)

The accompanying notes are an integral part of these Condensed Consolidated Financial Statements.

Common Stock

Number

of

Shares

Common

Stock

Par

Value

Additional

Paid-In

Capital Accumulated

Deficit

Total

Stockholders’

Equity Noncontrolling

Interests Total

Equity

Balance

—

January 1, 2015 23,028,014 $ 23,000 $ 117,226,000 $ (80,873,000) $ 36,376,000 $ (3,333,000) $ 33,043,000

Dividends paid to noncontrolling interests

—

—

—

—

—

(42,000) (42,000)

Decrease in non-controlling interests related to disposition

of a VIE

—

—

—

—

—

4,878,000 4,878,000

N

et loss

—

—

—

(1,973,000) (1,973,000) 37,000 (1,936,000)

Balance

—

March 31, 2015 23,028,014 $ 23,000 $ 117,226,000 $ (82,846,000) $ 34,403,000 $ 1,540,000 $ 35,943,000

5

SUMMIT HEALTHCARE REIT, INC. AND SUBSIDIARIES

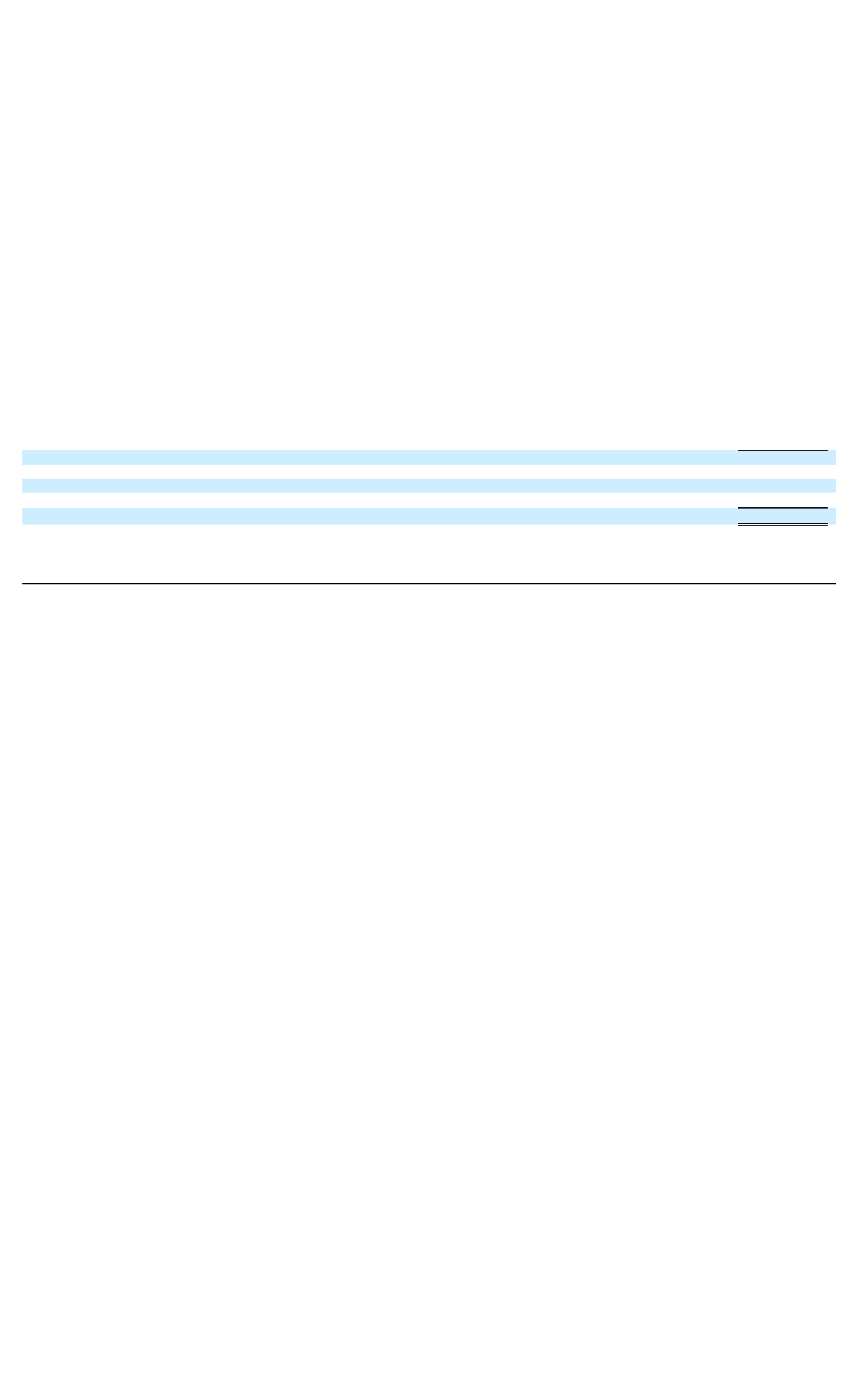

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited)

The accompanying notes are an integral part of these Condensed Consolidated Financial Statements.

Three Months Ended March 31,

2015 2014

Cash flows from o

p

eratin

g

activities:

N

et loss $ (1,936,000) $ (1,584,000)

Adjustments to reconcile net loss to net cash and cash equivalents provided by (used in) operating activities:

Amortization of deferred financing costs and debt discounts 74,000 47,000

Depreciation and amortization 1,245,000 1,238,000

Straight-line rents (356,000)65,000

Bad debt expense 8,000 37,000

Loss on disposition of VIE 1,582,000

—

Change in operating assets and liabilities:

Tenant and other receivables, net (319,000)72,000

Pre

p

aid and other assets 195,000 134,000

Pre

p

aid rent, securit

y

de

p

osit and deferred revenues 99,000

(

244,000

)

Related

p

art

y

receivables

(

1,000

)

(

123,000

)

Accounts payable and accrued liabilities 214,000 222,000

Accrued salaries and benefits (136,000)

—

Net cash and cash equivalents provided by (used in) operating activities 669,000 (136,000)

Cash flows from investing activities

Restricted cash (353,000)(99,000)

Deferred costs and deposits 15,000 (1,000)

Real estate acquisitions and capitalized costs (14,300,000)

—

Real estate improvements (70,000)(2,000)

Payments from note receivable 9,000

—

Net cash and cash equivalents used in investing activities

(

14,699,000)

(

102,000)

Cash flows from financin

g

activities:

Proceeds from issuance of loans

p

a

y

able 11,440,000

—

Pa

y

ments of loans

p

a

y

able

(

173,000

)

(

118,000

)

Non-controlling interest contribution

—

257,000

Distributions paid to non-controlling interests (42,000)(18,000)

Deferred financing costs

(

114,000)

—

Net cash and cash equivalents provided by financing activities 11,111,000 121,000

N

et decrease in cash and cash e

q

uivalents

(

2,919,000

)

(

117,000

)

Cash and cash equivalents - beginning of period 4,405,000 10,662,000

Cash and cash equivalents - end of period (including cash of VIE) 1,486,000 10,545,000

Less cash and cash equivalents of VIE held for sale

–

end of period (see Note 10)

—

(

45,000)

Cash and cash equivalents

–

end of perio

d

$ 1,486,000 $ 10,500,000

NON CASH INVESTING AND FINANCING

Su

pp

lemental disclosure of cash flow information:

Cash

p

aid for interest $ 998,000 $521,000

Securit

y

de

p

osit not receive

d

$ 198,000

—

Su

pp

lemental disclosure of non-cash investin

g

activities:

In January 2015, the Company sold its interests in Sherburne Commons for a note receivable for $5.0 million due in

December 2017

(

see Note 6

)

.

In Januar

y

2015, $207,000 of deferred costs were reclassified to real estate ac

q

uisitions.

6

SUMMIT HEALTHCARE REIT, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

MARCH 31, 2015

(Unaudited)

1. Organization

Summit Healthcare REIT, Inc., a Maryland Corporation, was formed on October 22, 2004 under the General Corporation Law of Maryland for the purpose o

f

engaging in the business of investing in and owning commercial real estate. As used in this report, the “Company”, “we”, “us” and “our” refer to Summi

t

Healthcare REIT, Inc. and its consolidated subsidiaries (including variable interest entities) except where the context otherwise requires. Until April 1, 2014 an

d

subject to certain restrictions and limitations, our business was managed pursuant to an advisory agreement (the “Advisory Agreement”) with Cornerstone Realt

y

Advisors, LLC (“CRA”). Beginning April 1, 2014, the Company became self-managed and hired employees to directly manage its operations.

Generally we conduct substantially all of our operations through Summit Healthcare Operating Partnership, L.P. (the “Operating Partnership”), a Delaware

limited partnership, which was formed on November 30, 2004. At March 31, 2015, we own a 99.88% general partner interest in the Operating Partnership while

CRA owns a 0.12% limited partnership interest. Our financial statements and the financial statements of the Operating Partnership are consolidated in the

accompanying condensed consolidated financial statements. These financial statements include consolidation of a variable interest entity (“VIE”) that was

classified as held for sale until January 7, 2015, at which time the VIE was sold (see Note 6).

In 2012, we formed Cornerstone Healthcare Partners LLC (“CHP LLC”) with Cornerstone Healthcare Real Estate Fund, Inc. (“CHREF”), an affiliate of CRA.

We own 95% of CHP LLC, with the remaining 5% owned by CHREF. As CHP LLC’s equity holders have voting rights disproportionate to their economic

interests in the entity, CHP LLC is considered to be a VIE. We have a controlling financial interest in CHP LLC because we have the power to direct the activities

of the VIE that most significantly impact its economic performance and we have the obligation to absorb the VIE’s losses and the right to receive benefits fro

m

the VIE. Consequently, we are deemed to be the primary beneficiary of the VIE, and therefore have consolidated the operations of the VIE.

During 2012, we acquired Sheridan Care Center, Fernhill Care Center, Farmington Square, Friendship Haven Healthcare and Rehabilitation Center (“Friendship

Haven”) and Pacific Health and Rehabilitation Center (“Pacific”) healthcare properties (collectively, the “JV Properties”) through CHP LLC. In the third quarte

r

of 2013, CHP LLC sold a portion of its interests in the JV Properties to third party investors. Proceeds from the sale of interests in these JV Properties were

approximately $0.9 million as of March 31, 2014, of which we received $0.9 million and CHREF received $41,000. As such, as of March 31, 2015, we owne

d

an 89.0% interest in the JV Properties, CHREF owned a 4.7% interest and third party investors owned 6.3%. The CHP LLC offering has been terminated.

In May 2014, we formed a taxable REIT subsidiary (“Friendswood TRS”) which became the licensed operator and tenant of Friendship Haven (see Note 4).

2. Summary of Significant Accounting Policies

For more information regarding our significant accounting policies and estimates, please refer to “Summary of Significant Accounting Policies” contained in ou

r

Annual Report on Form 10-K for the year ended December 31, 2014 filed with the Securities and Exchange Commission (“SEC”) on March 20, 2015. There have

been no material changes to our policies since that filing.

The accompanying condensed consolidated balance sheet at December 31, 2014 has been derived from the audited consolidated financial statements at that date.

We assume that users of these condensed consolidated financial statements have read or have access to the audited December 31, 2014 consolidated financial

statements and Management's Discussion and Analysis of Financial Condition and Results of Operations contained in our Annual Report on Form 10-K for the

year ended December 31, 2014 filed with the SEC on March 20, 2015 and that the adequacy of additional disclosure needed for a fair presentation, except i

n

regard to material contingencies, may be determined in that context. Accordingly, footnotes and other disclosures which would substantially duplicate those

contained in our most recent Annual Report on Form 10-K for the year ended December 31, 2014 have been omitted in this report.

7

P

rinci

p

les o

f

Consolidation and Basis o

f

Presentation

The accompanying condensed consolidated financial statements include the accounts of the Company, its wholly-owned subsidiaries, CHP LLC (of which the

Company owns 95%) and Nantucket Acquisition LLC, a variable interest entity through January 7, 2015 (see Note 6). All intercompany accounts and transactions

have been eliminated in consolidation.

The accompanying financial information reflects all adjustments, which are, in the opinion of management, of a normal recurring nature and necessary for a fai

r

p

resentation of our financial position, results of operations and cash flows for the interim periods. Interim results of operations are not necessarily indicative o

f

the results to be expected for the full year. Operating results for the three months ended March 31, 2015 are not necessarily indicative of the results that may be

expected for the year ending December 31, 2015.

R

ecentl

y

Issued Accountin

g

Pronouncements

The Financial Accounting Standards Board (“FASB”) has issued Accounting Standards Update (ASU) No. 2015-03, Interest - Imputation of Interest (Subtopic

835-30): Simplifying the Presentation of Debt Issuance Costs. The amendments in this ASU require that debt issuance costs related to a recognized debt liabilit

y

b

e presented in the balance sheet as a direct deduction from the carrying amount of that debt liability, consistent with debt discounts. The recognition an

d

measurement guidance for debt issuance costs are not affected by the amendments in this ASU.

For public business entities, the amendments are effective for financial statements issued for fiscal years beginning after December 15, 2015, and interim periods

within those fiscal years. For all other entities, the amendments are effective for financial statements issued for fiscal years beginning after December 15, 2015,

and interim periods within fiscal years beginning after December 15, 2016.

Early adoption of the amendments is permitted for financial statements that have not been previously issued.

The amendments should be applied on a retrospective basis, wherein the balance sheet of each individual period presented should be adjusted to reflect the

period-specific effects of applying the new guidance. Upon transition, an entity is required to comply with the applicable disclosures for a change in a

n

accounting principle. These disclosures include the nature of and reason for the change in accounting principle, the transition method, a description of the prior-

p

eriod information that has been retrospectively adjusted, and the effect of the change on the financial statement line items (i.e., debt issuance cost asset and the

debt liability). The Company has evaluated the impact of this new standard and does not expect it to have a significant effect on the consolidated financial

statements, when adopted.

R

eclassi

f

ications

Certain amounts in the Company’s condensed consolidated financial statements for prior year have been reclassified to conform to the current perio

d

p

resentation. Based on the intended use of the restricted cash, we have classified changes in restricted cash within the statements of cash flows as investing

activities and the prior year presentation has been revised to conform to this classification. These reclassifications had no effect on total consolidated assets or ne

t

loss.

3. Fair Value Measurements of Financial Instruments

Our condensed consolidated balance sheets include the following financial instruments: cash and cash equivalents, restricted cash, notes receivable (except as

noted below), certain other assets, deferred costs and deposits, tenant and other receivables, deferred leasing commissions, security deposits and loans payable.

With the exception of the Nantucket note receivable (see Note 6) and loans payable discussed below, we consider the carrying values to approximate fair value

for such financial instruments because of the short period of time between origination of the instruments and their expected payment.

8

As of March 31, 2015, the fair value of the Nantucket note receivable (see Note 6) was $4.9 million compared to the carrying value of $4.9 million. The fair value

of the note receivable was estimated based on cash flow analysis at an assumed market rate of interest. As the inputs to our valuation estimate are neithe

r

observable in nor supported by market activity, our notes receivable are classified as Level 3 assets within the fair value hierarchy.

As of March 31, 2015 and December 31, 2014, the fair value of loans payable was $91.3 million and $80.1 million compared to the carrying value of $90.0

million and $78.8 million, respectively. The fair value of loans payable is estimated using lending rates available to us for financial instruments with similar terms

and maturities. To estimate fair value as of March 31, 2015, we utilized a discount rate ranging from 4.4% to 4.75% and a weighted-average of 4.63%. As the

inputs to our valuation estimate are neither observable in nor supported by market activity, our loans payable are classified as Level 3 assets within the fair value

hierarchy.

As a result of our ongoing analysis for potential impairment of our investments in real estate, we may be required to adjust the carrying value of certain assets to

their estimated fair values, or estimated fair value less selling costs, under certain circumstances (see Note 4). No impairments were recorded during the three

months ended March 31, 2015.

At March 31, 2015 and December 31, 2014, we do not have any financial assets or financial liabilities that are measured at fair value on a recurring basis in ou

r

condensed consolidated financial statements.

4. Investments in Real Estate Properties

As of March 31, 2015 and December 31, 2014, adjusted cost and accumulated depreciation and amortization related to investments in real estate excluding assets

of variable interest entity held for sale, were as follows:

As of March 31, 2015, our portfolio consists of 17 properties which were 100% leased to the operators of the related facilities. The following table provides

summary information regarding our properties:

March 31, 2015 December 31, 2014

Land $ 8,932,000 $ 8,432,000

Buildin

g

s and im

p

rovements 101,560,000 88,241,000

Less: accumulated depreciation

(

4,554,000)

(

3,813,000)

Buildings and improvements, net 97,006,000 84,428,000

Furniture and fixtures 8,891,000 8,133,000

Less: accumulated depreciation (2,730,000) (2,271,000)

Furniture and fixtures, net 6,161,000 5,862,000

Real estate properties, net $ 112,099,000 $ 98,722,000

Pro

p

ert

y

(1) Location Date Purchased T

yp

ePurchase

Price

Loans

Payable

as of

March 31,

2015 Number of

Beds

Sheridan Care Cente

r

Sheridan, OR Au

g

ust 3, 2012 SNF $ 4,100,000 $ 5,145,000 51

Fernhill Care Cente

r

Portland, OR Au

g

ust 3, 2012 SNF 4,500,000 4,514,000 63

Farmin

g

ton S

q

uare Medford, OR Se

p

tember 14, 2012 AL/MC 8,500,000 6,840,000 71

Friendship Haven Healthcare and

Rehabilitation Center (2) Galveston County, TX September 14, 2012 SNF 15,000,000 6,374,000 150

Pacific Health and Rehabilitation

Cente

r

Ti

g

ard, OR December 24, 2012 SNF 8,140,000 7,525,000 73

Danb

y

House Winston-Salem, NC Januar

y

31, 2013 AL/MC 9,700,000 7,275,000 100

Brookstone of Aledo Aledo, IL Jul

y

2, 2013 AL 8,625,000 5,843,000 66

The Shelb

y

House Shelb

y

, NC October 4, 2013 AL 4,500,000 4,921,000 72

The Hamlet House Hamlet, NC October 4, 2013 AL 6,500,000 4,158,000 60

The Carteret House New

p

ort, NC October 4, 2013 AL 4,300,000 3,508,000 64

Sundial Assisted Livin

g

Reddin

g

, CA December 18, 2013 AL 3,500,000 2,800,000 65

Lamar Estates Lamar, CO Se

p

tember 22, 2014 SNF 4,500,000 3,418,000 60

Monte Vista Estates Monte Vista, CO Se

p

tember 22, 2014 SNF 3,400,000 2,582,000 60

M

y

rtle Point Care Cente

r

M

y

rtle Point, OR October 31, 2014 SNF 4,150,000 3,075,000 54

Gateway Care and Retirement

Cente

r

Portland, OR December 31, 2014 SNF/IL 11,250,000 8,435,000 91

Applewood

Retirement Community Salem, OR December 31, 2014 IL 2,900,000 2,165,000 69

Loving Arms Assisted Living Front Royal, VA January 23, 2015 AL 14,300,000 11,440,000 84

Total: $ 117,865,000 $ 90,018,000 1,253

(1) The above table excludes Sherburne Commons Residences, LLC (“Sherburne Commons”), a variable interest entity that on January 7, 2015 was sold

(see Note 6).

(2) We terminated the lease with the operator of this facility on March 16, 2014 and became the licensed operator of the facility on May 1, 2014 through a

wholly-owned taxable REIT subsidiary (Friendswood TRS).

9

Friendswood TRS

Beginning in January 2014, the tenant/operator of Friendship Haven ceased paying rent payments due to us under the lease agreement. On March 16, 2014, we

terminated the lease agreement. Effective May 1, 2014, we became the licensed operator of the facility through Friendswood TRS. Upon becoming the license

d

operator of the facility, we entered into a management agreement with an affiliate of Stonegate Senior Living (“Stonegate”). We plan to operate the facility wit

h

the Stonegate affiliate or another manager until a long-term lease agreement can be secured. We are currently seeking to secure a long term triple net lease wit

h

an operator and plan to finalize an arrangement in 2015.

L

easin

g

Commissions

Leasing commissions (paid to CRA prior to April 1, 2014) are capitalized at cost and amortized on a straight-line basis over the related lease term. As of Marc

h

31, 2015 and December 31, 2014, total costs incurred were $2.2 million and the unamortized balance of capitalized leasing commissions was $1.8 million an

d

$1.9 million, respectively. In March 2014, the amortization of Friendship Haven’s leasing commission totaling $0.4 million was accelerated due to the lease

termination on March 16, 2014. Amortization expense for the three months ended March 31, 2015 and 2014 was $40,000 and $409,000, respectively.

A

c

q

uisitions - 2015

Front Royal, Virginia

On January 23, 2015, we acquired an 84 bed assisted living facility in Front Royal, Virginia (“Loving Arms Assisted Living”) for a total purchase price of $14.3

million, which was funded through cash on hand plus a collateralized loan as described in Note 8. Loving Arms is leased to an affiliate of Meridian Senior Living,

LLC under a 15 year triple net lease.

The following sets forth the allocation of the purchase price of the property acquired in 2015 as well as the associated acquisitions costs, all of which have bee

n

capitalized. We have accounted for the acquisition as an asset purchase under generally accepted accounting principles (“GAAP”).

Total

Lan

d

$500,000

Buildin

g

s & im

p

rovements 12,707,000

Site im

p

rovements 540,000

Furniture & fixtures 760,000

Real estate acquisition and capitalized costs $ 14,507,000

Thir

d

-

p

art

y

ac

q

uisition costs, ca

p

italized

(

included above

)

$207,000

10

See Note 11, Subsequent Events for further information.

5. Concentration of Risk

Our cash is generally invested in investment-grade short-term instruments. As of March 31, 2015, we had cash and cash equivalent accounts in excess of FDIC-

insured limits. However, we do not believe the risk associated with this excess is significant.

As of March 31, 2015, we owned one property in California, seven properties in Oregon, four properties in North Carolina, one property in Texas, one property i

n

Illinois, two properties in Colorado and one property in Virginia. Accordingly, there is a geographic concentration of risk subject to economic conditions i

n

certain states. Additionally, as of March 31, 2015, we leased our 17 healthcare properties to six different tenants under long-term triple net leases, three of whic

h

comprise 35%, 28% and 13% of our tenant rental revenue. As of March 31, 2014, we leased our 11 healthcare properties to five different tenants under long-ter

m

triple net leases, two of which comprise 46% and 26% of our tenant rental revenue.

6. Notes Receivable

S

ervant Healthcare Investments, LLC

The Servant Healthcare Investments, LLC note was paid in full on May 2, 2014. For the three months ended March 31, 2015 and 2014, interest income related to

the note receivable was $0 and $4,000, respectively.

Fernhill Note

In September 2014, the Company loaned to the operator of the Fernhill facility approximately $140,000 for certain property improvements. The note provides fo

r

interest at a fixed rate of 6% and is payable in monthly installments through January 2019. As of March 31, 2015 and December 31, 2014, the balance on the note

was approximately $0.1 million.

N

antucket Note - Consolidation and Sale of VIE

We held a note receivable from a participating first mortgage loan made to Nantucket Acquisition LLC (“Nantucket”), a Delaware limited liability compan

y

owned and managed by Cornerstone Ventures Inc., an affiliate of CRA, which was collateralized by Sherburne Commons. We had not recorded interest income

on this note since October 2010 because of the doubtfulness of collection. In June 2011, as a result of our issuing a notice of default with respect to the note, we

determined that we were the primary beneficiary of the VIE. Therefore, we consolidated the operations of the VIE beginning June 30, 2011. Assets of the VIE

may only be used to settle obligations of the VIE and creditors of the VIE have no recourse to the general credit of the Company. The note receivable has bee

n

eliminated in consolidation.

As of October 19, 2011, the Sherburne Commons property was reclassified to real estate held for sale. Consequently, the related assets and liabilities of the

p

roperty were classified as assets of variable interest entity held for sale and liabilities of variable interest entity held for sale on our condensed consolidate

d

b

alance sheets. Operating results for the property have been reclassified to discontinued operations on our condensed consolidated statements of operations for all

periods presented. On October 6, 2014, we foreclosed on the Sherburne Commons property, however we did not take possession of the property.

On January 7, 2015, through our Operating Partnership, we sold Sherburne Commons to The Residences at Sherburne Commons, Inc. (“Sherburne Buyer”), a

n

unaffiliated Massachusetts non-

p

rofit corporation, in exchange for $5.0 million, as evidenced by a purchase money note from Sherburne Buyer to us as the lender.

In conjunction with the sale of the property, we assigned our foreclosure bid to the Buyer.

11

The $5.0 million purchase money note is secured by the Sherburne Commons property, bears an annual interest rate of 3.5% and matures on December 31, 2017.

At Sherburne Buyer’s election, interest may accrue and not be payable through December 31, 2015 with all accrued but unpaid interest being payable in full o

n

January 1, 2016. Outstanding and unpaid principal and interest due shall be paid from the net proceeds payable to Sherburne Buyer from the sale of the residential

cottages in Sherburne Commons. We may also participate in additional interest of up to $1 million from 50% of the net proceeds of cottage sales throug

h

December 31, 2018.

The sale of the property is being accounted for under the installment method and as such, the $5.0 million note has been reduced by approximately $0.2 millio

n

related to a deferred gain on the sale, which will be subsequently recognized as principal payments are received on the note. Interest payments on the note will

also be recorded as payments are received. Additionally, as part of the transaction, the note was reduced by approximately $0.1 million for certain relate

d

adjustments. As of March 31, 2015, we have not collected any funds related to the principal or interest on the note and the balance on the note receivable was $4.7

million.

As we are no longer the primary beneficiary of the VIE, it is no longer being consolidated as of March 31, 2015. As of December 31, 2014, the VIE was classifie

d

as assets of variable interest entity held for sale and liabilities of variable interest entity held for sale and for the period ended March 31, 2014, the results o

f

operations for the variable interest entity held for sale was presented in discontinued operations on the condensed consolidated statements of operations. As o

f

March 31, 2015, we recorded a loss on disposition of $1.6 million for this VIE, which is included in discontinued operations on the condensed consolidate

d

statements of operations.

7. Related Party Transactions with CRA

Related party transactions relate to fees paid and costs reimbursed to CRA for services rendered to us through March 31, 2014, prior to the termination of the

Advisory Agreement on April 1, 2014.

Specific fees described in the Advisory Agreement which would have been owed to CRA are described below. We do not believe that we owe CRA any amounts

due under the Advisory Agreement. The fees and expense reimbursements payable to CRA under the Advisory Agreement are described in more detail in ou

r

Annual Report filed on Form 10-K for the year ended December 31, 2014.

Organizational and Offering Costs - The Advisory Agreement provided for reimbursement by CRA for organizational and offering costs in excess of 3.5% of the

gross proceeds from our primary offering and follow-on offering. Under the Advisory Agreement, within 60 days after the end of the month in which our follow-

on offering terminates, CRA was obligated to reimburse us to the extent that the organization and offering expenses related to our follow-on offering borne by us

exceeded 3.5% of the gross proceeds of the follow-on Offering.

12

As of June 10, 2012, the date that our follow-on offering terminated, we had reimbursed CRA a total of $1.1 million in organizational and offering costs related to

our follow-on offering, of which $1.0 million was in excess of the contractual limit. Consequently, in the second quarter of 2012, we recorded a receivable fro

m

CRA for $1.0 million reflecting the excess reimbursement. However, based on our evaluation of various factors related to collectability of this receivable, we

reserved the full amount of the receivable.

As of March 31, 2015 and December 31, 2014, the gross balance of this receivable was $0.7 million. CRA has not made any payments in 2014 or 2015. The

balance of this receivable has been fully reserved for as of March 31, 2015 and December 31, 2014.

Acquisition Fees and Expenses – No acquisition fees were earned during the three months ended March 31, 2015 and 2014.

Management Fees and Expenses - For the three months ended March 31, 2015 and 2014, CRA earned $0 and $0.2 million of asset management fees, respectively.

These costs are included in asset management fees and expenses in our condensed consolidated statements of operations.

In addition, the Advisory Agreement provided for our reimbursement to CRA for the direct and indirect costs and expenses incurred by CRA in providing asse

t

management services to us, including related personnel and employment costs. For the three months ended March 31, 2015 and 2014, CRA was reimbursed $0

and $36,000, respectively, of such direct and indirect costs and expenses. These costs are included in asset management fees in our condensed consolidate

d

statements of operations.

As of March 31, 2014, we overpaid CRA $32,000 for asset management fees. We have recorded this amount as receivable from related party in our condense

d

consolidated balance sheets and reserved for the entire amount due to the uncertainty of collectability.

Operating Expenses - For the three months ended March 31, 2015 and 2014, $0 and $0.2 million of operating expenses incurred on our behalf were reimbursed to

CRA, respectively. These costs are included in general and administrative expenses on our condensed consolidated statements of operations. We paid $189,000 i

n

excess operating expense reimbursements to CRA in prior periods. Accordingly, we have recorded this receivable due from CRA and reserved for the entire

amount due to the uncertainty of collectability.

Pursuant to provisions contained in our terminated Advisory Agreement, our board of directors had the responsibility of limiting our total operating expenses fo

r

each trailing four consecutive quarters to amounts that do not exceed the greater of 2% of our average invested assets or 25% of our net income, calculated in the

manner set forth in our charter, unless a majority of the directors (including a majority of the independent directors) made a finding that a higher level of expenses

was justified (the “2%/25% Test”). In the event that a majority of the directors had not determined that such excess expenses were justified, CRA was required to

reimburse to us the amount of the excess expenses paid or incurred (the “Excess Amount”).

For each four-fiscal-quarter period prior to March 31, 2014, our board of directors determined that the Excess Amount was justified and had consequently waive

d

such Excess Amount. For the four-fiscal-quarter period ended March 31, 2014, our total operating expenses exceeded the greater of 2% of our average investe

d

assets and 25% of our net income. We incurred operating expenses of approximately $3.7 million and incurred an Excess Amount of approximately $1.7 millio

n

during this period. Our board of directors did not waive this Excess Amount and therefore such Excess Amount is due to the Company from CRA. Accordingly,

we have recorded this receivable and reserved for the entire amount due to the uncertainty of collectability.

Property Management and Leasing Fees and Expenses - For the three months ended March 31, 2015 and 2014, CRA earned approximately $0 an

d

$42,000, respectively, of property management fees. CRA did not earn any leasing fees for the three months ended March 31, 2015 and 2014. These costs are

included in property operating and maintenance expenses in our condensed consolidated statements of operations.

Disposition Fee – No disposition fees were earned during the three months ended March 31, 2015 and 2014.

13

Subordinated Participation Provisions – No subordinated participation fees were earned during the three months ended March 31, 2015 and 2014.

8. Loans Payable

As of March 31, 2015 and December 31, 2014, loans payable consisted of the following:

We have total debt obligations of approximately $90.0 million that will mature between 2016 and 2049. See Note 4 for loans payable balance for each property.

In connection with our loans payable, we incurred debt discounts and financing costs. The unamortized balance of the deferred financing costs totals $1.4 millio

n

and $1.5 million, as of March 31, 2015 and December 31, 2014, respectively. The capitalized financing costs and debt discounts are being amortized over the life

of their respective financing agreements using the straight-line basis which approximates the effective interest rate method. For the three months ended March 31,

2015 and 2014, $74,000 and $47,000, respectively, of deferred financing costs and debt discounts were amortized and included in interest expense in ou

r

condensed consolidated statements of operations.

The principal payments due on the loans payable (excluding debt discount) for the period from April 1, 2015 to December 31, 2015 and for each of the fou

r

following years and thereafter ending December 31 are as follows:

March 31, 2015 December 31, 2014

Loans payable to GE Capital Corporation in monthly installments of approximately $123,000, including interest

at LIBOR (floor of .50%) plus 4.5% (5.0% at March 31, 2015 and December 31, 2014, respectively), due in

September 2017 through July 2018, collateralized by Friendship Haven, Brookstone of Aledo, Redding, Gateway

and Applewood. $ 25,617,000 $ 25,617,000

Loans payable to The PrivateBank and Trust Company in monthly installments of approximately $96,000,

including interest at LIBOR (floor of up to 1.0%) plus 4% (4.50% to 5.0% and 5.0% at March 31, 2015 and

December 31, 2014, respectively), due in January 2016 through September 2017, collateralized by Danby House,

M

y

rtle Point, Lamar Estates, Monte Vista Estates and Lovin

g

Arms. 27,790,000 16,350,000

Loans payable to Lancaster Pollard Mortgage Company, LLC (insured by HUD) in monthly installments of

approximately $193,000, including interest ranging from a fixed rate of 3.75% to 3.78%, plus 0.65% for

mortgage insurance, due in September 2039 through December 2049, collateralized by Sheridan, Fernhill,

Tigard, Medford, Shelby, Hamlet and Carteret. 36,611,000 36,785,000

90,018,000 78,752,000

Less debt discount

(

864,000)

(

780,000)

Total loans payable $ 89,154,000 $ 77,972,000

Year Principal

Amount

April 1, 2015 to December 31, 2015 $ 1,210,000

2016 8,578,000

2017 40,131,000

2018 6,326,000

2019 and thereafter 33,773,000

$ 90,018,000

14

General Electric Capital Corporation (“GE”)

As of March 31, 2015 and December 31, 2014, we had net borrowings of $25.6 million under the GE loan agreements. See table above for further information.

During the three months ended March 31, 2015 and 2014, we incurred approximately $0.3 million and $0.4 million, respectively, of interest expense related to the

GE loans.

The PrivateBank and Trust Company (“PrivateBank”)

In January 2015, in conjunction with the acquisition of Loving Arms (see Note 4), we entered into a first priority mortgage loan collateralized by the Loving

Arms property and cross-collateralized with three of our other properties, Lamar Estates, Monte Vista Estates and Myrtle Point. On January 23, 2015, we

amended an existing loan agreement with PrivateBank to increase the principal amount available under that existing loan by $11.4 million for a total principal

availability of $20.5 million collateralized by a first priority security interest in the four properties noted above. All availability under this loan is outstanding. The

loan, which bears interest at the One Month LIBOR (London Interbank Rate), with a floor of 25 basis points, plus a spread of 4.50%, has a 25 year amortizatio

n

schedule and matures on September 21, 2017. The loan may be prepaid with no penalty if the four properties are refinanced through HUD (see below).

As of March 31, 2015 and December 31, 2014, we had net borrowings of $27.8 million and $16.4 million under the PrivateBank loans. See table above for furthe

r

information. During the three months ended March 31, 2015 and 2014, we incurred approximately $0.3 million and $0.2 million of interest expense,

respectively, related to the PrivateBank loans.

Lancaster Pollard Mortgage Company, LLC

In September 2014 and November 2014, we refinanced certain properties with Housing and Urban Development (“HUD”) insured loans from the Lancaste

r

Pollard Mortgage Company, LLC (“Lancaster Pollard”). See table above for further information.

HUD requires that our lender hold certain reserves for property tax, insurance, and capital expenditures. These reserves are included in restricted cash on the

Company’s condensed consolidated balance sheets.

As of March 31, 2015 and December 31, 2014, we had net borrowings of $36.6 million and $36.8 million under the HUD loans. During the three months ende

d

March 31, 2015, we incurred approximately $0.4 million of interest expense related to the HUD loans.

9. Commitments and Contingencies

We inspect our properties for the presence of hazardous or toxic substances. While there can be no assurance that a material environmental liability does not exist,

we are not currently aware of any environmental liability with respect to the properties that would have a material effect on our consolidated financial condition,

results of operations and cash flows. Further, we are not aware of any environmental liability or any unasserted claim or assessment with respect to a

n

environmental liability that we believe would require additional disclosure or the recording of a loss contingency.

Our commitments and contingencies include the usual obligations of real estate owners and operators in the normal course of business. In the opinion o

f

management, these matters are not expected to have a material impact on our consolidated financial condition, results of operations and cash flows. We are also

subject to contingent losses resulting from litigation against the Company.

On April 1, 2014 CRA and Cornerstone Ventures, Inc. filed a complaint in the Superior Court of California for the County of Orange-Central Justice Center, Case

N

o. 30-2014-00714004-CU-BT-CJC, naming the Company, its directors and two of its officers as defendants, seeking declaratory and injunctive relief an

d

compensatory and punitive damages. On April 17, 2014, Judge Nakamura denied in its entirety plaintiffs’ ex parte application for a temporary restraining order to

show cause why a preliminary injunction against the defendants should not issue. On May 19, 2014, the Company filed a counter claim against plaintiffs an

d

certain individuals affiliated with CRA and affiliated entities. The Company continues to believe that all of plaintiffs’ claims are without merit and will continue

to vigorously defend itself. Plaintiffs and defendants are conducting discovery.

15

In connection with our becoming the licensed operator of Friendship Haven through a wholly-owned taxable REIT subsidiary, we have entered into

a

management agreement with an affiliate of Stonegate. The management agreement calls for us to pay to Stonegate a termination fee if we terminate the agreemen

t

b

efore May 1, 2015. The termination fee is equal to three times the highest monthly management fee paid to Stonegate prior to the termination. As of March 31,

2015, the termination fee would have been approximately $110,000 however, as the agreement with them was not terminated before May 1, 2015, no fee will be

due.

P

urchase O

p

tion

As of March 31, 2015, we own one property with a book value of approximately $7.8 million that is subject to a purchase option that became exercisable o

n

September 14, 2014. The option provides the option holder with the right to purchase the property at increasing exercise price intervals based on elapsed time,

starting at $10.8 million. The option expires August 13, 2022. As of March 31, 2015, the option holder has not provided notice or exercised their option.

P

urchase A

g

reemen

t

In November 2013, a limited liability company in which we hold a minority interest entered into a build-to-suit purchase agreement whereby the entity agreed to

p

urchase a 70 unit assisted living facility in Athens, Georgia for approximately $12.4 million upon certificate of occupancy received for the facility. In the even

t

the entity defaults on the purchase of the building as provided for in the purchase agreement, the entity would be required to lease the facility from the seller for

a

ten year term at an annual rent amount equal to 8% of the cost of the facility. The Company executed a guarantee for the payments associated with that lease. I

n

the event that the lease is executed, the lease payment will equal approximately $1.0 million per year.

I

ndemni

f

ication A

g

reements

The Company has entered into indemnification agreements with certain officers of the Company against all judgments, penalties, fines and amounts paid i

n

settlement and all expenses actually and reasonably incurred by him or her in connection with any proceeding.

10. Discontinued Operations

D

ivestitures

In accordance with ASC 360, Property, Plant & Equipment, we report results of operations from real estate assets that meet the definition of a component of a

n

entity that have been sold, or meet the criteria to be classified as held for sale, as discontinued operations.

R

eal Estate Held for Sale and Disposed

As of December 31, 2014, the Sherburne Commons property had been classified as real estate held for sale and the results of operations for the variable interes

t

entity held for sale have been presented in discontinued operations in the Company’s condensed consolidated statements of operations for all periods presented.

On January 7, 2015, we sold the Sherburne Commons property. See Note 6 for further information.

The following is a summary of the components of loss from discontinued operations for the three months ended March 31, 2015 and 2014:

Three Months Ended

March 31,

2015 2014

Rental revenues, tenant reimbursements and other income $ - $ 554,000

Operating expenses and real estate taxes - (719,000)

Loss on disposition of VIE

(

1,582,000)-

Loss from discontinued operations $

(

1,582,000) $

(

165,000)

16

The following table presents balance sheet information for the properties classified as held for sale as of March 31, 2015 and December 31, 2014. FASB ASC 360

requires that assets classified as held for sale be carried at the lesser of their carrying amount or estimated fair value, less estimated selling costs.

N

o real estate investments were disposed of in 2014.

11. Subsequent Events

On April 29 2015, Summit Healthcare REIT, Inc., through our Operating Partnership, entered into a joint venture (“Joint Venture”) and limited liability compan

y

agreement (“LLC Agreement”) with Best Years, LLC (“Best Years”), a U.S. based affiliate of Union Life Insurance Co, Ltd. (“Union Life”).

In conjunction with the Joint Venture, the Operating Partnership contributed all of its limited liability company interest in each of six limited liability companies

that collectively own Lamar Estates, Monte Vista Estates, Myrtle Point Care Center, Gateway Care and Retirement Center, Applewood Retirement Communit

y

and Loving Arms Assisted Living (collectively, the “JV 2 Properties”) to the Joint Venture entity, resulting in the Joint Venture owning each of the JV 2

Properties. Best Years, in conjunction with the Joint Venture, contributed cash in the amount of approximately $9.9 million to the Joint Venture. At the close o

f

the Joint Venture transaction, the Operating Partnership received approximately net $9.2 million in cash from the Joint Venture, as concurrent with the

transaction, the principal amount of The PrivateBank loan cross-collateralized by four of the JV 2 Properties reduced the Front Royal Loan by $715,000. Unde

r

the LLC Agreement, as a result of these contributions and cash distributions, the Operating Partnership and Best Years own a 10% and 90% equity interest in the

Joint Venture, respectively.

Under the LLC Agreement, net operating cash flow of the Joint Venture will be distributed quarterly first to the Operating Partnership and Best Years pari passu

up to a 10% annual return, and thereafter to Best Years 75% and the Operating Partnership 25%. All capital proceeds (from the sale of the JV 2 Properties,

refinancing, or other capital event) will be paid first to the Operating Partnership and Best Years pari passu until each has received an amount equal to its accrue

d

but unpaid 10% return plus its total contribution, and thereafter to Best Years 75% and the Operating Partnership 25%.

As part of the Joint Venture, we formed Summit Healthcare Asset Management, LLC (the “Management Company”) as a wholly-owned taxable REIT subsidiar

y

(TRS). Under the LLC Agreement, Best Years paid the Management Company a one-time acquisition fee equal to 1% of the original purchase price paid for the

JV 2 Properties, and the Joint Venture will pay the Management Company annual asset management fees equal to .25% of the original purchase price paid for the

JV 2 Properties.

As a result of the Joint Venture, the JV 2 Properties will no longer be consolidated in the Company’s consolidated financial results, commencing April 30, 2015.

The Joint Venture will be accounted for under the equity method in the Company’s consolidated financial statements. As the JV 2 properties do not quality as

held for sale, they will continue to be recorded as held and used until April 30, 2015 and not be reported as discontinued operations for the period ended Marc

h

31, 2015.

For additional information on the Joint Venture, see the Company’s Form 8-K filed on May 1, 2015.

March 31,

2015 December 31,

2014

Assets of variable interest entit

y

held for sale:

Cash and cash equivalents $

—

$36,000

Investments in real estate, net

—

3,905,000

Accounts receivable, inventory and other assets

—

198,000

Total assets $

—

$ 4,139,000

Liabilities of variable interest entity held for sale:

Note

p

a

y

able $

—

$ 1,332,000

Loans

p

a

y

able

—

117,000

Accounts

p

a

y

able and accrued liabilities

—

466,000

Intan

g

ible lease liabilities, net

—

145,000

Interest payable

—

640,000

Liabilities of variable interest entity held for sale $

—

$ 2,700,000

17

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following “Management’s Discussion and Analysis of Financial Condition and Results of Operations” should be read in conjunction with our unaudite

d

consolidated financial statements and notes thereto contained elsewhere in this report. This section contains forward-looking statements, including estimates,

p

rojections, statements relating to our business plans, objectives and expected operating results, and the assumptions upon which those statements are based.

These forward-looking statements generally are identified by the words “believes,” “project,” “expects,” “anticipates,” “estimates,” “intends,” “strategy,” “plan,”

“may,” “will,” “would,” “will be,” “will continue,” “will likely result,” and similar expressions. Forward-looking statements are based on current expectations

and assumptions that are subject to numerous risks and uncertainties which may cause actual results to differ materially from the forward-looking statements.

Forward-looking statements that were true at the time made may ultimately prove to be incorrect or false. We undertake no obligation to update or revise publicl

y

any forward-looking statements, whether as a result of new information, future events or otherwise. All forward-looking statements should be read in light of the

risks identified in Part I, Item 1A of our annual report on Form 10-K for the year ended December 31, 2014 filed with the U.S. Securities and Exchange

Commission (the “SEC”) on March 20, 2015.

Overview

We were founded in October 2004 to invest and own commercial real estate. As of November 23, 2010 after raising $167.1 million of gross proceeds from the

sale of 20.9 million shares of our common stock, we stopped selling shares of our common stock.

We believe that becoming self-managed as of April 1, 2014 has provided us numerous intermediate and long term benefits, despite certain non-recurring

transition costs, and will allow us to realize increased funds from operations (“FFO”) and net asset value (“NAV”) in a shorter period of time than if we ha

d

remained externally managed.

Our revenues, which are comprised largely of rental income, including rents reported on a straight-line basis over the initial term of each lease, and fees earne

d

for resident care from Friendship Haven (see Note 4 to the accompanying Notes to Condensed Consolidated Financial Statements). Our growth depends, in part,

on our ability to acquire new healthcare properties at attractive prices, increase rental income from leases by increasing rental rates and by controlling ou

r

expenses. Our operations are impacted by property-specific, market-specific, general economic and other conditions.

Strategic Repositioning - In 2013, we completed phase one of our transition strategy by disposing of our industrial real estate. The second phase of our transitio

n

strategy is to acquire healthcare real estate assets, which commenced mid-2012 and will continue going forward. The third phase of our transition strategy will be

to grow our Company primarily by attracting and securing third party equity. Investing in healthcare real estate assets, more specifically senior housing facilities,

is believed to be accretive to earnings and potentially stockholder value. Senior housing facilities include independent living facilities (“IL”), skilled-nursing

facilities (“SNF”), assisted living facilities (“AL”), memory care (“MC”) and continuing care retirement communities (“CCRC”). Each of these caters to differen

t

segments of the senior population. The Company’s repositioning strategy includes purchasing SNF, AL, IL and MC facilities.

We may acquire additional properties through joint venture investments in the future, or sell a percentage of our existing properties to a joint venture partner,

which may result in the deconsolidation of properties we already own. We anticipate acquiring properties through joint ventures in order to diversify our portfolio

of properties in terms of geographic region, facility type and operator, among other reasons. Joint ventures typically also allow us to acquire an interest in

a

p

roperty without requiring that we fund the entire equity portion of the purchase price. In addition, certain properties may be available to us only through join

t

ventures. In determining whether to recommend a particular joint venture, management will evaluate the structure of the joint venture, the real property that suc

h

j

oint venture owns or is being formed to own under the same criteria. We may form additional entities in conjunction with joint ventures. These entities ma

y

employ debt financing consistent with our borrowing policies. Our joint ventures may take the form of equity joint ventures with one or more large institutional

partners. They may also include ventures with developers who contribute land, development services and expertise rather than cash.

18

P

ort

f

olio

At March 31, 2015, we own 17 healthcare facilities, located in seven states. The following tables summarize our investments in real estate as of March 31, 2015:

1 Represents Q1 2015 revenue based on in-place leases.

2 Represents Q1 2015 rent due under a lease between the Company and a wholly-owned taxable REIT subsidiary (“Friendswood TRS”).

Critical Accounting Policies

There have been no material changes to our critical accounting policies as previously disclosed in our Annual Report on Form 10-K for the year ende

d

December 31, 2014 as filed with the SEC on March 20, 2015.

Real Estate Properties:

Properties Beds Square

Footage Purchase

Price

SNF or SNF/IL 8 602 202,428 $ 55,040,000

AL or AL/MC 8 582 268,887 59,925,000

IL 1 69 45,563 2,900,000

Total Real Estate Properties 17 1,253 516,878 $ 117,865,000

Pro

p

ert

y

Location Date Purchased T

yp

e Beds Q1 2015

Revenue1

Sheridan Care Cente

r

Sheridan, OR Au

g

ust 3, 2012 SNF 51 $ 108,000

Fern Hill Care Cente

r

Portland, OR Au

g

ust 3, 2012 SNF 63 115,000

Farmin

g

ton S

q

uare Medford, OR Se

p

tember 14, 2012 AL/MC 71 202,000

Friendship Haven Healthcare and

Rehabilitation Cente

r

Galveston

Count

y

TX Se

p

tember 14, 2012 SNF 150 180,0002

Pacific Health and Rehabilitation Cente

r

Ti

g

ard, OR December 24, 2012 SNF 73 213,000

Danb

y

House Winston-Salem, NC Januar

y

31, 2013 AL/MC 100 226,000

Brookstone of Aledo Aledo, IL Jul

y

2, 2013 AL 66 166,000

The Shelby House Shelby, NC October 4, 2013 AL 72 98,000

The Hamlet House Hamlet, NC October 4, 2013 AL 60 141,000

The Carteret House Newport, NC October 4, 2013 AL 64 93,000

Sundial Assisted Living Redding, CA December 18, 2013 AL 65 81,000

Lamar Estates Lamar, CO September 22, 2014 SNF 60 113,000

Monte Vista Estates Monte Vista CO September 22, 2014 SNF 60 85,000

Myrtle Point Care Cente

r

Myrtle Point, OR October 31, 2014 SNF 54 104,000

Gateway Care and Retirement Cente

r

Portland, OR December 31, 2014 SNF/IL 91 281,000

Applewood Retirement Community Salem, OR December 31, 2014 IL 69 47,000

Lovin

g

Arms Assisted Livin

g

Front Ro

y

al, VA Januar

y

23, 2015 AL 84 223,000

Total 1,253

19

Results of Operations

Our results of operations for the three months ended March 31, 2015 compared to the three months ended March 31, 2014 were significantly impacted as

described below:

Total rental revenue for our healthcare properties includes rental revenues and tenant paid and/or reimbursements for property taxes and insurance. Propert

y

operating expenses include insurance, property taxes and other operating expenses. Resident services and fee income and resident services costs are generate

d

from Friendswood TRS, which began operations on May 1, 2014. Net operating income increased to approximately $2.9 million for the three month ende

d

March 31, 2015 from $1.6 million for the three months ended March 31, 2014, an increase of approximately $1.3 million. Approximately $1.0 million of the

increase is due to the revenue derived from our 2015 healthcare acquisition and owning the 2014 acquisitions purchased in the third and fourth quarters of 2014

and for the full period in 2015.

General and administrative expense was $0.9 million for the three months ended March 31, 2015 and $0.7 million for the three months ended March 31, 2014.

The increase was primarily due to increases in employee payroll expenses of $0.4 million, offset by lower advisor fees of $0.2 million due to the termination o

f

the Advisory Agreement in April 2014.

Three Months Ended

March 31,

2015 2014 $ Chan

g

e

Rental revenues, tenant

reimbursements & other income $ 2,983,000 $ 1,938,000 $ 1,045,000

Resident services and fee income 2,243,000

—

2,243,000

Total revenues 5,226,000 1,938,000 3,288,000

Less ex

p

enses:

Pro

p

ert

y

o

p

eratin

g

costs

(

575,000

)

(

348,000

)

(

227,000

)

Resident services costs (1,737,000)

—

(1,737,000)

N

et operating income (1) 2,914,000 1,590,000 1,324,000

Interest income from notes receivable 2,000 4,000 (2,000)

General and administrative (944,000) (670,000)(274,000)

Asset management fees and expenses

—

(205,000)205,000

Real estate acquisition costs

—

(4,000)4,000

Depreciation and amortization (1,245,000) (1,238,000) (7,000)

Reserve for excess advisor obli

g

ation

—

(

189,000

)

189,000

Interest and other expense and income (1,081,000) (707,000) (374,000)

Loss from continuin

g

o

p

erations

(

354,000

)

(

1,419,000

)

1,065,000

Loss from discontinued operations

(

1,582,000)

(

165,000)

(

1,417,000)

N

et loss

(

1,936,000

)

(

1,584,000

)

(

352,000

)

N

oncontrolling interests’ share in losses (37,000) 345,000 (382,000)

N

et loss applicable to common stockholders $

(

1,973,000) $

(

1,239,000) $

(

734,000)

(1)

N

et operating income (“NOI”) is a non-GAAP supplemental measure used to evaluate the operating performance of real estate properties. We define

N

OI as total rental revenues, resident service and fee income, tenant reimbursements and other income less property operating and resident services

costs. NOI excludes interest income from notes receivable, general and administrative expense, asset management fees and expenses, real estate

acquisition costs, depreciation and amortization, interest income, interest expense, and income from discontinued operations. We believe NOI provides

investors relevant and useful information because it measures the operating performance of the REIT’s real estate at the property level on an unleverage

d

basis. We use NOI to make decisions about resource allocations and to assess and compare property-level performance. We believe that net income

(loss) is the most directly comparable GAAP measure to NOI. NOI should not be viewed as an alternative measure of operating performance to ne

t

income (loss) as defined by GAAP since it does not reflect the aforementioned excluded items. Additionally, NOI as we define it may not be comparable

to NOI as defined b

y

other REITs or com

p

anies, as the

y

ma

y

use different methodolo

g

ies for calculatin

g

NOI.

20

There were no asset management fees for the three months ended March 31, 2015 and $0.2 million for the three months ended March 31, 2014. Asse

t

management fee and expense decreases are due to the termination of the Advisory Agreement in April 2014.

Depreciation and amortization increased by approximately $0.4 million for the first quarter of 2015 due to the timing of our 2014 property acquisitions. We

owned 17 healthcare properties for the first quarter of 2015 as opposed to 11 properties in the first quarter of 2014. Additionally, in the first quarter of 2014, we

recorded approximately $0.4 million in amortization expense for Friendship Haven’s leasing commission that was accelerated due to the lease termination o

n

March 16, 2014, and as such the total increase in depreciation and amortization was $7,000.

Reserve for excess advisor obligation represents organizational and offering costs incurred in excess of the 3.5% limitation of the gross proceeds from our follow-

on offering which terminated on June 10, 2012 (see Note 7 to the accompanying Notes to Condensed Consolidated Financial Statements). The Advisor

y

Agreement provided that CRA would reimburse any excess costs that were paid by us. In 2012, we recorded a receivable for the excess of $1.0 million which we

fully reserved for based on our evaluation of CRA’s ability to repay at that time. In March 2014, we increased our reserve by $0.2 million for additional excess

operating expenses paid to CRA in prior periods.

Interest, other expense and income increases in 2015 are primarily due to the increase in interest expense on our new loans payable for properties acquired at the

end of 2014 and for Front Royal acquired in the first quarter of 2015.

The loss from discontinued operations represents the Sherburne Commons activities in 2014. On January 7, 2015, we sold Sherburne Commons (see Note 10 to

the accompanying Notes to Condensed Consolidated Financial Statements) and recorded a loss on disposition of $1.6 million.

Liquidity and Capital Resources

As of March 31, 2015, we had approximately $1.5 million in cash and cash equivalents on hand and as of May 12, 2015, we had approximately $10.9 million i

n

cash and cash equivalents on hand. Based on current conditions and the $9.2 million proceeds from the Joint Venture with Best Years received in April 2015 (see

N

ote 11 to the accompanying Notes to Condensed Consolidated Financial Statements), we believe that we have sufficient capital resources for the next twelve

months.

Going forward, we expect our primary sources of cash to be rental revenues, tenant reimbursements, joint venture equity, asset management fees, and refinancing

of existing debt. In addition, we may increase cash through the sale of additional properties, which may result in the deconsolidation of properties we alread

y

own, or borrowing against currently-owned properties. For the foreseeable future, we expect our primary uses of cash to be for the repayment of principal o

n

loans payable, funding future acquisitions, operating expenses, and interest expense on outstanding indebtedness. We may also incur expenditures for renovations

of our existing properties, such as increasing the size of the properties by developing additional rentable square feet and/or making the space more appealing.

We continue to pursue options for repaying and/or refinancing debt obligations with long-term, fixed rate HUD-insured loans. We believe that conditions may be

acceptable to continue to raise capital through additional joint venture arrangements with either our existing joint venture partner or new partners, although there

can be no assurances that any such transactions will have terms acceptable to us or will be consummated.

Our Funds from Operations (“FFO”) have increased considerably over the past year primarily due to increased rental revenue from our acquisitions and reduce

d

expenses resulting from the termination of the Advisory Agreement and transition to self-management. FFO for the three months ended March 31, 2015 and 2014

were $878,000 and ($45,000), respectively.

Our liquidity will increase if cash from operations exceeds expenses, we receive net proceeds from the sale of whole or partial interest in a property or properties

or if refinancing results in excess loan proceeds, or decrease as proceeds are expended in connection with the acquisitions and operation of properties. Our abilit

y

to repay or refinance debt could be adversely affected by an inability to secure financing at reasonable terms, if at all.

Credit Facilities and Loan Agreements

As of March 31, 2015, we had debt obligations of approximately $90.0 million. The outstanding balance by lender is as follows:

•The PrivateBank and Trust Company

–

approximately $27.8 million maturing January 2016 through September 2017,

•GE Capital – approximately $25.6 million maturing September 2017 through July 2018,

•Lancaster Pollard (HUD) – approximately $24.0 million maturing from September 2039 through September 2049 and

•Lancaster Pollard (HUD)

–

approximately $12.6 million maturing December 2049

21

D

istributions

N

one during the three months ended March 31, 2015.

Funds from Operations

FFO is a non-GAAP supplemental financial measure that is widely recognized as a measure of REIT operating performance. We compute FFO in accordance

with the definition outlined by the National Association of Real Estate Investment Trusts (“NAREIT”). NAREIT defines FFO as net income (loss), computed i

n

accordance with GAAP, excluding extraordinary items, as defined by GAAP, and gains or losses from sales of property, plus depreciation, amortization an

d

impairments on real estate assets, and after adjustments for unconsolidated partnerships, joint ventures, noncontrolling interests and subsidiaries.

Our FFO may not be comparable to FFO reported by other REITs that do not define the term in accordance with the current NAREIT definition or that interpre

t

the current NAREIT definition differently than we do. We believe that FFO is helpful to investors and our management as a measure of operating performance

b

ecause it excludes depreciation and amortization, gains and losses from property dispositions, and extraordinary items, and as a result, when compared period to

p

eriod, reflects the impact on operations from trends in occupancy rates, rental rates, operating costs, development activities, general and administrative expenses,

and interest costs, which is not immediately apparent from net income. Historical cost accounting for real estate assets in accordance with GAAP implicitl

y

assumes that the value of real estate diminishes predictably over time. Since real estate values have historically risen or fallen with market conditions, man

y

industry investors and analysts have considered the presentation of operating results for real estate companies that use historical cost accounting alone to be

insufficient. As a result, our management believes that the use of FFO, together with the required GAAP presentations, provide a more complete understanding o

f

our performance. Factors that impact FFO include start-up costs, fixed costs, delays in buying assets, lower yields on cash held in accounts pending investment,

income from portfolio properties and other portfolio assets, interest rates on acquisition financing and operating expenses. FFO should not be considered as a

n

alternative to net income (loss), as an indication of our performance, nor is it indicative of funds available to fund our cash needs, including our ability to make

distributions.

The following is reconciliation from net loss applicable to common shares, the most direct comparable financial measure calculated and presented with GAAP, to

FFO for the three months ended March 31, 2015 and 2014:

Three months ended

March 31,

2015 2014

N