TARIFCPG11 5300011 Vol3 11

User Manual: 5300011

Open the PDF directly: View PDF ![]() .

.

Page Count: 114 [warning: Documents this large are best viewed by clicking the View PDF Link!]

PPSysB

Rev 18.02 PageLayout: CEX002 [SO] Page: 1 Processed: 10-01-2018 10:22:49 Job: TARIFC Unit: PG11

.

VOLUME 3 APPENDIX E

Volume 3

Appendix E

APPENDIX E

CUSTOMS PROCEDURE CODES

1.2.18/1 Customs Tariff Vol 311—1

.

VOLUME 3 APPENDIX E

PPSysB

Rev 18.02 PageLayout: CEX002 [E] Page: 2 Processed: 10-01-2018 10:22:49 Job: TARIFC Unit: PG11

Volume 3

Appendix E

1.2.18/1 Customs Tariff Vol 311—2

PPSysB

Rev 18.02 PageLayout: CEX002 [O] Page: 3 Processed: 10-01-2018 10:22:49 Job: TARIFC Unit: PG11

.

VOLUME 3 APPENDIX E

Volume 3

Appendix E

APPENDIX E

CUSTOMS PROCEDURE CODES (BOX 37)

The Customs Procedure Codes (CPCs) identify the customs and/or excise regimes to which goods are being entered and from which they

have been removed (where this applies).

The CPC is completed at export as well as import.

The CPC itself is based on a two digit Community Code which identifies a customs procedure, e.g. removal from warehouse, entry to free

zone, export under OPR. From this the CPC is built up into a 7 digit code.

First 2 digits: – Community Code for procedure applied for, ie regime to which goods are being entered.

Note: Special UK only codes of ‘00’ and ‘01’ are also used.

Second 2 digits: – Community Code for previous procedure, ie regime from which goods are being withdrawn (where there is none this

code will be ‘00’).

Note: If the first 2 digits are ‘00’ or ‘01’ then the second 2 digists will also be UK use only.

Third 3 digists: – National coding to breakdown Community headings into more detail.

List of procedures for coding purposes

(Two of these basic elements must be combined to produce a four-figure code)

05: – Free circulation with simultaneous entry under an inward processing procedure other than those referred to under codes 02 and

51.

07: – Free circulation with simultaneous entry of the goods under a warehouse procedure (including placing in other premises under

fiscal control).

10: – Permanent dispatch/export.

21: – Temporary dispatch/export under the customs outward processing procedure other than that referred to under code 25.

22: – Temporary dispatch/export under an outward processing procedure other than those referred to under codes 21 or 25.

23: – Temporary dispatch/export for return in an unaltered state.

31: – Redispatch/re-export of goods which are not in free circulation.

40: – Home use with simultaneous entry for free circulation.

41: – Home use with simultaneous entry for free circulation for the inward processing procedure (drawback system).

42: – Home use with simultaneous entry for free circulation of goods subject to a zero rated onward supply.

45: – Partial entry for home use with simultaneous entry for free circulation and for a warehousing procedure including deposit in other

premises under fiscal control.

46: – Free circulation under inward processing procedure (drawback system) in a customs warehouse.

47: – Free circulation under inward processing procedure (drawback system); in a free zone or free warehouse.

49: – Home use of goods previously released for free circulation in the special territories of the EU or those countries having a customs

union with the EU, such as Turkey, San Marino or Andorra (for goods in Chapters 25–97 of the Tariff); or goods originating in those

special territories or countries.

51: – Inward processing procedure (suspension system).

52: – Inward processing procedure other than those referred to under codes 02 and 51.

53: – Import under temporary import procedure. (Temporary Admission)

54(a): – Goods placed or obtained under the inward processing procedure (suspension system) carried out in another member state (and

not released for free circulation there).

61: – Reimportation with simultaneous entry for free circulation and home use.

63: – Reimportation with simultaneous entry for free circulation and home use of goods subject to a zero rated onward supply.

68: – Reimportation with simultaneous entry for free circulation and a warehouse procedure (including deposit in other premises under

fiscal control).

71: – Customs warehousing procedure including deposit in other premises under customs control.

1.2.18/1 Customs Tariff Vol 311—3

.

VOLUME 3 APPENDIX E

PPSysB

Rev 18.02 PageLayout: CEX002 [E] Page: 4 Processed: 10-01-2018 10:22:49 Job: TARIFC Unit: PG11

Volume 3

Appendix E

76: – Export warehousing or deposit in a free zone with advance payment of export refunds for products of goods intended for export

without further processing.

77: – Warehousing with intention to export with advance payment of export refunds for processed products and goods obtained from

basic products.

78: – Free zone except in the case provided for under code 76.

95: – Supplies for ships’ and aircraft stores.

96: – Supplies by duty – and tax-free shops at ports and airports.

NB: – The code 00 may be used to indicate no previous procedure (ie as the third and fourth digits only).

(a) – These codes cannot be used as the first two digits of the procedure code, but only to indicate the previous procedure,

eg 4054 % entry for free circulation and home use of goods previously placed under IPR – suspension system in another member

state.

1.2.18/1 Customs Tariff Vol 311—4

PPSysB

Rev 18.02 PageLayout: CEX002 [O] Page: 5 Processed: 10-01-2018 10:22:49 Job: TARIFC Unit: PG11

.

VOLUME 3 APPENDIX E

Volume 3

Appendix E

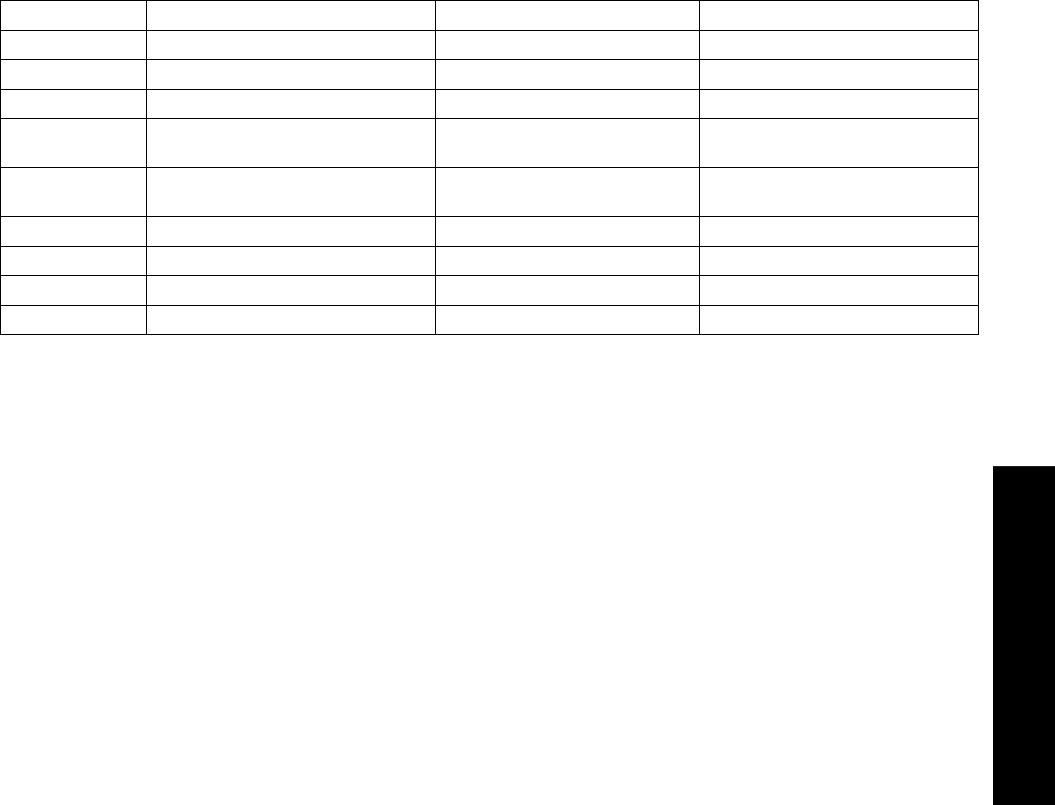

CUSTOMS PROCEDURE CODES FOR CFSP (BOX 37)

Digits1&2 Digit 3 Digit 4 Digits 5,6&7

Type of goods Release mechanism Regime entered to:

06 %CFSP 1 %Normal 0 %Frontier 000 %National Transit

2%Controlled goods 1 %Transit 001 %Community Transit (NCTS)

3%Controlled drugs 2 %Warehouse Type A, C, D and E 002 %National transit for Plant

Health material

4%Excise goods 3 %Removal from Temporary 040 %Free circulation

storage

4%Free Zone 061 %Simplified economic relief

9%FSD 071 %Warehousing

078 %Free Zone

09 %FSD

1.2.18/1 Customs Tariff Vol 311—5

.

VOLUME 3 APPENDIX E

PPSysB

Rev 18.02 PageLayout: CEX002 [E] Page: 6 Processed: 10-01-2018 10:22:49 Job: TARIFC Unit: PG11

Volume 3

Appendix E

1.2.18/1 Customs Tariff Vol 311—6

PPSysB

Rev 18.02 PageLayout: CEX002 [O] Page: 7 Processed: 10-01-2018 10:22:49 Job: TARIFC Unit: PG11

.

VOLUME 3 APPENDIX E1

Volume 3

Appendix E 1

APPENDIX E 1

EXPORTS

CUSTOMS PROCEDURE CODES

NOTES

1. Restricted Goods

(a) The use of the following CPCs does not obviate the need to comply with export licensing requirements or other export

prohibitions or restrictions. Details of these export controls are given in Part 4 of Volume 1.

(b) Additionally, examination of controlled drugs subject to Home Office licensing requirements will not be undertaken at

trader’s premises. Examination will be carried out at ship’s side only.

2. CAP Goods

(a) The use of the following CPCs does not relieve any requirements applying to the export of CAP goods. Failure to comply

with the requirements may lead to prohibition of the export, loss of security and loss of entitlement to export refund and/or

MCA payment. Full details of the requirements are given in Notices 790 (CAP: General) and Notice 800 (CAP: Export

Procedures).

(b) When CAP goods are pre-entered on a SAD under any of the following CPCs, unless otherwise stated:

(i) Form C88(CAP) must be presented with the copy 2 SAD export declaration for all CAP goods:

(1) which are subject to a charge at export (cereal Export Tax, for example);

(2) which are subject to mandatory CAP export licensing;

(3) which are subject to certain production aid (eg peas); and

(4) on which a claim to export refund is being made.

(ii) Security for export charges must be lodged at the place of export unless a guarantee to cover these charges has been

given to the Intervention Board.

(iii) If the goods are subject to CAP export licensing, the licence must be lodged with the copy 2 SAD export declaration

on which the number(s) of the licence has been entered in Box 44 unless the licence has been lodged with the Intervention

Board beforehand.

(iv) Any additional documentation required must be submitted with the copy 2 of the SAD.

(v) Additional requirements specific to the CAP goods exported must also be complied with.

(c) For exports by traders approved as CAP schedulers Form C88(CAP) is not required in certain specified circumstances. Special

rules apply to CAP schedulers and these are set out in Notice 800.

10

PERMANENT EXPORT/DISPATCH

10 00 001

Note: The use of this CPC does not relieve any documentary or other control requirement for the export of goods subject to export

licensing, other export prohibition and restriction or the provisions of the Common Agricultural Policy.

In addition to the requirements listed below, all documents required for the above specified controlled goods must be submitted with the

SAD export declaration on which any necessary additional information relating to those goods must be included

10 00 001

1. Goods Covered Free circulation goods being exported outside the EU.

1.1 This CPC must NOT be used for:

-Goods subject to a CAP refund or CAP export licensing

-Excise goods in excise duty suspension

-Non EU goods on which import charges have not been paid

-Goods subject to any other CPC or regime controls

1.2 If you are exporting:

-Low value goods which for a single consignment of goods:

,have a total value of less than £750, and weigh less than 1000kg, and

-are not dutiable or restricted.

use CPC 10 00 097.

-Non statistical goods - see Notice 275 Section 13, which:

,do not require an export licence, permit or certificate,

,are not being exported for commercial purposes, and

,are not under Community Transit (CT) or ATR (Turkish preference) document

use CPC 10 00 098

1.2.18/1 Customs Tariff Vol 311—7

.

VOLUME 3 APPENDIX E1

PPSysB

Rev 18.02 PageLayout: CEX002 [E] Page: 8 Processed: 10-01-2018 10:22:49 Job: TARIFC Unit: PG11

Volume 3

Appendix E 1

2. Notice 275 - Customs export procedures

3. Status of Goods T2 - Goods in free circulation and not subject to any other regime controls.

4. Specific Fields in the declaration/notes Additional information and completion notes for these and other boxes on the declaration

on completion are given in Volume 3 Part 1 of this Tariff.

Box 1:

1st sub division enter Either:

,‘CO’ for export to an EU Special Territory (see Tariff Volume 1 Part 2 Section 1),

,‘EX’ for export outside the EU; or

,‘EU’ for export to an EFTA country

in the 2nd sub division enter:

,‘D’ for a full declaration

,‘Y’ for a SDP supplementary declaration; or

,‘Z’ for a Customs Supervised Exits (CSE) supplementary declaration

Box 8 - consignee: the full name and address of the person to whom the goods are to be

delivered

Box 14(1): Enter the code for representation:

1 - self representation

2 - direct representation

3 - indirect representation

Box 17: Enter the code for the non EU country of ultimate destination, see Appendix C1

for Country Codes note - except for EU Special Territories or areas not under the control of

The Government of the Republic of Cyprus, this should not be an EU country)

Box 29: Office of exit

,Where export will be made via another EU country (Indirect Export) the Office of Exit in

that EU country must be declared as the movement is required to be controlled by the

EU Export Control System (ECS).

,If goods are being exported via another EU country under a Single Transport Contract

(STC) do not complete Box 29 (in such cases an Additional Information (AI) statement in

Box 44 must completed - see below).

Box 31: Description of goods - for each item declared enter a clear description of the

goods. Include package marks, number and kind and any container numbers where

relevant.

Box 33: The Commodity Code to 8 digits of the goods being declared for export (see

Volume 2 of this Tariff), further information about classifying goods is available in Notice

600 - Classifying your imports or exports).

Box 40 - previous document - Appendix C12 identifies types of documents and codes to

be declared:

,Except for supplementary declarations identify the relevant commercial document

and Traders own reference that provides an audit link to the consignment. For example

to identify a packing list enter:

,‘Z’ (for previous document)

,followed by code ‘271’ (for packing list)

,followed by the packing list reference eg 1234

the above components would be entered as ‘Z-271-1234’

,For supplementary declarations in respect of goods previously exported under SDP or

CSE using CPCs 10 00 011; 10 00 014; enter:

,‘Y-CLE’ for the initial SDP/CSE declaration

,followed by (date of entry'-(EPU no'-(entry no '

[the ‘date of entry’ in records should be in the format ‘yyyymmdd’, the ‘EPU no’ and

‘entry no’ are from the pre-shipment advice (PSA), and the components are

separated by a dash (-). For example—Y-CLE-20120701-120-A12345E.

Box 44: Additional Information

-For export under a Single Transport Contract enter Additional Information (AI)

statement ‘STC99’ (see Appendix C9).

-For Merchandise in Baggage (MiB) enter AI Code ‘MIB01’, see note 11.3

1.2.18/1 Customs Tariff Vol 311—8

PPSysB

Rev 18.02 PageLayout: CEX002 [O] Page: 9 Processed: 10-01-2018 10:22:49 Job: TARIFC Unit: PG11

.

VOLUME 3 APPENDIX E1

Volume 3

Appendix E 1

-If goods specified on the entry are being exported using Temporary Admission (TA)

non EU packing’s/ pallets/ containers, enter one of the following AI codes as

appropriate (see Appendix C9):

,‘PAL 06’ (for non EU packing’s—see Notice 200)

,‘PAL 07’ (for non EU pallets—see Notice 306)

,‘PAL08’ (for non EU containers—see Notice 306)

-Enter a Unique Consignment reference number (UCR), see note 11.4

-For A TR movement enter document code N018 (for details to be declared see

Appendix C11)

Box 46 statistical value - the value declared should be the cost of the goods to the

purchaser or, if not sold, the cost to a prospective purchaser

5. Additional documents required Any documents, licences or certificates required for goods being exported must be

identified in Box 44 using the appropriate:

,licence/certificate codes indicated in Appendix C11; and

,document status code indicated in Appendix C12 of this Tariff

6. Security required -

7. Additional information -

8. Pre-entry action Goods must be presented to Customs at the office of export or other designated place. EU

safety and security legislation sets minimum time limits for goods to be presented to

Customs:

,for ‘deep sea’ containerised cargo, at latest 24 hours before the goods are loaded

,for ‘short sea’ containerised cargo, at latest 2 hours before leaving the port

,for air traffic, at latest 30 minutes before departure from an airport

,for rail and inland waters traffic, at latest 2 hours before departure

,for road traffic, at latest 1 hour before departure

,.

9. Post Clearance Action -

10. VAT Documentary evidence of export is required to support a claim to VAT zero rating. The UK

supplier must ensure that they obtain and keep official or commercial evidence for all

consignments. If evidence of export is not obtained within the specified time limit then the

supply must not be zero-rated. For Full details on VAT time limits for exports and zero

rating see Notice 703

11. Notes 11.1 Goods imported into the EU are in free circulation in the EU if all import formalities

have been completed and all duties, levies or equivalent charges have been paid and not

refunded. Goods originating in the EU are also in free circulation.

11.2 For goods not declared electronically under the National Export System (NES) SAD

copies 2 and 3, and where required Community Transit documents (CT), must be lodged

with the National Clearance Hub (NCH) where Customs Input Entry (CIE) facilities exist for

the submission of export entries to CHIEF. The export declaration and CT documents will

not be accepted until the goods have been presented to Customs.

11.3 Merchandise in Baggage (MIB) are commercial or business goods you take with you

in your accompanied baggage or in your private vehicle, that are over £750 and less than

1000kg.

You should:

,Arrive well before your scheduled departure time (suggest a minimum of 2 hours), and

,Present the goods to the export officer at the (air)port, of departure together with a

copy of the completed Customs export declaration which should include the

Movement Reference Number (MRN) allocated by CHIEF

If an officer is not in attendance you must use the red phone at the the export point to

speak to an officer and follow the instructions given.

1.2.18/1 Customs Tariff Vol 311—9

.

VOLUME 3 APPENDIX E1

PPSysB

Rev 18.02 PageLayout: CEX002 [E] Page: 10 Processed: 10-01-2018 10:22:49 Job: TARIFC Unit: PG11

Volume 3

Appendix E 1

11.4 Unique Consignment reference number (UCR) - there are two main types -

Declaration UCRs (DUCR) and Master UCRs (MUCR). Every CHIEF declaration will have a

DUCR whilst MUCRs are used either to identify a consignment to a means of transport (air)

or to group together co-loaded consignments (maritime). The DUCR consists of up to 35

(alpha/numeric) characters and is split into four parts:

-1st part—the year in which the UCR was allocated, (2008 would equal 8)

-2nd part—the country code for the country in which the UCR was allocated, (Great

Britain would be GB)

-3rd part—the identity of the authorised trader (trader’s EORI number) followed by a

hyphen ‘-’.

-4th part—a series of characters that are unique to the trader (providing an audit trail

through their commercial accounting system).

If a manual declaration is made for input by HMRC (National Clearance Hub in Salford) and

a UCR is not supplied CHIEF will derive a UCR based upon the entry reference (EPU-Entry-

Number-Entry Date). For further information see Volume 3 Part 1 of this Tariff

11.5 Useful contact details:

-General Customs (including NES enquiries) - VAT, Excise & Customs Helpline

Phone: 0300 200 3700

-NES Helpdesk Phone: 0300 582 418 Email: export.enquirieswhmrc.gsi.gov.uk

-Website: hmrc.gov.uk

10 00 002

1. Goods Covered Excise goods already released to consumption in the UK (excise duty paid) exported to

non-EU countries and subject to a claim for drawback of excise duty.

2. Notice 197, 207

3. Status of the goods. Box 1 enter code EX followed by A or D as appropriate.

4. Specific Fields in the declaration/notes Box 33 – must show the Commodity Code to 8 digits of the goods being entered to the

on completion export procedure.

5. Additional documents required —

6. Security required —

7. Additional information —

8. Pre-export Action You must give written notice of intention to claim drawback to arrive at the Glasgow

Drawback Processing Centre at least 2 complete working days before packaging for

export. (exception- hydrocarbon oil shipped as stores. See Note 11.1)

9. Post export action CHIEF S8 report with either a departed status of 60 for a direct export or a departed status

of 62 for an indirect export will be required to accompany the drawback claim form as

evidence to support the claim.

A certified C&E 132 if the export is by post.

10. VAT —

11. Notes 1. For hydrocarbon oils shipped as stores, drawback claimants who opt for examination at

their premises are to submit form HO66 to the local Advice Centre at least 2 days prior to

dispatch of the oil to the ship etc.

2. Claimants for hydrocarbon oil shipped as stores and who operate the ‘netting’ scheme

[Notice 179 part 12] are to enter ‘DRAWBACK SCHEDULER’ in Box 44 on the SAD. Drawback

Schedulers are not required to present a control copy 1 of the SAD to Customs at the port.

1.2.18/1 Customs Tariff Vol 311—10

PPSysB

Rev 18.02 PageLayout: CEX002 [O] Page: 11 Processed: 10-01-2018 10:22:49 Job: TARIFC Unit: PG11

.

VOLUME 3 APPENDIX E1

Volume 3

Appendix E 1

10 00 004

1. Goods Covered Imported Tobacco products in a sound condition, returned by the UK importer to the

overseas supplier on credit for repayment of the Tobacco Products duty.

2. Notice 476

3. Status of the goods. Box 1 enter code EX followed by A or D as appropriate.

4. Specific Fields in the declaration/notes Box 31 – warehouse stock record reference numbers should be entered.

on completion Box 33 – must show the Commodity Code to 8 digits of the goods being entered to the

export procedure.

5. Additional documents required —

6. Security required —

7. Additional information —

8. Pre-export Action Notice of intention to pack these products for export must be given. SAD copy 3 (or

photocopy) is to be lodged with the Client Relation Manager’s team for the exporter at

least 24 hours before packing is due to start. This document serves as a ‘Notice to Pack’

(see paragraph 7). In addition the exporter is to complete an Excise Control Document

(Form EX 49) and attach it to the SAD copy 3 (or photocopy).

9. Post export action Copy 3 of the SAD (C88) certifying the export at the office of exit from the EU will be

required as evidence to support the claim.

10. VAT —

11. Notes Credit or repayment of tobacco products duty borne by imported tobacco products which

are returned to the overseas supplier is subject to the detailed conditions set out in Notice

476, Section 6B.

10 00 007

1. Goods Covered FOR USE BY EXPRESS INDUSTRY NATIONAL EXPORT SYSTEM (NES) APPROVED MOU

OPERATORS ONLY

Supplementary declaration by authorised NES MOU operators for goods:

,less than £873 in value

,less than 1000kg, and

,not dutiable or restricted,

that were exported under the NES MOU procedure, where the pre shipment advice was

made under:

,CSE using CPC 10 00 077; or

,SDP using CPC 10 00 067

This CPC must not be used for:

-bulking of multi consignments shipped to multi consignees

-re-exporting non EU goods on which import charges have not been paid

2. Notice Memorandum of Understanding arrangements require the express/fast parcel operator to

fulfil specific roles and conditions set out by HMRC. Express/Fast parcel operators who are

approved CSE or SDP Operators and can fulfil the requirements set out in the MOU can

apply by contacting the Express Industry Team in Cardiff on Tel: 03000 532 318 for

further information and advice.

3. Status of Goods T2 - goods in free circulation and not subject to any other regime controls

4. Specific Fields in the declaration/notes Full details can be found in the data requirements provided to NES MOU approved traders.

on completion

5. Additional documents required -

1.2.18/1 Customs Tariff Vol 311—11

.

VOLUME 3 APPENDIX E1

PPSysB

Rev 18.02 PageLayout: CEX002 [E] Page: 12 Processed: 10-01-2018 10:22:49 Job: TARIFC Unit: PG11

Volume 3

Appendix E 1

6. Security required -

7. Additional information -

8. Pre-export action See relevant pre shipment CPC CSE 10 00 077 or SDP 10 00 067.

9. Post Clearance Action An electronic aggregate supplementary declaration must be submitted using one of

the available methods within 14 calendar days of the date of departure of the export

means of transport. The CPC must be 10 00 007.

10. VAT Documentary evidence of export is required to support VAT zero-rating. The UK supplier

must ensure that they obtain and keep official or commercial evidence for all

consignments. If evidence of export is not obtained within the specified period then the

supply must not be zero-rated. For full details on VAT time limits for exports and zero-

rating see Notice 703.

11. Notes -

10 00 008

1. Goods Covered FOR USE BY EXPRESS INDUSTRY NATIONAL EXPORT SYSTEM (NES) APPROVED MOU

OPERATORS ONLY

Supplementary declaration by authorised NES MOU operators for goods:

,classified as non-statistical (see Notice 275) and

,not dutiable or restricted,

that were exported under the NES MOU procedure, where the pre shipment clearance

request / advice was made under:

,CSE using CPC 10 00 078; or

,SDP using CPC 10 00 068

This CPC must not be used for bulking of multi consignments shipped to multi consignees

under standard NES.

2. Notice Memorandum of Understanding arrangements require the express/fast parcel operator

to fulfil specific roles and conditions set out by HMRC. Express/Fast parcel operators

who are approved CSE or SDP Operators and can fulfil the requirements set out in the

MOU can apply by contacting the Express Industry Team in Cardiff on Tel: 03000 523

318 for further information and advice.

3. Status of Goods T2 - goods in free circulation and not subject to any other regime controls

4. Specific Fields in the declaration/notes Full details can be found in the data requirements provided to NES MOU approved traders.

on completion

5. Additional documents required -

6. Security required -

7. Additional information -

8. Pre-export action See relevant pre shipment CPC CSE 10 00 078 or SDP 10 00 068

9. Post Clearance Action An electronic aggregate supplementary declaration must be submitted using one of the

available methods within 14 calendar days of the date of departure of the export means

of transport. The CPC must be 10 00 008.

10. VAT Documentary evidence of export is required to support VAT zero-rating. The UK supplier

must ensure that they obtain and keep official or commercial evidence for all

consignments. If evidence of export is not obtained within the specified period then the

supply must not be zero-rated. For full details on VAT time limits for exports and zero

rating see Notice 703.

11. Notes -

1.2.18/1 Customs Tariff Vol 311—12

PPSysB

Rev 18.02 PageLayout: CEX002 [O] Page: 13 Processed: 10-01-2018 10:22:49 Job: TARIFC Unit: PG11

.

VOLUME 3 APPENDIX E1

Volume 3

Appendix E 1

10 00 009

1. Goods Covered FOR USE BY EXPRESS INDUSTRY NATIONAL EXPORT SYSTEM (NES) APPROVED MOU

OPERATORS ONLY

Supplementary declaration by authorised NES MOU operators for goods exported

under the NES MOU procedure that were:

,more than £750 but less than £2000 in value

,less than 1000kg; and

,not dutiable or restricted,

where the pre shipment advice was made under:

,CSE using CPC 10 00 079; or

,SDP using CPC 10 00 069

This CPC must not be used for bulking of multi consignments shipped to multi consignees

under standard NES.

2. Notice Memorandum of Understanding arrangements require the express/fast parcel operator

to fulfil specific roles and conditions set out by HMRC.

Express/Fast parcel operators who are approved to use Customs Supervised Exports

(CSE) or Simplified Declaration Procedures (SDP) and can fulfil the requirements set out

in the MOU can apply by contacting the Express Industry Team in Cardiff on Tel: 03000

523 318 for further information and advice.

3. Status of Goods T2 - goods in free circulation and not subject to any other regime controls

4. Specific Fields in the declaration; notes Full details can be found in the data requirements provided to NES MOU approved

on completion: operators.

5. Additional documents: -

6. Security required -

7. Additional information -

8. Pre-export action: See relevant pre shipment CPC CSE 10 00 079 or SDP 10 00 069

9. Post export action An electronic aggregate supplementary declaration at item level must be submitted using

one of the available methods within 14 calendar days of the date of departure of the

export means of transport. The CPC must be 10 00 009.

10. VAT Documentary evidence of export is required to support VAT zero-rating. The UK supplier

must ensure that they obtain and keep official or commercial evidence for all

consignments. If evidence of export is not obtained within the specified period then the

supply must not be zero-rated. For full details on VAT time limits for exports and zero

rating see Notice 703.

11. Notes -

10 00 011

1. Goods Covered Pre-shipment declaration for free circulation goods being exported outside the EU under

NES Simplified Declaration Procedures (SDP) by or on behalf of an NES approved SDP

operator.

This CPC must NOT be used for:

-Goods subject to a CAP refund or CAP export licensing

-Excise goods in excise duty suspension

-Non EU goods on which import charges have not been paid

-Goods subject to any other SDP CPC or regime controls

2. Notice 275 - Customs export procedures

3. Status of Goods T2 - Goods in free circulation and not subject to any other regime controls.

1.2.18/1 Customs Tariff Vol 311—13

.

VOLUME 3 APPENDIX E1

PPSysB

Rev 18.02 PageLayout: CEX002 [E] Page: 14 Processed: 10-01-2018 10:22:49 Job: TARIFC Unit: PG11

Volume 3

Appendix E 1

4. Specific Fields in the declaration/notes Additional information and completion notes for boxes on the declaration are given in

on completion Volume 3 Part 1 of this Tariff.

Box 1

1st sub division enter:

,‘CO’ for export to an EU Special Territory (see Tariff Volume 1 Part 2 Section 1),

,‘EX’ for export outside the EU; or

,‘EU’ for export to an EFTA country

2nd sub division: enter code ‘F’ (pre-shipment advice (PSA) goods not arrived)

Box 14(1): Enter the code for representation:

1—self representation

2—direct representation

3—indirect representation

Box 17: Enter the code for the non EU country of ultimate destination, see Appendix C1

for Country Codes note - except for EU Special Territories or areas not under the control of

The Government of the Republic of Cyprus, this should not be an EU country)

Box 29,The intended Office of Exit must be declared when the export is via another

Member State (Indirect Export) and the movement is required to be controlled

by the EU Export Control System (ECS).

,If goods are being exported via another EU country under a Single Transport Contract

(STC) do not complete Box 29 (in such cases an Additional Information (AI) statement in

Box 44 must be made—see below).

Box 44:

-Enter a Unique Consignment reference number (UCR), see CPC 10 00 001 note 11.4.

-For export under a Single Transport Contract enter Additional Information (AI)

statement ‘STC99’ (see Appendix C9).

5. Additional documents required -

6. Security required -

7. Additional information -

8. Pre-export action Goods to be presented to Customs at the Frontier office of export, Inland Clearance Depot

or other designated export place. EU safety and security legislation sets minimum time

limits for goods to be presented to Customs:

-for ‘deep sea’ containerised cargo, at latest 24 hours before the goods are loaded

-for ‘short sea’ containerised cargo, at latest 2 hours before leaving the port

-for air traffic, at latest 30 minutes before departure from an airport

-for rail and inland waters traffic, at latest 2 hours before departure

-for road traffic, at latest 1 hour before departure

-

9. Post Clearance Action A Supplementary Declaration using CPC 10 00 001 must be made within 14 calendar days

of the “goods departed message”.

10. VAT Documentary evidence of export is required to support a claim to VAT zero rating. The UK

supplier must therefore ensure that they obtain and keep official or commercial evidence

for all consignments. If evidence of export is not obtained within the specified time limit

then the supply must not be zero-rated. For Full details on VAT time limits for exports and

zero rating see Notice 703. Lack of official evidence may affect ability to zero rate goods.

11. Notes 11.1 Goods imported into the EU are in free circulation in the EU if all import formalities

have been completed and all duties, levies or equivalent charges have been paid and not

refunded. Goods originating in the EU are also in free circulation.

11.2 Declarations must be submitted electronically using one of the transmission routes

available to CHIEF within the specified timescale:

-Community Systems Provider (CSP) - Indirect link to CHIEF through a CSP using your

own software or that provided by an independent software company.

-NES Email - via the internet, in the form of an email attachment. You will need to

purchase commercial messaging software which translates the declaration sent to

and the messages received from CHIEF.

1.2.18/1 Customs Tariff Vol 311—14

PPSysB

Rev 18.02 PageLayout: CEX002 [O] Page: 15 Processed: 10-01-2018 10:22:49 Job: TARIFC Unit: PG11

.

VOLUME 3 APPENDIX E1

Volume 3

Appendix E 1

-NESWEB - via the interenet and the Government Gateway, using the NEWSWEB

facility. An export Declaration WEB form has been set up by HMRC which can be used

to submit information to CHIEF direct.

-NES XML - via the internet and the Government Gateway, using the NES XML facility.

You will need to purchase commercial messaging software to translate the messages

sent to and from CHIEF. In addition a Government Gateway Digital Certificate is

required for the CHIEF XML route.

11.3 Useful contact details:

-General Customs (including NES enquiries) -VAT, Excise & Customs Helpline Phone:

0300 200 3700

-NES Helpdesk Phone: 03000 582 418 Email: export.enquirieswhmrc.gsi.gov.uk

-Website: hmrc.gov.uk

10 00 012

1 Goods covered Goods under certain Commodity Codes indicated in the Tariff exported for Military Use

abroad.

2 Notice 2 – 11: The same requirements as for CPC 10 00 001 apply.

3 Status of goods

4 Specific fields on the declaration

5 Additional documents

6 Security required

7 Additional information

8 Pre-export action

9 Post-export action

10 VAT

11 Notes

10 00 013

1 Goods covered Goods which are free of duty and VAT, are owned by a visiting force or its personnel, and

have been obtained or imported under visiting forces relief.

2 Notice —

3 Status of goods T1.

4 Specific fields on the declaration Notes Box 8 must show the allocated TURN. The CPC (Box 37) must be 10 00 013 on

completion: Box 54 must be signed by an authorised signatory.

In addition only the following fields need to be completed: 2, 14, 17 and 31.

5 Additional documents —

6 Security required —

7 Additional information —

8 Pre-export action —

9 Post-export action —

1.2.18/1 Customs Tariff Vol 311—15

.

VOLUME 3 APPENDIX E1

PPSysB

Rev 18.02 PageLayout: CEX002 [E] Page: 16 Processed: 10-01-2018 10:22:49 Job: TARIFC Unit: PG11

Volume 3

Appendix E 1

10 VAT —

11 Notes Use of the CPC constitutes a declaration that the goods are the property of a visiting force

or its personnel and have been held in the UK under visiting forces relief.

Goods imported under other regimes are not proper to this CPC.

10 00 014

1. Goods Covered Pre-shipment declaration for free circulation goods being exported outside the EU under

NES CSE by or on behalf of an approved NES CSE Operator.

This CPC must not be used for:

-goods subject to a CAP refund or CAP export licensing

Excise goods in excise duty suspension

-Non EU goods on which import charges have not been paid

-Goods subject to any other CSE CPC

-Goods subject to any other regime controls

-Full declarations being made from an CSE location

2. Notice 275 Customs export procedures

3. Status of Goods T2 – Goods in free circulation and not subject to any other regime controls.

4. Specific Fields in the declaration/notes Additional information and completion notes for other boxes on the declaration are given

on completion in Volume 3 Part 1 of this Tariff.

Box 1:

1st sub division: enter:

,‘CO’ for export to an EU Special Territory (see Tariff Volume 1 Part 2 Section 1),

,‘EX’ for export outside the EU; or

,‘EU’ for export to an EFTA country

2nd sub division: enter code F (pre-shipment advice (PSA) goods not arrived).

Box 14(1): Enter the code for representation:

1—self representation

2—direct representation

3—indirect representation

Box 17: Enter the code for the non EU country of ultimate destination, see Appendix C1

for Country Codes

Box 29:

,The intended Office of Exit must be declared when the export is via another Member

State (Indirect Export) and the movement is required to be controlled by the EU Export

Control System (ECS).

If goods are being exported via another EU country under a Single Transport Contract

(STC) do not complete Box 29 (in such cases an Additional Information (AI) statement in

Box 44 must be made—see below).

Box 33:

The Commodity Code to 8 digits of the goods being declared for export (see Volume 2 of

this Tariff), further information about classifying goods is available in Notice 600—

Classifying your imports or exports).

Box 44:

-Enter a Unique Consignment reference number (UCR), see CPC 10 00 001 note 11.4.

-For export under a Single Transport Contract complete Additional Information (AI)

statement ‘STC99’ (see Appendix C9).

5. Additional documents required —

6. Security required —

7. Additional information —

8. Pre-export action Goods to be presented to Customs at the approved CSE Location.

1.2.18/1 Customs Tariff Vol 311—16

PPSysB

Rev 18.02 PageLayout: CEX002 [O] Page: 17 Processed: 10-01-2018 10:22:49 Job: TARIFC Unit: PG11

.

VOLUME 3 APPENDIX E1

Volume 3

Appendix E 1

9. Post Clearance Action A supplementary Declaration should be made using CPC 10 00 001 within 14 calendar

days of the “goods departed message”.

10. VAT Documentary evidence of export is required to support a claim to VAT zero rating. The UK

supplier must ensure that they obtain and keep official or commercial evidence for all

consignments. If evidence of export is not obtained within the specified time limit then the

supply must not be zero-rated. For Full details on VAT time limits for exports and zero

rating see Notice 703

11. Notes 11.1 Goods imported into the EU are in free circulation in the EU if all import formalities

have been completed and all duties, levies or equivalent charges have been paid and not

refunded. Goods originating in the EU are also in free circulation.

11.2 Declarations must be submitted electronically using one of the transmission routes

available to CHIEF within the specified timescale:

-Community Systems Provider (CSP) - Indirect link to CHIEF through a CSP using your

own software or that provided by an independent software company.

-NES Email - via the internet, in the form of an email attachment. You will need to

purchase commercial messaging software which translates the declaration sent to

and the messages received from CHIEF.

-NESWEB - via the interenet and the Government Gateway, using the NEWSWEB

facility. An export Declaration WEB form has been set up by HMRC which can be used

to submit information to CHIEF direct.

-NES XML - via the internet and the Government Gateway, using the NES XML facility.

You will need to purchase commercial messaging software to translate the messages

sent to and from CHIEF. In addition a Government Gateway Digital Certificate is

required for the CHIEF XML route.

11.3 Useful contact details:

-General Customs (including NES enquiries) -VAT, Excise & Customs Helpline Phone:

0300 200 3700

-NES Helpdesk Phone: 03000 582 418 Email: export.enquirieswhmrc.gsi.gov.uk

-Website: hmrc.gov.uk.

10 00 018

1. Goods covered All goods exported under the EU’s preferrential trade arrangements which are covered by

proofs of preferential origin (EUR1/EUR-MED Movement certificates/Invoice Declarations

or Origin Declarations (issued under the EU-Korea Trade Agreement))

2. Notice 827, 828, 832

3. Specific fields in the declaration/ 10 00 018 must be inserted in Box 37 of the export declaration

notes on completion

4. Additional documents required Exporters need to provide their cusotmers with proof of the preferential origin of their

goods (i.e. an EUR1 or EUR-MED Movement certificate where provided for, a declaration on

an invoice or other commercial documents)

5. Security required -

6. Additional information -

7. VAT -

8. Post Clearance Action -

9. Notes Under SAD Harmonisation, new document codes have been introduced which must be

input to CHIEF when this CPS is used. There are 4 possible alternatives. These are 9001

(Invoice Declarations), N954 (EUR 1), U045 (EUR-MED Certificates) and U048 (EUR-MED

Invoice Declarations). Please check Appendix C10/C11 of the Tariff for the appropriate

status codes for use with these document codes.

1.2.18/1 Customs Tariff Vol 311—17

.

VOLUME 3 APPENDIX E1

PPSysB

Rev 18.02 PageLayout: CEX002 [E] Page: 18 Processed: 10-01-2018 10:22:49 Job: TARIFC Unit: PG11

Volume 3

Appendix E 1

10 00 027

1. Goods Covered All CAP goods exported for which a mandatory licence is required to be presented prior to

export, but export refund is not being claimed. This will normally apply where there is a

zero-rate of refund in place. However, it can also apply where the Exporter chooses not to

claim refund even though a positive rate is in force.

Where a mandatory licence is required, but refund is being claimed (or a charge is due),

CPCs 10 00 E51 (Annex 1) or 10 00 E61 (Non Annex 1) should be used instead.

2. Notice 800

3. Status Of Goods Form T1 is required when goods are being exported to or via an EFTA country (for T5

requirements, see 7 ‘additional information’, below). A T1 may also be needed if goods are

shipped on a non-regular vessel which calls at another Community port.

4. Specific Fields in the declaration/notes Box 2: ‘Consignor/Exporter’ must be entered.

on completion Box 18: ‘Identity of means of transport at departure’ must be entered.

Box 21: ‘Nationality of active means of transport crossing the border’ must be entered.

Box 29: The ‘Office of Exit’ must be completed in accordance with the notes in Volume 3

Part 1.

Box 34a: ‘Country of origin code’ the code for the original country of origin of the goods

must be entered.

Box 37: Customs Procedure Code 10 00 027 must be entered.

Box 47e: Enter MOP %L

All refunds fields must be completed, even though refund is not claimable/being claimed.

(See 4.3A CAP Export Refund Claims)

5. Additional documents required – CAP licence (may be paper version especially if issued by Paying Agencies in other

Members States).

– Licence for food aid consignments.

– National/Community Transit documentation as required.

6. Security required The Rural Payments Agency (RPA) will notify you when licence securities are required and

these should be lodged with them before completion of the declaration. Likewise for

securities for export charges if implemented.

7. Additional information There are specific arrangements for goods from intervention and for food aid

consignments. You may have to provide additional information and/or security and/or

documentation to the RPA. 67

8. VAT -

9. Pre-Entry Action Full NES declaration to be made at time of export, using pre-entry or CSE format, as

appropriate, SDP cannot be used. Prior notification must be made at least 24 hours before

export, unless another period has been agreed with Customs at the point of loading.

Licence to be submitted where required. Ensure location is suitable for CAP export. Contact

Customs if in doubt.

10. Post Clearance Action None

11. Notes Under SAD Harmonisation new additional information codes, document codes and status

codes have been introduced which must be input to CHIEF Form T1 enter N821, form T5

enter N823. Refer to Tariff Volume 3 Appendix C9, C10 and C11.

1.2.18/1 Customs Tariff Vol 311—18

PPSysB

Rev 18.02 PageLayout: CEX002 [O] Page: 19 Processed: 10-01-2018 10:22:49 Job: TARIFC Unit: PG11

.

VOLUME 3 APPENDIX E1

Volume 3

Appendix E 1

10 00 028

1. Goods Covered Free circulation goods being exported outside the EU as part of a groupage consignment

where the total value of the shipment does not exceed £6000. Goods must be consigned

from one exporter to one consignee only.

There is no restriction on the number of consignments that can make up the shipment but

the total £6000 value limit should not be exceeded.

Consignments “bulked” under this export CPC must not be:

,subject to a CAP refund or CAP export licensing requirements,

,goods that are not in free circulation

,subject to any export licensing requirements, prohibition or restriction; or

,goods under SDP

2. Notice 275 Customs export procedures

3. Status of the goods. T2 - Goods in free circulation and not subject to any other regime controls.

4. Specific Fields in the declaration/notes Box 1:

on completion 1st sub division:

,‘CO’ for export to an EU Special Territory (see Tariff Volume 1 Part 2 Section 1),

,‘EX’ for export outside the EU; or

,‘EU’ for export to an EFTA country

2nd sub division: enter code ‘D’.

Box 2 - ‘Consignor/Exporter’ must be shown.

Box 8 - ‘Consignor/Importer’ must be shown.

Box 14(1): Enter the code for representation:

1 - self representation

2 - direct representation

3 - indirect representation

Box 17: Enter the code for the non EU country of ultimate destination, see Appendix C1

for Country Codes

Box 29:

,Where export will be made via another EU country (Indirect Export) the Office of

Exit in that EU country must be declared as the movement is required to be

controlled by the EU Export Control System (ECS).

-If goods are being exported via another EU country under a Single Transport

Contract (STC) do not complete Box 29 (in such cases an Additional Information (AI)

statement in Box 44 must made - see below).

Box 33 - ‘Commodity Code’ shown must indicate the Commodity Code of the highest

valued part of the shipment (see Volume 2 of this Tariff), further information about

classifying goods is available in Notice 600—Classifying your imports or exports).

Box 40:

-identify the relevant commercial document and Traders own ref that provides an

audit link to the consignment. For example a MUCR that provides an audit link to the

consignment. To identify a MUCR enter:

,‘Z’ (for previous document)

,followed by code ‘ZZZ’ (for other)

,followed by the MUCR reference

the above components would be entered as ‘Z-ZZZ-**********“’

Box 37 - ‘CPC’ 10 00 028 must be used.

Box 44: For export under a Single Transport Contract enter Additional Information (AI)

statement ‘STC99’ (see Appendix C9).

Box 46 - Statistical value must not exceed £6000

5. Additional documents required No additional documents are required however, operators using this CPC must retain

records to account for the value and nature of goods being exported.

6. Security required -

1.2.18/1 Customs Tariff Vol 311—19

.

VOLUME 3 APPENDIX E1

PPSysB

Rev 18.02 PageLayout: CEX002 [E] Page: 20 Processed: 10-01-2018 10:22:49 Job: TARIFC Unit: PG11

Volume 3

Appendix E 1

7. Additional information Where an appointed Freight Agent is declaring goods using this CPC on behalf of an

unregistered trader, the level of Representation must be indirect. Failure to comply with

the £6000 limit may result in use this CPC being withdrawn by the agent / operator

concerned.

8. VAT Operators must retain records to account for the exported ‘bulked’ goods.

9. Pre Entry Action A full NES declaration must be made at the time of export A full CSE entry must be made if

goods are declared at an HMRC approved inland premises.

10. Post Clearance Action Operators records must account for the actual nature of the goods supplied and the

values.

11. Notes 11.1 Goods imported into the EU are in free circulation in the EU if all import formalities

have been completed and all duties, levies or equivalent charges have been paid and not

refunded. Goods originating in the EU are also in free circulation.

11.2 Declarations must be submitted electronically using one of the transmission routes

available to CHIEF within the specified timescale:

-Community Systems Provider (CSP) - Indirect link to CHIEF through a CSP using your

own software or that provided by an independent software company.

-NES Email - via the internet, in the form of an email attachment. You will need to

purchase commercial messaging software which translates the declaration sent to

and the messages received from CHIEF.

-NESWEB - via the interenet and the Government Gateway, using the NEWSWEB

facility. An export Declaration WEB form has been set up by HMRC which can be used

to submit information to CHIEF direct.

-NES XML - via the internet and the Government Gateway, using the NES XML facility.

You will need to purchase commercial messaging software to translate the messages

sent to and from CHIEF. In addition a Government Gateway Digital Certificate is

required for the CHIEF XML route.

11.3 Useful contact details:

-General Customs (including NES enquiries) -VAT, Excise & Customs Helpline Phone:

0300 200 3700

-NES Helpdesk Phone: 03000 582 418 Email: export.enquirieswhmrc.gsi.gov.uk

-Website: hmrc.gov.uk

10 00 029

1. Goods Covered Any excise goods entered under SDP and presented for export at the Frontier.

2. Notice 179, 197 & 476

3. Status of the goods. Box 1 enter code EX followed by A or D as appropriate.

4. Specific Fields in the declaration/notes Box 31 – warehouse stock record reference numbers should be entered.

on completion Box 33 – must show the Commodity Code to 8 digits of the goods being entered to the

export procedure.

5. Additional documents required For goods moving in excise duty suspension the following documents are required:

For direct exports: Form W8 (from the approved warehouse to the port of exportation in

the UK)

For indirect exports: An AAD (from the approved warehouse to the place of exit from the

EU)

6. Security required For both direct and indirect exports, financial security is mandatory of both the AAD and

W8.

7. Additional information —

8. Pre-export Action —

1.2.18/1 Customs Tariff Vol 311—20

PPSysB

Rev 18.02 PageLayout: CEX002 [O] Page: 21 Processed: 10-01-2018 10:22:49 Job: TARIFC Unit: PG11

.

VOLUME 3 APPENDIX E1

Volume 3

Appendix E 1

9. Post export action Both the W8 and AAD must be discharged at the place of exit from the EU. Copy 3

(ENDORSED) must be returned to the warehouse of dispatch to discharge the movement.

10. VAT Documentary evidence of export is required to support a claim to VAT zero-rating. The UK

supplier must ensure that they obtain and keep official or commercial evidence for all

consignments.

If evidence of export is not obtained within the specified period then the supply must not

be zero rated. For full details on VAT time limits for exports and zero-rating see Notice

703.

11. Notes

10 00 030

1. Goods Covered Any excise goods already released to consumption in the UK (excise duly paid) entered for

export under Customs Supervised Procedure.

2. Notice 179, 197, & 476

3. Status of the goods. Box 1 enter code EX followed by A or D as appropriate.

4. Specific Fields in the declaration/notes Box 33 – must show the Commodity Code to 8 digits of the goods being entered to the

on completion export procedure.

5. Additional documents required -

6. Security required -

7. Additional information This CPC cannot be used for excise goods in duty suspension (under the cover of an AAD/

e-AD or W8/e-W8 or commercial equivalent documents) or for goods where drawback of

the UK excise duty is claimed.

8. Pre-export Action —

9. Post export action -

10. VAT Documentary evidence of export is required to support a claim to VAT zero-rating. The UK

supplier must ensure that they obtain and keep official or commercial evidence for all

consignments.

If evidence of export is not obtained within the specified period then the supply must not

be zero rated. For full details on VAT time limits for exports and zero-rating see Notice

703.

11. Notes —

10 00 041

1 Goods covered C21 Customs clearance request for goods recorded on a port or airport inventory system

that are not specified or covered by another CPC and:

-do not require formal C88 Customs export declaration as they are declared under

their own paper Customs form; or

-do not require a Customs declaration - for example free circulation goods being sent

via a third country to another EU Country, where the goods remain* loaded on board

the vessel or aircraft during the call at the port or airport outside the EU

*(if the goods will be unloaded to another vessel/aircraft in the third country, an exit

summary declaration using CPC 10 00 046 should be made)

-do not require a Customs declaration for example because they are intra EU

movements of Inward Processing (IP) goods being transferred under the paper 2-

copy or 3-copy SAD transfer process from an IP Authorisation holder (in the UK) to

another IP Authorisation holder (in another Member State (OMS));

1.2.18/1 Customs Tariff Vol 311—21

.

VOLUME 3 APPENDIX E1

PPSysB

Rev 18.02 PageLayout: CEX002 [E] Page: 22 Processed: 10-01-2018 10:22:49 Job: TARIFC Unit: PG11

Volume 3

Appendix E 1

-for similar 2-copy/3-copy SAD transfers for other CPEI procedures such as:

,Customs Warehousing (CW UK) to CW (OMS);

,Processing under Customs Control (PCC UK) to PCC (OMS); and

,Temporary Admission (TA UK) to TA (OMS).

2 Notice —

3 Status of goods —

4 Specific fields on the declaration Box 1: ,1st sub division: EX or EU as appropriate

2nd sub division: enter code K.

Box 30: Goods Location Code

,Part 1—Enter GB

,Part 2 - Enter from Appendix C2 the relevant goods location code for where the

goods are available for examination

,Part 3 - Only to be completed at locations where computerised inventory

systems are based on the use of transit shed identity codes. See Appendix C4.

Box 40: previous document—enter the document class code and type (see Appendix C12)

followed by the document reference against which the goods have been formally

declared.

For example for goods on an ATA carnet you would enter ‘Z-955-’ (followed by the ATA

carnet number).

Box 44: Additional Information, enter:

,the appropriate Additional Information code (see Appendix C9),

,Document Status code (see Appendix C10) and Document/Certificate Code (see

Appendix C11).

5 Additional documents The relevant formal Customs declaration form (excluding C88), if appropriate.

6 Security required —

7 Additional information Goods must be declared electronically using CHIEF format IECR (insert export clearance

request), so that the consignment can be processed and released under NES.

8 Pre-export action —

9 Post-export action —

10 VAT —

11 Notes Useful contact details:

-General Customs (including NES enquiries) -VAT, Excise & Customs Helpline Phone:

0300 200 3700

-NES Helpdesk Phone: 03000 582 418 email: export.enquirieswhmrc.gsi.gov.uk

-Website: hmrc.gov.uk

10 00 042

1 Goods covered C21 Customs clearance request for non EU goods travelling en route via the UK or non

EU goods removed from a Temporary Storage facility:

-For direct exit from UK outside the EU

-Departing the UK under NCTS Transit procedures for onward movement to another

EU Member State

-Departing the UK under NCTS Transit procedures for onward movement to another

EU Member State for exit from the EU.

NOTE – If the goods will exit the EU from an another EU Member State and an Exit

Summary Declaration (EXS) is required, CPC 10 00 046 should be made unless:

-the NCTS declaration contains the exit summary declaration data; and

1.2.18/1 Customs Tariff Vol 311—22

PPSysB

Rev 18.02 PageLayout: CEX002 [O] Page: 23 Processed: 10-01-2018 10:22:49 Job: TARIFC Unit: PG11

.

VOLUME 3 APPENDIX E1

Volume 3

Appendix E 1

-the office of destination is also the customs office of exit or the office of destination

is outside the EU.

A declaration is required on the NCTS for all goods to be moved under Community/

common transit or TIR unless simplified procedures for air, sea or rail are used.

2 Notice 216 at CCS-UK airports.

3 Status of goods T1 – goods not in free cirulation.

4 Specific fields on the declaration Box 6 – Packages.

Bulked goods enter 1 (with the exception of licensed goods)

Box 40 previous document – enter ‘Z’ followed by the document type code (see Appendix

C12) followed by the document reference.

Box 44 – If departing the UK under NCTS Transit procedures enter AI code ‘TRANS’.

5 Additional documents —

6 Security required For goods moving under NCTS Transit the normal guarantee requirements for the transit

procedure concerned apply.

7 Additional information Declaration should be in the format IECR (Insert export clearance request).

8 Pre-export action —

9 Post-export action —

10 VAT —

11 Notes Useful contact details:

-General Customs (including NES enquiries) – VAT, Excise & Customs Helpline Phone:

0300 200 3700

-NES Helpdesk Phone: 03000 582 418 email: export.enquirieswhmrc.gsi.gov.uk

-For Transit the NCTS helpdesk at the CCTO, Harwich Monday to Friday 08:00—17:00

Tel: 03000 575 988 email: ncts.helpdeskwhmrc.gsi.gov.uk

-Website: hmrc.gov.uk

10 00 043

1 Goods covered C21 Clearance request for EU goods from another EU country (under cover of a SAD Copy

3 or ECS equivalent document), being exported outside the EU via the UK. Use of this

facility is essential for movements through inventory-linked locations.

2 Notice 216 - Customs procedures at CCS-UK airports.

3 Status of goods T2 - Goods in free circulation and not subject to any other regime controls.

1.2.18/1 Customs Tariff Vol 311—23

.

VOLUME 3 APPENDIX E1

PPSysB

Rev 18.02 PageLayout: CEX002 [E] Page: 24 Processed: 10-01-2018 10:22:49 Job: TARIFC Unit: PG11

Volume 3

Appendix E 1

4 Specific fields on the declaration Box 1

1st sub division:

,‘EX’ for export outside the EU; or

,EU for export to an EFTA country

2nd sub division: enter code K.

Box 2 - Consignor

If the Consignor has a UK EORI this is to be quoted. If not enter:

,Private individuals can use GBPR where there is no commercial purpose involved

for example household effects.

,

Box 30: Goods Location Code

,Part 1—Enter GB

,Part 2 - Enter from Appendix C2 the relevant goods location code for where the

goods are available for examination

,Part 3—Only to be completed at locations where computerised inventory

systems are based on the use of transit shed identity codes (See appendix C4).

67

5 Additional documents SAD Copy 3 or ECS equivalent form (EAD) from Other Member State (OMS) Office of Export

for endorsement by the UK Office of Exit (ECS Helpdesk Central Community Transit Office).

6 Security required —

7 Additional information Declaration should be in the CHIEF format IECR (Input export clearance request).

8 Pre-export action —

9 Post-export action EAD (Export Accompanying Document) - with a Movement Reference Number (MRN) - to

be forwarded using the FREEPOST service to the ECS Helpdesk, Harwich, clearly showing

the NES C21 entry reference number.

10 VAT EAD (Export Accompanying Document) - without a Movement Reference Number (MRN) -

must be endorsed by the ECS Helpdesk in Harwich.

11 Notes Useful contact details:

-General Customs (including NES enquiries) -VAT, Excise & Customs Helpline Phone:

0300 200 3700

-NES Helpdesk Phone: 03000 582 418 Email: export.enquirieswhmrc.gsi.gov.uk

-Website: hmrc.gov.uk

10 00 044

1. Goods Covered CAP refund goods originally placed in control in another Member State, travelling under

cover of a Control Copy T5, and exiting from the EU via the UK.

2. Notice 800

3. Status Community Status Export.

4. Specific Fields in the declaration/notes Box 2 – Consignor/Exporter must be entered.

on completion Box 18: ‘Identity of means of transport at departure’ must be entered.

Box 21: ‘Nationality of active means of transport crossing the border’ must be entered.

Box 34a:‘Country of origin code’ for the original country of origin of the goods must be

entered.

Box 37: Customs Procedure Code 10 00 044 must be entered.

5. Additional documents required A certified Control Copy T5 must be presented to UK Customs.

1.2.18/1 Customs Tariff Vol 311—24

PPSysB

Rev 18.02 PageLayout: CEX002 [O] Page: 25 Processed: 10-01-2018 10:22:49 Job: TARIFC Unit: PG11

.

VOLUME 3 APPENDIX E1

Volume 3

Appendix E 1

6. Security required If licence securities are required these should be lodged with the payment agency of the

originating Member State before completion of the declaration. Likewise for securities for

export charges if implemented.

7. Additional information —

8. VAT —

9. Pre Entry Action It is important this request is lodged before export. Failure to do so prevents UK Customs

from endorsing the Control Copy T5. This could result in non-payment of CAP export

refund or forfeit of the licence security.

10. Post Clearance Action The T5 must be endorsed by UK Customs and sent to the originating authority in the

Member State of export.

11. Notes If a Copy 3 of the SAD is presented, the procedures are set out in CPC 10 00 043.

Under SAD Harmonisation new additional information codes, document codes and status

codes have been introduced which must be input to CHIEF. Form T5 enter N823. Refer to

Tariff Volume 3 Appendix C9, C10 and C11.

10 00 045

1. Goods Covered Indirect export via the UK of EU goods from other Member States where the consignment

value does not exceed 3000 Euros.

This CPC must not be used for:

,goods not in free circulation

,goods covered by EU export licenses where export has to be certified in the UK.

If goods are under cover of a SAD Copy 3 or ECS equivalent document from another EU

country CPC 10 00 043 should be used.

2. Notice —

3. Status of Goods T2 - Goods in free circulation and not subject to any other regime controls.

4. Specific Fields in the declaration/notes Box 1 –

on completion 1st sub division: CO, EX or EU as appropriate

2nd sub division: enter code K.

Box 2 – Consignor

If the Consignor has a UK EORI this is to be quoted.

,Private individuals can use GBPR where there is no commercial purpose involved

for example household effects.

,

Box 6 – Packages.

If Bulked goods enter 1.

Box 30: Goods Location Code

Part 1 – Enter GB

Part 2 – Enter from Appendix C2 the relevant goods location code for where the goods are

available for examination

Part 3 – Only to be completed at locations where computerised inventory systems are

based on the use of transit shed identity codes. See appendix C4.

Box 31 – Enter goods description “Bulked OMS goods – Not subject to any further

controls”. See Appendix C8 for appropriate package codes.

5. Additional documents required —

6. Security required —

7. Additional information Information declaration should be in the format Insert Export Clearance Request (IECR).

1.2.18/1 Customs Tariff Vol 311—25

.

VOLUME 3 APPENDIX E1

PPSysB

Rev 18.02 PageLayout: CEX002 [E] Page: 26 Processed: 10-01-2018 10:22:49 Job: TARIFC Unit: PG11

Volume 3

Appendix E 1

8. Pre-export action —

9. Post Clearance Action —

10. VAT —

11. Notes —

CPC 10 00 046

1. Goods Covered This CPC is for declarants making an Exit Summary Declaration (EXS) under ECS Safety and

Security requirements.

2. Notice 275

3. Status of Goods —

4. Specific Fields in the declaration/notes -Box 2 – Consignor TID

on completion If the Consignor is based in the UK, use GB pre-fixed EORI number.

If the Consignor is based in another EU MS, use non-GB pre-fixed EORI number and

provide full Consignor name and address details

If Consignor is not based in the EU and does not have an EORI number, the TID Field must

show full Consignor name and address details

-For intra-EU movements with a transhipment en route in a Third Country:–

Box 15a: Country of Despatch: Enter GB

Box 17a: Country of Destination: Enter country code for EU Member State to which goods

are going.

Box S13: Countries of Routing: Enter the country code(s) of the non EU transhipment

Countries where appropriate.

For the transhipment within the UK of non-EU status goods, the Dispatch Country field

should show GB with the originating country code being shown in Box 2 along with

Consignor details.

-The following Safety and Security items must be provided where known:–

Box 44: The transport document reference number.

Box S13: Countries of Routing Codes

Box S27: UN Dangerous Goods code (UNDG) if applicable.

Box S28: Seal Number

Box S29: Transport Charges Method of Payment Code (TCM)

-Box 31 – Goods description

Unless subject to an EU export declaration, all goods going to a country subject to EU

sanctions where a licence has been issued by the Department of Business Innovation &

Skills (BIS). The licence shall be declared in the format 'country code('licence type(

'licence identifier(

This information must be given in box 31 (goods description) as box 44 (documents)

cannot be used within the IEXS transaction.

5. Additional documents required —

6. Security required —

1.2.18/1 Customs Tariff Vol 311—26

PPSysB

Rev 18.02 PageLayout: CEX002 [O] Page: 27 Processed: 10-01-2018 10:22:49 Job: TARIFC Unit: PG11

.

VOLUME 3 APPENDIX E1

Volume 3

Appendix E 1

7. Additional information Transaction code is IEXS

Reduced Data sets:

There are three specific circumstances where a reduced data set can be used for the EXS

declaration. These are the only AI statements accepted under IEXS and should be declared

in Box 44 if the reduced data set is being used.

Table entry code – SPCIA-Postal and Express

Table entry code – SPCIB-Ship and Aircraft supplies

Table entry code – SPCIE-AEO

Sanctions

Unless subject to an EU export declaration, an EXS will be required for all goods going

to or from Countries that are subject to EU sanctions. Please refer to the FCO website

for details of countries subject to sanctions.

, http://www.fco.gov.uk/en/about-us/what-we-do/services-we-deliver/export-controls-

sanctions/eu-sanctions/

8. VAT —

9. Post Clearance Action —

10. Notes —

10 00 051

1 Goods covered The export from the EU of:

-Civil aircraft or parts of civil aircraft discharged of duty liability under Article 544(c)

of EC Regulation 2454/93;

-Spacecraft and parts of spacecraft discharged of duty liability under Article 544(d) of

EC Regulation 2454/93

2 Notice 3001

3 Status of goods 1st sub division: EX

2nd sub division enter code D

4 Specific fields on the declaration -Box 44 – see Note 7

5 Additional documents -

6 Security required If stated in IPR authorisation

7 Additional information In Box 44 of the SAD enter:

-Document code C601

-IPR authorisation number

-Do not enter a document status code

-Authorisation holders reference number as a GEN 45 AI statement – if any.

-Declare the full name and address of the supervising Customs Office as a SPOFF

Statement

-Enter “IP/S goods “ as a 10200 AI Statement

-Details of security if required-enter the appropriate RFS code from Appendix C10

8 Pre-export action —

9 Post-export action —

10 VAT —

11 Notes No preference documents can be issued in respect of these goods

1.2.18/1 Customs Tariff Vol 311—27

.

VOLUME 3 APPENDIX E1

PPSysB

Rev 18.02 PageLayout: CEX002 [E] Page: 28 Processed: 10-01-2018 10:22:49 Job: TARIFC Unit: PG11

Volume 3

Appendix E 1

10 00 052 Exportation

FOR USE ON FORM C21 AT ALL LOCATIONS WITH COMPUTERISED INVENTORY LINK

1. Goods Covered Goods exported or re-exported on an ATA carnet.

2. Notice 104.

3. Status of Goods —

4. Specific Fields on the declaration Box 1: 1st sub division: EX or EU as appropriate 2nd sub division: enter code K.

Box 30: Goods Location Code

Part 1 – Enter GB

Part 2 – Enter from Appendix C2 the relevant goods location code for where the goods are

available for examination

Part 3 – Only to be completed at locations where computerised inventory systems are

based on the use of transit shed identity codes. See Appendix C4.

Box 40: previous document - enter the document class code and type (see Appendix C12)

followed by the document reference against which the goods have been formally

declared. For example for goods on an ATA carnet you would enter ‘Z-955-’ (followed by

the ATA carnet number).

Box 44: Additional information, enter:

The appropriate Additional Information code IRQ02 (to request endorsement of the ATA

carnet by UK customs (see Appendix C9).

Document Status code AI code (see Appendix C10) and Document/Certificate Code ‘AC’ (see

Appendix C11).

Document code ‘N955’ to identify an ATA carnet.

5. Additional documents The signed ATA Carnet must be presented.

6. Security required Security is provided for under the ATA carnet by the issuing association and international

chain of guaranteeing associations

7. Additional information —

8. Pre-export action —

9. Post-export action The officer at the port/airport must forward the detached exportation (yellow) or re-

exportation voucher (white) from the ATA carnet promptly to the: National Carnet Unit

Ralli Quays, Stanley Street, Salford M60 9HL 03000 579 060.

10. VAT —

11. Notes Useful contact details:

General Customs (including NES enquiries) - VAT, Excise & Customs Helpline Phone: 0300

200 3700.

10 00 053 Exportation

1. Goods Covered Goods exported or re-exported on an ATA carnet which need a CHIEF declaration because

a licence needs to be declared.

2. Notice 104.

3. Status of Goods —

1.2.18/1 Customs Tariff Vol 311—28

PPSysB

Rev 18.02 PageLayout: CEX002 [O] Page: 29 Processed: 10-01-2018 10:22:49 Job: TARIFC Unit: PG11

.

VOLUME 3 APPENDIX E1

Volume 3

Appendix E 1

4. Specific Fields on the declaration Box 1: 1st sub division: EX or EU as appropriate 2nd sub division: enter code D.

Box 30: Goods Location Code

Part 1 – Enter GB

Part 2 – Enter from Appendix C2 the relevant goods location code for where the goods are

available for examination

Box 40: previous document - enter the document class code and type (see Appendix C12)

followed by the document reference against which the goods have been formally

declared. For ATA this is ‘Z-955-’ (followed by the ATA carnet number).

Box 44: Additional information, enter:

The appropriate Additional Information code (see Appendix C9), Document Status code

(see Appendix C10) and Document/Certificate Code (see Appendix C11). For ATA this is AI

code IRQ02 (to request endorsement of the ATA carnet by UK customs on export),

document status code ‘AC’ (to indicate the ATA carnet is being presented for certification

by customs), and document code ‘N955’ to identify an ATA carnet.

5. Additional documents The ATA must be presented.

6. Security required —

7. Additional information Goods must be declared electronically using CHIEF format IEFD (insert export full

clearance), so that the consignment can be processed and released under NES.

8. Pre-export action —

9. Post-export action The officer at the port/airport must forward the detached yellow exportation or white re-

exportation voucher from the ATA carnet promptly to the: National Carnet Unit Ralli

Quays, Stanley Street, Salford M60 9HL 03000 579 060 atacarnetunitwhmrc.gsi.gov.uk

10. VAT —

11. Notes Useful contact details:

General Customs (including NES enquiries) - VAT, Excise & Customs Helpline Phone: 0300

200 3700 - National Carnet Unit Tel: 03000 579 060

Website: hmrc.gov.uk

10 00 067

1. Goods Covered FOR USE BY EXPRESS INDUSTRY NATIONAL EXPORT SYSTEM (NES) APPROVED MOU

OPERATORS ONLY

SDP Pre-shipment advice for free circulation goods being exported outside the EU

under the NES MOU procedure by authorised NES MOU operators, for goods:

,less than £873 in value and

,less than 1000kg and

,not dutiable or restricted.

This CPC must not be used for bulking of multi consignments shipped to multi consignees

under standard NES.

2. Notice Memorandum of Understanding arrangements require the express/fast parcel operator to

fulfil specific roles and conditions set out by HMRC. Express/Fast parcel operators who are

approved CSE or SDP Operators and can fulfil the requirements set out in the MOU can

apply by contacting the Express Industry Team in Cardiff on Tel: 03000 523 318 for

further information and advice.

3. Status of Goods T2 - goods in free circulation and not subject to any other regime controls

4. Specific Fields in the declaration/notes Full details can be found in the data requirements provided to NES MOU approved traders.

on completion

5. Additional documents required —

6. Security required —

1.2.18/1 Customs Tariff Vol 311—29

.

VOLUME 3 APPENDIX E1

PPSysB

Rev 18.02 PageLayout: CEX002 [E] Page: 30 Processed: 10-01-2018 10:22:49 Job: TARIFC Unit: PG11

Volume 3

Appendix E 1

7. Additional information The MOU requires a pre-shipment declaration (IESP) to CHIEF.

8. Pre-entry action Goods to be presented to customs at approved locations. The authorised operator’s system

holding the information on the goods to be subjected to the variable tests agreed with the

authorised operator under the MOU. Goods selected by the variable tests for customs

examination must be presented to customs in accordance with the authorised procedure.

9. Post-export action A supplementary declaration (IESD) must be made electronically to CHIEF using CPC 10 00

007 within 14 calendar days of the “goods departed message”.