Executive_summary__30 11 Pharmax IPR 3000 Wg Pharma2902

User Manual: IPR 3000

Open the PDF directly: View PDF ![]() .

.

Page Count: 178 [warning: Documents this large are best viewed by clicking the View PDF Link!]

i

EXECUTIVESUMMARY

TheIndianpharmaceuticalIndustryhaswitnessedarobustgrowthofaround14%since

thebeginningofthe11thPlanin2007fromaboutRs71000crorestooverRs1laccrores

in2009‐10comprisingsomeRs62,055croresofdomesticmarketandexportsofoverRs

42,154crores.Thisalsoamountstoaround20%oftotalvolumeofglobalgenerics.

However,theIndustryisquitefragmentedandcomprisesofnearly10,500unitswith

majorityoftheminunorganizedsector.Ofthese,about300‐400unitsarecategorizedas

belongingtomediumtolargeorganizedsectorwiththetop10manufacturersaccounting

for36.5%ofthemarketshare.AsregardstheBulkdrugscomponentoftheindustry,the

marketisaroundRs42,000croresgivingitashareofaround50%ofthetotaldomestic

market.ThisgivestheIndianBulkDrugindustryashareofabout9%oftheglobalbulk

drugmarket.

Indiaisamongthetop20pharmaceuticalexportingcountriesandtheexportshave

grownverysignificantlyataCAGRofaround19%inthe11thplanperiod.Indiandrugs

areexportedtoaround200countriesintheworldwithhighlyregulatedmarketsofUSA,

UKetc.Themajortherapeuticcategoriesofexportareantiinfective,antiasthmaticand

antihypertensive.

TheDepartmentofPharmaceuticalshasaVisionforthedevelopmentoftheIndian

PharmaceuticalIndustry.ThisVisionis–

“TomakeIndiatheLargestGlobalProviderofQualityMedicinesatReasonablePrices.”

TheVisionistobeachievedasperthefollowingMission:

• DevelopHumanResourcesforPharmaceuticalIndustryandDrugResearchand

Development

• PromotePublic‐PrivatePartnershipfordevelopmentofpharmaceuticalsIndustry

• PromotePharmaBrandIndiathroughInternationalCooperation

• PromoteenvironmentallysustainabledevelopmentofPharmaceuticalIndustry

• Enableavailability,accessibilityandaffordabilityofdrugs

ii

InordertorealisetheMission,theDepartmenthassetthefollowingGoalsfor12thplan:

• ProductionsizeofUS$60bnandexportsizeofoverUS$25bn.

• UpgradationofSMEstoWHO‐GMPandtrainingofprofessionalstherein.

• EstablishmentofPharmaGrowthClusters.

• FacilitategrowthofCentralpharmaPSUs.

• DevelopPharmaInfrastructureandCatalyzeDrugDiscoveryandInnovation

• DevelopPharmaHumanResourcesthroughincreasedM.PharmaandPh.D

programsinNIPERS

• ProvideInfrastructureandstafffornewNIPERsandstrengthenNIPERMohali

• Open10newNIPERs

• JanAushadiCampaignandimplementationofBusinessPlanforsettingupof3000

JanAushadhiStores(uptoSubdivisionlevelinthecountry)

• IncentivizingPrivateSectorfordevelopmentofnewDrugsfordiseasesendemic

toIndia

FortheachievementoftheseGoals,itisnecessaryfortheIndianPharmaceuticalIndustry

tobecomegloballycompetitivethroughworldclassmanufacturingcapabilitieswith

qualityandcostefficiencyofproductioncapacityandradicalupgradationofresearchand

developmentcapabilitiesfornewdrugsandassociatedactivitieslikeclinicaltrialsand

contractmanufacturing.Thereisneedtodevelopworldclasssupportinfrastructure

bothforproductionandresearch.

Withthisapproach,thepreparationofthe12thPlaninvolvedadetailedSWOTanalysisof

theIndianPharmaceuticalsIndustry.Thisanalysishasrevealedthefollowingstrengths:

(a)StrongLowcostmanufacturingsector(b)Significantbreadthanddepthofproduct

expertise(c)LowcostofgrowingHumanresourcesinthePharmasector.Themajor

weaknessesare–(a)Highemphasisongenericsbothfordomesticandinternational

marketswherefilingandapprovalofANDAsandDMFshaveleftlittleroomforR&Don

drugsdevelopment(b)InadequateR&DInfrastructure(c)PoorIndustry‐Academia

linkage(d)Lackofrequiredhigh‐endproductdevelopmentcapablehumanresources(e)

Lackoftimedrivenregulatoryinfrastructure(f)PoorSMEbaseforhigh‐endmanufacture.

Themajoropportunitiesavailableare‐(a)GlobalopportunityforincreasingGenericsand

iii

bio‐genericsmarketbothindevelopedandemergingcountriesduetopressureon

budgetarylimitationsofthesecountriesaswellasemergentpatentcliffduetooff‐

patentingofmajorhigh‐valuedrugs(c)Lowcostgoodskilldestinationforcontract

researchandmanufacturingandresultantopportunitiesindrugdiscoveryaswellas

clinicaltrials(d)Highgrowthofdomesticmarketattractingmulti‐nationalsbothfor

brownfieldandgreenfieldinvestmentsinproductionandcapacitybuilding.Thethreats

totheindustryarefrom‐(a)Ever‐greeningstrategyofMNCsfordenyingandlimitingthe

patentcliffopportunitieswithdebatablerecoursetoTRIPsandFTAs(b)Increasingly

stringentregulatoryandnon‐tariffbarrierstogenericsmarketsindevelopedcountries(c)

Increasedcompetitionforgenericsandbio‐genericsproductionintermsofhighcapacity

andproductioncosts(d)High‐entrybarrierstoenablemarketshareindevelopmentof

newdrugs.

BasedontheaboveSWOTanalysis,recommendationshavebeenmadeinthe12thPlan

Documentfor–

1) DevelopmentandgrowthoftheIndustry

2) StrengtheningofR&DCapabilities

3) StrengtheningofhumanresourcebaseforIndustry

4) AffordabilityandAccesstoQualityDrugs

ThemajorrecommendationsconcerningsupportforIndustrygrowthare‐(a)Schemes

forUpgradationofSMEstoWHO‐GMP,USFDA/EDQM/TGAandotherInternational

Standards(b)Supportfornewgenericsandbio‐genericsthroughsettingupof

FormulationDevelopmentCentersandManufacturingStandardsTrainingCenters(c)

Regionalcluster‐basedIndustrydevelopmentthroughestablishmentandupgradationof

10PharmaGrowthAreaClusters(d)IndustrysupporttoInternationalmarketaccess

throughcapacitybuildingandinter‐governmentalcooperation.TheMedicalDevice

IndustryisalsoproposedtobesupportedthroughthedevelopmentofaMedicalDevices

ParkinAhmedabad,Gujarat.

iv

IntheareaofR&Dandhumanresourcedevelopmentthemajorrecommendations

concern(a)settingupofNationalExcellenceCentrescomprisingthreeforResearchand

DevelopmentinPhyto‐pharmaceuticals,Nano‐PharmaceuticalsandBio‐Similars,onefor

settingupofNationalfacilitiesforNewDrugsDevelopmentalongwithanotherforEnd

ToEndLarge‐ScaleAnimalHouseandsettingupofaNationalCentreforR&DinAPIs(b)

SchemesforsupportingR&DinIndustrythroughassistanceforsettingupof

GLP/GCP/AnimalHouseLabSchemes(c)SettingupofPharmaVentureCapitalFundto

fundinnovationsindrugdiscoveryincludingincubatordriventranslationalresearch(d)

PharmaInnovationandInfrastructureDevelopmentInitiativeforR&Dinfrastructure

developmentincludingfundingofprivatesectorinitiativesinPPPmode.Emphasison

supportingextramuralresearchindevelopmentofnewdrugsanddosageformsformass

afflictiondiseaseslikeJE,Chikungunya,TB(resistantstrains),leishmeinasis,malaria,and

therecentlifestylediseaseslikediabetesandCVD,etc.

AsregardsstrengtheningofHumanResourcebase,itisestimatedthatdirect

employmentinPharmaceuticalsIndustryhasincreasedfromabout6.9lacspeoplein

2006to8lacspeoplein2008with20%ofthismanpowerbeingengagedinresearchand

testing.Theprojectedhumanresourcerequirementisaroundanestimated21.5lacsby

2020.BasedonthisitisproposedtofilltheHRrequirementsthroughSchemessuchas

(a)ExpandingthestudentoutputatNIPERMohali(b)Developmentof6NewNIPERS

alreadysanctionedinthe11thPlanand(c)Settingupof10NewNIPERsetc.

The12thPlanDocumenthighlightsthevitalroleDrugpriceplayinaccesstoessential

medicinesacrosstheworld.WhileitisafactthatthedrugsmanufacturedinIndiaare

consideredtobeamongstthelowestpricedinternationally,still,avastsectionofIndian

populationisnotinapositiontoaccesstheneededhealthcareaswellasthemedicines

duetovariousreasonsofaccessandaffordability.Accordingly,therecommendations

madebytheTaskForceunderDr.PronabSenmadehavebeenconsideredandadraft

NationalPharmaceuticalsPricingPolicyhasbeenformulatedwhichseekstocontrolthe

pricesofessentialdrugsaspertheNationalListofEssentialMedicines2011(NLEM‐

2011).Furthertothis,theDepartmentwouldtakeupissuespertainingtoprescription

v

andpromotionofunbrandedgenericdrugswiththeDepartmentofHealth.Issues

relatedtopricingofpatentedmedicineswouldalsobesuitablyconsideredinthelightof

needforpromotingindustrygrowthandresearchaswellasdevelopmentofnewdrugs

alongwithaffordabilityofnewpatentedmedicinesforbettertherapeutictreatmentof

themasses,especiallyindiseasespertainingtocancerandHIV.Accordingly,itis

proposedtocontinueschemesforstrengtheningoftheNPPA,forsuchfunctionsas‐(a)

StrengthenMonitoringandEnforcementWork,(b)BuildingConsumerAwareness

aboutpricingandavailabilityand(c)CreationofNPPACellsinStates,etc.

ThepresentmarketsizeofMedicalDevicesandEquipmentsisaroundRs15,000crores.

ThemedicaldeviceIndustryinIndiaisverynascentandislargelyimportdependent.More

than65%ofIndia’srequirementofmedicaldevicesandequipmentsaremetthrough

importswithdomesticproductionbeinglargelyrestrictedtolowtechnologydisposable

equipments.TheSWOTanalysisofMedicalDeviceIndustryshowsthatitsmajorstrengths

are–(a)WelldevelopedMicroelectronic,Telecommunication,SoftwareandPrecision

EngineeringIndustry,(b)Abilitytoattractforeigninvestmentsand(c)Abilitytohandlelow

valuelargevolumeproductionasperglobalqualitystandards.Themajorweaknessesare–

(a)Lowpercapitaexpenditureonhealthcare&lowhealthinsurance,(b)Lackofadequate

andtrainedmanpower,(c)Lackofincubationandsuitableecosystem,(d)Lackof

regulation/standardsetc.Themajoropportunitiesare‐ (a)Hugemarketpotential,(b)

Growingopportunitiesinexportmarket,(c)Growingdemandonaccountofchanging

demographicprofile,increasingincidencesoflifestylediseaseslikecancer,CNSand

diabetics,etc.Themajorthreatsare–(a)Growingcompetitioninexportmarkets,(b)

Increasingdependencyonimports,(c)Unorganizedmarketformedicaldisposables,(d)

Lackofregulationsinmedicaldisposablesandsurgicalitems.Togiveaboosttothe

MedicaldevicesSector,anumberofschemeshavebeenproposedsuchasfor‐(a)

Settingupgreen‐fieldMedicalDevicesParkand(b)SettingupNationalCenterforR&Din

MedicalDevicesatNIPERAhmedabad

The11thPlanaimedatmakingthesickCPSUsfinanciallyviablethroughsupportfor

modernisationandrehabilitationaswellaswaiverofduesandpaymentofVRSpackages.

vi

Accordingly,HindustanAntibioticsLtd(HAL)andBengalChemicalsandPharmaceuticals

Ltd(BCPL)weregivensupportofoverRs.1000croresinthe11thPlanperiodinvolving

waiver,settlementandcashassistanceformodernisation.KarnatakaAntibioticsand

PharmaceuticalsLtd(KAPL)andRajasthanDrugsandPharmaceuticalsLtd(RDPL)were

alsogivenfinancialsupportfollowingtheirdelinkingfromHALandIDPLrespectivelyso

astomakethemindividuallymoreviableandindependentinpursuinggrowthplans.As

aresult,thePharmaPSUshavebeenabletoachieveacombinedbusinessofmorethan

Rs.600crores.Itisexpectedthattheywouldgrowinthe12thPlanforwhich

Governmentsupportformarketingwillberequired.Accordingly,nomajorschemehas

beenproposed.TherehabilitationofIndianDrugsandPharmaceuticalsLtd(IDPL)could

beconsideredduringthe12thPlanasperapprovaloftheCabinet.

Asregardsaccesstoqualitydrugsataffordableprices,apartfromthepricecontroland

monitoringinitiative,theGovernmentproposestofurtherexpandtheJanAushadhi

Schemestartedinthe11thPlanwiththeobjectiveofmakingavailableunbranded

genericmedicinesataffordablepricesthroughtheproposed3000dedicatedoutlets

acrossthecountry.The12thPlandocumenthassupportedtherevisedbusinessplanof

theJanAushadhiSchemewhichhasbeenpreparedafteradetailedanalysisofshortfalls

andpossiblesolutionsincludingspecialfocusonsupplychainmanagement.

Finally,theDepartmentofPharmaceuticalshasnotbeenabletotakeuporlaunchany

majornewactivityinlinewithitsmandateevenafterthreeyearsofitsexistence.The

mainreasonforthisliesinlackoftechnicalcapabilitysinceitsinception.Thereforethere

isanurgentneedofstrengthentheDepartmentintermsofrequiredhumanresources.

Forthis,supportofatechnicalcadrehasbeenproposed.

Itisexpectedthatgoingforwardinthe12thPlan,theDepartmentwouldbeabletoplaya

vitalcatalyticroleinspurringthegrowthofthepharmaceuticalindustryinthecountry

andstrengthenittobecomeagloballeaderinthecomityofnationsintheglobal

economy.

vii

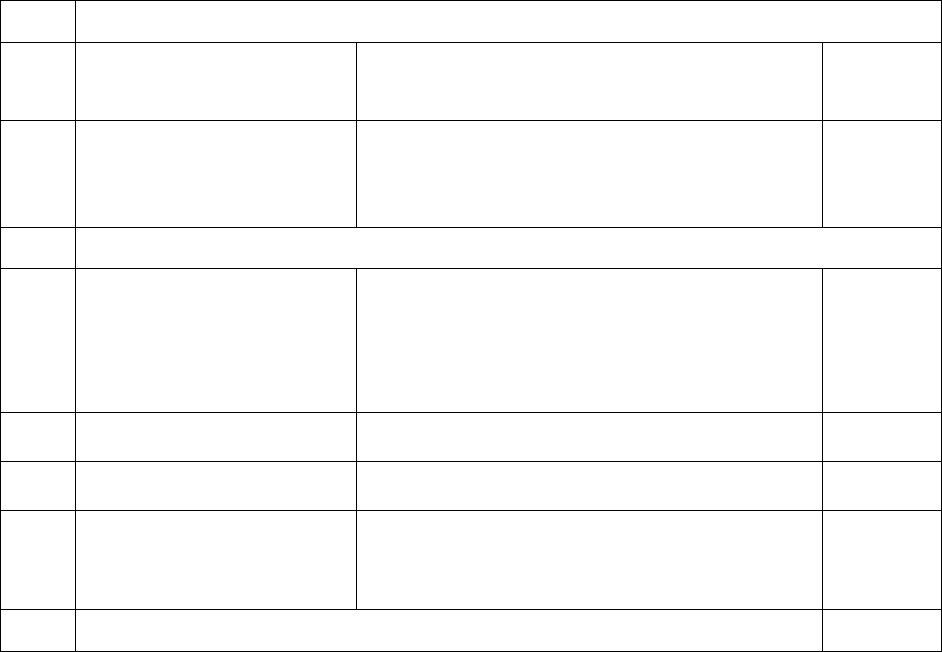

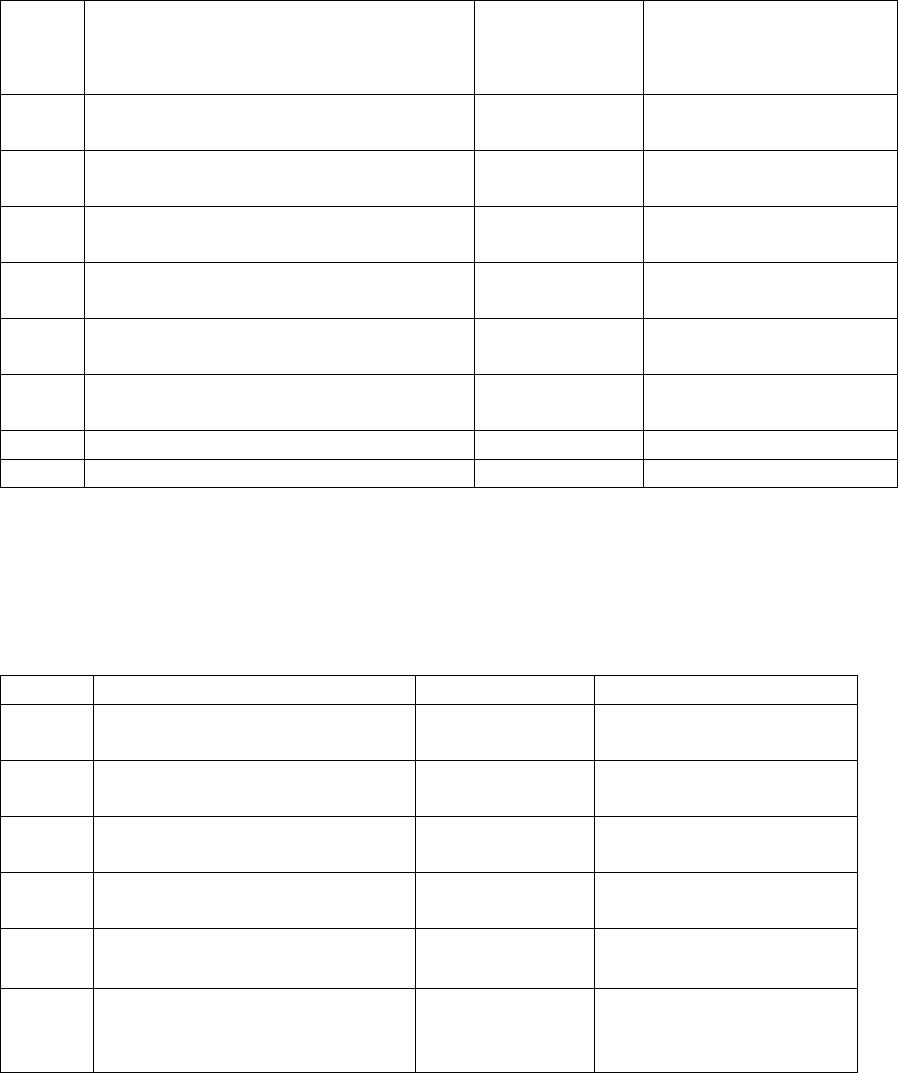

SUMMARYOFSCHEMES

SlNoSchemeBriefdescriptionBudget(Rs

Crores)

1INDUSTRYPROMOTION&DEVELOPMENT

1.1ExistingSchemes–Continued

from11thPlan

(i)PharmaPromotionand

DevelopmentScheme(PPDS)

GrantassistanceforIndustryStudies,Workshops,

Seminars,etc

10

(ii)IntellectualPropertyRights

FacilitationCenters

CapacitybuildingGrantassistance(capitaland

revenue)forsettingupofIPRcentresby

Pharmaexcil,Industrybodies,etctoassistindustryin

IPRmatters

26.5

1.2NewSchemes

(i)InternationalPharma

CooperationInitiative(IPCI)

SettingupofJointtestingandlabfacilitiesfor

certificationofIndianpharmaproducts,

developmentoflocallysustainableformulationsand

drugdeliverysystemsandothermutuallybeneficial

schemes

50

(ii)UpgradationofSMEsto

WHO‐GMPstandards

Interestbasedsubsidyschemeattherateofabout

Rs1crsperunitofassistancetobeimplementedin

partnershipwithIDBI/SIDBIforupgradingSMEsto

WHO‐GMPmanufacturingstandardstocapitalizeon

theGenericsOpportunity–about1200unitsoutof

about10,563SMEsinthecountry

1200

(iii)Capacitybuildingthrough

trainingof5000Working

ProfessionalsinWHO‐GMP

Toprovidemanufacturingcapabilityupgradation

assistanceforcapitalexpenditure,skilldevelopment

ofpersonnelrequiredforsuchupgradationand

sustenanceofsupplyofskilledpersonnel.

250

(iv)UpgradationofSMEsto

USFDA/EDQM/TGAandother

InternationalStandards

SpecificassistanceforstandardshigherthanWHO‐

GMPtoselectedSMEs–250innostobuild

Competitivenessofveryhighstandardsandsecond

lineofinternationallycapableindustryforhighvalue

pharmaproductsforstrongregulatedbuthighvalue

markets

500

(v)SettingupofoneNational

andfiveRegionalFormulation

Developmentand

Manufacturingstandards

trainingcentres

SchemetosetupFormulationdevelopmentcentres

totapthepatentcliffopportunityandbecome

globalleaderinGenericsandBio‐similars

160

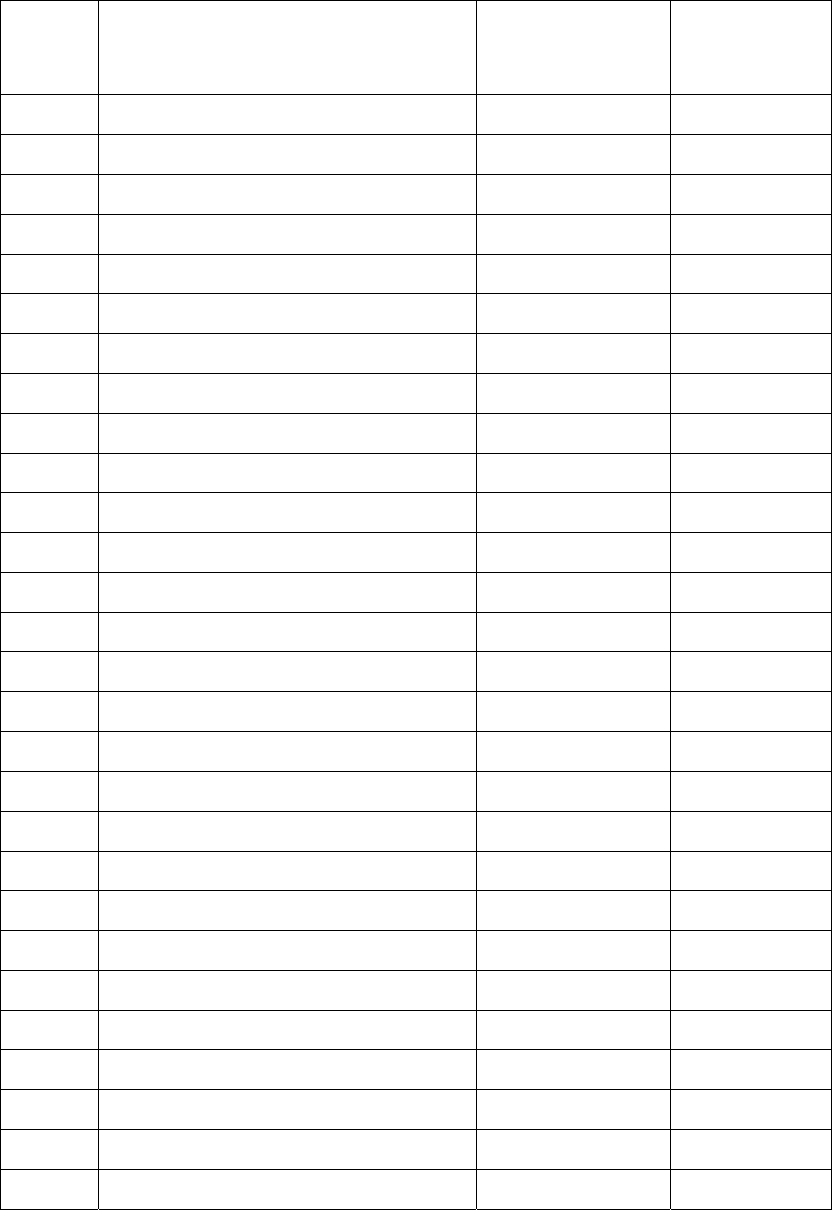

viii

(vi)Establishmentand

upgradationof10Pharma

GrowthClusters

Infrastructurebuildingforpharmaindustry

particularlyforSMEs–buildingonstrengthof

existingClusterssoastoprovideinfrastructuregaps

forhigherproductionincludingtakingcareof

environment,powerandlabstesting,etcneeds.

500

(vii)Infrastructuresupportfor

ColdChainforhighenddrugs

forexports

Inordertoenhanceexportscapabilityforhighend

drugsrequiringexactcoldchainstandardstillthe

timetheyareexportedfromthecountryinlightof

stringentdevelopedmarketrequirements

50

(viii)Schemeforenvironment

standardscomplianceand

requiredinfrastructure

supportincludingcapacity

building

providingfinancialandtechnicalassistanceto

improvefinancialsustainabilityofSMEsonone

handandalsosafeguardtheenvironmentfrom

thehazardsassociatedwiththeunplanned

growthoftheindustry.

100

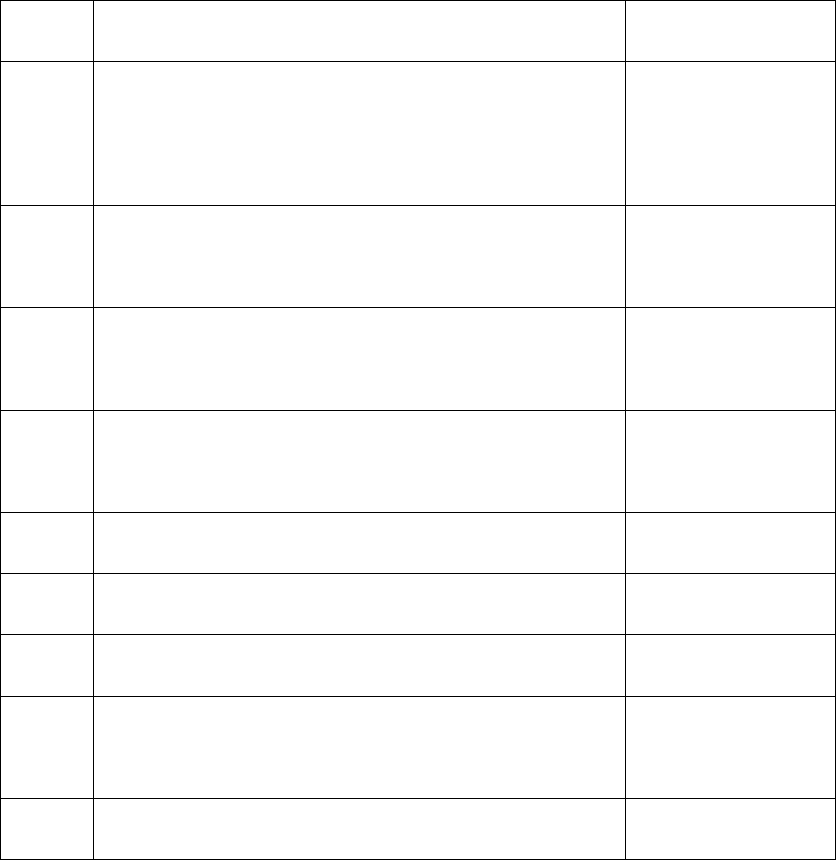

2R&D,CAPACITYBUILDINGANDEMPLOYMENT

2.1ContinuingSchemes

2.1.1ForNIPERMohali

(i)ThecontinuationofthePG

andthePhDeducation

ThecontinuationofthePGandthePhDeducation

atpresentstrengthlevelswouldrequirebudgetary

support

100

(ii)CapacityEnhancementfor

supportingrequiredindustry

humanresourcesandcapacity

buildingrequirementbythe

Institute

a. Additional1000PGsandPhDs

b. TrainingIndustryandRegulatorypersonnel

c. PublicHealthandPharmacovigilanceTrg.

d. InfrastructureUpgradation

200

25

25

250

2.1.2ForNewNIPERs

(i)Permanentestablishmentand

operationof6NewNIPERs

2000

2.1.3OtherSchemes

(i)SettingupofNationalCenter

forPhyto‐pharma

development

MajorcapitalexpenditureofaboutRs100crsbeing

metfromDONER.Presentallocationsoughtfor

initialyearsoperationasperadvicefromDONER

20

(ii)GLP/GCP/AnimalHouseLab

Schemes

ForsettingupofGLPcompliantLabs,GCPcompliant

LabandaAnimalHouseLabonPPPbasisisunder

implementation

50

ix

(iii)ContinuingR&DSchemesFor

NiperMohali

NiperMohaliispresentlyimplementinganumberof

projectsinR&Dforvariouspharmaareaslike

neglecteddiseases,infectiousdiseases,vectorborne

diseases,etc.Inadditionanumberofprojectsare

beingimplementedforPublichealth,

PHarmacovigilance,Regulatorycapacitybuildingfor

academiaandindustry,etc.

50

(iv)ContinuingschemeatNew

Nipers

JointdevelopmentofTuberculosisrelateddrugsat

NiperAhmedabadandAIIMS,Delhi

1

2.2NewSchemes

(i)EstablishmentofNewNew

NIPERs

Inordertomeetthegapofaverylowgraduateto

postgraduatepharmaeducationseatscapacityof

1:10(51000graduateseatsvs5100PGseatsinthe

entirecountry)thereisneedtosetupfurthernew

Nipersapartfromthe6approvedinthe11thplan.It

isproposedtosetup10NewnewNIPERs

3000

(ii)NewSchemesatNiperMohali R&DCentreforBiologicalsandNCEsR&DCentrefor

NDDS,Settingup20NewIncubators,Incentive

SchemeforCROsDevptforNew,DrugDiscovery

PartnershipwithInternationalCentresofExcellence

825

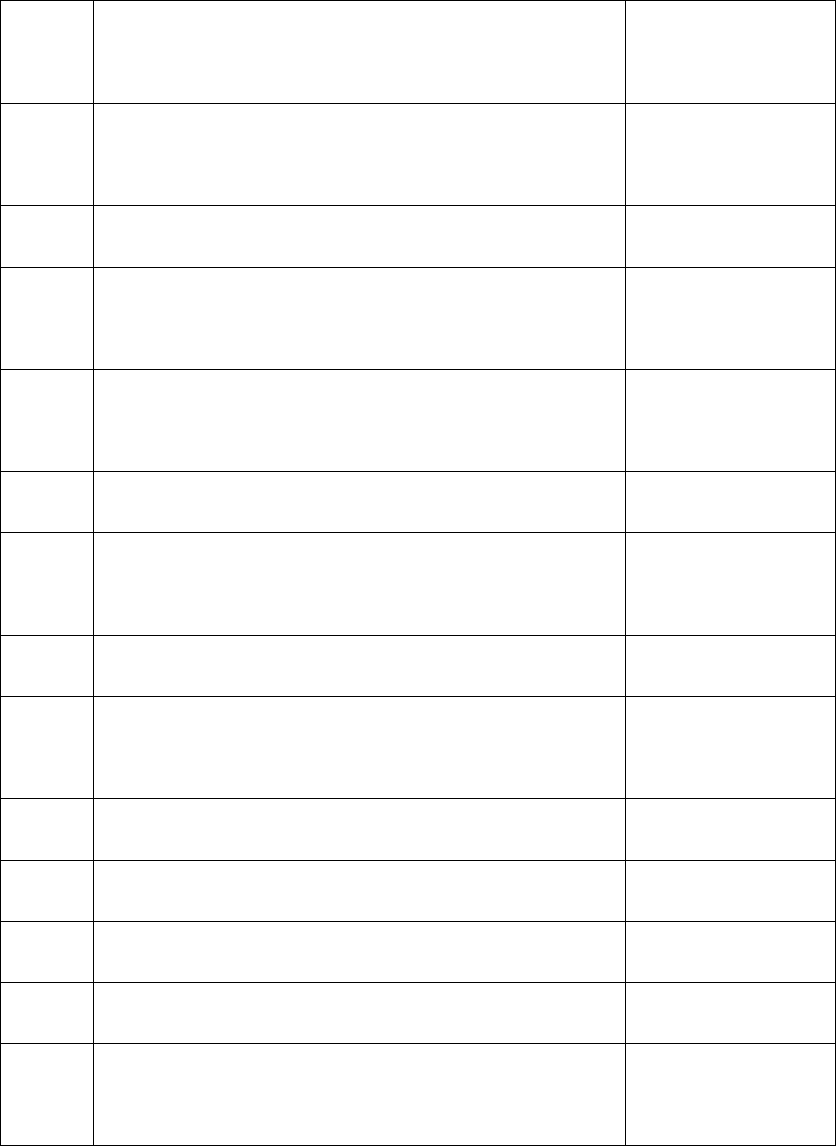

(iii)PharmaVentureCapitalFundToconsiderinvestmentofidentifiedfundsintoa

newlycreatedspecialisedprivateequity/venture

capitalfundthatundertakesR&Dinvestmentsinto

companiesinthepharmaceuticalindustry

500

(iv)PharmaInnovationand

InfrastructureDevelopment

Initiative(PIIDI)

Developtechnicalandinnovationcapacityof

Indianpharmaformanufacturingquality

affordablemedicines,developInternational

competitivenessoftheIndianPharmasoasto

bethelargestproducerofgenericmedicinesin

theworld,TomakeIndiaapreferred

destinationforglobalinitiativesincuringthe

world’sailmentsspeciallythedevelopingworld

inavaluebasedmanner

2000

(v)AtNIPERHyderabad:Setting

upNationalCenterforR&Din

BulkDrugsatNIPER

Hyderabad

BuildcompetitivenessthroughInnovationand

ProductivityefficienciesintheAPIindustry.Alsotap

Genericsopportunityandmeetcompetitionof

China,etc.

56

x

(vi)AtNIPERKolkattaNational

Pharmaceutical

NanotechnologyCenter

TobesetupatNIPERKolkattafordevelopmentof

Nano‐materialsfrominorganicsubstratesfor

innovativedrugsanddrugdeliverysystems

50

(vii)SettingupNationaland

RegionalBiosimilarExpertise

Centers

Toprovideexpertadviceandassistancetoindustry

onregulatoryissuespertainingtoClinicalTrials,

TestingandApprovalprocessforBiosimilars–One

nationalcentreatBangaloreand3regionalcentres

atChandigarh,HyderabadandAhmedabad

60

(viii)SettingupofaIndustry

focusedAnimalHouse

EndtoendservicesfromPrimatestosmallanimals

forpre‐clinicaldrugdevelopment

100

(ix)SupporttoAcademia,

ResearchInstitutionsand

privatesectorforExtraMural

Research

Forfundingbothacademiaindividually,asan

institutionandprivatecompaniesfortargeted

drugdevelopmentincludingassistancefor

clinicaltrials.

100

(x)SupporttoAcademia,

ResearchInstitutionsand

privatesectorforExtra

Labsupgradation

Forfundingupgradationoflabsintheprivateand

governmentsectorwithsharingbasison50‐50

patternforthelabupgradationforequipments

deployedfordrugdevelopmentunderspecifically

identifiableprojects

10

(xi)AllNIPERs:International

cooperationinR&D

TopromoteR&DinCISanddevelopingcountriesfor

mutualadvantages

25

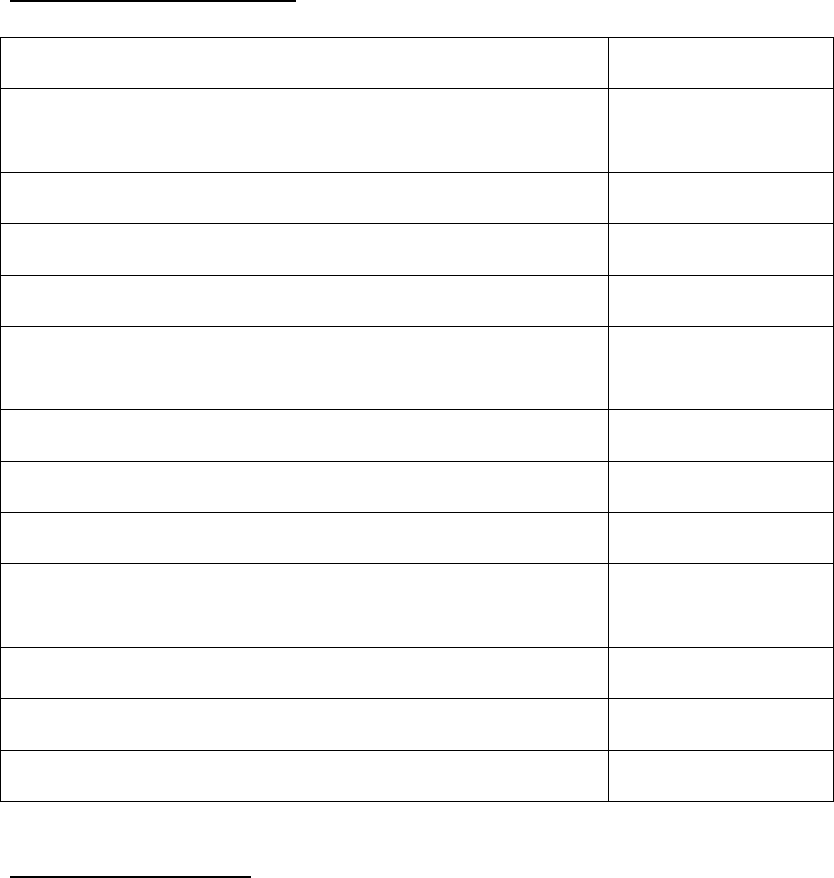

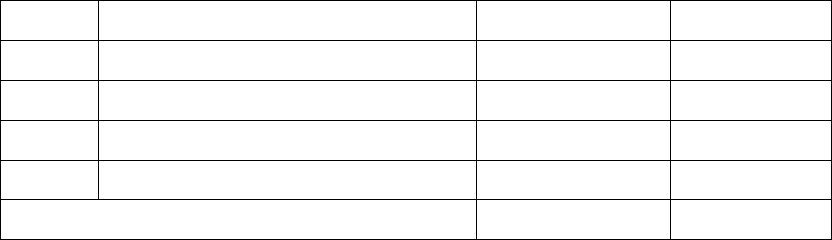

3Pricing

3.1Continuingschemes

(i)MonitoringandEnforcement

Work

StrengtheningtheExistingMonitoringand

EnforcementWork

2

(ii)AwarenessandPublicitytConsumerAwarenessandPublicitythroughPrint,

ElectronicandotherMedium

20

3.2NewSchemes

(i)CreationofNPPA‐State

GovernmentCoordination

CellsinStates

Schemeoriginallyproposedin11thPlanbutnot

approvedbyPlanningCommission.Henceproposed

for12thPlan.Willhelpinstrengtheningthe

MonitoringObjectiveofdrugsprices.

25

(ii)SchemeforInteractionwith

States

Schemeoriginallyproposedin11thPlanbutnot

approvedbyPlanningCommission.Henceproposed

for12thPlan.Willhelpinstrengtheningthe

MonitoringObjectiveofdrugsprices.

2

xi

4MedicalDevicesindustrydevelopment

(i)Settingupgreen‐fieldmedical

devicesandequipmentparks.

TappingtheopportunityUS$200Bnglobalindustry300

(ii)SettingupNationalCenterfor

MedicalDevicesatNIPER

Ahmedabad.

PromotingindigenousR&DinMedicaldevicessector50

5CPSUsandJanAushadhi

(i)IDPL

Tokenallocationforminimalregulatory

compliances.Actualwoulddependontheapproval

byCabinetforrevivalofIDPLpackage

10

(ii)HAL MinimalUpgradationoffacilities 10

(iii)BCPLMeetinggapsintherevivalpackage 10

(iv)JanAushadhiContinuingschemetobestrengthenedinthe12th

planforensuringaccesstoaffordablequality

unbrandedgenericmedicinesforthepoormasses

200

TOTAL12922.5

xii

METHODOLOGY

(A) ConstitutionofWorkingGroup

PlanningCommissionconstitutedaworkinggrouponDrugsandPharmaceuticals,videtheir

letternoI&M‐3(25)/2011,dated10.5.2011.

(a)TermsofReference(TOR)oftheWorkingGroup

TheworkinggroupwasgivenfollowingTermsofReference:

i. Toarticulatethelongtermgoalstobeachievedintermsofgrowth,

competitivenessandshareinglobaltradeforthedomesticDrugs&

PharmaceuticalIndustries.

ii. ToreviewthecurrentstatusofdomesticPharmaceuticalsSectorhighlightingthe

achievementsduringthe11thPlanandreasonsformajordeviation/shortfall,if

any,inrespectoffulfilmentoftargetsandidentifyingareasofstrengthand

weaknessoftheIndianindustryvis‐à‐visinternationalDrugsand

PharmaceuticalsIndustry.

iii. Tobenchmarkindigenousdrugs&pharmaceuticalsindustryagainstinternational

drugs&pharmaceuticalsindustryandsuggestappropriatemeasuresforbridging

thegapswherenecessary,includingtheneedsforfurtherR&Dactivitiesand/or

technologycollaborationforupgradingtechnology.

iv. Toexaminethestructureandcapabilityofthedomesticdrugs&pharmaceutical

industry,itsexporttrend&performanceandidentifyemergingareashaving

specificpotentialforgrowthandcompetitivenessaswellastosuggestmeasures

forputtingtheindigenousindustryonsoundfootingandgrowthpathkeepingin

viewthegoalstobearticulatedunderitem1above.

v. ToreviewthepresentstatusofWHO‐GMP(WorldHealthOrganization–Good

ManufacturingPractice)certificationandschedule‐Mcomplianceandsuggest

measuresforraisingthelevelofcompliancebymanufacturersofdrugsand

pharmaceuticalproductsinthecountry.

xiii

vi. Toexaminetheimpactofnewpatentregimeondomesticpharmaceutical

industryincludingitsimplicationondrugprices.

vii. Tostudytheefficacyandappropriatenessofcurrentdrugpricingsystemaswell

asitscontrolandenforcementmechanismandsuggestmeasuresforfurther

improvement,ifapplicable.

viii. Toassessthepresentcapabilityforinnovationvis‐à‐visR&Dstatusofthe

domesticDrugs&Pharmaceuticalsindustryandtosuggestwaysandmeansto

improvethedomesticefforts,enhanceindustryparticipationandintensify

Industry‐Institutional/academialinkagetopromotedomesticR&Dfor

establishmentofitsinternationalcompetitivenessandmeetingtheemerging

challengesarisingoutoftheWTOregime.

ix. Tostudychangeinstructureofdomesticpharmaceuticalsindustryinthelightof

currenttrendofmerger&acquisitions/takeovers/collaborationsandits

correlationwithrelatedFDInormsandsuggestmeasurestosafeguardnational

interests.

x. ToexaminethetrendofemploymentgrowthintheDrugsandPharmaceuticals

industryandprojectlikelyrequirementofskilledmanpowerduringtheTwelfth

Planperiodaswellastomeetthelongtermgoals.Tosuggestmeasuresfor

puttinginplaceadequateacademicandtraininginfrastructureandfacilitiesto

meettherequirements.

xi. Toassesstheadequacyandrelevanceofpresentregulatorymechanismofdrug

andpharmaceuticalssectorandexamineneedforfurtherstrengtheningtotackle

themenaceofspuriousdrugsetc.andexamineneedforanapexauthorityto

controlprice,qualityandsupplyofdrugs.

xii. Tosuggestmeasurestowardsimprovementofaccessibilityofessential

medicinesforcommonmanparticularlythepoorersectionsofthepopulation

andtoidentifystepsrequiredforfacilitatingimplementationoftheNational

HealthPolicy.

xiii. Toassessthecurrentstatusofdomesticmedical/surgicalequipmentindustry,its

exportpotentialandcompetitivenessandsuggestmeasuresforimprovement

andaugmentationofcapabilities,wherenecessary.

xiv

xiv. Toindicatethemilestonestobeachievedinthe12thPlaninthecontextoflong

termgoalsasperitem‐IoftheToRandrecommend

pogrammes/schemes/measuresthataretobeinitiated,continuedor

discontinuedinthe12thPlanperiodandestimatedfundrequirement.

xv. Tomakeanyotherrecommendationsasmaybeappropriateforsustained

growthandcompetitivenessofthesector.

(b)MembersoftheWorkingGroup

Theworkinggroupconsistedoffollowingmembers:

1.Secretary,DepartmentofPharmaceuticals(DOP) Chairman

2.Secretary,DepartmentofScientific&Industrial

Research/DG,CouncilofScientific&Industrial

ResearchorhisRepresentative

Member

3.PrincipalAdviser/Adviser(Health),Planning

Commission

Member

4.Secretary,MinistryofHealth&FamilyWelfareor

Nominee

Member

5.Secretary,DepartmentofScience&Technologyor

Nominee

Member

6.Secretary,DepartmentofBio‐TechnologyorNominee Member

7.Secretary,DepartmentofConsumerAffairsorNominee Member

8.Chairman,NationalPharmaceuticalPricingAuthority Member

9.AdditionalSecretary&FinancialAdviser,Department

ofPharmaceuticals(DOP)

Member

10.Adviser(I&VSE),PlanningCommission Member

xv

11.JointSecretary(PI),DepartmentofPharmaceuticals

(DOP)

Member

12.JointSecretary(Pharma),Departmentof

Pharmaceuticals(DOP)

Member

13.Director,CentralDrugsResearchInstitute,Lucknow Member

14.Director,NationalInstituteofPharmaceutical

Education&Research,Mohali,Punjab

Member

15.Chairman,PharmaceuticalsExportPromotionCouncil,

Hyderabad

Member

16.President,IndianDrugsManufacturesAssociation Member

17.Chairman,ConfederationofIndianPharmaceuticals

Industry

Member

18.SecretaryGeneral,IndianPharmaceuticalsAlliance Member

19.President,OrganisationofPharmaceuticalsProducers

ofIndia(OPPI)

Member

20.President,BulkDrugManufacturersAssociation Member

21.Chairman,Dr.Reddy’sLaboratoriesLtd.,Hyderabad Member

22.Chairman,CIPLALimited,Mumbai Member

23.Chairman,LupinLimited,Mumbai Member

24.EconomicAdviser,DepartmentofPharmaceuticals

(DOP)

Member

xvi

(B) ConstitutionofSubWorkingGroups

BasedonthethrustoftheToRs,DepartmentofPharmaceuticalsconstitutedfoursub

workinggroups.ThemembersandToRsofthesubworkinggroupsareasbelow:

(a) Sub‐GrouponStatusandStructureofthePharmaceuticalIndustry

CompositionoftheSub‐Group

1.JointSecretary(AJ),DepartmentofPharmaceuticals Chairman

2.NomineeofSecretary,DepartmentofScientific&Industrial

Research

Member

3.NomineeofSecretary,MinistryofHealth&FamilyWelfareMember

4.NomineeofSecretary,DepartmentofScience&Technology Member

5.Adviser(I&VSE),PlanningCommission Member

6.Chairman,PharmaceuticalExportPromotionCouncil,

Hyderabad

Member

7.President,IndianDrugsManufacturersAssociation Member

8.Chairman,ConfederationofIndianPharmaceuticalsIndustry Member

9.SecretaryGeneral,IndianPharmaceuticalsAlliance Member

10.President,OrganisationofPharmaceuticalsProductsof

India(OPPI)

Member

11.President,BulkDrugManufacturersAssociation Member

12.DeputyDirectorGeneral,DepartmentofPharmaceuticals Member

13.Director(BKS)MemberSecretary

TermsofReference(TOR)

(i) Toarticulatethelongtermgoalstobeachievedintermsofgrowth,

competitivenessandshareinglobaltradeforthedomesticDrugs&

PharmaceuticalIndustries.

xvii

(ii) ToreviewthecurrentstatusofdomesticPharmaceuticalsSectorhighlightingthe

achievementsduringthe11thPlanandreasonsformajordeviation/shortfall,if

any,inrespectoffulfilmentoftargetsandidentifyingareasofstrengthand

weaknessoftheIndianindustryvis‐à‐visinternationalDrugsand

PharmaceuticalsIndustry.

(iii) Tobenchmarkindigenousdrugs&pharmaceuticalsindustryagainstinternational

drugs&pharmaceuticalsindustryandsuggestappropriatemeasuresforbridging

thegapswherenecessary,includingtheneedsforfurtherR&Dactivitiesand/or

technologycollaborationforupgradingtechnology.

(iv) Toexaminethestructureandcapabilityofthedomesticdrugs&pharmaceutical

industry,itsexporttrend&performanceandidentifyemergingareashaving

specificpotentialforgrowthandcompetitivenessaswellastosuggestmeasures

forputtingtheindigenousindustryonsoundfootingandgrowthpathkeepingin

viewthegoalstobearticulatedunderitem1above.

(v) Tostudychangeinstructureofdomesticpharmaceuticalsindustryinthelightof

currenttrendofmerger&acquisitions/takeovers/collaborationsandits

correlationwithrelatedFDInormsandsuggestmeasurestosafeguardnational

interests.

(vi) Toassessthecurrentstatusofdomesticmedical/surgicalequipmentindustry,its

exportpotentialandcompetitivenessandsuggestmeasuresforimprovement

andaugmentationofcapabilities,wherenecessary.

(vii) Toindicatethemilestonestobeachievedinthe12thPlaninthecontextoflong

termgoalsasperitemIoftheToR(ByPlanningCommission)andrecommend

pogrammes/schemes/measuresthataretobeinitiated,continuedor

discontinuedinthe12thPlanperiodandestimatedfundrequirement.

(viii) Tomakeanyotherrecommendationsasmaybeappropriateforsustained

growthandcompetitivenessofthesector.

xviii

(b) Sub‐GrouponRegulatoryIssuesinthePharmaceuticalIndustry

CompositionoftheSub‐Group

1.JointSecretary(DC),DepartmentofPharmaceuticals Chairman

2.NomineeofSecretary,MinistryofHealth&FamilyWelfareMember

3.NomineeofSecretary,DepartmentofScience&TechnologyMember

4.NomineeofSecretary,DepartmentofBio‐TechnologyMember

5.PrincipalAdvisor/Advisor(Health)orNominee,Planning

Commission

Member

6.DrugControllergeneralofIndia/NomineeMember

7.President,IndianDrugManufacturersAssociation Member

8.Chairman,ConfederationofIndianPharmaceuticalsIndustry Member

9.SecretaryGeneral,IndianPharmaceuticalsAlliance Member

10.President,OrganisationofPharmaceuticalsProductsof

India(OPPI)

Member

11.President,BulkDrugManufacturersAssociation Member

12.Director(MV),DepartmentofPharmaceuticals MemberSecretary

TermsofReference(TOR)

i. ToreviewthepresentstatusofWHO‐GMP(WorldHealthOrganization–Good

ManufacturingPractice)certificationandschedule‐Mcomplianceandsuggest

measuresforraisingthelevelofcompliancebymanufacturersofdrugsand

pharmaceuticalproductsinthecountry.

xix

ii. Toassesstheadequacyandrelevanceofpresentregulatorymechanismofdrug

andpharmaceuticalssectorandexamineneedforfurtherstrengtheningtotackle

themenaceofspuriousdrugsetc.andexamineneedforanapexauthorityto

controlprice,qualityandsupplyofdrugs.

iii. Toindicatethemilestonestobeachievedinthe12thPlaninthecontextoflong

termgoalsasperitemIoftheToR(ByPlanningCommission)andrecommend

pogrammes/schemes/measuresthataretobeinitiated,continuedor

discontinuedinthe12thPlanperiodandestimatedfundrequirement.

iv. Tomakeanyotherrecommendationsasmaybeappropriateforsustained

growthandcompetitivenessofthesector.

(c)Sub‐GrouponPricingandAvailabilityofDrugs

CompositionoftheSub‐Group

1.Chairman,NationalPharmaceuticalPricingAuthority Chairman

2.NomineeofSecretary,MinistryofHealth&FamilyWelfareMember

3.NomineeofSecretary,DepartmentofConsumerAffairsMember

4.Adviser(I&VSE),PlanningCommission Member

5.MemberSecretary,NPPAMember

6.SecretaryGeneral,IndianPharmaceuticalsAlliance Member

7.President,OrganisationofPharmaceuticalsProductsofIndia

(OPPI)

Member

8.President,IndianDrugsManufacturersAssociation Member

9.Chairman,ConfederationofIndianPharmaceuticalsIndustry Member

10.President,BulkDrugManufacturersAssociation Member

11.Director(Monitoring),NPPAMemberSecretary

xx

TermsofReference(TOR)

i. Toexaminetheimpactofnewpatentregimeondomesticpharmaceutical

industryincludingitsimplicationondrugprices.

ii. Tostudytheefficacyandappropriatenessofcurrentdrugpricingsystemaswell

asitscontrolandenforcementmechanismandsuggestmeasuresforfurther

improvement,ifapplicable.

iii. Tosuggestmeasurestowardsimprovementofaccessibilityofessential

medicinesforcommonmanparticularlythepoorersectionsofthepopulation

andtoidentifystepsrequiredforfacilitatingimplementationoftheNational

HealthPolicy.

iv. Toindicatethemilestonestobeachievedinthe12thPlaninthecontextoflong

termgoalsasperitemIoftheToR(ByPlanningCommission)andrecommend

pogrammes/schemes/measuresthataretobeinitiated,continuedor

discontinuedinthe12thPlanperiodandestimatedfundrequirement.

v. Tomakeanyotherrecommendationsasmaybeappropriateforsustained

growthandcompetitivenessofthesector.

(d)Sub‐GrouponR&D,TrainingandEmploymentGenerationinthePharmaceutical

Industry

CompositionoftheSub‐Group

1.Director,NIPER,Mohali,Punjab Chairman

2.NomineeofDG,CouncilofScientific&IndustrialResearchMember

3.NomineeofSecretary,DepartmentofScience&TechnologyMember

4.NomineeofSecretary,DepartmentofBio‐TechnologyMember

xxi

5.ProjectDirector,NIPER,Hyderabad Member

6.Director,CentralDrugsResearchInstitute,Lucknow Member

7.SecretaryGeneral,IndianPharmaceuticalsAlliance Member

8.President,OrganisationofPharmaceuticalsProductsofIndia

(OPPI)

Member

9.Chairman,Dr.Reddy’sLaboratoriesLtd.,Hyderabad Member

10.Chairman,CIPLALimited,Mumbai Member

11.Chairman,LupinLimited,Mumbai Member

12.DeputyDirectorGeneral,DepartmentofPharmaceuticals. Member

13.Director(SCS),DepartmentofPharmaceuticals MemberSecretary

TermsofReference(TOR)

i. Toassessthepresentcapabilityforinnovationvis‐à‐visR&Dstatusofthe

domesticDrugs&Pharmaceuticalsindustryandtosuggestwaysandmeansto

improvethedomesticefforts,enhanceindustryparticipationandintensify

Industry‐Institutional/academialinkagetopromotedomesticR&Dfor

establishmentofitsinternationalcompetitivenessandmeetingtheemerging

challengesarisingoutoftheWTOregime.

ii. ToexaminethetrendofemploymentgrowthintheDrugsandPharmaceuticals

industryandprojectlikelyrequirementofskilledmanpowerduringtheTwelfth

Planperiodaswellastomeetthelongtermgoals.Tosuggestmeasuresfor

puttinginplaceadequateacademicandtraininginfrastructureandfacilitiesto

meettherequirements.

iii. Toindicatethemilestonestobeachievedinthe12thPlaninthecontextoflong

termgoalsasperitem‐IoftheToR(ByPlanningCommission)andrecommend

xxii

pogrammes/schemes/measuresthataretobeinitiated,continuedor

discontinuedinthe12thPlanperiodandestimatedfundrequirement.

iv. Tomakeanyotherrecommendationsasmaybeappropriateforsustained

growthandcompetitivenessofthesector.

AstheToRswerehavingnomentionofCentralPublicSectorUndertakings(CPSUs)inthe

DepartmentofPharmaceuticals,itwasdecidedtohaveasubgrouponCPSUsalso.

Thesubgroupconsistedoffollowingmembers

1.JointSecretary(DC),DepartmentofPharmaceuticals Chairman

2.CMD,IDPLMember

3.MD,HALMember

4.MD,KAPLMember

5.MD,BCPLMember

6.UnderSecretary(ShriA.K.Sah) MemberSecretary

TheToRsofthesubgroupareasbelow:

i.Toarticulatethelongtermgoalstobeachievedintermsofgrowthand

competitivenessofPharmaPSUs.

ii.Toindicatethemilestonestobeachievedinthe12thPlaninthecontextoflongterm

goalsasperitem(i)aboveandrecommendprogrammes/schemes/measuresthat

aretobeinitiated,continuedordiscontinuedinthe12thPlanperiodandestimated

fundrequirement.

iii.Tomakeanyotherrecommendationsasmaybeappropriateforsustainedgrowth

andcompetitivenessofthesector.

xxiii

TheworkinggrouponDrugsandPharmaceuticalsfirstmeton29.06.2011.Thereafter

differentsubworkinggroupsheldtheirmeetingsseparatelyandfinallysubmittedtheir

reportswhichwasseenandanalysedbytheworkinggroupmeetingheldon12.08.2011.

(C) RearrangementofToRs

TheToRshavebeenarrangedinvariousChaptersbasedonthefocusareaasbelow:

Chapter1‐IndustryStructure&SWOTAnalysisconsistsoffollowingToRs:

(i) Toarticulatethelongtermgoalstobeachievedintermsofgrowth,

competitivenessandshareinglobaltradeforthedomesticDrugs&

PharmaceuticalIndustries.

(ii) ToreviewthecurrentstatusofdomesticPharmaceuticalsSectorhighlightingthe

achievementsduringthe11thPlanandreasonsformajordeviation/shortfall,if

any,inrespectoffulfilmentoftargetsandidentifyingareasofstrengthand

weaknessoftheIndianindustryvis‐à‐visinternationalDrugsand

PharmaceuticalsIndustry.

(iii) Tobenchmarkindigenousdrugs&pharmaceuticalsindustryagainstinternational

drugs&pharmaceuticalsindustryandsuggestappropriatemeasuresforbridging

thegapswherenecessary,includingtheneedsforfurtherR&Dactivitiesand/or

technologycollaborationforupgradingtechnology.

(iv) Toexaminethestructureandcapabilityofthedomesticdrugs&pharmaceutical

industry,itsexporttrend&performanceandidentifyemergingareashaving

specificpotentialforgrowthandcompetitivenessaswellastosuggestmeasures

forputtingtheindigenousindustryonsoundfootingandgrowthpathkeepingin

viewthegoalstobearticulatedunderitem1above.

(v) ToreviewthepresentstatusofWHO‐GMP(WorldHealthOrganization–Good

ManufacturingPractice)certificationandschedule‐Mcomplianceandsuggest

measuresforraisingthelevelofcompliancebymanufacturersofdrugsand

pharmaceuticalproductsinthecountry.

xxiv

(ix) Tostudychangeinstructureofdomesticpharmaceuticalsindustryinthelightof

currenttrendofmerger&acquisitions/takeovers/collaborationsandits

correlationwithrelatedFDInormsandsuggestmeasurestosafeguardnational

interests.

(xi) Toassesstheadequacyandrelevanceofpresentregulatorymechanismofdrug

andpharmaceuticalssectorandexamineneedforfurtherstrengtheningtotackle

themenaceofspuriousdrugsetc.andexamineneedforanapexauthorityto

controlprice,qualityandsupplyofdrugs.

Chapter2:Research&DevelopmentconsistsoftheToR(viii)whichisasbelow:

(viii) Toassessthepresentcapabilityforinnovationvis‐à‐visR&Dstatusofthe

domesticDrugs&Pharmaceuticalsindustryandtosuggestwaysandmeansto

improvethedomesticefforts,enhanceindustryparticipationandintensify

Industry‐Institutional/academialinkagetopromotedomesticR&Dfor

establishmentofitsinternationalcompetitivenessandmeetingtheemerging

challengesarisingoutoftheWTOregime.

Chapter3:CapacityBuildingandEmploymentconsistsofToR(x),whichisasbelow:

(x) ToexaminethetrendofemploymentgrowthintheDrugsandPharmaceuticals

industryandprojectlikelyrequirementofskilledmanpowerduringtheTwelfth

Planperiodaswellastomeetthelongtermgoals.Tosuggestmeasuresfor

puttinginplaceadequateacademicandtraininginfrastructureandfacilitiesto

meettherequirements.

Chapter4:PricingandAvailabilityconsistsofToRs(vi),(vii)and (xii)whichareasbelow:

(vi) Toexaminetheimpactofnewpatentregimeondomesticpharmaceutical

industryincludingitsimplicationondrugprices.

xxv

(vii) Tostudytheefficacyandappropriatenessofcurrentdrugpricingsystemaswell

asitscontrolandenforcementmechanismandsuggestmeasuresforfurther

improvement,ifapplicable.

Chapter5MedicalDevicesconsistsofToR(xiii)whichisasbelow:

(xiii)Toassessthecurrentstatusofdomesticmedical/surgicalequipmentindustry,its

exportpotentialandcompetitivenessandsuggestmeasuresforimprovement

andaugmentationofcapabilities,wherenecessary.

Chapter6isrelatedtoCentralPublicSectorUndertakings.

Chapter7isResourceRequirementintheDepartmentofPharmaceuticals

Chapter8SchemesandProposalsconsistsofToRs(xiv)and(xv)whichreadasbelow:

(xiv) Toindicatethemilestonestobeachievedinthe12thPlaninthecontextoflong

termgoalsasperitem‐IoftheToRandrecommend

pogrammes/schemes/measuresthataretobeinitiated,continuedor

discontinuedinthe12thPlanperiodandestimatedfundrequirement.

(xv) Tomakeanyotherrecommendationsasmaybeappropriateforsustained

growthandcompetitivenessofthesector.

Page 1 of 153

Chapter1

PHARMACEUTICALSINDUSTRY:STRUCTURE&SWOTANALYSIS

1.1 INTRODUCTION

TheIndianpharmaceuticalIndustryisdrivenbyknowledge,skills,lowproduction

costs,quality.Duetothisthereisdemandfrombothdomesticaswellas

internationalmarkets.Thishasresultedinarobustgrowthofaround14%sincethe

beginningofthe11thPlanin2007fromaboutRs71000crorestooverRs1laccrores

in2009‐10comprisingsomeRs62,055croresofdomesticmarketandexportsof

overRs42,154crores(Table‐1).

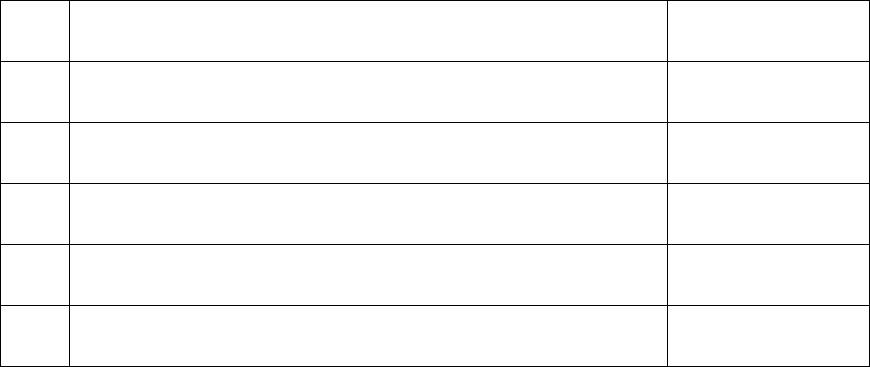

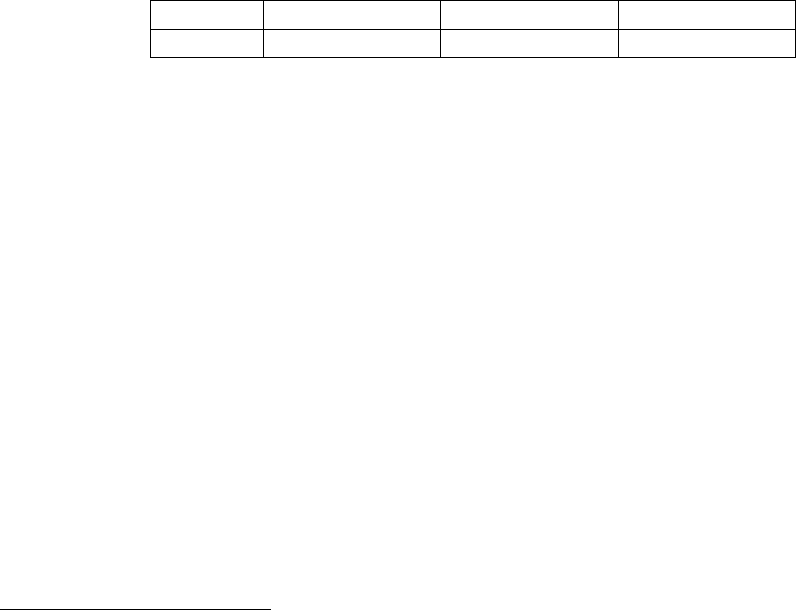

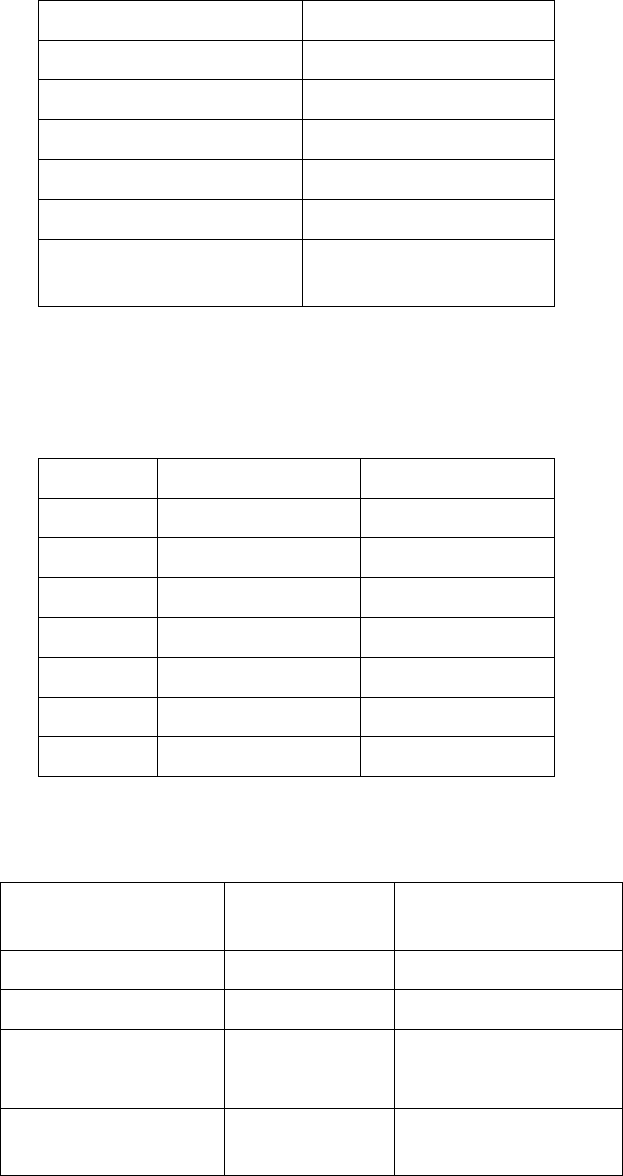

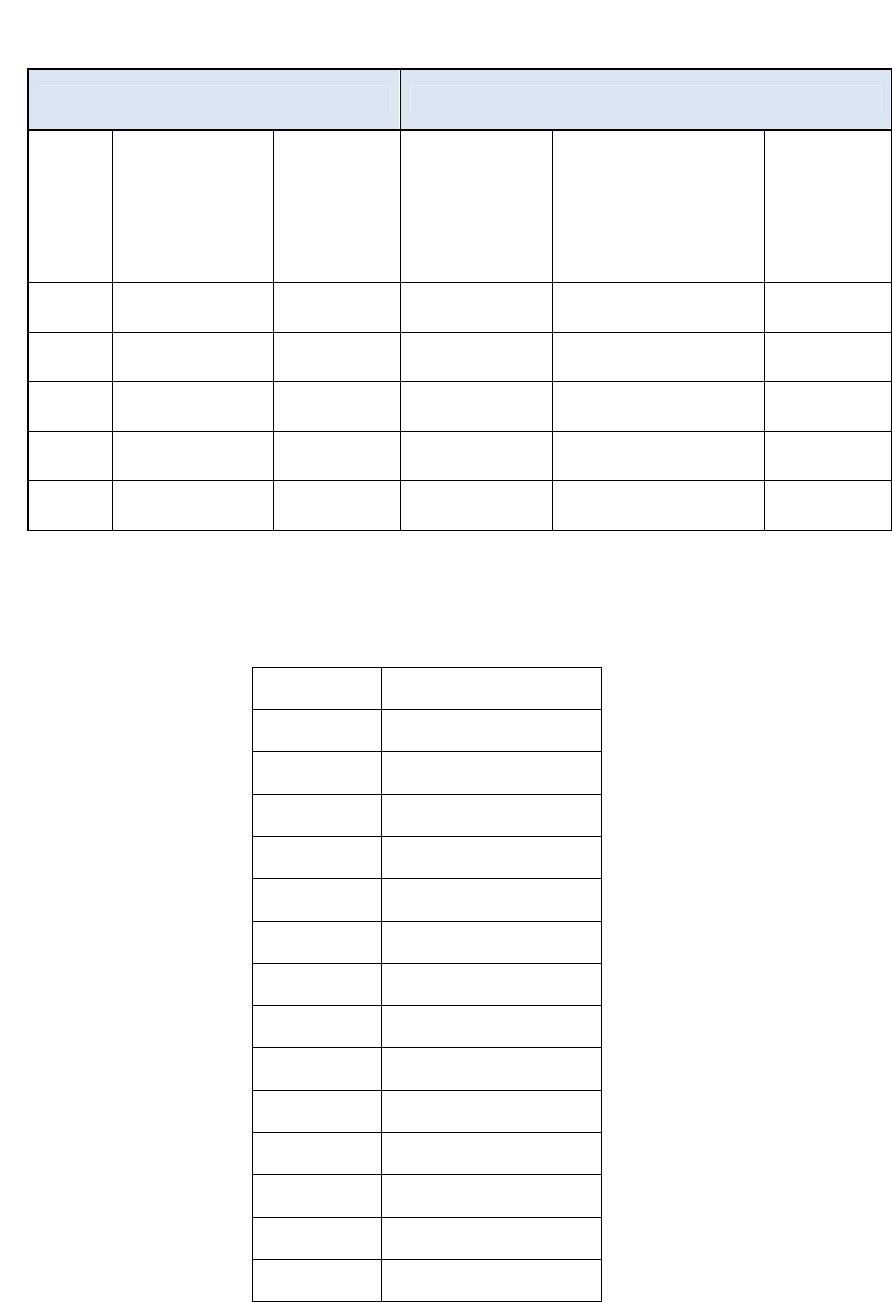

Table‐1:ExportandDomesticGrowth

*Provisional

TheIndustryisranked3rdgloballyinvolumeand14thinvalue,supplyingaround10%oftotal

globalproduction1.Thisalsoamountstoaround20%oftotalvolumeofglobalgenerics.Thus

every5thTablet,CapsuleandInjectableingenericsdrugsconsumedanywhereintheworld

ismanufacturedinIndia.Infact,Indiamanufactures30%oftheworldrequirementofAnti‐

HIVdrugs.Allofthisgrowthhasbeenwithaffordablepricetothecommonman–oneofthe

lowestintheworld.Goingforward,itisexpectedthatthegrowthwillbesustained

notwithstandingtherecentinitialdecreaseduetoglobaleconomicslowdownas

broughtoutinthedecreasedgrowthratefrom18.65%in2009‐10over2008‐09to

9.38%intheperiod2009‐102.

1.CygnusReport‐CygnusBusinessConsultingandResearchisaservicesorganizationfocusingonanalysisand

researchofEconomies,IndustriesandCompanies

2.FICCI‐IMSReport

YearExportsGrowth DomesticGrowth%TotalGrowth%

Mar20062123023.233998917.176121919.21

Mar20072566620.894536713.457103316.03

Mar20082935414.37 50946 12.30 8030013.04

Mar20093982135.66554548.859527518.65

Mar201042154*5.866205511.901042099.38

Page 2 of 153

Indianpharmaceuticalindustryistrulyinternationalwithleadinginternational

manufacturerscompetinginIndiandomesticmarketandseveralIndianpharma

companieshavingasignificantpresenceininternationalmarket,especiallyinthe

genericsegment.However,theIndustryisquitefragmentedandcomprisesofnearly

10,500unitswithmajorityoftheminsmallsector.Ofthese,about300‐400unitsare

categorizedasbelongingtomediumtolargeorganizedsectorwiththetop10

manufacturersaccountingfor36.5%ofthemarketshare3.

Medium&LargeDomesticCompanies:Themediumandlargedomesticcompanies

havebeenthedriversofgrowth,contributing75%ofdomesticsalesandover90%of

exports.Theexportoftop50companiesfortheyear2009‐10revealthat

pharmaceuticalindustry’sforayintheglobalmarketisdrivenmainlybythedomestic

companiesasmaybeseenbelow.Thustop50exportersaccountedfor76%oftotal

exportsofRs36,683crin2009‐10.Itisnoteworthythatonlytwoforeigncompanies

featureinthislistcontributinglessthan2%ofthetotalpharmaceuticalexports.

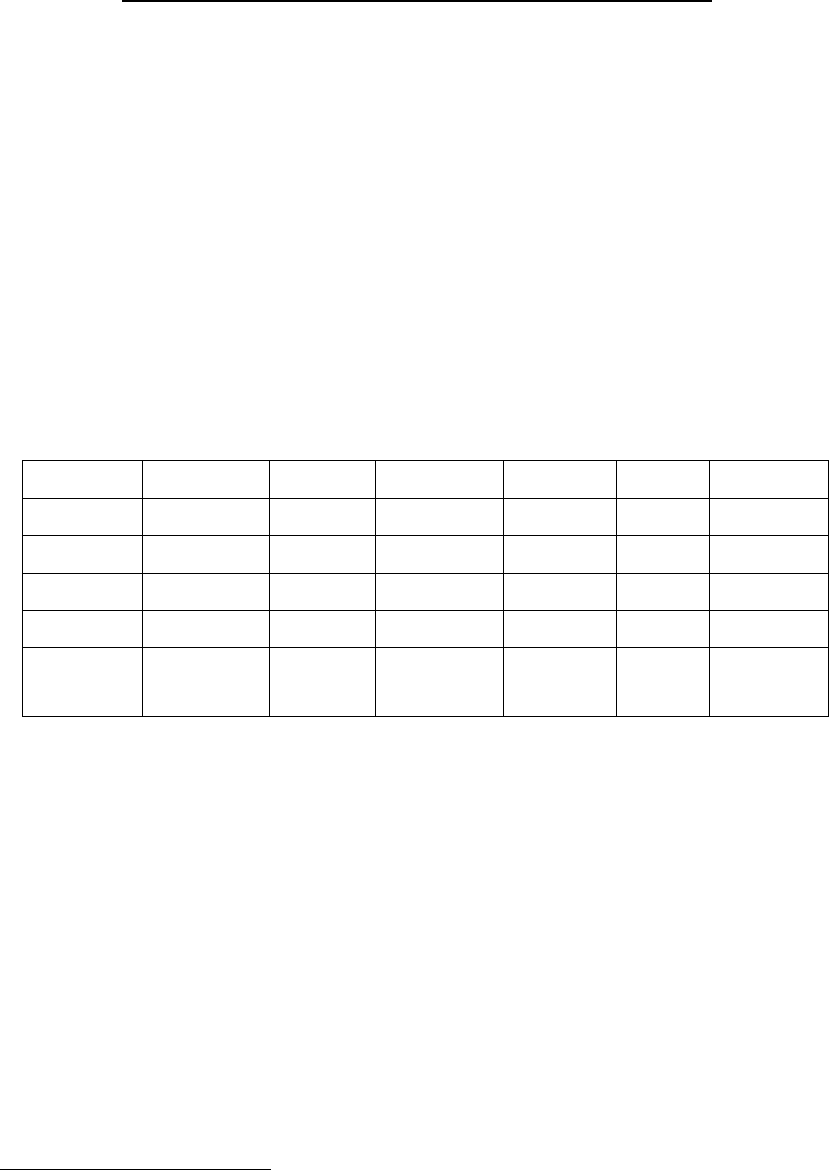

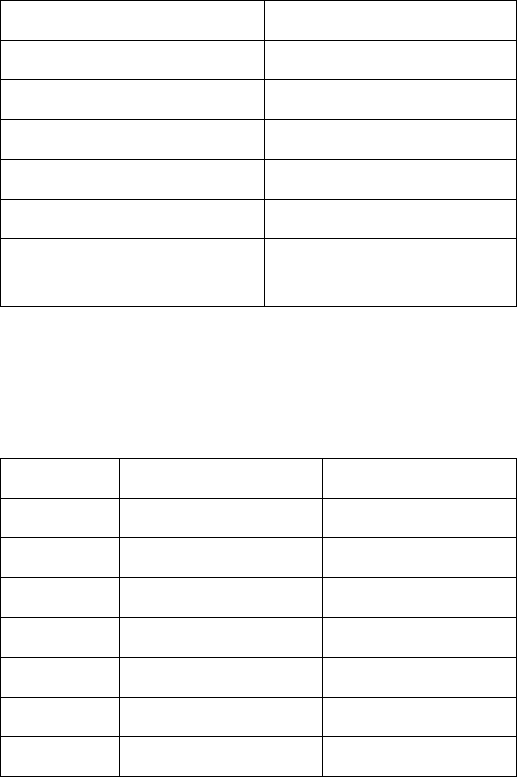

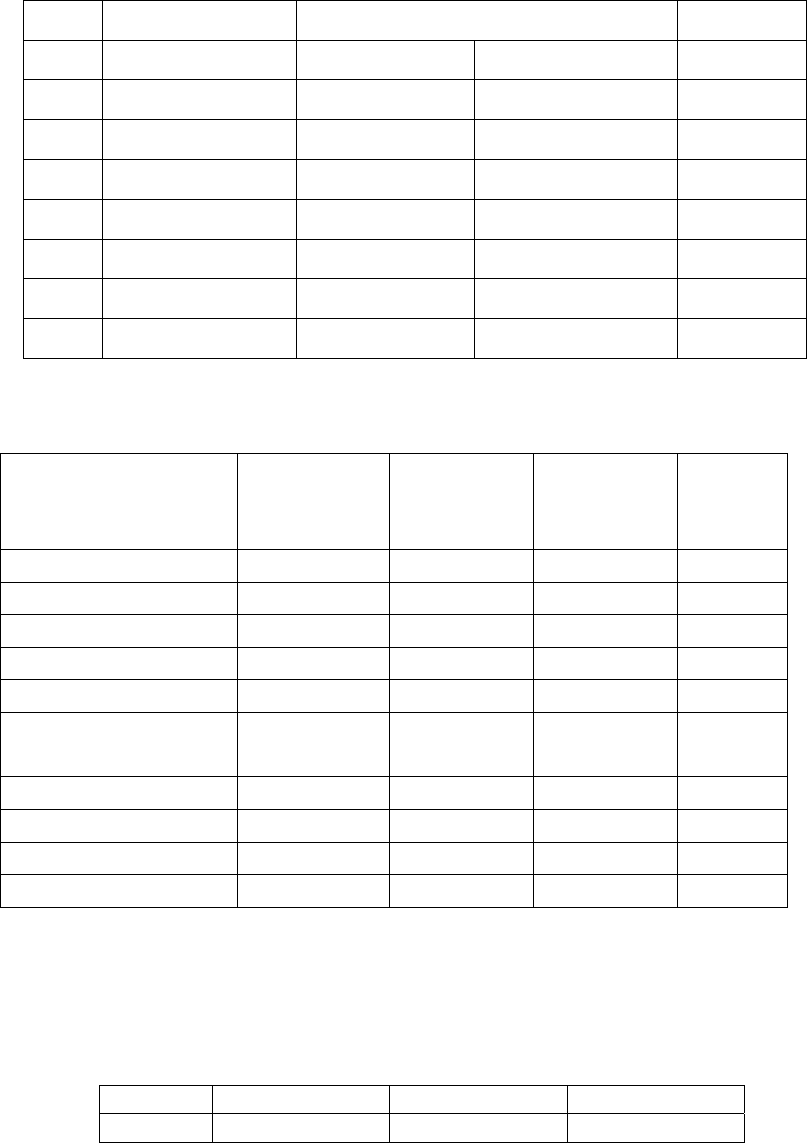

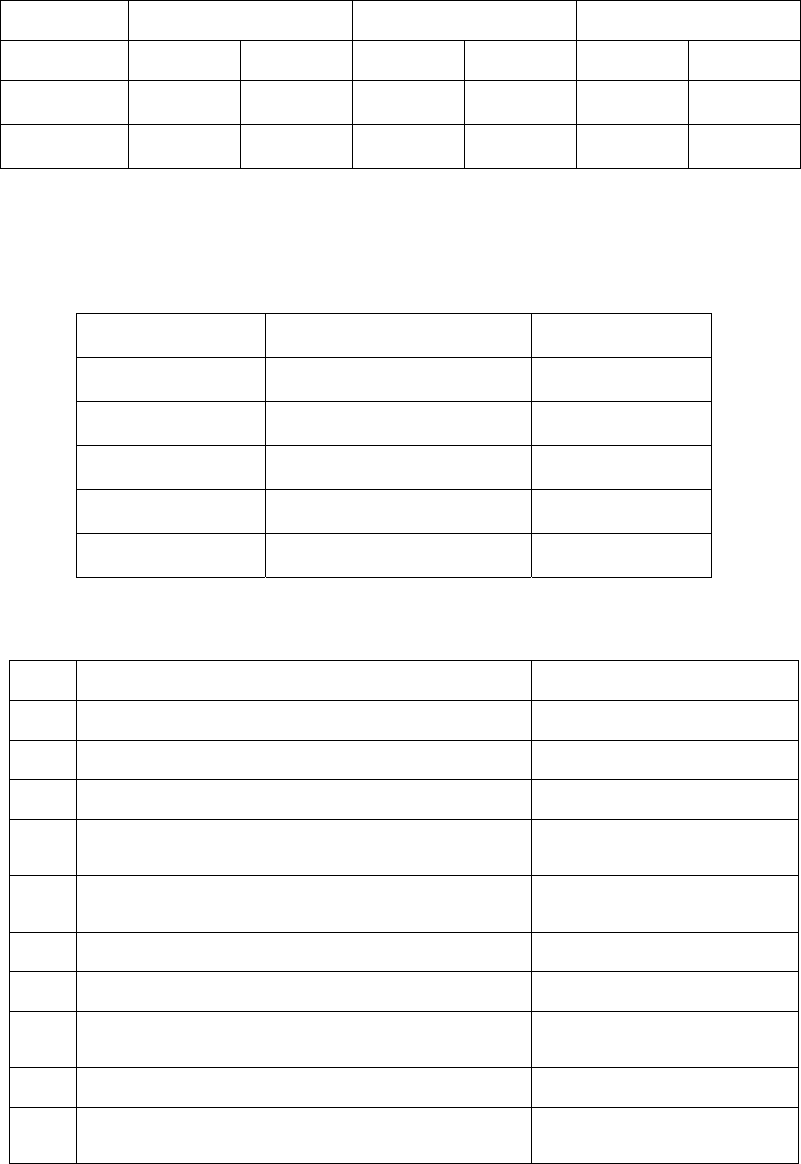

Table–2:Internationalsalesonconsolidatedbasis(Rscrore)2010‐114

3 Indian Institute of Management, Bangalore – Report on “Viable Strategies to make Pharmaceutical CPSEs

Self-Reliant” prepared for DoP in 2009-10

4 Pharmabiz analysis

Consolidated International Exports as % of net sales

net sales sales 2010-11

Ranbaxy Labs 8960.77 6771.74 75.6

Dr Reddy's Labs 7236.80 5940.70 82.1

Lupin 5706.82 3983.08 69.8

Cipla 6130.31 3361.49 54.8

Sun Pharma 5721.43 2898.20 50.7

Wockhardt 3751.24 2709.91 72.2

Jubilant Lifescience 3433.40 2369.11 69.0

Cadila Healthcare 4464.70 2288.70 51.3

Biocon 2300.52 1956.79 85.1

Glenmark Pharma 3089.59 1955.83 63.3

Stride Arcolab 1695.84 1637.67 96.6

Plethico Pharma 1535.20 1367.22 89.1

Piramal Healthcare 2509.86 1280.58 51.0

Divi's Labs 1307.11 1204.95 92.2

Aurobindo Pharma 4381.48 1112.06 25.4

Page 3 of 153

1.2DOMESTICMARKET

1.2.1Structure&GeographicalDistribution

TheDomesticPharmaceuticalMarkethasreachedtooverRs60,000croresin2009‐

10.Understandably,themarketisskewedtowardscitieswiththetop23cities

accountingforalmost25%ofpharmasalesofwhichtheTier‐Itownsaccountforone

thirdofsalesandTier‐IIcities(populationlessthanonelac)includingtherural

marketaccountingforabout40%ofmarketshare.Thisisfortheobviousreasonsof

betterhealthcareaccessibilityandpurchasingpoweroftheresidentmiddleclass

incomegroup.However,duetoshiftingruralandsemi‐urbaneconomicstatusas

wellaslivinglifestyles,theruralareasarewitnessingamarketincreasegrowthof

morethan30%annually.Thisincreaseinthegrowthiscatchingattentionofthe

majorcompanieswhoarenowfocusingonthemforfuturegrowth.

Statewisedistributionis:

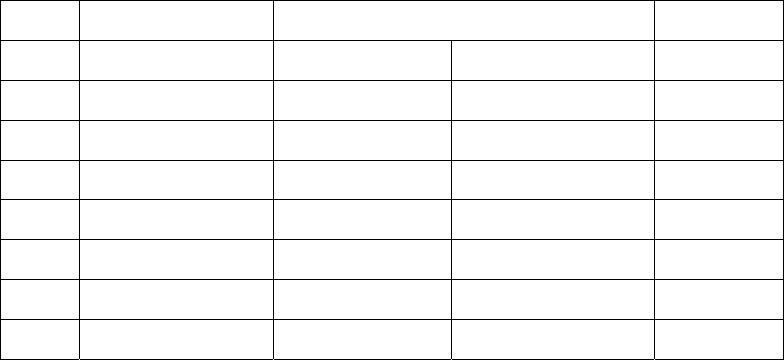

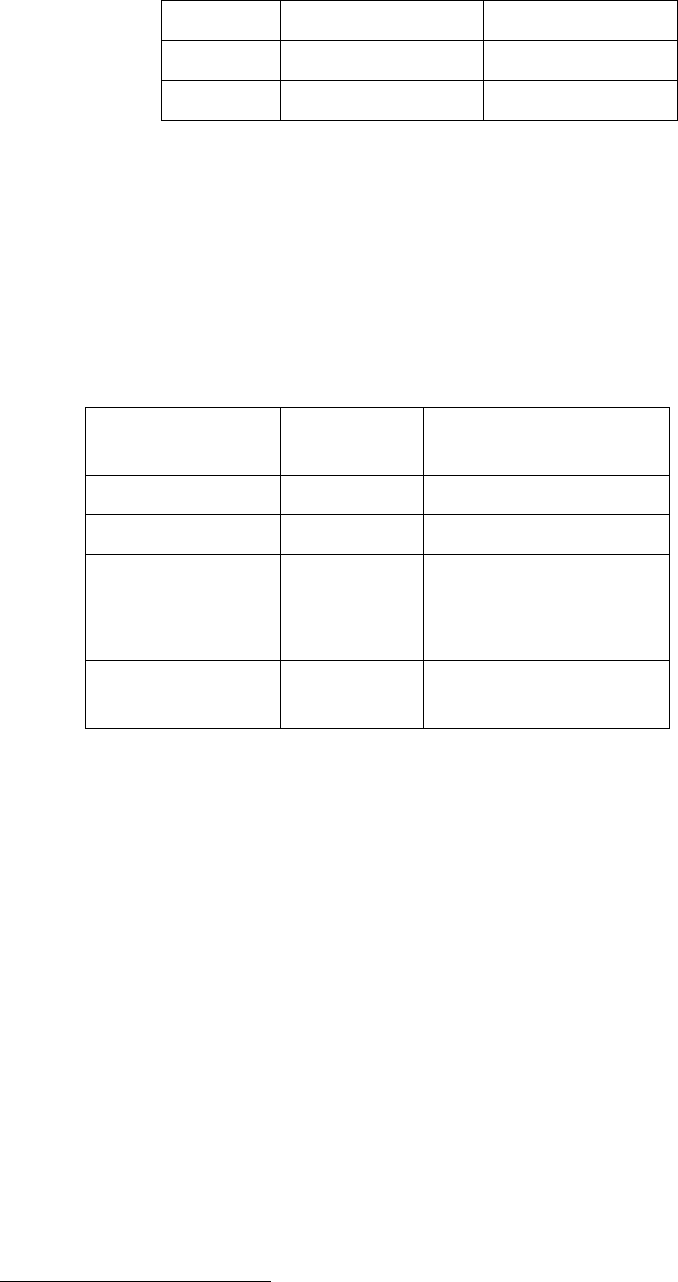

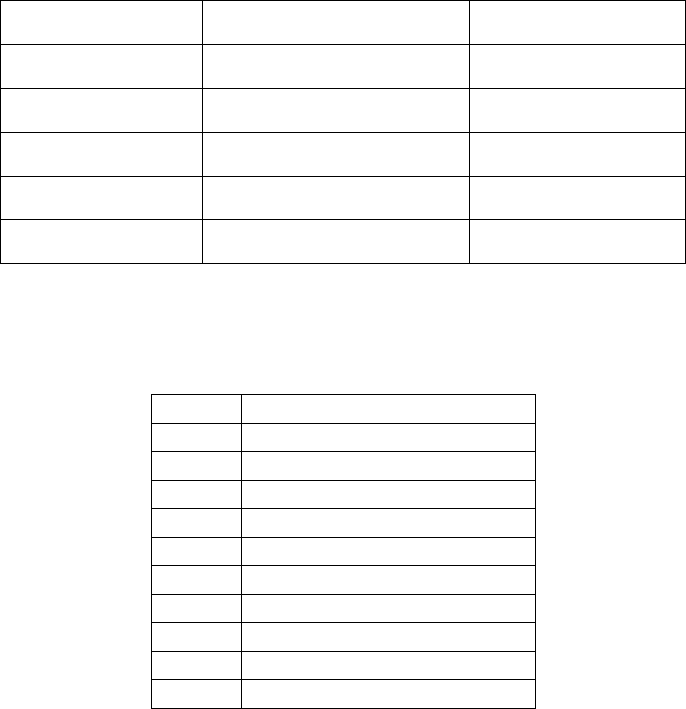

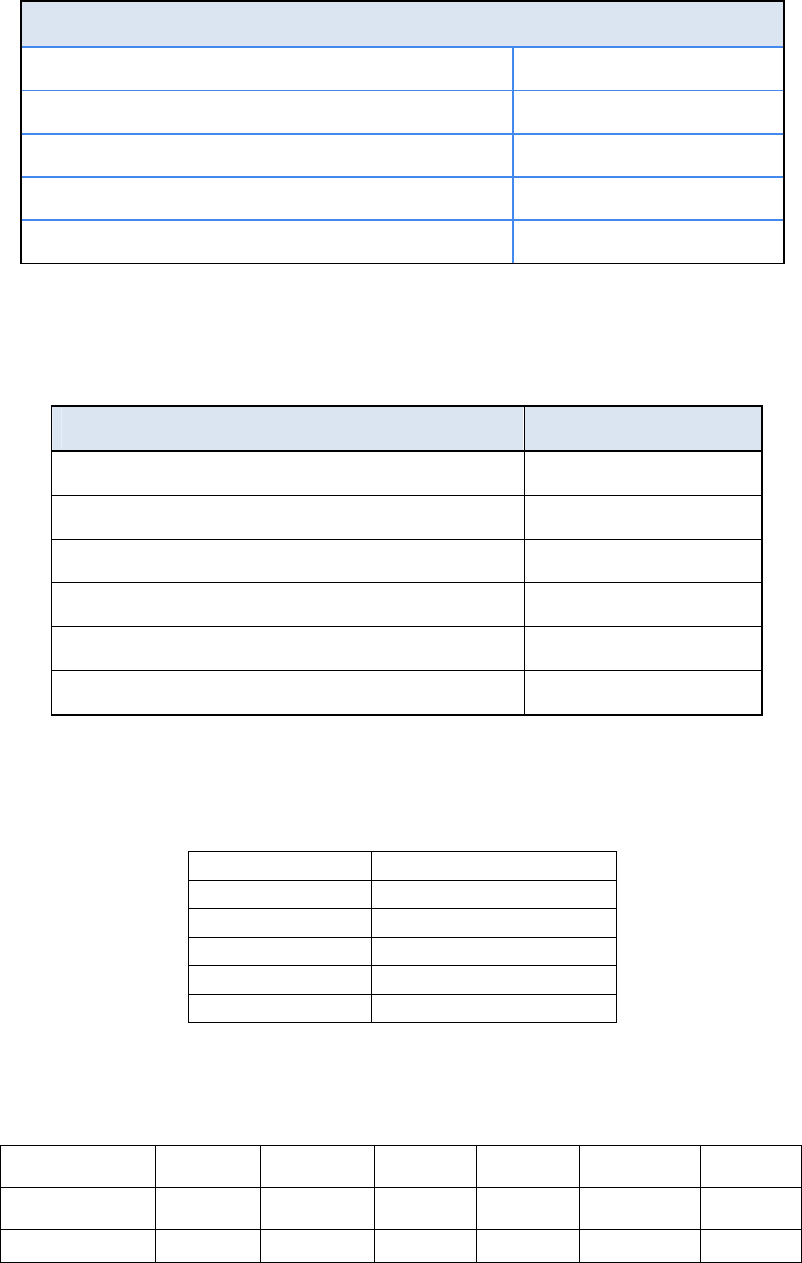

Table‐3:GeographicalDistributionofPharmaCompanies

S.No.StateNumberofManufacturingUnits Total

FormulationBulkDrugs

1.Maharashtra192812113139

2.Gujarat1129 397 1526

3.WestBengal69462756

4.AndhraPradesh528199727

5.TamilNadu47298570

6.Others34234223845

Total8174238910563

Torrent Pharma 2121.97 1101.57 51.9

Ipca Laboratories 1882.54 1025.18 54.5

Dishman Pharma 990.84 911.56 92.0

Orchid Chemicals 1781.79 725.85 40.7

Shasun Chemicals 799.42 676.78 84.7

Panacea Biotec 1143.78 610.44 53.4

Page 4 of 153

1.2.2FormulationsandTherapeuticsegmentsinthedomesticmarket:

WithintheDomesticformulationsmarketthemajortherapeuticcategoriesare‐

anti‐infective,gastrointestinal,cardiac,gynecologyanddermatology5.Theleading

drugclasseswereCephalosporin,Anti‐pepticulcerants,oralanti‐diabeticand

Ampicillin/Amoxycillin,etc.Thetoptendugclassescontributed35%oftotal

domesticmarket.AsperIMS‐Health6themajortherapeuticsegmentsasperMAT

valueare:

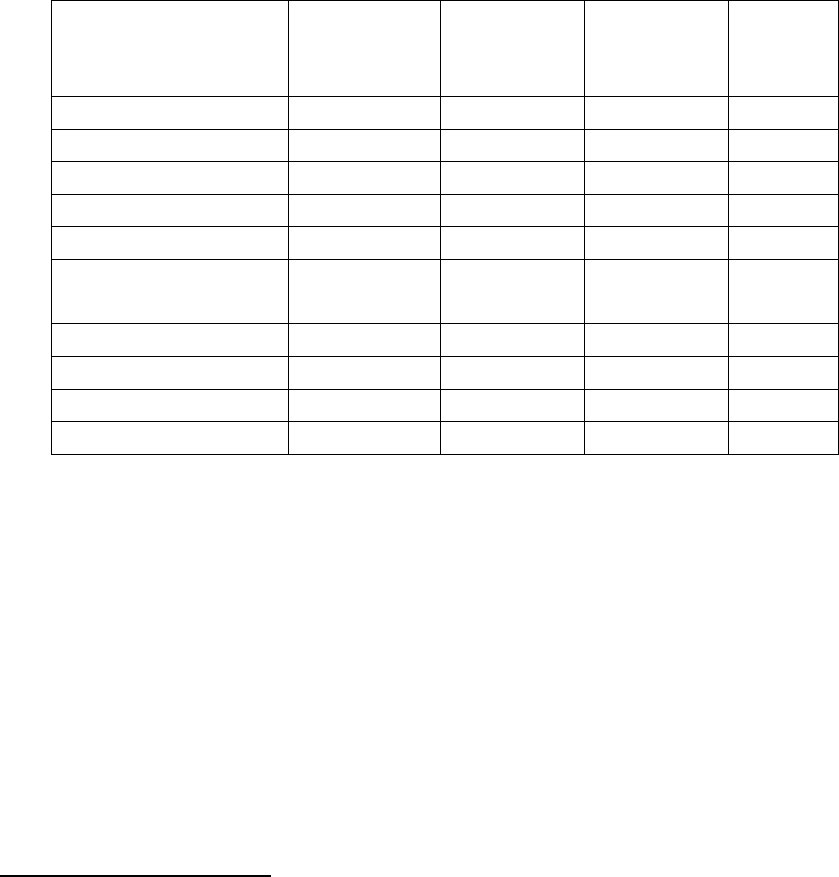

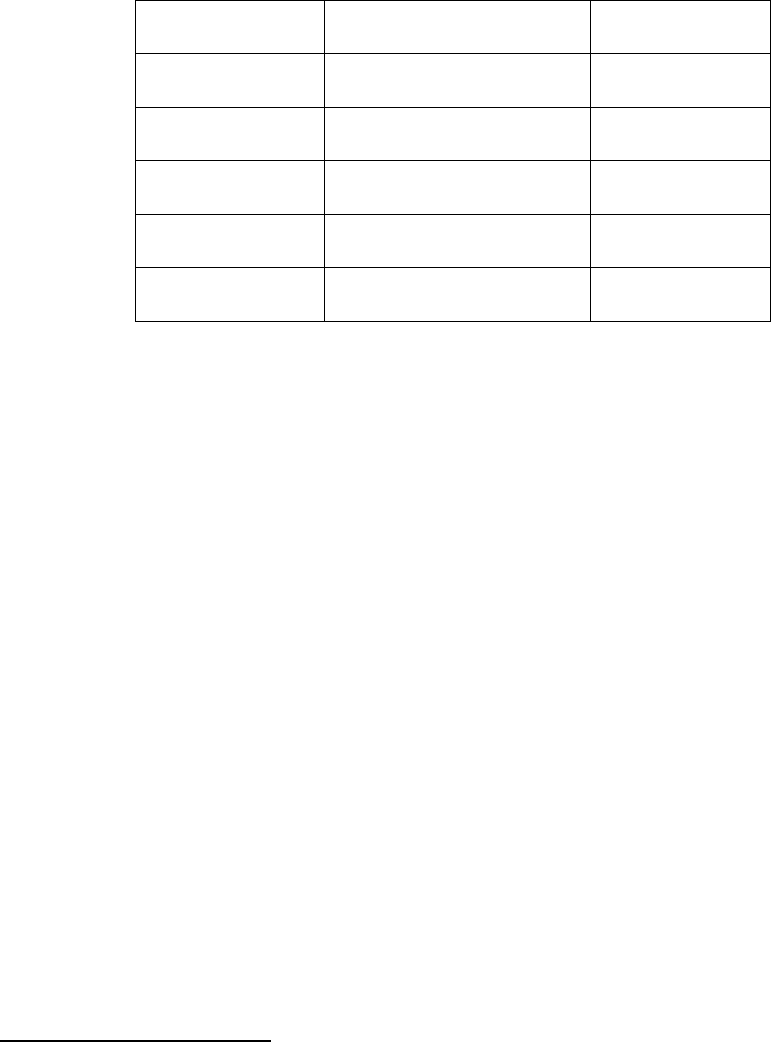

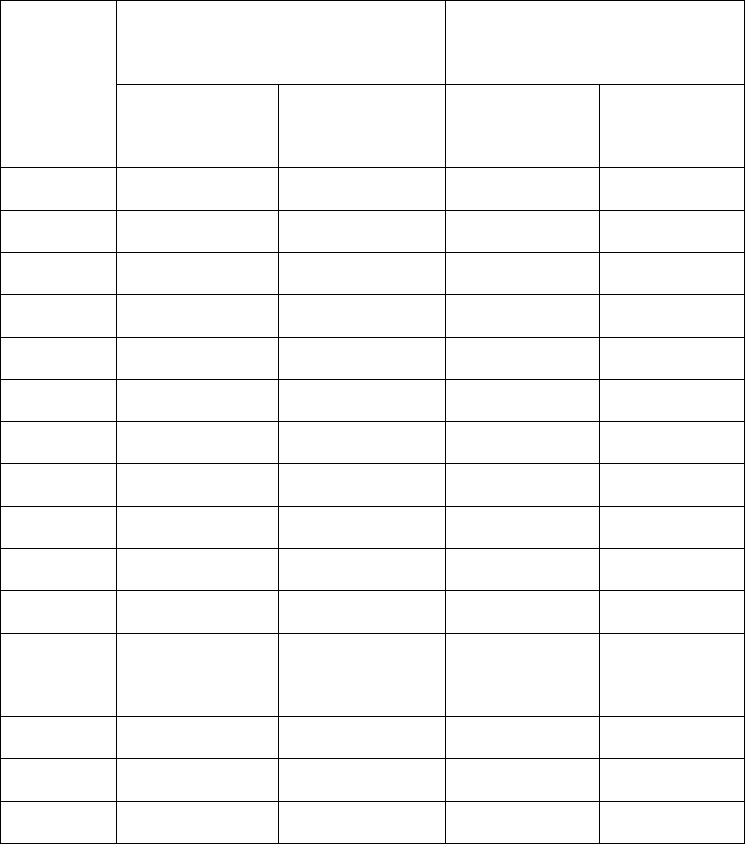

Table‐4:MarketTurnoverofMajorTherapeuticSegments

MajorTherapiesMATDEC'05

(ValinCrs)

%

Contribution

MATDEC'10

(ValinCrs)

%

Contribut

ion

Anti‐infectives4,056 17.6 8,060 17.2

Cardiac2,378 10.3 5,318 11.4

GastroIntestinal2,537 11.0 5,099 10.9

Respiratory2,170 9.4 4,080 8.7

Pain/Analgesics2,059 8.9 4,038 8.6

Vitamins/Minerals/

Nutrients2,1059.13,6257.7

AntiDiabetic 998 4.3 2,743 5.9

Gynaecology1,261 5.5 2,658 5.7

Neuro/CNS1,231 5.3 2,633 5.6

Derma1,255 5.4 2,554 5.5

Source:IMSHealth

Indiaislargelyself‐sufficientincaseofformulations,thoughsomelifesaving,new‐

generation‐technology‐barrierformulationscontinuetobeimported.Thisisevident

fromthefactthatoutofthelistof348medicinesenlistedas“EssentialMedicines”

intheNLEM2011,allaremanufacturedbydomesticpharmaindustry.

1.2.3BulkDrugIndustry

5 IMS-Health

6 IMS-Health

Page 5 of 153

The Bulk drugs component of the domestic industry is around Rs 42,000 crores giving

it a share of around 50% of the total domestic market7. This gives the Indian Bulk

Drug industry a share of about 9% of the global bulk drugs market of about US$ 102

Bn in 20098.

The bulk drugs produced in Indian market fall under 21 major therapeutic classes with

Antibiotics constituting more than 50% of the total production. This is because of

anti-infectives being the therapeutic segment of highest demand in accordance with

the prevailing disease class in India. Analgesics and Anti-pyretics account for 18%

and Anti-Dysentery and Vitamin constitute about 8%.

AsregardstheexportsofBulkdrugsithasshownaCAGRof16.98%inthelast3

years–seeTable‐5below:

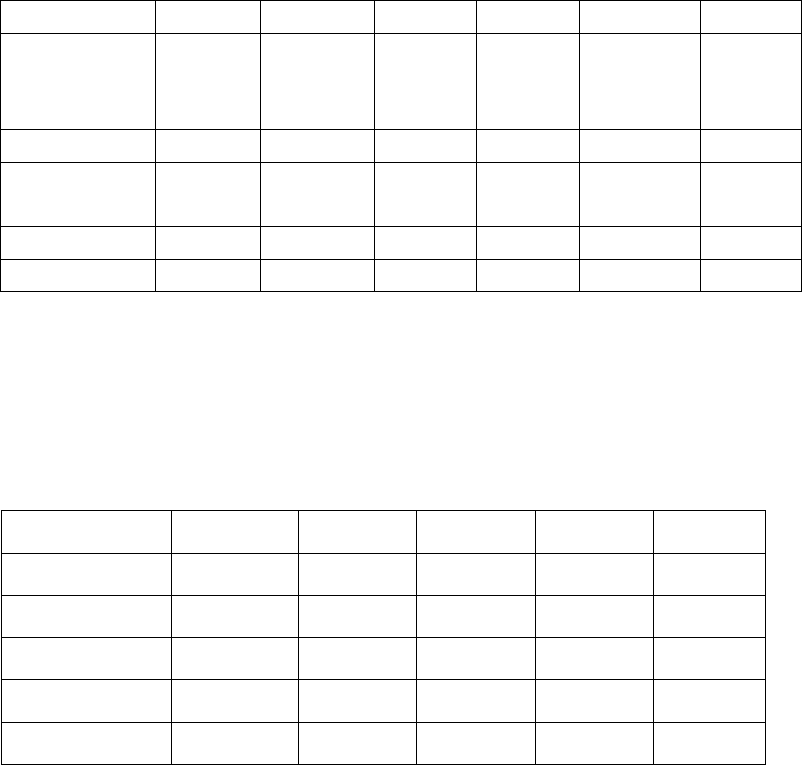

Table‐5:BulkIndustryGrowth

(InRsCrores)

2007‐082008‐09 2009‐10 CAGR

12,647.5116,360.71 17,307.02 16.98%

WhiletheIndianbulkdrugindustryiscateringtoaround70%requirementofIndian

PharmaceuticalIndustrythereisgrowingdependenceonChinawithlowimport

costs.ThisdependenceisparticularlymoreinfermentationbaseAPIssuchas

Pencillin,Erythromycin,etcwhereitisalmost100%dependentonChina.Thisissue

hasbeenvoicedatvariousforaincludingbyMoH&FWasbeingofstrategicconcern.

1.2.4BiopharmaIndustry

1.2.4.1OverviewoftheGlobalBiologicsSector

7 BDMA

8 Cygnus- Cygnus Business Consulting and Research is a services organisation focusing on analysis and

research of Economies, Industries and Companies

Page 6 of 153

Withglobalsalesofbiologicsreachingnearly$137billionin2009andthepatentson

atleast48biologicsduetoexpireoverthenextdecade,industryexpertspredictthat

theglobalbiosimilarsmarketcouldbeworthmorethan$43billionby2020.But

biologicsdifferfromconventionalpharmaceuticalsinsomefundamentalways.

1.2.4.2SizeandCompositionoftheGlobalBiologicsMarket

In2009,globalsalesofbiologicstotalled$136.6billion(Table‐6).Avastin

(bevacizumab)headedthelistofbestsellers,withsalesof$5.74billion,while

Rituxan(rituzimab)andHumira(adalimumab)camesecondandthird,respectivelyas

pertablebelow.

Table‐6:TheGlobalMarketforBiologicsin2009

Country 2009Sales($bn)

US69.02

Europe41.68

Japan10.29

Asia/Africa/Australasia14.4.0

LatinAmerica1.20

TotalBiologicDrugs

Market

136.59

Source:Visiongain&PricewaterhouseCoopersanalysis

Table‐7:The10TopSellingBiologicsin2009

BrandDrugName 2009Sales($bn)

Avastinbevacizumab 5.74

Rituxanrituximab5.62

Humiraadalimumab5.48

Herceptintrastuzumab4.86

Lantusinsulinglarine4.29

Enbreletanercept3.87

Remicadeinfliximab 3.51

Page 7 of 153

Neulastapegfilgrastim 3.35

Epogenepoetinalfa 2.56

Avonexinterferonbeta‐1a2.32

Source:EvaluatePharma

1.2.4.3SizeandCompositionoftheGlobalBiosimilarsMarket

Biosimilarsaccountedforsalesofjust$1.23billion–lessthan1%ofthetotal

biologicsmarket–in2009(Table8).However,thereisconsiderablepotentialfor

growth.

Table‐8:TheGlobalMarketforBiosimilarsin2009

Country2009Sales($

bn)

MarketShareof

Biosimilars(%)

US0.06 4.9

Europe0.14 11.4

OtherCountries

(incl.Chinaand

India)

1.03 83.7

TotalBiosimilars

Market

1.23 100

Source:IMSHealth&visiongain

1.2.5GROWTH

1.2.5.1DomesticIndustry:

Asstatedearlierabove,thedomesticpharmaceuticalIndustryhasgrownataround

12%CAGRsincethestartofthe11thPlanin2007,fromRs45,367croresin2007to

aboutRs62,055croresin2009‐10.Thisissustainedbythefollowingfactors‐

a) marketsizeincreaseduetoincreaseinthesizeofmiddlelevelincomeearning

populationsegmentasitgrowsinsizefromthecurrent270Mntosome583

Millionby20259;

b) Increaseinpurchasingpowerofthisgroup;

9 www.Mckinsey.com/mgi/mginews/bigspenders.asp

Page 8 of 153

c) AgingoftheIndianpopulationaslifeexpectancyhasincreasedfromabout42

yearsin1960sto66.95yearsatthebeginningofthe11thplantonow68.45years

in2010‐1110coupledwiththepurchasingpowerofthissegment.Itistobenoted

thatpeopleofoldagespendaround3to4timesmoreondrugsthanpeoplein

youngeragegroupsforobviousreasons;

d) greatermarketpenetrationduetoincreasingspreadofprivatesectormedical

insurancecoverdrivenbyliberalizationoftheinsurancesectorofthisburgeoning

middleclass;and

e) sustainedexpectedgrowthoftheIndianeconomyingeneralataGDPgrowth

rateofsome9%to9.5%inthe12thPlanperiod11

Goingforward,theabovefactorsforsustainedgrowthwillbematchedbythe

inherentabilityoftheIndianmanufacturerstoscaleupproductionwithlesscosts

andtime,aswitnessedintheoverRs29,000croresofinvestmentinsettingupof

newmanufacturingplantsinthecountryinthe11thplanperiod12.

Theproductpatentnowpermittedfollowingthe2005amendmentinthePatentAct

1970hasfurtherencouragedthenowreasonablypreparedIndianpharmaceutical

companiestomovefromitsexpertiseinprocesschemistrywhichhasserveditwell

forgenericsproductstomorecomplexskillsindrugmoleculeResearchand

Development.ThusR&Dinvestmentsofthetop15Indianmanufacturingcompanies

haveincreasedfrom3%ofsalesin2000tosome8.68%ofsalesin201013.Basedon

abovefacts,theprojectedgrowthofthepharmaceuticalsectorasperpresent

outlookis–

Table‐9:ProjectedGrowth

ValueinRscrs/Growthin%

YearDomesticExports Total

10 Census Commission

11 Planning Commission

12 IPA

13 IPA

Page 9 of 153

ValueGrowth Value Growth ValueGrowth

2016‐17130,00021% 158,000 16% 288,00018%

2019‐20233,00022% 248,000 17% 481,00019%

1.2.5.2BulkDrugIndustryGrowthcomponent:

InIndiathebulkdrugsindustryisamajordriverfortheoverallindustrygrowthbeing

drivenbythesame6reasonsasforthepharmaceuticalsformulationssector

mentionedearlier.AspertheestimatesofBulkDrugsManufacturersAssociation

(BDMA),thishighgrowthwillcontinueandthesectorwillbeofUSD20billionsizeby

2015growingataCAGRof20%from2008‐0914.Withtheseprojections,itis

expectedtotouchUS$28billionbyendof12thplanin2017.

1.3EXPORT:

1.3.1Structure

Indiaisamongthetop20pharmaceuticalexportingcountriesgloballyandhas

showncommendableexportperformancewithcontinuouspositivetradeofbalance.

ExportsconstituteamajorpartofIndianpharmaceuticalIndustryandatpresentitis

around45%oftotalturnoveroftheIndustry.AsperDGCIS,theexportduring2010‐

11hasreachedmorethanRs45,000crores.

Indiandrugsareexportedtoaround200countriesintheworldwithhighlyregulated

marketsofUSA,UKetc.ThetopfiveexportingdestinationcountriesareUSA,Russia,

Germany,AustriaandUKwithUSAaloneaccountingforalmost20%oftotalexport.

Themajortherapeuticcategoriesofexportareantiinfective,antiasthmaticandanti

hypertensive.Country‐wise,thepositionisasflows:

1.3.2Growth

14 BDMA

Page 10 of 153

ExportshavegrownverysignificantlyataCAGRofaround19%inthe11thPlan

period,fromRs25,666crsin2007tooverRs45,000croresduring2010‐1115.The

table‐10belowgivesapictureofgrowthofexportforlast5years.

Table‐10:ExportGrowth

YearExports(Rs.crores) Growth%

Mar20072566620.89

Mar20082935414.37

Mar20093982135.66

Mar2010421546.6

Mar2011457457.7

Thesustenanceinexportgrowthrateswillbedrivenbythreefactors–

i. Increaseddependenceongenericsproductionduetopatentexpiriesby

2015,estimatedatsomeUS$300Bnofconventionaland

biopharmaceuticals16;

ii. Slowdownindiscovery/inventionofnewmoleculesindevelopedcountries;

and

iii. pressureonthedevelopedcountrygovernmentslikeUS,Germany,Japan,etc

tocontaintheirhealthcareexpenditure;

Consequently,theglobalMNCsarenowincreasinglydependingontheIndian

genericsproducers,aswitnessedintheacquisitions/mergersofsixmajorIndian

PharmacompaniesataworthofoverUS$10billionsinthe2007‐2010periodwith

anaveragepurchasepriceofabout7to9timesthegrossrevenuesforagiven

company.

1.3.3GlobalShare

15DGCIS

16 McKinsey &Company,”Capturing the India Advantage-page 18

Page 11 of 153

India,atpresentisrecognizedasaleadingglobalplayerandholds3rdpositionin

termsofvolumeand14ththeintermsofvalueoftheproduction.Theglobalmarket

forgenericdrugsin2009wasworthUS$108billion(FICCI‐IMSreportonGlobal

GenericMarket)andIndianpharmamarket,whichaspointedoutearlierconsistsof

almostgenericdrugsonly,contributedaround20%intermsofvalue.Globally,inthe

overallpharmaceuticalsspace,withaturnoverofUS$21billionin2010,Indian

PharmaceuticalIndustryhasashareof2.4%intermsofvalueinglobal

pharmaceuticalindustrywhichishavingaturnoverofUS$878billionin201017.

1.3.4Regulatory

IndiaissignatorytotheWHOcertificationprotocolonthequalityofpharmaceuticals

productsandhasthereforeacceptedtheWHO‐GMPstandardsasanintegralpartof

thestandardsforexportofpharmaceuticalsproducts.Asperarrangement,WHO‐

GMPcertificationisgrantedbytheofficeoftheDCGI(CDSCO)andStateFDAs.The

certificationisfortwoyearsatatime.

Sinceexportofgenericstothehighgrowthemergingmarketsistobeakeystrategy

forgrowthofpharmaindustryinthecountry,henceupgradationofSMEstoWHO‐

GMPstandardswouldenablethemtoexporttheirproductsandtherebyincrease

profitability.Itisestimatedthatatpresentabout800unitsarecertifiedbyCDSCO

forWHO‐GMPproduction.Asthereareabout10,000plusPharmaSMEUnitsinthe

country,therefore,thenumberofWHO‐GMPstandardunitsneedstoberaisedtoat

least2000bytheendofthe12thplanin2017toenabletheSMEsectortoincrease

andsustainitsparticipationinthePharmaIndustrygrowthprocess.Accordingly

giventheambitioustargetofachievingUSD100Bnproductionby2020,itis

estimatedthatabout1000‐1200unitswillhavetobeassistedforraisingtheir

manufacturingstandardstoWHO‐GMPlevels.Atanaverageproductioncontribution

ofUSD10Mnperunit,thiswouldmeanadditionalcontributionofaboutRs.10Bn

fromtheabovetargetachievement.

17 April-10,2010. IMS – forecasts for global pharmaceutical market – Market Prognosis :

www.imshealth.com

Page 12 of 153

Further,thereisneedtoupgradeatleast250unitstoUSFDA/EDQM/TGAandother

InternationalStandardsby2017andtrainingof5000WorkingProfessionalsinWHO‐

GMPandotherInternationalStandardsGMPrequirements.

1.3.5CompetitivenessandBenchmarking

1.3.5.1Competitiveness

GlobalPharmaMarket

Theglobalmarketischaracterizedby‐

• Peakyearsofpatentexpiriesdrivinggrowthtowardgenerics

• Publiclyfundedmarketsfacingslowergrowthandaddeduncertainty

• Chinaonpathtobecomingworld’sthird‐largestmarketin2011

AsperestimatesofIMSHealth–aglobalpharmaconsultingorganization‐thesize

oftheglobalmarketforpharmaceuticalsisexpectedtogrownearly$300billionover

thenextfiveyears,reaching$1.1trillionin2014.The5‐8percentcompoundannual

growthrateduringthisperiodwouldreflecttheimpactofleadingproductslosing

patentprotectionindevelopedmarkets,aswellasstrongoverallgrowthinthe

world’semergingcountries.Itistobestatedthatglobalpharmaceuticalsalesgrew

at7.0percentto$837billionin2009,comparedwitha4.8percentgrowthratein

2008.

Themarketwillcontinuetodrivenbypatientdemanddespitetheongoingeffectsof

theeconomicdownturn.Indevelopedmarketswithpubliclyfundedhealthcare

plans,pressurebypayerstocurbdrugspendinggrowthwillonlyintensify,butthat

willbemorethanoffsetbytheongoing,rapidexpansionofdemandinthe

pharmergingmarkets.Netgrowthoverthenextfiveyearsisexpectedtobestrong

—evenastheindustryfacesthepeakyearsofpatentexpiriesforinnovativedrugs

introduced10‐15yearsagoandsubsequententryoflower‐costgeneric

alternatives.

Page 13 of 153

Goingforward,IMShasidentifiedthefollowingkeymarketdynamics:

i. Geographicbalanceofthepharmaceuticalmarketwillcontinuetoshift

towardpharmergingcountries.Pharmergingmarkets(BRIC,SouthKorea,

Turkey,ASEAN,etc.)areexpectedtogrowata14‐17percentpacethrough

2014,whilemajordevelopedmarkets(US.WestEurope)willgrow3‐6

percent.Asaresult,theaggregategrowththrough2014frompharmerging

marketswillbesimilartothegrowthexperiencedindevelopedmarkets—

about$120‐$140billion.Thiscomparestoaggregategrowthoverthepast

fiveyearsof$69billioninpharmergingmarketsand$126billionindeveloped

markets.TheU.S.willremainthesinglelargestmarket,with3‐6percent

growthexpectedannuallyinthenextfiveyearsandreaching$360‐$390

billionin2014,upfrom$300billionin2009.

ii. TheTherapyareagrowthdynamicswillbedrivenbyinnovationcycleand

areasofunmetneed.Asthepharmaceuticalindustry’sresearchand

developmentprogramsadjusttothebroadavailabilityoflow‐costgeneric

optionsinmanychronictherapyareas,highergrowthwilloccurinthose

therapyareaswherethereissignificantunmetclinicalneed,high‐costburden

ofdisease,andinnovativesciencethatcanbringnewtreatmentoptionsto

patients.Intheareasofoncology,diabetes,multiplesclerosisandHIV,

annualgrowthisexpectedtoexceed10percentthrough2014asnewdrugs

arebroughttomarket,patientaccessisexpandedandfundingisredirected

fromotherareaswherelower‐costgenericswillbeavailable.

iii. Broadcutsinspendingwillbeappliedbypublicpayerstoreducegrowthin

drugbudgets.Publiclyfundedhealthsystemsareunderincreasedpressure

toreducegrowthindrugbudgetsfollowingtheglobaleconomicdownturn.

Page 14 of 153

CountriesincludingTurkey,Spain,GermanyandFrancealreadyhave

announcedplanstoapplyacross‐the‐boardrestrictionsonaccessor

reductionsinreimbursementstoreducedrugspendinggrowth.Governments

inothercountriesseekingtorestorefiscalbalancemaytakesimilaractions,

orshiftmorecoststopatients.

iv. Peakyearsofpatentexpirieswillshiftmajortherapiestogeneric

dominance.Overthenextfiveyears,productswithsalesofmorethan$142

billionareexpectedtofacegenericcompetitioninmajordevelopedmarkets.

Collectively,theimpactofpatientsshiftingtolower‐costgenericsinmajor

therapyareassuchascholesterolregulators,antipsychoticsandanti‐

ulcerantswillreducetotaldrugspendingbyabout$80‐$100billion

worldwidethrough2014.ThisimpactparticularlywillbefeltintheU.S.,

wherenearlytwo‐thirdsofthetotalvalueofpatentexpirieswilloccur.

PatentexpiriesintheU.S.willpeakin2011and2012whensixoftoday’sten

largestproductsareexpectedtofacegenericcompetition.

v. Closerscrutinyofnewproductswillresultinrestrictedcontributestolower

initialspendingbypayers.Thenumberofnewmolecularentitieslaunched

annuallyoverthenextfiveyearsisexpectedtoremainintherangeof30to

35products.However,thesewillbesubjecttomorerigorousandcomplex

assessmentsbypayersbeforebeingacceptedintoclinicalpracticeand

reimbursed.Inmanycountries—includingChina,Spain,ItalyandCanada—

fundingandimplementationofhealthcareatregionalorlocallevelsis

becomingmoresignificant.Thisisexpectedtoextendthetimeittakesfor

newmedicinestobecomeavailabletopatients,andcontributetolower

initialspendingbypayers.

Page 15 of 153

Furtherthattheexpectedglobaleconomicrecoveryremovesanelementof

uncertaintyfortheindustryoverthenextfiveyears,althoughthewaypayers

addresslingeringbudgetdeficitswillremainanissueinmanymarkets.Health

systemreforms,suchasthosetobeimplementedintheU.S.,canspurfundamental

changeinthemarket—butthefullimpactmaynotbefeltuntilthelatterhalfofthis

decade.Leadingupto2020,IMSexpectstoseeacontinuingshifttoward

biopharmaceuticals,specialty‐drivenproducts,andchangesinthemixofdisease

areasofinterest.

1.3.5.2Benchmarking

i. Research,developmentandInnovation

ii. HumanResources

iii. TechnicalCapability

iv. Infrastructure

v. ColdChaininfrastructure

(i) Research,developmentandInnovation

ResearchandDevelopment(R&D)isthebackboneofthegloballeadersinthe

pharmaceuticalindustryallovertheworld.Thepharmacompaniesinthe

developingcountrieswithsomesizeableturnoverarenowincreasinglytherefore

lookingatinnovationandR&Daskeystrategiesforfuturegrowth.TheIndian

pharmaceuticalcompaniescannotaffordtobedifferent.SomeleadingIndian

companieslikeSun,ZydusCadilla,DRL,Lupin,etcareincreasinglyfocusedonR&D

totaptheupcomingopportunitiesfromexpirationofpatentsofseveral

blockbusterproducts.

TheglobalaverageR&Dexpenditurein2010was$68billionwhichwasaround8%

ofglobalPharmaceuticalsalesin2010i.e.$856billion1.Hence,althoughinterms

ofpercentagetheR&DexpenditureofbigPharmacompaniesinIndiaisalso

comparabletoglobalaverage,howeverthetotalexpenditureonR&DbyIndian

Page 16 of 153

firmsismuchlessascomparedtotheglobalexpenditure.Moredetailsofthisis

discussedinChapter3onR&D.

(ii) HumanResources

ThesubjectofHumanresourcesrequiredindetailintheChapter3onCapacity

BuildingandEmployment.Forsakeofacompletediscussionbrieflyitmaybe

mentionedherethattheGovernmentandtheprivatesectordoofferauseful

institutionalstructureforprovidingdiplomatoPhDlevelknowledgedevelopment

inthepharmaceuticalssector.TheGovernmentofIndia‐throughthehighend

NationalInstituteofPharmaceuticalEducationandResearchestablishedat

Mohali,Chandigarhin1997followedbysettingupofsixNationalInstitutesof

PharmaceuticalsEducationandResearch(NIPER)atRaeBareilly,Hajipur(Patna),

Hyderabad,Ahmedabad,GuwahatiandKolkata.Theseprovidepostgraduateand

PhDleveleducationandcontributetosome1800MastersandPhDsperyear.

Othercentralgovernmentinstitutesinclude–TheIndianInstituteofChemical

Technology(IICT),CentreforCellularandMolecularBiology(CCMB),National

InstituteofNutrition(NIN),CentreforDNAFingerprintingandDiagnostics(CDFD),

IndianImmunologicalLtd(IIL),etc.

AnumberofStateGovernmentUniversitiesandCollegesalsoofferbothgraduate

andpostgraduateeducationinpharmaceuticalsciences.Theaboveresourcesare

alsosupplementedbytheinstitutesandcollegesintheprivatesector.Together

boththegovernmentandprivatesectorrolloutsome51000graduatesand5200

PGsinpharmaceuticalsscienceseveryyear18.

(iii) TechnicalCapability

Thechemistryskillsproducedinthecountrythroughitscollegesanduniversities

supportedbytheirdemandinthegenericsdominatedproductionpatternin

IndianpharmahasplayedakeyroleinbuildingIndiandominanceintheglobal

genericssector.Thatthisskillhascomeatlowcostshasresultedamongstvarious

18 Report by Deloitte 2010 for DoP on setting up of new NIPERs

Page 17 of 153

otherfactorsinenablingIndianpharmatoproduceoneofthecheapestgood

qualitydrugsintheworld.AcomparisonofthedrugpricesinIndiaandPakistan

illustratesthispoint.Withhardlyanymanufacturingbasefordrugs,thepricesof

drugsinPakistanaremuchhigherthaninIndia(3to14times)eventhoughper

capitaincomesinboththecountriesaremoreorlesssame.HoweverwithChina

thereisatoughcompetitiononthisfront.Nevertheless,Indiaisamongstthefew

developingcountriestosucceedinbuildingstronglocalcapabilityinthe

technology‐intensivepharmaceuticalsector.

However,onceagainthetechnologydevelopmentbeinglimitedtogenericsAPIs

orformulationhasbeenmostlylimitedtocost‐effectiveprocessdevelopment.

Thishasresultedinpoordevelopmentofnewproducts.Howeveritcanbeargued

thatsincetheIndianpharmastarteddevelopmentonlyasfrom1960salbeitina

MNCdominatedenvironment,itisacredittoittobeabletodevelopeventothe

currentskillsascomparedtorestoftheworld.Surelyhighriskandhighskill

demandfornewdrugdevelopmentcanpossiblynotbedoneinbarely25yearsof

ahightechnologyindustryandtheIndianpharmarightlyfirstmettheneedsof

country’sdrugneedsinthemuchrequiredanti‐infectivessector(themoleculesin

thissegmentwereinearly1940‐50s)andisnowperhapswellplacedtotakeon

thenewdrugdevelopmentchallenges.Wereitnotso,Indiawouldnothavebeen

abletotaptheglobalizationandliberalizationopportunitynowwideopeninthe

genericssectorwithitslowcostgoodqualitybase.Thisisdiscussedmoreinthe

Section1.7onSWOTAnalysis.Goingforward,Indianpharmaindustrywould

needtofocusondevelopingcompetenceinadvancedareasofdrugmanufacture

e.g.biopharmaceuticals,DNAbaseddrugsetc.

(iv)Infrastructure

AlthoughIndianpharmahasgloballyrecognizedcapabilitiesingenerics

production,ChinaisforgingaheadwithhugeinvestmentsinAPIproductionwhich

requiresinter‐aliacheappowerandotherinfrastructurefacilities.Israel,Germany,

BrazilandTurkeyarealsobuildinglargestrengths.Inthefieldofmedicaldevices,

Page 18 of 153

theIndianindustryisinnascentstage.So,thereisaneedofdevelopingcommon

infrastructureindrugdiscoveryanddevelopment,manufacturing,distribution,

exports,medicaldevices,etc.

Thekeyareasare:

(a) GLPCompliantAnimalFacilities:Pre‐Clinicaltestingrequiresprimatebased

largeanimaltesting.Howevertherearelimitedprimatefacilitiesinthe

country.WhileICMRhasproposalsfortransgenicanimalfacilitiesanda

Nationalcenterfornon‐humanprimatebreedingcenterthereisneedtobuild

capacityinthisareaandtodoitfast.Thiswouldrequirelicensedbreeders

meetingandmaintainGLPstandards.

(b) BiologicalSampleStorageFacilities:Accesstostoragefacilitiesadheringto

appropriatebio‐safetylevelsisrequired,asIndiaaddresseschallengesof

infectiousdiseases.Currently,samplesusedinmanyoftheclinicaltrialsare

beingstored/archivedoutsideIndia.ManyIndianpharmaceuticalcompanies

outsourcesafety,pharmacologyandregulatorytoxicitystudiestoother

countries,duetolackofcomprehensivefacilityexistinginthecountry,which

couldcarryoutthesestudiesinanintegratedmanner.

(c)SharedInfrastructureforOptimalCapacityUtilization:Everyscientistore

R&Dinstitution/Industryfacilitydoesnotrequirecompleteself‐sufficiencyin

termsofin‐houseinfrastructure.Poolingofresourcesbetweengovernment

andindustryasalsoacademiaevenwhilesecrecyconditionswouldgoalong

wayinbuildingmutuallybeneficialpartnerships.

(v)ColdChainInfrastructure

ThePharmaceuticalSupplyChainisverycomplexandhighlyresponsibletoensure

thattheconcerneddrugreachesthetargetpeoplewithoutlosingitsefficacy

whereverthedrugsaretemperaturesensitivewheretheColdChainInfrastructure

Page 19 of 153

isparamount.ThisisparticularlyimportantforVaccinesandrelatedtreatments

likePolio,etc.

ThisfactisincreasinglyofimportancenowintheIndianmarketgiventhegrowing

accessalongwiththelargeandoftenpoorlyconnecteddistantplaceswhere

treatmentmedicinesaretobecarriedto.Hence,pharmaceuticalcompaniesin

IndiahaverealizedtheimportanceofSCMrelatedColdChainInfrastructureand

areaggressivelylookingforwaystoimprovethecostsassociatedwithSCM.

DistributioninIndiaisproportionallymuchmorecostlythanitisintheUSorEU

duetoinherentlypoortransportstructureavailablefordrugs.Uptoone‐thirdof

therevenuesareoftenspentonSCM.BecauseoflackofdevelopedSCM

infrastructurefordrugs,thecostishigherinIndiaascomparedtoUSandEU(2%

ofsalesinUS/EUascomparedto4‐%inIndia).(BioPharmInternational

www.biopharminternational.comSeptember200).

OneotherreasonfortheabsenceofamodernSCMinfrastructureisthatthe

medicinessupplychaininIndiaishighlyfragmentedwithmorethan550,000retail

pharmaciesspreadacrossvastdistancesoftenpoorlyconnectedinthecountry.

Thisalsoleadstosuchproblemsasconcerningrecallofdrugs.Newertechnologies

wouldhelpinkeepingtrackofproductsalongtheentirechainandwouldlimit

counterfeitdrugstoenterintothesystem.Theproblemsareobviously

compoundedwhenmandatedcoldchainrequirementsaretobemet.Thisisone

ofthemajorchallengesfacedbytheindustryiftheyaretoretainproductquality

duringshipmentspeciallythebiotechproducts.Thereforetheorganizeddrugretail

facesdauntingchallengeswhichwouldthereforebeakeyfactortoimprove

affordableandqualityhealthcareaccesstoall.

1.4IPRandInternationalCooperationIssues

1.4.1ThesubjectofIPR,TRIPS,PatentLinkage,FTAs,DataExclusivity,etc.aremuch

debatedinthenationalandinternationalfora.BothlargeandSMEunitsarefinding

itdifficulttocopeupwiththeincreasinglynewdemandsbeingplacedonthese

Page 20 of 153

issuesbythedevelopedmarkets.Itisalsowidelybelievedthatthisistobuildnon‐

tariffbarriersagainstthecapabilitiesoftheIndianpharmatogarneralargermarket

shareinthedevelopedmarketsnowhavingincreasingneedforgenericsforcost

containmentinthecontextoflimitedgovernmentbudgetsandthecontinuingslow

downoftheeconomies.

IndianPharmaIndustryconsistsof60%domesticand40%ofexportmarketon

accountofwhichtheexportswouldbeaffectedduetosuchanapproachofthe

developedmarketregulators.TheStandardOperatingProcedures(SOPs)ofdifferent

governmentsisdifferentinternationally.Thereforethereisarequirementto

educateSMEunitsaboutcountryspecificSOPsfortestingtheirproducts.

Inthisregard,thesituationisalreadypitiableevenfortestingofproductsforIndian

marketsduetolackofavailabilityofreferencestandardproductsasperIndian

Pharmacopeia(IP).Thuswhilemorethan1000moleculesarebeingmanufacturedor

marketedinthecountry,IPChasreferencestandardsforabout200productsonly.

Thusthesebatchspecificandtimelimitedreferenceproductshavetobeeither

importedorgotmanufacturedin‐houseorthroughotherunitswhichisavery

tediousandexpensiveprocess.Thereisaneedtolaunchpartnershipprogrammes

byDoPinpartnershipwithMoHFW/IPCtomakereferencestandardproducts

availablenotonlyforIPbutalsoforothercountrieswheremajorexportsare

focused.ThereisalsoneedforincreasedtrainingforSMEsregardingtheSOPsand

ensuringavailabilityofreferencestandardproductsfortestingandfulfilmentof

exportsrequirements.

1.4.2Non‐TariffBarriers(NTBs): Theexportingunitsbothbulkdrugsand

formulationsfacethreetypesofnon‐tariffbarriersrelatedtoregulatory

requirementsfromhighexportmarketsliketheEU.

Page 21 of 153

i. ThereisarequirementtoensurecompliancetoEDQMstandardswhichis

availableforonly3yearsatatimewithsuchhighcostsasEuro15,000

perdrugpertime.

ii. TheninadditiontoEDQMthereisfurtherneedtoobtaincertification

fromeachimportingcountry.

iii. Furtherinthecaseofbulkdrugs,athirdadditionalrequirementisofa

thirdpartyaudit.Thisauditcompelscompaniestodivulgetheir

intellectualpropertyinfringingontheirrighttoprotectdataguaranteed

underTRIPs.

iv. Then,EUisinsistingonverificationofpedigreeofActivePharmaceutical

Ingredientsincaseofexportofformulations.

Clearly,ifsuchNTBsaretobeaddressedthereisaneedtocreategreatersynergy

amongvariousgovernmentdepartments/ministriesviz.DepartmentofCommerce

(DoC),Pharmexcil,M/oHealth&FW,DoPforformulatinganintegratedstrategyto

tacklesuchbarriersandmayincludetakingcountermeasures.

Additionallythereseemstobelackofclarityinthemultipletradeagreementsviz.

TradeRelatedIntellectualPropertyRights(TRIPs)ofWTO,AntiCounterfeitTrade

Agreement(ACTA),etcduetoexportersarefacingproblemsinensuringtheir

compliancewhichisaffectingtheirexports.Theseissuesneedtobetackledina

comprehensivemannerbyjointeffortsofDoPandDoC.

Anotherissueconcernsarecentsteptakenbysomedevelopedcountiesintheform

ofTransPacificPartnershipAgreement(TPPA),anewregionalfreetradeagreement

whichincludetheUnitedStates,Australia,Peru,VietnamandMalaysia,Japan,etc.

TPPAhasdiscriminatoryarrangementsbetweensignatoryandnon‐signatory

countrieswhichisaviolationofTRIPs.

Page 22 of 153

AdditionalbarriersarealsobeingraisedinemergingmarketslikeArgentinawherein

thereisadiscriminationinimportregulationsbetweenbulkdrugs(whichare

allowed)againstformulationswhicharebanned.Hereinthereisalsoatrustdeficit

betweentheindustryandthegovernmentespeciallyinthecontextofgovernment

signingFreeTradeAgreement(s)withvariouscountrieswhereinfacilityofzeroduty

isbeingextendedthereiseverylikelihoodofcreationoffurtherproblemswithout

properinvolvementoftheIndustry.

InthespecialcontextoftheseregulationsimpingingonIndianPharma’sleadership

intheAPIsector,thereisaneedtostudythedetailsofAPIsproductionespeciallyin

Spain,Italy,PortugalandEasternEuropeandprepareareportonexportofIndian

APIs/formulationdrugstoEUanddetailsofAPIsbeingmanufacturedinthese

countries.Thereisaneedtotackletheseissuesinorganizedmannerwherein

representativesoftheindustryneedtobeco‐optedintheefforts.Itisproposedto

establishacellinIPA,tobefundedbyDoP,onallissuesrelatedtoIPR,regulatory

issues,etc.actingasbarriers.

Inthisconnectionthereisneedtotapanewdevelopment–Theadoptionof

recommendationsofPharmaceuticalInspectionConventionandPharmaceutical

InspectionCo‐operationScheme(jointlyreferredtoasPIC/S).Thisagreement

providesforinteraliacooperationbetweencountriesandpharmaceuticalinspection

authoritiesforenablinginternationaldevelopment,implementationand

maintenanceofharmonisedGoodManufacturingPractice(GMP)standardsand

qualitysystemsofinspectoratesinpharmaproducts.Thisistobeachievedby

developingandpromotingharmonisedGMPstandardsandguidancedocuments,

trainingcompetentauthoritiesandregulatorsinthepharmasector.

1.52DBarcoding

2DBarcodinghasbeenmadearegulatoryrequirementforexportofmedicinesby

DGFTtopreventfakemedicinesandmis‐representationofIndianexportsinthe

Page 23 of 153

nameofothercountrieslikeChinaetc.TheSSIunitsdoingcontractmanufacturefor

tradinghousesandotherpharmaneedtobesupportedbygovernmentschemesfor

buildingthiscompetenciesbothbywayofinfrastructureandfinancialsupport.

Furthertheimplementationof2DBarcodingattertiaryleveli.e.atstriplevelalso

envisagedbyDoCcouldbecomeveryexpensiveandoffsetIndianprice

competitivenessinemergingmarkets.TheMNCswhoexporthighpricedpatented

drugshavenosuchproblem.Inthe11thplanrecommendationhadbeenmadefora

Rs.100croresassistanceforassistingSMEstobuildexportcompetitive

infrastructureandtechnologysupport.Howeverthesamecouldnotbe

implemented.Thereisneedtodoitnowforthe12thPlan.

1.5.1ApexAuthoritytoControlPrices,Quality&SupplyofDrugs

NPPAismandatedforpricingofdrugsandDCGIistheauthorityforensuring

standardsformanufacturingandqualityofdrugsinadditiontothebasicelementof

introducingthedrugitselfinthecountryforanytherapeutictreatment.Aneedfora