Locks Form ST 120 Resale

User Manual: Locks Resale Mayflower Sales - Your Source for Architectural Hardware & Locksmith Supplies

Open the PDF directly: View PDF ![]() .

.

Page Count: 2

New York State Department of Taxation and Finance

New York State and Local Sales and Use Tax

Resale Certificate

Mark an X in the appropriate box: Single-use certificate Blanket certificate

Temporary vendors must issue a single-use certificate.

ST-120

(1/11)

Certification: I certify that the above statements are true, complete, and correct, and that no material information has been omitted. I make these

statements and issue this exemption certificate with the knowledge that this document provides evidence that state and local sales or use taxes

do not apply to a transaction or transactions for which I tendered this document and that willfully issuing this document with the intent to evade

any such tax may constitute a felony or other crime under New York State Law, punishable by a substantial fine and a possible jail sentence. I

understand that this document is required to be filed with, and delivered to, the vendor as agent for the Tax Department for the purposes of Tax

Law section 1838 and is deemed a document required to be filed with the Tax Department for the purpose of prosecution of offenses. I also

understand that the Tax Department is authorized to investigate the validity of tax exclusions or exemptions claimed and the accuracy of any

information entered on this document.

Name of seller Name of purchaser

Street address Street address

City State ZIP code City State ZIP code

Purchaser information – please type or print

I am engaged in the business of and principally sell

(Contractors may not use this certificate to purchase materials and supplies.)

Part 1 – To be completed by registered New York State sales tax vendors

I certify that I am:

a New York State vendor (including a hotel operator or a dues or admissions recipient), show vendor or entertainment vendor. My

valid Certificate of Authority number is

a New York State temporary vendor. My valid Certificate of Authority number is and expires on

I am purchasing:

A. Tangible personal property (other than motor fuel or diesel motor fuel)

• for resale in its present form or for resale as a physical component part of tangible personal property;

• for use in performing taxable services where the property will become a physical component part of the property upon which the

services will be performed, or the property will actually be transferred to the purchaser of the taxable service in conjunction with the

performance of the service; or

B. A service for resale, including the servicing of tangible personal property held for sale.

Part 2 – To be completed by non-New York State purchasers

I certify that I am not registered nor am I required to be registered as a New York State sales tax vendor. I am registered to collect sales

tax or value added tax (VAT) in the following state/jurisdiction and have

been issued the following registration number (If sales tax or VAT registration is not

required and a registration number is not issued by your home jurisdiction, indicate the location of your business and write not applicable on

the line requesting the registration number.)

I am purchasing:

C. Tangible personal property (other than motor fuel or diesel motor fuel) for resale, and it is being delivered directly by the seller to my

customer or to an unaffiliated fulfillment services provider in New York State.

D. Tangible personal property for resale that will be resold from a business located outside New York State.

Type or print name and title of owner, partner, or authorized person of purchaser

Signature of owner, partner, or authorized person of purchaser Date prepared

Substantial penalties will result from misuse of this certificate.

To the purchaser:

You may not use this certificate to purchase items or services that are not for resale. If you purchase tangible personal property or services

for resale, but use or consume the tangible personal property or services yourself in New York State, you must report and pay the unpaid tax

directly to New York State. Any misuse of this certificate will result in tax liabilities and substantial penalty and interest.

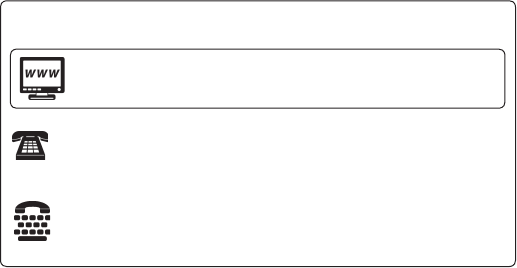

Need help?

Sales Tax Information Center: (518) 485-2889

To order forms and publications: (518) 457-5431

Text Telephone (TTY) Hotline

(for persons with hearing and

speech disabilities using a TTY): (518) 485-5082

Internet access: www.tax.ny.gov

(for information, forms, and publications)

Form ST-120, Resale Certificate, is a sales tax exemption certificate.

This certificate is only for use by a purchaser who:

A – is registered as a New York State sales tax vendor and has a

valid Certificate of Authority issued by the Tax Department and

is making purchases of tangible personal property (other than

motor fuel or diesel motor fuel) or services that will be resold or

transferred to the purchaser’s customers, or

B – is not required to be registered with the New York State Tax

Department;

– is registered with another state, the District of Columbia, a

province of Canada, or other country, or is located in a state,

province, or country which does not require sellers to register for

sales tax or VAT purposes; and

– is purchasing items for resale that will be either:

1) delivered by the seller to the purchaser’s customer or to an

unaffiliated fulfillment service provider located in New York

State, or

2) delivered to the purchaser in New York State, but resold from

a business located outside the state.

Note: For purposes of 1) above, delivery by the seller includes

delivery in the seller’s own vehicle or by common carrier,

regardless of who arranges for the transportation.

Non-New York State purchasers: registration

requirements

If, among other things, a purchaser has any place of business or

salespeople in New York State, or owns or leases tangible personal

property in the State, the purchaser is required to be registered for New

York State sales tax.

A business must register (unless the business can rebut the statutory

presumption as described in TSB-M-08(3.1)S, Additional Information

on How Sellers May Rebut the New Presumption Applicable to

the Definition of Sales Tax Vendor as Described in TSB-M-08(3)S)

for New York State sales tax if the business enters into agreements

with residents of New York State under which the residents

receive consideration for referring potential customers to the

business by links on a Web site or otherwise, and the value

of the sales in New York State made by the business through

those agreements totals more than $10,000 in the preceding

four sales tax quarters. See TSB-M-08(3)S, New Presumption Applicable

to Definition of Sales Tax Vendor, and TSB-M-08(3.1)S.

Also see TSB-M-09(3)S, Definition of a Sales Tax Vendor is Expanded

to Include Out-of-State Sellers with Related Businesses in New

York State, for information on sales tax registration requirements for

out-of-state businesses with New York affiliates.

A purchaser who is not otherwise required to be registered for New York

State sales tax may purchase fulfillment services from an unaffiliated

New York fulfillment service provider and have its tangible personal

property located on the premises of the provider without being required

to be registered for sales tax in New York State.

If you need help determining if you are required to register because you engage

in activity in New York State, contact the department (see Need help?).

If you meet the registration requirements and engage in business

activities in New York State without possessing a valid Certificate of

Authority, you will be subject to penalty of up to $500 for the first day on

which you make a sale or purchase, and up to $200 for each additional

day, up to a maximum of $10,000.

Limitations on use

Contractors cannot use this certificate. They must either:

• issue Form ST-120.1, Contractor Exempt Purchase Certificate, if the

tangible personal property being purchased qualifies for exemption

as specified by the certificate, or

• issue Form AU-297, Direct Payment Permit, or

• pay sales tax at the time of purchase.

Contractors are entitled to a refund or credit of sales tax paid on

materials used in repairing, servicing or maintaining real property, if

the materials are transferred to the purchaser of the taxable service

in conjunction with the performance of the service. For additional

information, see Publication 862, Sales and Use Tax Classifications of

Capital Improvements and Repairs to Real Property.

ST-120 (1/11) (back) Instructions

To the Purchaser

Enter all the information requested on the front of this form.

You may mark an X in the Blanket certificate box to cover all purchases

of the same general type of property or service purchased for resale.

If you do not mark an X in the Blanket certificate box, the certificate

will be deemed a Single-use certificate. Temporary vendors may not

issue a blanket certificate. A temporary vendor is a vendor (other than a

show or entertainment vendor), who, in no more than two consecutive

quarters in any 12-month period, makes sales of tangible personal

property or services that are subject to tax.

This certificate does not exempt prepaid sales tax on cigarettes. This

certificate may not be used to purchase motor fuel or diesel motor fuel.

Misuse of this certificate

Misuse of this exemption certificate may subject you to serious civil and

criminal sanctions in addition to the payment of any tax and interest

due. These include:

• A penalty equal to 100% of the tax due;

• A $50 penalty for each fraudulent exemption certificate issued;

• Criminal felony prosecution, punishable by a substantial fine and a

possible jail sentence; and

• Revocation of your Certificate of Authority, if you are required to

be registered as a vendor. See TSB-M-09(17)S, Amendments that

Encourage Compliance with the Tax Law and Enhance the Tax

Department’s Enforcement Ability, for more information.

To the Seller

If you are a New York State registered vendor and accept an exemption

document, you will be protected from liability for the tax, if the certificate

is valid.

The certificate will be considered valid if it was:

• accepted in good faith;

• in the vendor’s possession within 90 days of the transaction; and

• properly completed (all required entries were made).

A certificate is accepted in good faith when a seller has no knowledge

that the exemption certificate is false or is fraudulently given, and

reasonable ordinary due care is exercised in the acceptance of the

certificate.

You must get a properly completed exemption certificate from your

customer no later than 90 days after the delivery of the property or the

performance of the service. When you receive a certificate after the

90 days, both you and the purchaser are subject to the burden of proving

that the sale was exempt, and additional documentation may be required.

An exemption certificate received on time that is not properly completed

will be considered satisfactory if the deficiency is corrected within a

reasonable period. You must also maintain a method of associating an

invoice (or other source document) for an exempt sale made to a customer

with the exemption certificate you have on file from that customer.

Invalid exemption certificates – Sales transactions which are not

supported by valid exemption certificates are deemed to be taxable

retail sales. The burden of proof that the tax was not required to be

collected is upon the seller.

Retention of exemption certificates - You must keep this certificate

for at least three years after the due date of the return to which it

relates, or the date the return was filed, if later.