8:19 AM 401k Education Guide

User Manual: Pdf

Open the PDF directly: View PDF ![]() .

.

Page Count: 12

PayPal 401(k)

Savings Plan

PayPal encourages you to invest in yourself and your future by participating in the PayPal

401(k) Savings Plan (the “Plan”).

In order to help build toward financial stability in your retirement years, it is important to take

action now.

Our retirement plan service provider, Schwab Retirement Plan Services, Inc., provides tools

and resources to help you make informed choices about your retirement needs, investment

alternatives, and the benefits of long-term saving. The Plan is designed to help you make

pre-tax and/or Roth 401(k) contributions and invest them according to your personal level of

risk tolerance and timeline to retirement. In addition, PayPal provides a matching contribution*

to help with your savings goals.

This guide will assist you as you explore:

• What to consider as you build your retirement savings

• How to review your current financial objectives to help attain your retirement goals

• How to choose investments from those available in the Plan

• How to take action

Additionally, whether you are joining the Plan for the first time, currently participating in the

Plan or approaching retirement and looking for guidance on retirement options, a Participant

Services Representative is available to assist you every step of the way. PayPal considers this

Plan a very important benefit. We sincerely hope you will take this opportunity to save and

invest in your financial future.

*The employer contribution is paid on a pre-tax basis and may be taxable at withdrawal.

Welcome PayPal U.S. Employees

2 PayPal 401(k) Savings Plan Highlights

5 Investment Options

6 Investment Strategies

7 Act Now! Enroll.

Table of Contents

THE TIME TO BEGIN IS NOW.

The earlier you start, the longer your money has the

opportunity to work for you.

**Your company may have a maximum match as well as other

restrictions. The employer contribution is paid on a pre-tax basis

and may be taxable at withdrawal.

†Contributions to workplace retirement plans are typically on a

pre-tax basis; if you make Roth 401(k) contributions, the benefits

of pre-tax contributions are not applicable.

Hypothetical examples are for illustrative purposes only and are

not intended to represent the past or future performance of any

specific investment. The balances shown represent the amount

contributed and the interest compounded daily. Assumes a

hypothetical average rate of return of 6.5%, reinvestment of any

dividends and any capital gains, and no current taxes paid on

any earnings in a retirement plan account. Schwab Retirement

Plan Services, Inc. does not provide tax or legal advice.

(1114-7239)

Hypothetical earnings

Employer Match*

Employee Contributions†

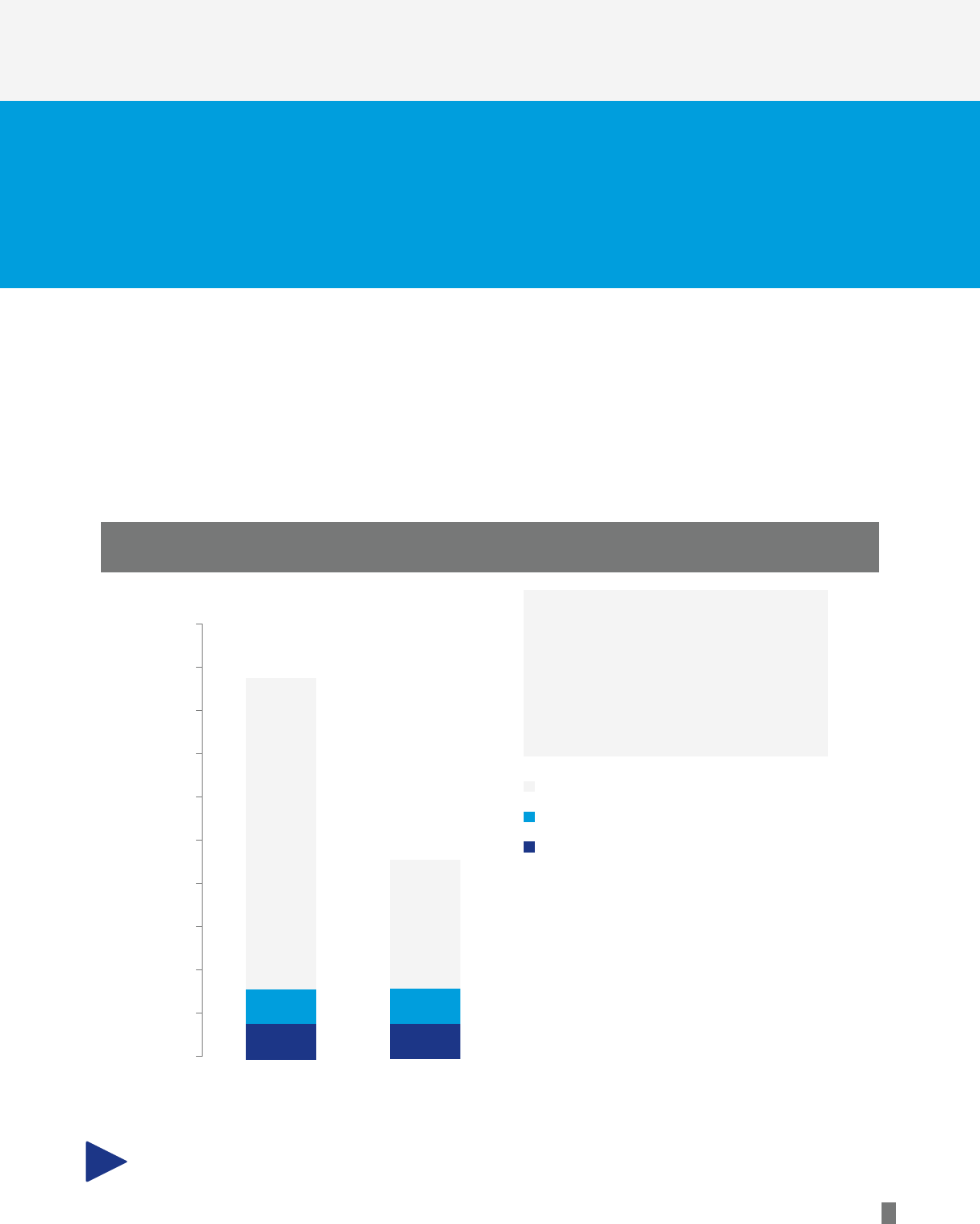

$294,290

$81,136

$81,136

Contributions Start at

Age 35; Stop at Age 65.

Withdrawals Start at

Age 65.

Jennifer

$874,513

Brian

$456,562

$712,241

$81,136

$81,136

Contributions Start at

Age 25; Stop at Age 55.

Withdrawals Start at

Age 65.

$1,000,000

$900,000

$800,000

$700,000

$600,000

$500,000

$400,000

$300,000

$200,000

$100,000

$-

1

The Power of Compounding

Although it is never too late to start saving for retirement, starting early is one of the best ways to help build retirement

savings. The sooner you start saving, the more you may benefit from tax-deferred compounding.

Start Early. It’s Important!

Jennifer and Brian both saved the same amount over 30 years. However, she started at age 25; he started at age 35.

Jennifer’s savings earned 10 additional years, worth of compound interest by the time they both started withdrawals at age

65. Jennifer benefited from starting early. When will YOU start saving?

Start Early. It’s Important.

Time in the market is more important than timing the market.

Assumptions for Both Individuals

$50,000 Annual Salary

$0 Starting Balance

4% Matching Contributions**

4% Employee Contributions†

2% Annual Salary Increase

6.5% Annual Return

Totals represent hypothetical balances at age 65

2

Plan Highlights

Eligibility and Enrollment

PayPal employees are immediately eligible to participate

in the Plan. Employees must be at least 18 years old

to participate.

Your Contributions

You can make pre-tax and/or Roth 401(k) contributions, up

to 50% of your earned compensation per pay period.

• Federal law limits the amount you can contribute every

year; the 2016 limit is $18,000.

• If you will be age 50 years or older by December 31,

2016, you may make an additional catch-up contribution

to the Plan. In 2016, the catch-up limit is $6,000.

• The Plan includes a Roth 401(k) option. If you decide to

make Roth 401(k) contributions, they will be deducted

from your paycheck after taxes. Your contributions and

any earnings may grow tax-free, and you will not pay

taxes on the money when it’s withdrawn—provided that

any distribution from the Plan account occurs at least

five years following the year you make your first Roth

401(k) contribution, and you have reached age 59½ or

have become disabled.

• You may elect two separate 401(k) deferrals—one

for your regular earnings and one for your bonus

earnings. These deferrals can be made on a pre-tax

basis, Roth 401(k) basis, or a combination of both.

Currently, the deferral rate you have designated to

your regular earnings also applies to your bonus

unless you change it.

You can change your contribution rate at any time by

calling Participant Services at 800-724-7526 or by visiting

workplace.schwab.com. Changes will be made as soon

as administratively feasible.

Company Contributions

To help you save more for the future, PayPal will make a

Safe Harbor Match of 100% of your earned compensation

you contribute, up to 4% of your earned compensation.

The employer contribution is paid on a pre-tax basis and

may be taxable at withdrawal.

Vesting

Vesting is your ownership of your account. You are

always 100% vested in your own contributions, any

earnings on your own contributions, the Safe Harbor

Match contribution and any earnings, and any rollovers

you make to your account.

Rollovers

You can roll over account balances from other employer-

sponsored qualified 401(k) plans into your Plan account.

You can obtain a copy of the Rollover Form online at

workplace.schwab.com or by calling Participant

Services at 800-724-7526.

Withdrawals

The Plan is designed primarily to help you save for

retirement; there are IRS restrictions on when money may

be withdrawn from your account. The IRS does, however,

recognize certain events may present a need for you to

access your savings. Under the following circumstances,

you may withdraw money from your account.

Retirement

You can withdraw money from your Plan account when

you reach the normal retirement age of 65.

Loans

You may borrow from your vested account balance.

Loan repayments are made through salary deductions

each pay period.

• The minimum loan amount is $1,000.

• The maximum loan amount is $50,000 or 50% of your

vested balance, whichever is less.

• The interest rate for the loan is the Prime Rate at the

time the loan is taken.

• One outstanding loan is allowed at any time.

• The maximum term for a general loan is 5 years, and

10 years for a residential loan.

Most of your retirement income will come from

savings accumulated during your working years.

The PayPal 401(k) Savings Plan can help you

build your retirement savings and help you stay on

track toward your retirement goals.

3

In Service

You can withdraw money from your Plan account while you

are still employed by PayPal if you are at least age 59½.

These withdrawals are allowed under certain circumstances.

Hardship Withdrawals

A “financial hardship” is defined as a heavy and immediate

financial need that cannot be satisfied by other resources

available to you, including taking a loan from the vested

portion of your Plan account. You may be eligible to

withdraw a portion of your account balance if you

experience a financial hardship. Qualified reasons for a

hardship withdrawal include:

• to prevent eviction from, or foreclosure of, your

primary residence;

• to purchase a primary residence;

• to pay for post-secondary education for you or an

immediate family member;

• to pay for uninsured medical expenses;

• to repair damage to your primary residence; and

• to cover funeral expenses.

Hardship withdrawals are subject to ordinary income tax

and may be subject to a 10% federal penalty. Residents of

certain states may also be subject to state penalties. You

will be prohibited from making elective contributions to the

Plan for at least six months after receipt of the hardship

distribution. Safe Harbor Match dollars are not eligible for

hardship withdrawals.

Termination

You may receive all of your vested balance of your account

upon termination of employment. Please note: If your vested

account balance upon termination, or at any point thereafter,

is $1,000 or less, including rollovers, your account will be

distributed to you as a single-sum cash distribution unless

you select another distribution option within 90 days of

termination. Taxes and penalties may apply.

If your vested account balance, including rollovers, is more

than $1,000 but less than $5,000, and you fail to elect either

a lump sum or rollover, the balance will be rolled over to a

Rollover IRA administered by Charles Schwab Bank.‡

If your vested account balance, including rollovers, is

greater than $5,000, your balance will remain in the Plan

until you request a distribution.

Disability

If you terminate your employment with PayPal because

you become permanently disabled, you are allowed to

withdraw your money.

Death

In the event of your death, your account balance will be

paid to your beneficiary as you have designated on your

account with Schwab Retirement Plan Services, Inc. If

there is no beneficiary on file with Schwab Retirement Plan

Services, Inc., your account balance will be paid per the

terms specified in the Plan Document.

For more information about your withdrawal options, call

Participant Services at 800-724-7526 to speak with a

Participant Services Representative.

‡Rollover funds in the Schwab Bank IRA are invested in an FDIC-

insured money market deposit account at Charles Schwab Bank.

Any account balances in Roth 401(k) sources will be rolled over into a

Roth IRA, and the five year qualification period will start over.

This information is not intended to be a substitute for specific

individualized tax, legal or investment planning advice. Where specific

advice is necessary or appropriate, you should consult with a qualified

tax advisor, CPA, Financial Planner or Investment Manager.

The above highlights section is only a brief overview of the Plan’s features

and does not constitute a legally binding document. A more detailed

Summary Plan Description is available at workplace.schwab.com. Please

review it carefully for additional information about the specific provisions

of the Plan. If you have further questions, call 800-724-7526 to speak

with a Participant Services Representative.

Go to workplace.schwab.com to access the Paycheck

Calculator located under the Calculators & Resources section.

This will help you run scenarios to see how different deferral

percentages will impact your take-home pay. You’ll see that with

pre-tax contributions, the net impact on your take-home pay is

much less than the amount you contribute. There are also several

worksheets available that you can use to help determine how

much savings you may need when you retire. This will help you

move from “How much can you save?” to “How much do you

need to save?”

4

Savings Advantages

Since Social Security may not provide enough income during your retirement years and inflation could reduce the

spending power of your savings, it is important to develop a sound retirement plan. Saving through an employer-

sponsored retirement plan is an important step in saving for retirement.

First—Consider the Tax Advantages

Pre-tax contributions: The amount you put into the Plan is deducted from your paycheck before it is taxed. The net

impact on your take-home pay will be less than the amount you are contributing to the Plan.

Tax-deferred earnings: In addition to the advantage of having your pre-tax contributions go into the Plan before taxes on

your pay are calculated, your money may grow tax-deferred. This means any current tax due on any earnings stays in the

Plan and contributes to the compounding in your account. Of course, at retirement the withdrawals you make from your

Plan account will be considered income and can be subject to regular income taxes, depending on your tax bracket at

that time. You may be in a lower tax bracket during retirement and your tax burden may be less than it is today.

Tax-free earnings: You also have an opportunity to have your money grow tax-free with the Roth 401(k). This means

you pay taxes at the time of the contribution. Assuming you meet the withdrawal qualifications, both your Roth 401(k)

contributions and any associated investment earnings are distributed from the Plan tax-free. Some of the factors to

consider include your current tax rate, anticipated tax rate at retirement, and how long you anticipate the money will

stay in your retirement account.

Plus, There Is the Company Contribution

When you ask the question, “How much should I save for retirement?,” invariably you will hear the answer, “As much

as you can!” That may be true, but if you’re looking for a number, consider this: You can contribute from 1% to 50% of

your eligible compensation to the Plan, up to $18,000. If you are 50 years of age or older in 2016 and make the additional

catch-up contribution of $6,000, you can contribute a total of $24,000 in 2016. So, save as much as you can, and

remember, PayPal makes a 4% matching contribution as well.

Three steps to enrollment

Step 1 - Decide how much to save.

Quick Tip!

A note about risk: PayPal has made

available different investments in the

hope of meeting the various savings

and investment goals for all participants.

As you make your investment choices,

keep in mind that there is risk involved.

The funds differ in growth potential and

risk. Pursuant to Department of Labor

Regulation 2550.404c-(b)(2)(i)(B)(1)(i), this

Plan is intended to qualify as an ERISA

404(c) Plan that relieves plan fiduciaries

of liability for any investment losses that

result from investment directions made by

Plan participants.

The values of the target funds will

fluctuate up to and after the target

date. There is no guarantee the funds

will provide adequate income at or

through retirement. Diversification

and asset allocation strategies do not

ensure a profit and cannot protect

against losses in a declining market.

The Funds are subject to market

volatility and risks associated with

the underlying investments. Risks

include exposure to international and

emerging markets, small company

and sector equity securities, and fixed

income securities subject to changes

in inflation, market valuations, liquidity,

prepayments, and early redemption.

The funds are built for investors who

expect to start gradual withdrawals

of fund assets on the target date to

begin covering expenses in retirement.

The principal value of the funds is not

guaranteed at any time.

5

Three steps to enrollment

Step 2 - Decide which investments are right for you.

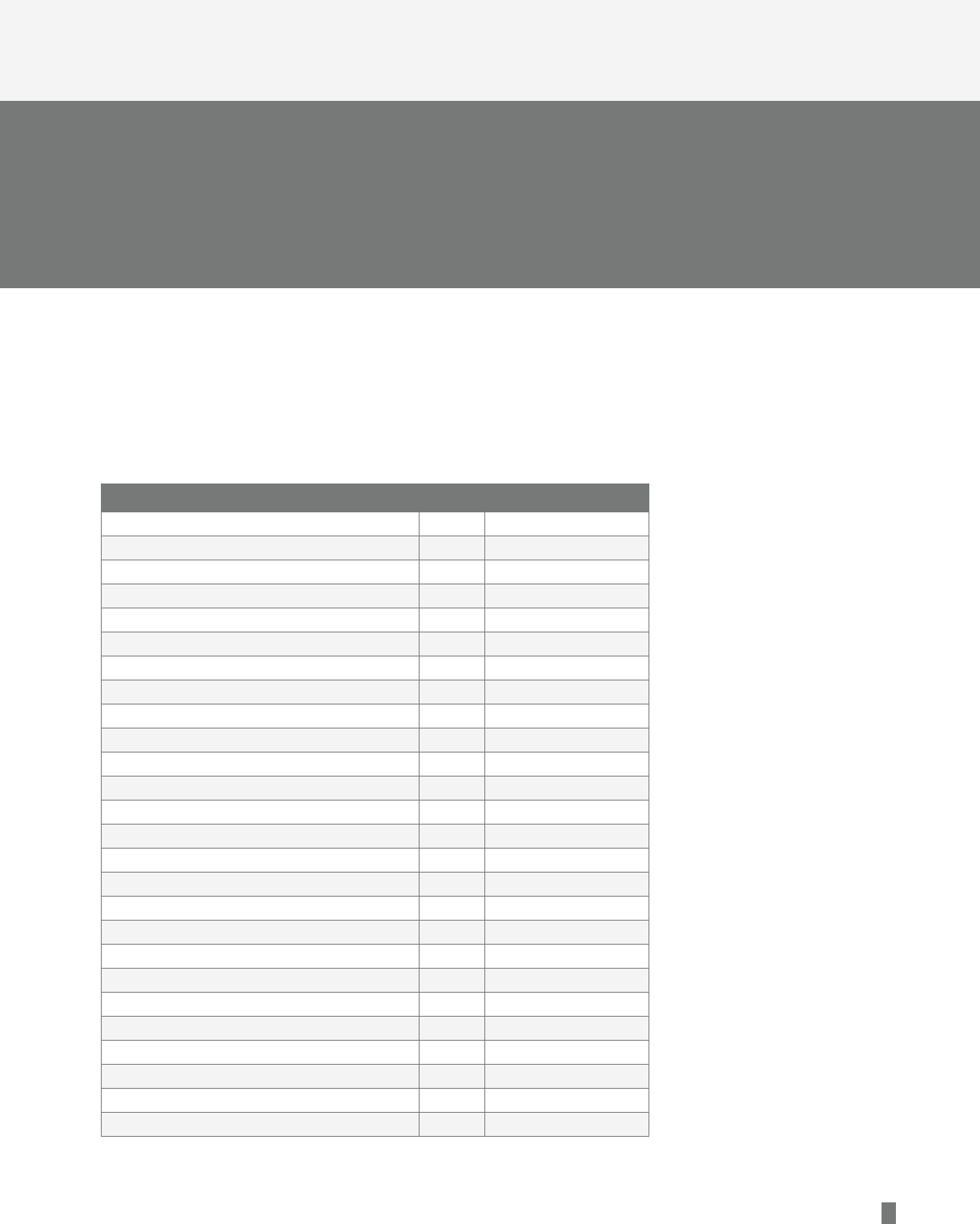

Fund Name Ticker Asset Category

Vanguard Prime Money Market Instl VMRXX Money Market

Galliard Stable Value Fund - PayPal 1 N/A Stable Value

Metropolitan West Total Return Bond I MWTIX Intermediate-Term Bond

Vanguard Total Bond Market Index I VBTIX Intermediate-Term Bond

Dodge & Cox Balanced DODBX Moderate Allocation

Dodge & Cox Stock DODGX Large Value

Harbor Capital Appreciation Fund HACAX Large Growth

Artisan Mid Cap Value Investor ARTQX Mid-Cap Value

Fidelity Spartan Extended Mkt Index Inv FSEMX Mid-Cap Blend

AMG TimesSquare Mid Cap Growth Instl TMDIX Mid-Cap Growth

Boston Partners Small Cap Value II Instl BPSIX Small Value

Morgan Stanley Instl Small Co. Growth IS MFLLX Small Growth

American Funds EuroPacific Growth R6 RERGX Foreign Large Blend

BlackRock EAFE Equity Index Collective T 1 N/A Foreign Large Blend

American Funds Capital World G/I R6 RWIGX World Stock

Schwab Managed Retirement Trust Cl IV 2010 2 N/A Target Retirement

Schwab Managed Retirement Trust Cl IV 2015 2 N/A Target Retirement

Schwab Managed Retirement Trust Cl IV 2020 2 N/A Target Retirement

Schwab Managed Retirement Trust Cl IV 2025 2 N/A Target Retirement

Schwab Managed Retirement Trust Cl IV 2030 2 N/A Target Retirement

Schwab Managed Retirement Trust Cl IV 2035 2 N/A Target Retirement

Schwab Managed Retirement Trust Cl IV 2040 2 N/A Target Retirement

Schwab Managed Retirement Trust Cl IV 2045 2 N/A Target Retirement

Schwab Managed Retirement Trust Cl IV 2050 2 N/A Target Retirement

Schwab Managed Retirement Trust Cl IV 2055 2 N/A Target Retirement

Schwab Managed Retirement Trust Cl IV Income 2 N/A Target Retirement

Investment Options

The following funds are the investment options available in the Plan. If you do not

make investment choices, your account balance will be invested in an age-appropriate

Schwab Managed Retirement Trust Fund™2 based on your expected retirement year,

as determined by the Plan. For more information on choosing the investments that are

right for you, review the Investment Strategies section of this guide.

6

Changing Your Investments

Your contributions will be deducted automatically from

your paycheck and deposited into your account according

to your investment instructions. You may change your

investment elections for future contributions or rebalance

your investments at any time, subject to prospectus

requirements.

Need More Information?

Visit workplace.schwab.com or call and speak with a

Participant Services Representative at 800-724-7526.

Investment Options – Continued

Investment Strategies

We offer different options based on the kind of investor you may be to help you choose your investments. Based on your

answer to the question below, choose one of the following strategies.

Do you have the time or expertise to make investment decisions for your retirement account on your own?

“No, I prefer to do my retirement

investing with some help.”

Target Date Retirement Funds

If you are looking for a single strategy within

the Plan’s retirement savings options, target

date retirement funds may be right for you.

These funds provide an asset allocation

glidepath, are managed by investment

professionals, and are adjusted to become

more conservative over time.

By choosing the fund that most closely

matches your expected retirement date,

as well as other factors important to your

planning objectives and retirement goals, you

set your retirement plan in motion.

To Select the Target Date Retirement Funds:

Go to workplace.schwab.com or call

Participant Services at 800-724-7526 to

access your account or enroll.

We suggest you review your investments at

least annually or whenever there is a change

in life events.

“Yes, I prefer to do my retirement

investing on my own.”

Plan-Selected Funds

If you like making your own investment

decisions, the Plan has a pre-screened group

of funds known as Plan-Selected Funds from

which to choose.

After you review these funds, you can select

the funds in which you’d like to invest and

determine the percentage you want to

allocate to each fund.

You manage your own portfolio.

For help, complete the Investor Profile

Questionnaire at workplace.schwab.com.

To Select Your Own Investments:

Go to workplace.schwab.com or call

800-724-7526 to access your account.

Review/change your contribution rate.

Select your investments from the

Plan-Selected Funds list.

Re-evaluate your financial plan and investment

risk regularly to meet your retirement goals.

7

Three steps to enrollment

Step 3 - Act now! Enroll.

Enroll Online at

workplace.schwab.com.

• Go to the Plan Participant Login box and click on

New User.

• Enter your Social Security number as your Login ID

(no dashes).

• Enter your default password, which is your four-

digit month and day of birth (e.g., if your birthday is

November 30, your default password is 1130).

• Click Login.

Once you are logged in, you’ll be asked to create a new

Login ID and password.

Enroll by Phone at 800-724-7526.

• Enter your Social Security number, then hit the “#” key.

• You’ll be asked to enter your password. Press “*1”

and you will bypass this step and be transferred to a

Participant Services Representative.

• The Representative will ask you some questions to

verify your identity.

• Once your identity has been verified, tell them you

would like to enroll in the PayPal 401(k) Savings Plan.

Enroll on Your Mobile Device

The Schwab Workplace Retirement app is available for

iPad®

, iPhone®

, Android™, or Kindle Fire.

Get on-the-go access to your retirement savings account:

• Enroll in your plan.

• Check your progress—see how much you’re saving

and how your balance may be changing.

• Monitor your personal performance.

• Make contribution elections.

• Set up investment instructions for future contributions.

• Securely access the full website without logging

in again.

• Read the latest market news.

Visit workplace.schwab.com/mobile today to download

the Schwab Workplace Retirement app.

Don’t Forget to Complete Your

Beneciary Designation Online.

• It is important and only takes a minute to go online and

designate the beneficiary for your Plan account.

• You may also designate your beneficiary via phone by

speaking to a Participant Services Representative at

800-724-7526.

This lets Schwab Retirement Plan Services, Inc. and

PayPal know who should receive your account balance in

the event of your death.

Feature availability depends on both plan and participant settings.

Requires a wireless signal or mobile connection.

System availability and response times are subject to market

conditions and mobile connection limitations.

Apple, the Apple logo, iPad, and iPhone are trademarks of Apple Inc.

registered in the U.S. and other countries.

Android is a trademark of Google Inc. Use of this trademark is subject

to Google Permissions.

Kindle, Kindle Fire, and Amazon are trademarks of Amazon.com, Inc.

or its affiliates.

Access to electronic services may be limited or unavailable during

periods of peak demand, market volatility, systems upgrades,

maintenance, or for other reasons.

8

Notes

9

Notes

1 This investment option is a collective trust and is not a registered investment company product.

2 The Schwab Managed Retirement Trust Funds™ and Schwab Institutional Trust Funds® are collective trust funds maintained by Charles Schwab

Bank (“Schwab Bank”), as trustee of the Funds. They are available for investment only by eligible retirement plans and entities. Schwab Bank

Collective Trust Funds (“Funds”) are not insured by FDIC or any other type of deposit insurance; are not deposits or other obligations of, and are

not guaranteed by Schwab Bank or any of its affiliates; and involve investment risks, including possible loss of principal invested. The Funds are

not mutual funds and are exempt from registration and regulation under the Investment Company Act of 1940 (“1940 Act”), and their units are not

registered under the Securities Act of 1933, or applicable securities laws of any state or other jurisdiction. Unit holders of the Funds are not entitled to

the protections of the 1940 Act. The decision to invest in the Funds should be carefully considered. The Funds’ unit values will fluctuate and may be

worth more or less when redeemed, so unit holders may lose money. The Funds are not sold by prospectus and are not available for investment by

the public; Fund prices are not quoted in newspapers.

Schwab Retirement Plan Services, Inc. provides recordkeeping and related services with respect to retirement plans and has provided this

communication to you as part of the recordkeeping services it provides to the Plan.

CC0391665 (XXXX-XXXX) GDE89466PAY-01 (12/15)

00159516