A Practical Guide To Quantitative Portfolio Trading

User Manual: Pdf

Open the PDF directly: View PDF ![]() .

.

Page Count: 743 [warning: Documents this large are best viewed by clicking the View PDF Link!]

- Introduction

- I Quantitative trading in classical economics

- Risk, preference, and valuation

- Introduction to asset management

- Portfolio management

- Portfolio construction

- A market equilibrium theory of asset prices

- Risk and return analysis

- Introduction to financial time series analysis

- Prologue

- An overview of data analysis

- Asset returns and their characteristics

- Introducing the volatility process

- II Statistical tools applied to finance

- Filtering and smoothing techniques

- Presenting time series analysis

- Basic principles of linear time series

- Linear time series

- Forecasting

- Nonstationarity and serial correlation

- Multivariate time series

- Some conditional heteroscedastic models

- Exponential smoothing and forecasting data

- Filtering and forecasting with wavelet analysis

- III Quantitative trading in inefficient markets

- Introduction to quantitative strategies

- Describing quantitative strategies

- Portfolio management under constraints

- Introduction

- Robust portfolio allocation

- Empirical log-optimal portfolio selections

- A simple example

- Value at Risk

- IV Quantitative trading in multifractal markets

- The fractal market hypothesis

- Fractal structure in the markets

- The R/S analysis

- Hurst exponent estimation methods

- Testing for market efficiency

- Presenting the main controversy

- Using the Hurst exponent to define the null hypothesis

- Measuring temporal correlation in financial data

- Applying R/S analysis to financial data

- Some critics at Lo's modified R/S statistic

- The problem of non-stationary and dependent increments

- Some results on measuring the Hurst exponent

- The multifractal markets

- Multifractality as a new stylised fact

- Holder exponent estimation methods

- The need for time and scale dependent Hurst exponent

- Local Holder exponent estimation methods

- Analysing the multifractal markets

- Some multifractal models for asset pricing

- Systematic trading

- The fractal market hypothesis

- V Numerical Analysis

- Presenting some machine-learning methods

- Introducing Differential Evolution

- Introduction

- Calibration to implied volatility

- Nonlinear programming problems with constraints

- Handling the constraints

- The proposed algorithm

- Describing some benchmarks

- Minimisation of the sphere function

- Minimisation of the Rosenbrock function

- Minimisation of the step function

- Minimisation of the Rastrigin function

- Minimisation of the Griewank function

- Minimisation of the Easom function

- Image from polygons

- Minimisation problem g01

- Maximisation problem g03

- Maximisation problem g08

- Minimisation problem g11

- Minimisation of the weight of a tension/compression spring

- Introduction to CUDA Programming in Finance

- Appendices

- Review of some mathematical facts

- Some probabilities

- Some definitions

- Random variables

- Introducing stochastic processes

- The characteristic function and moments

- Conditional moments

- About fractal analysis

- Some continuous variables and their distributions

- Some results on Normal sampling

- Some random sampling

- Stochastic processes and Time Series

- Defining market equilibrirum and asset prices

- Pricing and hedging options

- Some results on signal processing

Quantitative Analytics

A Practical Guide To Quantitative Portfolio

Trading

Daniel Bloch

30th of December 2014

The copyright to this computer software and documentation is the property of Quant Finance Ltd. It may be

used and/or copied only with the written consent of the company or in accordance with the terms and conditions

stipulated in the agreement/contract under which the material has been supplied.

Copyright ©2015 Quant Finance Ltd

Quantitative Analytics, London

Created: 14 January 2015

A Practical Guide To Quantitative Portfolio Trading

Daniel BLOCH 1

QUANT FINANCE LTD

eBook

30th of December 2014

Version 1.01

1db@quantfin.eu

Abstract

We discuss risk, preference and valuation in classical economics, which led academics to develop a theory of

market prices, resulting in the general equilibrium theories. However, in practice, the decision process does not follow

that theory since the qualitative aspect coming from human decision making process is missing. Further, a large

number of studies in empirical finance showed that financial assets exhibit trends or cycles, resulting in persistent

inefficiencies in the market, that can be exploited. The uneven assimilation of information emphasised the multifractal

nature of the capital markets, recognising complexity. New theories to explain financial markets developed, among

which is a multitude of interacting agents forming a complex system characterised by a high level of uncertainty.

Recently, with the increased availability of data, econophysics emerged as a mix of physical sciences and economics

to get the best of both world, in view of analysing more deeply assets’ predictability. For instance, data mining and

machine learning methodologies provide a range of general techniques for classification, prediction, and optimisation

of structured and unstructured data. Using these techniques, one can describe financial markets through degrees

of freedom which may be both qualitative and quantitative in nature. In this book we detail how the growing use

of quantitative methods changed finance and investment theory. The most significant benefit being the power of

automation, enforcing a systematic investment approach and a structured and unified framework. We present in a

chronological order the necessary steps to identify trading signals, build quantitative strategies, assess expected returns,

measure and score strategies, and allocate portfolios.

Quantitative Analytics

I would like to thank my wife and children for their patience and support during this adventure.

1

Quantitative Analytics

I would like to thank Antoine Haddad and Philippe Ankaoua for giving me the opportunity, and

the means, of completing this book. I would also like to thank Sebastien Gurrieri for writing a

section on CUDA programming in finance.

2

Contents

0.1 Introduction ................................................ 21

0.1.1 Preamble ............................................. 21

0.1.2 An overview of quantitative trading ............................... 21

I Quantitative trading in classical economics 25

1 Risk, preference, and valuation 26

1.1 A brief history of ideas .......................................... 26

1.2 Solving the St. Petersburg paradox .................................... 28

1.2.1 The simple St. Petersburg game ................................. 28

1.2.2 The sequential St. Petersburg game ............................... 29

1.2.3 Using time averages ....................................... 30

1.2.4 Using option pricing theory ................................... 32

1.3 Modelling future cashflows in presence of risk .............................. 33

1.3.1 Introducing the discount rate ................................... 33

1.3.2 Valuing payoffs in continuous time ............................... 34

1.3.3 Modelling the discount factor .................................. 36

1.4 The pricing kernel ............................................. 38

1.4.1 Defining the pricing kernel .................................... 39

1.4.2 The empirical pricing kernel ................................... 40

1.4.3 Analysing the expected risk premium .............................. 41

1.4.4 Infering risk premium from option prices ............................ 42

1.5 Modelling asset returns .......................................... 43

1.5.1 Defining the return process .................................... 43

1.5.2 Valuing potfolios ......................................... 44

1.5.3 Presenting the factor models ................................... 46

1.5.3.1 The presence of common factors ........................... 46

1.5.3.2 Defining factor models ................................ 46

1.5.3.3 CAPM: a one factor model .............................. 47

1.5.3.4 APT: a multi-factor model ............................... 48

1.6 Introducing behavioural finance ..................................... 48

1.6.1 The Von Neumann and Morgenstern model ........................... 49

1.6.2 Preferences ............................................ 50

1.6.3 Discussion ............................................ 52

1.6.4 Some critics ............................................ 53

1.7 Predictability of financial markets .................................... 54

1.7.1 The martingale theory of asset prices .............................. 54

1.7.2 The efficient market hypothesis ................................. 55

3

Quantitative Analytics

1.7.3 Some major critics ........................................ 56

1.7.4 Contrarian and momentum strategies .............................. 57

1.7.5 Beyond the EMH ......................................... 59

1.7.6 Risk premia and excess returns .................................. 62

1.7.6.1 Risk premia in option prices .............................. 62

1.7.6.2 The existence of excess returns ............................ 63

2 Introduction to asset management 64

2.1 Portfolio management ........................................... 64

2.1.1 Defining portfolio management ................................. 64

2.1.2 Asset allocation .......................................... 66

2.1.2.1 Objectives and methods ................................ 66

2.1.2.2 Active portfolio strategies ............................... 68

2.1.2.3 A review of asset allocation techniques ........................ 69

2.1.3 Presenting some trading strategies ................................ 70

2.1.3.1 Some examples of behavioural strategies ....................... 70

2.1.3.2 Some examples of market neutral strategies ..................... 71

2.1.3.3 Predicting changes in business cycles ......................... 73

2.1.4 Risk premia investing ....................................... 74

2.1.5 Introducing technical analysis .................................. 75

2.1.5.1 Defining technical analysis .............................. 75

2.1.5.2 Presenting a few trading indicators .......................... 77

2.1.5.3 The limitation of indicators .............................. 79

2.1.5.4 The risk of overfitting ................................. 79

2.1.5.5 Evaluating trading system performance ........................ 80

2.2 Portfolio construction ........................................... 80

2.2.1 The problem of portfolio selection ................................ 81

2.2.1.1 Minimising portfolio variance ............................. 81

2.2.1.2 Maximising portfolio return .............................. 83

2.2.1.3 Accounting for portfolio risk ............................. 84

2.3 A market equilibrium theory of asset prices ............................... 85

2.3.1 The capital asset pricing model .................................. 85

2.3.1.1 Markowitz solution to the portfolio allocation problem ................ 85

2.3.1.2 The Sharp-Lintner CAPM ............................... 87

2.3.1.3 Some critics and improvements of the CAPM .................... 89

2.3.2 The growth optimal portfolio ................................... 91

2.3.2.1 Discrete time ...................................... 91

2.3.2.2 Continuous time .................................... 95

2.3.2.3 Discussion ....................................... 99

2.3.2.4 Comparing the GOP with the MV approach ..................... 99

2.3.2.5 Time taken by the GOP to outperfom other portfolios ................ 102

2.3.3 Measuring and predicting performances ............................. 102

2.3.4 Predictable variation in the Sharpe ratio ............................. 104

2.4 Risk and return analysis .......................................... 105

2.4.1 Some financial meaning to alpha and beta ............................ 105

2.4.1.1 The financial beta ................................... 105

2.4.1.2 The financial alpha .................................. 107

2.4.2 Performance measures ...................................... 107

2.4.2.1 The Sharpe ratio .................................... 108

2.4.2.2 More measures of risk ................................. 109

4

Quantitative Analytics

2.4.2.3 Alpha as a measure of risk ............................... 109

2.4.2.4 Empirical measures of risk .............................. 110

2.4.2.5 Incorporating tail risk ................................. 111

2.4.3 Some downside risk measures .................................. 111

2.4.4 Considering the value at risk ................................... 113

2.4.4.1 Introducing the value at risk .............................. 113

2.4.4.2 The reward to VaR ................................... 114

2.4.4.3 The conditional Sharpe ratio ............................. 114

2.4.4.4 The modified Sharpe ratio ............................... 114

2.4.4.5 The constant adjusted Sharpe ratio .......................... 115

2.4.5 Considering drawdown measures ................................ 115

2.4.6 Some limitation .......................................... 117

2.4.6.1 Dividing by zero .................................... 117

2.4.6.2 Anomaly in the Sharpe ratio .............................. 117

2.4.6.3 The weak stochastic dominance ............................ 118

3 Introduction to financial time series analysis 119

3.1 Prologue .................................................. 119

3.2 An overview of data analysis ....................................... 120

3.2.1 Presenting the data ........................................ 120

3.2.1.1 Data description .................................... 120

3.2.1.2 Analysing the data ................................... 120

3.2.1.3 Removing outliers ................................... 120

3.2.2 Basic tools for summarising and forecasting data ........................ 121

3.2.2.1 Presenting forecasting methods ............................ 121

3.2.2.2 Summarising the data ................................. 122

3.2.2.3 Measuring the forecasting accuracy .......................... 125

3.2.2.4 Prediction intervals .................................. 127

3.2.2.5 Estimating model parameters ............................. 128

3.2.3 Modelling time series ....................................... 128

3.2.3.1 The structural time series ............................... 128

3.2.3.2 Some simple statistical models ............................ 129

3.2.4 Introducing parametric regression ................................ 131

3.2.4.1 Some rules for conducting inference ......................... 132

3.2.4.2 The least squares estimator .............................. 132

3.2.5 Introducing state-space models .................................. 135

3.2.5.1 The state-space form .................................. 135

3.2.5.2 The Kalman filter ................................... 136

3.2.5.3 Model specification .................................. 138

3.3 Asset returns and their characteristics .................................. 138

3.3.1 Defining financial returns ..................................... 138

3.3.1.1 Asset returns ...................................... 139

3.3.1.2 The percent returns versus the logarithm returns ................... 141

3.3.1.3 Portfolio returns .................................... 141

3.3.1.4 Modelling returns: The random walk ......................... 142

3.3.2 The properties of returns ..................................... 143

3.3.2.1 The distribution of returns ............................... 143

3.3.2.2 The likelihood function ................................ 144

3.3.3 Testing the series against trend .................................. 144

3.3.4 Testing the assumption of normally distributed returns ..................... 146

5

Quantitative Analytics

3.3.4.1 Testing for the fitness of the Normal distribution ................... 146

3.3.4.2 Quantifying deviations from a Normal distribution .................. 147

3.3.5 The sample moments ....................................... 149

3.3.5.1 The population mean and volatility .......................... 149

3.3.5.2 The population skewness and kurtosis ........................ 150

3.3.5.3 Annualisation of the first two moments ........................ 151

3.4 Introducing the volatility process ..................................... 152

3.4.1 An overview of risk and volatility ................................ 152

3.4.1.1 The need to forecast volatility ............................. 152

3.4.1.2 A first decomposition ................................. 153

3.4.2 The structure of volatility models ................................ 153

3.4.2.1 Benchmark volatility models ............................. 155

3.4.2.2 Some practical considerations ............................. 156

3.4.3 Forecasting volatility with RiskMetrics methodology ...................... 157

3.4.3.1 The exponential weighted moving average ...................... 157

3.4.3.2 Forecasting volatility ................................. 158

3.4.3.3 Assuming zero-drift in volatility calculation ..................... 159

3.4.3.4 Estimating the decay factor .............................. 160

3.4.4 Computing historical volatility .................................. 161

II Statistical tools applied to finance 164

4 Filtering and smoothing techniques 165

4.1 Presenting the challenge ......................................... 165

4.1.1 Describing the problem ...................................... 165

4.1.2 Regression smoothing ...................................... 166

4.1.3 Introducing trend filtering .................................... 167

4.1.3.1 Filtering in frequency ................................. 167

4.1.3.2 Filtering in the time domain .............................. 168

4.2 Smooting techniques and nonparametric regression ........................... 169

4.2.1 Histogram ............................................. 169

4.2.1.1 Definition of the Histogram .............................. 169

4.2.1.2 Smoothing the histogram by WARPing ........................ 172

4.2.2 Kernel density estimation .................................... 173

4.2.2.1 Definition of the Kernel estimate ........................... 173

4.2.2.2 Statistics of the Kernel density ............................ 174

4.2.2.3 Confidence intervals and confidence bands ...................... 176

4.2.3 Bandwidth selection in practice ................................. 177

4.2.3.1 Kernel estimation using reference distribution .................... 177

4.2.3.2 Plug-in methods .................................... 177

4.2.3.3 Cross-validation .................................... 178

4.2.4 Nonparametric regression .................................... 180

4.2.4.1 The Nadaraya-Watson estimator ........................... 181

4.2.4.2 Kernel smoothing algorithm .............................. 186

4.2.4.3 The K-nearest neighbour ............................... 186

4.2.5 Bandwidth selection ....................................... 187

4.2.5.1 Estimation of the average squared error ........................ 187

4.2.5.2 Penalising functions .................................. 189

4.2.5.3 Cross-validation .................................... 190

6

Quantitative Analytics

4.3 Trend filtering in the time domain .................................... 190

4.3.1 Some basic principles ...................................... 190

4.3.2 The local averages ........................................ 192

4.3.3 The Savitzky-Golay filter ..................................... 194

4.3.4 The least squares filters ...................................... 195

4.3.4.1 The L2 filtering .................................... 195

4.3.4.2 The L1 filtering .................................... 196

4.3.4.3 The Kalman filters ................................... 197

4.3.5 Calibration ............................................ 198

4.3.6 Introducing linear prediction ................................... 199

5 Presenting time series analysis 202

5.1 Basic principles of linear time series ................................... 202

5.1.1 Stationarity ............................................ 202

5.1.2 The autocorrelation function ................................... 203

5.1.3 The portmanteau test ....................................... 204

5.2 Linear time series ............................................. 205

5.2.1 Defining time series ....................................... 205

5.2.2 The autoregressive models .................................... 206

5.2.2.1 Definition ....................................... 206

5.2.2.2 Some properties .................................... 206

5.2.2.3 Identifying and estimating AR models ........................ 208

5.2.2.4 Parameter estimation ................................. 209

5.2.3 The moving-average models ................................... 209

5.2.4 The simple ARMA model .................................... 210

5.3 Forecasting ................................................ 211

5.3.1 Forecasting with the AR models ................................. 212

5.3.2 Forecasting with the MA models ................................. 212

5.3.3 Forecasting with the ARMA models ............................... 213

5.4 Nonstationarity and serial correlation ................................... 213

5.4.1 Unit-root nonstationarity ..................................... 213

5.4.1.1 The random walk ................................... 214

5.4.1.2 The random walk with drift .............................. 215

5.4.1.3 The unit-root test ................................... 215

5.4.2 Regression models with time series ............................... 216

5.4.3 Long-memory models ...................................... 217

5.5 Multivariate time series .......................................... 218

5.5.1 Characteristics .......................................... 218

5.5.2 Introduction to a few models ................................... 219

5.5.3 Principal component analysis .................................. 220

5.6 Some conditional heteroscedastic models ................................ 221

5.6.1 The ARCH model ........................................ 221

5.6.2 The GARCH model ....................................... 224

5.6.3 The integrated GARCH model .................................. 225

5.6.4 The GARCH-M model ...................................... 225

5.6.5 The exponential GARCH model ................................. 226

5.6.6 The stochastic volatility model .................................. 227

5.6.7 Another approach: high-frequency data ............................. 228

5.6.8 Forecasting evaluation ...................................... 229

5.7 Exponential smoothing and forecasting data ............................... 229

7

Quantitative Analytics

5.7.1 The moving average ....................................... 230

5.7.1.1 Simple moving average ................................ 230

5.7.1.2 Weighted moving average ............................... 231

5.7.1.3 Exponential smoothing ................................ 231

5.7.1.4 Exponential moving average revisited ......................... 233

5.7.2 Introducing exponential smoothing models ........................... 234

5.7.2.1 Linear exponential smoothing ............................. 235

5.7.2.2 The damped trend model ............................... 236

5.7.3 A summary ............................................ 237

5.7.4 Model fitting ........................................... 242

5.7.5 Prediction intervals and random simulation ........................... 245

5.7.6 Random coefficient state space model .............................. 246

6 Filtering and forecasting with wavelet analysis 248

6.1 Introducing wavelet analysis ....................................... 248

6.1.1 From spectral analysis to wavelet analysis ............................ 248

6.1.1.1 Spectral analysis .................................... 248

6.1.1.2 Wavelet analysis .................................... 249

6.1.2 The a trous wavelet decomposition ................................ 249

6.2 Some applications ............................................. 251

6.2.1 A brief review .......................................... 251

6.2.2 Filtering with wavelets ...................................... 252

6.2.3 Non-stationarity ......................................... 253

6.2.4 Decomposition tool for seasonality extraction .......................... 253

6.2.5 Interdependence between variables ............................... 254

6.2.6 Introducing long memory processes ............................... 254

6.3 Presenting wavelet-based forecasting methods .............................. 255

6.3.1 Forecasting with the a trous wavelet transform ......................... 255

6.3.2 The redundant Haar wavelet transform for time-varying data .................. 256

6.3.3 The multiresolution autoregressive model ............................ 257

6.3.3.1 Linear model ...................................... 257

6.3.3.2 Non-linear model ................................... 258

6.3.4 The neuro-wavelet hybrid model ................................. 258

6.4 Some wavelets applications to finance .................................. 259

6.4.1 Deriving strategies from wavelet analysis ............................ 259

6.4.2 Literature review ......................................... 259

III Quantitative trading in inefficient markets 261

7 Introduction to quantitative strategies 262

7.1 Presenting hedge funds .......................................... 262

7.1.1 Classifying hedge funds ..................................... 262

7.1.2 Some facts about leverage .................................... 263

7.1.2.1 Defining leverage ................................... 263

7.1.2.2 Different measures of leverage ............................ 263

7.1.2.3 Leverage and risk ................................... 264

7.2 Different types of strategies ........................................ 264

7.2.1 Long-short portfolio ....................................... 264

7.2.1.1 The problem with long-only portfolio ......................... 264

8

Quantitative Analytics

7.2.1.2 The benefits of long-short portfolio .......................... 265

7.2.2 Equity market neutral ....................................... 266

7.2.3 Pairs trading ........................................... 267

7.2.4 Statistical arbitrage ........................................ 269

7.2.5 Mean-reversion strategies .................................... 270

7.2.6 Adaptive strategies ........................................ 270

7.2.7 Constraints and fees on short-selling ............................... 271

7.3 Enhanced active strategies ........................................ 271

7.3.1 Definition ............................................. 271

7.3.2 Some misconceptions ...................................... 272

7.3.3 Some benefits ........................................... 273

7.3.4 The enhanced prime brokerage structures ............................ 274

7.4 Measuring the efficiency of portfolio implementation .......................... 275

7.4.1 Measures of efficiency ...................................... 275

7.4.2 Factors affecting performances .................................. 276

8 Describing quantitative strategies 278

8.1 Time series momentum strategies ..................................... 278

8.1.1 The univariate time-series strategy ................................ 278

8.1.2 The momentum signals ...................................... 279

8.1.2.1 Return sign ....................................... 279

8.1.2.2 Moving Average .................................... 279

8.1.2.3 EEMD Trend Extraction ................................ 280

8.1.2.4 Time-Trend t-statistic ................................. 280

8.1.2.5 Statistically Meaningful Trend ............................ 280

8.1.3 The signal speed ......................................... 281

8.1.4 The relative strength index .................................... 281

8.1.5 Regression analysis ........................................ 282

8.1.6 The momentum profitability ................................... 283

8.2 Factors analysis .............................................. 284

8.2.1 Presenting the factor model ................................... 284

8.2.2 Some trading applications .................................... 287

8.2.2.1 Pairs-trading ...................................... 287

8.2.2.2 Decomposing stock returns .............................. 287

8.2.3 A systematic approach ...................................... 288

8.2.3.1 Modelling returns ................................... 288

8.2.3.2 The market neutral portfolio .............................. 289

8.2.4 Estimating the factor model ................................... 290

8.2.4.1 The PCA approach .................................. 290

8.2.4.2 The selection of the eigenportfolios .......................... 291

8.2.5 Strategies based on mean-reversion ............................... 292

8.2.5.1 The mean-reverting model ............................... 292

8.2.5.2 Pure mean-reversion .................................. 294

8.2.5.3 Mean-reversion with drift ............................... 294

8.2.6 Portfolio optimisation ...................................... 295

8.2.7 Back-testing ........................................... 297

8.3 The meta strategies ............................................ 297

8.3.1 Presentation ............................................ 297

8.3.1.1 The trading signal ................................... 297

8.3.1.2 The strategies ..................................... 298

9

Quantitative Analytics

8.3.2 The risk measures ........................................ 298

8.3.2.1 Conditional expectations ............................... 298

8.3.2.2 Some examples .................................... 299

8.3.3 Computing the Sharpe ratio of the strategies ........................... 300

8.4 Random sampling measures of risk .................................... 301

8.4.1 The sample Sharpe ratio ..................................... 301

8.4.2 The sample conditional Sharpe ratio ............................... 301

9 Portfolio management under constraints 303

9.1 Introduction ................................................ 303

9.2 Robust portfolio allocation ........................................ 304

9.2.1 Long-short mean-variance approach under constraints ..................... 304

9.2.2 Portfolio selection ........................................ 307

9.2.2.1 Long only investment: non-leveraged ......................... 308

9.2.2.2 Short selling: No ruin constraints ........................... 310

9.2.2.3 Long only investment: leveraged ........................... 312

9.2.2.4 Short selling and leverage ............................... 313

9.3 Empirical log-optimal portfolio selections ................................ 314

9.3.1 Static portfolio selection ..................................... 314

9.3.2 Constantly rebalanced portfolio selection ............................ 315

9.3.2.1 Log-optimal portfolio for memoryless market process ................ 316

9.3.2.2 Semi-log-optimal portfolio .............................. 318

9.3.3 Time varying portfolio selection ................................. 318

9.3.3.1 Log-optimal portfolio for stationary market process ................. 318

9.3.3.2 Empirical portfolio selection ............................. 319

9.3.4 Regression function estimation: The local averaging estimates ................. 320

9.3.4.1 The partitioning estimate ............................... 320

9.3.4.2 The Nadaraya-Watson kernel estimate ........................ 321

9.3.4.3 The k-nearest neighbour estimate ........................... 322

9.3.4.4 The correspondence .................................. 322

9.4 A simple example ............................................. 322

9.4.1 A self-financed long-short portfolio ............................... 322

9.4.2 Allowing for capital inflows and outflows ............................ 325

9.4.3 Allocating the weights ...................................... 326

9.4.3.1 Choosing uniform weights .............................. 326

9.4.3.2 Choosing Beta for the weight ............................. 326

9.4.3.3 Choosing Alpha for the weight ............................ 327

9.4.3.4 Combining Alpha and Beta for the weight ...................... 327

9.4.4 Building a beta neutral portfolio ................................. 327

9.4.4.1 A quasi-beta neutral portfolio ............................. 327

9.4.4.2 An exact beta-neutral portfolio ............................ 328

9.5 Value at Risk ............................................... 328

9.5.1 Defining value at risk ....................................... 328

9.5.2 Computing value at risk ..................................... 329

9.5.2.1 RiskMetrics ...................................... 329

9.5.2.2 Econometric models to VaR calculation ........................ 330

9.5.2.3 Quantile estimation to VaR calculation ........................ 332

9.5.2.4 Extreme value theory to VaR calculation ....................... 334

10

Quantitative Analytics

IV Quantitative trading in multifractal markets 337

10 The fractal market hypothesis 338

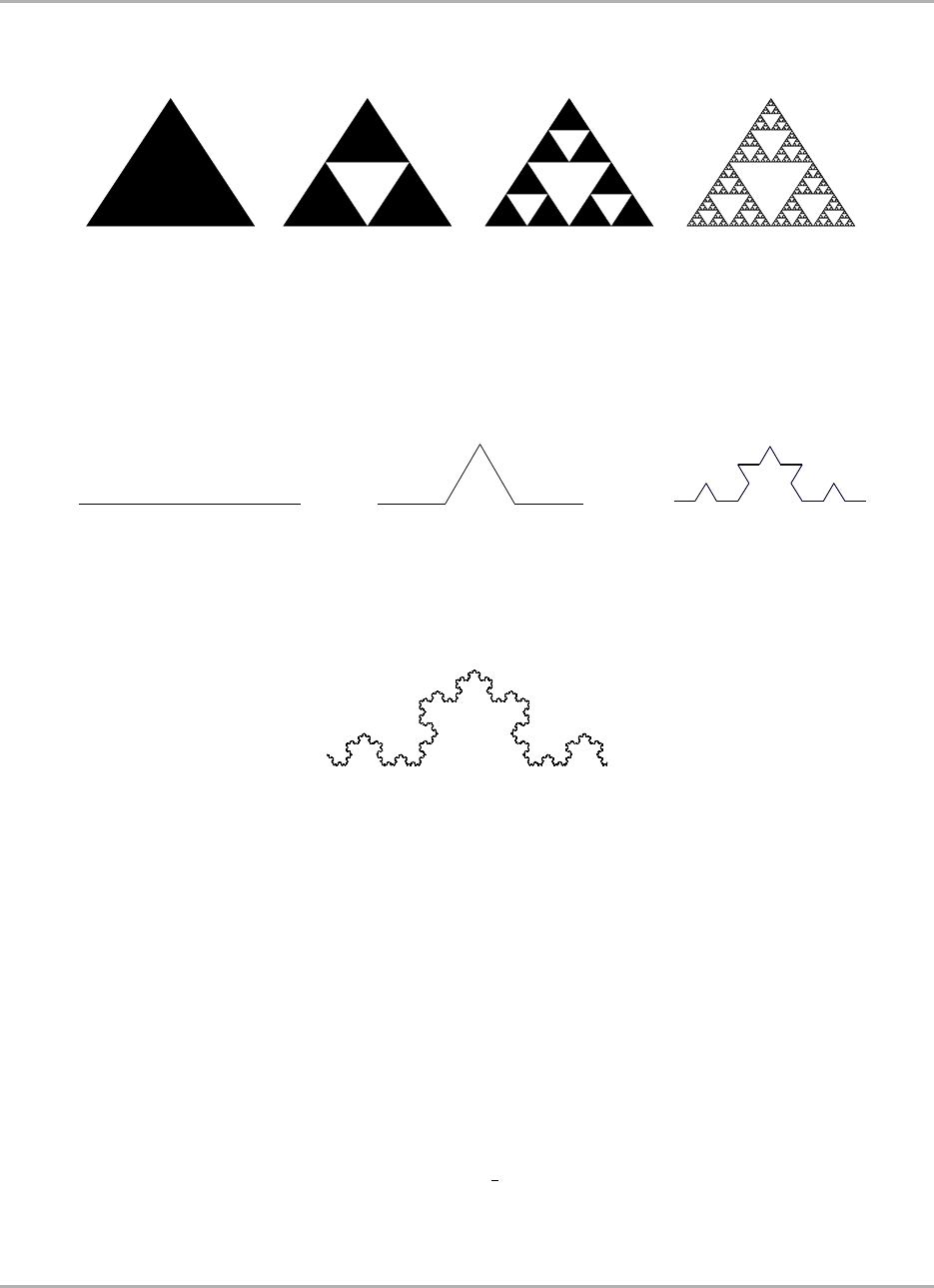

10.1 Fractal structure in the markets ...................................... 338

10.1.1 Introducing fractal analysis .................................... 338

10.1.1.1 A brief history ..................................... 338

10.1.1.2 Presenting the results ................................. 339

10.1.2 Defining random fractals ..................................... 342

10.1.2.1 The fractional Brownian motion ............................ 342

10.1.2.2 The multidimensional fBm .............................. 344

10.1.2.3 The fractional Gaussian noise ............................. 344

10.1.2.4 The fractal process and its distribution ........................ 345

10.1.2.5 An application to finance ............................... 346

10.1.3 A first approach to generating random fractals .......................... 347

10.1.3.1 Approximating fBm by spectral synthesis ...................... 347

10.1.3.2 The ARFIMA models ................................. 348

10.1.4 From efficient to fractal market hypothesis ........................... 350

10.1.4.1 Some limits of the efficient market hypothesis .................... 350

10.1.4.2 The Larrain KZ model ................................. 351

10.1.4.3 The coherent market hypothesis ............................ 352

10.1.4.4 Defining the fractal market hypothesis ........................ 353

10.2 The R/S analysis ............................................. 353

10.2.1 Defining R/S analysis for financial series ............................ 353

10.2.2 A step-by-step guide to R/S analysis ............................... 355

10.2.2.1 A first approach .................................... 355

10.2.2.2 A better step-by-step method ............................. 356

10.2.3 Testing the limits of R/S analysis ................................. 357

10.2.4 Improving the R/S analysis .................................... 358

10.2.4.1 Reducing bias ..................................... 358

10.2.4.2 Lo’s modified R/S statistic .............................. 359

10.2.4.3 Removing short-term memory ............................ 360

10.2.5 Detecting periodic and nonperiodic cycles ............................ 360

10.2.5.1 The natural period of a system ............................ 360

10.2.5.2 The V statistic ..................................... 361

10.2.5.3 The Hurst exponent and chaos theory ......................... 361

10.2.6 Possible models for FMH .................................... 362

10.2.6.1 A few points about chaos theory ........................... 362

10.2.6.2 Using R/S analysis to detect noisy chaos ...................... 363

10.2.6.3 A unified theory .................................... 364

10.2.7 Revisiting the measures of volatility risk ............................. 365

10.2.7.1 The standard deviation ................................. 365

10.2.7.2 The fractal dimension as a measure of risk ...................... 366

10.3 Hurst exponent estimation methods .................................... 367

10.3.1 Estimating the Hurst exponent with wavelet analysis ...................... 367

10.3.2 Detrending methods ....................................... 369

10.3.2.1 Detrended fluctuation analysis ............................ 370

10.3.2.2 A modified DFA .................................... 372

10.3.2.3 Detrending moving average .............................. 372

10.3.2.4 DMA in high dimensions ............................... 373

10.3.2.5 The periodogram and the Whittle estimator ...................... 374

11

Quantitative Analytics

10.4 Testing for market efficiency ....................................... 374

10.4.1 Presenting the main controversy ................................. 374

10.4.2 Using the Hurst exponent to define the null hypothesis ..................... 375

10.4.2.1 Defining long-range dependence ........................... 375

10.4.2.2 Defining the null hypothesis .............................. 376

10.4.3 Measuring temporal correlation in financial data ........................ 376

10.4.3.1 Statistical studies ................................... 376

10.4.3.2 An example on foreign exchange rates ........................ 377

10.4.4 Applying R/S analysis to financial data ............................. 378

10.4.4.1 A first analysis on the capital markets ......................... 378

10.4.4.2 A deeper analysis on the capital markets ....................... 378

10.4.4.3 Defining confidence intervals for long-memory analysis ............... 379

10.4.5 Some critics at Lo’s modified R/S statistic ........................... 380

10.4.6 The problem of non-stationary and dependent increments .................... 381

10.4.6.1 Non-stationary increments ............................... 381

10.4.6.2 Finite sample ..................................... 381

10.4.6.3 Dependent increments ................................. 382

10.4.6.4 Applying stress testing ................................ 382

10.4.7 Some results on measuring the Hurst exponent ......................... 383

10.4.7.1 Accuracy of the Hurst estimation ........................... 383

10.4.7.2 Robustness for various sample size .......................... 385

10.4.7.3 Computation time ................................... 387

11 The multifractal markets 390

11.1 Multifractality as a new stylised fact ................................... 390

11.1.1 The multifractal scaling behaviour of time series ........................ 390

11.1.1.1 Analysing complex signals .............................. 390

11.1.1.2 A direct application to financial time series ...................... 391

11.1.2 Defining multifractality ...................................... 391

11.1.2.1 Fractal measures and their singularities ........................ 391

11.1.2.2 Scaling analysis .................................... 394

11.1.2.3 Multifractal analysis .................................. 396

11.1.2.4 The wavelet transform and the thermodynamical formalism ............. 399

11.1.3 Observing multifractality in financial data ............................ 400

11.1.3.1 Applying multiscaling analysis ............................ 400

11.1.3.2 Applying multifractal fluctuation analysis ...................... 401

11.2 Holder exponent estimation methods ................................... 402

11.2.1 Applying the multifractal formalism ............................... 402

11.2.2 The multifractal wavelet analysis ................................ 403

11.2.2.1 The wavelet transform modulus maxima ....................... 404

11.2.2.2 Wavelet multifractal DFA ............................... 405

11.2.3 The multifractal fluctuation analysis ............................... 406

11.2.3.1 Direct and indirect procedure ............................. 406

11.2.3.2 Multifractal detrended fluctuation ........................... 407

11.2.3.3 Multifractal empirical mode decomposition ..................... 408

11.2.3.4 The R/S ananysis extented .............................. 408

11.2.3.5 Multifractal detrending moving average ....................... 409

11.2.3.6 Some comments about using MFDFA ......................... 409

11.2.4 General comments on multifractal analysis ........................... 411

11.2.4.1 Characteristics of the generalised Hurst exponent .................. 411

12

Quantitative Analytics

11.2.4.2 Characteristics of the multifractal spectrum ...................... 411

11.2.4.3 Some issues regarding terminology and definition .................. 412

11.3 The need for time and scale dependent Hurst exponent ......................... 415

11.3.1 Computing the Hurst exponent on a sliding window ....................... 415

11.3.1.1 Introducing time-dependent Hurst exponent ..................... 415

11.3.1.2 Describing the sliding window ............................ 415

11.3.1.3 Understanding the time-dependent Hurst exponent .................. 416

11.3.1.4 Time and scale Hurst exponent ............................ 417

11.3.2 Testing the markets for multifractality .............................. 417

11.3.2.1 A summary on temporal correlation in financial data ................. 417

11.3.2.2 Applying sliding windows ............................... 418

11.4 Local Holder exponent estimation methods ............................... 421

11.4.1 The wavelet analysis ....................................... 421

11.4.1.1 The effective Holder exponent ............................ 421

11.4.1.2 Gradient modulus wavelet projection ......................... 422

11.4.1.3 Testing the performances of wavelet multifractal methods .............. 423

11.4.2 The fluctuation analysis ..................................... 423

11.4.2.1 Local detrended fluctuation analysis ......................... 423

11.4.2.2 The multifractal spectrum and the local Hurst exponent ............... 425

11.4.3 Detection and localisation of outliers .............................. 425

11.4.4 Testing for the validity of the local Hurst exponent ....................... 426

11.4.4.1 Local change of fractal structure ........................... 426

11.4.4.2 Abrupt change of fractal structure ........................... 427

11.4.4.3 A simple explanation ................................. 427

11.5 Analysing the multifractal markets .................................... 428

11.5.1 Describing the method ...................................... 428

11.5.2 Testing for trend and mean-reversion .............................. 430

11.5.2.1 The equity market ................................... 430

11.5.2.2 The FX market ..................................... 431

11.5.3 Testing for crash prediction ................................... 432

11.5.3.1 The Asian crisis in 1997 ................................ 432

11.5.3.2 The dot-com bubble in 2000 .............................. 433

11.5.3.3 The financial crisis of 2007 .............................. 434

11.5.4 Conclusion ............................................ 435

11.6 Some multifractal models for asset pricing ................................ 436

12 Systematic trading 441

12.1 Introduction ................................................ 441

12.2 Technical analysis ............................................. 442

12.2.1 Definition ............................................. 442

12.2.2 Technical indicator ........................................ 443

12.2.3 Optimising portfolio selection .................................. 443

12.2.3.1 Classifying strategies ................................. 444

12.2.3.2 Examples of multiple rules .............................. 445

V Numerical Analysis 446

13 Presenting some machine-learning methods 448

13.1 Some facts on machine-learning ..................................... 448

13

Quantitative Analytics

13.1.1 Introduction to data mining .................................... 448

13.1.2 The challenges of computational learning ............................ 449

13.2 Introduction to information theory .................................... 451

13.2.1 Presenting a few concepts .................................... 451

13.2.2 Some facts on entropy in information theory .......................... 452

13.2.3 Relative entropy and mutual information ............................ 453

13.2.4 Bounding performance measures ................................. 455

13.2.5 Feature selection ......................................... 457

13.3 Introduction to artificial neural networks ................................. 460

13.3.1 Presentation ............................................ 460

13.3.2 Gradient descent and the delta rule ................................ 461

13.3.3 Introducing multilayer networks ................................. 462

13.3.3.1 Describing the problem ................................ 463

13.3.3.2 Describing the algorithm ............................... 463

13.3.3.3 A simple example ................................... 465

13.3.4 Multi-layer back propagation ................................... 465

13.3.4.1 The output layer .................................... 466

13.3.4.2 The first hidden layer ................................. 466

13.3.4.3 The next hidden layer ................................. 468

13.3.4.4 Some remarks ..................................... 470

13.4 Online learning and regret-minimising algorithms ............................ 471

13.4.1 Simple online algorithms ..................................... 471

13.4.1.1 The Halving algorithm ................................ 471

13.4.1.2 The weighted majority algorithm ........................... 471

13.4.2 The online convex optimisation ................................. 473

13.4.2.1 The online linear optimisation problem ........................ 473

13.4.2.2 Considering Bergmen divergence ........................... 473

13.4.2.3 More on the online convex optimisation problem ................... 474

13.5 Presenting the problem of automated market making .......................... 475

13.5.1 The market neutral case ..................................... 475

13.5.2 The case of infinite outcome space ................................ 476

13.5.3 Relating market design to machine learning ........................... 479

13.5.4 The assumptions of market completeness ............................ 480

13.6 Presenting scoring rules .......................................... 480

13.6.1 Describing a few scoring rules .................................. 480

13.6.1.1 The proper scoring rules ................................ 480

13.6.1.2 The market scoring rules ............................... 481

13.6.2 Relating MSR to cost function based market makers ...................... 482

14 Introducing Differential Evolution 483

14.1 Introduction ................................................ 483

14.2 Calibration to implied volatility ...................................... 483

14.2.1 Introducing calibration ...................................... 483

14.2.1.1 The general idea .................................... 483

14.2.1.2 Measures of pricing errors ............................... 484

14.2.2 The calibration problem ..................................... 485

14.2.3 The regularisation function .................................... 486

14.2.4 Beyond deterministic optimisation method ........................... 487

14.3 Nonlinear programming problems with constraints ........................... 487

14.3.1 Describing the problem ...................................... 487

14

Quantitative Analytics

14.3.1.1 A brief history ..................................... 487

14.3.1.2 Defining the problems ................................. 487

14.3.2 Some optimisation methods ................................... 489

14.3.2.1 Random optimisation ................................. 489

14.3.2.2 Harmony search .................................... 490

14.3.2.3 Particle swarm optimisation .............................. 491

14.3.2.4 Cross entropy optimisation .............................. 492

14.3.2.5 Simulated annealing .................................. 493

14.3.3 The DE algorithm ........................................ 494

14.3.3.1 The mutation ...................................... 494

14.3.3.2 The recombination ................................... 494

14.3.3.3 The selection ...................................... 495

14.3.3.4 Convergence criterions ................................ 495

14.3.4 Pseudocode ............................................ 495

14.3.5 The strategies ........................................... 496

14.3.5.1 Scheme DE1 ...................................... 496

14.3.5.2 Scheme DE2 ...................................... 496

14.3.5.3 Scheme DE3 ...................................... 496

14.3.5.4 Scheme DE4 ...................................... 496

14.3.5.5 Scheme DE5 ...................................... 497

14.3.5.6 Scheme DE6 ...................................... 497

14.3.5.7 Scheme DE7 ...................................... 497

14.3.5.8 Scheme DE8 ...................................... 498

14.3.6 Improvements ........................................... 498

14.3.6.1 Ageing ......................................... 498

14.3.6.2 Constraints on parameters ............................... 499

14.3.6.3 Convergence ...................................... 499

14.3.6.4 Self-adaptive parameters ............................... 499

14.3.6.5 Selection ........................................ 499

14.4 Handling the constraints ......................................... 500

14.4.1 Describing the problem ...................................... 500

14.4.2 Defining the feasibility rules ................................... 500

14.4.3 Improving the feasibility rules .................................. 501

14.4.4 Handling diversity ........................................ 502

14.5 The proposed algorithm .......................................... 503

14.6 Describing some benchmarks ....................................... 504

14.6.1 Minimisation of the sphere function ............................... 505

14.6.2 Minimisation of the Rosenbrock function ............................ 505

14.6.3 Minimisation of the step function ................................ 505

14.6.4 Minimisation of the Rastrigin function .............................. 506

14.6.5 Minimisation of the Griewank function ............................. 506

14.6.6 Minimisation of the Easom function ............................... 506

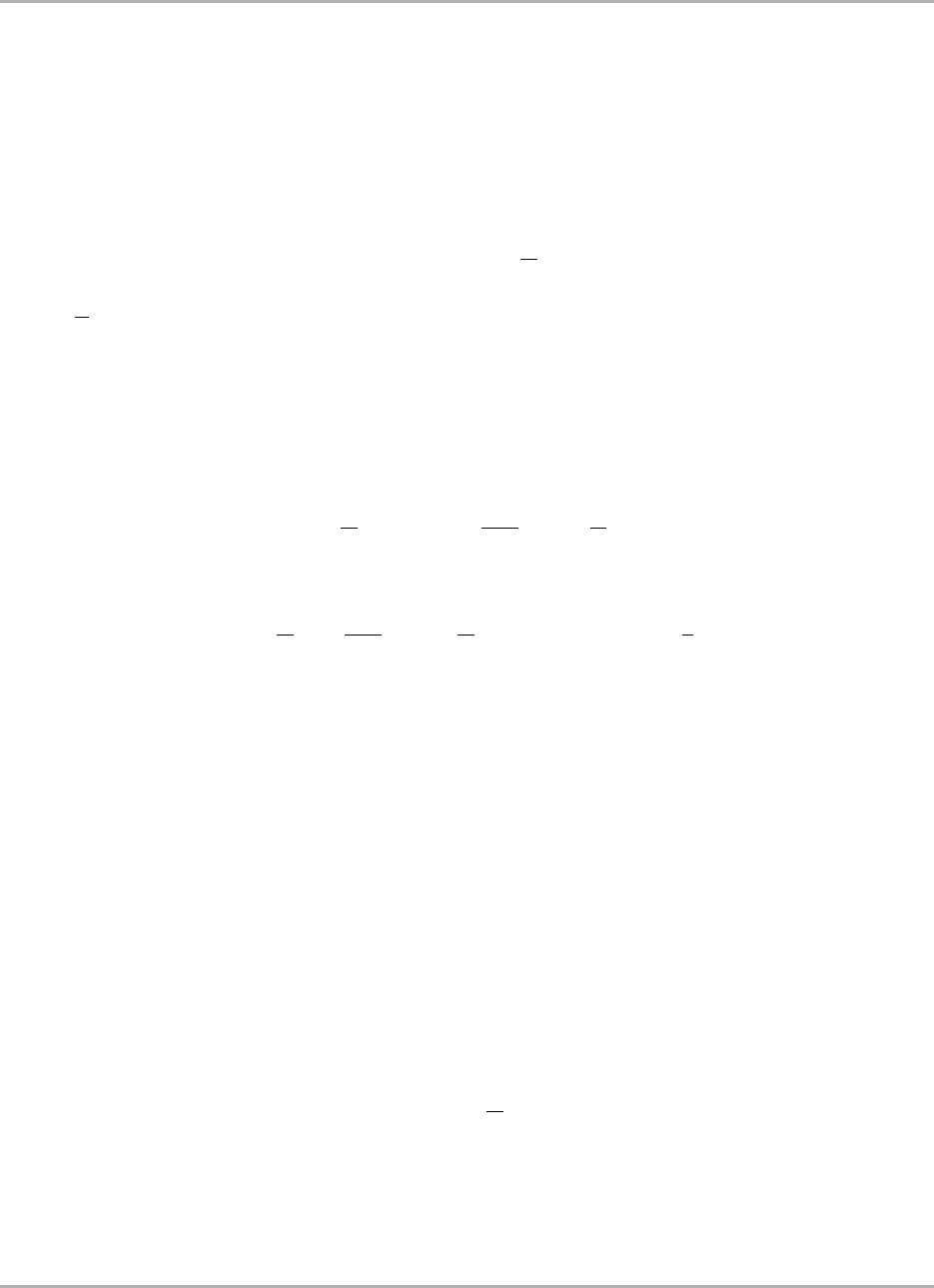

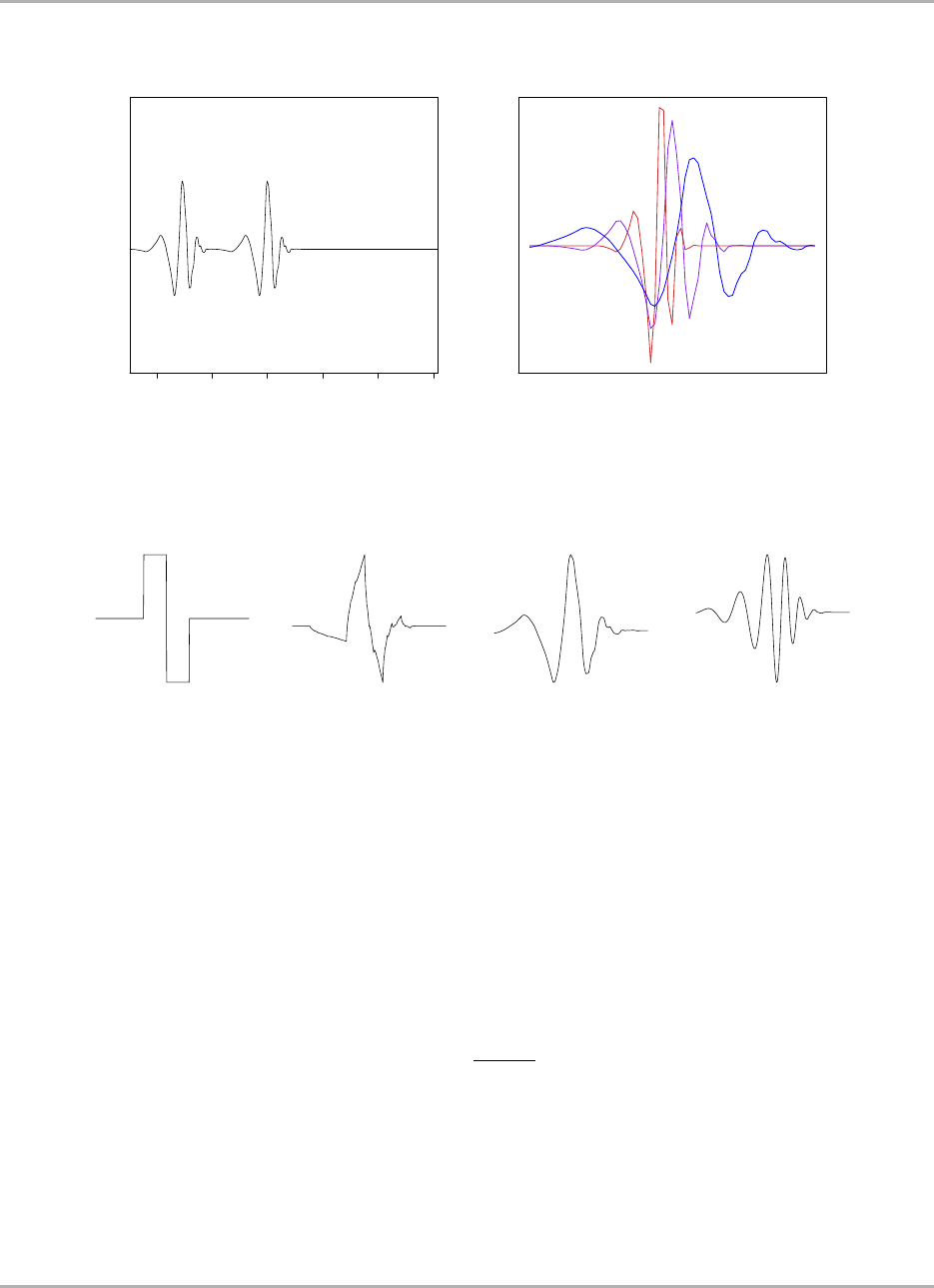

14.6.7 Image from polygons ....................................... 507

14.6.8 Minimisation problem g01 .................................... 507

14.6.9 Maximisation problem g03 .................................... 508

14.6.10 Maximisation problem g08 .................................... 508

14.6.11 Minimisation problem g11 .................................... 508

14.6.12 Minimisation of the weight of a tension/compression spring .................. 508

15

Quantitative Analytics

15 Introduction to CUDA Programming in Finance 510

15.1 Introduction ................................................ 510

15.1.1 A birief overview ......................................... 510

15.1.2 Preliminary words on parallel programming ........................... 511

15.1.3 Why GPUs? ........................................... 512

15.1.4 Why CUDA? ........................................... 513

15.1.5 Applications in financial computing ............................... 513

15.2 Programming with CUDA ........................................ 514

15.2.1 Hardware ............................................. 514

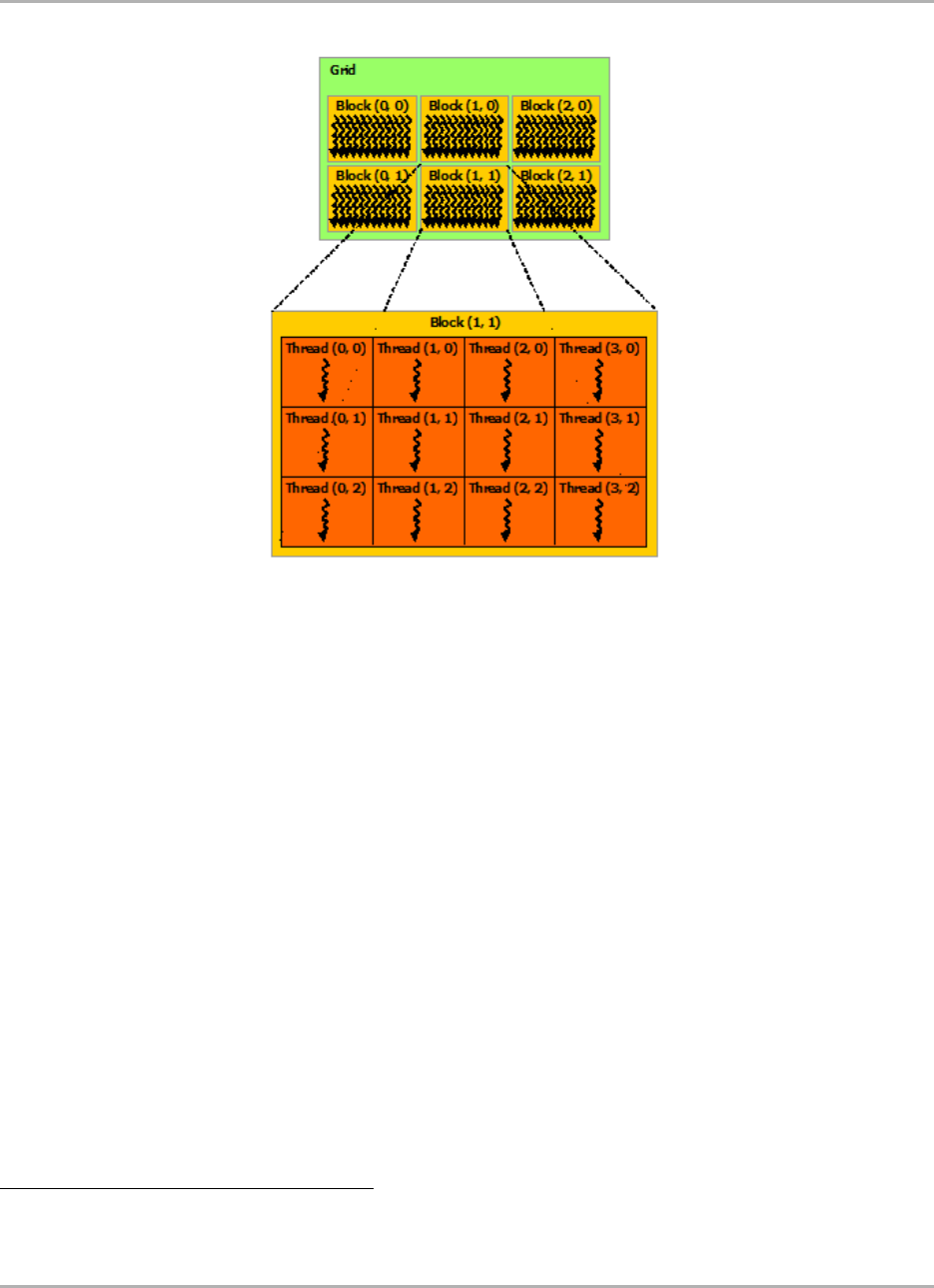

15.2.2 Thread hierarchy ......................................... 514

15.2.3 Memory management ...................................... 515

15.2.4 Syntax and connetion to C/C++ ................................. 516

15.2.5 Random number generation ................................... 520

15.2.5.1 Memory storage .................................... 521

15.2.5.2 Inline .......................................... 521

15.3 Case studies ................................................ 522

15.3.1 Exotic swaps in Monte-Carlo ................................... 522

15.3.1.1 Product and model ................................... 522

15.3.1.2 Single-thread algorithm ................................ 522

15.3.1.3 Multi-thread algorithm ................................ 523

15.3.1.4 Using the texture memory ............................... 524

15.3.2 Volatility calibration by differential evolution .......................... 525

15.3.2.1 Model and difficulties ................................. 525

15.3.2.2 Single-thread algorithm ................................ 526

15.3.2.3 Multi-thread algorithm ................................ 526

15.4 Conclusion ................................................ 527

Appendices 528

A Review of some mathematical facts 529

A.1 Some facts on convex and concave analysis ............................... 529

A.1.1 Convex functions ......................................... 530

A.1.2 Concave functions ........................................ 530

A.1.3 Some approximations ...................................... 532

A.1.4 Conjugate duality ......................................... 532

A.1.5 A note on Legendre transformation ............................... 533

A.1.6 A note on the Bregman divergence ................................ 533

A.2 The logistic function ........................................... 534

A.3 The convergence of series ......................................... 536

A.4 The Dirac function ............................................ 538

A.5 Some linear algebra ............................................ 538

A.6 Some facts on matrices .......................................... 542

A.7 Utility function .............................................. 544

A.7.1 Definition ............................................. 544

A.7.2 Some properties ......................................... 545

A.7.3 Some specific utility functions .................................. 547

A.7.4 Mean-variance criterion ..................................... 548

A.7.4.1 Normal returns ..................................... 548

A.7.4.2 Non-normal returns .................................. 549

A.8 Optimisation ............................................... 549

16

Quantitative Analytics

A.9 Conjugate gradient method ........................................ 551

B Some probabilities 554

B.1 Some definitions ............................................. 554

B.2 Random variables ............................................. 556

B.2.1 Discrete random variables .................................... 556

B.2.2 Continuous random variables .................................. 557

B.3 Introducing stochastic processes ..................................... 557

B.4 The characteristic function and moments ................................. 558

B.4.1 Definitions ............................................ 558

B.4.2 The first two moments ...................................... 559

B.4.3 Trading correlation ........................................ 560

B.5 Conditional moments ........................................... 560

B.5.1 Conditional expectation ..................................... 560

B.5.2 Conditional variance ....................................... 563

B.5.3 More details on conditional expectation ............................. 564

B.5.3.1 Some discrete results ................................. 564

B.5.3.2 Some continuous results ................................ 565

B.6 About fractal analysis ........................................... 566

B.6.1 The fractional Brownian motion ................................. 566

B.6.2 The R/S analysis ......................................... 567

B.7 Some continuous variables and their distributions ............................ 568

B.7.1 Some popular distributions .................................... 568

B.7.1.1 Uniform distribution .................................. 568

B.7.1.2 Exponential distribution ................................ 568

B.7.1.3 Normal distribution .................................. 568

B.7.1.4 Gamma distribution .................................. 569

B.7.1.5 Chi-square distribution ................................ 569

B.7.1.6 Weibull distribution .................................. 569

B.7.2 Normal and Lognormal distributions ............................... 570

B.7.3 Multivariate Normal distributions ................................ 570

B.7.4 Distributions arising from the Normal distribution ........................ 571

B.7.4.1 Presenting the problem ................................ 571

B.7.4.2 The t-distribution ................................... 572

B.7.4.3 The F-distribution ................................... 573

B.8 Some results on Normal sampling .................................... 574

B.8.1 Estimating the mean and variance ................................ 574

B.8.2 Estimating the mean with known variance ............................ 574

B.8.3 Estimating the mean with unknown variance .......................... 575

B.8.4 Estimating the parameters of a linear model ........................... 575

B.8.5 Asymptotic confidence interval ................................. 575

B.8.6 The setup of the Monte Carlo engine ............................... 576

B.9 Some random sampling .......................................... 577

B.9.1 The sample moments ....................................... 577

B.9.2 Estimation of a ratio ....................................... 579

B.9.3 Stratified random sampling .................................... 580

B.9.4 Geometric mean ......................................... 584

17

Quantitative Analytics

C Stochastic processes and Time Series 585

C.1 Introducing time series .......................................... 585

C.1.1 Definitions ............................................ 585

C.1.2 Estimation of trend and seasonality ............................... 586

C.1.3 Some sample statistics ...................................... 587

C.2 The ARMA model ............................................ 588

C.3 Fitting ARIMA models .......................................... 599

C.4 State space models ............................................ 606

C.5 ARCH and GARCH models ....................................... 608

C.5.1 The ARCH process ........................................ 608

C.5.2 The GARCH process ....................................... 609

C.5.3 Estimating model parameters ................................... 610

C.6 The linear equation ............................................ 610

C.6.1 Solving linear equation ...................................... 610

C.6.2 A simple example ........................................ 611

C.6.2.1 Covariance matrix ................................... 611

C.6.2.2 Expectation ...................................... 612

C.6.2.3 Distribution and probability .............................. 612

C.6.3 From OU to AR(1) process .................................... 613

C.6.3.1 The Ornstein-Uhlenbeck process ........................... 613

C.6.3.2 Deriving the discrete model .............................. 614

C.6.4 Some facts about AR series ................................... 615

C.6.4.1 Persistence ....................................... 615

C.6.4.2 Prewhitening and detrending ............................. 615

C.6.4.3 Simulation and prediction ............................... 616

C.6.5 Estimating the model parameters ................................. 616

D Defining market equilibrirum and asset prices 618

D.1 Introducing the theory of general equilibrium .............................. 618

D.1.1 1 period, (d+ 1) assets, kstates of the world .......................... 618

D.1.2 Complete market ......................................... 620

D.1.3 Optimisation with consumption ................................. 620

D.2 An introduction to the model of Von Neumann Morgenstern ...................... 622

D.2.1 Part I ............................................... 622

D.2.2 Part II ............................................... 623

D.3 Simple equilibrium model ........................................ 624

D.3.1 magents, (d+ 1) assets ..................................... 624

D.3.2 The consumption based asset pricing model ........................... 625

D.4 The n-dates model ............................................. 627

D.5 Discrete option valuation ......................................... 628

D.6 Valuation in financial markets ...................................... 629

D.6.1 Pricing securities ......................................... 629

D.6.2 Introducing the recovery theorem ................................ 631

D.6.3 Using implied volatilities ..................................... 632

D.6.4 Bounding the pricing kernel ................................... 633

18

Quantitative Analytics

E Pricing and hedging options 634

E.1 Valuing options on multi-underlyings .................................. 634

E.1.1 Self-financing portfolios ..................................... 634

E.1.2 Absence of arbitrage opportunity and rate of returns ...................... 637

E.1.3 Numeraire ............................................ 638

E.1.4 Evaluation and hedging ...................................... 639

E.2 The dynamics of financial assets ..................................... 642

E.2.1 The Black-Scholes world ..................................... 642

E.2.2 The dynamics of the bond price ................................. 643

E.3 From market prices to implied volatility ................................. 645

E.3.1 The Black-Scholes formula .................................... 645

E.3.2 The implied volatility in the Black-Scholes formula ....................... 645

E.3.3 The robustness of the Black-Scholes formula .......................... 646

E.4 Some properties satisfied by market prices ................................ 647

E.4.1 The no-arbitrage conditions ................................... 647

E.4.2 Pricing two special market products ............................... 647

E.4.2.1 The digital option ................................... 647

E.4.2.2 The butterfly option .................................. 648

E.5 Introduction to indifference pricing theory ................................ 648

E.5.1 Martingale measures and state-price densities .......................... 648

E.5.2 An overview ........................................... 649

E.5.2.1 Describing the optimisation problem ......................... 649

E.5.2.2 The dual problem ................................... 650

E.5.3 The non-traded assets model ................................... 651

E.5.3.1 Discrete time ...................................... 651

E.5.3.2 Continuous time .................................... 651

E.5.4 The pricing method ........................................ 652

E.5.4.1 Computing indifference prices ............................ 653

E.5.4.2 Computing option prices ............................... 654

F Some results on signal processing 657

F.1 A short introduction to Fourier transform methods ............................ 657

F.1.1 Some analytical formalism .................................... 657

F.1.2 The Fourier integral ....................................... 659

F.1.3 The Fourier transformation .................................... 661

F.1.4 The discrete Fourier transform .................................. 662

F.1.5 The Fast Fourier Transform algorithm .............................. 663

F.2 From spline analysis to wavelet analysis ................................. 665

F.2.1 An introduction to splines .................................... 665

F.2.2 Multiresolution spline processing ................................ 667

F.3 A short introduction to wavelet transform methods ........................... 669

F.3.1 The continuous wavelet transform ................................ 669

F.3.2 The discrete wavelet transform .................................. 675

F.3.2.1 An infinite summations of discrete wavelet coefficients ............... 675

F.3.2.2 The scaling function .................................. 676

F.3.2.3 The FWT algorithm .................................. 678

F.3.3 Discrete input signals of finite length .............................. 679

F.3.3.1 Discribing the algorithm ................................ 679

F.3.3.2 Presenting thresholding ................................ 681

F.3.4 Wavelet-based statistical measures ................................ 682

19

Quantitative Analytics

F.4 The problem of shift-invariance ...................................... 684

F.4.1 A brief overview ......................................... 684

F.4.1.1 Describing the problem ................................ 684

F.4.1.2 The a trous algorithm ................................. 685

F.4.1.3 Relating the a trous and Mallat algorithms ...................... 685

F.4.2 Describing some redundant transforms ............................. 687

F.4.2.1 The multiresolution analysis .............................. 687

F.4.2.2 The standard DWT .................................. 690

F.4.2.3 The -decimated DWT ................................ 691

F.4.2.4 The stationary wavelet transform ........................... 692

F.4.3 The autocorrelation functions of compactly supported wavelets ................. 693

20

Quantitative Analytics

0.1 Introduction

0.1.1 Preamble

There is a vast literature on the investment decision making process and associated assessment of expected returns on

investments. Traditionally, historical performances, economic theories, and forward looking indicators were usually

put forward for investors to judge expected returns. However, modern finance theory, including quantitative models

and econometric techniques, provided the foundation that has revolutionised the investment management industry over

the last 20 years. Technical analysis have initiated a broad current of literature in economics and statistical physics

refining and expanding the underlying concepts and models. It is remarkable to note that some of the features of

financial data were general enough to have spawned the interest of several fields in sciences, from economics and

econometrics, to mathematics and physics, to further explore the behaviour of this data and develop models explaining

these characteristics. As a result, some theories found by a group of scientists were rediscovered at a later stage

by another group, or simply observed and mentioned in studies but not formalised. Financial text books presenting

academic and practitioners findings tend to be too vague and too restrictive, while published articles tend to be too

technical and too specialised. This guide tries to bridge the gap by presenting the necessary tools for performing

quantitative portfolio selection and allocation in a simple, yet robust way. We present in a chronological order the

necessary steps to identify trading signals, build quantitative strategies, assess expected returns, measure and score

strategies, and allocate portfolios. This is done with the help of various published articles referenced along this guide,

as well as financial and economical text books. In the spirit of Alfred North Whitehead, we aim to seek the simplest

explanations of complex facts, which is achieved by structuring this book from the simple to the complex. This

pedagogic approach, inevitably, leads to some necessary repetitions of materials. We first introduce some simple

ideas and concepts used to describe financial data, and then show how empirical evidences led to the introduction of

complexity which modified the existing market consensus. This book is divided into in five parts. We first present

and describe quantitative trading in classical economics, and provide the paramount statistical tools. We then discuss

quantitative trading in inefficient markets before detailing quantitative trading in multifractal markets. At last, we we

present a few numerical tools to perform the necessary computation when performing quantitative trading strategies.

The decision making process and portfolio allocation being a vast subject, this is not an exhaustive guide, and some

fields and techniques have not been covered. However, we intend to fill the gap over time by reviewing and updating

this book.

0.1.2 An overview of quantitative trading

Following the spirit of Focardi et al. [2004], who detailed how the growing use of quantitative methods changed

finance and investment theory, we are going to present an overview of quantitative portfolio trading. Just as automation

and mechanisation were the cornerstones of the Industrial Revolution at the turn of the 19th century, modern finance

theory, quantitative models, and econometric techniques provide the foundation that has revolutionised the investment

management industry over the last 20 years. Quantitative models and scientific techniques are playing an increasingly

important role in the financial industry affecting all steps in the investment management process, such as

• defining the policy statement

• setting the investment objectives

• selecting investment strategies

• implementing the investment plan

• constructing the portfolio

• monitoring, measuring, and evaluating investment performance

21

Quantitative Analytics

The most significant benefit being the power of automation, enforcing a systematic investment approach and a struc-

tured and unified framework. Not only completely automated risk models and marking-to-market processes provide

a powerful tool for analysing and tracking portfolio performance in real time, but it also provides the foundation for

complete process and system backtests. Quantifying the chain of decision allows a portfolio manager to more fully

understand, compare, and calibrate investment strategies, underlying investment objectives and policies.

Since the pioneering work of Pareto [1896] at the end of the 19th century and the work of Von Neumann et al.

[1944], decision making has been modelled using both

1. utility function to order choices, and,

2. some probabilities to identify choices.

As a result, in order to complete the investment management process, market participants, or agents, can rely either

on subjective information, in a forecasting model, or a combination of both. This heavy dependence of financial asset

management on the ability to forecast risk and returns led academics to develop a theory of market prices, resulting in

the general equilibrium theories (GET). In the classical approach, the Efficient Market Hypothesis (EMH) states that

current prices reflect all available or public information, so that future price changes can be determined only by new

information. That is, the markets follow a random walk (see Bachelier [1900] and Fama [1970]). Hence, agents are

coordinated by a central price signal, and as such, do not interact so that they can be aggregated to form a representative

agent whose optimising behaviour sets the optimal price process. Classical economics is based on the principles that

1. the agent decision making process can be represented as the maximisation of expected utility, and,

2. that agents have a perfect knowledge of the future (the stochastic processes on which they optimise are exactly

the true stochastic processes).

The essence of general equilibrium theories (GET) states that the instantaneous and continuous interaction among

agents, taking advantage of arbitrage opportunities (AO) in the market is the process that will force asset prices toward

equilibrium. Markowitz [1952] first introduced portfolio selection using a quantitative optimisation technique that

balances the trade-off between risk and return. His work laid the ground for the capital asset pricing model (CAPM),

the most fundamental general equilibrium theory in modern finance. The CAPM states that the expected value of

the excess return of any asset is proportional to the excess return of the total investible market, where the constant of

proportionality is the covariance between the asset return and the market return. Many critics of the mean-variance

optimisation framework were formulated, such as, oversimplification and unrealistic assumption of the distribution

of asset returns, high sensitivity of the optimisation to inputs (the expected returns of each asset and their covariance

matrix). Extensions to classical mean-variance optimisation were proposed to make the portfolio allocation process

more robust to different source of risk, such as, Bayesian approaches, and Robust Portfolio Allocation. In addition,

higher moments were introduced in the optimisation process. Nonetheless, the question of whether general equilibrium

theories are appropriate representations of economic systems can not be answered empirically.

Classical economics is founded on the concept of equilibrium. On one hand, econometric analysis assumes that, if

there are no outside, or exogenous, influences, then a system is at rest. The system reacts to external perturbation by

reverting to equilibrium in a linear fashion. On the other hand, it ignores time, or treats time as a simple variable by

assuming the market has no memory, or only limited memory of the past. These two points might explain why classical

economists had trouble forecasting our economic future. Clearly, the qualitative aspect coming from human decision

making process is missing. Over the last 30 years, econometric analysis has shown that asset prices present some

level of predictability contradicting models such as the CAPM or the APT, which are based on constant trends. As a