My Access Data Gartner E Discovery MQ

2012-09-27

: Pdf Accessdata Gartner E-Discovery Mq AccessData_Gartner_E-Discovery_MQ

Open the PDF directly: View PDF ![]() .

.

Page Count: 40

- Strategic Planning Assumption

- Market Definition/Description

- Magic Quadrant

- Inclusion and Exclusion Criteria

- Context

- Market Overview

- Recommended Reading

- List of Tables

- List of Figures

G00235189

Magic Quadrant for E-Discovery Software

Published: 24 May 2012

Analyst(s): Debra Logan, Sheila Childs

The e-discovery market landscape has shifted dramatically as end users

have begun to demand more complete e-discovery functionality. Many

vendors are responding with broader end-to-end functionality. New

products, acquisitions and shifts in buying patterns have led to a radically

altered picture.

Strategic Planning Assumption

E-discovery vendors will generate up to one-third of their revenues outside North America during

the next three years, up from 15% in 2010.

Market Definition/Description

The market covered by this Magic Quadrant contains vendors of e-discovery software solutions for

the identification, preservation, collection, processing, review, analysis and production of

electronically stored information (ESI) in support of the common-law discovery process for litigation,

regardless of delivery method.

Magic Quadrant

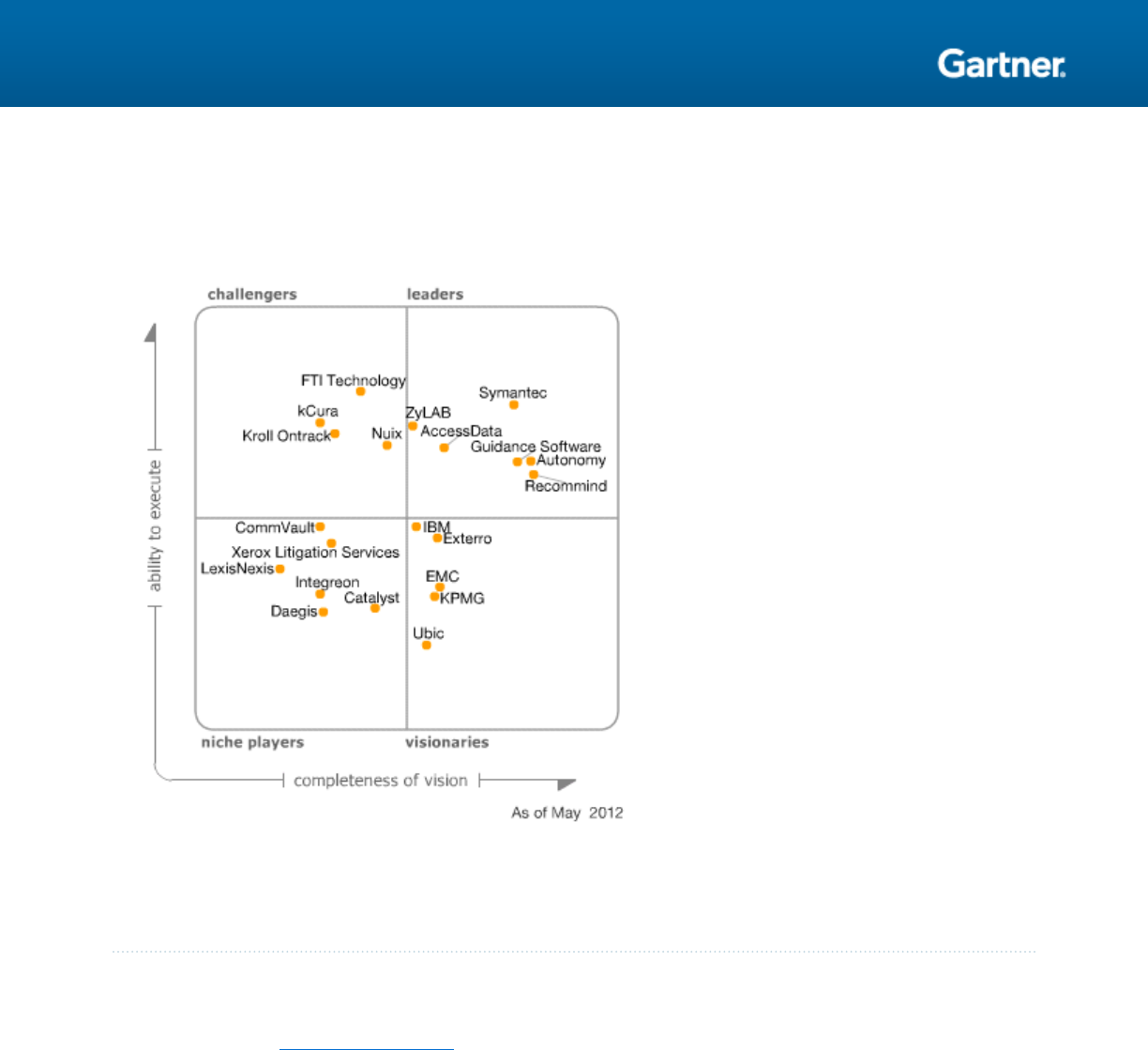

Figure 1. Magic Quadrant for E-Discovery Software

Source: Gartner (May 2012)

Vendor Strengths and Cautions

AccessData

Founded in 1987, AccessData Group is a privately held company, with a workforce of over 450, that

has addressed the e-discovery market since 2008. In 2010, AccessData merged with CT

Summation, and it retained the Summation brand together with the AccessData FTK brand.

Together, the two product sets give AccessData coverage of the Electronic Discovery Reference

Model (EDRM — see "The Electronic Discovery Reference Model and Market Demand Use Cases"

in the Market Overview section for more information), from identification to production. It also has

early case assessment (ECA) capabilities. The AccessData eDiscovery solution is built on the

company's forensics processing and collection technology, FTK, which enables targeted forensic

collection of data from a wide variety of sources, including desktops, servers and structured data

stores. In addition, AccessData's search methodology supports multiple relevancy models, file-

culling methods and concepts, which enables the solution to be used for a wide range of

investigation types, including those into inappropriate activity, remote intrusion, e-discovery and

personally identifiable information (PII). AccessData added ECA capabilities to its solution in 2009.

Page 2 of 40 Gartner, Inc. | G00235189

The company's Summation suite — including heritage products iBlaze, Enterprise and

CaseVantage, as well as the newer Summation Express and Pro products and Summation Litigation

Support Services — covers the review, analysis and production stages of the EDRM.

Strengths

■Identification, preservation and collection are difficult and technically complex parts of the

process, so the ease of use of AccessData's software in these areas is a differentiator, as is its

method of collecting electronic material without disturbing metadata.

■One of the most widely known litigation support applications, Summation, part of the

AccessData Summation product set, is an important asset, which gives it full-spectrum EDRM

coverage.

Cautions

■AccessData has a large customer base of small legal clients, which it will need to continue to

support from a sales and service perspective. This may limit its ability to expand into the large

enterprise segment without additional investment.

■The company must invest further in its marketing and sales organizations to ensure the market

understands its technically revamped and integrated product suite, as well as to continue the

strong growth it saw in 2011.

Autonomy

Autonomy was acquired by publicly traded HP (NYSE: HPQ) in October 2011, and is being operated

as a separate information management software group within HP. Founded in 1996, Autonomy

entered the e-discovery business in 2007 via its acquisition of Zantaz. The company offers

Autonomy eDiscovery, which is the newest release, and also incorporates what was known as

Autonomy Stratify, Introspect and Investigator & ECA. This modular application spans investigation

through review and production. In addition, the company offers Autonomy Legal Hold (ALH) for the

preservation and collection of data. A set of information management products, including records

management, archiving and data protection, is available as well. Products are offered on-premises

or as a service, and over half its customers are corporate (25% are law firms and 10% are service

providers). Traditionally, Autonomy has primarily sold direct, but the acquisition by HP is changing

this — for example, the company recently launched an e-discovery appliance that it has put into the

HP reseller and distribution channel. Customers should expect improved strategic partnerships

(with HP Enterprise Services, PwC and Accenture, for example) as part of the HP deal as well.

Autonomy shows up in many competitive situations — buyers like the company for its broad set of

functionality, vision and market leadership.

Strengths

■Autonomy's technology is rated very highly by many customers: positive feedback includes

ease of use, extensive functionality and scalability, as well as a good focus on the legal user.

Gartner, Inc. | G00235189 Page 3 of 40

■Autonomy has a wide range of products that cover each stage of the EDRM model, with various

deployment models available for each.

Cautions

■Some customers report that support is not responsive, even in the face of substantial

deployment or functionality issues, and that their issues are ignored until they are escalated.

These customers report that it takes a big effort to get Autonomy to respond.

■Feedback from clients and prospects indicates that the sales teams can be difficult to negotiate

with, that the product is expensive, and that sales is not selling the right solution to the problem.

Catalyst

Catalyst, a privately held company with over 140 employees, entered the e-discovery market in

2000. Catalyst's platform is grid-based, allows for automated loading of data, and covers

processing through search, analytics, review and production. In addition, Catalyst recently released

OnRamp, which is an enterprise connector that allows corporations to automatically load raw or

processed files into the Catalyst e-discovery platform. It is designed as a product to be delivered via

the cloud, but with the user having full control over the platform and processes. It is sold using a

software-as-a-service (SaaS) model. Catalyst is focused on automating as much of the e-discovery

process as possible; it supplements the rest of the processing through production phases with

human expertise where necessary. Catalyst has a partnership with BIA, which allows the remote

collection of data from multiple sources into the Catalyst repository. Catalyst also has an integration

with Exterro, its preferred partner for full EDRM coverage. Catalyst provides specialized consulting

services around its product and services, notably expert assistance with large-volume data

searching, analytics and information retrieval using subject matter experts.

Strengths

■Catalyst's foreign-language capabilities are industry-leading and its search technology is best-

in-class, as is its focus on search expertise.

■Catalyst's products for uploading and processing data and producing data as a business

process utility are highly scalable and cost-effective. This focus on cloud-based self-service is a

key differentiator.

Cautions

■Recent partnership announcements with BIA and Exterro, while positive, demonstrate the

extent to which the market has shifted to favor full EDRM solutions, which Catalyst does not

have.

■Catalyst must focus more on marketing to emphasize its differentiation from other SaaS review

and analysis vendors.

Page 4 of 40 Gartner, Inc. | G00235189

CommVault

CommVault is a publicly traded company (NYSE: CVLT) that entered the e-discovery market in

2007. It came from a content archiving and unified data management background, and has moved

into the information governance and management space with a set of product capabilities that

address the needs of legal and compliance archiving buyers. Its current product, Simpana Archive,

is sold with modules for ESI collection, including cloning (backup) and archiving, and content

indexing for search and e-discovery. Simpana's content index and search capabilities are based on

Fast Search & Transfer indexing technology. Simpana's archiving technology focuses on retention

life cycle management, enterprise search, information workflow, records declaration, privacy and

security, e-discovery and compliance, again drawing on the core platform features. Simpana

Content Director is an add-on process and workflow engine that provides content classification and

e-discovery functions. CommVault's key differentiators are deduplication across the entire body of

collected and archived information (as well as backup), the ability to retain and dispose of data in

this archive, and an information governance message, which together give it a larger technological

and strategic footprint than other vendors.

Strengths

■CommVault's unique vision of the market — which encompasses archiving, backup and a

proactive approach to information management as the ultimate answer to e-discovery — is not

an easy one to communicate to the market. The company's comprehensiveness with respect to

information management precludes it from selling to clients that need a quick response to an

imminent e-discovery situation.

■CommVault has a larger technological and strategic footprint than other vendors.

Cautions

■CommVault must gain market share in the core information archiving sector to be on a par with

its most direct competitors.

■Because CommVault's value proposition is based on the underlying archiving platform, decision

cycles are longer. In addition, implementation delays result from the need to have various

decision makers involved. CommVault has a limited ability to sell to legal buying centers, which

is essential in this market.

Daegis

Daegis is a publicly traded company (Nasdaq: DAEG) that has competed in the e-discovery market

since 2003. Daegis's e-discovery capabilities extend from information management through

processing, analysis, review and production. Daegis believes that its Cross-Matter Management

methodology helps increase efficiency throughout the e-discovery process by repurposing

custodian data and attorney work products across multiple matters, eliminating data handoffs and

double processing, while targeting and reducing datasets through iterative search. Daegis' e-

discovery platform, which is available as a hosted offering, is an integrated technology and services

Gartner, Inc. | G00235189 Page 5 of 40

solution. The company's hybrid business model also includes e-discovery-related services such as

project management and document review.

Strengths

■Customers report that they are impressed with the quality of Daegis's project managers, service

and support, which they cite as being highly personalized.

■Daegis has products that span the EDRM.

Cautions

■Daegis's growth has not kept pace with the rest of the market.

■Daegis's staffing profile indicates that the majority of its revenue comes from services.

EMC

Publicly traded EMC (NYSE: EMC) acquired Kazeon in 2009 and offers the product as its e-

discovery solution. The company claims over 500 customers, 70% of which are corporate clients.

The solution is largely targeted at the IT buyer. Kazeon is packaged as an appliance, and offers

functionality predominately focused on collection and ECA. The product can capture data from

various data sources, including file shares, SharePoint, Documentum and EMC SourceOne

archiving, and Symantec Enterprise Vault archive repositories, among others. Kazeon has recently

been integrated with EMC Avamar to support collection from endpoint devices as well. Data can be

held in place or collected into one of the Kazeon supported repositories (such as Documentum or

SharePoint). Kazeon also supports processing functionality, including deduplication, ingestion of

native files, classification and categorization using rule-based methodologies. Many customers cite

the product's low price — EMC tends to include Kazeon as part of larger deals for Documentum or

storage. EMC also offers SourceOne, sold through the backup and recovery solutions division, as a

solution for the information management (archiving) component of the EDRM model.

Strengths

■EMC offers technologies that complement Kazeon in terms of providing more comprehensive

information management: for example, integration with Avamar File System enables the

collection of data from endpoints, while integration with SourceOne enables support for data

captured in an EMC archiving repository.

■Users cite scalability, searching and culling as positive product features; sales and support are

responsive, and professional services are highly rated.

Cautions

■Some customers express dissatisfaction with Kazeon's integration with partner products, and

look to EMC to improve both partner relationships and platform support.

Page 6 of 40 Gartner, Inc. | G00235189

■Clarity of product direction and support for emerging technologies are cited as areas for

improvement, particularly in the broader context of EMC product offerings.

Exterro

Exterro is a privately held company, founded in 2004, which entered the e-discovery market with its

workflow software in 2005. It is an enterprise software development company that specializes in

workflow management, with a well-regarded suite of applications for data mapping, in-house

litigation holds and project management. It has one of the few platforms on the market that includes

data mapping, which enables organizations to track their ESI at an organizational level. Exterro's

Fusion Integration Hub allows integration of existing legal, e-discovery and other systems, such as

archiving and content management systems. Exterro has expanded the applications in the Fusion

suite to span the EDRM and includes in-place ECA, collection, culling, review and production

capabilities, giving it the range of functions most often requested by organizations wanting to bring

e-discovery tasks in-house.

Strengths

■Exterro's software is easy to understand and purchase, and it fulfills the very important need of

legal departments to manage litigation processes flexibly.

■Exterro now has full-spectrum EDRM capability and clients report that pricing is very

reasonable.

Cautions

■Exterro must grow and differentiate to gain market share in a market that is consolidating in

terms of functionality and number of vendors.

■Exterro must invest in marketing to make the market aware of its full-spectrum capabilities.

FTI Technology

FTI Technology is a separately reported business unit of FTI Consulting (NYSE: FCN), a publicly

traded company founded in 1982. FTI has acquired two well-known companies in the e-discovery

market: Ringtail Solutions and Attenex. In 2010, FTI released a version of Ringtail's software that

combines familiar features from both of these companies' well-known products in a simplified and

modernized product set. It performs functions from processing through to production — including

ECA, review and analysis — and is available via a SaaS or enterprise model. Pricing models include

user-based on-premises and SaaS. In addition to software, FTI provides a broad range of e-

discovery consulting and other services, from international data collection and on-site analysis and

review with its Investigate offering, to legal review and full legal process outsourcing with its Acuity

offering. FTI Harvester for Microsoft SharePoint combines software and services for the collection of

SharePoint data.

Gartner, Inc. | G00235189 Page 7 of 40

Strengths

■FTI has powerful technology and a leading platform for machine-assisted review, pushing the

limits of scalability and performance. A recently revamped user interface has made the product

even stronger.

■The breadth and depth of the expertise at FTI makes it a leading global provider among large

litigious companies that frequently need expert assistance, global evidence-gathering teams

and productivity-enhancing products. The company performs well all over the world, whereas

others in its class do not necessarily have the presence or "bench strength" to cover the globe,

which is what many corporations need.

Cautions

■FTI needs to expand its EDRM coverage to reclaim a leadership position.

■FTI has many advanced features and must invest in educating the market about the power of its

solution, which many end users still perceive as complex.

Guidance Software

Guidance Software is a publicly traded company (NYSE: GUID) that was founded in 1997 with a

focus on forensic data collection and analysis. In early 2012, Guidance acquired CaseCentral, a

privately held company founded in 1993, and entered the e-discovery market in 1994. Guidance

now has over 500 employees, post-acquisition. Guidance Software provides coverage for the full

range of EDRM functionality, including an auditable repository-based means of identifying,

collecting, preserving and processing data for e-discovery and a fully featured SaaS-based review

and analysis platform with CaseCentral. The EnCase product range allows data to be searched and

categorized for ECA before or after collection. There are three EnCase products, which all use the

same underlying technology, applicable to this market: EnCase Enterprise (for internal investigations

and small-scale e-discovery collection and processing); EnCase eDiscovery (for small-scale to

large-scale e-discovery); and EnCase Cybersecurity (for information management, such as data

auditing and clean-up). The CaseCentral eDiscovery Platform is used for ECA, analysis, review and

production of documents and emails pertaining to litigation, regulatory requests and internal

investigations. CaseCentral has multimatter management, along with sophisticated semantic

analysis capabilities for legal review and analysis, workflow and reporting features to track and

manage the progress of review, and a range of configurable options. The latest release includes

machine-assisted review features.

Strengths

■The CaseCentral acquisition gives Guidance Software full-spectrum e-discovery coverage.

■Guidance's pricing for CaseCentral review and production is fully transparent and easy to

understand, similar to its enterprise software pricing.

Page 8 of 40 Gartner, Inc. | G00235189

Cautions

■Although it can be used for single cases, CaseCentral's model is most advantageous to those

with multiple cases, because of its multimatter management strategy, which allows attorney

work product reuse.

■Legal users of EnCase say that they would like to have more training, while the product receives

lower ease-of-use ratings than some of its competitors. However, the acquisition of

CaseCentral may change this dynamic.

IBM

IBM (NYSE: IBM) offers e-discovery as part of its Information Lifecycle Governance (ILG) strategy. In

October 2010, IBM acquired PSS Systems and its Atlas portfolio, subsequently launching a new

strategy focused on defensible disposal. IBM's new ILG portfolio is segmented into the following

solution areas, supporting functionality across much of the EDRM model: defensible disposal, e-

discovery, value-based archiving, and records and retention management. The e-discovery solution

area includes IBM Atlas eDiscovery Process Management for both legal and IT, IBM Atlas

eDiscovery Cost Forecasting and IBM Atlas eDiscovery Policy Federation Framework. The Atlas

portfolio provides APIs that support a wide variety of connections to other systems, including email

systems, SharePoint, document management systems and desktops (via the IBM FastBack

product), among others. IBM eDiscovery Manager and eDiscovery Analyzer are also part of this

solution area. IBM Content Collector for Email, Files and SharePoint are part of the value-based

archiving solutions. Analysis capabilities include cost forecasting, with dynamic re-forecasting as

data is collected and production decisions are made. Prior to the acquisition by IBM, PSS had

founded the Compliance, Governance and Oversight Council (CGOC) — a forum of over 1,700

legal, IT, records and information management professionals dedicated to discovery, retention,

privacy and governance practices. IBM continues to play a leading role in this group.

Strengths

■IBM's brand and marketing power, along with its deep customer relationships, enable it to

reach a large base of potential clients.

■Clients report that Content Collector, eDiscovery Analyzer and eDiscovery Manager are easy to

use and have improved dramatically in the past few years. With expanded policy syndication

functionality, IBM retention and hold policy syndication includes InfoSphere Optim's structured

data archive repositories, enabling this functionality across both structured and unstructured

data.

Cautions

■Requests for improvements from customers most frequently concern Atlas products' ease of

use, particularly for larger holds, support for emerging technology and clarity of product

direction. IBM sought to address these issues in 2011 with the launch of Atlas 6.

Gartner, Inc. | G00235189 Page 9 of 40

■Total cost of ownership for the solution can sometimes be high — cost and functionality were

cited most frequently as reasons why organizations purchased an alternative solution. IBM must

work to overcome the perception that IBM solutions are only for "IBM shops."

Integreon

Integreon is a private company, founded in 1998, specializing in providing support services for law

firms and corporate legal departments. Integreon has made significant investments in its e-

discovery business since entering the market in 2005, including acquisitions of Bowne's litigation

support business in 2006, Datum Legal in 2008 and Onsite3 in 2009. Integreon has invested in

defensible process capabilities and software to create an integrated end-to-end e-discovery

solution, from collection to global managed document review, with a mix of its own products and

those of a wide array of third parties. Integreon's collection product (Seek & Collect), hosted review

product (eView) and enterprise processing product (Electronic Evidence Enterprise) were evaluated

for this analysis. These products focus on the collection, processing, review, analysis and

production of ESI, and are available under SaaS and enterprise pricing models.

Strengths

■Integreon has a strong brand and reputation in the legal community, and the ability to access

legal buying centers.

■Integreon has deep client relationships, and provides a range of services, including concierge-

style offerings, to a select client base.

Cautions

■Integreon differentiates on its service offerings, but although it rates very highly in that respect it

needs more software focus to compete in this market. Integreon must invest in marketing to

raise its visibility in the market.

■As a major provider of legal process outsourcing solutions, Integreon is a diversified company

that also provides other legal products and services — which means that software development

may compete internally for resources, resulting in less frequent or expansive software releases.

kCura

A privately held company founded in 2001, kCura entered the e-discovery market in 2006. With an

exclusive focus on the review, analysis and production of documents, kCura's Relativity product is

now considered "best in class" by many legal end users, particularly legal solution providers. While

the Relativity team at kCura focuses on technology development, the product itself is sold directly

to corporations and is also available as a SaaS offering from a wide range of well-known service

providers and hosting partners. Historically, the attorney review application market was dominated

by three or four products, which sufficed before the huge increase in the numbers and types of

electronic information that lawyers have to deal with. Relativity is a product designed in, and for, the

present age of ever-increasing volume, velocity and variety of data.

Page 10 of 40 Gartner, Inc. | G00235189

Strengths

■kCura focuses exclusively on legal end users and the review of production parts of the e-

discovery process. This focus has enabled it to produce best-of-breed technology and to grow

very quickly and profitably.

■kCura's technology is flexible and open, which allows customers to easily customize the

workflows and integrate it with other software.

Cautions

■kCura must increase its focus on building corporate relationships.

■kCura must acquire partners addressing the left-hand side of the EDRM, as the market

increasingly demands a full-spectrum EDRM solution.

KPMG

KPMG has moved decisively from being primarily a service provider to fielding a robust technology

suite that covers the identification to production phases of the EDRM. Its identification, collection

and processing capabilities are called Discover Radar Collector, while additional processing review

analysis and production capabilities are offered via the SaaS-delivered Discovery Radar. Key

differentiators for KPMG include its Global Evidence Tracking System (GETS) and its software-

assisted review, which includes software-based, integrated, flexible sampling methodologies, along

with a review cost estimator.

Strengths

■KPMG is not a traditional software vendor and its business model does not include

commission-based selling, but rather focuses on business development via long-standing

corporate relationships. This positions it very well to sell to the corporate market.

■KPMG has learnt lessons from its experiences as an e-discovery service and software provider

in very difficult and high-stakes cases. Its expertise shows in the approach it takes to building

scalable software for process efficiency and flexibility.

Cautions

■KPMG's business model relies on deep and long-standing relationships with a select client

base, which contrasts with many of the other vendors that are aiming at the mass market with

large sales forces.

■KPMG is perceived as an expensive, high-value option in the marketplace.

Gartner, Inc. | G00235189 Page 11 of 40

Kroll Ontrack

Privately held Kroll Ontrack, founded in 1985, launched its new e-discovery product, Verve, in late

2011. In addition to Verve, Kroll Ontrack offers an outsourced review platform (Ontrack Inview), early

data assessment (Ontrack Advanceview), and a hosted e-discovery repository solution (Ontrack

Guardian) ancillary to its services business. Verve is a SaaS or cloud-based version of these

platforms, purchasable and accessible via the Web by customers wanting to upload data, select

processing criteria, conduct early data assessment and review, and manage production within their

organizations. While 50% of Kroll Ontrack's customers are corporate, its penetration into law firms

is significant and represents the other 50% of its customer base. As a dominant review platform

player, its support for identification, collection or preservation is currently minimal, although

enhanced functionality in this area is on the road map. ECA and machine-assisted review

capabilities are available today in Ontrack Advanceview and Ontrack Inview, respectively. Both

capabilities are also available in Verve. Kroll Ontrack's representation as a solid service provider of

processing, analysis and review means that its new on-premises SaaS/cloud products will be

considered by enterprises that want to bring e-discovery in-house. In addition, as Verve is a new

product, Kroll Ontrack is just beginning to build channel and service provider programs — none are

available at present.

Strengths

■Hosted services are easy to use, and Kroll Ontrack is responsive to requests for enhancements.

Sales and support staff are attentive and easy to work with.

■Kroll Ontrack has a trusted brand, a well-established presence and a reputation for service

excellence, which will continue to serve it well as a service provider and should carry over into

dealings with its software customers.

Cautions

■Verve is a new product and, as such, features may be limited. For example, collection from

database management systems is limited to support for Microsoft SQL Server only, and no API

is available.

■Prospects cite the e-discovery service's high cost and inflexible pricing model as a reason for

selecting an alternative vendor.

LexisNexis

LexisNexis is a private subsidiary of a public company, Reed Elsevier (NYSE: ENL, NYSE: RUK). It

entered the e-discovery market in 2003. For this Magic Quadrant we evaluate only the traditional

Concordance and LAW PreDiscovery software offerings. Concordance is a document review tool

covering review, analysis and production on the right-hand side of the EDRM. It has a long history

and a great deal of brand recognition within the legal industry, being familiar to many lawyers.

Concordance software has long been the mass-market tool of the legal profession for document

review. LAW PreDiscovery is a processing and culling tool that allows all documents to be

processed ahead of legal review, allowing for ECA. Concordance and LAW work together to cover

Page 12 of 40 Gartner, Inc. | G00235189

processing, review, analysis and production, in addition to ECA. LexisNexis has made significant

investments in its products.

Strengths

■LexisNexis is a strong and trusted brand in the legal profession, for which it offers a range of

products and services.

■Pricing for both Concordance and LAW PreDiscovery software is deemed very reasonable by

users, and there is solid and responsive customer support.

Cautions

■LexisNexis has been slow to respond to changes in the market, and its software development

lags behind that of its competitors.

■LexisNexis ends up on many shortlists but it is frequently discounted for its lack of functionality.

Nuix

Nuix is a privately held company that was founded in 2000 and entered the e-discovery market in

2007. It is based in Sydney, Australia, and its geographic progress has been from Asia/Pacific to

EMEA and on to North America. Nuix's biggest strength and most proven technology lies in the fast

processing of data and enabling of early assessment of data in any given matter. It is also

particularly strong in its support for multiple languages, especially double-byte character set ones,

and in its ability directly to support and index difficult container files types, such as major archives

and entire email and workplace collaboration systems (for example, EMC EmailXtender, Symantec

Enterprise Vault, IBM Lotus Notes, Microsoft Exchange and SharePoint), and all major forensic

collection formats. Nuix is building software to carry out litigation holds and can collect data from a

variety of sources. Nuix modules are collectively called the Nuix eDiscovery Platform, Nuix

Enterprise Collection Centre, Nuix Fast Review and Nuix Legal Hold. Because of the technical

architecture, Nuix clients report that these tasks can often be accomplished more rapidly than with

competitive products. This makes the Nuix toolset popular with legal discovery service providers,

many of which use the product as part of their own workflow systems.

Strengths

■Nuix's capabilities extend beyond what it can do in e-discovery, and clients report that although

they buy it for its processing and data analysis capabilities for litigation, they end up using it for

information governance, data categorization and clean-up exercises.

■Nuix has an outstanding feature set, transparent and affordable pricing, and a clear corporate

strategic vision.

Cautions

■Nuix needs to increase its presence in direct corporate sales via its growing channel.

Gartner, Inc. | G00235189 Page 13 of 40

■Nuix needs to expand its functionality by adding more review-focused capabilities in order to

meet growing client demand for full-spectrum EDRM.

Recommind

Recommind is a privately held company that was founded in 2000 and has competed in the e-

discovery market since 2007. Recommind had a strong background in providing search, knowledge

management and information retrieval to law firms, which positioned it well for the surge in demand

for e-discovery software. Recommind's Axcelerate eDiscovery suite can perform litigation holds,

collection, processing, review, analysis and production. With a heritage in enterprise software,

Recommind's pricing is straightforward for all deployment options, including on-premises and in the

cloud. Recommind has long been known for its effective approach to search, and it has used its

engineering knowledge of semantic analysis to launch predictive coding, which helps reduce the

amount of manual labor required in the initial stages of a document review exercise. As review is the

most expensive part of the discovery process, predictive coding has the potential to reduce costs

dramatically. Based on its range of functionality, Recommind should be on the shortlist of any

company with a high case load that aims to bring e-discovery in-house or use a hybrid/hosted

model in order to cut costs.

Strengths

■Recommind developed and helped popularize predictive coding, and has garnered market

attention and market share with its patented predictive coding workflow.

■Recommind has full-spectrum EDRM functionality and multiple deployment options, including

on-premises, cloud-based and hybrid.

Cautions

■Recommind is generally regarded as a relatively expensive option, and although it makes

customer shortlists quite frequently, it has sometimes been discounted because of its price. The

company says it has recognized this issue and as of 1Q12 has issued revised pricing with more

flexible options.

■Recommind must educate the market about its full-spectrum capabilities, as well as its

comprehensive list of deployment options, as it is still perceived as a behind-the-firewall, right-

hand-side solution.

Symantec

Symantec is a publicly traded security, storage and information management company (NYSE:

SYMC) that acquired Clearwell Systems in May 2011 for its e-discovery products. Clearwell covers

the identification, preservation, collection, processing, review, analysis and production stages of the

EDRM, along with ECA. Symantec has a large number of customers across its e-discovery portfolio.

Clearwell supports connectors to SharePoint, document management systems (Alfresco,

Documentum, IBM Content Manager and FileNet, Interwoven, and OpenText), numerous email

archives, file systems and network-attached storage. The Identification and Collection Module is

Page 14 of 40 Gartner, Inc. | G00235189

integrated with the other Clearwell Modules, so collected data can be processed, analyzed,

reviewed and produced without import/export. Analysis is supported via a Web browser, and

iClearwell provides access to the eDiscovery Platform from an iPhone or iPad. The solution is

offered as an appliance, and is available through a network of partners and via legal services

providers as hosted SaaS. In addition to Clearwell, Symantec offers Enterprise Vault as an on-

premises archiving solution, and has recently acquired LiveOffice, its longtime OEM partner for

Enterprise Vault.cloud. Both of these archiving solutions include e-discovery functionality. Symantec

is highly committed to the information governance market, as evidenced by these recent

acquisitions and by the formation of a separate information management group with a dedicated

sales force.

Strengths

■Symantec (Clearwell) is cited by its customers as being easy to buy, implement and use. It is

particularly well regarded by legal professionals in terms of ease of use.

■Symantec (Clearwell) is one of the most referenceable brands in the market, and is often cited

by organizations as their primary e-discovery provider/solution.

Cautions

■Integration of Clearwell and Enterprise Vault is under way, as is integration of Clearwell and

Enterprise Vault.cloud. Customers should understand the road map and potential disruptions to

Symantec's established portfolio.

■Some customers state that Clearwell lacks key functional requirements, particularly in linear

document review. Prospects and customers state that they would like an alternative to

Symantec's volume-based pricing model.

Ubic

Ubic is a publicly traded company and a new entrant to this year's Magic Quadrant. It has a suite of

products for e-discovery, which it calls Lit i View. The majority of Ubic's business involves

Japanese, Chinese and South Korean companies involved in common-law litigation. Ubic has

extensive experience and expertise in handling hundreds of international matters, with its

specialized focus on Asian languages, and its facilities, language skills and staff in those regions,

being a strong differentiating factor. Ubic's software supports the two distinct clusters of e-

discovery functionality: preservation and collection behind the firewall on the left-hand side of the

EDRM; and processing, review and analysis via hosted SaaS on the right-hand side.

Strengths

■Ubic has full-spectrum EDRM coverage, from identification to production.

■Ubic is uniquely competent in Asian-language processing and review.

Gartner, Inc. | G00235189 Page 15 of 40

Cautions

■Ubic must establish itself against very strong U.S.-based brands if it wants to make inroads into

the U.S. market, as this is where the majority of the business is and will remain.

■Ubic must differentiate beyond its Asian-language competence against a number of similar

offerings.

Xerox Litigation Services

Xerox (NYSE: XRX) entered the e-discovery market in 2002 and has over 300 employees working in

its e-discovery business, Xerox Litigation Services. It is focused on collection, processing and

hosting, along with review and analysis and production, through the OmniX review platform and

CategoriX automated document classification system. All the offerings are delivered via a SaaS

model. Xerox Litigation Services covers the collection, processing, review, analysis and production

phases of the EDRM. Its targets are Fortune 100 companies with large litigation portfolios. Xerox

believes in the traditional e-discovery service provider model, which relies on reasonable software

for review and analysis, and excellent project managers and e-discovery consultants, along with

deep customer relationships. Xerox's acquisition of Affiliated Computer Services (ACS), a business

process outsourcing and IT services consultancy, has added depth and breadth to Xerox's sales

and delivery capabilities in the e-discovery market.

Strengths

■Connection to Xerox's R&D resources (Parc and Xerox Research Center Europe) for semantic

modules and other technologies will continue to enable Xerox Litigation Services to respond

flexibly and capably to demands to process increasing volumes of ever-more-diverse data.

Examples of commercialized technology from Xerox R&D include CategoriX, email analytics,

clustering and foreign-language identification tools that are widely used by Xerox Litigation

Services' client base.

■Access to the ACS sales force, along with a core of experienced and well-known discovery

attorneys, gives Xerox Litigation Services an opportunity quickly to claim mind share and

market share against SaaS and service provider competitors.

Cautions

■Xerox does not aim to break out of the traditional litigation service provider model, and although

Gartner believes this approach to be sustainable, it is also limited.

■Despite having long-standing client relationships — including Fortune 500 corporate clients that

have worked with Xerox Litigation Services since the company's inception — the company

competes in a part of the market in which clients sometimes use multiple vendors for different

types of matter and where there is therefore little brand loyalty.

Page 16 of 40 Gartner, Inc. | G00235189

ZyLAB

ZyLAB is a privately held company that was founded in 1983. It is now a veteran information

retrieval and archiving vendor specializing in e-discovery, and has language capabilities and a

geographic distribution wider than those of any other vendor. It offers the ZyLAB eDiscovery and

Production system, which is based on the ZyLAB Information Management platform. Thanks to its

long heritage in search and information retrieval, ZyLAB's capabilities include identification,

collection, preservation, processing, review, production and ECA, based on strong textual analytics

and other semantic technologies. The company offers its products through a software licensing and

installation model, and as SaaS. ZyLAB is highly referenceable, extremely stable and enjoys a loyal

client following, despite its low-key approach to marketing. ZyLAB's ability to recruit and retain

talented personnel is key to its success, and its recruitment of thought leaders in 2010

demonstrated this again. ZyLAB's functionality is equal to any of the market leaders, and it should

be considered alongside them.

Strengths

■ZyLAB is very well known to, and represented in, federal, state and local governments; legal

teams and courts; corporate counsels and executive boards; and law enforcement, security,

intelligence and investigative agencies.

■ZyLAB addresses text, images, audio and video very effectively.

Cautions

■ZyLAB is — and, according to the company's founder, will remain — privately held, which is

sometimes a hurdle for corporate procurement departments.

■ZyLAB supports only Microsoft operating systems.

Vendors Added or Dropped

We review and adjust our inclusion criteria for Magic Quadrants and MarketScopes as markets

change. As a result of these adjustments, the mix of vendors in any Magic Quadrant or

MarketScope may change over time. A vendor's appearance in a Magic Quadrant or MarketScope

one year and not the next does not necessarily indicate that we have changed our opinion of that

vendor. It may be a reflection of a change in the market and, therefore, changed evaluation criteria,

or of a change of focus by a vendor.

Added

KPMG met the inclusion criteria for the 2012 Magic Quadrant.

Ubic met the inclusion criteria for the 2012 Magic Quadrant.

Note: HP entered the market in October 2011 via its acquisition of Autonomy. HP has retained the

Autonomy brand and is therefore referred to in this document as Autonomy.

Gartner, Inc. | G00235189 Page 17 of 40

Dropped

CaseCentral was acquired by Guidance Software in early 2012.

Clearwell Systems was acquired by Symantec in 2011.

Epiq did not meet one or more of this year's inclusion criteria.

Iron Mountain's digital business was acquired by Autonomy in 2011.

Ipro did not meet one or more of this year's inclusion criteria.

Inclusion and Exclusion Criteria

To be included in this Magic Quadrant, a vendor must sell enterprise software licenses, a software

appliance or SaaS conforming to Gartner's definition of SaaS (see Note 1). This Magic Quadrant

contains only vendors that sell software licenses, software appliances or software subscriptions,

although some of these vendors do also provide legal services — indeed, in some cases that is the

main part of their business in financial terms.

To be included in this Magic Quadrant, a vendor must also address at least two of three broad

functional areas, relating to the EDRM, that we have chosen to reflect the clustering of users' wants

and needs and the process of e-discovery. Although we have seen a shift in buyers asking for end-

to-end functionality, there are still a significant number that will want left-hand-side or right-hand-

side EDRM functionality only:

■Left-hand side of the EDRM: Identification, collection, preservation and processing vendors

that have either a workflow-based system for attorneys to track custodian-led collection, or a

search and information access system for IT and legal departments to use. Vendors that focus

on this functionality should also have ECA or early data assessment functionality. The target

end users for this kind of e-discovery software are IT and legal professionals (for Gartner's

definition of ECA, see Note 2 and "Early Case Assessment: E-Discovery Beyond Judges and

Regulators Is About Risks, Costs and Choices").

■Right-hand side of the EDRM: Vendors focused on processing, reviewing, analyzing and

producing documents, either in ECA or at a later state of review, whose products include

features such as document categorization, redaction and mechanisms to mark documents as

privileged or to categorize and process them in other ways. This category includes vendors of

the attorney review platforms that the legal community has used for 10 years or more to

perform document review (it encompasses the older term "litigation support databases"). Many

vendors that offer right-hand-side review capability are also increasingly offering some form of

machine-assisted review. Broadly speaking, this is the application of machine learning and

analysis techniques to enable document prioritization for human review or to otherwise enable a

focus on a reduced set of potentially responsive documents. The target end users for this kind

of e-discovery software are legal professionals.

Page 18 of 40 Gartner, Inc. | G00235189

■Information management: Vendors offering information management or repository

functionality plus e-discovery functionality on the left-hand side of the model, typically functions

for litigation hold, collection and export of data from the repository for review. Vendors must

have components that allow for ad hoc collection of data outside the archive, conforming to

what is described in the first bullet above. If the software does not include components for

identification, custodian-led collection tracking, preservation and collection outside the normal

archiving process, it is not included in this Magic Quadrant. The target end users for this kind of

software are IT and legal professionals.

Vendors with end-to-end functionality covering the whole EDRM are also included. There has been

a definite increase in customer demand for end-to-end e-discovery functionality in 2011 and 2012.

In addition, vendors must satisfy quantitative requirements regarding market penetration and

customer base. Specifically, they must:

■Generate at least $20 million in revenue per year from the sale of e-discovery software.

■Own the intellectual property and copyright to the software.

■Have at least 50 customers in production.

The vendors shown in this Magic Quadrant have met these inclusion criteria, including the revenue

threshold. However, there are many other vendors in the market that Gartner tracks. The following

list (which is purely representative) details e-discovery vendors that Gartner tracks but does not

formally rate in its Magic Quadrant.

Epiq Systems

Epiq Systems is a public company (Nasdaq: EPIQ) that provides software and services globally and

covers a wide range of e-discovery and document review solutions. All of Epiq's offerings can be

delivered on-premises, as hosted solutions or as SaaS.

Ipro

Ipro is a private company that was founded in 1989 as an e-discovery specialist. It has evolved over

the years and enjoys a strong reputation among law firms and service providers. It now offers full-

spectrum EDRM coverage. It supports SaaS and concurrent-user pricing. Ipro has focused its

efforts on software engineering to produce robust code that can be deployed in different ways. Its

software is easy to use, the company offers transparent pricing, and it is willing to work with other

vendors in collaborative partnerships. The company thoroughly understands the changing market

landscape for e-discovery and has a good road map for meeting the evolving market conditions. It

must acquire channel partners and other means of addressing the corporate e-discovery market.

Ipro has demonstrated more vision than many competitors in the e-discovery market in terms of

both functionality and acknowledgment of changing market conditions by seeking partnerships with

corporate software providers. It has a strong brand, a sterling reputation in the legal community and

the ability to access legal buying centers.

Gartner, Inc. | G00235189 Page 19 of 40

Orange Legal Technologies

Founded in 1995 as The Litigation Document Group, the company rebranded itself as Orange Legal

Technologies in 2008 to correspond with the introduction of its proprietary e-discovery technology,

the OneO Discovery Platform. OneO is an integrated and Web-accessible platform that provides

online ECA, processing and review of unstructured data from a hosted centralized repository. In

2011, the company introduced its second proprietary offering, PurpleBox. This is a downloadable

virtual appliance that enables in-place collection and assessment of newly discovered and

previously privileged (work product) ESI across multiple document repositories. Additionally, the

company has strong partnerships that allow for the integration of emerging technologies, to include

predictive coding and legal hold, into its offerings.

ZL Technologies

ZL's Unified Archive provides a highly scalable platform for archiving, e-discovery, records

management and compliance, which can support billions of messages and/or documents within

one repository, with fast ingestion and search. It provides the complete suite of e-discovery

functions in the archive, including preservation/legal hold, collection, processing, case

management, review, analytics, data visualization, redaction and production.

Evaluation Criteria

Ability to Execute

Product/Service: The core goods and services offered by the vendor that competes in/serves the

defined market. According to the selection criteria, vendors that address the left-hand side of the

EDRM must have some instantiation of identification, preservation or litigation hold, collection and

processing (which some call "culling") functionality. First-pass review, preliminary document

categorization and tagging, or what some vendors term ECA, is a highly desirable function, but

varies significantly in how vendors implement it. Vendors addressing the right-hand side of the

EDRM must offer some processing, review and analysis features, such as search, categorization

and tagging capabilities. Ease of use, intuitive user interfaces, attorney-focused workflow, advanced

but transparent semantic analysis features, native file format review, and foreign-language support

are all considered desirable features from the end user's point of view. Vendors were also evaluated

by customer ratings for ease of use, platform support, support for emerging technologies and

overall functionality. The rating also took into account the number of times a vendor appeared on

prospect shortlists but was not selected because of a lack of product functionality.

Overall Viability (Business Unit, Financial, Strategy, Organization): Viability includes an

assessment of the overall organization's financial health, the financial and practical success of the

business unit, and the likelihood that the business unit will continue to invest in the product, offer

the product and advance the state of the art within the organization's product portfolio. Gartner has

a standard financial rating methodology that we used to rate the vendors. It is based on publicly

reported numbers for public companies, and on numbers supplied to Gartner and verified by us, for

their last business year. It does not depend on absolute values but on relative ones, and thus seeks

to remove the disparities that exist in a market where a vendor the size of HP or IBM competes with

Page 20 of 40 Gartner, Inc. | G00235189

startups. These ratings, plus relative growth, provide us with our final rating. This rating is not just

numeric, but also takes into account factors such as whether there is a strong management team,

employee retention and longevity. Gartner estimates that the enterprise e-discovery software

market came to $1.0 billion in total software vendor revenue in 2010. The five-year compound

annual growth rate (CAGR) is approximately 16%.

Sales Execution/Pricing: This covers a vendor's capabilities in all sales and presales activities, and

the structure that supports them. This includes deal management, pricing and negotiation, presales

support and the overall size and effectiveness of the sales channel. One of the major demands of

today's corporate market is transparent, predictable and flexible pricing. Vendors that do not

address, or are not trying to address, this demand are demonstrating that they do not understand

the direction in which the market is moving. Other factors considered include the fielding of legal

overlay sales teams to champion the company, act as thought leaders and close deals, if

necessary. This is an especially important consideration for technology companies. Transparent,

flexible and predictable pricing is essential in the e-discovery market to address the increasing

influence of corporate buying centers in deciding the terms of many e-discovery purchases. All

vendors had to document their deployment and pricing models — that is, whether their software

was available as an appliance, through a standard enterprise software license or as SaaS. The

experience, professionalism and responsiveness of a company's sales teams is important, and we

evaluate these factors on the basis of client and reference input. A vendor's ability and willingness

to perform proofs of concept (POCs) is also important, and references told us that, with certain

vendors, "try before you buy" arrangements or POCs were so successful that they did not even

open their tendering process to competitive bidding. For smaller vendors, having service providers,

technology-focused system integrators or larger technology vendors as channels is particularly

important. There was also a customer rating component to this criterion.

Market Responsiveness and Track Record: The ability to respond, change direction, be flexible

and achieve competitive success as opportunities develop, competitors act, customer needs evolve

and market dynamics change. This criterion also considers the vendor's history of responsiveness.

It concerns the organization's ability to meet its goals and commitments. Factors include the quality

of the organizational structure, including skills, experiences, programs, systems and other vehicles

that enable the organization to operate effectively and efficiently. Track record is determined by how

quickly a company can respond to changing market needs. Here, we looked at the company's

overall customer numbers and accounts, along with how frequently they were mentioned as

potential providers on prospect shortlists. This data came from customer references and Gartner's

inquiry service.

Marketing Execution: The consistency, clarity, quality, creativity and efficacy of programs

designed to deliver the organization's message to influence the market, promote the brand and the

business, increase awareness of the products, and establish a positive identification with the

product, brand and organization in the minds of buyers. This "mind share" can be driven by a

combination of publicity, promotional initiatives, thought leadership, word of mouth and sales

activities. For vendors that come from technology markets, presence in legally focused publications

and at tradeshows, and membership of professional and trade associations, is important. Equally,

for vendors that come from legal markets, presence in technology-focused publications and at

tradeshows, and membership of professional associations, is important. All vendors will benefit

Gartner, Inc. | G00235189 Page 21 of 40

from an ability to attract and retain industry thought leaders, especially those known in legal circles.

Finally, and perhaps most importantly, vendors must have a clearly articulated product set that

clients can quickly understand and purchase. How well a vendor executed was also evaluated on

the basis of the number of customer references it had, other than those it explicitly provided to us.

Customer Experience: Relationships, products and services or programs that enable clients to

succeed with the products evaluated. Specifically, this criterion includes implementation

experience, and the ways customers receive technical support or account support. It can also

include ancillary tools, the existence and quality of customer support programs, availability of user

groups, service-level agreements and so on. We judge these factors on the basis of written and oral

interviews with reference clients, as well as client inquiry data. Evidence of vendor displacement,

poor client service and incompetent or overly aggressive sales techniques was taken into account.

Additionally, reports of "shelfware" or displacement were taken into account when checking client

references, as software that ends up not being deployed, or that is displaced, is clearly not meeting

users' basic needs. Customer experience was rated by a numeric scale provided by references on

support and sales, along with a count of how many times references reported that vendors were

being replaced and the numbers of negative comments Gartner received about the vendor, both

from reference surveys and through Gartner's inquiry service.

Operations: Not rated, but we include operational criteria within Marketing Responsiveness and

Track Record, rating the organization's ability to deliver on its stated aims as a direct result of

operational effectiveness.

Table 1. Ability to Execute Evaluation Criteria

Evaluation Criteria Weighting

Product/Service High

Overall Viability (Business Unit, Financial, Strategy, Organization) Standard

Sales Execution/Pricing Standard

Market Responsiveness and Track Record Standard

Marketing Execution High

Customer Experience High

Operations No Rating

Source: Gartner (May 2012)

Completeness of Vision

Market Understanding: A vendor's ability to understand buyers' wants and needs and to translate

that understanding into products and services. Vendors that show the highest degree of vision

listen to and understand buyers' wants and needs, and can shape or enhance them. In the e-

Page 22 of 40 Gartner, Inc. | G00235189

discovery market, vendors demonstrate understanding through their interpretation of existing and

emergent case law and timing of responses to that case law, and by whether and how they address

the market's three segments (law firms, corporations and service providers), and two buying centers

(IT and legal end users). We used customers' numeric rating of a vendor's legal and technical

expertise as one component in determining a score for this criterion. We also used a correlation

between what various vendors said about each other to determine whether or not they had an

independently verifiable view of the competitive landscape, which any vendor must understand in

order to be at maximum effectiveness. Everyone has competitors, and a realistic understanding and

recognition of the strengths and weakness of one's competitors is a large component of market

understanding.

Marketing Strategy: A clear, differentiated set of messages, communicated consistently

throughout the organization and externalized through a website, advertising, customer programs

and positioning statements. In the e-discovery market, vendors must understand the dual buying

centers of the legal and IT departments and create appropriate marketing programs to reach them.

They should understand and use the EDRM in their marketing communications; have a clear

statement of differentiation — for example, forensically sound collection, advanced search, and

predictive coding functions, or full EDRM coverage; and demonstrate thought leadership by hiring

appropriate legal personnel to champion them in industry forums.

Sales Strategy: The strategy for selling products that uses an appropriate network of direct and

indirect sales, marketing, service and communication affiliates to extend the scope and depth of

market reach, skills, expertise, technologies, services and the customer base. Vendors selling to

enterprises' legal departments or law firms must have legal expertise to champion their services and

close deals. Gartner also looks for consistency in sales techniques, and for willingness and ability to

perform POCs and other demonstrations that the software can do what it claims. Although POCs

are impossible in some cases, the number of vendors that offer them is substantial. Finally, the

ability to sell and deploy tools quickly is important because of the sometimes unforgiving deadlines

that regulators and investigators impose on organizations.

Offering (Product) Strategy: There were two major trends that characterized this year's market.

First, clients were looking for broader functionality across the EDRM, encompassing both the left-

and right-hand sides. Second, machine-assisted review, referred to by some vendors as predictive

coding, a form of machine learning, has become a requirement for products that lawyers use.

Companies that have not responded to these trends are now "behind the curve." Vendors were

rated on both the presence of these differentiators and how well they worked. Additionally, we

factored in whether vendors also offered "additional" functionality that related to e-discovery,

specifically archiving and multimatter management of cases. The market has become increasingly

intolerant of "point" solutions for things like litigation hold functionality and of moving data from one

system to another. In 2011, increased emphasis was placed on machine-assisted review

techniques, particularly those that use machine learning to help human experts train systems to

categorize documents appropriately. This trend has a long way to run, as the underlying issues and

technologies must be tested and understood by the legal community, but the outcome is inevitable

due to the nature of the problem. Reliable machine-assisted techniques are essential in order for the

system to continue to function effectively and — to quote from the first rule in the U.S. Federal

Gartner, Inc. | G00235189 Page 23 of 40

Rules of Civil Procedure — "secure the just, speedy and inexpensive determination of every action

and proceeding."

Business Model: The soundness and logic of the vendor's underlying business proposition. A

business model is the rationale for how an organization creates, delivers and captures value. A

number of factors were considered. A vendor's mix of corporate, law firm and solution provider

clients is an important factor. Buying decisions, even for attorney review platforms, are increasingly

being made by corporations, not law firms. Although a vendor can address all three segments, and

some do, being too ambitious here or failing to match products, marketing and sales resources to

these segments indicates a lack of market understanding and therefore an unworkable business

model. The second key consideration in this criterion was the number of service and project

management personnel a company had in its e-discovery groups, versus the number of software

developers, with the software development model being favored over the service delivery one. In

the e-discovery market it is also important that companies that combine products and services have

a clear differentiation between the two, and that the incentives for their sales forces do not rely on

using software to sell services. Because this Magic Quadrant has a software focus, Gartner has

paid particular attention to the way in which a company is earning its money and subsequently

investing it. In our evaluation of vendors' business models, Gartner evaluated the subcriteria of

goals (whether there is a vision that can be expressed in a single declarative sentence), objectives

(whether there are quantitative targets), audience (whether the company has a clear understanding

of its current and prospective clients), strategy (whether there is a road map tying goals, objectives

and audience together) and tactics (whether the company is doing the right things to achieve its

objectives).

We have excluded three vision criteria from our evaluation of the e-discovery market:

■Vertical/Industry Strategy: This is not important at this stage in the market's development. If a

company has such a strategy, it is covered by the Market Understanding criterion with its three

segments of law firms, corporations and service providers.

■Innovation: Gartner's formal definition of innovation is not "product innovation" but "direct,

related, complementary and synergistic layouts of resources, expertise or capital for

investment, consolidation, defensive or pre-emptive purposes."

■Geographic Strategy: Given the jump from 7% to 15% of vendor revenue coming from outside

North America, we would expect most vendors, particularly the larger ones, to have a sales and

marketing presence in Europe and Asia/Pacific, and also to have a strategy for addressing

these growing markets. Next year, depending on the data from the various markets, we will add

this to our evaluation criteria.

Page 24 of 40 Gartner, Inc. | G00235189

Table 2. Completeness of Vision Evaluation Criteria

Evaluation Criteria Weighting

Market Understanding Standard

Marketing Strategy Standard

Sales Strategy Standard

Offering (Product) Strategy High

Business Model High

Vertical/Industry Strategy No Rating

Innovation No Rating

Geographic Strategy No Rating

Source: Gartner (May 2012)

Quadrant Descriptions

Leaders

The Leaders in this year's Magic Quadrant have three primary characteristics.

First, they have functionality that covers both the left-hand side (identification, preservation or

litigation hold, collection, ECA and processing) and right-hand side (processing, review, analysis

and production) of the EDRM. A presence in the enterprise information archiving (EIA) market, as

evidenced by inclusion in "Magic Quadrant for Enterprise Information Archiving," and functionality

known in the market as machine-assisted review or predictive coding, were also factors that we

considered. While Gartner recognizes that not all enterprises — or even the majority of them — will

want to perform legal review work in-house, more and more are dictating what review tools will be

used by their outside counsel and/or legal service providers. As practitioners become more

sophisticated, they are demanding that the data change hands as few times as possible. They see

this as a way to reduce both costs and risks. This is a continuation of a trend we saw developing

last year, but it has risen dramatically in importance, as evidenced both by inquiries from Gartner

clients and as reported by the vendors themselves, as the priorities of their customers and

prospects.

The second characteristic is that Leaders' business models clearly demonstrate that their primary

focus is software development and sales, versus provision of services. There are several vendors

with mixed software and service models in the Leaders quadrant, but their commitment to software

Gartner, Inc. | G00235189 Page 25 of 40

development, as evidenced by the size of their development teams, contrasts with their professional

services personnel.

The third characteristic is that Leaders performed well financially and from a growth perspective.

This does not favor only large companies, but takes into account a number of factors, including

overall average market growth (see "Market Trends: Expect Disruption and Divergence in the E-

Discovery Software Market, 2012").

Full-spectrum EDRM coverage is now a requirement, not an option, for a vendor to be considered a

Leader. Thus, a number of vendors that had previously been considered Leaders have moved into

the Challengers or Visionaries quadrants.

There are six Leaders this year.

Autonomy was acquired by HP in October 2011, and is retaining its brand as the information

management software business unit of HP. Autonomy is a brand and marketing powerhouse that

appears on many clients' shortlists. It was well positioned to capitalize on the demand for full-

spectrum EDRM. It also has a leading enterprise information archiving product.

AccessData and Guidance Software both have strong forensic collection tools, having evolved from

that space. Both have also acquired attorney review products — Guidance bought CaseCentral and

AccessData bought Summation — and both focus on software development and sales, rather than

professional services.

Recommind evolved from the enterprise search space, thus qualifying it to perform left-hand-side

collection tasks. Its attorney review tool features well-developed predictive coding functionality, and

Recommind led the market in developing and marketing this functionality.

Symantec purchased Clearwell in 2011, giving the company breadth in its offering. Symantec now

appears on almost all shortlists and is cited by many of its competitors as being among their top

three competitive threats.

ZyLAB is a privately held company that has been in business for many years, serving the enterprise

search, government forensics and law enforcement markets. Last year it changed its strategy to

focus solely on the e-discovery market. It has extremely high rates of customer satisfaction for both

functionality and support.

Challengers

Challengers score strongly for their ability to execute, but fall short in some aspects of their vision.

Former Leaders that have moved into the Challengers quadrant this year failed to anticipate market

demand for full-spectrum EDRM coverage. One of the primary features of the e-discovery market is

that many large litigious companies continue to pursue hybrid strategies when it comes to

managing their litigation burdens: that is, they use in-house and outsourced capabilities. Many of

the Challengers address this aspect of the market very well; that is, they offer legal process

outsourcing with good software solutions that clients can buy in several ways, or they serve the still

very large legal solution provider channel.

Page 26 of 40 Gartner, Inc. | G00235189

There are four Challengers this year.

FTI Technology has a good blend of software and services, as well as being one of the largest

vendors in the market in terms of revenue. FTI is one of the most technically capable vendors in the

market, turning its field experience into high-quality review software that is well regarded. It has a

very high proportion of developers and a favorable mix of corporate clients, as compared to law

firms, as Gartner believes law firms are increasingly being dictated to by their corporate clients in

terms of which review software to buy. The sophistication of Ringtail (a processing, review analysis

and production engine) as a review tool is rated very highly by its users. The product has advanced

visualization capabilities and very solid technology-assisted review features. To reclaim a position in

the Leaders quadrant, FTI must address clients' desire to move the upfront part of the e-discovery

process in-house, by addressing the left-hand side of the EDRM.

kCura has strong market penetration among law firms and service providers, and has demonstrated

leadership characteristics in the market for attorney review platforms, or right-hand-side EDRM.

Although kCura has continued to grow its market share, its focus on developing its right-hand-side

capabilities may serve to limit its ultimate progress, given the market demand for full-spectrum

EDRM. It is trying to break into the enterprise market, but currently does most of its business

through solution providers.

Kroll Ontrack is a large and powerful competitor in the e-discovery software and services market.

Like FTI, it is a good example of a provider that customers can turn to for both software and

services. Kroll has recently revamped its software offerings and that change has been well received

in the market. It has also made significant strides in making its pricing and provisioning strategies

more transparent.

Nuix offers strong choices for preservation, collection and processing, along with ECA, and is

frequently seen on shortlists alongside several Leaders. It has achieved very strong revenue growth

during the past year, driven by its transparent pricing model and relatively low cost. It must continue

to increase its market share and expand its functionality. Nuix's vision ultimately reaches into

information governance, and because the market is headed in that direction (Gartner believes), it is

well positioned to continue to do well.

Visionaries

Visionaries are either on a par with or ahead of the market in terms of their product offerings. This

year's Visionaries share several characteristics, the first of which is that they offer full-spectrum

EDRM coverage. We also looked at their business models, in terms of their mix of corporate clients

to other types, such as law firms and service providers. Finally, Visionaries show a strong

commitment to continued innovation, evidenced by their investment in technical development

resources.

There are five Visionaries this year.

EMC has moved from a position in the Challengers quadrant. It acquired Kazeon, which does have

review capabilities, to round out its offerings, but does not seem to be making effective use of the

Gartner, Inc. | G00235189 Page 27 of 40

asset to gain traction in the marketplace. Based on our reference survey and Gartner inquiry data,

EMC is on far fewer shortlists than its main rivals and overall has less of an impact on the market.

This accounts for its position in the Visionaries quadrant. It must demonstrate more sales and

marketing effectiveness in order to fulfill the promise of its early vision.

Exterro's Fusion platform is alone in being built on top of a general-purpose workflow engine and

integration hub. This means it can handle not only the e-discovery process across departmental and

complex organizational structures, but can also serve as a platform for integrating IT systems (for