Direct Edge XPRS API Manual V 1.30

User Manual: Pdf

Open the PDF directly: View PDF ![]() .

.

Page Count: 49

Edge XPRS Specifications

(High Performance API)

Version 1.30

June 10, 2013

Produced by:

Direct Edge

545 Washington Blvd, Jersey City NJ 07310

www.directedge.com

Direct Edge API Specifications for Equities 3

Direct Edge API Specifications for Equities

4

Table of contents

Chapter 1

About this Document............................................................................................... 5

1.1

Summary of Changes ....................................................................................................... 5

Chapter 2.

Overview ................................................................................................................... 9

2.1

Hours of Operation ........................................................................................................... 9

2.2.

Contact Information ........................................................................................................... 9

2.3.

Connectivity and Testing ................................................................................................... 9

Chapter 3.

Message Exchange Protocol ................................................................................ 10

3.1

Packages......................................................................................................................... 10

3.2.

Login ................................................................................................................................ 10

3.3.

Package Sequence ......................................................................................................... 10

3.4.

Heartbeats ....................................................................................................................... 11

3.5.

End of Session ................................................................................................................ 11

3.6.

Data Types ...................................................................................................................... 11

3.7.

Summary of MEP Messages........................................................................................... 11

3.8.

MEP Message Formats ................................................................................................... 12

Chapter 4.

Order Types Supported by the API ...................................................................... 15

4.1.

Enter Order –Short and Extended Format ...................................................................... 15

Chapter 5

Direct Edge Order API ........................................................................................... 17

5.1

API Architecture .............................................................................................................. 17

5.2

Data Types ...................................................................................................................... 17

5.3

Supported Messages ...................................................................................................... 17

5.4

Message Formats ........................................................................................................... 22

Chapter 6

Appendices ............................................................................................................. 49

6.1

Appendix A: Direct Edge Symbology .............................................................................. 49

6.2

Appendix B: Lock/Cross Re-Pricing Options .................................................................. 50

Direct Edge API Specifications for Equities 5

Chapter 1 About this Document

This document provides guidelines for accessing all of the Direct Edge Stock Exchange

platforms. It contains information regarding API connectivity and provides formats for submitting

orders to the EDGX Exchange and EDGA Exchange.

1.1 Summary of Changes

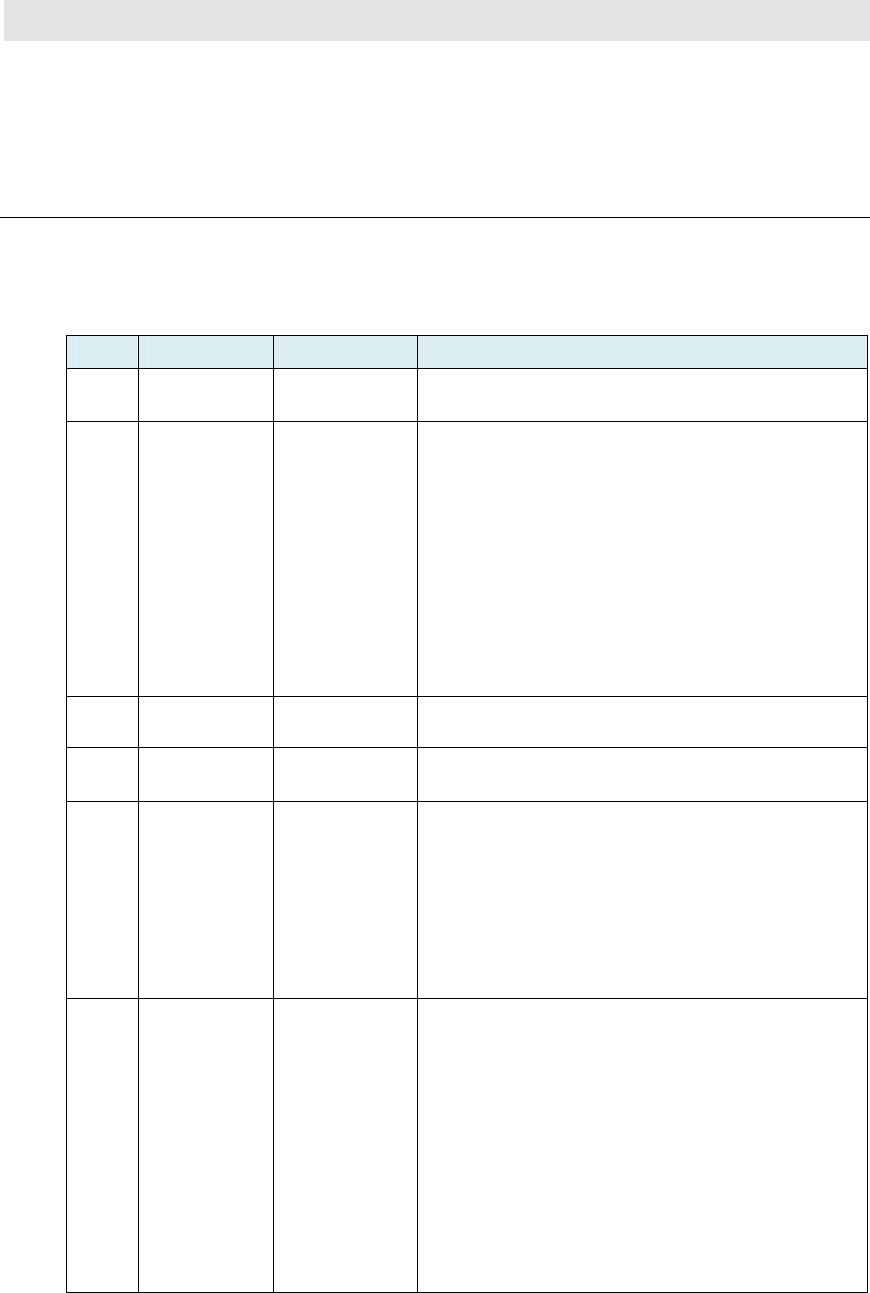

A history of significant changes to this template is described in the table below.

Issue Prepared By Date Changes

1.0 Bill

Ciabattoni

Sept 22,

2009

First Version

1.1 Bill

Ciabattoni

Oct 8, 2009 • Section 3.8:

• Login Request – Increased Requested

Sequence Number message length to 20

from 12.

• Login Accepted - Increased Sequence

Number message length to 20 from 12.

• Section 5.4:

• Reject reason code “P” added.

• Added Super Aggressive and Aggressive

options to Routing Instructions field.

1.2 Bill Ciabattoni Jan 22, 2010 Change made to End of Session message in

Sections 3.5, 3.7, and 3.8.

1.3 Bill Ciabattoni Feb 12, 2010 Section 5.4: Corrected inaccurate offset values in

“Replaced Message”.

1.4 Bill Ciabattoni March 25,

2010

Section 3.8: Removed “A message with zero

length is a special end of session marker” from

Sequenced and Un-Sequenced Data message

descriptions.

Section 5.4: Removed reference to fee schedule

and added actual liquidity flags in the Liquidity

Flag field for the Executed Order message

description.

1.5 Bill Ciabattoni April 16, 2010 Section 3.2: Updated to state “Authentication of the

Login Request message only requires Username.

The password will be ignored at this time.”

Section 4.1: Updated list of functionality

supported and not supported by High

Performance API.

Section 5.4:

Corrected Liquidity Flag field in Execution

Message to Alpha-numeric.

Added IOC to all Directed ISO strategy

descriptions in Enter Order-Extended Format

and Accepted Message- Extended Format.

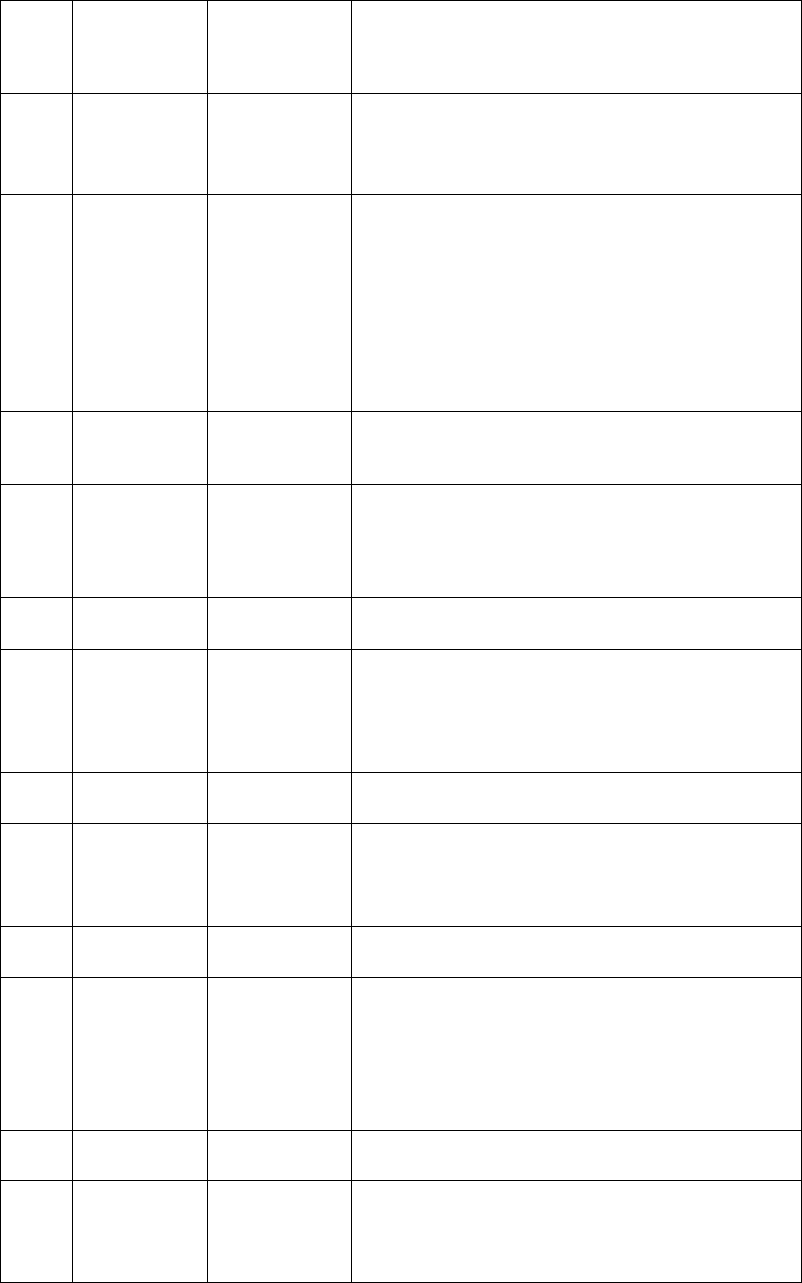

Direct Edge API Specifications for Equities

6

1.6 Bill Ciabattoni April 26, 2010 Section 5.4: Added “For all Directed ISO strategies

Inter-market Sweep Eligibility must equal “Y” and

Time in Force must equal “0” (IOC), or the order will

be rejected” to Route Strategy description in Enter

Order – Extended Format message.

1.7 Bill Ciabattoni July 6, 2010 Section 5.4: Added new “Z” value to “Display” field in

Accepted Message – Short and Extended Formats.

1.8 Bill Ciabattoni Sept 1, 2010 • Auction process named Competition for Price

Improvement

SM

(CPI)

• Dark Ping process named Comprehensive

Liquidity Check

SM

(CLC)

• Section 5.4:

o Updated description on Max Floor field

to indicate the zero may be entered

when not sending a Reserve Order.

o Updated Discretionary Offset to

indicate that sign will be ignored.

1.9 Bill Ciabattoni Oct 1, 2010 • Sell Short Exempt added. Effective upon launch

of new SS Circuit Breakers on November 10,

2010.

• Directed ISO Strategy (ISBY) added for BATS

“Y” Exchange. Effective upon launch of BYX.

1.10 Bill Ciabattoni Jan 3, 2011 Section 5.4:

• Added Anti-Internalization Modifier Message

• Added AI Additional Info Message

Please note that above changes will be live on EDGA

on 1/10/2011 and EDGX on 1/18/2011.

1.11 Bill Ciabattoni Jan 20, 2011 Section 5.4:

• Added SWPA, SWPB, IOCM, and ICMT

strategies to Extended Order Enter Message and

Accepted Extended Order Message.

• Added “SW” Liquidity Flag to Executed Order

Message.

1.12 Bill Ciabattoni Feb 1, 2011 Section 5.4:

• Added “RT” and “RX” Liquidity Flags to Executed

Order Message.

• Updated description of “K” Liquidity Flag in

Executed Order Message.

• Updated description of “Z” Liquidity Flag in

Executed Order Message.

1.13 Bill Ciabattoni Feb 3, 2011 Section 5.4:

• Added ROOC and ROBY strategies to Extended

Order Enter Message and Accepted Extended

Order Message.

• Added 8, 9, BY, CL, and DM Liquidity Flags to

Executed Order Message.

• Added “D” value to Special Order Type field in

for Midpoint Discretionary Order

1.14 Bill Ciabattoni Feb 24, 2011 Section 5.4:

• CPI removed from all routing strategies.

1.15 Bill Ciabattoni Mar 29, 2011 Section 5.4:

Direct Edge API Specifications for Equities 7

• ROUT, ROUD, ROUZ, ROUE, ROOC, and

RDOT strategies updated to include Select CLCs

and/or Low Cost venues as possible

destinations.

1.16 Bill Ciabattoni May 9, 2011 Section 5.4:

• ROBB, ROCO, and SWPC strategies added to

Extended Order Enter Message and Accepted

Extended Order Message.

1.17 Bill Ciabattoni June 28, 2011 • Updated Route Out Eligibility field in Order Enter

and Extended Order Enter message to state that

Post Only orders marked HideNotSlide or Hidden

may be executed as a Taker if price improved on

EDGX; Post Only instructions may not be

included on Hidden orders or Odd Lot orders on

EDGA; Post Only Discretionary orders executed

in their discretionary range will be charged the

Hidden order rate on EDGA. Live date August 1,

2011.

1.18 Bill Ciabattoni July 12, 2011 • Updated Route Out Eligibility field in Order Enter

and Extended Order Enter message descriptions

to reflect changes for 15c3-5 compliance.

1.19 Bill Ciabattoni July 22, 2011 • Updated Route Out Eligibility field in Order Enter

and Extended Order Enter messages to state

that Post Only may not be included on

Discretionary Orders on EDGA. Live date

August 1, 2011.

1.20 Bill Ciabattoni Sept 29, 2011 • Added PI and RR Liquidity Flags in the Executed

Order Message

1.21 Bill Ciabattoni Jan 30, 2012 • Reject Message can now be sent in response to

a Cancel Message.

• Added new value “b” (Post to EDGX for orders

originating on EDGA) to Route Out Eligibility field

in Enter Order Message.

1.22 Bill Ciabattoni Feb 29, 2012 • Added several new Liquidity Flags in the

Executed Order Message

1.23 Bill Ciabattoni Mar 20, 2012 • Added RMPT Routing Strategy to Enter Order

Messages.

• Added Post to Away Destinations to Route Out

Eligibility field in Enter Order Messages.

1.24 Bill Ciabattoni May 1, 2012 • Added BB Liquidity Flag in the Executed Order

Message.

1.25 Bill Ciabattoni June 26, 2012 • Added new value in Special Order Type field for

Midpoint Discretionary Order.

• Added RQ, DM, and DT Liquidity Flags to the

Executed Order Message.

• Added new “Displayed with Attribution” value to

Displayed field. Expected live date is Sept 2012.

1.26 Bill Ciabattoni June 28, 2012 • Added new Reject Reason Codes A, H, and I.

1.27 Bill Ciabattoni Sept 4, 2012 • Added value in Special Order Type field for

Route Peg Order.

• Added “RP” liquidity flag for Route Peg Orders to

Executed Order Message.

Direct Edge API Specifications for Equities

8

• Removed Post to CHX option from Route Out

Eligibility field.

• Removed “RM” liquidity flag from Executed

Order Message.

1.28 Bill Ciabattoni Dec 6, 2012 • Added new Reject Reason Code R.

1.29 Bill Ciabattoni April 15, 2013 • Added optional Extended Reject Message format

1.30 Bill Ciabattoni June 10, 2013 • Added new value in Special Order Type field for

NBBO Offset Peg (Market Maker Peg)

• Updated “Replace Order” description to state

that decrementing quantity will not generate a

new timestamp.

• Updated Liquidity Flag field to include ZA and ZR

flags.

Direct Edge API Specifications for Equities 9

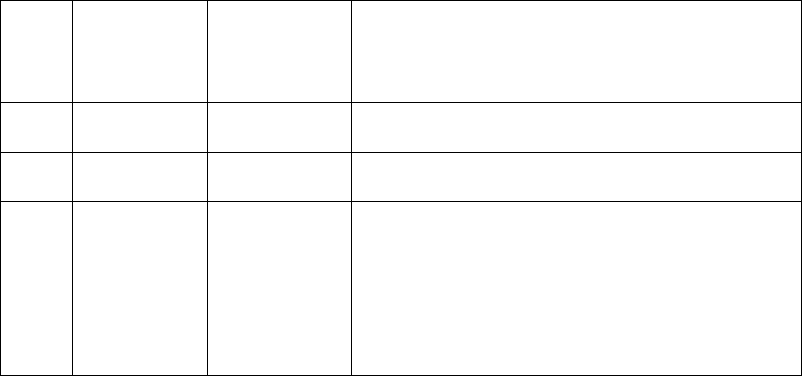

Chapter 2. Overview

2.1 Hours of Operation

EDGX and EDGA Exchanges

Session

Start Time

End Time

Begin Order Acceptance – Pre-Market Orders

(Pre-Market orders will be accepted but will not

begin trading until 8:00 AM.)

6:00 AM 8:00 AM

Begin Order Acceptance – Regular Session Orders

(Regular Session orders will be accepted but will not

begin trading until 9:30 AM.)

6:00 AM 9:30 AM

Pre-Market Session 8:00 AM 9:30 AM

Regular Trading Session 9:30 AM 4:00 PM

Post Market Session 4:00 PM 8:00 PM

MidPoint Match Dark Pool

Session

Start Time

End Time

Begin Order Acceptance

(MidPoint Match orders will be accepted but will not

begin trading until 9:30 AM.)

6:00 AM 9:30 AM

Regular Trading Session 9:30 AM 4:00 PM

2.2. Contact Information

Department Email Address Phone

Market Operations/FIX Support decs@directedge.com 201-942-8220

Sales sales@directedge.com 866-472-5267

Finance and Billing billing@directedge.com 201-942-8247

2.3. Connectivity and Testing

New order routing connections must pass certification testing before they are permitted to

enter the production marketplace. Please call 201-942-8220 for more information.

Direct Edge API Specifications for Equities

10

Chapter 3. Message Exchange Protocol

Direct Edge has developed a lightweight point-to-point protocol, built on top of TCP/IP

sockets. It is identified as the Message Exchange Protocol (MEP). The MEP is used in

systems when a server needs to deliver a logical stream of sequenced messages to a client

application. MEP also supports the sending of unsequenced messages. Sequenced

messages are recoverable after a socket disruption but unsequenced messages are not.

The MEP itself has no true business functionality. It is a session level protocol and transport

built to carry higher-level application messages.

The MEP client and server communicate by exchanging a series of logical packages.

3.1 Packages

Each MEP logical package has:

• Two byte big-endian length that indicates the length of the rest of the packet

(meaning the length of the payload plus the length of the packet type – which is 1)

• Single byte header which indicates the package type.

• Variable length payload.

3.2. Login

The MEP also includes a simple scheme that allows the server to authenticate the client

upon login. Authentication of the Login Request message only requires Username. The

password will be ignored at this time.

3.3. Package Sequence

A MEP connection begins with the client opening a TCP/IP socket to the server and sending

a Login Request Package. If the Login Request is valid, the server responds with a Login

Accepted Package and begins sending Sequenced Data Packages. The connection

continues until the TCP/IP socket is broken.

Each Sequenced Data Package carries a single, higher-level protocol message.

Sequenced Data Packages do not contain an explicit sequence number; instead both client

and server compute the sequence number locally by counting messages as they go. The

sequence number of the first sequenced message in each session is always 1.

Typically, when initially logging into a server, the client will set the Requested Sequence

Number field to 1 and leave the Requested Session field blank in the Login Request

Package. The client will then inspect the Login Accepted Package to determine the currently

active session. Starting at 1, the client begins incrementing its local sequence number each

time a Sequenced Data Package is received. If the TCP/IP connection is ever broken, the

client can then re-log into the server indicating the current session and its next expected

sequence number.

Clients send messages to the server using Unsequenced Data Packages. Messages may

be sent at any time after the Login Accepted Package is received. These messages may be

Direct Edge API Specifications for Equities 11

lost during TCP/IP socket connection failures. The higher level application protocol must

handle this.

3.4. Heartbeats

MEP uses logical heartbeat packages to quickly detect link failures. The server must send a

Server Heartbeat Package anytime more than 1 second has passed since the server last

sent any data. This ensures that the client will receive data on a regular basis. If the client

does not receive anything (neither data nor heartbeats) for an extended period of time, it

can assume that the link is down and attempt to reconnect using a new TCP/IP socket.

Similarly, once logged in, the client must send a Client Heartbeat Package anytime more

than 1 second has passed since the client last sent anything. If the server doesn't receive

anything from the client for an extended period of time, it can close the existing socket and

listen for a new connection. Direct Edge waits for 15 missed heartbeats (15 seconds)

before it drops the connection.

3.5. End of Session

The server indicates that the current session has terminated by sending the End of Session

message. This indicates that there will be no more messages contained in this session.

The client will have to reconnect and re-login with a new Session ID to begin receiving

messages for the next available session.

3.6. Data Types

The data types are:

o Character and Alphanumeric data fields are standard ASCII bytes padded on the

right with spaces.

o Integer fields are binary in big-endian format.

o Non applicable Alpha fields should be filled with spaces to match the proper field

length.

o Non applicable Integer fields should be filled with zeros to match the proper field

length.

3.7. Summary of MEP Messages

The table below shows the origin and sequence of packages.

Message Notes

From Client From Server

Login Request The MEP client must send a Login Request Package immediately

upon establishing a new TCP/IP socket connection to the server.

The server can terminate an incoming TCP/IP socket if it does not

receive a Login Request Package within a reasonable period of time

(typically 30 seconds).

Login

Accepted

The MEP server sends a Login Accepted Package in response to

receiving a valid Login Request from the client.

This package will always be the first non-debug package sent by the

server after a successful Login Request.

Direct Edge API Specifications for Equities

12

Login Reject The MEP server sends this package in response to an invalid Login

Request Package from the client. The server closes the socket

connection after sending the Login Reject Package.

This is the only non-Debug Package sent by the server in the case

of an unsuccessful login attempt.

Unsequenced

Data

This package is a container that carries the higher level application

messages from the client to the server. Up to 100 messages may be

included in a single, unsequenced package. These messages are

not sequenced and may be lost in the event of a socket failure.

The higher-level protocol must be able to handle these lost

messages in the case of a TCP/IP socket connection failure.

Sequenced

Data

This package is a container that carries the higher level application

messages from the server to the client. The sequence number of

each message is implied; the initial sequence number of the first

Sequenced Data Package for a given TCP/IP connection is

specified in the Login Accepted Package and the sequence number

increments by 1 for each Sequenced Data Package transmitted.

Since MEP logical packages are carried via TCP/IP sockets, the

only way logical packages can be lost is in the event of a TCP/IP

socket connection failure. In this case, the client can reconnect to

the server and request the next expected sequence number and

pick up where it left off.

Client Heartbeat The client should send a Client Heartbeat Package anytime more

than 1 second passes where no data has been sent to the server.

The server can then assume that the link is lost if it does not receive

anything for an extended period of time.

Server

Heartbeat

The server should send a Server Heartbeat Package anytime more

than 1 second passes where no data has been sent to the client.

The client can then assume that the link is lost if it does not receive

anything for an extended period of time.

Debug A Debug Package can be sent by either side of the MEP connection

at anytime. Debug Packages should be ignored by both client and

server application software.

Debug See above.

Logout Request The client may send a Logout Request Package to request the

connection be terminated. Upon receiving a Logout Request

Package, the server will immediately terminate the connection and

close the associated TCP/IP socket.

End of

Session

The server indicates that the current session has terminated by

sending an End of Session message. This indicates that there will

be no more messages contained in this session.

3.8. MEP Message Formats

Message

Field

Offset

Length

Value

Notes

Login

Request

Package

Length 0 2 Integer Number of bytes after this

field until the next package

Package

Type 2 1 "L"

Username 3 6 Alphanumeric

Username. Case

insensitive.

Password 9 10 Alphanumeric

Password. Case insensitive.

Requested

Session 19 10 Alphanumeric

Specifies the session or all

blanks for the currently

active session.

Direct Edge API Specifications for Equities 13

Message

Field

Offset

Length

Value

Notes

Requested

Sequence

Number 29 20

Numeric Specifies the next sequence

number in 0 to start

receiving the most recently

generated message. Note

that this field is expressed in

ASCII format. (Left padded

with spaces)

Login

Accepted

Package

Length 0 2 Integer Number of bytes after this

field until the next package

Package

Type 2 1 "A"

Session 3 10 Alphanumeric

The session ID of the

session that is now logged

into.

Sequence

Number

13 20

Numeric The sequence number of

the next Sequenced

Message to be sent. Note

that this field is expressed in

ASCII format. (Left padded

with spaces)

Login

Rejected

Package

Length 0 2 Integer Number of bytes after this

field until the next package

Package

Type 2 1 "J"

Reject

Reason

Code

3 1

Alpha Login Reject Codes Reason

codes:

“A” = Not Authorized.

Invalid username and

password combination.

“S” = Session not available.

The Requested Session in

the Login Request Package

was either invalid or not

available.

Sequenced

Data

Package

Length 0 2 Integer Number of bytes after this

field until the next package

Package

Type 2 1 "S"

Message

3 N

All Defined by a higher-level

protocol. May contain a

combination of ASCII and

binary data.

Unsequenced

Data

Package

Length 0 2 Integer Number of bytes after this

field until the next package

Package

Type 2 1 "U"

Message

3 N

All Defined by a higher-level

protocol. May contain a

combination of ASCII and

binary data.

Server

Heartbeat

Package

Length 0 2 Integer Number of bytes after this

field until the next package

Package

Type 2 1 "H"

Client

Heartbeat

Package

Length 0 2 Integer Number of bytes after this

field until the next package

Package

Type 2 1 "R"

Direct Edge API Specifications for Equities

14

Message

Field

Offset

Length

Value

Notes

Logout

Request

Package

Length 0 2 Integer Number of bytes after this

field until the next package

Package

Type 2 1 "O"

Debug Package

Length 0 2 Integer Number of bytes after this

field until the next package

Package

Type 0 1 "+"

Text 1 N Alphanumeric

Free form human readable

text.

End of

Session

Package

Length 0 2 Integer Number of bytes after this

field until the next package

Package

Type 2 1 “Z”

Direct Edge API Specifications for Equities 15

Chapter 4. Order Types Supported by the API

4.1. Enter Order –Short and Extended Format

The table below describes the order types and instructions that are available on the Enter Order -

Short Format and the Enter Order – Extended Format messages.

Or

der Type/Instruction

Enter Order

–

Short

Format Enter Order - Extended Format

Market Orders No No

Limit Orders Yes Yes

Symbols with Suffixes No Yes

Full Routing Capabilities No Yes

IOC Yes Yes

FOK Yes Yes

Day Yes Yes

Good Till Time (GTT) No Yes

ISO Yes Yes

ISO Post Only Yes Yes

Hidden Orders Yes Yes

MidPoint Match (EDGX only) Yes Yes

Re-Pricing Options:

• Hide Not Slide

• Price Adjust

• Single Re-Price

• Cancel Back

Yes Yes

Midpoint Pegged Orders

(EDGA only) Yes Yes

Midpoint Discretionary Orders Yes Yes

Primary Pegged Orders No Yes

Market Pegged Orders No Yes

Pegged Discretionary Orders No Yes

Absolute Limit on Pegged

Discretionary Orders No No

Minimum Execution Quantity –

All Executions No Yes

Minimum Execution Quantity –

First Execution Only No No

Direct Edge API Specifications for Equities

16

Reserve Orders No Yes

Random Replenish on

Reserve Orders No No

Discretionary Orders No Yes

Direct Edge API Specifications for Equities 17

Chapter 5 Direct Edge Order API

Direct Edge Order API is a simple protocol that allows Direct Edge participants to enter

orders, cancel existing orders, and receive executions.

5.1 API Architecture

The Direct Edge Order API protocol is composed of logical messages passed between the

Direct Edge Order API host and the client application. The Message Exchange Protocol

(MEP) is used for session management and transport. Each message type has a fixed

message length. Messages may contain ASCII and binary data.

All messages sent from the Direct Edge Order API host to the client are sequenced and their

delivery is ensured by the MEP.

Messages sent from the Direct Edge Order API client to the host are inherently non-

guaranteed, even if they are carried by a lower level protocol that guarantees delivery (like

TCP/IP sockets). Therefore, all host-bound messages are designed so that they can be re-

sent for robust recovery from connection and application failures.

Each physical Direct Edge Order API host port is bound to a Direct Edge assigned logical

Direct Edge Order API Account. On a given day, every order entered on Direct Edge Order

API is uniquely identified by the combination of the logical Direct Edge Order API Account

and the participant created Token field.

The Direct Edge Order API is designed to offer high performance under very demanding

conditions. Performance can be increased further by batching multiple messages in a

single, unsequenced MEP package. Up to 100 messages may be placed in a single

unsequenced MEP package.

5.2 Data Types

All integer fields are expressed in unsigned, big-endian binary format.

All signed integer fields are expressed in two’s complement, big-endian binary format.

Alpha fields are left-justified and padded on the right with spaces.

Prices are 4 byte integer fields. Prices contain 5 whole number digits followed by 5 decimal

digits. For example, a price of $21.57 expressed in the API integer format would be

2157000. The maximum price allowable is through the API is $42949.67296.

Timestamp fields (8 bytes) are given in microseconds past midnight Eastern Time.

5.3 Supported Messages

Message

Notes

From

Direct

Edge

From

Member

Direct Edge API Specifications for Equities

18

Enter Order

(Short

Format)

The Enter Order message lets you enter a new order into

Direct Edge.

Each new order must have a Token that is unique to the day

and that logical Direct Edge API account.

If you send a valid order, you should receive an Accepted

Order message.

If you send an Enter Order message with a previously used

Token, the new order will be ignored.

Enter Order

(Extended

Format)

The Enter Order Extended message lets you enter a new

order into Direct Edge for a symbol having a suffix. It also

allows the use of additional order types and instructions that

are not available in the short format message.

Each new order must have a Token that is unique to the day

and that logical Direct Edge API account.

If you send a valid order, you should receive an Accepted

Order message.

If you send an Enter Order message with a previously used

Token, the new order will be ignored.

Suffixes are entered into the Stock Suffix field in the record

that has been added as the last field in this message.

Accepted

Message

(Short

Format)

An Accepted message acknowledges the receipt and

acceptance of a valid Enter Order message. The data fields

from the Enter Order message are echoed back in the

Accepted message.

Note that the accepted values may differ from the entered

values for some fields. You will always receive an Accepted

message for an order before you get any Canceled Order

messages or Executed Order messages for the order.

Accepted

Message

(Extended

Format)

An Extended Accepted message acknowledges the receipt

and acceptance of a valid Enter Order Extended message.

The data fields from the Enter Order Extended message are

echoed back in the Extended Accepted message.

Note that the accepted values may differ from the entered

values for some fields. You will always receive an Extended

Accepted message for an order before you get any Canceled

Order messages or Executed Order messages for the order.

Executed

Order

An Executed Order message informs you that all or part of an

order has been executed.

Direct Edge API Specifications for Equities 19

Rejected

Message

A Rejected message may be sent in response to an Enter

Order, Cancel, or Replace message if it cannot be accepted

at this time. The reason for the rejection is given. No further

actions are permitted on this order.

The Token of a rejected order cannot be re-used.

Cancel Order

The Cancel Order message is used to request that an order

be canceled or reduced. In the Cancel Order message, you

must specify the new "intended order size" for the order. The

"intended order size" is the maximum number of shares that

can be executed in total after any partial executions and the

cancel are applied.

To cancel the entire balance of an order, you would enter a

Cancel Order message with a Shares field of zero.

Note that the only acknowledgement to a Cancel Order

message is the resulting Canceled Order message.

Any superfluous Cancel Order messages will trigger a Reject

Message with reason code = “I” (Order Not Found). This

includes, non-active orders that have already been filled or

canceled.

Canceled

Message

A Canceled message informs you that an order has been

reduced or canceled. This could be acknowledging a Cancel

Order message or it could be the result of an order time out or

automatic cancel.

Note that a Canceled message does not necessarily mean

the entire order is dead. Some portion of the order may still be

alive.

Cancel

Pending

A Cancel Pending message is sent in response to a Cancel

Order request that cannot be immediately processed due to a

route out. The cancel instructions will be applied to any

unexecuted portion of the order when it returns from the away

market destination.

After receiving the Cancel Pending, you may still receive

executions on the order. If the entire quantity is executed,

you will not get a canceled message. If only part of the order

is executed, you will receive a cancel message for the

remaining balance.

Direct Edge API Specifications for Equities

20

Replace

Order

The Replace Order message allows you to alter the quantity

and price of an existing order in a single message. Replacing

an order with a larger quantity or new price will create a new

timestamp for the order. Orders that are decremented to a

smaller quantity will retain their timestamp.

Any superfluous Replace Order messages will trigger a

Reject Message with reason code = “I” (Order Not Found).

This includes, non-active orders that have already been filled

or canceled.

Replaced

Message

A Replaced message informs you that a Cancel Replace

message has been processed.

Replace

Pending

A Replace Pending message is sent in response to a Replace

Order request that cannot be processed due to a route out.

The replace instructions will be applied to any unexecuted

portion of the order when it returns from the away market

destination.

Important Note: When a replace is pending, no other order

modifications can be made until it has been replaced or

executed. All subsequent replace requests will be rejected

until the first request is completed.

System

Event

System Event messages signal events that affect the entire

Direct Edge system.

Broken

Trade

A Broken Trade message informs you that an execution has

been broken. The trade is no longer good and will not clear.

The reason for the break is given.

You will always get an Executed Order message prior to

getting a Broken Trade message for a given order/execution.

Price

Correction

A Price Correction message informs you that an execution

has been price-corrected.

You will always get an Executed Order message prior to

getting a Price Correction message for a given

order/execution.

Anti-

Internalization

Modifier

The Anti-Internalization Modifier can be included in the un-

sequenced data package if the user wants to control AI

instructions at the Order Level. The orders processed in this

envelope will use the supplied Anti-Internalization Modifier

from the envelope. Within the same envelope, members can

include more than one Anti-Internalization Modifier that will

impact all subsequent orders.

Direct Edge API Specifications for Equities 21

AI

Additional

Info

Message

The AI Additional Information Message provides members

with information about the order that was canceled due to

Anti-Internalization instructions. This is an optional message

that members can choose to receive or they can just receive

the Canceled Message, or both messages. If the member

chooses to receive both messages, the AI Additional

Information Message will immediately follow the Canceled

Message, there will be no messages sent in between.

Direct Edge API Specifications for Equities

22

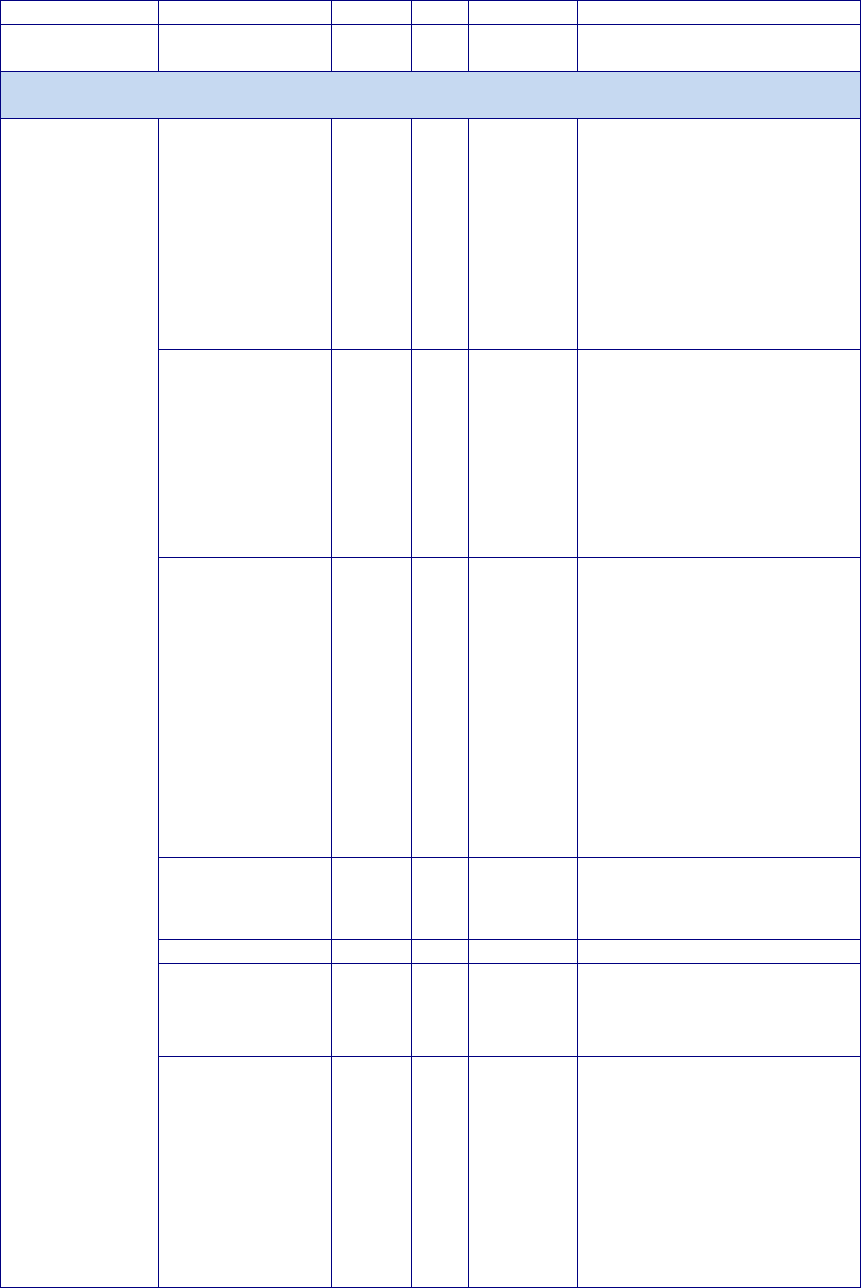

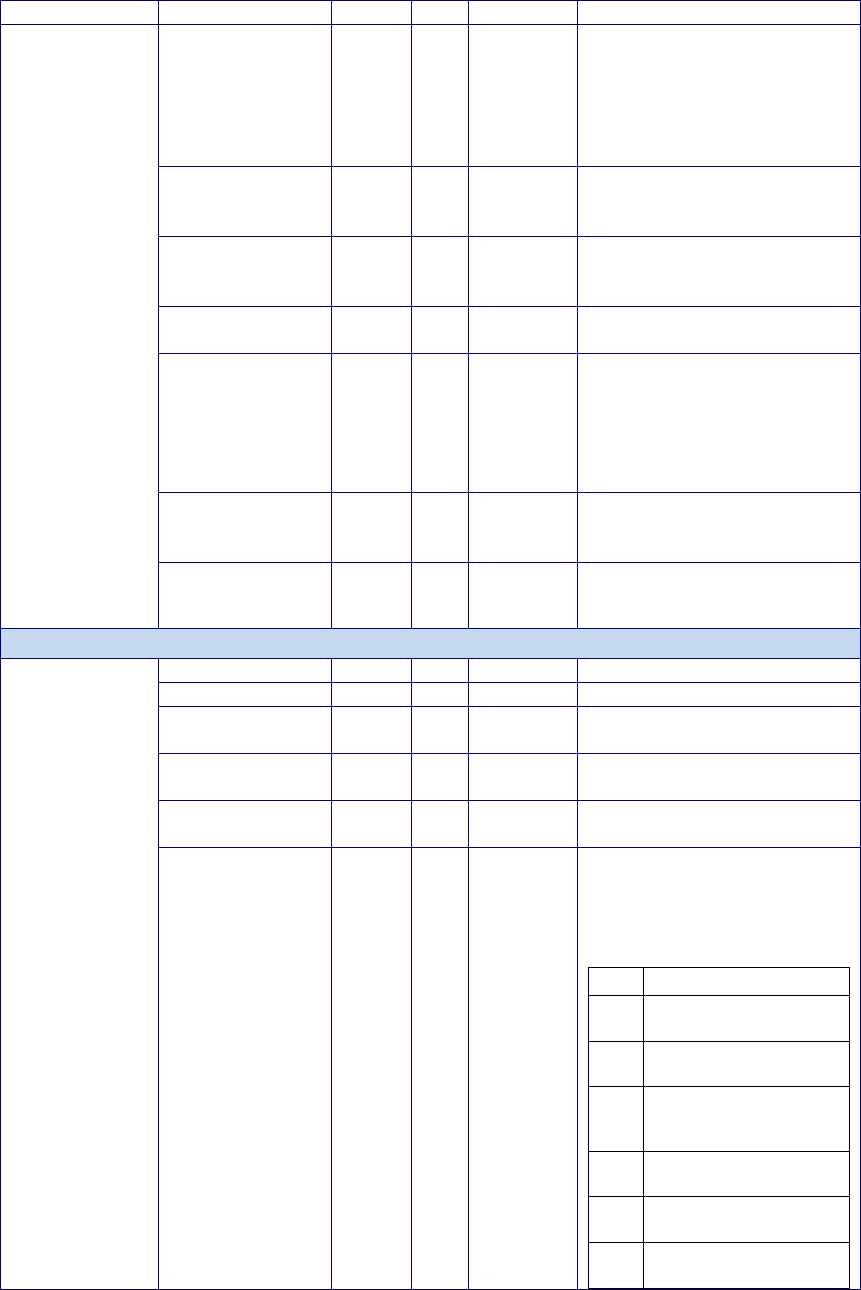

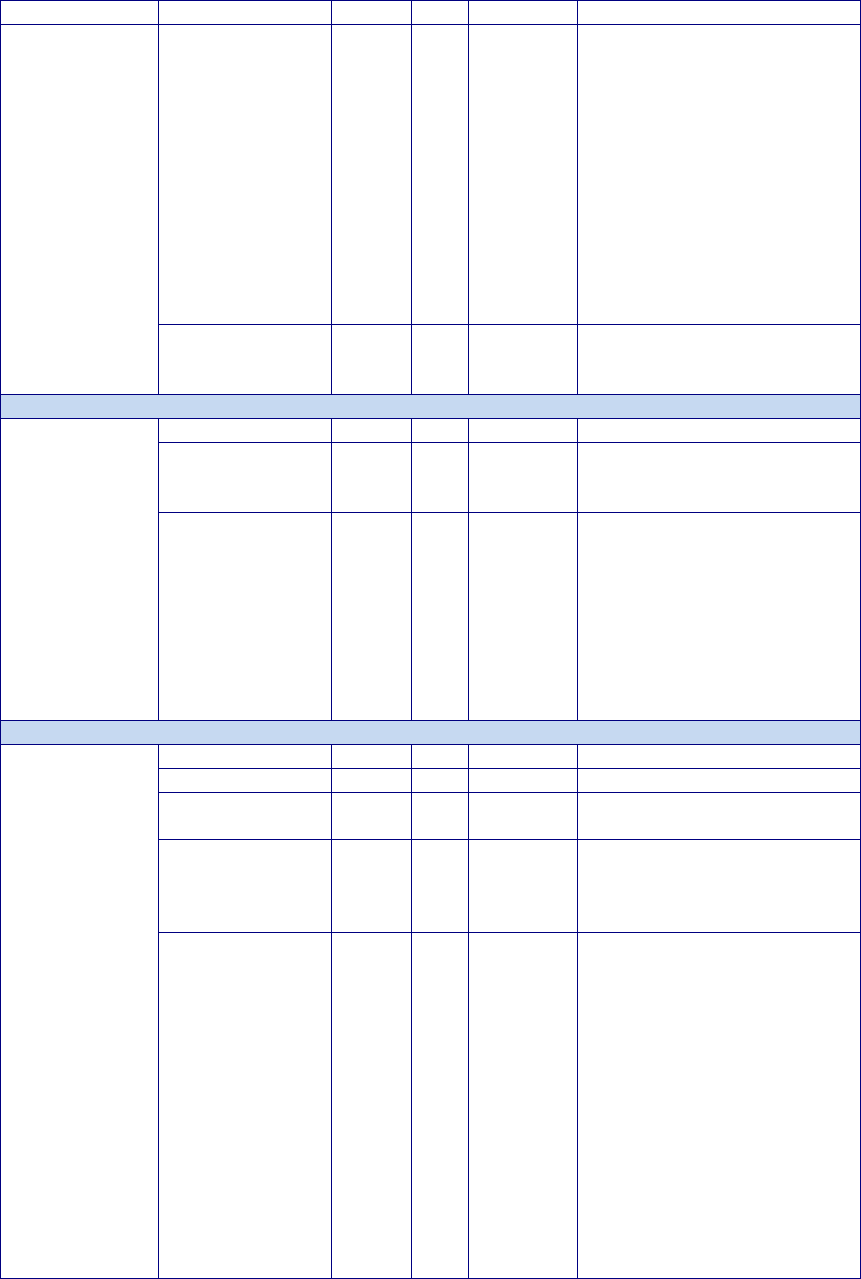

5.4 Message Formats

Message

Name

Offset

Len

Value

Notes

Enter Order –

Short Format

(from Member)

Type 0 1 “O” Identifies this message as an

Enter Order – Short Format

message type. The Short

Format of this message

allows for less order type

features than the Extended

Format message.

Order Token 1 14 Alpha-

numeric

This is a free-form, alpha-

numeric field. You can enter

any information you like.

Token must be day-unique

for each Direct Edge API

account. Token is case

sensitive, but mixing upper-

case and lower-case Tokens

is not recommended.

Buy/Sell

Indicator

15 1 Alpha “B” = Buy order

“S” = Sell order

"T" = Sell Short – Client

affirms ability to borrow

securities.

“E” = Sell Short Exempt –

Client affirms ability to

borrow.

“X” = Sell Short/SS Exempt –

Client does not affirm

ability to borrow

securities. (Results in

rejection of the order.)

Quantity 16 4 Integer Total number of shares

Symbol 20 6 Alpha Stock Symbol

Price 26 4 Integer The limit price of the order.

The price is a 5 digit whole

number followed by a 5

decimal digits.

Time in Force 30 1 Integer The values for Time in Force

are:

0 = Immediate or Cancel

1 = Day

2 = Fill or Kill

Display 31 1 Alpha “Y” = Displayed

“N” = Hidden

“A” = Displayed with

Attribution*

* Expected live date

September 2012

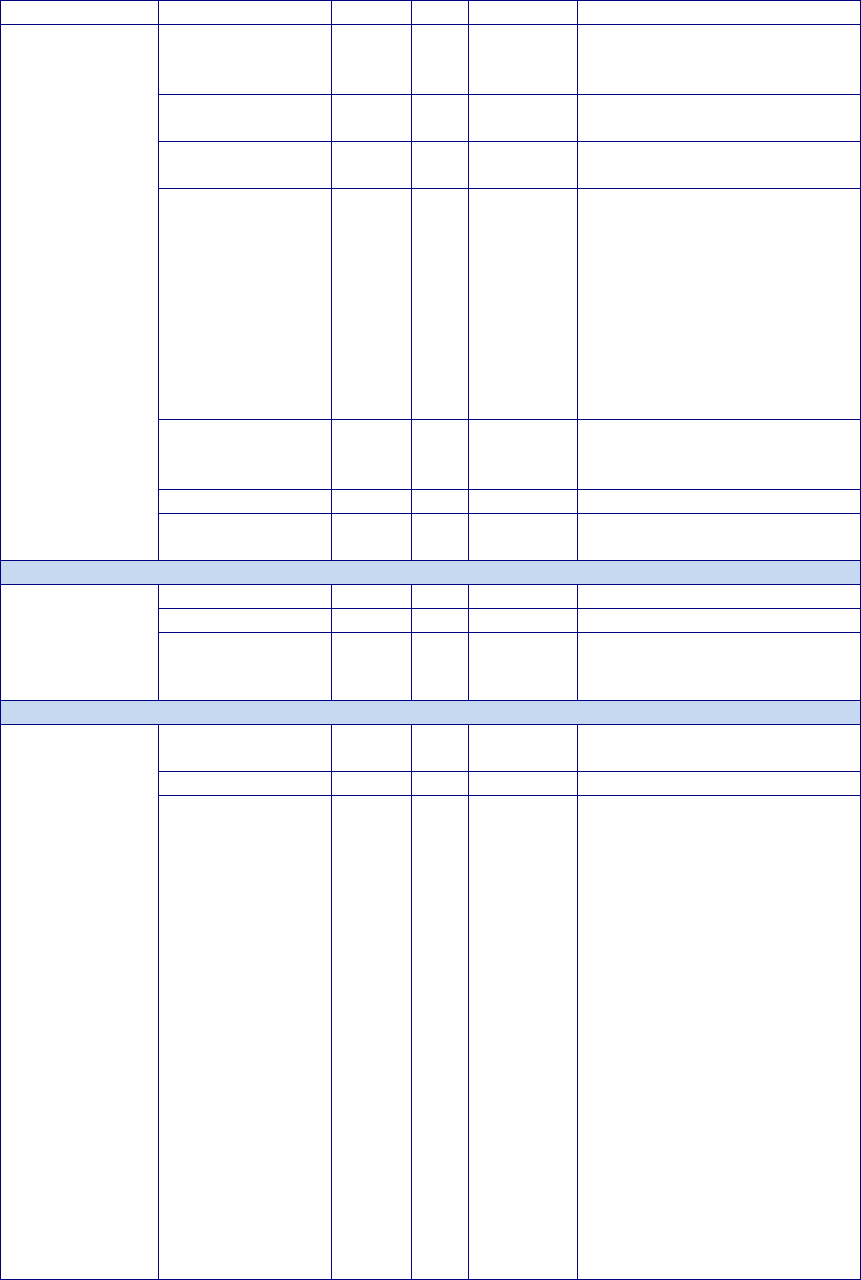

Direct Edge API Specifications for Equities 23

Message

Name

Offset

Len

Value

Notes

Special Order

Type

32 1 Alpha “M”= MidPoint Match EDGX/

MidPoint Peg EDGA

“D” = Midpoint Discretionary

Order – EDGA Only*

“U” = Route Peg Order

“N” = NBBO Offset Peg

(Market Maker Peg)

Re-Pricing Options:

“S” = Hide Not Slide

“P” = Price Adjust

“R” = Single Re-Price

“C” = Cancel Back

(See Appendix B for details

on Re-Pricing options.)

*Midpoint Discretionary

Orders require a “Y” in the

Display field.

Enter a space for this field if

not applicable.

Extended Hrs

Eligible

33 1 Alpha “R” = Regular Session Only

“P” = Pre-Market and

Regular Session

Eligible

“A” = Regular Session and

Post-Market Eligible

“B” = All Sessions Eligible

Capacity 34 1 Alpha “A” = Agency

“P” = Principal

“R” = Riskless Principal

Route out

Eligibility

35 1 Alpha “Y” = Routable (ROUT

strategy only)**

“N” = Book Only***

“P” = Post-Only*&***

“S” = Super Aggressive -

Cross or Lock (Order will be

removed from book and

routed to any quote that is

crossing or locking the order)

“X” = Aggressive - Cross

only (Order will be removed

from book and routed to any

quote that is crossing)

a = Post to EDGA (for orders

originating from EDGX, ROUT,

ROUX, ROUE only)

b = Post to EDGX for orders

originating on EDGA (for ROUT,

Direct Edge API Specifications for Equities

24

Message

Name

Offset

Len

Value

Notes

ROUD, ROUE, ROUX, ROUZ,

ROUQ, RDOT, RDOX, ROPA,

ROBA, ROBX, ROBY, ROBB,

ROCO, ROLF, INET, IOCT,

IOCX, IOCM, ICMT only)

c = Post to NYSE Arca (ROUT,

ROUX, ROUE only)

d = Post to NYSE (ROUT,

ROUX, ROUE only)

e = Post to NASDAQ (ROUT,

ROUX, ROUE only)

f = Post to NASDAQ OMX BX

(ROUT, ROUX, ROUE only)

g = Post to NASDAQ OMX PSX

(ROUT, ROUX, ROUE only)

h = Post to BATS BYX (ROUT,

ROUX, ROUE only)

i = Post to BATS BZX (ROUT,

ROUX, ROUE only)

j = Post to LavaFlow (ROUT,

ROUX, ROUE only)

k = Post to CBSX (ROUT,

ROUX, ROUE only)

l = Post to AMEX (ROUT,

ROUX, ROUE only)

n = Post to NSX (ROUT, ROUX,

ROUE only)

(Use the Enter Order -

Extended Format to enter

routing strategies other than

ROUT)

Enter a space for this field if

not applicable.

*Post Only orders marked

HideNotSlide or Hidden may be

executed as a Taker if price

improved on EDGX.

Post Only instructions may not

be included on Hidden Orders,

Discretionary Orders, or Odd Lot

quantities on EDGA.

**All routing strategies are

subject to erroneous checks

pursuant to 15c3-5

compliance.

***Book Only and Post Only

orders are not subject to

erroneous checks pursuant to

15c3-5 compliance.

Inter-market 36 1 Alpha “Y” = ISO Eligible

Direct Edge API Specifications for Equities 25

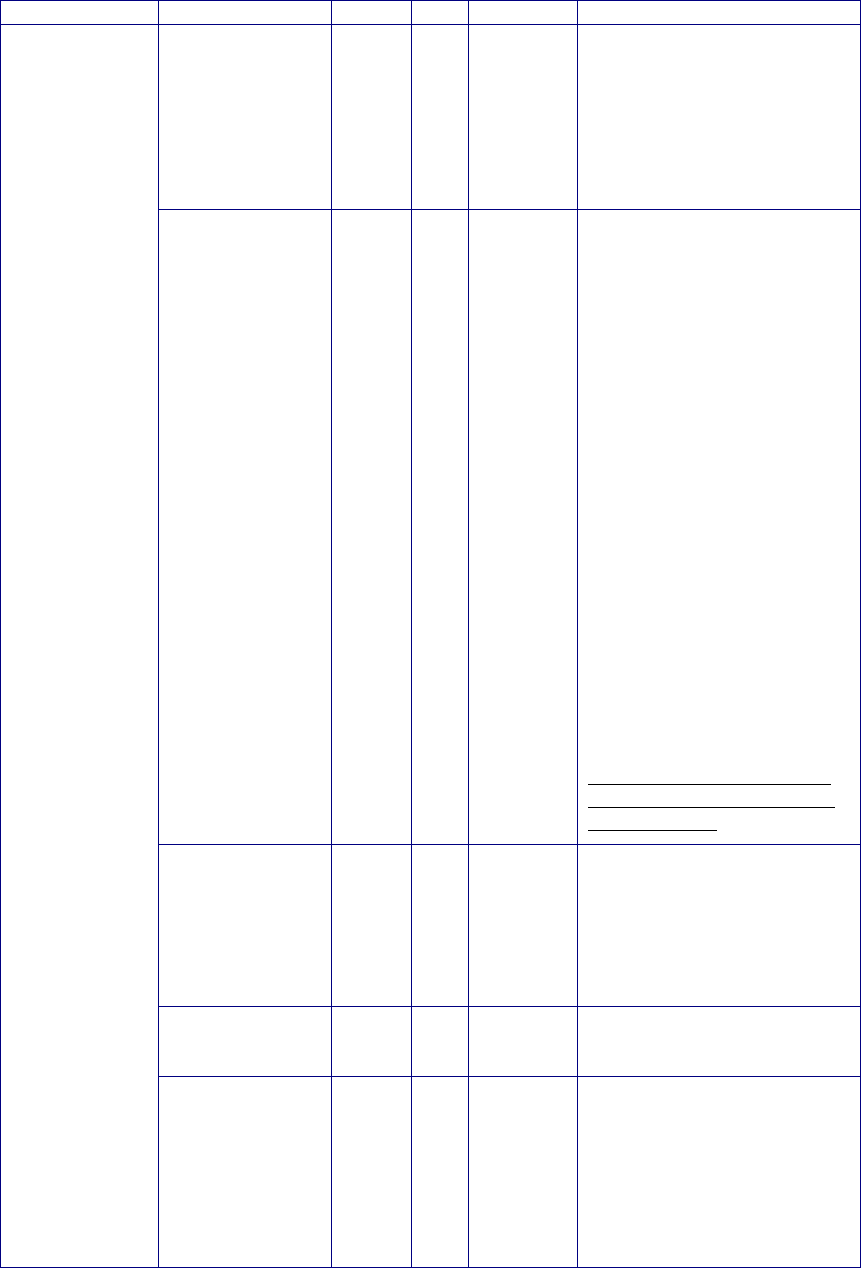

Message

Name

Offset

Len

Value

Notes

Sweep (ISO)

Eligibility

“N” = Not ISO Eligible

Enter Order –

Extended

Format

(from Member)

Type 0 1 “N” Identifies this message as an

Enter Order - Extended

Format message type. This

is an alternative to the Enter

Order - Short Format

message. It is to be used

when additional order type

functionality is needed that is

not supported in the Short

Format message.

Order Token 1 14 Alpha-

numeric

This is a free-form, alpha-

numeric field. You can enter

any information you like.

Token must be day- unique

for each Direct Edge API

account. Token is case

sensitive, but mixing upper-

case and lower-case Tokens

is not recommended.

Buy/Sell

Indicator

15 1 Alpha “B” = Buy order

“S” = Sell order

"T" = Sell Short – Client

affirms ability to borrow

securities.

“E” = Sell Short Exempt –

Client affirms ability to

borrow.

“X” = Sell Short/SS Exempt –

Client does not affirm

ability to borrow

securities. (Results in

rejection of the order.)

Quantity 16 4 Integer Total number of shares

entered

Symbol 20 6 Alpha Stock Symbol

Price 26 4 Integer The limit price of the order.

The price is a 5 digit whole

number followed by a 5

decimal digits.

Time in Force 30 1 Integer The values for Time in Force

are:

0 = Immediate or Cancel

1 = Day

2 = Fill or Kill

3 = Good Till Time

For Good Till Time, Expire

Time must also be

populated.

Direct Edge API Specifications for Equities

26

Message

Name

Offset

Len

Value

Notes

Display 31 1 Alpha “Y” = Displayed

“N” = Hidden

“A” = Displayed with

Attribution*

* Expected live date

September 2012

Special Order

Type

32 1 Alpha “M”= MidPoint Match EDGX/

MidPoint Peg EDGA

“D” = Midpoint Discretionary

Order – EDGA Only*

“U” = Route Peg Order

“N” = NBBO Offset Peg

(Market Maker Peg)

“X” = Primary Peg

“Y” = Market Peg

Re-Pricing Options:

“S” = Hide Not Slide

“P” = Price Adjust

“R” = Single Re-Price

“C” = Cancel Back

(See Appendix B for details

on Re-Pricing options.)

*Midpoint Discretionary

Orders require a “Y” in the

Display field.

Ignored for routable orders.

Enter a space for this field if

not applicable.

Extended Hrs

Eligible

33 1 Alpha “R” = Regular Session Only

“P” = Pre-Market and

Regular Session

Eligible

“A” = Regular Session and

Post-Market Eligible

“B” = All Sessions Eligible

Capacity 34 1 Alpha “A” = Agency

“P” = Principal

“R” = Riskless Principal

Route out

Eligibility

35 1 Alpha “Y” = Routable**

“N” = Book Only***

“P” = Post Only*&***

“S” = Super Aggressive -

Cross or Lock (Order will be

removed from book and

routed to any quote that is

crossing or locking the order)

Direct Edge API Specifications for Equities 27

Message

Name

Offset

Len

Value

Notes

“X” = Aggressive -

Cross only

(Order will be removed from

book and routed to any quote

that is crossing)

a = Post to EDGA (for orders

originating from EDGX, ROUT,

ROUX, ROUE only)

b = Post to EDGX for orders

originating on EDGA (for ROUT,

ROUD, ROUE, ROUX, ROUZ,

ROUQ, RDOT, RDOX, ROPA,

ROBA, ROBX, ROBY, ROBB,

ROCO, ROLF, INET, IOCT,

IOCX, IOCM, ICMT only)

c = Post to NYSE Arca (ROUT,

ROUX, ROUE only)

d = Post to NYSE (ROUT,

ROUX, ROUE only)

e = Post to NASDAQ (ROUT,

ROUX, ROUE only)

f = Post to NASDAQ OMX BX

(ROUT, ROUX, ROUE only)

g = Post to NASDAQ OMX PSX

(ROUT, ROUX, ROUE only)

h = Post to BATS BYX (ROUT,

ROUX, ROUE only)

i = Post to BATS BZX (ROUT,

ROUX, ROUE only)

j = Post to LavaFlow (ROUT,

ROUX, ROUE only)

k = Post to CBSX (ROUT,

ROUX, ROUE only)

l = Post to AMEX (ROUT,

ROUX, ROUE only)

n = Post to NSX (ROUT, ROUX,

ROUE only)

Enter a space for this field if

not applicable.

*Post Only orders marked

HideNotSlide or Hidden may

be executed as a Taker if

price improved on EDGX.

Post Only instructions may not

be included on Hidden Orders,

Discretionary Orders, or Odd Lot

quantities on EDGA.

**All routing strategies are

subject to erroneous checks

pursuant to 15c3-5

compliance.

Direct Edge API Specifications for Equities

28

Message

Name

Offset

Len

Value

Notes

***Book Only and Post Only

orders are not subject to

erroneous checks pursuant

to 15c3-5 compliance.

Inter-market

Sweep (ISO)

Eligibility

36 1 Alpha “Y” = ISO Eligible

“N” = Not ISO Eligible

Routing Delivery

Method

37 1 Alpha “I” = Route to Improve

“F” = Route to Fill

“C” = Route to Comply

Route to Improve: Ability to

receive price improvement

will take priority over speed

of execution.

Route to Fill: Speed of

execution will take priority

over potential price

improvement.

Route to Comply: If quantity

showing at away markets are

not enough to fill order in its

entirety, ISO orders will be

sent to clear better priced

quotations and the balance

of the order will be posted on

the Direct Edge book.

Ignored for non-routable

orders. Enter a space for this

field if not applicable.

Route Strategy 38 2 Integer 1 = ROUT (Book + Low

Cost/CLC + Street (Default if

not specified))

2 = ROUD (Book + Select

CLC)

3 = ROUE (Book + Low

Cost/Select CLC + Street)

4 = ROUX (Book + Street)

5 = ROUZ (Book + Low

Cost/CLC)

6 = ROUQ (Book +Select

Fast CLCs)

7= RDOT (Book + Low

Cost/CLC + DOT)

8 = RDOX (Book + DOT)

9 = ROPA (Book + IOC

ARCA)

Direct Edge API Specifications for Equities 29

Message

Name

Offset

Len

Value

Notes

10 = ROBA (Book + IOC

BATS)

11 = ROBX (Book + IOC

Nasdaq BX)

12 = INET (Book + Nasdaq)

13 = IOCT (EDGA/X Book +

CLC+ Other EDGA/X Book)

14 = IOCX (EDGA/X Book +

Other EDGA/X Book)

15 = ISAM (Directed IOC

ISO routed to AMEX)

16 = ISPA (Directed IOC ISO

routed to ARCA)

17 = ISBA (Directed IOC ISO

routed to BATS)

18 = ISBX (Directed IOC ISO

routed to Nasdaq BX)

19 = ISCB (Directed IOC ISO

routed to CBSX)

20 = ISCX (Directed IOC ISO

routed to CHSX)

21 = ISCN (Directed IOC ISO

routed to NSX)

22 = ISGA (Directed IOC ISO

routed to EDGA)

23 = ISGX (Directed IOC ISO

routed to EDGX)

24 = ISLF (Directed IOC ISO

routed to LavaFlow)

25 = ISNQ (Directed IOC

ISO routed to Nasdaq)

26 = ISNY (Directed IOC ISO

routed to NYSE)

27 = ISPX (Directed IOC ISO

routed to PHLX)

29 = ROUC (Book + CLC +

Nasdaq BX + DOT + Posted

to EDGX)

30 = ROLF (Book +

LavaFlow)

31 = ISBY (Directed IOC ISO

routed to BYX)

32 = SWPA (IOC ISO Sweep

of All Protected Mkts)

33= SWPB (IOC ISO Sweep

of All Protected Mkts)*

34 = IOCM (EDGA Book +

IOC MPM to EDGX)

Direct Edge API Specifications for Equities

30

Message

Name

Offset

Len

Value

Notes

35 = ICMT (EDGA Book +

CLC+ IOC MPM to EDGX)

36= ROOC (Listing Mkt

Open + Book + Low

Cost/CLC + Street + Listing

Mkt Close)**

37 = ROBY (Book + IOC

BYX)

38 = ROBB (EDGA Book +

IOC Nasdaq BX + IOC

BYX)***

39 = ROCO (EDGA Book +

IOC Nasdaq BX + IOC BYX

+ CLC + EDGX MPM)***

40 = SWPC (IOC ISO Sweep

of All Protected Markets and

Post Remainder)

42 = RMPT (Book + EDGX

MPM + CLC Midpoint +

Street Midpoint)****

Please note:

CLC = Comprehensive Liquidity

Check

For all Directed ISO strategies Inter-

market Sweep Eligibility must equal

“Y” and Time in Force must equal

“0” (IOC), or the order will be

rejected.

* SWPB orders will be canceled

immediately if the order quantity is

not enough to clear all protected

quotes at or better than the specified

price on the order.

** Book Only version of ROOC will

not access CLC and Street.

***Available on EDGA Only.

****RMPT is for EDGA only and

must be used in conjunction with

Midpoint Peg Order type.

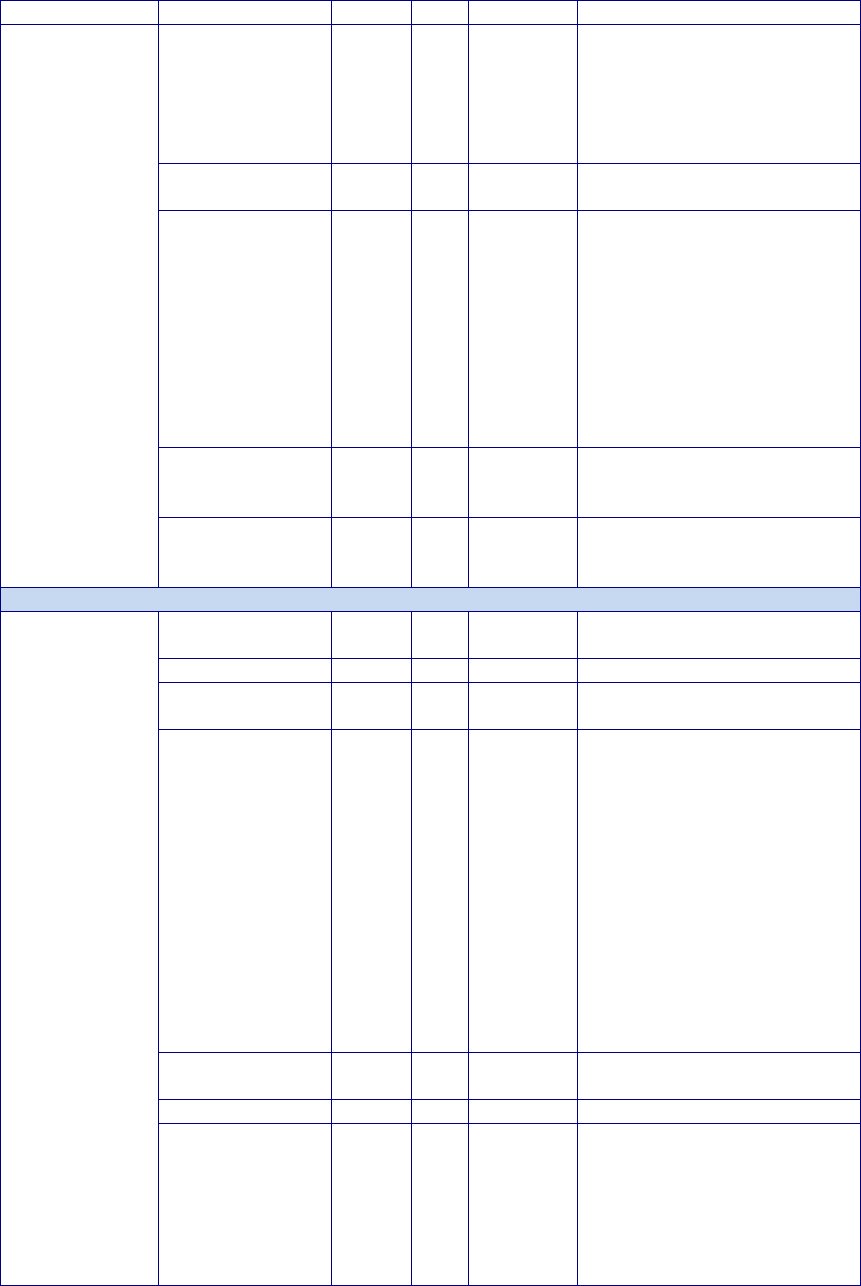

Minimum

Quantity

40 4 Integer Minimum execution quantity

on hidden or IOC order.

(Applies to all executions.)

Max Floor 44 4 Integer Displayed quantity of a

reserve order.

This field is optional. Use 0

(zero) when not sending a

Reserve Order.

Direct Edge API Specifications for Equities 31

Message

Name

Offset

Len

Value

Notes

Please note: MaxFloor=0

does NOT indicate a Hidden

Order in the High

Performance API as it does

in the Direct Edge FIX API.

Peg Difference 48 1 Signed

Integer

Valid Values -99 thru +99

cents

Discretionary

Offset

49 1 Signed

Integer

Valid Values -99 thru 99 cents

Sign may be entered but will

be ignored. Regardless of

sign, offset will always be

added to Buys and

subtracted from Sells in

relation to the limit price of

the order.

Expire Time 50 8 Integer Expire time for GTT orders

represented in Timestamp

format.

Symbol Suffix 58 6 Alpha See Appendix A for

Symbology details.

Accepted

Message -

Short Format

(from Direct

Edge)

Message Type 0 1 “A” Accepted Message – Short

Format identifier.

Timestamp 1 8 Integer Timestamp

Token 9 14 Alpha-

numeric

The order Token field as

entered.

Buy/Sell

Indicator

23 1 Alpha Buy/sell indicator as entered:

“B” = Buy order

“S” = Sell order

"T" = Sell Short – Client

affirms ability to borrow

securities.

“E” = Sell Short Exempt –

Client affirms ability to

borrow.

“X” = Sell Short/SS Exempt –

Client does not affirm

ability to borrow

securities. (Results in

rejection of the order.)

Quantity 24 4 Integer Total number of shares

accepted.

Symbol 28 6 Alpha Stock symbol as entered.

Price 34 4 Integer The accepted limit price of

the order. Note that the

accepted price could

potentially be different than

the entered price if the order

was re-priced by Direct Edge

on entry. The accepted price

Direct Edge API Specifications for Equities

32

Message

Name

Offset

Len

Value

Notes

will always be better than or

equal to the entered.

Time in Force 38 1 Integer The values for Time in Force

are:

0 = Immediate or Cancel

1 = Day

2 = Fill or Kill

Display 39 1 Alpha “Y” = Displayed

“N” = Hidden

“A” = Displayed with

Attribution*

“Z” = Initial Display Price

Differs from Original

Order Price (“Z” value

applies to Hide not Slide

and Price Adjust orders

only.)

* Expected live date

September 2012

Special Order

Type

40 1 Alpha “M”= MidPoint Match EDGX/

MidPoint Peg EDGA

“D” = Midpoint Discretionary

Order – EDGA Only

“U” = Route Peg Order

“N” = NBBO Offset Peg

Re-Pricing Options:

“S” = Hide Not Slide

“P” = Price Adjust

“R” = Single Re-Price

“C” = Cancel Back

(See Appendix B for details

on Re-Pricing options.)

Ignored for routable orders.

Extended Hrs

Eligible

41 1 Alpha “R” = Regular Session Only

“P” = Pre-Market and

Regular Session

Eligible

“A” = Regular Session and

Post-Market Eligible

“B” = All Sessions Eligible

Order Reference

Number

42 8 Integer The day-unique Order

Reference Number assigned

by Direct Edge to this order.

Capacity 50 1 Alpha The capacity specified on the

order:

“A” = Agency

Direct Edge API Specifications for Equities 33

Message

Name

Offset

Len

Value

Notes

“P” = Principal

“R” = Riskless Principal

Route out

Eligibility

51 1 Alpha “Y” = Routable

“N” = Book Only

“P” = Post-Only

“S” = Super Aggressive -

Cross or Lock

“X” = Aggressive - Cross

only

“b”=Post to EDGX for orders

originating on EDGA

Inter-market

Sweep (ISO)

Eligibility

52 1 Alpha “Y” = ISO Eligible

“N” = Not ISO Eligible

Accepted

Message -

Extended

Format

(from Direct

Edge)

Message Type 0 1 “P” Accept Order Message

Extended Format identifier.

Timestamp 1 8 Integer Timestamp

Token 9 14 Alpha-

numeric

The order Token field as

entered.

Buy/Sell

Indicator

23 1 Alpha Buy/sell indicator as entered:

“B” = Buy order

“S” = Sell order

"T" = Sell Short – Client

affirms ability to borrow

securities.

“E” = Sell Short Exempt –

Client affirms ability to

borrow.

“X” = Sell Short/SS Exempt –

Client does not affirm

ability to borrow

securities. (Results in

rejection of the order.)

Quantity 24 4 Integer Total number of shares

accepted.

Symbol 28 6 Alpha Stock symbol as entered.

Price 34 4 Integer The accepted limit price of

the order. Note that the

accepted price could

potentially be different than

the entered price if the order

was re-priced by Direct Edge

on entry. The accepted price

will always be better than or

equal to the entered.

Time in Force 38 1 Integer The values for Time in Force

are:

0 = Immediate or Cancel

1 = Day

2 = Fill or Kill

3 = Good Till Time

Direct Edge API Specifications for Equities

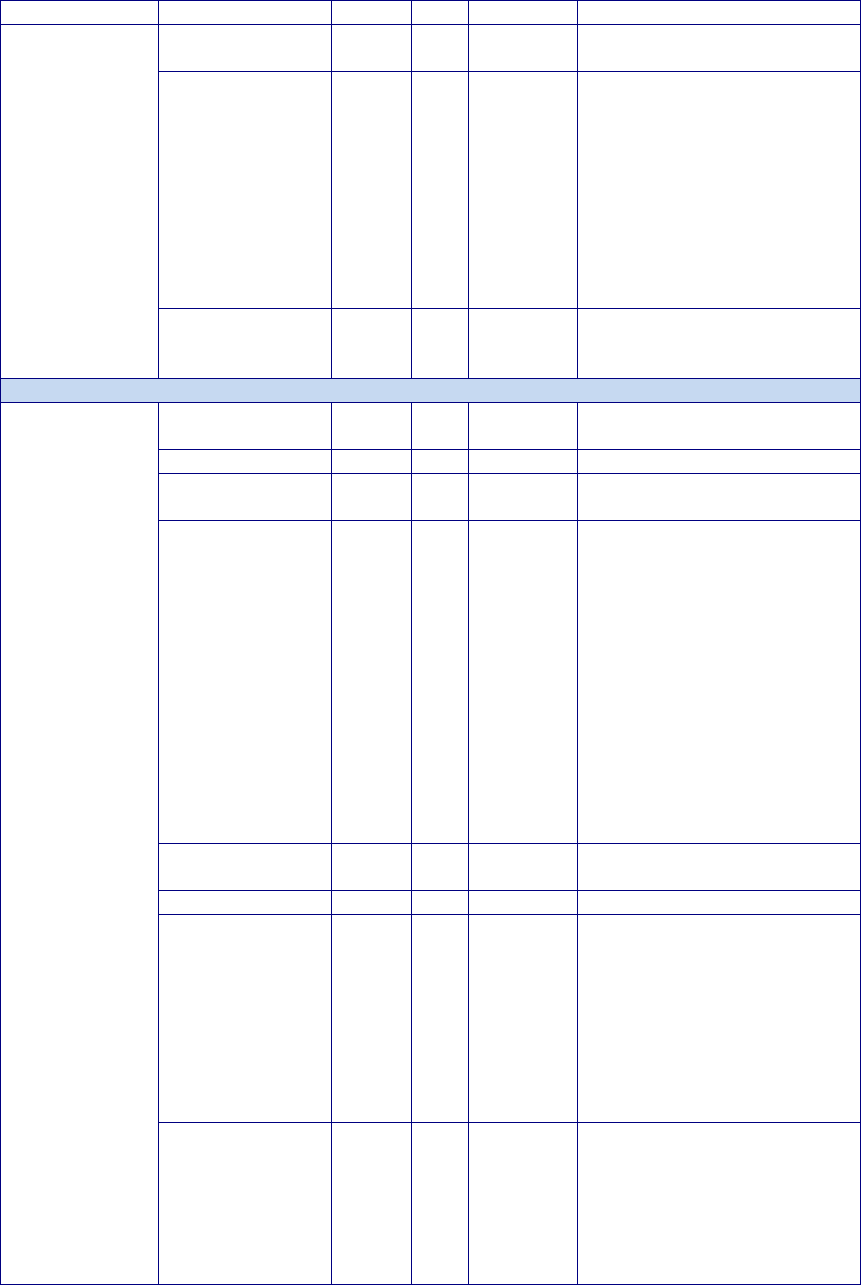

34

Message

Name

Offset

Len

Value

Notes

Display 39 1 Alpha “Y” = Displayed

“N” = Hidden

“A” = Displayed with

Attribution*

“Z” = Initial Display Price

Differs from Original

Order Price (“Z” value

applies to Hide not Slide

and Price Adjust orders

only.)

* Expected live date

September 2012

Special Order

Type

40 1 Alpha “M”= MidPoint Match EDGX/

MidPoint Peg EDGA

“D” = Midpoint Discretionary

Order – EDGA Only

“N” = NBBO Offset Peg

“U” = Route Peg Order

“X” = Primary Peg

“Y” = Market Peg

Re-Pricing Options:

“S” = Hide Not Slide

“P” = Price Adjust

“R” = Single Re-Price

“C” = Cancel Back

(See Appendix B for details

on Re-Pricing options.)

Ignored for routable orders.

Extended Hrs

Eligible

41 1 Alpha “R” = Regular Session Only

“P” = Pre-Market and

Regular Session

Eligible

“A” = Regular Session and

Post-Market Eligible

“B” = All Sessions Eligible

Order Reference

Number

42 8 Integer The day-unique Order

Reference Number assigned

by Direct Edge to this order.

Capacity 50 1 Alpha The capacity specified on the

order:

“A” = Agency

“P” = Principal

“R” = Riskless Principal

Route out

Eligibility

51 1 Alpha “Y” = Eligible

“N” = Book Only

“P” = Post-Only

“S” = Super Aggressive -

Direct Edge API Specifications for Equities 35

Message

Name

Offset

Len

Value

Notes

Cross or Lock

“X” = Aggressive - Cross

only

a = Post to EDGA (for orders

originating from EDGX, ROUT,

ROUX, ROUE only)

b = Post to EDGX for orders

originating on EDGA (for ROUT,

ROUD, ROUE, ROUX, ROUZ,

ROUQ, RDOT, RDOX, ROPA,

ROBA, ROBX, ROBY, ROBB,

ROCO, ROLF, INET, IOCT,

IOCX, IOCM, ICMT only)

c = Post to NYSE Arca (ROUT,

ROUX, ROUE only)

d = Post to NYSE (ROUT,

ROUX, ROUE only)

e = Post to NASDAQ (ROUT,

ROUX, ROUE only)

f = Post to NASDAQ OMX BX

(ROUT, ROUX, ROUE only)

g = Post to NASDAQ OMX PSX

(ROUT, ROUX, ROUE only)

h = Post to BATS BYX (ROUT,

ROUX, ROUE only)

i = Post to BATS BZX (ROUT,

ROUX, ROUE only)

j = Post to LavaFlow (ROUT,

ROUX, ROUE only)

k = Post to CBSX (ROUT,

ROUX, ROUE only)

l = Post to AMEX (ROUT,

ROUX, ROUE only)

n = Post to NSX (ROUT, ROUX,

ROUE only)

Inter-market

Sweep (ISO)

Eligibility

52 1 Alpha “Y” = ISO Eligible

“N” = Not ISO Eligible

Routing Delivery

Method

53 1 Alpha “I” = Route to Improve

“F” = Route to Fill

“C” = Route to Comply

Route Strategy 54 2 Integer 1 = ROUT (Book + Low

Cost/CLC + Street (Default if

not specified))

2 = ROUD (Book + Select

CLC)

3 = ROUE (Book + Low

Cost/Select CLC + Street)

Direct Edge API Specifications for Equities

36

Message

Name

Offset

Len

Value

Notes

4 = ROUX (Book + Street)

5 = ROUZ (Book + Low

Cost/CLC)

6 = ROUQ (Book +Select

Fast CLCs)

7= RDOT (Book + Low

Cost/CLC + DOT)

8 = RDOX (Book + DOT)

9 = ROPA (Book + IOC

ARCA)

10 = ROBA (Book + IOC

BATS)

11 = ROBX (Book + IOC

Nasdaq BX)

12 = INET (Book + Nasdaq)

13 = IOCT (EDGA/X Book +

CLC+ Other EDGA/X Book)

14 = IOCX (EDGA/X Book +

Other EDGA/X Book)

15 = ISAM (Directed IOC

ISO routed to AMEX)

16 = ISPA (Directed IOC ISO

routed to ARCA)

17 = ISBA (Directed IOC ISO

routed to BATS)

18 = ISBX (Directed IOC ISO

routed to Nasdaq BX)

19 = ISCB (Directed IOC ISO

routed to CBSX)

20 = ISCX (Directed IOC ISO

routed to CHSX)

21 = ISCN (Directed IOC ISO

routed to NSX)

22 = ISGA (Directed IOC ISO

routed to EDGA)

23 = ISGX (Directed IOC ISO

routed to EDGX)

24 = ISLF (Directed IOC ISO

routed to LavaFlow)

25 = ISNQ (Directed IOC

ISO routed to Nasdaq)

26 = ISNY (Directed IOC ISO

routed to NYSE)

27 = ISPX (Directed IOC ISO

routed to PHLX)

28 = ISTR (Directed IOC ISO

routed to TRAC)

29 = ROUC (Book + CLC +

Direct Edge API Specifications for Equities 37

Message

Name

Offset

Len

Value

Notes

Nasdaq BX + DOT + Posted

to EDGX)

30 = ROLF (Book +

LavaFlow)

31 = ISBY (Directed IOC ISO

routed to BYX)

32 = SWPA (IOC ISO Sweep

of All Protected Mkts)

33= SWPB (IOC ISO Sweep

of All Protected Mkts)*

34 = IOCM (EDGA Book +

IOC MPM to EDGX)

35 = ICMT (EDGA Book +

CLC+ IOC MPM to EDGX)

36= ROOC (Listing Mkt

Open + Book + Low

Cost/CLC + Street + Listing

Mkt Close)**

37 = ROBY (Book + IOC

BYX)

38 = ROBB (EDGA Book +

IOC Nasdaq BX + IOC

BYX)***

39 = ROCO (EDGA Book +

IOC Nasdaq BX + IOC BYX

+ CLC + EDGX MPM)***

40 = SWPC (IOC ISO Sweep

of All Protected Markets and

Post Remainder)

42 = RMPT (Book + EDGX

MPM + CLC Midpoint +

Street Midpoint)****

Please note:

CLC = Comprehensive Liquidity

Check

For all Directed ISO strategies Inter-

market Sweep Eligibility must equal

“Y” and Time in Force must equal

“0” (IOC), or the order will be

rejected.

* SWPB orders will be canceled

immediately if the order quantity is

not enough to clear all protected

quotes at or better than the specified

price on the order.

** Book Only version of ROOC will

not access CLC and Street.

***Available on EDGA Only.

****RMPT is for EDGA only and

Direct Edge API Specifications for Equities

38

Message

Name

Offset

Len

Value

Notes

must be used in conjunction with

Midpoint Peg Order type.

Minimum

Quantity

56 4 Integer Minimum execution quantity

on hidden or IOC order.

(Applies to all executions.)

Max Floor 60 4 Integer Displayed quantity of a

reserve order.

Peg Difference 64 1 Signed

Integer

Valid Values -99 thru +99

cents

Discretionary

Offset

65 1 Signed

Integer

Valid Values -99 thru +99

cents

Offset will always be in

relation to the limit price of

the order.

Expire Time 66 8 Integer Expire time for GTT orders

represented in Timestamp

format.

Symbol Suffix 74 6 Alpha See Appendix A for Direct

Edge Symbology details.

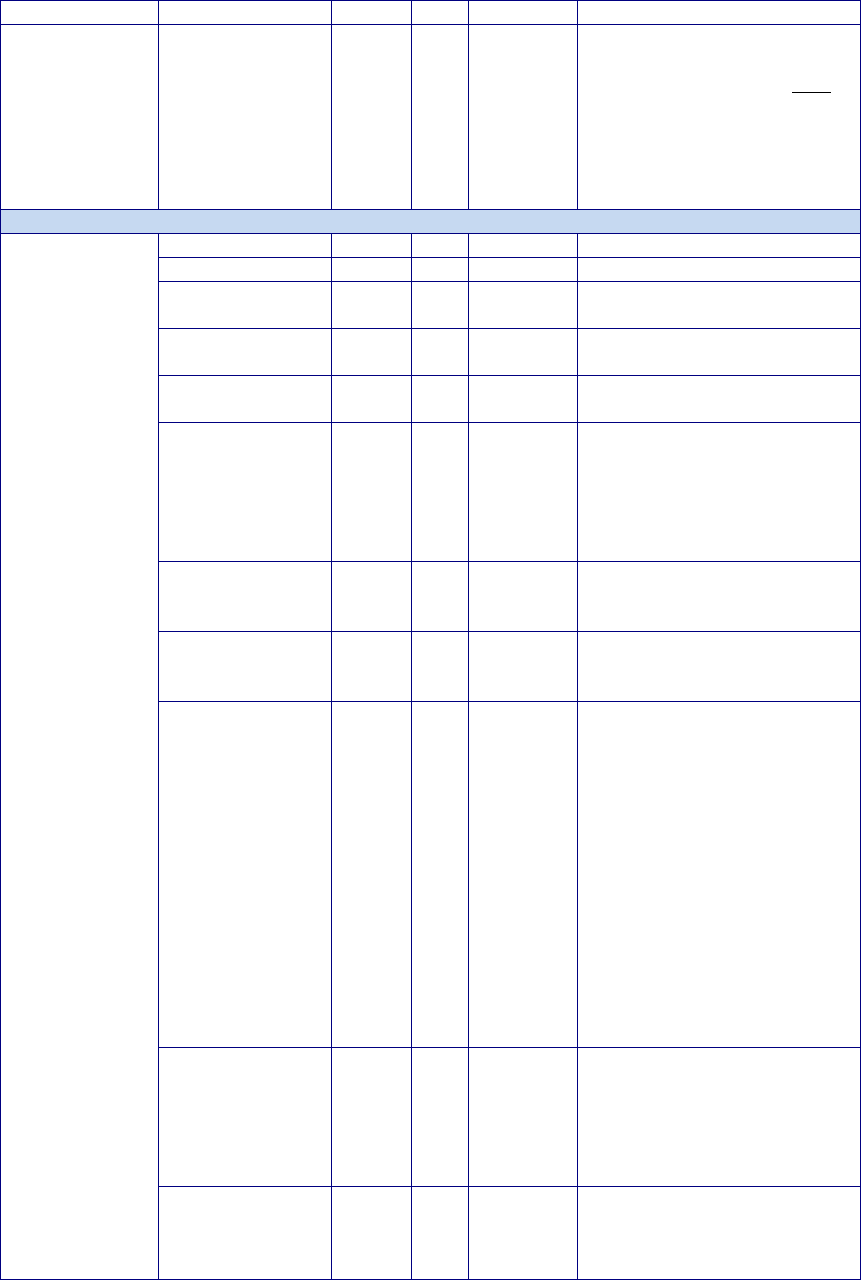

Executed

Order

(from Direct

Edge)

Message Type 0 1 “E” Order Executed message.

Timestamp 1 8 Integer Timestamp

Order Token 9 14 Alpha-

numeric

The Order Token as entered.

Executed

Quantity

23 4 Integer Incremental number of

shares executed.

Execution Price 27 4 Integer The price at which these

shares were executed.

Liquidity Flag 31 5 Alpha-

numeric

Liquidity Flag from Execution

Liquidity flags can be from one

to five characters in length. This

field will be left justified and

padded with spaces.

Flag Description

A Routed to Nasdaq, Adds

Liquidity

B Add liquidity to our Book

(Tape B)

C Routed to Nasdaq BX

(Tapes A & C), Removes

Liquidity

D Routed or Re-routed to

NYSE, Removes Liquidity

EA Customer Internalization

– Added Liquidity

ER Customer Internalization

– Removed Liquidity

Direct Edge API Specifications for Equities 39

Message

Name

Offset

Len

Value

Notes

F Routed to NYSE, Adds

Liquidity

G Routed to ARCA (Tapes

A & C), Removes

Liquidity

HA Hidden Order Adds

Liquidity

HR Hidden Order Removes

Liquidity (EDGA only)

I Routed to EDGA (for

EDGX orders) or to

EDGX (for EDGA orders)

J Routed to Nasdaq,

Removes Liquidity

K Routed to BATS using

ROBA Order Type

(EDGA + BATS) or

Routed to Nasdaq PSX

using ROUC Order Type

L Routed to Nasdaq using

INET Order Type,

Removes Liquidity

(Tapes A & C)

M Add Liquidity on

LavaFlow

N Remove Liquidity from

our Book (Tape C)

O Listing Market Opening

Cross

P Add Liquidity on EDGX

via an EDGA originated

ROUC Order Type

Q Routed using ROUQ or

ROUC Order Types

R Re-routed by Exchange

S Directed ISO Order

T Routed using

ROUD/ROUE Order Type

U Remove Liquidity from

LavaFlow

V Add Liquidity to our Book

(Tape A)

W Remove Liquidity from

our Book (Tape A)

X Routed

Y Add Liquidity to our Book

(Tape C)

Z Routed using ROUZ

Order Type or Executed

in CLC process using

ICMT Order Type

2 Routed to Nasdaq using

INET Order Type,

Removes Liquidity (Tape

B)

3 Add Liquidity – Pre &

Post Market (Tapes A &

Direct Edge API Specifications for Equities

40

Message

Name

Offset

Len

Value

Notes

C)

4 Add Liquidity – Pre &

Post Market (Tape B)

5 Customer Internalization

– Pre & Post Market

6 Remove Liquidity – Pre &

Post Market (All Tapes)

7 Routed – Pre & Post

Market

8 Routed to AMEX, Adds

Liquidity

9 Routed to ARCA, Adds

Liquidity (Tapes A & C)

10 Routed to ARCA , Adds

Liquidity (Tape B)

AA Midpoint Match Cross

(same MPID)

BB Remove Liquidity from

our Book (Tape B)

BY Routed to BYX using

ROBY or ROUC Order

Type

CL Listing Market Close,

excluding NYSE ARCA

CR Liquidity Remover via

CLC Eligible Routing

Strategy (EDGA only)

DM Non-Displayed Orders –

Adds Liquidity using MDO

DT Non-Displayed Orders –

Removes Liquidity using

MDO

MM Midpoint Match Maker

MT Midpoint Match Taker

OO Direct Edge Opening

PA Midpoint Routing Strategy

(RMPT), Adds Liquidity

PI Removed Liquidity from

Midpoint Match on EDGX

PR Liquidity Remover via

CLC Only Routing

Strategy (EDGA only)

PT Midpoint Routing Strategy

(RMPT), Removes

Liquidity

PX Midpoint Routing Strategy

(RMPT), Routed Out

RB Routed to Nasdaq BX,

Adds Liquidity

RC Routed to NSX, Adds

Liquidity

RP Added Liquidity using

Route PegOrder

RQ Routed using ROUQ

RR Routed to EDGA (for

Direct Edge API Specifications for Equities 41

Message

Name

Offset

Len

Value

Notes

EDGX orders) or to

EDGX (for EDGA orders)

using IOCT or IOCX

RS Routed to Nasdaq PSX,

Adds Liquidity

RT Routed using ROUT

Order Type (EDGA Only)

RW Routed to CBSX, Adds

Liquidity

RX Routed using ROUX

Order Type (EDGA Only)

RY Routed to BATS BYX,

Adds Liquidity

RZ Routed to BATS BZX,

Adds Liquidity

SW Routed using

SWPA/SWPB (All mkts

except NYSE)

XR Liquidity Remover via

Non -CLC Eligible

Routing Strategy (EDGA

only)

ZA Retail Order, Adds

Liquidity

ZR Retail Order, Removes

Liquidity

Match Number 36 8 Integer Assigned by Direct Edge to

each match executed. Each

match consists of one buy

and one sell. The matching

buy and sell executions do

not share the same match

number.

Rejected

Message

(from Direct

Edge)

Message Type 0 1 “J” Rejected Order, Cancel or

Replace message.

Timestamp 1 8 Integer Timestamp

Order Token 9 14 Alpha-

numeric

This is the order Token field

as transmitted with the order

when entered.

Reason 23 1 Alpha This is the reason the

message was rejected.

Clients should anticipate

additions to this list and thus

support all capital letters of

the English alphabet.

“A” = Order characteristics

not supported in current

trading session

"B" = Number of orders in the

bulk order message

exceeded threshold

“C” = Exchange closed

“D” = Invalid Display Type

Direct Edge API Specifications for Equities

42

Message

Name

Offset

Len

Value

Notes

"E" = Exchange option

“F” = Halted

“H” = Cannot execute in

current trading state

“I” = Order Not Found

“L” = Firm not authorized for

clearing (invalid firm)

"O" = Other

“P” = Order already in a

pending cancel or

replace state

"Q" = Invalid quantity

“R” = Risk Control Reject

“S” = Invalid stock

“T” = Test Mode

"U" = Order has an invalid or

unsupported

characteristic

“V” = Order is rejected

because maximum

order rate is exceeded.

“X” = Invalid price

Extended

Rejected

Message*

(from Direct

Edge)

*Optional - Please

contact DE FIX

Support to activate

Extended Rejected

Msg in place of

standard Rejected

Msg

Message Type 0 1 “L” Rejected Order, Cancel or

Replace message.

Timestamp 1 8 Integer Timestamp

Order Token 9 14 Alpha-

numeric

This is the order Token field

as transmitted with the order

when entered.

Reason 23 1 Alpha This is the reason the

message was rejected.

Clients should anticipate

additions to this list and thus

support all capital letters of

the English alphabet.

“A” = Order characteristics

not supported in current

trading session

"B" = Number of orders in the

bulk order message

exceeded threshold

“C” = Exchange closed

“D” = Invalid Display Type

"E" = Exchange option

“F” = Halted

“H” = Cannot execute in

current trading state

“I” = Order Not Found

“L” = Firm not authorized for

clearing (invalid firm)

"O" = Other

“P” = Order already in a

pending cancel or

Direct Edge API Specifications for Equities 43

Message

Name

Offset

Len

Value

Notes

replace state

"Q" = Invalid quantity

“R” = Risk Control Reject

“S” = Invalid stock

“T” = Test Mode

"U" = Order has an invalid or

unsupported

characteristic

“V” = Order is rejected

because maximum

order rate is exceeded.

“X” = Invalid price

InResponseTo 24 1 Alpha “O” = New Order

“X” = Cancel

“U” = Replace

Cancel Order

(from Member)

Type 0 1 “X” Cancel Order message.

Order Token 1 14 Alpha-

numeric

The Order Token as

originally transmitted in an

Enter Order message.

Quantity 15 4 Integer This is the new intended

order size. This limits the

maximum number of shares

that can potentially be

executed in total after the

cancel is applied. Entering a

zero here will cancel any

remaining open shares on

this order.

Canceled

Message

(from Direct

Edge)

Message Type 0 1 “C” Canceled Order message.

Timestamp 1 8 Integer Timestamp

Order Token 9 14 Alpha-

numeric

The order Token field as

entered.

Decremented

Quantity

23 4 Integer The number of shares just

decremented from the order.

This number is incremental,

not cumulative.

Reason 27 1 Alpha The reason the order was

reduced or canceled. Clients

should anticipate additions to

this list and thus support all

capital letters of the English

alphabet.

“U”= User requested cancel.

Sent in response to a

Cancel Request

message.

“I” = Immediate or Cancel

order. This order was

originally sent with a

timeout of zero and no

further matches were

Direct Edge API Specifications for Equities

44

Message

Name

Offset

Len

Value

Notes

available on the book so

the remaining

unexecuted shares were

immediately canceled.

“T”=Timeout. The Time In

Force for this order has

expired.

“S”=This order was manually

canceled or reduced by

Direct Edge. This is

usually in response to a

participant request via

telephone.

“D”=This order cannot be

executed because of a

regulatory restriction

(e.g. short sale or trade

through restrictions).

“A” =This order cannot be

posted because it will

result in a locked or

crossed market.

“B” = Order was canceled

due to Anti-

Internalization settings.

Cancel

Pending

(from Direct

Edge)

Message Type 0 1 “I” Cancel Pending message

Timestamp 1 8 Integer See Data Types above.

Order Token 9 14 Alpha-

numeric

Order Token for the order

that is cancel pending.

Replace Order

(from Member)

Message Type 0 1 “U” Replace Order message

Existing Order

Token

1 14 Alpha-

numeric

This must be filled out with

the exact Order Token sent

on the Enter Order Message

or last Replace Order

Message.

Replacement

Order Token

15 14 Alpha-

numeric

Client ID for the order.

Token should be day-unique

for each API account.

Quantity 29 4 Integer Total quantity of order

including any previously

executed shares.

Price 33 4 Integer Price of replacement order.

The price is a 5 digit whole

number followed by a 5

decimal digits.

Replaced

Message

(from Direct

Message Type 0 1 “R” Replaced Message Identifier

Timestamp 1 8 Integer Timestamp

Replacement

Order Token

9 14 Alpha-

numeric

The Replacement Order

Token field as entered.

Direct Edge API Specifications for Equities 45

Message

Name

Offset

Len

Value

Notes

Edge) Buy/Sell

Indicator

23 1 Alpha Buy/Sell indicator as entered

on the original order in the

chain.

Quantity 24 4 Integer Total number of shares

outstanding.

Symbol 28 6 Alpha Stock symbol as entered on

the original.

Price 34 4 Integer The accepted price of the

replacement order. Please

note that the accepted price

could potentially be different

than the entered price if the

order was re-priced by Direct

Edge on entry. The

accepted price will always be

better than or equal to the

entered price.

Order Reference

Number

38 8 Integer The day-unique Order

Reference Number assigned

by Direct Edge.

Capacity 46 1 Alpha Capacity of original order.

Previous Order

Token

47 14 Alpha-

numeric

The Order Token of the order

that was replaced.

Pending

Replace

(from Direct

Edge)

Message Type 0 1 “D” Pending Replace message

Timestamp 1 8 Integer Timestamp

Order Token 9 14 Alpha-

numeric

Order Token for the order

that is Pending Replace.

System Event

(from Direct

Edge)

Message Type 0 1 “S” System Event message

identifier.

Timestamp 1 8 Integer Timestamp

Event Code 9 1 Alpha Event Codes

“S” = Start of Day. This is

always the first

message each day. It

indicates that Direct

Edge is open and

ready to start accepting

orders.

“E” = End of Day. This

indicates that Direct

Edge is now closed

and will not accept any

new orders in this

session. There will not

be any more

executions during this

session; however it is

still possible to receive

Broken Trade

messages and

Canceled Order

Direct Edge API Specifications for Equities

46

Message

Name

Offset

Len

Value

Notes

messages.

Broken Trade

(from Direct

Edge)

Message Type 0 1 “B” Broken Trade message.

Timestamp 1 8 Integer Timestamp.

Order Token 9 14 Alpha-

numeric

The order Token field as

entered.

Match Number 23 8 Integer Match Number as

transmitted in a preceding

Executed Order message.

Reason 31 1 Alpha The reason the trade was

broken. Clients should

anticipate additions to this list

and thus support all capital

letters of the English

alphabet.

“S”=The trade was manually

broken by Direct Edge.

Price

Correction

(from Direct

Edge)

Message Type 0 1 “K” Price Correction message.

Timestamp 1 8 Integer Timestamp.

Order Token 9 14 Alpha-

numeric

The order Token field as

entered.