Wiley And SAS Business Series : Fraud Analytics Using Descriptive, Predictive, Social Network Techniques A Guide To Data S (Wiley Series) Bart Baesens, Veronique Van Vlasselaer, Wouter Verbeke Analyti

User Manual: Pdf

Open the PDF directly: View PDF ![]() .

.

Page Count: 402 [warning: Documents this large are best viewed by clicking the View PDF Link!]

- Cover

- Title Page

- Copyright

- Contents

- List of Figures

- Foreword

- Preface

- Acknowledgments

- Chapter 1 Fraud: Detection, Prevention, and Analytics!

- Chapter 2 Data Collection, Sampling, and Preprocessing

- Introduction

- Types of Data Sources

- Merging Data Sources

- Sampling

- Types of Data Elements

- Visual Data Exploration and Exploratory Statistical Analysis

- Benford's Law

- Descriptive Statistics

- Missing Values

- Outlier Detection and Treatment

- Red Flags

- Standardizing Data

- Categorization

- Weights of Evidence Coding

- Variable Selection

- Principal Components Analysis

- RIDITs

- PRIDIT Analysis

- Segmentation

- References

- Chapter 3 Descriptive Analytics for Fraud Detection

- Chapter 4 Predictive Analytics for Fraud Detection

- Introduction

- Target Definition

- Linear Regression

- Logistic Regression

- Variable Selection for Linear and Logistic Regression

- Decision Trees

- Neural Networks

- Support Vector Machines

- Ensemble Methods

- Multiclass Classification Techniques

- Evaluating Predictive Models

- Other Performance Measures for Predictive Analytical Models

- Developing Predictive Models for Skewed Data Sets

- Fraud Performance Benchmarks

- References

- Chapter 5 Social Network Analysis for Fraud Detection

- Chapter 6 Fraud Analytics: Post-Processing

- Chapter 7 Fraud Analytics: A Broader Perspective

- About the Authors

- Index

- EULA

Fraud Analytics Using

Descriptive, Predictive,

and Social Network

Techniques

Wiley & SAS Business

Series

The Wiley & SAS Business Series presents books that help senior-level

managers with their critical management decisions.

Titles in the Wiley & SAS Business Series include:

Analytics in a Big Data World: The Essential Guide to Data Science and Its

Applications by Bart Baesens

Bank Fraud: Using Technology to Combat Losses by Revathi Subrama-

nian

Big Data Analytics: Turning Big Data into Big Money by Frank Ohlhorst

Big Data, Big Innovation: Enabling Competitive Differentiation through

Business Analytics by Evan Stubbs

Business Analytics for Customer Intelligence by Gert Laursen

Business Intelligence Applied: Implementing an Effective Information and

Communications Technology Infrastructure by Michael Gendron

Business Intelligence and the Cloud: Strategic Implementation Guide by

Michael S. Gendron

Business Transformation: A Roadmap for Maximizing Organizational

Insights by Aiman Zeid

Connecting Organizational Silos: Taking Knowledge Flow Management to

the Next Level with Social Media by Frank Leistner

Data-Driven Healthcare: How Analytics and BI Are Transforming the

Industry by Laura Madsen

Delivering Business Analytics: Practical Guidelines for Best Practice by

Evan Stubbs

Demand-Driven Forecasting: A Structured Approach to Forecasting,

second edition by Charles Chase

Demand-Driven Inventory Optimization and Replenishment: Creating a

More Efficient Supply Chain by Robert A. Davis

Developing Human Capital: Using Analytics to Plan and Optimize Your

Learning and Development Investments by Gene Pease, Barbara Beres-

ford, and Lew Walker

The Executive’s Guide to Enterprise Social Media Strategy: How Social Net-

works Are Radically Transforming Your Business by David Thomas and

Mike Barlow

Economic and Business Forecasting: Analyzing and Interpreting Economet-

ric Results by John Silvia, Azhar Iqbal, Kaylyn Swankoski, Sarah

Watt, and Sam Bullard

Financial Institution Advantage and The Optimization of Information

Processing by Sean C. Keenan

Foreign Currency Financial Reporting from Euros to Yen to Yuan: A Guide

to Fundamental Concepts and Practical Applications by Robert Rowan

Harness Oil and Gas Big Data with Analytics: Optimize Exploration and

Production with Data Driven Models by Keith Holdaway

Health Analytics: Gaining the Insights to Transform Health Care by Jason

Burke

Heuristics in Analytics: A Practical Perspective of What Influences Our Ana-

lytical World by Carlos Andre Reis Pinheiro and Fiona McNeill

Human Capital Analytics: How to Harness the Potential of Your Organi-

zation’s Greatest Asset by Gene Pease, Boyce Byerly, and Jac Fitz-enz

Implement, Improve and Expand Your Statewide Longitudinal Data Sys-

tem: Creating a Culture of Data in Education by Jamie McQuiggan and

Armistead Sapp

Killer Analytics: Top 20 Metrics Missing from Your Balance Sheet by Mark

Brown

Predictive Analytics for Human Resources by Jac Fitz-enz and John

Mattox II

Predictive Business Analytics: Forward-Looking Capabilities to Improve

Business Performance by Lawrence Maisel and Gary Cokins

Retail Analytics: The Secret Weapon by Emmett Cox

Social Network Analysis in Telecommunications by Carlos Andre Reis

Pinheiro

Statistical Thinking: Improving Business Performance, second edition by

Roger W. Hoerl and Ronald D. Snee

Taming the Big Data Tidal Wave: Finding Opportunities in Huge Data

Streams with Advanced Analytics by Bill Franks

Too Big to Ignore: The Business Case for Big Data by Phil Simon

The Value of Business Analytics: Identifying the Path to Profitability by

Evan Stubbs

The Visual Organization: Data Visualization, Big Data, and the Quest for

Better Decisions by Phil Simon

Understanding the Predictive Analytics Lifecycle by Al Cordoba

Unleashing Your Inner Leader: An Executive Coach Tells All by Vickie

Bevenour

Using Big Data Analytics: Turning Big Data into Big Money by Jared

Dean

Win with Advanced Business Analytics: Creating Business Value from Your

Data by Jean Paul Isson and Jesse Harriott

For more information on these and other titles in the series, please

visit www.wiley.com.

Fraud Analytics

Using Descriptive,

Predictive, and

Social Network

Techniques

A Guide to Data Science

for Fraud Detection

Bart Baesens

Véronique Van Vlasselaer

Wouter Verbeke

Copyright © 2015 by John Wiley & Sons, Inc. All rights reserved.

Published by John Wiley & Sons, Inc., Hoboken, New Jersey.

Published simultaneously in Canada.

No part of this publication may be reproduced, stored in a retrieval system, or

transmitted in any form or by any means, electronic, mechanical, photocopying,

recording, scanning, or otherwise, except as permitted under Section 107 or 108 of the

1976 United States Copyright Act, without either the prior written permission of the

Publisher, or authorization through payment of the appropriate per-copy fee to the

Copyright Clearance Center, Inc., 222 Rosewood Drive, Danvers, MA 01923, (978)

750-8400, fax (978) 646-8600, or on the Web at www.copyright.com. Requests to the

Publisher for permission should be addressed to the Permissions Department, John

Wiley & Sons, Inc., 111 River Street, Hoboken, NJ 07030, (201) 748-6011, fax (201)

748-6008, or online at http://www.wiley.com/go/permissions.

Limit of Liability/Disclaimer of Warranty: While the publisher and author have used

their best efforts in preparing this book, they make no representations or warranties

with respect to the accuracy or completeness of the contents of this book and

specifically disclaim any implied warranties of merchantability or fitness for a particular

purpose. No warranty may be created or extended by sales representatives or written

sales materials. The advice and strategies contained herein may not be suitable for your

situation. You should consult with a professional where appropriate. Neither the

publisher nor author shall be liable for any loss of profit or any other commercial

damages, including but not limited to special, incidental, consequential, or other

damages.

For general information on our other products and services or for technical support,

please contact our Customer Care Department within the United States at (800)

762-2974, outside the United States at (317) 572-3993 or fax (317) 572-4002.

Wiley publishes in a variety of print and electronic formats and by print-on-demand.

Some material included with standard print versions of this book may not be included

in e-books or in print-on-demand. If this book refers to media such as a CD or DVD

that is not included in the version you purchased, you may download this material at

http://booksupport.wiley.com. For more information about Wiley products, visit

www.wiley.com.

Library of Congress Cataloging-in-Publication Data:

Baesens, Bart.

Fraud analytics using descriptive, predictive, and social network techniques : a guide

to data science for fraud detection / Bart Baesens, Veronique Van Vlasselaer, Wouter

Verbeke.

pages cm. — (Wiley & SAS business series)

Includes bibliographical references and index.

ISBN 978-1-119-13312-4 (cloth) — ISBN 978-1-119-14682-7 (epdf) —

ISBN 978-1-119-14683-4 (epub)

1. Fraud—Statistical methods. 2. Fraud—Prevention. 3. Commercial

crimes—Prevention. I. Title.

HV6691.B34 2015

364.16

′

3015195—dc23

2015017861

Cover Design: Wiley

Cover Image: ©iStock.com/aleksandarvelasevic

Printed in the United States of America

10987654321

To my wonderful wife, Katrien, and kids, Ann-Sophie, Victor,

and Hannelore.

To my parents and parents-in-law.

To my husband and soul mate, Niels, for his never-ending

support.

To my parents, parents-in-law, and siblings-in-law.

To Luit and Titus.

Contents

List of Figures xv

Foreword xxiii

Preface xxv

Acknowledgments xxix

Chapter 1 Fraud: Detection, Prevention, and Analytics! 1

Introduction 2

Fraud! 2

Fraud Detection and Prevention 10

Big Data for Fraud Detection 15

Data-Driven Fraud Detection 17

Fraud-Detection Techniques 19

Fraud Cycle 22

The Fraud Analytics Process Model 26

Fraud Data Scientists 30

A Fraud Data Scientist Should Have Solid Quantitative

Skills 30

A Fraud Data Scientist Should Be a Good Programmer 31

A Fraud Data Scientist Should Excel in

Communication and Visualization Skills 31

A Fraud Data Scientist Should Have a Solid Business

Understanding 32

A Fraud Data Scientist Should Be Creative 32

A Scientific Perspective on Fraud 33

References 35

Chapter 2 Data Collection, Sampling, and Preprocessing 37

Introduction 38

Types of Data Sources 38

Merging Data Sources 43

Sampling 45

Types of Data Elements 46

ix

xCONTENTS

Visual Data Exploration and Exploratory Statistical

Analysis 47

Benford’s Law 48

Descriptive Statistics 51

Missing Values 52

Outlier Detection and Treatment 53

Red Flags 57

Standardizing Data 59

Categorization 60

Weights of Evidence Coding 63

Variable Selection 65

Principal Components Analysis 68

RIDITs 72

PRIDIT Analysis 73

Segmentation 74

References 75

Chapter 3 Descriptive Analytics for Fraud Detection 77

Introduction 78

Graphical Outlier Detection Procedures 79

Statistical Outlier Detection Procedures 83

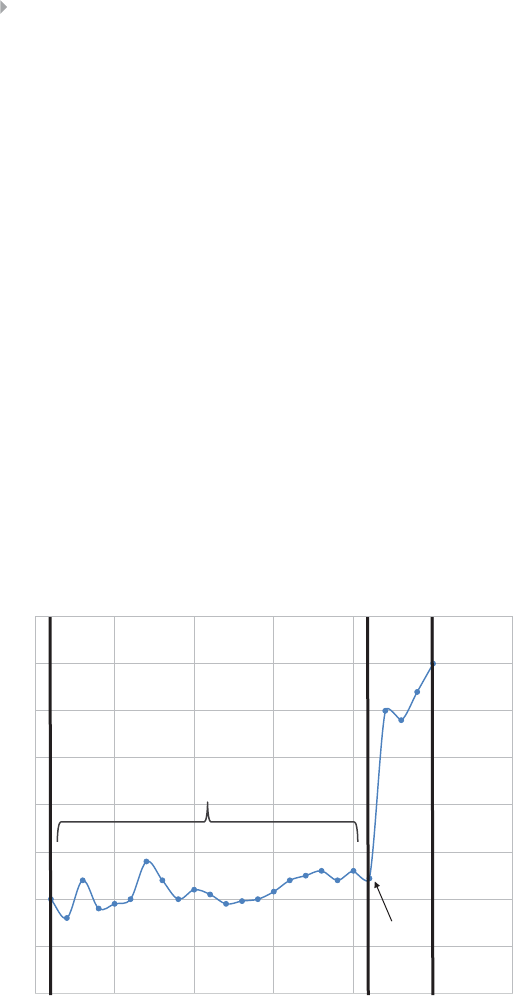

Break-Point Analysis 84

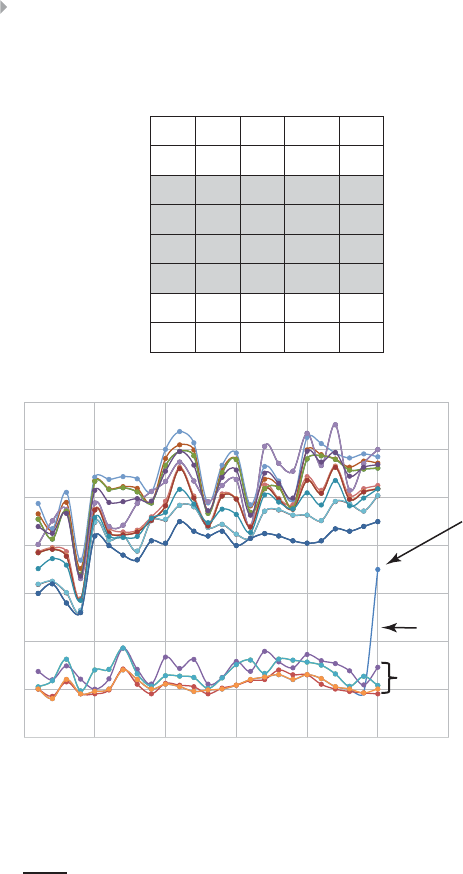

Peer-Group Analysis 85

Association Rule Analysis 87

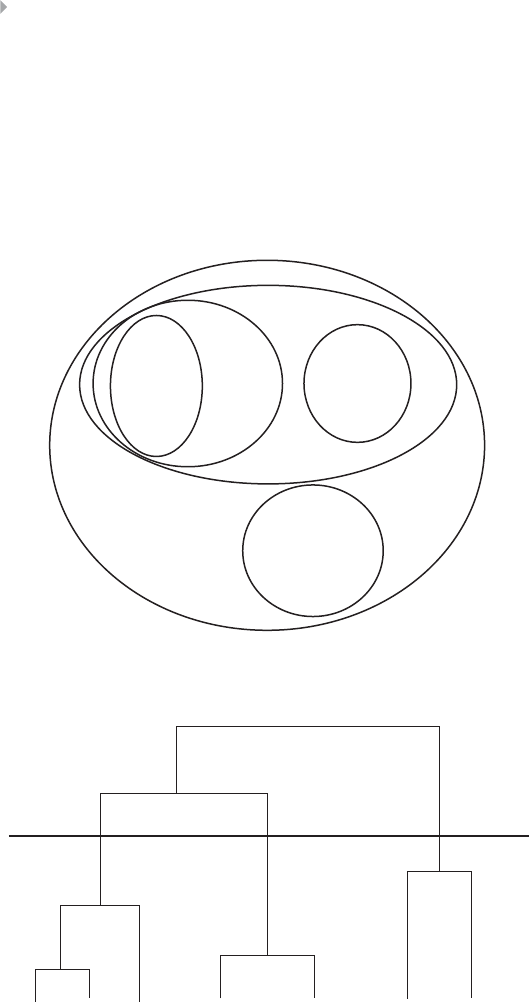

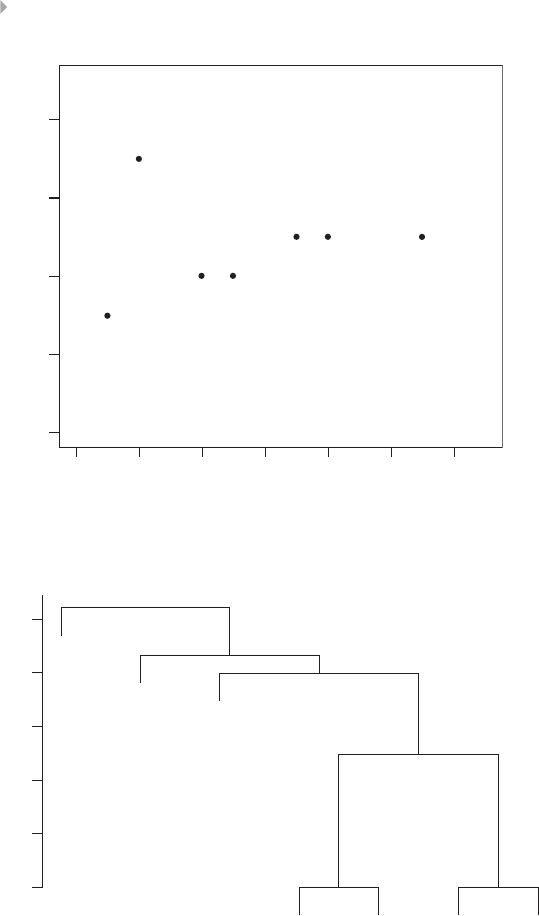

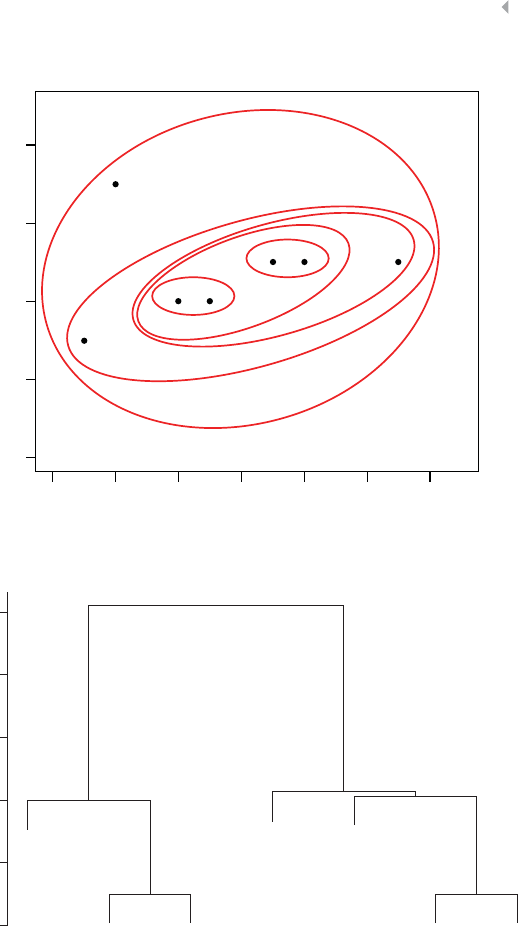

Clustering 89

Introduction 89

Distance Metrics 90

Hierarchical Clustering 94

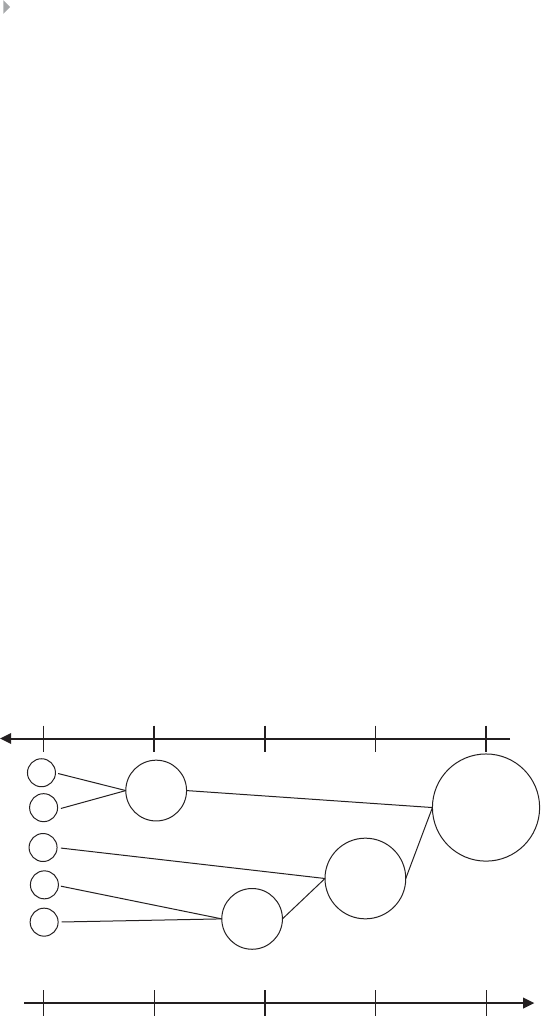

Example of Hierarchical Clustering Procedures 97

k-Means Clustering 104

Self-Organizing Maps 109

Clustering with Constraints 111

Evaluating and Interpreting Clustering Solutions 114

One-Class SVMs 117

References 118

Chapter 4 Predictive Analytics for Fraud Detection 121

Introduction 122

Target Definition 123

Linear Regression 125

Logistic Regression 127

Basic Concepts 127

Logistic Regression Properties 129

Building a Logistic Regression Scorecard 131

CONTENTS xi

Variable Selection for Linear and Logistic Regression 133

Decision Trees 136

Basic Concepts 136

Splitting Decision 137

Stopping Decision 140

Decision Tree Properties 141

Regression Trees 142

Using Decision Trees in Fraud Analytics 143

Neural Networks 144

Basic Concepts 144

Weight Learning 147

Opening the Neural Network Black Box 150

Support Vector Machines 155

Linear Programming 155

The Linear Separable Case 156

The Linear Nonseparable Case 159

The Nonlinear SVM Classifier 160

SVMs for Regression 161

Opening the SVM Black Box 163

Ensemble Methods 164

Bagging 164

Boosting 165

Random Forests 166

Evaluating Ensemble Methods 167

Multiclass Classification Techniques 168

Multiclass Logistic Regression 168

Multiclass Decision Trees 170

Multiclass Neural Networks 170

Multiclass Support Vector Machines 171

Evaluating Predictive Models 172

Splitting Up the Data Set 172

Performance Measures for Classification Models 176

Performance Measures for Regression Models 185

Other Performance Measures for Predictive Analytical

Models 188

Developing Predictive Models for Skewed Data Sets 189

Varying the Sample Window 190

Undersampling and Oversampling 190

Synthetic Minority Oversampling Technique (SMOTE) 192

Likelihood Approach 194

Adjusting Posterior Probabilities 197

Cost-sensitive Learning 198

Fraud Performance Benchmarks 200

References 201

xii CONTENTS

Chapter 5 Social Network Analysis for Fraud Detection 207

Networks: Form, Components, Characteristics, and Their

Applications 209

Social Networks 211

Network Components 214

Network Representation 219

Is Fraud a Social Phenomenon? An Introduction to

Homophily 222

Impact of the Neighborhood: Metrics 227

Neighborhood Metrics 228

Centrality Metrics 238

Collective Inference Algorithms 246

Featurization: Summary Overview 254

Community Mining: Finding Groups of Fraudsters 254

Extending the Graph: Toward a Bipartite Representation 266

Multipartite Graphs 269

Case Study: Gotcha! 270

References 277

Chapter 6 Fraud Analytics: Post-Processing 279

Introduction 280

The Analytical Fraud Model Life Cycle 280

Model Representation 281

Traffic Light Indicator Approach 282

Decision Tables 283

Selecting the Sample to Investigate 286

Fraud Alert and Case Management 290

Visual Analytics 296

Backtesting Analytical Fraud Models 302

Introduction 302

Backtesting Data Stability 302

Backtesting Model Stability 305

Backtesting Model Calibration 308

Model Design and Documentation 311

References 312

Chapter 7 Fraud Analytics: A Broader Perspective 313

Introduction 314

Data Quality 314

Data-Quality Issues 314

Data-Quality Programs and Management 315

Privacy 317

The RACI Matrix 318

Accessing Internal Data 319

CONTENTS xiii

Label-Based Access Control (LBAC) 324

Accessing External Data 325

Capital Calculation for Fraud Loss 326

Expected and Unexpected Losses 327

Aggregate Loss Distribution 329

Capital Calculation for Fraud Loss Using Monte Carlo

Simulation 331

An Economic Perspective on Fraud Analytics 334

Total Cost of Ownership 334

Return on Investment 335

In Versus Outsourcing 337

Modeling Extensions 338

Forecasting 338

Text Analytics 340

The Internet of Things 342

Corporate Fraud Governance 344

References 346

About the Authors 347

Index 349

List of Figures

Figure 1.1 Fraud Triangle 7

Figure 1.2 Fire Incident Claim-Handling Process 13

Figure 1.3 The Fraud Cycle 23

Figure 1.4 Outlier Detection at the Data Item Level 25

Figure 1.5 Outlier Detection at the Data Set Level 25

Figure 1.6 The Fraud Analytics Process Model 26

Figure 1.7 Profile of a Fraud Data Scientist 33

Figure 1.8 Screenshot of Web of Science Statistics for

Scientific Publications on Fraud between 1996

and 2014 34

Figure 2.1 Aggregating Normalized Data Tables into a

Non-Normalized Data Table 44

Figure 2.2 Pie Charts for Exploratory Data Analysis 49

Figure 2.3 Benford’s Law Describing the Frequency

Distribution of the First Digit 50

Figure 2.4 Multivariate Outliers 54

Figure 2.5 Histogram for Outlier Detection 54

Figure 2.6 Box Plots for Outlier Detection 55

Figure 2.7 Using the z-Scores for Truncation 57

Figure 2.8 Default Risk Versus Age 60

Figure 2.9 Illustration of Principal Component Analysis in a

Two-Dimensional Data Set 68

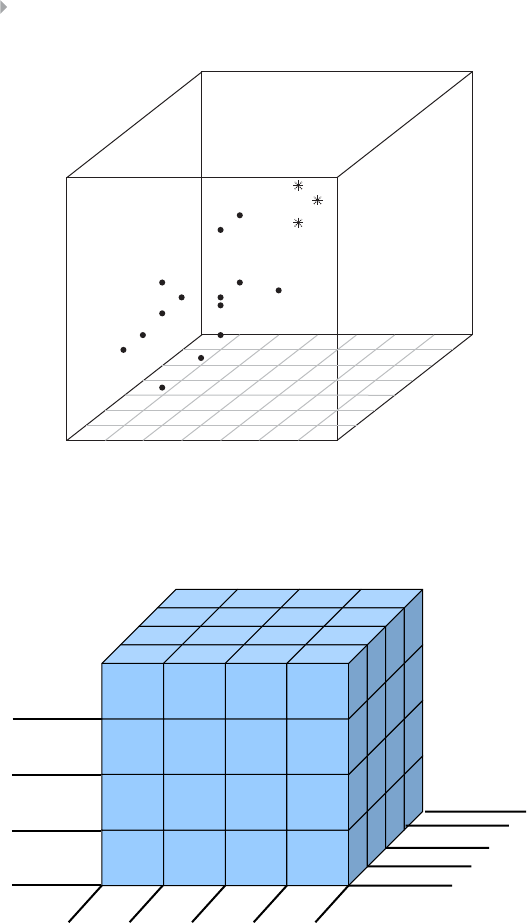

Figure 3.1 3D Scatter Plot for Detecting Outliers 80

Figure 3.2 OLAP Cube for Fraud Detection 80

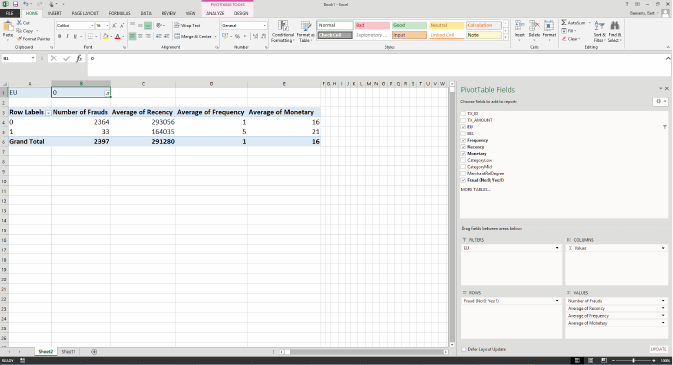

Figure 3.3 Example Pivot Table for Credit Card Fraud

Detection 82

xv

xvi LIST OF FIGURES

Figure 3.4 Break-Point Analysis 84

Figure 3.5 Peer-Group Analysis 86

Figure 3.6 Cluster Analysis for Fraud Detection 91

Figure 3.7 Hierarchical Versus Nonhierarchical Clustering

Techniques 91

Figure 3.8 Euclidean Versus Manhattan Distance 92

Figure 3.9 Divisive Versus Agglomerative Hierarchical

Clustering 94

Figure 3.10 Calculating Distances between Clusters 95

Figure 3.11 Example for Clustering Birds. The Numbers

Indicate the Clustering Steps 96

Figure 3.12 Dendrogram for Birds Example. The Thick Black

Line Indicates the Optimal Clustering 96

Figure 3.13 Screen Plot for Clustering 97

Figure 3.14 Scatter Plot of Hierarchical Clustering Data 98

Figure 3.15 Output of Hierarchical Clustering Procedures 98

Figure 3.16 k-Means Clustering: Start from Original Data 105

Figure 3.17 k-Means Clustering Iteration 1: Randomly

Select Initial Cluster Centroids 105

Figure 3.18 k-Means Clustering Iteration 1: Assign Remaining

Observations 106

Figure 3.19 k-Means Iteration Step 2: Recalculate Cluster

Centroids 107

Figure 3.20 k-Means Clustering Iteration 2: Reassign

Observations 107

Figure 3.21 k-Means Clustering Iteration 3: Recalculate

Cluster Centroids 108

Figure 3.22 k-Means Clustering Iteration 3: Reassign

Observations 108

Figure 3.23 Rectangular Versus Hexagonal SOM Grid 109

Figure 3.24 Clustering Countries Using SOMs 111

Figure 3.25 Component Plane for Literacy 112

LIST OF FIGURES xvii

Figure 3.26 Component Plane for Political Rights 113

Figure 3.27 Must-Link and Cannot-Link Constraints in

Semi-Supervised Clustering 113

Figure 3.28 𝛿-Constraints in Semi-Supervised Clustering 114

Figure 3.29 𝜀-Constraints in Semi-Supervised Clustering 114

Figure 3.30 Cluster Profiling Using Histograms 115

Figure 3.31 Using Decision Trees for Clustering

Interpretation 116

Figure 3.32 One-Class Support Vector Machines 117

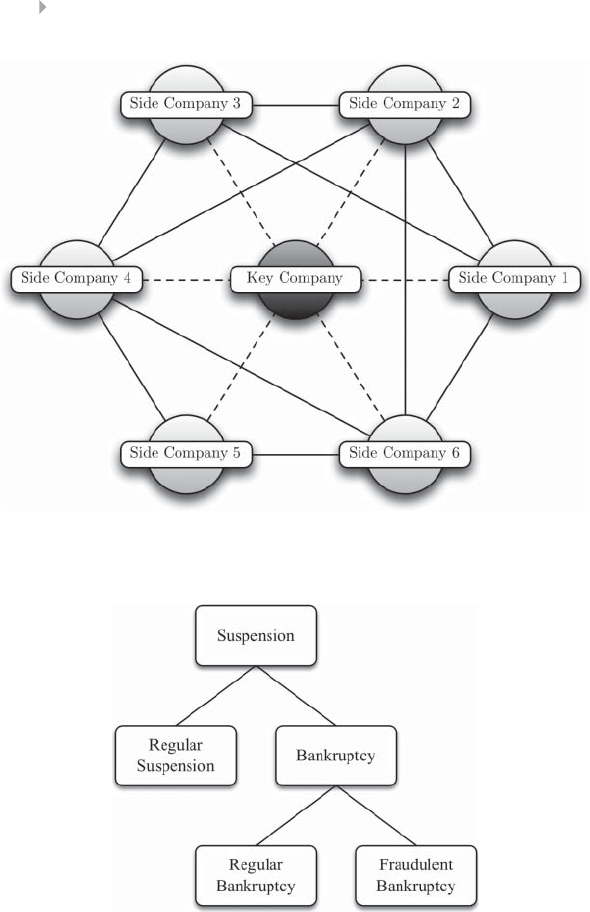

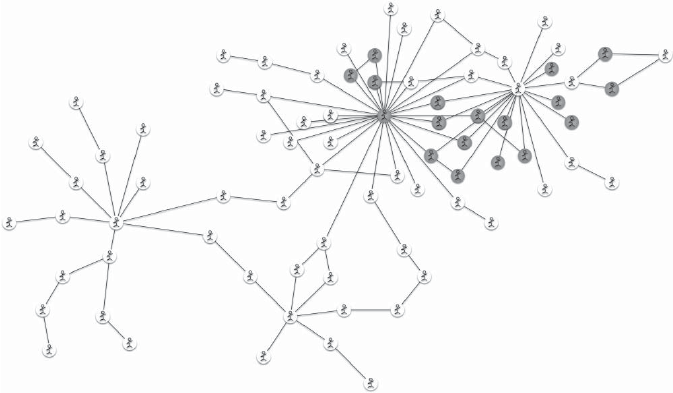

Figure 4.1 A Spider Construction in Tax Evasion Fraud 124

Figure 4.2 Regular Versus Fraudulent Bankruptcy 124

Figure 4.3 OLS Regression 126

Figure 4.4 Bounding Function for Logistic Regression 128

Figure 4.5 Linear Decision Boundary of Logistic Regression 130

Figure 4.6 Other Transformations 131

Figure 4.7 Fraud Detection Scorecard 133

Figure 4.8 Calculating the p-Value with a Student’s

t-Distribution 135

Figure 4.9 Variable Subsets for Four Variables V1,V2,V3,

and V4135

Figure 4.10 Example Decision Tree 137

Figure 4.11 Example Data Sets for Calculating Impurity 138

Figure 4.12 Entropy Versus Gini 139

Figure 4.13 Calculating the Entropy for Age Split 139

Figure 4.14 Using a Validation Set to Stop Growing a

Decision Tree 140

Figure 4.15 Decision Boundary of a Decision Tree 142

Figure 4.16 Example Regression Tree for Predicting the

Fraud Percentage 142

Figure 4.17 Neural Network Representation of Logistic

Regression 145

xviii LIST OF FIGURES

Figure 4.18 A Multilayer Perceptron (MLP) Neural Network 145

Figure 4.19 Local Versus Global Minima 148

Figure 4.20 Using a Validation Set for Stopping Neural

Network Training 149

Figure 4.21 Example Hinton Diagram 151

Figure 4.22 Backward Variable Selection 152

Figure 4.23 Decompositional Approach for Neural Network

Rule Extraction 153

Figure 4.24 Pedagogical Approach for Rule Extraction 154

Figure 4.25 Two-Stage Models 155

Figure 4.26 Multiple Separating Hyperplanes 157

Figure 4.27 SVM Classifier for the Perfectly Linearly

Separable Case 157

Figure 4.28 SVM Classifier in Case of Overlapping

Distributions 159

Figure 4.29 The Feature Space Mapping 160

Figure 4.30 SVMs for Regression 162

Figure 4.31 Representing an SVM Classifier as a Neural

Network 163

Figure 4.32 One-Versus-One Coding for Multiclass Problems 171

Figure 4.33 One-Versus-All Coding for Multiclass Problems 172

Figure 4.34 Training Versus Test Sample Set Up for

Performance Estimation 173

Figure 4.35 Cross-Validation for Performance Measurement 174

Figure 4.36 Bootstrapping 175

Figure 4.37 Calculating Predictions Using a Cut-Off 176

Figure 4.38 The Receiver Operating Characteristic Curve 178

Figure 4.39 Lift Curve 179

Figure 4.40 Cumulative Accuracy Profile 180

Figure 4.41 Calculating the Accuracy Ratio 181

Figure 4.42 The Kolmogorov-Smirnov Statistic 181

LIST OF FIGURES xix

Figure 4.43 A Cumulative Notch Difference Graph 184

Figure 4.44 Scatter Plot: Predicted Fraud Versus Actual

Fraud 185

Figure 4.45 CAP Curve for Continuous Targets 187

Figure 4.46 Regression Error Characteristic (REC) Curve 188

Figure 4.47 Varying the Time Window to Deal with Skewed

Data Sets 190

Figure 4.48 Oversampling the Fraudsters 191

Figure 4.49 Undersampling the Nonfraudsters 191

Figure 4.50 Synthetic Minority Oversampling Technique

(SMOTE) 193

Figure 5.1a Köningsberg Bridges 210

Figure 5.1b Schematic Representation of the Köningsberg

Bridges 211

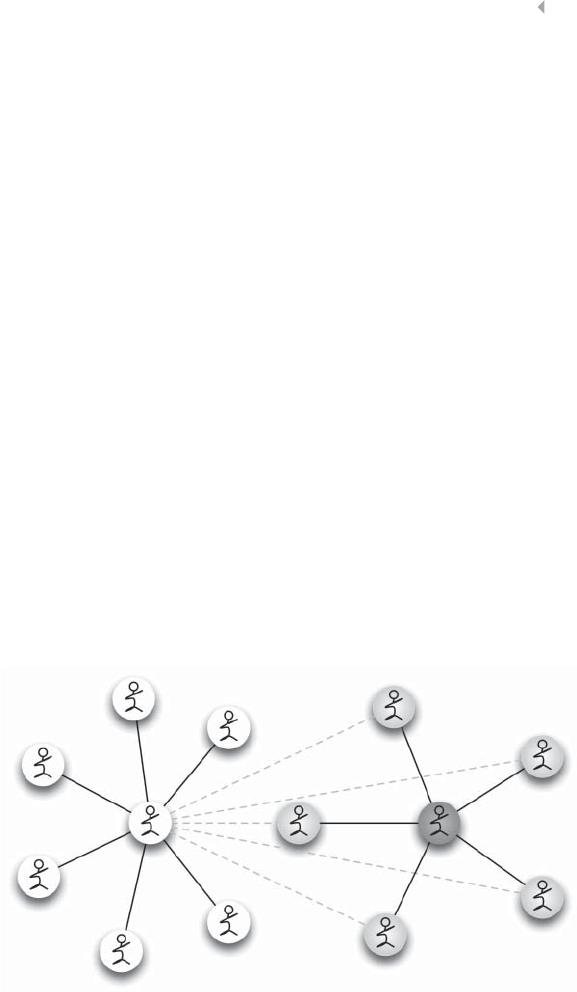

Figure 5.2 Identity Theft. The Frequent Contact List of a

Person is Suddenly Extended with Other Contacts

(Light Gray Nodes). This Might Indicate that a

Fraudster (Dark Gray Node) Took Over that

Customer’s Account and “shares” his/her

Contacts 213

Figure 5.3 Network Representation 214

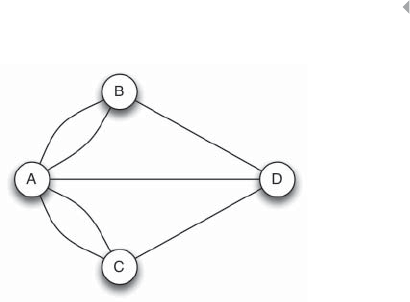

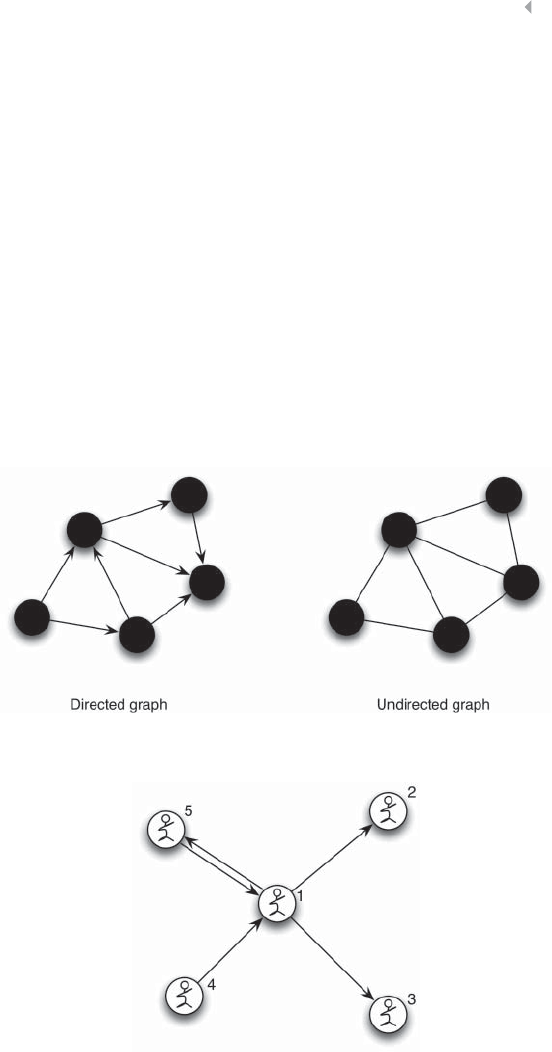

Figure 5.4 Example of a (Un)Directed Graph 215

Figure 5.5 Follower–Followee Relationships in a Twitter

Network 215

Figure 5.6 Edge Representation 216

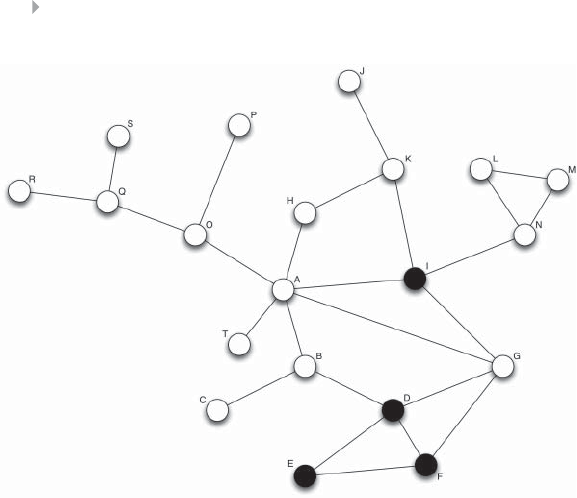

Figure 5.7 Example of a Fraudulent Network 218

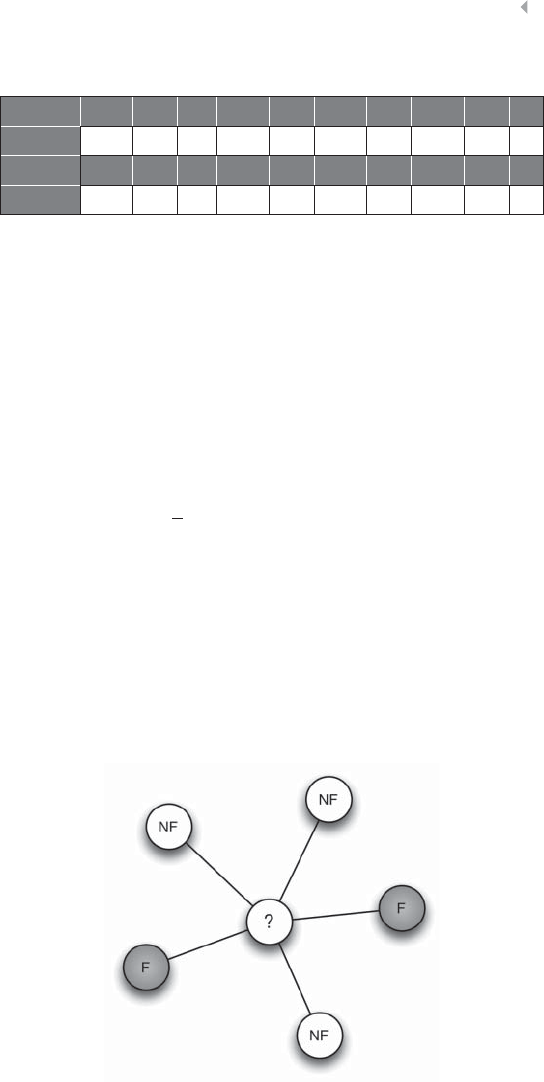

Figure 5.8 An Egonet. The Ego is Surrounded by Six Alters,

of Whom Two are Legitimate (White Nodes) and

Four are Fraudulent (Gray Nodes) 218

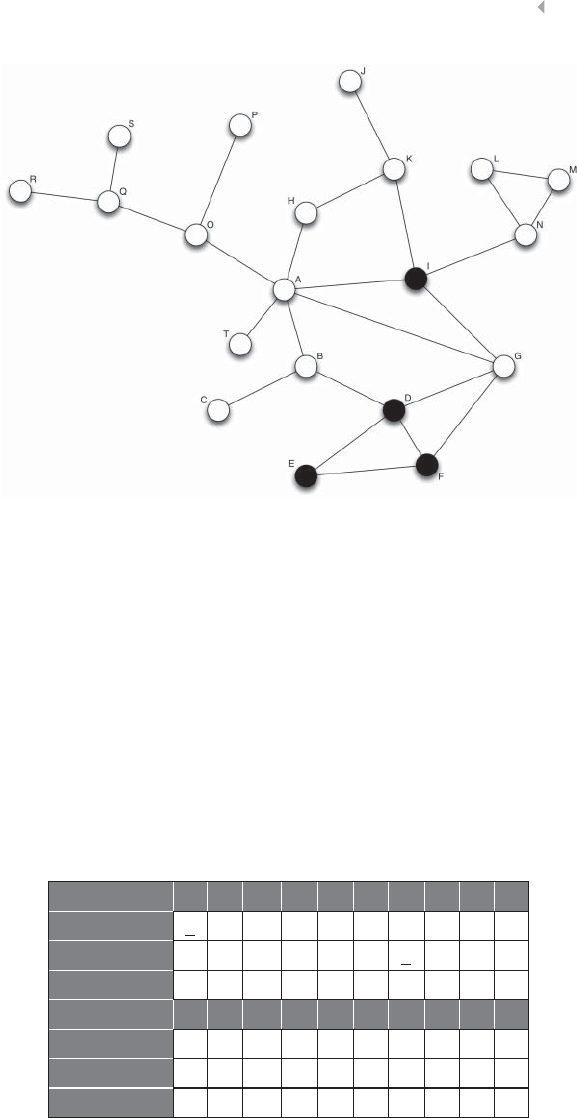

Figure 5.9 Toy Example of Credit Card Fraud 220

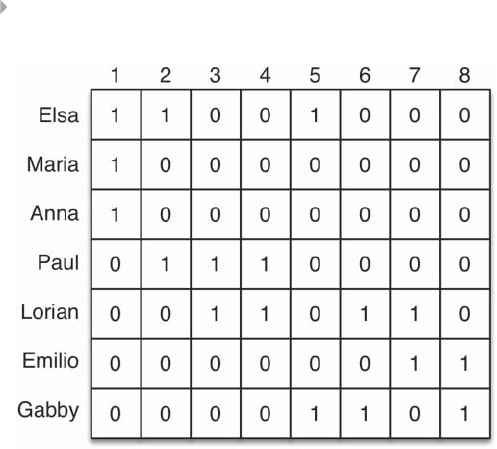

xx LIST OF FIGURES

Figure 5.10 Mathematical Representation of (a) a Sample

Network: (b) the Adjacency or Connectivity Matrix;

(c) the Weight Matrix; (d) the Adjacency List; and

(e) the Weight List 221

Figure 5.11 A Real-Life Example of a Homophilic Network 224

Figure 5.12 A Homophilic Network 225

Figure 5.13 Sample Network 229

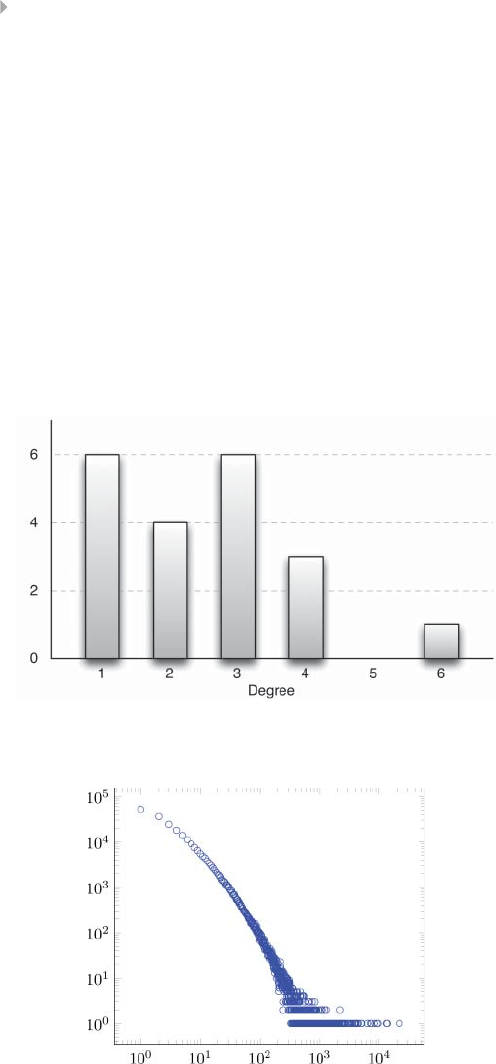

Figure 5.14a Degree Distribution 230

Figure 5.14b Illustration of the Degree Distribution for a

Real-Life Network of Social Security Fraud.

The Degree Distribution Follows a Power Law

(log-log axes) 230

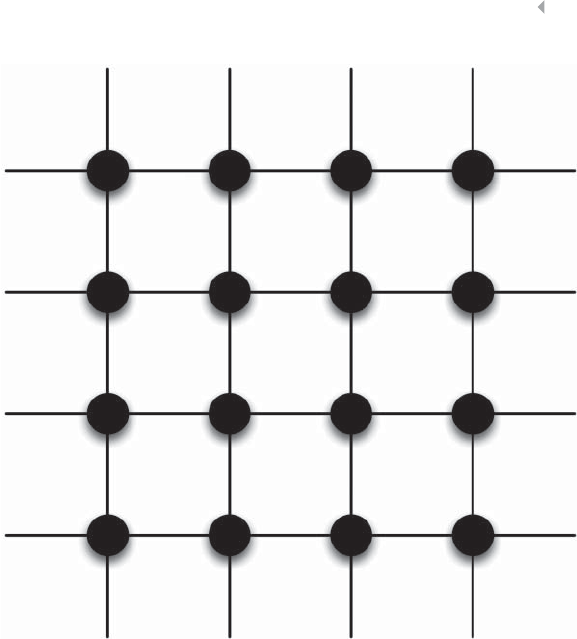

Figure 5.15 A4-regular Graph 231

Figure 5.16 Example Social Network for a Relational Neighbor

Classifier 233

Figure 5.17 Example Social Network for a Probabilistic

Relational Neighbor Classifier 235

Figure 5.18 Example of Social Network Features for a

Relational Logistic Regression Classifier 236

Figure 5.19 Example of Featurization with Features

Describing Intrinsic Behavior and Behavior of

the Neighborhood 237

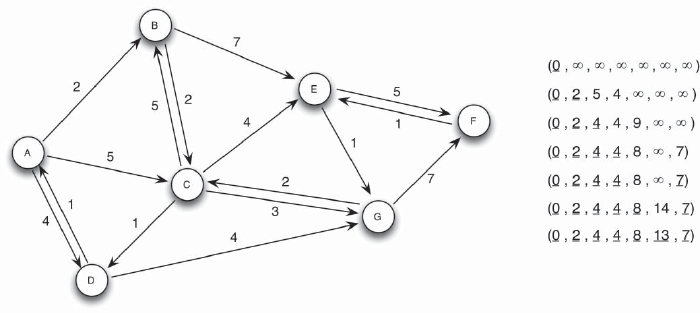

Figure 5.20 Illustration of Dijkstra’s Algorithm 241

Figure 5.21 Illustration of the Number of Connecting Paths

Between Two Nodes 242

Figure 5.22 Illustration of Betweenness Between Communities

of Nodes 245

Figure 5.23 Pagerank Algorithm 247

Figure 5.24 Illustration of Iterative Process of the PageRank

Algorithm 249

Figure 5.25 Sample Network 254

Figure 5.26 Community Detection for Credit Card Fraud 259

Figure 5.27 Iterative Bisection 261

LIST OF FIGURES xxi

Figure 5.28 Dendrogram of the Clustering of Figure 5.27 by

the Girvan-Newman Algorithm. The Modularity

Qis Maximized When Splitting the Network into

Two Communities ABC – DEFG 262

Figure 5.29 Complete (a) and Partial (b) Communities 264

Figure 5.30 Overlapping Communities 265

Figure 5.31 Unipartite Graph 266

Figure 5.32 Bipartite Graph 267

Figure 5.33 Connectivity Matrix of a Bipartite Graph 268

Figure 5.34 A Multipartite Graph 269

Figure 5.35 Sample Network of Gotcha! 270

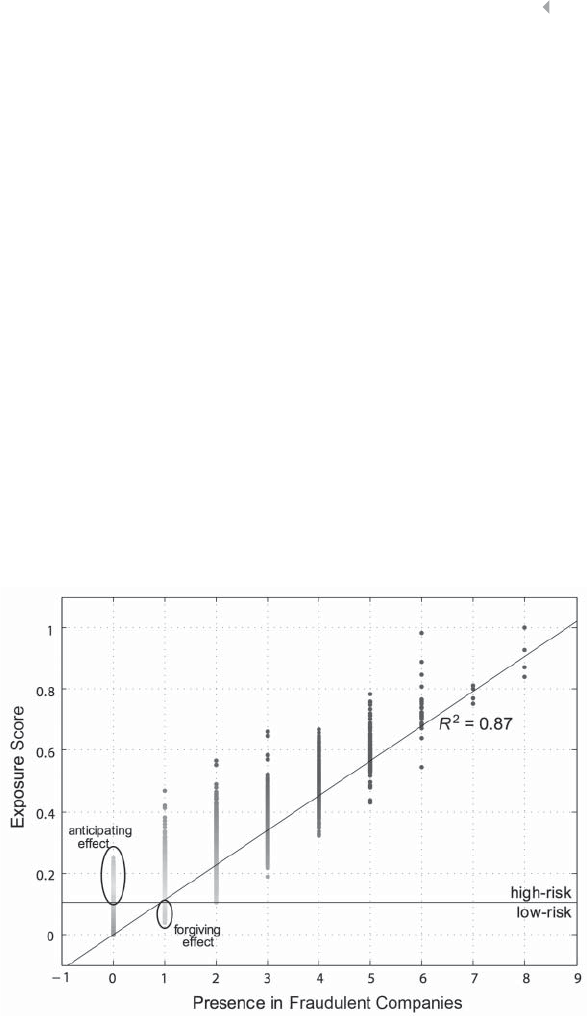

Figure 5.36 Exposure Score of the Resources Derived by a

Propagation Algorithm. The Results are Based

on a Real-life Data Set in Social Security Fraud 273

Figure 5.37 Egonet in Social Security Fraud. A Company Is

Associated with its Resources 274

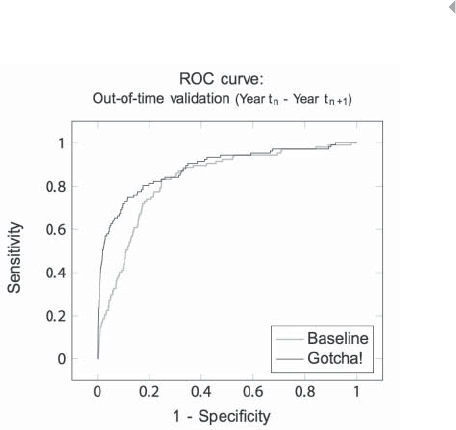

Figure 5.38 ROC Curve of the Gotcha! Model, which

Combines both Intrinsic and Relational Features 275

Figure 6.1 The Analytical Model Life Cycle 280

Figure 6.2 Traffic Light Indicator Approach 282

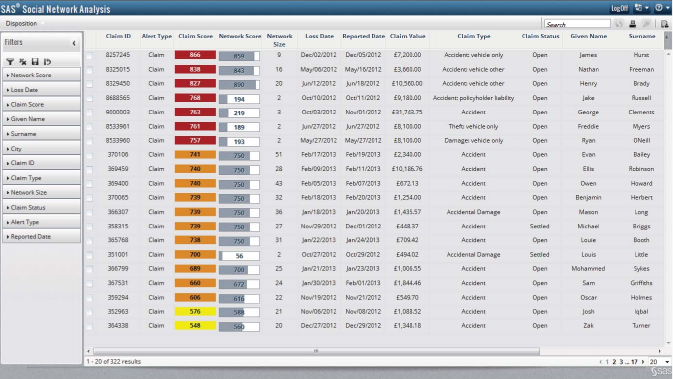

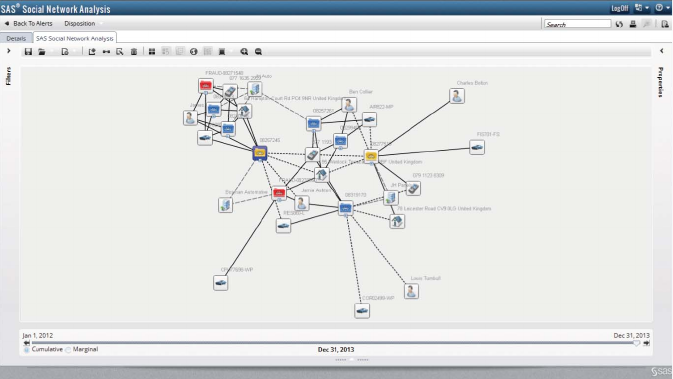

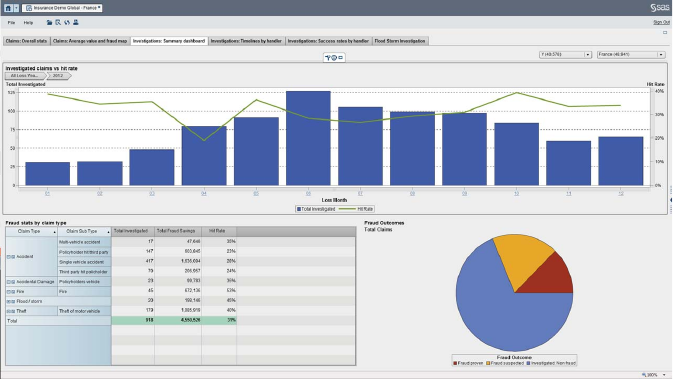

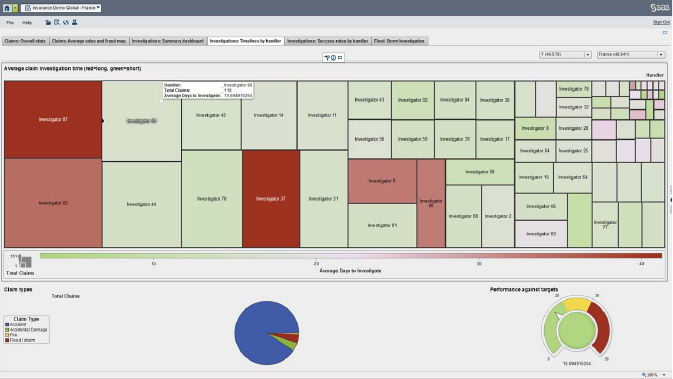

Figure 6.3 SAS Social Network Analysis Dashboard 293

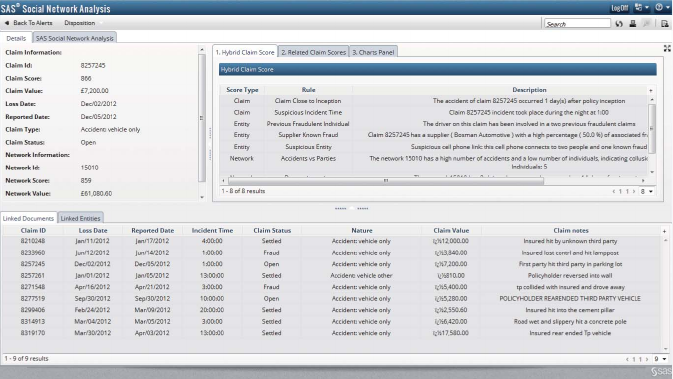

Figure 6.4 SAS Social Network Analysis Claim Detail

Investigation 294

Figure 6.5 SAS Social Network Analysis Link Detection 295

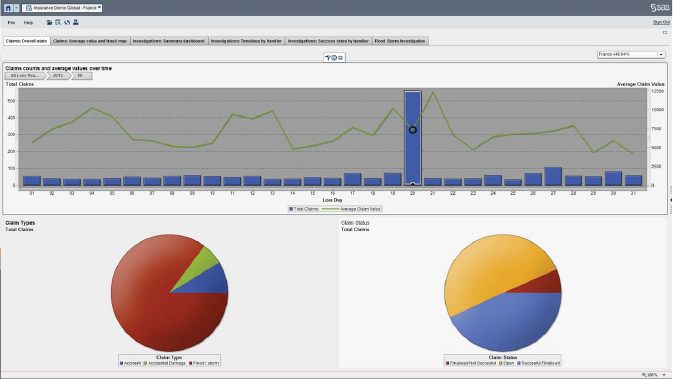

Figure 6.6 Distribution of Claim Amounts and Average

Claim Value 297

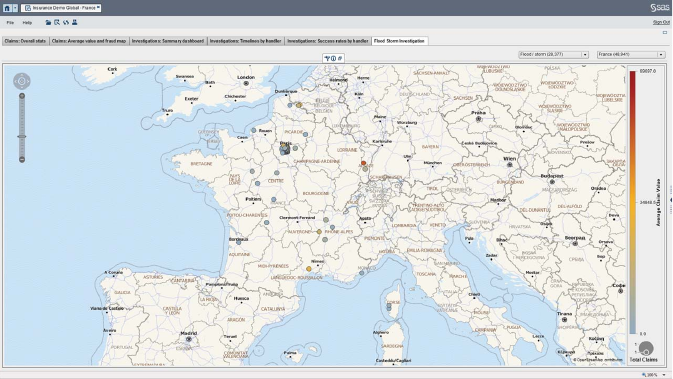

Figure 6.7 Geographical Distribution of Claims 298

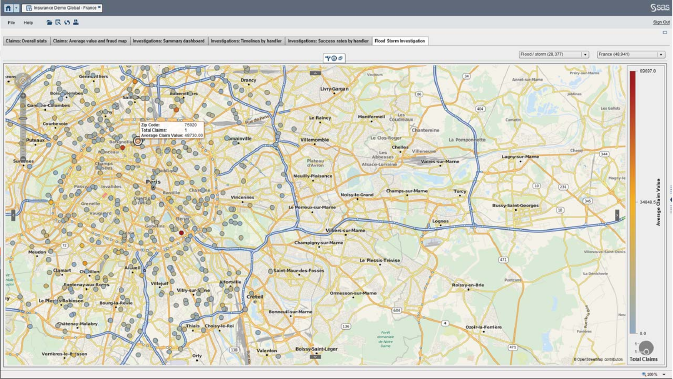

Figure 6.8 Zooming into the Geographical Distribution

of Claims 299

Figure 6.9 Measuring the Efficiency of the Fraud-Detection

Process 300

Figure 6.10 Evaluating the Efficiency of Fraud Investigators 301

xxii LIST OF FIGURES

Figure 7.1 RACI Matrix 318

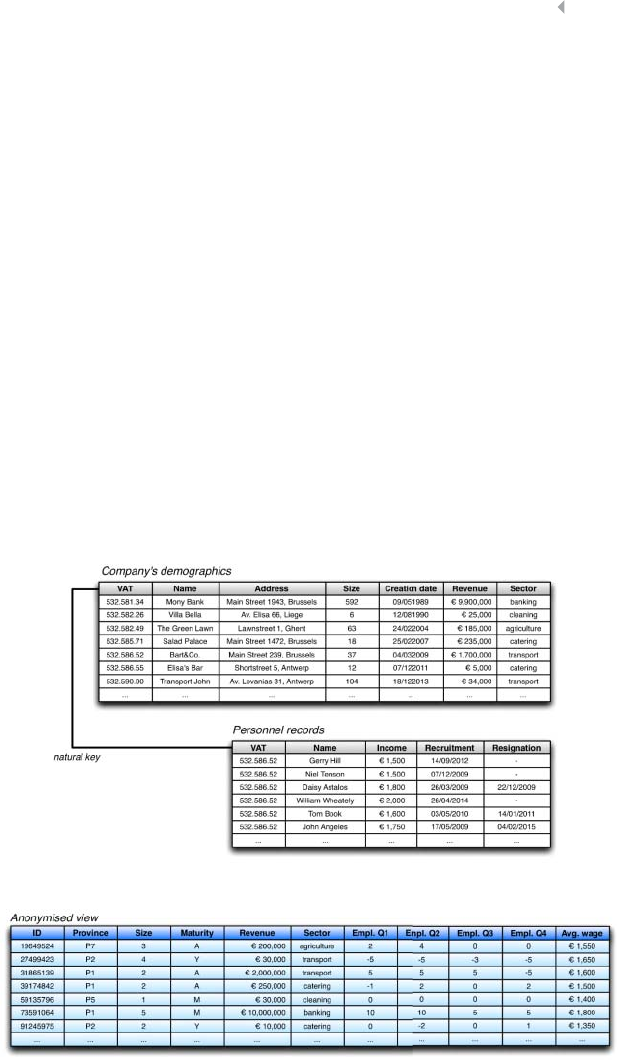

Figure 7.2 Anonymizing a Database 321

Figure 7.3 Different SQL Views Defined for a Database 323

Figure 7.4 Aggregate Loss Distribution with Indication

of Expected Loss, Value at Risk (VaR) at

99.9 Percent Confidence Level and Unexpected

Loss 331

Figure 7.5 Snapshot of a Credit Card Fraud Time Series

Data Set and Associated Histogram of the Fraud

Amounts 332

Figure 7.6 Aggregate Loss Distribution Resulting from a

Monte Carlo Simulation with Poisson

Distributed Monthly Fraud Frequency and

Associated Pareto Distributed Fraud Loss 334

Foreword

Fraud will always be with us. It is linked both to organized crime and to

terrorism, and it inflicts substantial economic damage. The perpetrators

of fraud play a dynamic cat and mouse game with those trying to stop

them. Preventing a particular kind of fraud does not mean the fraud-

sters give up, but merely that they change their tactics: they are con-

stantly on the lookout for new avenues for fraud, for new weaknesses

in the system. And given that our social and financial systems are

forever developing, there are always new opportunities to be exploited.

This book is a clear and comprehensive outline of the current state-

of-the-art in fraud-detection and prevention methodology. It describes

the data necessary to detect fraud, and then takes the reader from

the basics of fraud-detection data analytics, through advanced pattern

recognition methodology, to cutting-edge social network analysis and

fraud ring detection.

If we cannot stop fraud altogether, an awareness of the contents of

this book will at least enable readers to reduce the extent of fraud, and

make it harder for criminals to take advantage of the honest. The read-

ers’ organizations, be they public or private, will be better protected if

they implement the strategies described in this book. In short, this book

is a valuable contribution to the well-being of society and of the people

within it.

Professor David J. Hand

Imperial College, London

xxiii

Preface

It is estimated that a typical organization loses about 5 percent of its

revenues due to fraud each year. In this book, we will discuss how

state-of-the-art descriptive, predictive and social network analytics can

be used to fight fraud by learning fraud patterns from historical data.

The focus of this book is not on the mathematics or theory, but

on the practical applications. Formulas and equations will only be

included when absolutely needed from a practitioner’s perspective.

It is also not our aim to provide exhaustive coverage of all analytical

techniques previously developed but, rather, give coverage of the ones

that really provide added value in a practical fraud detection setting.

Being targeted at the business professional in the first place, the

book is written in a condensed, focused way. Prerequisite knowledge

consists of some basic exposure to descriptive statistics (e.g., mean,

standard deviation, correlation, confidence intervals, hypothesis

testing), data handling (using for example, Microsoft Excel, SQL,

etc.), and data visualization (e.g., bar plots, pie charts, histograms,

scatter plots, etc.). Throughout the discussion, many examples of

real-life fraud applications will be included in, for example, insurance

fraud, tax evasion fraud, and credit card fraud. The authors will also

integrate both their research and consulting experience throughout

the various chapters. The book is aimed at (senior) data analysts,

(aspiring) data scientists, consultants, analytics practitioners, and

researchers (e.g., PhD candidates) starting to explore the field.

Chapter 1 sets the stage on fraud detection, prevention, and analyt-

ics. It starts by defining fraud and then zooms into fraud detection and

prevention. The impact of big data for fraud detection and the fraud

analytics process model are reviewed next. The chapter concludes by

summarizing the key skills of a fraud data scientist.

Chapter 2 provides extensive discussion on the basic ingredient

of any fraud analytical model: data! It introduces various types of

xxv

xxvi PREFACE

data sources and discusses how to merge and sample them. The next

sections discuss the different types of data elements, visual exploration,

Benford’s law, and descriptive statistics. These are all essential tools

to start understanding the characteristics and limitations of the data

available. Data preprocessing activities are also extensively covered:

handling missing values, detecting and treating outliers, defining red

flags, standardizing data, categorizing variables, weights of evidence

coding, and variable selection. Principal component analysis is out-

lined as a technique to reduce the dimensionality of the input data.

This is then further illustrated with RIDIT and PRIDIT analysis. The

chapter ends by reviewing segmentation and the risks thereof.

Chapter 3 continues by exploring the use of descriptive analytics

for fraud detection. The idea here is to look for unusual patterns or

outliers in a fraud data set. Both graphical and statistical outlier detec-

tion procedures are reviewed first. This is followed by an overview of

break-point analysis, peer group analysis, association rules, clustering,

and one-class SVMs.

Chapter 4 zooms into predictive analytics for fraud detection. We

start from a labeled data set of transactions whereby each transaction

has a target of interest that can either be binary (e.g., fraudulent or

not) or continuous (e.g., amount of fraud). We then discuss various

analytical techniques to build predictive models: linear regression,

logistic regression, decision trees, neural networks, support vector

machines, ensemble methods, and multiclass classification techniques.

A next section reviews how to measure the performance of a pre-

dictive analytical model by first deciding on the data set split-up and

then on the performance metric. The class imbalance problem is

also extensively elaborated. The chapter concludes by giving some

performance benchmarks.

Chapter 5 introduces the reader to social network analysis and

its use for fraud detection. Stating that the propensity to fraud is

often influenced by the social neighborhood, we describe the main

components of a network and illustrate how transactional data sources

can be transformed in networks. In the next section, we elaborate

on featurization, the process on how to extract a set of meaningful

features from the network. We distinguish between three main types

of features: neighborhood metrics, centrality metrics, and collective

PREFACE xxvii

inference algorithms. We then zoom into community mining, where

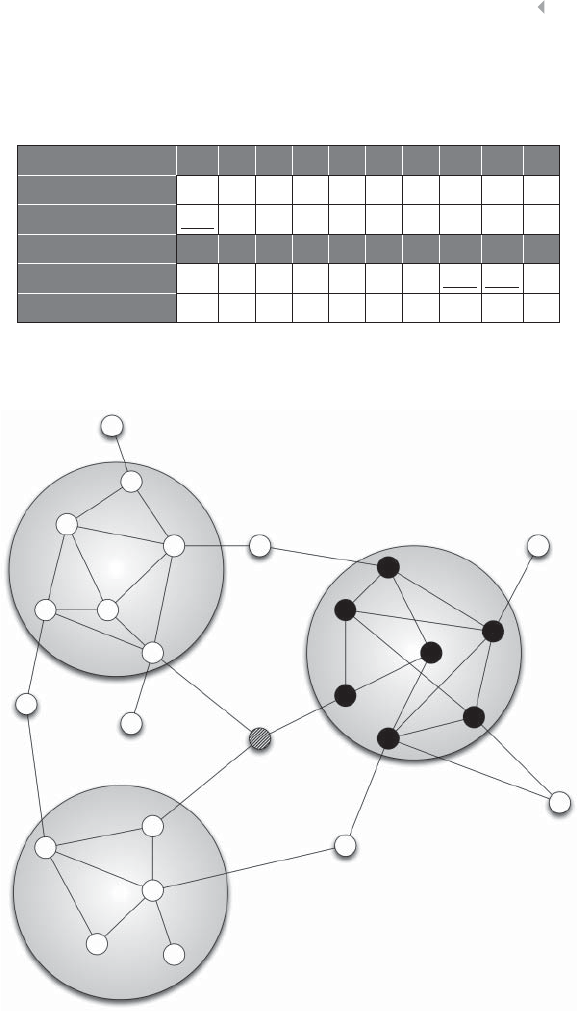

we aim at finding groups of fraudsters closely connected in the

network. By introducing multipartite graphs, we address the fact that

fraud often depends on a multitude of different factors and that the

inclusion of all these factors in a network representation contribute to

a better understanding and analysis of the detection problem at hand.

The chapter is concluded with a real-life example of social security

fraud.

Chapter 6 deals with the postprocessing of fraud analytical models.

It starts by giving an overview of the analytical fraud model lifecycle. It

then discusses the traffic light indicator approach and decision tables as

two popular model representations. This is followed by a set of guide-

lines to appropriately select the fraud sample to investigate. Fraud alert

and case management are covered next. We also illustrate how visual

analytics can contribute to the postprocessing activities. We describe

how to backtest analytical fraud models by considering data stability,

model stability, and model calibration. The chapter concludes by giving

some guidelines about model design and documentation.

Chapter 7 provides a broader perspective on fraud analytics. We

provide some guidelines for setting up and managing data quality

programs. We zoom into privacy and discuss various ways to ensure

appropriate access to both internal and external data. We discuss how

analytical fraud estimates can be used to calculate both expected and

unexpected losses, which can then help to determine provisioning

and capital buffers. A discussion of total cost of ownership and return

on investment provides an economic perspective on fraud analytics.

This is followed by a discussion of in- versus outsourcing of analytical

model development. We briefly zoom into some interesting modeling

extensions, such as forecasting and text analytics. The potential and

danger of the Internet of Things for fraud analytics is also covered.

The chapter concludes by giving some recommendations for corporate

fraud governance.

Acknowledgments

It is a great pleasure to acknowledge the contributions and assistance of

various colleagues, friends, and fellow analytics lovers to the writing of

this book. This book is the result of many years of research and teaching

in analytics, risk management, and fraud. We first would like to thank

our publisher, John Wiley & Sons, for accepting our book proposal less

than one year ago.

We are grateful to the active and lively analytics and fraud detec-

tion community for providing various user fora, blogs, online lectures,

and tutorials, which proved very helpful.

We would also like to acknowledge the direct and indirect contribu-

tions of the many colleagues, fellow professors, students, researchers,

and friends with whom we collaborated during the past years.

Last but not least, we are grateful to our partners, parents, and

families for their love, support, and encouragement.

We have tried to make this book as complete, accurate, and

enjoyable as possible. Of course, what really matters is what you, the

reader, think of it. Please let us know your views by getting in touch.

The authors welcome all feedback and comments—so do not hesitate

to let us know your thoughts!

Bart Baesens

Véronique Van Vlasselaer

Wouter Verbeke

August 2015

xxix

Fraud Analytics Using

Descriptive, Predictive,

and Social Network

Techniques

CHAPTER 1

Fraud: Detection,

Prevention, and

Analytics!

1

INTRODUCTION

In this first chapter, we set the scene for what’s ahead by introducing

fraud analytics using descriptive, predictive, and social network tech-

niques. We start off by defining and characterizing fraud and discuss

different types of fraud. Next, fraud detection and prevention is dis-

cussed as a means to address and limit the amount and overall impact of

fraud. Big data and analytics provide powerful tools that may improve

an organization’s fraud detection system. We discuss in detail how and

why these tools complement traditional expert-based fraud-detection

approaches. Subsequently, the fraud analytics process model is intro-

duced, providing a high-level overview of the steps that are followed

in developing and implementing a data-driven fraud-detection sys-

tem. The chapter concludes by discussing the characteristics and skills

of a good fraud data scientist, followed by a scientific perspective on

the topic.

FRAUD!

Since a thorough discussion or investigation requires clear and precise

definitions of the subject of interest, this first section starts by defining

fraud and by highlighting a number of essential characteristics. Sub-

sequently, an explanatory conceptual model will be introduced that

provides deeper insight in the underlying drivers of fraudsters, the

individuals committing fraud. Insight in the field of application—or

in other words, expert knowledge—is crucial for analytics to be suc-

cessfully applied in any setting, and matters eventually as much as

technical skill. Expert knowledge or insight in the problem at hand

helps an analyst in gathering and processing the right information in

the right manner, and to customize data allowing analytical techniques

to perform as well as possible in detecting fraud.

The Oxford Dictionary defines fraud as follows:

Wrongful or criminal deception intended to result in

financial or personal gain.

On the one hand, this definition captures the essence of fraud

and covers the many different forms and types of fraud that will be

2

FRAUD: DETECTION, PREVENTION, AND ANALYTICS! 3

discussed in this book. On the other hand, it does not very precisely

describe the nature and characteristics of fraud, and as such, does not

provide much direction for discussing the requirements of a fraud

detection system. A more useful definition will be provided below.

Fraud is definitely not a recent phenomenon unique to modern

society, nor is it even unique to mankind. Animal species also engage

in what could be called fraudulent activities, although maybe we should

classify the behavior as displayed by, for instance, chameleons, stick

insects, apes, and others rather as manipulative behavior instead of fraud-

ulent activities, since wrongful or criminal are human categories or con-

cepts that do not straightforwardly apply to animals. Indeed, whether

activities are wrongful or criminal depends on the applicable rules or

legislation, which defines explicitly and formally these categories that

are required in order to be able to classify behavior as being fraudulent.

A more thorough and detailed characterization of the multifaceted

phenomenon of fraud is provided by Van Vlasselaer et al. (2015):

Fraud is an uncommon, well-considered,

imperceptibly concealed, time-evolving and often

carefully organized crime which appears in many

types of forms.

This definition highlights five characteristics that are associated

with particular challenges related to developing a fraud-detection

system, which is the main topic of this book. The first emphasized

characteristic and associated challenge concerns the fact that fraud

is uncommon. Independent of the exact setting or application, only

a minority of the involved population of cases typically concerns

fraud, of which furthermore only a limited number will be known to

concern fraud. This makes it difficult to both detect fraud, since the

fraudulent cases are covered by the nonfraudulent ones, as well as to

learn from historical cases to build a powerful fraud-detection system

since only few examples are available.

In fact, fraudsters exactly try to blend in and not to behave different

from others in order not to get noticed and to remain covered by non-

fraudsters. This effectively makes fraud imperceptibly concealed,since

fraudsters do succeed in hiding by well considering and planning how

4FRAUD ANALYTICS

to precisely commit fraud. Their behavior is definitely not impulsive

and unplanned, since if it were, detection would be far easier.

They also adapt and refine their methods, which they need to do

in order to remain undetected. Fraud-detection systems improve and

learn by example. Therefore, the techniques and tricks fraudsters adopt

evolve in time along with, or better ahead of fraud-detection mecha-

nisms. This cat-and-mouse play between fraudsters and fraud fighters

may seem to be an endless game, yet there is no alternative solution

so far. By adopting and developing advanced fraud-detection and pre-

vention mechanisms, organizations do manage to reduce losses due to

fraud because fraudsters, like other criminals, tend to look for the easy

way and will look for other, easier opportunities. Therefore, fighting

fraud by building advanced and powerful detection systems is defi-

nitely not a pointless effort, but admittedly, it is very likely an effort

without end.

Fraud is often as well a carefully organized crime, meaning that

fraudsters often do not operate independently, have allies, and may

induce copycats. Moreover, several fraud types such as money laun-

dering and carousel fraud involve complex structures that are set up in

order to commit fraud in an organized manner. This makes fraud not

to be an isolated event, and as such in order to detect fraud the context

(e.g., the social network of fraudsters) should be taken into account.

Research shows that fraudulent companies indeed are more connected

to other fraudulent companies than to nonfraudulent companies, as

shown in a company tax-evasion case study by Van Vlasselaer et al.

(2015). Social network analytics for fraud detection, as discussed

in Chapter 5, appears to be a powerful tool for unmasking fraud by

making clever use of contextual information describing the network or

environment of an entity.

A final element in the description of fraud provided by Van

Vlasselaer et al. indicates the many different types of forms in which

fraud occurs. This both refers to the wide set of techniques and

approaches used by fraudsters as well as to the many different settings

in which fraud occurs or economic activities that are susceptible to

fraud. Table 1.1 provides a nonexhaustive overview and description of

a number of important fraud types—important being defined in terms of

frequency of occurrence as well as the total monetary value involved.

FRAUD: DETECTION, PREVENTION, AND ANALYTICS! 5

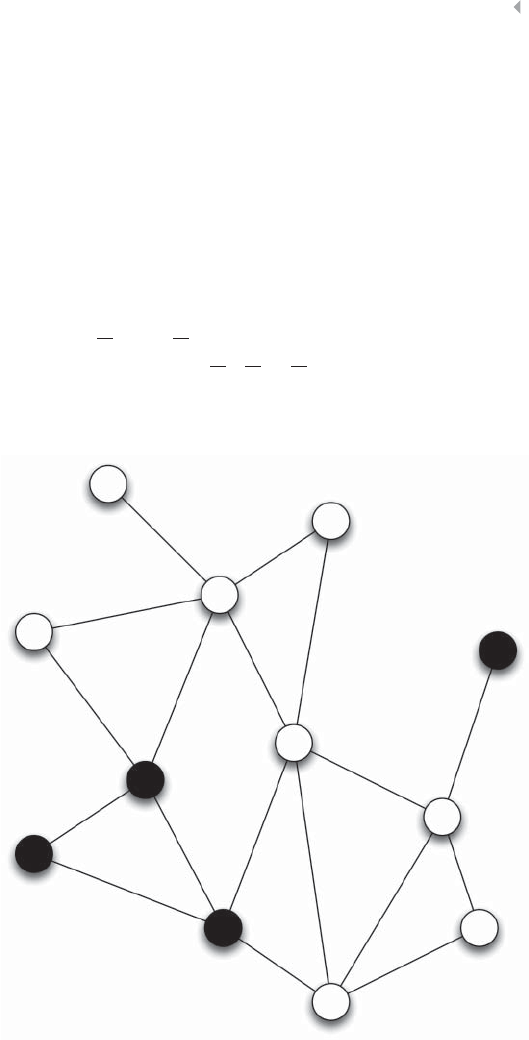

Table 1.1 Nonexhaustive List of Fraud Categories and Types

Credit card fraud In credit card fraud there is an unauthorized taking of another’s credit.

Some common credit card fraud subtypes are counterfeiting credit cards

(for the definition of counterfeit, see below), using lost or stolen cards, or

fraudulently acquiring credit through mail (definition adopted from

definitions.uslegal.com). Two subtypes can been identified, as described

by Bolton and Hand (2002): (1) Application fraud, involving individuals

obtaining new credit cards from issuing companies by using false

personal information, and then spending as much as possible in a short

space of time; (2) Behavioral fraud, where details of legitimate cards are

obtained fraudulently and sales are made on a “Cardholder Not Present”

basis. This does not necessarily require stealing the physical card, only

stealing the card credentials. Behavioral fraud concerns most of the credit

card fraud. Also, debit card fraud occurs, although less frequent. Credit

card fraud is a form of identity theft, as will be defined below.

Insurance fraud Broad category-spanning fraud related to any type of insurance, both from

the side of the buyer or seller of an insurance contract. Insurance fraud

from the issuer (seller) includes selling policies from nonexistent

companies, failing to submit premiums and churning policies to create

more commissions. Buyer fraud includes exaggerated claims (property

insurance: obtaining payment that is worth more than the value of the

property destroyed), falsified medical history (healthcare insurance: fake

injuries), postdated policies, faked death, kidnapping or murder (life

insurance fraud), and faked damage (automobile insurance: staged

collision) (definition adopted from www.investopedia.com).

Corruption Corruption is the misuse of entrusted power (by heritage, education,

marriage, election, appointment, or whatever else) for private gain. This

definition is similar to the definition of fraud provided by the Oxford

Dictionary discussed before, in that the objective is personal gain. It is

different in that it focuses on misuse of entrusted power. The definition

covers as such a broad range of different subtypes of corruption, so does

not only cover corruption by a politician or a public servant, but also, for

example, by the CEO or CFO of a company, the notary public, the team

leader at a workplace, the administrator or admissions-officer to a private

school or hospital, the coach of a soccer team, and so on (definition

adopted from www.corruptie.org).

Counterfeit An imitation intended to be passed off fraudulently or deceptively as

genuine. Counterfeit typically concerns valuable objects, credit cards,

identity cards, popular products, money, etc. (definition adopted from

www.dictionary.com).

(continued)

6FRAUD ANALYTICS

Table 1.1 (Continued)

Product warranty

fraud

A product warranty is a type of guarantee that a manufacturer or similar

party makes regarding the condition of its product, and also refers to the

terms and situations in which repairs or exchanges will be made in the

event that the product does not function as originally described or

intended (definition adopted from www.investopedia.com). When a

product fails to offer the described functionalities or displays deviating

characteristics or behavior that are a consequence of the production

process and not a consequence of misuse by the customer, compensation

or remuneration by the manufacturer or provider can be claimed. When

the conditions of the product have been altered due to the customer’s use

of the product, then the warranty does not apply. Intentionally wrongly

claiming compensation or remuneration based on a product warranty is

called product warranty fraud.

Healthcare fraud Healthcare fraud involves the filing of dishonest healthcare claims in

order to make profit. Practitioner schemes include: individuals obtaining

subsidized or fully covered prescription pills that are actually unneeded

and then selling them on the black market for a profit; billing by

practitioners for care that they never rendered; filing duplicate claims for

the same service rendered; billing for a noncovered service as a covered

service; modifying medical records, and so on. Members can commit

healthcare fraud by providing false information when applying for

programs or services, forging or selling prescription drugs, loaning or

using another’s insurance card, and so on (definition adopted from

www.law.cornell.edu).

Telecommunica-

tions fraud

Telecommunication fraud is the theft of telecommunication services

(telephones, cell phones, computers, etc.) or the use of

telecommunication services to commit other forms of fraud (definition

adopted from itlaw.wikia.com). An important example concerns cloning

fraud (i.e. the cloning of a phone number and the related call credit by a

fraudster), which is an instance of superimposition fraud in which

fraudulent usage is superimposed on (added to) the legitimate usage of

an account (Fawcett and Provost 1997).

Money

laundering

The process of taking the proceeds of criminal activity and making them

appear legal. Laundering allows criminals to transform illegally obtained

gain into seemingly legitimate funds. It is a worldwide problem, with an

estimated $300 billion going through the process annually in the United

States (definition adopted from legal-dictionary.thefreedictionary.com).

Click fraud Click fraud is an illegal practice that occurs when individuals click on a

website’s click-through advertisements (either banner ads or paid text

links) to increase the payable number of clicks to the advertiser. The

illegal clicks could either be performed by having a person manually click

the advertising hyperlinks or by using automated software or online bots

that are programmed to click these banner ads and pay-per-click text ad

links (definition adopted from www.webopedia.com).

FRAUD: DETECTION, PREVENTION, AND ANALYTICS! 7

Table 1.1 (Continued)

Identity theft The crime of obtaining the personal or financial information of another

person for the purpose of assuming that person’s name or identity in order

to make transactions or purchases. Some identity thieves sift through

trash bins looking for bank account and credit card statements; other more

high-tech methods involve accessing corporate databases to steal lists of

customer information (definition adopted from www.investopedia.com).

Tax evasion Tax evasion is the illegal act or practice of failing to pay taxes that are

owed. In businesses, tax evasion can occur in connection with income

taxes, employment taxes, sales and excise taxes, and other federal, state,

and local taxes. Examples of practices that are considered tax evasion

include knowingly not reporting income or underreporting income (i.e.,

claiming less income than you actually received from a specific source)

(definition adopted from biztaxlaw.about.com).

Plagiarism Plagiarizing is defined by Merriam Webster’s online dictionary as to steal

and pass off (the ideas or words of another) as one’s own, to use

(another’s production) without crediting the source, to commit literary

theft, to present as new and original an idea or product derived from an

existing source. It involves both stealing someone else’s work and lying

about it afterward (definition adopted from www.plagiarism.org).

In the end, fraudulent activities are intended to result in gains or

benefits for the fraudster, as emphasized by the definition of fraud pro-

vided by the Oxford Dictionary. The potential, usually monetary, gain or

benefit forms in the large majority of cases the basic driver for commit-

ting fraud.

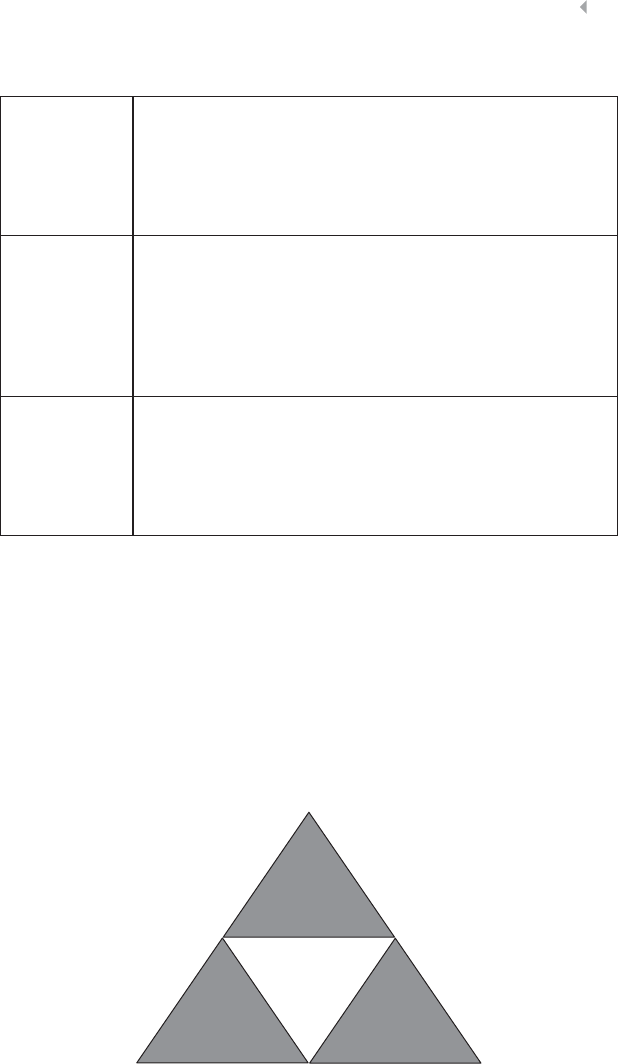

The so-called fraud triangle as depicted in Figure 1.1 provides a

more elaborate explanation for the underlying motives or drivers for

Pressure

RationalizationOpportunity

Fraud Triangle

Figure 1.1 Fraud Triangle

8FRAUD ANALYTICS

committing occupational fraud. The fraud triangle originates from a

hypothesis formulated by Donald R. Cressey in his 1953 book Other

People’s Money: A Study of the Social Psychology of Embezzlement:

Trusted persons become trust violators when they conceive

of themselves as having a financial problem which is

non-shareable, are aware this problem can be secretly

resolved by violation of the position of financial trust, and

are able to apply to their own conduct in that situation

verbalizations which enable them to adjust their

conceptions of themselves as trusted persons with their

conceptions of themselves as users of the entrusted funds

or property.

This basic conceptual model explains the factors that together cause

or explain the drivers for an individual to commit occupational fraud,

yet provides a useful insight in the fraud phenomenon from a broader

point of view as well. The model has three legs that together institute

fraudulent behavior:

1. Pressure is the first leg and concerns the main motivation for

committing fraud. An individual will commit fraud because a

pressure or a problem is experienced of financial, social, or any

other nature, and it cannot be resolved or relieved in an autho-

rized manner.

2. Opportunity is the second leg of the model, and concerns

the precondition for an individual to be able to commit

fraud. Fraudulent activities can only be committed when

the opportunity exists for the individual to resolve or relieve

the experienced pressure or problem in an unauthorized but

concealed or hidden manner.

3. Rationalization is the psychological mechanism that explains

why fraudsters do not refrain from committing fraud and think

of their conduct as acceptable.

An essay by Duffield and Grabosky (2001) further explores

the motivational basis of fraud from a psychological perspective.

FRAUD: DETECTION, PREVENTION, AND ANALYTICS! 9

It concludes that a number of psychological factors may be present

in those persons who commit fraud, but that these factors are also

associated with entirely legitimate forms of human endeavor. And so

fraudsters cannot be distinguished from nonfraudsters purely based

on psychological characteristics or patterns.

Fraud is a social phenomenon in the sense that the potential bene-

fits for the fraudsters come at the expense of the victims. These victims

are individuals, enterprises, or the government, and as such society as

a whole. Some recent numbers give an indication of the estimated size

and the financial impact of fraud:

◾A typical organization loses 5 percent of its revenues to fraud

each year (www.acfe.com).

◾The total cost of insurance fraud (non–health insurance) in the

United States is estimated to be more than $40 billion per year

(www.fbi.gov).

◾Fraud is costing the United Kingdom £73 billion a year (National

Fraud Authority).

◾Credit card companies “lose approximately seven cents per

every hundred dollars of transactions due to fraud” (Andrew

Schrage, Money Crashers Personal Finance, 2012).

◾The average size of the informal economy, as a percent of offi-

cial GNI in the year 2000, in developing countries is 41 percent,

in transition countries 38 percent, and in OECD countries 18

percent (Schneider 2002).

Even though these numbers are rough estimates rather than exact

measurements, they are based on evidence and do indicate the impor-

tance and impact of the phenomenon, and therefore as well the need

for organizations and governments to actively fight and prevent fraud

with all means they have at their disposal. As will be further elaborated

in the final chapter, these numbers also indicate that it is likely worth-

while to invest in fraud-detection and fraud-prevention systems, since

a significant financial return on investment can be made.

The importance and need for effective fraud-detection and fraud-

prevention systems is furthermore highlighted by the many different

10 FRAUD ANALYTICS

forms or types of fraud of which a number have been summarized in

Table 1.1, which is not exhaustive but, rather, indicative, and which

illustrates the widespread occurrence across different industries and

product and service segments. The broad fraud categories enlisted and

briefly defined in Table 1.1 can be further subdivided into more specific

subtypes, which, although interesting, would lead us too far into the

particularities of each of these forms of fraud. One may refer to the fur-

ther reading sections at the end of each chapter of this book, providing

selected references to specialized literature on different forms of fraud.

A number of particular fraud types will also be further elaborated in

real-life case studies throughout the book.

FRAUD DETECTION AND PREVENTION

Two components that are essential parts of almost any effective strat-

egy to fight fraud concern fraud detection and fraud prevention.Fraud

detection refers to the ability to recognize or discover fraudulent activ-

ities, whereas fraud prevention refers to measures that can be taken

to avoid or reduce fraud. The difference between both is clear-cut; the

former is an ex post approach whereas the latter an ex ante approach.

Both tools may and likely should be used in a complementary manner

to pursue the shared objective, fraud reduction.

However, as will be discussed in more detail further on, preventive

actions will change fraud strategies and consequently impact detection

power. Installing a detection system will cause fraudsters to adapt and

change their behavior, and so the detection system itself will impair

eventually its own detection power. So although complementary, fraud

detection and prevention are not independent and therefore should be

aligned and considered a whole.

The classic approach to fraud detection is an expert-based approach,

meaning that it builds on the experience, intuition, and business

or domain knowledge of the fraud analyst. Such an expert-based

approach typically involves a manual investigation of a suspicious

case, which may have been signaled, for instance, by a customer

complaining of being charged for transactions he did not do. Such

a disputed transaction may indicate a new fraud mechanism to have

been discovered or developed by fraudsters, and therefore requires

FRAUD: DETECTION, PREVENTION, AND ANALYTICS! 11

a detailed investigation for the organization to understand and sub-

sequently address the new mechanism.

Comprehension of the fraud mechanism or pattern allows extend-

ing the fraud detection and prevention mechanism that is often imple-

mented as a rule base or engine, meaning in the form of a set of If-Then

rules, by adding rules that describe the newly detected fraud mecha-

nism. These rules, together with rules describing previously detected

fraud patterns, are applied to future cases or transactions and trigger

an alert or signal when fraud is or may be committed by use of this

mechanism. A simple, yet possibly very effective, example of a fraud

detection rule in an insurance claim fraud setting goes as follows:

IF:

◾Amount of claim is above threshold OR

◾Severe accident, but no police report OR

◾Severe injury, but no doctor report OR

◾Claimant has multiple versions of the accident OR

◾Multiple receipts submitted

THEN:

◾Flag claim as suspicious AND

◾Alert fraud investigation officer.

Such an expert approach suffers from a number of disadvantages.

Rule bases or engines are typically expensive to build, since they

require advanced manual input by the fraud experts, and often turn

out to be difficult to maintain and manage. Rules have to be kept

up to date and only or mostly trigger real fraudulent cases, since

every signaled case requires human follow-up and investigation.

Therefore, the main challenge concerns keeping the rule base lean

and effective—in other words, deciding when and which rules to add,

remove, update, or merge.

It is important to realize that fraudsters can, for instance by trial

and error, learn the business rules that block or expose them and will

devise inventive workarounds. Since the rules in the rule-based detec-

tion system are based on past experience, new emerging fraud pat-

terns are not automatically flagged or signaled. Fraud is a dynamic

12 FRAUD ANALYTICS

phenomenon, as will be discussed below in more detail, and therefore

needs to be traced continuously. Consequently, a fraud detection and

prevention system also needs to be continuously monitored, improved,

and updated to remain effective.

An expert-based fraud-detection system relies on human expert

input, evaluation, and monitoring, and as such involves a great deal

of labor intense human interventions. An automated approach to

build and maintain a fraud-detection system, requiring less human

involvement, could lead to a more efficient and effective system

for detecting fraud. The next section in this chapter will introduce

several alternative approaches to expert systems that leverage the

massive amounts of data that nowadays can be gathered and pro-

cessed at very low cost, in order to develop, monitor, and update a

high-performing fraud-detection system in a more automated and

efficient manner. These alternative approaches still require and build

on expert knowledge and input, which remains crucial in order to

build an effective system.

EXAMPLE CASE: EXPERT-BASED APPROACH TO

INTERNAL FRAUD DETECTION IN AN INSURANCE

CLAIM-HANDLING PROCESS

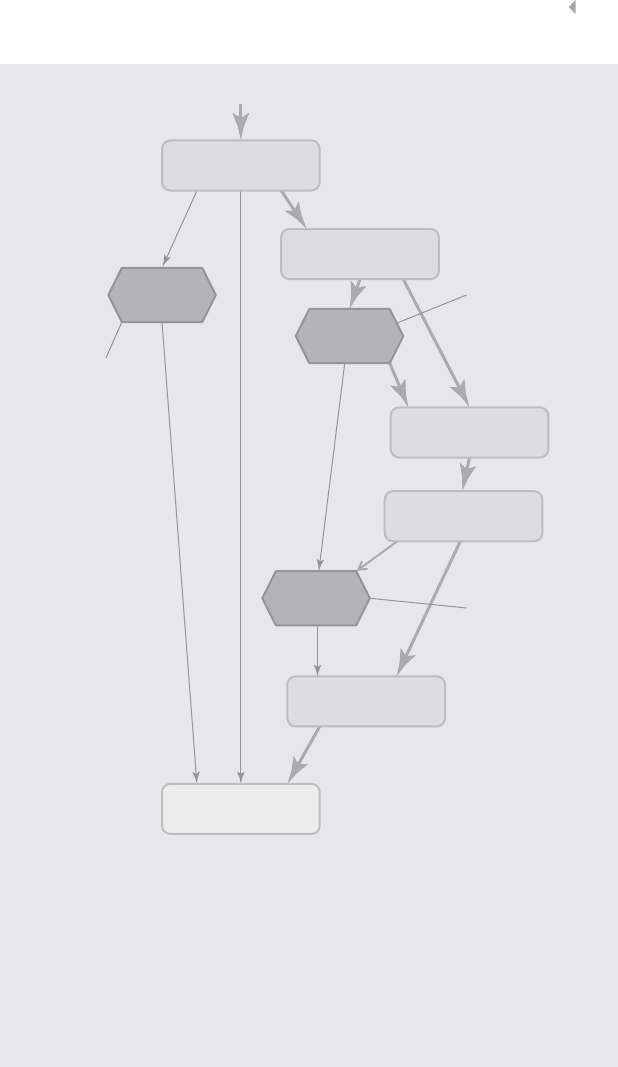

EXAMPLE CASE

An example expert-based detection and prevention system to signal potential

fraud committed by claim handling officers concerns the business process

depicted in Figure 1.2, illustrating the handling of fire incident claims without

any form of bodily injury (including death) (Caron et al. 2013). The process

involves the following types of activities:

◾Administrative activities

◾Evaluation-related activities

◾In-depth assessment by internal and external experts

◾Approval activities

◾Leniency-related activities

◾Fraud investigation activities

FRAUD: DETECTION, PREVENTION, AND ANALYTICS! 13

Additional evaluation

activities

Leniency-related

activities

Approval cycle

Update provision

complete

0.380

Discard provisions

complete

0.660

Compensate complete

0.415

Cluster 37

2 elements

–0.092

Register compensation

agreement complete

0.413

Cluster 38

7 elements

–0.033

Send claim acceptance

letter complete

0.369

Consult Policy complete

0.518

Cluster 33

5 elements

–0.033

Figure 1.2 Fire Incident Claim-Handling Process

A number of harmful process deviations and related risks can be

identified regarding these activities:

◾Forgetting to discard provisions

◾Multiple partial compensations (exceeding limit)

14 FRAUD ANALYTICS

◾Collusion between administrator and experts

◾Lack of approval cycle

◾Suboptimal task allocation

◾Fraud investigation activities

◾Processing rejected claim

◾Forced claim acceptance, absence of a timely primary evaluation

Deviations marked in bold may relate to and therefore indicate fraud. By

adopting business policies as a governance instrument and prescribing

procedures and guidelines, the insurer may reduce the risks involved in

processing the insurance claims. For instance:

Business policy excerpt 1 (customer relationship

management related): If the insured requires immediate assistance (e.g.,

to prevent the development of additional damage), arrangements will be made

for a single partial advanced compensation (maximum x% of expected

covered loss).

◾Potential risk: The expected (covered) loss could be exceeded

through partial advanced compensations.

Business policy excerpt 2 (avoid financial loss): Settlements

need to be approved.

◾Potential risk: Collusion between the drafter of the settlement and

the insured

Business policy excerpt 3 (avoid financial loss): The proposal of

a settlement and its approval must be performed by different actors.

◾Potential risk: A person might hold both the team-leader and the

expert role in the information system.

Business policy excerpt 4 (avoid financial loss): After approval of

the decision (settlement or claim rejection) no changes may occur.

◾Potential risk: The modifier and the insured might collude.

◾Potential risk: A rejected claim could undergo further processing.

FRAUD: DETECTION, PREVENTION, AND ANALYTICS! 15

Since detecting fraud based on specified business rules requires prior

knowledge of the fraud scheme, the existence of fraud issues will be the direct

result of either:

◾An inadequate internal control system (controls fail to prevent

fraud); or

◾Risks accepted by the management (no preventive or corrective

controls are in place).

Some examples of fraud-detection rules that can be derived from these

business policy excerpts and process deviations, and that may be added to the

fraud-detection rule engine are as follows:

Business policy excerpt 1:

◾IF multiple advanced payments for one claim, THEN suspicious

case.

Business policy excerpt 2:

◾IF settlement was not approved before it was paid, THEN suspi-

cious case.

Business policy excerpt 3:

◾IF settlement is proposed AND approved by the same person, THEN

suspicious case.

Business policy excerpt 4:

◾IF settlement is approved AND changed afterward, THEN suspi-

cious case.

◾IF claim is rejected AND processed afterward (e.g., look for a set-

tlement proposal, payment,…activity), THEN suspicious case.

BIG DATA FOR FRAUD DETECTION

When fraudulent activities have been detected and confirmed to effec-

tively concern fraud, two types of measures are typically taken:

1. Corrective measures, that aim to resolve the fraud and correct the

wrongful consequences—for instance by means of pursuing

16 FRAUD ANALYTICS

restitution or compensation for the incurred losses. These cor-

rective measures might also include actions to retrospectively

detect and subsequently address similar fraud cases that made

use of the same mechanism or loopholes in the fraud detection

and prevention system the organization has in place.

2. Preventive measures, which may both include actions that aim at

preventing future fraud by the caught fraudster (e.g., by ter-

minating a contractual agreement with a customer, as well as

actions that aim at preventing fraud of the same type by other

individuals). When an expert-based approach is adopted, an

example preventive measure is to extend the rule engine by

incorporating additional rules that allow detecting and prevent-

ing the uncovered fraud mechanism to be applied in the future.

A fraud case must be investigated thoroughly so the underlying

mechanism can be unraveled, extending the available expert

knowledge and allowing it to prevent the fraud mechanism to

be used again in the future by making the organization more

robust and less vulnerable to fraud by adjusting the detection

and prevention system.

Typically, the sooner corrective measures are taken and therefore

the sooner fraud is detected, the more effective such measures may

be and the more losses can be avoided or recompensed. On the other

hand, fraud becomes easier to detect the more time has passed, for a

number of particular reasons.

When a fraud mechanism or path exists—meaning a loophole in the

detection and prevention system of an organization—the number of

times this path will be followed (i.e., the fraud mechanism used) grows

in time and therefore as well the number of occurrences of this partic-

ular type of fraud. The more a fraud path is taken the more apparent it

becomes and typically, in fact statistically, the easier to detect. The num-

ber of occurrences of a particular type of fraud can be expected to grow

since many fraudsters appear to be repeat offenders. As the expression

goes, “Once a thief, always a thief.” Moreover, a fraud mechanism may

well be discovered by several individuals or the knowledge shared

between fraudsters. As will be shown in Chapter 5 on social network

analytics for fraud detection, certainly some types of fraud tend to

FRAUD: DETECTION, PREVENTION, AND ANALYTICS! 17

spread virally and display what are called social network effects,

indicating that fraudsters share their knowledge on how to commit

fraud. This effect, too, leads to a growing number of occurrences and,

therefore, a higher risk or chance, depending on one’s perspective, of

detection.

Once a case of a particular type of fraud has been revealed, this will

lead to the exposition of similar fraud cases that were committed in the

past and made use of the same mechanism. Typically, a retrospective

screening is performed to assess the size or impact of the newly detected

type of fraud, as well as to resolve (by means of corrective measures,

cf. supra) as much as possible fraud cases. As such, fraud becomes

easier to detect the more time has passed, since more similar fraud

cases will occur in time, increasing the probability that the particular

fraud type will be uncovered, as well as because fraudsters committing

repeated fraud will increase their individual risk of being exposed. The

individual risk will increase the more fraud a fraudster commits for the

same basic reason: The chances of getting noticed get larger.

A final reason why fraud becomes easier to detect the more time

has passed is because better detection techniques are being developed,

are getting readily available, and are being implemented and applied by

a growing amount of organizations. An important driver for improve-

ments with respect to detection techniques is growing data availability.

The informatization and digitalization of almost every aspect of society

and daily life leads to an abundance of available data. This so-called big

data can be explored and exploited for a range of purposes including

fraud detection (Baesens 2014), at a very low cost.

DATA-DRIVEN FRAUD DETECTION

Although classic, expert-based fraud-detection approaches as discussed

before are still in widespread use and definitely represent a good start-

ing point and complementary tool for an organization to develop an

effective fraud-detection and prevention system, a shift is taking place

toward data-driven or statistically based fraud-detection methodolo-

gies for three apparent reasons:

1. Precision. Statistically based fraud-detection methodologies offer

an increased detection power compared to classic approaches.

18 FRAUD ANALYTICS

By processing massive volumes of information, fraud patterns

may be uncovered that are not sufficiently apparent to the

human eye. It is important to notice that the improved power

of data-driven approaches over human processing can be

observed in similar applications such as credit scoring or cus-

tomer churn prediction. Most organizations only have a limited

capacity to have cases checked by an inspector to confirm

whether or not the case effectively concerns fraud. The goal

of a fraud-detection system may be to make the most optimal

use of the limited available inspection capacity, or in other

words to maximize the fraction of fraudulent cases among

the inspected cases (and possibly in addition, the detected

amount of fraud). A system with higher precision, as delivered

by data-based methodologies, directly translates in a higher

fraction of fraudulent inspected cases.

2. Operational efficiency. In certain settings, there is an increasing

amount of cases to be analyzed, requiring an automated pro-

cess as offered by data-driven fraud-detection methodologies.

Moreover, in several applications, operational requirements

exist, imposing time constraints on the processing of a case.

For instance, when evaluating a transaction with a credit

card, an almost immediate decision is required with respect to

approve or block the transaction because of suspicion of fraud.

Another example concerns fraud detection for customs in a

harbor, where a decision has to be made within a confined

time window whether to let a container pass and be shipped

inland, or whether to further inspect it, possibly causing delays.

Automated data-driven approaches offer such functionality and

are able to comply with stringent operational requirements.

3. Cost efficiency. As already mentioned in the previous section,

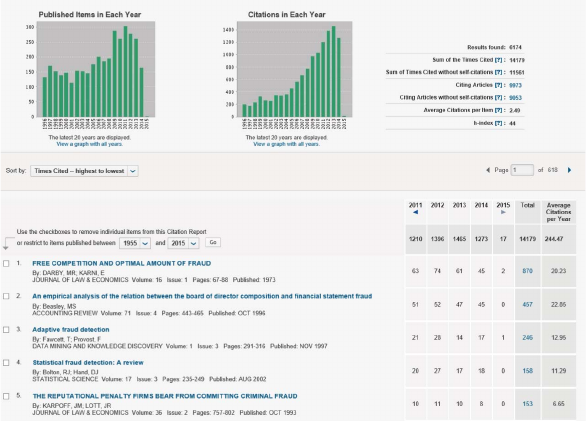

developing and maintaining an effective and lean expert-based

fraud-detection system is both challenging and labor intensive.

A more automated and, as such, more efficient approach to

develop and maintain a fraud-detection system, as offered

by data-driven methodologies, is preferred. Chapters 6 and

7 discuss the cost efficiency and return on investment of

data-driven fraud-detection models.

FRAUD: DETECTION, PREVENTION, AND ANALYTICS! 19

An additional driver for the development of improved fraud-

detection technologies concerns the growing amount of interest that

fraud detection is attracting from the general public, the media, gov-

ernments, and enterprises. This increasing awareness and attention

for fraud is likely due to its large negative social as well as financial

impact, and leads to growing investments and research into the

matter, both from academia, industry, and government.

Although fraud-detection approaches have gained significant

power over the past years by adopting potent statistically based

methodologies and by analyzing massive amounts of data in order

to discover fraud patterns and mechanisms, still fraud remains hard

to detect. It appears the Pareto principle holds with respect to the

required effort and difficulty of detecting fraud: It appears the prin-

ciple of decreasing returns holds with respect to the required effort

and so forth. In order to explain the hardness and complexity of

the problem, it is important to acknowledge the fact that fraud is a

dynamic phenomenon, meaning that its nature changes in time. Not

only fraud-detection mechanisms evolve, but also fraudsters adapt

their approaches and are inventive in finding more refined and less

apparent ways to commit fraud without being exposed. Fraudsters

probe fraud-detection and prevention systems to understand their

functioning and to discover their weaknesses, allowing them to adapt

their methods and strategies.

FRAUD-DETECTION TECHNIQUES

Indeed, fraudsters develop advanced strategies to cleverly cover their

tracks in order to avoid being uncovered. Fraudsters tend to try and

blend in as much as possible into the surroundings. Such an approach