Core API Training User Guide Destop Full

User Manual: Pdf

Open the PDF directly: View PDF ![]() .

.

Page Count: 106 [warning: Documents this large are best viewed by clicking the View PDF Link!]

Version: 1.6

Last Updated: 8/30/2016

BLOOMBERG OPEN API – CORE DEVELOPER GUIDE

©2016 BLOOMBERG L.P. ALL RIGHTS RESERVED 2

RELATED DOCUMENTS

DOCUMENT NAME

Core User Guide

Enterprise User Guide

Enterprise Developer Guide

Publishing User Guide

Publishing Developer Guide

Reference Guide — Bloomberg Services and Schemas

All materials including all software, equipment and documentation made available by Bloomberg are for informational purposes only. Bloomberg and its

affiliates make no guarantee as to the adequacy, correctness or completeness of, and do not make any representation or warranty (whether express or

implied) or accept any liability with respect to, these materials. No right, title or interest is granted in or to these materials and you agree at all times to

treat these materials in a confidential manner. All materials and services provided to you by Bloomberg are governed by the terms of any applicable

Bloomberg Agreement(s).

BLOOMBERG OPEN API – CORE DEVELOPER GUIDE

©2016 BLOOMBERG L.P. ALL RIGHTS RESERVED 3

Contents

Contents

Contents .................................................................................................................................................................................. 3

1. About This Guide............................................................................................................................................................. 6

1.1. Overview ................................................................................................................................................................. 6

1.1.1. API Features ................................................................................................................................................... 6

1.1.2. Bloomberg Product Features .......................................................................................................................... 7

2. Subscription Overview .................................................................................................................................................... 9

2.1. Subscription Life Cycle ............................................................................................................................................ 9

2.2. Starting a Subscription .......................................................................................................................................... 10

2.3. Building a Subscription .......................................................................................................................................... 13

2.4. Example of Building a Subscription....................................................................................................................... 13

2.5. Subscription Method ............................................................................................................................................. 15

2.6. Subscription Status Messages .............................................................................................................................. 15

2.7. Subscription Data Messages ................................................................................................................................ 18

2.8. Subscription Errors/Exceptions ............................................................................................................................. 21

2.9. Modifying an Existing Subscription ....................................................................................................................... 22

2.10. Stopping a Subscription ........................................................................................................................................ 23

2.11. Overlapping Subscriptions .................................................................................................................................... 23

2.12. Receiving Data from a Subscription ...................................................................................................................... 24

2.13. Snapshot Requests for Subscriptions ................................................................................................................... 25

3. Subscription Classes ..................................................................................................................................................... 25

3.1. SessionOptions Class ........................................................................................................................................... 26

3.2. Session Class ........................................................................................................................................................ 26

3.3. Establishing a Connection ..................................................................................................................................... 27

4. Data Requests ............................................................................................................................................................... 29

5. Bloomberg Services ...................................................................................................................................................... 30

5.1. Service Schemas .................................................................................................................................................. 30

5.2. Accessing a Service .............................................................................................................................................. 31

5.3. Market Data Service .............................................................................................................................................. 32

5.4. Reference Data Service ........................................................................................................................................ 34

5.4.1. Requesting Reference Data .......................................................................................................................... 34

5.4.2. Handling Reference Data Messages ............................................................................................................ 35

5.4.3. Handling Reference Data (Bulk) Messages .................................................................................................. 37

5.5. Source Reference Service .................................................................................................................................... 38

5.6. Custom VWAP Service ......................................................................................................................................... 40

5.7. Market Depth Data Service ................................................................................................................................... 40

BLOOMBERG OPEN API – CORE DEVELOPER GUIDE

©2016 BLOOMBERG L.P. ALL RIGHTS RESERVED 4

5.8. Market Bar Service ................................................................................................................................................ 41

5.9. Market List (Mktlist) Service .................................................................................................................................. 42

5.10. API Field Service (APIflds) .................................................................................................................................... 45

5.11. API Field Service — Field List ............................................................................................................................... 45

5.12. API Field Service — Field Information .................................................................................................................. 46

5.13. API Field Service — Field Search ......................................................................................................................... 47

5.14. API Field Service — Categorized Field Search .................................................................................................... 48

5.15. Instruments ............................................................................................................................................................ 49

5.16. Page Data ............................................................................................................................................................. 49

5.17. Technical Analysis................................................................................................................................................. 50

5.18. Historical End-of-Day Study Request.................................................................................................................... 51

5.19. Intraday Bar Study Request .................................................................................................................................. 53

5.20. Real-time Study Request ...................................................................................................................................... 55

6. Best Practices ............................................................................................................................................................... 56

6.1. Name Class ........................................................................................................................................................... 56

6.2. Session Object ...................................................................................................................................................... 56

6.3. EventQueue .......................................................................................................................................................... 56

6.4. Getting Values from Elements .............................................................................................................................. 57

6.5. MaxEventQueueSize ............................................................................................................................................ 57

6.6. Message Iterator ................................................................................................................................................... 58

6.7. CorrelationID Object .............................................................................................................................................. 58

6.8. DateTime ............................................................................................................................................................... 58

6.9. If Chains ................................................................................................................................................................ 59

6.10. Invariants: Un-Optimized ....................................................................................................................................... 60

6.10.1. Invariants: Corrected ..................................................................................................................................... 61

7. Event Handling .............................................................................................................................................................. 62

7.1. Asynchronous vs. Synchronous ............................................................................................................................ 63

7.2. Multiple Sessions .................................................................................................................................................. 63

8. Message Types ............................................................................................................................................................. 64

9. Error Codes ................................................................................................................................................................... 65

9.1. Common Error Message Codes ............................................................................................................................ 65

9.2. Message Return Codes (v3 API ONLY)................................................................................................................ 65

9.2.1. General .......................................................................................................................................................... 65

9.2.2. API Error Code number ................................................................................................................................. 67

9.2.3. //BLP/APIAUTH ............................................................................................................................................. 67

9.2.4. //BLP/MKTDATA and //BLP/MKTVWAP ....................................................................................................... 69

9.2.5. //BLP/REFDATA ............................................................................................................................................ 70

10. Event Types .............................................................................................................................................................. 72

BLOOMBERG OPEN API – CORE DEVELOPER GUIDE

©2016 BLOOMBERG L.P. ALL RIGHTS RESERVED 5

10.1. Message Types ..................................................................................................................................................... 72

11. Handling Reference Errors/Exceptions ..................................................................................................................... 74

12. SDK for BLPAPI ........................................................................................................................................................ 78

13. Request/Response .................................................................................................................................................... 80

13.1. Requesting Historical Data .................................................................................................................................... 80

13.2. Handling Historical Data Messages ...................................................................................................................... 81

13.3. Requesting Intraday Bar Data ............................................................................................................................... 82

13.4. Handling Intraday Bar Data Messages ................................................................................................................. 83

13.5. Requesting Intraday Tick Data .............................................................................................................................. 85

13.6. Handling Intraday Tick Data Messages ................................................................................................................ 87

13.7. sendRequest Method ............................................................................................................................................ 88

14. Multi-Threading and the API ..................................................................................................................................... 89

14.1. Combining Reference and Subscription Data ....................................................................................................... 89

15. Converting from Excel Formulas (TransExcelFormToCOM) .................................................................................... 90

15.1. BDP(): Streaming Data (Real-Time or Delayed). .................................................................................................. 90

15.2. BDP(): Reference Data (Static) ............................................................................................................................. 90

15.3. BDS(): Bulk Data (Static) ...................................................................................................................................... 91

15.4. BDH(): Historical “End-of-Day” Data (Static) ......................................................................................................... 92

15.5. BDH(): Intraday Ticks (Static) ............................................................................................................................... 95

15.6. BDH()/BRB(): Intraday Bar Data (Static/Subscription) .......................................................................................... 98

15.7. BEQS(): Bloomberg Equity Screening ................................................................................................................ 101

16. Troubleshooting....................................................................................................................................................... 104

16.1. Troubleshooting Scenarios ................................................................................................................................. 105

16.2. BLP API Logging ................................................................................................................................................. 105

BLOOMBERG OPEN API – CORE DEVELOPER GUIDE

©2016 BLOOMBERG L.P. ALL RIGHTS RESERVED 6

About This Guide

1.

The Core API “Developer’s Guide” is the starting point for learning the core usage of the Bloomberg L.P. API libraries.

This knowledge will form the basis for developing applications for the Desktop API, Server API, B-PIPE and Platform

products.

If the goal is to develop applications for one of the Bloomberg Enterprise products (including Server API, B-PIPE or

Platform), then, upon completion of this core guide, the user will want to continue with the Enterprise User and

Developer’s guides.

1.1. OVERVIEW

All API products share the same programming interface and behave almost identically. The main difference is that

customer applications using the enterprise API products (which exclude the Desktop API) have some additional

responsibilities, such as performing authentication, authorization and permissioning before distributing/receiving data.

1.1.1. API FEATURES

LANGUAGES

The Bloomberg v3 API is available in many popular programming and scripting languages, including Java, C/C++, .NET,

Perl and Python. Bloomberg also provides a COM Data Control interface for development within Excel. The Java, .NET

and C++ object models are identical, while the C interface provides a C-style version of the object model.

The Java, C and .NET API are written completely native, with .NET being written natively in C#. The C++, Python, Perl

and COM Data Control interfaces are built on top of the C API libraries. Applications can be effortlessly ported among

these languages as application needs change.

LIGHTWEIGHT INTERFACES

The API v3 programming interface implementations are very lightweight. The design makes the process of receiving data

from Bloomberg and delivering it to applications as efficient as possible. It is possible to get maximum performance from

the available versions of the interface.

EXTENSIBLE SERVICE-ORIENTED DATA MODEL

The API generically understands the concepts of subscription and request-response services. The subscribe and request

methods allow the sending of requests to different data services with potentially different or overlapping data dictionaries

and different response schemas at runtime. Thus the Bloomberg API can support additional services without additions to

the interface—simplifying writing applications that can adapt to changes in services or entirely new services.

SUMMARY EVENTS

When subscribing to market data for a security, the API performs two actions:

1. Retrieves and delivers a summary of the current state of the security—made up of elements known as “fields.”

2. Streams all market data updates as they occur and continues to do so until subscription cancellation.

REQUEST SIZE RESTRICTIONS

Limitations exist on the number of fields for reference and historical data request: 400 fields for reference data request

and 25 fields for historical data request. There is also a limit on the number of securities enforced by the Session’s

MaxPendingRequests. API will split the securities in the request into groups of 10 securities and fields into groups of 128

fields. Therefore, depending of the number of securities and fields provided, the number of requests many exceed the

default 1,024 MaxPendingRequests limit.

CANONICAL DATA FORMAT

Each data field returned to an application via the API is accompanied by an in-memory dictionary element that indicates

the data type (e.g., double) and provides a description of the field; the data is self-describing. Data elements may be

simple or complex, e.g., bulk fields. All data is represented in the same canonical form.

BLOOMBERG OPEN API – CORE DEVELOPER GUIDE

©2016 BLOOMBERG L.P. ALL RIGHTS RESERVED 7

THREAD-SAFETY

The interface is thread safe and thread aware, giving applications the ability to utilize multiple processors efficiently.

32- AND 64-BIT PROGRAMMING SUPPORT

The Java and .NET API work on both 32- and 64-bit platforms, while the C/C++ API libraries are currently available in

both 32- and 64-bit versions.

PURE JAVA IMPLEMENTATION

The Java API is implemented entirely in Java. Bloomberg did not use JNI to wrap either the existing C library or the new

C++ library.

FULLY INTROSPECTIVE DATA MODEL

An application can discover a service and its attributes at runtime.

BANDWIDTH OPTIMIZED

The Bloomberg API automatically breaks large results into smaller chunks and can provide conflated streaming data to

improve the bandwidth usage and the latency of applications.

THE THREE PARADIGMS

Before exploring the details for requesting and receiving data, the following three paradigms used by the Bloomberg API

are described:

Request/Response

Subscription

Publishing

1.1.2. BLOOMBERG PRODUCT FEATURES

FIELD-LEVEL SUBSCRIPTIONS

Updates can be requested for only the fields of interest to the application rather than receiving all trade and quote fields

when a subscription is established. This reduces the overhead of processing unwanted data within both the API and the

application and also reduces network bandwidth consumption between Bloomberg and its customers. Depending on a

user’s product, additional related fields may be included for API efficiencies, but only the fields requested should be relied

upon.

INTERVAL-BASED SUBSCRIPTIONS

Many users of API data are interested in subscribing to large sets of streaming data, but only need summaries of each

requested security to be delivered at periodic intervals.

24X7 ACCESS TO BLOOMBERG DATA

Provides developers with 24x7 programmatic access to data from the Bloomberg Data Center to be used in customer

applications.

SECURITY LOOKUP FUNCTIONALITY

Perform a security, curve and government lookup request similar to what can be accomplished using {SECF <GO>}.

API DATA DICTIONARY ACCESS

Query the API Data Dictionary of available fields, providing functionality similar to what can be accomplished using {FLDS

<GO>}.

BLOOMBERG OPEN API – CORE DEVELOPER GUIDE

©2016 BLOOMBERG L.P. ALL RIGHTS RESERVED 8

COMMON API CONCEPTS

The following concepts must be understood before successfully requesting or subscribing to Bloomberg financial data via

the API:

Securities

Fields/Overrides (with interactive demo)

Historical Dates

THE THREE PARADIGMS

Request/Response

Data is requested by issuing a Request and is returned in a Message sequence consisting of zero or more

PARTIAL_RESPONSE Message Events followed by exactly one RESPONSE Message Event. The final RESPONSE

indicates that the Request has been completed. In general, applications using this paradigm will perform extra processing

after receiving the final RESPONSE from a Request, such as performing calculations, updating a display with all data at

one time stored in a cache, etc.

Subscription

A Subscription is created that results in a stream of updates being delivered in SUBSCRIPTION_DATA Message Events

until the Subscription is explicitly cancelled (unsubscribed) by the application. By default, all data is returned. It is possible

to set an interval where if any of the fields have changed since the last interval, a new Message is sent containing the

fields that changed. Processing of interval data is the same as processing non-interval updates.

Publishing

The Bloomberg API allows customer applications to publish page-based and record-based data as well as consume it.

Customer data can be published for distribution within the customer’s enterprise, contributed to the Bloomberg

infrastructure, distributed to others or used for warehousing. This is done via the suitable Bloomberg Platform product.

Publishing applications might simply broadcast data or they can be “interactive,” responding to feedback from the

infrastructure about the currently active subscriptions of data consumers. Contributions and local publishing/subscribing

via the Bloomberg Platform are outside the scope of this course and will be discussed in their own course.

In the case of the first two paradigms, the service usually defines which paradigm is used to access it. For example, the

streaming real-time market data service (//blp/mktdata) uses the Subscription paradigm, whereas the reference data

service (//blp/refdata) uses the Request/Response paradigm.

Note: Applications that make heavy use of real-time market data should use the streaming real-time market data

service. However, real-time information is available through the reference data service requests, which include the

current value in the response.

BLOOMBERG OPEN API – CORE DEVELOPER GUIDE

©2016 BLOOMBERG L.P. ALL RIGHTS RESERVED 9

Subscription Overview

2.

Subscriptions are ideal for data that changes frequently and/or at unpredictable intervals. Instead of repeatedly polling for

the current value, the application gets the latest value as soon as it is available without spending time and bandwidth if

there have been no changes. This module contains more details on how to start, modify and stop subscriptions as well as

what to expect as the result of a subscription and how to handle those results.

Currently, the subscription-based Bloomberg API core services are market data (//blp/mktdata), market bar (//blp/mktbar)

and Custom VWAP (//blp/mktvwap). Some subscription-based services are only available for B-PIPE users, such as

market depth, market list and source reference data. In the future, the Bloomberg API may support delivering information

other than market data through a subscription service.

This section offers a demonstration of how to subscribe to streaming data and handle its data responses.

Following are the basic steps to subscribe to market data:

1. Establish a connection to the product’s communication server using the Session.Start method.

2. Open the “//blp/mktdata” service using the Session.OpenService method.

3. Build the subscription. For C/C++ API or Java API: Create a SubscriptionList object, which is a list of subscriptions

used when subscribing and unsubscribing. Using its add method, add one security, along with one or more fields,

desired options (e.g., Interval, Delayed) and a correlation identifier. For .NET API: Declare and instantiate a Generic

List variable of Subscriptions and then add a new Subscription object to it for each subscription.

4. Submit the SubscriptionList or Generic List variable using the Session.subscribe method.

5. Handle the data and status responses, either synchronously or asynchronously, which are then returned as Events.

An Event containing data will be identified by an Event type of SUBSCRIPTION_DATA, while a status Message will

be of type SUBSCRIPTION_STATUS.

2.1. SUBSCRIPTION LIFE CYCLE

The life cycle of a subscription has several key points:

Startup: Subscriptions are started by the subscribe method of Session. An Event object is generated to report the

successful creation of any subscriptions and separate Events for each failure, if any.

Data Delivery: Data is delivered in Event objects of type SUBSCRIPTION_DATA. Each Event has one or more

Messages and each Message object has one or more correlation IDs to identify the associated subscriptions. Since

each Message object may contain more data than requested in any individual subscription (with the exception of B-

PIPE customers, who have had field filtering enabled and will, therefore, only receive the fields they subscribed), the

code managing each subscription must be prepared to extract its data of interest from the Message object. Note:

Customer applications must not rely on the delivery of data that was not explicitly requested in the subscription.

Modification: A list of subscriptions (each identified by its correlation ID) can be modified by the resubscribe method

of the Session.

Cancellation: Subscriptions (each identified by its correlation ID) can be cancelled by the unsubscribe method of the

Session.

Failure: A subscription failure (e.g., a server-side failure) is indicated by an Event of type SUBSCRIPTION_STATUS

containing a Message to describe the problem.

BLOOMBERG OPEN API – CORE DEVELOPER GUIDE

©2016 BLOOMBERG L.P. ALL RIGHTS RESERVED 10

2.2. STARTING A SUBSCRIPTION

There are four parts to creating a subscription; however, several have default values:

The service name (for example, “//blp/mktdata”). If users do not specify the service name, the

defaultSubscriptionService of the SessionOptions object is used.

The topic. In the case of “//blp/mktdata,” the topic value consists of an optional symbology identifier followed by

an instrument identifier. For example, “/cusip/ 097023105” and “/sedol1/2108601” include the symbology

identifier, whereas “IBM US Equity” omits the symbology identifier. If users do not specify the symbology identifier,

then the defaultTopicPrefix of the SessionOptions object is used.

Note: The topic’s form may be different for different subscription services.

The options. These are qualifiers that can affect the content delivered. Examples in “//blp/mktdata” include

specifying an interval for conflated data.

The correlation ID. Data for each subscription is tagged with a correlation ID (represented as a CorrelationID object)

that must be unique to the Session. The customer application can specify that value when the subscription is created.

If the customer application does not specify a correlation ID, the Bloomberg infrastructure will supply a suitable value;

however, in practice, the internally generated correlation ID is rarely used. Most customer applications assign

meaningful correlation IDs that allow the mapping of incoming data to the originating request or subscription.

A user can represent any subscription as a single string that includes the service name, topic and options. For example:

“//blp/mktdata/cusip/097023105?fields=LAST_PRICE,LAST_TRADE_ACTUAL” represents a subscription

using the market data service to an instrument (BA) specified by CUSIP where any changes to the fields

LAST_PRICE or LAST_TRADE_ACTUAL from the Bloomberg data model should generate an update.

“IBM US Equity?fields=BID,ASK&interval=2” represents a subscription using the market data service to an

instrument (IBM) specified by Bloomberg Ticker where any changes to the fields BID or ASK from the Bloomberg data

model should generate an update subject to conflation restriction of at least two seconds between updates. In this

case, the assumption is that the Session has a defaultSubscriptionService of “//blp/mktdata” and a

defaultTopicPrefix of “ticker/”.

The Bloomberg API provides methods that accept the subscription specification as a single string as well as methods that

specify the different elements of the subscription as separate parameters. Subscriptions are typically manipulated in

groups, so the Bloomberg API provides methods that operate on a list of subscriptions. This example shows subscription

creation by several of these methods.

BLOOMBERG OPEN API – CORE DEVELOPER GUIDE

©2016 BLOOMBERG L.P. ALL RIGHTS RESERVED 11

……

SubscriptionList subscriptions = new

SubscriptionList(); CorrelationID subscriptionID_IBM =

new CorrelationId(10); subscriptions.add(new

Subscription("IBM US Equity",

"LAST_TRADE",

subscriptionID_IBM)));

subscriptions.add(new Subscription("/ticker/GOOG US Equity",

"BID,ASK,LAST_PRICE",

new CorrelationID(20)));

subscriptions.add(new Subscription("MSFT US Equity",

"LAST_PRICE",

"interval=.5",

new CorrelationID(30)));

subscriptions.add(new Subscription(

"/cusip/097023105?fields=LAST_PRICE&interval=5.0", //BA US

Equity new CorrelationID(40)));

session.subscribe(subscriptions);

………

NOTE: SubscriptionList in C# is simply an alias to

System.Collections.Generic.List<Bloomberglp.Blpapi.Subscription>, created with:

using SubscriptionList =

System.Collections.Generic.List<Bloomberglp.Blpapi.Subscripti

on>; SubscriptionList sl = new SubscriptionList();

sl.Add(new Subscription("4444 US Equity"));

Subscribing to this list of subscriptions returns an Event of type SUBSCRIPTION_STATUS consisting of a Message

object of type SubscriptionStarted for each CorrelationID. For example, the user-defined “dump” method used in previous

examples shows:

BLOOMBERG OPEN API – CORE DEVELOPER GUIDE

©2016 BLOOMBERG L.P. ALL RIGHTS RESERVED 12

eventType=SUBSCRIPTION_STATUS messageType=SubscriptionStarted

CorrelationID=User: 10 SubscriptionStarted = {

}

messageType=SubscriptionStarted CorrelationID=User: 20 SubscriptionStarted =

{

}

messageType=SubscriptionStarted CorrelationID=User: 30 SubscriptionStarted =

{

}

messageType=SubscriptionStarted CorrelationID=User: 40 SubscriptionStarted =

{

}

In case of an error, an Event is available to report the subscriptions that failed. For example, if the specification for MSFT

(CorrelationID 30) above was mistyped (MSFTT),that would result in the following Event:

eventType=SUBSCRIPTION_STATUS

messageType=SubscriptionFailure

CorrelationID=User: 30

SubscriptionFailure = {

reason = {

source =

BBDB@p111

errorCode = 2

category =

BAD_SEC

description = Invalid security

}

}

BLOOMBERG OPEN API – CORE DEVELOPER GUIDE

©2016 BLOOMBERG L.P. ALL RIGHTS RESERVED 13

2.3. BUILDING A SUBSCRIPTION

Several typical subscription parts have default values:

• Service Name (e.g., “//blp/mktdata”): If the service name is not specified, the defaultSubscriptionService of the

SessionOptions object is used, which is “//blp/mktdata”.

• Topic: In the case of “//blp/mktdata,” the topic value consists of an optional topic prefix followed by an instrument

identifier. For example, “/cusip/097023105” and “/sedol1/2108601” include the topic prefix, whereas “IBM US

Equity” omits the topic prefix. If the topic prefix is not specified, the defaultTopicPrefix of the SessionOptions object is

used, which is “/ticker” by default. Therefore, if using a ticker, such as IBM, the security string would be “IBM US

Equity,” with the “/ticker” topic prefix is implied. Note: The topic’s form may be different for different subscription

services.

• Fields: API fields define the type of data to retrieve for the specified topic. These are required, comma-delimited and

are prefixed with a question mark immediately following the topic. Make sure that the fields being used are real-time

fields, indicated by white text on {FLDS <GO>} on the Bloomberg Professional® service. Otherwise, an invalid field

error within the response for that security’s subscription will be returned.

• Options: These are optional qualifiers that can affect the content delivered. Examples for

“//blp/mktdata” include specifying an interval for conflated data (i.e., interval=n, where n is measured in seconds) or

indicating receipt of delayed data, which is accomplished via the “delayed” option. They are prefixed by an ampersand

(&). If using the “//blp/mktvwap” service, specify one or more override field/value pairings. If using the Desktop API,

the “useGMT” option can be used—that will ensure that all time data being returned is converted to GMT/UTC. This

option is available only for the Desktop API because the streaming data is initially being adjusted based on the

Bloomberg Professional service’s {TZDF <GO>} settings. All other products will default to receiving time-specific

streaming data in GMT/UTC (unadjusted).

• Correlation ID (optional): Data for each subscription is tagged with a correlation ID, represented as a CorrelationID

object, that must be unique to the session. The customer application can specify that value when the subscription is

created. If the customer application does not specify a correlation ID, the Bloomberg infrastructure will supply a

suitable value. In practice, the internally generated correlation ID is rarely used. Most customer applications assign

meaningful correlation IDs that allow the mapping of incoming data to the originating request or subscription.

2.4. EXAMPLE OF BUILDING A SUBSCRIPTION

The Bloomberg API provides class methods that accept the subscription specification as a single string as well as

methods wherein the different elements of the subscription are specified as separate parameters. Subscriptions are

typically manipulated in groups so Bloomberg provides methods that operate on a list of subscriptions. To start with some

sample subscription strings:

“//blp/mktdata/cusip/097023105?fields=LAST_PRICE,LAST_TRADE_ACTUAL”: Represents a subscription

using the market data service for an instrument (Boeing Co.) specified by CUSIP where any changes to the fields

LAST_PRICE or LAST_TRADE_ACTUAL from the Bloomberg data model should generate an update.

“IBM US Equity?fields=BID,ASK&interval=2”: Represents a subscription using the market data service to an

instrument (IBM) specified by a Bloomberg Ticker where any changes to the fields BID or ASK from the Bloomberg data

model should generate an update subject to conflation restriction of at least two seconds between updates. In this case,

based on the assumption that the Session has a defaultSubscriptionService of “//blp/mktdata” and a defaultTopicPrefix of

“ticker/”.

“GOOG US Equity?fields=LAST_PRICE,BID,ASK&delayed”: Represents a delayed subscription using the market

data service to an instrument (GOOG) specified by a Bloomberg Ticker where any changes to the fields LAST_PRICE,

BID or ASK from the Bloomberg data model should generate a delayed update. As in the previous example, based on the

assumption that the Session has a defaultSubscriptionService of “//blp/mktdata” and a defaultTopicPrefix of

“ticker/.”

BLOOMBERG OPEN API – CORE DEVELOPER GUIDE

©2016 BLOOMBERG L.P. ALL RIGHTS RESERVED 14

As an alternative to representing a subscription as a single string that includes the service name, topic, fields and options,

the subscription string can be broken down into separate parameters. In the following example, subscriptions are created

using both methods:

const char *security1 = “IBM US Equity”;

const char *security2 = “/cusip/912828GM6@BGN”;

SubscriptionList subscriptions;

subscriptions.add(security1,

"BID,ASK,LAST_PRICE",

"interval=3",

CorrelationID((char *)security2));

subscriptions.add(security2,

"LAST_PRICE",

"interval=.5",

CorrelationID(10));

subscriptions.add(security1,

"LAST_PRICE",

“delayed”);

CorrelationID(20));

subscriptions.add("/cusip/097023105?fields=LAST_PRICE&interval=5.0",

//BA Equity

CorrelationID(30));

subscriptions.add("//blp/mktdata/isin/US0970231058?fields=LAST_PRICE&in

terval=5.0", //BA Equity

CorrelationID(40));

session.subscribe(subscriptions);

BLOOMBERG OPEN API – CORE DEVELOPER GUIDE

©2016 BLOOMBERG L.P. ALL RIGHTS RESERVED 15

2.5. SUBSCRIPTION METHOD

The Subscribe method is a member of the Session class and is used to submit a list of subscriptions to be filled by the

Bloomberg Data Center along with a user’s Identity object if required.

Add one or more subscriptions to the subscription list utilizing any of the ADD method overloads of the SubscriptionList

class. The SubscriptionList object is then submitted via the Subscribe method. The two method overload definitions are:

void blpapi::Session::subscribe(const SubscriptionList &subList,

const char *requestLabel=0, int requestLabelLen=0)

void blpapi::Session::subscribe(const SubscriptionList &subList, const Identity &ID,

const char *requestLabel=0, int requestLabelLen=0)

Begin subscriptions for each entry in the specified SubscriptionList using the specified identity for authorization. Optional

requestLabel and requestLabelLen define a string that will be recorded along with any diagnostics for this operation.

There must be at least requestLabelLen printable characters at the location requestLabel. A SUBSCRIPTION_STATUS

Event will be generated for each entry in the SubscriptionList.

Several supporting methods are available to resend, modify and cancel an existing subscription.

.NET API Developers

Unlike when working with the Java and C++ API interfaces—instead of using the subscriptionList object, instantiate a

Generic List variable of Subscriptions and then add a new Subscription object to it for each subscription.

2.6. SUBSCRIPTION STATUS MESSAGES

Irrespective of handling Messages synchronously or asynchronously, the status subscription Messages that are returned

are captured in the same manner. This is done by handling the Event object’s SESSION_STATUS, SERVICE_STATUS,

SUBSCRIPTION_STATUS, and AUTHORIZATION_STATUS messages.

A SUBSCRIPTION_STATUS Event type, for instance, may contain a SubscriptionStarted or SubscriptionFailure Message

type.

Notes:

When using an asynchronous Session, the application must be aware that because the callbacks are generated from

another thread, they may be processed before the call that generates them has returned. For example, the

SESSION_STATUS Event generated by a startAsync may be processed before startAsync has returned (even though

startAsync itself will not block).

Subscription data Messages are also handled in this same event handler. They were omitted in the code for simplicity.

Following is the skeleton status code placed within the Event handler. In this case, the messages are handled

asynchronously inside the Session’s processEvent handler:

<C++>

public void processEvent(Event event, Session session) {

switch (event.eventType())

{

case Event::SERVICE_STATUS: {

BLOOMBERG OPEN API – CORE DEVELOPER GUIDE

©2016 BLOOMBERG L.P. ALL RIGHTS RESERVED 16

// If service opened successfully, send request.

break;

}

case Event::SUBSCRIPTION_STATUS: {

// If subscription fails, then perform appropriate action

break;

}

case Event::AUTHORIZATION_REQUEST:

// If authorization was successful, perform next action.

break;

}

default: {

// Handle unexpected response.

break;

}

}

}

Following is the processing of the Event returned for starting the Session. If successful, the code will attempt to open the

needed service. Since the openServiceAsync method generates an exception on failure, but processEvent is not allowed

to omit an exception, that call must be surrounded by a try-catch block. In event of failure, the example chooses to

terminate the process.

<C++>

Case Event::SESSION_STATUS: {

MessageIterator iter = event.messageIterator();

while (iter.hasNext()) {

Message message = iter.next();

if (message.messageType().equals("SessionStarted")) {

try {

session.openServiceAsync("//blp/mktdata",

CorrelationID(99));

} catch (Exception &e) {

std::cerr << "Could not open //blp/mktdata for async";

std::exit(-1);

BLOOMBERG OPEN API – CORE DEVELOPER GUIDE

©2016 BLOOMBERG L.P. ALL RIGHTS RESERVED 17

}

} else {

// Handle error.

}

}

break;

}

On receipt of a SERVICE_STATUS type Event, the Messages are searched for one indicating that the openServiceAsync

call was successful. The Message type must be “ServiceOpened” and the correlation ID must match the value assigned

when the request was sent.

If the service was successfully opened, users can create, initialize and send a request. The only difference is that the call

to subscribe must be guarded against the transmission of exceptions—not a concern until now.

<C++>

public void processEvent(Event event, Session session) {

switch (event.eventType())

{

case Event::SERVICE_STATUS: {

// If service opened successfully, send request.

break;

}

case Event::SUBSCRIPTION_STATUS: {

// If subscription fails, then perform appropriate action

break;

}

case Event::AUTHORIZATION_REQUEST:

// If authorization was successful, perform next action.

break;

}

default: {

// Handle unexpected response.

break;

}

}

BLOOMBERG OPEN API – CORE DEVELOPER GUIDE

©2016 BLOOMBERG L.P. ALL RIGHTS RESERVED 18

}

2.7. SUBSCRIPTION DATA MESSAGES

Once a subscription has started, the application will receive updates for the requested data in the form of Messages

contained within Event objects of type SUBSCRIPTION_DATA. Within each Message there is a CorrelationID to identify

the subscription that requested the data.

The “//blp/mktdata” service typically responds with Messages that have more data than was requested for the

subscription. In this example, only updates to the LAST_TRADE field of IBM were requested in the subscription

corresponding to CorrelationID 10. Applications must be prepared to extract the data they need and to discard the rest.

Here is a sample dump of a subscription data Message:

eventType=SUBSCRIPTION_DATA

messageType=MarketDataEvents

CorrelationID=User: 10

MarketDataEvents = {

LAST_PRICE = 212.64

BID = 212.63

ASK = 212.64

MKTDATA_EVENT_TYPE = SUMMARY

MKTDATA_EVENT_SUBTYPE = INITPAINT

IS_DELAYED_STREAM = false

…

In the above output, the Event type is “SUBSCRIPTION_DATA”. This is the Event type handled in the code.

The next step would be taking a deeper look into a subscription-based data event handler. Displayed below is the partial

code sample that handles those particular subscription Messages. The handleOtherEvent function definition has been

removed for brevity.

<C++>

#include <blpapi_correlationid.h>

#include <blpapi_event.h>

#include <blpapi_message.h>

#include <blpapi_request.h>

#include <blpapi_session.h>

#include <blpapi_subscriptionlist.h>

BLOOMBERG OPEN API – CORE DEVELOPER GUIDE

©2016 BLOOMBERG L.P. ALL RIGHTS RESERVED 19

#include <iostream>

using namespace BloombergLP;

using namespace blpapi;

static void handleDataEvent(const Event& event, int updateCount)

{

std::cout << "EventType=" << event.eventType() << std::endl;

std::cout << "updateCount = " << updateCount << std::endl;

MessageIterator iter(event);

while (iter.next()) {

Message message = iter.message();

std::cout << "correlationId = " << message.correlationId() <<

std::endl;

std::cout << "messageType = " << message.messageType() << std::endl;

message.print(std::cout);

}

}

int main(int argc, char **argv)

{

SessionOptions sessionOptions;

sessionOptions.setServerHost("localhost");

sessionOptions.setServerPort(8194);

Session session(sessionOptions);

if (!session.start()) {

std::cerr <<"Failed to start session." << std::endl;

return 1;

}

if (!session.openService("//blp/mktdata")) {

std::cerr <<"Failed to open //blp/mktdata" << std::endl;

return 1;

}

CorrelationId subscriptionId((long long)2);

SubscriptionList subscriptions;

subscriptions.add("AAPL US Equity", "LAST_PRICE", "", subscriptionId);

BLOOMBERG OPEN API – CORE DEVELOPER GUIDE

©2016 BLOOMBERG L.P. ALL RIGHTS RESERVED 20

session.subscribe(subscriptions);

int updateCount = 0;

while (true) {

Event event = session.nextEvent();

switch (event.eventType()) {

case Event::SUBSCRIPTION_DATA:

handleDataEvent(event, updateCount++);

break;

default:

handleOtherEvent(event); // This function, if shown,

// would handle Status messages,

// such as session terminated,

// and so forth

break;

}

}

return 0;

}

In the previous code sample, it is important to observe the following:

The tick data from the subscribe call is being handled in synchronous mode. This is determined by the combination of

the nextEvent call and the fact that no EventHandler is being provided to the Session object when it is being created.

Remember that if nextEvent is called when an EventHandler is provided, then an exception will be thrown.

When the Event type is Event::SUBSCRIPTION_DATA, the handleDataEvent method is then called where a

MessageIterator is created and used to iterate over the Message objects within the Event.

The Event type and counter are then printed and, for each tick update, the correlation ID, Message type and tick data

dump are also sent to std::cout.

The correlation ID in this case will be the value of the subscriptionId variable that was sent with the subscription. In an

application with more than the one security being subscribed, assign a different correlation id to each SubscriptionList

item and use them to map the tick update to the actual subscription that was sent.

Not displayed in this code snippet is the handleOtherEvent method code.

BLOOMBERG OPEN API – CORE DEVELOPER GUIDE

©2016 BLOOMBERG L.P. ALL RIGHTS RESERVED 21

2.8. SUBSCRIPTION ERRORS/EXCEPTIONS

When handling the subscription status Messages, a “reason” Message type denotes a subscription failure. If an

“exceptions” Message type is received, this usually means that at least one field was valid while others were invalid. In the

latter case, check the number of exceptions and determine the invalid field(s) in the handler. Following is sample code

that demonstrates how to handle a “reason” Message type:

<C++>

if (msg.hasElement(“reason”)) {

Element reason = msg.getElement(“reason”);

fprintf(stdout, " %s: %s\n",

reason.getElement(“category”).getValueAsString(),

reason.getElement(“description”).getValueAsString());

}

BLOOMBERG OPEN API – CORE DEVELOPER GUIDE

©2016 BLOOMBERG L.P. ALL RIGHTS RESERVED 22

Following is a sample printout of a “reason” Message that includes the category and description:

SubscriptionFailure = {

reason = {

category = BAD_SEC

description = Invalid security

}

}

Following is sample code that demonstrates how to handle an “exceptions” Message type:

<C++>

if (msg.hasElement(“exceptions”)) {

Element exceptions = msg.getElement(“exceptions”);

for (size_t i = 0; i < exceptions.numValues(); ++i) {

Element exInfo = exceptions.getValueAsElement(i);

Element fieldId = exInfo.getElement(“fieldId”);

Element reason = exInfo.getElement(“reason”);

fprintf(stdout, " %s: %s\n",

fieldId.getValueAsString(),

reason.getElement(“category”).getValueAsString());

}

}

2.9. MODIFYING AN EXISTING SUBSCRIPTION

Once a subscription has been created, the options can be modified (e.g., to change the fields in the subscription) using

the resubscribe method of the Session.

Note: Use of the resubscribe method is generally preferred to cancelling the subscription (unsubscribe

method) and creating a new subscription because updates might be missed between the unsubscribe and

subscribe calls.

The resubscribe method accepts a SubscriptionList. For example, let’s say that users initially subscribed to “IBM US

Equity” along with LAST_PRICE and BID, passing subscriptionID_IBM as the correlation identifier. This would look

like the following:

SubscriptionList subscriptions = new SubscriptionList;

subscriptions.add("IBM US Equity", "LAST_PRICE, BID", subscriptionID_IBM);

session.subscribe(subscriptions);

BLOOMBERG OPEN API – CORE DEVELOPER GUIDE

©2016 BLOOMBERG L.P. ALL RIGHTS RESERVED 23

If users would like to modify that subscription and remove the LAST_PRICE field, retain the BID field and add the ASK

field, the following code fragment can be used:

SubscriptionList subscriptions = new SubscriptionList;

subscriptions.add("IBM US Equity", "BID,ASK", subscriptionID_IBM));

session.resubscribe(subscriptions);

In the above code snippet, BID was included in the initial subscription, so it will continue being subscribed, while

LAST_PRICE will be unsubscribed and ASK will be subscribed. This resubscribed list will simply replace the initial one

made under the same correlation identifier.

Note: The client receives an Event object indicating successful resubscription (or not) before receipt of any

data from that subscription. Also, the behavior is undefined if the topic of the subscription (e.g., the security

itself) is changed.

2.10. STOPPING A SUBSCRIPTION

The Bloomberg API provides a cancel method that will cancel a single subscription (specified by its CorrelationID) and

another method (unsubscribe) that will cancel a list of subscriptions. The following code fragment utilizes the unsubscribe

method to cancel all of the subscriptions created earlier:

SubscriptionList subscriptions = new SubscriptionList;

for (int id = 10; id <= 40; id += 10) {

subscriptions.add("IBM US Equity", new CorrelationID(id));

// Note: The topic string is ignored for unsubscribe.

}

session.unsubscribe(subscriptions);

Note: No Event is generated for unsubscribe.

2.11. OVERLAPPING SUBSCRIPTIONS

An application may make subscriptions that “overlap.”

One form of overlap occurs when a single incoming update may be relevant to more than one subscription. For example,

two or more subscriptions may specify the updates for the same data item. This can easily happen inadvertently by “topic

aliasing”, where one subscription specifies a security by ticker, the other by CUSIP.

Another form of overlap occurs when separate data items intended for different subscriptions on the customer application

process arrive in the same Message object. For example, the Bloomberg infrastructure can improve performance by

packaging two data items within the same Message object. This can occur when a customer’s application process has

made two separate subscriptions, where one includes a request for “IBM US Equity” and “LAST_TRADE,” while the

second includes “IBM US Equity” and “LAST_TRADE”.

The customer application developer can specify how the Bloomberg API should handle overlapping subscriptions. The

behavior is controlled by the allowMultipeCorrelatorsPerMsg option to the SessionOptions object accepted by the Session

constructor.

BLOOMBERG OPEN API – CORE DEVELOPER GUIDE

©2016 BLOOMBERG L.P. ALL RIGHTS RESERVED 24

If the allowMultipeCorrelatorsPerMsg option is false (the default), then a Message object that matches more than one

subscription will be returned multiple times from the MessageIterator, each time with a single, different CorrelationID.

If the allowMultipleCorrelatorsPerMsg object is true, then a Message object that matches more than one subscription will

be returned just once from the MessageIterator. The customer application developer must supply logic to examine the

multiple CorrelationID values (see the numCorrelationIds and correlationIDAt methods of the Message class) and

dispatch the appropriate data to the correct application software.

2.12. RECEIVING DATA FROM A SUBSCRIPTION

Once a subscription has started, the application will receive updates for the requested data in Message objects arriving as

Event objects of type SUBSCRIPTION_DATA. With each Message, there is a CorrelationID to identify the subscription that

requested the data.

The “//blp/mktdata” service typically responds with Messages that have more data than was requested for the

subscription. In this example, only updates to the LAST_TRADE field of IBM were requested in the subscription

corresponding to CorrelationID 10.

Applications must be prepared to extract the data that they need and to discard the rest.

For additional information, refer to “"//blp/mktdata” service.

eventType=SUBSCRIPTION_DATA

messageType=MarketDataEvents

CorrelationID=User: 10

MarketDataEvents = {

IND_BID_FLAG = false

IND_ASK_FLAG = false

IS_DELAYED_STREAM = true

TIME =

14:34:44.000+00:00

VOLUME = 7589155

RT_OPEN_INTEREST = 8339549

RT_PX_CHG_PCT_1D = -0.32

VOLUME_TDY =

7589155

LAST_PRICE =

118.15

HIGH = 118.7

LOW = 116.6

LAST_TRADE =

118.15

OPEN = 117.5

P

R

E

V

_

S

E

S

_

L

A

S

T

_

P

R

I

C

E

PREV_SES_LAST_PRICE = 118.53

EQY_TURNOVER_REALTIME = 8.93027456E8

RT_PX_CHG_NET_1D = -0.379999

OPEN_TDY = 117.5

LAST_PRICE_TDY = 118.15

HIGH_TDY = 118.7

LOW_TDY = 116.6

RT_API_MACHINE = p240

BLOOMBERG OPEN API – CORE DEVELOPER GUIDE

©2016 BLOOMBERG L.P. ALL RIGHTS RESERVED 25

API_MACHINE = p240

RT_PRICING_SOURCE =

US EXCH_CODE_LAST = D

EXCH_CODE_BID = O

SES_START = 09:30:00.000+00:00

SES_END = 16:30:00.000+00:00

}

2.13. SNAPSHOT REQUESTS FOR SUBSCRIPTIONS

For applications that require data on an on-demand basis from subscription services, snapshot functionality is available.In

this type of request, a subscription is created, but messages are sent to the application only when called. This reduces

latency for receiving the latest data when compared to starting a new subscription each time.

A RequestTemplate is used to maintain the subscription for snapshot, which remains open and updating until the template

is canceled as per any subscription. Responses to the snapshot request are the same as a regular subscription with the

event type “Summary”, and the event subtype “INITPAINT”.

NOTE: This is only available in Enterprise Products

CODE EXAMPLE

A code example is available in the C++, Java, and .NET SDK as SnapshotRequestTemplateExample:

<C++>

//Create template for request

std::vector<RequestTemplate> snapshots;

std::string subscriptionString(d_service + d_topic + fieldsStr);

snapshots.push_back(session.createSnapshotRequestTemplate(

subscriptionString.c_str(),

CorrelationId(d_topic),

subscriptionIdentity));

// Request snapshot based on a specific template

session.sendRequest(snapshots[0], correlationID(0));

Subscription Classes 3.

Before delving deeper into the various classes and class members available via the API libraries, it is important to have a

high-level understanding of the typical structure of a Bloomberg API application and how it may differ depending upon the

product used. This module will describe the core components that make up a typical Bloomberg API application.

The two API classes that are responsible for both connecting users application to their Bloomberg API product’s

communication server process and performing the necessary authentication, authorization and data request duties are

SessionOptions and Session, which will be covered next.

BLOOMBERG OPEN API – CORE DEVELOPER GUIDE

©2016 BLOOMBERG L.P. ALL RIGHTS RESERVED 26

3.1. SESSIONOPTIONS CLASS

The SessionOptions class is used to create well-defined defaults for various options. Following is a list of a few of the

important methods/properties of this class. Note that there may be slight differences in the names of some of the class

members depending upon the API language interface used:

SERVERHOST

Read/write property representing the host-name or the IP address of where the communication process is running. The

default is “localhost”.

SERVERPORT

Read/write property representing the port number of the communication process. The default is 8194.

DEFAULTSUBSCRIPTIONSERVICE

Read/write property representing the name of the service to be used by default for subscriptions. The default is

“//blp/mktdata”.

DEFAULTTOPICPREFIX

Read/write property representing the name of the topic prefix to be used for subscriptions if one is not provided. The

default is “/ticker”.

AUTORESTARTONDISCONNECTION

Read/write property that accepts a Boolean value and determines whether the session is automatically restarted if there is

a connection failure. Set the NumStartAttempts property in tandem with this property.

ALLOWMULTIPLECORRELATORSPERMSG

Read/write property that accepts a Boolean value and allows a data response comprising multiple correlators.

SERVERADDRESSES (SERVER API, B-PIPE, PLATFORM)

Read/write property used in tandem with the ServerAddress class; used to set one or more port and host pairings that will

be used in order if the connection is lost to the primary host/port.

AUTHENTICATIONOPTIONS (B-PIPE)

Method used for both user and application authentication. In this method, pass a string, which specifies the

AuthenticationType, for a user (choices are OS_LOGON and DIRECTORY_SERVICE) and AuthenticationMode and

ApplicationAuthenticationType parameters with values of APPLICATION_ONLY and APPNAME_AND_KEY, respectively,

for an application.

The authentication and permissioning systems of Server API and B-PIPE require use of the //blp/apiauth service. This

defines the requests and responses that will come from the API.

The SessionOptions class is used to set the Session parameters prior to making the connection to the Bloomberg

Communication Server (bbcomm, Server API, B-PIPE) process. The SessionOptions class is then used as an argument

when creating an instance of the Session object.

Note for Desktop API Developers: Desktop API developers will rarely need to use the SessionOptions object in their

application as they always connect to BBComm, which runs on the same PC as the Bloomberg Professional service

(localhost) and usually connects on port 8194, which are the defaults of the ServerHost and ServerPort properties,

respectively.

3.2. SESSION CLASS

The Session class provides a session for establishing a connection along with data-request–related tasks. Following are

important constructor overloads:

Session(SessionOptions sessionOptions): Creates a Session with the specified Session Options

Session(SessionOptions sessionOptions, EventHandler handler): Creates a Session with the specified Session

Options and dispatches Events on this Session to the specified handler.

BLOOMBERG OPEN API – CORE DEVELOPER GUIDE

©2016 BLOOMBERG L.P. ALL RIGHTS RESERVED 27

Important methods of the Session class that are used by all API products include:

START

This establishes a connection with the product’s communication server process. It issues a blocking call to start the

Session.

STOP

This stops the operation of the Session.

OPENSERVICE

It opens the service having the specified URI (e.g., “//blp/refdata”, “//blp/mktdata”, etc).

GETSERVICE

This service returns a handle to a Bloomberglp.Blpapi.Service object representing the service identified by the specified

URI. This method is not used for a subscription-based request (e.g., “//blp/mktdata”).

SENDREQUEST

This sends a completed request to the service, including “//blp/refdata”, “//blp/apiflds” and “//blp/tasvc”.

SUBSCRIBE

This sends a subscription list to be subscribed. It is used for services such as “//blp/mktdata”, “//blp/mktvwap”,

and “//blp/mktbar”.

RESUBSCRIBE

Modifies each subscription in the specified SubscriptionList (for C++ API and Java) or generic List<Subscription> (for Java

API and .NET API) to reflect the modified options specified.

UNSUBSCRIBE

Cancels previous requests for asynchronous topic updates associated with the CorrelationIDs listed in the specified

SubscriptionList (for C++ API and Java) or generic List<Subscription> (for Java API and .NET API).

CREATESNAPSHOTREQUESTTEMPLATE

Creates template to be used for snapshot subscription requests.

CANCEL

Cancels outstanding subscriptions, templates or requests represented by the specified CorrelationIDs or generic

List<CorrelationID>.

Following are a few of the important methods of the Session class needed by the enterprise API products (Server API,

Platform and B-PIPE):

GENERATETOKEN

Requests a token string for the specified application and/or user entered in EMRS, which is then used for authorization.

SENDAUTHORIZATIONREQUEST

Sends a completed authorization request to the authorization service (“//blp/apiauth”).

CREATEIDENTITY

Returns an identity that is valid but not authorized.

3.3. ESTABLISHING A CONNECTION

In most cases, both the Session and SessionOptions classes will be used to establish a connection between an

application and the communication server process associated with the product (e.g., serverapi, bbcomm, etc.). Take a

look at the accompanying slide for a code sample for establishing a connection.

As mentioned earlier, a Desktop API application will always connect to bbcomm, which will be running on the same PC on

port 8194. Since the default values of the ServerHost and ServerPort properties of the SessionOptions object are

“localhost” and 8194, respectively, a Desktop API application would not be required to set them. In fact, it is not

BLOOMBERG OPEN API – CORE DEVELOPER GUIDE

©2016 BLOOMBERG L.P. ALL RIGHTS RESERVED 28

uncommon to find a Desktop API application that does not use this class object for this reason, but may call its other class

members.

This is not the case for the enterprise API products, which will require that at least one of these two properties be set or

possibly not used at all. In place of those two properties, an enterprise application wishing to handle failover situations

would use the ServerAddresses and AutoRestartOnDisconnection members of the SessionOptions class. If the

connection is lost to the primary host/server, the application will connect to the next pairing specified by the

ServerAddresses property. To use this property, the AutoRestartOnDisconnection property must be set to true (default is

false). Failover will be covered in detail within the Enterprise documentation.

In an Enterprise application that is not handling failover, the ServerHost and ServerPort properties will be set. For

instance, if the serverapi process was installed on a Windows, Solaris or Linux box with the defaults, it will most likely be

listening on port 8194, which is the default of the SessionOptions.ServerPort property as previously mentioned. Since the

server process is probably not installed on the same machine as the application (unless possibly testing on a

development machine), the SessionOptions.ServerHost property will not be the default “localhost” value.

Once the required properties are set, the SessionOptions object will be used when instantiating the Session object. The

settings will take effect when the Session.Start method is called on to establish a connection between the application and

the communication server process.

BLOOMBERG OPEN API – CORE DEVELOPER GUIDE

©2016 BLOOMBERG L.P. ALL RIGHTS RESERVED 29

Data Requests

4.

STREAMING DATA (MARKET DATA)

Real-time and/or delayed streaming tick data is retrieved by subscribing to or monitoring a list of securities and real-time

fields. Once a subscription is made, continuous or intervalized tick updates will be sent from the Bloomberg Data Center

until the user cancels or unsubscribes from that subscription. The Subscribe method will be used.

PER REQUEST DATA (REFERENCE DATA / BULK DATA)

Data retrieved by sending a Request object via the SendRequest method. Per request data comprises of values for the

requested securities/fields at that moment in time, assuming the user has real-time entitlements to that data. Otherwise,

delayed values will be received. Static fields (e.g., PX_LAST instead of LAST_PRICE, where the latter is a real-time field)

should be used. However, real-time fields will also work in this type of request as each has an equivalent static field.

Bulk data is also a of data, but it is represented by more than one piece of data and requires special handling. For

instance, “COMPANY_ADDRESS” is a bulk field and returns multiple lines of information. Bulk fields are identified on

{FLDS <GO>} by the “Show Bulk Data…” text in its Value column. For both types of data, a Request object of type

“ReferenceDataRequest” is created.

This can be tested by loading “IBM US Equity” on the Bloomberg Professional service, running {FLDS <GO>} in the same

window and entering “company address” in the yellow query field below the security and pressing {<GO>}.

HISTORICAL DATA

Data represented by a single point of data for each day specified in the date range of the historical request. Use the

SendRequest method to make this request. A Request object of type “HistoricalDataRequest” will be created. Before

submitting the Request object to Bloomberg, add any securities and (historical) fields, a start and end date range, and set

any applicable elements to customize the request. For instance, to only receive data for trading days or data for all

calendar days, fill in the non-trading days with the previous trading day’s value.

INTRADAY DATA

Data available as:

Tick data — Each tick over a defined period of time

Bar data — A series of intraday summaries over a defined period of time for a security and Event type pair

In both cases, pass the request using the SendRequest method, but only specify one security for each

Request object submitted. For intraday ticks, create an object of type “IntradayTickRequest.” For bars, create an object of

type “IntradayBarRequest.”

BLOOMBERG OPEN API – CORE DEVELOPER GUIDE

©2016 BLOOMBERG L.P. ALL RIGHTS RESERVED 30

Bloomberg Services

5.

There are two Core service schemas and several additional services that are common to all or some of the API products.

SERVICES

1. Market Data — //blp/mktdata: Used when subscribing to streaming real-time and delayed market data.

2. Reference Data — //blp/refdata: Used when requesting reference data such as pricing, historical/time-series and

intraday bars and ticks.

3. Source Reference — //blp/srcref: Used to subscribe to the source reference and tick-size data available for the

specified entitlement ID.

4. Vwap — //blp/mktvwap: Subscription-based service used when requesting streaming custom Volume-Weighted-

Average-Price data.

5. Market Depth (B-PIPE ONLY) — //blp/mktdepthdata: Market Depth Data service.

6. Market Bar — //blp/mktbar: Subscription-based service used when requesting streaming real-time intraday market

bar data. This service is currently unavailable to B-PIPE users.

7. Market List — //blp/mktlist: Used to perform two types of list data operations. The first is to subscribe to lists of

instruments, known as “chains,” using the “chain” <subservice name> (i.e., //blp/mktlist/chain). The second is to request a

list of all the instruments that match a given topic key using the “secids” <subservice name> (i.e., //blp/mktlist/secids). The

//blp/mktlist service is available to both BPS (Bloomberg Professional service) and NONBPS users.

8. API Fields — //blp/apiflds: Used to perform queries on the API Field Dictionary. It provides functionality similar to

{FLDS <GO>}.

9. Instruments — //blp/instruments: The Instruments service is used to perform three types of operations. The first is

a Security Lookup Request, the second is a Curve Lookup Request and the third is a Government Lookup Request.

10. Page Data — //blp/pagedata: Subscription-based service providing access to GPGX pages and the data they

contain. The GPGX number, the monitor number, the page number and the required rows (fields) must be provided.

11. Technical Analysis — //blp/tasvc: The Technical Analysis service downloads data and brings it into an application

using Bloomberg API.

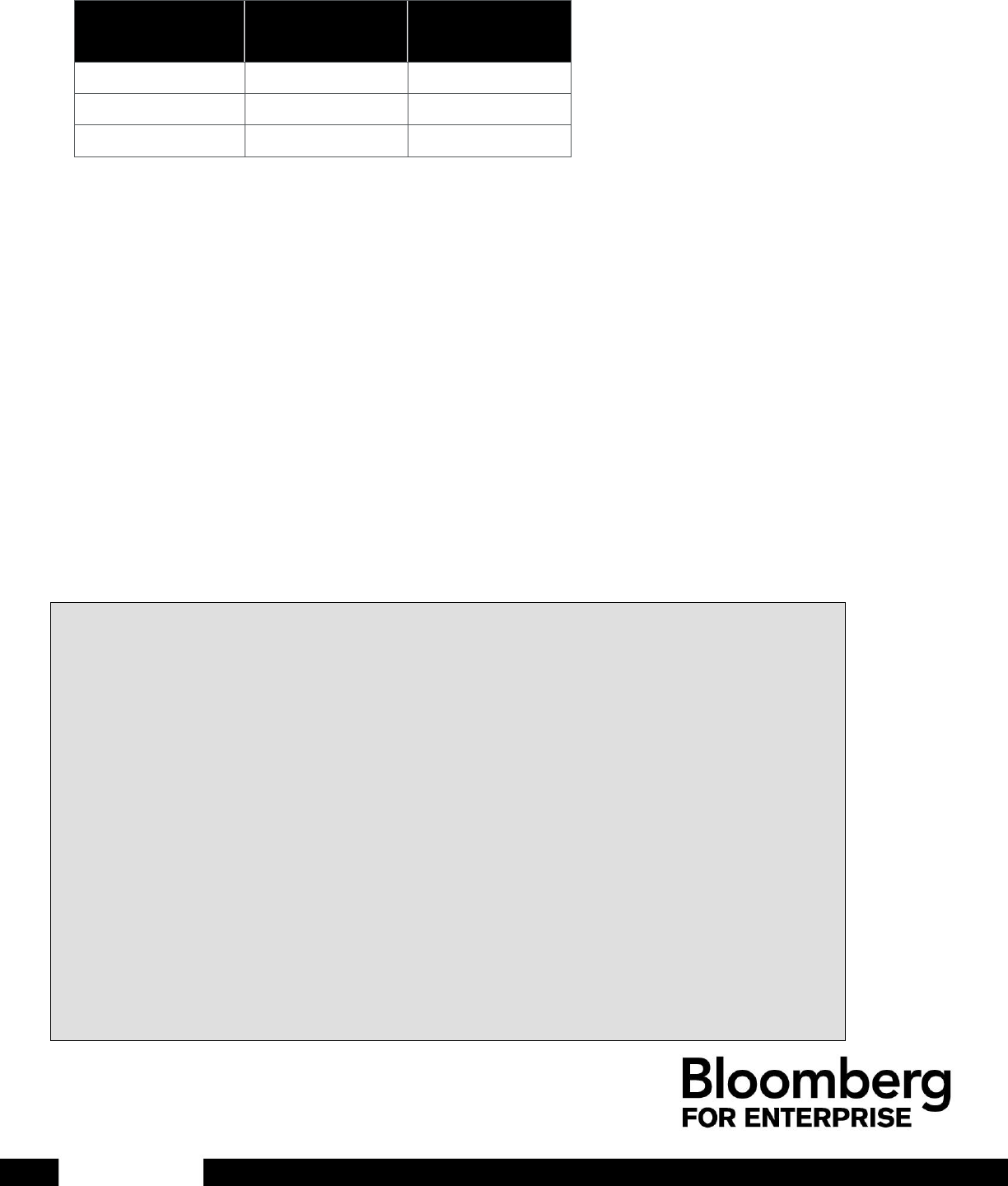

12. Curves Toolkit — //blp/irdctk3: The CTK (Curves Toolkit) service allows users to interact with interest rate curves

directly and retrieve the data available on the ICVS <GO> function.

5.1. SERVICE SCHEMAS

The role of the schema is to define the format of requests to the service, as well as the Events returned from that service.

Within a service, one or more Event types may exist, each having its own schema. The schema is the shape of the data.

For instance, market data is flat, while reference data is nested (like XML).

Each element has the following properties and attributes:

Name: The name of the element.

Status: ACTIVE — Available or INACTIVE — Unavailable

Type: Data type of that element. This includes SEQUENCE (group), ENUMERATION, BOOL, STRING, etc.

Minimal Occurrence: 0 — Optional or 1 — Required

Maximal Occurrence: 1 — Element or –1 — Array

BLOOMBERG OPEN API – CORE DEVELOPER GUIDE

©2016 BLOOMBERG L.P. ALL RIGHTS RESERVED 31

Description

Minimal

Occurrence

Maximal

Occurrence

Optional Field

0

1

Required Field

1

1

Array

1

–1

5.2. ACCESSING A SERVICE

All Bloomberg data provided by the Bloomberg API is accessed through a “service” (URI), which provides a schema to

define the format of requests to the service and the Events returned from that service. The customer application’s

interface to a Bloomberg service is a Service object.

Accessing a service is normally a two-step process:

1. Open the service using either openService or the openServiceAsync methods of the Session object.

2. Obtain a Service object for the opened service using the getService method of the Session object.

In both steps, the service is identified by its “name,” an ASCII string formatted as:

“//namespace/service”; (for example, “//blp/refdata” for reference data or “//blp/apiauth” for authorization

functions)

Once a service has been successfully opened, it remains available for the lifetime of that Session object.

Important Note: When making a subscription-based request (via “//blp/mktdata”, “//blp/mktvwap”, or other

subscription-based services), the getService method is not used.

Building upon the code from the establishing a connection section, following is an example of how these service-related

methods might be used.

<C++>

int main()

{

SessionOptions sessionOptions;

sessionOptions.setServerHost("10.10.10.10"); // Or specify machine name

sessionOptions.setServerPort(8194);

//Establish Session

Session session(sessionOptions);

//Attempt to Start Session

if (!session.start()) {

std::cerr <<"Failed to start session." << std::endl;

return 1;

}

//Attempt to open reference data service

BLOOMBERG OPEN API – CORE DEVELOPER GUIDE