Etaxguide GST Guide On Hand Carried Exports Scheme 20130930

User Manual: Pdf

Open the PDF directly: View PDF ![]() .

.

Page Count: 1

GST:

Guide on Hand-Carried Exports Scheme

IRAS e-Tax Guide

GST: Guide on Hand-Carried Exports Scheme

4

Published by

Inland Revenue Authority of Singapore

Published on 30 Sept 2013

Disclaimers: IRAS shall not be responsible or held accountable in any way for any damage, loss or

expense whatsoever, arising directly or indirectly from any inaccuracy or incompleteness in the Contents

of this e-Tax Guide, or errors or omissions in the transmission of the Contents. IRAS shall not be

responsible or held accountable in any way for any decision made or action taken by you or any third party

in reliance upon the Contents in this e-Tax Guide. This information aims to provide a better general

understanding of taxpayers’ tax obligations and is not intended to comprehensively address all possible

tax issues that may arise. While every effort has been made to ensure that this information is consistent

with existing law and practice, should there be any changes, IRAS reserves the right to vary our position

accordingly.

© Inland Revenue Authority of Singapore

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any

means, including photocopying and recording without the written permission of the copyright holder,

application for which should be addressed to the publisher. Such written permission must also be obtained

before any part of this publication is stored in a retrieval system of any nature.

GST: Guide on Hand-Carried Exports Scheme

5

Table of Contents

1. Aim………………... ...................................................................................... 1

2 At a glance ................................................................................................... 1

3 Overview of the Scheme…………………………………………………………...2

4 Responsibilities of the supplier…………………………………………………...3

4.1 Key Responsibilities as a supplier ........................................................ 3

4.2 Operational procedures and conditions to ensure when selling goods to

overseas customer…………………………………………………………..3

4.3 Export Permit Declaration .................................................................... 4

4.4 Documents to maintain ......................................................................... 5

4.5 Making and reporting a sale in GST return ........................................... 6

5 Responsibilities of carrier ............................................................................ 9

6 Offences under the Scheme ...................................................................... 10

7 Exemption from the Scheme ..................................................................... 10

8 Contact information ................................................................................... 11

Appendix 1: Application for Exemption from Hand-Carried Export Scheme…12

Appendix 2: List of compulsory documents to be maintained by GST-

registered persons who are exempted from the Scheme ........... 16

Appendix 3: Specimen format of the carrier’s declaration for goods hand-

carried out of Singapore via Changi International Airport ........... 17

Appendix 4: Frequently Asked Questions (FAQ) ............................................. 18

GST: Guide on Hand-Carried Exports Scheme

1

1 Aim

1.1 The Hand-Carried Exports Scheme (referred to as “the Scheme” in this

guide) was introduced to meet the following objectives:

(a) To guide GST-registered persons in obtaining the required

documentary proof that goods are hand-carried out of Singapore via

Changi International Airport; and

(b) To assure the Comptroller of GST that the goods are indeed exported

out of Singapore via Changi International Airport.

This guide sets out the kinds of documentary evidence required for goods

hand-carried out of Singapore via Changi International Airport, to be zero-

rated for GST purposes.

This Scheme is compulsory for all GST-registered persons who export their

goods by hand-carrying them out of Singapore via Changi International

Airport and wish to zero-rate the supplies of such goods.

This Scheme, however, does not apply to:

(a) goods that are hand-carried out of Singapore via Seletar Airport, sea or

land1.

(b) goods that are purchased by departing passengers from shops located

after the immigration check-in area of Changi International Airport2.

This guide should be read together with the e-Tax Guide “A Guide on

Exports”3.

2 At a glance

2.1 GST-registered local suppliers who wish to zero-rate the supplies of hand-

carried goods out of Singapore via Changi International Airport, may refer to

this guide for the documents required to prove the zero-rating.

This guide also describes the GST reporting requirements a local supplier

needs to be aware of, e.g. he is able to receive the endorsed export permit

within 60 days from the date of supply.

It is also essential for a local supplier to know what the qualifying conditions

of a carrier in this Scheme are and what he needs to inform the carrier

1 GST-registered persons are required to maintain the export documents listed in the e-Tax Guide “A Guide on

Exports” for their hand-carried exports made via Changi International Airport before 1 April 2009, Seletar

Airport, sea or land.

2 GST-registered persons operating retail shop(s) in the restricted area of the airport can zero-rate their supplies

of goods made to departing passengers. Such retailers must sight the passenger's passport and boarding

pass at the time of sale to verify that the passenger is indeed departing Singapore, before the sale can be

zero-rated.

3 This guide states the export documents that are required to be maintained to support the zero-rating of

supplies for GST purposes under different export scenarios.

GST: Guide on Hand-Carried Exports Scheme

2

before he departs Singapore via Changi International Airport with the hand-

carried goods.

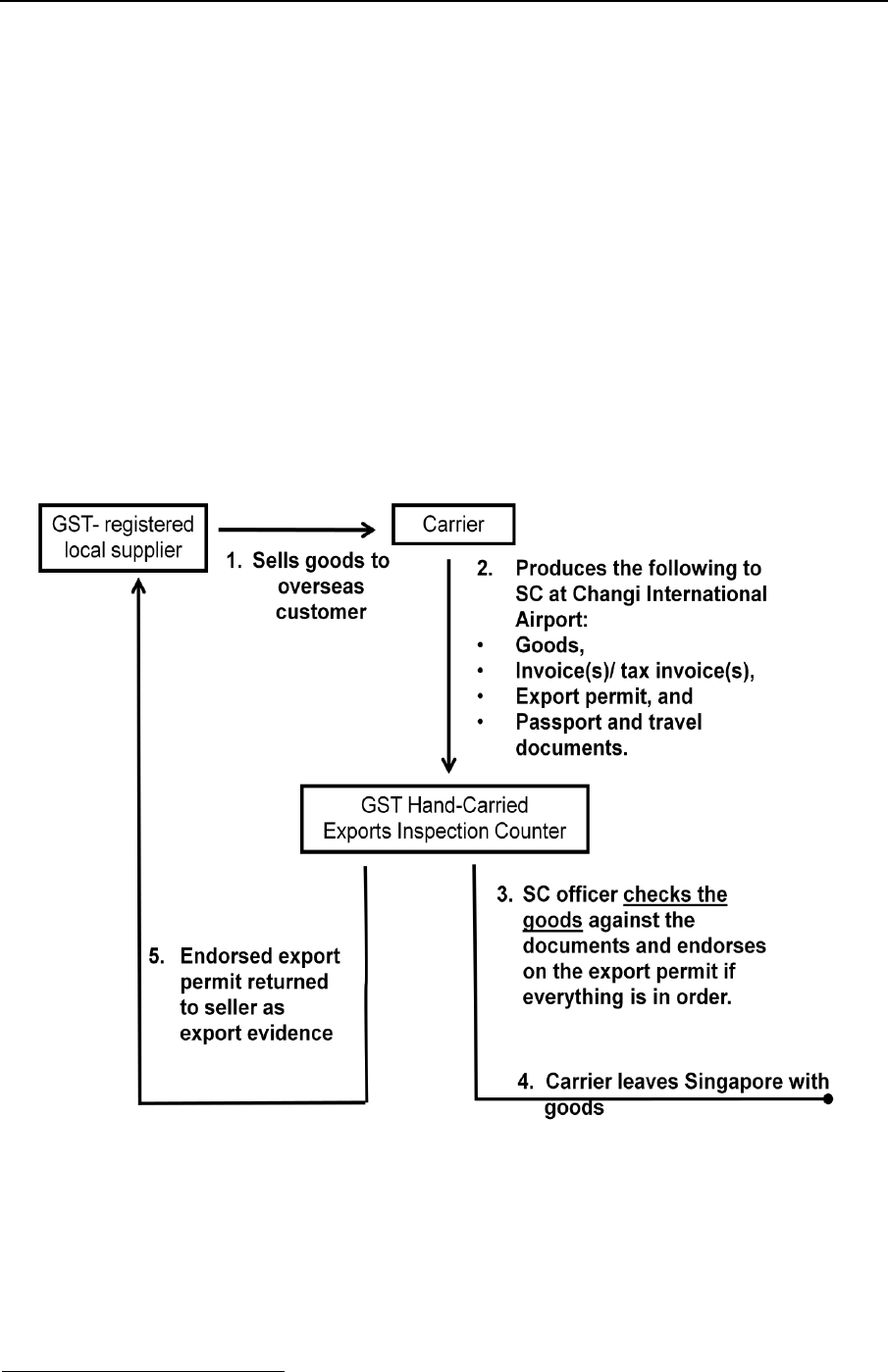

3. Overview of the Scheme

3.1 Under this Scheme, hand-carried goods must be supported by a valid export

permit4. The same goods must also be presented to the designated counters

of Singapore Customs (referred to as “SC” in this guide) at the airport for

inspection. After SC has inspected the goods, SC will endorse on the export

permit if SC is satisfied that the goods tally with the quantity and description

declared in the permit.

3.2 GST-registered persons who zero-rate their supplies of hand-carried goods

under this Scheme must retain the export permit endorsed by SC as proof of

their exports. Below is a diagram showing how the Scheme works.

3.3 As compliance with this Scheme is mandatory for the zero-rating of all hand-

carried exports via Changi International Airport, GST-registered persons are

required to apply to the Comptroller for exemption from the Scheme if they

meet the qualifying conditions (see paragraph 7) and wish to be exempted

from the Scheme.

4 Export permit is also known as “Out Permit” or “Cargo Clearance Permit”.

GST: Guide on Hand-Carried Exports Scheme

3

4 Responsibilities of the supplier

4.1 The key areas of responsibilities of a GST-registered person, as a local

supplier, are as follows:

- Operational procedures and conditions when selling goods to overseas

customer;

- Export permit declaration;

- Documents to maintain; and

- Making and reporting a sale in GST return.

4.2 Operational procedures and conditions to comply with when selling

goods to overseas customer

4.2.1 A GST-registered person, as a local supplier, has to ensure that the goods

must be hand-carried out of Singapore via Changi International Airport.

4.2.2 The person bringing the goods out of Singapore is referred to as “the

carrier” in this guide. The carrier of the goods must be at least 16 years of

age at the time of presenting the goods to SC at the airport.

The carrier who carries the goods out of Singapore can be a local person or

a foreign person. He can be:

(i) The local supplier himself;

(ii) The overseas customer; or

(iii) A person who is appointed and authorised by the GST-registered

supplier or the overseas customer to bring the goods out of Singapore

(e.g. employee or representative).

4.2.3 After issuing invoice(s) / tax invoice(s) to the overseas customers, the GST-

registered local supplier has to ensure that the following procedures are

followed:

Procedures to follow after issuing invoice(s)/tax invoice(s) to

overseas customers

(a)

Confirm that the carrier is leaving Singapore with the goods via the

Changi International Airport;

(b)

Declare the goods in an export permit via TradeNet;

(c)

Give the carrier his invoice(s)/tax invoice(s) and the completed

export permit. Local supplier should also keep a copy of these

documents as his records;

(d)

Provide the carrier a self-addressed envelope with prepaid

postage for the carrier to return the export permit endorsed by SC;

GST: Guide on Hand-Carried Exports Scheme

4

(e)

Inform the carrier to produce the goods together with the invoice(s)

/ tax invoice(s), export permit, passport and travel documents to

SC at the airport for inspection and endorsement;

(f)

Inform the carrier to arrive earlier at the airport to allow sufficient

time for the inspection of goods and endorsement of the export

permit by SC prior to departure;

(g)

Inform the carrier to carry small items especially those of high

value as hand luggage;

(h)

Inform the carrier to bring the goods with him out of Singapore

either in his hand luggage or check-in luggage;

(i)

Inform the carrier to return the endorsed export permit to him

within 60 days of the date of the supply of his goods; and

(j)

Inform the carrier that he must depart from Singapore within 12

hours after getting the endorsement by SC on the export permit.

4.2.4 It is important for the local supplier to take note of and communicate the

following to his overseas customers and carriers:

(a) When the carrier presents the export permit to SC, he is making a

declaration that he is bringing the goods out of Singapore. It is an

offence to make a false declaration;

(b) The carrier must produce the goods to SC for inspection and for the

export permit to be endorsed. The Comptroller of GST does not

accept endorsement by any other authorities; and

(c) The carrier must check in the goods or bring the goods out with him on

his departing flight after getting the export permit endorsed by SC. It is

a serious offence for him to pass the goods to another person or bring

the goods back to Singapore after the export permit is endorsed.

4.3 Export Permit Declaration

4.3.1 It is a requirement under this Scheme that an export permit5 must be

obtained for all goods to be hand-carried out of Singapore, regardless of the

value and quantity of goods.

4.3.2 A local supplier may subscribe for TradeNet and make declaration for the

export permit on his own. If the local supplier is not a TradeNet user, he can

obtain the export permit by appointing a TradeNet declaring agent such as

TradeNet Service Centre, freight forwarder or cargo agent to declare his

export.

4.3.3 The export permit declared under this Scheme must contain the following

information:

5 For more information on the export procedures and requirements, please visit the website of Singapore

Customs on http://www.customs.gov.sg and https://www.tradexchange.gov.sg.

GST: Guide on Hand-Carried Exports Scheme

5

S/N

Compulsory details to be shown

on the export permit:

To be shown in this field

of the export permit:

1

Business name of the local supplier

“Exporter”

2

The carrier’s name, passport number,

date of birth and the scheduled

departure time of his flight

“Trader’s remarks”

3

Date of the carrier’s departure from

Singapore

“Departure date”

4

Flight number that the carrier is

departing on

“Voyage/Flight number”

5

Destination country for the hand-

carried goods

“Country of final destination”

6

Invoice / Tax invoice number for the

hand-carried goods

“Trader’s remarks”

7

Description for each type of the hand-

carried goods

“Description”

8

Total units for each type of the hand-

carried goods

“HS quantity & unit”

9

Total value for each type of the hand-

carried goods

“FOB value”

4.3.4 It is important for the local supplier to ensure that:

(a) All information declared in the export permit are accurate;

(b) He is declared as the exporter in the export permit; and

(c) The description of his goods declared in the export permit is adequate

for SC to identify and inspect the goods. The quantity of his hand-

carried goods must also be correctly declared in the export permit. SC

will not endorse on the export permit when the goods presented for

inspection do not tally with the quantity or description of the goods

declared in the export permit, or when there is manual alteration made

to the quantity or description of goods in the export permit.

4.4 Documents to maintain

4.4.1 To qualify for zero-rating of hand-carried goods under this Scheme, it is

important to maintain the following documents for at least 5 years:

(a) A list of the invoices / tax invoices and export permits issued under the

Scheme;

(b) Copies of the invoices / tax invoices issued for the goods sold;

(c) Original copies of export permits endorsed by SC; and

GST: Guide on Hand-Carried Exports Scheme

6

(d) Evidence of payment made to the customer for the refund of GST that

was previously charged and collected from the customer at the time of

sale6

4.5 Making and reporting a sale in GST return

4.5.1 A GST-registered person must issue invoice/tax invoice to an overseas

customer for the sale of goods. The local supplier has the following options:

(a) Charge GST at the prevailing tax rate and collect the GST from the

overseas customer. The local supplier must issue invoice / tax invoice

to the overseas customer;

[The supplier must report the value of sale in Box 1 “Total value of

standard-rated supplies” and the corresponding GST collected in Box 6

“Output tax due” of his GST return for the prescribed accounting period

in which the sale takes place if he has not received the endorsed

export permit at the time of filing his GST return.

The supplier should also agree with the customer on whether any

administrative fee is involved and how the refund of GST will be made

after the supplier receives the export permit endorsed by SC.]

(b) Not to charge and collect GST from the overseas customer at the time

of sale. If the local supplier’s GST return is due to be filed within 60

days of the date of his supply, he can report the sale as zero-rated

supply provisionally in his GST return for the prescribed accounting

period in which the sale takes place.

However, if he does not receive the endorsed export permit within the

60-day period, he must standard-rate the supply and account for the

output tax using the tax fraction (7/107) either by filing GST F7 for the

prescribed accounting period in which the sale took place or in his next

GST return (subject to the conditions for filing GST F7).

Tables A and B summarises what the local supplier should do when he files

his GST return for the prescribed accounting period in which the sale takes

place.

6 This is relevant for instances where the local supplier has previously standard-rated the supply and

subsequently made a refund of GST to the customer upon receiving the export permit that contains the original

endorsement of SC; see paragraph Table B Column III Row (b).

GST: Guide on Hand-Carried Exports Scheme

7

Table A

Supplier has not received the endorsed export permit

at the time of filing GST return

< 60 days

from the date of supply

> 60 days

from the date of supply

I

II

(a) GST was not charged to

the overseas customer.

To report as zero-rated

supply provisionally.

To report as standard-rated

supply and account for the

output tax.

(b) GST was charged to the

overseas customer.

To report as standard-

rated supply and account

for the output tax.

Table B

Supplier has received the endorsed export permit at

the time of filing GST return

< 60 days

from the date of supply

> 60 days

from the date of supply

III

IV

(a) GST was not charged to

the overseas customer.

To report as zero-rated

supply.

To report as standard-rated

supply and account for the

output tax if he receives the

endorsed export permit after

60 days of the date of

supply7.

(b) GST was charged to the

overseas customer.

The local supplier does

not need to report this

supply as standard-rated

supply and need not

account for output tax in

his GST return first.

The local supplier should

refund the GST back to

the overseas customer.

He may issue a credit

note to the overseas

customer.

4.5.2 What must the local supplier do when he receives the export permit

endorsed by SC?

The local supplier must:

(a) check that the export permit contains the original endorsement of SC;

and

(b) ensure that the endorsed export permit is received within 60 days of

the date of his supply of goods.

7 In the event that the supplier receives the endorsed export permit after 60 days due to unforeseen

circumstances that are beyond his control, IRAS may make an exception and allow him to zero-rate his supply

of goods. The exception shall be granted on a case-by-case basis and the supplier should write in to IRAS for

approval.

Endorsed permit

received?

Whether GST

charged?

Endorsed permit

received?

Whether GST

charged?

GST: Guide on Hand-Carried Exports Scheme

8

4.5.3 If the local supplier has charged and collected GST from the customer at the

time of sale, what must he do to claim back the output tax which he has

already accounted to the Comptroller for the sale?

The local supplier must have done all the following before he can claim back

the output tax previously accounted to the Comptroller:

(a) Has originally accounted for the output tax on the sale at the prevailing

tax rate in his GST return (see paragraph 4.5.1a);

(b) Has already received the endorsed export permit within 60 days of the

date of his supply of goods;

(c) Has already refunded the tax to his overseas customer. If the supplier

refunds the tax via cheque to his customer, he can recover the tax from

the Comptroller of GST only after the cheque has been encashed by

the customer; and

(d) Maintain documents and records to show that the above conditions

have been satisfied (see paragraph 4.4).

You may refer to Table B Column III Row (b) on page 7 for a summary on

the above.

4.5.4 If the local supplier satisfies all the above conditions, he can proceed to

make the following adjustments in his GST return for the prescribed

accounting period in which he has refunded the tax to the customer:

(a) Include the value of the sale in Box 2 “Total value of zero-rated

supplies”;

(b) Reduce by the value of this sale from Box 1 “Total value of standard-

rated supplies”; and

(c) Reduce by the amount of GST that he has refunded to his customer on

this sale in Box 6 “Output tax due”.

4.5.5 The local supplier may issue a credit note to the overseas customer for the

amount of GST that he has refunded to the latter.

GST: Guide on Hand-Carried Exports Scheme

9

5 Responsibilities of carrier

There are four broad responsibilities of a carrier:

Products and documents

Inspection and endorsement

For the purposes of SC’s inspection

of goods, the carrier needs to bring

the following:

a) Physical goods,

b) Invoice(s) / tax invoice(s);

c) Export permit; and

d) Passport and travel documents

such as boarding pass or

confirmed air-ticket.

The carrier must present the goods

and documents for endorsement at:

a) GST Hand-carried Exports

Inspection Counter8 in the airport.

Type of items

Returning of endorsed permit

For bulky items or goods packed in

luggage that are to be checked in,

the goods and documents have to

be presented to SC for inspection

and endorsement before the

immigration check-in area.

For small items that can be hand-

carried, SC reserves the right to

request that these be produced for

verification after the immigration

check-in area, located in the

Departure Lounge.

After getting the export permit

endorsed by SC, the carrier must

check in the goods or hand-carry

the goods with him on a departing

flight.

The export permit bearing the

original endorsement of SC must be

returned to the local supplier within

60 days of the date of his supply.

The overseas carrier may return the

endorsed permit to the local

supplier by:

(a) enclosing the endorsed export

permit in a pre-paid postage

envelope addressed to the local

supplier [see paragraph

4.2.3(d)], and drop it in the

mailbox located next to the GST

Hand-carried Exports Inspection

Counter at the airport.

(b) mailing the endorsed export

permit back to the local supplier

from overseas.

(c) bringing the endorsed export

permit back to the local supplier

on his next visit to Singapore.

8 These counters are located before and after the immigration check-in area in all airport terminals. They can

be found next to the GST Refund Inspection Counters for tourists claiming GST refunds on goods purchased

in Singapore from retailers operating the Tourist Refund Scheme.

GST: Guide on Hand-Carried Exports Scheme

10

6 Offences

6.1 All GST-registered persons who zero-rate their supplies of hand-carried

goods under this Scheme must comply with the conditions laid out in

Regulation 105A of the GST (General) Regulations and this e-Tax Guide.

Please note that failure to comply with the regulations will lead to the zero-

rating of supplies being denied and the GST-registered person will have to

account for the GST on the supplies. Penalties will also be imposed on the

GST-registered person.

6.2 Any person (including the GST-registered person and the carrier) who is

guilty of an offence made under the Scheme shall be liable, on conviction, to

a fine not exceeding $5,000 and an imprisonment term not exceeding 6

months in default of payment.

7 Exemption from the Scheme

7.1 A local supplier may apply to be exempted from this Scheme by completing

an application form (see Appendix 1)9 and submit his application to the

Comptroller of GST.

7.2 To qualify for the exemption, the local supplier must satisfy all of the

following criteria:

(a) He must satisfy the Comptroller of GST that there are valid commercial

reasons for not being able to present the goods for inspection at the

airport. These commercial reasons must also be consistent with

international practices and norms related to the particular trade.

(b) He must have good compliance records for GST and Income Tax (e.g.

good filing and payment records). He must continue to have good

compliance records for GST and Income Tax.

(c) He must maintain a comprehensive list of documents as required by

the Comptroller in Appendix 2 of this guide.

7.3 For the protection of revenue, the Comptroller of GST may exercise his

discretion to vary the requirements or impose additional requirements for the

approval of this exemption.

7.4 Prior to receiving a written approval on the exemption from the Comptroller

of GST, the local supplier must adhere to the requirements of the Scheme

for all of his hand-carried exports.

7.5 Upon obtaining a written approval from the Comptroller of GST on his

application for exemption from the Scheme, the local supplier will not be

9 This application form “GST F17: Application for Exemption from Hand-Carried Exports Scheme” can also be

downloaded from IRAS website at http://www.iras.gov.sg.

GST: Guide on Hand-Carried Exports Scheme

11

required to present the hand-carried goods and export permits to SC for

inspection and endorsement at the airport.

7.6 To support the zero-rating of his hand-carried items that are exempted from

this Scheme, the local supplier must obtain the documents as listed in

Appendix 2 within 60 days of the date of his supply of goods.

8 Contact information

For any clarifications on this e-Tax Guide or the Hand-Carried Exports

Scheme, please contact:

Goods & Services Tax Division

Inland Revenue Authority of Singapore

55 Newton Road

Singapore 307987

Tel: 1800 356 8633

Fax: (+65) 6351 3553

Email: gst@iras.gov.sg

GST: Guide on Hand-Carried Exports Scheme

12

Appendix 1:

GST F17

APPLICATION FOR EXEMPTION FROM

HAND-CARRIED EXPORTS SCHEME

The Comptroller of Goods and Services Tax

55 Newton Road, Revenue House, Singapore 307987. Tel: 1800-356 8633

For more information, please visit IRAS website at http://www.iras.gov.sg

Important Notes:

(1) This form may take 20 minutes to complete.

(2) To qualify for the exemption, you must satisfy the Comptroller of GST that there are valid commercial

reasons for not being able to present the goods for inspection at the airport. These commercial reasons

must also be consistent with international practices and norms related to the particular trade. In

addition, you must have good compliance records for GST and Income Tax (e.g. good filing and

payment records).

(3) You do not need to attach any document to this application form.

(4) You will be notified in writing when your application has been approved.

(5) Prior to receiving a written approval on the exemption from the Comptroller of GST, you are still

required to adhere to the requirements of the Hand-Carried Exports Scheme for all of your hand-carried

exports.

(6) You are required to notify IRAS if you no longer require the exemption after your application has been

approved.

(7) Please send this completed form by post or submit it at IRAS Taxpayer Services Centre.

Please complete the form and indicate ‘NA’ where not applicable.

SECTION 1: APPLICANT’S PARTICULARS

Full name of the applicant (as registered for GST)

Address of correspondences

Block/House

#

Storey

-

Unit

Street Name

Postal code

Business Registration Number /

Unique Entity Number

Name of contact

Designation

Email Address

Office Number

Company website (if any)

Mobile Number

Fax Number

GST: Guide on Hand-Carried Exports Scheme

13

SECTION 2: BUSINESS DETAILS OF APPLICANT

(i) Please give a brief description of the business activities carried out by you (including how

the transactions are being carried out to give rise to your making of zero-rated supplies).

(ii) Country where most of your goods are exported to via Changi International Airport:

1

5

2

6

3

7

4

8

(iii) Products that you are dealing in (please tick accordingly):

1

Jewellery

Please elaborate:

2

Loose Diamonds

3

Luxury Watches

Please state 3 major brands:

a)

b)

c)

4

Other products

Please elaborate:

(iv) Average number of hand-carried exports via Changi International Airport made per month for

the past 12 months:

1 to 5

5-10

More than 10

(v) Percentage of total value of hand-carried exports via Changi International Airport to

total value of zero-rated supplies for the past 12 months:

(vi) Average value of hand-carried exports via Changi International Airport

made per month for the past 12 months:

$

GST: Guide on Hand-Carried Exports Scheme

14

SECTION 3: REASON FOR EXEMPTION

(i) Please state the reason(s) for applying for the exemption.

(ii) Please explain the problems/difficulties you would face if the exemption is not granted.

(iii) Please state the product type on which you would like to apply for exemption.

1

Jewellery

Please elaborate:

2

Diamond Jewellery

3

Loose Diamonds

4

Luxury Watches

5

Other products

Please specify the ‘other products’ here:

GST: Guide on Hand-Carried Exports Scheme

15

SECTION 4: DECLARATION

I, ___________________________________ NRIC / Passport / Fin Number _____________

(Full Name of Signatory)

declare that all the details and information given in this form and in any accompanying

document are true and complete.

I understand that once my application has been approved, I am required to maintain the

documents as stipulated in Appendix 2 of the e-Tax Guide “GST: Guide on Hand-Carried

Exports Scheme” to prove my hand-carried exports and fulfill any conditions as

imposed by the Comptroller of Goods and Services Tax.

Signature

Date

Designation (Please tick the appropriate box):

(For sole-proprietor / partnership, it must be signed by the sole-proprietor / partner.)

Sole-

proprietor

Partner

Director

Company

Secretary

Authorized

Official

Please ensure that this form is fully completed and duly signed before submission.

GST/FORM019/0309

GST: Guide on Hand-Carried Exports Scheme

16

Appendix 2: List of compulsory documents to be maintained by GST-

registered persons who are exempted from the Scheme

a) Invoice / Tax invoice to overseas customer;

b) One of the following documents listed in (i) to (iv) below:

(i) Written declaration by the person who hand-carries the goods that the

goods are for export. This declaration should be signed by him and

contain his full name, address and passport / NRIC number. A

specimen format of the carrier’s declaration can be found in Appendix 4:

(ii) Extract of the carrier’s passport with the relevant immigration

endorsement of his exit from Singapore or entry to a foreign country and

copy of transport evidence such as the electronic air-ticket or flight

itinerary bearing the carrier’s name. For goods exported as

accompanied baggage, a copy of airline excess baggage receipt (where

applicable);

(iii) Confirmation of receipt of goods from the overseas customer; and

(iv) Import permit or other relevant documents to prove that the goods are

brought into the country of destination.

c) Export permit (subject to the requirements of Singapore Customs for export

permits); and

d) Evidence of payment received from the overseas customer.

GST: Guide on Hand-Carried Exports Scheme

17

Appendix 3: Specimen format of the carrier’s declaration for goods hand-

carried out of Singapore via Changi International Airport

Declaration of Carrier for Goods Hand-Carried Out of Singapore

(By Individual Carrier)

To

(Name and address of supplier who is exempted from the Hand-Carried Exports Scheme)

I, ___________________(name of carrier as shown in passport), hereby confirm that I will be

hand-carrying the following goods out of Singapore via Changi International Airport.

Details of Goods

Name of Customer (as per invoice)

Invoice Date

Invoice Number

Quantity of Goods

* Value of goods hand-carried out by me

Description of Goods

Details of Departure

Date of Departure

Flight Number

Time of Flight

Name of Airline

Destination

Details of Carrier

Relationship to customer or seller

(delete where not applicable)

Address

Nationality

Passport Number

Signature of carrier ______________________

Date of declaration ______________________

* If the goods are to be hand-carried out by different carriers, then the value of the goods shown

in each carrier’s declaration should be the invoiced value for the quantity hand-carried out by

that respective carrier.

GST: Guide on Hand-Carried Exports Scheme

18

Appendix 4: Frequently Asked Questions (FAQ)

FAQs for the GST-registered local supplier

Q1 Is there any qualifying threshold on the value or quantity of goods for the

Hand-Carried Exports Scheme?

A1 No. All goods that are hand-carried out of Singapore via Changi International

Airport must come under the Hand-Carried Exports Scheme if the GST-

registered suppliers wish to zero-rate the supplies of such goods. This

Scheme is compulsory for all such hand-carried goods regardless of their

value and quantity.

Q2 If I’m selling my goods to a local customer who says that he will be hand-

carrying the goods out of Singapore via the airport, can I zero-rate my supply

to him under this Scheme?

A2 No. The Hand-Carried Exports Scheme only applies to goods that are sold to

overseas customers. As you are selling your goods to a local customer, you

must standard-rate the supply and charge GST on this local sale. This is the

case even though your local customer claims that he or his appointed carrier

will be bringing your goods out of Singapore.

Q3 I am selling my goods to an overseas customer and my goods will be hand-

carried out of Singapore via Changi International Airport. Can I choose to

standard-rate my supply and account for the output tax instead of zero-rating

the supply under the Hand-Carried Exports Scheme?

A3 If you wish to treat this as a local sale (notwithstanding that the goods are sold

to your overseas customer) and not a zero-rated supply under the Hand-

Carried Exports Scheme, then you must standard-rate your supply and

account for the output tax in your GST return. In this instance, you do not

need to fulfill the conditions of the Hand-Carried Exports Scheme. However

to avoid any misunderstanding by the customer, you should inform him that

this is a standard-rated local sale and that he is not entitled to claim any GST

refund from the Comptroller.

Q4 What if my hand-carried goods are not exported for sale but are brought to an

overseas country for other purposes (e.g. for testing or repair services, as

trade samples, for participation in an exhibition etc)? As there is no supply of

goods, do I need to report the value of goods exported as zero-rated supply in

my GST return? Should I make declaration for an export permit for these

goods and get it endorsed by Singapore Customs at the airport under this

Scheme?

A4 Yes, for GST reporting, you must declare the value of the goods exported as

zero-rated supply in your GST return even though you did not make a supply

of these goods and may not issue any invoice / tax invoice. You are also

GST: Guide on Hand-Carried Exports Scheme

19

required to take up an export permit and get it endorsed by SC under the

Hand-Carried Exports Scheme so that you can prove to the Comptroller that

the goods are indeed taken out of Singapore. If you subsequently sell these

goods when they are outside Singapore, the endorsed export permit will

provide evidence that your supply of goods has taken place outside

Singapore.

The above requirements would not apply if you are merely bringing the goods

(e.g. tools and equipment) for use when you perform services in an overseas

location and you intend to bring these goods back to Singapore after your

services have been performed.

If you wish to export the goods under the Temporary Export Scheme or export

goods which are previously imported under the Temporary Import Scheme,

please visit the website of SC on http://www.customs.gov.sg and

https://www.tradexchange.gov.sg to find out more about the permit

requirements.

Q5 What happens if:

(a) the particulars of the carrier (e.g. his name, passport number, date of

departure from Singapore, his departure flight number etc) as required in

paragraph 4.3.3 are not available when I make declaration for an export

permit; or

(b) there is a change in the carrier or in the carrier’s flight details after I have

declared all the required information in the export permit?

A5 Please refer to paragraph 4.3.3 You will have to declare certain information

such as the carrier's departure flight number and date of departure from

Singapore for the export permit to be approved. If there is a change in such

information, you should amend the information in the export permit via

TradeNet before the permit is presented to SC for endorsement.

Alternatively, you can re-apply for a new export permit via TradeNet and

present this new permit to SC for endorsement.

You may, however, manually correct the information declared in the “Trader's

remarks” field.

Q6 My goods are distributed among several carriers to hand-carry out of

Singapore via the airport. How should I declare for the export permit?

A6 If all the carriers are departing on the same flight, you only need to make

declaration for a single export permit for your hand-carried goods. Preferably,

the personal particulars (i.e. names, passport numbers and dates of birth) of

all the carriers should be indicated on your export permit. You should also

inform the carriers that they must present themselves and the goods together

to SC at the airport.

GST: Guide on Hand-Carried Exports Scheme

20

On the other hand, if all the carriers are departing on different flights, you

should take up different export permits for the goods to be hand-carried out by

each individual carrier. Each export permit should show the particulars of the

individual carrier as well as the quantity and description of the goods to be

hand-carried by that carrier (i.e. the information as required in paragraph

4.3.3).

Please note that SC will not endorse on the export permit if the goods

presented for inspection do not tally with the quantity or description declared

in the export permit. Hence, you are reminded to declare the correct quantity

and description of the hand-carried goods in your export permit.

Q7 What if there is a change in the quantity of my goods to be hand-carried out

after I have declared for an export permit, say from 10 units to 30 units of my

goods?

A7 You should amend the quantity of your goods in the export permit via

TradeNet, before the goods and export permit are presented to SC for

endorsement. When it is not possible to amend the export permit through

TradeNet and:

(a) if the quantity of your goods to be hand-carried out via the airport (e.g. 30

units) is more than what you have declared in the export permit, you

should take up another export permit for the additional goods (i.e. the

additional units) to be hand-carried out. All export permits declared for

the quantity of your hand-carried goods must be presented to SC at the

airport for endorsement.

(b) if you are exporting a lower quantity of goods (e.g. 8 units), you would

have to re-apply a new export permit via TradeNet. You should also

cancel the previous export permit via TradeNet if it is within the validity

period of the permit.

Please be reminded that the quantity of goods presented to SC for inspection

must tally with the quantity declared in the export permit(s). The Comptroller

of GST and SC do not accept any manual alteration made to the quantity of

goods in the export permits.

Q8 Must I get the original export permit for SC to endorse? Will SC endorse on a

copy of the export permit?

A8 Whenever possible, you should obtain the original export permit for SC to

endorse under this Scheme. In the event that you are unable to get the

original permit, SC will endorse on the copy of export permit (e.g. photocopy,

faxed copy or copy of the scanned image) that is presented together with the

goods, provided that all information on the copy of export permit is legible.

GST: Guide on Hand-Carried Exports Scheme

21

Q9 What happens if:

(a) the original copy of the export permit endorsed by SC is misplaced or

lost in mail?

(b) I only received a photocopy instead of the original copy of the endorsed

export permit?

A9 To zero-rate your supply under this Scheme, you must maintain the export

permit which bears the original endorsement made by SC. Without the original

copy of the endorsed export permit, you cannot zero-rate your supply under

this Scheme. Therefore, you must standard-rate your supply and account for

the output tax in your GST return.

Q10 Can I zero-rate my supply if I received the endorsed export permit from my

overseas customer or the carrier after 60 days of the date of my supply?

A10 If you receive the endorsed export permit after 60 days due to unforeseen

circumstances that are beyond your control, you may write in to the

Comptroller of GST and request for approval to zero-rate your supply. The

Comptroller will review your request on a case-by-case basis.

Q11 Under what circumstances would SC not endorse on an export permit?

A11 Examples of the circumstances under which SC will not endorse on the export

permit under the Scheme are:

(a) The person who presents the goods and export permit to SC is below

16 years old;

(b) The passport or travel document (e.g. boarding pass or confirmed air-

ticket) does not belong to the person who presents the goods and export

permit to SC;

(c) The travel document shows that the carrier’s departing flight is not

scheduled to leave Singapore within 12 hours. In this instance, SC may

request the carrier to come back at a later time for the inspection of

goods and endorsement of export permit;

(d) The quantity of goods presented for inspection does not tally with the

quantity declared in export permit;

(e) The nature of goods presented for inspection is different from the

description of goods declared in export permit;

(f) There is a manual alteration made to the quantity or description of goods

in the export permit; and

(g) The carrier arrives late at the airport and there is insufficient time for SC

to carry out the inspection required.

Please note that the above list is not exhaustive. In the event that SC deem

that certain condition(s) of the Scheme is not satisfied, SC will not endorse on

GST: Guide on Hand-Carried Exports Scheme

22

the export permit and will indicate the reason for rejection on the export

permit.

Once SC has refused to endorse on the export permit, no further request or

appeal for re-endorsement shall be considered regardless of the reasons

cited.

Q12 What if the export permit is not endorsed by SC and I cannot find any reason

for rejection indicated by SC on the permit?

A12 Please refer to A9. It is likely that the export permit is not presented to SC for

endorsement at the airport.

Q13 I have been granted approval by IRAS to be exempted from this Scheme and

I’m required to maintain all the compulsory documents listed in Appendix 2 for

my hand-carried exports. What if I’m unable to obtain any of the compulsory

documents for my hand-carried exports?

A13 The compulsory documents listed in Appendix 2 are the basic documents for

you to prove that the hand-carried goods are taken out of Singapore. If you

fail to maintain any of the compulsory documents, you will not be allowed to

zero-rate your supply of goods and you must charge GST on these supplies.

Q14 I understand that the Scheme does not apply to goods that are hand-carried

out of Singapore via:

Changi International Airport before 1 April 2009;

Seletar Airport;

Sea; or

Land.

What export documents should I maintain to support the zero-rating of my

supplies of such hand-carried exports?

A14 For the above hand-carried exports that do not fall under the Scheme, you are

required to maintain the export documents as specified in our e-Tax Guide “A

Guide on Exports”. You can download a copy of this e-Tax Guide from our

website at www.iras.gov.sg

In addition, you should comply with the requirements of SC and take up an

export permit if necessary. Unlike the Scheme, such hand-carried exports

need not be presented to SC for inspection and you do not need to get SC to

endorse on the export permit (unless you are required by SCs or other

government agency to do so).

Q15 I have been operating the Tourist Refund Scheme to allow my foreign

customers to claim back the GST paid on the goods which they have

purchased from me and brought out of Singapore. How would the Scheme

affect me? Would the Tourist Refund Scheme still continue after the Scheme

GST: Guide on Hand-Carried Exports Scheme

23

is implemented? If yes, when should I use the Scheme instead of the Tourist

Refund Scheme?

A15 The Tourist Refund Scheme will still continue, even after the Hand-Carried

Exports Scheme is implemented on 1 April 2009.

As the purpose of the Tourist Refund Scheme is to enable tourists to obtain

GST refund on goods which they have purchased in Singapore and brought

out of Singapore, you should use the Tourist Refund Scheme only when your

customer is a bona fide tourist and satisfies all eligibility criteria under that

scheme.

On the other hand, if you are selling goods to an overseas customer whom

you know is not a bona fide tourist and your goods are hand-carried out of

Singapore via Changi International Airport, you should use the Scheme if you

wish to zero-rate the supplies of such goods. However unlike the Tourist

Refund Scheme, there is no facility at Changi International Airport for your

overseas customer or the carrier of your goods to obtain the GST refund in

cash under the Scheme. Your overseas customer can only get the GST

refund from you if you have collected GST from him on the sale.

For more information on the Tourist Refund Scheme, please refer to our e-Tax

Guide “Guide to Retailers Operating Tourist Refund Scheme” which can be

downloaded from our website at www.iras.gov.sg

FAQs for the carrier

Q16 Where are the inspection counters for the Scheme located in Changi

International Airport?

A16 The GST Hand-Carried Exports Inspection Counters are located next to the

GST Refund Inspection Counters in all terminals of Changi International

Airport.

If your goods are bulky or need to be checked in, you need to present the

goods and export permit to SC for inspection and endorsement at the

inspection counter located in the Departure Check-In Hall before you check in

for your flight and clear the departure immigration.

For goods which you hand-carry into the aircraft, please clear the departure

immigration and produce your goods and export permit to SC at the inspection

counter located in the Departure Lounge.

Q17 What should I produce to SC at the inspection counters in Changi International

Airport?

A17 You should produce all of the following to SC at the inspection counters:

(a) Your passport;

GST: Guide on Hand-Carried Exports Scheme

24

(b) Your travel document (e.g. boarding pass, confirmed air-ticket, etc) as

proof of your intention to depart from Singapore;

(c) The export permit(s) for the goods which you are bringing out of

Singapore;

(d) The goods; and

(e) The supporting invoice(s) or tax invoice(s) for the goods which you are

bringing out of Singapore.

Q18 What if I turn up at the inspection counter not within 12 hours of the scheduled

departure time of my flight?

A18 One of the conditions of this Scheme is that the carrier must depart from

Singapore within 12 hours after getting the endorsement by SC on the export

permit. Hence, if you turn up at the inspection counter not within 12 hours of

the scheduled departure time, SC will not inspect your goods but will request

you to return at a later time for inspection and endorsement.

Q19 What should I do after getting the export permit endorsed by SC?

A19 You should either check in your goods or hand-carry the goods with you on

your departing flight, and leave Singapore within 12 hours.

If you have a postage prepaid envelope which is addressed to the local

supplier, you may enclose the endorsed export permit in the envelope and

drop it in the mailbox located next to the inspection counters at the airport

before boarding the plane.