E Tax Guide For The Insurance Industry (for Fourth Edition) Caa 23 Jan 2...x Etaxguide GST

User Manual: Pdf

Open the PDF directly: View PDF ![]() .

.

Page Count: 27

GST: Guide for the Insurance Industry

IRAS e-Tax Guide

GST: Guide for the Insurance Industry

(Fourth Edition)

GST: Guide for the Insurance Industry

Published by

Inland Revenue Authority of Singapore

Published on 8 Feb 2017

First edition on 31 Mar 2014

Second edition on 14 Nov 2014

Third edition on 10 Jun 2016

Disclaimers: IRAS shall not be responsible or held accountable in any way for any damage, loss or

expense whatsoever, arising directly or indirectly from any inaccuracy or incompleteness in the

Contents of this e-Tax Guide, or errors or omissions in the transmission of the Contents. IRAS shall

not be responsible or held accountable in any way for any decision made or action taken by you or

any third party in reliance upon the Contents in this e-Tax Guide. This information aims to provide

a better general understanding of taxpayers’ tax obligations and is not intended to comprehensively

address all possible tax issues that may arise. While every effort has been made to ensure that this

information is consistent with existing law and practice, should there be any changes, IRAS reserves

the right to vary its position accordingly.

© Inland Revenue Authority of Singapore

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by

any means, including photocopying and recording without the written permission of the copyright

holder, application for which should be addressed to the publisher. Such written permission must

also be obtained before any part of this publication is stored in a retrieval system of any nature.

GST: Guide for the Insurance Industry

Table of Contents

Page

1

Aim ........................................................................................................... 1

2

At a glance ................................................................................................ 1

3

Insurance Companies ............................................................................... 2

4

Reinsurance Companies......................................................................... 12

5

Insurance Intermediaries ........................................................................ 12

6

Tax Invoice ............................................................................................. 16

7

Self-Billing ............................................................................................... 17

8

Summary: GST Treatment of Insurance Products and

Brokerage/Commission .................................................................................. 19

9

Contact Information ................................................................................ 21

10

Updates and Amendments ..................................................................... 22

Appendix 1 ..................................................................................................... 23

Appendix 2 ..................................................................................................... 24

GST: Guide for the Insurance Industry

1

1 Aim

1.1 This guide explains the GST principles applicable to the insurance industry

1

.

Specifically, it highlights the GST treatment of insurance products, fees,

charges, and commissions for insurance companies, reinsurance

companies, and insurance intermediaries, such as agents and brokers.

1.2 The guide also clarifies the distinction between life business and life policy.

2 At a glance

2.1 Generally, the provision of an insurance contract by a GST-registered

insurance company in Singapore is a taxable supply of services. GST is

charged on the insurance premiums at the standard rate

2

.

2.2 Where the insurance services qualify for zero-rating as an international

service (see paragraph 3.3) or exemption from GST (see paragraph 3.1), no

GST is charged on the insurance premiums.

2.3 The terms “life business” and “general business” are used in the Insurance

Act to indicate the nature of business that insurance companies are allowed

to operate depending on the nature of the license issued. These terms are

not synonymous with and should not be confused with the terms “life policy”

and “general policy”.

2.4 Insurance companies that are in the life business may issue life policies and

long-term health and accident policies. For GST purposes, only premiums

arising from life insurance contracts are exempt from GST. Therefore, not all

policies issued by life insurance companies are exempt from GST.

1

This e-Tax guide replaces the IRAS’ e-Tax guide “GST: The Insurance Industry (Fourth Edition)”

published on 01 Oct 2012.

2

GST should be charged at the prevailing rate, which is currently at 7%.

GST: Guide for the Insurance Industry

2

3 Insurance Companies

3.1 Life Insurance

3.1.1 The provision or transfer of ownership, of a life insurance contract is exempt

from GST under paragraph 1(l) of Part I of the Fourth Schedule to the GST

Act. This exemption is not extended to brokerage services and services of

arranging for sale of life policies

3

.

3.1.2 For GST purposes, a life insurance contract refers to a contract for the

provision of a life policy within the meaning of the Insurance Act. Examples

of policies that fall within the definition of “life policy” include endowment

policies, investment-linked policies and whole life policies.

3.1.3 Policy and administration fees, which are incidental to the provision of a life

policy contract, may also be exempt.

3.1.4 As long-term personal accident or medical insurance policies (which may be

issued by a life insurance company) do not fall within the description of ‘life

policy’ in the Insurance Act, such insurance policies do not qualify for

exemption from GST.

3.1.5 Currently, all non-life riders (e.g. medical or personal accident riders)

attached to individual life policies are treated as being incidental in nature to

the main life policy. Hence, premiums paid on an individual life insurance

policy, including a personal accident, health or other general rider attached

to the main policy are wholly exempt from GST.

3.1.6 On the other hand, for a group life policy with medical and personal accident

rider issued by an insurance company, only the premiums for the life

component is exempt.

3.1.7 Life policies supplied under a contract with a person belonging outside

Singapore and directly benefiting a person belonging outside Singapore can

be zero-rated under Section 21(3)(j) of the GST Act. For “offshore” life

insurance business, “offshore” life insurance provided to persons belonging

outside Singapore can be zero-rated. However, as an administrative

concession

4

, such insurance policies provided by “offshore” life insurance

business eligible for classification as “onshore” based on guidelines set by

the Monetary Authority of Singapore (“MAS”) may be treated as exempt (and

not zero-rated) for GST purposes.

3

For more information on GST principles applicable to insurance intermediaries, such as agents and

brokers, please refer to paragraph 5.

4

Based on MAS guidelines, offshore life business is eligible for classification as onshore life business

provided it does not exceed S$5 million. Hence, this administrative concession is given to ease

compliance so that the offshore life business does not need to distinguish between zero-rated and

exempt supplies.

GST: Guide for the Insurance Industry

3

3.2 General Insurance

3.2.1 The provision of general insurance contracts is a taxable supply of services.

The GST-registered insurance company is required to charge and account

for GST at the prevailing GST rate on the general insurance premiums unless

the supply qualifies as an international service

5

and can be zero-rated.

3.2.2 Examples of general policies are motor, fire, personal accident, medical and

health, workmen’s compensation, professional indemnity, fidelity guarantee

insurance etc.

3.3 Zero-rating of Insurance Services

3.3.1 As highlighted in paragraph 2.2, the provision of direct insurance services

can be zero-rated if it falls within the description of international services

listed under Section 21(3) of the GST Act.

3.3.2 Generally, the provision of insurance services can be zero-rated if the

policyholder belongs outside Singapore and is outside Singapore at the time

the service is performed

6

. However, for certain general insurance policies

7

,

the belonging status of the insured may be relevant to determine if zero-

rating can apply.

3.3.3 On the other hand, some insurance policies can be zero-rated even though

the policyholder belongs in Singapore. Such policies include those that relate

to international transportation, export of goods, land or goods outside

Singapore.

3.3.4 The zero-rating provisions relevant to the insurance industry are listed below:

(A) Where policyholder may belong in or outside Singapore

• Section 21(3)(c)

8

– Direct insurance relating to international

transportation of goods and passengers from:

a) From a place outside Singapore to another place outside Singapore;

b) From a place in Singapore to a place outside Singapore or

c) From a place outside Singapore to a place in Singapore.

Policies that qualify for zero-rating under Section 21(3)(c) include:

a) Marine/Aviation Cargo Insurance

b) Marine/Aviation Hull Insurance

5

Under Section 21(3) of the GST Act.

6

For life policies, the insured is not regarded as a direct beneficiary for the purpose of zero-rating

under Section 21(3)(j).

7

Examples include directors’ liability insurance where the director’s personal liability is also covered.

8

Section 21(3)(c) allows the zero-rating of services (other than the letting on hire of any means of

transport) comprising the insuring or the arranging of the insurance or the arranging of the transport

of passengers or goods to which any provision of paragraphs (a) and (b) applies.

GST: Guide for the Insurance Industry

4

Only applicable for insurance purchased in respect of commercial

vessels/aircraft involved in the international transportation of goods or

passengers

9

. Hull insurance for pleasure crafts, barges, boats, etc. not

involved in international transportation will not qualify for zero-rating

and is subject to GST.

c) Travel Insurance

Only if the insurance contract is identifiable with international journeys

involving the carriage of passengers to and from outside Singapore.

Policies that do not qualify for zero-rating under Section 21(3)(c) include:

a) Insurance policies taken up by policyholders for the purpose of

overseas employment or study or

b) Health insurance policy with overseas medical coverage

As the above policies do not directly relate to the export of goods, land or

goods outside Singapore or international travel, the premiums are

standard-rated if supplied to a local policyholder

10

. The location of

coverage is not relevant in determining whether the policy can be zero-

rated.

• Section 21(3)(e) – Insurance services supplied directly in connection with

land or any improvement thereto situated outside Singapore.

For example: Insurance premiums charged for fire insurance in respect of

a property in Vietnam or insurance premiums charged for property risk

insurance in respect of a property in Malaysia

• Section 21(3)(f) – Insurance services supplied directly in connection with

goods situated outside Singapore when the services are performed.

• Section 21(3)(h) – Insurance (not reinsurance) upon or against any risks

incurred in the making of advance or the granting of credit directly relating

to –

a) the export of goods (not services) outside Singapore or

b) the supply of goods which involves the removal of goods from a place

outside Singapore to another place outside Singapore.

For example: Export credit insurance

(B) Where policyholder must belong outside Singapore for zero-rating

• Section 21(3)(g) – Insurance services supplied directly in connection

11

with goods for export outside Singapore, where the risk cover is supplied

9

With effect from 1 July 2010, hull insurance for cruise liners used only for cruises to nowhere can

be zero-rated under Section 21(3)(c).

10

See “Belonging status of your customer (an individual)” in paragraph 3.3.4(B).

11

Refer to e-tax Guide ‘Clarification on "Directly in Connection With" and "Directly Benefit"’.

GST: Guide for the Insurance Industry

5

to a person not belonging in Singapore at the time the services are

performed.

• Section 21(3)(j) – Insurance services provided under a contract with a

person who belongs outside Singapore and directly benefit

12

a person

who belongs outside Singapore and who is not in Singapore when the

insurance cover is provided. The cover must not be directly in connection

with any land or goods in Singapore.

For example: Health policy provided to policyholder who is an overseas

individual

Belonging status of your customer (an individual)

For the purpose of Section 21(3)(j), an individual belongs in Singapore if

his usual place of residence is in Singapore during the period the

insurance services are supplied.

Administratively, the Comptroller of GST regards the residential address

of an individual as his "usual place of residence". Hence, if your customer

provides a Singapore residential address, he shall be regarded as

belonging in Singapore for GST purposes.

However, if the individual stays overseas to study or work and he has

more than one residential address, the Comptroller is prepared to accept

that the individual belongs overseas if all of the following conditions are

satisfied:

a) He is absent from Singapore for a continuous period of at least one

year. It does not matter that he spends his holidays in Singapore

during that one year. During that year, his temporary return to

Singapore for vacation or other reasonable purposes is acceptable;

b) He stays at a fixed place in the overseas country and

c) Where he is working in the overseas country, his overseas assignment

must not be incidental to his employment in Singapore.

For example: student insurance policy providing insurance coverage of

more than a year while the student stays overseas

Policies that do not qualify for zero-rating under Section 21(3)(j) include:

Insurance policies taken up by local policyholders to insure against losses

to their shareholdings in overseas companies or loans provided to

overseas persons.

3.4 Time of Supply for Premiums

3.4.1 Where premiums are paid in a lump sum, output tax will be accounted for

based on the earlier of the following:

12

Refer to e-tax Guide on “GST: Clarification on ‘Directly in Connection With’ and ‘Directly Benefit’”.

GST: Guide for the Insurance Industry

6

a) When an invoice is issued or

b) When payment is received.

The issuance of any type of invoice will be an event that triggers the time of

supply. This includes a tax invoice as well as any document that serves as a

bill for payment for supplies made by a GST-registered supplier. An example

of such document would be a debit note.

3.4.2 In general, documents, such as sales order, pro-forma invoice, statement of

accounts and letter/statement of claims are not considered invoices for GST

time of supply purposes. This is because these documents are often not

billing for payments and would therefore not be treated as invoices based on

normal commercial practices. For more details, please refer to the e-Tax

Guide on “GST: Time of Supply Rules”.

3.4.3 Where premiums are in instalments, the time of supply is the earlier of:

a) The date when each instalment payment becomes due or

b) The date of payment.

3.5 Estimation of Output Tax for Premiums Collected on Behalf of the Insurance

Company

3.5.1 An insurance intermediary may collect premiums on behalf of the insurance

company from the policyholder. For GST purposes, premiums collected by

the insurance intermediary are considered as received by the insurance

company. If the tax invoice has not been issued earlier, the collection of

premiums by the insurance intermediary on behalf of the insurance company

would trigger the time of supply.

3.5.2 The insurance intermediary should then inform the insurance company on

the collection of premiums, as the insurance company is required to account

for GST on insurance premiums collected on insurance contracts that do not

qualify for exemption or zero-rating.

3.5.3 However, the insurance company may face difficulties in capturing the exact

amount of output tax in a prescribed accounting period if the insurance

intermediary does not inform the insurance company on time. In view of such

difficulties, the insurance company may apply to the Comptroller of GST in

writing for estimation of output tax under Regulation 60 of the GST (General)

Regulations.

3.5.4 Upon approval, the insurance company will be allowed to estimate whole or

a portion of the output tax payable in an accounting period based on a

formula allowed by the Comptroller. The estimated output tax for the previous

accounting period will be adjusted in the next accounting period when the tax

invoices for premiums received are issued.

3.5.5 Example: Insurance Company A collected $90,000 in premiums for the

period Jul to Sep 2016. Company A’s backlog in issuing tax invoices is one

GST: Guide for the Insurance Industry

7

month and it estimates the output tax due to the Comptroller for the last

month of the next quarter (Oct to Dec 2016) with the following formula:

Estimated output tax for Dec 2016

= Monthly average of actual premiums for previous quarter (i.e. Jul to

Sep 2016) multiplied by 1 month of backlog multiplied by prevailing

GST rate

13

(i.e. 7%)

= ($90,000/3) X 1 month X 7%

= $2,100

Assuming Company A collected S$75,000 in premiums for Oct to Nov 2016,

GST amount is $5,250.

Company A should declare in its GST return:

In Box 1: $75,000 +$30,000 (estimated) = $105,000 (Value of standard-rated

supplies)

In Box 6: $5,250 + $2,100 (estimated as above) = $7,350.

In the next quarter, Company A would have known the exact amount of

premiums and GST collected for Dec 2016 (assuming $40,000 and GST

amount: $2,800) and is required to make adjustments in the next quarter

(January to Mar 2017).

The Company is required to deduct from Box 1 ($30,000) and Box 6 ($2,100)

and add the exact amount of premiums and GST collected to Box 1 ($40,000)

and 6 ($2,800).

Company A will have to compute the amount of estimated output tax for the

month of Mar 2017 based on the monthly average of actual premiums for Oct

to Dec 2016.

3.6 Specific Issues Affecting Insurance Companies

3.6.1 Cash Payments

GST-registered insurance companies are allowed a credit for input tax

deemed incurred on the Cash Payments when the conditions listed in

paragraph 3.2 of the e-Tax guide “GST Guide on Insurance: Cash Payments

and Input Tax on Motor Car Expenses” are satisfied.

3.6.2 Input Tax on Motor Car Expenses

The insurance company is allowed to claim input tax incurred on goods or

services purchased for the purpose of its business of making taxable supplies.

A GST-registered insurance company is allowed to claim input tax incurred

on motor car expenses if all conditions listed in paragraph 4.4 of the e-Tax

13

GST rate was increased from 5% to 7% in Jul 2007.

GST: Guide for the Insurance Industry

8

guide “GST Guide on Insurance: Cash Payments and Input Tax on Motor Car

Expenses” are satisfied.

3.6.3 Premium Refunds

Insurance companies may make refunds to policyholders under certain

conditions. Some insurance companies may use the refunds to offset

premiums payable.

Generally, the insurance company should not reduce the value of insurance

services previously supplied and corresponding output tax when a refund is

made upon the occurrence of an insured event, or an event other than the

insured event, e.g. no claims being made, or termination of the policy plan

after a specified minimum number of years etc.

However, the refunds can be treated as discounts against the insurance

premiums if the payment of the refund is connected with the renewal of the

insurance contract, and the refund is offset against the premium. GST on the

subsequent premium may be accounted on the net premium payable.

3.6.4 Investment-Linked Policies (ILP)

Life insurance companies may offer ILP with a combination of protection and

investment elements. Premiums received from the policyholder are typically

invested in professionally-managed investment-linked funds (ILFs), in return

for units allocated to the policyholder.

Generally, the insurance company charges fees, such as fund management

fees, surrender fees and redemption fees, to defray its costs of administering

the ILP. Such fees and charges are separately disclosed and typically settled

via a reduction in units of ILFs allocated to the policyholder.

For GST purposes, we are prepared to treat an ILP as a single supply of life

policy and exempt the premiums from GST for the ILP on the following basis:

a) The main purpose of the policyholder is to purchase a life insurance

policy and not merely an investment product;

b) The investment element is always provided together as a package

with the life insurance contract

14

and

c) The ILP falls within the definition of a ‘life policy’ in the Insurance Act.

Similarly, fees and charges in relation with an ILP will be treated as additional

consideration for an exempt supply arising from the provision of a life

insurance contract, under paragraph 1(l) of Part I of the Fourth Schedule to

the GST Act.

14

The investment element can be considered as an enhancement to the life protection element of

the policy as it allows for the potential of higher returns to increase the cash value of the policy, as

opposed to leaving the investment decisions to the insurance company in traditional life policies.

GST: Guide for the Insurance Industry

9

3.6.5 Insurance Excess

There are some situations where the policyholder is not fully-insured and is

required to bear an amount of excess in the event of loss.

The following section describes the scenarios when the recovery of insurance

excess is treated as a supply and the corresponding GST treatment:

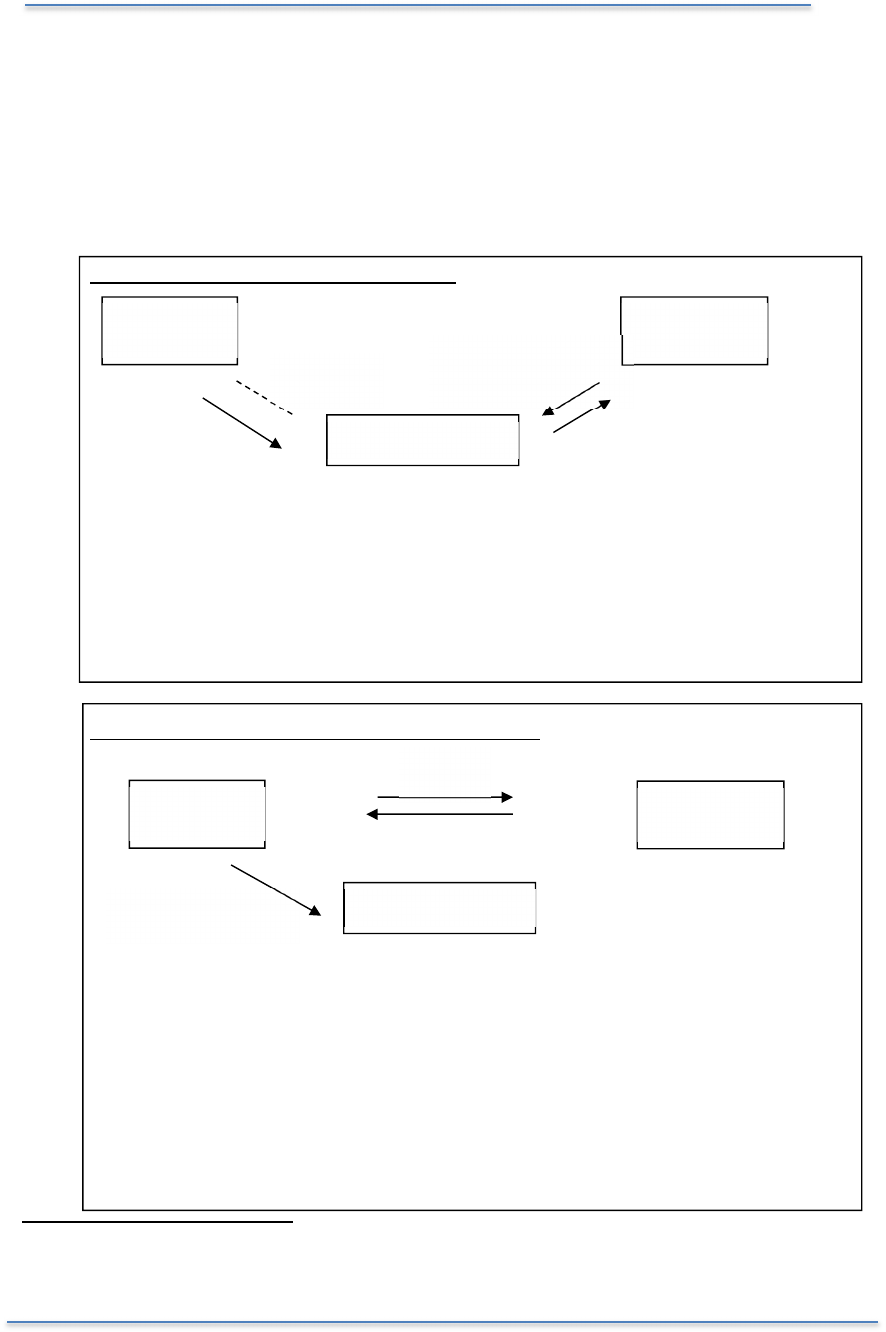

Scenario 1: Supplier bills the insured

When the supplier bills the policyholder for vehicle repair services, the

insured cannot claim the GST incurred if he is a non- GST registered person.

Assuming the insurance company will bear the amount of expenses

exceeding $500, the policyholder will recover $1,000 from the insurance

company. In this case, the insurance company is treated as making a Cash

Payment indemnifying the insured according to the insurance contract

15

.

Scenario 2: Supplier bills insurance company

If the insurance company contracted for the supply of 3rd party services to fulfill its

obligations under the insurance contract to the policyholder, the 3rd party would bill

the insurance company for the full value of services rendered. The insurance

company will recover the excess from the policyholder. The recovery of excess by

the insurance company is treated as a taxable supply of service and hence GST is

chargeable on the recovery of excess from the policyholder.

Whether the recovery of excess $500 should be treated as inclusive of GST or

exclusive of GST depends on terms and conditions of the insurance contract

between the policyholder and insurance company16.

15

See section 3.2 of the e-Tax Guide “GST Guide on Insurance: Cash Payments and Input Tax on

Motor Car Expenses” on conditions of claiming deemed input tax for Cash Payment.

16

For both the examples under Scenarios 2 and 3, it is assumed that the policyholder only bears

excess of $500 inclusive of GST. If the excess is inclusive of GST, GST is computed by using the

Insurance

Company

Supplier

Policyholder

Cash payment

$1,000

Excess of

$500

Tax invoice of

$1,500 (inclusive of

GST

Pays

$1,500

Supplier

Insurance

Company

Policyholder

Tax invoice of $1,500

(inclusive of GST)

Tax invoice $500

(inclusive of GST)

Pays

$1,500

GST: Guide for the Insurance Industry

10

Scenario 3: Supplier issues two invoices (where the supplier has two

contracts of services; one with the insurance company for part of the bill

payable by the insurance company and the other with the policyholder for the

amount of excess payable by the policyholder)

Feedback from the industry highlighted that it is a common market practice

for the supplier to split their bills between the insured and the insurance

company. In order not to disrupt this business practice, the supplier is allowed

to continue this practice to split the bill and issue 2 tax invoices to the

policyholder and the insurance company respectively.

When the supplier splits its bill, both bills should attract GST, as there is a

taxable supply of services provided to both the insurance company and the

policyholder. Whatever the excess amount the supplier collects from the

policyholder, the amount should be treated as inclusive of GST.

3.6.6 Recovery of Third Party Claims

Where a third party (i.e. Policyholder A) causes the damage, the insurance

company of the victim (i.e. Company Y) usually recovers the full amount or

part of the repair cost

17

from the third party or the insurance company of the

third party. Company Y is not regarded as making any supply to the third

party or his insurance company X when it recovers the cost. This is because

the payment is regarded as a form of compensation from the third party or

his insurance company.

tax fraction [i.e. GST rate / (100% + GST rate)] multiplied by the excess recovered. If it is exclusive,

GST is computed using the prevailing GST rate multiplied by the excess recovered.

17

Assumption: Both cars belonging to the victim and the party at fault are damaged. Hence, there

are two suppliers (repair workshops) involved.

Insurance

Company

Supplier

Policyholder

Tax invoice $500

(inclusive of GST)

Tax invoice

$1,000 (inclusive

of GST

Insurance

Company X

Policyholder A

(at fault)

Person B (Victim) or

Person B’s Insurance

Company Y

Insurance policy

Recovers an

agreed amount

Supplier 1

Issues tax

invoice

Issues tax

invoice &

recovers excess

of $500

Makes Cash Payment

Supplier 2

Issues tax

invoice

GST: Guide for the Insurance Industry

11

3.6.7 Recovery of Medical Expenses from Agents / Policyholders

The insurance company may require potential policyholders to undergo

medical check-ups to ascertain their risk profile and the premiums required

to underwrite the policies. The insurance company would generally bear the

medical costs of the compulsory medical check-ups undergone by the

policyholders.

However, the insurance company may recover the cost of medical check-ups

from the agent or policyholder in certain situations.

In general, the recovery of expenses is treated as a taxable supply of services

where GST is chargeable. However, where one party breaches his

contractual obligations and causes the other party to incur a loss, the

recovery of expenses is not a supply and is not subject to GST. The GST

treatment for the scenarios in which the insurance company may recover

medical expenses from the policyholder or insurance agent is shown below:

Scenario Taxable?

Reason

(a) The insurance company

unilaterally cancels the insurance

policy even though the insurance

agent did not breach any of the

terms in the agency agreement

and recovers medical expenses

from the insurance agent.

Yes The recovery of expenses

from the insurance agent did

not result from a breach of

terms of contract by the

insurance agent. Rather, it is

the unilateral decision of the

insurance company to

cancel the policy.

(b) The insurance company

cancels the insurance policy due

to fraud or misrepresentation by

the policyholder and recovers

medical expenses from the

insurance agent.

Yes The recovery of expenses

from the insurance agent did

not result from a breach of

terms of contract by the

insurance agent.

(c) The insurance agent breaches

any of his obligations under the

agency agreement with the

insurance company, resulting in a

loss to the insurance company

and the latter recovers the medical

expenses from the agent.

No The recovery of expenses

from the agent resulted from

a breach of the terms under

the agency agreement.

(d) The potential policyholder

failed to pay the first premium or

first installment of premium within

the grace period stated in letter of

acceptance and the insurance

company recovers the medical

Yes The recovery of expenses

from the insurance agent did

not result from a breach of

terms of contract by the

insurance agent. Rather, it is

the unilateral decision of the

GST: Guide for the Insurance Industry

12

expenses from the insurance

agent.

policyholder not to pay the

premiums.

(e) The policyholder decides not to

take up the policy within the free

look period after signing the policy

and the insurance company

recovers the cost of medical

checkups from the policyholder.

Yes The policyholder did not

breach any terms of the

insurance contract as he has

the right to cancel the policy

within the free look period.

4 Reinsurance Companies

4.1 The provision of general reinsurance or life reinsurance contract is an exempt

supply of financial service under the Fourth Schedule to the GST Act. Hence,

premiums arising from such reinsurance contracts placed locally are exempt

from GST.

4.2 The premiums of a reinsurance contract would qualify for zero-rating under

Section 21(3)(j) if it is a supply made ‘under a contract with’, and which

‘directly benefits’ a person belonging outside Singapore, and who is outside

Singapore when the service is performed. Hence, reinsurance premiums

received from cedants belonging outside Singapore can be zero-rated.

4.3 It should be noted that reinsurance cover is not treated as supplied directly

in connection with goods or land. Hence, the only zero-rating provision for

reinsurance cover is Section 21(3)(j). It is not necessary to ascertain if

reinsurance coverage would qualify for zero-rating under other provisions

such as Sections 21(3)(e), (f), (g) and (h).

5 Insurance Intermediaries

5.1 Commissions and Fees Received for Arranging Direct General/ Life

18

Insurance

5.1.1 Insurance companies may engage insurance intermediaries, such as agents,

brokers

19

and financial advisers

20

to solicit, sell and arrange for insurance

contracts with policyholders.

5.1.2 Generally, the commissions and fees (including profit commission, overriding

commission or other product-related payments) charged by a GST-

registered insurance intermediary for introducing and arranging direct

general or life insurance policies (“introductory services”) is subject to GST

18

As mentioned in paragraph 3.1.1, brokerage and commission arising from the arranging for the

sale of life policies is not exempt from GST.

19

The GST-registered agent/broker refers to an agent/broker who carries on a business and is

registered independently for GST purposes. An agent employed under a contract of employment

with the insurance company is an employee and is not required to register for GST.

20

Financial advisers are licensed under the Financial Advisers Act.

GST: Guide for the Insurance Industry

13

at the standard-rate if the recipient of the services (the insurance company

or policyholder depending on who the insurance intermediary has a contract

with) belongs in Singapore and at 0% if the recipient belongs outside

Singapore.

5.1.3 An insurance business is treated as belonging in Singapore when:

a) It has a business establishment or some fixed establishment in Singapore

and nowhere else;

b) It is legally constituted in Singapore (e.g. company incorporated in

Singapore) and has no business or fixed establishment in any other

country or

c) It has establishments both in Singapore and outside of Singapore but

services are most directly used or to be used by the establishment in

Singapore.

5.2 Overseas Insurance Companies with Branches in Singapore

5.2.1 In Singapore, MAS requires overseas insurance companies to set up local

branches in order to conduct insurance business in Singapore

21

. Only the

local branch that is registered with the MAS can carry on an insurance

business in Singapore. Its overseas head office or other overseas branches,

are not allowed to solicit insurance business in Singapore. Hence, the local

branch is regarded as carrying on the business of the overseas insurance

company in Singapore and therefore belongs in Singapore for GST purposes.

5.2.2 Singapore policies

Only the licensed local branch can market and sell insurance policies

covering domestic risk (“Singapore policies”) to residents in Singapore

22

.

Commissions received for providing introductory services in respect of

Singapore policies is standard-rated

23

, unless the Singapore policies qualify

for zero-rating as described in paragraph 5.2.6 below

24

.

5.2.3 Offshore policies

21

According to the Insurance Act, “insurance business in Singapore” means the business of

assuming risk or undertaking liability in Singapore under policies, and of —

(a) receiving proposals for policies in Singapore;

(b) issuing policies in Singapore or

(c) collecting or receiving premiums on policies in Singapore.

22

The local branches can only sell MAS-approved products to local policyholders and they have to

record such insurance premiums (regardless of whether the policies are underwritten by the

overseas establishment or the local branches) in their books. For definitions of ‘residents in

Singapore’, please refer to the Insurance Act.

23

This is so even if you do not liaise with the local branch in your day-to-day operations.

24

For insurance intermediaries that have sought MAS's approval to solicit Singapore insurance

business for unlicensed overseas insurance companies, such introductory services can be zero-

rated if all the conditions under Section 21(3)(j) are satisfied. This is so even if the policyholder may

be a local person. However, if your introductory services are provided to the local policyholder and

the policyholder pays you a fee, the fee will be subject to GST at the standard rate.

GST: Guide for the Insurance Industry

14

In Singapore, both the licensed local branch and the overseas insurance

company can sell policies that relate to risks outside Singapore (“offshore

policies”). Hence, when the insurance intermediary provides introductory

services for offshore policies, it is required to establish whether its

introductory services are provided to the local branch or the overseas

insurance company. Information, such as which insurance entity records the

insurance premiums in its accounting books or which entity is responsible for

paying the commission for the introductory service rendered can help to

determine this fact.

5.2.4 If the introductory services in respect of offshore policies are provided to the

local branch, the GST-registered insurance intermediary should account for

GST on its commission and fees. However, if the insurance intermediary’s

introductory service for offshore policies is provided to an overseas insurance

company

25

, the commission charged will qualify for zero-rating under Section

21(3)(j) of the GST Act.

5.2.5 It should be noted that commissions and fees charged for services provided

by the insurance intermediary are not treated as supplied directly in

connection with any land or goods.

5.2.6 Where the insurance intermediary’s brokerage services supplied involve the

arranging of insurance policies relating to international transportation of

goods or passengers, it will qualify for zero-rating under Section 21(3)(c) of

the GST Act. Generally, commission charged for the arranging of the

following policies can be zero-rated:

a) Marine cargo /marine hull insurance

b) Aviation cargo, aviation hull insurance

c) Travel insurance (which is identifiable with journeys involving carriage

of passengers to and from outside Singapore).

5.2.7 In the event that the insurance company cannot zero-rate the premiums of

the above policies, the insurance intermediary’s commission will similarly not

qualify for zero-rating.

Other non-monetary commission

5.2.8 The GST-registered insurance intermediary may receive services or goods

as commission. These are non-monetary consideration received for services

provided by the insurance intermediary. Hence, if the insurance intermediary

is GST-registered, he is also required to account for GST based on the open

market value of the goods or services received.

Lucky draws

5.2.9 Instead of commission, the GST-registered insurance intermediary may

receive a chance to participate in a lucky draw organized by the insurance

25

The contract for introductory services must not be with the local branch for zero-rating to apply.

GST: Guide for the Insurance Industry

15

company in return for meeting sales targets. He is not required to account

for GST on the value of lucky draw chance received.

5.2.10 If the insurance intermediary wins a prize through the lucky draw, the prize

is not regarded as a consideration for the services rendered by him

26

. Hence,

the GST-registered insurance intermediary is not required to account for GST

on goods or services received as prizes through lucky draws.

5.2.11 On the other hand, the GST-registered insurance company is deemed to be

making a supply of goods if the goods are given away as lucky draw prizes.

Hence, it is required to account for GST based on the open market value of

the goods unless

27

:

The cost of the gift is $200 or less; or

It had not claimed GST on the purchase or import of the goods.

5.3 Brokerage/Commission for Reinsurance Contracts

5.3.1 In inward reinsurance, reinsurance commission (including overriding

commission and profit commission) payable to the GST-registered cedant is

exempt from GST if the reinsurance company belongs in Singapore and

zero-rated if the reinsurance company belongs outside Singapore.

5.3.2 In outward reinsurance, the reinsurance commission payable to the

reinsurance company by the retrocessionaire is exempt from GST if the

retrocessionaire belongs in Singapore and zero-rated if the retrocessionaire

belongs outside Singapore.

5.3.3 If a GST-registered insurance intermediary arranges for the provision of

reinsurance contract, the commission charged by him is exempt from GST if

the recipient of his services belongs in Singapore and zero-rated if the

recipient belongs outside Singapore.

5.4 Time of Supply for Commissions and Fees

5.4.1 For commissions and fees, the insurance intermediary should account for

output tax based on the earlier of the following:

a) When an invoice

28

is issued by the GST-registered insurance

intermediary or the insurance company under self-billing arrangement

or

26

For GST purposes, there is no direct nexus between the lucky draw prize received and the services

rendered by the insurance intermediary.

27

Prior to 1 Oct 2012, if the cost of the goods given free to the insurance intermediary is not more

than $200 and the goods do not form a series or succession of gifts given to the same insurance

intermediary, no supply is treated as being made by the GST-registered insurance company.

28

Prior to 1 January 2011, the issuance of a tax invoice, and not any other type of invoice is an event

that will trigger the time of supply. With effect from 1 January 2011, the issuance of any type of

invoice will be an event that triggers the time of supply. This includes a tax invoice and any document

that serves as a bill for payment for supplies made by a GST-registered supplier. An example would

GST: Guide for the Insurance Industry

16

b) When payment is received.

5.4.2 If payment is received before an invoice is issued, a tax invoice has to be

issued within 30 days to the GST-registered insurance company from the

date the payment is received. This is because GST-registered customers

require a tax invoice to support their input tax claims.

5.4.3 When payment is regarded as received

For GST-registered insurance intermediaries that are required to pay the

gross premiums collected from policyholders (without deducting

commissions) to the insurance companies, they should account for output

tax on the commissions in the prescribed accounting period when the

commissions are received from the insurance companies, if no tax invoice

has been issued previously. A tax invoice should then be issued to the

insurance companies within 30 days from the receipt of commissions.

For GST-registered insurance intermediaries that are allowed to deduct their

commissions directly from the premiums collected before remitting the net

amount to the insurance companies, they are required to account for output

tax on the commissions once premiums have been collected from the

policyholders. A tax invoice should be issued to the insurance company

within 30 days from the receipt of premiums if it was not issued earlier.

This is because the payment of premiums by the policyholder to the

insurance intermediary is deemed as received by the insurance company.

The insurance company is regarded as having accepted the insurance

business and the service provided by the insurance intermediary is complete

once the latter receives the premiums. Hence, the insurance intermediary

would be entitled to the commission once premiums are received from the

policyholder.

6 Tax Invoice

29

6.1 It should be noted that insurance premiums and commissions are

consideration for separate supplies of services. The premium is due to the

insurance company for its supply of insurance services to the policyholder.

On the other hand, commission is consideration due to the insurance

intermediary for its supply of services (of arranging direct insurance) to the

insurance company.

be a debit note. In general, documents, such as sales order, pro-forma invoice, statement of

accounts and letter/statement of claims are not considered as invoices for GST time of supply

purposes. This is because these documents are often not billing for payments and would therefore

not be treated as invoices based on normal commercial practices.

29

For details on the particulars required on a tax invoice, refer to “GST: General Guide for

Businesses”.

GST: Guide for the Insurance Industry

17

6.2 GST on insurance premiums is based on the value of the premiums while

GST on commissions is based on the value of commissions. The calculation

of GST should not be based on the net value of the premium and commission.

6.3 There should be separate tax invoices issued by the GST-registered

insurance company to the policyholder for the premiums

30

and the GST-

registered insurance intermediary to the insurance company for the

commission charged.

6.4 The insurance intermediary may raise a debit note to the policyholder for the

collection of the insurance premium on behalf of the insurance company. As

it is the insurance company that supplies the insurance services to the

policyholder, the insurance company should issue a tax invoice to the

policyholder. Therefore, the debit note issued by the insurance intermediary

should not be mistaken as a tax invoice for GST purposes.

6.5 The insurance intermediary is advised to attach the tax invoice issued by the

insurance company to his own debit note when he bills the policyholder. The

insurance intermediary should indicate the following words on his debit

note

31

“This is not a Tax Invoice. The insurance company’s tax invoice is

attached or will be sent to you shortly.”

6.6 The insurance company may also choose to issue a receipt instead of a tax

invoice to a non-GST registered policyholder for the premium. The receipt

must be serially printed and must show the following:

Insurance company’s name and GST registration number

Date of receipt;

Total amount payable including total GST; and

The words "price payable includes GST".

The insurance company must retain a duplicate of the receipts issued.

7 Self-Billing

7.1 It is a common practice for insurance companies to determine the value of

an insurance intermediary’s commission and other compensation

32

. For

administrative ease, the insurance company may wish to adopt self-billing so

that the insurance company prepares the tax invoice, on behalf of the

insurance intermediary, for services provided by the latter.

30

Refer to Appendix 1 for a sample of the tax invoice to be issued by the insurance company.

31

Refer to Appendix 2 for a specimen of the debit note to be issued by the insurance intermediary.

32

Insurance companies would have readily available information, such as agency contracts to

determine the final value of commissions payable to the insurance intermediaries.

GST: Guide for the Insurance Industry

18

7.2 Specifically, self-billing can be used to cover transactions with GST-

registered insurance intermediaries, such as cash agents

33

as well as credit

agents and brokers

34

with principal accounts.

7.3 Self-billing can only be used after the insurance company has performed a

self-review and made a declaration that it is able to satisfy all the conditions

indicated on the ‘Checklist for Self-Review of Eligibility and Declaration on

Use of Self-Billing’.

7.4 GST-registered insurance intermediaries that do not have existing self-billing

arrangements with the GST-registered insurance companies they are acting

for, should ensure that they issue tax invoices according to rules outlined in

paragraph 5.4.3.

33

A cash agent is one who does not have a Principal’s Account (i.e. a separate bank account opened

and maintained by the agent as trustee for the insurer who is the principal). It receives payment on

the insurance premiums made to the insurance company by the policyholder and hands over all

premiums collected from the policyholder to the insurance company.

34

Credit agents and brokers refer to those that operate a Principal’s Account and receive payment

on the insurance premiums from the policyholders. They deposit the premiums collected into the

Principal’s Account after deducting the commissions due to them.

GST: Guide for the Insurance Industry

19

8 Summary: GST Treatment of Insurance Products and

Brokerage/Commission

8.1 The following table states generally the GST treatment for various types of

insurance products and the relevant zero-rating provisions. It is not meant to

be exhaustive and the insurance companies should determine the GST

treatment for their policies based on the nature of the insurance contracts

(and not merely based on the terminology used for their policies).

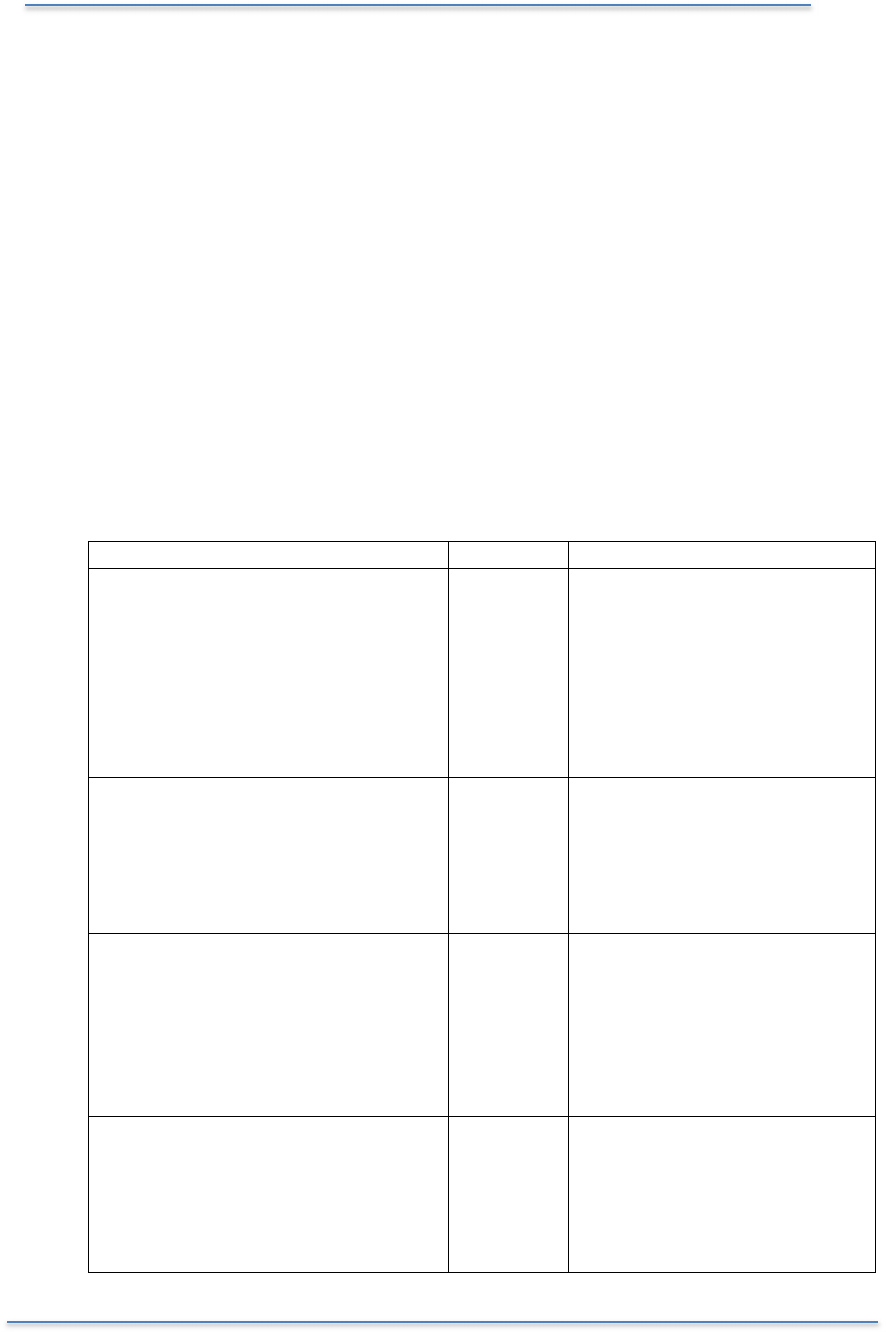

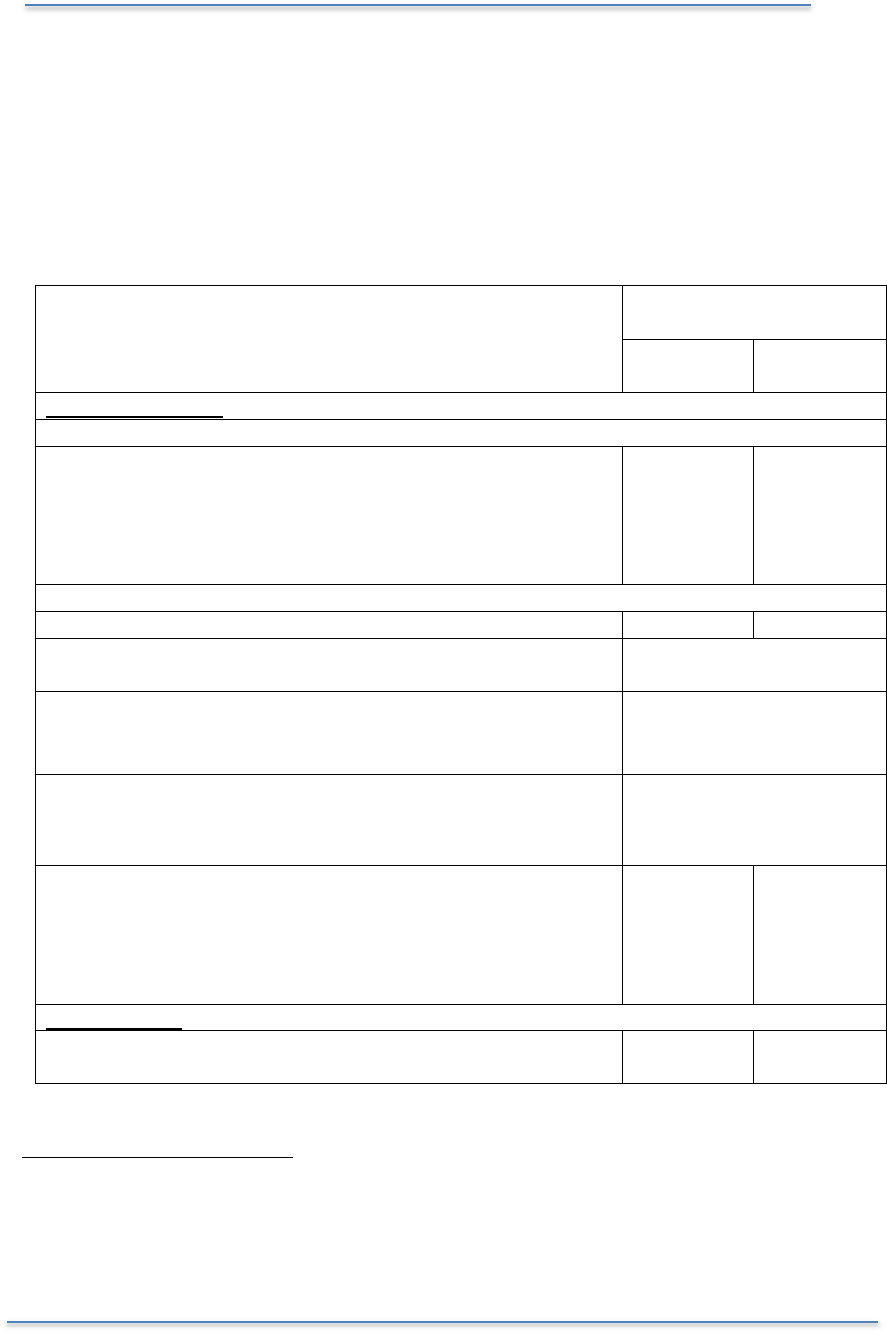

Type Of Insurance Policy

GST treatment for

customer belonging

In

Singapore

Outside

Singapore

Direct Insurance

Premiums

–

Life Policies

−

Life Policy - Individual

35

(e.g. endowment, whole life)

− Life Policy - Group

36

− Life Annuity

− Term Life Insurance

− Investment Linked Policy

EX ZR

[s21(3)(j)]

Premiums

-

General Insurance Policies

Workmen’s Compensation Insurance SR NA

Motor Insurance in respect of vehicles registered in

Singapore SR

−

Aviation/ Marine Hull Insurance

37

− Aviation/ Marine Cargo Insurance

38

− Travel Insurance

ZR [s21(3)(c)]

Fire and Theft

− In respect of land/goods in Singapore

− In respect of land/goods outside Singapore

SR

ZR [s21(3)(e), s21(3)(f)]

−

Public Liability Insurance

− Medical and Accident Insurance

− Professional Indemnity Insurance

− Mortgagee’s Interest Insurance

− Political Risk Insurance

SR ZR

[s21(3)(j)]

39

Reinsurance

Reinsurance Policy EX ZR

[s21(3)(j)]

35

Including personal accident or medical rider attached to main policy.

36

Excluding riders attached to the main policy, riders are standard-rated if customer belongs in

Singapore.

37

Vessel/aircraft must be used for international transportation of goods/passengers.

38

Cargo must be carried in an international voyage.

39

Customers for general policies may refer to both the policyholder and the insured depending on

the type of coverage.

GST: Guide for the Insurance Industry

20

Abbreviation:

SR – Standard-rated EX – Exempt ZR – Zero-rated NA – Not applicable

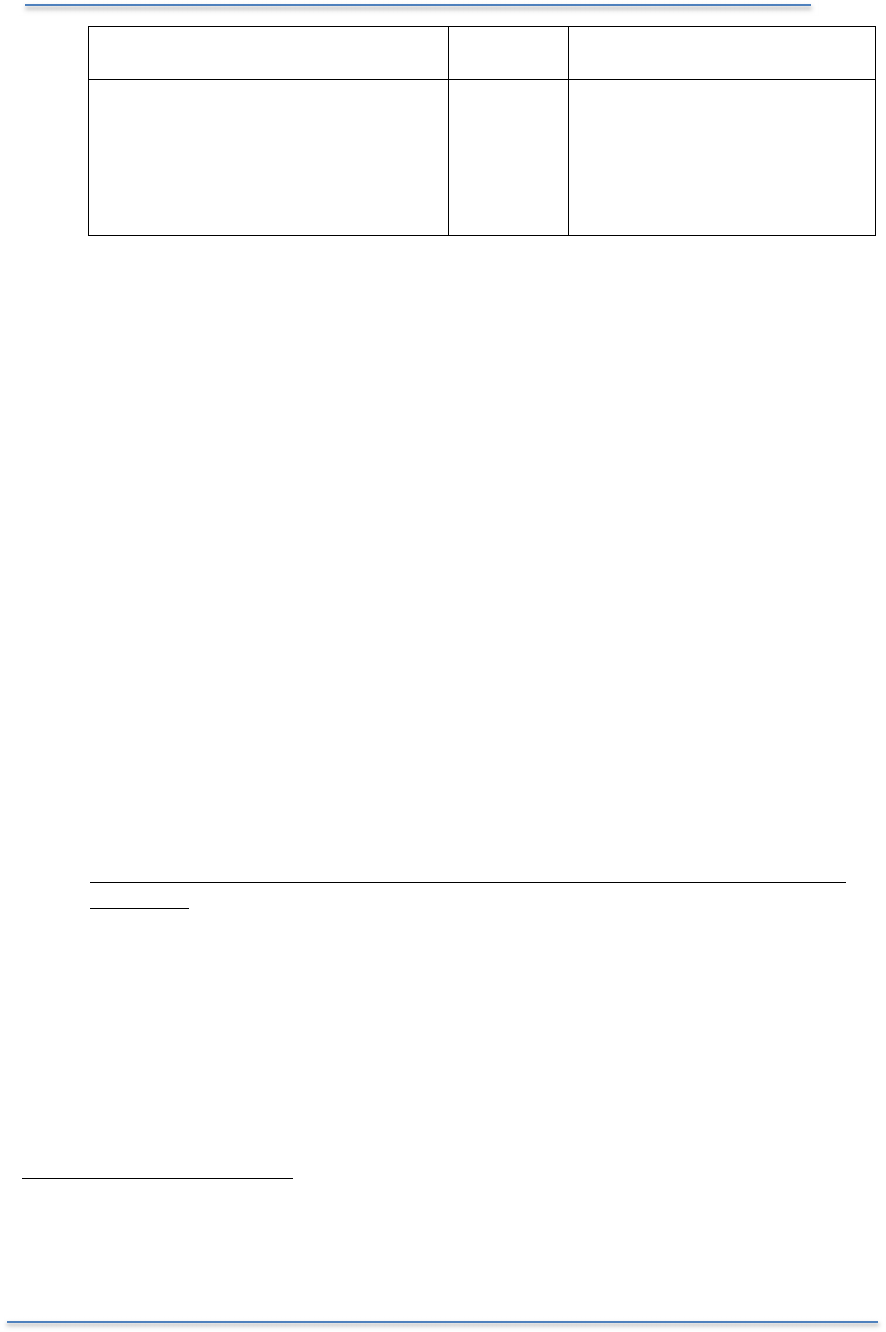

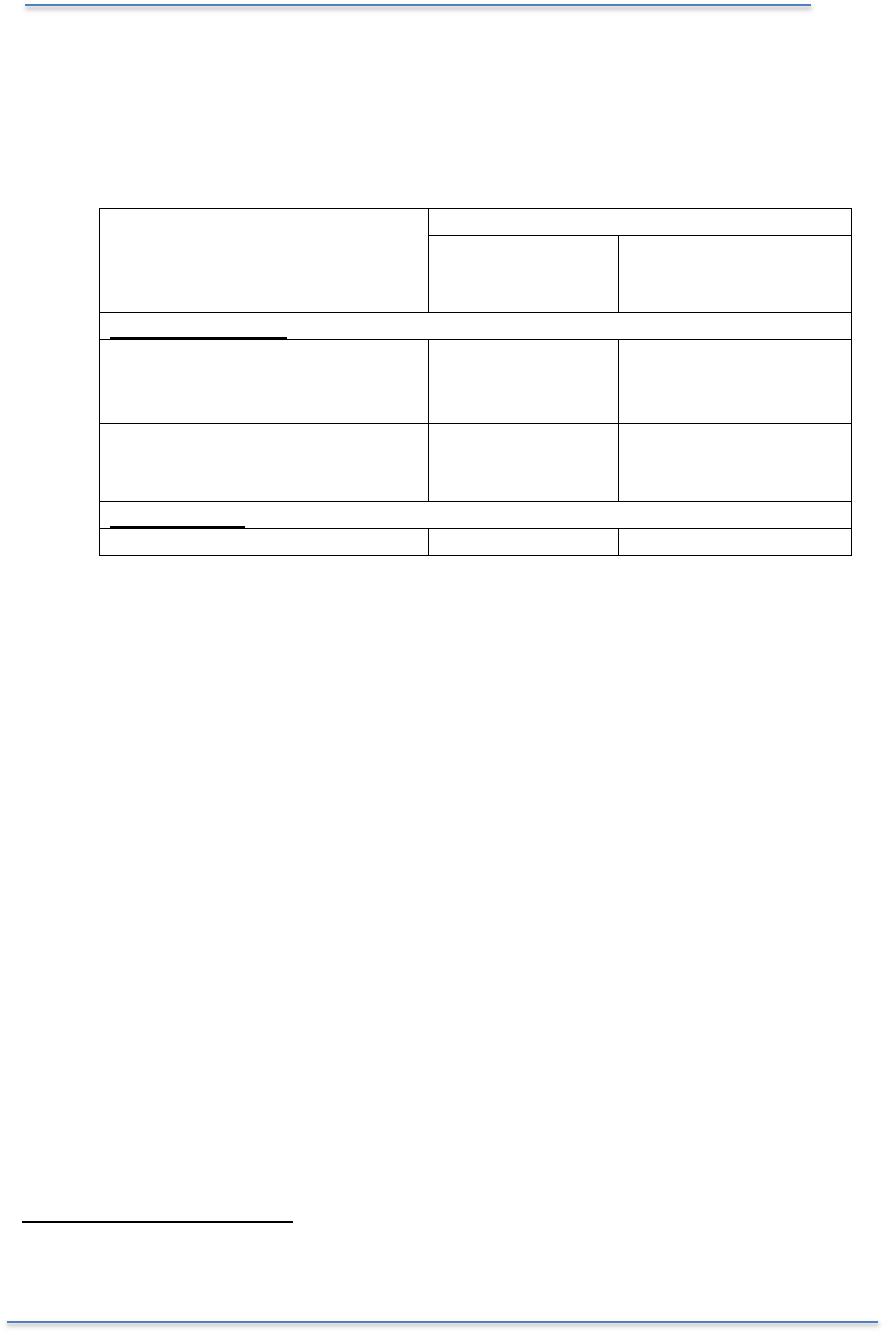

8.2 The following table states generally the GST treatment for brokerage,

commission and other fees received by insurance intermediaries for their

services.

Brokerage, commission and

other fees charged for

arranging the following

policies:

GST treatment for customer

40

belonging

In Singapore Outside Singapore

Direct Insurance

−

Aviation/ Marine Hull

− Aviation/ Marine Cargo

− Travel

ZR [s21(3)(c)] ZR [s21(3)(c)]

All other life or general

insurance products excluding

the above

SR ZR [s21(3)(j)]

41

Reinsurance

Reinsurance commission EX ZR [s21(3)(j)]

40

Customer can refer to either the insurance company or the policyholder, depending on who has

contracted for the insurance intermediary’s services.

41

Where the arranging services are zero-rated under Section 21(3)(j), the overseas customer must

be outside Singapore when the services performed.

GST: Guide for the Insurance Industry

21

9 Contact Information

9.1 For enquiries on this e-tax guide, please contact:

Goods & Services Tax Division

Inland Revenue Authority of Singapore

55 Newton Road

Singapore 307987

Tel: 1800 356 8633

Fax: (+65) 6351 3553

Email: gst@iras.gov.sg

GST: Guide for the Insurance Industry

22

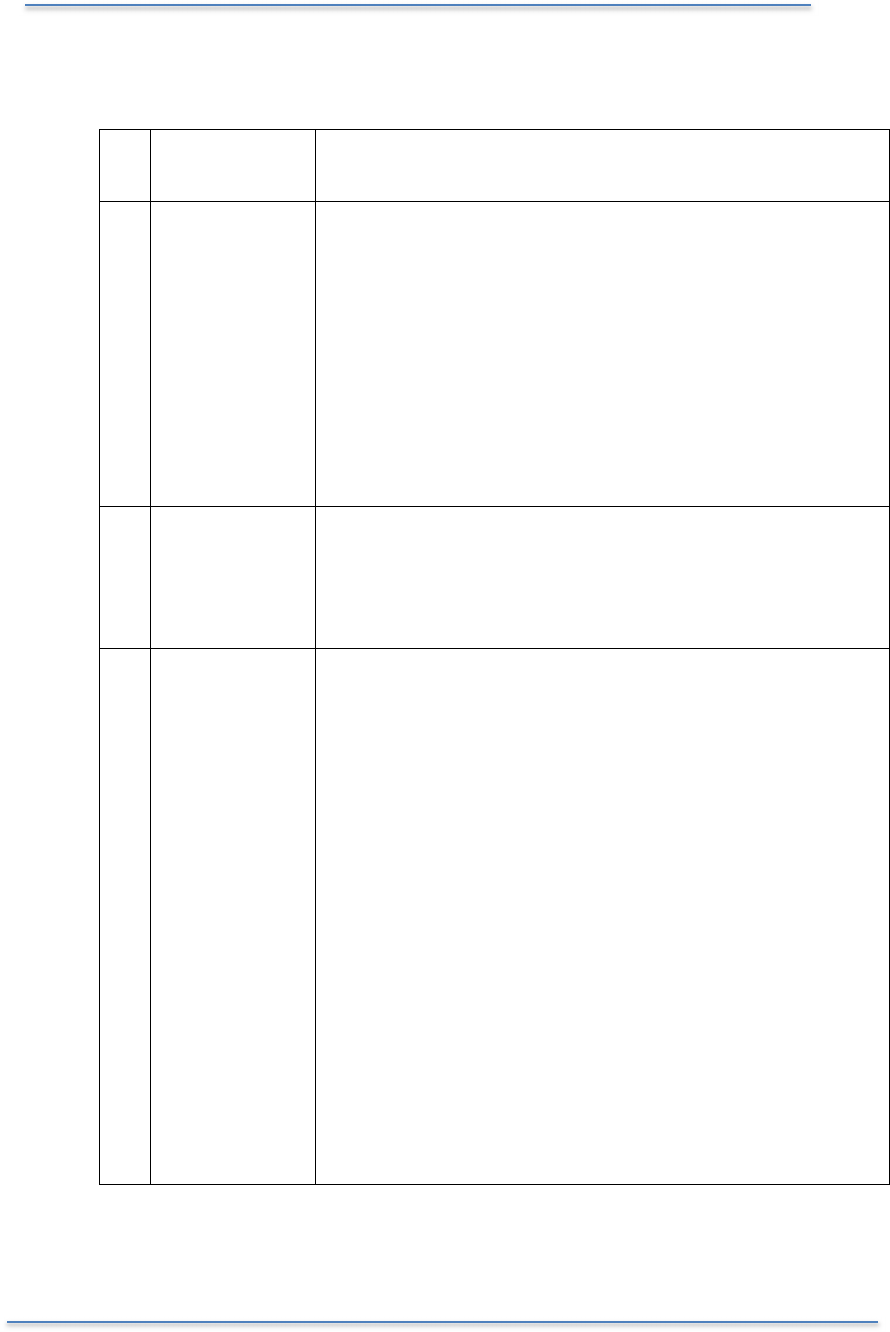

10 Updates and Amendments

Date of

amendment Amendments made

1 14 Nov 2014 (i) Inserted paragraphs 5.1.6 to 5.1.9 (GST treatment

on non-monetary consideration received by brokers

/ agents) and 6.6 (information required on receipt

issued).

(ii) Revised paragraphs 3.3.2 and 3.3.3 (relevancy of

insured for zero-rating of general insurance policies).

(iii) Inserted footnotes 4, 6, 7, 20, 21, 25, 26 and 30.

(iv) Editorial amendments to paragraphs 2.2 and 3.1.4

and footnotes 10 and 15. Re-formatting of tables

under paragraphs 8.1 and 8.2.

2 10 Jun 2016 (i) Inserted paragraphs 5.1.2, 5.2, 5.2.1 to 5.2.4 and

footnotes 20 to 25 (belonging status of insurance

companies and introductory services provided to

overseas insurance companies with branches in

Singapore).

3 8 Feb 2017 (i) Revised paragraph 3.4.1 to remove time of supply

rules applicable to premiums prior to 1 Jan 2011.

(ii) Inserted paragraph 5.1.1 and amended paragraphs

5.1.2, 5.2.1 and footnote 24 to clarify GST treatment

of introductory services provided by insurance

intermediaries.

(iii) Revised paragraphs 5.4.1 to 5.4.3 to remove time of

supply rules applicable to commissions and fees

prior to 1 Jan 2011, and elaborate time of supply

rules for insurance intermediaries.

(iv) Revised paragraphs 7.1 to 7.4 and inserted footnote

32 to extend self-billing to cover transactions

between GST-registered insurance companies and

GST-registered credit insurance intermediaries.

(v) Inserted footnote 40 to explain the type of customers

that may contract for the insurance intermediary’s

services.

(vi) Editorial changes.

GST: Guide for the Insurance Industry

23

Appendix 1

TAX INVOICE

Date of issue: 01 Jul 2007 ABC INSURANCE COMPANY

888 Jalan Ang Teng

Singapore 560009

GST registration number: M2-1234567-1

Serial number:

Name of Policyholder

Address of Policyholder

Policy Details:

Type of Policy:

Policy Number:

Policy period:

Premium (S$)

Premium before GST: 1,000

GST @ 7%: 70

Gross Premium: 1,070

Total amount payable: 1,070

Name of Broker:

Address of Broker:

GST: Guide for the Insurance Industry

24

Appendix 2

Debit Note

Type of Policy:

Policy Number:

(Policyholder’s Name)

(Policyholder’s Address)

(Policyholder’s Address)

(Policyholder’s Address)

Broker’s Name:

Broker’s Address:

Date of Issue: 1 Jul 2007

Period of Insurance:

Description of insurance services supplied:

Gross Premium collected on behalf of insurance company ABC: S$ 1,070

This is not a Tax Invoice. The insurance company’s tax invoice is attached or will be

sent to you shortly.