Form ST-11 Commonwealth of Virginia Sales and Use Tax Certificate of Exemption

File info: application/pdf · 2 pages · 610.13KB

Form ST-11 Commonwealth of Virginia Sales and Use Tax Certificate of Exemption

ST-11 Manufacturing Exemption Certificate

ST-11, Manufacturing, Exemption, Certificate

Form ST-11 Commonwealth of Virginia Sales and Use Tax ...

Extracted Text

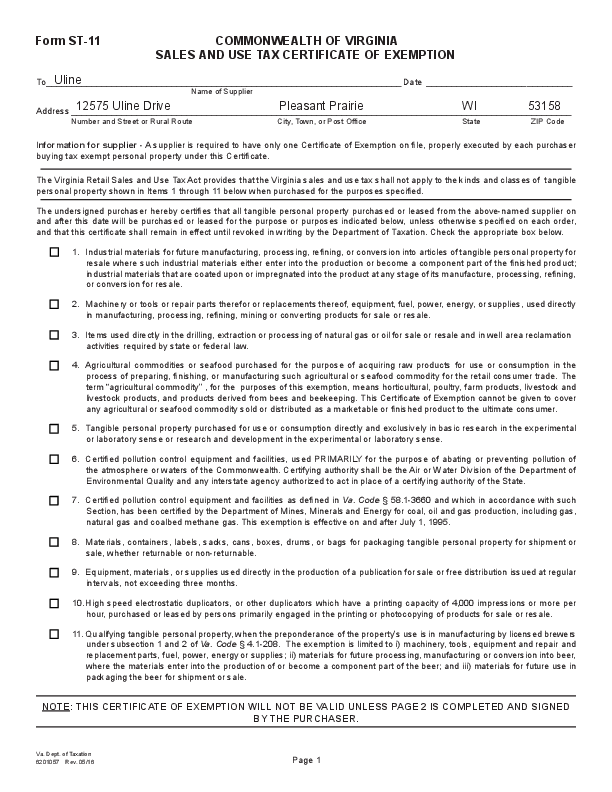

Form ST-11 COMMONWEALTH OF VIRGINIA SALES AND USE TAX CERTIFICATE OF EXEMPTION To___U__li_n_e_________________________________________________________________ Date______________________________ Name of Supplier Address__1__2_5_7__5__U_l_i_n_e__D__ri_v_e_______________________P__le__a_s_a_n__t_P__ra__ir_i_e_____________________W__I___________5_3_1__5_8___ Number and Street or Rural Route City, Town, or Post Office State ZIP Code Information for supplier - A supplier is required to have only one Certificate of Exemption on file, properly executed by each purchaser buying tax exempt personal property under this Certificate. The Virginia Retail Sales and Use Tax Act provides that the Virginia sales and use tax shall not apply to the kinds and classes of tangible personal property shown in Items 1 through 11 below when purchased for the purposes specified. The undersigned purchaser hereby certifies that all tangible personal property purchased or leased from the above-named supplier on and after this date will be purchased or leased for the purpose or purposes indicated below, unless otherwise specified on each order, and that this certificate shall remain in effect until revoked in writing by the Department of Taxation. Check the appropriate box below. c 1. Industrial materials for future manufacturing, processing, refining, or conversion into articles of tangible personal property for resale where such industrial materials either enter into the production or become a component part of the finished product; industrial materials that are coated upon or impregnated into the product at any stage of its manufacture, processing, refining, or conversion for resale. c 2. Machinery or tools or repair parts therefor or replacements thereof, equipment, fuel, power, energy, or supplies, used directly in manufacturing, processing, refining, mining or converting products for sale or resale. c 3. Items used directly in the drilling, extraction or processing of natural gas or oil for sale or resale and in well area reclamation activities required by state or federal law. c 4. Agricultural commodities or seafood purchased for the purpose of acquiring raw products for use or consumption in the process of preparing, finishing, or manufacturing such agricultural or seafood commodity for the retail consumer trade. The term "agricultural commodity'' , for the purposes of this exemption, means horticultural, poultry, farm products, livestock and livestock products, and products derived from bees and beekeeping. This Certificate of Exemption cannot be given to cover any agricultural or seafood commodity sold or distributed as a marketable or finished product to the ultimate consumer. c 5. Tangible personal property purchased for use or consumption directly and exclusively in basic research in the experimental or laboratory sense or research and development in the experimental or laboratory sense. c 6. Certified pollution control equipment and facilities, used PRIMARILY for the purpose of abating or preventing pollution of the atmosphere or waters of the Commonwealth. Certifying authority shall be the Air or Water Division of the Department of Environmental Quality and any interstate agency authorized to act in place of a certifying authority of the State. c 7. Certified pollution control equipment and facilities as defined in Va. Code � 58.1-3660 and which in accordance with such Section, has been certified by the Department of Mines, Minerals and Energy for coal, oil and gas production, including gas, natural gas and coalbed methane gas. This exemption is effective on and after July 1, 1995. c 8. Materials, containers, labels, sacks, cans, boxes, drums, or bags for packaging tangible personal property for shipment or sale, whether returnable or non-returnable. c 9. Equipment, materials, or supplies used directly in the production of a publication for sale or free distribution issued at regular intervals, not exceeding three months. c 10. High speed electrostatic duplicators, or other duplicators which have a printing capacity of 4,000 impressions or more per hour, purchased or leased by persons primarily engaged in the printing or photocopying of products for sale or resale. c 11. Qualifying tangible personal property, when the preponderance of the property's use is in manufacturing by licensed brewers under subsection 1 and 2 of Va. Code � 4.1-208. The exemption is limited to i) machinery, tools, equipment and repair and replacement parts, fuel, power, energy or supplies; ii) materials for future processing, manufacturing or conversion into beer, where the materials enter into the production of or become a component part of the beer; and iii) materials for future use in packaging the beer for shipment or sale. NOTE: THIS CERTIFICATE OF EXEMPTION WILL NOT BE VALID UNLESS PAGE 2 IS COMPLETED AND SIGNED BY THE PURCHASER. Va. Dept. of Taxation 6201057 Rev. 05/16 Page 1 Virginia Account Name of Purchaser __________________________________ No., if any_________________________________________________ Trading as___________________________________________________________________________________________________ Address_____________________________________________________________________________________________________ Number and Street or Rural Route City, Town, or Post Office State ZIP Code Kind of business engaged in by purchaser__________________________________________________________________________ I certify that I am authorized to sign this Certificate of Exemption and that, to the best of my knowledge and belief, it is true and correct, made in good faith, pursuant to the Virginia Retail Sales and Use Tax Act. By_______________________________________________ Title____________________________________________________ If the purchaser is a corporation, an officer of the corporation or other person authorized to sign on behalf of the corporation must sign; if a partnership, one partner must sign; if an unincorporated association, a member must sign; if a sole proprietorship, the proprietor must sign. Page 2