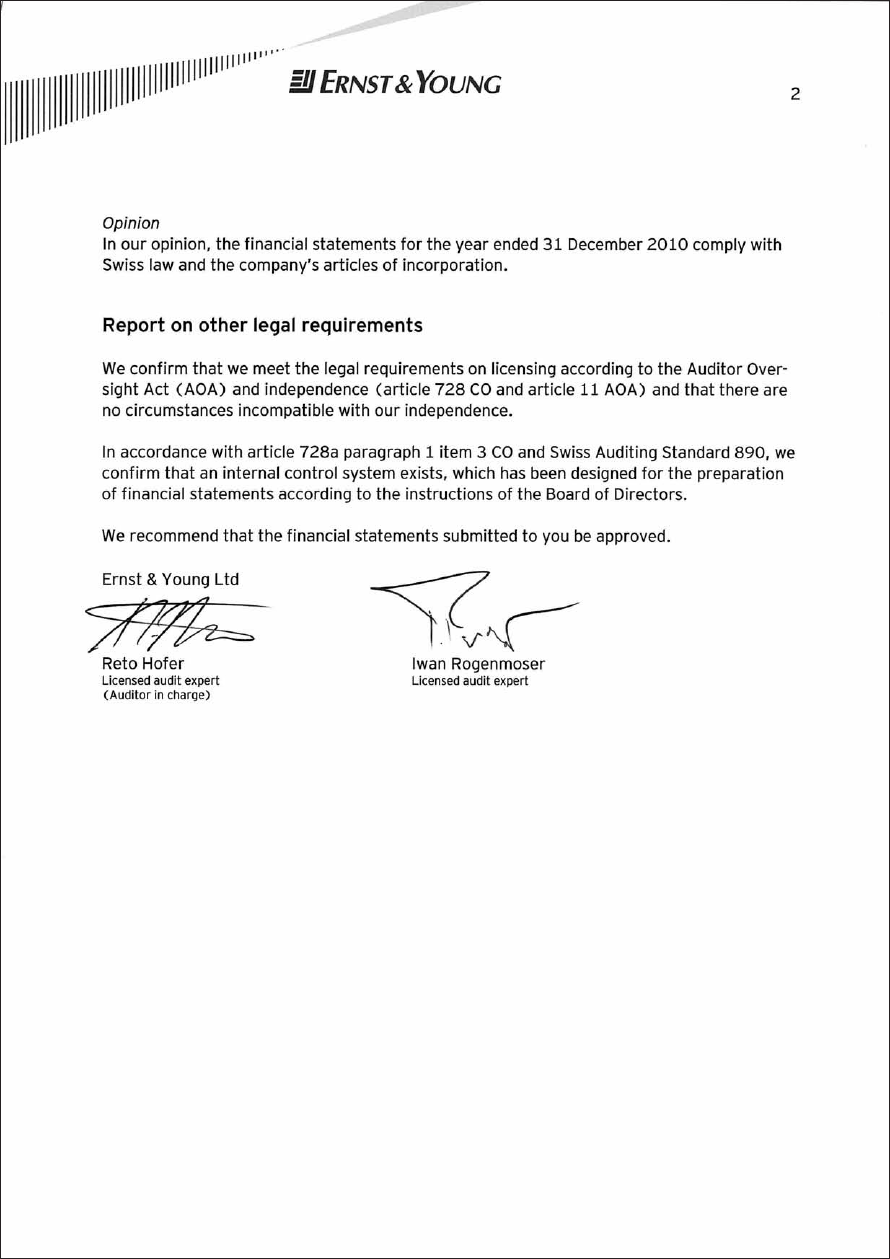

PBF206 Annual Report 2010

User Manual: PBF206

Open the PDF directly: View PDF ![]() .

.

Page Count: 156 [warning: Documents this large are best viewed by clicking the View PDF Link!]

Petroplus

Annual Report 2010

Petroplus Annual Report 2010

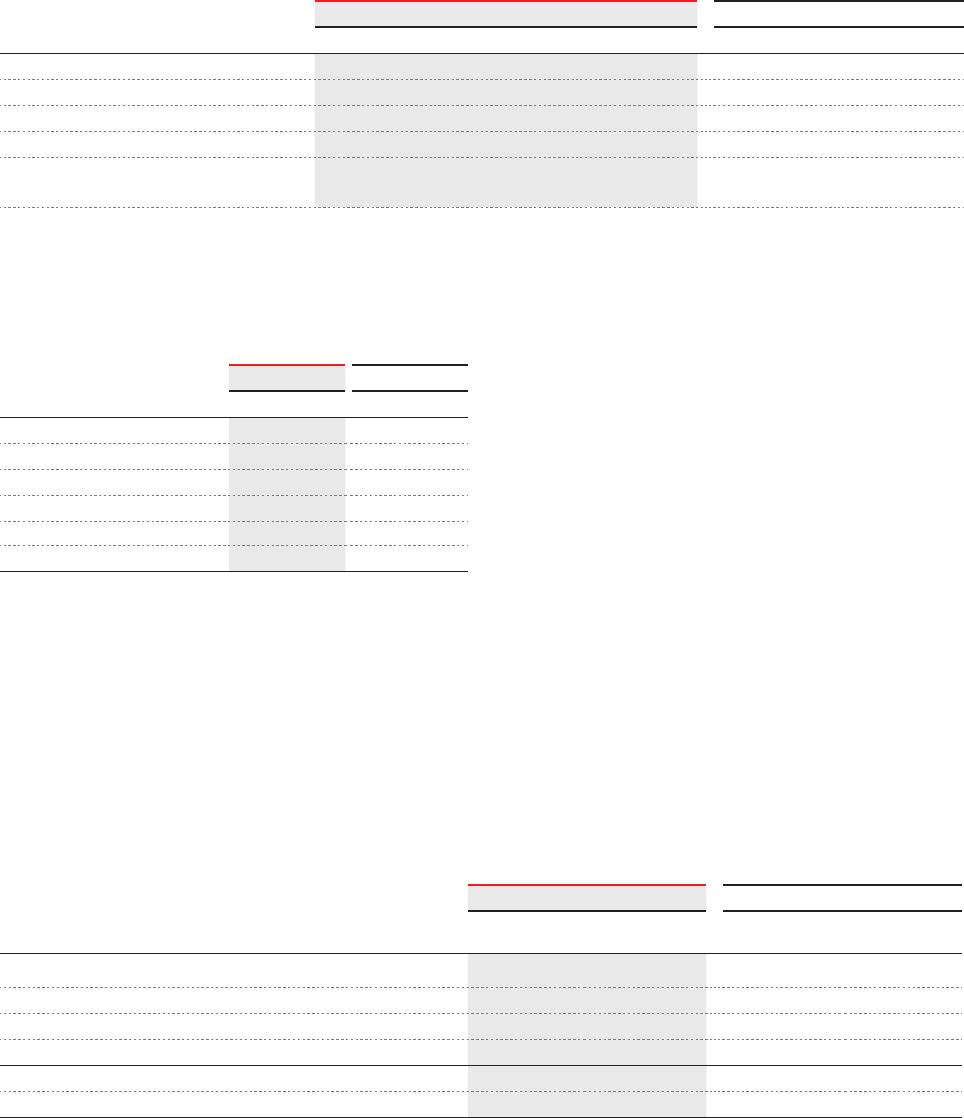

Financial Highlights

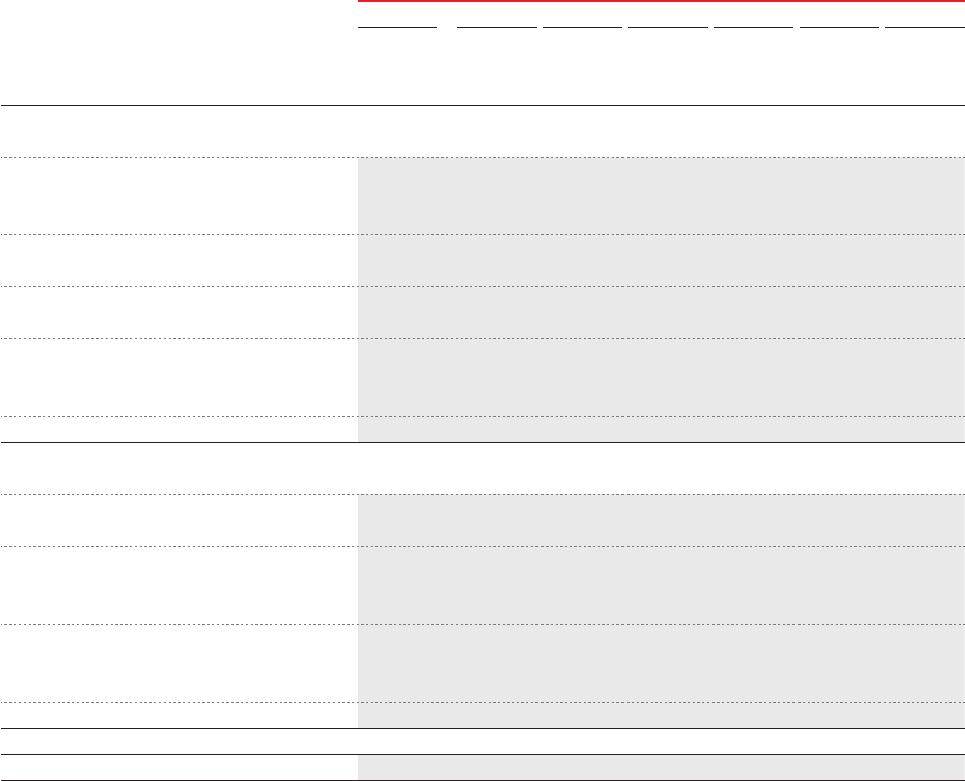

2010 2009 20081)2) 20071)2) 20061)2)

Selected Operating Data

Revenue inmillionsofUSD 20,735.0 14,797.8 24,302.0 10,581.0 3,797.5

Gross margin inmillionsofUSD 1,328.6 1,205.4 948.6 913.0 405.7

Net (loss)/income

from continuing operations

inmillionsofUSD (106.9) (108.8) (333.0) 206.2 104.6

Net (loss)/income inmillionsofUSD (112.3) (249.9) (516.6) 303.3 443.6

Basic earnings per shareinUSD (1.22) (3.20) (6.94) 4.22 10.06

Diluted earnings per shareinUSD (1.22) (3.20) (6.94) 4.09 9.71

EmployeesNumber 2,575 2,845 2,882 1,827 925

Total throughputinthousandsofbpd3) 596.2 529.1 4) 569.4 4) 384.8 201.0

Total productioninthousandsofbpd3) 608.3 539.6 4) 580.6 4) 391.0 202.1

Selected Statement of Financial Position

Cash and short-term

deposits

inmillionsofUSD 179.0 11.2 209.8 62.5 91.6

Current ratio5) 1.26 1.18 1.13 1.26 1.57

Net current assets6) inmillionsofUSD 656.1 397.8 341.1 832.2 648.6

Total assets inmillionsofUSD 6,769.6 6,678.3 6,914.9 7,466.8 3,014.8

Total debt inmillionsofUSD 1,692.0 1,833.4 1,881.9 1,333.1 –

Total equity inmillionsofUSD 2,003.9 1,988.0 1,987.6 2,501.5 1,555.1

Selected Share Data7)

(ISIN: CH0027752242;

Symbol: PPHN)

Issued shares at

December 31

Number 95,230,953 86,325,289 69,060,231 68,641,599 61,036,600

Nominal value inCHF 7.48 7.58 8.18 9.18 9.18

Share price: high

low

inCHF

inCHF

22.58

9.12

28.24

13.78

84.15

18.05

133.00

70.00

79.90

66.90

Share price at December 31 inCHF 12.32 19.03 20.96 87.70 74.00

Market capitalization at

December 31

inmillionsofCHF 1,173.2 1,642.8 1,447.5 6,019.9 4,516.7

1)IncludesthePetitCouronneandReichstettrefineries(acquiredonMarch31,2008),theCorytonrefinery(acquiredonMay31,2007),theIngolstadt

refinery(acquiredonMarch31,2007),theAntwerprefinery(acquiredonMay31,2006)andtheCressierrefinery.

2)The2008,2007and2006financialshavebeenre-presentedtoreflecttheimpactofdiscontinuedoperationsrelatedtotheTeessiderefiningoperations

andtheAntwerpProcessingfacility.

3)Barrelsperday(“bpd”)

4)ExcludesthroughputandproductionoftheTeessiderefinery.

5)Currentassetsdividedbycurrentliabilities.

6)Currentassetsminuscurrentliabilities(excludesnetassets/liabilitiesheldforsaleofUSD57.6millionin2009andUSD41.8millionin2006).

7)ThesharesofPetroplusHoldingsAGweretradedontheSIXSwissStockExchangeonNovember30,2006forthefirsttime.

Petroplus Holdings AG | Annual Report 2010 | 3

The Petroplus Company

Listed on the SIX Swiss Exchange, Petroplus Holdings AG,

together with its subsidiaries (“Petro plus”, the “Company”, the

“Group”, “we”, “our”, or “us”) focuses on refining and currently

owns and operates six refineries across Europe: The Coryton

refinery on the Thames Estuary in the United Kingdom, the

Antwerp refinery in Antwerp, Belgium, the Petit Couronne

refinery in Petit Couronne, France, the Ingolstadt refinery in

Ingolstadt, Germany, the Reichstett refinery near Strasbourg,

France, and the Cressier refinery in the canton of Neuchâtel,

Switzerland. The refineries have a combined throughput ca-

pacity of approximately 752,000 barrels per day. The Company

also owns the Teesside facility in Teesside, United Kingdom,

which operates as a marketing and storage facility.

Petroplus produces a variety of finished products including

diesel, heating oil, gasoline, aviation fuels, light and heavy fuel

oils, gasoline components and other petroleum products. We

sell our refined products on an unbranded basis to distributors

and end customers, primarily in the United Kingdom, France,

Switzerland, Germany and the Benelux countries, as well as

on the global spot market.

Our supply and distribution group, centrally based in Zug, Swit-

zerland, is responsible for all physical supply and commercial

optimization activities for our refineries. The group’s primary

goal is to optimize both the supply of crude oil and feedstocks

for each refinery and the off-take of each refinery’s petroleum

products. We source our crude oil on a global basis through

a combination of spot market purchases and short-term pur-

chase contracts. We believe purchasing based on spot mar-

ket pricing provides us flexibility in obtaining crude oil at lower

prices and on a “as needed” basis. Since all of our refineries

have access, either directly or through pipeline connections to

deepwater terminals, we have the flexibility to purchase crude

oil originating from a number of different countries.

Petroplus employs approximately 2,600 employees through-

out Europe and we consider good corporate citizenship to be

a core responsibility of our business.

Our Strategy

We are a “pure play” refiner able to source crude on a global

basis not integrated with retail outlets. As a result, we are free

to supply our products into the distribution channel or market

that we believe will maximize profit. Petroplus strives for safe

and reliable business operations and searches for opportun-

ities to expand our key business area – the refining of crude oil

and wholesale marketing of refined petroleum products.

Our Key Values

Above all else, our focus is to operate our refineries in a safe

and reliable manner. We devote significant time and resources

to improving the safety, reliability and environmental compli-

ance of our operations. We are also determined to improve

our competitiveness in the marketplace. We highly value our

employees and we are dedicated to providing them with devel-

opment opportunities throughout our organization. With these

priorities in place, our management team remains committed

to creating value for our shareholders.

Building

Shareholder

Value

Enabling

Employees

to Excel

Improving

Competi-

tiveness

Safety is

our Number 1

Priority

Welcome to Petroplus

Forward-Looking Statement

Certain portions of this document contain forward-looking statements that reflect our current judgment

regarding conditions we expect to exist and the course of action we expect to take in the future. Even though

we believe our expectations regarding future events are based on reasonable assumptions, forward-looking

statements are not guarantees of future performance. In some cases, these forward-looking statements can

be identified by the use of forward-looking terminology, including the words “aims”, “believes”, “estimates”,

“anticipates”, “expects”, “intends”, “may”, “will”, “plans”, “continue” or “should” and in each case, their nega-

tive or other variations or comparable ter mi nology or by discussions of strategies, plans, objectives, targets,

goals, future events or intentions. These forward-looking statements include all matters that are not historical

facts. Our assumptions rely on our operational analysis and expectations for the operating performance of our

assets based on their historical operating performance, management expectations as described in this report

and historical costs associated with the operations of those assets. Factors beyond our control could cause

our actual results to vary materially from our expectations and are discussed in “Outlook” and elsewhere in

this document. Any prospective financial information included in this document is not fact and should not be

relied upon as being necessarily indicative of future results, and you are cautioned not to place undue reliance

on this prospective financial information. We undertake no obligation to update any forward-looking state-

ments contained in this document as a result of new information, future events or subsequent developments,

or otherwise.

Content

6 I Letter to the Shareholders

8 I Company Overview

8 I Executive Committee

9 I Organizational Structure

10 I Petroplus at a Glance

12 I Operating and Financial Review

12 I Management Discussion and Analysis

29 I Outlook

39 I Corporate Responsibility

45 I Corporate Governance

67 I Financial Reporting

67 I Consolidated Financial Statements of Petroplus Holdings AG

135 I Statutory Financial Statements of Petroplus Holdings AG

6 | Petroplus Holdings AG | Annual Report 2010

Letter to the Shareholders

Dear Shareholders,

2010 was a better year for the refining industry and for Petroplus.

As we look back over 2010, refining margins were better as compared to 2009. Economic activity increased

throughout the year, and global oil demand recovered. The momentum from 2010 should continue into

2011. Global oil demand is expected to be up by another 1.4 million barrels per day, led by China and other

developing nations, but also with stable recovery from North America and Northwest Europe. Specifically,

the market for 2010 was different from 2009 as we saw petrochemical demand for naphtha increase both

in Europe and the Far East, thereby improving margins to make naphtha and gasoline. Distillates, which

spent most of 2009 in a very deep contango, started to improve in the second quarter as margins for gasoil

increased to over US-Dollar 10 per barrel and contango disappeared, alleviating the barrels stored both

in tank and in vessels on the water. Not as positively, in our niche inland markets, we saw a weaker Rhine

freight in 2010 versus 2009, impacting overall premiums for the gasoline and distillates sold in those markets.

Petroplus’ 2010 results strengthened over 2009. Our operating profit more than doubled, and we ended

the year in a stronger financial position with higher cash and no short-term cash borrowings. Our net

debt-to-net capitalization ratio improved from 48 % to 43 % year-over-year, and as of December 31, 2010,

we are in compliance with all financial covenants under our credit facility and bond indentures. From

an

operational perspective, we processed 25 million more barrels of crude in 2010 than in 2009, primarily

due to increased reliability across our system. While our throughput levels improved significantly, we

did face some operating challenges during the year. Our Antwerp and Cressier sites experienced major

turnarounds, and the labor strikes in France during September and October forced the shutdown of

three of our refineries due to a shortage of crude supply. Management continues to focus on increasing

the reliability of our assets as this is the key to better performance. Despite our improved financial

position and better reliability of our assets, we ended the year with a net loss on an IFRS basis.

However, these tough times give us the chance to rise to the challenge of turning Petroplus back into

a profitable company. During 2010, we have made three significant changes throughout our organization

that will enable us to move the Company forward:

First of all, we re-designed the operating structure of the Company. The new structure is designed both

to be more reactive to market opportunities and to streamline processes and reduce inefficiencies by

centralizing decision-making, optimizing our supply-chain management, and strengthening the support

functions across the organization.

Secondly, we conducted a thorough review of our portfolio of assets, resulting in some tough decisions.

We sold our interest in the investment vehicle, PBF Energy Company LLC, based in the United States.

Further, we entered into a consultation process to propose terms for a project to cease refining operations

at our Reichstett refinery. These actions are driven to free up some liquidity and focus our attention and

resources on our core business of European oil refining.

Thirdly, we have implemented our Three-Year Improvement Plan, a comprehensive program designed

to increase gross margin capture, lower operating costs, increase energy efficiency, and improve opera-

tional reliability.

Petroplus Holdings AG | Annual Report 2010 | 7

Together, these changes enable us to focus on unlocking the hidden value in our refineries. With our new,

lean organization, a streamlined asset portfolio and operational improvement program in place, we are

well-positioned to capture better results. 2010, the first year of this plan, demonstrated an overall improve-

ment of USD 1 per barrel, largely ahead of our 2012 target of USD 1.25 per barrel.

We have also made a lot of progress in the area of safety, health and environmental compliance, reducing

the number of incidents significantly over the past year. These areas continue to be a top priority for

Petroplus, and we strive to operate our refineries at the highest standards of safety. In addition, we

successfully launched our REACH compliance program, ensuring that all requirements were met at

December 1, 2010, the effective date of this new European Union legislation.

Our Board of Directors and our Executive Committee also experienced some changes during the year.

Thomas D. O’Malley, our Chairman, announced his retirement from Petroplus, effective from February 2,

2011, and is succeeded by Patrick Monteiro de Barros. Mr. de Barros has been a member of our Board

of Directors since 2006 and, during these years, served as our Vice Chairman. He brings along a proven

track record of leadership within the refining industry. We are pleased to have had Joseph D. Watson,

our new Chief Financial Officer, join us in 2010, as he brings a wealth of knowledge and background in the

refining industry. In addition, Peter F. Senkbeil joined our executive team as General Manager, Refining.

Mr. Senkbeil has an established career in the oil refining industry, including serving for many years as the

Refinery Manager at our Ingolstadt site.

As we look to 2011 and beyond, we believe that the global economy will continue to recover, led by

emerging markets but also with solid improvement from North America and Northwest Europe. We have

ambitious targets to strengthen Petroplus’ performance through our Three-Year Improvement Plan,

focusing on organic improvements that will produce measurable financial results in four key areas: Gross

Margin Capture, Energy Efficiency, Operating Expenses, and General and Administrative Costs. The

Three-Year Improvement Plan is the cornerstone for our success in the next years. Our efforts in 2010

have already provided enough improvement that we can hope we will have to increase our targets before

the end of the plan! Our management team is focused on these initiatives, and we will continue to report

the results of our efforts to our shareholders.

I thank you, our shareholders, for your loyalty and continued confidence in Petroplus. I also thank all of

the Directors for their continuing support and employees for their hard work and dedication.

I look forward to facing the challenges to come and I am confident that better times are ahead.

Kindest regards,

Jean-Paul Vettier

Chief Executive Officer

Executive Committee

Jean-Paul Vettier

Chief Executive Officer

Chester J. Kuchta

Chief Operating Officer

Joseph D. Watson

Chief Financial Officer

W. Thomas Skok

General Counsel and

Corporate Secretary

Peter F. Senkbeil

General Manager Refining

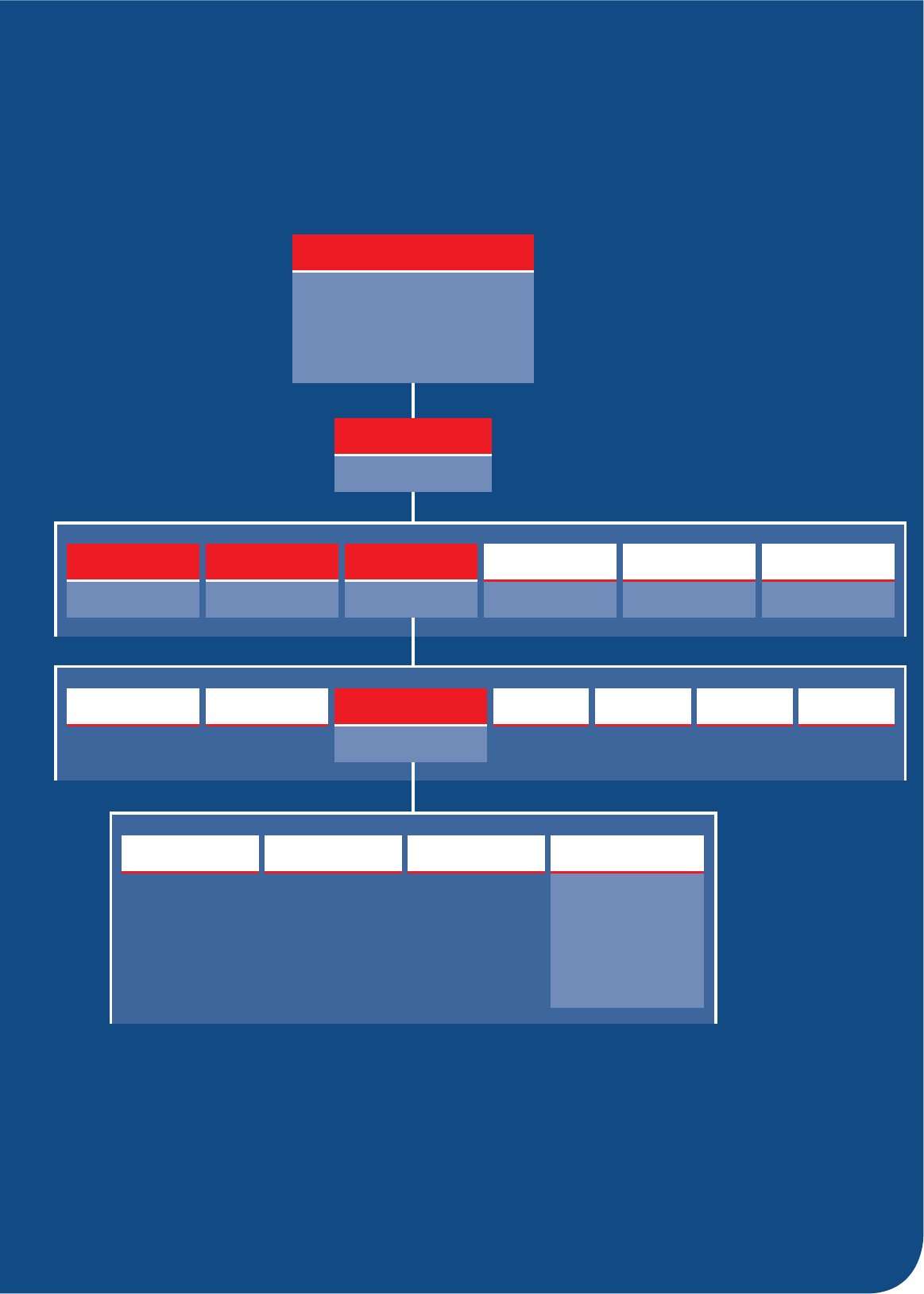

Organizational Structure

Jean-Paul Vettier*

Chief Executive Officer

Chairman:

Patrick Monteiro de Barros

(effective as of February 3, 2011)

Thomas D. O’Malley

(retired as of February 2, 2011)

Board of Directors

Joseph D. Watson*

Chief

Financial Officer

W. Thomas Skok*

General Counsel and

Corporate Secretary

Jim McCoy

Strategy & Business

Development

Crude Supply

Logistics, Quality &

Corporate Projects Procurement Wholesale

Marketing Shipping &

Scheduling Business Unit

Management

*Member of the Executive Committee

Chester J. Kuchta*

Chief

Operating Officer

Jack McDermott

Human Resources

Christophe Henrat

Risk Management

Peter F. Senkbeil*

General Manager

Refining

Safety, Health &

Environment Capital Projects Refineries

– Coryton

– Antwerp

– Petit Couronne

– Ingolstadt

– Reichstett

– Cressier

– Teesside Marketing

& Storage Facility

Technical Assistance

People

Employees

Total

2 575

Employees 2010

France

836

United Kingdom

615

Belgium

217

0

100

200

300

400

500

600

700

800

900

Switzerland

494

Germany

411

Czech Republic

2

Petroplus

at a Glance

1 Coryton Refinery

2 Petit Couronne Refinery

3 Reichstett Refinery 4 Cressier Refinery

Marketing & Sales Offices

1 Zug, Switzerland

2 Paris, France

3 Middlesbrough, United Kingdom

4 Swansea, United Kingdom

5 Antwerp, Belgium

6 Ingolstadt, Germany

7 Prague, Czech Republic

1

7

4

3

2

6

1

2

5

3

4

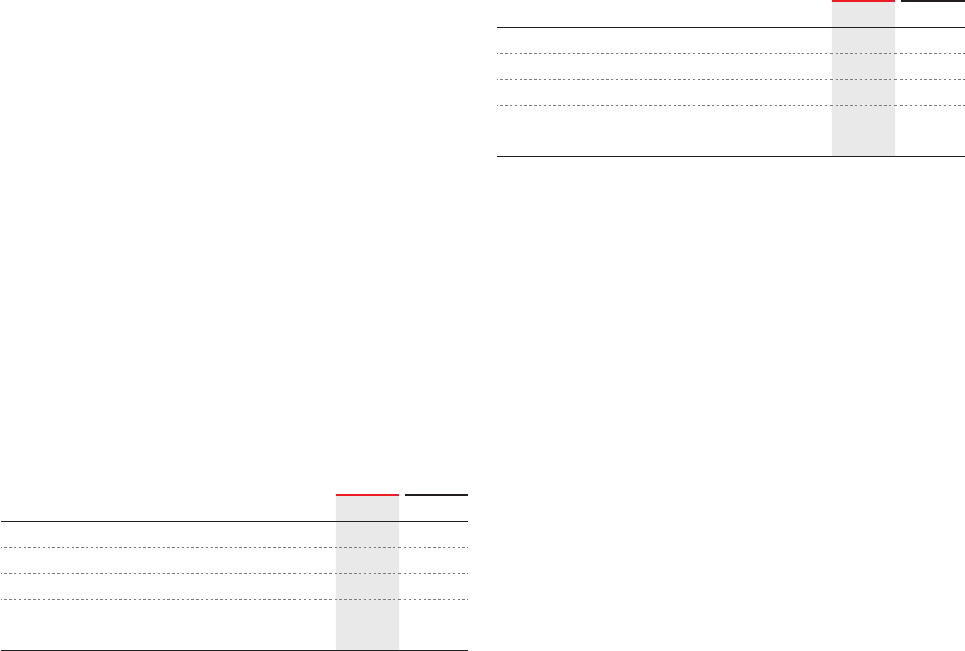

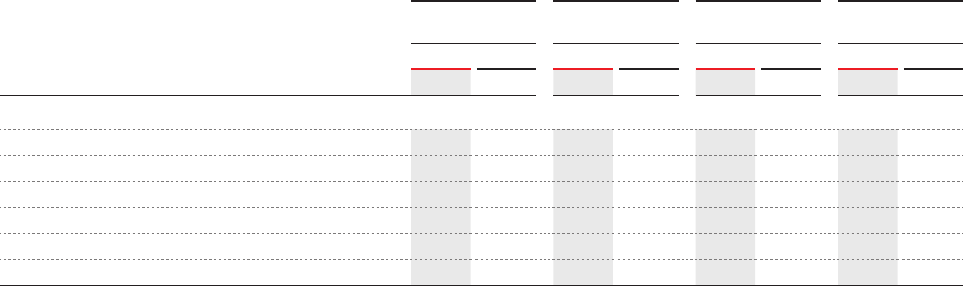

Results

EBIT from

continuing

operations

(in millions of USD)

Production 2010

(in percent)

2010

50 %

Middle distillates

5 % Naphtha/Petrochemicals

5 %

Solid by-products/fuel & loss

5 % LPG

10 % Fuel oil/Bitumen

27 % Gasoline

50 % Middle distillates

Throughput

(in thousands of bpd)

2010

596 200

bpd

0

150

300

450

600

569.4 529.1

2008 2009 2010

Total capital expenditures

(in millions of USD)

2010

226.9

millions of USD

0

100

200

300

400

2008 2009 2010

2010

161.7

millions of USD

0

–150

50

–100

100

–50

–200

–250

150

200

2010

2009

2008

0

1

2

3

4

5

6

2008 2009 2010

2010

3.48

USD per barrel

Petroplus Market Indicator (PMI)

(in USD per barrel)

Market

Operations

5 Ingolstadt Refinery

6 Antwerp Refinery

7 Teesside Marketing &

Storage Facility

596.2

321.5 347.7 226.9

5.17 3.482.53

–232.2

161.766.2

Excludes throughput of the Teesside refinery

5

7

6

12 | Petroplus Holdings AG | Annual Report 2010 | Operating and Financial Review

Operating and Financial Review

Management Discussion and Analysis of the Financial Condition and the Results of Operations

New Chief Financial Officer

Effective August 5, 2010, Joseph D. Watson was appointed

Chief Financial Officer (“CFO”), replacing Karyn F. Ovelmen

who resigned as CFO effective August 4, 2010.

New General Manager Refining

Effective February 2, 2010, Peter F. Senkbeil was appointed

General Manager Refining.

Main Activities during 2010

Reichstett Refinery

In the beginning of 2010, the Company launched a strategic

review of its Reichstett refinery in France to evaluate alterna-

tives for the site. The Company considered several possibili-

ties, including a potential sale, further investments to improve

its competitiveness, as well as a shutdown of refining opera-

tions and conversion to a terminal.

The process for a possible sale of the refinery concluded without

presenting any ultimate buyers, and the Company determined

that, in the current challenging refining market and capital-con-

strained environment, the Company cannot justify further size-

able capital investments in the plant. As a consequence, on Oc-

tober 21, 2010, the Company informed the Works Council of the

Reichstett refinery that it intended to commence a formal infor-

mation and consultation process to propose terms for a project

to cease refining operations and convert the site to a terminal.

The information and consultation process formally commenced

on November 24, 2010. A decision with respect to the future of

the site can and will only be made when Petroplus has received

the opinion of the Works Council which is expected around the

end of the first quarter of 2011, until which time, the refinery will

continue to operate.

Shutdowns at Refineries due to Strike Actions

During October 2010, throughput at the Petit Couronne,

Reichstett and Cressier refineries was impacted due to labor

strike actions in France.

Petroplus’ Share in Investment Vehicle PBF Energy

Company LLC

Acquisition of Delaware City Refinery Assets

On June 1, 2010, the Company’s investment vehicle, PBF En-

ergy Company LLC (“PBF”), a partnership entered into with

The Blackstone Group and First Reserve Corporation, com-

pleted its purchase of the Delaware City refinery in Delaware

City, Delaware from Valero Energy Corporation. On May 28,

2010, the Company contributed

US-Dollar (“USD”)

76.4 million

to PBF related to the purchase of the Delaware City refinery.

The following discussion and analysis is derived from, and

should be read in conjunction with, the Petroplus Holdings AG

Consolidated Financial Statements and the related notes to

those financial statements included elsewhere in this 2010 An-

nual Report. The following discussion of our financial condition

and results of operations contains forward-looking statements

that are based on assumptions about future business develop-

ments. As a result of many factors, including the risks set forth

under the caption “Risks Relating to Our Business and Our

Industry” in this 2010 Annual Report, our actual results may

differ materially from those anticipated by these forward-look-

ing statements.

Company Overview

We are the largest independent refiner and wholesaler of pe-

troleum products in Europe. We are focused on refining and

currently own and operate six refineries across Europe, spe-

cifically in the United Kingdom, Belgium, France, Germany and

Switzerland. The six refineries have a combined throughput

capacity of approximately 752,000 barrels per day (“bpd”). We

also own a marketing and storage facility, located in the United

Kingdom. We sell our refined petroleum products to distribu-

tors and end customers, primarily in the United Kingdom,

France, Switzerland, Germany and the Benelux countries, as

well as on the global spot market.

Change in Board of Directors and

Executive Committee

New Chairman of the Board of Directors

Thomas D. O’Malley’s retirement as Chairman and Member

of the Board of Directors, originally announced on December

8, 2010 and effective May 5, 2011, was brought forward to

the Petroplus Board meeting on February 2, 2011, due to the

continuing rapid development of PBF Energy Company LLC,

of which he is Chairman of the Board of Directors. Patrick

Monteiro de Barros, formerly Vice Chairman of the Board, has

succeeded Mr. O’Malley as Chairman.

With the recent sale of Petroplus’ interest in PBF Energy Com-

pany LLC and the pending development of PBF into an op-

erating Atlantic Basin oil refiner, the Petroplus Board and Mr.

O’Malley decided that, from a corporate governance perspec-

tive, it would not be advisable for him to remain as Chairman of

both organizations.

Petroplus Holdings AG | Annual Report 2010 | Operating and Financial Review | 13

Sale of Petroplus’ Share in Investment Vehicle PBF

On September 26, 2010, the Company reached an agreement

in principle with the Blackstone Group and First Reserve, its

partners in PBF, for the sale of Petroplus’ 32.62 % share of PBF

in the amount of USD 91.0 million. Cash proceeds received on

October 18, 2010, amounted to USD 81.9 million after with-

holding tax.

This transaction represents a strategic shift for the Company

mainly caused by the expected rapid expansion rate of PBF in

the United States, which would require large investments by

the Company to maintain a meaningful position in PBF and the

amount and timing of such investments would not be entirely

within the Company’s control.

Management believes it is most important to focus the Com-

pany’s resources on our core European operations and to pur-

sue strategies to improve the competitiveness of the existing

asset base.

Repayment of Nominal Share Capital

At the ordinary shareholders’ meeting of the Company which

took place on May 5, 2010, the shareholders resolved to re-

duce the share capital by CHF 0.10 per share. The entry of the

share capital reduction in the commercial register took place

on July 15, 2010, and the repayment of CHF 0.10 per regis-

tered share was paid to shareholders on July 26, 2010.

Issuance of Shares

During May 2010, the Company completed a private place-

ment whereby the Company issued 8,650,000 new registered

shares from existing authorized capital. The shares were sold

at a price of CHF 17.50. The first trading day of the new shares

was May 7, 2010. The gross proceeds amounted to USD 136.4

million, excluding share issue costs of USD 5.6 million.

Sale of PBF generates

USD 81.9 million in cash

in 2010

Discontinued Operations

Sale of the Antwerp Processing Facility

On October 23, 2009, the Company entered into a definitive

agreement

with Eurotank Belgium B.V., a wholly-owned sub-

sidiary of

Vitol Tank Terminals International B.V., part of the

Vitol Group of companies (“Vitol”) for the sale of Petroplus Re-

fining Ant werp N.V. and Petroplus Refining Antwerp Bitumen

N.V. (the “Antwerp Processing facility”). The sale was closed

on January 12, 2010. The proceeds received were USD 56.3

million, including hydrocarbon inventory on site.

Operations of the Teesside Refinery

Due to the low complexity configuration of the facility, the un-

favorable market environment and the significant regulatory

capital expenditures required to maintain refinery operations,

we suspended the Teesside facility’s refining operations in No-

vember 2009. The refinery had been shut down for economic

reasons since the second quarter of 2009. During 2010, the

refinery was converted to a marketing and storage facility. The

refinery’s 117,000 bpd throughput capacity had represented

approximately 14 % of our combined throughput capacity.

The results of the above operations, including impairment

charges recorded in 2009, have been reclassified to the sepa-

rate line item “Discontinued operations” in our Consolidated

Statement of Comprehensive Income for the years ended De-

cember 31, 2010 and 2009.

Successful Sale

of Antwerp Processing

Facility completed in

January 2010

14 | Petroplus Holdings AG | Annual Report 2010 | Operating and Financial Review

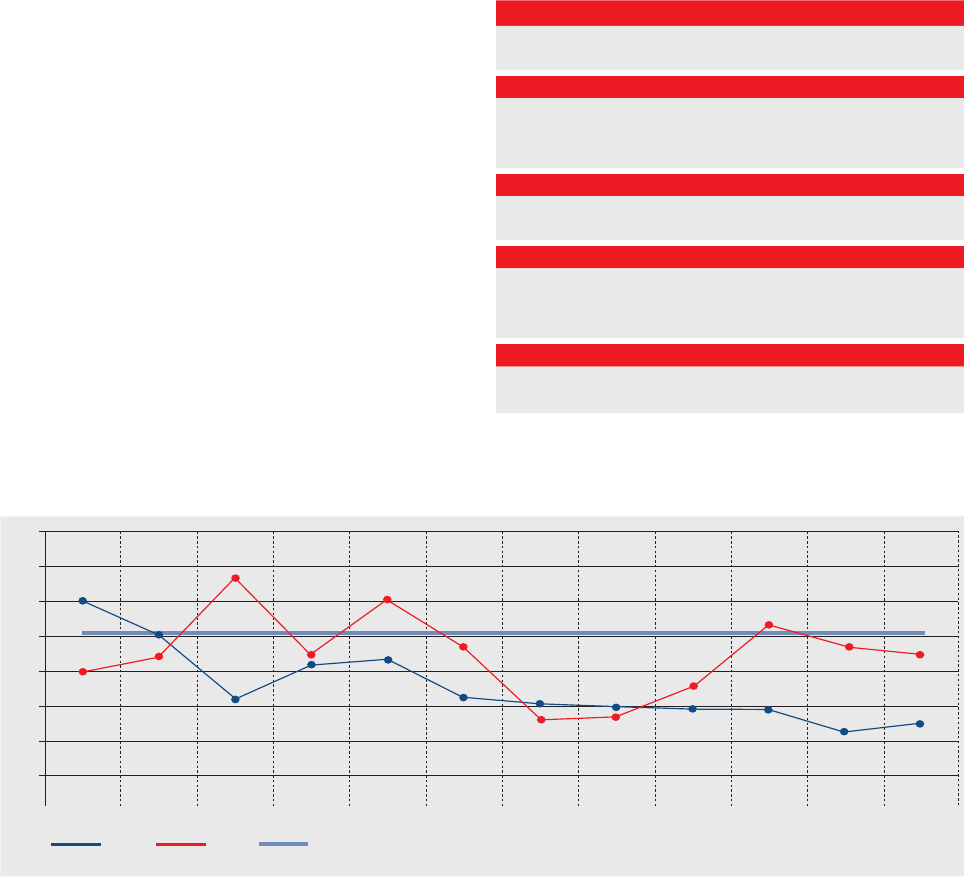

Market and Benchmark Indicators

PMI – An Indicator of the Market

At the beginning of 2010, Petroplus developed a tool, the

Petroplus Market Indicator (“PMI”), which gives a “flavor” of

the refining margin environment. The PMI is a daily indicator

and is structured on a typical refinery in Northwest Europe

(“NWE”). It simulates the possible refining margin for a hypo-

thetical Topping/Reforming/Cracking/Visbreaking refinery lo-

cated on the sea with an average crude distillation capacity

of 100,000 bpd. The model uses a crude basket consisting of

four crude oils (13 % Bonny Light, 40 % Urals, 12 % CPC, 35 %

Forties) typically processed by NWE refiners. The PMI index

is calculated and reported after variable costs. While the PMI

does not reflect the Company’s actual refining margin, it does

give an indication of the current market condition. Petroplus

refinery margins may be better or worse than the PMI depend-

ing on, among other factors, location, configuration, crude diet

and specialties. The PMI for 2010 was USD 3.48 per barrel

versus USD 2.53 per barrel for 2009. The market in 2010 has

improved but is still below historical crack levels.

Benchmark Refining Margin Indicators

In addition to utilizing the PMI as an indicator of the current

market, we assess our operating performance by comparing

the refining margins (revenue less materials cost) of each of

our refineries against a specific benchmark industry refining

margin based on crack spreads. Benchmark refining margins

take into account both crude and refined petroleum product

prices. When these prices are combined in a formula, they

provide a single value – a gross margin per barrel – that, when

multiplied by a throughput number, provides an approximation

of the gross margin generated by refining activities.

As the performance of our refineries does not closely follow

any of the currently published industry benchmark refining

margins, we have created benchmark refinery margins, based

upon publicly available pricing information, for each of our re-

fi neries that more closely reflect each of our refineries’ actual

performance.

The benchmark refining margins for the six refineries we oper-

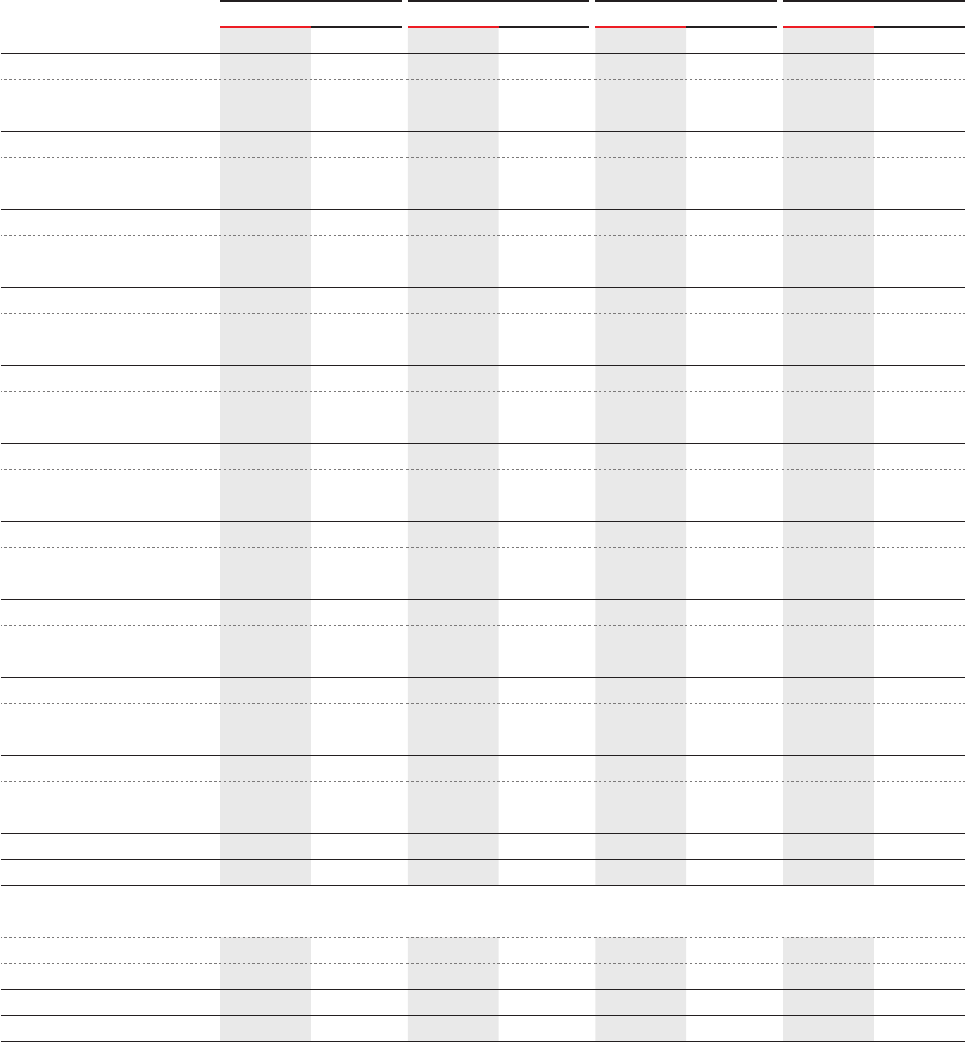

ated during the year 2010 are set forth in the following table:

Coryton Refinery 5/2/2/1

five Dated Brent/two gasoline/two ULSD/one 3.5 % fuel oil

Antwerp Refinery 6/1/2/2/1

six Dated Brent/one gasoline/two gasoil/two VGO/

one 3.5 % fuel oil

Petit Couronne and Reichstett refineries 4/1/2/1

four Dated Brent/one gasoline/two ULSD/one 3.5 % fuel oil

Ingolstadt Refinery 10/1/3/5/1

ten Dated Brent/one naphtha/three gasoline/five ULSD/one

3.5 % fuel oil

Cressier Refinery 7/2/4/1

seven Dated Brent/two gasoline/four gasoil/one 1 % fuel oil

7

6

5

4

3

2

1

0

DecNov

Petroplus Market Indicator (“PMI”) – On a Monthly Basis1)

2009 2010 Avg 2006–2010 Monthly average of daily prices during the relevant month

Jan Feb Mar Apr May Jun Jul Aug Sep Oct

USD/bbl

1)The PMI is NOT the Petroplus Margin. Petroplus margin may be better or worse depending on location configuration, crude diet, specialties, etc.

Petroplus Holdings AG | Annual Report 2010 | Operating and Financial Review | 15

The following table provides the average price of Dated Brent,

PMI and benchmark refining margin indicators by refinery for

the years ended December 31, 2010 and 2009. The bench-

mark refining margins are expressed in USD per barrel and

serve as proxy for the per barrel margin that a Dated Brent

crude oil refinery situated in NWE would earn assuming it sold

the benchmark production for the relevant refinery margin:

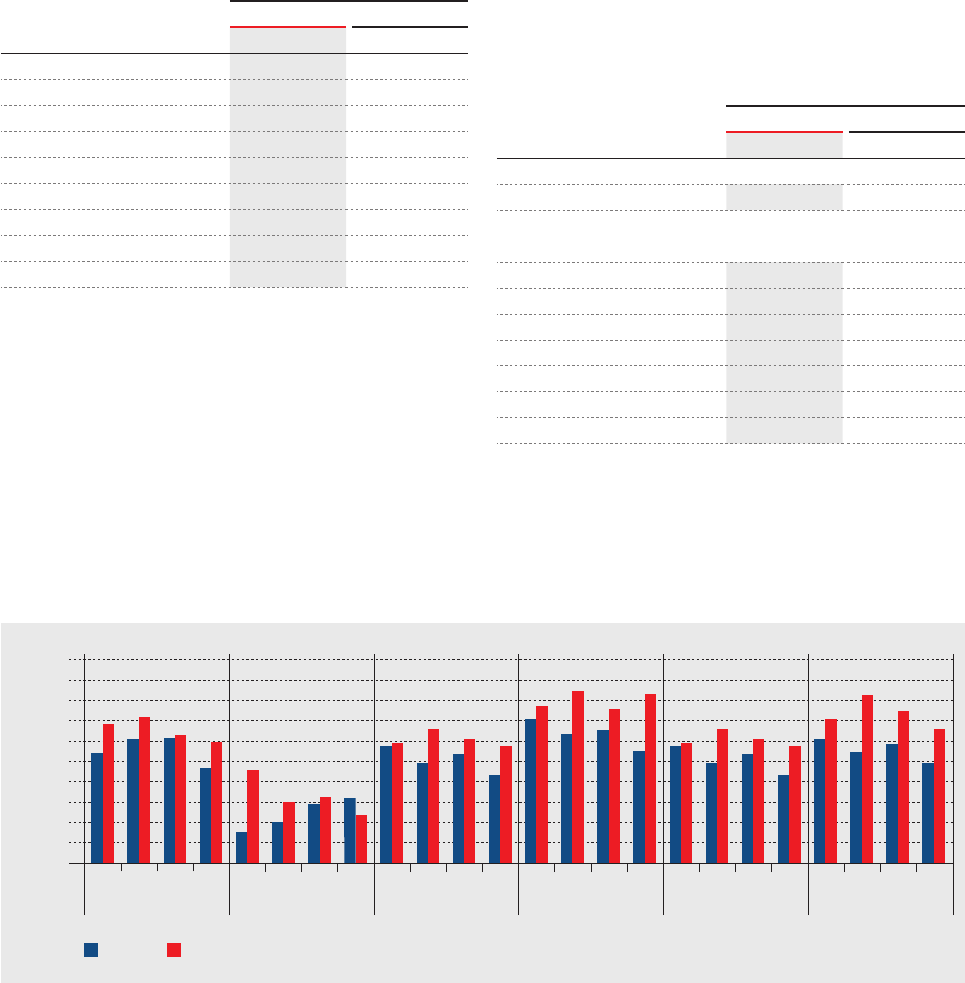

Benchmark Refining Margin Indicators

While the benchmark refinery margins presented in the table

above are representative of the results of our refineries, each

refinery’s realized gross margin on a per barrel basis will

differ from the benchmark due to a variety of factors affecting

the performance of the relevant refinery to its corresponding

benchmark. These factors include the refinery’s actual type of

For the year ended December 31,

(in USD per barrel) 2010 2009

Dated Brent 79.73 62.04

Petroplus Market Indicator1) 3.48 2.53

Benchmark refining margins

5/2/2/1 Coryton6.43 5.50

6/1/2/2/1 Antwerp 3.25 2.36

4/1/2/1 Petit Couronne5.96 4.99

10/1/3/5/1 Ingolstadt7.88 6.28

4/1/2/1 Reichstett5.96 4.99

7/2/4/1 Cressier 7.21 5.50

1)Net of variable operating costs.

crude oil throughput, product yield differentials and any other

factors not reflected in the benchmark refining margins, such

as transportation costs, fuel consumed during production

and any product premiums or discounts, as well as inventory

fluctuations, timing of crude oil and other feedstock purchases,

a rising or declining crude and product pricing environment

and commodity price management activities.

The following table sets forth historical benchmark crude and

refined petroleum product pricing information used in calcu-

lating each of our refineries’ benchmark refining margins:

Reference Benchmark Crude and Product Prices

For the year ended December 31,

(in USD per barrel) 2010 2009

Crude Oil1)

Dated Brent 79.73 62.04

Products Differential to Dated Brent1)

Naphtha 0.23 (2.05)

95 RON gasoline 8.33 7.55

ULSD 12.68 9.93

Gasoil2) 10.07 7.33

VGO 0.44 (0.30)

1 % Fuel Oil (6.44) (5.89)

3.5 % Fuel Oil (9.85) (7.44)

Source: Bloomberg

1)Average of daily prices for trading days during the relevant period.

2)Based on the quoted price for heating oil.

Benchmark Refining Margin Indicators by Petroplus Refineries – On a Quarterly Basis

$10.00

$ 8.00

$ 6.00

$ 4.00

$ 2.00

Sources: Bloomberg, Platt’s

Coryton Antwerp Petit Couronne Ingolstadt Reichstett Cressier

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2009 2010

16 | Petroplus Holdings AG | Annual Report 2010 | Operating and Financial Review

Commodity Price Management

The nature of our business requires us to maintain a sub-

stantial investment in petroleum inventories. Since petroleum

feedstocks and products are global commodities, we have no

control over the changing market value of these inventories.

To supply our refineries with crude oil on a timely basis, we

enter into purchase contracts that fix the price of crude oil from

one to several weeks in advance of receiving and processing

that crude oil. In addition, as part of our marketing activities

we may enter into fixed price contracts for sales of our refined

petroleum products in advance of producing and delivering

the products. Prior to delivery of the crude oil and sale of

the related refined petroleum products, the market value of

the crude oil and products may change as prices related to

the fixed purchase and sale commitments rise and fall.

On average, throughout 2010, we have held approximately

21 million barrels of crude and product inventory on hand.

This level fluctuates on a daily basis, depending on timing

of crude purchases and product sales, operations and op-

timization of crude and product pricing. We are exposed to

the fluctuation in crude and product pricing on the inventory

we hold. Currently, we primarily use a commodity price

management program to manage the fluctuation associated

with commodity pricing on a defined volume of inventory.

Under this program we enter into commodity Intercontinental

Exchange (“ICE”) futures contracts and counterparty swaps

to lock in the price of certain commodities.

Most derivative transactions are not designated as effective

hedges, therefore any gains or losses arising from changes in

the fair value of these instruments are recorded in our Consoli-

dated Statement of Comprehensive Income in the line item “Ma-

terials cost”. Our derivative contracts are classified as derivative

instruments and are recorded in our Consolidated State-

ment of Financial Position at fair market value. We currently

do not enter into material derivative financial instruments for

speculative transactions and do not hedge our Group refining

margin. This strategy is continually reviewed and adapted

for current economic and market conditions.

As noted above, our refineries’ results will differ from the

reference benchmarks due to our hedging or commodity price

management activities.

Factors Affecting Operating Results

Overview

Our earnings and cash flows from operations are primarily

affected by the relationship between refined product prices

and the prices for crude oil and other feedstocks. The cost to

acquire crude oil and other feedstocks and the price of refined

petroleum products ultimately sold depend on numerous fac-

tors beyond our control, including the supply of, and demand

for, crude oil, gasoline, diesel and other refined petroleum pro-

ducts, which, in turn, depend on, among other factors, changes

in global and regional economies, weather conditions, global

and regional political affairs, production levels, the availability

of imports, the marketing of competitive fuels, pipeline capac-

ity and availability, prevailing exchange rates and the extent of

government regulation. Our revenue and operating income fluc-

tuate significantly with movements in refined petroleum product

prices; our materials costs fluctuate significantly with move-

ments in crude oil prices and our other operating expenses

fluctuate with movements in the price of energy to meet the

power needs of our refineries. In addition, the effect of changes

in crude oil prices on our operating results is influenced by how

the prices of refined products adjust to reflect such changes.

Crude oil and other feedstock costs and the prices of refined pe-

t roleum products have historically been subject to wide fluctua-

tions. Expansion and upgrading of existing facilities and installa-

tion of additional refinery distillation or conversion capacity, price

volatility, international political and economic developments and

other factors beyond our control are likely to continue to play

an important role in refining industry economics. These factors

can impact, among other things, the level of inventories in the

market, resulting in price volatility and a reduction or increase in

product margins. Moreover, the industry typically experiences

seasonal fluctuations in demand for refined petroleum products,

such as for gasoline and diesel, during the summer driving sea-

son and for home heating oil during the winter.

There is a lag between the time we purchase crude oil to the

time we process and sell finished refined products. Timing

of purchases depends on a number of factors, including the

relevant refinery’s planned throughput, unit disruptions which

may cause usage of lighter and sweeter crude oil and avail-

ability of crude oil. Unplanned downtime has a more economic

impact due to the disruption to the refinery’s normal operating

throughput, which results in a longer time lag between pur-

chases and processing of crude oil. In addition, during un-

planned downtime the timing of crude purchases is disrupted;

which may cause a significant impact on realized gross margin.

Petroplus Holdings AG | Annual Report 2010 | Operating and Financial Review | 17

Our operating results are also affected by safety, reliability and

the environmental performance of our refinery operations. Un-

planned downtime of our refinery assets generally results in

lost margin opportunity and increased maintenance expense.

The financial impact of planned downtime, such as major turn-

around maintenance, is managed through a planning process

that considers such things as, but not limited to, the margin

environment, the availability of resources to perform the need-

ed maintenance and feedstock logistics.

Foreign Currency Fluctuation Management

We are a USD functional currency Company as the majority of

our financing activities and costs of sales are incurred in USD.

We are primarily exposed to the fluctuation in the USD versus

the Swiss Franc (“CHF”), Euro (“EUR”) and the British Pound

(“GBP”) as our local marketing sales are invoiced in local cur-

rencies, and a portion of our local capital expenditures, oper-

ating and personnel costs are incurred in local currencies. We

are also exposed to foreign currency risk because certain of our

assets and liabilities are denominated in currencies other than

USD. To manage foreign currency exposure risk, we enter into

both swaps and forward derivative contracts. As we have not

currently designated our derivative financial instruments as ef-

fective hedges, any gains or losses arising from changes in the

fair value of these instruments are recorded in our Consolidated

Statement of Comprehensive

Income. The Company does not

use derivative contracts to

manage fluctuations on personnel

and operating costs.

Credit Risk Management

Credit risk refers to the risk that a counterparty will default

on its contractual obligations resulting in financial loss to the

Company. Our exposure to credit risk is represented by the

carrying amount of cash and receivables that are presented

in the Consolidated Statement of Financial Position, including

derivatives with positive market values. To minimize credit risk,

all customers are subject to credit verification procedures and

extensions of credit above defined thresholds are subject to

an approval process. We also maintain relationship with sev-

eral different banks in order to minimize our concentration of

risk. Our intention is to grant trade credit only to recognized

creditworthy third parties. In addition, receivable balances are

monitored on an ongoing basis. We also limit the risk of bad

debts by obtaining bank securities such as guarantees or let-

ters of credit and credit insurance.

Other Factors

Our operating cost structure is also important to our profitabil-

ity. Major operating costs include costs relating to employees

and contract labor, energy, maintenance and environmental

compliance. The predominant variable costs are energy re-

lated, in particular, the price of electricity and natural gas. In

addition, operating costs will vary with movements in foreign

currency.

18 | Petroplus Holdings AG | Annual Report 2010 | Operating and Financial Review

2010 Compared to 2009

The following table provides the Consolidated Financial Income

data of Petroplus Holdings AG.

Financial income data

For the year ended December 31,

(in millions of USD) 2010 2009

Revenue 20,735.0 14,797.8

Materials cost (19,406.4) (13,592.4)

Gross margin 1,328.6 1,205.4

Personnel expenses (351.9) (351.1)

Operating expenses (439.8) (451.2)

Depreciation and

amortization

(338.8) (282.1)

Other administrative

expenses

(42.7) (55.7)

Operating profit 155.4 65.3

Financial expense, net (186.5) (164.6)

Foreign currency exchange

(loss)/gain

(2.2) 2.5

Share of income/(loss)

from associates

8.5 (1.6)

Loss before income taxes (24.8) (98.4)

Income tax expense (82.1) (10.4)

Net loss from continuing

operations

(106.9) (108.8)

Loss from discontinued

operations, net of tax

(5.4) (141.1)

Net loss (112.3) (249.9)

Other financial data

EBITDA1) 500.5 348.3

Net loss per share available to shareholders(in USD):

Basic (1.22) (3.20)

Diluted (1.22) (3.20)

1)Earnings before Interest, Tax, Depreciation and Amortization (“EBITDA”)

from Continuing Operations.

Overview

Our operating profit from continuing operations was USD

155.4 million for the year ended December 31, 2010 as com-

pared to an operating profit of USD 65.3 million for the same

period in 2009. Our net loss from continuing operations for

the year ended December 31, 2010 was USD 106.9 million

as compared to a net loss from continuing operations of

USD 108.8 million for the same period in 2009. Our net loss

after discontinued operations attributable to shareholders was

USD 112.3 million (USD 1.22 per share) for the year ended De -

cember 31, 2010 as compared to a net loss of USD 249.9 mil-

lion (USD 3.20 per share) for the same period in 2009. The

net loss in 2010 is mainly attributable to the low, but improved

refining margin environment compared to 2009, and tax im-

pacts resulting from the movement in foreign exchange rates.

Additionally, tax expense was impacted by derecognized and

unrecognized tax losses.

The loss from discontinued operations of USD 5.4 million for

the year ended December 31, 2010 related mainly to the sale

of the Antwerp Processing facility in January 2010, whereas

the loss of USD 141.1 million in 2009 related to discontinued

operations related to the Antwerp Processing facility and the

Teesside refinery.

Revenue

Our revenue increased by USD 5,937.2 million, or 40.1 %, to

USD 20,735.0 million for the year ended December 31, 2010

from USD 14,797.8 million for the year ended December 31,

2009. The increase in revenue is mainly attributable to higher

refined petroleum product prices and increased volumes sold

during 2010 compared to the same period in 2009.

Gross Margin

Our gross margin from continuing operations increased by

USD 123.2 million, or 10.2 %, to USD 1,328.6 million for the

year ended December 31, 2010 from USD 1,205.4 million for

the year ended December 31, 2009. Market conditions im-

proved significantly in 2010 compared to 2009, as reflected in

the PMI which increased by 38 % from USD 2.53 per barrel in

2009 to USD 3.48 per barrel in 2010. This market improvement

is reflected in our gross margin in 2010 which was marked by

positive impacts from increasing global oil demand, improved

refining margin cracks for gasoline and middle distillates, in-

creased throughput and rising oil prices. These impacts were

partially offset by higher cost of fuel consumed by our refiner-

ies due to the increased crude oil price environment. Addition-

ally, gross margin in 2010 was further impacted by the turn-

arounds at the Cressier and Antwerp refineries. Gross margin

in 2009 was impacted by lower refining cracks and reduced

Petroplus Holdings AG | Annual Report 2010 | Operating and Financial Review | 19

throughput at the Cressier and Reichstett refineries due to the

August 2009 incident at the Société du Pipeline Sud-Européen

(“SPSE”) pipeline. Gross margin in 2009 was further impacted

by reduced throughput at the Coryton refinery due to a major

turnaround and a turnaround at the Reichstett refinery.

The 5/2/2/1 benchmark refining margin for the Coryton refin-

ery increased 17 % for the year ended December 31, 2010 as

compared to the same period in 2009 as a result of increased

ULSD and gasoline cracks partially offset by decreased fuel oil

cracks to Dated Brent. The 6/1/2/2/1 benchmark refining mar-

gin for the Antwerp refinery increased 38 % for the year ended

December 31, 2010 as compared to the same period in 2009

as a result of improved gasoil, gasoline and VGO cracks partial-

ly offset by a decline in fuel oil cracks. The 4/1/2/1 benchmark

refining margin for the Petit Couronne and Reichstett refiner-

ies increased 19 % for the year ended December 31, 2010 as

compared to the same period in 2009 as a result of increased

ULSD and gasoline cracks partially offset by decreased fuel

oil cracks to Dated Brent. The 10/1/3/5/1 benchmark refining

margin for the Ingolstadt refinery increased 25 % for the year

ended December 31, 2010 as compared to the same period in

2009. The increase was primarily due to improved ULSD and

gasoline cracks. The 7/2/4/1 benchmark refining margin for the

Cressier refinery increased 31 % for the year ended December

31, 2010 as compared to the same period in 2009 as a result

of higher gasoil and gasoline cracks.

Inland market premiums during 2010 declined compared to

2009. The Cressier refinery earns premiums to market prices,

in part based on the freight rates on the Rhine river, which

is the means of transport for Swiss customers purchasing

refined product from the ARA region. In 2010, Rhine Freight

averaged approximately CHF 18 per ton as compared to

CHF 31 per ton in 2009. In Germany, many of our refined prod-

ucts are based on an Oil Market Report (“OMR”) price. The

average OMR price premium to Platt’s middle distillates dur-

ing 2010 was USD 6 per barrel as compared to an average of

USD 7 per barrel during 2009.

Fuel consumed in the production process has a negative im-

pact on our realization of the benchmark refining margin, fluc-

tuating with the absolute crude price. Dated Brent increased

from approximately USD 62 per barrel on average in the year

ended December 31, 2009 to approximately USD 80 per barrel

in the year ended December 31, 2010. The increase of about

USD 18 per barrel resulted in higher cost of fuel consumed by

the refineries (representing approximately 5 % across our refin-

ing system) which negatively impacted our realized margin by

approximately USD 0.90 per barrel.

We use a commodity price management program to man-

age a small portion of our exposure to fluctuations in com-

modity pricing. Under this program, we enter into commodity

ICE futures contracts and counterparty swaps to lock in the

price of certain commodities. Any gains or losses arising from

changes in the fair value of these instruments are recorded in

our Consolidated Statement of Comprehensive Income in the

line item “Materials cost”. Materials cost included a derivative

gain of USD 21.9 million in 2010 and a loss of USD 5.7 million

in 2009.

Personnel Expenses

Our personnel expenses increased by USD 0.8 million to

USD 351.9 million for the year ended December 31, 2010 from

USD 351.1 million for the same period in 2009. Personnel

costs for the year ended December 31, 2010 were positively

impacted by the strengthening of the USD as personnel costs

are paid in various local currencies, such as the EUR and GBP.

However, this impact was more than offset by higher incen-

tive compensation accrued due to improved Company perfor-

mance in 2010 and termination benefits paid.

Operating Expenses

Our operating expenses decreased by USD 11.4 million to

USD 439.8 million for the year ended December 31, 2010 from

USD 451.2 million for the same period in 2009. The decrease

is mainly attributable to lower maintenance expenses in 2010

due to reduced use of contractors and lower levels of un-

planned maintenance activities than 2009. In addition, operat-

ing expenses were positively impacted by the strengthening

of the USD versus the EUR and GBP in 2010 as compared to

2009, as a significant portion of variable costs such as chemi-

cals and energy, are paid in local currencies. The decrease

was partially offset by higher consumption of natural gas dur-

ing 2010 as the Coryton refinery faced a major turnaround in

2009. Additionally, for economic reasons, we purchased more

natural gas to fuel refinery operations which allowed us to re-

cover and sell our higher-valued, internally produced Liquefied

Petroleum Gas (“LPG”).

Depreciation and Amortization

Our depreciation and amortization expenses increased by

USD 56.7 million, to USD 338.8 million for the year ended De-

cember 31, 2010 from USD 282.1 million for the same period in

2009. The increase in depreciation is mainly attributable to ad-

ditional capital expenditures associated with the turnarounds

at the Coryton and Reichstett refineries in the fourth quarter

of 2009.

20 | Petroplus Holdings AG | Annual Report 2010 | Operating and Financial Review

Other Administrative Expenses

Our other administrative expenses decreased by USD 13.0

million to USD 42.7 million for the year ended December 31,

2010 from USD 55.7 million for the same period in 2009. This

decrease is mainly attributable to a reduction in third party

service fees, including external legal expenses, and reduced

insurance premiums.

Financial Expense, Net

Our net financial expense increased by USD 21.9 million to

USD 186.5 million for the year ended December 31, 2010 from

USD 164.6 million for the same period in 2009. The increase in

2010 is mainly attribut able to higher interest expenses result-

ing from the Company’s refinancing activities which were com-

pleted in October 2009 and partly offset by lower bond accre-

tion expenses during 2010. In addition, expenses increased

related to letter of credit fees due to the higher crude oil price

environment and a one-time fee payment of USD 5.3 million in

the first quarter of 2010 for the Revolving Credit Facility (“RCF”)

covenant waiver.

Foreign Currency Exchange Loss/Gain

Our foreign currency exchange results show a loss of USD 2.2

million for the year ended December 31, 2010 as compared to

a gain of USD 2.5 million for the same period in 2009. The loss

mainly represents the revaluation of certain CHF, GBP and

EUR monetary items against the USD.

Coryton

Throughput in 2010 was impacted by a

planned catalyst change at the naph-

tha desulfurization unit and unplanned

maintenance at the reformer.

Throughput in 2009 was mainly impact-

ed by the fourth quarter planned major

turnaround, which lasted 72 days.

Antwerp

Throughput in 2010 was impacted by a

planned refinery-wide turnaround during

the second quarter. The restart was de-

layed and carried over into July. During

the last quarter, run rates were impacted

by an unplanned shutdown of the hydro-

desulfurization unit.

Throughput in 2009 was impacted by

planned and unplanned maintenance

throughout the year.

Petit Couronne

Throughput in 2010 was impacted by

planned and unplanned shutdowns of

the hydrodesulfurization and lube unit

and by unplanned maintenance at the

vacuum tower in the second quarter.

During the third and fourth quarter, run

rates were reduced as a result of strike

actions in France.

Throughput in 2009 was reduced as a

result of planned maintenance activities

and an unplanned shutdown of the fluid

catalytic cracking unit late in the year.

Refinery Operations – Throughput by Refinery

(in thousands of bpd)

2009 20092010 2010

81.2 111.7

2009

145.7 88.8 122.3

2010

181.2

Petroplus Holdings AG | Annual Report 2010 | Operating and Financial Review | 21

Income Tax Expense

Our income tax expense increased by USD 71.7 million to USD

82.1 million for 2010 as compared to an expense of USD 10.4

million for 2009. The tax rate was impacted by non-cash tax

effects resulting from the movement in foreign exchange rates

and lower realized refining margins. Additionally, the tax rate

was impacted by derecognized and unrecognized tax losses.

Ingolstadt

Throughput in 2010 was impacted by a

planned reformer catalyst regeneration

and planned catalyst changes at hydro-

desulfurization units.

Throughput in 2009 was reduced as a

result of planned downtime on the re-

former unit and minor unplanned down-

time.

Reichstett

Throughput in 2010 was impacted

by a planned fluid catalytic cracking

unit turnaround followed by a delayed

start-up. Furthermore, operations were

affected during the first quarter by un-

planned repairs on the debutanizer col-

umn. During the third and fourth quar-

ter, run rates were reduced as a result of

strike actions in France.

T

hroughput in 2009 was impacted by the

incident at the SPSE pipeline, which lim-

ited crude supply causing downtime and

the acceleration of the turnaround of cer-

tain units originally scheduled for 2010.

Cressier

Throughput in 2010 was impacted by a

planned turnaround in the second quar-

ter of 2010.

Furthermore, throughput was

impacted due to the

labor strike at the

port in Fos Sur Mer, France.

Throughput in 2009 was impacted by

the SPSE pipeline incident in August

2009.

2009

44.1

2009

53.3

2009

93.1

2010

55.2

2010

50.5

2010

98.2

22 | Petroplus Holdings AG | Annual Report 2010 | Operating and Financial Review

Refinery Operations – Throughput and Production Data

The following table provides a summary of total throughput and crude types processed, total production and refined petroleum

products produced by our six refineries for the years ended December 31, 2010 and 2009:

For the year ended December 31,

(in thousands of bpd) 2010 2009

Throughput

Crude Unit Throughput

Light sweet 260.3 44 % 200.3 38 %

Medium sweet 31.3 5 % 17.0 3 %

Heavy sweet – – 1.4 0 %

Light sour 107.4 18 % 128.1 24 %

Medium sour 114.0 19 % 84.6 16 %

Heavy sour 18.3 3 % 25.9 5 %

Total Crude Unit Throughput 531.3 89 % 457.3 86 %

Other throughput 64.9 11 % 71.8 14 %

Total Throughput 596.2 100 % 529.1 100 %

For the year ended December 31,

(in thousands of bpd) 2010 2009

Production

Light Products

Gasoline 161.4 27 % 145.6 28 %

Diesels and gasoils 261.5 44 % 228.0 43 %

Jet fuel 35.0 6 % 29.1 5 %

Petrochemicals 11.9 2 % 11.0 2 %

Naphtha 20.1 3 % 17.5 3 %

Liquefied petroleum gas (LPG) 29.9 5 % 29.8 6 %

Total Light Products 519.8 87 % 461.0 87 %

Fuel oil/Bitumen 60.2 10 % 52.3 10 %

Solid by-products/fuel consumed in process/fuel & loss1) 28.3 5 % 26.3 5 %

Total Production 608.3 102 % 539.6 102 %

1)The fuel consumed in-process is a percentage of the total crude, feedstock and gasoline/diesel blending additives used.

Petroplus Holdings AG | Annual Report 2010 | Operating and Financial Review | 23

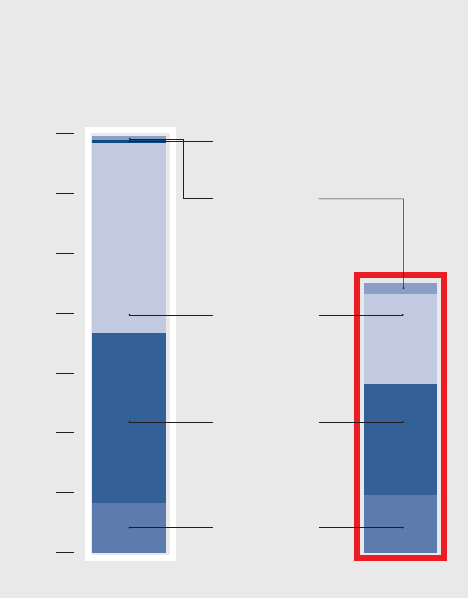

Petroplus Throughput

Petroplus Production

2010

2010

2009

2009

Sweet 41 %49 %

Other throughput

Light sour 24 %18 %

Medium sour

11 % 14 %

Heavy sour

19 % 16 %

5 %

3 %

Gasoline 28 %27 %

6 %

5 %

Middle distillates 48 %50 %

Fuel oil/Bitumen10 % 10 %

LPG

Naphtha/Petrochemicals

Solid by-products/fuel & loss

5 % 5 %

5 %

5 %

24 | Petroplus Holdings AG | Annual Report 2010 | Operating and Financial Review

Liquidity and Capital Resources

Cash Flows

The following table summarizes the cash flow activity for the periods indicated, including cash flows from discontinued operations:

For the year ended December 31,

(in millions of USD) 2010 2009

Cash flows from operating activities 429.7 (97.1)

Cash flows from investing activities (230.8) (272.6)

Cash flows from financing activities (40.4) 159.3

Net increase/(decrease) in cash and short-term deposits 158.5 (210.4)

Net foreign exchange differences 9.3 11.8

Cash and short-term deposits at beginning of period 11.2 209.8

Cash and short-term deposits at end of period 179.0 11.2

Cash Flows from Operating Activities

Net cash flows provided by operating activities were USD

429.7 million for the year ended December 31, 2010 as com-

pared to net cash used in operating activities of USD 97.1 mil-

lion for the same period in 2009. Net result, after excluding

non-cash depreciation and amortization and income tax ex-

penses, contributed USD 309.5 million for 2010 versus USD

162.8 million for 2009. Cash flows from operating activities

were positively impacted by higher oil prices and improved re-

fining margin cracks for middle distillates and gasoline in 2010

compared to 2009. Net changes in working capital provided

an additional USD 163.0 million in cash flow for the year ended

December 31, 2010 as compared to USD 248.4 million used

for the same period in 2009.

Cash Flows from Investing Activities

Net cash flows used in investing activities were USD 230.8

million for the year ended December 31, 2010 as compared

to net cash used in investing activities of USD 272.6 mil-

lion for the same period in 2009. The cash used in investing

activities in 2010 resulted primarily from planned capital ex-

penditures and turnaround activity in the fourth quarter 2009

and during 2010. The disposal of PBF generated a net cash

inflow of USD 5.5 million after the cash contribution of USD

76.4 million in May 2010 and the subsequent disposal in Octo-

ber 2010 which resulted in cash proceeds of USD 81.9 million.

On January 12, 2010, the Company completed the sale of the

Antwerp Processing facility and associated working capital,

which resulted in net cash proceeds of USD 56.2 million.

Net cash used in investing activities in 2009 resulted primarily

from capital expenditures in addition to turnaround activities

at the Coryton, Petit Couronne, Reichstett and Ingolstadt re-

fineries.

Cash Flows from Financing Activities

Net cash flows used in financing activities were USD 40.4 mil-

lion for the year ended December 31, 2010 as compared to net

cash provided by financing activities of USD 159.3 million for

the same period in 2009. Financing activities in 2010 primar-

ily represent net cash repayments on the RCF. Additionally,

in May 2010, the Company completed a private placement of

shares which resulted in gross proceeds of USD 136.4 million.

In September 2009, the Company issued Senior Notes,

9.375 % due 2019, resulting in net proceeds of USD 385.5 mil-

lion which were used to repurchase a portion of the Convert-

ible Bond, 3.375 % due 2013, in October 2009. Additionally,

the Company issued a USD 150.0 million Convertible Bond,

4.0 % due 2015, and completed a rights offering which result-

ed in net proceeds of USD 272.0 million. Additional financing

activities represent repayment of borrowings under the work-

ing capital facility.

Petroplus Holdings AG | Annual Report 2010 | Operating and Financial Review | 25

Capital Spending

We classify our capital expenditures, excluding acquisition

expenditures, into five major categories:

Permit-related capital expenditures include capital expen-

ditures for improvements and upgrades to our production

facilities required by local authorities as a condition of the

granting or renewal of the operating permits for our facilities.

These include process safety improvements and installation of

equipment to reduce emissions to the environment.

Sustaining capital expenditures include regular, non-permit

related capital expenditures we incur to maintain our produc-

tion facilities and to facilitate reliable operations.

Turnaround capital expenditures include capital expenditures

incurred in connection with planned shutdowns to make ne-

cessary repairs, perform preventative maintenance, replace

catalysts and implement improvements. We perform major

scheduled turnarounds on each of our refineries generally

every four to five years, with an intermediate, minor turnaround

generally two years following each scheduled major mainten-

ance turnaround.

Project-related capital expenditures include capital expendi-

tures for improvements or upgrades to our production facilities

that have been identified to provide significant gross margin

returns. These projects are expected to either add capacity

or increase product yields in higher value petroleum products.

Information technology (“IT”)/Intangibles capital expenditures

include costs associated with software integration primarily

from acquisitions and system upgrades. This category also in-

cludes other hardware and capital expenditures for intangible

assets.

Our total capital expenditures are summarized in the follow-

ing table by major category for the years ended December 31

2009 and 2010:

Information about our 2011 planned capital expenditures is

discussed in the “Outlook” section.

Turnaround

Total

347.7

Total

226.9

3.7

1.9

158.8

41.7

9.9

–

75.7

92.9

48.4

Sustaining

Permit-

related

0

50

100

150

200

250

300

350

2009 2010

Projects

IT/

Intangibles

Actual Capital Expenditures

(in millions of USD)

141.6

26 | Petroplus Holdings AG | Annual Report 2010 | Operating and Financial Review

Summary of Indebtedness

Overview

The following table sets forth our financial indebtedness and

cash balances as of December 31:

The following table illustrates the Company’s maturity profile

for long-term interest-bearing loans and borrowings:

The following description is a summary of our credit facilities

and other financing arrangements, including a description of

the usage of such facilities and arrangements.

(in millions of USD) 2010 2009

Long-term debt 1,692.0 1,683.8

Working capital facilities – 149.6

Total financial debt 1,692.0 1,833.4

Cash and short-term

deposits

179.0 11.2

Net financial debt 1,513.0 1,822.2

Maturity Profile

(in millions of USD)

600

500

400

300

200

100

Senior Notes Convertible Bonds

0

2014

600

2015

150

2011 20162012 2017

600

2013 2018 2019

400

Working Capital Facilities

Revolving Credit Facility (“RCF”)

Certain of our subsidiaries are party to a USD 1.05 billion com-

mitted multicurrency secured RCF agreement dated October

16, 2009, which replaced our former revolving credit facility.

The RCF includes an option to increase the committed facil-

ity amount up to USD 2.0 billion on a pre-approved but not

pre-committed basis in the event of increased working capital

needs or future acquisitions. The Company also has access to

significant uncommitted lines from committed banks, providing

increased liquidity on an as needed basis. As of December 31,

2010, the Company had additional uncommitted lines under the

RCF of USD 1.07 billion, bringing the total size of the RCF to

USD 2.12 billion.

The RCF is available, subject to a current asset borrowing

base, primarily in the form of letters of credit and short-term

loan advances. Not more than 60 % of the committed line util-

izations may be in the form of short-term cash borrowings.

The rate of interest on cash borrowings is the aggregate of

LIBOR plus a margin plus mandatory costs, if any. The mar-

gin is subject to a pricing grid determined by reference to the

Company’s ratio of Net Debt to Net Capitalization and ranges

from 2.75 % to 4.00 % for a ratio below 25 % or above 60 %,

respectively. Commissions on payment instruments are also

subject to a pricing grid determined by reference to the Com-

pany’s ratio of Net Debt to Net Capitalization.

Borrowings under the RCF are jointly and severally guaranteed

by certain of our subsidiaries. Such borrowings are secured

by certain assets of the borrowers and of the guarantors.

The form of such security includes certain pledges of bank

accounts held at participating banks, oil inventory, trade re-

ceivables and other assets. In certain conditions related to

an event of default as defined in the RCF, the RCF Security

Agent can enforce the pledge over the pledged assets. These

pledges will expire together with the RCF on October 16, 2012.

As of December 31, 2010, we have no cash borrowings under

the RCF. The related financing costs of USD 15.1 million are

capitalized and amortized over the three-year term of the RCF.

The carrying amount of these costs under the RCF amounts to

USD 9.0 million as of December 31, 2010.

Other Working Capital Facilities

One of our subsidiaries has a smaller working capital facility

available in relation to Swiss compulsory stocks of which USD

nil (2009: USD 24.3 million) was drawn upon as of December

31, 2010.

Petroplus Holdings AG | Annual Report 2010 | Operating and Financial Review | 27

Covenants

The RCF contains covenants that could restrict certain of

our activities, including restrictions on creating or permitting

to subsist certain securities, engaging in certain mergers or

consolidations, sales or other disposals of certain assets, giv-

ing certain guarantees, making certain loans, making certain

investments, incurring certain additional indebtedness, en-

gaging in different businesses, making certain debt or other

restricted payments, and amending or waiving certain material

agreements.

The RCF also includes three financial covenants, calculated on

a quarterly basis, requiring us to maintain:

–

a minimum Consolidated Tangible Net Worth of USD 1.5 billion;

– a minimum ratio of Group Clean EBITDA (as defined in the

RCF documentation) to Net Interest Expense of 2.5 to 1.0 for

the four prior rolling consecutive quarters; and

–

a minimum ratio of Current Assets to Current Liabilities of 1.05:1.

Compliance with these covenants is determined in the manner

specified in the documentation governing the RCF.

At December 31, 2009, the Clean EBITDA to Net Interest Ex-

pense ratio was below 2.5 to 1.0. On January 27, 2010, the

Company received a waiver for the fourth quarter 2009 through

the third quarter 2010. During the waiver period, and, as long

as the ratio of the Clean EBITDA to Net Interest Expense ratio

covenant was below 2.5 to 1.0, the interest rate margin on cash

borrowings was increased by 0.25 % and the Company was

required to meet an additional covenant. The Company’s Free

Cash Flow before working capital changes, as defined in the

waiver documentation, could not be more negative than minus

USD 250 million for the period starting from January 1, 2010

to each quarter end during the waiver period. The Company

fulfilled this temporary covenant throughout the year 2010. The

Company is in compliance with all financial covenants based

on year-end 2010 financial figures, and has, therefore, exited

the waiver period.

Long-Term Debt

Convertible Bond USD 150 million, 4.0 % due 2015

(the “2015 CB”)

On October 16, 2009, Petroplus Finance Ltd., a subsidiary of

the Company, issued USD 150.0 million in guaranteed senior

secured convertible bonds due 2015. The debt is guaranteed

by the Company as well as by certain of its subsidiaries. Each

bond in the principal amount of USD 100,000 is convertible

into common shares of the Company at a conversion price of

CHF 30.42 (subsequent to a reduction of CHF 0.19 due to the

nominal value repayment on July 26, 2010) per share with a

fixed exchange rate on conversion of USD/CHF 1.0469. The

2015 CB bears interest at the rate of 4.0 % per annum, with the

interest payable semi-annually in arrears on October 16 and

April 16 of each year the debt is outstanding, commencing on

April 16, 2010. The financing costs related to the issuance of

the 2015 CB have been capitalized in the aggregate amount of

USD 2.6 million and are amortized over six years.

Convertible Bond USD 500 million, 3.375 % due 2013

(the “2013 CB”) redeemed on October 16, 2009

On October 12, 2009, Petroplus announced the successful re-

sult of the tender offer to repurchase all of its outstanding USD

500.0 million in guaranteed, convertible bonds due in 2013.

The 2013 CB was redeemed on October 16, 2009 at the ag-

gregate principal amount of USD 500.0 million, plus accrued

interest calculated from September 26, 2009 until October 16,

2009 (20 days). The related remaining capitalized financing

costs of USD 6.0 million and the difference between the carry-

ing amount and the fair value of the liability portion of USD 2.1

million were written off and included in the line item “Financial

expenses” in the Consolidated Statement of Comprehensive

Income. The remaining difference of USD 35.0 million between

the repurchase price of the bond and the fair value of the liabil-

ity portion was recorded as a reduction of equity. The costs of

the tender offer amounted to USD 2.6 million and were includ-

ed in the line item “Financial expenses” in the Consolidated

Statement of Comprehensive Income.

Senior Notes USD 400 million, 9.375 % due 2019

(the “2019 SN”)

On September 17, 2009, Petroplus Finance 3 Limited, Ber-

muda, an unrestricted subsidiary of the Company, issued USD

400.0 million aggregate principal amount of 9.375 % senior

notes due 2019 at an issue price of 98.42 % giving a yield of

9.625 %. The coupon is payable semi-annually in arrears on

March 15 and September 15, beginning March 15, 2010. The

2019 SN are presented net of capitalized financing costs of

USD 8.7 million which are amortized over ten years. The pro-

ceeds from the 2019 SN were used to repurchase or redeem

a portion of the 2013 CB on October 16, 2009.

Upon successful completion of the tender offer and subse-

quent repayment of the 2013 CB, Petroplus Finance Limited

assumed the obligations of Petroplus Finance 3 Limited un-

der the 2019 SN, the Company and certain of its subsidiaries

became guarantors of the 2019 SN and Petroplus Finance 3

Limited was released of all obligations under the 2019 SN.

28 | Petroplus Holdings AG | Annual Report 2010 | Operating and Financial Review

Liquidity

Our ability to pay interest and principal on our indebtedness

and to satisfy our other debt obligations will depend upon our

future operating performance and the availability of new and

refinancing indebtedness, which can be affected by prevailing

economic conditions and financial, business and other fac-

tors, some of which are beyond our control.

We believe that our cash flows from operations, borrowings

under our existing credit facilities and other capital resources

will be sufficient to satisfy the anticipated cash requirements

associated with our existing operations during the next twelve

months. Our ability to generate sufficient cash from our oper-

ating activities depends on our future performance and global

oil market pricing, which are subject to general economic,

political, financial, competitive and other factors beyond our

control. The Company could, during periods of economic

downturn, access the capital markets and/or other available

financial resources to strengthen its financial position. In ad-

dition, our future capital expenditures and other cash require-

ments could be higher than we currently expect as a result of

various factors, including any acquisitions that we may complete.

Contractual Obligations

The following table summarizes our material contractual obli-

gations and commitments as of December 31, 2010:

Payment due by Period

(in millions of USD) Total < 1 year 1 – 5 years > 5 Years

Interest-bearing loans and borrowings1) 2,506.5 126.0 1,185.3 1,195.2

Finance lease commitments 30.2 3.4 13.4 13.4

Operating lease commitments 66.9 17.6 26.6 22.7

Purchase commitments2) 40.8 40.8 – –