Investor's Eye Sep30_11.pmd DPG110/120 BAJCORP 20110930

User Manual: DPG110/120

Open the PDF directly: View PDF ![]() .

.

Page Count: 6

Visit us at www.sharekhan.com September 30, 2011

Index

Stock Update >> Bajaj Corp

Viewpoint >> Rupa & Co

For Private Circulation only

Sharekhan Ltd, Regd Add: 10th Floor, Beta Building, Lodha iThink Techno Campus, Off. JVLR, Opp. Kanjurmarg Railway

Station, Kanjurmarg (East), Mumbai – 400 042, Maharashtra. Tel: 022 - 61150000. BSE Cash-INB011073351; F&O-

INF011073351; NSE – INB/INF231073330; CD - INE231073330; MCX Stock Exchange: CD - INE261073330 DP: NSDL-IN-DP-NSDL-

233-2003; CDSL-IN-DP-CDSL-271-2004; PMS INP000000662; Mutual Fund: ARN 20669. Sharekhan Commodities Pvt. Ltd.: MCX-

10080; (MCX/TCM/CORP/0425); NCDEX -00132; (NCDEX/TCM/CORP/0142)

2

Sharekhan Home Next

September 30, 2011

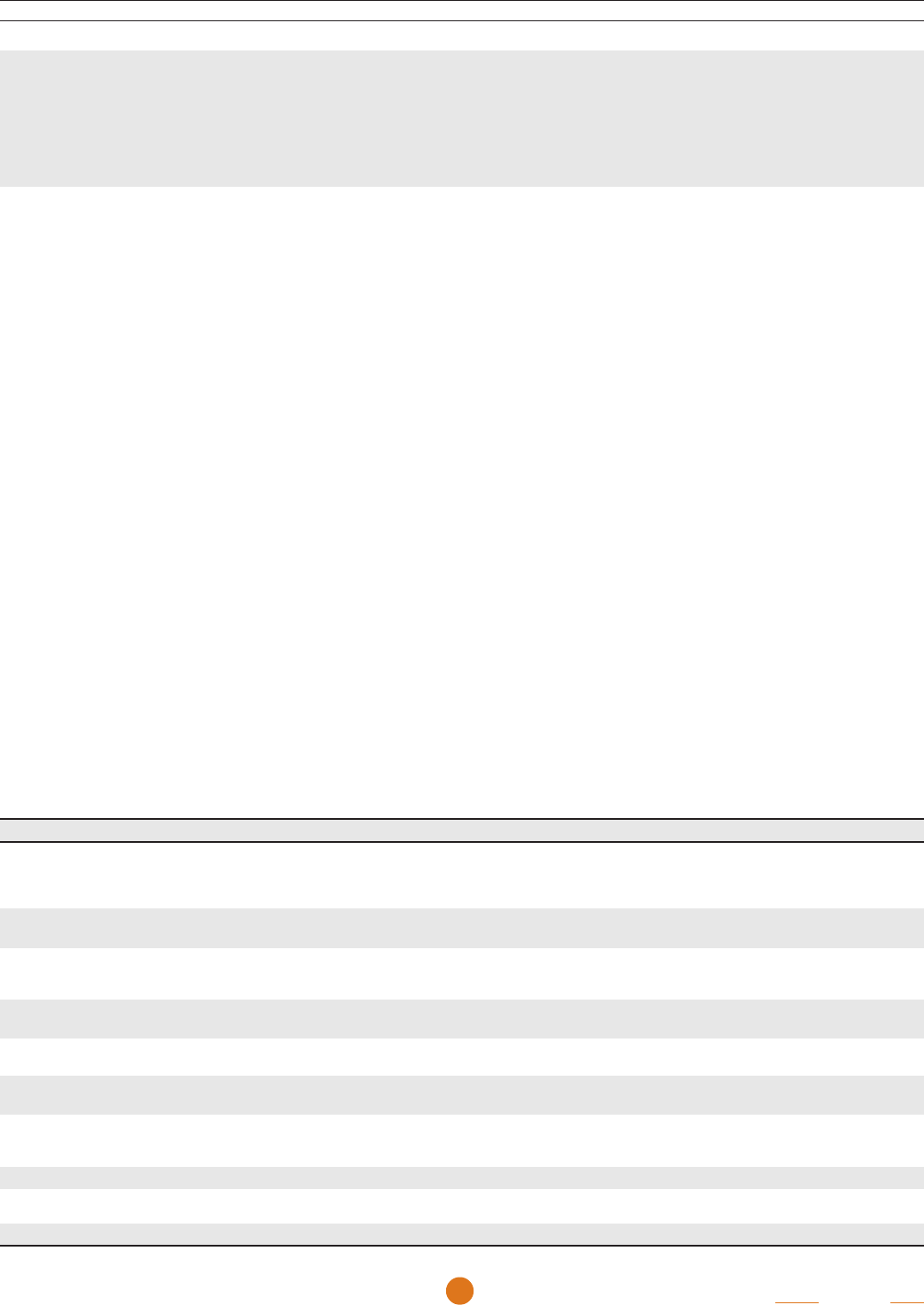

Promoter

s

86%

Domestic

institutions

4%

Others

5%

FIIs

5%

investor’s eye stock updateinvestor’s eye stock update

Company details

Price chart

Shareholding pattern

Price performance

(%) 1m 3m 6m 12m

Absolute 4.1 4.1 31.7 -14.3

Relative 2.3 16.1 49.0 0.9

to Sensex

Price target: Rs142

Market cap: Rs1,563 cr

52 week high/low: Rs146/73

NSE volume: 42,263

(No of shares)

BSE code: 533229

NSE code: BAJAJCORP

Sharekhan code: BAJAJCORP

Free float: 2.2 cr

(No of shares)

Event: acquisition of property for Rs75 crore for its corporate office

Bajaj Corp Ltd (BCL) has acquired Uptown Properties and Leasing Pvt Ltd (Uptown)

for Rs75 crore (including liabilities of Rs49.5 crore). Uptown owns a building in

Worli (Mumbai) with a built-up area of 33,600 square feet. The sole reason behind

the acquisition is to develop a corporate office on the acquired plot to bring in all

the scattered divisions at various locations under one roof to improve the

operational efficiencies.

Expensive acquisition compared to recent deals

Judicious utilisation of free cash on the books to expand its product range or to

grow inorganically was one of the key triggers in the stock and the market was

enthused by the recent launch of the cooling hair oil, Kailash Parbat, which was in

line with the stated strategy.

However, the move to spend a substantial chunk of this cash on non-yielding assets

such as property, that too at a premium, would dilute its earnings and is seen as a

de-rating factor by us. More so, since the company would have to spend additional

Rs15-20 crore on either refurbishing the existing property or rebuilding a new

structure.

Valuation corrects in response to move

To factor in the deal, we have downgraded our earnings estimates by 1.6% and

2.4% for FY2012 and FY2013 respectively. The BCL stock has already reacted

negatively to the announcement of the property deal and factors in the negative

implication of the same at the current market price. Going forward, any initiative

on the company’s part to expand its limited product portfolio or strengthen its

core business would be the key upside trigger for the stock.

At the current market price the stock trades at 13.4x its FY2012E earnings per

share (EPS) of Rs7.8 and 11.1x its FY2013E EPS of Rs9.5. We maintain our Buy

recommendation on the stock with the price target of Rs142 (15x FY2013E earnings

Valuation table

Particulars FY2009 FY2010 FY2011 FY2012E FY2013E

Net sales (Rs cr) 244.4 294.9 359.4 464.2 550.4

Operating profit (Rs cr) 51.3 97.7 108.9 126.2 153.5

Adjusted PAT (Rs cr) 46.8 83.9 103.1 115.5 139.7

EPS (Rs.) 3.2 5.7 7.0 7.8 9.5

OPM (%) 21.0 33.1 30.3 27.2 27.9

PE (x) 33.0 18.4 15.0 13.4 11.1

Market Cap / sales (x) 2.1 4.4 4.3 3.3 2.8

EV/EBIDTA (x) 9.2 13.2 13.3 8.8 6.5

RoE(%) 181.4 211.0 49.2 26.8 26.6

RoCE(%) 204.9 256.2 59.2 33.7 33.5

Bajaj Corp Ugly Duckling

Stock Update

Price target revised to Rs142 Buy; CMP: Rs104

60

70

80

90

100

110

120

130

140

150

Sep-10

Dec-10

Mar-11

Jun-11

Sep-11

3

Sharekhan September 30, 2011 Home Next

investor’s eye stock updateinvestor’s eye stock update

as against 16x earlier due to the not so judicious use of

free cash on the books).

Aiming for an acquisition: The company is looking to

carry out an acquisition in the personal care segment in

either the domestic market or the international market.

The acquisition could be of a brand or of an entity with a

decent portfolio of brands that suits BCL’s existing product

portfolio. After paying for the acquisition of Uptown, the

company would have cash of around Rs325 crore in

balance. This combined with debt (if required) can be

utilised for a strategic buy-out.

Q2FY2012 to be another good quarter: The company

has yet to feel the heat of the current inflationary

situation and expect its strong volume growth to sustain

in the coming quarters. For Q2FY2012, we expect the

company’s top line to grow by 29% year on year (YoY) to

Rs105.0 crore with a sales volume growth of around 18%

YoY. The prices of the key raw materials such as liquid

paraffin and glass bottles remained firm during the

quarter. Hence, we expect the gross profit margin to

decline by 334 basis points YoY and the operating profit

margin (OPM) to decline by 192 basis points YoY in

Q2FY2012. However, with a higher other income YoY, we

expect the bottom line to grow by 29% YoY to Rs25.7 crore

during the quarter.

Outlook and valuation: To factor in the deal, we have

downgraded our earnings by 1.6% and 2.4% for FY2012

and FY2013 respectively. The BCL stock has already

reacted negatively to the announcement of the property

deal and factors in the negative implication of the same

at the current market price. Going forward, any

initiative on the company’s part to expand its portfolio

or strengthen its core business would be the key upside

trigger for the stock.

At the current market price the stock trades at 13.4x its

FY2012E EPS of Rs7.8 and 11.1x its FY2013E EPS of Rs9.5.

We maintain our Buy recommendation on the stock with

the price target of Rs142 (15x FY2013E earnings as against

16x earlier due to the not so judicious use of free cash on

the books).

The author doesn’t hold any investment in any of the companies mentioned in the article.

4

Sharekhan Home Next

September 30, 2011

Rupa & Co

Viewpoint

Good brands + strong distribution reach < Valuation CMP: Rs152

We attended the analyst meet of Rupa & Co (Rupa). We

present below the key takeaways from the meet. Amongst

the listed innerwear players we continue to like Page

Industries.

Present in fast growing underpenetrated men’s inner-

wear segment

India’s domestic branded innerwear market is currently

valued at Rs13,000 crore (CRISIL estimate) of which men’s

innerwear segment is worth close to Rs5500 crore. The

men’s segment has grown at a compounded annual growth

rate (CAGR) of 12.7% over the last four years and is

expected to grow at 17.3% for the next three years.

Further, the penetration of brands is abysmally low in

India, providing huge opportunity for branded players to

encash on the strong consumer wave.

Largest men’s innerwear company with bouquet of brands

Rupa is the largest men’s innerwear player by volume (in

FY2011, it sold 168 million pieces). It has presence across

the value chain with products in categories ranging from

basic to mid premium, premium and super premium

(entered into the last category recently). Its flagship

investor’s eye viewpoint

brands Rupa, Frontline, Jon and Air are in the basic and

mid premium categories while brands like Euro, Macro

Man and Macro Man M Series target the premium and

super premium categories.

Strong distribution reach—deep and wide

The company sells its products through multi-brand

outlets, hosiery stores and national chain stores. It does

not have any exclusive outlets at present. It has an

enviable distribution network, serving one lakh retail

outlets through a strong network of 950 distributors.

All set to focus on high-end premium and super

premium category

Amongst the three listed innerwear players, Rupa earns

relatively lower operating profit margin (OPM) in the band

of 10-11% vs 18-19% enjoyed by the peers Page Industries

and Lovable Lingerie. This is largely due to the fact that

the company is present in mainly mass and basic segments

because of which it has to compete with unbranded/

regional players. Its margins are therefore low. In an effort

to enhance its margins, productivity and move up the

value chain the company is now focusing on the premium

Business comparison

Particulars Page Industries Lovable Lingerie Rupa & Co

Brands Jockey Daisy Dee, Lovable Rupa: Frontline, Thermocot, Rupa

Macro Man, Macro Man M Series,

Euro and Bumchums

Brand status Exclusive licencee; pays royalty Owned Owned

@ 5% sales

Positioning Premium to mid premium Premium Largely basic and mid premium

(80%)

Category Largely men’s (85% share), ventured Women Largely men’s; >98%, entered the

into women's in 2005 women's segment recently

Market share 25% 30% -

Competitors Hanes, Chromosome, Fruit of the loom Triumph, Enamour, VIP, Amul, Lux and regional players

Amante in basic; Jockey in premium

Channel mix MBOs, EBOs, Hosiery, and national MBOs, EBOs, national MBO’s, hosiery,

chain stores chain stores national chain stores

Distributors 400 100 950

Retail reach 20,000 8,500 100,000

EBOs 72 - -

5

Sharekhan September 30, 2011 Home Next

investor’s eye viewpoint

and super-premium brands like Macro Man, Macro Man M

Series and Euro.

Raw material sensitivity high: Its basic products constitute

around 40% of its overall top line. Thus Rupa’s margins

and volumes are most sensitive to the vagaries of the

raw material prices (cotton yarn), as the brands/products

compete with the regional/unbranded players. Thus any

sharp movement leads to a constant revision in the price

of the final product and in the margin.

We prefer Page Industries: Amongst the listed innerwear

players, we continue to be bullish on Page Industries,

given its superior growth levels, brand equity strength

(which is creating strong entry barrier for new players),

enviable margins, return ratios (best in the industry,

averaging 45-48%), and proactive management approach

(it has now entered the swimwear and sportswear

categories by bagging the exclusive Speedo licence for

Indian operations).

Financial comparison

Particulars Page Lovable Rupa

Top line FY11 492 104 639

Sales CAGR (FY08-11) (%) 36.7 20.1 22.2

Operating profit (FY11) 93.0 19.5 66.8

Operating profit CAGR (FY08-11) (%) 36.1 38 31.2

Operating profit margin (%) 19.1 18.70 10.5

Net profit (Rs cr) 58.6 14.1 32

Net profit CAGR (FY08-11) (%) 34.9 53.1 40.0

Debt equity 0.9 - 1.1

RoCE (%) 47 22 22

RoE (%) 52.7 17 22

Market cap 2,827.0 749 1264

PER (x) 48.3 53.1 39.5

EV (x) 2,942.2 749 1282

EV/EBITDA (x) 31.6 38.4 19.2

No of pieces sold (mn pcs) 62.7 8.7 168

Realisation per piece 78.4 119.6 38.0

Profit per piece 9.3 16.2 1.9

The author doesn’t hold any investment in any of the companies mentioned in the article.

6

Sharekhan Home Next

September 30, 2011

Evergreen

Housing Development Finance Corporation

HDFC Bank

Infosys

Larsen & Toubro

Reliance Industries

Tata Consultancy Services

Emerging Star

Axis Bank (UTI Bank)

Cadila Healthcare

Eros International Media

Greaves Cotton

IL&FS Transportation Networks

IRB Infrastructure Developers

Max India

Opto Circuits India

Patels Airtemp India

Thermax

Yes Bank

Zydus Wellness

Apple Green

Apollo Tyres

Bajaj Auto

Bajaj FinServ

Bajaj Holdings & Investment

Bank of Baroda

Bank of India

Bharat Electronics

Bharat Heavy Electricals

Bharti Airtel

Corporation Bank

Crompton Greaves

Divi's Laboratories

GAIL India

Glenmark Pharmaceuticals

Godrej Consumer Products

Grasim Industries

HCL Technologies

Hindustan Unilever

ICICI Bank

Indian Hotels Company

ITC

Mahindra & Mahindra

Marico

Maruti Suzuki India

Lupin

Piramal Healthcare (Nicholas Piramal India)

PTC India

Punj Lloyd

Sintex Industries

State Bank of India

Tata Global Beverages (Tata Tea)

Wipro

Ugly Duckling

Ashok Leyland

Bajaj Corp

CESC

Deepak Fertilisers & Petrochemicals Corporation

Federal Bank

Gayatri Projects

Genus Power Infrastructures

India Cements

Ipca Laboratories

ISMT

Jaiprakash Associates

Kewal Kiran Clothing

NIIT Technologies

Orbit Corporation

Polaris Software Lab

Pratibha Industries

Provogue India

Punjab National Bank

Ratnamani Metals and Tubes

Selan Exploration Technology

Shiv-Vani Oil & Gas Exploration Services

Subros

Sun Pharmaceutical Industries

Torrent Pharmaceuticals

UltraTech Cement

Union Bank of India

United Phosphorus

V-Guard Industries

Vulture’s Pick

Mahindra Lifespace Developers

Orient Paper and Industries

Tata Chemicals

Unity Infraprojects

Cannonball

Allahabad Bank

Andhra Bank

IDBI Bank

Madras Cements

Phillips Carbon Black

Shree Cement

To know more about our products and services click here.

Sharekhan Stock Idea

Disclaimer

“This document has been prepared by Sharekhan Ltd.(SHAREKHAN) This Document is subject to changes without prior notice and is intended only for the person or entity to which it is addressed to and may contain confidential and/or

privileged material and is not for any type of circulation. Any review, retransmission, or any other use is prohibited. Kindly note that this document does not constitute an offer or solicitation for the purchase or sale of any financial

instrument or as an official confirmation of any transaction.

Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. SHAREKHAN will not treat recipients as customers by virtue of their receiving this report.

The information contained herein is from publicly available data or other sources believed to be reliable. While we would endeavour to update the information herein on reasonable basis, SHAREKHAN, its subsidiaries and associated

companies, their directors and employees (“SHAREKHAN and affiliates”) are under no obligation to update or keep the information current. Also, there may be regulatory, compliance, or other reasons that may prevent SHAREKHAN and

affiliates from doing so. We do not represent that information contained herein is accurate or complete and it should not be relied upon as such. This document is prepared for assistance only and is not intended to be and must not alone

betaken as the basis for an investment decision. The user assumes the entire risk of any use made of this information. Each recipient of this document should make such investigations as it deems necessary to arrive at an independent

evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved), and should consult its own advisors to determine the merits and risks of such an investment. The investment

discussed or views expressed may not be suitable for all investors. We do not undertake to advise you as to any change of our views. Affiliates of Sharekhan may have issued other reports that are inconsistent with and reach different

conclusion from the information presented in this report.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or

use would be contrary to law, regulation or which would subject SHAREKHAN and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all

jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction.

SHAREKHAN & affiliates may have used the information set forth herein before publication and may have positions in, may from time to time purchase or sell or may be materially interested in any of the securities mentioned or related

securities. SHAREKHAN may from time to time solicit from, or perform investment banking, or other services for, any company mentioned herein. Without limiting any of the foregoing, in no event shall SHAREKHAN, any of its affiliates

or any third party involved in, or related to, computing or compiling the information have any liability for any damages of any kind. Any comments or statements made herein are those of the analyst and do not necessarily reflect those

of SHAREKHAN.”