Analytics In A Big Data World Bart Baesens The Essential Guide To Science And Its Applicati

Bart%20Baesens%20Analytics%20in%20a%20Big%20Data%20World%20The%20Essential%20Guide%20to%20Data%20Science%20and%20its%20Applicati

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 252 [warning: Documents this large are best viewed by clicking the View PDF Link!]

- Analytics in a Big Data World

- Wiley & SAS Business Series

- Contents

- Preface

- Acknowledgments

- CHAPTER 1 Big Data and Analytics

- CHAPTER 2 Data Collection, Sampling, and Preprocessing

- CHAPTER 3 Predictive Analytics

- CHAPTER 4 Descriptive Analytics

- CHAPTER 5 Survival Analysis

- CHAPTER 6 Social Network Analytics

- CHAPTER 7 Analytics: Putting It All to Work

- CHAPTER 8 Example Applications

- CHURN PREDICTION

- RECOMMENDER SYSTEMS

- WEB ANALYTICS

- SOCIAL MEDIA ANALYTICS

- BUSINESS PROCESS ANALYTICS

- NOTES

- About the Author

- INDEX

Analytics in a Big

Data World

Wiley & SAS

Business Series

The Wiley & SAS Business Series presents books that help senior‐level

mana

g

ers with their critical mana

g

ement decisions.

Tit

l

es in t

h

e Wi

l

e

y

& SAS Business Series inc

l

u

d

e:

A

ctivity‐Base

d

Mana

g

ement

f

or Financia

l

Institutions: Drivin

g

Bottom‐

L

ine

R

esults

b

y

Brent Bahnub

Bank Fraud: Using Technology to Combat Losse

s

by Revathi Subramanian

Big Data Analytics: Turning Big Data into Big Money b

y

Frank Ohlhorst

Branded! How Retailers En

g

a

g

e Consumers with Social Media and Mobil-

it

y

by Bernie Brennan and Lori Schafer

Business Analytics for Customer Intelligence b

y

Gert Laursen

Business Analytics for Mana

g

ers: Takin

g

Business Intelli

g

ence beyond

Reporting by Gert Laursen and Jesper Thorlund

The Business Forecasting Deal: Exposing Bad Practices and Providing

Practical Solutions by Michael Gilliland

Business Intelligence Applied: Implementing an Effective Information and

Communications Technolo

g

y Infrastructure b

y

Michael Gendron

Business Intelligence in the Cloud: Strategic Implementation Guide by

Michael S. Gendron

Business Intelli

g

ence Success Factors: Tools for Ali

g

nin

g

Your Business in

the Global Economy by Olivia Parr Rud

CIO Best Practices: Enabling Strategic Value with Information Technology,

secon

d

e

d

ition

b

y Joe Stenze

l

Connectin

g

Or

g

anizationa

l

Si

l

os: Ta

k

in

g

Know

l

e

dg

e F

l

ow Mana

g

ement to

t

h

e

N

ext Leve

l

wit

h

Socia

l

Me

d

ia

by

Fran

k

Leistner

Cre

d

it Ris

k

Assessment: T

h

e New Len

d

ing System

f

or Borrowers, Len

d

ers,

and

I

nvestors

by

C

l

ar

k

A

b

ra

h

ams an

d

Min

gy

uan Z

h

an

g

Cre

d

it Ris

k

Scorecar

d

s: Deve

l

opin

g

an

d

Imp

l

ementin

g

Inte

ll

i

g

ent Cre

d

it

Scoring b

y

Naeem Siddi

q

i

The Data Asset: How Smart Companies Govern Their Data for Business

Success by Tony Fisher

Delivering Business Analytics: Practical Guidelines for Best Practice by

Evan Stubbs

Demand‐Driven Forecasting: A Structured Approach to Forecasting,

S

ec-

ond Edition by Charles Chase

Demand‐Driven Inventory Optimization and Replenishment: Creating a

M

ore E

f

cient Supp

l

y C

h

ain

b

y Ro

b

ert A. Davis

T

h

e Executive’s Gui

d

e to Enterprise Socia

l

Me

d

ia Strategy: How Socia

l

Net-

works Are Radically Transformin

g

Your Busines

s

b

y

David Thomas and

Mike Barlo

w

Economic and Business Forecastin

g

: Analyzin

g

and Interpretin

g

Econo-

metric Results b

y

John Silvia, Azhar I

q

bal, Ka

y

l

y

n Swankoski, Sarah

Watt

,

and Sam Bullard

Executive’s Guide to Solvency II

by David Buckham, Jason Wahl, and

I

St

uar

t

Rose

Fair Lendin

g

Compliance: Intelli

g

ence and Implications for Credit Risk

Management

by Clark R. Abrahams and Mingyuan Zhang

t

Forei

g

n Currency Financial Reportin

g

from Euros to Yen to Yuan: A Guide

to Fundamental Conce

p

ts and Practical A

pp

lications b

y

Robert Rowan

Health Analytics: Gainin

g

the Insi

g

hts to Transform Health Car

e

by Jason

Burke

Heuristics in Analytics: A Practical Perspective of What In uences Ou

r

Analytical World

by Carlos Andre Reis Pinheiro and Fiona McNeill

d

Human Capital Analytics: How to Harness the Potential of Your Or

g

aniza

-

t

i

on’s

G

reatest Asse

t

by Gene Pease, Boyce Byerly, and Jac Fitz‐enz

t

Imp

l

ement, Improve an

d

Expan

d

Your Statewi

d

e Longitu

d

ina

l

Data Sys-

tem: Creating a Cu

l

ture o

f

Data in E

d

ucation

b

y Jamie McQuiggan an

d

Armistea

d

Sa

pp

In

f

ormation Revo

l

ution: Using t

h

e In

f

ormation Evo

l

ution Mo

d

e

l

to Grow

Your Bus

in

es

s

by

Jim Davis, G

l

oria J. Mi

ll

er, an

d

A

ll

an Russe

ll

Killer Analytics: Top 20 Metrics Missing from Your Balance Sheet

b

y

Mark

t

B

ro

w

n

M

anufacturin

g

Best Practices: Optimizin

g

Productivity and Product Qual-

it

y

by Bobby Hull

M

arketing Automation: Practical Steps to More Effective Direct Marketing

b

y Jeff LeSueur

M

astering Organizational Knowledge Flow: How to Make Knowledge

Sharing Work

by Frank Leistner

k

The New Know: Innovation Powered by Analytics by Thornton May

Per

f

ormance Management: Integrating Strategy Execution, Met

h

o

d

o

l

ogies,

Ris

k

, an

d

Ana

l

ytics

b

y Gary Co

k

ins

Predictive Business Analytics: Forward‐Lookin

g

Capabilities to Improve

Business Per

f

ormance b

y

Lawrence Maisel and Gar

y

Cokins

Retail Analytics: The Secret Weapon by Emmett Cox

Social Network Anal

y

sis in Telecommunications b

y

Carlos Andre Reis

Pinh

e

ir

o

Statistical Thinkin

g

: Improvin

g

Business Performance

,

second edition by

Ro

g

er W. Hoerl and Ronald D. Snee

Tamin

g

the Bi

g

Data Tidal Wave: Findin

g

Opportunities in Hu

g

e Data

Streams with Advanced Analytics by Bill Franks

Too Bi

g

to I

g

nore: The Business Case for Bi

g

Dat

a

b

y

Phil Simon

The Value of Business Analytics: Identifyin

g

the Path to Pro tabilit

y

b

y

Evan Stubbs

Visual Six Si

g

ma: Makin

g

Data Analysis Lea

n

b

y

Ian Cox, Marie A.

Gaudard, Philip J. Ramsey, Mia L. Stephens, and Leo Wright

Win with Advanced Business Analytics: Creatin

g

Business Value from

Your

Data

b

y

Jean Paul Isson and Jesse Harriott

For more in

f

ormation on an

y

o

f

t

h

e a

b

ove tit

l

es,

pl

ease visit ww

w

.wi

l

e

y

.com .

Analytics in a Big

Data World

The Essential

G

uide to Data

S

cience

and Its Application

s

B

ar

t

Baesen

s

Cover ima

g

e: ©iStoc

kph

oto/v

l

astos

Cover desi

g

n: Wile

y

Co

py

ri

gh

t © 2014

by

Bart Baesens. A

ll

ri

gh

ts reserve

d

.

Pu

bl

is

h

e

d

by

Jo

h

n Wi

l

e

y

& Sons, Inc., Ho

b

o

k

en, New Jerse

y

.

Published simultaneousl

y

in Canada.

No part o

f

t

h

is pu

bl

ication may

b

e repro

d

uce

d

, store

d

in a retrieva

l

system,

or transmitte

d

in any

f

orm or

b

y any means, e

l

ectronic, mec

h

anica

l

,

photocopying, recording, scanning, or otherwise, except as permitted under

Section 107 or 108 of the 1976 United States Copyright Act, without either the

prior written permission of the Publisher, or authorization through payment

of the appropriate per-copy fee to the Copyright Clearance Center, Inc., 222

Rosewood Drive, Danvers, MA 01923, (978) 750-8400, fax (978) 646-8600, or

on the Web at www.copyright.com. Requests to the Publisher for permission

should be addressed to the Permissions Department, John Wiley & Sons, Inc.,

111 River Street, Hoboken, NJ 07030,

(

201

)

748-6011, fax

(

201

)

748-6008, or

online at http://www.wiley.com/go/permissions.

Limit of Liability/Disclaimer of Warranty: While the publisher and author have

used their best efforts in preparing this book, they make no representations

or warranties with respect to the accuracy or completeness of the contents of

this book and s

p

eci call

y

disclaim an

y

im

p

lied warranties of merchantabilit

y

or tness for a

p

articular

p

ur

p

ose. No warrant

y

ma

y

be created or extended

by

sales re

p

resentatives or written sales materials. The advice and strate

g

ies

contained herein ma

y

not be suitable for

y

our situation. You should consult

with a

p

rofessional where a

pp

ro

p

riate. Neither the

p

ublisher nor author shall

b

e liable for an

y

loss of

p

ro t or an

y

other commercial dama

g

es, includin

g

but

not limited to s

p

ecial, incidental, conse

q

uential, or other dama

g

es.

For

g

eneral information on our other

p

roducts and services or for technical

su

pp

ort,

p

lease contact our Customer Care De

p

artment within the United

States at

(

800

)

762-2974, outside the United States at

(

317

)

572-3993 or

fax (317) 572-4002.

Wile

y

p

ublishes in a variet

y

of

p

rint and electronic formats and b

y

p

rint-on

-

demand. Some material included with standard

p

rint versions of this book

ma

y

not be included in e-books or in

p

rint-on-demand. If this book refers to

media such as a CD or DVD that is not included in the version

y

ou

p

urchased,

y

ou ma

y

download this material at htt

p

://booksu

pp

ort.wile

y

.com. For more

information about Wile

y

p

roducts, visit www.wile

y

.com.

Library of Congress Cataloging-in-Publication Data:

Baesens

,

Bart.

Anal

y

tics in a bi

g

data world : the essential

g

uide to data science and its

applications / Bart Baesens.

1 online resource. — (Wile

y

& SAS business series

)

Descri

p

tion based on

p

rint version record and CIP data

p

rovided b

y

p

ublisher;

resource not viewe

d

.

ISBN 978-1-118-89271-8

(

ebk

)

; ISBN 978-1-118-89274-9

(

ebk

)

;

ISBN 978-1-118-89270-1 (c

l

ot

h

) 1. Big

d

ata. 2. Management—Statistica

l

met

h

o

d

s. 3. Mana

g

ement—Data

p

rocessin

g

. 4. Decision ma

k

in

g

—Data

processing. I. Tit

l

e.

HD

30.215

658.4’038

d

c23

2014004

7

28

Printe

d

in t

h

e Unite

d

States o

f

America

1

0

9

8

7

6

5

4

3

2

1

T

o m

y

won

d

er

f

u

l

wi

f

e, Katrien, an

d

m

y

k

i

d

s,

A

nn-So

ph

ie, Victor, an

d

Hanne

l

ore.

To my parents an

d

parents-in-

l

aw

.

ix

Contents

Preface xii

i

Acknowledgments xv

C

h

apter 1 B

i

g Data an

d

Ana

l

yt

i

cs

1

E

xam

pl

e

Appli

cat

i

ons 2

Basic

No

m

e

n

cla

t

u

r

e

4

A

na

ly

t

i

cs

P

rocess

M

o

d

e

l

4

Job

P

r

o

les

I

nv

ol

v

ed

6

A

na

ly

t

i

cs

7

A

na

ly

t

i

ca

l

M

o

d

e

l

R

e

q

u

i

rements

9

No

t

es

1

0

Chapter 2 Data Collection, Sampling,

an

d

Preprocess

i

ng 13

Typ

es of Data

S

ources 13

S

ampling 1

5

T

ypes o

f

D

ata

El

ements 17

Vi

sua

l

D

ata

E

x

pl

orat

i

on an

d

E

x

pl

orator

y

S

tatistical Anal

y

sis 1

7

Mi

ss

i

ng

V

a

l

ues 1

9

Ou

tli

e

r D

e

t

ec

ti

o

n

a

n

d

Tr

ea

tm

e

nt 2

0

S

tandardizin

g

Data 2

4

C

ate

g

orization 2

4

Wei

g

hts of Evidence

C

odin

g

28

V

ariable

S

election 2

9

x

▸

CO

NTENT

S

S

egmentation 3

2

N

otes 3

3

Chapter 3 Predictive Analytics 35

T

arget De nition 35

Linear Regression 3

8

Logistic Regression 3

9

D

ec

i

s

i

o

n Tr

ees

4

2

N

eu

r

a

l N

e

tw

o

rk

s

4

8

S

u

pp

ort Vector Machines 5

8

En

se

m

b

l

e

M

e

th

ods

6

4

Multiclass Classi cation Techni

q

ues 67

E

va

l

uat

i

ng

P

re

di

ct

i

ve

M

o

d

e

l

s 7

1

No

t

es

8

4

Chapter 4 Descriptive Analytics 87

Associa

t

io

n

Rules

87

S

e

q

uence Rules 9

4

S

egmentation 9

5

No

t

es

1

0

4

Chapter 5 Survival Analysis 10

5

S

urvival Anal

y

sis Measurements 106

K

a

pl

an

M

e

i

er

A

na

ly

s

i

s 109

Parametric Survival Anal

y

sis 111

P

roport

i

ona

l

H

azar

d

s

R

egress

i

on 114

Extensions of

S

urvival Anal

y

sis Models 116

Evaluating Survival Analysis Models 11

7

No

t

es

11

7

Chapter 6 Social Network Analytics 11

9

Soc

i

a

l N

e

tw

o

rk D

e

niti

o

n

s

11

9

Soc

i

a

l N

e

tw

o

rk M

e

tri

cs

121

S

ocial Network Learnin

g

12

3

Relational Nei

g

hbor

C

lassi er 124

C

ONTENTS ◂x

i

Probabilistic Relational Nei

g

hbor

C

lassi er 12

5

R

e

l

at

i

ona

l

L

og

i

st

i

c

R

egress

i

on 126

Collective Inferencing 12

8

E

gonets 12

9

Bigraphs 130

N

o

t

es

1

32

Chapter 7 Anal

y

tics: Puttin

g

It All to Work 13

3

Backtesting Analytical Models 134

Benchmarking 146

Data

Q

ualit

y

14

9

So

ftw

a

r

e

1

53

P

r

i

vac

y

15

5

M

o

d

e

l

D

es

i

gn an

d

D

ocumentat

i

on 15

8

Cor

p

orate Governance 159

No

t

es

1

59

Cha

p

ter 8 Exam

p

le A

pp

lications 161

Credit Risk Modeling 16

1

F

r

aud

De

t

ec

t

io

n 1

65

N

et

Lif

t

R

esponse

M

o

d

e

li

ng 16

8

C

h

u

rn Pr

ed

i

c

ti

o

n 17

2

Recommender

Sy

stems 176

W

e

b

A

na

ly

t

i

cs 18

5

S

ocial Media Anal

y

tics 195

B

us

i

ness

P

rocess

A

na

ly

t

i

cs 204

No

t

es

22

0

About the Author 223

In

de

x 22

5

x

iii

Preface

C om

p

anies are bein

g

ooded with tsunamis of data collected in a

multichannel business environment, leavin

g

an unta

pp

ed

p

oten

-

tia

l

f

or ana

ly

tics to

b

etter un

d

erstan

d

, mana

g

e, an

d

strate

g

ica

lly

ex

pl

oit t

h

e com

pl

ex

dy

namics o

f

customer

b

e

h

avior. In t

h

is

b

oo

k

, we

wi

ll

d

iscuss

h

ow ana

ly

tics can

b

e use

d

to create strate

g

ic

l

evera

g

e an

d

identif

y

new business o

pp

ortunities.

The focus of this book is not on the mathematics or theor

y

, but on

the practical application. Formulas and equations will only be included

when absolutel

y

needed from a

p

ractitioner’s

p

ers

p

ective. It is also not

our aim to

p

rovide exhaustive covera

g

e of all anal

y

tical techni

q

ues

previously developed, but rather to cover the ones that really provide

added value in a business settin

g

.

The book is written in a condensed, focused wa

y

because it is tar

-

geted at the business professional. A reader’s prerequisite knowledge

should consist of some basic ex

p

osure to descri

p

tive statistics (e.

g

.,

mean, standard deviation, correlation, con dence intervals, hypothesis

testing), data handling (using, for example, Microsoft Excel, SQL, etc.),

and data visualization (e.

g

., bar

p

lots,

p

ie charts, histo

g

rams, scatter

plots). Throughout the book, many examples of real‐life case studies

will be included in areas such as risk mana

g

ement, fraud detection,

customer relationshi

p

mana

g

ement, web anal

y

tics, and so forth. The

author will also integrate both his research and consulting experience

throu

g

hout the various cha

p

ters. The book is aimed at senior data ana

-

l

ysts, consu

l

tants, ana

l

ytics practitioners, an

d

P

h

D researc

h

ers starting

to ex

pl

ore t

h

e

e

ld

.

C

h

a

p

ter 1

d

iscusses

b

i

g

d

ata an

d

ana

ly

tics. It starts wit

h

some

examp

l

e app

l

ication areas,

f

o

ll

owe

d

b

y an overview o

f

t

h

e ana

l

ytics

p

rocess mo

d

e

l

an

d

j

o

b

p

ro

l

es invo

l

ve

d

, an

d

conc

l

u

d

es

by

d

iscussin

g

k

e

y

ana

ly

tic mo

d

e

l

re

q

uirements. C

h

a

p

ter 2

p

rovi

d

es an overview o

f

x

iv

▸

P

REFA

C

E

data collection, sam

p

lin

g

, and

p

re

p

rocessin

g

. Data is the ke

y

in

g

redi-

ent to an

y

anal

y

tical exercise, hence the im

p

ortance of this cha

p

ter.

It discusses sampling, types of data elements, visual data exploration

and exploratory statistical analysis, missing values, outlier detection

and treatment, standardizing data, categorization, weights of evidence

coding, variable selection, and segmentation. Chapter 3 discusses pre

-

dictive analytics. It starts with an overview of the target de nition

and then continues to discuss various analytics techniques such as

linear regression, logistic regression, decision trees, neural networks,

su

pp

ort vector machines, and ensemble methods (ba

gg

in

g

, boost

-

ing, ran

d

om

f

orests). In a

dd

ition, mu

l

tic

l

ass c

l

assi

cation tec

h

niques

are covere

d

, suc

h

as mu

l

tic

l

ass

l

ogistic regression, mu

l

tic

l

ass

d

eci

-

sion trees, mu

l

tic

l

ass neura

l

networ

k

s, an

d

mu

l

tic

l

ass support vector

machines. The chapter concludes by discussing the evaluation of pre

-

dictive models. Cha

p

ter 4 covers descri

p

tive anal

y

tics. First, association

rules are discussed that aim at discoverin

g

intratransaction

p

atterns.

This is followed by a section on sequence rules that aim at discovering

intertransaction

p

atterns. Se

g

mentation techni

q

ues are also covered.

Cha

p

ter 5 introduces survival anal

y

sis. The cha

p

ter starts b

y

introduc

-

ing some key survival analysis measurements. This is followed by a

discussion of Ka

p

lan Meier anal

y

sis,

p

arametric survival anal

y

sis, and

p

ro

p

ortional hazards re

g

ression. The cha

p

ter concludes b

y

discussin

g

various extensions and evaluation of survival analysis models. Chap

-

ter 6 covers social network anal

y

tics. The cha

p

ter starts b

y

discussin

g

exam

p

le social network a

pp

lications. Next, social network de nitions

and metrics are given. This is followed by a discussion on social network

learnin

g

. The relational nei

g

hbor classi er and its

p

robabilistic variant

together with relational logistic regression are covered next. The chap-

ter ends by discussing egonets and bigraphs. Chapter 7 provides an

overview of ke

y

activities to be considered when

p

uttin

g

anal

y

tics to

wor

k

. It starts wit

h

a reca

p

itu

l

ation o

f

t

h

e ana

ly

tic mo

d

e

l

re

q

uirements

an

d

t

h

en continues wit

h

a

d

iscussion o

f

b

ac

k

testin

g

,

b

enc

h

mar

k

in

g

,

d

ata qua

l

ity, so

f

tware, privacy, mo

d

e

l

d

esign an

d

d

ocumentation, an

d

cor

p

orate

g

overnance. C

h

a

p

ter 8 conc

l

u

d

es t

h

e

b

oo

k

by

d

iscussin

g

var

-

ious exam

pl

e a

ppl

ications suc

h

as cre

d

it ris

k

mo

d

e

l

in

g

,

f

rau

d

d

etection,

net

l

i

f

t response mo

d

e

l

ing, c

h

urn pre

d

iction, recommen

d

er systems,

we

b

ana

ly

tics, socia

l

me

d

ia ana

ly

tics, an

d

b

usiness

p

rocess ana

ly

tics.

xv

Acknowledgments

I would like to acknowled

g

e all m

y

collea

g

ues who contributed to

this text: Se

pp

e vanden Broucke, Alex Seret, Thomas Verbraken,

Aimée Backiel, Véroni

q

ue Van Vlasselaer, Helen Mo

g

es, and Barbara

D

er

g

ent.

Analytics in a Big

Data World

1

C

HAPTER

1

Big Data and

Analytics

D ata are ever

y

w

h

ere. IBM

p

ro

j

ects t

h

at ever

y

d

a

y

we

g

enerate 2.5

quinti

ll

ion

b

ytes o

f

d

ata.

1

In re

l

ative terms, t

h

is means 90 percent

o

f

t

h

e

d

ata in t

h

e wor

ld

h

as

b

een create

d

in t

h

e

l

ast two

y

ears.

Gartner

p

ro

j

ects t

h

at

by

2015, 85

p

ercent o

f

Fortune 500 or

g

anizations

wi

ll

b

e una

bl

e to exp

l

oit

b

ig

d

ata

f

or competitive a

d

vantage an

d

a

b

out

4.4 mi

ll

ion

j

o

b

s wi

ll

b

e create

d

aroun

d

b

i

g

d

ata.

2

A

l

t

h

ou

gh

t

h

ese esti

-

mates s

h

ou

ld

not

b

e inter

p

rete

d

in an a

b

so

l

ute sense, t

h

e

y

are a stron

g

in

d

ication o

f

t

h

e u

b

iquity o

f

b

ig

d

ata an

d

t

h

e strong nee

d

f

or ana

l

ytica

l

s

k

i

ll

s an

d

resources

b

ecause, as t

h

e

d

ata

p

i

l

es u

p

, mana

g

in

g

an

d

ana

ly

z-

in

g

t

h

ese

d

ata resources in t

h

e most o

p

tima

l

wa

y

b

ecome critica

l

suc

-

cess

f

actors in creating competitive a

d

vantage an

d

strategic

l

everage.

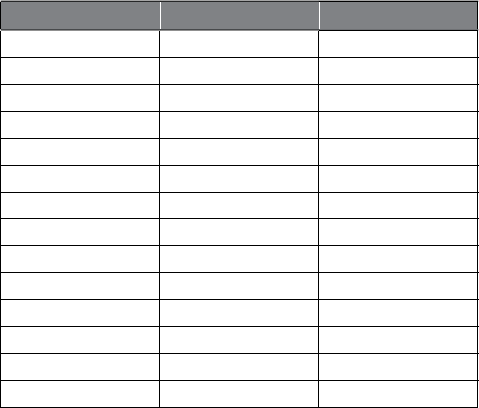

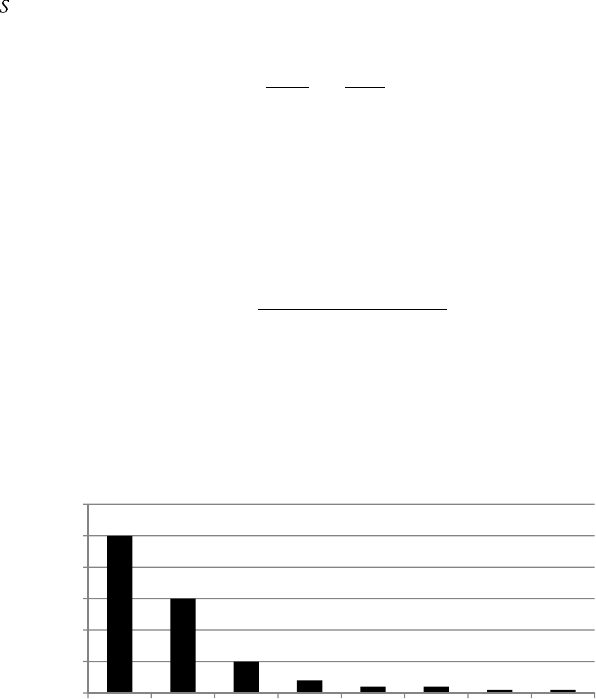

Fi

g

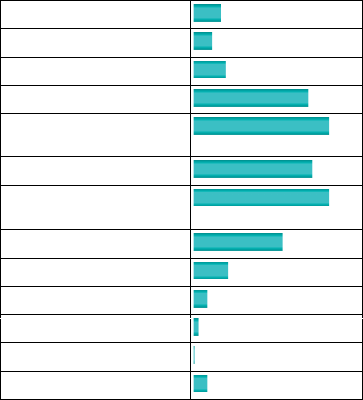

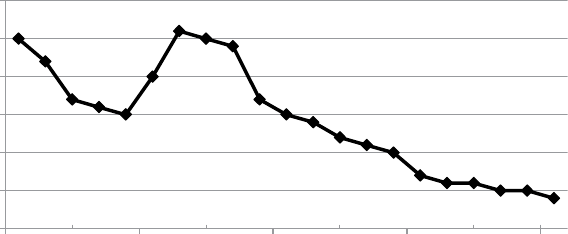

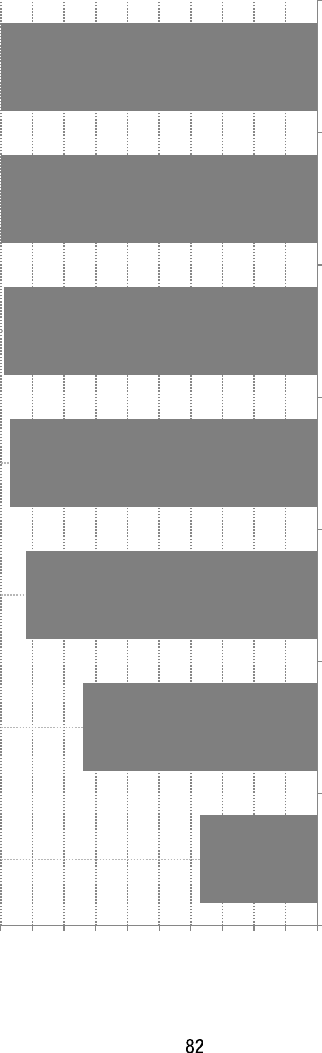

ure 1.1 s

h

ows t

h

e resu

l

ts o

f

a KDnu

gg

ets

3

p

o

ll

con

d

ucte

d

d

ur

-

in

g

A

p

ri

l

2013 a

b

out t

h

e

l

ar

g

est

d

ata sets ana

ly

ze

d

. T

h

e tota

l

num

b

er

o

f

respon

d

ents was 322 an

d

t

h

e num

b

ers per category are in

d

icate

d

b

etween

b

rac

k

ets. T

h

e me

d

ian was estimate

d

to

b

e in t

h

e 40 to 50

g

i

g

a

-

by

te (GB) ran

g

e, w

h

ic

h

was a

b

out

d

ou

bl

e t

h

e me

d

ian answer

f

or a simi

-

l

ar

p

o

ll

run in 2012 (20 to 40 GB). T

h

is c

l

ear

ly

s

h

ows t

h

e

q

uic

k

increase

in size of data that analysts are working on. A further regional break-

down of the

p

oll showed that U.S. data miners lead other re

g

ions in bi

g

data, with about 28% of them workin

g

with terab

y

te (TB) size databases.

A main obstacle to fully harnessing the power of big data using ana-

l

y

tics is the lack of skilled resources and “data scientist” talent re

q

uired to

2

▸ANALYTI

CS

IN A BI

G

DATA W

O

RL

D

ex

pl

oit

b

i

g

d

ata. In anot

h

er

p

o

ll

ran

by

KDnu

gg

ets in Ju

ly

2013, a stron

g

nee

d

emerge

d

f

or ana

l

ytics/

b

ig

d

ata/

d

ata mining/

d

ata science e

d

uca

-

tion.

4

It is t

h

e

p

ur

p

ose o

f

t

h

is

b

oo

k

to tr

y

an

d

ll

t

h

is

g

a

p

by

p

rovi

d

in

g

a

concise an

d

f

ocuse

d

overview o

f

ana

ly

tics

f

or t

h

e

b

usiness

p

ractitioner.

EXAMPLE APPLICATIONS

Ana

l

ytics is everyw

h

ere an

d

strong

l

y em

b

e

dd

e

d

into our

d

ai

l

y

l

ives. As I

am writin

g

t

h

is

p

art, I was t

h

e su

bj

ect o

f

various ana

ly

tica

l

mo

d

e

l

s to

d

a

y

.

W

h

en I c

h

ec

k

e

d

my p

h

ysica

l

mai

lb

ox t

h

is morning, I

f

oun

d

a cata

l

ogue

sent to me most

p

ro

b

a

bly

as a resu

l

t o

f

a res

p

onse mo

d

e

l

in

g

ana

ly

tica

l

exercise t

h

at in

d

icate

d

t

h

at,

g

iven m

y

c

h

aracteristics an

d

p

revious

p

ur

-

c

h

ase

b

e

h

avior, I am

l

i

k

e

l

y to

b

uy one or more pro

d

ucts

f

rom it. To

d

ay,

I was t

h

e su

bj

ect o

f

a

b

e

h

aviora

l

scorin

g

mo

d

e

l

o

f

m

y

nancia

l

institu

-

tion. T

h

is is a mo

d

e

l

t

h

at wi

ll

l

oo

k

at, among ot

h

er t

h

ings, my c

h

ec

k-

in

g

account

b

a

l

ance

f

rom t

h

e

p

ast 12 mont

h

s an

d

m

y

cre

d

it

p

a

y

ments

d

urin

g

t

h

at

p

erio

d

, to

g

et

h

er wit

h

ot

h

er

k

in

d

s o

f

in

f

ormation avai

l

a

bl

e

to my

b

an

k

, to pre

d

ict w

h

et

h

er I wi

ll

d

e

f

au

l

t on my

l

oan

d

uring t

h

e

next

y

ear. M

y

b

an

k

nee

d

s to

k

now t

h

is

f

or

p

rovisionin

g

p

ur

p

oses. A

l

so

to

d

a

y

, m

y

te

l

e

ph

one services

p

rovi

d

er ana

ly

ze

d

m

y

ca

ll

in

g

b

e

h

avior

Fi

g

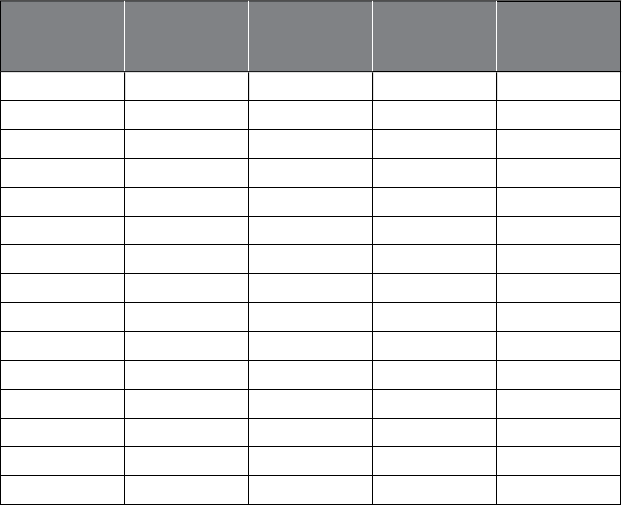

ure 1.1 Results

f

rom a KDnu

gg

ets Poll about Lar

g

est Data Sets Anal

y

ze

d

S

ource: www.

kd

nuggets.com/po

ll

s/2013/

l

argest‐

d

ataset‐ana

l

yze

d

‐

d

ata‐m

i

ne

d

‐2013.

h

tm

l

.

Less than 1 MB (12) 3.7%

1.1 to 10 MB (8) 2.5%

11 to 100 MB (14) 4.3%

101 MB to 1 GB (50) 15.5%

1.1 to 10 GB (59)

18%

11 to 100 GB (52) 16%

101 GB to 1 TB

(59) 18%

1.1 to 10 TB (39) 12%

11 to 100 TB (15) 4.7%

101 TB to 1 PB (6) 1.9%

1.1 to 10 PB (2) 0.6%

11 to 100 PB (0) 0%

Over 100 PB (6) 1.9%

B

I

G

DATA AND ANALYTI

CS

◂

3

an

d

m

y

account in

f

ormation to

p

re

d

ict w

h

et

h

er I wi

ll

c

h

urn

d

urin

g

t

h

e

next three months. As I lo

gg

ed on to m

y

Facebook

p

a

g

e, the social ads

appearing there were based on analyzing all information (posts, pictures,

my friends and their behavior, etc.) available to Facebook. My Twitter

posts will be analyzed (possibly in real time) by social media analytics to

understand both the subject of my tweets and the sentiment of them.

As I checked out in the supermarket, my loyalty card was scanned rst,

followed by all my purchases. This will be used by my supermarket to

analyze my market basket, which will help it decide on product bun

-

dlin

g

, next best offer, im

p

rovin

g

shelf or

g

anization, and so forth. As I

ma

d

e t

h

e payment wit

h

my cre

d

it car

d

, my cre

d

it car

d

provi

d

er use

d

a

f

rau

d

d

etection mo

d

e

l

to see w

h

et

h

er it was a

l

egitimate transaction.

W

h

en I receive my cre

d

it car

d

statement

l

ater, it wi

ll

b

e accompanie

d

b

y

various vouchers that are the result of an analytical customer segmenta

-

tion exercise to better understand m

y

ex

p

ense behavior.

To summarize, the relevance, im

p

ortance, and im

p

act of anal

y

tics

are now bigger than ever before and, given that more and more data

are bein

g

collected and that there is strate

g

ic value in knowin

g

what

is hidden in data, anal

y

tics will continue to

g

row. Without claimin

g

to

b

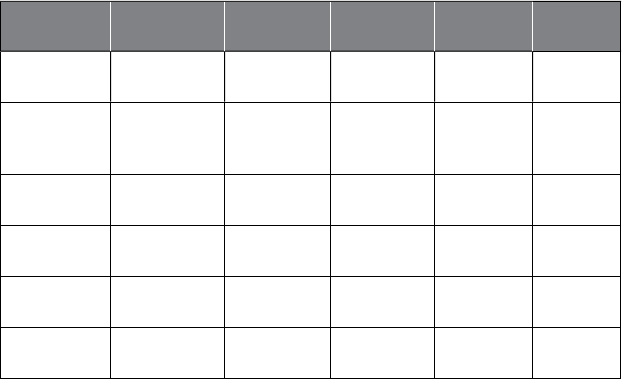

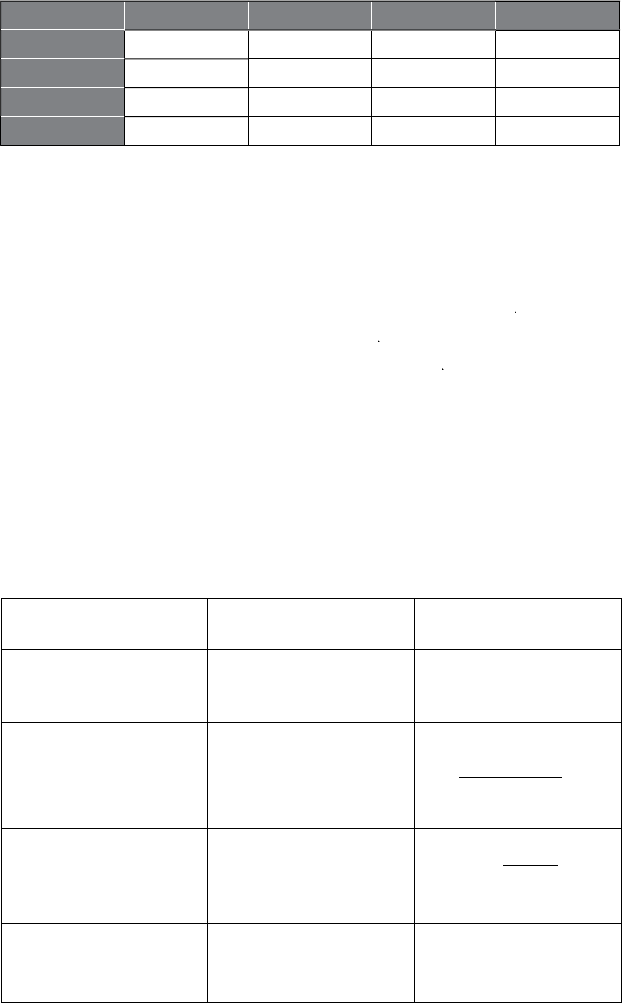

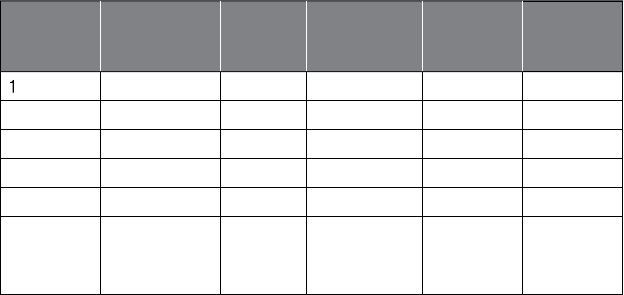

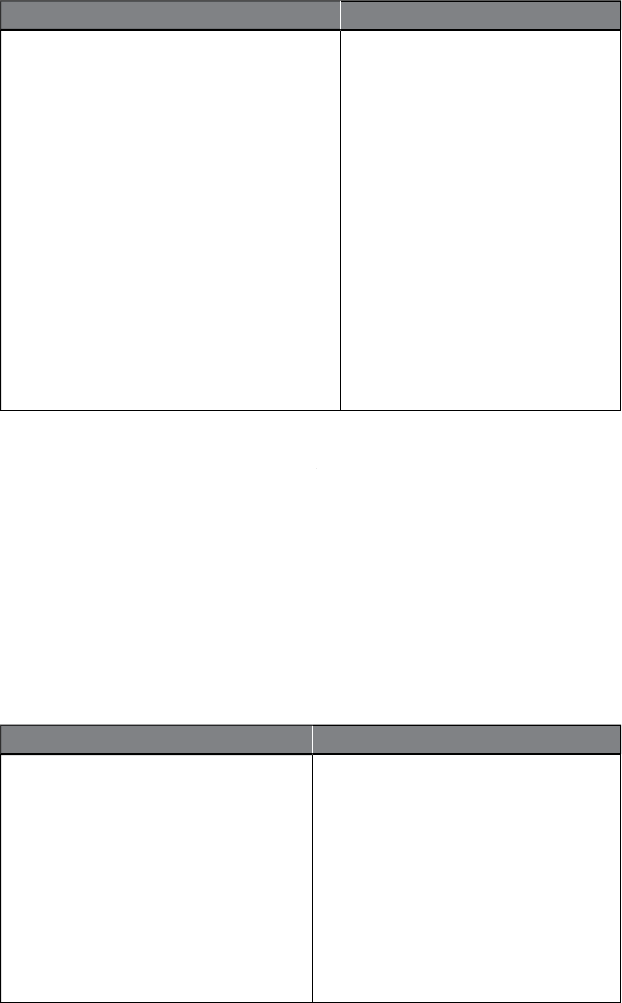

e exhaustive, Table 1.1 presents some examples of how analytics is

a

pp

lied in various settin

g

s.

Ta

bl

e 1.1 Examp

l

e Ana

l

yt

i

cs App

li

cat

i

ons

Marketing Risk

Management Government Web Logistics Other

R

es

p

onse

m

odelin

g

C

redit ris

k

modelin

g

T

ax avo

id

anc

e

W

e

b

ana

ly

t

i

c

s

D

eman

d

forecastin

g

T

ext

anal

y

tic

s

Net li

f

t

m

odelin

g

M

ar

k

et r

i

s

k

modelin

g

Social

s

ecurity

f

rau

d

Social media

analytic

s

Supply chain

analytic

s

B

us

i

ness

process

analytic

s

R

e

t

e

nti

o

n

m

o

d

e

li

n

g

O

p

erational

r

i

s

k

mo

d

e

li

n

g

M

one

y

l

aun

d

er

i

n

g

Mu

ltiv

a

ri

a

t

e

t

est

i

n

g

Ma

r

ke

t

baske

t

a

na

l

ys

is

F

r

aud

d

etect

i

o

n

Te

rr

o

r

is

m

d

etect

i

o

n

R

eco

mm

e

n

de

r

s

y

stem

s

Cus

t

o

m

e

r

se

g

mentat

i

o

n

4

▸ANALYTI

CS

IN A BI

G

DATA W

O

RL

D

It is the

p

ur

p

ose of this book to discuss the underl

y

in

g

techni

q

ues

and ke

y

challen

g

es to work out the a

pp

lications shown in Table 1.1

using analytics. Some of these applications will be discussed in further

detail in Chapter 8 .

BASIC NOMENCLATURE

In order to start doing analytics, some basic vocabulary needs to be

de ned. A rst important concept here concerns the basic unit of anal

-

y

sis. Customers can be considered from various

p

ers

p

ectives. Customer

l

i

f

etime va

l

ue (CLV) can

b

e measure

d

f

or eit

h

er in

d

ivi

d

ua

l

customers

or at t

h

e

h

ouse

h

o

ld

l

eve

l

. Anot

h

er a

l

ternative is to

l

oo

k

at account

b

e

h

avior. For examp

l

e, consi

d

er a cre

d

it scoring exercise

f

or w

h

ic

h

the aim is to predict whether the applicant will default on a particular

mort

g

a

g

e loan account. The anal

y

sis can also be done at the transac

-

tion level. For exam

p

le, in insurance fraud detection, one usuall

y

p

er-

forms the analysis at insurance claim level. Also, in web analytics, the

b

asic unit of anal

y

sis is usuall

y

a web visit or session.

It is also im

p

ortant to note that customers can

p

la

y

different roles.

For example, parents can buy goods for their kids, such that there is

a clear distinction between the

p

a

y

er and the end user. In a bankin

g

settin

g

, a customer can be

p

rimar

y

account owner, secondar

y

account

owner, main debtor of the credit, codebtor, guarantor, and so on. It

is ver

y

im

p

ortant to clearl

y

distin

g

uish between those different roles

when de nin

g

and/or a

gg

re

g

atin

g

data for the anal

y

tics exercise.

Finally, in case of predictive analytics, the target variable needs to

b

e a

pp

ro

p

riatel

y

de ned. For exam

p

le, when is a customer considered

to be a churner or not, a fraudster or not, a responder or not, or how

should the CLV be appropriately de ned?

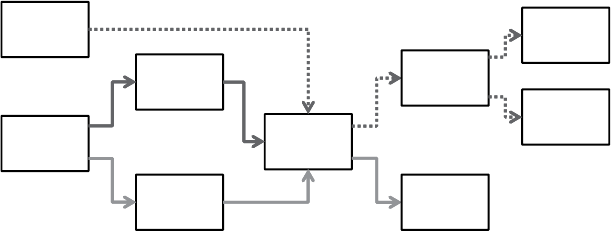

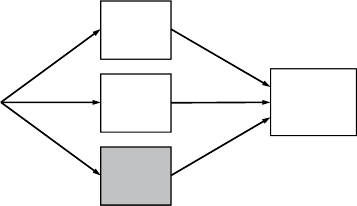

ANALYTICS PROCESS MODEL

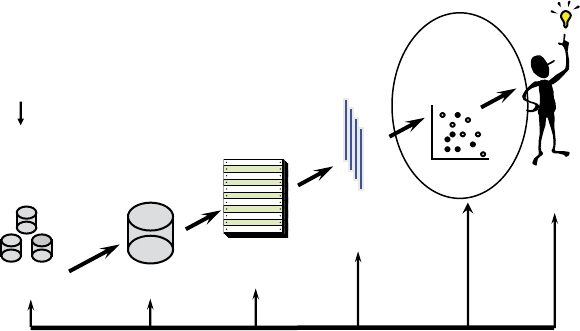

Figure 1.2 gives a

h

ig

h

‐

l

eve

l

overview o

f

t

h

e ana

l

ytics process mo

d

e

l

.

5

As a

rst ste

p

, a t

h

orou

gh

d

e

nition o

f

t

h

e

b

usiness

p

ro

bl

em to

b

e

so

l

ve

d

wit

h

ana

ly

tics is nee

d

e

d

. Next, a

ll

source

d

ata nee

d

to

b

e i

d

enti-

e

d

t

h

at cou

ld

b

e o

f

potentia

l

interest. T

h

is is a very important step, as

d

ata is t

h

e

k

e

y

in

g

re

d

ient to an

y

ana

ly

tica

l

exercise an

d

t

h

e se

l

ection o

f

B

I

G

DATA AND ANALYTI

CS

◂

5

data will have a deterministic im

p

act on the anal

y

tical models that will

b

e built in a subse

q

uent ste

p

. All data will then be

g

athered in a sta

g-

ing area, which could be, for example, a data mart or data warehouse.

Some basic exploratory analysis can be considered here using, for

example, online analytical processing (OLAP) facilities for multidimen

-

sional data analysis (e.g., roll‐up, drill down, slicing and dicing). This

will be followed by a data cleaning step to get rid of all inconsistencies,

such as missing values, outliers, and duplicate data. Additional trans-

formations may also be considered, such as binning, alphanumeric to

numeric codin

g

,

g

eo

g

ra

p

hical a

gg

re

g

ation, and so forth. In the anal

y

t-

ics step, an ana

l

ytica

l

mo

d

e

l

wi

ll

b

e estimate

d

on t

h

e preprocesse

d

an

d

trans

f

orme

d

d

ata. Di

ff

erent types o

f

ana

l

ytics can

b

e consi

d

ere

d

h

ere

(e.g., to

d

o c

h

urn pre

d

iction,

f

rau

d

d

etection, customer segmentation,

market basket analysis). Finally, once the model has been built, it will

b

e inter

p

reted and evaluated b

y

the business ex

p

erts. Usuall

y

, man

y

trivial

p

atterns will be detected b

y

the model. For exam

p

le, in a market

b

asket analysis setting, one may nd that spaghetti and spaghetti sauce

are often

p

urchased to

g

ether. These

p

atterns are interestin

g

because

the

y

p

rovide some validation of the model. But of course, the ke

y

issue

here is to nd the unexpected yet interesting and actionable patterns

(sometimes also referred to as knowled

g

e diamond

s

) that can

p

rovide

added value in the business settin

g

. Once the anal

y

tical model has

b

een appropriately validated and approved, it can be put into produc-

tion as an anal

y

tics a

pp

lication (e.

g

., decision su

pp

ort s

y

stem, scorin

g

en

g

ine). It is im

p

ortant to consider here how to re

p

resent the model

output in a user‐friendly way, how to integrate it with other applica-

tions (e.

g

., cam

p

ai

g

n mana

g

ement tools, risk en

g

ines), and how to

make sure the analytical model can be appropriately monitored and

b

acktested on an ongoing basis.

It is im

p

ortant to note that the

p

rocess model outlined in Fi

g

-

ure 1.2 is iterative in nature, in t

h

e sense t

h

at one ma

y

h

ave to

g

o

b

ac

k

to

p

revious ste

p

s

d

urin

g

t

h

e exercise. For exam

pl

e,

d

urin

g

t

h

e ana

ly

t-

ics step, t

h

e nee

d

f

or a

dd

itiona

l

d

ata may

b

e i

d

enti

e

d

, w

h

ic

h

may

necessitate a

dd

itiona

l

c

l

eanin

g

, trans

f

ormation, an

d

so

f

ort

h

. A

l

so, t

h

e

most time consumin

g

ste

p

is t

h

e

d

ata se

l

ection an

d

p

re

p

rocessin

g

ste

p

;

t

h

is usua

ll

y ta

k

es aroun

d

80% o

f

t

h

e tota

l

e

ff

orts nee

d

e

d

to

b

ui

ld

an

ana

ly

tica

l

mo

d

e

l

.

6

▸ANALYTI

CS

IN A BI

G

DATA W

O

RL

D

JOB PROFILES INVOLVED

Anal

y

tics is essentiall

y

a multidisci

p

linar

y

exercise in which man

y

different

j

ob

p

ro les need to collaborate to

g

ether. In what follows, we

will discuss the most important job pro les.

The database or data warehouse administrator (DBA) is aware of

all the data available within the rm, the stora

g

e details, and the data

de nitions. Hence, the DBA plays a crucial role in feeding the analyti

-

cal modelin

g

exercise with its ke

y

in

g

redient, which is data. Because

anal

y

tics is an iterative exercise, the DBA ma

y

continue to

p

la

y

an

important role as the modeling exercise proceeds.

Another ver

y

im

p

ortant

p

ro le is the business ex

p

ert. This could,

for exam

p

le, be a credit

p

ortfolio mana

g

er, fraud detection ex

p

ert,

b

rand manager, or e‐commerce manager. This person has extensive

b

usiness experience an

d

b

usiness common sense, w

h

ic

h

is very va

l

u-

able. It is

p

recisel

y

this knowled

g

e that will hel

p

to steer the anal

y

tical

mo

d

e

l

in

g

exercise an

d

inter

p

ret its

k

e

y

n

d

in

g

s. A

k

e

y

c

h

a

ll

en

g

e

h

ere

is t

h

at muc

h

o

f

t

h

e expert

k

now

l

e

d

ge is tacit an

d

may

b

e

h

ar

d

to e

l

icit

at t

h

e start o

f

t

h

e mo

d

e

l

in

g

exercise.

Le

g

a

l

ex

p

erts are

b

ecomin

g

more an

d

more im

p

ortant

g

iven t

h

at

not a

ll

d

ata can

b

e use

d

in an ana

l

ytica

l

mo

d

e

l

b

ecause o

f

privacy,

Fi

g

ure 1.2 The Anal

y

tics Process Model

Understanding

what data is

needed for the

application

Data Cleaning

Interpretation

and

Evaluation

Data

Transformation

(binning, alpha to

numeric, etc.)

Analytics

Data

Selection

Source

Data

Analytics

Application

Preprocessed

Data

Transformed

Data

Patterns

Data Mining

Mart

Dumps of Operational Data

B

IG DATA AND ANALYTICS ◂

7

discrimination, and so forth. For exam

p

le, in credit risk modelin

g

, one

can t

yp

icall

y

not discriminate

g

ood and bad customers based u

p

on

gender, national origin, or religion. In web analytics, information is

typically gathered by means of cookies, which are les that are stored

on the user’s browsing computer. However, when gathering informa-

tion using cookies, users should be appropriately informed. This is sub-

j

ect to regulation at various levels (both national and, for example,

European). A key challenge here is that privacy and other regulation

highly vary depending on the geographical region. Hence, the legal

ex

p

ert should have

g

ood knowled

g

e about what data can be used

w

h

en, an

d

w

h

at regu

l

ation app

l

ies in w

h

at

l

ocation.

T

h

e

d

ata scientist,

d

ata miner, or

d

ata ana

l

yst is t

h

e person respon

-

si

bl

e

f

or

d

oing t

h

e actua

l

ana

l

ytics. T

h

is person s

h

ou

ld

possess a t

h

or

-

ough understanding of all techniques involved and know how to

im

p

lement them usin

g

the a

pp

ro

p

riate software. A

g

ood data scientist

should also have

g

ood communication and

p

resentation skills to re

p

ort

the analytical ndings back to the other parties involved.

The software tool vendors should also be mentioned as an

im

p

ortant

p

art of the anal

y

tics team. Different t

yp

es of tool vendors can

b

e distinguished here. Some vendors only provide tools to automate

s

p

eci c ste

p

s of the anal

y

tical modelin

g

p

rocess (e.

g

., data

p

re

p

rocess-

in

g

). Others sell software that covers the entire anal

y

tical modelin

g

process. Some vendors also provide analytics‐based solutions for spe-

ci c a

pp

lication areas, such as risk mana

g

ement, marketin

g

anal

y

tics

and cam

p

ai

g

n mana

g

ement, and so on.

ANALYTICS

A

nal

y

tics is a term that is often used interchan

g

eabl

y

with

d

ata science

,

data mining, knowledge discovery

,

and others. The distinction between

all those is not clear cut. All of these terms essentiall

y

refer to extract-

ing use

f

u

l

b

usiness patterns or mat

h

ematica

l

d

ecision mo

d

e

l

s

f

rom a

p

re

p

rocesse

d

d

ata set. Di

ff

erent un

d

er

ly

in

g

tec

h

ni

q

ues can

b

e use

d

f

or

t

h

is

p

ur

p

ose, stemmin

g

f

rom a variet

y

o

f

d

i

ff

erent

d

isci

pl

ines, suc

h

as:

■ Statistics (e.g.,

l

inear an

d

l

ogistic regression)

■ Mac

h

ine

l

earnin

g

(e.

g

.,

d

ecision trees)

8

▸ANALYTI

CS

IN A BI

G

DATA W

O

RL

D

■ Biolo

gy

(e.

g

., neural networks,

g

enetic al

g

orithms, swarm intel

-

l

i

g

ence)

■ Kernel methods (e.

g

., su

pp

ort vector machines)

Basically, a distinction can be made between predictive and descrip

-

tive analytics. In predictive analytics, a target variable is typically avail

-

able, which can either be categorical (e.g., churn or not, fraud or not)

or continuous (e.g., customer lifetime value, loss given default). In

descriptive analytics, no such target variable is available. Common

exam

p

les here are association rules, se

q

uence rules, and clusterin

g

.

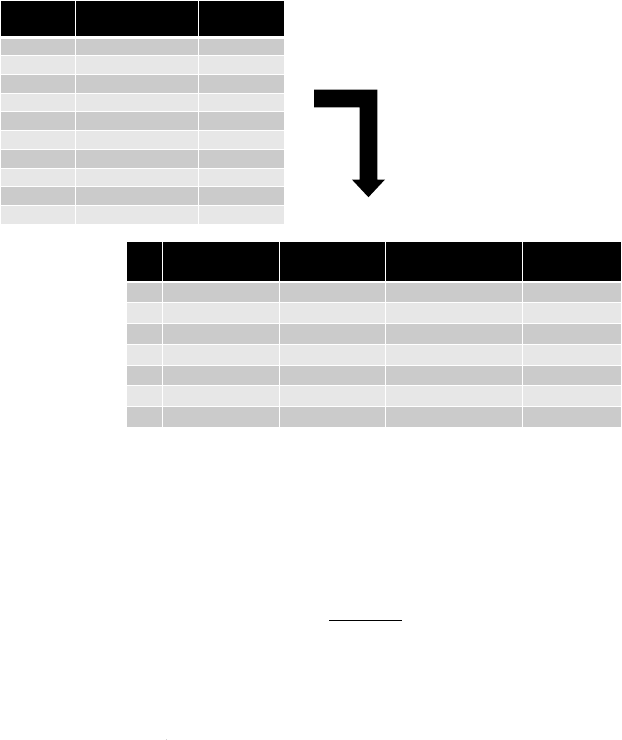

Figure 1.3 provi

d

es an examp

l

e o

f

a

d

ecision tree in a c

l

assi

cation

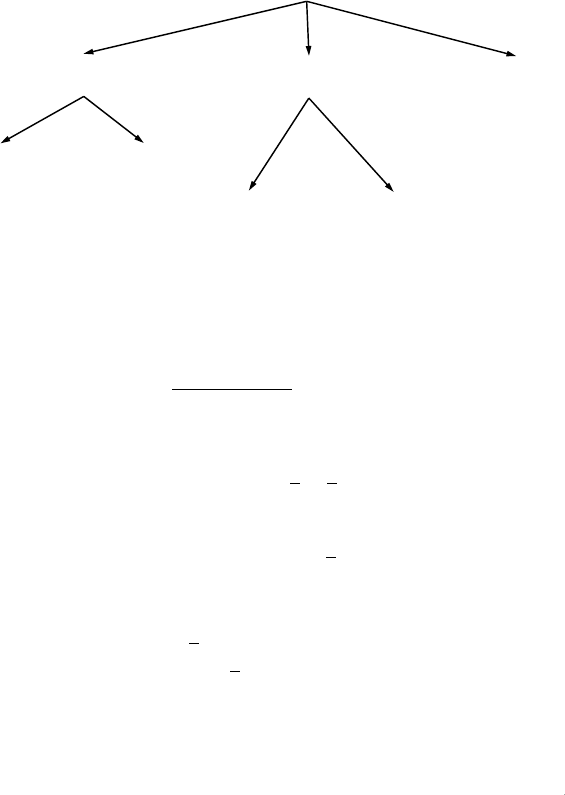

pre

d

ictive ana

l

ytics setting

f

or pre

d

icting c

h

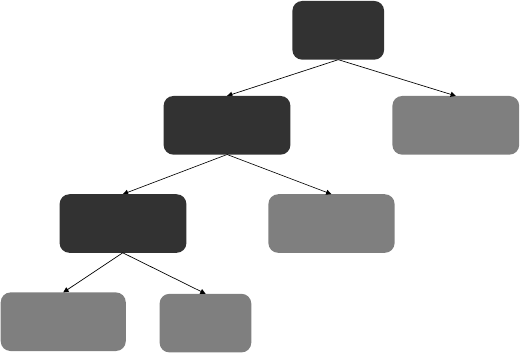

urn.

More t

h

an ever

b

e

f

ore, ana

l

ytica

l

mo

d

e

l

s steer t

h

e strategic ris

k

decisions of companies. For example, in a bank setting, the mini-

mum e

q

uit

y

and

p

rovisions a nancial institution holds are directl

y

determined b

y

, amon

g

other thin

g

s, credit risk anal

y

tics, market risk

analytics, operational risk analytics, fraud analytics, and insurance

risk anal

y

tics. In this settin

g

, anal

y

tical model errors directl

y

affect

p

ro tabilit

y

, solvenc

y

, shareholder value, the macroeconom

y

, and

society as a whole. Hence, it is of the utmost importance that analytical

F

i

gure 1.3 Example o

f

Classi

cation Predictive Analytics

Customer Age Recency Frequency Monetary Churn

John 35 5 6 100 Yes

Sophie 18 10 2 150 No

Victor 38 28 8 20 No

Laura 44 12 4 280 Yes

Analytics

Software

Age < 40

Yes

Yes

Churn No Churn Churn No Churn

Yes

No

No No

Recency < 10 Frequency < 5

B

I

G

DATA AND ANALYTI

CS

◂

9

models are develo

p

ed in the most o

p

timal wa

y

, takin

g

into account

various re

q

uirements that will be discussed in what follows.

ANALYTICAL MODEL REQUIREMENTS

A good analytical model should satisfy several requirements, depend-

ing on the application area. A rst critical success factor is business

relevance. The analytical model should actually solve the business

problem for which it was developed. It makes no sense to have a work

-

in

g

anal

y

tical model that

g

ot sidetracked from the ori

g

inal

p

roblem

statement. In or

d

er to ac

h

ieve

b

usiness re

l

evance, it is o

f

k

ey impor-

tance t

h

at t

h

e

b

usiness pro

bl

em to

b

e so

l

ve

d

is appropriate

l

y

d

e

ne

d

,

qua

l

i

e

d

, an

d

agree

d

upon

b

y a

ll

parties invo

l

ve

d

at t

h

e outset o

f

t

h

e

analysis.

A second criterion is statistical

p

erformance. The model should

have statistical si

g

ni cance and

p

redictive

p

ower. How this can be mea-

sured will depend upon the type of analytics considered. For example,

in a classi cation settin

g

(churn, fraud), the model should have

g

ood

discrimination

p

ower. In a clusterin

g

settin

g

, the clusters should be as

homogenous as possible. In later chapters, we will extensively discuss

various measures to

q

uantif

y

this.

De

p

endin

g

on the a

pp

lication, anal

y

tical models should also be

interpretable and justi able. Interpretability refers to understanding

the

p

atterns that the anal

y

tical model ca

p

tures. This as

p

ect has a

certain de

g

ree of sub

j

ectivism, since inter

p

retabilit

y

ma

y

de

p

end on

the business user’s knowledge. In many settings, however, it is con

-

sidered to be a ke

y

re

q

uirement. For exam

p

le, in credit risk modelin

g

or medical diagnosis, interpretable models are absolutely needed to

get good insight into the underlying data patterns. In other settings,

such as res

p

onse modelin

g

and fraud detection, havin

g

inter

p

retable

mo

d

e

l

s ma

y

b

e

l

ess o

f

an issue.

J

usti

a

b

i

l

it

y

re

f

ers to t

h

e

d

e

g

ree to

w

h

ic

h

a mo

d

e

l

corres

p

on

d

s to

p

rior

b

usiness

k

now

l

e

dg

e an

d

intu

-

i

t

i

on.

6

For examp

l

e, a mo

d

e

l

stating t

h

at a

h

ig

h

er

d

e

b

t ratio resu

l

ts

in more cre

d

itwort

hy

c

l

ients ma

y

b

e inter

p

reta

bl

e,

b

ut is not

j

usti

-

a

bl

e

b

ecause it contra

d

icts

b

asic

nancia

l

intuition. Note t

h

at

b

ot

h

interpreta

b

i

l

ity an

d

justi

a

b

i

l

ity o

f

ten nee

d

to

b

e

b

a

l

ance

d

against

statistica

l

p

er

f

ormance. O

f

ten one wi

ll

o

b

serve t

h

at

h

i

gh

p

er

f

ormin

g

10

▸

A

NALYTI

CS

IN A BI

G

DATA W

O

RL

D

anal

y

tical models are incom

p

rehensible and black box in nature.

A

p

o

p

ular exam

p

le of this is neural networks, which are universal

approximators and are high performing, but offer no insight into the

underlying patterns in the data. On the contrary, linear regression

models are very transparent and comprehensible, but offer only

limited modeling power.

Analytical models should also be

operationally ef cient

. This refers to

t

the efforts needed to collect the data, preprocess it, evaluate the model,

and feed its outputs to the business application (e.g., campaign man-

a

g

ement, ca

p

ital calculation). Es

p

eciall

y

in a real‐time online scorin

g

environment (e.g.,

f

rau

d

d

etection) t

h

is may

b

e a crucia

l

c

h

aracteristic.

Operationa

l

e

f

ciency a

l

so entai

l

s t

h

e e

ff

orts nee

d

e

d

to monitor an

d

b

ac

k

test t

h

e mo

d

e

l

, an

d

reestimate it w

h

en necessary.

Another key attention point is the

e

co

n

omic cos

t

needed to set up

t

the anal

y

tical model. This includes the costs to

g

ather and

p

re

p

rocess

the data, the costs to anal

y

ze the data, and the costs to

p

ut the result-

ing analytical models into production. In addition, the software costs

and human and com

p

utin

g

resources should be taken into account

here. It is im

p

ortant to do a thorou

g

h cost–bene t anal

y

sis at the start

of the project.

Finall

y

, anal

y

tical models should also com

p

l

y

with both local and

in

t

erna

t

ional re

g

ulation and le

g

islation . For exam

p

le, in a credit risk set

-

ting, the Basel II and Basel III Capital Accords have been introduced

to a

pp

ro

p

riatel

y

identif

y

the t

yp

es of data that can or cannot be used

to build credit risk models. In an insurance settin

g

, the Solvenc

y

II

Accord plays a similar role. Given the importance of analytics nowa

-

da

y

s, more and more re

g

ulation is bein

g

introduced relatin

g

to the

development and use of the analytical models. In addition, in the con-

text of privacy, many new regulatory developments are taking place at

various levels. A

p

o

p

ular exam

p

le here concerns the use of cookies in

a we

b

ana

ly

tics context.

NOTES

1. IBM, www.i

b

m.com/

b

i

g

‐

d

ata/us/en , 2013.

2. www.

g

artner.com/tec

h

no

l

o

gy

/to

p

ics/

b

i

g

‐

d

ata.

j

s

p

.

3. www.

kd

nu

gg

ets.com/

p

o

ll

s/2013/

l

ar

g

est‐

d

ataset‐ana

ly

ze

d

‐

d

ata‐mine

d

‐2013.

h

tm

l

.

4. www.

kd

nu

gg

ets.com/

p

o

ll

s/2013/ana

ly

tics‐

d

ata‐science‐e

d

ucation.

h

tm

l

.

BI

G

DATA AND ANALYTI

CS

◂

11

5. J. Han an

d

M. Kam

b

er, Data Minin

g

: Concepts an

d

Tec

h

niques

,

2n

d

e

d

. (Mor

g

an

Kaufmann, Waltham, MA, US, 2006); D. J. Hand, H. Mannila, and P. Sm

y

th, Prin-

ciples of Data Minin

g

(MIT Press, Cambrid

g

e

,

Massachusetts, London, En

g

land, 2001);

P. N. Tan, M. Steinbach, and V. Kumar, Introduction to Data Mining (Pearson, Upper

Saddle River, New Jerse

y

, US, 2006).

6. D. Martens, J. Vanthienen, W. Verbeke, and B. Baesens, “Performance of Classi ca

-

tion Models from a User Perspective.” Special issue,

D

ecision Support System

s

51, no. 4

(

2011

)

: 782–793.

13

C

HAPTER

2

Data Collection,

Sampling, and

Preprocessing

D ata are

k

ey ingre

d

ients

f

or any ana

l

ytica

l

exercise. Hence, it is

im

p

ortant to t

h

orou

ghly

consi

d

er an

d

l

ist a

ll

d

ata sources t

h

at are

o

f

p

otentia

l

interest

b

e

f

ore startin

g

t

h

e ana

ly

sis. T

h

e ru

l

e

h

ere is

t

h

e more

d

ata, t

h

e

b

etter. However, rea

l

l

i

f

e

d

ata can

b

e

d

irty

b

ecause

o

f

inconsistencies, incom

pl

eteness,

d

u

pl

ication, an

d

mer

g

in

g

p

ro

bl

ems.

T

h

rou

gh

out t

h

e ana

ly

tica

l

mo

d

e

l

in

g

ste

p

s, various

d

ata

l

terin

g

mec

h

a

-

nisms wi

ll

b

e app

l

ie

d

to c

l

ean up an

d

re

d

uce t

h

e

d

ata to a managea

bl

e

an

d

re

l

evant size. Wort

h

mentionin

g

h

ere is t

h

e

g

ar

b

a

g

e in,

g

ar

b

a

g

e

out (GIGO)

p

rinci

pl

e, w

h

ic

h

essentia

lly

states t

h

at mess

y

d

ata wi

ll

y

ie

ld

messy ana

l

ytica

l

mo

d

e

l

s. It is o

f

t

h

e utmost importance t

h

at every

d

ata

p

re

p

rocessin

g

ste

p

is care

f

u

lly

j

usti

e

d

, carrie

d

out, va

l

i

d

ate

d

, an

d

d

oc

-

umente

d

b

e

f

ore

p

rocee

d

in

g

wit

h

f

urt

h

er ana

ly

sis. Even t

h

e s

l

i

gh

test

mista

k

e can ma

k

e t

h

e

d

ata tota

ll

y unusa

bl

e

f

or

f

urt

h

er ana

l

ysis. In w

h

at

f

o

ll

ows, we wi

ll

e

l

a

b

orate on t

h

e most im

p

ortant

d

ata

p

re

p

rocessin

g

steps t

h

at s

h

ou

ld

b

e consi

d

ere

d

d

uring an ana

l

ytica

l

mo

d

e

l

ing exercise.

TYPES OF DATA SOURCES

As previously mentioned, more data is better to start off the analysis.

Data can ori

g

inate from a variet

y

of different sources, which will be

ex

p

lored in what follows.

1

4

▸

A

NALYTI

CS

IN A BI

G

DATA W

O

RL

D

Transactions are the rst im

p

ortant source of data. Transactional

data consist of structured, low‐level, detailed information ca

p

turin

g

the key characteristics of a customer transaction (e.g., purchase, claim,

cash transfer, credit card payment). This type of data is usually stored

in massive online transaction processing (OLTP) relational databases.

It can also be summarized over longer time horizons by aggregating it

into averages, absolute/relative trends, maximum/minimum values,

and so on.

Unstructured data embedded in text documents (e.g., emails, web

p

a

g

es, claim forms) or multimedia content can also be interestin

g

to

ana

l

yze. However, t

h

ese sources typica

ll

y require extensive preprocess

-

ing

b

e

f

ore t

h

ey can

b

e success

f

u

ll

y inc

l

u

d

e

d

in an ana

l

ytica

l

exercise.

Anot

h

er important source o

f

d

ata is qua

l

itative, expert‐

b

ase

d

data. An expert is a person with a substantial amount of subject mat-

ter ex

p

ertise within a

p

articular settin

g

(e.

g

., credit

p

ortfolio mana

g

er,

b

rand mana

g

er). The ex

p

ertise stems from both common sense and

b

usiness experience, and it is important to elicit expertise as much as

p

ossible before the anal