Microsoft Combinedppt Sansa E200 Combinedppt2

User Manual: Sansa e200

Open the PDF directly: View PDF ![]() .

.

Page Count: 94

Nelson Chan

EVP, Consumer

Products Business

and Corporate

Marketing

2 February 23, 2006

Agenda

Global Market Share Opportunities

Global Sales Expansion

Key Market Segments and Product Strategies

Branding and Advertising

3 February 23, 2006

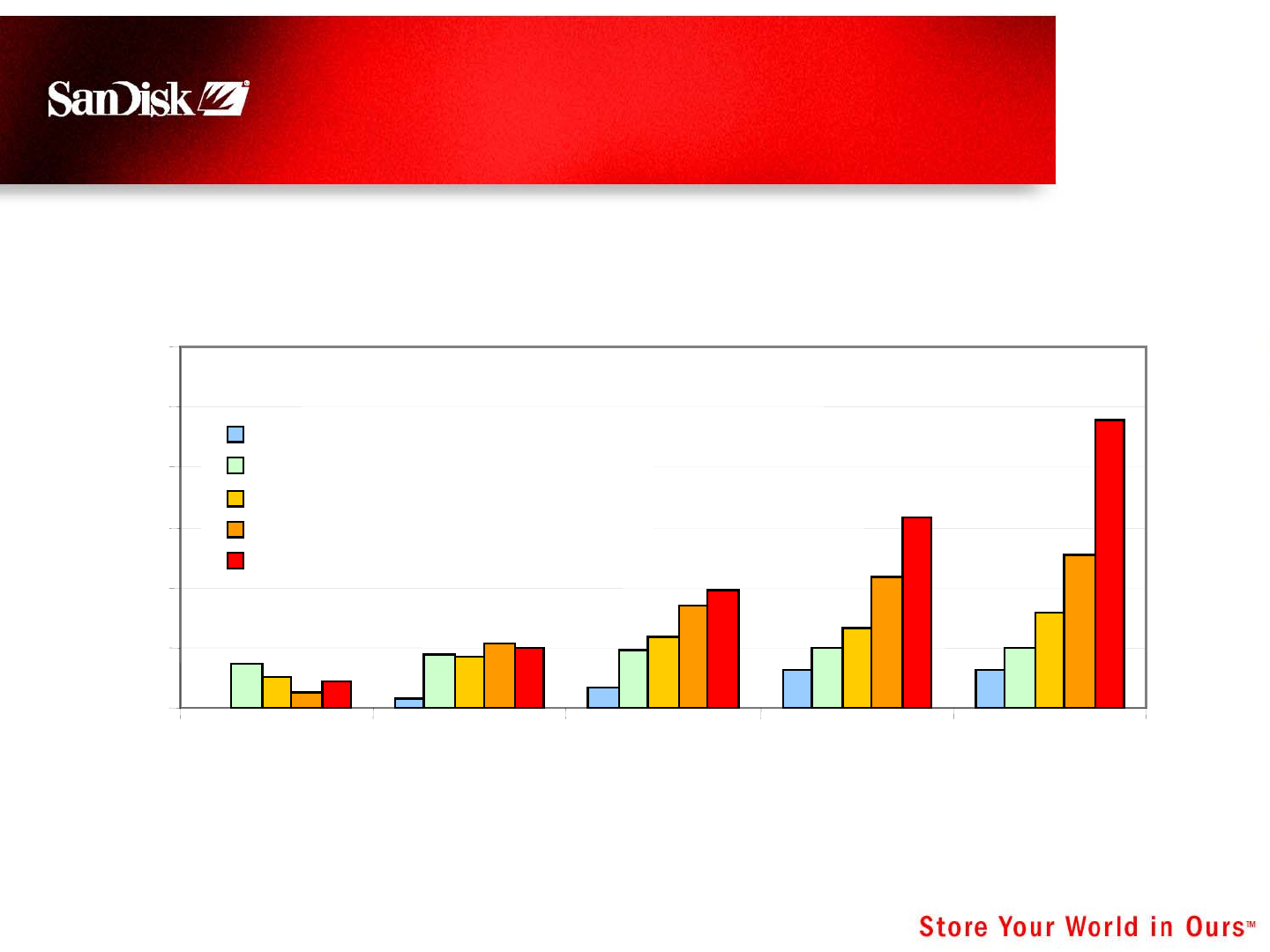

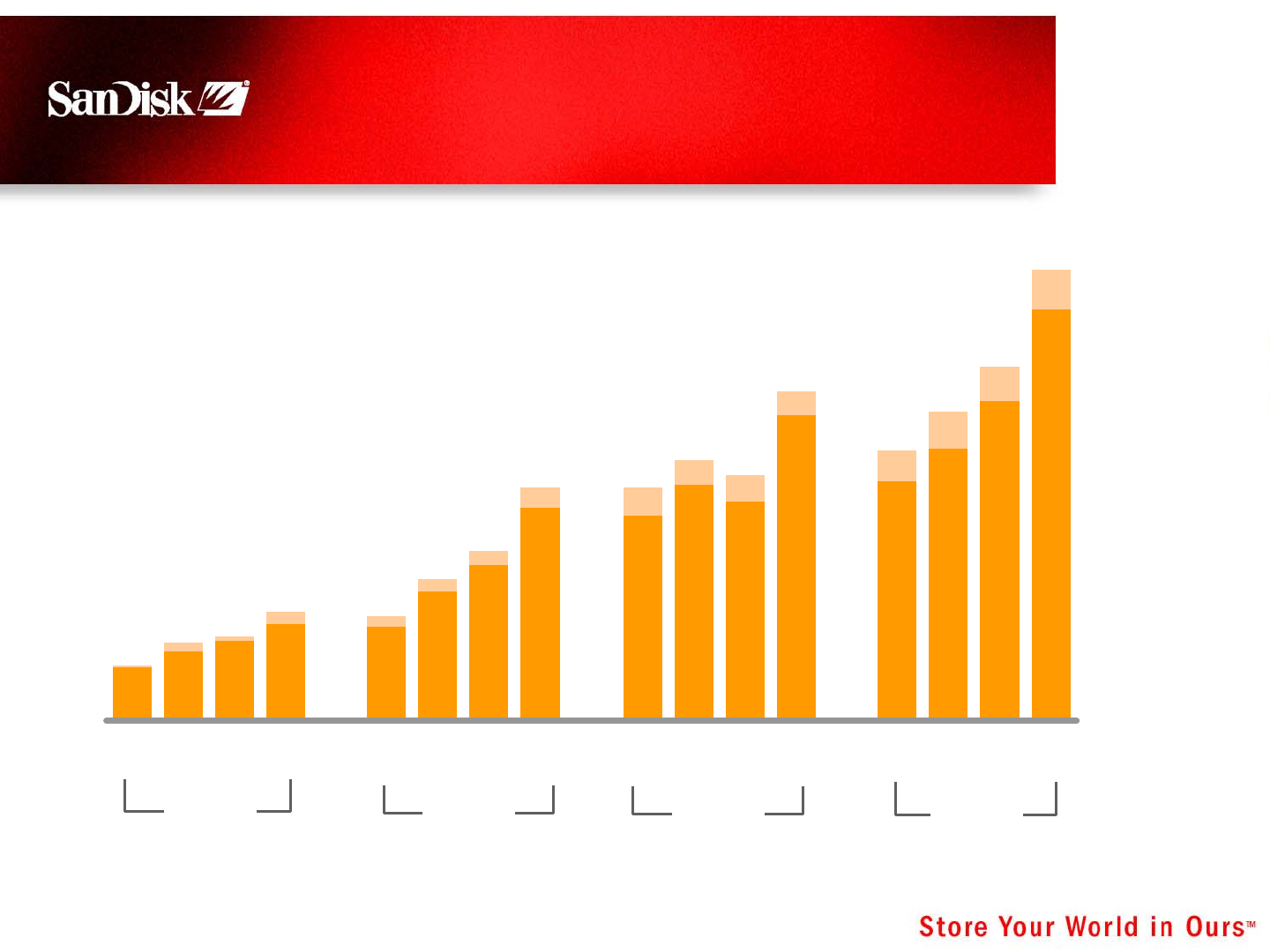

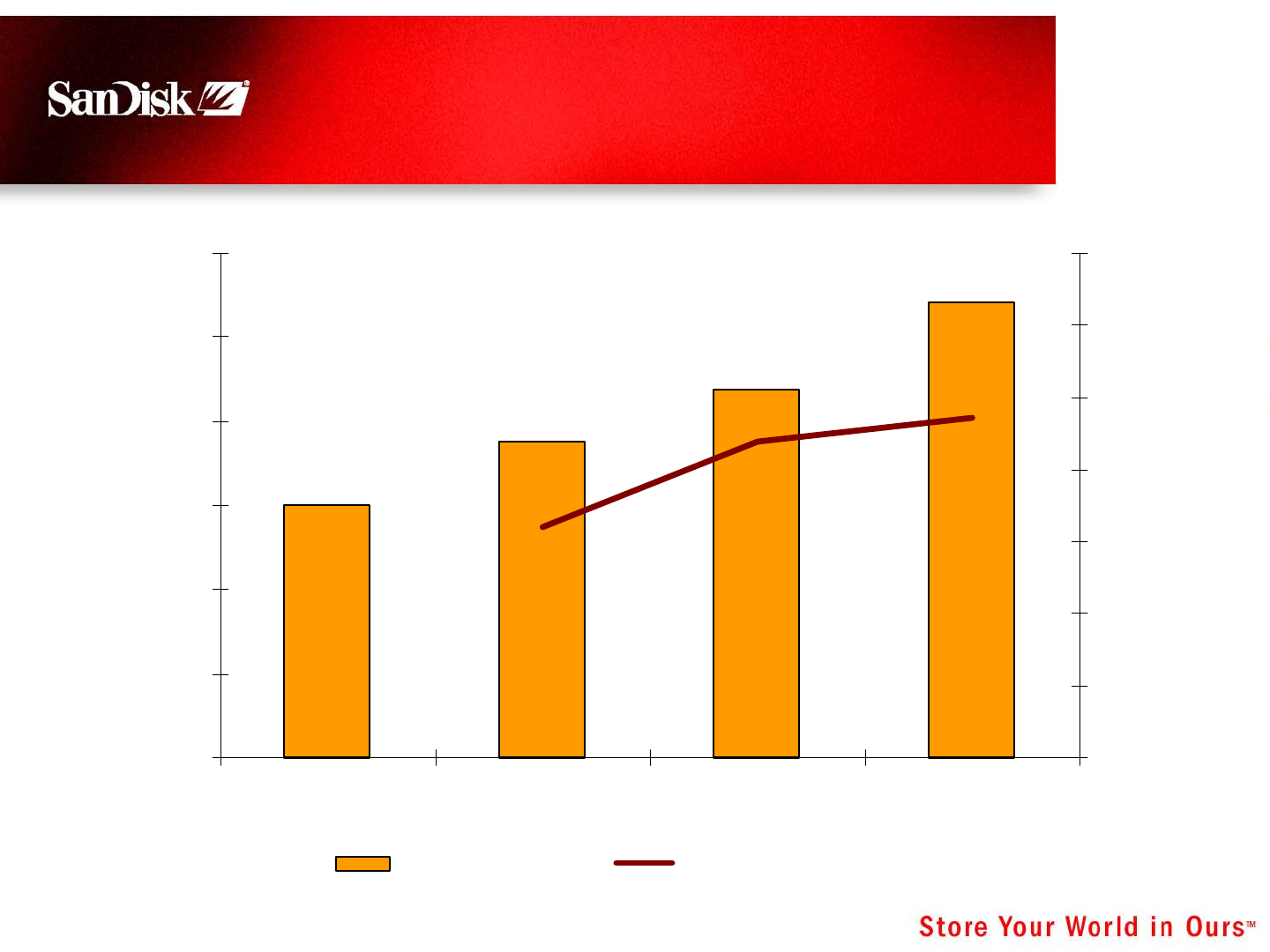

Key Markets

Sources: Gaming - IDC Jan06 / SanDisk, Flash Audio - Gartner Feb06 , DSCs - IDC Aug05/Feb06,

UFDs - Gartner Feb06, Phone Slots - Strategy Analytics Feb06

Million Units

CAGR 2005-08

0

100

200

300

400

500

600

2004 2005 2006 2007 2008

Gaming w. slot or USB 62%

Digital Cameras 3%

USB Drives 24%

Flash Audio Players 33%

Phone Slots 68%

4 February 23, 2006

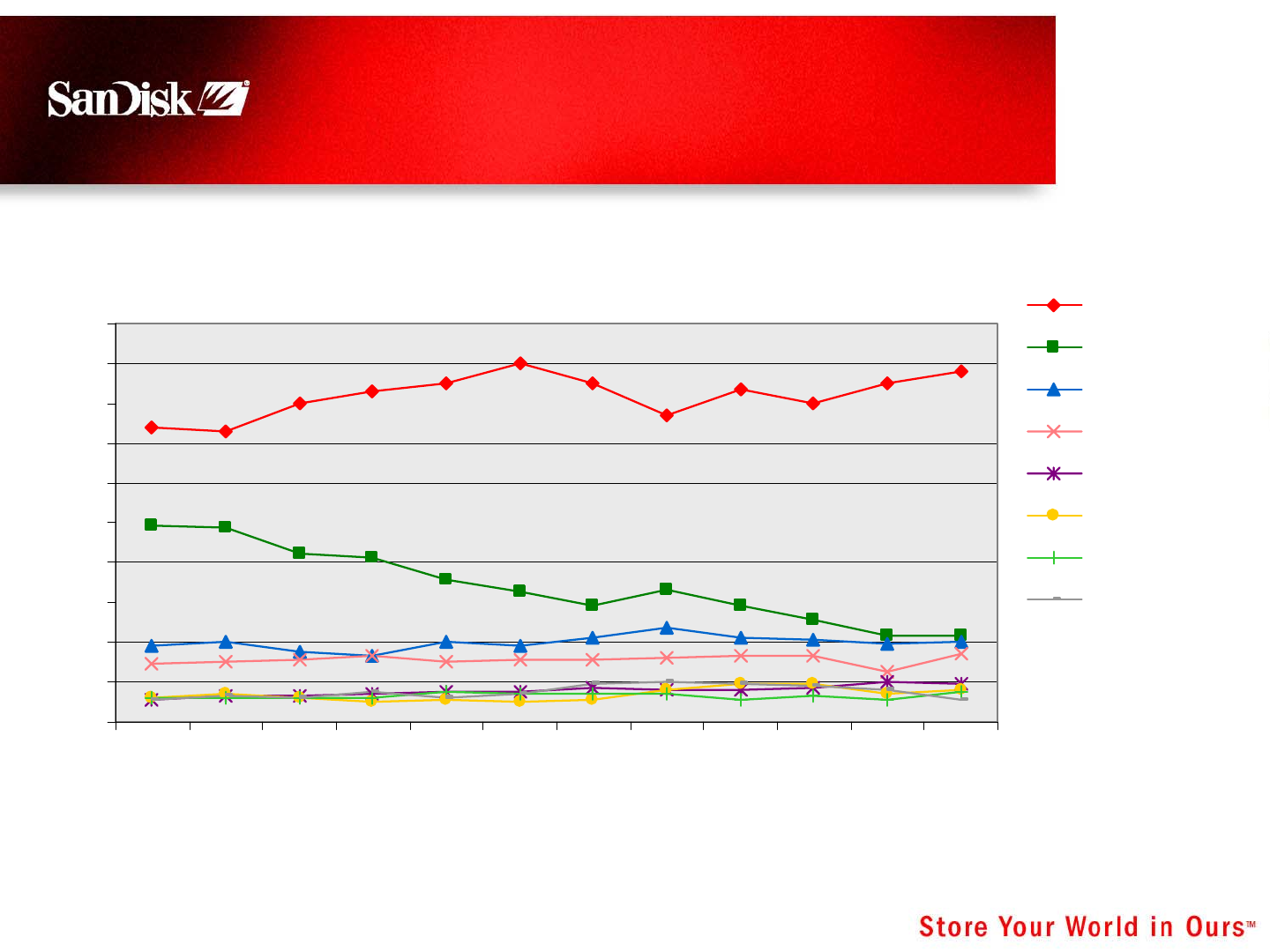

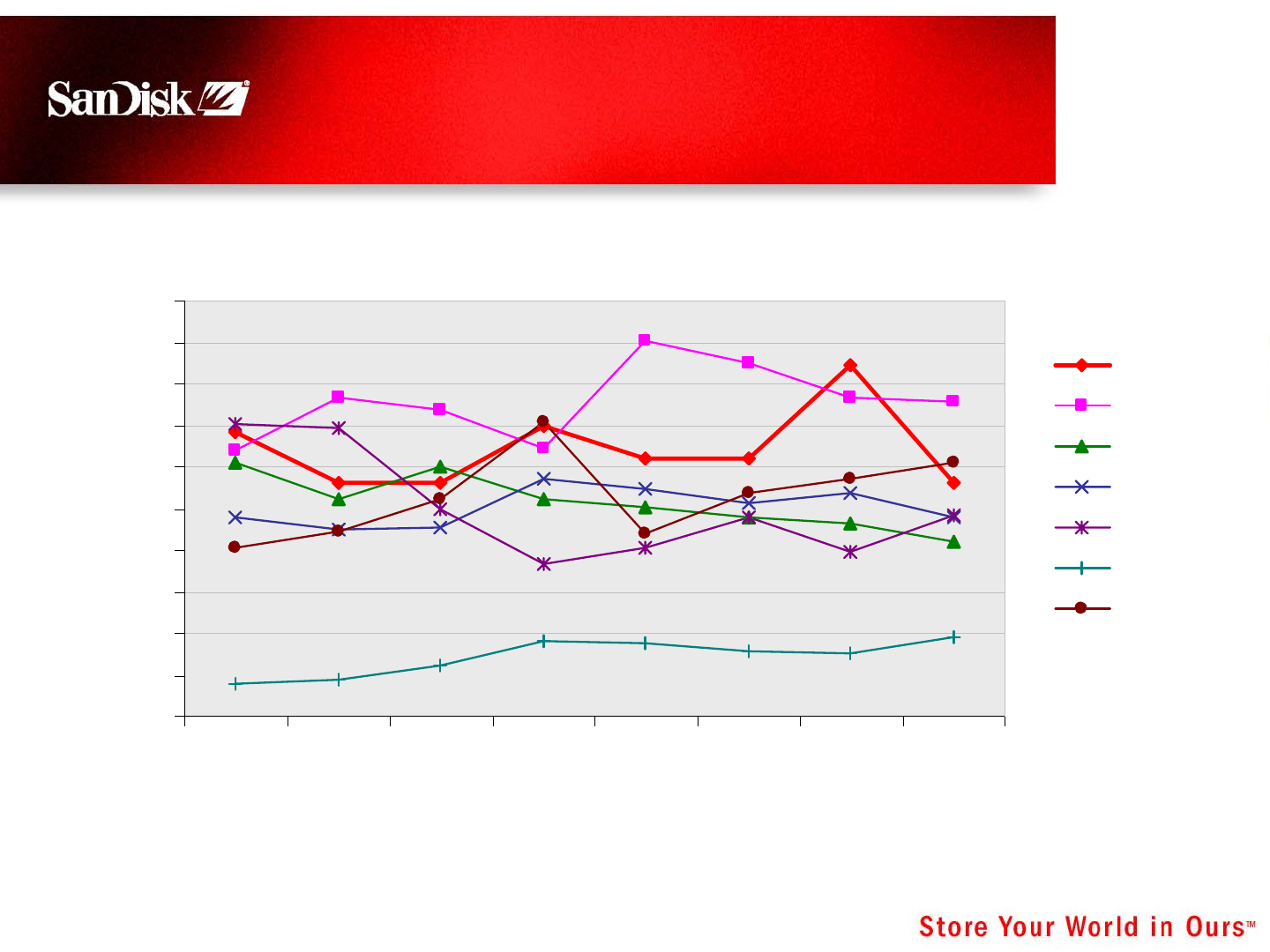

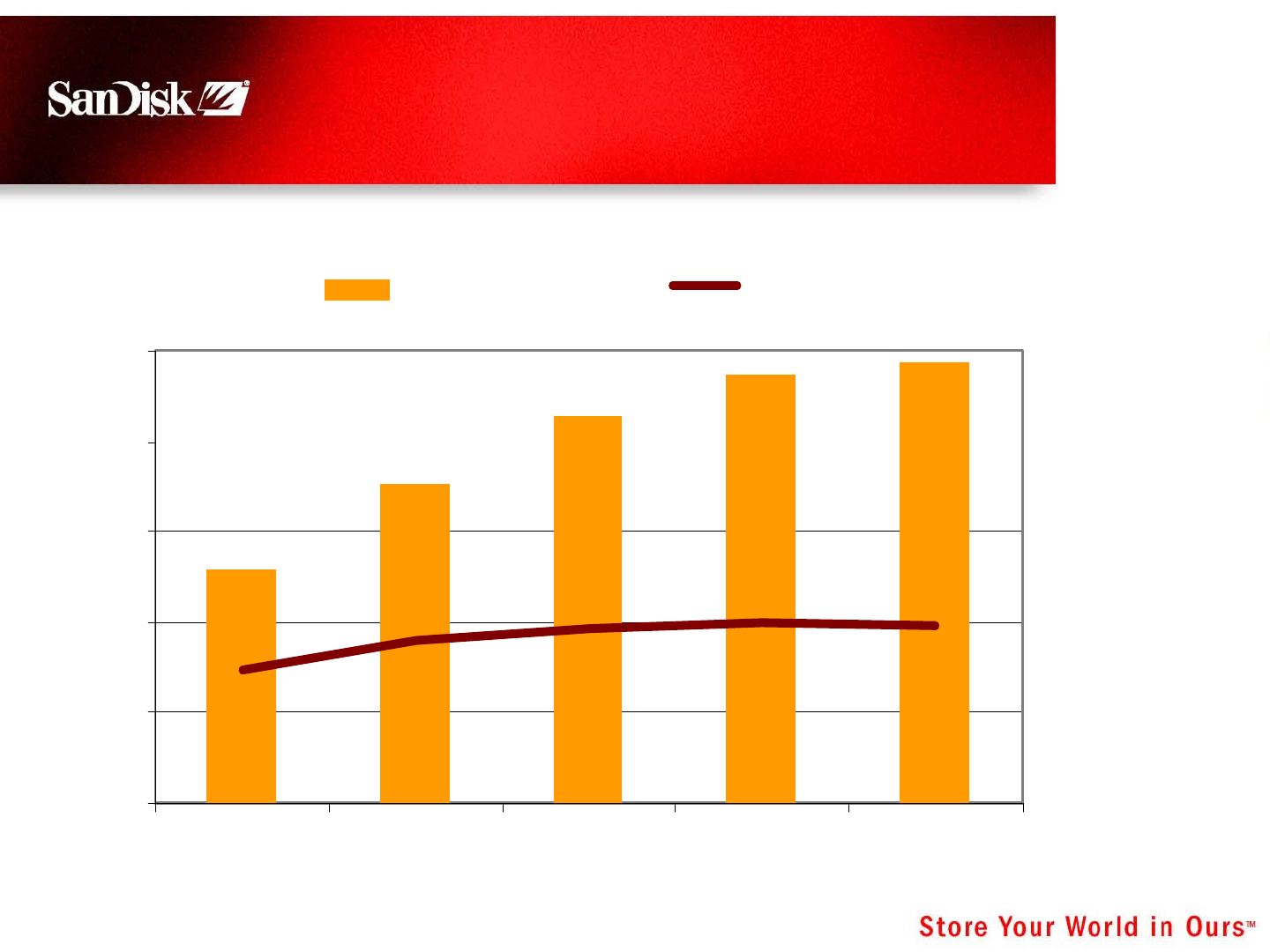

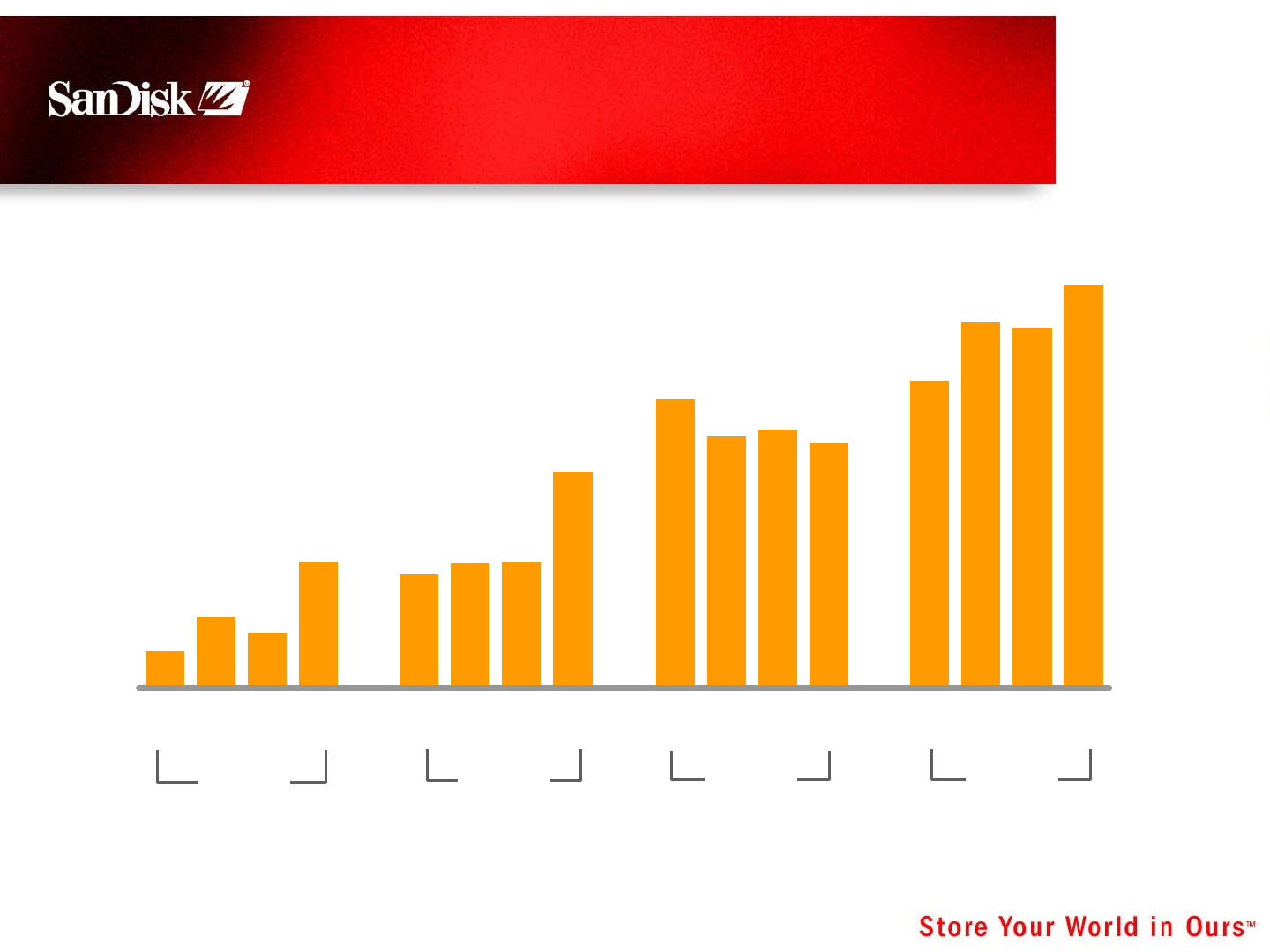

Growing Market Share: Leader in U.S.

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2005-01

2005-02

2005-03

2005-04

2005-05

2005-06

2005-07

2005-08

2005-09

2005-10

2005-11

2005-12

SanDisk

Lexar

PNY

Sony

Kodak

Memorex

Fujifilm

Kingston

Source: NPD Group

Retail Revenue Shares – Cards & UFDs

5 February 23, 2006

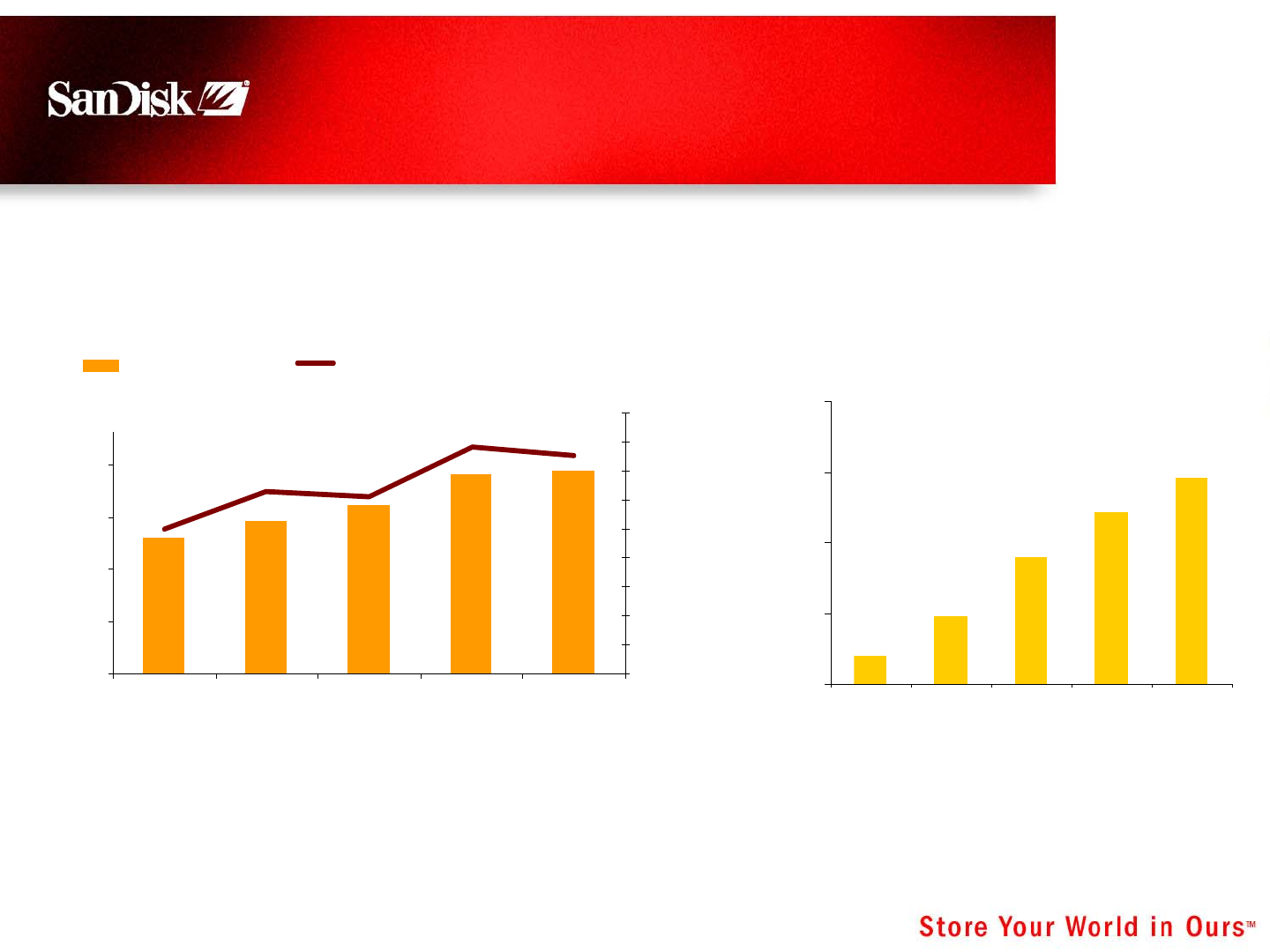

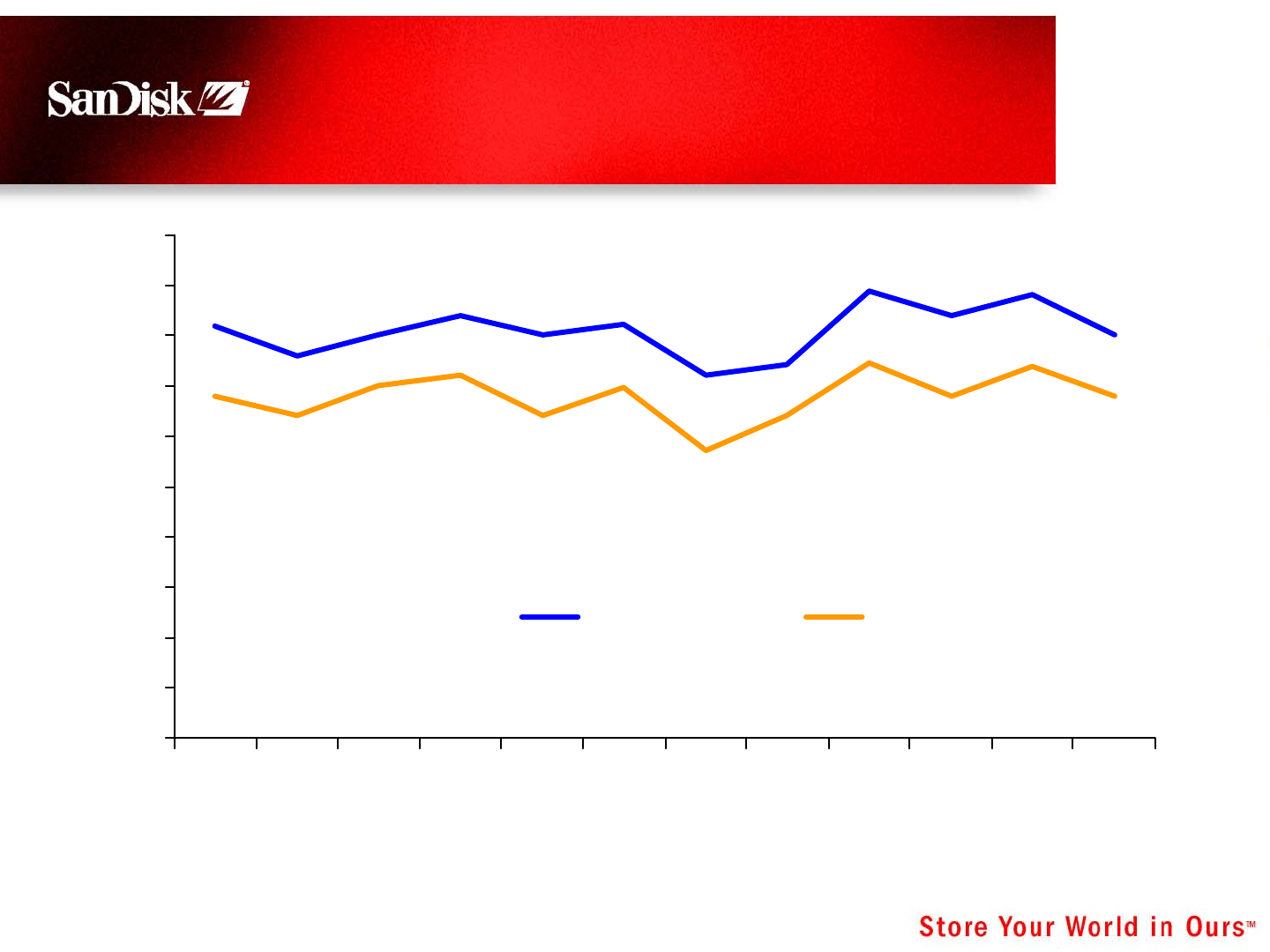

Europe: Opportunity for Growth in

2006

0%

5%

10%

15%

20%

25%

2005-01

2005-02

2005-03

2005-04

2005-05

2005-06

2005-07

2005-08

2005-09

2005-10

2005-11

2005-12

Source: GfK (France, Germany, UK)

Retail Revenue Shares – Cards + UFDs

SANDISK

PNY TECH

TRADEBRAND

SONY

FUJIFILM

HAMA

LEXAR

OLYMPUS

DANE ELEC

KINGSTON

UNBRANDED

6 February 23, 2006

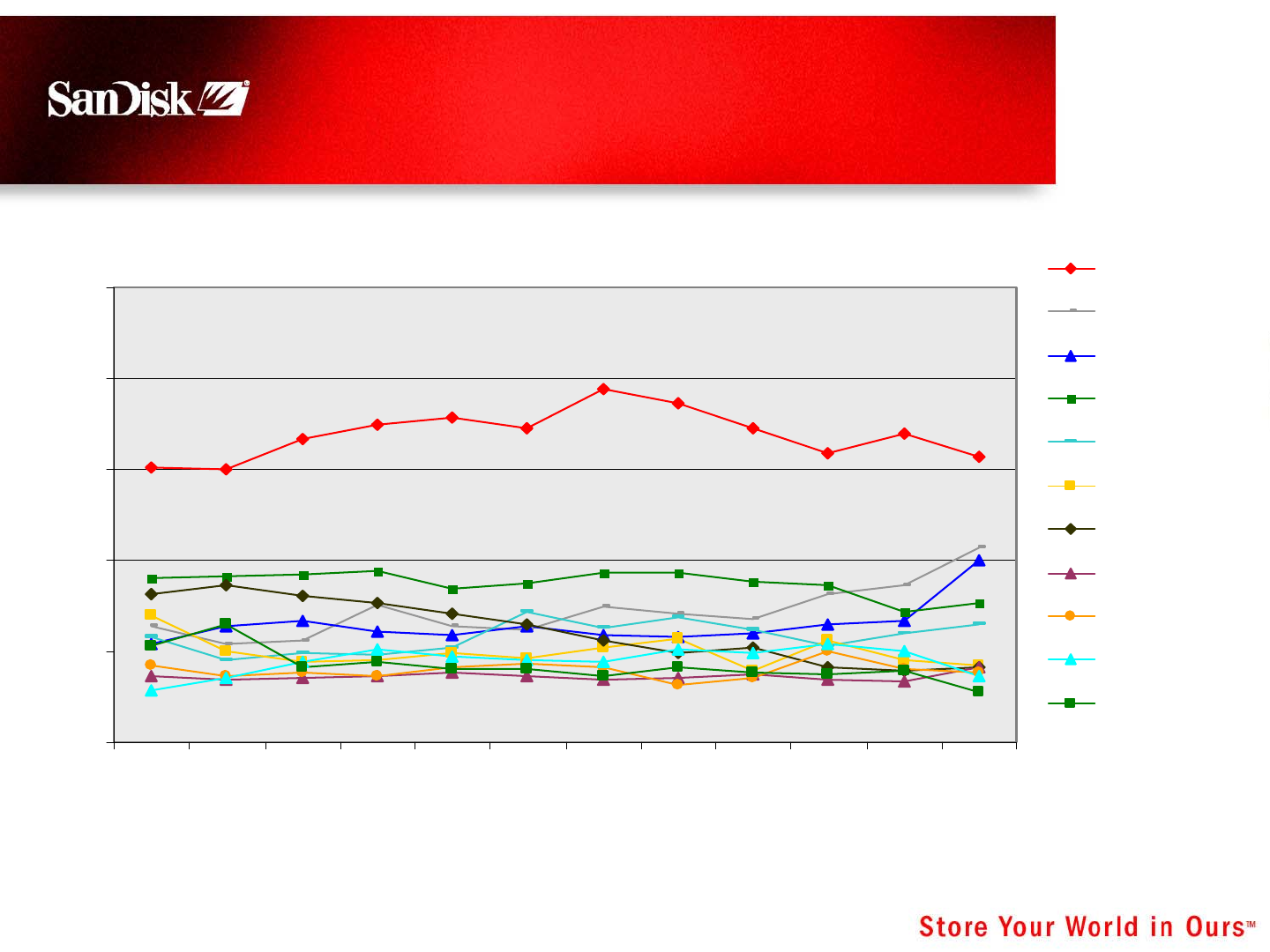

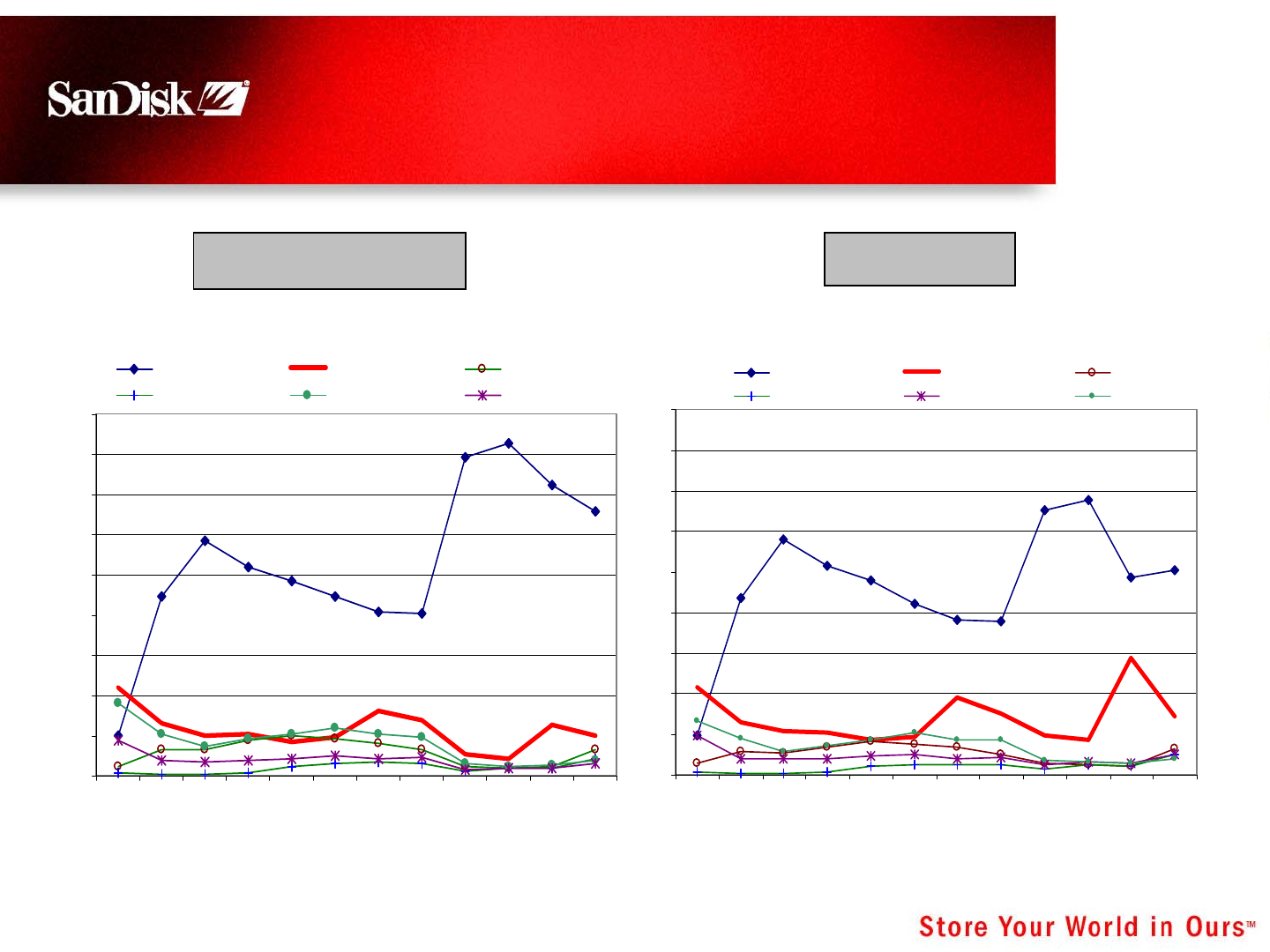

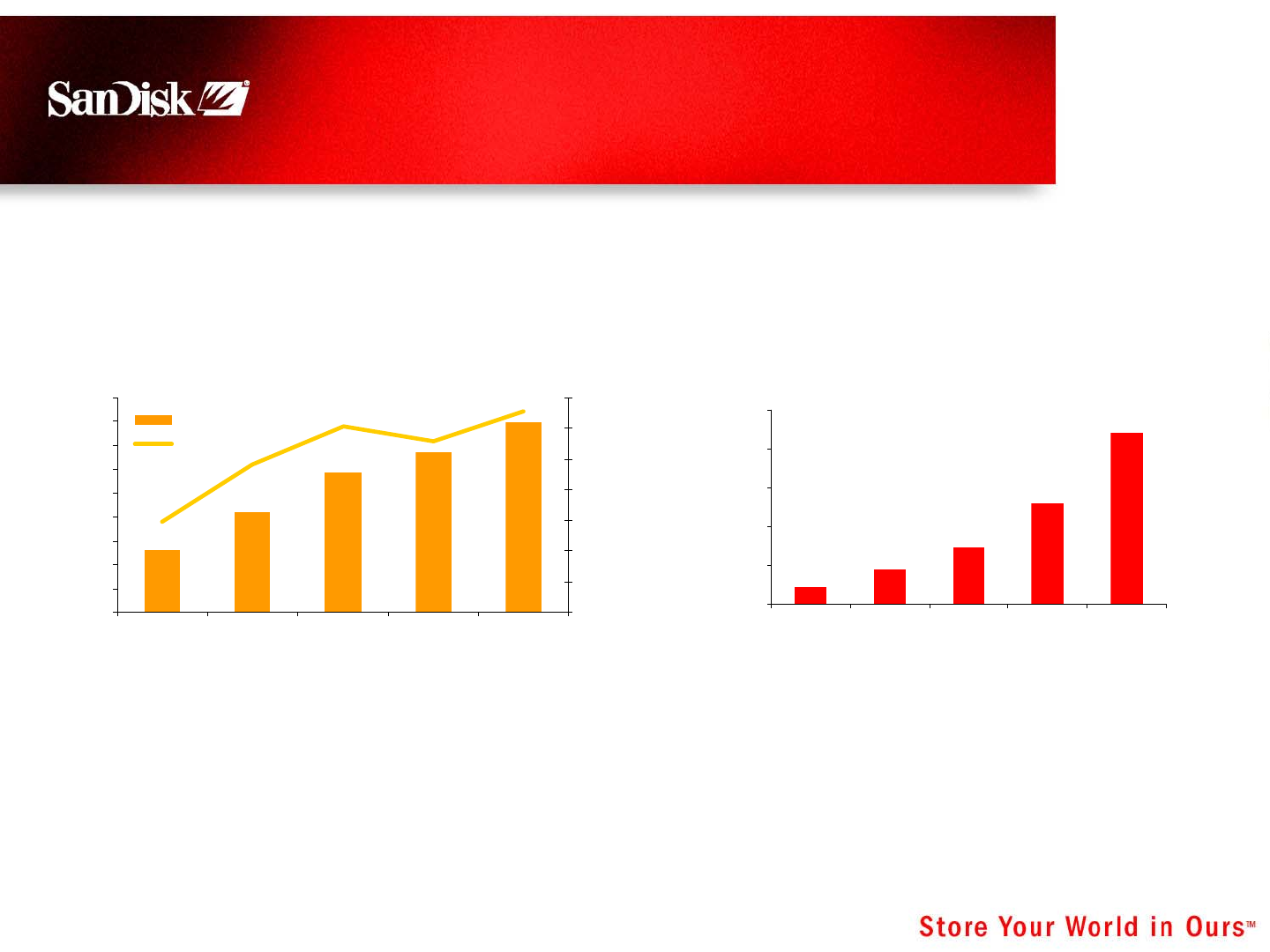

APAC: Opportunity for Growth

in 2006

0%

5%

10%

15%

20%

25%

30%

2005-01

2005-02

2005-03

2005-04

2005-05

2005-06

2005-07

2005-08

2005-09

2005-10

2005-11

2005-12

Source: GfK (China, Korea, Hong Kong, Taiwan, Singapore)

All Formats per Brand −Revenue

SANDISK

SONY

KINGSTON

TOSHIBA

OLYMPUS

ADATA

FUJIFILM

TRANSCEND

LG

AIGO

7 February 23, 2006

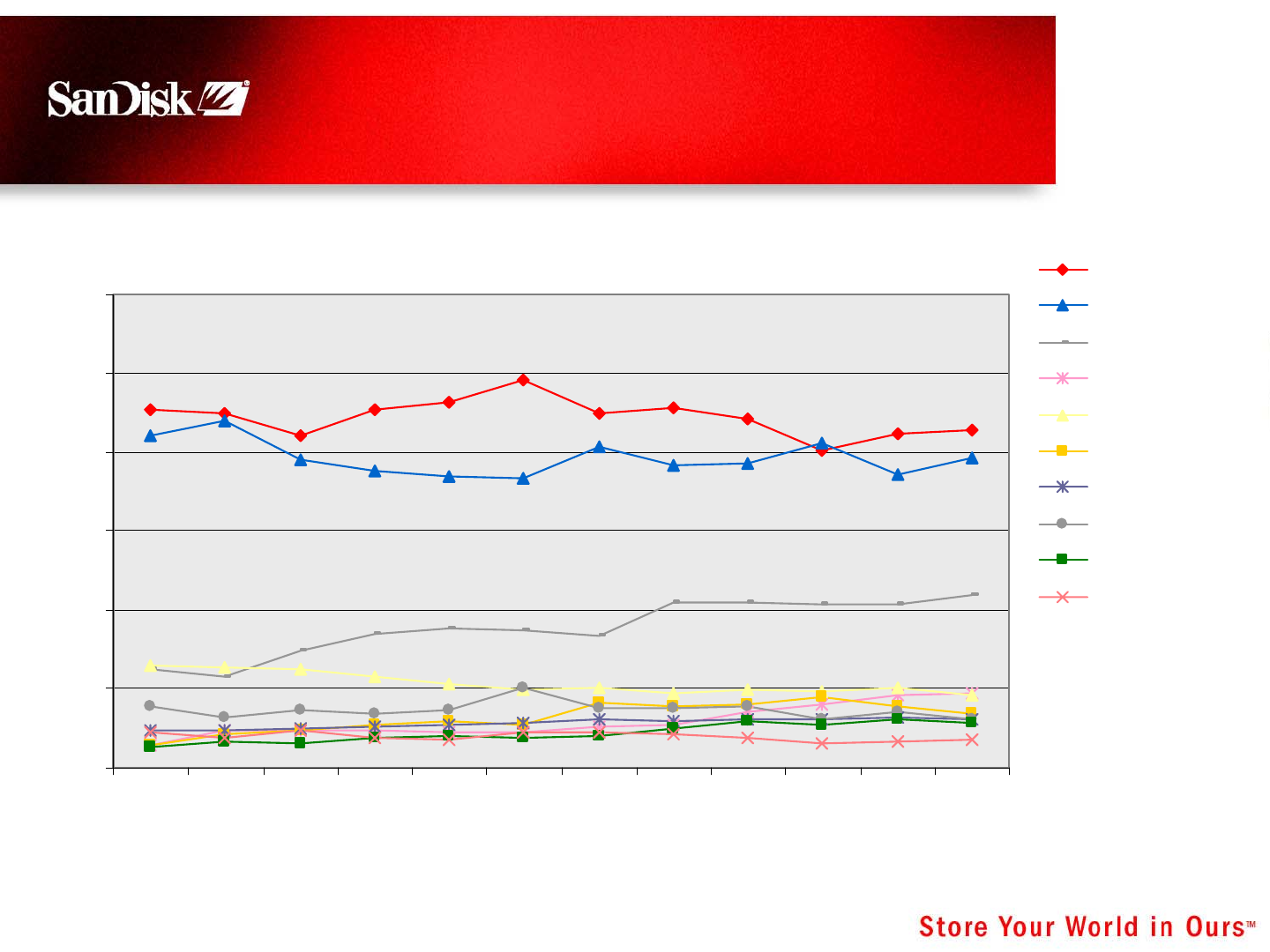

Japan: Opportunity to Lead

In Highly Fragmented Market

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

2004 Q1

Q2

Q3

Q4

2005Q1

Q2

Q3

Q4

SanDisk

Buffalo

Hagiwara

Panasonic

I-O Data

Lexar

Sony

All Formats per Brand −Shipments

Source: TSR

8 February 23, 2006

Flash Digital Audio Players: US

Market Shares

0

10

20

30

40

50

60

70

80

90

Jan-05

Feb-05

Mar-05

Apr-05

May-05

Jun-05

Jul-05

Aug-05

Sep-05

Oct-05

Nov-05

Dec-05

Apple SanDisk Samsung

Sony Creative Labs iRiver

Source: NPD Group

Revenue Share Unit Share

0

10

20

30

40

50

60

70

80

90

Jan-05

Feb-05

Mar-05

Apr-05

May-05

Jun-05

Jul-05

Aug-05

Sep-05

Oct-05

Nov-05

Dec-05

Apple SanDisk Samsung

Sony iRiver Creative Labs

9 February 23, 2006

Be Everywhere where people will purchase

…with the broadest product offering

Retail Sales and Marketing Strategy

1

2

3Build the Brand –

Predispose the Customer

to choose SanDisk

Own the Store – “Store in Store”

Segment, Differentiate, Promote, Train,

Merchandise

10 February 23, 2006

HQ –

Sunnyvale

Retail/OEM

Direct/

Distribution

CE/Mobile

Photo

Food/Drug

US

Canada

Mexico

Sales Ops

Doubling direct sales in EMEA and APAC

(with focus on China)

Added new sales team in Australia

Regional marketing staff in EMEA, APAC and Japan

Worldwide Sales Structure:

Aggressive Expansion Outside

the US

Dublin

Retail/OEM

CE/Mobile/

Photo

Germany

UK, France

Nordic

S Europe

E Europe

Middle East

Africa

Sales Ops

Field Eng

Hong Kong

Retail/OEM

CE/Mobile

China

Taiwan

Korea

S Asia

India

Yokohama

Retail/OEM

CE/Mobile/

Photo

Sales Ops

Field Eng

Sydney

Retail

CE/Mobile/

Photo

Australia

New Zealand

11 February 23, 2006

Global Reach: Over 150,000

Storefronts Worldwide

AAFES

Best Buy

Brooks/Eckerd

Circuit City

CompUSA

Wal-Mart

Costco

K-Mart

Musicland

Office Depot

Staples

Sears

Rite Aid

Radio Shack

Meijer/Food

Safeway

Kroger

HEB

MDI

GameStop

Sprint

Verizon

Bell World

Best Buy

Blacks

Costco

London

Drugs

Radio Shack

Sears

Shoppers

Drug Mart

West Fair

Canada Tire

T Mobile

Carphone

Warehouse

Woolworths

Dixons

Orange

Wal-Mart

Camara

Euronix

FotoSistema

Fotoco

FNAC

Foto Service

Germanos

Internet shops

Knut Leclerc

MakroMarkt

PhotoStation

Pulsat

RIC

Ringfoto

Schlecker

Aeon

BIC

Best

Edion

K’s

Kitamura

Kojima

Lawsons

Matsukiyo

Yamada

Yodobashi

Canada

5,000+

Canada

5,000+

Japan

14,000+

Japan

14,000+

Asia/

Pac Rim

27,000+

Asia/

Pac Rim

27,000+

USA, Mexico &

So. America

51,000+

USA, Mexico &

So. America

51,000+ Europe

51,000+

Europe

51,000+

20,000+ Food & Drug Stores

30,000+ Mobile Stores

20,000+ Food & Drug Stores

30,000+ Mobile Stores

Best

Coles

Fortress

Broadway

Lotte

Costco

Sunfar

GoMe

SuNing

DahZong

Officeworks

Big W

Harris Tech.

Good Guys

H Norman

Woolworths

48,000 store fronts added in 2005!

12 February 23, 2006

World Class Customers

13 February 23, 2006

Personal

Data Storage

Core

Digital

Imaging

Shoot & Store™ Family

Blue Family

SanDisk Ultra®Family

SanDisk Extreme®Family

Best

Good

Better

Emerging High Growth

Mobile

Phones

Memory Stick

PRO Duo™

miniSD™

MMCmobile™

microSD™

iNAND™

Digital

Audio

Sansa®e100

SansaTM m200

SansaTM c100

SansaTMe200

Gaming

SD™

Memory Stick

PRO Duo™

Cruzer Crossfire™

Cruzer®Mini

Cruzer®Micro Skins

Cruzer®Titanium II

Cruzer®Micro II

Differentiated and Segmented

Strategy

14 February 23, 2006

Source: DSCs-IDC Aug ’05/Feb ‘06, Installed Base-SanDisk Estimates

Digital Still Camera Market:

Growing Installed Base

-

50

100

150

200

250

2004 2005 2006 2007 2008

Installed Base 4 Years shipments

DSC Shipments & Installed Base

Life Span 4 Years

15 February 23, 2006

Card Capacities Increasing

Source: Web-Feet Research, Feb ‘06

0

500

1,000

1,500

2,000

2004 2005 2006 2007 2008

Digital Camera Market Average Capacities

0

50

100

150

200

250

2004 2005 2006 2007 2008

M Units

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

M $

Cards for DSCs Units Car ds f or DSCs $ TA M

NAND Units for DSCs DSC NAND $ TAM

MB

16 February 23, 2006

Digital Imaging Segments

MainstreamProsumerProfessionalValue-Conscious

17 February 23, 2006

USB Flash Drive Market

0

20

40

60

80

100

120

140

160

180

2004 2005 2006 2007 2008

M Units

0

500

1,000

1,500

2,000

2,500

3,000

3,500

M $

UFD Units

UFD $ TA M

0

500

1,000

1,500

2,000

2,500

2004 2005 2006 2007 2008

M B

USB Drive Market Average Capacities

Source: Gartner Feb ‘06

18 February 23, 2006

USB Flash Drive Products

New

Product

New

Product

19 February 23, 2006

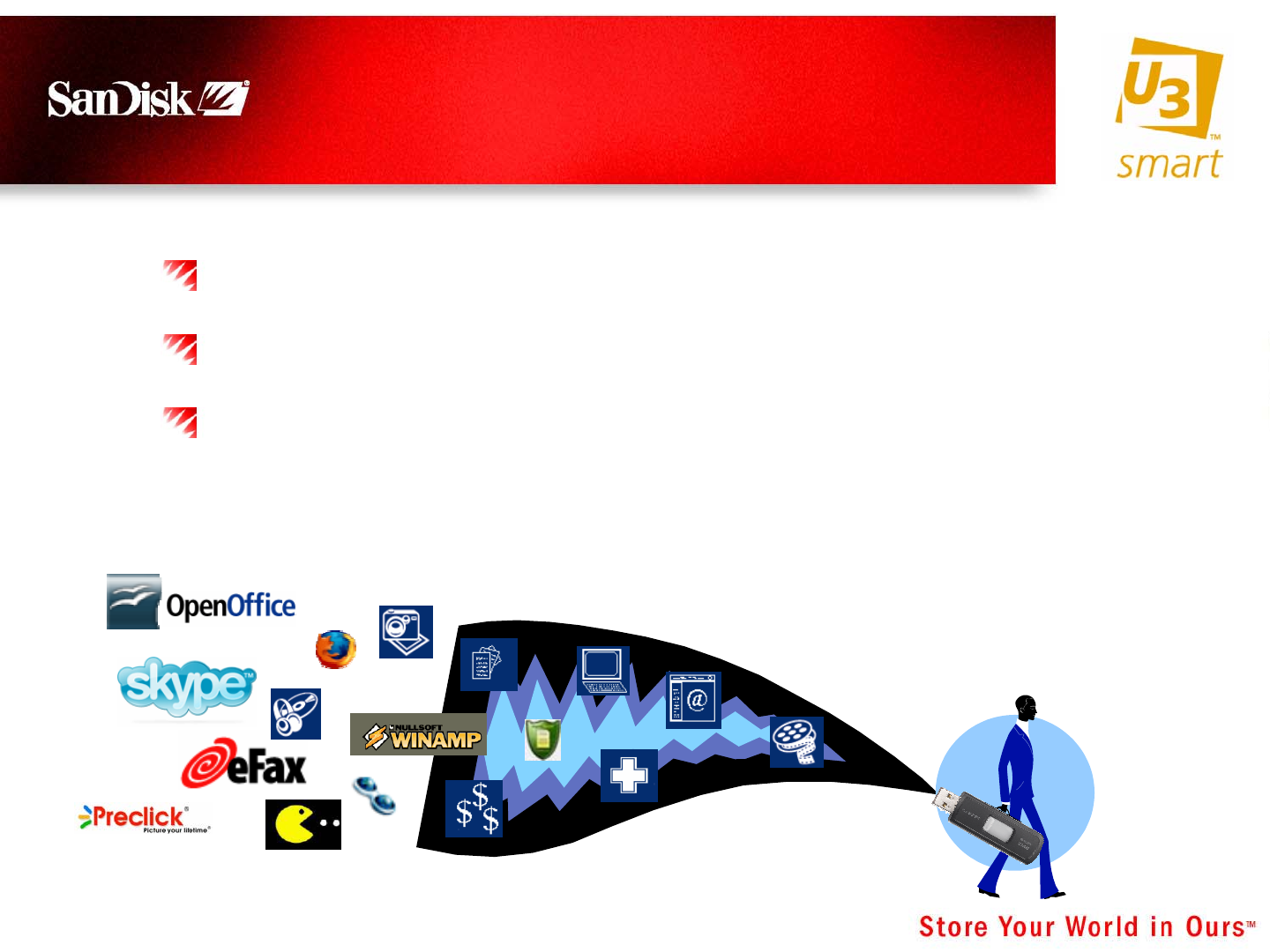

U3TM – Transforming the USB Market

Transform USB Drives from Today’s ‘Floppy Drive

Replacement’ into a Portable Personal Workspace

Enable a Continuum of Online and Offline Activity

Participate in the Shift from The PC-Centric

Paradigm to Access of Data “Anytime, Anywhere”

Home Office Friend’s

House

Business

Center

Internet

Cafe

20 February 23, 2006

U3 Fuels Demand for Flash

Increases Average Drive Capacity Usage

Expands the Market Through New Uses

Meets Individual Needs Through Software

Personalization

21 February 23, 2006

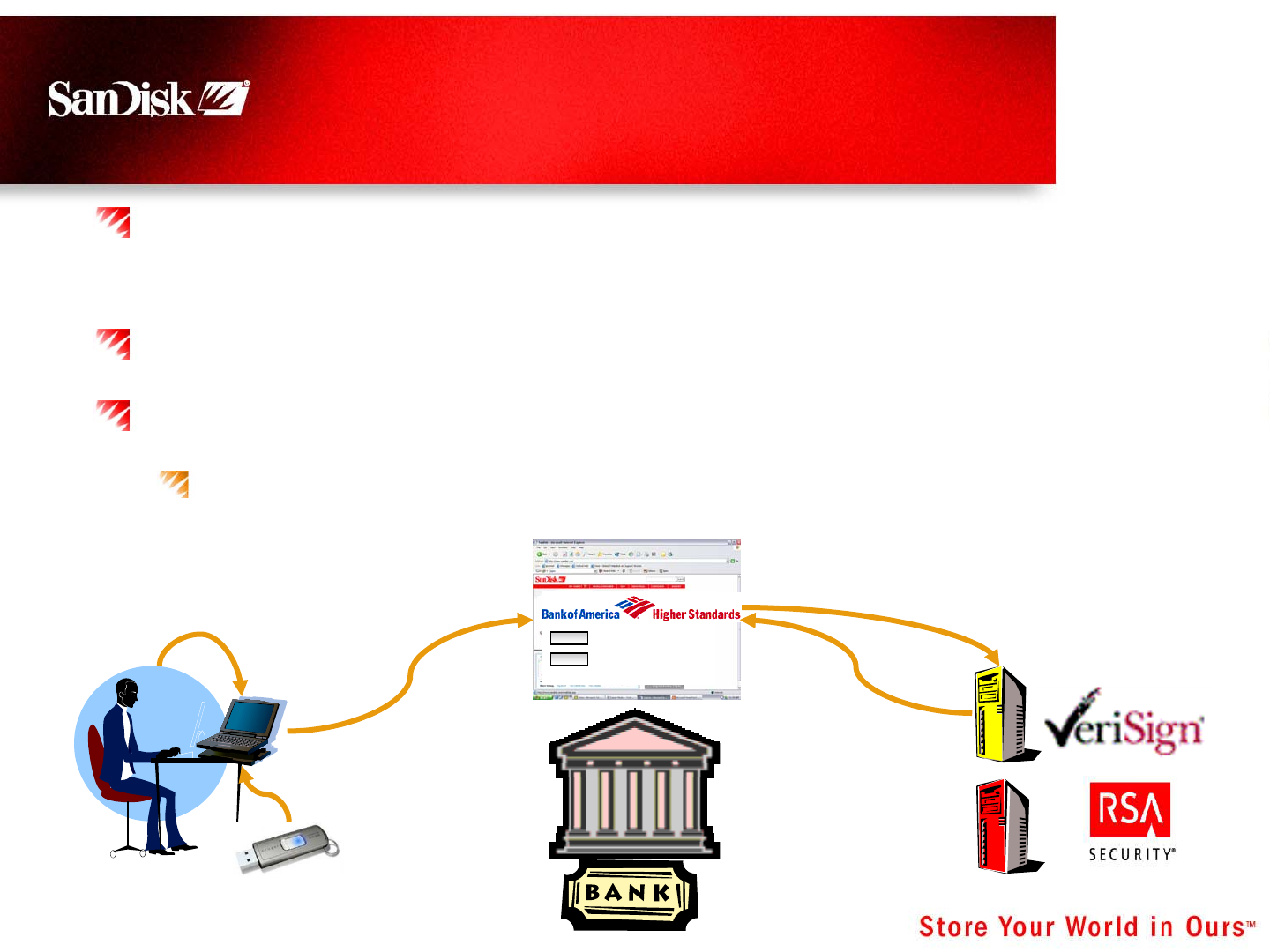

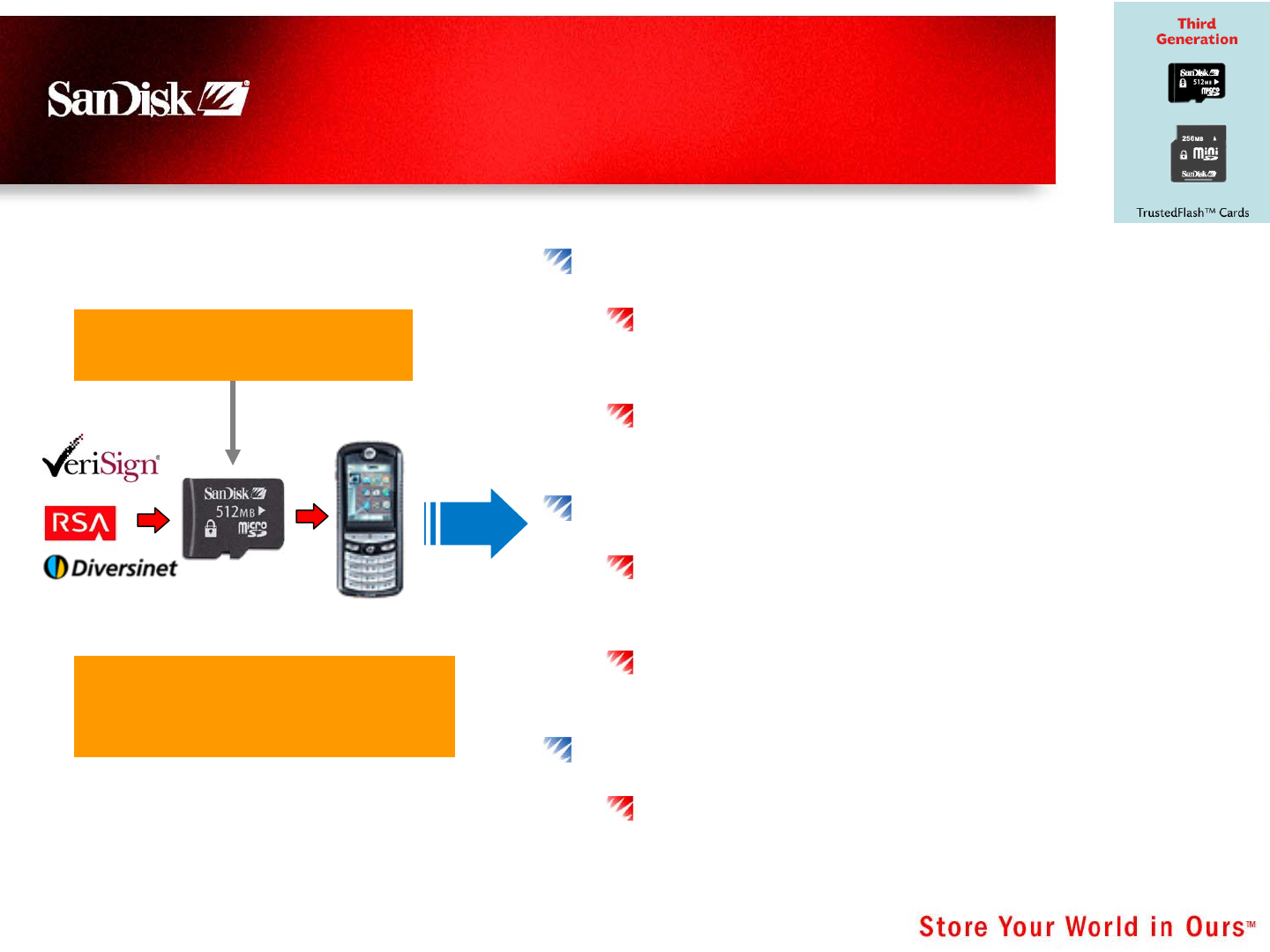

Growing the Market and Increasing

Differentiation: Protection Against

Online Fraud

Ideal for Many Online Applications (Banking, Trading,

E-Commerce, etc.)

Uses Highly Secure, Dual-Factor Authentication

Partnering with the Security Industry’s Leaders

RSA & Verisign

Password

Crypto-Secret

Password

+

Crypto-Secret

Request

Authentication

Username

Password

Authenticate

22 February 23, 2006

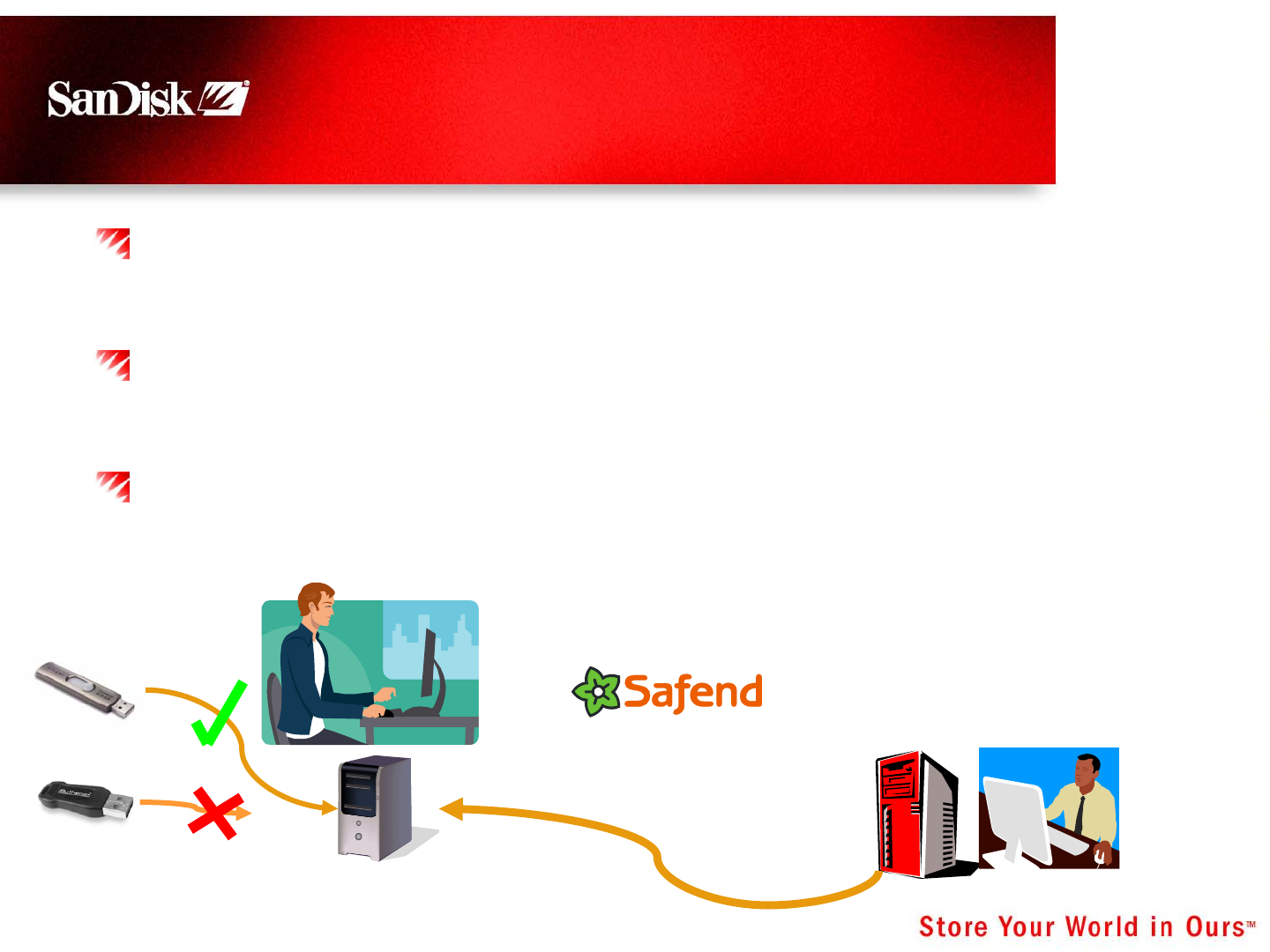

Growing the Market and

Increasing Differentiation:

Protection for the Enterprise

SanDisk is Partnering with Key Companies to Provide

Highly Secure Enterprise Solutions

Goal −Ensure Sensitive Data Doesn’t “Walk Out the

Door” via an Unsecured USB Drive

Working to Create the Right Solutions PLUS Provide

Methods for Managing Fleets of Devices

Authorized UFD

IT Manager

Remote Device

Administration

Personal UFD

23 February 23, 2006

Gaming Card Market

0

10

20

30

40

50

60

70

80

2004 2005 2006 2007 2008

M Units

0

200

400

600

800

1,000

1,200

M $

Gaming Card Units

Gaming Card $

0

200

400

600

800

1,000

2004 2005 2006 2007 2008

Gaming Card Market Average Capacities

Source: Web-Feet May ‘05

MB

24 February 23, 2006

New Gaming Consoles

All Major New In-Home Consoles are USB/Card Enabled

Content import, downloads and game saves are primary

drivers

Sony®PS3™

CF, SD, and MS slot

6 USB ports

Microsoft®Xbox 360™

Proprietary memory unit with USB interface

3 USB ports

Nintendo®Revolution

SD slot

2 USB ports

25 February 23, 2006

Gaming – Incremental Store

Fronts and Shelf Space

New

Products

26 February 23, 2006

Gaming In Retail

27 February 23, 2006

Flash-Based Digital Audio Players

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

$20

2004 2005 2006 2007 2008

IDC Sept 2005

Gartner Feb

2006

Billions

28 February 23, 2006

Significant Cost Advantage Due to

Vertical Integration

Leverage Established Global Retail Sales

Channels

Rapid global expansion – Europe and Asia

Develop “Cool” Products at Very Attractive Price

Points

“Good, Better, Best” product portfolio

Cards slots for expandability and portability

Own the Market Sweet Spot: $49-$149

Allow Customer Choice

Support of Microsoft PlaysForSure DRM

(RealNetworks, Napster and Yahoo Music)

Flash Audio Player Strategy

TM

29 February 23, 2006

Strong Channel Presence

“Own the store” −Educate,

Promote and Merchandise

Promote Media Centers

and “Store Within a Store”

Concepts

“Dramatically Increase In-Store

Adjacencies”

30 February 23, 2006

Building the Brand

Increase Sales in Established and New Markets

~2% of revenues for branding and merchandising

Building Global Brand Awareness

Engaging Grey San Francisco for global advertising and

MetaDesign for brand identity communication

Predispose Consumers to Buy SanDisk

Premium brand at everyday price

31 February 23, 2006

Drive the Brand Globally

Focus on high growth

geographies (EMEA, China, etc.)

Focus Global Marketing Campaigns

on Key Areas

SanDisk brand and products

Digital audio

Mobile (handsets)

High-performance card line (digital

imaging)

Promote Usage of Flash Cards in

Mobile Phones and Drive Retail

Attach Rates

Establish SanDisk Brand in Digital

Audio and Solidify #2 Position

Marketing Objectives

33 February 23, 2006

Summary

Focusing on Multiple High-Growth Markets

Unrivaled Product Lines

Both breadth and depth

Highly segmented and differentiated

Strong new product pipeline and innovation

Drive Global Expansion and Market Share Gain

Exceptional Channel Strength and Coverage

Leveraging Key OEM and Retail Partnerships

Slots ÆBundles ÆAftermarket

Investing to Build a Global Consumer Brand

Yoram Cedar

EVP of Handset

Business and

Corporate

Engineering

35 February 23, 2006

-

200

400

600

800

1,000

1,200

2004 2005 2006 2007 2008

Million Units

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

Mobile Flash Card

Revenue, $K

Total Mobile Phones (000)'s Units Mobile Phone Card Slots (000)'s Units Total Mobile Card Revenue, $K

Worldwide Mobile Phone Card TAM

Sources: Phones - Strategy Analytics,

Mobile Revenue - SanDisk, 2006

36 February 23, 2006

Primary Mobile Card Usages

Memory Expansion

Digital audio

Personal images and video recording

Personal data backup

Variety of files (email, presentations…)

Protected Content Storage

Pre-loaded

Downloaded

Mobile User Authentication (Dual Factor

Authentication)

Securely access the enterprise, banking and other

sensitive services

37 February 23, 2006

Applications Are Storage Intensive

Content will follow successful CE Applications

Music Phone

Camera Phone

PDA Phone

Game Phone

Video Phone

GPS Phone

MobileTV

PC, CE Markets Mobile Market

Email Imaging Music Game

Video Map TV / STB Application

38 February 23, 2006

Source: SanDisk, 2006

Worldwide Mobile Card Usage

2005 Retail

Others

13%

Picture

26% Music

61%

39 February 23, 2006

0

500

1000

1500

2000

2500

2005 2008

Others (Games, Maps, …)

Video Clip (Sports,

MusicTV, Comedy, Films)

Digital Music

Personal Picture

Personal Video

Applications Drive Retail Card

Capacity

Source: Usage from SanDisk Estimates, Q1’06

Digital Rights Management (DRM) Solutions Expected to Accelerate Consumption

40 February 23, 2006

Evangelize to Grow Mobile TAM

Leverage Relationships with Mobile Phone

Ecosystem

Provide Leading Technical Expertise for Rapid

Adoption and Time-to-Market

Drive Content Security Solutions

Support OEM ÆSupport Retail

41 February 23, 2006

Mobile Phone Ecosystem

Partnership to Drive Market Adoption

ASSP,

OS

Security Content and

Service

Providers

Content and

Service

Providers

Mobile

Operators

Mobile

Operators

Handset

Vendors

Handset

Vendors

42 February 23, 2006

microSD Adoption Accelerating

Source: SanDisk, 2006

0

50

100

150

200

250

300

350

400

450

Q304 Q404 Q105 Q205 Q305 Q405

microSD

miniSD

SD

All Others

Number of Models

Flash Card Adoption in Handsets

43 February 23, 2006

Overwhelming Adoption of SDTM

Formats

SD format adopter

Source: SanDisk, 2006

Manufacturer 2005

Nokia RSMMC, miniSD, microSD

Motorola SD, miniSD, microSD

Samsung RSMMC,SD, miniSD,

microSD

Siemens/BenQ RSMMC, SD, microSD

LG miniSD, microSD

SEMC MS Pro Duo

PMC miniSD

Alcatel miniSD

NEC miniSD, microSD

Kyocera miniSD, microSD

Sharp SD, miniSD

Sagem miniSD, microSD

Philips SD

Mitsubishi MS Duo, miniSD

Sanyo miniSD

44 February 23, 2006

OEM Business

Customers and Strategy for Growth

Added Value and Functionality

Customization

Security and DRM

Collaboration on Future Designs

Design know-how

Custom solutions

All Relevant Form Factors

Embedded Solutions as Needed

Retail Strength

45 February 23, 2006

Retail Business

Most Comprehensive Mobile Card Line Up

Partner with Retailers and Market

Drivers to Increase Adoption Rates

In-Store education

Joint promotion

Customized content (e.g.,

Verizon VCast)

35k Storefronts and Growing

Broad Product Offering

All major form factors

46 February 23, 2006

Poised for Mobile Growth

Huge Addressable Market

Projected $7B TAM in 2008

Technology and Product Leadership

Pioneer of mobile cards

Right solutions to satisfy and grow market

Channel Strength

Right customers; Right channels

New Technologies for

Emerging Markets

48 February 23, 2006

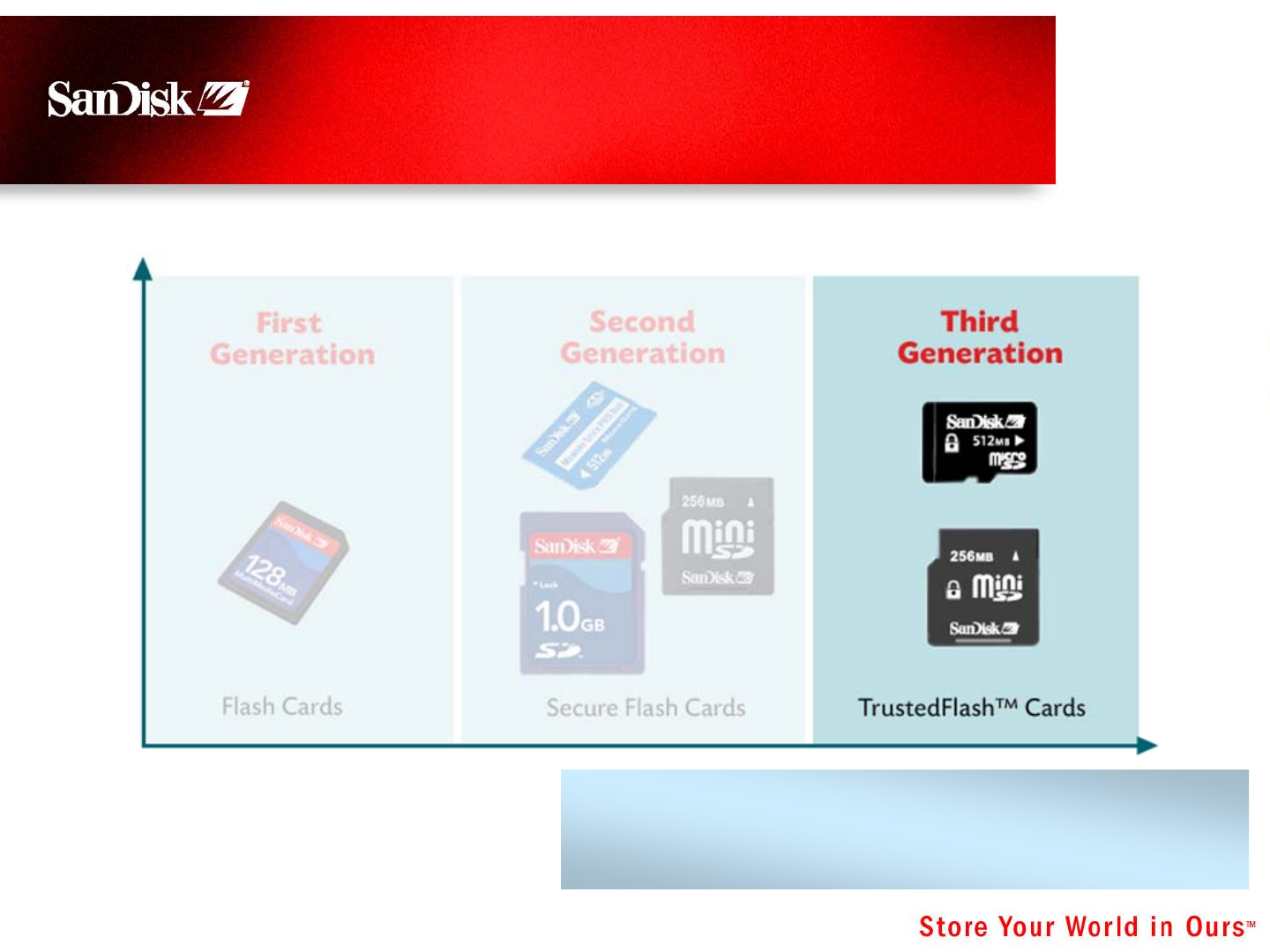

Third Generation Flash Cards

TrustedFlashTM Technology

Accelerating Consumption of Storage/Capacity

9Card-Based Content Protection and

Digital Rights Management (DRM) Solution

9State-of-Art Security Architecture

49 February 23, 2006

Mobile Content TAM

Projected for 2007

Source: Arc Group, IDC, iSuppli, Strategy Analytics, Gartner

Content Goes Mobile

TrustedFlash Technology

Portability

Ease of Use

Flexibility

Increased Security

Music – $ 9B

Games – $ 5B

Video – $ 10B

50 February 23, 2006

Mobile User Authentication

(Dual-Factor Authentication)

TrustedFlash Technology

Mobile Enterprise

Authenticate employees to provide

VPN access

No key fob required

Mobile and PC Banking

Authenticate users to banks for

secure access through PC and mobile

No dedicated token required

e-Commerce

Authenticate buyers to merchants for

both mobile and PC e-commerce

Credentials are stored in

card tamper-resistant area

* Source: Diversinet, 2005

On-Line Users:*

2005 270M

2010 1B

51 February 23, 2006

TrustedFlash Value

Proposition

Consumer: Can Own Content and Play on Multiple

Devices

Content Owner/Distributor: Content Safely Stored

on Card

MNO: Consumers can Seamlessly Upgrade

Handsets

Handset Manufacturer: No Need to Design-in

Costly Security and Tamper Resistance – Zero

Liability for Content Protection

TM

52 February 23, 2006

CTIA Innovative Product 2005

CES Innovations 2006

Disney’s Best of CES 2006

Demonstrating power

of TrustedFlash technology

TrustedFlash Technology in a Card

TM

53 February 23, 2006

54 million K-12 Students in

the US

17 Million College Students

Need for Simple, Portable

Distribution of Textbooks and

Classroom Materials

Positive Feedback from

Several Beta Sites

Evaluating Cruzer Freedom

Education

TrustedFlash Technology

Judy Bruner

EVP and CFO

56 February 23, 2006

Agenda

Financial Review

Modeling our Future Success

Revenue drivers

Fab capacity and investments

Gross margin factors

Target Financial Model

57 February 23, 2006

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Revenue Growth

2002 2003

----$1.08B----

----$541M----

----$1.78B----

2004

License/

Royalty

Product

2005

-----$2.3B-----

58 February 23, 2006

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2002 2003

$ in Millions

-----$97M-----

----$48M------

-----$174M-----

2004 2005

IP Leadership: License

and Royalty Revenue

-----$239M-----

59 February 23, 2006

Consistent Gross Margins

44%

40%

37%

34%

42%

40%

38% 40%

36%

41%

37%

41%

44%

42%

34%

32%

35%

32%

34%

29%

32% 35%

37%

36%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Q103

Q203

Q303

Q403

Q104

Q204

Q304

Q404

Q105

Q205

Q305

Q405

Total GM% Product GM%

60 February 23, 2006

Excellent Gross Margin in 2005

Reflects 90nm Cost Structure & Effective Fab 3

Transition

42.2%

35.5%

38.6%

40.6%

34.9%

31.9%

34.7%

28.5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

2002 2003 2004 2005

Total GM% Product GM%

61 February 23, 2006

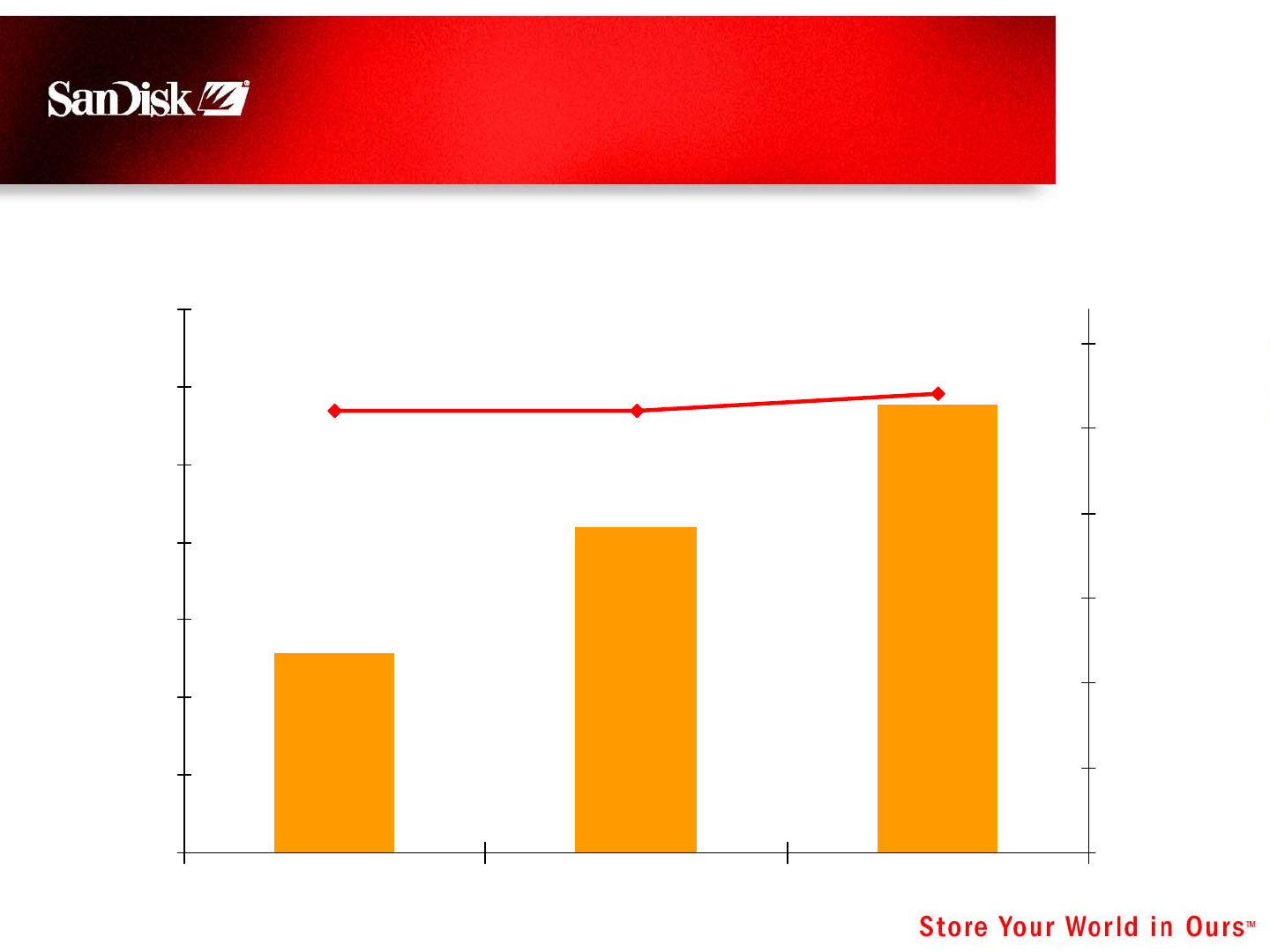

2005 Record Operating

Income and Margin

13 Consecutive Quarters 20%+

$0

$100

$200

$300

$400

$500

$600

$700

2003 2004 2005

-2%

3%

8%

13%

18%

23%

28%

$ in

Millions % of

Revenue

$257

$419

24% 24%

25%

$577

62 February 23, 2006

EPS $2.00, Up 39% Y/Y

$0.00

$1.00

$2.00

$ per

Share

2003 2004 2005

$1.02

$1.44

$2.00

63 February 23, 2006

Strong Balance Sheet

Focus area for reduced

cycle time & increased

flexibility

Cash up $375M Y/Y

January 1, 2006

$ millions

Cash & Short-term investments 1,698

Accounts Receivable (DSO = 44) 329

Inventory (Turns = 5.4) 332

Other current assets 217

Total Current Assets 2,576

PP&E 211

Note Receivable, FlashVision 62

Investment in FlashVision 161

Investment in Flash Partners 42

Other non-current assets 68

Total Assets 3,120

Current Liabilities 571

Non-current Liabilities 25

Total Liabilities 596

Stockholders' Equity 2,524

Total Liabilities & Stockholders' Equity 3,120

Operating Lease Guarantees - Fabs 278

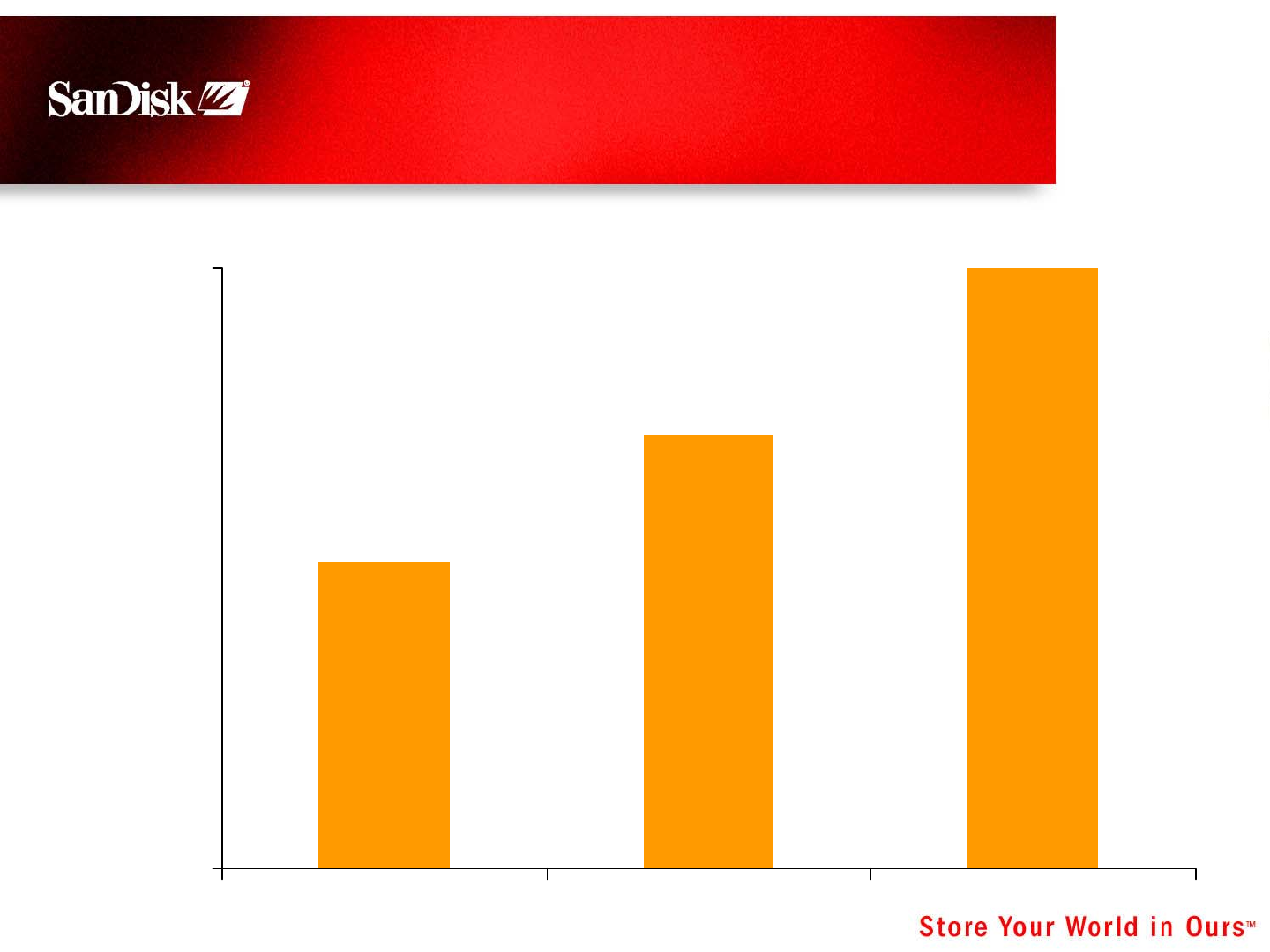

64 February 23, 2006

Significant Cash Flow

From Operations

$0

$100

$200

$300

$400

$500

$600

$ Millions

2003 2004 2005

$273

$228

$481

65 February 23, 2006

Revenue per Employee

Increasing Productivity

599

751

876

1083

0

200

400

600

800

1000

1200

2002 2003 2004 2005

Headcount

0

0.5

1

1.5

2

2.5

3

3.5

$ millions

Ending headcount Revenue $ per Employee

$1.6M

$2.2M

$2.4M

66 February 23, 2006

Modeling our Future Success

Revenue Drivers

Markets

Elasticity

TB growth and pricing

Fab Capacity and Investment

Gross Margin Factors

67 February 23, 2006

Revenue Base Diversifying

End Markets as a % of Revenue

2003 2004 2005

Imaging 75% 65% 52%

USB 3% 13% 12%

Mobile Handset 4% 6% 13%

Digital Audio - 1% 6%

Gaming - - 3%

Other Products 9% 5% 4%

License and Royalty 9% 10% 10%

68 February 23, 2006

Portfolio of Markets at Different Stages

Terabyte Growth by End Market

2003 2004 2005

Imaging 226% 130% 119%

USB 1178% 909% 142%

Mobile Handset Year 1 316% 916%

Digital Audio Year 1 791%

Gaming Year 1

Industrial/Other 146% 24% -16%

Total 238% 167% 166%

69 February 23, 2006

Strong Elasticity

Retail Capacity vs. Price per MB

(40%)

(30%)

(20%)

(10%)

0%

10%

20%

30%

40%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

% Quarterly

Change Average Retail Capacity per Card

Price per MB

Retail Channel Only

2002 2003 2004

+8%

-13%

2005

70 February 23, 2006

Elasticity

Capacity & Unit Growth ÆMB’s Sold

(40%)

(20%)

0%

20%

40%

60%

80%

100%

120%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Megabytes Sold

Price per MB

2002 2003

% Quarterly

Change

2004 2005

All Channels

Seasonality also a factor

71 February 23, 2006

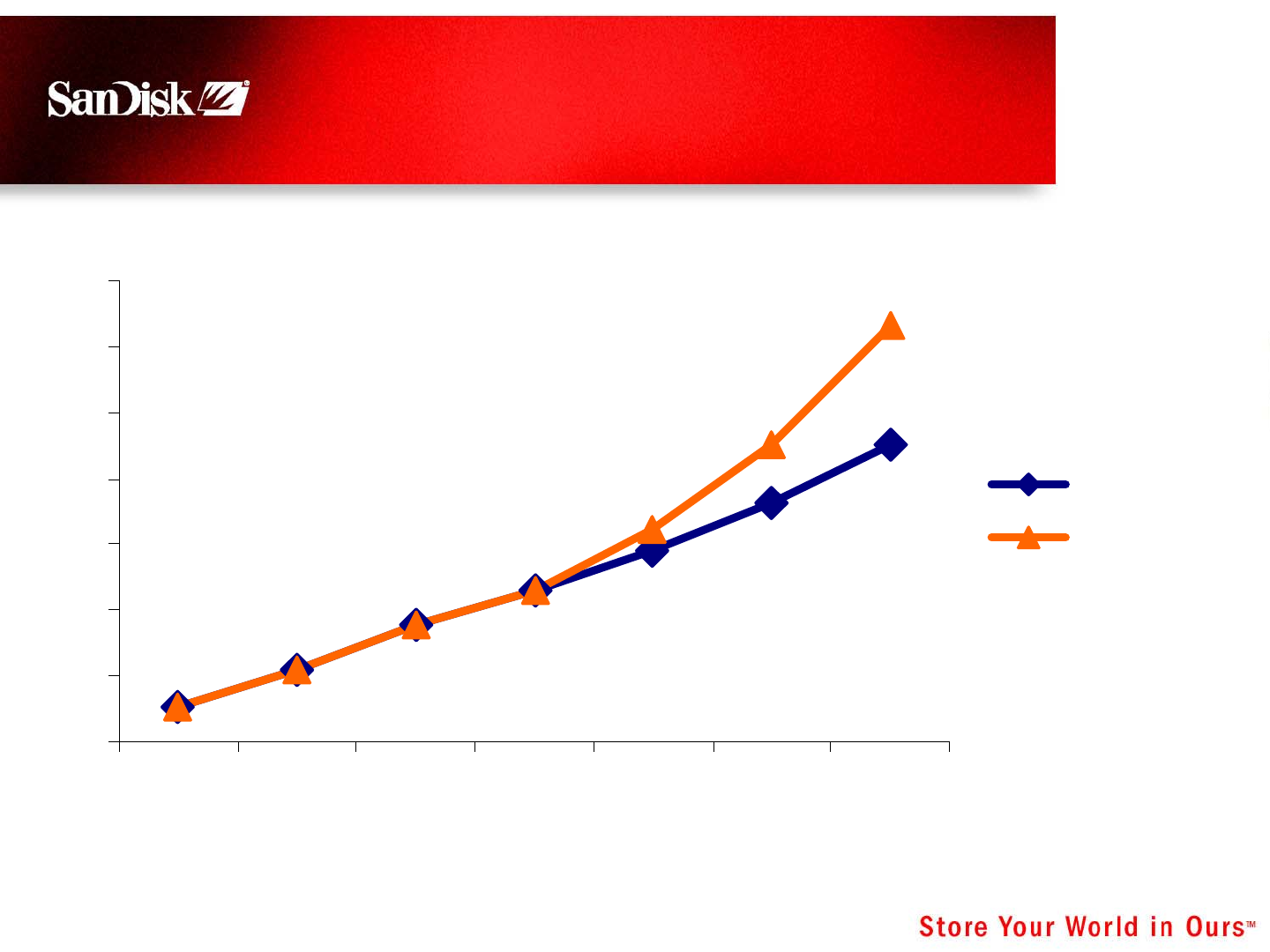

TB Growth Forecasted to Accelerate in 2006

Fueled by Fab 3 Supply, Market Demand

2001 2002 2003 2004 2005 2006

Terabytes Sold

ASP per MB

Terabytes Sold ASP per MB

+233% +238%

+167%

+166%

+180-190%

72 February 23, 2006

Revenue Growth Forecast

Actual Actual Projected What we said last year

2002 - 2005 2005 2005 - 2008 for 2004 - 2007

CAGR Growth CAGR CAGR

Terabyte Growth 189% 166% 130 - 170% 100 - 150%

ASP per MB Decline 44% 52% 40 - 50% 35 - 45%

Total SNDK Revenue Growth * 62% 30% 25 - 40% 25 - 35%

* Projected Revenue CAGR includes NAND Products, License & Royalty and 3D Products

73 February 23, 2006

More on Revenue Growth

Revenue Revenue Revenue

2005 2006 CAGR

Nand Products $2067M MB +180-190% ~ 25% - 40% 2005 - 2008

ASP/MB -(50-55%)

3D Products * $60 - 90M ~ 50% - 75% 2006 - 2008

License & Royalty $239M ~$350M ~ 30% - 40% 2005 - 2008

Total $2306M ~ 25% - 40% 2005 - 2008

* 2005 3D Revenue not included in SNDK

74 February 23, 2006

Planning for Fab Capacity and

Capital Investment

TB Growth CAGR 2005 - 2008

130% Fab “4” needed 1st H 2009

150% Fab “4” needed 2nd H 2008

170% Fab “4” needed 1st H 2008

All Scenarios Assume 70% Captive/30% Non-captive Model

75 February 23, 2006

2005 SanDisk Fab Investment

Significant Funding from FP Working Capital

Analyst Day

($ in millions) Last Year

Actual 2005 Forecast 2005

Capital Investment

Flash Partners 519 470

FlashVision 90 80

SNDK owned Equipment at FlashVision 39 50

Total Capital Investment 648 600

Payment

SNDK Cash 95 360

FP/FV Working Capital 328

Operating Leases - Flash Partners 225 240

648 600

Impact on SNDK Balance Sheet

Investment & Notes Receivable - Flash Partners 22 230

Investment & Notes Receivable - FlashVision 34 80

Capital Equipment 39 50

95 360

End of Year Operating Lease Guarantee

Flash Partners 203

FlashVision 75

Total Operating Lease Guarantee 278

76 February 23, 2006

Fab 3 Investment

2006 Investment Reflects Accelerated Ramp

Cumulative Last Years'

Forecast Forecast

($ in millions) Actual Actual Committed thru thru

2004 2005 2006 2006 2006

Gross SNDK Capital Investment 23 519 1,200 1,742 (1) 1,253

Less: Flash Partners Working Capital 0 (272) (200) (472) (2) (100)

Net SNDK Investment 23 247 1,000 1,270 1,153

Source of Funding - Net Investment Forecast

SNDK Cash Investment in FP 23 22 500 545 563

Operating Leases/Other Financing 0 225 500 725 590

23 247 1,000 1,270 1,153

Source of Funding - Total Investment

Funding by SNDK Cash or FP Working Capital 23 294 700 1,017 58% 663 53%

Funding by Leases or Other Financing 0 225 500 725 42% 590 47%

Total SNDK Capital Investment 23 519 1,200 1,742 1,253

(1) Capital Investment by SNDK up from last year's forecast due to acceleration of Fab 3 expansion

to 70,000 wafers/month (SNDK's share 50%) expected by March 2007, up from 48,750 w/m

(2) Flash Partners working capital contributions greater than previously forecasted

This is SanDisk's share of FP working capital

77 February 23, 2006

Potential Future Fab & Capex Investment

($ in millions) Actual Actual Forecast

Capital Investments 2004 2005 2006 2007 2008 5 YrTotal

FlashVision Investment 33 91 124

Fab 3 Investment 23 519 1,200 1,100 700 3,542

Potential Fab "4" Investment 400 1,200 1,600

Total Gross SNDK Fab Venture Investment 56 610 1,200 1,500 1,900 5,266

SNDK owned fab equipment- FV 63 39 102

Non-Fab Capex Investment 63 95 200 300 500 1,158

Total SNDK Capex Investments 126 134 200 300 500 1,260

Total SNDK Capital Investments (Fab & Capex) 182 744 1,400 1,800 2,400 6,526

Funding

Fab Ventures Working Capital 328 200 350 450 1,328

Committed Operating Leases * 225 150 375

SanDisk Cash spent 182 191

Remaining Funding Required 0 0 1,050 1,450 1,950 4,823

* Committed Operating Leases = SanDisk's 50% share of 85B Yen

Potential

Assumes Fab 3 at capacity of 100K w/m by end of 2007

78 February 23, 2006

Fab and Capex Financing Strategy

Potential Expansion Suggests Funding Requirement of

Approximately $4.8B for 2006-2008

Strategy Remains 50% Cash and 50% Other Financing

50% Cash Funding

Cash flow from operations a significant source

Maintain minimum cash balance of $1B

50% Other Financing

Diversification of funding sources & maturities

Operating lease financing remains high priority −attractive

cost of capital

79 February 23, 2006

Fab 3 ROI

Return = Gross Margin Delta of Captive vs. Non-captive,

After Tax

Investment = Capital Provided to Flash Partners

Projections Analyzed Through 2010

Pricing Assumed to Follow Forecasted Cost Reduction

No Industry Downturn Factored In

ROI

0% operating leases ~35% ROI

25% operating leases ~50% ROI

50% operating leases ~90% ROI

80 February 23, 2006

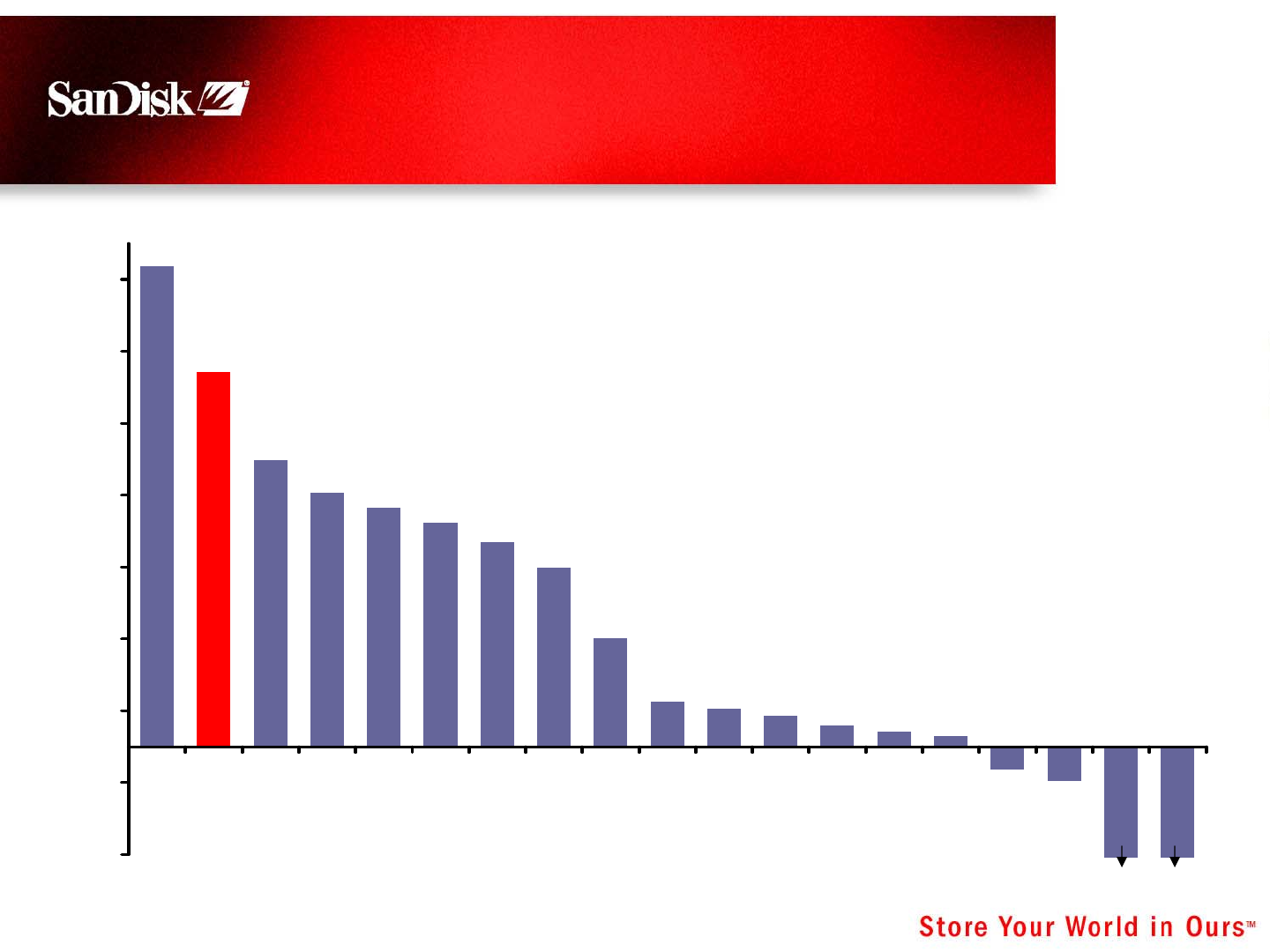

SanDisk Producing Strong ROIC

-15%

-5%

5%

15%

25%

35%

45%

55%

65%

NVIDIA

SanDisk

QualComm

M-Systems

Motorola

Broadcom

TI

Intel

Xilinx

AMD

Rambus

ARM

ST-Micro

Kodak

Micron

Infineon

Cypress

Silicon Storage

Lexar

ROIC

ROIC Last Four Quarters

81 February 23, 2006

Key Gross Margin Drivers

Technology Transitions

300mm vs. 200mm Wafer Mix

Captive vs. Non-Captive Mix

Fab Start-up Costs & Fab Ramp-Up

Non-memory Cost Reduction

Average Capacity of Card Sales

Product Line Mix

ASP/MB converging for leading form factors

Flash memory as % of BOM

MP3 devices – lower margin %, higher margin $

82 February 23, 2006

Captive & Non-Captive Gross Margins

2003 2004 2005

Captive Gross Margin ~40% ~42% ~45%

Non-Captive Gross Margin ~19% ~13% ~18%

Non-Captive Mix 26% 35% 35%

License/Royalty GM Contribution 6% 7% 7%

Total Gross Margin 41% 39% 42%

83 February 23, 2006

Planning for Strong Growth

No Industry Downturn Assumed

0

1

2

3

4

5

6

7

2002 2003 2004 2005 2006 2007 2008

Revenue $ in billions

25% CAGR

40% CAGR

84 February 23, 2006

Scaling the Infrastructure

Requires Targeted Investments

Investing in Systems

Application upgrades/replacements

Automation of manual processes

Network speed, redundancy, security

Organization

Raising the bar

International

Design centers, fab operations, local sales support

Process Re-engineering & Cycle Time Reduction

Supply chain – assembly & test

Customer fulfillment

Etc.

85 February 23, 2006

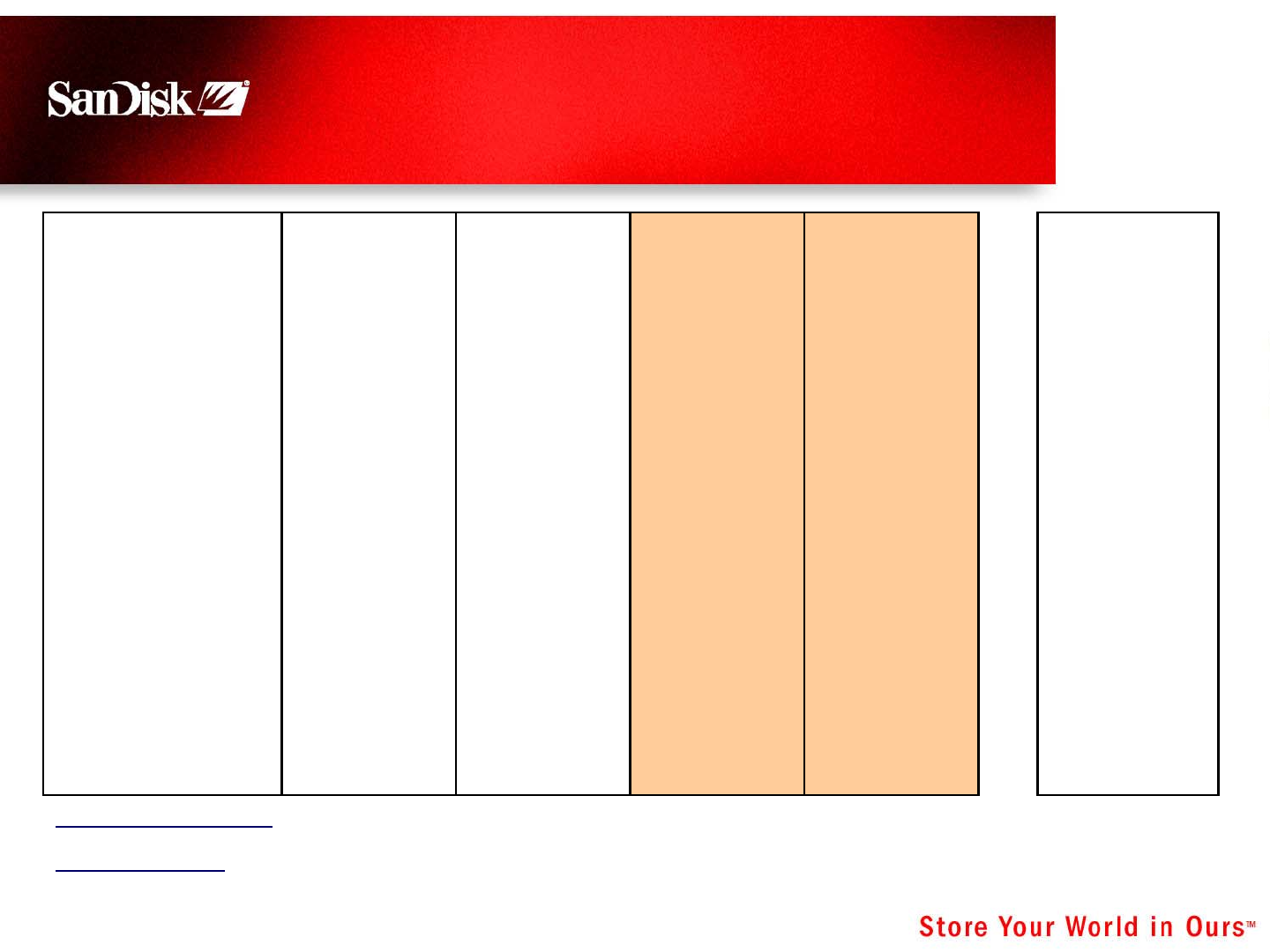

Target Financial Model – Non-GAAP

Non-GAAP excludes: stock compensation and acquisition related charges for in-process R&D and amortization of intangibles

Reconciliation to ‘GAAP Target Model for 2006-2008’ and ‘GAAP Guidance for 2006’ included in Appendix

Non-GAAP Non-GAAP Last Years'

A

nnual

A

nnual Target

Target Model Guidance Model

2004 2005 2006 - 2008 2006 2005 - 2007

Revenue $1,777M $2,306M

Revenue Growth 65% 30% 25 - 40% CAGR 25 - 35% CAGR

Total Gross Margin 38.6% 42.2% 35 - 42% 39 - 42% 35 - 40%

R&D 7.0% 8.4% 7 - 9% 7 - 9%

S&M 5.1% 5.3% 5 - 6% 5 - 6%

G&A 2.9% 3.4% 3 - 4% 3%

Oper Expenses 15.0% 17.2% 15 - 18% 17 - 18% 15 - 18%

Oper Income 23.6% 25.0% 20 - 24% 22 - 24% 20 - 24%

Tax Rate 37% 37% 35%

86 February 23, 2006

Stock Compensation Strategy

End of % of Shares

(in millions)

2005 Outstanding

Shares Outstanding 188.2

Incentives Issued 2005 - gross 6.5 3.4%

Incentives Issued 2005 - net 5.7 3.0%

Stock Incentives Outstanding 20.4 11%

2006

Reduced size of new hire and annual grants; believe

market is doing the same

Given significant growth in new hires, including

Matrix, expect incentive issuance to remain at

approximately 3-3.5%

See Appendix for estimated impact on GAAP results

87 February 23, 2006

Growth & Profitability

Last Four Quarters

QCOM

INTC

XLNX

ALTR

TXN

MU

BRCM

STM

RMBS

ARM

EK

SNDK

AMD

CY

IFX

SSTI

NVDA

FLSH

-20%

-10%

0%

10%

20%

30%

40%

50%

-20% -10% 0% 10% 20% 30% 40% 50% 60%

Y-o-Y Revenue Growth

Operating Margin

88 February 23, 2006

Summary

Attractive and Consistent Business Model

Fab Investments Providing Strong Returns

Planning for Projected Growth

Diversifying revenue base

Diversification of funding sources

Scaling the infrastructure

Appendix

90 February 23, 2006

GAAP Financial Guidance −2006

Non-GAAP

A

djustments GAAP

Total Gross Margin 39% - 42% 1%

(1)

38% - 41%

Operating Expenses 17% - 18% $145 - $175

(2)

21% - 24%

Operating Margin 22% - 24% 5% - 7%

(3)

15% - 19%

Tax Rate 35% >35%

(4)

(4)

Effective GAAP tax rate will reflect the non-deductibility of in-process R&D and incentive stock option expense

2006

(1)

Estimate of stock compensation & acquisition related intangible amortization to be included in cost of sales

(2)

Includes stock compensation of approximately $100 million, in-process research and development of $30 to $50

million related to the Matrix acquisition and amortizaton of acquisition related intangibles of $15 - 25 million

(3)

Reflects estimate of impact on operating margin of stock compensation, in-process R&D and amortization of

acquisition related intangibles expected in cost of sales and operating expenses

91 February 23, 2006

GAAP Target Model

Non-GAAP

A

djustments GAAP

Total Gross Margin 35% - 42% 1%

(1)

34% - 41%

Operating Expenses 15% - 18% 4% - 6%

(2)

19% - 24%

Operating Margin 20% - 24% 5% - 7%

(3)

13% - 19%

Annual Target Model 2006 - 2008

(1)

Estimate of stock compensation & acquisition related intangible amortization to be included in cost of

sales

(2)

Includes stock compensation, acquisition related in-process research and development, and

amortizaton of acquisition related intangibles

(3)

Reflects estimate of impact on operating margin of stock compensation, in-process R&D and

amortization of acquisition related intangibles expected in cost of sales and operating expenses

Q&A

93 February 23, 2006

3-5 Year Outlook

Flash Markets Expected to Grow

3X-4X (>$30B). In Five Years,

Primarily Handsets and CE

Investing to Meet Market

Challenges and Growth

Opportunities to Become

Consumer Branded Powerhouse

in Next Five Years

Uniquely Positioned to Meet

Competition Challenges and

Capitalize on Massive Global

Consumerism in Coming Decade

Creating Shareholder Value

SanDisk, the SanDisk logo, Store Your World in Ours, Cruzer,

SanDisk Extreme and SanDisk Ultra are trademarks of

SanDisk Corporation, registered in the United States and other

countries. Cruzer Crossfire, gruvi, the gruvi logo, Sansa, and

Shoot & Store are trademarks of SanDisk Corporation.

SanDisk Corporation is an authorized licensee of SD. The

PlaysForSure logo is a trademark or registered trademark of

Microsoft Corporation in the United States and/or other

countries. Memory Stick PRO Duo is a trademark of Sony

Corporation. PSP and PlayStation are registered trademarks

or trademarks of Sony Computer Entertainment, Inc. (SCEI).

Skype and the Skype logo are trademarks of Skype

Technologies S.A. U3 and the U3 smart logo are trademarks

of U3, LLC.

Other brand names mentioned herein are for identification

purposes only and may be trademarks of their respective

holder(s).

© 2006 SanDisk Corporation. All rights reserved.