FOREIGN EXCHANGE DEPARTMENT Master Circular On Memorandum Of Instructions Governing Money Changing Activities

User Manual:

Open the PDF directly: View PDF ![]() .

.

Page Count: 80

RBI/2013-14/10

Master Circular No. 10/2013-14 July 01, 2013

To,

All Authorised Persons in Foreign Exchange

Madam / Sir,

Master Circular on Memorandum of Instructions

governing money changing activities

This Master Circular consolidates the existing instructions on the subject of

“Memorandum of Instructions governing money changing activities” at one place.

The list of underlying circulars/ notifications is set out in Appendix.

2. This Master Circular is being issued with a sunset clause. It will stand withdrawn

on July 1, 2014 and would be replaced by an updated Master Circular on the

subject.

Yours faithfully,

(Rudra Narayan Kar)

Chief General Manager-in-Charge

INDEX

SECTION-I..............................................................................................................................2

Guidelines for Licencing and other Approvals for Authorised Money Changers (AMCs)....2

SECTION II .............................................................................................................................7

Guidelines for Grant of Authorisation for Additional Branches :-.........................................7

SECTION III ..........................................................................................................................10

Guidelines for appointment of Agents / Franchisees by Authorized Dealer Category – I

Banks, Authorized Dealers Category - II and FFMCs :-....................................................10

SECTION IV..........................................................................................................................15

Guidelines for Renewal of licences of existing FFMCs :...................................................15

SECTION V...........................................................................................................................16

Operational Instructions ....................................................................................................16

SECTION VI..........................................................................................................................27

KYC/ AML/ CFT Guidelines ..............................................................................................27

SECTION VII.........................................................................................................................28

Revocation of Licence....................................................................................................28

SECTION VIII........................................................................................................................29

‘Fit and proper’ criteria for directors of FFMCs / non-bank ADs Category - II ...................29

Annex-I..................................................................................................................................32

KYC / AML / CFT Guidelines for money changing activities .............................................32

Annex-II.................................................................................................................................61

Application Form for FFMC licence under section 10(1) of FEMA, 1999..........................61

Annex-III................................................................................................................................63

Form RMC-F .....................................................................................................................63

Annex-IV ...............................................................................................................................64

FLM 1................................................................................................................................64

Annex-V ................................................................................................................................65

FLM 2................................................................................................................................65

Annex-VI ...............................................................................................................................66

FLM 3................................................................................................................................66

Annex-VII ..............................................................................................................................67

FLM 4................................................................................................................................67

Annex-VIII .............................................................................................................................68

FLM 5................................................................................................................................68

Annex-IX ...............................................................................................................................69

FLM 6................................................................................................................................69

Annex-X ................................................................................................................................70

FLM 7................................................................................................................................70

Annex- XI ..............................................................................................................................71

FLM 8................................................................................................................................71

Annex- XII .............................................................................................................................75

Statement of Purchase transactions of USD 10,000 and above.......................................75

Annex- XIII ............................................................................................................................76

Statement showing summation of Foreign Currency Account opened in India out of export

proceeds of Foreign Currency Notes/ encashed Travellers' Cheques..............................76

Annex- XIV............................................................................................................................77

Statement of the amount of foreign currency written off during the financial year ............77

Appendix ...............................................................................................................................78

1

SECTION-I

Guidelines for Licencing and other Approvals for Authorised Money Changers

(AMCs)

1. Introduction

Authorised Money Changers (AMCs) are entities, authorised by the Reserve Bank

under Section 10 of the Foreign Exchange Management Act, 1999. An AMC is a Full

Fledged Money Changer (FFMC). In addition to Authorised Dealer Category -I

Banks (AD Category–I Banks) and Authorised Dealers Category - II (ADs Category–

II), Full Fledged Money Changers (FFMCs) are authorised by the Reserve Bank to

deal in foreign exchange for specified purposes, to widen the access of foreign

exchange facilities to residents and tourists while ensuring efficient customer service

through competition. FFMCs are authorised to purchase foreign exchange from

residents and non-residents visiting India and to sell foreign exchange for certain

approved purposes. AD Category –I Banks / ADs Category – II / FFMCs may

appoint franchisees to undertake purchase of foreign currency*. No person shall

carry on or advertise that he carries on money changing business unless he is in

possession of a valid money changer’s licence issued by the Reserve Bank. Any

person found undertaking money changing business without a valid licence is liable

to be penalised under the Act ibid.

* Note :- Franchisees of AD Category –I Banks / ADs Category – II / FFMCs

functioning within 10 kms from the borders of Pakistan and Bangladesh may

also sell the currency of the bordering country, with the prior approval of the

Regional offices concerned of the Reserve Bank. Other franchises of AD

Category –I Banks / ADs Category – II / FFMCs cannot sell foreign currency.

2. Guidelines for issuance of FFMC Licence :-

The guidelines for issue of new FFMC licence and renewal of FFMC licence, branch

licensing, approval for appointment of agents / franchisees and Know Your

2

Customer (KYC) / Anti Money Laundering (AML) / Combating the Financing of

Terrorism (CFT) Guidelines for Authorised Persons are given below.

(i) Entry Norms

(i) The applicant has to be a company registered under the Companies

Act, 1956.

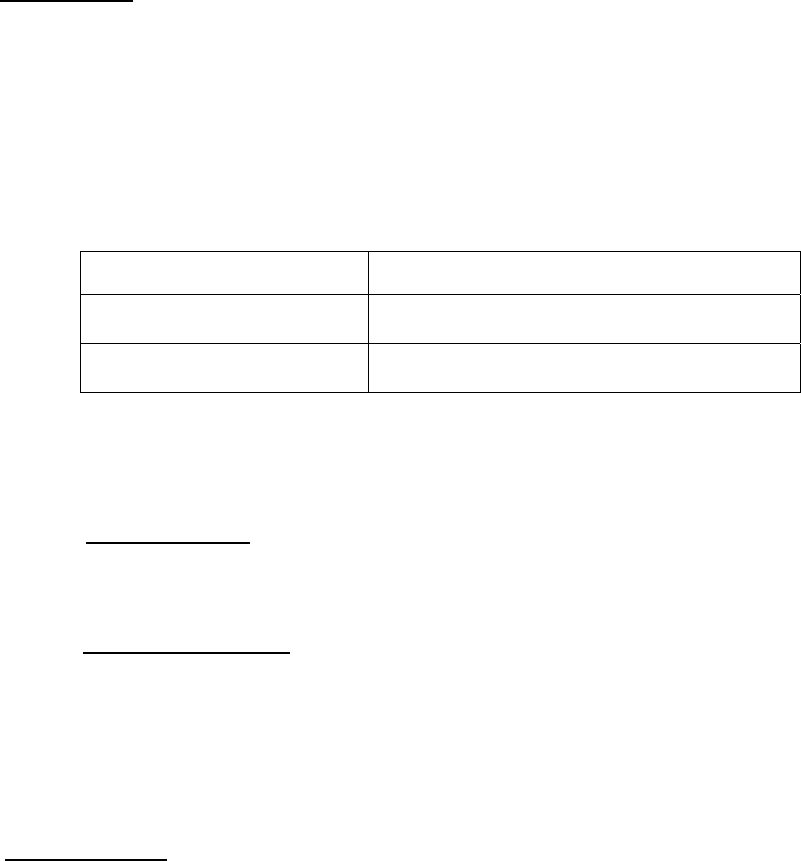

(ii) The minimum Net Owned Funds (NOF) required for consideration as

FFMC are as follows:

Category Minimum Net Owned Funds

Single branch FFMC Rs.25 lakh

Multiple branch FFMC Rs.50 lakh

Note :- The Net Owned Funds of applicants, other than banks, should be

calculated as per the following.

(a) Owned Funds :- (Paid-up Equity Capital + Free reserves + Credit

balance in Profit & Loss A/c) minus (Accumulated balance of loss,

Deferred revenue expenditure and Other intangible assets)

(b) Net Owned Funds :- Owned funds minus the amount of investments

in shares of its subsidiaries, companies in the same group, all (other)

non-banking financial companies as also the book value of debentures,

bonds, outstanding loans and advances made to and deposits with its

subsidiaries and companies in the same group in excess of 10 per cent

of the Owned funds.

(ii) Documentation

Application in the form, as at Annex - II, should be submitted to the respective

Regional Office of the Foreign Exchange Department of the Reserve Bank under

whose jurisdiction the registered office of the applicant falls, along with the following

documents:

(a) Copy each of the Certificate of Incorporation and Certificate of

Commencement of Business of the company.

3

(b) Memorandum and Articles of Association containing a provision for

undertaking money changing business or an appropriate amendment

to this effect filed with the Company Law Board.

(c) Copy of the latest audited accounts with a certificate from the Statutory

Auditors certifying the Net Owned Funds as on the date of application.

Copies of the audited Balance Sheet and Profit & Loss Account of the

company for the last three years, wherever applicable.

(d) Confidential Report from the applicant's banker in a sealed cover.

(e) A declaration to the effect that no proceedings have been initiated by /

are pending with the Directorate of Enforcement (DoE) / Directorate of

Revenue Intelligence (DRI) or any other law enforcing authorities,

against the applicant company or its directors and that no criminal

cases are initiated / pending against the applicant company or its

directors.

(f) A declaration to the effect that proper policy framework on KYC / AML /

CFT, in accordance with the guidelines issued vide A.P.(DIR Series)

Circular No. 17[ A.P.(FL/RL Series) Circular No. 04] dated November

27, 2009, as amended from time to time, will be put in place on

obtaining the approval of the Reserve Bank and before

commencement of operations.

(g) Details of sister / associated concerns operating in the financial sector,

like NBFCs, etc.

(h) A certified copy of the board resolution for undertaking money

changing business.

(iii) Basis for Approval

(i) Since several FFMCs are already functioning, fresh licences will be

issued on a selective basis to those who comply with all the licencing

requirements.

4

(ii) 'Fit and proper' criteria for the applicant FFMCs #

If any case by DoE / DRI or any other case by any other law enforcing

authorities, is initiated / pending against any company / its directors,

the company will not be considered as 'fit and proper' and its

application will not be considered for licencing as FFMC.

(# Also applicable to non-bank ADs Category - II)

(iii) ‘Fit and proper’ criteria for directors of FFMCs *

Please see SECTION- VIII for the details in this regard.

(* Also applicable to non-bank ADs Category - II)

(iv) Clearance by the Empowered Committee

The request for issuance of FFMC licence would be considered by the

Regional Office concerned of the Reserve Bank on the basis of the

clearance by an Empowered Committee, set up for the purpose.

(v) Reserve Bank’s decision in the matter of granting approval or

otherwise will be final and binding.

(vi) On obtaining approval from the Reserve Bank, a copy of the

registration under Shops & Establishment Act or any other

documentary evidence such as rent receipt, copy of lease agreement,

etc. should be submitted to the Regional Office concerned of the

Reserve Bank before commencement of the business.

(vii) The FFMC should commence its operations within a period of six

months from the date of issuance of licence and inform the Regional

Office concerned of the Reserve Bank.

5

(viii) New FFMCs should carry out their activities as per the instructions

specified in SECTIONS V and VI below and other instructions issued

by the Reserve Bank from time to time.

[Note:- Urban Cooperative Banks (UCBs), fulfilling the eligibility norms,

would be considered for authorization as Authorised Dealer Category-I /

Authorised Dealer Category-II only.]

6

SECTION II

Guidelines for Grant of Authorisation for Additional Branches :-

1. No FFMC shall carry on money changing business at any additional place of

business other than its permanent place of business except with the prior approval

of the Reserve Bank. An FFMC which intends to commence money changing

business at any additional place of business shall apply in writing to the respective

Regional Office of the Foreign Exchange Department under whose jurisdiction the

registered office of the applicant falls and the Reserve Bank may approve the

additional place of business subject to such conditions as deem fit. It is expected

that branches of Authorised Persons should be diversified and should be meeting

the demand of tourists,etc. Preference will be given to applications for branches in

remote areas of tourist attraction.

2. Applications for additional locations (places of business) should be accompanied

by the following:-

(a) Copy of the latest audited accounts with a certificate from the Statutory

Auditors regarding the position of Net Owned Funds as on the date of

application.

(b) Confidential Report from the applicant's banker in a sealed cover.

(c) A declaration to the effect that no proceedings have been initiated by /

are pending at the Directorate of Enforcement (DoE) / Directorate of

Revenue Intelligence (DRI) or any other law enforcing authorities

against the applicant or its directors and that no criminal cases are

initiated / pending against the applicant or its directors. No new branch

license will be issued to any FFMC, against whom any major DoE /

DRI case is pending. In DoE / DRI pending cases of a minor nature, a

7

decision will be taken by the Reserve Bank on a case by case basis.

The categorization of pending DoE / DRI cases as major / minor will be

at the discretion of the Reserve Bank and the decision of the Reserve

Bank will be final and binding. Where any DoE / DRI case is

adjudicated and penalty is imposed, a view will be taken, on the basis

of the nature of the offence, provided no fresh case is instituted by DoE

/ DRI.

(d) A copy of the KYC / AML/ CFT policy framework existing in the

company.

(e) Brief write-up on the internal control systems, including internal and

external audit.

3. A copy of the registration under Shops & Establishment Act or any other

documentary evidence such as rent receipt, copy of lease agreement, etc. should be

submitted to the Regional Office concerned of the Reserve Bank before

commencement of business at an additional branch.

4. For opening Foreign Exchange Counters (full-fledged branches/ extension

counters) at the international airports in India, AD Category-I banks/ AD Category –

II/ FFMCs should adhere to following conditions.

(a) Foreign Exchange Counters in the arrival halls in international airports in India

shall ideally be established after the Customs Desk (Green Channel/Red

Channel). However, Foreign Exchange Counters may also be established

between the Immigration Desk and the Customs Desk in international airports

in India subject to the condition that these counters shall only purchase

foreign currency and sell Indian Rupees (INR) and "Encashment Certificates"

shall invariable be issued by the money changers to the customers.

(b) Foreign Exchange Counters in the departure halls in international airports in

India shall be established only before the Customs Desk or the immigration

desk, whichever comes first. Putting up suitable display at these counters,

8

reminding the passengers that the area is the last point for non-residents to

possess Indian Rupees (INR) may be followed up with the Airport Authorities.

5. The FFMC should commence operations of its additional branch within a period of

six months from the date of issuance of licence and inform the Regional Office

concerned of the Reserve Bank.

9

SECTION III

Guidelines for appointment of Agents / Franchisees by Authorized Dealer Category

– I Banks, Authorized Dealers Category - II and FFMCs :-

1. Under the Scheme, the Reserve Bank permits AD Category – I Banks, ADs

Category - II and FFMCs to enter into [franchisee (also referred as agency)]

agreements at their option for the purpose of carrying on Restricted Money

Changing business i.e. conversion of foreign currency notes, coins or travellers'

cheques into Indian Rupees.

2. Franchisee

A franchisee can be any entity which has a place of business and a minimum Net

Owned Funds of Rs.10 lakh. Franchisees can undertake only restricted money

changing business.

3. Franchisee Agreement

AD Category-I Banks / ADs Category-II / FFMCs as the franchisers are free to

decide on the tenor of the arrangement as also the commission or fee through

mutual agreement with the franchisee.

The Agency / Franchisee agreement to be entered into should include the following

salient features:

(a) The franchisees should display the names of their franchisers, exchange

rates and that they are authorized only to purchase foreign currency,

prominently in their offices. Exchange Rate for conversion of foreign currency

into Rupees should be the same or close to the daily exchange rate charged

by the AD Category – I Banks / ADs Category - II / FFMC at its branches.

10

(b) The foreign currency purchased by the franchisee should be surrendered only

to its franchiser within 7 working days from the date of purchase.

(c) The maintenance of proper record of transactions by the franchisee.

(d) The on-site inspection of the franchisee by the franchiser should be

conducted at least once a year.

4. Procedure for application

An AD Category – I Bank / AD Category - II/ FFMC should apply to the respective

Regional Office of the Reserve Bank, in Form RMC-F (Annex-III) for appointment of

franchisees under this Scheme. The application should be accompanied by a

declaration that while selecting the franchisees, adequate due diligence has been

carried out and that such entities have undertaken to comply with all the provisions

of the franchising agreement and prevailing Reserve Bank regulations regarding

money changing. Approval would be granted by the Reserve Bank for the first

franchisee arrangement. Thereafter, as and when new franchisee agreements are

entered into, these would have to be reported to the Reserve Bank in Form RMC-F

(Annex-III) on a post-facto basis along with similar declaration as indicated above.

5. Due Diligence of Franchisees

The AD Category Banks – I / ADs Category – II / FFMCs should undertake the

following minimum checks while conducting the due diligence of the franchisees :

• existing business activities of the franchisee/ its position in the area.

• minimum Net Owned Funds of the franchisee.

• Shops & Establishments / other applicable municipal certification in favour

of the franchisee.

• verification of physical existence of location of the franchisee, where

restricted money changing activities will be conducted.

11

• conduct certificate of the franchisee from the local police authorities.

(certified copy of Memorandum and Articles of Association and Certificate

of Incorporation in respect of incorporated entities).

Note: Obtaining of Conduct Certificate of the franchisee from the local police

authorities is optional for the franchisers. However, the franchisers may take

due care to avoid appointing individuals/ entities as franchisees who have

cases / proceedings initiated / pending against them by any law enforcing

agencies.

• declaration regarding past criminal case, if any, cases initiated / pending

against the franchisee or its directors / partners by any law enforcing

agency, if any.

• PAN Card of the franchisee and its directors / partners.

• photographs of the directors / partners and the key persons of franchisee.

The above checks should be done on a regular basis, at least once in a year. The

AD Category – I Banks / ADs Category – II / FFMCs should obtain from the

franchisees proper documentary evidence confirming the location of the franchisees

in addition to personal visits to the site. The AD Category –I Banks / ADs Category –

II / FFMCs should also obtain a Chartered Accountant's certificate confirming the

maintenance of the Net Owned Funds of the franchisee, i.e., ` 10 lakh on an

ongoing basis.

6. Selection of Centers

(i) The AD Category-I banks / AD Category –II / FFMCs may appoint franchisees

within a distance of 100 kms. from their controlling branches concerned.

(ii) However, this distance criterion is exempted in case of a recognized group/

chain of hotels appointed as franchisees, provided the headquarters of the group/

12

chain of hotels falls within a distance of 100 kms. of the controlling branch of the AD

Category – I banks / AD Category – II/ FFMCs (franchiser) concerned.

(iii) Further, in case of areas declared as hilly areas (as defined by the respective

State Governments/ Union Territories) and the North-Eastern States, the distance

restriction given in point (i) above is not applicable.

7. Training

Franchisers are expected to impart training to the franchisees as regards operations

and maintenance of records.

8. Reporting, Audit and Inspection

The franchisers, i.e. the AD Category–I Banks / ADs Category–II / FFMCs, are

expected to put in place adequate arrangements for reporting of transactions by the

franchisees to the franchisers on a regular basis (at least monthly). Regular spot

audits of all locations of franchisees, at least once in six months, should be

conducted by AD Category–I Banks / ADs Category–II / FFMCs. Such audits should

involve a dedicated team and 'mystery customer' (individuals acting as potential

customers to experience and measure the extent up to which people and

process perform as they should) concept should be used to test the compliance

level of the franchisees. A system of annual inspection of the books of the

franchisees should also be put in place. The purpose of such inspection is to ensure

that the money changing business is being carried out by the franchisees in

conformity with the terms of the agreement and prevailing Reserve Bank guidelines

and that necessary records are being maintained by the franchisees.

9. Anti Money Laundering (AML) / Know Your Customer (KYC) / Combating the

Financing of Terrorism (CFT) Guidelines

Franchisees are required to strictly adhere to the AML / KYC/ CFT guidelines, as

applicable to AD Category–I Banks / ADs Category – II / FFMCs.

13

Note:- No licence for appointment of franchisees will be issued to any FFMC /

non-bank AD Category - II, against whom any major DoE / DRI / CBI / Police

case is pending. In case where any FFMC / non-bank AD Category - II has

received one-time approval for appointing franchisees and subsequent to the

date of approval, any DoE / DRI / CBI / Police case is filed, the FFMC / non-

bank AD Category - II should not appoint any further franchisees and bring

the matter to the notice of the Reserve Bank immediately. A decision will be

taken by the Reserve Bank regarding allowing the FFMC / non-bank AD

Category - II to appoint franchisees.

14

SECTION IV

Guidelines for Renewal of licences of existing FFMCs :

1. The applicant should be a company registered under the Companies Act,

1956 having registered office within the area of jurisdiction of the respective

Regional Office of the Foreign Exchange Department.

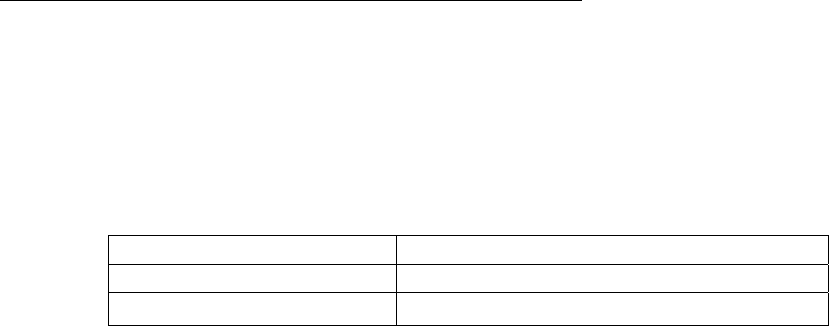

2. The Net Owned Funds required are as follows:

Category Minimum Net Owned Funds

Single branch FFMC Rs..25 lakh

Multiple branch FFMC Rs..50 lakh

3. Applications for renewal should be submitted along with the documents,

mentioned below.

(a) Copy of the latest audited accounts with a certificate from the Statutory

Auditors regarding the position of Net Owned Funds as on date.

(b) Confidential Report from the applicant's banker in a sealed cover.

(c) A declaration to the effect that no proceedings have been initiated by/

are pending with the Directorate of Enforcement / Directorate of

Revenue Intelligence or any other law enforcing authorities against the

applicant company or its directors and that no criminal cases are

initiated/ pending against the applicant company or its directors.

(d) A copy of the KYC / AML / CFT policy framework existing in the

company.

Note :- An application for the renewal of a money-changer’s licence shall be

made not later than one month, or such other period as the Reserve Bank may

prescribe, before the expiry of the licence. Where a person submits an

application for the renewal of his money changer’s licence, the licence shall

continue in force until the date on which the licence is renewed or the

application is rejected, as the case may be. No application for renewal of a

money-changer’s licence shall be made after the expiry of the licence.

15

SECTION V

Operational Instructions

1. Bringing in and taking out of Foreign Exchange

(i) Foreign exchange in any form can be brought into India freely without limit

provided it is declared on the Currency Declaration Form (CDF) on arrival to the

Custom Authorities. When foreign exchange brought in the form of currency notes or

travellers' cheques does not exceed US$ 10,000/- or its equivalent and / or the value

of foreign currency notes does not exceed US$ 5,000/- or its equivalent, declaration

thereof on CDF is not insisted upon.

(ii) Taking out foreign exchange in any form, other than foreign exchange obtained

from an authorized dealer or a money changer is prohibited unless it is covered by a

general or special permission of the Reserve Bank. Non-residents, however, have

general permission to take out an amount not exceeding the amount originally

brought in by them, subject to compliance with the provisions of sub-para (i) above.

2. Purchases of Foreign Currency from Public

(i) Authorised Money Changers (AMCs) / franchisees may freely purchase

foreign currency notes, coins and travellers cheques from residents as well as non-

residents. Where the foreign currency was brought in by declaring on form CDF, the

tenderer should be asked to produce the same. The AMC should invariably insist on

production of declaration in CDF.

(ii) AMCs may sell Indian Rupees to foreign tourists / visitors against

International Credit Cards / 1International Debit Cards and take prompt steps to

obtain reimbursement through normal banking channels.

1 A.P.(DIR Series) Circular No.96 dated 05.04.2013

16

3. Encashment Certificate

(i) AMCs may issue certificate of encashment when asked for in cases of

purchases of foreign currency notes, coins and travellers cheques from residents as

well as non-residents. These certificates bearing authorized signatures should be

issued on the letter head of the money changer and proper record should be

maintained.

(ii) In cases where encashment certificate is not issued, attention of the

customers should be drawn to the fact that unspent local currency held by non-

residents will be allowed to be converted into foreign currency only against

production of a valid encashment certificate.

4. Purchases from other AMCs and Authorized Dealers (ADs)

AMCs may purchase from other AMCs and ADs any foreign currency notes, coins

and encashed travellers’ cheques tendered in the normal course of business. Rupee

equivalent of the amount of foreign exchange purchased should be paid only by way

of crossed account payee cheque/Demand Draft/Bankers' cheque / Pay order.

5. Sale of foreign exchange

(I) Private Visits

AMCs may sell foreign exchange up to the prescribed ceiling (currently US $ 10,000)

specified in Schedule III to the Foreign Exchange Management (Current Account

Transaction) Rules, 2000 during a financial year to persons resident in India for

undertaking one or more private visits to any country abroad (except Nepal and

Bhutan). Exchange for such private visits will be available on a self-declaration basis

to the traveller regarding the amount of foreign exchange availed during a financial

year. Foreign nationals permanently resident in India are also eligible to avail of this

quota for private visits provided the applicant is not availing of facilities for remittance

of his salary, savings, etc., abroad in terms of extant regulations.

17

(II) Business visits

AMCs may sell foreign exchange to persons resident in India for undertaking

business travel or for attending a conference or specialized training or for

maintenance expenses of a patient going abroad for medical treatment or check up

abroad or for accompanying as attendant to a patient going abroad for medical

treatment / check-up up to the limits (currently US $ 25,000 per visit) specified in

Schedule III to FEMA (Current Account Transactions) Rules, 2000.

(III) Forex Pre-paid Cards

Authorised Dealers Category-II may issue forex pre-paid cards to residents travelling

on private/business visit abroad, subject to KYC/AML/CFT requirements. However,

the settlement in respect of forex pre-paid cards may be effected through AD

Category-I banks.

Conditions

i. The Reserve Bank will not generally, prescribe the documents which should be

verified by the AMCs while releasing foreign exchange. In this connection,

attention of AMCs is drawn to sub-section (5) of Section 10 of FEMA, 1999.

ii. In case of issue of travellers’ cheques, the traveler should sign the cheques in

the presence of an authorized official and the purchaser’s acknowledgement for

receipt of the travellers’ cheques should be held on record.

iii. AMCs may release foreign exchange for travel purposes on the basis of a

declaration given by the traveler regarding the amount of foreign exchange

availed of during the financial year.

iv. AMCs may accept payment in cash up to Rs.50,000/- (Rupees fifty thousand

only) against sale of foreign exchange for travel abroad (for private visit or for any

other purpose). Wherever the sale of foreign exchange exceeds the amount

equivalent to Rs.50,000/-, the payment must be received only by a crossed

cheque drawn on the applicant’s bank account or crossed cheque drawn on the

bank account of the firm / company sponsoring the visit of the applicant or

18

Banker’s cheque / Pay Order / Demand Draft. For this purpose, where the Rupee

equivalent of foreign exchange drawn exceeds Rs. 50,000/- either for any single

drawal or more than one drawal reckoned together for a single journey visit, it

should be paid by crossed cheque/ Banker’s cheque / Pay Order / Demand

Draft. In addition to the payment by Rupees/ through crossed cheque/ Banker’s

cheque/ Pay order/ Demand draft, AMCs may also accept the payments made

by the traveller through debit cards/ credit cards/ prepaid cards for travel abroad

(for private visit or for any other purpose) provided- (i) KYC/ AML / CFT

guidelines are complied with, (ii) sale of foreign currency/ issue of foreign

currency travellers’ cheques is within the limits (credit/ prepaid cards) prescribed

by the bank, (iii) the purchaser of foreign currency/ foreign currency travellers’

cheque and the credit/ debit/ prepaid card holder is one and the same person.

v. The sale of foreign currency notes and coins within the overall entitlement of

foreign exchange should be restricted to the limits prescribed by the Reserve

Bank from time to time for the country of visit of the traveller.

6. Sales against Reconversion of Indian Currency

AMCs may convert into foreign currency, unspent Indian currency held by non-

residents at the time of their departure from India, provided a valid Encashment

Certificate is produced.

Note (1) : AMCs may convert at their discretion, unspent Indian currency up to

`.10,000 in the possession of non-residents if, for bonafide reasons, the person is

unable to produce an Encashment Certificate after ensuring that the departure is

scheduled to take place within the following seven days.

Note (2) : ADs Category – I, ADs Category – II and FFMCs may provide facility for

reconversion of Indian Rupees to the extent of Rs.50,000/- to foreign tourists (not

NRIs) against ATM Receipts based on the following documents.

• Valid Passport and VISA

• Ticket confirmed for departure within 7 days.

• Original ATM slip (to be verified with the original debit/ credit card).

19

7. Cash Memo

AMCs may issue a cash memo, if asked for, on official letterhead to travellers to

whom foreign currency is sold by them. The cash memo may be required for

production to emigration authorities while leaving the country.

8. Rates of Exchange

AMCs may put through transactions relating to foreign currency notes and travellers'

cheques at rates of exchange determined by market conditions and in alignment

with the ongoing market rates.

9. Display of Exchange Rate Chart

AMCs should display at a prominent place in or near the public counter, a chart

indicating the rates for purchase/sale of foreign currency notes and travellers'

cheques for all the major currencies and the card rates for any day, should be

updated, latest by 10:30 a.m.

10. Foreign Currency Balances

(i) AMCs should keep balances in foreign currencies at reasonable levels and

avoid build up of idle balances with a view to speculating on currency movements.

(ii) Franchisees should surrender foreign currency notes, coins and travellers'

cheques purchased only to their franchisers within seven working days.

(iii) The transactions between authorized dealers and FFMCs should be settled

by way of account payee crossed cheques / demand drafts. Under no circumstances

should settlement be made in cash.

11. Replenishment of Foreign currency Balances

(i) AMCs may obtain their normal business requirements of foreign currency

notes from other AMCs / authorized dealers in foreign exchange in India, against

payment in rupees made by way of account payee crossed cheque / Demand Draft.

20

(ii) Where AMCs are unable to replenish their stock in this manner, they may

make an application to the Forex Markets Division, Foreign Exchange Department,

Central Office, Reserve Bank of India, Mumbai through an AD Category-I for

permission to import foreign currency into India. The import should take place

through the designated AD Category-I through whom the application is made.

12. Export / Disposal of surplus Foreign Currency Notes / Travellers'

Cheques

AMCs may export surplus foreign currency notes / encashed travellers' cheques to

an overseas bank through designated Authorized Dealer Category - I in foreign

exchange for realization of their value through the latter. FFMCs may also export

surplus foreign currency to private money changers abroad subject to the condition

that either the realizable value is credited in advance to the AD Category – I bank’s

nostro account or a guarantee is issued by an international bank of repute covering

the full value of the foreign currency notes / coins to be exported.

13. Write-off of fake foreign currency notes

In the event of foreign currency notes purchased being found fake/forged

subsequently, AMCs may write- off up to US $ 2000 per financial year after approval

of their Top Management after exhausting all available options for recovery of the

amount. Any write-off in excess of the above amount, would require the approval of

the Regional Office concerned of the Foreign Exchange Department of the Reserve

Bank.

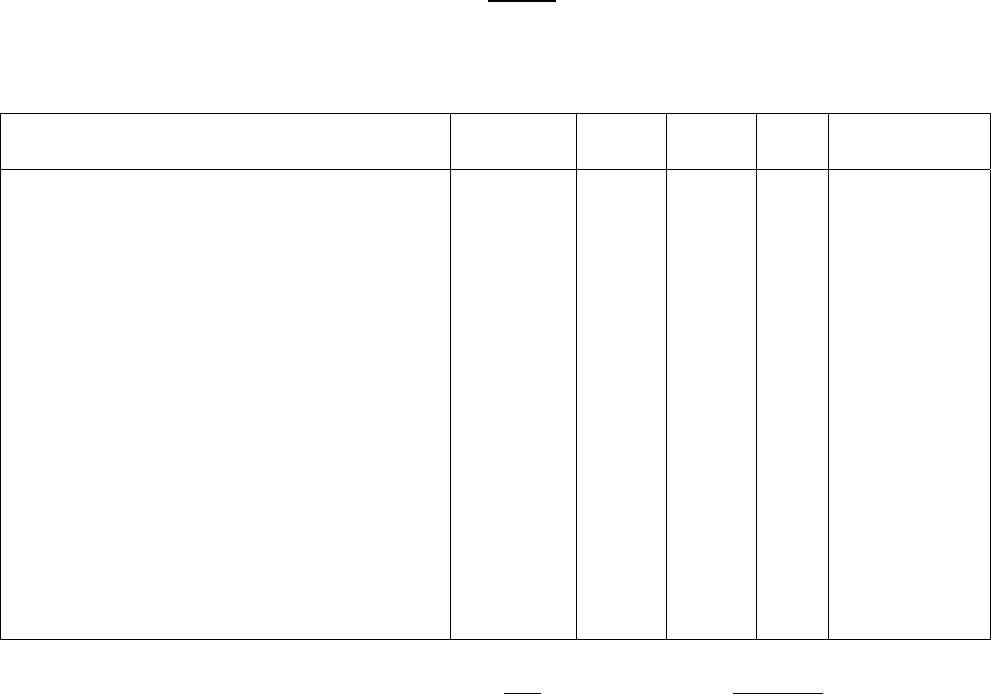

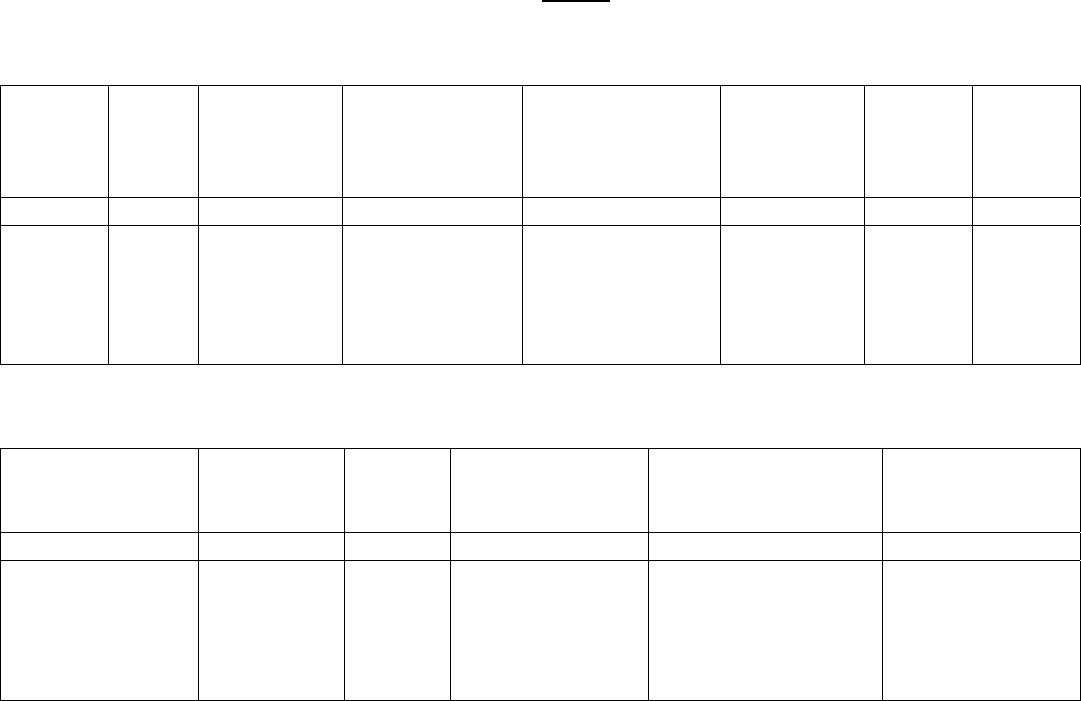

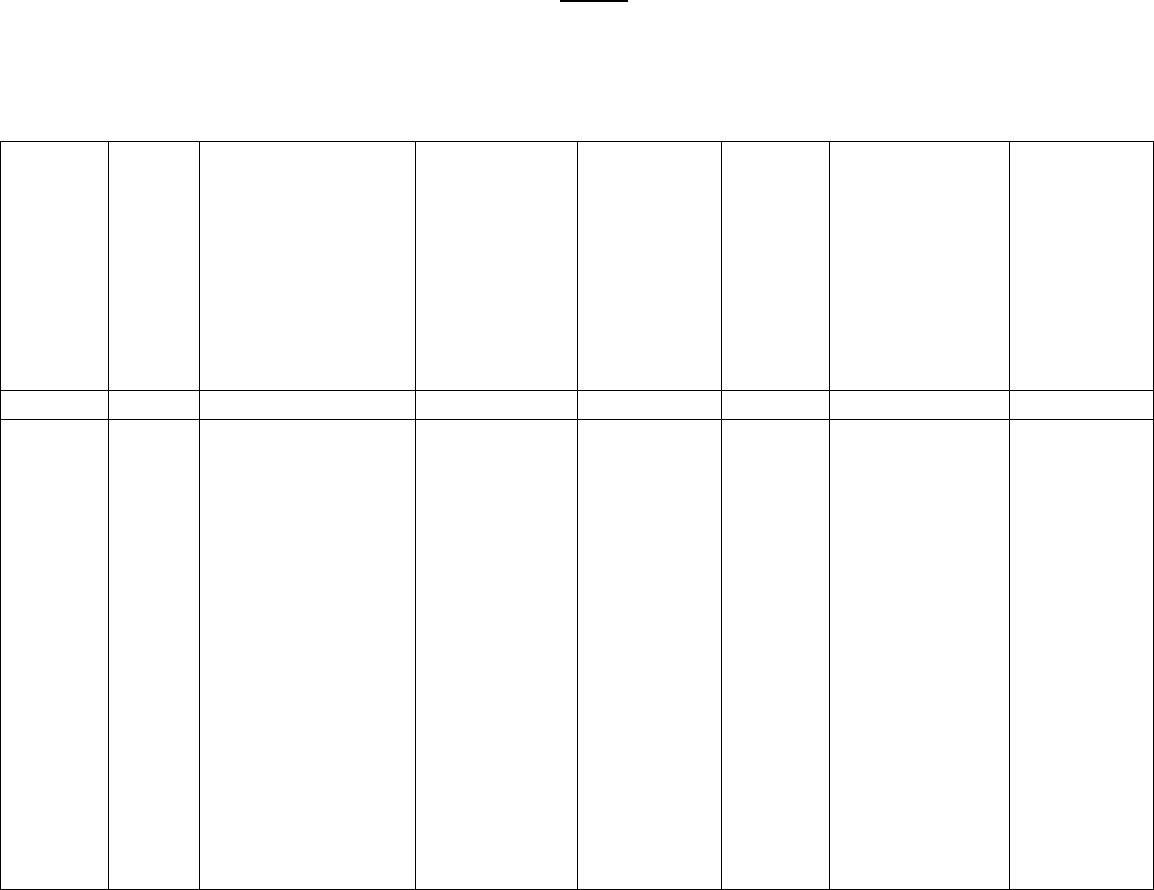

14. Registers and Books of Accounts of Money-changing Business

(i) AMCs shall maintain the following Registers in respect of their money-

changing transactions :

(a) Daily Summary and Balance Book (Foreign currency notes / coins) in

form FLM 1 (Annex-IV).

(b) Daily Summary and Balance Book (Travellers' cheques) in form FLM 2

(Annex-V).

21

(c) Register of purchases of foreign currencies from the public in form

FLM 3 (Annex-VI).

(d) Register of purchases of foreign currency notes / coins from authorized

dealers and authorized money changers in form FLM 4 (Annex-VII).

(e) Register of sales of foreign currency notes / coins and foreign currency

travellers' cheques to the public in form FLM 5 (Annex-VIII).

(f) Register of sales of foreign currency notes / coins to authorized

dealers / Full Fledged Money Changers / overseas banks in form FLM

6 (Annex-IX).

(g) Register of travellers' cheques surrendered to authorized dealers /

authorized money changers / exported in form FLM 7 (Annex-X).

(ii) All registers and books should be kept up-to-date, cross-checked and

balances verified daily.

(iii) Transactions not pertaining to money changing business of the AMC should

not be mixed up with money changing transactions. In other words, the

registers and books of account should show clearly the trail of transactions

pertaining to money changing business.

(iv) Separate registers should be maintained for each establishment, if the AMC

maintains more than one place of business.

Note :- Inter-branch transfer of foreign currencies should be accounted as

stock transfer and not as sales.

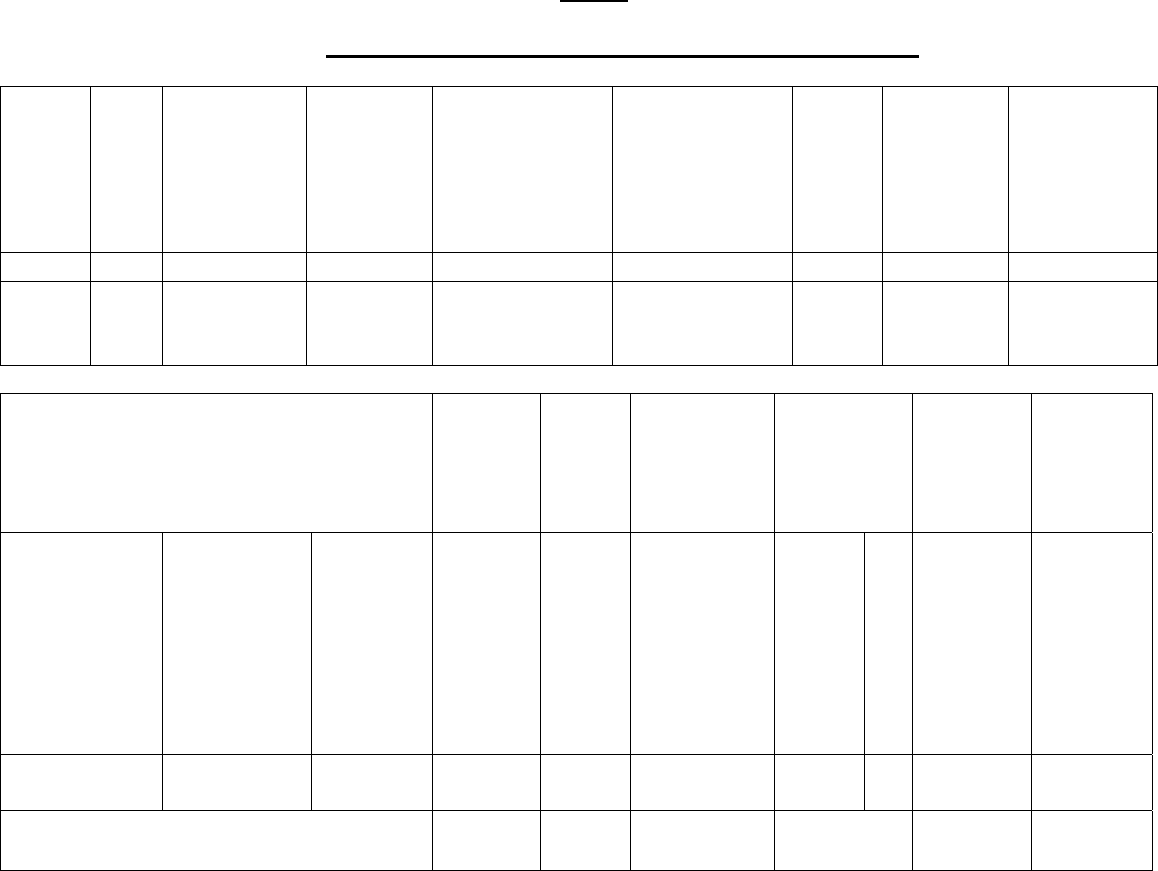

15. Submission of Statements to the Reserve Bank

(i) AMCs should submit to the office of the Reserve Bank which has issued the

license, a monthly consolidated statement for all its offices in respect of sale

and purchase of foreign currency notes in form FLM 8 (Annex-XI) so as to

reach not later than the 10th of the succeeding month.

(ii) AMCs should submit to the Regional Office concerned of the Foreign

Exchange Department, Reserve Bank, a monthly statement indicating details

22

of receipt / purchase of US $ 10,000 (or its equivalent) and above per

transactions in the enclosed format as at Annex-XII, within 10 days of the

close of the month. FFMCs / ADs Category - II should include transactions of

their franchisees in their statement.

(iii) AMCs should submit a quarterly statement regarding Foreign Currency

Account/s maintained in India in their names with AD Category-I Banks to the

Regional Office concerned of the Foreign Exchange Department, Reserve

Bank as per the format in Annex-XIII.

(iv) An Annual Statement should be submitted by all the AMCs to the respective

Regional Offices of the Foreign Exchange Department, Reserve Bank which

have issued the licenses within one month of the financial year-end, giving

the details of the amount written off during the financial year, as per the

format as at Annex-XIV.

16. Inspection of Transactions of AMCs

Section 12(1) of Foreign Exchange Management Act 1999, empowers any officer of

Reserve Bank specially authorized in this behalf to inspect the books and accounts

and other documents of AMCs. The AMCs should provide all assistance and co-

operation to Inspecting Officers in carrying out their inspection. Failure to produce

any books of account or other document or to furnish any statement or information

or to answer any question relating to the money changing transactions to the

Inspecting Officers, shall be deemed to be a contravention of the provisions of the

Act ibid.

17. Concurrent Audit

(i) AMCs should put in place a system of Concurrent Audit of the transactions

undertaken by them.

(ii) All single branch AMCs having a turnover of more than US $ 100,000 or

equivalent per month . Single branch AMCs having turnover of less than US $

100,000 or its equivalent may institute a system of quarterly audit. AMCs having

23

multiple branches, may put in place a system of Concurrent Audit which will cover 80

per cent of the transactions value-wise under a system of monthly audit and rest 20

per cent of the transactions value-wise under quarterly audit.

(iii) Appointment / selection of concurrent auditors is left to the discretion of the

AMCs. The concurrent auditors should check all the transactions of the AMCs and

ensure that all the instructions issued by the Reserve Bank from time to time have

been complied with. The Statutory Auditors are required to certify that the

Concurrent Audit and the internal control systems are working satisfactorily.

18. Temporary Money Changing Facilities

AMCs are authorized to transact money changing business only at the location or

locations specifically indicated in the licence. If it is intended to provide money

changing facilities on a temporary basis on certain special occasions, a separate

application should be made for the purpose to the Regional Office concerned of the

Foreign Exchange Department of the Reserve Bank. Full details such as period for

which the exchange counter will be operated, volume of business expected, manner

of accounting of the transactions, letter from organizers making available venue for

the money changing facilities, etc. should be submitted.

19. (A) Opening of Foreign Currency Accounts by AMCs

AMCs, with the approval of the respective Regional Offices of the Foreign Exchange

Department, may be allowed to open Foreign Currency Accounts in India, subject to

the following conditions:-

(i) Only one account may be permitted at a particular centre.

(ii) Only the value of foreign currency notes/ encashed TCs exported through the

specific bank and realized can be credited to the account.

(iii) Balances in the accounts shall be utilized only for settlement of liabilities on

account of-

24

(a) TCs sold by the AMCs and

(b) Foreign currency notes acquired by the AMCs from AD Category-I

banks.

(iv) No idle balance shall be maintained in the said account.

(B) Opening of Nostro Account by Authorised Dealers Category-II

Authorised Dealers Category-II may open Nostro Accounts after getting one time

approval from the Reserve Bank, subject to following terms and conditions.

i) Only one Nostro account for each currency may be opened;

ii) Balances in the account should be utilized only for the settlement of

remittances sent for permissible purposes and not for the settlement in respect

of forex prepaid cards;

iii) No idle balance shall be maintained in the said account; and

iv) They will be subject to reporting requirements as prescribed from time to

time.

20. Submission of Balance Sheet and maintenance of NOF

All AMCs are required to submit their annual audited balance sheet to the respective

Regional office of the Reserve Bank for the purpose of verification of their Net

Owned Funds along-with a certificate from the statutory auditors regarding the NOF

as on the date of the balance sheet. As AMCs are expected to maintain the

minimum NOF on an ongoing basis, if there is any erosion in their NOF below the

minimum level, they are required to bring it to the notice of the Reserve Bank

immediately along with a detailed time bound plan for restoring the Net Owned

Funds to the minimum required level.

25

21. Participation by Full Fledged Money Changers (FFMCs) and Authorised

Dealers Category-II (ADs Category-II) in the Currency Futures and

Exchange traded Currency Options markets

FFMCs and ADs Category-II [which are not Regional Rural Banks (RRBs), Local

Area Banks (LABs), Urban Co-operative Banks (UCBs) and Non-Banking Financial

Companies (NBFCs)], having a minimum net worth of ` 5 crore, may participate in

the designated currency futures and currency options on exchanges recognized by

the Securities and Exchange Board of India (SEBI) as clients only for the purpose of

hedging their underlying foreign exchange exposures. FFMCs and ADs Category–II

which are RRBs, LABs, UCBs and NBFCs, may be guided by the instructions issued

by the respective regulatory Departments of the Reserve Bank in this regard.

26

SECTION VI

KYC/ AML/ CFT Guidelines

Detailed Know Your Customer (KYC) /Anti-Money Laundering (AML) /Combating the

Financing of Terrorism (CFT) guidelines in respect of money changing activities are

detailed in Annex-I.

27

SECTION VII

Revocation of Licence

The Reserve Bank reserves the right to revoke the licence granted to an AMC at any

time if the Reserve Bank is satisfied that (a) it is in public interest to do so or (b) the

AMC has failed to comply with any condition subject to which the authorisation is

granted or has contravened any of the provisions of the Foreign Exchange

Management Act, 1999 or any rule, regulation, notification, direction or order made

there-under. The Reserve Bank also reserves the right to revoke the authorisation of

any of the offices for infringement of any statutory or regulatory provision. The

Reserve Bank may at any time vary or revoke any of the existing conditions of a

money changer’s licence or impose new conditions.

28

SECTION VIII

[See SECTION I, Paragraph 2 (iii) (iii)]

‘Fit and proper’ criteria for directors of FFMCs / non-bank ADs Category - II

(a) The Boards of FFMCs / non-bank ADs Category - II should undertake a

process of due diligence to determine the suitability of the person for appointment /

continuing to hold appointment as a director on the Board, based upon qualification,

expertise, track record, integrity and other ‘fit and proper’ criteria. For assessing

integrity and suitability, factors like criminal record, if any, financial position, civil

action initiated to pursue personal debts, refusal of admission to or expulsion from

professional bodies, sanctions imposed by regulators or similar bodies, previous

questionable business practices, etc. should be considered. The Board of Directors

should assess ‘fit and proper’ status by calling for information by way of self-

declaration, verification reports from market, etc. FFMCs / non-bank ADs Category -

II should obtain necessary information and declaration from the proposed / existing

directors for the purpose in Proforma given at the end.

(b) The process of due diligence should be undertaken by the FFMCs / non-bank

ADs Category - II at the time of appointment / renewal of appointment.

(c) The Boards of the FFMCs / non-bank ADs Category - II should constitute

Nomination Committees to scrutinize the declarations.

(d) Based on the information provided in the signed declaration, Nomination

Committees should decide on the acceptance or otherwise and may make

references, where considered necessary to the appropriate authority / persons, to

ensure their compliance with the requirements indicated.

(e) FFMCs / non-bank ADs Category - II should obtain annually as on 31st March

a simple declaration that the information already provided has not undergone

29

change and where there is any change, requisite details are furnished by the

directors forthwith.

(f) Further, the candidate should normally not exceed 70 years of age, should

not be a Member of Parliament / Member of Legislative Assembly / Member of

Legislative Council.

(g) Any change in directors during the year should be reported to the Regional

Office concerned of the Foreign Exchange Department, Reserve Bank of India in the

Proforma given below.

(h) Comments of respective Departments of the Reserve Bank will be obtained on

the operations of an applicant who / whose parent organisation is already licenced /

authorised by the Reserve Bank.

Proforma

Information about New Directors / Change of Directors of the FFMC / non-bank

AD Category – II

1. Name :

2. Designation :

3. Nationality :

4. Age :

5. Business Address :

6. Residential Address :

7. Educational / professional qualifications :

8. Line of business or vocation :

9. Name/s of other companies in which the person has

held the post of Chairman / Managing Director /

Director / Chief Executive Officer

:

30

10. (i) Whether associated as promoter, Managing

Director, Chairman or Director with any other FFMC /

AD Category - II?

:

(ii) If yes, the name/s of the company/ies :

11. (i) Whether prosecuted/convicted for any economic

offence either in the individual capacity or as a

partner / director of any firm / company

:

(ii) If yes, particulars thereof :

12. Experience in money changing business (number of

years)

:

13. Equity shareholding in the company

No. of shares

Face value

Percentage to total equity share capital of the

company:

:

:

:

Signature

Date

Place

:

:

:

Name

Designation

(Chief Executive Officer)

Company

:

:

:

31

Annex-I

[See SECTION VI]

PART A

KYC / AML / CFT Guidelines for money changing activities

Know Your Customer (KYC) norms / Anti-Money Laundering (AML) standards /

Combating the Financing of Terrorism (CFT) / Obligation of APs under

Prevention of Money Laundering Act, (PMLA), 2002, as amended by

Prevention of Money Laundering (Amendment) Act, 2009 – Money Changing

activities

1. Introduction

The offence of Money Laundering has been defined in Section 3 of the Prevention of

Money Laundering Act, 2002 (PMLA) as "whosoever directly or indirectly attempts to

indulge or knowingly assists or knowingly is a party or is actually involved in any

process or activity connected with the proceeds of crime and projecting it as

untainted property shall be guilty of offence of money laundering". Money

Laundering can be called a process by which money or other assets obtained as

proceeds of crime are exchanged for "clean money" or other assets with no obvious

link to their criminal origins.

There are three stages of money laundering during which there may be numerous

transactions made by launderers that could alert an institution to criminal activity –

• Placement - the physical disposal of cash proceeds derived from illegal

activity.

• Layering - separating illicit proceeds from their source by creating complex

layers of financial transactions designed to disguise the audit trail and provide

anonymity.

• Integration - the provision of apparent legitimacy to criminally derived wealth.

If the layering process has succeeded, integration schemes place the

32

laundered proceeds back into the economy in such a way that they re-enter

the financial system appearing to be normal business funds.

2. The objective

The objective of prescribing KYC/AML/CFT guidelines is to prevent the system of

purchase and / or sale of foreign currency notes / Travellers' cheques by Authorised

Persons (referred as APs hereinafter) from being used, intentionally or

unintentionally, by criminal elements for money laundering or terrorist financing

activities. KYC procedures also enable APs to know/understand their customers and

their financial dealings better which in turn help them manage their risks prudently.

3. Definition of Customer

For the purpose of KYC policy, a ‘Customer’ is defined as :

• a person who undertakes occasional/regular transactions;

• an entity that has a business relationship with the AP;

• one on whose behalf the transaction is made (i.e. the beneficial owner)

[In view of Government of India Notification dated February 12, 2010 - Rule 9,

sub-rule (1 A) of PML Rules - ' Beneficial Owner' means the natural person who

ultimately owns or controls a client and or the person on whose behalf a

transaction is being conducted, and includes a person who exercise ultimate

effective control over a juridical person].

4. Guidelines

4.1 General

APs should keep in mind that the information collected from the customer while

undertaking transactions is to be treated as confidential and details thereof are not to

be divulged for cross selling or any other like purposes. APs should, therefore,

ensure that information sought from the customer is relevant to the perceived risk, is

33

not intrusive, and is in conformity with the guidelines issued in this regard. Any other

information from the customer, wherever necessary, should be sought separately

with his/her consent.

4.2 KYC Policy

APs should frame their KYC policies incorporating the following four key elements:

a) Customer Acceptance Policy;

b) Customer Identification Procedures;

c) Monitoring of Transactions; and

d) Risk Management.

4.3 Customer Acceptance Policy (CAP)

a) Every AP should develop a clear Customer Acceptance Policy laying down

explicit criteria for acceptance of customers. The Customer Acceptance Policy must

ensure that explicit guidelines are in place on the following aspects of customer

relationship in the AP:

(i) No transaction is conducted in anonymous or fictitious/benami

name(s).

[In view of In terms of Government of India Notification dated June 16,

2010 Rule 9, sub-rule (1C) - APs should not allow any transaction in any

anonymous or fictitious name (s) or on behalf of other persons whose

identity has not been disclosed or cannot be verified].

(ii) Parameters of risk perception are clearly defined in terms of the nature

of business activity, location of customer and his clients, mode of

payments, volume of turnover, social and financial status etc. to enable

categorisation of customers into low, medium and high risk (APs may

choose any suitable nomenclature viz. level I, level II and level III).

Customers requiring very high level of monitoring, e.g. Politically

34

Exposed Persons (PEPs) may, if considered necessary, be

categorised even higher.

(iii) Documentation requirements and other information to be collected in

respect of different categories of customers depending on perceived

risk and keeping in mind the requirements of Prevention of Money

Laundering Act, (PMLA), 2002, as amended by Prevention of Money

Laundering (Amendment) Act, 2009, Prevention of Money-Laundering

(Maintenance of Records of the Nature and Value of Transactions, the

Procedure and Manner of Maintaining and Time for Furnishing

Information and Verification and Maintenance of Records of the

Identity of the Clients of the Banking Companies, Financial Institutions

and Intermediaries) Rules, 2005 as well as instructions/guidelines

issued by the Reserve Bank, from time to time.

(iv) Not to undertake any transaction where the AP is unable to apply

appropriate customer due diligence measures i.e. AP is unable to

verify the identity and /or obtain documents required as per the risk

categorisation due to non cooperation of the customer or non reliability

of the data/information furnished to the AP. It is, however, necessary to

have suitable built in safeguards to avoid harassment of the customer.

In the circumstances when an AP believes that it would no longer be

satisfied that it knows the true identity of the customer (individual/

business entity), the AP should file an STR with FIU-IND.

(v) Circumstances, in which a customer is permitted to act on behalf of

another person/entity, should be clearly spelt out, the beneficial owner

should be identified and all reasonable steps should be taken to verify

his identity.

b) APs should prepare a profile for each customer, where a business

relationship is established, based on risk categorisation. The customer profile may

35

contain information relating to customer’s identity, his sources of funds,

social/financial status, nature of business activity, information about his clients’

business and their location etc. The nature and extent of due diligence will depend

on the risk perceived by the AP. However, while preparing customer profile, APs

should take care to seek only such information from the customer, which is relevant

to the risk category. The customer profile is a confidential document and details

contained therein should not be divulged for cross selling or any other purposes.

c) For the purpose of risk categorisation, individuals (other than High Net Worth)

and entities whose identities and sources of wealth can be easily identified and

transactions by whom by and large conform to the known profile, may be

categorised as low risk. Customers that are likely to pose a higher than average risk

should be categorised as medium or high risk depending on customer's background,

nature and location of activity, country of origin, sources of funds and his client

profile etc. APs should apply enhanced due diligence measures based on the risk

assessment, thereby requiring intensive ‘due diligence’ for higher risk customers,

especially those for whom the sources of funds are not clear. Examples of

customers requiring enhanced due diligence include (a) nonresident customers;(b)

customers from countries that do not or insufficiently apply the FATF standards (c)

high net worth individuals; (d) trusts, charities, NGOs and organizations receiving

donations; (e) companies having close family shareholding or beneficial

ownership; (f) firms with 'sleeping partners '; (g) politically exposed persons (PEPs);

(h) non-face to face customers ; and (i) those with dubious reputation as per public

information available etc. However, only Non Profit Organisations (NPOs)/ Non

Government Organisations (NGOs) promoted by United Nations or its agencies may

be classified as low risk customer.

d) It is important to bear in mind that the adoption of customer acceptance policy

and its implementation should not become too restrictive and must not result in

denial of money changing services to general public.

36

4.4 Customer Identification Procedure (CIP)

a) The policy approved by the Board of APs should clearly spell out the

Customer Identification Procedure to be carried out at different stages i.e. while

establishing a business relationship; carrying out a financial transaction or when the

AP has a doubt about the authenticity/veracity or the adequacy of the previously

obtained customer identification data. Customer identification means identifying the

customer and verifying his/her identity by using reliable, independent source

documents, data or information. APs need to obtain sufficient information necessary

to establish, to their satisfaction, the identity of each new customer, whether

occasional or business relationship, and the purpose of the intended nature of

relationship. Being satisfied means that the AP must be able to satisfy the

competent authorities that due diligence was observed based on the risk profile of

the customer in compliance with the extant guidelines in place. Such risk based

approach is considered necessary to avoid disproportionate cost to APs and a

burdensome regime for the customers.

Besides risk perception, the nature of information/documents required would

also depend on the type of customer (individual, corporate etc.). For customers that

are natural persons, the APs should obtain sufficient identification document/s to

verify the identity of the customer and his address/location. For customers that are

legal persons or entities, the AP should (i) verify the legal status of the legal

person/entity through proper and relevant documents; (ii) verify that any person

purporting to act on behalf of the legal person/entity is so authorised and identify and

verify the identity of that person; and (iii) understand the ownership and control

structure of the customer and determine who are the natural persons who ultimately

control the legal person. Customer identification requirements in respect of a few

typical cases, especially, legal persons requiring an extra element of caution are

given in paragraph 4.5 below for guidance of APs. APs may, however, frame their

own internal guidelines based on their experience of dealing with such

persons/entities, their normal prudence and the legal requirements as per

established practices. If the AP decides to undertake such transactions in terms of

37

the Customer Acceptance Policy, the AP should take reasonable measures to

identify the beneficial owner(s) and verify his/ her/t heir identity in a manner so that it

is satisfied that it knows who the beneficial owner(s) is/are [In view of Government

of India Notification dated June 16, 2010 - Rule 9 sub-rule (1A) of PML Rules].

Note : Rule 9(1A) of Prevention of Money Laundering Rules 2005 requires that every

Authorised Person under money changing activity shall identify the beneficial owner and

take all reasonable steps to verify his identity while undertaking money changing

activities. The term "beneficial owner" has been defined as the natural person who

ultimately owns or controls a client and/or the person on whose behalf the transaction is

being conducted, and includes a person who exercises ultimate effective control over a

juridical person. Government of India has since examined the issue and has specified

the procedure for determination of Beneficial Ownership. The procedure as advised by

the Government of India is as under:

A. Where the client is a person other than an individual or trust, the Authorised Person

shall identify the beneficial owners of the client and take reasonable measures to verify

the identity of such persons, through the following information:

(i) The identity of the natural person, who, whether acting alone or together, or

through one or more juridical person, exercises control through ownership or who

ultimately has a controlling ownership interest.

Explanation: Controlling ownership interest means ownership of/entitlement to

more than 25 percent of shares or capital or profits of the juridical person, where

the juridical person is a company; ownership of/entitlement to more than 15% of

the capital or profits of the juridical person where the juridical person is a

partnership; or, ownership of/entitlement to more than 15% of the property or

capital or profits of the juridical person where the juridical person is an

unincorporated association or body of individuals.

(ii) In cases where there exists doubt under (i) as to whether the person with the

controlling ownership interest is the beneficial owner or where no natural person

exerts control through ownership interests, the identity of the natural person

exercising control over the juridical person through other means.

Explanation: Control through other means can be exercised through voting rights,

agreement, arrangements, etc.

(iii) Where no natural person is identified under (i) or (ii) above, the identity of the

relevant natural person who holds the position of senior managing official.

B. Where the client is a trust, the Authorised Person shall identify the beneficial owners

of the client and take reasonable measures to verify the identity of such persons,

through the identity of the settler of the trust, the trustee, the protector, the beneficiaries

with 15% or more interest in the trust and any other natural person exercising ultimate

effective control over the trust through a chain of control or ownership.

38

C. Where the client or the owner of the controlling interest is a company listed on a stock

exchange, or is a majority-owned subsidiary of such a company, it is not necessary to

identify and verify the identity of any shareholder or beneficial owner of such companies.

b) Some close relatives, e.g., wife, son, daughter and parents etc. who live with

their husband, father/mother and son/ daughter, as the case may be, may find it

difficult to undertake transactions with APs as the utility bills required for address

verification are not in their name. It is clarified, that in such cases, APs can obtain an

identity document and a utility bill of the relative with whom the prospective customer

is living along with a declaration from the relative that the said person (prospective

customer) wanting to undertake a transaction is a relative and is staying with

him/her. APs can use any supplementary evidence such as a letter received through

post for further verification of the address. While issuing operational instructions to

the branches on the subject, APs should keep in mind the spirit of instructions

issued by the Reserve Bank and avoid undue hardships to individuals who are,

otherwise, classified as low risk customers.

c) APs should introduce a system of periodic updation of customer identification

data (including photograph/s) if there is a continuing business relationship.

d) An indicative list of the nature and type of documents/information that may be

may be relied upon for customer identification is given in PART B of Annex-I of this

circular. It is clarified that correct permanent address, as referred to in PART B of

Annex-I, means the address at which a person usually resides and can be taken as

the address as mentioned in a utility bill or any other document accepted by the AP

for verification of the address of the customer. When there are suspicions of money

laundering or financing of the activities relating to terrorism or where there are

doubts about the adequacy or veracity of previously obtained customer identification

data, APs should review the due diligence measures including verifying again the

identity of the client and obtaining information on the purpose and intended nature of

the business relationship, as the case may be. [In view of Government of India

Notification dated June 16, 2010- Rule 9 sub-rule (1D) of PML Rules].

39

e) Purchase of foreign exchange from customers

(i) For purchase of foreign currency notes and/ or Travellers’ Cheques from

customers for any amount less than Rs.50,000/- or its equivalent, photocopies of the

identification document need not be obtained. However, full details of the

identification document should be maintained. If the Authorised Person has reason

to believe that a customer is intentionally structuring a transaction into a series of

transactions below the threshold of Rs.50000/-, the A.P. should verify identity and

address of the customer and also consider filing a suspicious transaction report to

FIU-IND.

(ii) For purchase of foreign currency notes and/ or Travellers’ Cheques from

customers for any amount equal to or in excess of Rs.50,000/- or its equivalent, the

identification documents, as mentioned at PART B of Annex-I of this circular,

should be verified and copies retained.

(iii) (a) Requests for payment in cash in Indian Rupees to resident customers

towards purchase of foreign currency notes and/ or Travellers’ Cheques from them

may be acceded to the extent of only US $ 1000 or its equivalent per transaction.

(b) Requests for payment in cash by foreign visitors / Non-Resident Indians

may be acceded to the extent of only US $ 3000 or its equivalent.

(c) All purchases within one month, i.e. within 30 days from the date of last

transaction, may be treated as single transaction for the above purpose and

also for reporting purposes.

(d) In all other cases, APs should make payment by way of 'Account Payee'

cheque / demand draft only.

(iv) Where the amount of forex tendered for encashment by a non-resident or a

person returning from abroad exceeds the limits prescribed for Currency Declaration

Form (CDF), the AP should invariably insist for production of declaration in CDF.

40

(v) In case of any suspicion of money laundering or terrorist financing, irrespective

of the amount involved, enhanced Customer Due Diligence (CDD) should be

applied. Whenever there is a suspicion of money laundering or terrorist financing or

when other factors give rise to a belief that the customer does not in fact pose a low

risk, APs should carry out a full scale CDD before undertaking any transaction for

the customer.

f) Sale of foreign exchange to customers

(i) In all cases of sale of foreign exchange, irrespective of the

amount involved, for identification purpose the passport of the customer

should be insisted upon and sale of foreign exchange should be made only

on personal application and after verification of the identification document. A

copy of the identification document should be retained by the AP.

(ii) Payment in excess of Rs.50,000/- towards sale of foreign exchange

should be received only by crossed cheque drawn on the bank account of the

applicant’s firm/ company sponsoring the visit of the applicant / Banker’s

cheque / Pay Order / Demand Draft. Such payment can also be received

through debit cards/ credit cards/ prepaid cards provided (a) KYC/ AML / CFT

guidelines are complied with, (b) sale of foreign currency/ issue of Foreign

Currency Travellers’ cheques is within the limits (credit/ prepaid cards)

prescribed by the bank, (c) the purchaser of foreign currency/ Foreign

Currency Travellers’ cheque and the credit/ debit/ prepaid card holder is one

and the same person.

(iii) All purchases made by a person within one month i.e. within 30 days from the

date of last transaction, may be treated as single transaction for the above purpose

and also for reporting purposes. For sale of foreign exchange to a person within

his/her eligibility through more than one drawal within 30 days or for a single

journey/visit abroad, APs may receive second and subsequent payments only by

crossed cheque drawn on the bank account of the applicant's firm/company

41

sponsoring the visit of the applicant/Bank's cheque / Pay Order / Demand Draft /

debit cards / credit cards / prepaid cards, if the total rupee payment, including

payments on earlier drawal /s, exceeds Rs. 50,000/- on the second or subsequent

drawals.

(iv) Encashment Certificate, wherever required, should also be insisted upon.

g) Establishment of business relationship

Relationship with a business entity like a company / firm/ trusts and foundations

should be established only after conducting due diligence by obtaining and verifying

suitable documents, as mentioned at PART B of Annex-I of this circular. Copies of

all documents called for verification should be kept on record. APs should obtain

information on the purpose and intended nature of the business relationship. APs

should exercise ongoing due diligence with respect to the business relationship with

every client and closely examine the transactions in order to ensure that they are

consistent with their knowledge of the customer, its business and risk profile. APs

should ensure that documents, data or information collected under the Customer

Due Diligence process is kept up-to-date and relevant by undertaking reviews of

existing records, particularly for higher risk categories of customers or business

relationships. When a business relationship is already in existence and it is not

possible to perform customer due diligence on the customer in respect of business

relationship, APs should terminate the business relationship and make a Suspicious

Transaction Report to FIU-IND. In the circumstances when an AP believes that it

would no longer be satisfied that it knows the true identity of the customer

(individual/ business entity), the AP should also file an STR with FIU-IND.

4.5 Customer Identification Requirements – Indicative Guidelines

i) Transactions by Trust/Nominee or Fiduciary Customers

There exists the possibility that trust/nominee or fiduciary relationship can be used to

circumvent the customer identification procedures. APs should determine whether

the customer is acting on behalf of another person as trustee/nominee or any other

42

intermediary. If so, APs should insist on receipt of satisfactory document of identity

of the intermediaries and of the persons on whose behalf they are acting, as also

obtain details of the nature of the trust or other arrangements in place. While

undertaking a transaction for a trust, APs should take reasonable precautions to

verify the identity of the trustees and the settlers of trust (including any person

settling assets into the trust), grantors, protectors, beneficiaries and signatories. In

all cases beneficiaries should be identified with reference to necessary documents.

In the case of a 'foundation', steps should be taken to verify the founder managers/

directors and the beneficiaries.

ii) Transactions by companies and firms

APs need to be vigilant against business entities being used by individuals as a

‘front’ for undertaking transactions with APs. APs should examine the control

structure of the entity, determine the source of funds and identify the natural persons

who have a controlling interest and who comprise the management. These

requirements may be moderated according to the risk perception e.g. in the case of

a company that is listed on a recognized stock exchange, it will not be necessary to

identify all the shareholders.

iii) Transactions by Politically Exposed Persons (PEPs)

Politically exposed persons are individuals who are or have been entrusted with

prominent public functions in a foreign country, e.g., Heads of States or of

Governments, senior politicians, senior government/judicial/military officers, senior

executives of state-owned corporations, important political party officials, etc. APs

should gather sufficient information on any person/customer of this category