New Horizons HSi S6W2 Ey Health Care Industry Report 2014

User Manual: HSi S6W2

Open the PDF directly: View PDF ![]() .

.

Page Count: 116 [warning: Documents this large are best viewed by clicking the View PDF Link!]

Health Care Industry Report 2014

New horizons

Voyage to value

Featuring exclusive interviews with

the International Consortium for Health Outcomes Measurement,

the Center for Healthcare Quality and Payment Reform

and the Robert Wood Johnson Foundation

To our clients

and other friends

Jonathan G. Weaver

EY Americas Health Care Sector Leader

Jim Costanzo

National Practice Leader

EY Health Care Advisory Services

A profound tidal shift is under way in the

US health care system. In the wake of

uneven quality and unsustainable spending,

the old volume-driven model is being

jettisoned. A new tide is rolling in to

transform how care is delivered and paid

for, rewarding those who improve patient

outcomes and do so at lower costs. The

ultimate destination is a more efcient,

higher-quality, consumer-focused health

care system — one rmly anchored in value.

“Like sailboats at sea, health

care organizations will need

to steer condently through

the shifting winds and changing

currents that continue to

challenge their course.”

The journey forward is an arduous one.

Ongoing implementation of the Affordable

Care Act, emerging health insurance

exchanges, mounting pressures for price

transparency, a heightened focus on

population health, massive investments

in health information technology,

an increased impetus to gain scale and

market share, a growing call to engage

patients in their care — these are among

the converging forces the industry must

deftly navigate.

And they are only the beginning. In the

years ahead, health care providers and

payers can expect rising pressures from

every direction. Like sailboats at sea, they

will need to steer condently through the

shifting winds and changing currents that

continue to challenge their course.

This edition of New horizons is focused

on how health care organizations can

best nd their way on the voyage to

value. Along with an overview of recent

industry developments, we include brief

proles of several organizations and

programs that are in the vanguard of value

creation. Questions are also provided to

serve as a gauge of today’s initiatives — and

tomorrow’s imperatives.

As your organization sails toward the

new horizon, we hope this report will help

inform your discussions and enrich your

decisions. If you have any questions about

the issues explored in New horizons, please

contact your local EY executive.

i

1

Prelude

Value and viability

Setting sail

Feature

Value-based health care:

measuring outcomes that

matter to patients

A conversation with

Jens Deerberg‑Wittram, MD,

President, the International

Consortium for Health

Outcomes Measurement

31

Chapter 2

Value in delivery

Changing tack

43

Chapter 3

Value in information

technology

Supporting the journey

Feature

The move to meaningful

use and ICD-10: finding

the bearings

A roundtable discussion with

EY Health Care Advisory

Services leaders

71

Chapter 5

Value in transactions

Gaining the wind

59

Chapter 4

Value in compliance

Heeding the warnings

11

Chapter 1

Value in payment

Making headway

Feature

Accountable payment

models: paying to support

higher-quality, lower-cost

health care

A conversation with

Harold D. Miller, President

and CEO, the Center for

Healthcare Quality and

Payment Reform

Contents

ii New horizons: voyage to value

93

Postscript

Value in leadership

Taking the helm

Feature

Leadership in transformative

times: navigating the

changing tides

A conversation with

Risa Lavizzo‑Mourey, MD, MBA,

President and CEO, the Robert

Wood Johnson Foundation

83

Chapter 6

Value in measurement

Sounding the depth

107

EY thought leadership

publications

99

Appendix

Value in government

initiatives

Reading the forecast

106

Frequently used

acronyms

108

Acknowledgments

iii

{ }

“To reach a port we must set sail — sail, not tie

at anchor; sail, not drift.”

Franklin D. Roosevelt, 32nd US President

Prelude

Value and viability

Setting sail

The demand to derive greater value from health care, producing the best patient outcomes

at the lowest cost, is pervasive and urgent. Compared with the rest of the world, the US

spends the most money for health care. Yet our overall health is not improving, especially

within the most costly patient populations — those with chronic diseases.

Value Outcomes

Cost

To close the value gap, the health care industry today has set sail on a new course.

Since passage in 2010 of the Patient Protection and Affordable Care Act (ACA),

where the term “value” appears prominently, the pursuit of value-based care has rapidly

emerged in industry and policy discussions. The ultimate goal on the “voyage to value” is

to create an economically sustainable approach to how care is delivered and how it is paid

for. Advocates maintain that costs can best be controlled by re-engineering care delivery

and rewarding improved value: keeping people healthy, using medical interventions

appropriately, and preventing and managing the chronic illnesses that consume a large

part of our health care dollars.

“Value is the only goal that unites the interests of all the parties in the

healthcare system.”

Michael E. Porter, PhD

Bishop William Lawrence University Professor

The Institute for Strategy and Competitiveness

Harvard Business School

1

In the consumer world, value is a familiar

concept. Consumers tend to equate

good value with products of the highest

quality for the lowest price. When applied

to health care, however, value is more

complex, as the consumer — from patients

and providers to payers and purchasers,

and the product — patient outcomes, can

vary widely. According to the Institute of

Medicine (IOM), an organization that has

studied the issue closely, value is in the

eye of the beholder, representing different

things to different stakeholders.

Value for health care providers, for

example, hinges on making decisions

based on appropriateness of care.

For payers, it means using evidence-

based interventions and paying based on

outcomes. For employers, value is keeping

workers and their families healthy and more

productive at lower costs. And for patients,

value is having a high-quality relationship

with care providers, meeting personal

health goals and being assured that out-

of-pocket payments are targeted to these

goals. Reconciling stakeholder perspectives

in a way that creates value for all is a

challenge requiring thoughtful discussion,

diligent focus and unied action.

Driven by the value challenge, industry

stakeholders are pursuing a variety of

strategies. Health care providers are

embracing payer incentives to deliver

high-value care through such models as

pay-for-performance, bundled-payment,

global budgets and nancial-risk-sharing

within accountable care organizations

(ACOs). Payers are nding new ways to

partner with providers to add value to the

patient experience. Employers are striving

to rein in rising health care premiums while

pursuing affordable, high-value products

and services that enhance employee health

and productivity. Product manufacturers

are investing in innovations that deliver

value by improving quality of life. Patients

are looking to access tools and transparent

information that help them make the most

informed value-based decisions.

In this edition of New horizons, we look at

the voyage to value in health care and the

course ahead in delivering on the value

promise. Throughout, “Value vignettes”

prole real-world examples of how payers,

providers and industry groups are pursuing

value. “Viewnder” questions at the end of

each chapter offer considerations for your

board and leadership team as you pursue

value initiatives within your organizations

and with partners across the continuum

of care.

Our launching point is a conversation

with Dr. Jens Deerberg-Wittram, who

leads the International Consortium for

Health Outcomes Measurement. His

organization has been instrumental in

dening and driving the adoption of a

global set of outcome measures for a full

range of medical conditions. In focusing

on the outcomes that matter most to

patients —the center of the health care

universe — these efforts are helping the

industry set sail toward the full potential

of value-based care.

2New horizons: voyage to value

3

Feature

Value-based health

care: measuring

outcomes that

matter to patients

A conversation with

Jens Deerberg‑Wittram, MD,

President, the International

Consortium for Health Outcomes

Measurement (ICHOM)

(www.ichom.org)

Dr. Deerberg‑Wittram leads ICHOM,

a global organization cofounded

by Professor Michael Porter of

the Institute for Strategy and

Competitiveness at Harvard Business

School, the Karolinska Institute in

Sweden and the Boston Consulting

Group to help advance value‑

based health care. We talked with

Dr. Deerberg‑Wittram about the

concept of value and the importance

of measuring outcomes that matter

to patients.

You’ve observed health care systems

around the world. What does value

mean, from your perspective? Why

has it been so difficult to consistently

deliver health care value — and

measure it?

The term “value” was best dened for

health care by Professor Michael Porter of

the Harvard Business School: the outcomes

we achieve for the money we spend. The

term “outcome” hasn’t been clearly dened

in the past. If we look at different sources

that deal with outcome measurement,

what is called an outcome is really an

output. An outcome from our perspective

is only one thing: the results that matter

to a patient after a care delivery process.

It’s an exciting formula because it offers a

new perspective on value with a different

measure of success.

“An outcome from our perspective

is only one thing: the results that

matter to a patient after a care

delivery process.”

Although physicians are striving to improve

patients’ health, historically, the more

broad measures of health care system

outcomes have not been aligned with

specic patient health outcomes. In an

outcomes-based world focused on patients’

health, we say: “Let’s do this differently.

Let’s move away from volume and measure

value based on the results that matter to

patients. To what extent can we achieve

these results? And how much money do

we need to get there?”

Let’s look at an example. If you have a

patient who is suffering from prostate

cancer, and you ask physicians what kind of

outcomes they are measuring, they will tell

you that they measure a lot of things — for

example, length of stay, appropriate MRI

scans, PSA level, number of procedures

and patient satisfaction. All these kinds

of measures may be interesting, but

not relevant. They are not what matter

to patients.

If you ask patients their denition of an

outcome, they will tell you clearly and

consistently. Michael Porter has rendered

these responses as an outcome measures

hierarchy (see diagram on the next page).

The rst tier is the health status achieved

or retained. Do I survive as a patient who

is suffering from cancer? What will be

the status of my health or degree of my

recovery? Will my quality of life be good?

Will I be in pain? Will I be able to sleep?

What about anxiety?

The second tier is the process of recovery.

How much time will it take to return to

normal activities? What difculties and

complications might I face in my care

or treatment?

The third tier is health sustainability. Will my

illness recur? Will my treatment have any

long-term consequences? For example,

apatient with cancer treated with beam

radiotherapy may see great results for a

year, but two or three years later may be

complaining about complications caused

by the treatment.

We believe that if you want to determine

value, you need to measure the outcome

of every medical condition from the patient

perspective. Standardized outcomes can

help clinicians decide on treatments that

improve patients’ quality of life.

4New horizons: voyage to value

What is the process for obtaining these

outcomes that matter to patients?

Measuring outcomes systematically

requires having the right data sources.

Some outcomes can be determined

only by asking the patient directly — for

example, “Do you have pain?” and “How

would you rate your quality of life?” We call

these “patient-reported outcomes,” and

they are an essential part of outcomes

measurement. Yet patients can’t report

on a number of other outcomes that

matter to them, such as complications

that happen during surgery. You have

to ask the physician about that, because

the patient doesn’t know. These are

“physician-reported outcomes.” One of

the most difcult outcomes to measure

is mortality —a patient with cancer who

dies two years after treatment, for instance.

The patient by denition is not able to

report. In this case it might be helpful to

get access to the national death registry,

if it is available.

At ICHOM, in dening health outcomes,

we directly involve patients in the process.

All of our patient representatives have been

treated for the condition being evaluated.

We also bring together leading physicians

from across the globe who specialize in

treating this condition. As patients and

physicians discuss and reach consensus

on the outcomes that matter most to them,

the ICHOM team serves as facilitator.

What role does technology play

in this process?

We’re looking more and more at technology

solutions to collect meaningful outcomes

data. For example, a key resource is mobile

devices. If you want to measure the mobility

of a patient after orthopedic surgery,

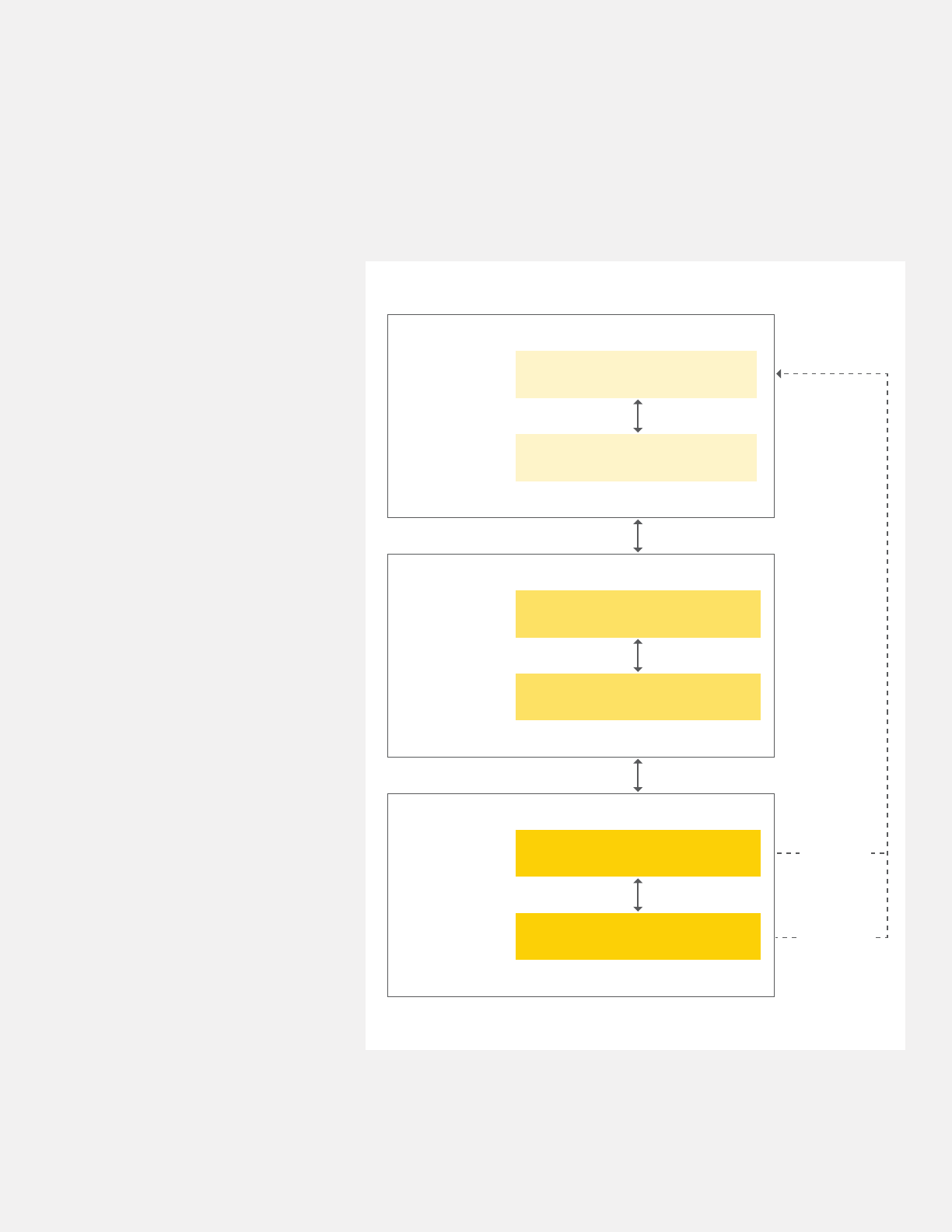

Tier 1

Health status

achieved or

retained

The outcome measures hierarchy

Survival

Degree of health or recovery

Tier 2

Process

of recovery

Time to recovery and time to return

to normal activities

Difficulty of care or treatment process (e.g.,

diagnostic errors, ineffective care, treatment-

related discomfort, complications, adverse effects)

Tier 3

Sustainability

of health

Sustainability of health or recovery

and nature of recurrences

Source: Professor Michael Porter, “What is value in health care?”

New England Journal of Medicine, December 23, 2010. Used with permission.

Recurrences

Care-induced

illnesses

Long-term consequences of therapy

(e.g., care-induced illnesses)

5

it’s probably much easier to look at GPS

data on his or her mobile phone than to ask

how many miles or meters were walked this

week. This new measuring and reporting

capability is a huge step forward and one

that will help greatly in collecting more

relevant data on outcomes.

However, in the outcome measurement

eld today, we’ve found that large

information technology vendors are not

the drivers of innovation. Numerous smaller

companies are making the greatest strides

in this space, developing ready-to-use

plug-and-play apps for outcomes collection.

The challenge will be to integrate their

solutions into larger systems.

Tell us more about the mission of

ICHOM. How did your organization

come together? What are your plans

for the future?

In the early ’90s, Michael Porter began

writing the rst paper about creating

value-based competition in health care.

In 2006, he published a book on this topic,

Redening Health Care. It provides the

argument for using health outcomes data

to redene the nature of competition in the

industry. Over the past eight years, we have

offered many courses at Harvard and other

institutions worldwide where we teach

the value concept to providers, payers,

pharmaceutical companies and medical

technology companies.

People quickly “got it.” They agreed

we needed to move to value as the

new denition of success in health care.

Further discussions led to the idea of

standardization. It doesn’t make sense

to tell surgeons around the world that

they should measure incontinence, for

example —and then nd years later they’re

all measuring it in a different way. We would

have no chance to compare outcomes.

We concluded we needed a standard set

of measures ready to use, simple to handle

and comprehensive enough to cover the

relevant aspects of a patient’s condition

from a patient’s perspective — but not

too complex to overstretch organizations.

And, we needed to offer these measures for

free. In the summer of 2012, we launched

ICHOM as a nonprot organization and

started our work.

Our rst goal was to show that it’s possible

to dene meaningful patient outcome

standards and test them in the eld.

We agreed to begin with four medical

conditions, and for these reasons:

1. Coronary artery disease, which is the

number one cause of death globally and

also one of the most costly conditions to

treat. But it’s also preventable through

patients’ lifestyle changes.

2. Localized prostate cancer, one of

the most common types of cancer

in men. It has different ways of being

treated — from active surveillance

to radical prostatectomy — and can

produce wide variations in outcomes

that matter to patients. For example,

the average incontinence level

one year after prostate surgery in

Germany and Sweden is around 50%,

while organizations performing best

in this procedure worldwide show

a post-surgery incontinence level

of 5% — a tenfold difference.

3. Cataracts, a health issue found in

patients around the globe. Cost for

treatment shows wide variations.

In India, for example, the cost is 1% of

what it is in the most expensive centers

in the US.

4. Low back pain, a condition that is

one of the greatest causes of sick

leave in the workforce and has a

huge impact on global economies.

It is also a condition involving

different medical specialties and many

different treatments. We need to

better understand which options offer

patients the best long-term outcomes.

“Our ve-year goal is to cover 50

medical conditions that represent

about 70% of the disease burden

in industrialized countries.”

Within a year, we completed four Standard

Sets of outcomes for our rst four medical

conditions. In November 2013, we unveiled

these at a Harvard conference drawing

health care leaders from more than 20

countries. These standards have also been

submitted to leading journals and are in

the process of being published. In 2014,

we’re studying more medical conditions

6New horizons: voyage to value

and plan to have Standard Sets for 12 more

conditions by the end of the year. Our ve-

year goal is to cover 50 medical conditions

that represent about 70% of the disease

burden in industrialized countries.

You’ve had the opportunity to observe

health care value in many countries

around the world. How does the US

measure up?

I would say the US has a long way to go

but is denitely on its way. Historically, it’s

been a nation willing to try new approaches.

We see lots of interest and energy to move

forward and improve. The momentum

is coming from providers — from small

organizations that want to begin measuring

value, to well-known leaders that have the

bandwidth and funding for pilot testing.

It’s also coming from payer organizations

that want to reimburse based on outcomes,

and from the ACA itself, which has opened

many opportunities to measure and pay

for outcomes.

You’ve had considerable experience

as a hospital executive and

understand the unique challenges

faced by C-suites and board members.

How can executive leadership best

support outcomes measurement in

their own organizations?

Perhaps my personal experience can shed

some light. For eight years, I ran a 4,800-

bed for-prot system and was also a health

care consultant. I saw rsthand the impact

outcomes can have on managing health

care costs, and I came to believe that health

care should be organized around improving

outcomes and value.

Before this realization, I tried everything

I could to change clinician behavior in a

systematic way, from clinical pathways

to lean management. But it didn’t work.

If you tell a physician, “The antibiotics

you use cost 25% more than those of your

colleagues,” they may not care. If you

say, “I have a clinical pathway in my

computer that tells me what to do,” they

may not take it. They’ll say, “I’m not a

technician. I’m a physician.”

“I have found the only thing that

works — and drives organizational

change — is providing outcomes

information.”

I have found that the only thing that works —

and drives organizational change — is

providing outcomes information. This is

something you must believe or experience

as a health care executive. Then you will

take the right steps.

The rst step is to commit yourself

to outcomes measurement. Walk the

walk. Tell your people, “I want you to

measure outcomes. I want you to know

how to do this, and I want to discuss

with you how we can do better from a

patient perspective.”

Second, don’t wait for a big-bang

information technology x. It isn’t coming.

Third, try to nd payer partners who

are ready to tie money to outcomes.

The ACA gives most organizations room

to do just that.

Last, seek out the “evangelists” in your

organization who are already measuring

outcomes. Give them the bandwidth,

support and funds to run pilots. Celebrate

their successes. In the new world of value-

based health care systems, one successful

pilot can position your organization for

lasting leadership.

7

8New horizons: voyage to value

Viewfinders

Considerations for your board and executive leaders

•Is value the “wind in the sails” of your

organization’s mission and leadership?

•Have you dened your organization’s

core value proposition and

overarching strategy to succeed

in avalue-based world?

•How are you building your reputation in

the community as a provider of value?

•Have you developed a culture of

collaboration and accountability to

support value-based approaches?

In what ways are your employees at

every level empowered to deliver value

in their daily work?

•What tools have you built into your

processes for continuous feedback

and action to support the voyage from

volume to value?

•How do you know you are delivering the

outcomes that matter to patients?

9

{ }

“Price is what you pay. Value is what you get.“

Warren Buffett, 20th‑century American investment entrepreneur

Chapter 1

Value in payment

Making headway

Voyage to value

In pursuing value-based health care, payers are partnering with

providers to create high-value payment systems that reward quality over

quantity. Varied routes are being tried to shape the payment model of

the future, from changing payment incentives to adopting performance

measurements. Value-based payments can spur the health care system

to make delivery more efcient, steer clear of waste and reward

providers for helping patients stay healthy.

Meanwhile, with mounting nancial pressures, health care organizations

are “battening down the hatches” through a range of methods designed

to streamline operations and better manage their bottom lines. This dual

focus — looking externally to leverage new payment opportunities and

internally to curtail costs — is a promising approach in making headway

toward the value destination.

11

Government and market forces are propelling the health

care industry in a new direction — one that moves away

from paying for volume and toward paying for value.

In these deep currents of change, health care providers

and payers must pilot a variety of nancial decisions, new

business processes and strategic opportunities. In this

chapter, we look at payment systems driven by policy and

by the market. We also explore several approaches health

care organizations are taking to lower their costs in a

world of reduced margins and value-driven operations.

Value-based payment models:

considering the options

The move toward value-based payment,

in motion for many years, has been

accelerated by the Affordable Care Act.

The law includes several nancial incentives

for providers to better coordinate

health care delivery. Different payment

methodologies have been proposed as

the prime solution for stimulating delivery

system change. A range of government

initiatives are in play to improve quality

through payment models (see Exhibit 1-1

on page 13). Commercial payers, too, are

pairing payment incentives with changes

aimed at producing better-coordinated,

higher-quality and more-efcient care.

According to Catalyst for Payment Reform,

a national organization for health care

purchasers, 10.9% of commercial payments

today are value-oriented, designed to

either improve performance or cut waste.

This marks a signicant leap from 2010,

when 1%–3% of payments were value-based.

Exhibit 1-2 on page 14 illustrates the

continuum of value-based payment models,

from lowest to highest risk, accompanied by

a discussion of how these models are being

pursued today.

Fee-for-service (FFS)

Paying health care providers on an FFS

basis has been cited as a key contributor

to the nation’s cost and quality challenges.

In the FFS system, each procedure or

service is billed and paid for separately.

These payments may encourage the use

of more, and more expensive, services and

fail to reward high-quality care. FFS also

makes coordination of care across multiple

providers and varied settings difcult and

burdensome for patients, as they receive

different bills from different clinicians and

may not have a designated care manager

to help them with treatment decisions.

Pay-for-performance (P4P)

The P4P model typically pays fees for

individual services, with some form of a

nancial incentive payment to physicians

based on their performance compared with

a set of performance metrics. While early

P4P programs used quality and access

measures to determine incentive awards,

current models often include measures of

physician practice efciency, such as use

of lower-cost generic pharmaceuticals.

In the government sector, the P4P

model is implemented through hospital

value-based purchasing, penalties for

readmissions and penalties for hospital-

acquired infections (see Exhibit 1-1 on

page 13). In the private payer sector, P4P

is evident in a wide range of quality-based

commercial contracts.

“The way we price health care

cannot be understood by a human

being of average intelligence and

limited patience.”

Michael Leavitt

Former Secretary

US Department of Health and Human

Services (HHS)

Care management fees

In this model, health plans pay providers,

typically organized as patient-centered

medical homes, for better care coordination.

Payments are intended to provide an

investment in practice functions that

traditionally have not been reimbursed,

such as educating patients in self-

management.

12 New horizons: voyage to value

Exhibit 1-1. Government initiatives in the shift from volume-driven to value-driven payment

•Bundled Payment for Care Initiative

(BPCI). A total of 299 hospitals and

166 post-acute care organizations are

part of BPCI, a Medicare pilot program.

Providers are reimbursed for certain

care episodes through single case rates

and can participate in gainsharing.

•Comprehensive Primary Care

Initiative (CPCI). A four-year public-

private partnership, CPCI is designed

to test a model of improved access

to quality health care at lower cost.

Atotal of 500 primary care practices

in eight states are participating.

CMS is paying primary care practices

a care management fee to coordinate

services for Medicare fee-for-service

beneciaries.

•Hospital Acquired Condition (HAC)

Reduction Program. Beginning

October 1, 2014, the HAC Reduction

Program, mandated by the ACA,

requires the Centers for Medicare &

Medicaid Services (CMS) to reduce

hospital payments by 1% for hospitals

that rank among the lowest-

performing 25% in HACs.

•Hospital Value-Based Purchasing

(HVBP) Program. Created under the

ACA and launched in October 2012,

the HVBP Program lays the groundwork

for Medicare to become a value-based

purchaser of health care services.

Payment adjustments, up or down

by as much as 1.25%, are based on

hospital performance across two dozen

measures of clinical processes, patient

satisfaction and outcomes.

•Medicare Hospital Readmissions

Reduction Program. Under this

program, the government is looking

at the number of heart attack, heart

failure and pneumonia patients who

return to the hospital within 30 days

of discharge. The program will be

expanded in October 2014 to add

two additional conditions, elective

hip or knee replacements and chronic

obstructive pulmonary disease.

Hospitals with more readmissions than

Medicare expected given their mix of

patients were penalized by losing up

to 1% of their regular payments during

the program’s rst year, scal 2013.

The maximum penalty ramped up to

2% beginning October 2013 and is 3%

beginning October 2014 — rising to 8%

in 2017.

•Medicare Shared Savings Program

(MSSP) ACOs. In December 2013,

CMS named 123 new ACOs as

members of its MSSP, the largest

group announced since the program

started in 2012. These ACOs will cover

1.5 million Medicare beneciaries.

CMS will begin accepting applications

for its 2015 class of MSSP participants

in the summer of 2014.

•Pioneer ACOs. In July 2013, CMS

released the rst-year results from

the Pioneer program, sponsored by

the Center for Medicare & Medicaid

Innovation. All 32 Pioneer ACOs

improved quality, but only 13 were able

to save enough money to share in the

savings with Medicare. In the wake of

these results, nine Pioneers announced

they were dropping out of the program.

Seven of those ACOs planned to

transition to the lower-risk MSSP, while

two left the sea of Medicare ACOs

entirely. CMS is considering opening

the application process to allow more

organizations to join the program.

•Value-Based Physician Payment

Modier (VBPPM). Applied by CMS

to physician performance, the VBPPM

is a method for paying physicians

differentially based on the quality and

cost of their care, as reported through

Medicare’s Physician Quality Reporting

System. Using quality and cost

data reported for 2013, differential

payment is scheduled to begin in 2015

for large group practices and in 2017

will be applied to most or all physicians

who submit claims under the Medicare

physician fee schedule.

Source: CMS, 2014.

13

Since mid-2011, when the Obama

Administration began promoting the

medical home model, the number of

medical home practices has been growing

rapidly (see Chapter 2, page 34). According

to Modern Healthcare, Medicare and

43 other payers, including commercial

plans and state Medicaid programs, are

supporting 500 medical home practices

with per-member, per-month, care

management fees.

Bundled payments

Under the bundled payment model,

sometimes referred to as an “episode

of care” payment, instead of being paid

separately for each individual service,

providers receive one payment for all

services delivered to a patient during a

single episode of care — for example, a hip

replacement or a coronary artery bypass

graft. The payment is made for all services

that the patient is expected to use, from

physician and hospital services to post-

discharge services such as home health

and rehabilitation. Bundled payments

are also applied to treating such chronic

conditions as diabetes, with payments

made in anticipation of all services to be

received in treating the condition over a

dened timeframe.

If the costs of care are less than the

bundled payment amount, participating

providers keep the difference. If costs

exceed payment, they absorb the loss.

Bundled payments give participating

providers an incentive to coordinate their

activities, eliminate unnecessary services

and avoid complications that require

additional services.

In the government payer sector, CMS

has piloted bundled payments through

its Acute Care Episode Demonstration

project and Bundled Payment for Care

Initiative (see Exhibit 1-1 on page 13).

In 2012, bundled payments made their

way into the state-driven Medicaid sector

with the Arkansas Health Care Payment

Improvement Initiative. Currently the

country’s only Medicaid bundled payment

model, it is mandated for state providers

within ve episodes of care.

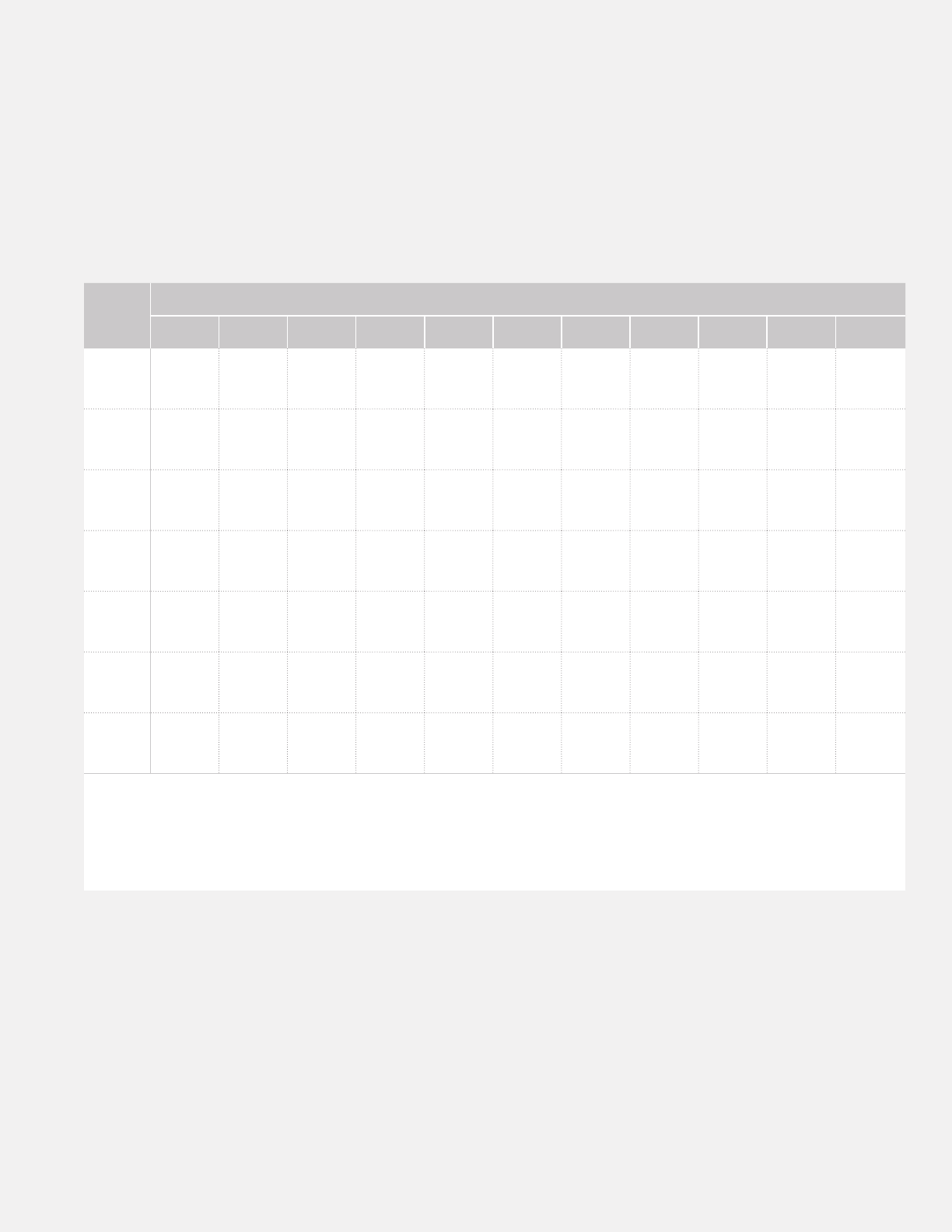

Exhibit 1-2. Spectrum of payment models

Providers are paid

Fee-for-service Pay-for-

performance

Care

management

fees

Bundled

payments

Shared savings

and shared loss

Global

payments

Provider-

sponsored

health plans

A specic price

for each service

rendered

Fee-for-service

payments

plus incentive

payments for

quality and

efciency

Per-member,

per-month

fees — typically

for providers

organized

as patient-

centered

medical homes —

to fund

investments

in care

coordination

One lump sum

for all services

rendered to a

patient during a

hospitalization

or episode

of care — or

to treat a

particular

disease for a

dened time

period

Payments

closely tied to

controlling the

overall cost of

the care that

patients receive

while achieving

quality targets —

sharing in

savings if

costs are less

than target

and sharing in

losses if costs

are greater than

target

A xed dollar

amount, usually

prepaid monthly,

designed to

account for

most or all of

the expected

cost of care

for a group of

patients for a

dened time

period; may be

supplemented

with incentive

payments

for achieving

quality goals

Through

ownership of

the provider’s

own health plan,

assuming 100%

of the nancial

risk for insuring

a patient

population

Less risk, less value More risk, more value

Source: EY analysis, 2014.

14 New horizons: voyage to value

The private payer sector also reects a

wide range of bundled payment initiatives.

For example:

•Geisinger Health System in Danville, PA,

developed its ProvenCare as a bundled

payment model for coronary artery

bypass graft surgery and has since added

additional bundles.

•Horizon Healthcare Services, Inc.,

New Jersey’s oldest and largest health

insurer, started its bundled payment

program with total joint replacements

and has expanded to include such

episodes of care as pregnancy and

adjuvant breast cancer treatment.

•The PROMETHEUS Payment model,

launched in 2006 with the support of the

Robert Wood Johnson Foundation, now

includes 21 bundles with the potential

to affect payment for almost 30% of the

insured adult population.

•Several major national employers

have started their own bundled

payment arrangements with hospitals

(see Value vignette above).

Shared savings and shared loss

In the shared savings and shared loss

model — the payment strategy for such

structures as ACOs — providers are paid

based on achieving dened performance

goals. Those that meet or exceed certain

quality and cost performance benchmarks

can share in any resulting cost savings.

Those that do not meet goals will share

in losses.

Value vignette

Employers Centers of Excellence Network: bundling payments for value

Beginning January 1, 2014, a

rst-of-its-kind coalition of large US

employers — including Lowe’s and

Walmart — began offering knee- and

hip-replacement surgeries to more

than 1.5 million employees and their

dependents. The companies joined

the Pacic Business Group on Health

(PBGH) Negotiating Alliance to create

the Employers Centers of Excellence

Network (ECEN).

According to PBGH, these elective

surgeries represent a growing portion of

employer health care spending. Prices can

vary between $15k and $125k, without

correlation to quality. As of early 2014,

the network is offering these procedures

at four US health care systems:

• Johns Hopkins Bayview Medical Center

in Baltimore, MD

• Kaiser Permanente Orange County-

Irvine Medical Center in Irvine, CA

• Mercy Hospital in Springeld, MO

• Virginia Mason Medical Center in

Seattle, WA

ECEN assists members that want their

employees to have high-quality elective

surgical care by providing information on

which surgeons perform best on these

procedures. The network evaluates and

selects centers of excellence (COEs),

negotiates bundled payments and

encourages member organizations to

promote use of these COEs to their

employees. According to ECEN, each

COE is committed to the highest-quality

standards and has performed far better

than national norms for complications,

reoperations and patient experience.

In addition to total hip and knee

replacements, other elective surgeries

such as spine/low back and cardiac

surgeries will be added. Participating

employers receive discounted rates

for care.

For employees, participation in ECEN is

voluntary. Those who take part receive

100% coverage for their surgical care,

with no deductibles or co-pays, as well as

travel, lodging and living expenses for the

patient and a caregiver. Each employee

is assigned to a patient advocate, who

schedules the surgery and selects the

center. After surgery, the same advocate

assists with insurance claims, as well as

the transition back to the patient’s home

physician. The COE also assigns a patient

navigator to guide the patient while he or

she is on-site.

“[ECEN] is designed to serve as a

model for delivering high-quality

health care with transparent and

predictable costs.”

David Lansky

PBGH President and CEO

Lowe’s and Walmart have tested the

waters before with bundled payments.

Lowe’s entered into a bundled-payment

agreement with Cleveland Clinic for

cardiac surgery, and Walmart and six

hospitals, including Cleveland Clinic and

Mayo Clinic, have launched bundled

payments for workers’ cardiac and

spinal surgeries.

Sources: PBGH website; Walmart website; “Wal‑Mart, Lowe’s, PBGH form network for ‘no‑cost’ knee/hip replacements,” San Francisco Business Times,

October 8, 2013, via The Business Journals, www.bizjournal.com; “Wal‑Mart, Lowe’s to offer employees leg up on knee and hip work — at certain systems,”

Modern Healthcare, October 8, 2013.

15

The concept behind ACOs is that by linking

provider payment to cost and quality

outcomes, the provision of unnecessary

treatments and services is discouraged

while prevention, care coordination, quality

and value are emphasized.

Along with the Medicare Shared Savings

Program and Pioneer ACO program in

the public sector, several commercial

ACO contracts have emerged. Current

estimates (Leavitt Partners, May 2014)

put the number of ACOs in the US at

626; 329 have government contracts,

210 have commercial contracts

and 74 have both government and

commercial contracts. The remaining

13 ACOs have not yet made specic

announcements about their contracts or

are still in the process of nalizing them.

Among recent developments:

•Anthem Blue Cross and Blue Shield plans

to form an ACO with Franciscan Alliance,

a Catholic health care system in Indiana.

•Memorial Healthcare and Florida Blue

have formed a new ACO, Memorial

Health Networks. The ACO marks the

tenth accountable care arrangement

between Florida Blue and hospital

systems throughout the state — and the

fth in south Florida.

•UnitedHealthcare, the Minnetonka,

MN–based health insurer subsidiary

of UnitedHealth Group, plans to more

than double its accountable care

health plan contracts with hospitals

and physicians over the next four

years. UnitedHealthcare currently ties

$20 billion of its contract payments to

quality and cost efciency, and plans

to allocate $50 billion by 2017.

Global payments

A comprehensive payment to a group of

providers, global payments are meant to

account for most or all of the expected cost

of care for a group of patients for a dened

timeframe. These agreements pay on a

per-member, per-month basis. The model

offers providers incentives to keep their

patient populations healthy and maintain

low utilization of clinical services.

While generally synonymous with the term

“capitation,” the term “global payment” is

preferred by advocates to distinguish it

from early capitation models, under which

some providers suffered nancial losses.

Today, global payments have evolved

considerably compared with earlier

efforts. For example, some payers are

using risk-adjustment methods to account

for the relative illness burden of the

population and risk sharing to protect

the provider if costs are higher than

anticipated. This way, providers are not

facing potential catastrophic nancial

losses — or an incentive to curtail care,

acommon concern with early versions

of capitation arrangements. A leading

example of a global payment model is the

Alternative Quality Contract (AQC) from

Blue Cross Blue Shield of Massachusetts

(see Value vignette below).

“Ending fee-for-service payment

in favor of accountable care

organizations and bundled payment

once and for all is unlikely to be

feasible for quite some time, but

gradually increasing disincentives for

providers that do not participate in

reformed payment approaches is a

practical way to move forward.”

Paul B. Ginsburg

President

Center for Studying Health System Change

“Achieving health care cost containment through

provider payment reform that engages patients

and providers”

Health Affairs, May 2013

Value vignette

The Alternative Quality Contract: increasing value through accountability

The Alternative Quality Contract,

apayment model from Blue Cross

Blue Shield of Massachusetts (BCBSMA),

illustrates current trends in payer-

provider cost-saving initiatives. Launched

in 2009, the AQC is one of the largest

commercial payment reform initiatives

in the US. It includes more than three-

quarters of BCBSMA’s overall network

of contracted primary care providers and

specialists who care for nearly 700,000

BCBS members. BCBSMA notes that

the AQC arrangement is a ve-year

agreement that encourages providers

to invest in long-term initiatives —

signicantly longer than BCBSMA’s

traditional contracts, which are typically

three years for hospitals and one year

for physicians.

The model combines a per-patient global

budget with signicant performance

incentives based on nationally endorsed

quality measures. BCBSMA links its

contracts with providers to dozens

of quality metrics that track whether

patients get the right screenings

and exams, whether physicians and

hospitals prescribe the correct drug and

whether patients are satised with their

care. A study nds that this approach

improved quality of care while cutting

costs as much as 10% below their fee-for-

service level.

Source: BCBSMA, http://www.bluecrossma.com/visitor/about‑us/affordability‑quality/aqc.html

16 New horizons: voyage to value

Provider-sponsored health plans

As many health care providers are

assuming risk through new contracts with

payers, others are taking risk-bearing

to a higher level by becoming provider-

sponsored health plans. Financial pressures,

the wave of new entrants in the insurance

market and the move toward population

health have spurred several health systems

to launch their own health insurance plans.

Now isn’t the rst time providers have

taken on the payer side of business.

The most notable example of provider

initiatives in the payer space is California’s

Kaiser Permanente, which started as

a hospital in the 1930s and has since

grown to nearly 8.9 million health plan

members — making it the largest US health

plan by medical enrollment. Today’s four

largest provider-sponsored health plans

after Kaiser, according to data from AIS’s

Directory of Health Plans: 2013, were also

early risk-bearing pioneers: University of

Pittsburgh Medical Center (UPMC) Health

Plan (founded 1998), Healthrst (founded

1993), Henry Ford Health System’s

Health Alliance Plan (founded 1960) and

Spectrum’s Priority Health (founded 1992).

Since the shift to value-based care, the

concept is again attractive to many

providers, who are nding that creating

and offering their own health plans is a

route to achieving competitive advantage.

According to the American Hospital

Association, about one in eight hospitals —

primarily not-for-prot health systems and

nonacademic systems — operated health

plans in 2011.

Recent activity reects the growing trend.

For example:

•In Massachusetts, Partners Healthcare

in Boston, the state’s largest hospital

and physician organization, acquired

Neighborhood Health Plan, a nonprot

organization insuring more than

240,000 mostly low-income residents

across the state.

•In New York, North Shore–Long Island

Jewish Health System — with 16

hospitals and more than 300 outpatient

centers — has launched its own health

plan, CareConnect, on the state health

insurance exchange (HIX).

•In Ohio, Cincinnati-based Catholic Health

Partners is selling health plans through

its subsidiary, HealthSpan, on the

Ohio exchange.

•In Texas, Baylor Scott & White recently

expanded the nonprot Scott & White

Health Plan to portions of Baylor’s

market area, covering more than

240,000 members across 71 counties

in the central part of the state.

•In Virginia, Falls Church–based Inova

Health System has partnered with

Aetna to establish a 50-50 ownership

joint venture, the Innovation Health

insurance plan.

Providers that are considering forming a

health plan need to carefully weigh the

benets against the risks (see Exhibit 1-3).

The quest for efficiency:

controlling costs in a value-

driven world

Regardless of which payment model

organizations adopt or where they are

in their voyage to value, increasing

efciencies and reducing operating costs

are always worthwhile goals. A survey

from the Health Information Management

Systems Society and AVIA (The 2013

Healthcare Provider Innovation Survey)

reveals that while providers have numerous

priorities — from reducing medical errors

to improving patient satisfaction — cutting

costs is still at the top of the list. As margins

tighten for US hospitals, especially for

Exhibit 1-3. Potential benefits and risks for providers considering health

plan formation

Potential benets Potential risks

• Greater nancial rewards. With a

projected drop in inpatient service

utilization, forming a health plan can

help providers hedge against potential

revenue loss.

• Improved market share. Incentives

are created to keep patients within the

system, providing the opportunity for

deeper market penetration.

• Better population health

management. Critical decisions

around what care to provide and what

to pay for are under the provider’s

control. With more tightly integrated

clinical and nancial performance

data and metrics, health systems

may be better positioned to improve

outcomes and lower costs around

specic patient populations.

• High start-up costs. Providers need to

have enough funds to cover start-up

costs and regulatorily required capital

thresholds, and enough potential

covered lives to absorb actuarial and

other risks.

• Payer pull-outs. Hospitals that

start their own health plans will be

competing with other plans in their

markets. Commercial payers may

choose to end contracts, posing a new

set of challenges for hospitals.

• New responsibilities. Changing from

being a provider to being a provider-

payer will require a different mindset,

skill set and knowledge base with a

corresponding learning curve.

Source: EY analysis, 2014.

17

those with higher levels of Medicaid and

Medicare patients (see Exhibit 1-4), hospital

executives are using a range of strategies

to control costs. Highlighted below are

prevalent approaches.

Readmission reduction

Nearly one in ve Medicare patients

returns to the hospital within a month

of discharge. From the government’s

vantage point, readmissions are a leading

symptom of inadequate quality and a

costly, uncoordinated system. The ACA

charged the Department of Health and

Human Services (HHS) with creating

the Hospital Readmissions Reduction

Program, effective for discharges beginning

October 1, 2012. With an initial penalty

rate of 1% of Medicare payments for

failure to substantially reduce readmission

rates, the penalty continues to rise (see

page 13). CMS reports an estimated 2,225

hospitals were penalized $227 million in

2013 because of excess readmissions.

What are the causes of unnecessary

readmissions? A seminal report from

the Robert Wood Johnson Foundation

highlights a variety of catalysts

(see Exhibit 1-5 on page 20).

A scan of the health care horizon nds a

range of cost-effective solutions to reduce

readmission rates. For example:

•In California, Napa’s Queen of the

Valley Medical Center uses the Case

Management, Advocacy, Resource/

Referral, Education (CARE) Network,

through which a social worker and

nurse visit patient homes to make

sure the patient understands post-

discharge care plans. Over a one-year

span, the CARE program yielded a

60% reduction in ED visits and a 40%

reduction in hospitalizations for the

patient population.

•In Ohio, Cincinnati’s Mercy Health has

used nurses specially trained to act as

patient guides through the discharge

process. In less than a year, the

program has yielded savings in avoided

readmissions of about $495,000 and

a 15% drop in all-cause readmission

rates for heart failure, acute myocardial

infarction and pneumonia.

•In Utah, Salt Lake City’s University of

Utah Health Care hired a hospital-based

transitions navigator to help patients

transition safely from hospital to medical

home. Over three months, the program

yielded a 23% reduction in the hospital’s

30-day readmission rate.

To prevent hospital-acquired infections

(HAIs), a major cause of readmission, many

providers are implementing automated

infection control and patient surveillance

systems. These systems provide real-time

alerts, pushing time-sensitive patient

information directly to the treating

physician to act quickly in reducing adverse

events. Studies have found 10%–70%

of HAIs could be prevented through

systematic surveillance and standard

preventive guidelines.

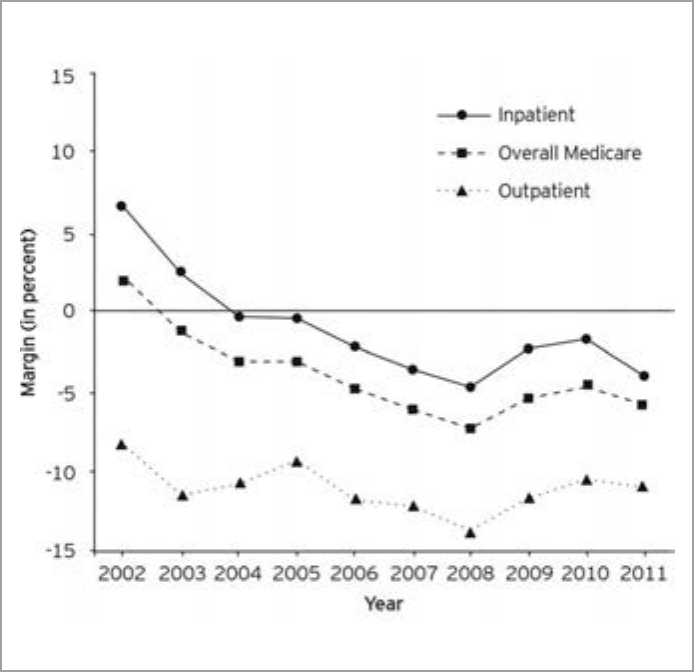

Exhibit 1-4. Trending of Medicare margins

Source: Medicare Payment Advisory Commission (MedPAC) report, March 2013.

18 New horizons: voyage to value

19

Patient flow improvement

Regardless of how many hospital beds are

available, inefcient processes, inadequate

care transitions and a eet of other

challenges can lead to poor use of capacity.

Patient-ow problems not only create

operational bottlenecks, but they often

set the course for patients’ perceptions of

their entire stays. If the hospital encounter

starts with a long wait to get a bed, the

hospital may already have lost the battle

for delivering a positive patient experience.

Providers nationwide are taking action

to address the patient-ow challenge.

For example:

•In Connecticut, Yale-New Haven Hospital

implemented process changes that led

to an 84% improvement in discharges by

11:00 a.m., a decreased length of stay

from 5.23 to 5.05 days and the ability

to accommodate 45 additional patients

each day.

•In Ohio, Cincinnati Children’s Hospital

Medical Center improved surgical

scheduling practices, resulting in fewer

delays and cancellations of elective

surgeries because beds were not

available, as well as a more predictable

ow of patients through the intensive

care unit. The changes also saved the

facility $100 million in capital costs by

eliminating the need for 75 new beds.

•In Washington, at Seattle-based Virginia

Mason Health System, nurses analyzed

their workows and took steps to

improve efciency. A key change was

reorganizing nurses’ care patterns on

the hospital oor so that they could

care for patients who were in groups of

rooms rather than spread across a unit.

In areas where this change has been

implemented, Virginia Mason reports its

nurses now spend 90% of their time on

direct patient care and attend to patients’

needs faster and more effectively.

A key area of focus for improving patient-

ow is the Emergency Department.

Automated patient-ow solutions are

helping relieve ED overcrowding by

speeding up throughput processes.

To reduce heavy patient volumes in the

ED, some health care systems have also

created transfer centers — hubs for patient

referrals between the system and all the

clinics, hospitals and physician ofces in

the region. These centers enable referring

providers to make one phone call to send

their patients directly from their facilities

to the appropriate level of acute care,

bypassing an unnecessary ED visit. Patients

can readily receive the care they need, while

hospitals can decrease the number of patients

entering the hospital through the ED.

Supply chain retooling

On average, the supply chain represents the

second-highest component of a hospital’s

operating costs — eclipsed only by the

cost of labor. More and more hospitals

are recognizing the value that the supply

chain can bring to their organizations and

have moved to add supply chain strategic

initiatives to their overall goals. Approaches

range from rightsizing inventory, to joining

purchasing collaboratives for best-price

negotiation, to building and automating

warehouses and ordering directly from

manufacturers. For example:

•In Arizona, Phoenix-based Banner Health

saved $226 million in ve years by

aligning supply chain management with

efforts to improve quality, remove waste

and disseminate best practices.

•In Florida, University of Florida and

Shands Teaching Hospital in Gainesville

are collaborating with Orlando Health

in joint supply purchasing decisions —

resulting in millions of dollars in savings

for both organizations.

•In Mississippi, Meridian’s Anderson

Regional Medical Center rightsized its

inventory levels and gained savings

of $1.5 million.

Exhibit 1-5. What leads to needless hospital readmissions?

1. Some patients leave the hospital with

a treatment plan for one illness when

other problems of equal importance

are ignored.

2. Many patients are discharged without

understanding their illnesses or

treatment plans or they inadvertently

discontinue the medicines needed to

stay well.

3. Family members who may be the

patient’s central caregivers are often

not included in discharge planning.

4. The physicians caring for the patient

may not communicate with each other

or may not develop a coordinated plan

for care after discharge.

5. Patients may not have the right

prescriptions or cannot ll them.

6. Appointments with primary care

clinicians or with specialists may not

occur soon enough after discharge.

Missed clinician visits lead to missed

opportunities to recognize that the

patient is not improving.

7. Information about a patient’s hospital

stay does not always go to the

appropriate community clinicians.

8. Clarity is lacking on which clinician

is responsible for care after patient

discharge; accountability is spread

among hospital staff, community

physicians and nurses, skilled nursing

facilities and families. Without clear

accountability, problems that could be

prevented are missed, leading to ED

visits and repeat hospitalizations.

Source: The Revolving Door: A Report on U.S. Hospital Readmissions, RWJF, February 2013.

20 New horizons: voyage to value

Many hospitals have found the most

effective way to reduce costs for

those supplies over which physicians

have the greatest inuence, such as

implants, medical devices and high-cost

pharmaceuticals, is to involve them

vigorously in cost-saving initiatives.

“Hospitals have got to start engaging

the right executives and physicians

and share data with them. They’re

scientists by nature. You’ve got

to give doctors input on what is

being used.”

Brent Johnson

Vice President of Supply Chain & Support Services

Intermountain Healthcare

Healthcare Finance News, September 2013

Revenue cycle re-engineering

From offering online scheduling to issuing

easy-to-understand bills, the revenue

cycle presents a distinct opportunity to

make the transactional side of health care

more nancially sound for providers — and

more satisfying for patients. The goal is

to transform the process from reactive to

proactive, from one that begins after the

patient receives care to one that starts

with the patient’s rst interaction with the

provider organization.

Forward-thinking providers are unlocking

the value in their revenue cycles by

becoming more patient-centric at all patient

touch points. They are empowering patients

through self-service communication tools

such as patient account portals, scheduling

apps and registration kiosks; using

analytics to improve processes and patient

communications; keeping patients informed

of, and prepared for, their nancial

obligations; and making the billing process

more consumer friendly. For example:

•In Nebraska, Omaha’s Bergan Mercy

Medical Center offers “My Cost,” a

customized, online tool. Patients can

obtain out-of-pocket cost information

By the numbers

• Without major health care redesign

or intervention, by 2022, health care

costs in the US could make up as much

as 19.9% of GDP — up from 17.2%

in 2012 (source: CMS, 2014).

• According to an annual survey of

governance structure and practices

in the nation’s nonprot hospitals and

health systems, 52% of respondents

have added value-based payment

goals to their strategic and nancial

plans (source: Governance Institute,

2013 biennial survey).

• The US health care system wastes

30 cents of every dollar spent

(source: IOM, 2012).

• The number of physicians accepting

new Medicare patients increased by

3% between 2007 and 2012 and is

higher than the number of physicians

accepting new private insurance

patients (source: HHS Ofce of the

Assistant Secretary for Planning

and Evaluation).

• Family premiums increased 4% in

2013, the same as in 2012, and

individual premiums increased 5%

versus 3% in 2012 (source: Kaiser

Family Foundation, “2013 Employer

Health Benets Survey”).

• High-deductible plans can reduce

health care costs by 5% to 14%

(source: Robert Wood Johnson

Foundation, 2012 report).

• A recent study nds that although

20% of health plans say value-based

payment models support more

than half of their business today,

60% of respondents anticipate they

will support more than half their

business within ve years (source:

Availity, “Health Plan Readiness to

Operationalize New Payment Models,”

May 2013).

• A recent survey nds that only 14%

of adults understand basic insurance

(source: Carnegie Mellon survey,

July 2013).

• Despite increasing health care costs,

less than 15% of internal medicine

residency programs feature curricula

aimed at teaching residents to

be more cost-conscious (source:

Journal of the American Medical

Association (JAMA), research letter,

December 27, 2013).

• 5% of all inpatients will develop a

hospital-associated infection — at an

average cost of tens of thousands of

dollars (source: Agency for Healthcare

Research and Quality (AHRQ), 2014).

• The $2.4 billion hospital revenue cycle

management industry for software

and services is expected to see double-

digit increases in 2014 (source: Black

Book Rankings LLC, 2013).

• Patients satised with hospital

billing processes are ve times more

likely to recommend the hospital

to a friend (source: Connance,

December 14, 2011).

• A cost analysis of more than

10.2 million patient discharges for

various conditions revealed that,

at 24.2% of costs, supplies and

devices were the leading contributors

to the increase in average cost per

discharge — surpassing intensive

care unit charges, imaging and other

advanced technological services

(source: Jared Lane Maeda, PhD,

et al., “What Hospital Inpatient

Services Contributed the Most to the

2001 to 2006 Growth in the Cost Per

Case?” Health Services Research,

August 29, 2012).

21

Value vignette

An employer view on value: exploring leading practices

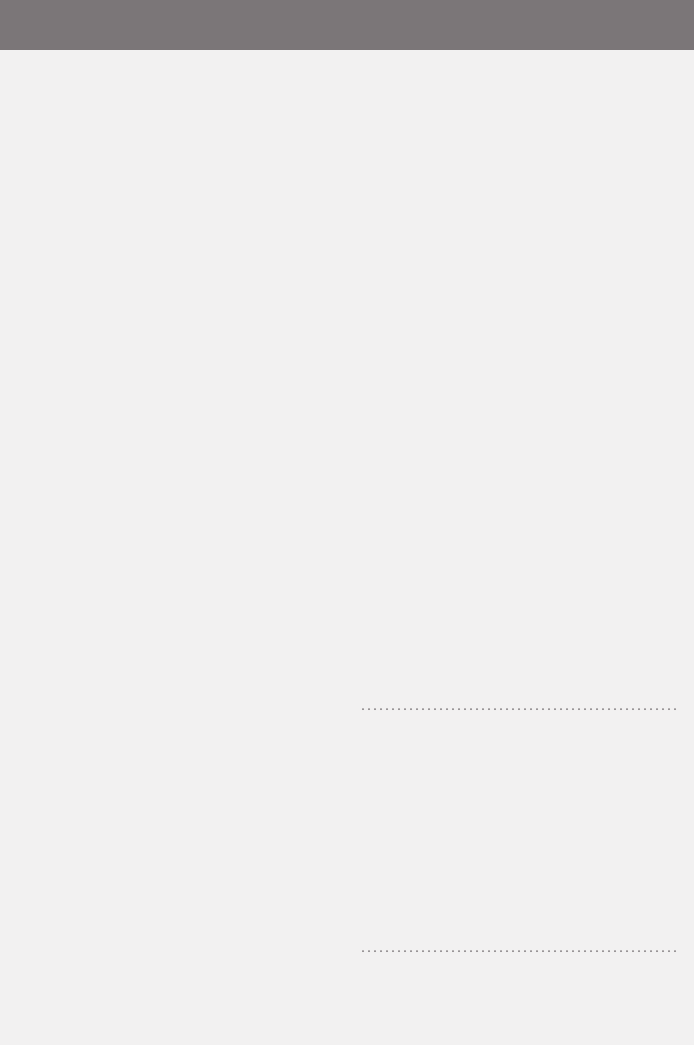

The Towers Watson/National Business

Group on Health Employer Survey on

Purchasing Value in Health Care, now

in its 19th year, tracks strategies and

practices employers are using in the quest

for health care value. The 2014 report,

The New Health Care Imperative: Driving

Performance, Connecting to Value,

proles the activities of high-performing

companies, as well as current trends in

the health care benet programs of US

employers with at least 1,000 employees.

The survey was completed by 595

employers between November 2013 and

January 2014. Respondents collectively

employ 11.3 million full-time employees,

have 7.8 million employees enrolled in

their health care programs and represent

all major industry sectors.

The survey found that employers are

committed to providing subsidized health

care benets to active employees —

even in an environment of continued

health care cost increases, uncertainty

about some provisions of health care

reform and a slow-to-recover economy.

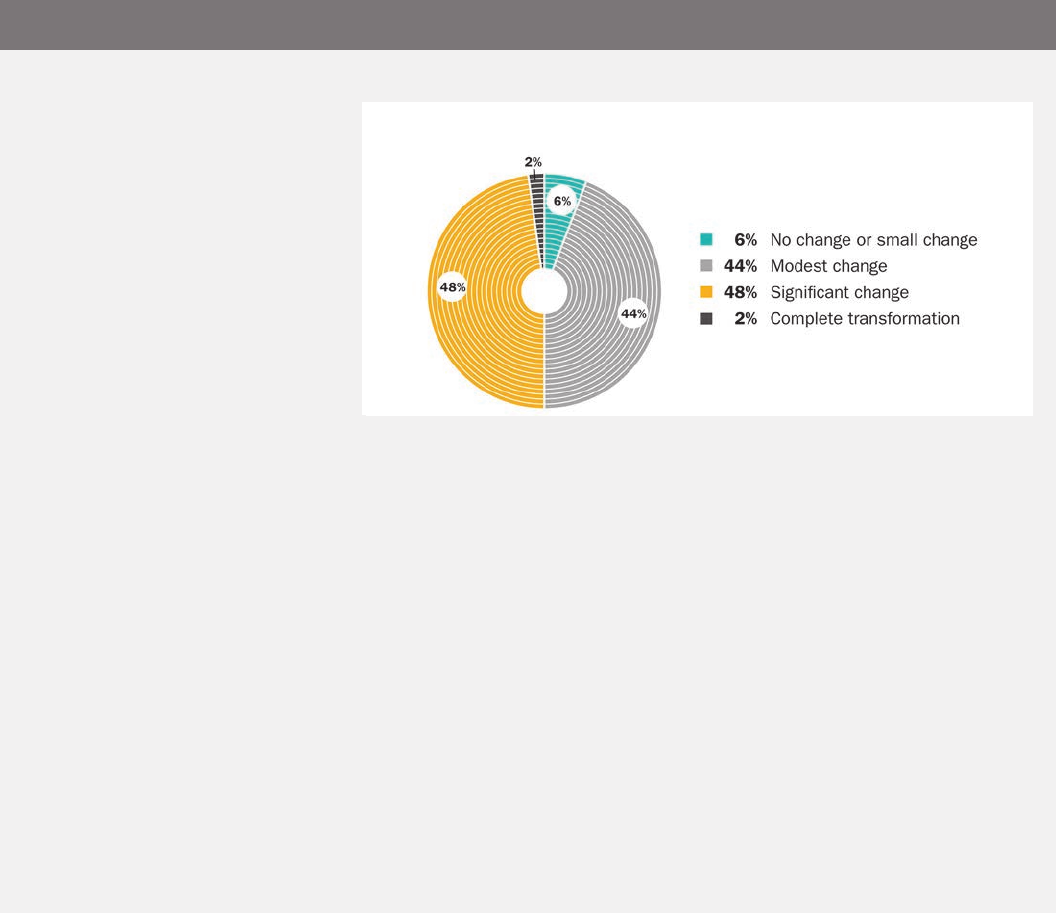

Yet 94% of respondents expect employer-

sponsored health care benets to undergo

modest or major changes over ve

years’ time (see chart).

Survey responses indicate that employers

are taking steps to derive the most value

from their health benet programs. In the

view of the report’s authors, employers

who want their health plans to stay

viable over the long term will need to

take a holistic approach that includes

ve key steps:

1. Optimize benet delivery channels.

Improve self-managed programs and

explore alternatives such as private

exchanges or hybrid arrangements.

2. Restructure benets. Consider

offering new plan options, redesigning

benets, recalibrating contribution

strategy and tier structures, and linking

health savings account strategies

with your approach to retiree

health benets.

3. Enhance network and value-

based contracting. Reduce unit

costs, and improve efciency,

quality outcomes, and risk-transfer

arrangements to providers.

4. Focus on population health

management. Improve chronic-

condition management, reduce risk

factors and improve care gaps.

5. Engage employees and improve

their accountability. Use quality and

transparency tools, point-of-care

cost-sharing designs, account-based

strategies and incentive approaches.

Source: Towers Watson, www.towerswatson.com/en‑US/Insights/IC‑Types/Survey‑Research‑Results/2014/03/towers‑watson‑nbgh‑employer‑survey‑on‑purchasing‑value‑

in‑health‑care

Nearly all employers anticipate signicant or modest changes in health benet

programs by 2018

22 New horizons: voyage to value

for specic medical tests or procedures,

customized to their insurance

plan designs.

•In Ohio, Riverside Methodist Hospital in

Columbus has made nancial counseling

a priority in its revenue cycle, including

all patient accounts in one seamless

discussion of patient responsibility and

nancial aid resources, as opposed to

discussions with every visit. Hospital

executives report Riverside has increased

point-of-service collections by an average

of $50,000 per month.

•In Oklahoma, Saint Francis Hospital,

the agship facility for Tulsa’s Saint

Francis Health System, has taken steps

to limit how often it asks for patient

information and to integrate registration

systems throughout the organization

so that — regardless of setting — patient

information can be collected in a

unied way.

In a value-based world, creating a positive

care experience is integral not only to

building lasting patient relationships

but also to maintaining a healthy cash

ow. Putting the patient at the center of

the revenue cycle brings an unparalleled

opportunity to generate loyalty today — and

provide for viability tomorrow.

No turning back: sailing

to tomorrow

US health care is at a pivotal point in its

journey. The realities of rapidly surging

health care costs, attening Medicare

reimbursement and the rising tide of

demand for services from the newly insured

are forcibly coming together, leaving

the industry with no easy route to make

headway toward the new horizon. Most

agree the best course forward is to continue

to pursue value-based approaches — while

looking carefully within to better manage

operating costs. The conditions are often

uncertain. Yet for those whose sails are well

set, the voyage to value can be a perfect

opportunity for creating a stronger, more

efcient and more resilient organization.

Our chapter concludes in a conversation

with Harold Miller, who leads the Center for

Healthcare Quality and Payment Reform.

He offers his viewpoint on which payment

models are the most effective in delivering

long-term value.

Value vignette

Capacity management: reducing bottlenecks for a better patient experience

A recent study from software provider

Central Logic — featuring input from

such health care leaders as UPMC,

Dartmouth-Hitchcock and Memorial

Sloan-Kettering — offers six tips for how

hospitals can better manage capacity to

reduce length of stay and improve the

patient-care experience:

1. Focus on accurate patient placement.

Conrm that patients are in the right

bed, at the right level of care, at the

right time.

2. Conduct daily, multidisciplinary

rounds and bed meetings. Make

sure care teams work cohesively,

appropriate tests are ordered,

procedures are completed promptly,

discharge plans are followed and

capacity is optimized.

3. Discharge patients as soon

as possible, at any time of

the day. Focus on helping patients

reach discharge as quickly as is

clinically feasible.

4. Smooth patient census. Look at peak

census patterns by time of day and

day of week. Consider scheduling

elective surgeries on weekends to

relieve congestion, free up resources

and reduce length of stay.

5. Communicate consistently with

staff and patients. Streamline

communication through case

managers to facilitate communication

across silos. Help patients manage

expectations for length of stay.

6. Measure and distribute the correct

metrics. Evaluate such indicators as

30-day readmission rates, average

daily admits, observation volumes,

case mix index and length of stay by

diagnostic group against the impact

on your organization’s overall capacity

management. Discuss metrics to

ensure hospital administrators

understand data implications for

optimizing capacity.

Source: Central Logic, www.centrallogic.com/check-gate resource?le=/public/uploads/global/2013/10/

CapacityManagementSixThoughts.Final.pdf

23

Accountable payment

models: paying to

support higher-quality,

lower-cost health care

A conversation with Harold D. Miller,

President and CEO, the Center for

Healthcare Quality and Payment

Reform (CHQPR) (www.chqpr.com)

Harold Miller is a nationally recognized

expert on health care payment and

delivery systems and has worked with

the federal government and several

states and regions in designing and

implementing system reforms. Along

with his role in leading CHQPR, he

also serves as adjunct professor of

public policy and management at

Carnegie Mellon University. We talked

with him about how new payment

models can improve the quality of

care for patients, lower costs for

employers and improve the nancial

viability of health care providers.

You have said that the biggest need in

health care today is to change the way

doctors and hospitals are paid, and the

second-biggest need is to change the

benefit designs for patients. Why are

these the greatest concerns? And how

should we address them?

Both the public and private sectors need

to nd a way to control health care

spending — but to do it without harming

patients. The biggest barrier to higher-

quality, lower-cost care is that we don’t pay

physicians and hospitals for many services

that would help patients stay well, and the

fee-for-service payment system penalizes

providers nancially for achieving better

outcomes and avoiding unnecessary tests

and procedures.

Patient benet designs also tend to do just

the opposite of what is needed to support

higher-quality, lower-cost care. High cost-

sharing and high deductibles discourage

people from getting services that will

help them stay healthy, such as seeing a

primary care physician early when they

have a health problem and taking their

medications regularly. On the other hand,

if patients need an expensive procedure,

such as a knee replacement or a cardiac

stent, they will likely pay the same amount

whether they go to a high-cost provider

or a low-cost provider, because the cost

is typically well above their deductible or

out-of-pocket limit. So if they believe that

higher cost means higher quality (even

though evidence shows it doesn’t), they will

have a natural incentive to use the higher-

cost provider.

We need to start paying doctors and

hospitals for keeping patients healthy and