Set In Georgia 50pt WFC CLO Style Guide

User Manual: Pdf

Open the PDF directly: View PDF ![]() .

.

Page Count: 34

- The Guide to the CLO Style Guide

- Slide Number 2

- Slide Number 3

- Slide Number 4

- Slide Number 5

- Slide Number 6

- Slide Number 7

- Slide Number 8

- Slide Number 9

- Slide Number 10

- Slide Number 11

- Slide Number 12

- Slide Number 13

- Slide Number 14

- Slide Number 15

- Slide Number 16

- Slide Number 17

- Slide Number 18

- Slide Number 19

- Slide Number 20

- Slide Number 21

- Slide Number 22

- Slide Number 23

- Slide Number 24

- Slide Number 25

- Slide Number 26

- Slide Number 27

- Slide Number 28

- Slide Number 29

- Slide Number 30

- Slide Number 31

- Slide Number 32

- Slide Number 33

- Slide Number 34

The Guide to the CLO Style Guide

October 10, 2017

David Preston, CFA

CLO and Commercial ABS Research

(704) 410-3080

david.preston@wellsfargo.com

Geoff Horton, CFA

CLO and Commercial ABS Research

(704) 410-3352

geoffrey.horton@wellsfargo.com

Mackenzie Miller

CLO and Commercial ABS Research

(704) 410-3358

mackenzie.miller@wellsfargo.com

Please see page 32 for the rating definitions, important disclosures and

required analyst certifications. 10/10/17 at 3:00 p.m. ET

This report is available on wellsfargoresearch.com and on Bloomberg WFRE

All estimates/forecasts are as of 10/10/17 unless otherwise stated.

Contents

2

Introduction Min. OC Cushion

Overview / Caveats 3Summary 18

Metric Summary Table 5History / Common Metric Pairings 19

WAS Caa/CCC

Summary 6Summary 20

History / Common Metric Pairings 7History / Common Metric Pairings 21

WARF 2nd Lien Exposure

Summary 8Summary 22

History / Common Metric Pairings 9History / Common Metric Pairings 23

Adj. NAV < 80 Exposure

Summary 10 Summary 24

History / Common Metric Pairings 11 History / Common Metric Pairings 25

Diversity Score Wt. Avg Bid Depth

Summary 12 Summary 26

History / Common Metric Pairings 13 History / Common Metric Pairings 27

Normalized Eq. Pmt MV NAV

Summary 14 Summary 28

History / Common Metric Pairings 15 History / Common Metric Pairings 29

Leverage BB MVOC

Summary 16 Summary 30

History / Common Metric Pairings 17 History / Common Metric Pairings 31

We present The Guide to the CLO Style Guide, a companion to our monthly CLO

Manager Style Guide.

We believe that evaluating manager performance should always be viewed within the

appropriate context. This report intends to give investors the tools needed to evaluate

the CLOs in their respective portfolios.

We provide descriptions and strengths/weaknesses for 14 different metrics. Investors

may prioritize certain performance metrics; using these metrics, investors can

evaluate holdings using market and manager data for a specific metric.

The data are only a snapshot (based on each deal’s most recent Intex update), yet

investors can also use the data to infer prior tactical or strategic maneuvers.

Investors can compare relative position within various metrics. We urge investors not

to focus on the specific number; differences can be small.

CLO Style Guide Data: Overview and Caveats

3

In addition to the individual strengths and weaknesses listed, we also note that ALL the

metrics listed are subject to the following drawbacks:

All the data are a snapshot - as of the latest Intex update within the three months prior to the

Style Guide (with the exception of price data, leverage and equity payment data), and does not

account for the starting point or the path taken to the current point.

Therefore, the managers’ style may have changed over time. A manager could have had a high-

spread portfolio in 2014 but have since rotated to lower-spread assets.

Deals with lower OC cushions may have been issued with tighter cushion.

Similarly, loans <80 do not account for purchase price. A manager may have purchased loans

at 50 versus purchasing the loans at new issue.

All the metrics are averages, and may mask distortions, such as barbelling.

All the data are subject to vintage biases – for example, 2016 deals have a very different profile

than 2013 or 2014 deals. Therefore, if a manager’s outstanding deals are overweight one vintage,

their data may be skewed.

We believe that even given these drawbacks, the metrics, when combined, can provide a

directional look at manager style / performance.

4

CLO Style Guide Data: Overview and Caveats

Metric Description Curr. Mkt Avg. Strength Weakness

WAS

The calculated Wt. Avg Spread of the portfolio – giving

no credit for LIBOR or for LIBOR floors

357

Straightforward - loan market's perception of

risk expressed as average coupon

Does not account for liquidity

May not match CLO reported WAS

WARF

Measures the weighted average Moody's rating of

the assets.

Lower WARF = Higher average credit rating

Higher WARF = Lower average credit rating

2802

Commonly used, expresses average rating of

portfolio

Assumes ratings are a good proxy for risk

May not be calculated the same way across all deals

Adj. NAV

Adj. NAV is the equity NAV of the CLO, but not carrying

all loans at their current market value.

Calculated using loans trading at 85+ carried at par; 75 -

85 = 80; and < 75 = 65.

67.1%

Compensates for weaknesses of liquidation NAV

and par based NAV

Less intiutive;

Does not adequately punish very low priced loans (< 50)

NAV is affected by vintage and how notes/equity are sold at new issue

Div.

Moody’s diversity score: based on how many assets,

how many industries and how big the positions are. A

par weighted calculation that indicates collateral

concentration in terms of both issuer and industry

concentration.

74

Commonly used measure of portfolio

concentration

Diversity score may not be correlated with credit quality

Industry classifications may not be standardized

Norm. Eq. Pmt

The total sum of all equity payments made during

reinvestment, converted to an average quarterly

payment. Equity distribution is the quarterly equity

payment divided by the equity notional value.

4.3%

Looks at avg equity pmt over time

Adjusts for the fact that the first equity pmts

often differ in payment period length, and

differing first pmt periods can produce high or

low first pmts

Does not account for debt cost or vintage differences

Not adjusted for refi/ reset, which can affect equity NAV & payments

Lev.

Leverage provided by CLO structure; Total initial deal

balance / equity notional balance.

10.8

Easy to calculate in Intex

Uses equity notional balance - similar to equity

pmt data

Based on structural leverage, not actual asset leverage, which

technically would be more accurate

Min. OC

Difference between actual OC level and OC Test limit

for the tightest OC test in the deal (not including Int.

Diversion tests – only true OC tests)

419

Intuitive & commonly used

Lower OC cushion are typically indicative of

losses or stressed assets

Does not account for initial structuring or OC calculation differences

Only a snapshot; does not show OC gained or lost

Caa/CCC

Intex’s fields show % of the portfolio rated Caa or

below, and the % of the portfolio rated CCC or below

4.3% / 3.8%

Intuitive & commonly used

Quick measure of lower rated assets

May be calculated differently from deal to deal Also, the data reported

in Intex may refer to concentration limits, not to Excess Caa or Excess

CCC Test levels used for OC test calculation

May not include data from deals not rated by that rating agy

2nd Lien

The percent of 2nd lien loans held by the CLO 1.77 The percent of 2nd lien loans held by the CLO Not much differentiation; may not serve as a stand alone proxy for risk

<80

Average # of loans in the pool that have current

market prices below 80

2.4%

Current data on loan market's view of more

likely default candidates

Commonly used metric for tail risk in CLO

portfolios

Does not account for purchase price

At times, $80 may be not be the right cut-off price

Bid Depth

Weighted average of the # of bids on the loans in the

CLO portfolio.

4.9

Proxy for liqudity of underlying loans - which

can be used as a proxy for holdings of smaller

or "lightly syndicated" loans

Does not account for quality/size of bids in the market

NAV

Equity Net Asset Value; the current liquidation valueo

of the portfolio, less outstanding note balance.

58.0% Commonly used metric for equity valuation

CLO is not a mark to market vehicle; liklely is only an estimate of true

liquidation value due to transaction costs and management fees senior

to equity.

NAV is affected by vintage and how notes/equity are sold at new issue

BB MVOC

The Market Value OC Ratio of the BB notes (Portfolio

liquidation value coverage of BB notes)

107.0 Commonly used metric CLO is not a mark to market vehicle

CLO Metric Summary

5

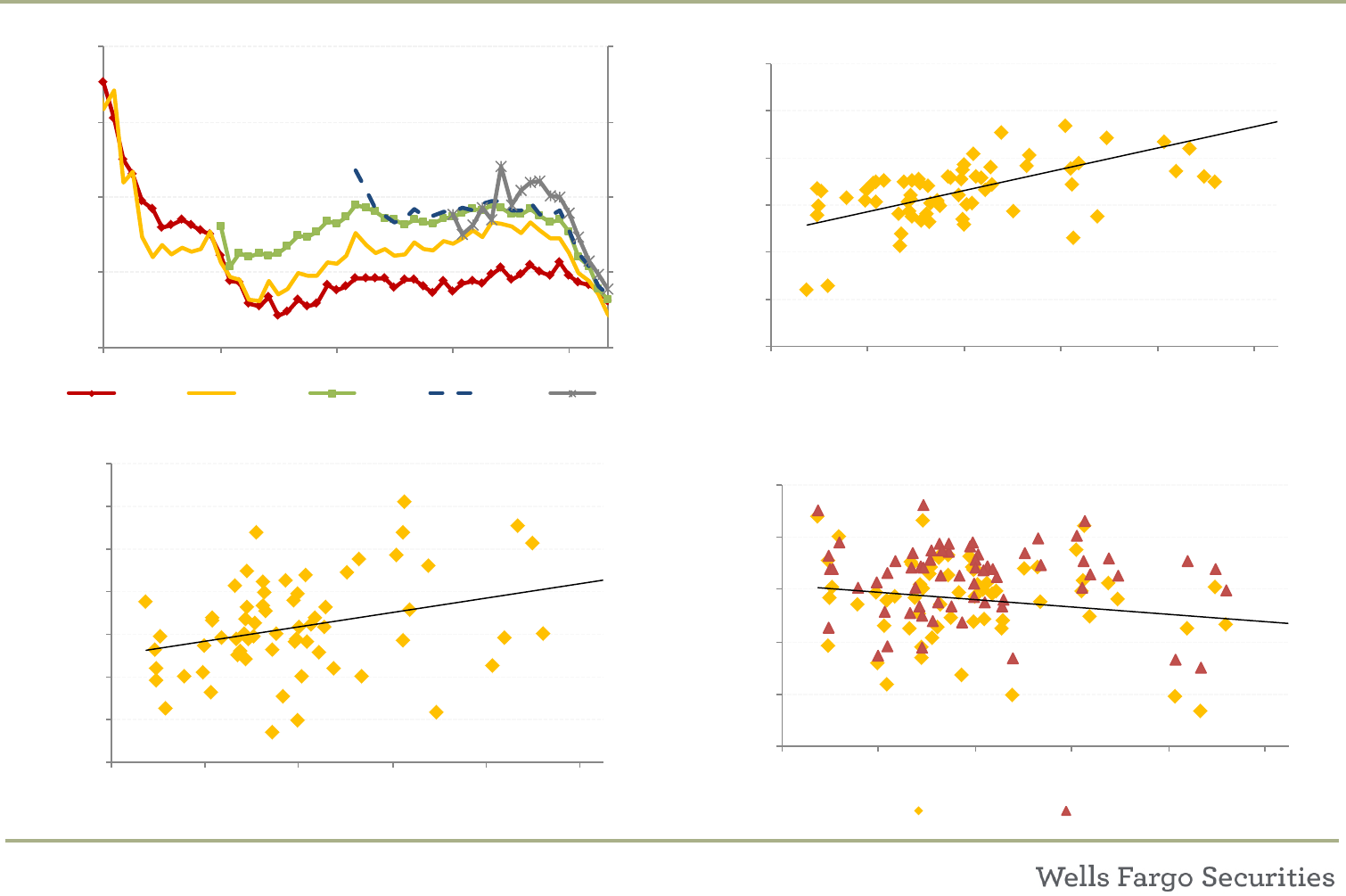

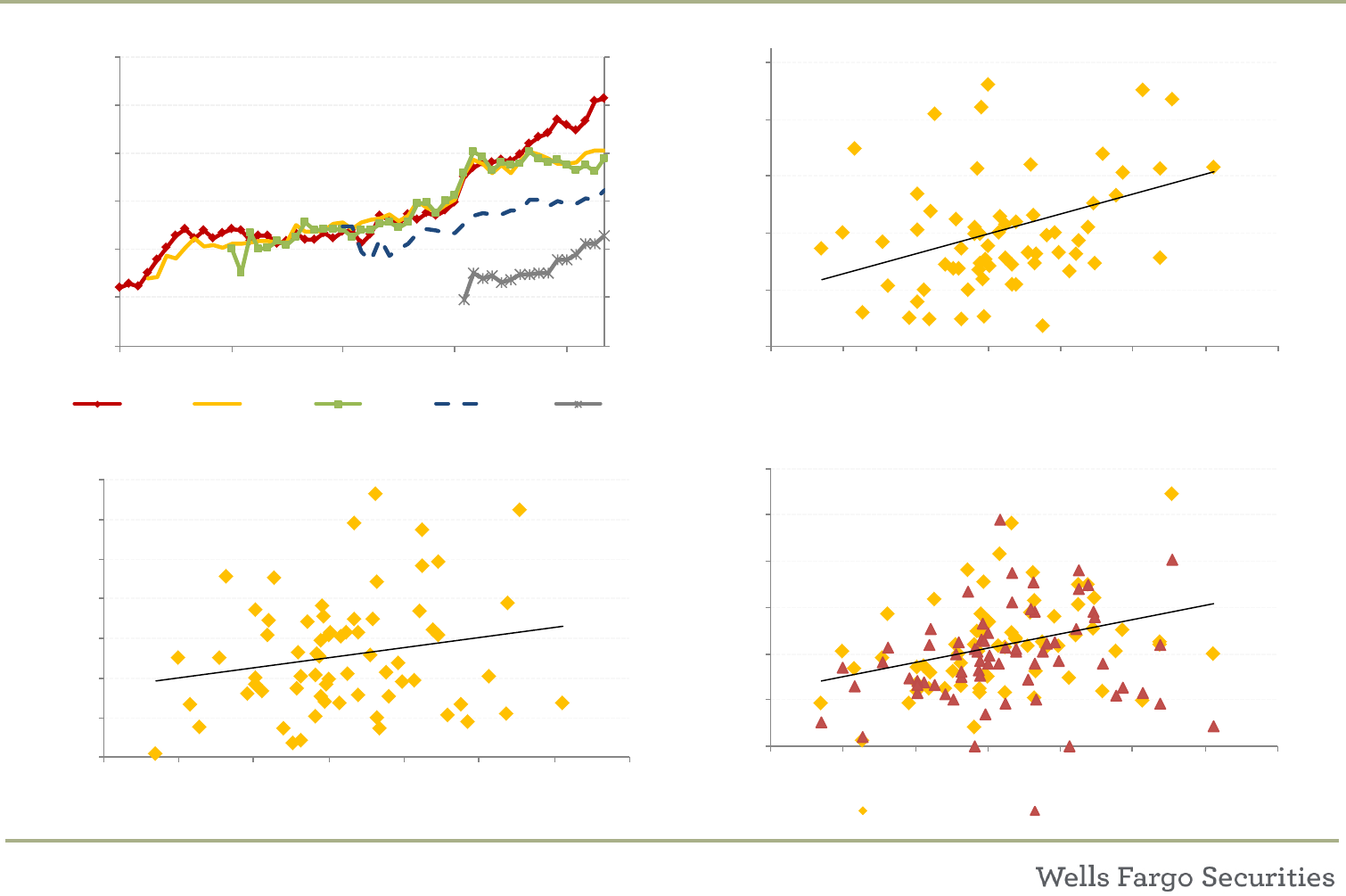

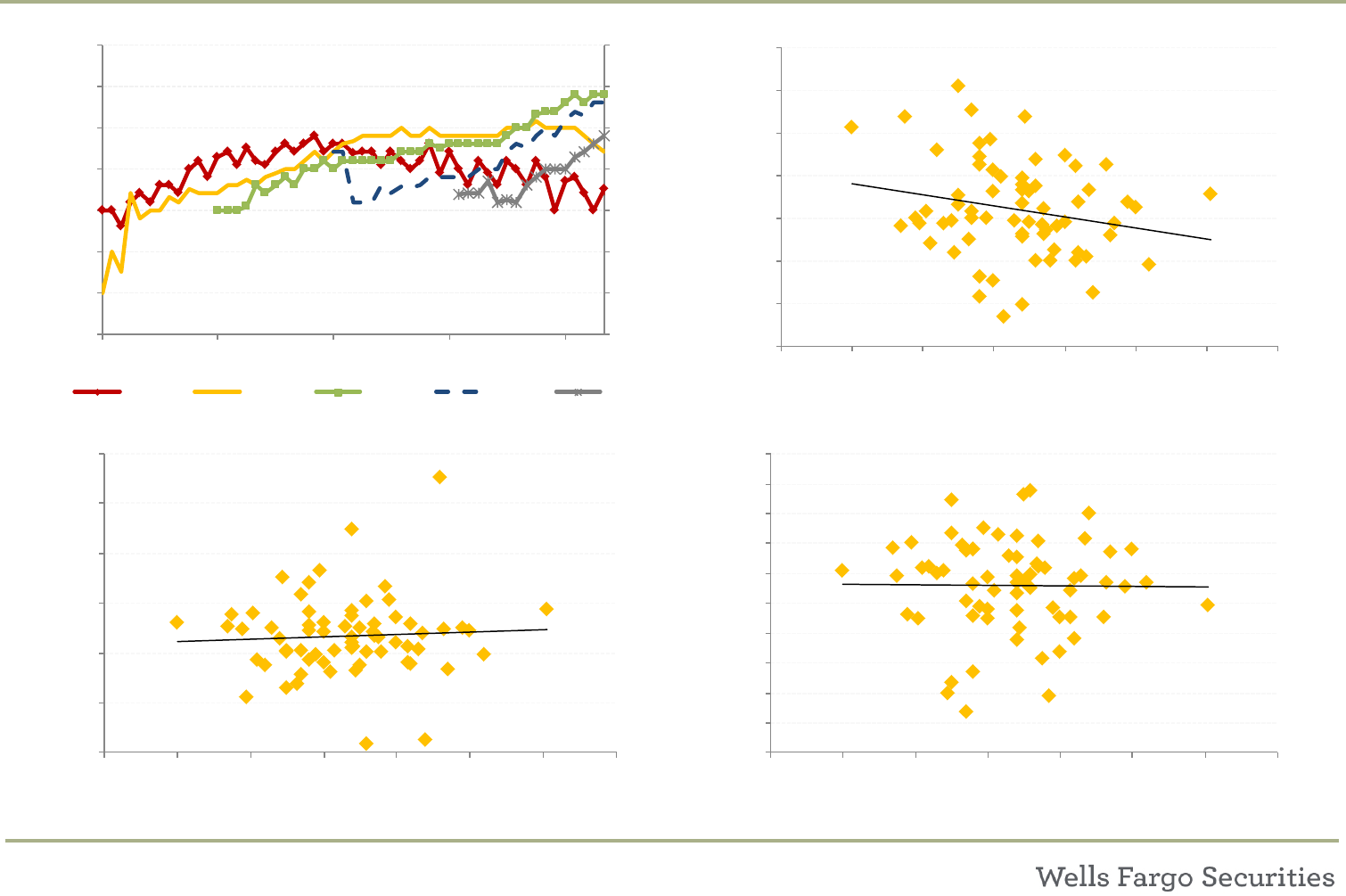

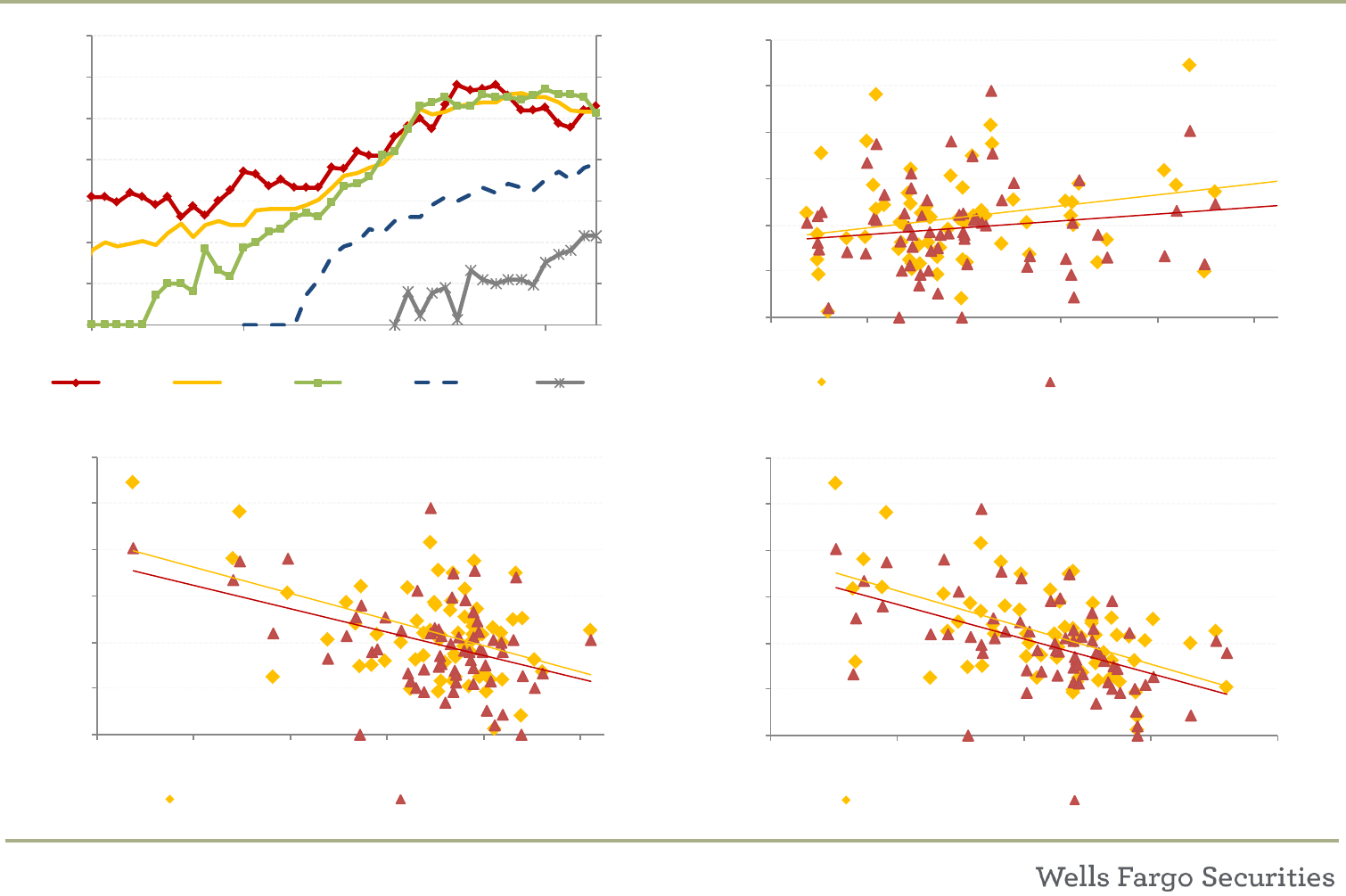

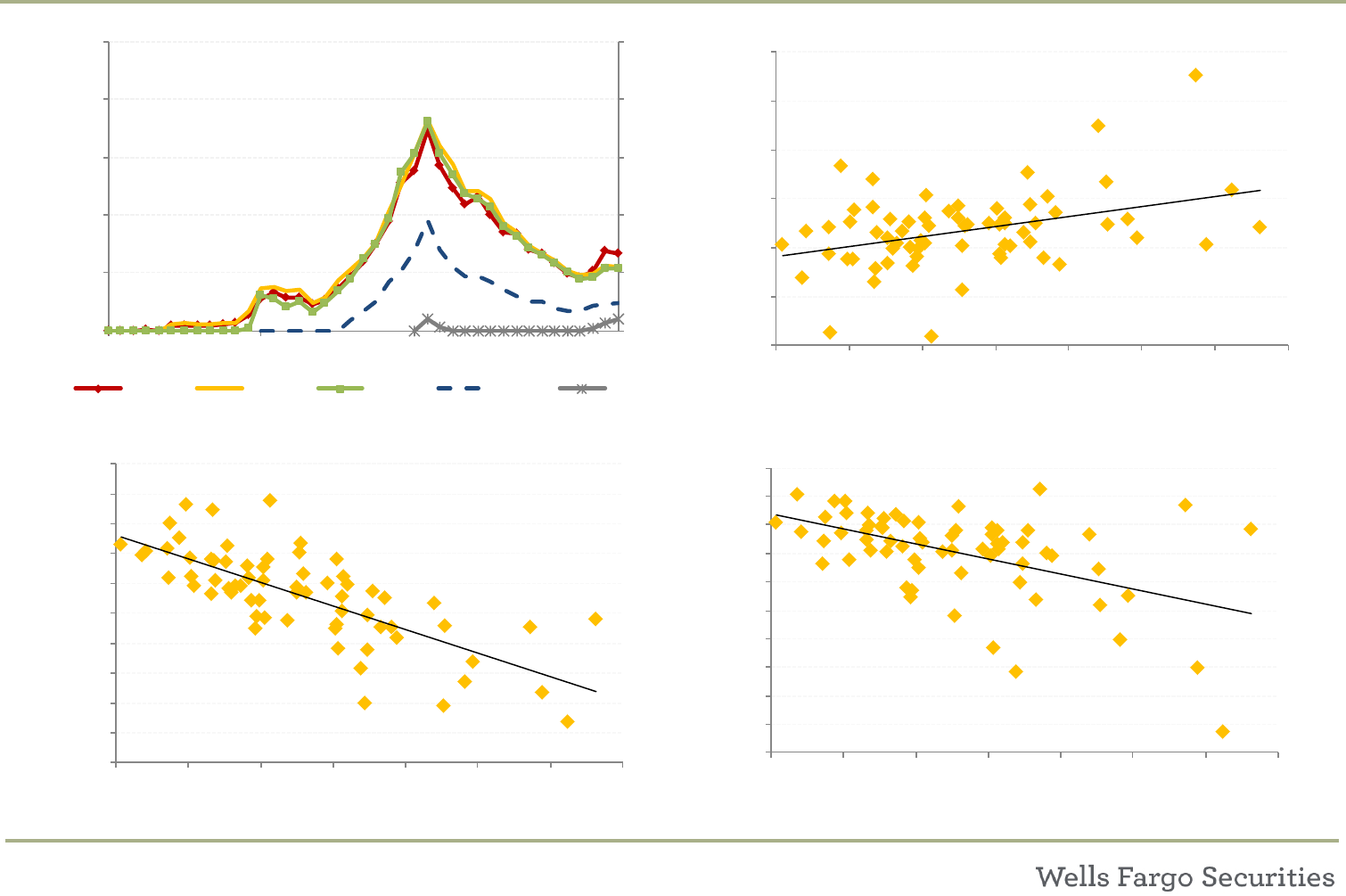

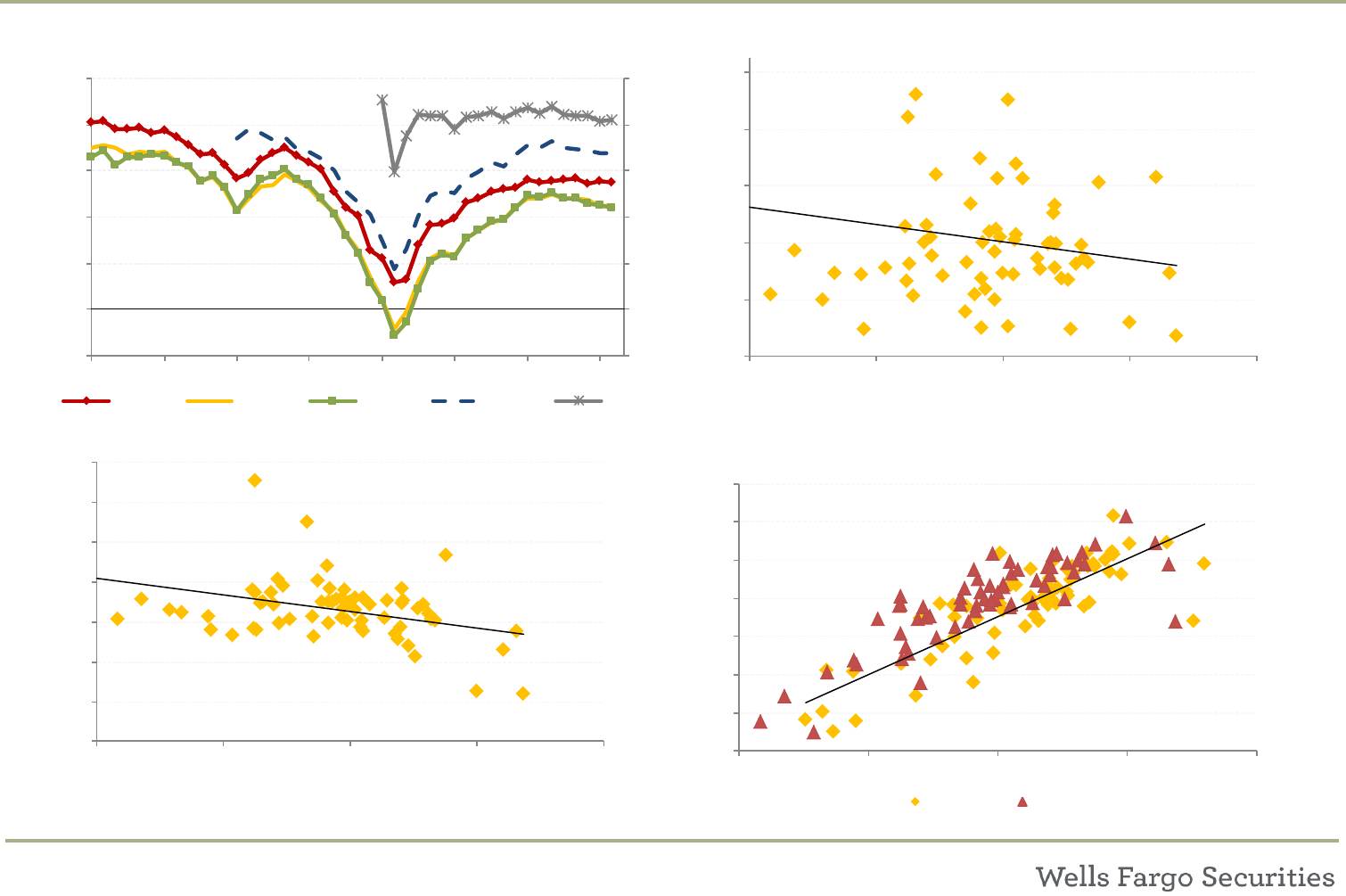

CLO Metrics: Weighted Average Spread (WAS)

6

Metric Weighted Average Spread (WAS)

Description/ Uses

Time

Median Level Chg. From Current

Current (Sep 2017)

357

12M Ago (Sep 2016)

384 -27

18M Ago (Mar 2016)

381 -24

Higher equity payments Lower equity payments

More risky assets - higher WARF/ Caa/ CCC/ 2nd Lien Less risky assets - lower WARF/ Caa/ CCC/ 2nd Lien

Lower market-value metrics - NAV, Adj. NAV, BB MVOC Higher market-value metrics - NAV, Adj. NAV, BB MVOC

Asset Holding ($mm) 3mL + Spread

Loan 1 53mL + 300

Loan 2 2.5 3mL + 350

Loan 3 2.5 3mL + 425

Weighted Avg. Spread 3mL + 344

Data Source Intex

● Easy to calculate/provided in Intex

●

Straightforward - loan market's perception of risk

expressed as average coupon

● Strong relationship with Equity Payments

The calculated Wt. Avg Spread of the portfolio – giving no credit for LIBOR or for LIBOR floors

i.e. if all the loans are L+350, the metric would be 350 bps

Can infer risk appetite / risk profile of the loan pool.

All else equal, a lower spread manager should have less risky assets. if a manager has low spread – and low equity

distributions – investors may expect a higher NAV, since they are taking less risk in the portfolio.

Calculation Example

Market Stats

Weaknesses

Lower Spread Pool

Metric Analysis

Common Metric

Pairs/Tradeoffs

● Subject to vintage bias - spread levels are dependent on

loans available in the market

● Managers that have a larger share of deals issued in

2016/2017 may have lower WAS levels than managers with

a larger share of 2013/2014 deals

● May not account for liquidity / size of underlying loans

Higher Spread Pool

Strengths

CLO Metrics: Weighted Average Spread (WAS)

7

3.50

3.70

3.90

4.10

4.30

3.50

3.70

3.90

4.10

4.30

Jan-13 Jan-14 Jan-15 Jan-16 Jan-17

Median WAS by Vintage

The Median WAS has dropped

over the past 18 Months

2012 2013 2014 2015 2016

2,500

2,600

2,700

2,800

2,900

3,000

3,100

3,200

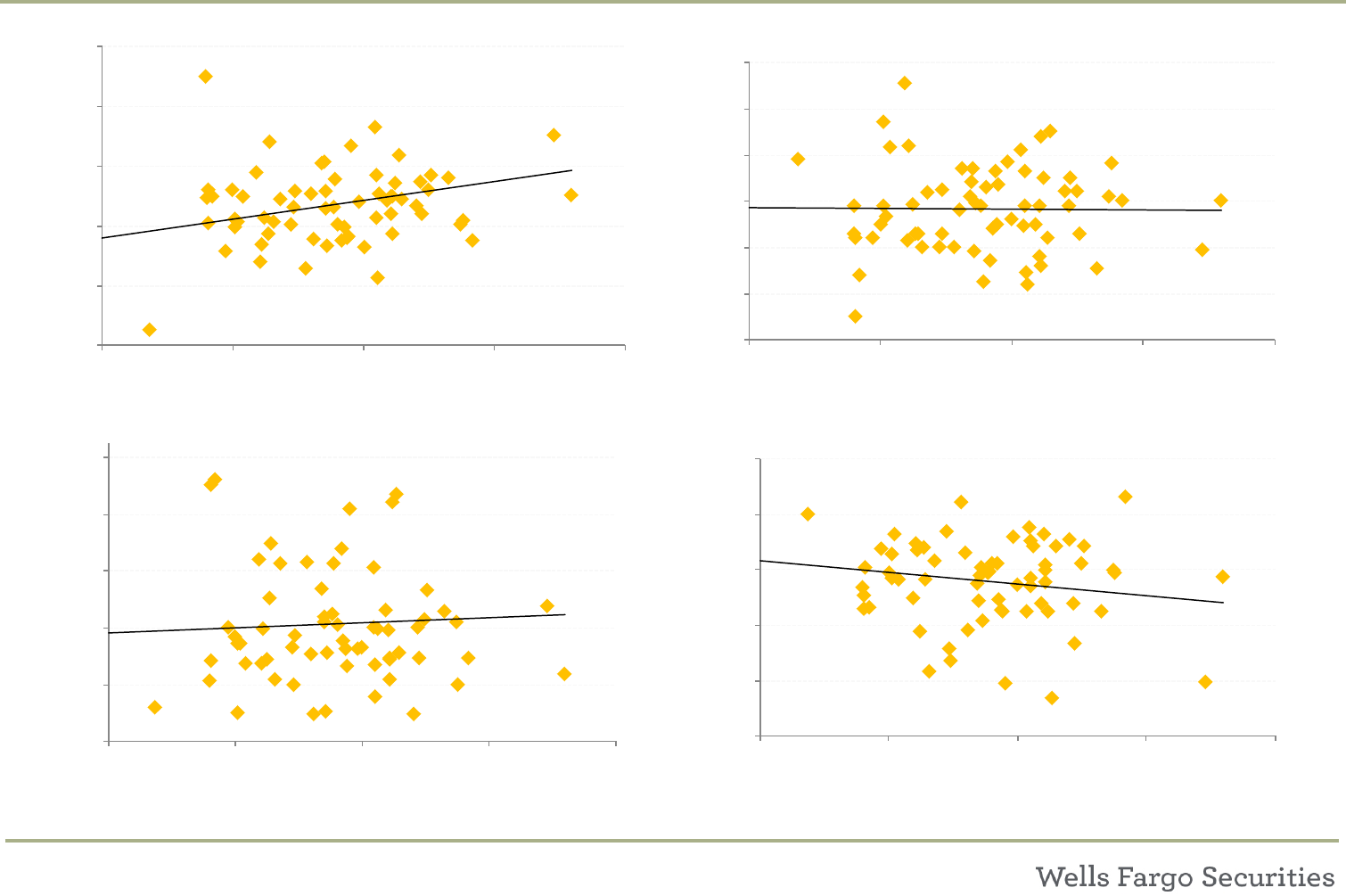

320 340 360 380 400 420

WARF

WAS

Higher WAS Often Associated with

Higher WARF (Lower-Rated Assets)

0%

20%

40%

60%

80%

100%

320 340 360 380 400 420

NAV and Adj. NAV

WAS

Higher WAS Often Associated with

Lower Market Value Metrics

MV NAV Adj. NAV

Sources: Intex, LPC Collateral

Scatter plots show manager median data from the 9/2017 Style Guide

1%

2%

3%

4%

5%

6%

7%

320 340 360 380 400 420

Norm. Equity Pmt.

WAS

Higher WAS Often Associated with

Higher Equity Pmts.

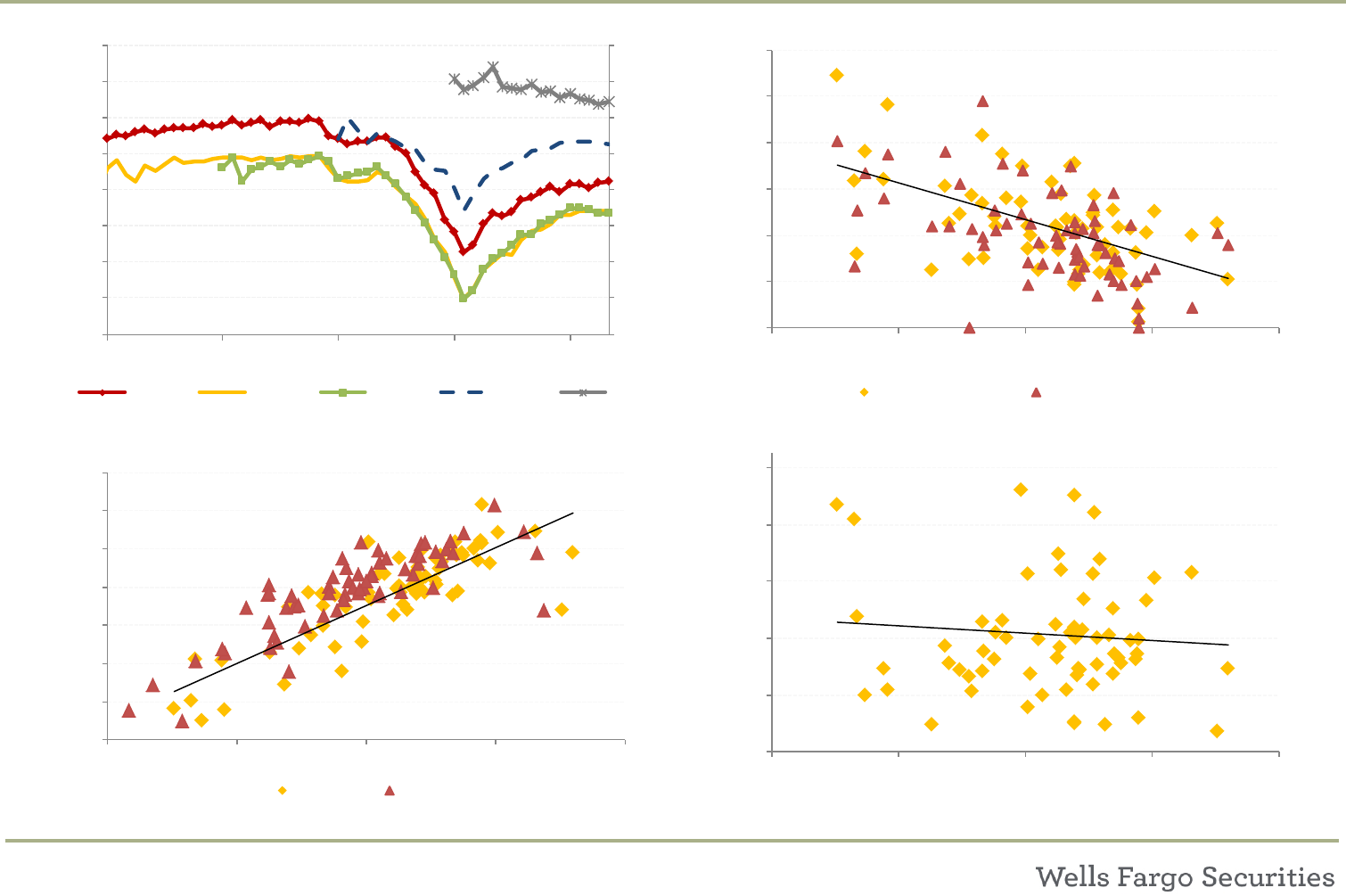

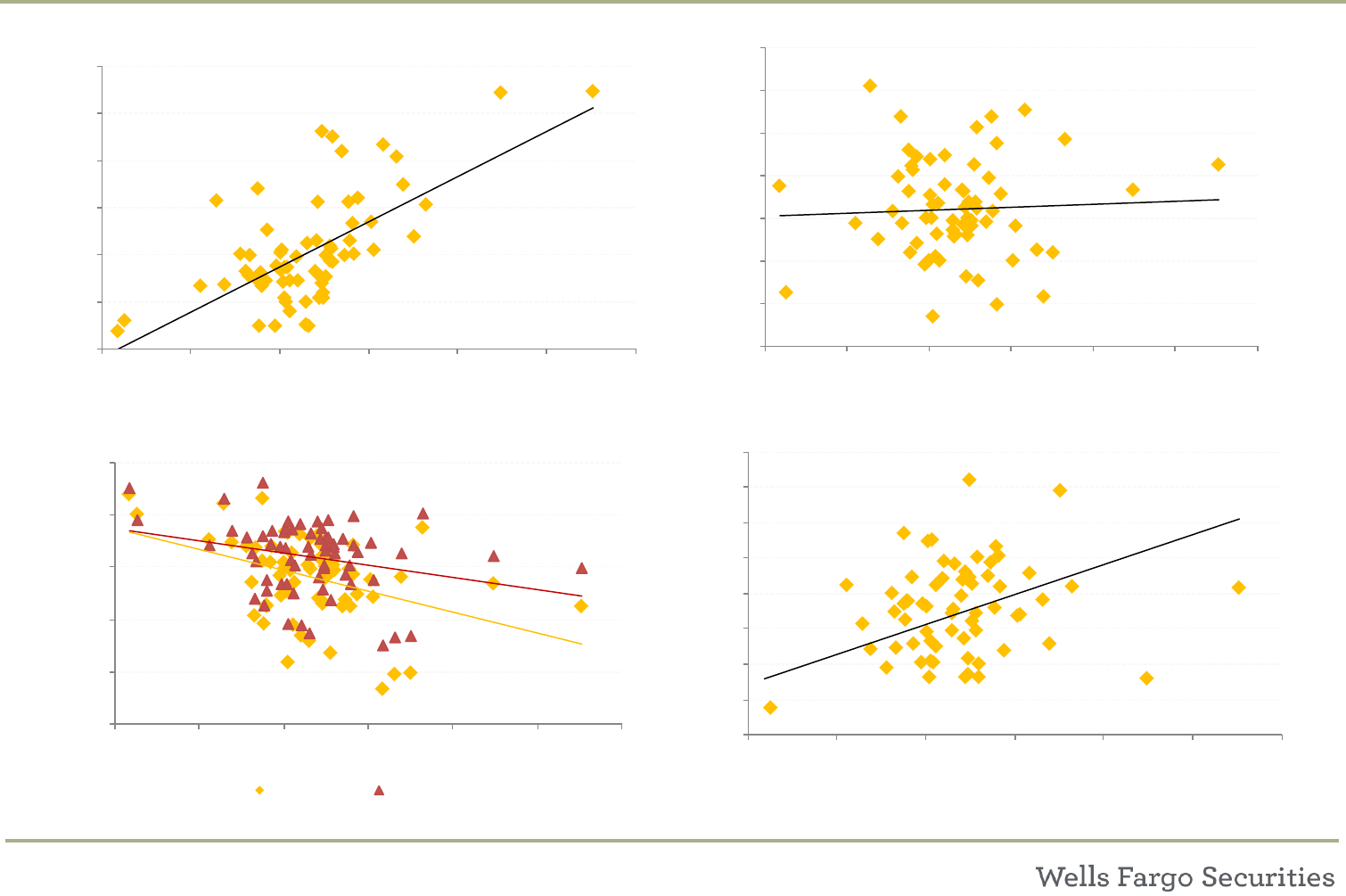

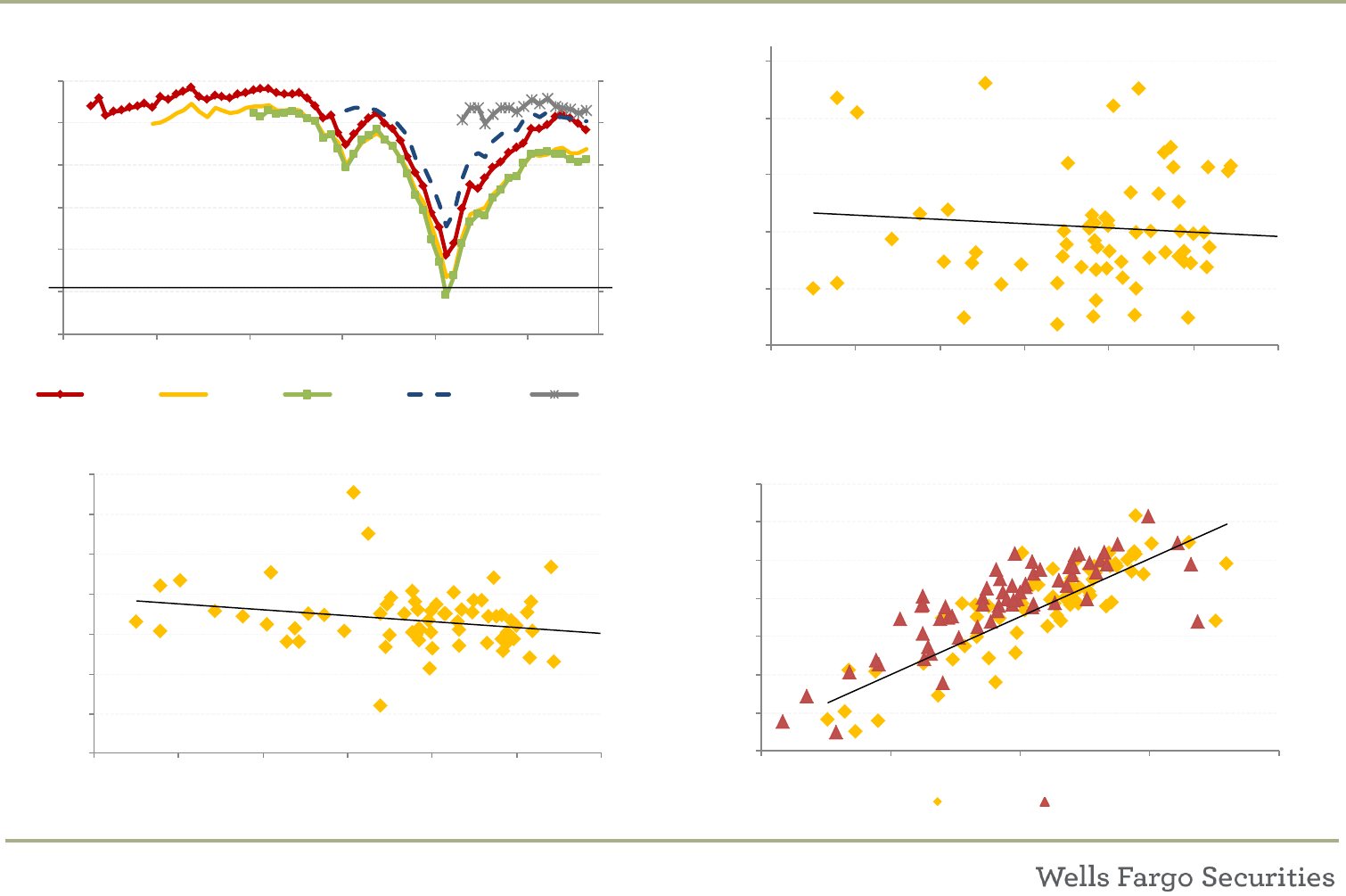

CLO Metrics: Weighted Average Rating Factor (WARF)

8

Metric Weighted Average Rating Factor (WARF)

Description/ Uses

Time

Median Level Chg. From Current

Current (Sep 2017)

2802

12M Ago (Sep 2016)

2861 -59

18M Ago (Mar 2016)

2801 1

Higher WAS and potentially higher equity payments Lower WAS and potentially lower equity payments

Lower rated assets - more exposure to Caa/ CCC/ 2nd Lien Higher rated assets - Less exposure to Caa/ CCC/ 2nd Lien

Lower market-value metrics - NAV, Adj. NAV, BB MVOC Higher market-value metrics - NAV, Adj. NAV, BB MVOC

Data Source Intex

Calculation Notes

Measures the weighted average Moody's rating of the assets. Used to determine the risk in the pool.

Lower WARF = Higher average credit rating

Higher WARF = Lower average credit rating

Some investors may view WARF as a "filter" metric; for example, an investor prefers deals with WARF below a certain level.

For reference, a CLO with a WARF of 2,833 is roughly equivalent to a B2 rating.

Market Stats

Common Metric

Pairs/Tradeoffs

Higher WARF Pool

Lower WARF Pool

Metric Analysis

Strengths

Weaknesses

● Easy to calculate/provided in Intex

● Assumes ratings are a good proxy for risk

● May not be calculated the same way across all deals

Each obligor is assigned a Rating Factor based on Moody's

Default Probability Rating; this represents the idealized default

rate at a 10-year time horizon, multiplied by 10,000. For

example: an Obligor with a rating of Baa3 may have a Rating

Factor of 610, or a 610/10,000 (6.1%) probability that it will

default within a 10-year time horizon.

**Many CLOs use the Moody's Corporate Family Rating (CFR)

when calculating WARF. CFRs may be 1-2 notches lower than the

rating on a 1st lien sr secured loan. Also, the Moody’s rating for

WARF may be adjusted if the loan is on watch or outlook.

Moody's

Rating

Equiv.

S&P

Rating

Factor

Moody's

Rating

Equiv.

S&P

Rating

Factor

Aaa AAA 1Ba1 BB+ 940

Aa1 AA+ 10 Ba2 BB 1,350

Aa2 AA 20 Ba3 BB- 1,766

Aa3 AA- 40 B1 B+ 2,220

A1 A+ 70 B2 B2,720

A2 A120 B3 B- 3,490

A3 A- 180 Caa1 CCC+ 4,770

Baa1 BBB+ 260 Caa2 CCC 6,500

Baa2 BBB 360 Caa3 CCC- 8,070

Baa3 BBB- 610 Ca CC 10,000

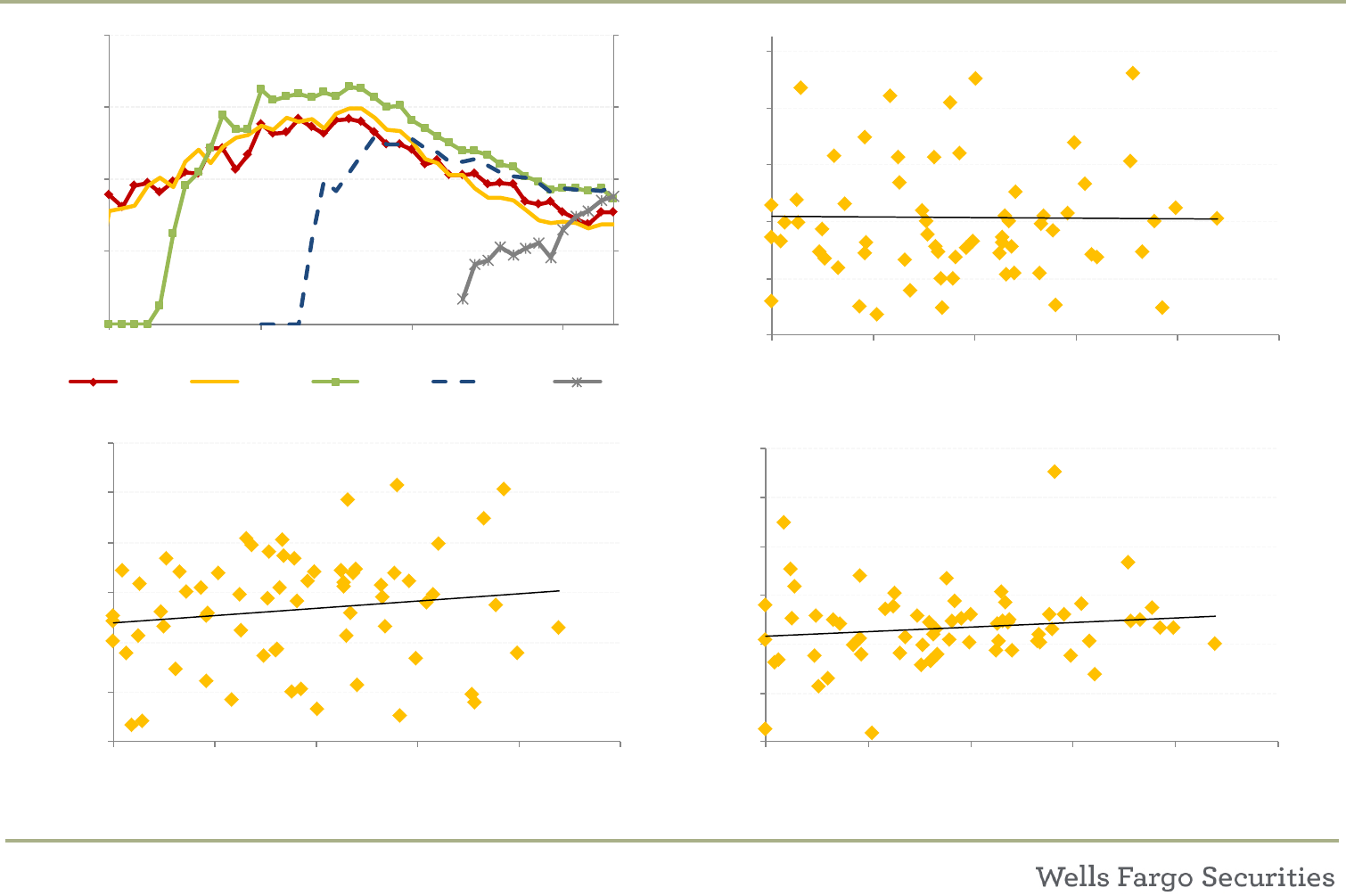

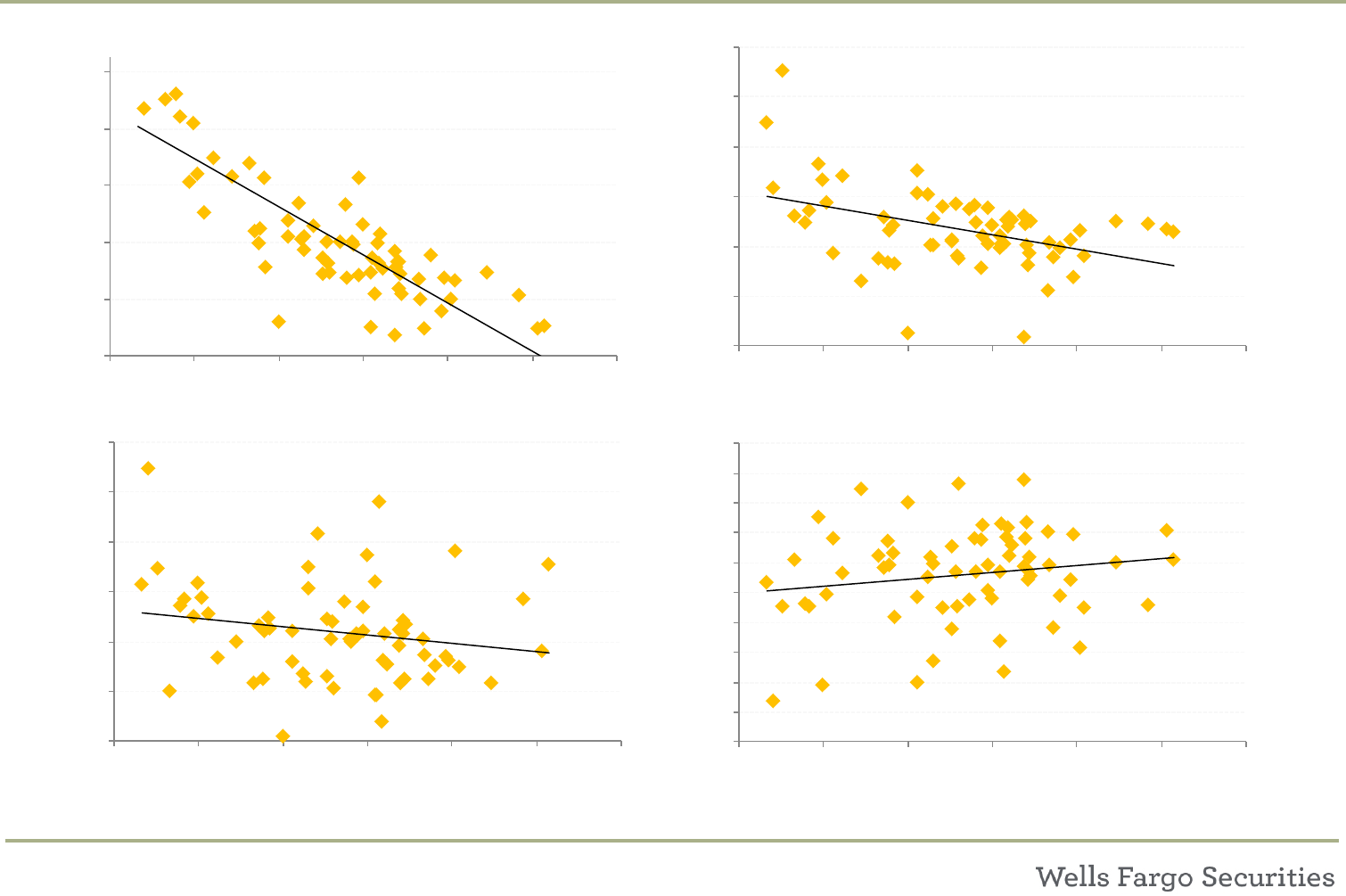

CLO Metrics: Weighted Average Rating Factor (WARF)

9

Sources: Intex, LPC Collateral

Scatter plots show manager median data from the 9/2017 Style Guide

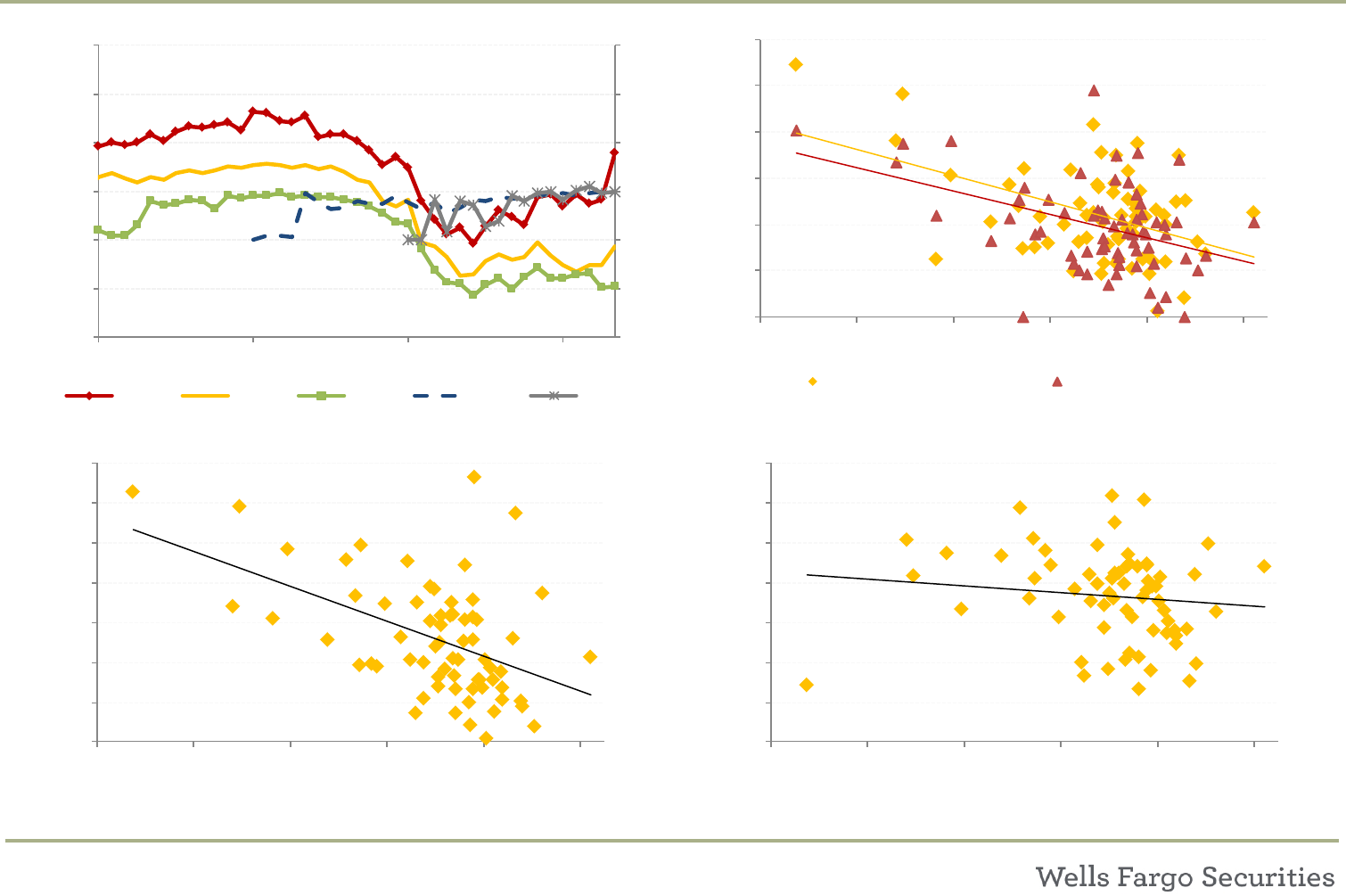

320

340

360

380

400

420

2,500 2,600 2,700 2,800 2,900 3,000 3,100 3,200

WAS

WARF

Higher WARF Often Associated with

Higher WAS (Higher-Spread Pools)

0%

2%

4%

6%

8%

10%

12%

2,500 2,600 2,700 2,800 2,900 3,000 3,100 3,200

Caa and CCC %

WARF

Lower WARF Often Associated with

Lower Caa or CCC Exposure

% Caa Exposure % CCC Exposure

0%

1%

2%

3%

4%

5%

6%

7%

2,500 2,600 2,700 2,800 2,900 3,000 3,100 3,200

% < $80

WARF

Lower WARF Often Associated with

Lower Exposure to Loans < $80

2,500

2,600

2,700

2,800

2,900

3,000

3,100

2,500

2,600

2,700

2,800

2,900

3,000

3,100

Jan-13 Jan-14 Jan-15 Jan-16 Jan-17

Median WARF by Vintage

The Median WARF has Increased Since 2013

2012 2013 2014 2015 2016

CLO Metrics: Adjusted Net Asset Value (Adj. NAV)

10

Metric Adjusted Net Asset Value (Adj. NAV)

Description/ Uses

Time

Median Level Chg. From Current

Current (Sep 2017)

67.1%

12M Ago (Sep 2016)

53.9% 13.2%

18M Ago (Mar 2016)

41.1% 26.0%

Lower risky-asset exposure (Caa/CCC/ 2nd liens)

Higher risky-asset exposure (Caa/CCC/2nd liens)

Higher BB MVOC Lower BB MVOC

Lower equity distributions Higher equity distributions

Tranche Rating Size Assets $ Holdings Mkt. Px NAV Adj. NAV

AAAA 307,500 Loans 1-105 240,000 100.3 100.3 100.0

BAA 63,750 Loans 106-130 120,000 99.5 99.5 100.0

C A 28,125 Loans 131-160 80,000 94.0 94.0 100.0

DBBB 31,250 Loans 161-171 28,000 84.0 84.0 80.0

EBB 29,375 Loans 171-176 10,000 74.5 74.5 65.0

F B 5,938 Loans 176-180 14,000 63.0 63.0 65.0

Subord NR 44,385 Par or Mkt Val 492,000 475,110 478,000

Total 510,323 NAV 21% 27%

Data Source Intex, Wells Fargo Securities

Calculation Example

Adjusted NAV is an attempt to compensate for the weaknesses of both pure market value NAV and a par-based measurement.

Adj. NAV is the equity NAV of the CLO, but not carrying all loans at their current market value.

Calculated using loans trading at 85+ carried at par; 75 - 85 carried at 80; and < 75 carried at 65 (low end of hist. recovery).

Market Stats

Common Metric

Pairs/Tradeoffs

Higher Adj. NAV Pool

Lower Adj. NAV Pool

Metric Analysis

Strengths

Weaknesses

● Compensates for weaknesses of pure market-value NAV

and is less volatile

● Used as a proxy for how many loans are “money good”

(Loans 85+) – so this NAV would be a proxy for ultimate

terminal value for the equity – a PO estimate – as opposed

to liquidation value.

● Not easily provided in Intex

● NAV metrics affected by vintage & equity / note prices

● May not adequately punish very low priced loans (ex <$50)

● Only provides a snapshot of the loan prices on a specific

day;this applies to all market-value metrics (NAV, loans < 80,

BB MVOC).

Liabilities

Assets

In a loan market selloff, if the average loan price drops to $96 or $94, the loans would likely still be money good but the typical

MV NAV would look worse; Adj. NAV would hold these loans at par.

CLO Metrics: Adjusted Net Asset Value (Adj. NAV)

11

Sources: Intex, LPC Collateral

Scatter plots show manager median data from the 9/2017 Style Guide

0%

2%

4%

6%

8%

10%

12%

20% 40% 60% 80% 100%

Caa and CCC %

Adj. NAV

Higher Adj. NAV Often Associated with

Lower Caa or CCC Exposure

% Caa Exposure % CCC Exposure

103

104

105

106

107

108

109

110

20% 40% 60% 80% 100%

BB MVOC

Market Value Metrics Tend to Move Together

Adj. NAV NAV

320

340

360

380

400

420

20% 40% 60% 80% 100%

WAS

Adj. NAV

Higher Adj. NAV Often Associated with

Lower WAS (Lower-Spread Pools)

20

30

40

50

60

70

80

90

100

20

30

40

50

60

70

80

90

100

Jan-13 Jan-14 Jan-15 Jan-16 Jan-17

Adj. NAV by Vintage

The Median Adj. NAV is ~60%

2012 2013 2014 2015 2016

CLO Metrics: Moody’s Diversity Score

12

Metric Moody's Diversity Score

Description/ Uses

Time

Median Level Chg. From Current

Current (Sep 2017)

74

12M Ago (Sep 2016)

70 4

18M Ago (Mar 2016)

68 6

Data Source Intex

Calculation Notes

Moody's diversity score is provided in Intex.

A deal's minimum diversity limit is calculated based on the Moody's Matrix, which is a sliding scale based on WAS, WARF, loan

recovery levels and diversity.

● More diversity is generally associated with low er

idiosyncratic risk and industry risk.

● On the flip side, extremely diverse pools could be

overweight smaller names or industries relative to the

market.

● Low er diversity could be a sign of manager conviction in a

certain name or industry.

Metric Analysis

Strengths

Weaknesses

● Easy to calculate/provided in Intex

● Diversity score may not be correlated with credit quality

● Managers may increase diversity to help with matrix tests

● Industry classifications may not be standardized

Moody’s diversity score: based on how many assets, how many industries and how big the positions are. A par weighted

calculation that indicates collateral concentration in terms of both issuer and industry concentration.

The Moody’s Diversity score has three primary inputs: 1) number of industries, 2) number of assets and 3) par value of each

asset. The drivers of a higher diversity score are one or more of the following: more assets, less correlated assets (widely

distributed across more industries) and more evenly distributed par amount of the assets.

Market Stats

Common Metric

Pairs/Tradeoffs

Higher Diversity Pool

Lower Diversity Pool

CLO Metrics: Moody’s Diversity Score

13

Sources: Intex, LPC Collateral

Scatter plots show manager median data from the 9/2017 Style Guide

45

50

55

60

65

70

75

80

45

50

55

60

65

70

75

80

Jan-13 Jan-14 Jan-15 Jan-16 Jan-17

Diversity by Vintage

The Median Div. Score for newer post-crisis

vintages has ticked up in recent months.

2012 2013 2014 2015 2016

2,500

2,600

2,700

2,800

2,900

3,000

3,100

3,200

40 50 60 70 80 90 100 110

WARF

Diversity

Higher Diversity Often Associated with

Lower WARF

2%

3%

4%

5%

6%

7%

8%

40 50 60 70 80 90 100 110

Norm. Eq Pmt.

Diversity

Higher Diversity Has Slightly Positive

Relationship with Norm. Eq Pmts.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

40 50 60 70 80 90 100 110

MV NAV

Diversity

Higher Diversity Generally Unrelated to NAV

CLO Metrics: Normalized Equity Payment

14

Metric Median Normalized Quarterly Equity Payment

Description/ Uses

Time

Median Level Chg.

Current (Sep 2017)

4.3%

12M Ago (Sep 2016)

4.8% -0.5%

Example: 2016-Vintage Deal Payment Dates Payment Not. Equity Bal.

Issue Date 4/7/2016 10/27/2016 8,382,123 44,900,000

Days Outstanding as of last payment date 470 1/27/2017 1,646,869 44,900,000

Qtrs Outstanding as of last payment date 5.15 4/27/2017 1,567,600 44,900,000

Payments / Equity Balance 29.8% 7/27/2017 1,798,126 44,900,000

Normalized Qtrly Payment/Equity Balance 5.79% Total 13,394,718

Data Source Intex, Wells Fargo Securities

Total Equity Distributions (during Reinvest. Period), converted to quarterly payments. The total sum of all equity payments

made during reinvestment, converted to an average quarterly payment. Equity distribution is the quarterly equity payment

divided by the equity notional value.

We can think of the quarterly distributions (the IO) and the NAV (the PO) as the two parts of the return – with the total return

as the distributions received to date plus the current portfolio value. If a manager has a low WAS portfolio – and low equity

distributions – then, all else equal, they should have a higher NAV, since they are taking less risk in the portfolio.

Market Stats

Common Metric

Pairs/Tradeoffs

Higher Normalized Equity Payments

Lower Normalized Equity Payments

● Higher WAS - and potentially higher exposure to riskier

assets (Caa/CCC/2nd lien)

● Higher leverage

● Low er market-value metrics (Eq. NAV, BB MVOC)

● Low er WAS - and potentially cleaner pools (low er

Caa/CCC/2nd lien)

● Lower leverage

● Higher market-value metrics (Eq. NAV, BB MVOC)

Calculation Notes

Metric Analysis

Strengths

Weaknesses

● Looks at average equity payments over time

● Adjusts for the fact that the first equity payments often differ

in payment period length, and differing first payment periods

can produce high or low first payments.

● Not provided in Intex

● Does not take into account the PO value of the pool

● Not adjusted for refi/ reset, which can affect equity NAV

& payments.

● Does not account for debt cost or vintage differences.

CLO Metrics: Normalized Equity Payment

15

Sources: Intex, LPC Collateral

Scatter plots show manager median data from the 9/2017 Style Guide

0%

20%

40%

60%

80%

100%

2% 3% 4% 5% 6% 7% 8%

NAV and Adj. NAV

Norm. Eq. Pmts.

Higher Eq. Pmts. Often Associated with

Lower Market Value Metrics

MV NAV Adj. NAV

320

340

360

380

400

420

440

2% 3% 4% 5% 6% 7% 8%

WAS

Norm. Eq. Pmts.

Higher Equity Pmts. Strongly Associated with

Higher WAS

9.0

9.5

10.0

10.5

11.0

11.5

12.0

12.5

13.0

2% 3% 4% 5% 6% 7% 8%

Leverage

Norm. Eq. Pmts.

Higher Equity Pmts. Often Associated with

Higher Leverage

2,500

2,600

2,700

2,800

2,900

3,000

3,100

3,200

2% 3% 4% 5% 6% 7% 8%

WARF

Norm. Eq. Pmts.

Higher Eq. Pmts. Often Associated with

Higher WARF (Lower-Rated Assets)

CLO Metrics: Leverage

16

Metric Median Leverage

Description/ Uses

Time

Median Level Chg.

Current (Sep 2017)

10.8

12M Ago (Sep 2016)

10.5 0.3

18M Ago (Mar 2016)

10.4 0.4

Tranche Rating Size

AAAA 372,000

BAA 84,000

C A 36,000 Leverage = 608,000 / 56,000

DBBB 36,000 10.9

EBB 24,000

Subord NR 56,000

Total 608,000

Data Source Intex, Wells Fargo Securities

Structural Leverage

Metric Analysis

Strengths

Weaknesses

● Easy to calculate in Intex

● Uses equity notional balance - similar to equity payment data

● Less volatile than calculating based on asset leverage which

is constantly changing

● More levered deals will show faster moves in market value

metrics (NAV, MVOC)

● Based on structural leverage, not actual asset leverage

– not based on assets/ (assets-debt), which technically

would be more accurate; based on total deal balance /

equity notional.

● We use structural leverage because a) equity pmts are

frequently quoted as a pct of notional par and b) the asset

balance is constantly changing.

Calculation Example

● Total initial deal balance / equity notional balance.

● The leverage category can be used to show how the manager is w orking to achieve equity returns: structural leverage vs.

leverage in the assets. When structuring a CLO, there are certain trade-offs – all else equal, a lower WARF (higher rated

assets) or higher diversity should allow for more leverage on the pool.

Market Stats

Common Metric

Pairs/Tradeoffs

Higher Leverage

Lower Leverage

● One manager style is to add an extra turn or tw o of

leverage, but with a very clean pool (below avg WAS, better

than avg WARF).

● Higher structural leverage allow s more room for low er asset

leverage (potentially lower WAS or WARF)

● Higher diversity

● Higher WARF (low er rated assets)

● Low er diversity

CLO Metrics: Leverage

17

Sources: Intex, LPC Collateral

Scatter plots show manager median data from the 9/2017 Style Guide

2%

3%

4%

5%

6%

7%

9 10 11 12 13

Norm. Equity Pmt.

Leverage

Higher Leverage Often Associated with

Higher Equity Pmts.

45

55

65

75

85

95

105

9 10 11 12 13

Diversity

Leverage

Higher Leverage Could be Offset by

Higher Diversity

320

340

360

380

400

420

9 10 11 12 13

WAS

Leverage

Higher Leverage Often Associated with

Higher WAS (Higher-Spread Pools)

0%

20%

40%

60%

80%

100%

9 10 11 12 13

MV NAV

Leverage

Higher Leverage Often Associated with

Lower MV NAV

CLO Metrics: Min. OC Cushion

18

Metric Median Minimum Overcollateralization Cushion (Min OC Cushion)

Description/ Uses

Time

Median Level Chg.

Current (Sep 2017)

419

12M Ago (Sep 2016)

391 28

18M Ago (Mar 2016)

425 -5

Tranche Rating Size Numer. Curr. Val Trigger Cushion (bps) P/F

A-1 AAA 372 600 1.61 PASS

A-2 AA 84 600 1.32 1.21 1058 PASS

B A 36 600 1.22 1.14 795 PASS

CBBB 36 600 1.14 1.08 564 PASS

DBB 24 600 1.09 1.05 400 PASS

Subord NR 56

Total Liabilities 608

OC Ratio Numerator This example deal has a min. OC cushion of 400 bps.

595

Total Assets 600

Data Source Intex, Wells Fargo Securities

Denominator Calc

[372 + 84 + 36 + 36 + 24]

Metric Analysis

Strengths

Weaknesses

● Included in Intex

● Provides a proxy for par building

● Haircut for excess Caa / CCC exposure, defaulted

assets and discount purchases

● Some deals may have single B OC tests (~ 20-30% of

single-B tranches have OC tests)

● Does not account for initial structuring or OC calculation

differences.

● Only a snapshot; does not show OC gained or lost

Calculation Example

[372]

[372 + 84]

Agg. Principal Value of Underlying Assets

Cash & Eligible Investments

[372 + 84 + 36]

[372 + 84 + 36 + 36]

5

● Difference betw een actual OC level and OC Test limit for the tightest OC test in the deal (not including Int. Diversion

tests – only true OC tests). Used to show how close an equity cashflow diversion is.

● OC Test: Par-based asset/liability coverage test. Given a tranche, X, the OC ratio = Adj. Principal Value of Collateral / Sum

of prin. for tranche X and all tranches senior to X

Market Stats

Common Metric

Pairs/Tradeoffs

Higher Min. OC

Lower Min. OC

● Low er Caa / CCC / Defaulted asset exposure - w hich

can sometimes be haircut in the min. OC cushion

calculation

d h ( ll l b l $ )

● In theory, we would hope a manager with low er Min. OC

cushion would have recently cleaned up their pool/sold

assets at a discount at the cost of min. OC

CLO Metrics: Min. OC Cushion

19

Sources: Intex, LPC Collateral

Scatter plots show manager median data from the 9/2017 Style Guide

3.0

3.5

4.0

4.5

5.0

5.5

6.0

3.0

3.5

4.0

4.5

5.0

5.5

6.0

Jan-14 Jan-15 Jan-16 Jan-17

Median Min OC Cushion

The median Min. OC Cushion Declined in H1 2016

but has since remained generally flat

2012 2013 2014 2015 2016

0%

2%

4%

6%

8%

10%

12%

50 150 250 350 450 550

Caa and CCC %

Min OC Cushion

Higher Min OC Often Associated with

Lower Caa or CCC Exposure

% Caa Exposure % CCC Exposure

0%

1%

2%

3%

4%

5%

6%

7%

50 150 250 350 450 550

Loans < $80

Min. OC Cushion

Higher Min OC Often Associated with

Lower Loans < $80

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

50 150 250 350 450 550

Bid Depth

Min. OC Cushion

Higher Min OC Slightly Associated with

Lower Bid Depth

CLO Metrics: Caa Exposure and CCC Exposure

20

Metric Median Caa Exposure and Median CCC Exposure

Description/ Uses

Time

Med. Caa Chg. Med. CCC Chg.

Current (Sep 2017)

4.30 3.80

12M Ago (Sep 2016)

4.88 -0.58 3.93 -0.13

18M Ago (Mar 2016)

3.97 0.33 2.45 1.35

Security Prin. Bal. MDY Rtg S&P Rtg Caa Exp CCC Exp

Company 1 3.0 B3 CCC 3.0

Company 2 2.9 B3 CCC+ 2.9

Company 3 2.9 Caa1 CCC- 2.9 2.9

Company 4 2.5 Caa3 CCC- 2.5 2.5

Company 5 3.7 Caa1 CCC 3.7 3.7

Company 6-200 479.3 B2 BB Total Caa or CCC 9.1 15.0

Total Assets 494.3 494.3

Total Asset Bal 494.3 % Exposure 1.8% 3.0%

Calculation Example

● Intex’s fields show % of the portfolio rated Caa or below , and the % of the portfolio rated CCC or below

● Generally, we have found that Moody's Caa exposure in a CLO is based on facility rating, while S&P's CCC exposure is based

on issuer rating.

Market Stats

Common Metric

Pairs/Tradeoffs

Higher Caa or CCC Exposure

Lower Caa or CCC Exposure

● Higher spread assets (higher WAS)

● Higher WARF

● Low er Min OC Cushion

● Low er market-value metrics (NAV, Adj. NAV, BB MVOC)

● Cleaner pools - low er WARF

● Low er spread pools

● Higher Min OC Cushion

● Higher market-value metrics (NAV, BB MVOC)

Metric Analysis

Strengths

Weaknesses / Caveats

● Included in Intex

● Clear calculation of low er-rated assets in the portfolio

● May be calculated differently from deal to deal.

● Also, the data reported in Intex may refer to concentration

limits, not to Excess Caa or Excess CCC Test levels used for

OC test calculation; Actual Caa or CCC holdings may be

higher or lower.

● May not include data from deals not rated by that rating

agy. If Moody's did not rate the deal, we may not have Caa%

data.

CLO Metrics: Caa Exposure and CCC Exposure

21

Sources: Intex, LPC Collateral

Scatter plots show manager median data from the 9/2017 Style Guide

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Jan-14 Jan-15 Jan-16 Jan-17

Med. Reported Caa Holdings

Median Caa Exposure Increased During 2016

but has Since Flattened or Dropped

2012 2013 2014 2015 2016

0%

2%

4%

6%

8%

10%

12%

320 340 360 380 400 420

Caa and CCC %

WAS

Higher Caa or CCC Often Associated with

Higher WAS

% Caa Exposure % CCC Exposure

0%

2%

4%

6%

8%

10%

12%

50 150 250 350 450 550

Caa and CCC %

Min OC Cushion

Higher Caa or CCC Often Associated with

Lower Min OC Cushion

% Caa Exposure % CCC Exposure

0%

2%

4%

6%

8%

10%

12%

20% 40% 60% 80% 100%

Caa and CCC %

Adj. NAV

Higher Caa or CCC Exposure Often Associated

with Lower MV Metrics

% Caa Exposure % CCC Exposure

CLO Metrics: Second Lien Exposure

22

Metric Median 2nd Lien Exposure

Description/ Uses

Time

Med. Caa Chg.

Current (Sep 2017)

1.77

12M Ago (Sep 2016)

2.14 -0.37

18M Ago (Mar 2016)

2.64 -0.87

Provided in Intex as a percent of the deal's asset balance

Data Source Intex, Wells Fargo Securities

Calculation Example

● The percent of 2nd lien loans held by the CLO

● Used as a proxy for portfolio risk

Market Stats

Common Metric

Pairs/Tradeoffs

Higher 2nd Lien Exposure

Lower 2nd Lien Exposure

● In general, we would expect higher 2nd liens to be

associated with:

● Higher spread assets (higher WAS)

● Higher WARF

● Low er market-value metrics (NAV, Adj. NAV, BB MVOC)

However, some managers appear to employ a barbell

approach, where higher second lien exposure doesn't

necessarily equate to a riskier portfolio

● Cleaner pools - low er WARF

● Low er spread pools

● Higher market-value metrics (NAV, BB MVOC)

Metric Analysis

Strengths

Weaknesses / Caveats

● Included in Intex

● Clear calculation of se cond-lien assets in portfolio

● Does not stand alone as a proxy for risk - managers may

employ a barbell approach in choosing assets

● Deals with high 2nd lien holdings may see a disconnect

between Caa and CCC % (facility rating vs. issuer rating)

CLO Metrics: Second Lien Exposure

23

Sources: Intex, LPC Collateral

Scatter plots show manager median data from the 9/2017 Style Guide

0.0

1.0

2.0

3.0

4.0

0.0

1.0

2.0

3.0

4.0

Jan-14 Jan-15 Jan-16 Jan-17

Med. 2nd Lien Exposure

Second Lien Exposure has declined since Jan

2015 but has recently ticked up

2012 2013 2014 2015 2016

320

340

360

380

400

420

- 1.0 2.0 3.0 4.0 5.0

WAS

2nd Liens (% Exp)

Higher 2nd Liens Generally Unrelated to

WAS Level

3.5

4.0

4.5

5.0

5.5

6.0

6.5

- 1.0 2.0 3.0 4.0 5.0

Bid Depth

2nd Liens (% Exp)

Higher 2nd Lien managers tend to have more

liquid portfolios (higher bid depth)

2%

3%

4%

5%

6%

7%

8%

- 1.0 2.0 3.0 4.0 5.0

Norm. Eq Pmt.

2nd Liens (% Exp)

Higher 2nd Liens Have Slightly Positive

Relationship with Norm. Eq Pmts.

CLO Metrics: < $80 Exposure

24

Metric Median Exposure to Loans Trading < $80

Description/ Uses

Time

Loans < $80 Chg.

Current (Sep 2017)

2.4%

12M Ago (Sep 2016)

4.5% -2.1%

18M Ago (Mar 2016)

9.5% -7.1%

Calculation Example Provided in LPC Collateral's Database by Deal

Data Source LPC Collateral

Metric Analysis

Strengths

Weaknesses / Caveats

● Trading prices can be a good proxy for whether market

believes a loan will default

● Commonly used metric for tail risk in CLO portfolios

● Does not account for purchase price. Manager could have

bought a loan at $0.25 which now trades at $0.79 and it

would still be included in our metric.

● Also, at various points, <80 is arguably too high or too low

a cut-off for tail risk.

● Based on a snapshot of the loan prices on the day we

determine the underlying portfolio market value - this applies

to all market-value metrics (NAV, loans < 80, BB MVOC).

● Average # of loans in the pool that have current market prices below 80 – the traditional cut-off for a ‘distressed loan’ in the

loan market.

● Used to illustrate tail risk or as a proxy for near term (12-24 month) default risk in the pool.

● If average recoveries (measured by post default trading price) are ~65, then a loan trading below 80 is typically trading as if

the market thinks it will default.

Market Stats

Common Metric

Pairs/Tradeoffs

Higher Loans < $80

Lower Loans < $80

● Higher spread assets (higher WAS)

● Higher WARF

● Low er Min OC Cushion

● Low er market-value metrics (NAV, Adj. NAV, BB MVOC)

● Cleaner pools - low er WARF

● Low er spread pools

● Higher Min OC Cushion

● Higher market-value metrics (NAV, Adj. NAV, BB MVOC)

CLO Metrics: < $80 Exposure

25

Sources: Intex, LPC Collateral

Scatter plots show manager median data from the 9/2017 Style Guide

0%

3%

6%

9%

12%

15%

0%

3%

6%

9%

12%

15%

Jan-14 Jan-15 Jan-16 Jan-17

Med. Pct. of Loans < 80

Loans below $80 have

ticked up in recent months

2012 2013 2014 2015 2016

2%

3%

4%

5%

6%

7%

8%

0% 1% 2% 3% 4% 5% 6% 7%

Norm. Eq Pmt.

Loans < $80

Higher Loans < $80 Have Positive Relationship

with Norm. Eq Pmts.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0% 1% 2% 3% 4% 5% 6% 7%

MV NAV

Loans < $80

Higher Loans < $80 Associated with

Lower MV Metrics

50

100

150

200

250

300

350

400

450

500

550

0% 1% 2% 3% 4% 5% 6% 7%

Min OC Cushion

Loans < $80

Higher Loans < $80 Have Negative Relationship

with Min OC Cushion

CLO Metrics: Wtd. Avg. Bid Depth

26

Metric Median Weighted Average Bid Depth

Description/ Uses

Time

Bid Depth Chg.

Current (Sep 2017)

4.90

12M Ago (Sep 2016)

4.42 0.48

Assets $ Holdings Bid Depth

Loans 1-70 161,676 1

Loans 71-144 136,292 2

Loans 145-193 103,743 3

Loans 194-257 135,003 5

Loans 258-304 125,990 7

Loans 305-341 63,643 9

Loans 341-363 64,052 10

Total 790,399

Wtd. Avg. Bid Depth 4.45

Data Source LPC Collateral

Calculation Example

Example Deal: Assets

Metric Analysis

Strengths

Weaknesses / Caveats

● Can help investors understand how a CLO manager may

be achieving higher spread pools or driving a favorable

WAS/WARF ratio.

● Does not account for quality/size of bids in the market.

● Average of the # of bids on the loans in the CLO portfolio used in our portfolio pricing, per our CLO asset pricing tool

● Avg. Bid depth is an attempt to show the level of liquidity on assets in underlying CLO portfolios. Used to show which

managers are taking liquidity risk – typically, we would think of loans with fewer bids as smaller loans – ‘upper middle market’

or ‘lightly syndicated loans.’

● Because a CLO is not a mark to market vehicle, and the CLO does not have forced liquidation provisions, we believe liquidity

risk within a CLO portfolio is acceptable – however, we also want CLO investors to understand how certain managers may be

achieving higher spread pools or driving a favorable WAS/WARF ratio.

Market Stats

Common Metric

Pairs/Tradeoffs

Higher Bid Depth

Lower Bid Depth

● More volatile market-value metrics, due to increased

liquidity

● Low er spread pools

● Typically, a lower bid depth corresponds with higher spread

portfolios.

● More stable market-value metrics, due to less liquidity—but

may face larger jumps in prices in a stress period.

CLO Metrics: Wtd. Avg. Bid Depth

27

Sources: Intex, LPC Collateral

Scatter plots show manager median data from the 9/2017 Style Guide

320

340

360

380

400

420

3.5 4.0 4.5 5.0 5.5 6.0 6.5

WAS

Bid Depth

Lower Bid Depth Often Associated with

Higher WAS (Higher-Spread Pools)

2%

3%

4%

5%

6%

7%

8%

3.5 4.0 4.5 5.0 5.5 6.0 6.5

Normalized Eq. Pmt

Bid Depth

Lower Bid Depth Often Associated with

Higher Eq. Pmts.

0%

2%

4%

6%

8%

10%

12%

3.5 4.0 4.5 5.0 5.5 6.0 6.5

Caa %

Bid Depth

Lower Bid Depth Often Associated with

Higher Caa Exposure

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

3.5 4.0 4.5 5.0 5.5 6.0 6.5

MV NAV

Bid Depth

Lower Bid Depth Often Associated with

Lower MV NAVs

CLO Metrics: MV NAV

28

Metric Market Value NAV

Description/ Uses

Time

Median Level Chg.

Current (Sep 2017) 58.0%

12M Ago (Sep 2016) 42.3% 15.7%

18M Ago (Mar 2016) -0.8% 58.8%

Lower risky-asset exposure (Caa/CCC/ 2nd liens) Higher risky-asset exposure (Caa/CCC/2nd liens)

Lower loans < $80 exposure Higher loans < $80 exposure

Tranche Rating Size Assets $ Holdings Mkt. Px

AAAA 314,100 Loans 1-105 240,000 100.3

BAA 60,900 Loans 106-130 120,000 99.5

C A 36,000 Loans 131-160 86,000 98.0

DBBB 25,700 Loans 161-171 28,000 87.0

EBB 23,300 Loans 171-180 20,000 70.0

Subord NR 52,500 Par or Mkt Val 494,000 482,760

Total 512,500 NAV 43%

Data Source Markit, Wells Fargo Securities

Calculation Example

Liabilities

Assets

The equity market value NAV of the CLO equity tranche (expressed as a pct of equity notional balance). Can be thought of as

the liquidation value of the CLO – the value to the equity if the manager sold all the assets and paid off the notes. Calculated

by taking the market value of the portfolio minus the face value of all debt tranches outstanding, divided by equity notional.

May not account for incentive mgmt. fees or deferred fees.

Market Stats

Common Metric

Pairs/Tradeoffs

Higher NAV Pool

Lower NAV Pool

Metric Analysis

Strengths

Weaknesses

● Provides proxy for liquidation value of the CLO - if

we sold the assets today and paid off all the debts

● Can be used to proxy total returns to equity -

Equitiy NAV (PO) + Cashflows paid to date

● Commonly used in pricing and trading secondary

equity.

● CLO is not a mark to market vehicle, and the CLO does not have

forced liquidation provisions. A CLO provides the equity investor

with term leverage with no mark to market pressure, and investors

can’t force a liquidation prior to the call – so measuring daily loan

price movements may not always make sense. For example – if loan

outflows lead to loan market selling, all loans may fall in price. If half

the pool drops from 99 to 94, the NAV drops 25 points – but we

wouldn’t think the actual credit quality has actually changed.

● A snapshot of the loan prices on the day we determine the

underlying portfolio market value

● Not adjusted for refi/ reset, which can affect NAV and eq. pmts.

● Does not account for initial structuring differences.

CLO Metrics: MV NAV

29

Sources: Intex, LPC Collateral

Scatter plots show manager median data from the 9/2017 Style Guide

103

104

105

106

107

108

109

110

20% 40% 60% 80% 100%

BB MVOC

Market Value Metrics Tend to Move Together

Adj. NAV NAV

320

340

360

380

400

420

20% 40% 60% 80% 100%

WAS

MV NAV

Higher MV NAV Often Associated with

Lower WAS (Lower-Spread Pools)

1%

2%

3%

4%

5%

6%

7%

8%

20% 40% 60% 80% 100%

Norm. Eq. Pmts.

MV NAV

Higher MV NAV (PO) Often Associated with

Lower Equity Pmts. (IO)

-20

0

20

40

60

80

100

-20

0

20

40

60

80

100

Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17

Median Equity NAV

MV NAV has moved sideways in 2017 due to

limited loan market volatility

2012 2013 2014 2015 2016

CLO Metrics: BB MVOC

30

Metric BB MVOC

Description/ Uses

Time

Median Level Chg.

Current (Sep 2017) 107.0

12M Ago (Sep 2016) 105.7 1.3

18M Ago (Mar 2016) 101.1 5.9

Lower risky-asset exposure (Caa/CCC/ 2nd liens) Higher risky-asset exposure (Caa/CCC/2nd liens)

Lower loans < $80 exposure Higher loans < $80 exposure

Tranche Rating Size OC Coverage OC Ratio

AAAA 314 = 490 / [314] 156.0

BAA 61 = 490 / [314+61] 130.7

C A 36 = 490 / [314+61+36] 119.2

DBBB 26 = 490 / [314+61+36+26] 112.2

EBB 23 = 490 / [314+61+36+26+23] 106.5

Subord NR 53

Par Value of Liabilities 513

Market Value of Assets 490

Data Source Markit, Wells Fargo Securities

Calculation Example

Liabilities

OC Calculations

The BB tranche is 1.06x covered on a market value basis

● The Market Value OC Ratio of the BB notes. For example, if we liquidated the pool today, how covered are BB notes. OC ratio

uses the most recent market value of the collateral instead of the par / haircut value.

● Class B MVOC = market value of collateral / (Par value class A notes + Par value class B notes outstanding).

Market Stats

Common Metric

Pairs/Tradeoffs

Higher BB MVOC Pool

Lower BB MVOC Pool

Metric Analysis

Strengths

Weaknesses

● Provides proxy for market value coverage of the BB

tranche

● Commonly used in pricing and trading secondary

tranches

● Data is based on a snapshot of the loan prices on the day we

determine the underlying portfolio market value

● Does not account for initial structuring differences. Deals may have

higher or lower OC cushion at issuance due to trade-offs in the

structuring process.

● CLO is not a mark to market vehicle, and the CLO does not have

forced liquidation provisions. A CLO provides the equity investor with

term leverage with no mark to market pressure, and investors can’t

force a liquidation prior to the call – so measuring daily loan price

movements may not always make sense.

CLO Metrics: BB MVOC

31

Sources: Intex, LPC Collateral

Scatter plots show manager median data from the 9/2017 Style Guide

103

104

105

106

107

108

109

110

20% 40% 60% 80% 100%

BB MVOC

Market Value Metrics Tend to Move Together

Adj. NAV NAV

320

340

360

380

400

420

103 104 105 106 107 108 109

WAS

BB MVOC

Higher BB MVOC Often Associated with

Lower WAS (Lower-Spread Pools)

1%

2%

3%

4%

5%

6%

7%

8%

103 104 105 106 107 108 109

Norm. Eq. Pmts.

BB MVOC

Higher MV Metrics (like BB MVOC) Often

Associated with Lower Equity Pmts. (IO)

98

100

102

104

106

108

110

Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17 98

100

102

104

106

108

110

At the trough of 2016 volatility, the average BB

tranche was not covered on a MV basis

2012 2013 2014 2015 2016

Disclosure Appendix

32

Additional information is available on request.

Analyst’s Certification

The research analyst(s) principally responsible for the report certifies to the following: all views expressed in this research report accurately reflect the analysts’ personal

views about any and all of the subject securities or issuers discussed; and no part of the research analysts’ compensation was, is, or will be, directly or indirectly, related

to the specific recommendations or views expressed by the research analyst(s) in this research report.

Important Disclosures Relating to Conflicts of Interest and Potential Conflicts of Interest

Wells Fargo Securities does not compensate its research analysts based on specific investment banking transactions. Wells Fargo Securities research analysts receive

compensation that is based on and affected by the overall profitability of their respective department and the firm, which includes, but is not limited to, investment

banking revenue. Wells Fargo Securities may sell or buy the subject securities to/from customers on a principal basis or act as a liquidity provider in such securities.

Wells Fargo Securities Fixed Income Research analysts interact with the firm’s trading and sales personnel in the ordinary course of business. The firm trades or may

trade as a principal in the securities or related derivatives mentioned herein. The firm’s interests may conflict with the interests of investors in those instruments.

About Wells Fargo Securities

Wells Fargo Securities is the global brand name for the capital markets and investment banking services of Wells Fargo & Company and its subsidiaries, including but

not limited to Wells Fargo Securities, LLC, a U.S. broker-dealer registered with the U.S. Securities and Exchange Commission and a member of NYSE, FINRA, NFA and

SIPC, Wells Fargo Prime Services, LLC, a member of FINRA, NFA and SIPC, Wells Fargo Bank, N.A., Wells Fargo Securities Asia Limited, a Hong Kong Incorporated

investment firm licensed and regulated by the Securities and Futures Commission to carry Types 1, 4, 6 and 9 regulated activities and Wells Fargo Securities

International Limited, a U.K. entity investment firm authorized and regulated by the Financial Conduct Authority. The Wells Fargo Securities legal entity that takes

responsibility for the production of the Product is the legal entity which the first named author is employed by. Non-US analysts may not be associated persons of Wells

Fargo Securities, LLC. and therefore may not be subject to FINRA Rule 2242 restrictions on communications with subject company, public appearances and trading

securities by the analysts, but will be subject to their own local regulatory requirements.

Notice to U.S. Investors

Unless prohibited by the provisions of Regulation S of the 1933 Act, this material is distributed in the U.S., by Wells Fargo Securities, LLC, which takes responsibility for

its contents in accordance with the provisions of Rule 15a-6 and the guidance thereunder, under the U.S. Securities Exchange Act of 1934. Any transactions in securities

identified herein may be effected only with or through Wells Fargo Securities, LLC.

Disclosure Appendix

33

Important Information for Non-U.S. Clients

EEA

The securities and related financial instruments described herein may not be eligible for sale in all jurisdictions or to certain categories of investors. For recipients in the

EEA, Wells Fargo Securities International Limited (“WFSIL”) disseminates Research which has been approved for the purposes of Section 21 of the Financial Services

and Markets Act 2000 (“the Act”). WFSIL is a U.K. incorporated investment firm authorized and regulated by the Financial Conduct Authority. For the purposes of

Section 21 of the Act, WFSIL does not deal with retail clients. The FCA rules made under the Financial Services and Markets Act 2000 for the protection of retail clients

will therefore not apply, nor will the Financial Services Compensation Scheme be available. This report is not intended for, and should not be relied upon by, retail

clients.

Australia

Each of Wells Fargo Securities, LLC, Wells Fargo Securities Asia Limited and Wells Fargo Securities International Limited is exempt from the requirements to hold an

Australian financial services license in respect of the financial services it provides to wholesale clients in Australia. Wells Fargo Securities, LLC is regulated under U.S.

laws, Wells Fargo Securities Asia Limited is regulated under Hong Kong law, and Wells Fargo Securities International Limited is regulated under U.K. law, all of which

differ from Australian laws. Any offer or documentation provided to Australian recipients by Wells Fargo Securities in the course of providing the financial services will

be prepared in accordance with the laws of the United States, Hong Kong or U.K. and not Australian laws.

Hong Kong

This report is issued and distributed in Hong Kong by Wells Fargo Securities Asia Limited (“WFSAL”), a Hong Kong incorporated investment firm licensed and regulated

by the Securities and Futures Commission ("SFC") to carry on types 1, 4, 6 and 9 regulated activities (as defined in the Securities and Futures Ordinance (Cap. 571 of The

Laws of Hong Kong), “the SFO”). This report is not intended for, and should not be relied on by, any person other than professional investors (as defined in the SFO).

Any securities and related financial instruments described herein are not intended for sale, nor will be sold, to any person other than professional investors (as defined in

the SFO). The author or authors of this report may or may not be licensed by the SFC. Professional investors who receive this report should direct any queries regarding

its contents to Mark Jones at WFSAL (email: wfsalresearch@wellsfargo.com ).

Japan

This report is distributed in Japan by Wells Fargo Securities (Japan) Co., Ltd, registered with the Kanto Local Finance Bureau to conduct broking and dealing of type 1

and type 2 financial instruments and agency or intermediary service for entry into investment advisory or discretionary investment contracts. This report is intended for

distribution only to professional investors (Tokutei Toushika) and is not intended for, and should not be relied upon by, ordinary customers (Ippan Toushika).

The ratings stated on the document are not provided by rating agencies registered with the Financial Services Agency of Japan (JFSA) but by group companies of JFSA-

registered rating agencies. These group companies may include Moody’s Investors Services Inc, Standard & Poor’s Rating Services and/or Fitch Ratings. Any decisions

to invest in securities or transactions should be made after reviewing policies and methodologies used for assigning credit ratings and assumptions, significance and

limitations of the credit ratings stated on the respective rating agencies’ websites.

Disclosure Appendix

34

Published reports and additional disclosure information are available at www.wellsfargoresearch.com.

This report is for your information only and is not an offer to sell, or a solicitation of an offer to buy, the securities or

instruments named or described in this report. Interested parties are advised to contact the Wells Fargo entity in their

local jurisdiction with which they deal, or the entity that provided this report to them, if they desire further information

or if they wish to effect transactions in the security discussed in this report. The information in this report has been

obtained or derived from sources believed by Wells Fargo Securities, to be reliable, but Wells Fargo Securities does not

represent that this information is accurate or complete. Certain text, images, graphics, screenshots and audio or video

clips included in this report are protected by copyright law and owned by third parties (collectively, “Third Party

Content”). Third Party Content is made available to clients by Wells Fargo under license or otherwise in accordance

with applicable law. Any use or publication of Third Party Content included in this report for purposes other than fair

use requires permission from the copyright owner. Certain website links included in this publication are not

maintained, controlled or operated by Wells Fargo Securities. Wells Fargo Securities does not provide the products and

services on these external websites and the views expressed on these websites do not necessarily represent those of

Wells Fargo Securities. Please review the applicable privacy and security policies and terms and conditions for the

website you are visiting. Credit Strategists focus on investment themes across the credit markets and sectors. Any

discussion within a Credit Strategy report of specific securities is not intended to provide a fundamental analysis of any

individual company described therein. The information provided in Credit Strategy reports is subject to change

without notice, and investors should not expect continuing information or additional reports relating to any security

described therein. Any opinions or estimates contained in this report represent the judgment of Wells Fargo Securities

at this time, and are subject to change without notice. For the purposes of the U.K. Financial Conduct Authority's rules,

this report constitutes impartial investment and substantive research. Each of Wells Fargo Securities, LLC, and Wells

Fargo Securities International Limited is a separate legal entity and distinct from affiliated banks. Copyright © 2017

Wells Fargo Securities, LLC.

This report was prepared by Wells Fargo Securities, LLC.

SECURITIES: NOT FDIC-INSURED * NOT BANK-GUARANTEED * MAY LOSE VALUE